choose well. live well. it’s your path · choose well. live well. it’s your path ... every...

TRANSCRIPT

Choose Well. Live Well. it’s your path

Your 2017 Guide to Benefits Enrollment

January 2017

The information in this Enrollment Guide is presented for illustrative purposes and is based on information provided by the employer. The text contained in this Guide was taken from various summary plan descriptions and benefit information. While every effort was taken to accurately report your benefits, discrepancies or errors are always possible. In case of discrepancy between the Guide and the plan documents, the actual plan documents will prevail. Information is confidential, pursuant to the Health Insurance Portability and Accountability Act of 1996. If you have any questions about the Guide, contact HR.

4 5 6 7

8 10

11 16 19 21

28

What’s Inside Changes This Year Contact Information Eligibility & Enrollment Qualifying Events Medical Coverage Prescription Coverage Dental Coverage Vision Coverage Flexible Spending Accounts Life and AD&D Coverage Disability Coverage Employee Assistance Program Notifications

31 332

Welcome to Your Benefits Open

Enrollment! We are pleased to present this

guide, which highlights the comprehensive coverage

available to you.

This guide includes only highlights of your benefits. The specific terms of coverage, exclusions & limitations are contained in the plan documents and insurance certificates. All coverage and coverage costs are subject to change at any time in the future. If you have any questions about a specific service or treatment, please contact the appropriate insurance carrier.

This booklet has been created to help you understand the benefit plans that are being offered to you. Our benefits program is designed to offer employees substantial coverage to meet both individual and family needs. Please take the time to review the information in this guide. We want you to be fully informed of the benefits available to you and your family. This guide also incorporates information on when you may change your benefit elections.

The information in this Enrollment Guide is presented for illustrativepurposes and is based on information provided by the employer. The textcontained in this Guide was taken from various summary plan descriptionsand benefit information. While every effort was taken to accurately reportyour benefits, discrepancies or errors are always possible. In case ofdiscrepancy between the Guide and the plan documents, the actual plandocuments will prevail. Information is confidential, pursuant to the HealthInsurance Portability and Accountability Act of 1996. If you have anyquestions about the Guide, contact HR.

Welcome to Benefits Open Enrollment!

We are pleased to present this guide which highlights the comprehensive coverage

available to you.

This guide includes only highlights. The specific terms of coverage, exclusions & limitations are contained in the plan documents and insurance certificates. All coverage and coverage costs are subject to change at any time in the future. If you have any questions about a specific service or treatment, please contact the appropriate insurance carrier.

This booklet has been created to help you understand the benefit plans that are being offered to you. Our benefits program is designed to offer employees substantial coverage to meet both individual and family needs. Please take the time to review the information in this guide. We want you to be fully informed of the benefits available to you and your family. This guide also incorporates information on when you may change your benefit elections.

3

MEDICAL COVERAGECHANGES THIS YEAR

Beginning Jan. 1, 2017, upon a group’s renewal, some pharmacy benefit plans will include a Preferred Pharmacy Network. This network includes at least one major chain, a grocery chain and independent pharmacies, among others. These are the participating pharmacies in the 2017 Preferred Pharmacy Network:• Walgreens• Walmart (including Sam’s Club Pharmacy)• Pharmacy Providers of Oklahoma, Inc. (PPOK) (a group of independent pharmacies)• AccessHealth (a group of independent pharmacies)

When members fill a prescription for up to a 30-day supply of a covered prescription drug from a retail pharmacy that contracts to participate in the Preferred Pharmacy Network, they may pay the lowest copay/coinsurance amount. If members fill a prescription at a non-preferred in-network pharmacy, they may pay a higher copay/coinsurance amount.For up to a 90-day supply of a covered prescription drug, members can either fill these prescriptions through the home delivery pharmacy service or at a retail pharmacy participating in the Preferred Pharmacy Network. Members will pay 3x copay of one 30-day prescription. A list of all participating pharmacies’ locations will be posted on the bcbsok.com website once available.

Letters will be sent to impacted members who are affected by one or more of these changes that will explain how the change (s) will impact them. Members will be encouraged to talk with their doctor(s) about their prescribed medications and if any changes in their drug therapy may be right for them.

All standard plans will move to the new Performance Drug List. Groups on a standard plan will also have the Preferred Pharmacy Network added to their pharmacy benefit plan. Additionally, CVS will be excluded from the Broad Pharmacy Network on Jan. 1, 2017 (regardless of renewal date).

Pharmacy Changes

4

CONTACT INFORMATIONRefer to this list when you need to contact one of your benefit vendors.

For general information contact Human Resources.

CONTACT PHONE WEBSITE / EMAIL GROUP #Human Resources: Oklahoma Baptist University· Kami Fullingim

405-585-5130 [email protected]

Medical: BlueCross Blue Shield· Member Services

(800) 942-5837 www.bcbsok.com Y04400

Dental: Delta Dental of OK· Member Services

(800) 522-0188 www.deltadentalok.org 3502-0013502-002

Vision: VSP· Member Services

(888) 600-1600 www.vsp.com 30002022

Life / AD&D and Vol. Life:Dearborn National

· Member Services

(800) 775-8805 www.dearbornnational.com F019973

Long- Term Disability (LTD):Cigna· Member Services

(800) 362-4462 www.cigna.com/customer-forms 964483

Employee Assistance Program (EAP):Cigna· Member Services

(800)538-3543 www.CignaBehavioral.com/CGI

Flexible Spending Account (FSA):Ameriflex· Member Services

(888)868-3539 https://participant.ameriflexbenefits.com

AMFOKBUOK

Broker Services:NFPKelley HarmonCortney Washington

(888) 460-8704

(405) 513-8988(405) 513-8948

www.nfp.com/CSOK

[email protected]@nfp.com

5

ELIGIBILITY& ENROLLMENT

Who is Eligible All employees who work at least 30 hours per week, and their eligible dependents, are eligible for the benefits outlined in this guide. Your coverage begins upon your hire date, provided you have completed the enrollment process within 31 days of hire date.

After your initial enrollment, you will have the opportunity to re-enroll in the Benefits Program each year during the Annual Open Enrollment period.

Eligible Dependents Your eligible dependents include: • Your spouse (unless you are legally separated)• Your dependent children who are under age 26.

How to Enroll If you are enrolling in our benefits for the first time, or wanting to make a plan/election change, just follow these simple steps:

• Request enrollment/change form(s) from yourBenefits Administrator.

• Read this guide and the instructions on your enrollmentform(s). These contain important information about yourbenefit options.

• Complete the enrollment form(s) by making your benefitelections and sign; and

• Send the enrollment form(s) to Human Resources by theenrollment deadline.

What Changes Can I Make?• Enroll if not currently on the plan• Switch to another plan option (if available)• Cancel coverage• Add/drop dependents

What is the deadline to submit changes?All Open Enrollment paperwork must be submitted to your Benefits Administrator no later than November 11, 2016.

What Happens if you Don’t Enroll For New Hires and Newly Eligible EmployeesIf you are a new hire or become eligible for benefits, and do not enroll when you are first eligible, you will receive only minimal levels of benefit coverage. In this case, you must wait until the next Annual Open Enrollment period to enroll for the coverage you want and need. If you don’t enroll, the only benefit coverage you will receive is: • Basic Life and AD&D Insurance• Long-term Disability Insurance

For Active EmployeesIf you are an active employee and don’t enrollfor benefits during the Annual Open Enrollmentperiod, your current benefit elections will automatically carry over to the next plan year – excluding your current Flexible Spending Account elections and any plans not offered in the new plan year. This feature is designed to make the enrollment process as easy as possible for employees who want to keep current coverage for another year.

When Coverage Ends If your employment ends or you lose eligibility, your coverage will end on the last day of the month following your event date. Depending upon the circumstances of your termination, you may be able to continue certain coverages under COBRA or State Continuation. For more information, refer to your continuation notice included with this guide.

6

QUALIFYING EVENTSMost individuals go through a number of life events that affect their health benefit needs and the choices they make. There are several important federal laws that affect your benefits under a job-based health plan.

While you are generally only allowed to change your benefits elections during the open enrollment period each year, certain life events provide an exception. Those life events allow you to change your benefits elections in the middle of the plan year if certain requirements are met. The following are examples of types of life events that may allow you to change your benefit elections during a plan year:

• Change in marital status (marriage, death of spouse, divorce/annulment, legal separation)

• Change in number of dependents (birth, death, adoption, eligibility status, child support order)

• Change in employment status for you or your spouse (commencement, termination, leave of absence, full-time/part-time status change)

• Change in Insurance coverage (gain or involuntary loss of coverage through another plan, including Medicaid or CHIP)

• Change of address (when you move outside the service area of your network)• Dependent child reaches limiting age

Generally, changes in your coverage elections must be made within 30 days of the qualifying event. YOU are responsible for notifying the Human Resources Department of any qualifying event and for requesting information to change your elections.

For further information on eligible qualifying events, please contact the Human Resources Department and also refer to the attached Special Enrollment Notice for qualifying events.

DON’T FORGET!Newborns will NOT be automatically

added to your coverage. You must take action within 30 days of the birth.

You are responsible

For notifying HR

Within 30 Days!

7

MEDICAL COVERAGEMEDICAL COVERAGE

Visit the link to view more information

about your benefits

QUESTIONS?

Medical CoverageHaving access to high quality, affordable health care is a great concern for most people. That’s why we are pleased to offer employees and their families comprehensive medical coverage administered by BlueCross & BlueShield of Oklahoma.

The Freedom To ChooseYou can choose between two medical Networks .Note: Plan changes can only be made during open enrollment.

• Blue Preferred – Base Plan• Lower premium option• Deeper negotiated discounts

• Blue Choice – Buy-up Plan• You have the option to buy up to this plan• Larger network of providers

These plans allow you the freedom to choose either an in-network or out-of-network provider for your health care needs. When you receive care from an in-network provider you will experience significant savings. This is because in-network providers have agreed to negotiated discounts for our employees. Should you choose to receive care from an out-of-network provider, you may have to file the claim to receive reimbursement for covered expenses and your out-of-pocket costs will be much higher.

If you are uncertain if a physician or medical facility is in your plan’s network, visit www.bcbsok.com/providers or call Customer Service at (800) 942-5837.

Blue Access for MembersSave time with self-service support tools and health and wellness resources on a convenient and secure online site.

Register for Blue Access for Members: www.bcbsok.com/member to review claims status, coverage details, download Explanation of Benefits (EOBs), request new ID cards, learn how to save money on gym memberships, hearing aids and diet-related services, and much more.

Prescription Drug CoverageWhen you enroll in our medical plan, you automatically receive prescription drug coverage.

