christophe schmitt evp faurecia emissions control technologies

TRANSCRIPT

Investor day •

November 25, 2013

Christophe Schmitt EVP

Faurecia

Emissions Control Technologies

Prop

erty

of Fa

urec

ia -D

uplic

ation

proh

ibite

d

2Investor day • November 25, 2013

FECT is the world market leader in emissions control

Complete lines11m parts/year

Mufflers20m

parts/year

Catalytic converters23m

parts/year

Manifolds4m parts/year

Diesel particulate filter3m

parts/year

FECT is number 1 in emissions control

Widest geographical presence for manufacturing and engineering

Large portfolio of products and technologies for every type of vehicle and engine

Global program management25% market share

North

America

South America

AsiaEurope

1 R&D center10 plants

2 JIT

1 R&D center3 plants

6 JIT

2 R&D centers19 plants

16 JIT 3 R&D centers

18 plants5 JIT

Commercial vehicles

0.5m parts/year

7R&D centers

22Countries

19,800 Employees

79 Sites

€6.1bn Total sales 2012€3.2bn

Product sales

Prop

erty

of Fa

urec

ia -D

uplic

ation

proh

ibite

d

3Investor day • November 25, 2013

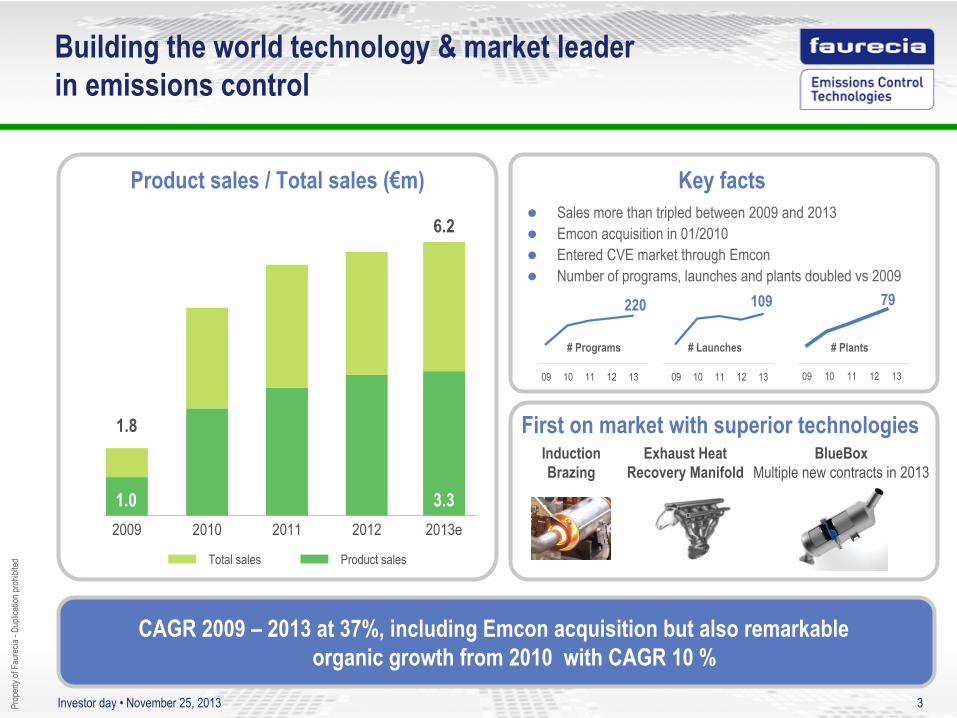

CAGR 2009 –

2013 at 37%, including Emcon

acquisition but also remarkable organic growth from 2010 with CAGR 10 %

Product sales / Total sales (€m)

2009 2010 2011 2012 2013e

6.2

Product salesTotal sales

Sales more than tripled between 2009 and 2013

Emcon

acquisition in 01/2010

Entered CVE market through Emcon

Number of programs, launches and plants doubled vs

2009

220

09 10 11 12 13 09 10 11 12 13 09 10 11 12 13

109 79

# Plants# Launches# Programs

1.8

Building the world technology & market leader in emissions control

Key facts

First on market with superior technologies Induction Brazing

Exhaust

Heat

Recovery

ManifoldBlueBox

Multiple new contracts

in 2013

3.31.0

Prop

erty

of Fa

urec

ia -D

uplic

ation

proh

ibite

d

4Investor day • November 25, 2013

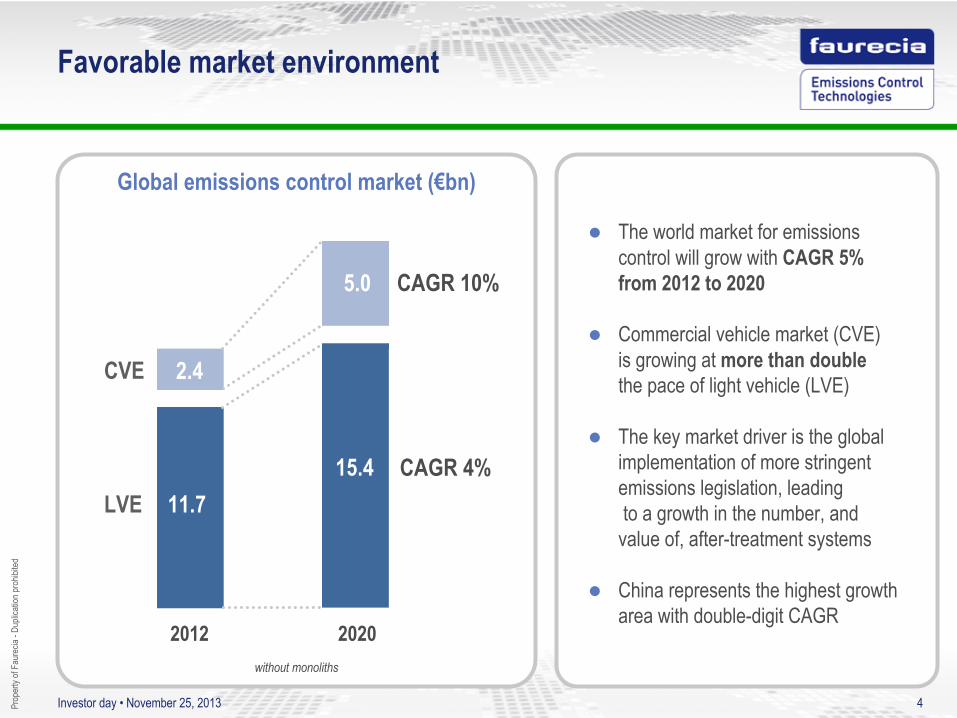

2020

CAGR 10%

CAGR 4%

5.0

15.4

without

monoliths

Favorable market

environment

Global emissions

control market

(€bn)

The world market for emissions control will grow with CAGR 5% from 2012 to 2020

Commercial vehicle market (CVE) is growing at more than double

the pace of light vehicle (LVE)

The key market driver is the global implementation of more stringent emissions legislation, leading

to a growth in the number, and value of, after-treatment systems

China represents the highest growth area with double-digit CAGR

2012

11.7

2.4CVE

LVE

Prop

erty

of Fa

urec

ia -D

uplic

ation

proh

ibite

d

5Investor day • November 25, 2013

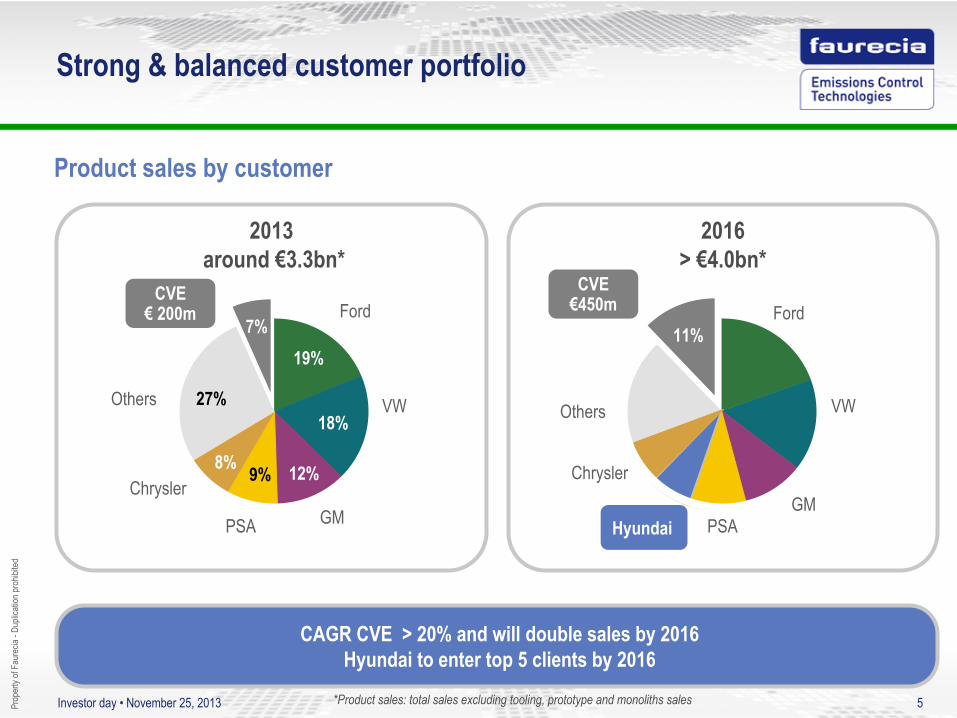

Strong

& balanced

customer

portfolio

Product sales by customer

2013 around €3.3bn*

2016> €4.0bn*

CAGR CVE > 20% and will double sales by 2016Hyundai to enter top 5 clients by 2016