Coverage ConsiderationsOur prescription drug benefit plan provides coverage for up to a 30-day supply of medication, with some exceptions. Our plan also provides coverage for up to a 90-day supply of maintenance medications. These medications are those drugs you may take on an ongoing basis for conditions such as high blood pressure, diabetes or high cholesterol.

Prior Authorization (PA): Our benefit plan requires prior authorization for certain drugs. This means that your doctor will need to submit a prior authorization request for coverage of these medications, and the request will need to be approved, before the medication will be covered under our plan.

Step Therapy (ST): Our benefit plan includes a step therapy program. This means you may need to try another proven, cost-effective medication before coverage may be available for the drug included in the program. Many brand drugs have less-expensive generic or brand alternatives that might be an option for you.

Dispensing Limits (DL): Drug Dispensing limits are designed to help encourage medication use as intended by the FDA. Coverage limits are placed on medications in certain drug categories. Limits may include: quantity of covered medication per prescription, quantity of covered medication in a given time period, coverage only for members within a certain age range, and coverage only for members of a specific gender. If your doctor prescribes a greater quantity of medication than what the dispensing limit allows, you can still get the medication. However, you will be responsible for the full cost of the prescription beyond what our coverage allows.

Remember, medication decisions are between you and your doctor. Discuss any questions or concerns you have about medications you are taking or are prescribed with your doctor.

8

MEDICAL COVERAGEMEDICAL COVERAGE

COVERED SERVICES Blue Preferred “Base Plan’’ BlueChoice “Buy-Up”Deductible (D)

IndividualFamily

$2,500$7,500

$2,500$7,500

Coinsurance (C) Plan 80% / You 20% Plan 80% / You 20%

Out-of-pocket Max*Includes Deductible, Coinsurance and Medical Copays

$6,600 Individual$13,200 Family

$6,600 Individual$13,200 Family

Physician Visit-Primary Care-Specialist

$30 Copay$50 Copay

$30 Copay$50 Copay

Diagnostics, Lab & X-RayComplex Imaging

Included in Office VisitDeductible + Coinsurance

Included in Office VisitDeductible + Coinsurance

Preventive Care 100% of Allowed Amount 100% of Allowed Amount

Hospitalization –-Inpatient

- Outpatient$200+ Deductible + Coinsurance

Deductible + Coinsurance$200 + Deductible + Coinsurance

Deductible + Coinsurance

Emergency Room $200 Copay (waived if admitted) then Deductible & Coinsurance

$200 Copay (waived if admitted) then Deductible & Coinsurance

Urgent Care $30 Copay $30 Copay

Medical Plans Compared The following chart compares a highlight of the in-network benefits of our plans. See the attached benefit summaries for more detail.

*The out-of-pocket limit is the most you could pay during a coverage period (usually one year) for your share of the cost of covered services.*Note: Please visit www.bcbsok.com for the most up to date hospital / provider listings.

Your Cost Per MonthOklahoma Baptist University pays 80% of the premium for employee only coverage, and 73% of dependents for eligible employees for the Blue Preferred Network. You have the option of buying up to the Blue Choice Network.

FILING STATUS OBU Cost Per Month Blue Preferred "Base Plan" BlueChoice "Buy-Up"Employee Only $308.62 $77.16 $147.24

Family $778.82 $288.04 $480.48

MEDICAL COVERAGE

9

MEDICAL COVERAGEMEDICAL COVERAGE

PRESCRIPTION DRUG COVERAGEWe offer a comprehensive prescription drug benefit plan. Our plan classifies prescription drugs into the following four tiers:

• Generic drugs have the same formula make-up as their brand-name counterparts but with a lower cost.• Preferred Name Brand are brand name drugs that are available to you at a discounted rate.• Non-Preferred Brand are brand name drugs that do not offer a manufacturer discount.• Special Drugs typically require special handling and administration and will need special approval to order.

FORMULARY TIERS PHARMACY COST 30 DAY SUPPLY

MAIL ORDER COST90 DAY SUPPLY

Generic $15 $37.50

Preferred Name Brand $35 $87.50

Non-preferred Name Brand $60 $150

Specialty Drugs $60 N/A

Have a Monthly Rx?You can receive up to a 90-day supply of long-term medicine for 2.5x the copay (specialty drugs not available thru mail order). For more information visit www.bcbs.com or call PrimeMail at 877.357.7463

Making the Most of Rx Benefits Use these tips to make sure you get the most out of your Rx benefits.

• Use a network pharmacy• Use generic drugs when available• Ask if your Rx is on the Wal-Mart or Target $4 List• Enroll in a discount program from pharmaceutical companies

10

MEDICAL COVERAGEDENTAL COVERAGE

Dental CoverageToo often people forget about dental care. That’s unfortunate, because having healthy teeth is an important part of your overallwell-being.

Our dental plans are administered by Delta Dental of Oklahoma. Our Plans pay for preventive services without requiring a deductible for exams, x-rays and cleanings. It also includes coverage for restorative and major services including fillings, crowns and bridges.

Delta Dental PPO – Plus Premier combines the Delta Dental PPO and Delta Dental Premier networks for maximum access and savings opportunities. Members may select a dentist from either the PPO or Premier network with no balance billing (subscribers are responsible for their deductible and coinsurance amounts). Greater network savings are available when utilizing a PPO provider.

To locate a participating PPO or Premier dentist, contact Delta Dental at 1-800-522-0188 or visit their website at www.deltadentalok.org.

COVERED SERVICES IN-NETWORKPPO PLUS PREMIER

Calendar Year DeductibleWaived for Preventive Services

$100 (3 per family)

Preventive ServicesCleanings & exams Plan pays 100%

Basic ServicesFillings & extractions

Plan pays 80% after deductible

Major ServicesCrowns, caps, dentures

Plan pays 50% after deductible

Orthodontic Services(Only up to age 26) Plan pays 50% after

deductible

Annual Max BenefitOrthodontic Lifetime Max

$1,000$1,500 per child

The following is a listing of common services available through your Dental PPO Plus Premier plan.

Your Cost Per MonthOklahoma Baptist University pays 80% of the employee premium, and 73% of dependents for dental.

FILING STATUS YOUR COST PER MONTH

Employee Only $17.26

Family $79.94

FILING STATUS YOUR COST PER MONTH

Employee Only $4.46

Family $17.66

COVERED SERVICES IN-NETWORKPPO

Calendar Year DeductibleWaived for Preventive Services

$100 (3 per family)

Preventive ServicesCleanings & exams Plan pays 100%

Basic ServicesFillings & extractions

Plan pays 80% after deductible

Major ServicesCrowns, caps, dentures

Plan pays 50% after deductible

Orthodontic Services N/A

Annual Max BenefitOrthodontic Lifetime Max

$1,000N/A

Benefit HighlightsThe following is a listing of common services available through your Dental PPO Plan.

11

UW-01, Revised: Nov 2015

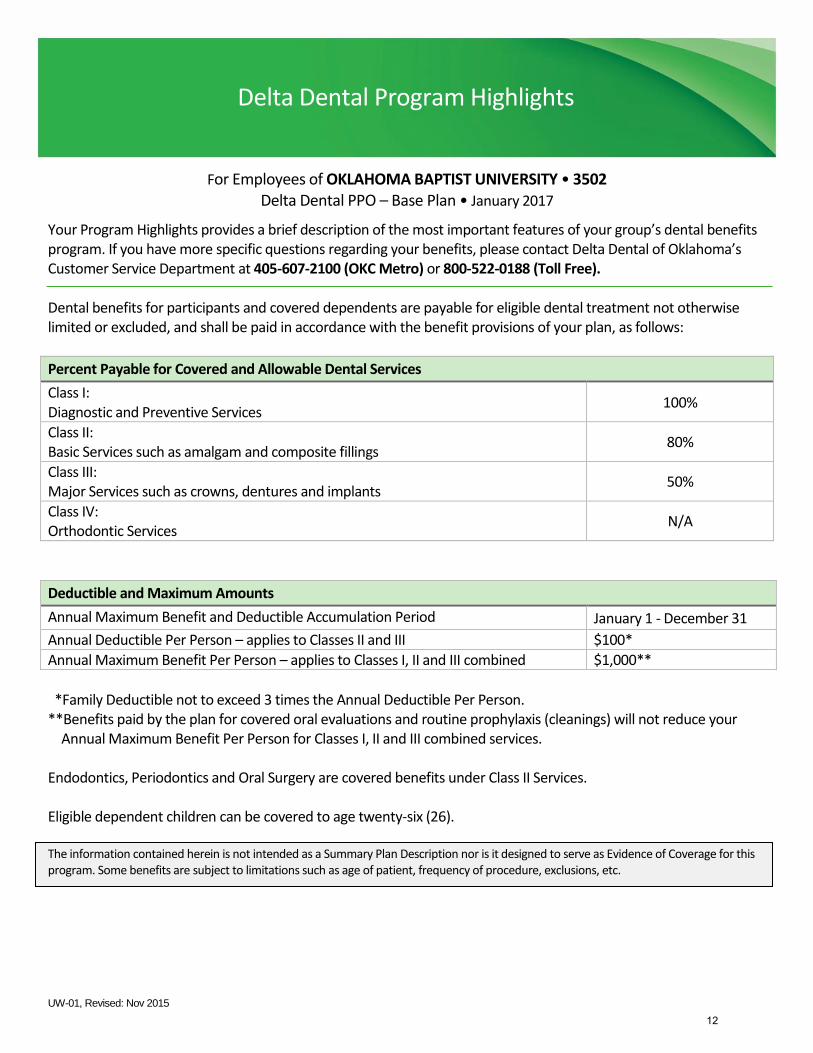

For Employees of OKLAHOMA BAPTIST UNIVERSITY • 3502 Delta Dental PPO – Base Plan • January 2017

Your Program Highlights provides a brief description of the most important features of your group’s dental benefits program. If you have more specific questions regarding your benefits, please contact Delta Dental of Oklahoma’s Customer Service Department at 405-607-2100 (OKC Metro) or 800-522-0188 (Toll Free).

Dental benefits for participants and covered dependents are payable for eligible dental treatment not otherwise limited or excluded, and shall be paid in accordance with the benefit provisions of your plan, as follows:

Percent Payable for Covered and Allowable Dental Services

Class I: Diagnostic and Preventive Services

100%

Class II: Basic Services such as amalgam and composite fillings

80%

Class III: Major Services such as crowns, dentures and implants

50%

Class IV: Orthodontic Services

N/A

Deductible and Maximum Amounts

Annual Maximum Benefit and Deductible Accumulation Period January 1 - December 31

Annual Deductible Per Person – applies to Classes II and III $100*

Annual Maximum Benefit Per Person – applies to Classes I, II and III combined $1,000**

*Family Deductible not to exceed 3 times the Annual Deductible Per Person.**Benefits paid by the plan for covered oral evaluations and routine prophylaxis (cleanings) will not reduce your

Annual Maximum Benefit Per Person for Classes I, II and III combined services.

Endodontics, Periodontics and Oral Surgery are covered benefits under Class II Services.

Eligible dependent children can be covered to age twenty-six (26).

The information contained herein is not intended as a Summary Plan Description nor is it designed to serve as Evidence of Coverage for this program. Some benefits are subject to limitations such as age of patient, frequency of procedure, exclusions, etc.

Delta Dental Program Highlights

12

UW-01, Revised: Nov 2015

Your dental benefits program allows payment for eligible services performed by any properly licensed dentist. However, maximum savings and lower out-of-pocket expenses are achieved when treatment is provided by a Delta Dental participating dentist. Below is an illustration of a typical 100/80/50/50 plan, assuming annual deductible has been satisfied.

Delta Dental PPO participating dentist Delta Dental Premier participating dentist Out-of-Network dentist

Dentist Charge $100 Dentist Charge $100 Dentist Charge $100

PPO Maximum Allowable $70 Premier Maximum Allowable $85 Prevailing Fee $75

Plan pays 80% of PPO Allowable

$56 Plan pays 80% of PPO Allowable

$56 Plan pays 80% of PPO Allowable

$56

You pay 20% of PPO Allowable

$14 You pay Difference between PPO Payment and Premier Allowable

$29 You pay Balance of the dentist charge

$44

How to use your dental program: Call the dental office of your choice and make an appointment. During your first appointment be sure to provide your dentist with the following information:

Your Group name

Your Group number

The employee’s social security or member ID number

Your dental program allows you to:

Change dentists and visit a specialist of your choice at any time without preapproval

Select a different dentist for each member of your family

Receive dental care anywhere in the world

Find a Delta Dental participating dentist: Two-thirds of the nation’s practicing dentists are Delta Dental participating dentists. To find a participating dentist, refer to our National Dentist Directory at www.DeltaDentalOK.org or call Delta Dental’s Customer Service Department at 405-607-2100 (OKC Metro) or 800-522-0188 (Toll Free).

Benefit Payment Procedure Delta Dental pays participating dentists directly. You are responsible for any co-insurance percentages, deductible amounts, charges for non-covered services and amounts in excess of your annual maximum benefit. A Delta Dental participating dentist cannot charge you for amounts payable by Delta Dental. If you obtain treatment from a nonparticipating dentist, you may have to pay the entire bill in advance. Delta Dental will directly reimburse you, or any other participant or beneficiary, if required by law, up to your plan’s maximum allowable amount.

The advantage of predetermination If you are scheduled for dental treatment that will cost more than $250, your dentist can request a predetermination of benefits by Delta Dental to determine if the proposed treatment is covered under your program, approximately how much the service will cost and your estimated share of the cost.

Filing your claim A Delta Dental participating dentist will file your claim at no charge. If necessary, a printable claim form may be obtained on our website at www.DeltaDentalOK.org. Completed claim forms should be submitted to the address below:

Delta Dental of Oklahoma - Claims Processing Center P.O. Box 548809

Oklahoma City, OK 73154-8809

13

UW-01, Revised: Nov 2015

For Employees of OKLAHOMA BAPTIST UNIVERSITY • 3502 Delta Dental PPO – Plus Premier – Buy Up Plan • January 2017

Your Program Highlights provides a brief description of the most important features of your group’s dental benefits program. If you have more specific questions regarding your benefits, please contact Delta Dental of Oklahoma’s Customer Service Department at 405-607-2100 (OKC Metro) or 800-522-0188 (Toll Free).

Dental benefits for participants and covered dependents are payable for eligible dental treatment not otherwise limited or excluded, and shall be paid in accordance with the benefit provisions of your plan, as follows:

Percent Payable for Covered and Allowable Dental Services

Class I: Diagnostic and Preventive Services

100%

Class II: Basic Services such as amalgam and composite fillings

80%

Class III: Major Services such as crowns, dentures and implants

50%

Class IV: Orthodontic Services are available to dependent children under age 26

50%

Deductible and Maximum Amounts

Annual Maximum Benefit and Deductible Accumulation Period January 1 - December 31

Annual Deductible Per Person – applies to Classes II and III $100*

Annual Maximum Benefit Per Person – applies to Classes I, II and III combined $1,000**

Lifetime Maximum Benefit Payment Per Child – applies to Class IV only $1,500

*Family Deductible not to exceed 3 times the Annual Deductible Per Person.**Benefits paid by the plan for covered oral evaluations and routine prophylaxis (cleanings) will not reduce your

Annual Maximum Benefit Per Person for Classes I, II and III combined services.

Endodontics, Periodontics and Oral Surgery are covered benefits under Class II Services.

Eligible dependent children can be covered to age twenty-six (26).

The information contained herein is not intended as a Summary Plan Description nor is it designed to serve as Evidence of Coverage for this program. Some benefits are subject to limitations such as age of patient, frequency of procedure, exclusions, etc.

Delta Dental Program Highlights

14

UW-01, Revised: Nov 2015

Your dental benefits program allows payment for eligible services performed by any properly licensed dentist. However, maximum savings and lower out-of-pocket expenses are achieved when treatment is provided by a Delta Dental participating dentist. Below is an illustration of a typical 100/80/50/50 plan, assuming annual deductible has been satisfied.

Delta Dental PPO participating dentist Delta Dental Premier participating dentist Out-of-Network dentist

Dentist Charge $100 Dentist Charge $100 Dentist Charge $100

PPO Maximum Allowable $70 Premier Maximum Allowable $85 Prevailing Fee $75

Plan pays 80% of PPO Allowable

$56 Plan pays 80% of Premier Allowable

$68 Plan pays 80% of Prevailing Fee

$60

You pay 20% of PPO Allowable

$14 You pay 20% of Premier Allowable

$17 You pay Balance of the dentist charge

$40

How to use your dental program: Call the dental office of your choice and make an appointment. During your first appointment be sure to provide your dentist with the following information:

Your Group name

Your Group number

The employee’s social security or member ID number

Your dental program allows you to:

Change dentists and visit a specialist of your choice at any time without preapproval

Select a different dentist for each member of your family

Receive dental care anywhere in the world

Find a Delta Dental participating dentist: Two-thirds of the nation’s practicing dentists are Delta Dental participating dentists. To find a participating dentist, refer to our National Dentist Directory at www.DeltaDentalOK.org or call Delta Dental’s Customer Service Department at 405-607-2100 (OKC Metro) or 800-522-0188 (Toll Free).

Benefit Payment Procedure Delta Dental pays participating dentists directly. You are responsible for any co-insurance percentages, deductible amounts, charges for non-covered services and amounts in excess of your annual maximum benefit. A Delta Dental participating dentist cannot charge you for amounts payable by Delta Dental. If you obtain treatment from a nonparticipating dentist, you may have to pay the entire bill in advance. Delta Dental will directly reimburse you, or any other participant or beneficiary, if required by law, up to your plan’s maximum allowable amount.

The advantage of predetermination If you are scheduled for dental treatment that will cost more than $250, your dentist can request a predetermination of benefits by Delta Dental to determine if the proposed treatment is covered under your program, approximately how much the service will cost and your estimated share of the cost.

Filing your claim A Delta Dental participating dentist will file your claim at no charge. If necessary, a printable claim form may be obtained on our website at www.DeltaDentalOK.org. Completed claim forms should be submitted to the address below:

Delta Dental of Oklahoma - Claims Processing Center P.O. Box 548809

Oklahoma City, OK 73154-8809

15

MEDICAL COVERAGEVISION COVERAGE

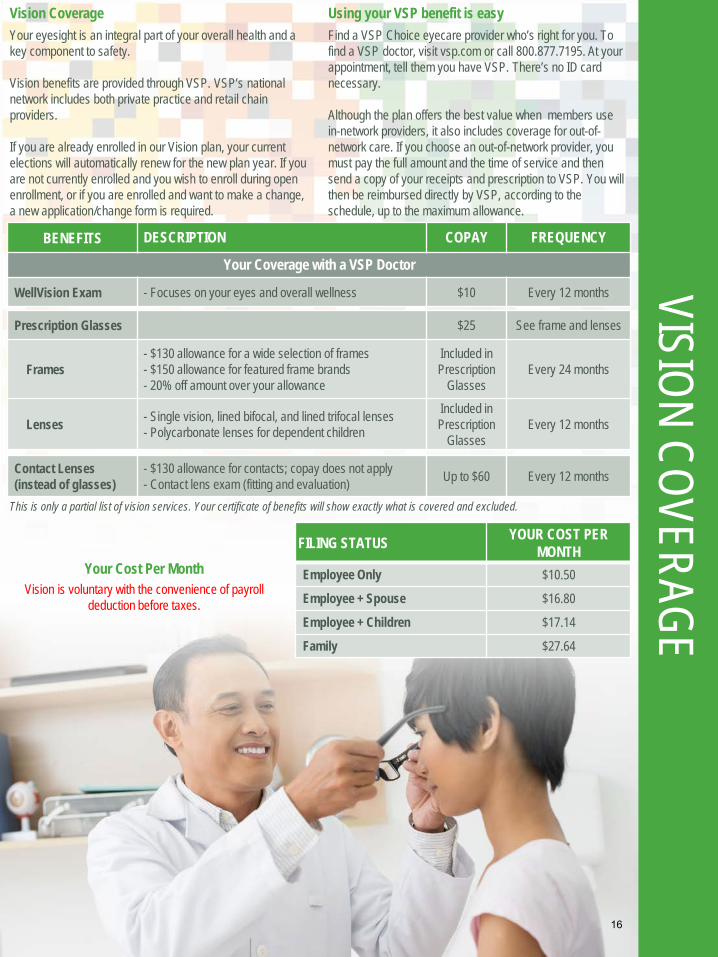

Vision CoverageYour eyesight is an integral part of your overall health and a key component to safety.

Vision benefits are provided through VSP. VSP’s national network includes both private practice and retail chain providers.

If you are already enrolled in our Vision plan, your current elections will automatically renew for the new plan year. If you are not currently enrolled and you wish to enroll during open enrollment, or if you are enrolled and want to make a change, a new application/change form is required.