*Product sales: total sales excluding

tooling, prototype and monoliths

sales

19%

18%27% VW

GMPSA

Others

Ford

Chrysler

CVE€

200m 7%

Hyundai

VW

GMPSA

Others

Ford

Chrysler

11%

CVE€450m

8% 9% 12%

Prop

erty

of Fa

urec

ia -D

uplic

ation

proh

ibite

d

6Investor day • November 25, 2013

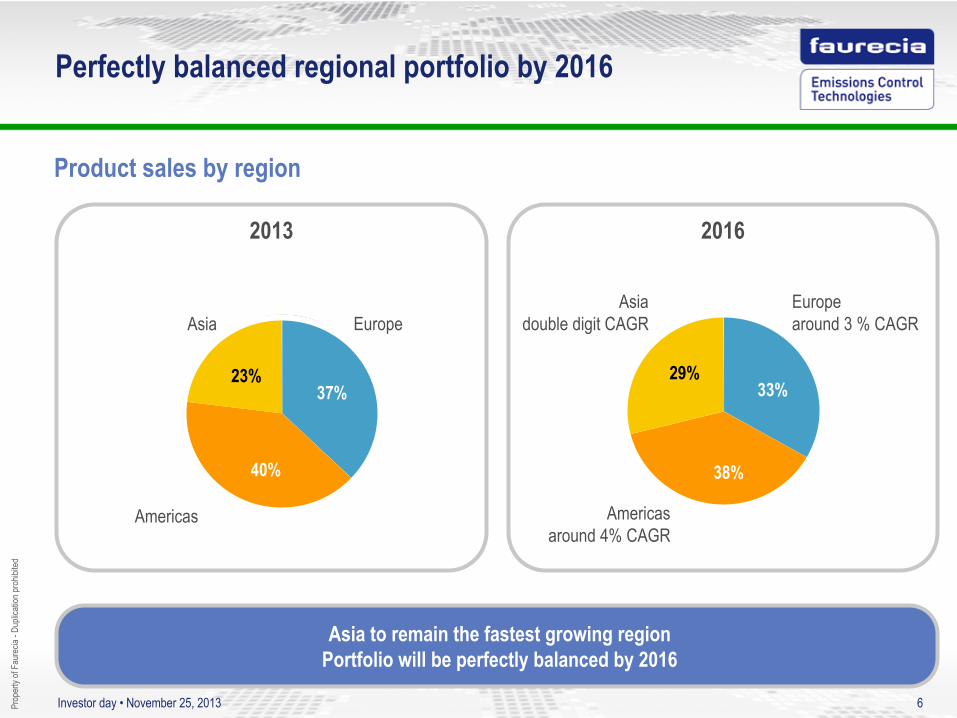

Perfectly balanced regional portfolio by 2016

23%

40%

37%29%

38%

33%

EuropeAsiaEuropearound

3 % CAGR

Americasaround

4% CAGR

Asia

double digit CAGR

Americas

CAGR > 5 %

Asia to remain the fastest growing regionPortfolio will

be

perfectly

balanced

by 2016

Product sales by region

2013 2016

Prop

erty

of Fa

urec

ia -D

uplic

ation

proh

ibite

d

7Investor day • November 25, 2013

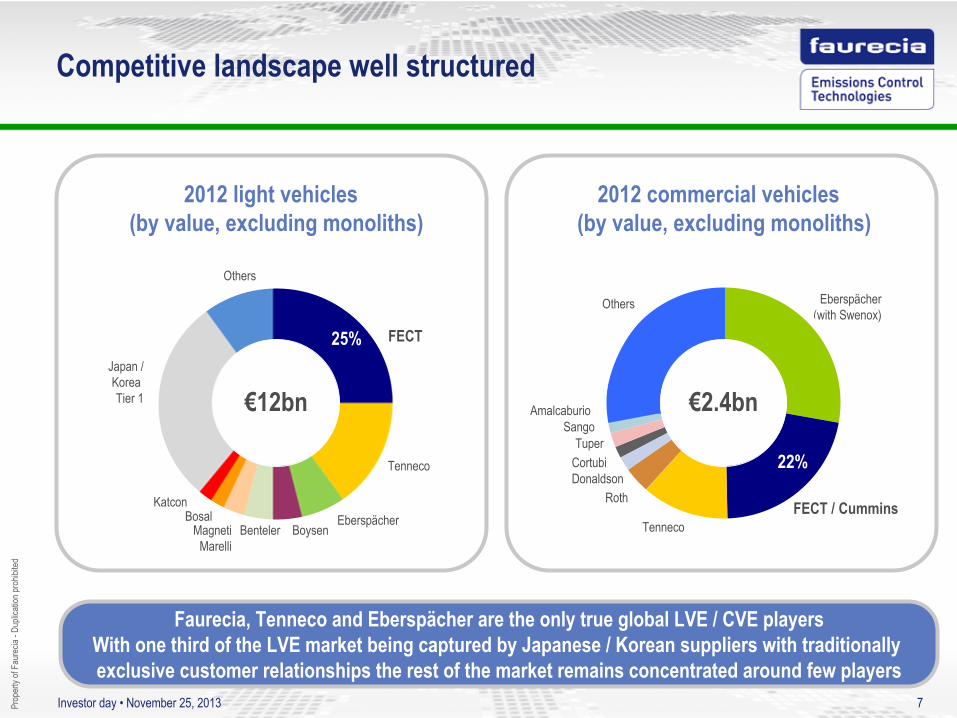

Competitive

landscape

well structured

2012 light vehicles (by value, excluding monoliths)

2012 commercial vehicles (by value, excluding monoliths)

22%

Others Eberspächer(with Swenox)

RothDonaldsonCortubiTuper

SangoAmalcaburio

Tenneco

Faurecia, Tenneco and Eberspächer

are the only true global LVE / CVE playersWith

one third

of the LVE market

being

captured

by Japanese

/ Korean

suppliers

with

traditionally exclusive customer

relationships

the rest

of the market

remains

concentrated

around

few players

25%

Others

KatconBosal

Tenneco

FECT

€12bn

Magneti

Marelli

Japan /

Korea Tier 1

Eberspächer

€2.4bn

BoysenBentelerFECT / Cummins

22%

Prop

erty

of Fa

urec

ia -D

uplic

ation

proh

ibite

d

8Investor day • November 25, 2013

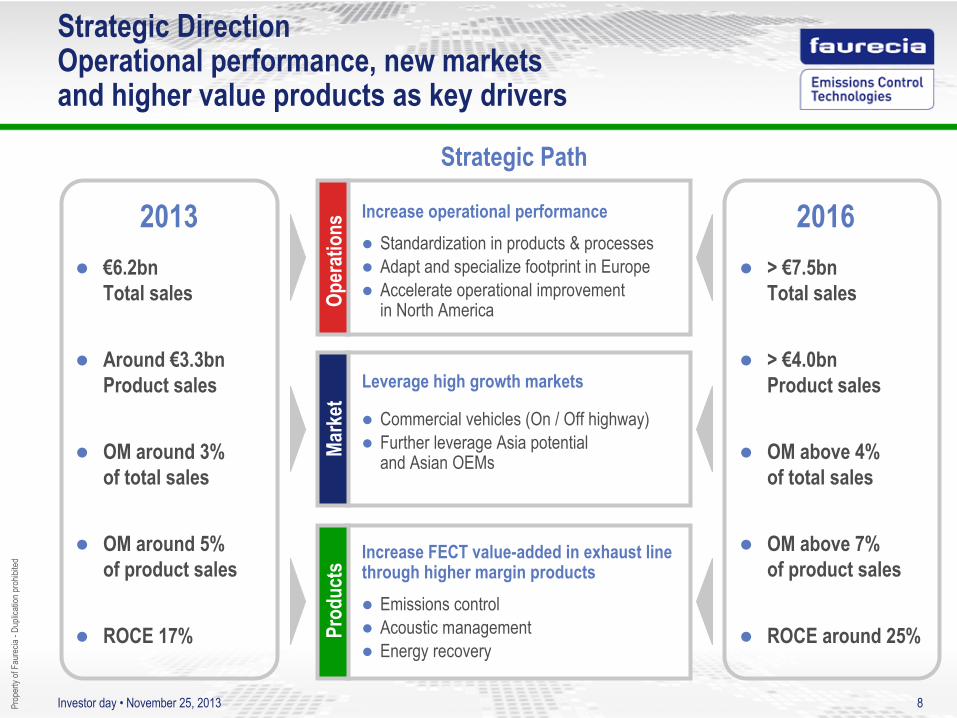

Prod

ucts

Emissions control

Acoustic management

Energy

recovery

Increase FECT value-added in exhaust line

through higher margin products

Mark

et

Commercial vehicles (On / Off highway)