BENEFITS DESCRIPTION COPAY FREQUENCY

Your Coverage with a VSP Doctor

WellVision Exam - Focuses on your eyes and overall wellness $10 Every 12 months

Prescription Glasses $25 See frame and lenses

Frames- $130 allowance for a wide selection of frames- $150 allowance for featured frame brands- 20% off amount over your allowance

Included in Prescription

GlassesEvery 24 months

Lenses - Single vision, lined bifocal, and lined trifocal lenses- Polycarbonate lenses for dependent children

Included in Prescription

GlassesEvery 12 months

Contact Lenses (instead of glasses)

- $130 allowance for contacts; copay does not apply- Contact lens exam (fitting and evaluation) Up to $60 Every 12 months

Using your VSP benefit is easyFind a VSP Choice eyecare provider who’s right for you. To find a VSP doctor, visit vsp.com or call 800.877.7195. At your appointment, tell them you have VSP. There’s no ID card necessary.

Although the plan offers the best value when members use in-network providers, it also includes coverage for out-of-network care. If you choose an out-of-network provider, you must pay the full amount and the time of service and then send a copy of your receipts and prescription to VSP. You will then be reimbursed directly by VSP, according to the schedule, up to the maximum allowance.

This is only a partial list of vision services. Your certificate of benefits will show exactly what is covered and excluded.

FILING STATUS YOUR COST PER MONTH

Employee Only $10.50

Employee + Spouse $16.80

Employee + Children $17.14

Family $27.64

Your Cost Per MonthVision is voluntary with the convenience of payroll

deduction before taxes.

16

Enroll in VSP today. You'll be glad you did.

Contact us. 800.877.7195 vsp.com

Get the best in eyecare and eyewear with OKLAHOMA BAPTIST UNIVERSITY and VSP® Vision Care. Why enroll in VSP? We invest in the things you value most—the best care at the lowest out-of-pocket costs. Because we’re the only national not-for-profit vision care company, you can trust that we’ll always put your wellness first.

You’ll like what you see with VSP.• Value and Savings. You’ll enjoy more value and the lowest out-of-

pocket costs.

• High Quality Vision Care. You’ll get the best care from a VSP provider,including a WellVision Exam®—the most comprehensive exam designedto detect eye and health conditions. Plus, when you see a VSP provider,your satisfaction is guaranteed.

• Choice of Providers. The decision is yours to make—choose a VSPprovider or any out-of-network provider.

• Great Eyewear. It’s easy to find the perfect frame at a price that fitsyour budget.

Using your VSP benefit is easy. • Register at vsp.com.

Once your plan is effective, review your benefit information.

• Find an eyecare provider who's right for you.To find a VSP provider, visit vsp.com or call 800.877.7195.

• At your appointment, tell them you have VSP. There’s no ID cardnecessary. If you’d like a card as a reference, you can print one onvsp.com.

That’s it! We’ll handle the rest—there are no claim forms to complete when you see a VSP provider.

Choice in Eyewear From classic styles to the latest designer frames, you'll find hundreds of options. Choose from featured frame brands like Anne Klein, bebe®, Calvin Klein, Flexon®, Lacoste, Nike, Nine West, and more1. Visit vsp.com to find a VSP provider who carries these brands.

17

Your VSP Vision Benefits Summary OKLAHOMA BAPTIST UNIVERSITY and VSP provide you with an affordable eyecare plan.

VSP Coverage Effective Date: 01/01/2015 VSP Provider Network: VSP Signature

Visit vsp.com for more details on your vision benefit and for exclusive savings

and promotions for VSP members.

CopayDescriptionBenefit FrequencyYour Coverage with a VSP Provider

WellVision Exam • Focuses on your eyes and overall wellness $10 Every calendar year

Prescription Glasses $25 See frame and lenses

Frame • $130 allowance for a wide selection of frames• $150 allowance for featured frame brands• 20% savings on the amount over your allowance

Included in Prescription

Glasses Every other calendar year

Lenses • Single vision, lined bifocal, and lined trifocal lenses• Polycarbonate lenses for dependent children

Included in Prescription

Glasses Every calendar year

Lens Enhancements

• Standard progressive lenses• Premium progressive lenses• Custom progressive lenses• Average savings of 35-40% on other lens enhancements

$50 $80 - $90

$120 - $160 Every calendar year

Contacts (instead of glasses)

• $130 allowance for contacts; copay does not apply• Contact lens exam (fitting and evaluation) Up to $60 Every calendar year

Extra Savings

Glasses and Sunglasses • Extra $20 to spend on featured frame brands. Go to vsp.com/specialoffers for details.• 30% savings on additional glasses and sunglasses, including lens enhancements, from the same VSP provider on

the same day as your WellVision Exam. Or get 20% from any VSP provider within 12 months of your last WellVisionExam.

Retinal Screening • No more than a $39 copay on routine retinal screening as an enhancement to a WellVision Exam

Laser Vision Correction • Average 15% off the regular price or 5% off the promotional price; discounts only available from contracted facilities• After surgery, use your frame allowance (if eligible) for sunglasses from any VSP doctor

Visit vsp.com for details, if you plan to see a provider other than a VSP network provider.

Exam ...................................................up to $50 Frame .................................................up to $70

Single Vision Lenses ..................up to $50 Lined Bifocal Lenses ..................up to $75

Lined Trifocal Lenses .................up to $100 Progressive Lenses .....................up to $75

Contacts ...........................................up to $105

Your Coverage with Out-of-Network Providers

VSP guarantees coverage from VSP network providers only. Coverage information is subject to change. In the event of a conflict between this information and your organization’s contract with VSP, the terms of the contract will prevail. Based on applicable laws, benefits may vary by location.

1 Brands/Promotion subject to change.

©2014 Vision Service Plan. All rights reserved. VSP, VSP Vision care for life, and WellVision Exam are registered

trademarks of Vision Service Plan. Flexon is a registered trademark of Marchon Eyewear, Inc. All other brands are

trademarks or registered trademarks of their respective owners.

Enroll in VSP today. You'll be glad you did. Contact us. 800.877.7195 vsp.com 18

FLEXIBLE SPENDINGMEDICAL COVERAGE

FLEXIBLE SPENDINGACCOUNTS

What is an FSA?A FSA is a Flexible Spending Account that allows participants to set aside money, before taxes, to use on eligible healthcare and dependent care expenses. Since the monies are withheld from your paycheck on a pre-tax basis, you save tax dollars and lower your taxable income.

Two Types of FSA’sHealthcare FSA: MedicalThe annual maximum amount each participant may contribute to the Health Care FSA is $2,550 per plan year.

• Deductible, Coinsurance, Office Visit Copays• Prescription• Hearing Services, Hearing Aids and Batteries• Vision Services and Eye Surgery• Dental Services and Orthodontia

Dependent Care FSA: DaycareThe annual maximum amount each participant may contribute to the Dependent Care FSA is $5,000 per plan year / per household (or $2,500 if married filingseparately).

• Before / After School Care Programs• Day Care and Nursery Schools• Preschool• Dependent Adult Day Care• Transportation Provided by Care Provider

Who is Our FSA Provider?Our Flexible Spending Accounts are administered by Ameriflex. If you have any questions regarding these benefits, please contact Ameriflex Customer Service Center at 888.868.3539 or visit https://participant.ameriflexbenefits.com.

When Can I Use My Funds?Healthcare FSA’s are fully funded at the beginning of your plan year for immediate use. Dependent Care FSA’s require that the funds be contributed before they can be used.

Use It or Lose It!Regarding the Healthcare FSA, any contributions that are not claimed for the plan year must be forfeited as required by Internal Revenue Service regulations (often referred to as the “use it or lose it” rule). You have a grace period to utilize the Prior Year’s funds until March 15, 2017. All Claims For Prior Year Funds Must Be Filed By March 31, 2017. Regarding the Dependent Care FSA, any funds left in this account at the end of the plan year will be forfeited. When you are no longer an employee, and have a balance in your FSA account, you will have 30 days to utilize those monies, or you will lose them.

How to Use Your FundsPay Me Back (Health Care or Dependent Care)Use out-of-pocket funds then request reimbursement from your FSA. File a claim online, by fax, email or mail.

19

For Non-Cardholders:

*Name - enter participants First and Last name*Employee ID - enter participant's social security number without dashes*Employer ID - this can be obtained by calling AmeriFlex’s Customer Service Dept.*New User ID - create a username specific to you*Password - create a password specific to you*Security Word - enter Mother's Maiden Name*E-Mail Address - enter your email address

Balances:Select the Accounts tab to view balances in all accounts. You can also view the Plan Year, Account Type, YTD Contributions, Annual Election, Disbursements YTD, and Disbursable Balance.

Statements:Under the Accounts tab, select Statement to prepare and print a cardholder statement. The statement will illustrate only those transactions that were successfully deducted from or deposited into the account.

History:Under the Accounts tab, select History to show a complete Transaction History. The Transaction History includes all attempted charges regardless of the success of those transactions.

Lost/Stolen Card:Under the Home tab, select Lost/Stolen Card to report your card lost or stolen. Please contact AmeriFlex to have a new cardissued.

Frequently Asked Questions:Under the Home tab, select Frequently Asked Questions to view FAQs such as definitions of terms, How Do I questions, etc.

Change Log-In Information:Select User Options from the top right corner of the screen. Within User Options you can change your password and email address.

AMERIFLEX® 302 FELLOWSHIP RD., STE. 100, MOUNT LAUREL, NEW JERSEY 08054 C ALL TOLL-FREE: 888.868.FLEX (3539) FAX: 888.631.1038

AmeriFlex Online Account InstructionsAccessing Your AmeriFlex Account via the Internet:Go to www.flex125.com. Select Employee from the left navigation menu. Next, select View Your Account Activity. You will be redirected to www.benefitspaymentsystem.com. Please note that pop-up blockers will need to be disabled in order to access this site.

To Create an Account:Click on the Participant Login button, then select Create Account from the main screen. All fields MUST be completed to create an account.

AMERIFLEX WEB-BASED FLEX ACCOUNT UTILIZATION®

www.flex125.com

20

MEDICAL COVERAGELIFE AND AD&D

COVERAGEBasic Life and AD&DLife insurance isn’t a fun thing to think about, and it may seem like an unnecessary expense. But if you have people who depend on you for financial support, then life insurance is really about protecting them in case something happens to you – your designated beneficiary would collect a financial benefit upon your death. The plans are administered by Dearborn National.

As your employer, we automatically provide a certain level of coverage for you and give you the opportunity to purchase additional coverage for you and your dependents.

Beneficiary DesignationIt is very important to designate a beneficiary for your life, supplemental life and AD&D policies - the person(s) who would receive your account balance in the event of your death. You may change/update your beneficiary information at any time. To name your beneficiary, you must complete a beneficiary designation form.