Further

leverage

Asia

potential

and Asian

OEMs

Leverage high growth markets

Oper

atio

ns

Standardization in products & processes

Adapt and specialize footprint in Europe

Accelerate operational improvement in North America

Increase operational performance2013

€6.2bn Total sales

Around €3.3bn Product sales

OM around 3% of total sales

OM around 5% of product

sales

ROCE 17%

Strategic

Direction Operational

performance, new markets

and higher

value products

as key

drivers

Strategic

Path

2016

> €7.5bn Total sales

> €4.0bn Product sales

OM above 4% of total sales

OM above 7% of product sales

ROCE around 25%

Prop

erty

of Fa

urec

ia -D

uplic

ation

proh

ibite

d

9Investor day • November 25, 2013

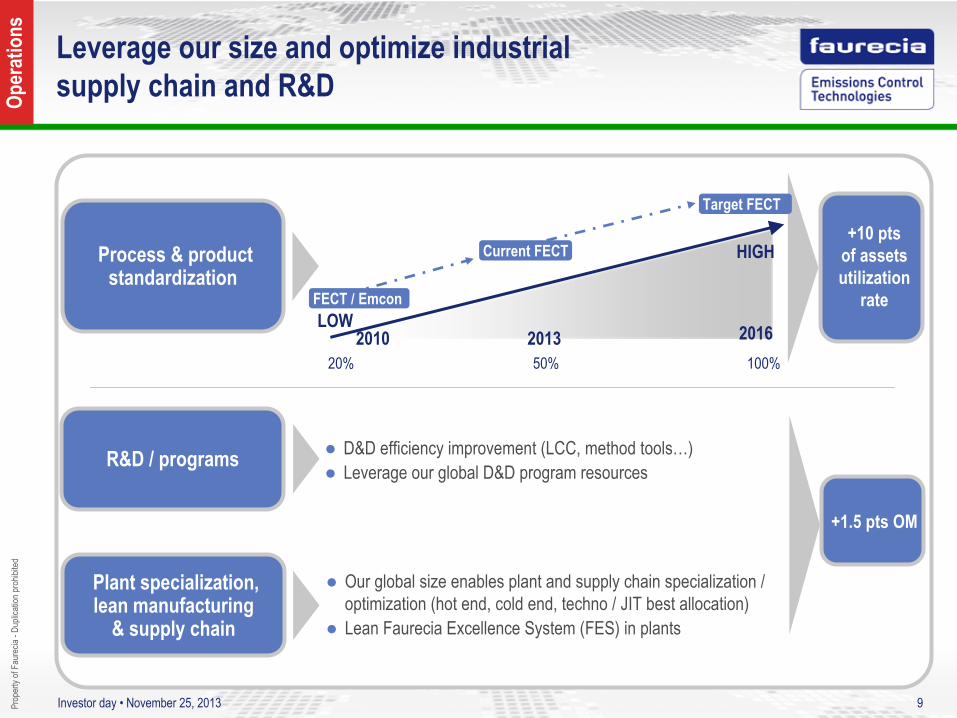

Leverage our size and optimize industrial supply chain and R&D

Process & product standardization

LOW

HIGH

20% 50% 100%

Current FECT

Target FECT

2010 2016

FECT / Emcon

D&D efficiency improvement (LCC, method tools…)

Leverage our global D&D program resourcesR&D / programs

Our global size enables plant and supply chain specialization / optimization (hot end, cold end, techno / JIT best allocation)

Lean Faurecia

Excellence System (FES) in plants

Plant specialization, lean manufacturing

& supply chain

2013

+10 pts of assets utilization

rate

+1.5 pts OM

Oper

atio

ns

Prop

erty

of Fa

urec

ia -D

uplic

ation

proh

ibite

d

10Investor day • November 25, 2013

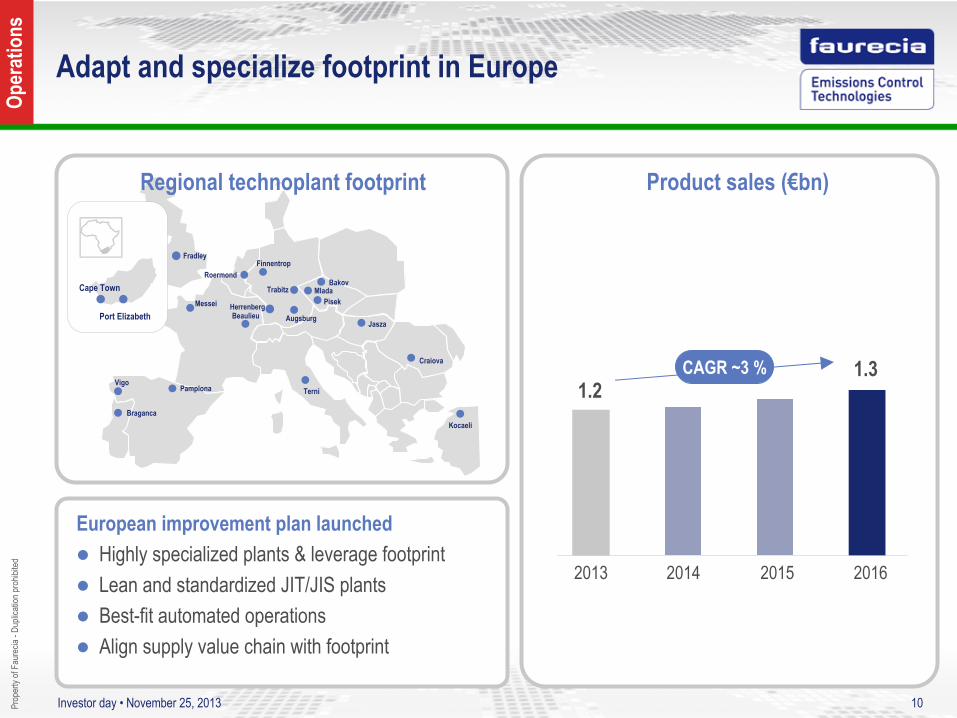

Adapt and specialize footprint in Europe

1.31.2

European improvement plan launched Highly specialized plants & leverage footprint Lean and standardized JIT/JIS plants Best-fit automated operations Align supply value chain with footprint

Braganca

PamplonaVigo

Beaulieu

BakovMlada

AugsburgJasza

Terni

Pisek

Roermond

Trabitz

Fradley

Kocaeli

Craiova

HerrenbergMessei

Finnentrop

Port Elizabeth

Cape Town

2013 2014 2015 2016

CAGR ~3 %

Oper

atio

ns

Product sales (€bn)Regional technoplant

footprint

Prop

erty

of Fa

urec

ia -D

uplic

ation

proh

ibite

d

11Investor day • November 25, 2013

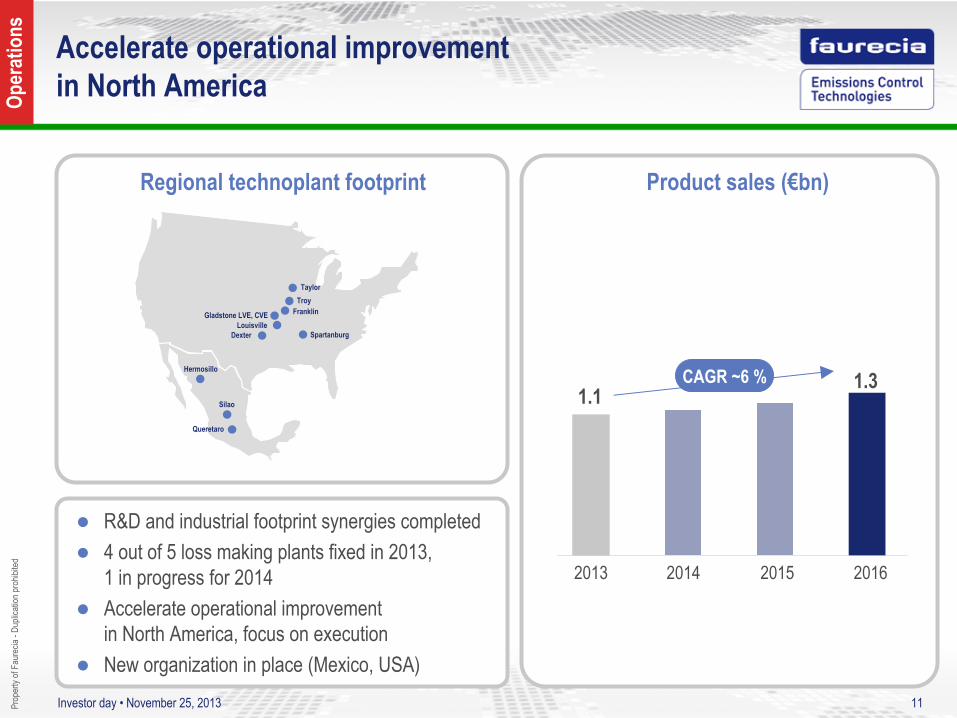

Accelerate operational improvement in North America

1.31.1

R&D and industrial footprint synergies completed

4 out of 5 loss making

plants fixed

in 2013, 1 in progress

for 2014

Accelerate operational improvement in North America, focus on execution

New organization in place (Mexico, USA)

2013 2014 2015 2016

CAGR ~6 %Hermosillo

Silao

Queretaro

Dexter SpartanburgLouisville

Gladstone LVE, CVE

TaylorTroy

Franklin

Oper

atio

ns

Product sales (€bn)Regional technoplant

footprint

Prop

erty

of Fa

urec

ia -D

uplic

ation

proh

ibite

d

12Investor day • November 25, 2013

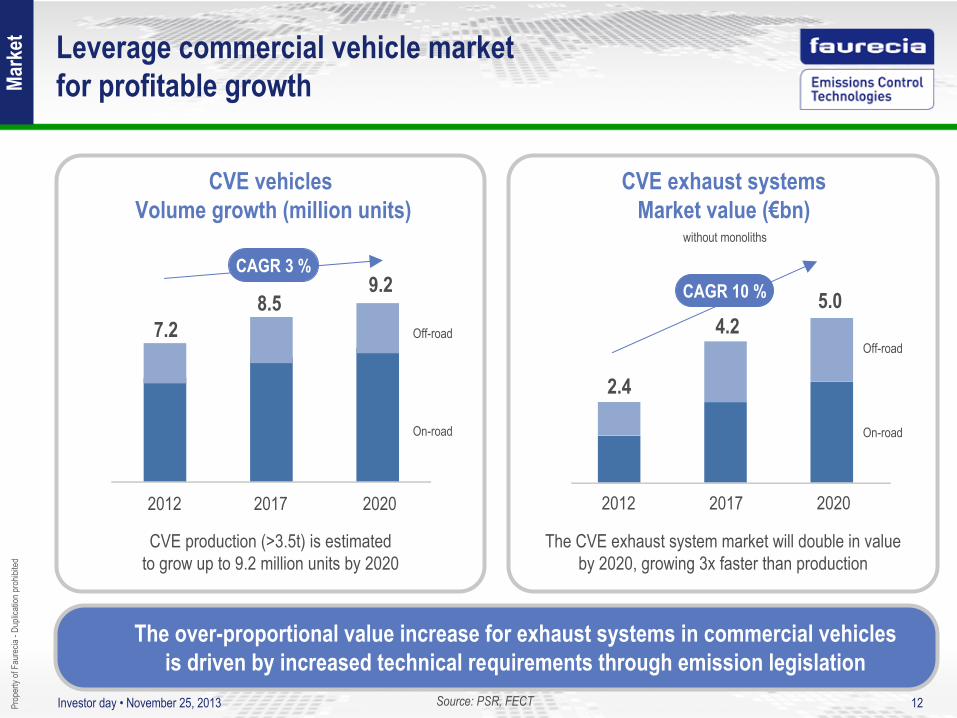

Leverage commercial vehicle market for profitable growth

The over-proportional value increase for exhaust systems in commercial vehicles is driven by increased technical requirements through emission legislation