Optional Life & AD&DEmployees who wish to supplement their basic life insurance benefit may purchase additional coverage with the convenience of payroll deduction.

Guaranteed Issued Amounts (GI)Newly eligible employees are guaranteed a policy up tothe amount of $100,000 without being required toprovide any health information. For the spouse of anewly eligible employee, the GI amount is $25,000 andfor eligible dependents the GI amount is $10,000.

Evidence of Insurability (EOI)The GI amounts are only available to employees that enroll when they are first eligible. Anyone who chooses not to sign up during their initial enrollment opportunity will be required to provide evidence of good health and may be denied coverage. Evidence of insurability is also required if you elect an amount in excess of the GI amounts.

Note: No eligible person may be covered more than once under the Policy.

OPTIONAL LIFE AND AD&D

EmployeeYou must enroll to cover your dependents

- $10,000 to $500,000 Max - $10,000 Increments- $100,000 GI

Spouse

- $5,000 to $100,000 Max- Not to exceed 50% ofEmployee’s Election

- $5,000 Increments- $25,000 GI

Child(ren)Six months to 19 years (23 if FT Student)

- $10,000 Maximum- $1,000 Birth - six months

-$1,000-$10,000– six months-19 years- $1,000 Increments

AD&D Same as Optional Life

Age Reduction Schedule Same as Basic Life

Portability

If your employment ends, you may be able to convert your Group Life coverage to an Individual Life insurance policy or apply to port your group term life insurance coverage.

BASIC LIFE AND AD&D

Employee Protection1.5 times annual earnings to $200,000 Maximum.$200,000 GI

AD&D Coverage

Provides up to 100% of the Life benefit for loss of life and pays a percentage for loss of a limb due to an accident.

Age Reduction Schedule

Benefits will reduce to 35% at age 65 and to50% of original amount at age 70. Benefits terminate atretirement.

21

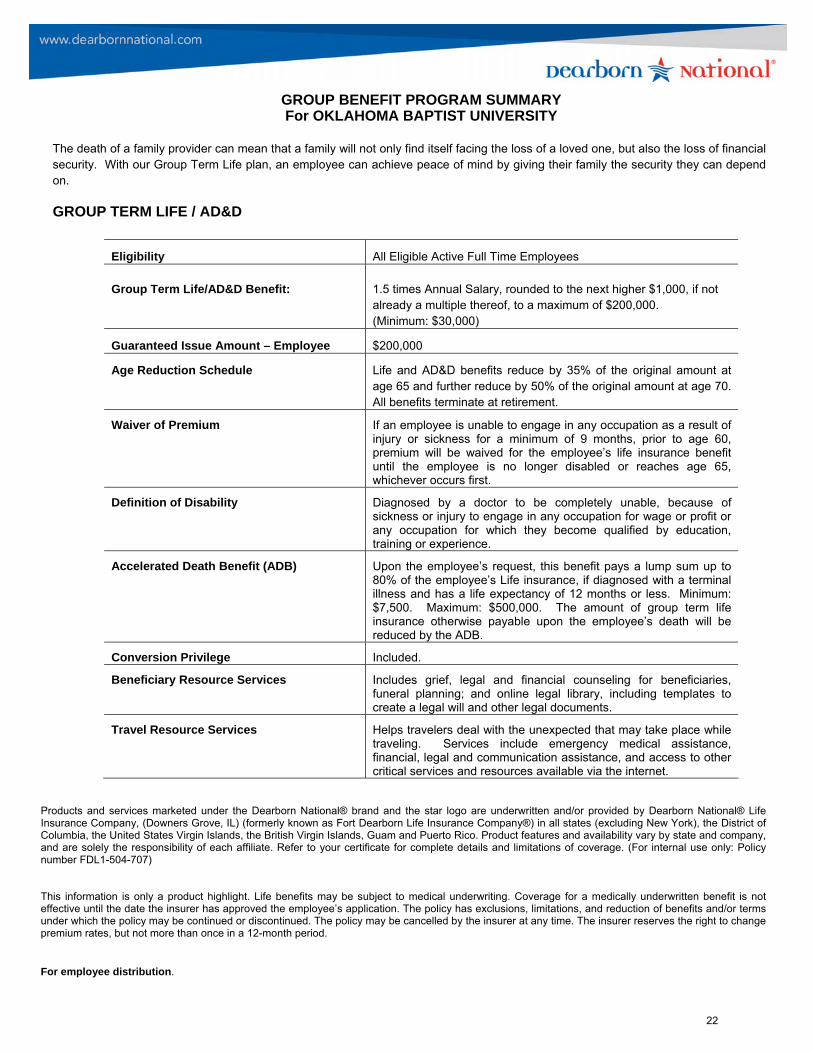

GROUP BENEFIT PROGRAM SUMMARY For OKLAHOMA BAPTIST UNIVERSITY

The death of a family provider can mean that a family will not only find itself facing the loss of a loved one, but also the loss of financial security. With our Group Term Life plan, an employee can achieve peace of mind by giving their family the security they can depend on.

GROUP TERM LIFE / AD&D

Products and services marketed under the Dearborn National® brand and the star logo are underwritten and/or provided by Dearborn National® Life Insurance Company, (Downers Grove, IL) (formerly known as Fort Dearborn Life Insurance Company®) in all states (excluding New York), the District of Columbia, the United States Virgin Islands, the British Virgin Islands, Guam and Puerto Rico. Product features and availability vary by state and company, and are solely the responsibility of each affiliate. Refer to your certificate for complete details and limitations of coverage. (For internal use only: Policy number FDL1-504-707)

This information is only a product highlight. Life benefits may be subject to medical underwriting. Coverage for a medically underwritten benefit is not effective until the date the insurer has approved the employee’s application. The policy has exclusions, limitations, and reduction of benefits and/or terms under which the policy may be continued or discontinued. The policy may be cancelled by the insurer at any time. The insurer reserves the right to change premium rates, but not more than once in a 12-month period.

For employee distribution.

Eligibility All Eligible Active Full Time Employees

Group Term Life/AD&D Benefit: 1.5 times Annual Salary, rounded to the next higher $1,000, if not already a multiple thereof, to a maximum of $200,000. (Minimum: $30,000)

Guaranteed Issue Amount – Employee $200,000

Age Reduction Schedule Life and AD&D benefits reduce by 35% of the original amount at age 65 and further reduce by 50% of the original amount at age 70. All benefits terminate at retirement.

Waiver of Premium If an employee is unable to engage in any occupation as a result of injury or sickness for a minimum of 9 months, prior to age 60, premium will be waived for the employee’s life insurance benefit until the employee is no longer disabled or reaches age 65, whichever occurs first.

Definition of Disability Diagnosed by a doctor to be completely unable, because of sickness or injury to engage in any occupation for wage or profit or any occupation for which they become qualified by education, training or experience.

Accelerated Death Benefit (ADB) Upon the employee’s request, this benefit pays a lump sum up to 80% of the employee’s Life insurance, if diagnosed with a terminal illness and has a life expectancy of 12 months or less. Minimum: $7,500. Maximum: $500,000. The amount of group term life insurance otherwise payable upon the employee’s death will be reduced by the ADB.

Conversion Privilege Included.

Beneficiary Resource Services Includes grief, legal and financial counseling for beneficiaries, funeral planning; and online legal library, including templates to create a legal will and other legal documents.

Travel Resource Services Helps travelers deal with the unexpected that may take place while traveling. Services include emergency medical assistance, financial, legal and communication assistance, and access to other critical services and resources available via the internet.

22

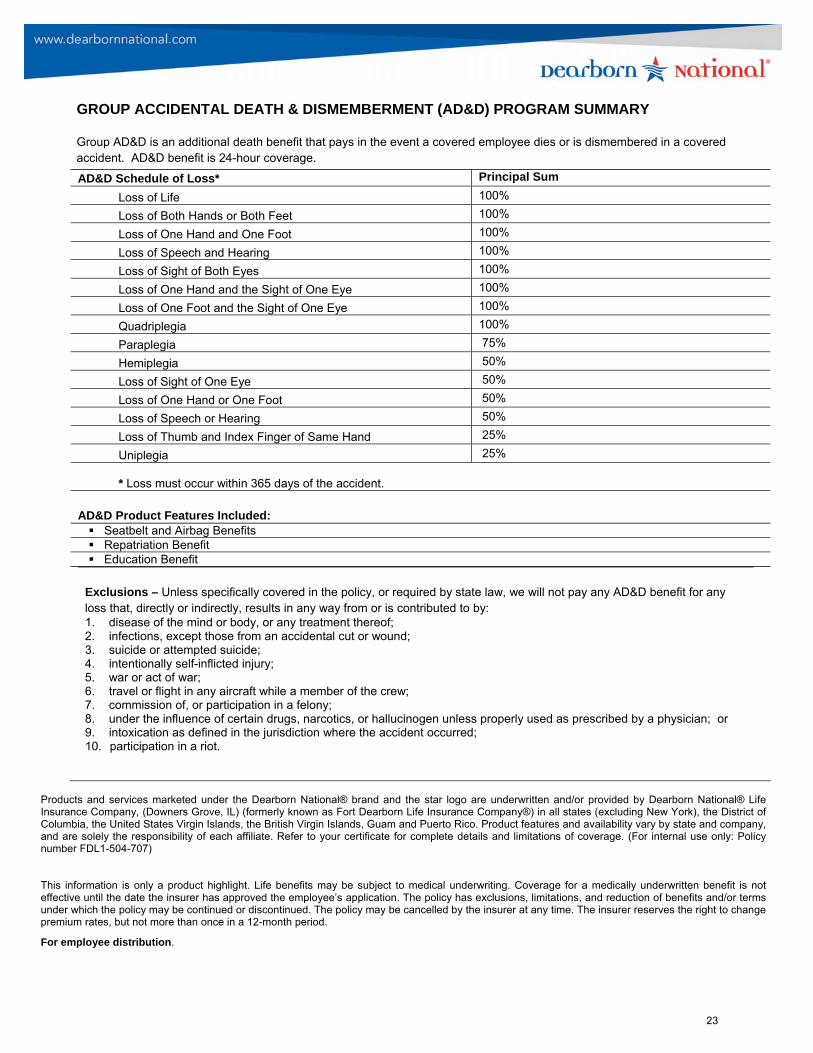

GROUP ACCIDENTAL DEATH & DISMEMBERMENT (AD&D) PROGRAM SUMMARY

Group AD&D is an additional death benefit that pays in the event a covered employee dies or is dismembered in a covered accident. AD&D benefit is 24-hour coverage.