CVE vehicles Volume growth (million units)

CVE exhaust systemsMarket value (€bn)

CVE production (>3.5t) is estimated to grow up to 9.2 million units by 2020

The CVE exhaust system market will double in value by 2020, growing 3x faster than production

7.28.5

9.2

2.4

4.25.0

2012 2017 2020 2012 2017 2020

Off-road

On-road

Off-road

On-road

CAGR 10 %CAGR 3 %

without

monoliths

Source: PSR, FECT

Mark

et

Prop

erty

of Fa

urec

ia -D

uplic

ation

proh

ibite

d

13Investor day • November 25, 2013

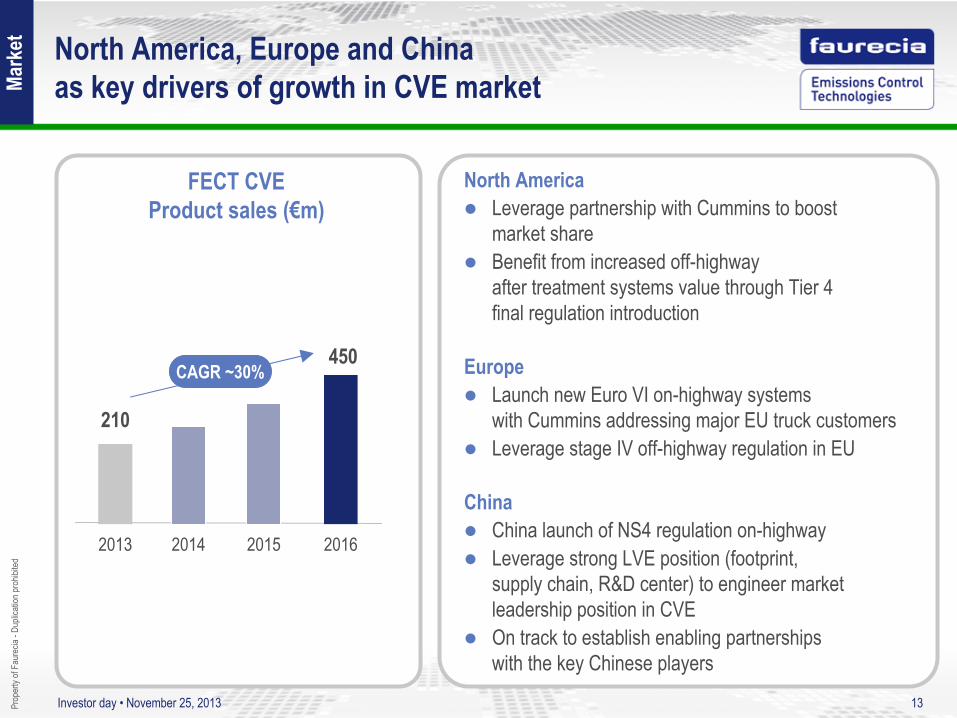

North

America, Europe and China as key

drivers of growth

in CVE market

North America

Leverage partnership with Cummins to boost market share

Benefit from increased off-highway after treatment systems value through Tier 4

final regulation introduction

Europe

Launch new Euro VI on-highway systems with Cummins addressing major EU truck customers

Leverage stage IV off-highway regulation in EU

China

China launch of NS4 regulation on-highway

Leverage strong LVE position (footprint, supply chain, R&D center) to engineer market leadership position in CVE

On track to establish enabling partnerships with the key Chinese players

210

450

2013 2014 2015 2016

FECT CVE Product sales (€m)