AD&D Schedule of Loss* Principal Sum

Loss of Life 100%

Loss of Both Hands or Both Feet 100%

Loss of One Hand and One Foot 100%

Loss of Speech and Hearing 100%

Loss of Sight of Both Eyes 100%

Loss of One Hand and the Sight of One Eye 100%

Loss of One Foot and the Sight of One Eye 100%

Quadriplegia 100%

Paraplegia 75%

Hemiplegia 50%

Loss of Sight of One Eye 50%

Loss of One Hand or One Foot 50%

Loss of Speech or Hearing 50%

Loss of Thumb and Index Finger of Same Hand 25%

Uniplegia 25%

* Loss must occur within 365 days of the accident.

AD&D Product Features Included: Seatbelt and Airbag Benefits Repatriation Benefit Education Benefit

Exclusions – Unless specifically covered in the policy, or required by state law, we will not pay any AD&D benefit for any loss that, directly or indirectly, results in any way from or is contributed to by: 1. disease of the mind or body, or any treatment thereof;2. infections, except those from an accidental cut or wound;3. suicide or attempted suicide;4. intentionally self-inflicted injury;5. war or act of war;6. travel or flight in any aircraft while a member of the crew;7. commission of, or participation in a felony;8. under the influence of certain drugs, narcotics, or hallucinogen unless properly used as prescribed by a physician; or9. intoxication as defined in the jurisdiction where the accident occurred;10. participation in a riot.

Products and services marketed under the Dearborn National® brand and the star logo are underwritten and/or provided by Dearborn National® Life Insurance Company, (Downers Grove, IL) (formerly known as Fort Dearborn Life Insurance Company®) in all states (excluding New York), the District of Columbia, the United States Virgin Islands, the British Virgin Islands, Guam and Puerto Rico. Product features and availability vary by state and company, and are solely the responsibility of each affiliate. Refer to your certificate for complete details and limitations of coverage. (For internal use only: Policy number FDL1-504-707)

This information is only a product highlight. Life benefits may be subject to medical underwriting. Coverage for a medically underwritten benefit is not effective until the date the insurer has approved the employee’s application. The policy has exclusions, limitations, and reduction of benefits and/or terms under which the policy may be continued or discontinued. The policy may be cancelled by the insurer at any time. The insurer reserves the right to change premium rates, but not more than once in a 12-month period.

For employee distribution.

23

.

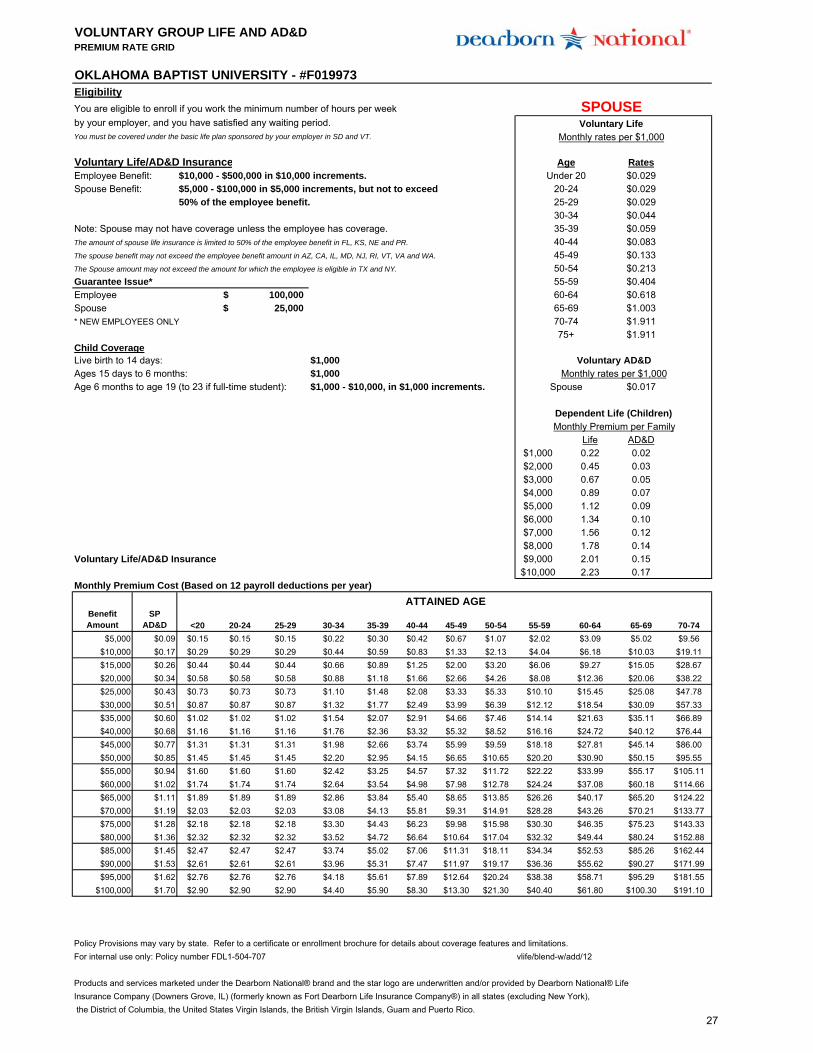

GROUP BENEFIT PROGRAM SUMMARY For OKLAHOMA BAPTIST UNIVERSITY - #F019973

The death of a family provider can mean that a family will not only find itself facing the loss of a loved one, but also the loss of financial security. With our Group Term Life plan, an employee can achieve peace of mind by giving their family the security they can depend on.

VOLUNTARY GROUP TERM LIFE/AD&D

Eligibility All Eligible Active Full Time Employees electing Voluntary Life

Group Term Life/AD&D Benefit: Employee $10,000 - $500,000, in increments of $10,000

Guaranteed Issue Amount* – Employee $100,000 *Guarantee issue amounts are based on a minimum participation requirement of 22% of alleligible employees. If participation requirements are not achieved, underwriting will beutilized on all employees and spouse applications.

Group Term Life/AD&D Benefit: Spouse (Includes Domestic Partners)

$5,000 - $100,000, in increments of $5,000, not to exceed 50% of the employee benefit amount.

Guaranteed Issue Amount – Spouse $25,000

Group Term Life/AD&D Benefit: Child(ren) Birth to 14 days: $1,000 Age 15 days to 6 months: $1,000 Age 6 months to 19 years (23 if full-time student): $1,000 - $10,000, in increments of $1,000

Grandfathered Benefits (Up to $500,000): If the Voluntary Life Participation Minimum stated in the Plan Design Summary above is met, all current amounts in force will be grandfathered, subject to the plan design maximums and the grandfathering limits stated. The Guarantee Issue amount shown above will only be offered to employees whose initial eligibility date (new hires) is on or after the effective date of coverage. Employees not previously covered, or those who have selected to increase their coverage, will need to provide satisfactory Evidence of Insurability. Should the Voluntary Life Participation Minimum not be met, grandfathering will not apply and satisfactory Evidence of Insurability will be required for all amounts by all applicants, including those participating in the prior carrier's plan.

Age Reduction Schedule None

Employee Contribution 100%

Waiver of Premium If an employee is unable to engage in any occupation as a result of injury or sickness for a minimum of 9 months, prior to age 60, premium will be waived for the employee’s life insurance benefit until the employee is no longer disabled or reaches age 65, whichever occurs first.

Accelerated Death Benefit (ADB) Upon the employee’s request, this benefit pays a lump sum up to 80% of the employee’s Life insurance, if diagnosed with a terminal illness and has a life expectancy of 12 months or less. Minimum: $7,500. Maximum: $500,000. The amount of group term life insurance otherwise payable upon the employee’s death will be reduced by the ADB.

Portability Feature (Life coverage) Included. (Employee & Dependent)

Conversion Privilege (Life coverage) Included.

Travel Resource Services Helps travelers deal with the unexpected that may take place while traveling. Services include emergency medical assistance, financial, legal and communication assistance, and access to other critical services and resources available via the internet.

Exclusions One-year suicide exclusion applies to Voluntary Group Term Life coverage. AD&D exclusions are the same as Basic AD&D exclusions.

This information is only a product highlight. Life benefits may be subject to medical underwriting. Coverage for a medically underwritten benefit is not effective until the date the insurer has approved the employee’s application. The policy has exclusions, limitations, and reduction of benefits and/or terms under which the policy may be continued or discontinued. The policy may be cancelled by the insurer at any time. The insurer reserves the right to change premium rates, but not more than once in a 12-month period.

Products and services marketed under the Dearborn National® brand and the star logo are underwritten and/or provided by Dearborn National® Life Insurance Company, (Downers Grove, IL) (formerly known as Fort Dearborn Life Insurance Company®) in all states (excluding New York), the District of Columbia, the United States Virgin Islands, the British Virgin Islands, Guam and Puerto Rico. Product features and availability vary by state and company, and are solely the responsibility of each affiliate. Refer to your certificate for complete details and limitations of coverage. (For internal use only: Policy number FDL1-504-707)

24

For employee distribution

GROUP ACCIDENTAL DEATH & DISMEMBERMENT (AD&D) PROGRAM SUMMARY

Group AD&D is an additional death benefit that pays in the event a covered employee dies or is dismembered in a covered accident. AD&D benefit is 24-hour coverage.

AD&D Schedule of Loss* Principal Sum

Loss of Life 100%

Loss of Both Hands or Both Feet 100%

Loss of One Hand and One Foot 100%

Loss of Speech and Hearing 100%

Loss of Sight of Both Eyes 100%

Loss of One Hand and the Sight of One Eye 100%

Loss of One Foot and the Sight of One Eye 100%

Quadriplegia 100%

Paraplegia 75%

Hemiplegia 50%

Loss of Sight of One Eye 50%

Loss of One Hand or One Foot 50%

Loss of Speech or Hearing 50%

Loss of Thumb and Index Finger of Same Hand 25%

Uniplegia 25%

* Loss must occur within 365 days of the accident.

AD&D Product Features Included: Seatbelt and Airbag Benefits Repatriation Benefit Education Benefit

Exclusions – Unless specifically covered in the policy, or required by state law, we will not pay any AD&D benefit for any loss that, directly or indirectly, results in any way from or is contributed to by: 1. disease of the mind or body, or any treatment thereof;2. infections, except those from an accidental cut or wound;3. suicide or attempted suicide;4. intentionally self-inflicted injury;5. war or act of war;6. travel or flight in any aircraft while a member of the crew;7. commission of, or participation in a felony;8. under the influence of certain drugs, narcotics, or hallucinogen unless properly used as prescribed by a physician; or9. intoxication as defined in the jurisdiction where the accident occurred;10. participation in a riot.