CAGR ~30%

Mark

et

Prop

erty

of Fa

urec

ia -D

uplic

ation

proh

ibite

d

14Investor day • November 25, 2013

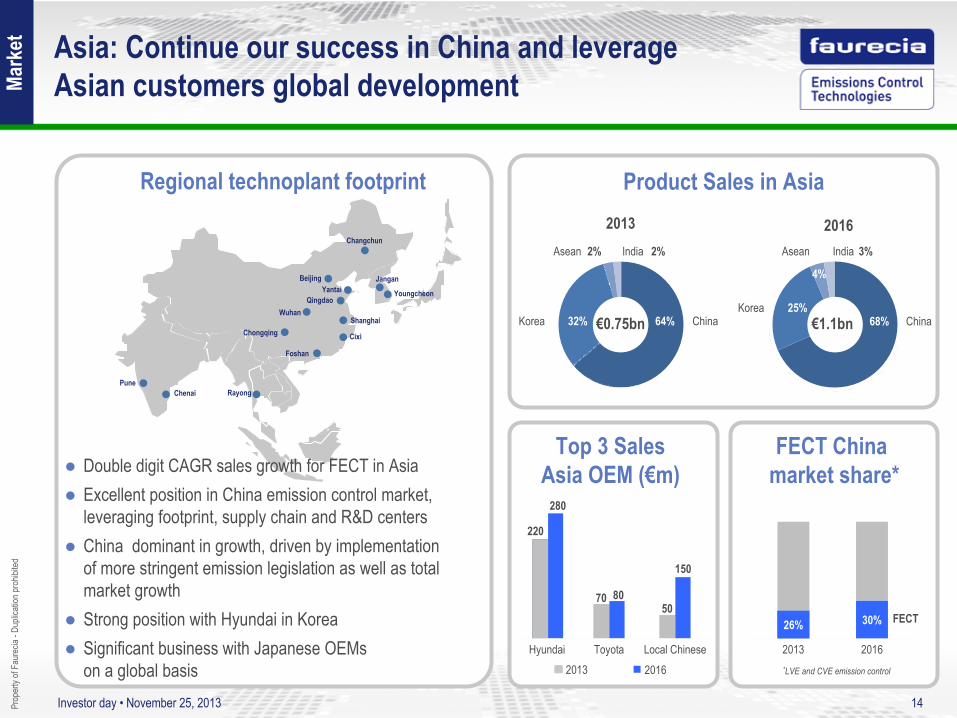

Regional technoplant

footprint Product Sales in Asia2013

64% 32% ChinaKorea

Asean India 2%

ChinaKorea

68% 25%

2016

4%

2% Asean India 3%

€1.1bn€0.75bn

Top 3 Sales Asia

OEM (€m)

FECT China market

share*

*LVE and CVE emission

control

FECT

2013 2016

220

280

70 8050

150

Hyundai Toyota Local Chinese2013 2016

Asia: Continue our

success

in China and leverage Asian

customers

global development

YoungcheonYantai Qingdao

Jangan

Rayong

WuhanShanghai

Changchun

Foshan

Beijing

Chenai

CixiChongqing

Pune

Double digit CAGR sales growth

for FECT in Asia

Excellent position in China emission

control market,

leveraging

footprint, supply

chain

and R&D centers

China dominant in growth, driven by implementation

of more stringent emission legislation as well as total

market growth

Strong

position with

Hyundai in Korea

Significant

business with

Japanese

OEMs

on a global basis

Mark

et

26% 30%

Prop

erty

of Fa

urec

ia -D

uplic

ation

proh

ibite

d

15Investor day • November 25, 2013

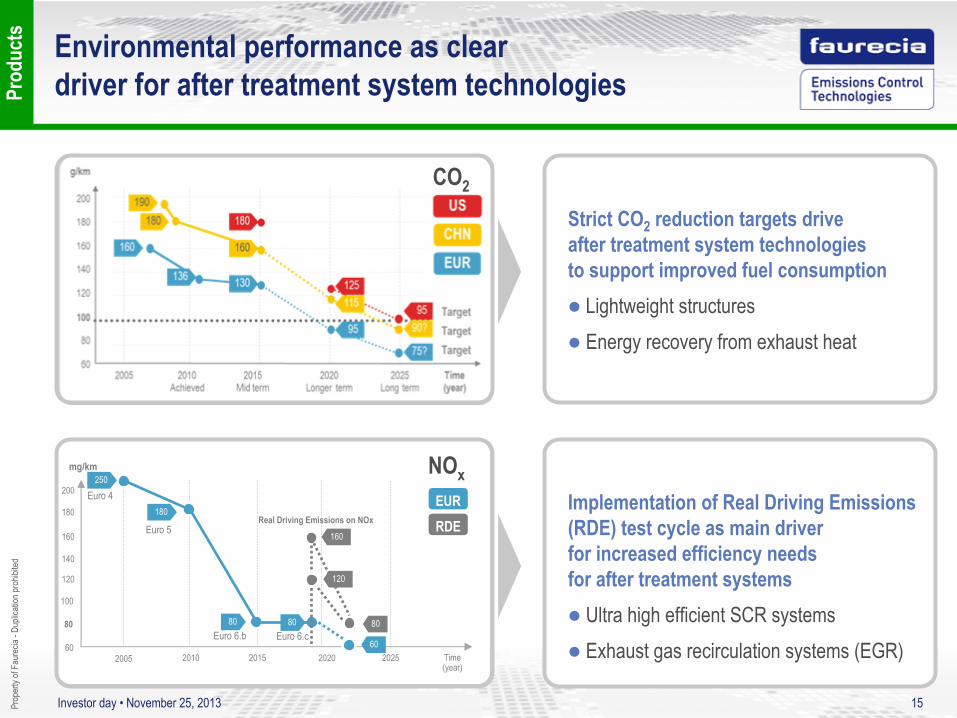

Time(year)

Diesel European NOx

emissions standards for passenger carsmg/km

EUR

2005 2010 2015 2020 202560

80

100

120

140

160

180

200 Euro 4

Euro 5

Euro 6.b Euro 6.c60

8080

250

Real Driving

Emissions on NOx RDE160

80

120

180

Time(year)

Environmental

performance as cleardriver for after

treatment

system technologies

Strict CO2

reduction targets drive after treatment system technologies

to support improved fuel consumption Lightweight structures Energy recovery from exhaust heat

CO2

NOx

Implementation of Real Driving Emissions (RDE) test cycle as main driver

for increased efficiency needs for after treatment systems

Ultra high efficient SCR systems Exhaust gas recirculation systems (EGR)