This information is only a product highlight. Life benefits may be subject to medical underwriting. Coverage for a medically underwritten benefit is not effective until the date the insurer has approved the employee’s application. The policy has exclusions, limitations, and reduction of benefits and/or terms under which the policy may be continued or discontinued. The policy may be cancelled by the insurer at any time. The insurer reserves the right to change premium rates, but not more than once in a 12-month period.

Products and services marketed under the Dearborn National® brand and the star logo are underwritten and/or provided by Dearborn National® Life Insurance Company, (Downers Grove, IL) (formerly known as Fort Dearborn Life Insurance Company®) in all states (excluding New York), the District of Columbia, the United States Virgin Islands, the British Virgin Islands, Guam and Puerto Rico. Product features and availability vary by state and company, and are solely the responsibility of each affiliate. Refer to your certificate for complete details and limitations of coverage. (For internal use only: Policy number FDL1-504-707)

For employee distribution

25

VOLUNTARY GROUP LIFE AND AD&DPREMIUM RATE GRID

Eligibility

You are eligible to enroll if you work the minimum number of hours per week by your employer, and you have satisfied any waiting period.You must be covered under the basic life plan sponsored by your employer in SD and VT.

Voluntary Life/AD&D Insurance RatesEmployee Benefit: $10,000 - $500,000 in $10,000 increments. $0.029Spouse Benefit: $5,000 - $100,000 in $5,000 increments, but not to exceed $0.029

50% of the employee benefit. $0.029$0.044

Note: Spouse may not have coverage unless the employee has coverage. $0.059The amount of spouse life insurance is limited to 50% of the employee benefit in FL, KS, NE and PR. $0.083The spouse benefit may not exceed the employee benefit amount in AZ, CA, IL, MD, NJ, RI, VT, VA and WA. $0.133The Spouse amount may not exceed the amount for which the employee is eligible in TX and NY. $0.213Guarantee Issue* $0.404Employee $0.618Spouse $1.003* NEW EMPLOYEES ONLY $1.911

$1.911Child CoverageLive birth to 14 days: $1,000Ages 15 days to 6 months: $1,000Age 6 months to age 19 (to 23 if full-time student): $1,000 - $10,000, in $1,000 increments. $0.017

Life AD&D$1,000 0.22 0.02$2,000 0.45 0.03$3,000 0.67 0.05$4,000 0.89 0.07$5,000 1.12 0.09$6,000 1.34 0.10$7,000 1.56 0.12$8,000 1.78 0.14

Voluntary Life/AD&D Insurance $9,000 2.01 0.15$10,000 2.23 0.17

Monthly Premium Cost (Based on 12 payroll deductions per year)

Benefit Amount

EE AD&D <20 20-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70-74

$10,000 $0.17 $0.29 $0.29 $0.29 $0.44 $0.59 $0.83 $1.33 $2.13 $4.04 $6.18 $10.03 $19.11$20,000 $0.34 $0.58 $0.58 $0.58 $0.88 $1.18 $1.66 $2.66 $4.26 $8.08 $12.36 $20.06 $38.22$30,000 $0.51 $0.87 $0.87 $0.87 $1.32 $1.77 $2.49 $3.99 $6.39 $12.12 $18.54 $30.09 $57.33$40,000 $0.68 $1.16 $1.16 $1.16 $1.76 $2.36 $3.32 $5.32 $8.52 $16.16 $24.72 $40.12 $76.44$50,000 $0.85 $1.45 $1.45 $1.45 $2.20 $2.95 $4.15 $6.65 $10.65 $20.20 $30.90 $50.15 $95.55$60,000 $1.02 $1.74 $1.74 $1.74 $2.64 $3.54 $4.98 $7.98 $12.78 $24.24 $37.08 $60.18 $114.66$70,000 $1.19 $2.03 $2.03 $2.03 $3.08 $4.13 $5.81 $9.31 $14.91 $28.28 $43.26 $70.21 $133.77$80,000 $1.36 $2.32 $2.32 $2.32 $3.52 $4.72 $6.64 $10.64 $17.04 $32.32 $49.44 $80.24 $152.88$90,000 $1.53 $2.61 $2.61 $2.61 $3.96 $5.31 $7.47 $11.97 $19.17 $36.36 $55.62 $90.27 $171.99

$100,000 $1.70 $2.90 $2.90 $2.90 $4.40 $5.90 $8.30 $13.30 $21.30 $40.40 $61.80 $100.30 $191.10$110,000 $1.87 $3.19 $3.19 $3.19 $4.84 $6.49 $9.13 $14.63 $23.43 $44.44 $67.98 $110.33 $210.21$120,000 $2.04 $3.48 $3.48 $3.48 $5.28 $7.08 $9.96 $15.96 $25.56 $48.48 $74.16 $120.36 $229.32$130,000 $2.21 $3.77 $3.77 $3.77 $5.72 $7.67 $10.79 $17.29 $27.69 $52.52 $80.34 $130.39 $248.43$140,000 $2.38 $4.06 $4.06 $4.06 $6.16 $8.26 $11.62 $18.62 $29.82 $56.56 $86.52 $140.42 $267.54$150,000 $2.55 $4.35 $4.35 $4.35 $6.60 $8.85 $12.45 $19.95 $31.95 $60.60 $92.70 $150.45 $286.65$200,000 $3.40 $5.80 $5.80 $5.80 $8.80 $11.80 $16.60 $26.60 $42.60 $80.80 $123.60 $200.60 $382.20$250,000 $4.25 $7.25 $7.25 $7.25 $11.00 $14.75 $20.75 $33.25 $53.25 $101.00 $154.50 $250.75 $477.75$300,000 $5.10 $8.70 $8.70 $8.70 $13.20 $17.70 $24.90 $39.90 $63.90 $121.20 $185.40 $300.90 $573.30$350,000 $5.95 $10.15 $10.15 $10.15 $15.40 $20.65 $29.05 $46.55 $74.55 $141.40 $216.30 $351.05 $668.85$400,000 $6.80 $11.60 $11.60 $11.60 $17.60 $23.60 $33.20 $53.20 $85.20 $161.60 $247.20 $401.20 $764.40$450,000 $7.65 $13.05 $13.05 $13.05 $19.80 $26.55 $37.35 $59.85 $95.85 $181.80 $278.10 $451.35 $859.95$500,000 $8.50 $14.50 $14.50 $14.50 $22.00 $29.50 $41.50 $66.50 $106.50 $202.00 $309.00 $501.50 $955.50

Policy Provisions may vary by state. Refer to a certificate or enrollment brochure for details about coverage features and limitations.For internal use only: Policy number FDL1-504-707 vlife/blend-w/add/12

Products and services marketed under the Dearborn National® brand and the star logo are underwritten and/or provided by Dearborn National® LifeInsurance Company (Downers Grove, IL) (formerly known as Fort Dearborn Life Insurance Company®) in all states (excluding New York), the District of Columbia, the United States Virgin Islands, the British Virgin Islands, Guam and Puerto Rico.

OKLAHOMA BAPTIST UNIVERSITY - #F019973

100,000$

45-49

Age

ATTAINED AGE

35-3940-44

60-6455-5950-54

30-34

20-24

Monthly Premium per Family

25,000$

25-29

EMPLOYEE Voluntary Life Monthly

rates per $1,000

Dependent Life (Children)

65-69

EmployeeMonthly rates per $1,000

70-7475+

Voluntary AD&D

Under 20

26

VOLUNTARY GROUP LIFE AND AD&DPREMIUM RATE GRID

Eligibility

You are eligible to enroll if you work the minimum number of hours per week by your employer, and you have satisfied any waiting period.You must be covered under the basic life plan sponsored by your employer in SD and VT.

Voluntary Life/AD&D Insurance RatesEmployee Benefit: $10,000 - $500,000 in $10,000 increments. $0.029Spouse Benefit: $5,000 - $100,000 in $5,000 increments, but not to exceed $0.029

50% of the employee benefit. $0.029$0.044

Note: Spouse may not have coverage unless the employee has coverage. $0.059The amount of spouse life insurance is limited to 50% of the employee benefit in FL, KS, NE and PR. $0.083The spouse benefit may not exceed the employee benefit amount in AZ, CA, IL, MD, NJ, RI, VT, VA and WA. $0.133The Spouse amount may not exceed the amount for which the employee is eligible in TX and NY. $0.213Guarantee Issue* $0.404Employee $0.618Spouse $1.003* NEW EMPLOYEES ONLY $1.911

$1.911Child CoverageLive birth to 14 days: $1,000Ages 15 days to 6 months: $1,000Age 6 months to age 19 (to 23 if full-time student): $1,000 - $10,000, in $1,000 increments. $0.017

Life AD&D$1,000 0.22 0.02$2,000 0.45 0.03$3,000 0.67 0.05$4,000 0.89 0.07$5,000 1.12 0.09$6,000 1.34 0.10$7,000 1.56 0.12$8,000 1.78 0.14

Voluntary Life/AD&D Insurance $9,000 2.01 0.15$10,000 2.23 0.17

Monthly Premium Cost (Based on 12 payroll deductions per year)

Benefit Amount

SP AD&D <20 20-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70-74

$5,000 $0.09 $0.15 $0.15 $0.15 $0.22 $0.30 $0.42 $0.67 $1.07 $2.02 $3.09 $5.02 $9.56$10,000 $0.17 $0.29 $0.29 $0.29 $0.44 $0.59 $0.83 $1.33 $2.13 $4.04 $6.18 $10.03 $19.11$15,000 $0.26 $0.44 $0.44 $0.44 $0.66 $0.89 $1.25 $2.00 $3.20 $6.06 $9.27 $15.05 $28.67$20,000 $0.34 $0.58 $0.58 $0.58 $0.88 $1.18 $1.66 $2.66 $4.26 $8.08 $12.36 $20.06 $38.22$25,000 $0.43 $0.73 $0.73 $0.73 $1.10 $1.48 $2.08 $3.33 $5.33 $10.10 $15.45 $25.08 $47.78$30,000 $0.51 $0.87 $0.87 $0.87 $1.32 $1.77 $2.49 $3.99 $6.39 $12.12 $18.54 $30.09 $57.33$35,000 $0.60 $1.02 $1.02 $1.02 $1.54 $2.07 $2.91 $4.66 $7.46 $14.14 $21.63 $35.11 $66.89$40,000 $0.68 $1.16 $1.16 $1.16 $1.76 $2.36 $3.32 $5.32 $8.52 $16.16 $24.72 $40.12 $76.44$45,000 $0.77 $1.31 $1.31 $1.31 $1.98 $2.66 $3.74 $5.99 $9.59 $18.18 $27.81 $45.14 $86.00$50,000 $0.85 $1.45 $1.45 $1.45 $2.20 $2.95 $4.15 $6.65 $10.65 $20.20 $30.90 $50.15 $95.55$55,000 $0.94 $1.60 $1.60 $1.60 $2.42 $3.25 $4.57 $7.32 $11.72 $22.22 $33.99 $55.17 $105.11$60,000 $1.02 $1.74 $1.74 $1.74 $2.64 $3.54 $4.98 $7.98 $12.78 $24.24 $37.08 $60.18 $114.66$65,000 $1.11 $1.89 $1.89 $1.89 $2.86 $3.84 $5.40 $8.65 $13.85 $26.26 $40.17 $65.20 $124.22$70,000 $1.19 $2.03 $2.03 $2.03 $3.08 $4.13 $5.81 $9.31 $14.91 $28.28 $43.26 $70.21 $133.77$75,000 $1.28 $2.18 $2.18 $2.18 $3.30 $4.43 $6.23 $9.98 $15.98 $30.30 $46.35 $75.23 $143.33$80,000 $1.36 $2.32 $2.32 $2.32 $3.52 $4.72 $6.64 $10.64 $17.04 $32.32 $49.44 $80.24 $152.88$85,000 $1.45 $2.47 $2.47 $2.47 $3.74 $5.02 $7.06 $11.31 $18.11 $34.34 $52.53 $85.26 $162.44$90,000 $1.53 $2.61 $2.61 $2.61 $3.96 $5.31 $7.47 $11.97 $19.17 $36.36 $55.62 $90.27 $171.99$95,000 $1.62 $2.76 $2.76 $2.76 $4.18 $5.61 $7.89 $12.64 $20.24 $38.38 $58.71 $95.29 $181.55

$100,000 $1.70 $2.90 $2.90 $2.90 $4.40 $5.90 $8.30 $13.30 $21.30 $40.40 $61.80 $100.30 $191.10

Policy Provisions may vary by state. Refer to a certificate or enrollment brochure for details about coverage features and limitations.For internal use only: Policy number FDL1-504-707 vlife/blend-w/add/12

Products and services marketed under the Dearborn National® brand and the star logo are underwritten and/or provided by Dearborn National® LifeInsurance Company (Downers Grove, IL) (formerly known as Fort Dearborn Life Insurance Company®) in all states (excluding New York), the District of Columbia, the United States Virgin Islands, the British Virgin Islands, Guam and Puerto Rico.

Voluntary AD&DMonthly rates per $1,000

Spouse

Dependent Life (Children)Monthly Premium per Family

ATTAINED AGE

25,000$ 65-6970-7475+

50-5455-59

100,000$ 60-64

20-2425-2930-3435-3940-4445-49

OKLAHOMA BAPTIST UNIVERSITY - #F019973

SPOUSEVoluntary Life

Monthly rates per $1,000

AgeUnder 20

27

MEDICAL COVERAGEDISABILITY COVERAGE

Disability CoverageYou receive Long Term Disability coverage to replace a portion or your income if you become disabled due to a non-work related injury or illness.

An illness or injury that keeps you out of work for a long period of time can be financially devastating for you and your family. These plans are designed to help protect your financial security by providing replacement income if you are disabled due to anon-work related injury or illness.

Your disability benefits coordinate with other sources of disability income you receive, such as Social Security, Workers Compensation and State Disability, to provide you with a steady source of income.

LONG-TERM DISABILITY (LTD)

Benefits Begin After 90 Days of Disability

Benefit Duration Normal Retirement Age

Income Replaced 60% of Earnings

Maximum Benefit $8,000 Per Month

28

How do I report a long-term disability (LTD) claim? Simply do one of the following:

Call toll-free 1.800.36.Cigna (24462) or 1.866.562.8421(Español). A representative will walk you through the process.

Fill out a claim form online at myCigna.com.

When do I report a claim? At least 30 days before the start of your LTD.

What information do I need? Before you call or go online, please have this information handy:

Your name, address, phone number, birth date, Social Securitynumber and email address.

Employment information, such as date hired and job title.

The reason for your claim – illness, injury or pregnancy.

A description of your illness, symptoms, and/or diagnosis.Include the date your symptoms started and if you’ve had thesesymptoms before.

Workers’ compensation claims you’ve filed or plan to file.

Details about doctor, hospital or clinic visits, including datesand contact information.

What happens next? During the call, we’ll ask for your permission to get your medical

information. Here’s how it works:

After you give us your claim information, you’ll be transferred toa recorded message.

Listen to the recording and answer “Yes” or “No” to the questions.

At the end of the recording, say “Yes” if you give permission or“No” if you do not.

You can cancel your permission at any time by calling yourCigna claim manager.

After the call, Cigna will send you a letter. It’ll include a copy of the recorded message for your records. It’ll also include a form that gives us permission to get other information we may need to finish

processing your claim. Please sign and return that form. Check with your doctor to see if there are any other forms you need to sign.

A Cigna claim manager will call you and your employer for a list of

your job requirements. The claim manager will also call your doctor for your medical records. This information will help us figure out how long you may be out of work, and the benefits you may be able

to receive.

What happens if my claim is approved? Cigna will send you an approval letter that gives you an

explanation of your benefits.

Cigna will tell your employer that we approved your claim, andthe date you plan to return to work.

What happens if my claim is denied? Cigna will send you a letter that explains why. The letter will also

tell you how you can appeal the decision.

Cigna will let your employer know the claim is denied.

You should call your employer when you get the letter to discussyour return-to-work date.

How to report a LONG-TERM DISABILITY CLAIM Under your company’s group disability insurance plan

How to Report a Disability 1.800.36.Cigna (24462) or 1.866.562.8421 (Español)

Visit: myCigna.com

Please have this information handy:

Your name, address, phone number, birth date, date of hire,Social Security number and your employer’s name, address andphone number.

Date of your claim and when you plan to return to work. If you’repregnant, give your expected delivery date.

Name, address and phone number of each doctor you areseeing for this absence.

Cut and carry for easy reference

If you need immediate medical attention, please call 911

29

What can I expect while I’m out? Your Cigna claim manager will stay in touch to help you return to work quickly and safely. We may work with you, your doctor and your employer to talk about different work options. This may include

an adjustment to your job or work schedule. Your employer may also call you to check on your progress and offer support.

What if I plan to return to work when my long-term disability benefits end? Your Cigna claim manager may work with your employer on any

return-to-work plans. Your benefit payments will be calculated by the exact date you return to work, and whether or not you return to work part-time or full-time. This will also help determine if you qualify

for continued payments.

Question? Call 1.800.36.Cigna (24462). A Cigna representative is available to help you between 7:00 am and 7:00 pm CST.

If you have a question regarding an existing claim or you need plan

information, please contact your (inset claim office name claim

office) claim office at (insert claim office phone number).

“Cigna” is a registered service mark, and the “Tree of Life” logo and GO YOU are service marks, of Cigna Intellectual Property, Inc., licensed for use by Cigna Corporation and its operating subsidiaries. All products and services are provided exclusively by such operating subsidiaries and not by Cigna Corporation. Such operating subsidiaries include Life Insurance Company of North America, Cigna Life Insurance Company of New York, and Connecticut General Life Insurance Company. All models are used for illustrative purposes only. ©2012 Cigna. Some content provided under license. 617496l LTD 859634

30

MEDICAL COVERAGEEm

ployee Assistance (EAP) / Life Assistance Program (LAP)

Employee Assistance ProgramPersonal issues, planning for life events or simply managing daily life can affect your work, health and family.Cigna provides support, resources and information for personal and work-life issues. Cigna is company-sponsored, confidential and provided at no charge to you and your dependents.

Confidential CounselingThis no-cost counseling service helps you address stress, relationship and other personal issues you and your family may face. Cigna Advocates, who are available to you 24/7, will listen to your concerns and quickly refer you to in-person counseling and other local resources for:

• Stress, anxiety and depression • Job pressures• Relationship/marital conflicts • Grief and loss• Problems with children • Substance abuse

Other Information and ResourcesIn addition to Confidential Counseling services, Cigna provides many services and resources to assist you with:

• Financial Information and Resources• Legal Consultation• Parenting• Online Skill Builders• Self- Service Support• Help for New Parents

Call to get the assistance you need:Toll Free – 800-538-3543or visit www.cignabehavior.com/CGI.com

31

Whatever life throws at you - THROW IT OUR WAY.

“Cigna,” the “Tree of Life” logo and “GO YOU” are registered service marks of Cigna Intellectual Property, Inc., licensed for use by Cigna Corporation and its operating subsidiaries. All products and services are provided by or through such operating subsidiaries and not by Cigna Corporation. Such operating subsidiaries include Connecticut General Life Insurance Company, Cigna Health and Life Insurance Company, Life Insurance Company of North America, Cigna Life Insurance Company of New York, Cigna Behavioral Health, Inc., and HMO or service company subsidiaries of Cigna Health Corporation.

877376 06/14 © 2014 Cigna. Some content provided under license.

1. Some Healthy Rewards programs are not available in all states. If your Cigna plan includes coverage for any of these services, this program is in addition to, not instead of, your plan benefits. A discount program is NOT insurance, and you must pay the entire discounted charge.

2. Legal consultations and discounts are excluded for employment-related issues.

Life. Just when you think you have it figured out, along comes a challenge. But whether those challenges are big or small, your Life Assistance Program is available to help you and your family find a solution and restore your peace of mind.

Call us anytime, any day.

We’re just a phone call away whenever you need us – at no cost to you. An advocate is ready to help assess your needs and develop a solution to help resolve your concerns. He or she can also direct you to an array of resources in your community and online tools, including an article library.

Visit a specialist.

For face-to-face assistance, you have three sessions available to you and your household members. Call us to request a referral.

Reward yourself.

Access your Healthy Rewards®1 discount program for discounts on a range of health and wellness services and products from participating providers.

Achieve work/life balance.

It’s a constant challenge. If you’d like help handling life’s demands, call us for extra support. We can provide guidance or a referral to a service in your community on topics such as:

Legal consultation.2 Receive a 30-minute free consultation and up to a 25% discount on select fees.

Parenting. Receive guidance on child development, sibling rivalry, separation anxiety and much more.

Senior care. Learn about challenges and solutions associated with caring for an aging loved one.

Child care. Whether you need care all day or just after school, find a place that’s right for your family.

Pet Care. From grooming to boarding to veterinary services, find what you need to care for your pet.

Temporary back-up care. Don’t let an unplanned event get the best of you – find back-up child care.

Life Assistance Program 24/7