Prod

ucts

Prop

erty

of Fa

urec

ia -D

uplic

ation

proh

ibite

d

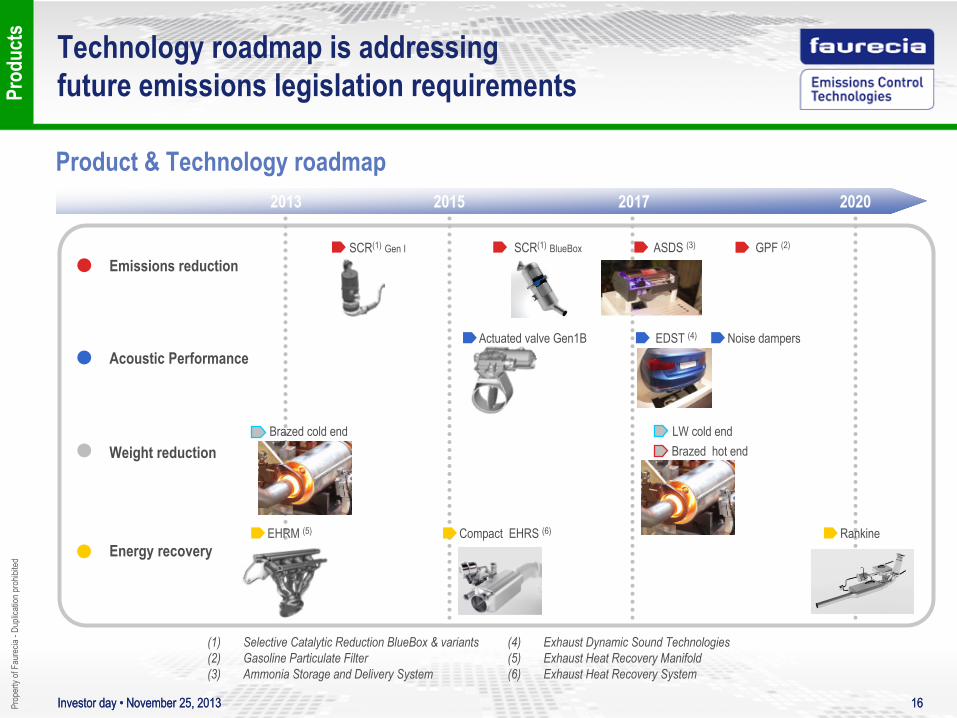

16Investor day • November 25, 2013 16Investor day •

November 25, 2013

2015 20202013 2017

(1)

Selective Catalytic Reduction BlueBox

& variants (2)

Gasoline Particulate Filter (3)

Ammonia Storage and Delivery System

Product & Technology roadmap

Acoustic PerformanceEDST (4) Noise dampersActuated

valve Gen1B

Technology roadmap is addressing future emissions legislation requirements

(4)

Exhaust Dynamic Sound Technologies(5)

Exhaust Heat Recovery Manifold (6)

Exhaust Heat Recovery System

Emissions reductionSCR(1)

BlueBox ASDS (3) GPF (2)SCR(1)

Gen

I

Weight reduction Brazed

hot endLW cold endBrazed

cold end

Prod

ucts

Energy recoveryEHRM (5) Compact EHRS (6) Rankine

Prop

erty

of Fa

urec

ia -D

uplic

ation

proh

ibite

d

17Investor day • November 25, 2013 17Investor day •

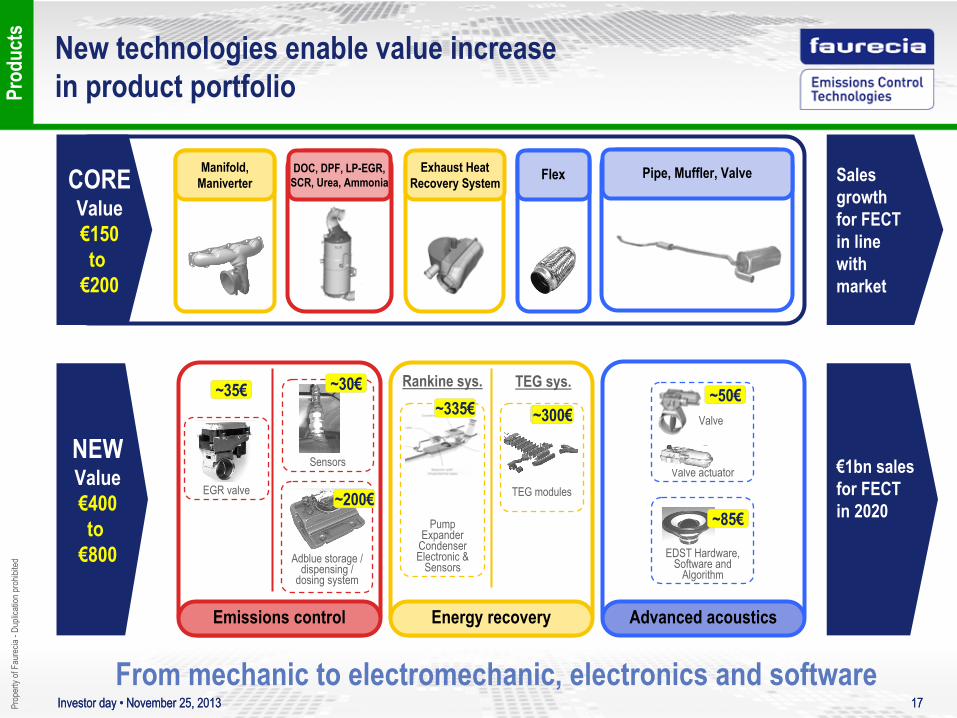

November 25, 2013

Sensors

EGR valve

Adblue

storage

/dispensing

/dosing

system

PumpExpander

CondenserElectronic &

Sensors

TEG modules

Rankine sys. TEG sys.

Valve actuator

EDST Hardware,Software and

Algorithm

Valve

NEWValue

€400 to

€800

Emissions control Energy

recovery Advanced acoustics

COREValue

€150 to

€200

Pipe, Muffler, ValveManifold,Maniverter

Exhaust

HeatRecovery

SystemDOC, DPF, LP-EGR,

SCR, Urea, Ammonia Flex

From mechanic to electromechanic, electronics and software

~85€

~300€

~200€

~300€~50€

~300€~335€~35€ ~30€

New technologies enable

value increase in product

portfolio

€1bn salesfor FECTin 2020

Sales

growth

for FECT in line with

market

Prod

ucts

Prop

erty

of Fa

urec

ia -D

uplic

ation

proh

ibite

d

18Investor day • November 25, 2013

Steady

growth

driven

by regulation

and technology and improving

profitability

Current Situation

Market & technology leadership position engineered

Favorable

environment forward

Current operating margin around 3% of total sales and around 5% of product sales

Strategic levers

Operational improvement plan launched in Europe, benchmark operations in North America

Commercial vehicle growth

Asian growth

Value up through technologies

2016 vision

Above 5% CAGR leading to total sales above €7.4bn

Operating margin above 4% of total sales and 7% of product sales

ROCE around 25%