ci segregated · pdf file2005 annual report ci segregated funds as at december 31, 2005...

TRANSCRIPT

2005 Annual Report

CI Segregated Funds

as at December 31, 2005

managed by CI Investments Inc. issued by Unity Life of Canada

A look inside

A Message From The Presidents ..........................................................................................1

A Message From

Altrinsic Global Advisors, LLC.....................................................................................................2

Harbour Advisors.........................................................................................................................3

Signature Advisors ......................................................................................................................4

Synergy Asset Management.......................................................................................................5

Trilogy Advisors, LLC ...................................................................................................................6

Equity Funds

CI Global Segregated Fund ............................................................................................................7

CI Global Value Segregated Fund................................................................................................10

CI Harbour Segregated Fund........................................................................................................13

CI Harbour Growth & Income Segregated Fund..........................................................................16

CI Synergy American Segregated Fund.......................................................................................19

Fixed Income

CI Money Market Segregated Fund ............................................................................................22

Notes to the Financial Statements .......................................................................................25

Management and Audit Reports ...........................................................................................26

– 1 –

A Message from the President

2005 Annual Report as at December 31, 2005

issued by Unity Life of Canadamanaged by CI Investments Inc.

Dear Policyholder,

The past year was generally positive for investors, with most financial markets making gains. The resource-rich Canadian stock

market was especially buoyant in 2005, led by strong demand for energy, metals and other commodities. Healthy global economic

activity helped to boost the U.S. and many overseas equity markets, although for Canadian investors the rewards from these regions

were somewhat muted by the continued strength of the Canadian dollar.

As a CI Segregated Fund investor, you benefit from market gains with the security of knowing that your investment is guaranteed at

maturity or death. Among their many advantages, the guarantees of the CI Segregated Funds are backed by Unity Life of Canada.

CI Investments manages the CI Segregated Funds, including selecting and monitoring the portfolio managers. CI Investments is a

subsidiary of CI Financial Inc., one of Canada’s largest wealth management companies with $71.7 billion in fee-earning assets.

If you have any questions about these financial statements or your policy, please contact your financial advisor or CI Client Services

at 1-800-563-5181 or [email protected].

Thank you for investing with us.

Sincerely,

Peter W. AndersonPresident and Chief Executive OfficerCI Investments [email protected]

December 31, 2005

– 2 –

A Message from Altrinsic Global Advisors, LLC

2005 Annual Report as at December 31, 2005

Global equity markets delivered strong performance during 2005,

resulting from growing optimism in Japan, as well as abundant global

liquidity, healthy corporate earnings and strong mergers and

acquisitions activity.

In 2005, our research team met with over 850 company management

teams in 17 countries. The result of this effort is portfolios with emphasis

on Japanese financial stocks, U.S. health-care stocks, insurance

stocks in North America and Europe, multinational consumer staples

domiciled in Europe and, increasingly, telecommunications stocks

in Europe.

In financials, our Japanese holdings have delivered strong performance

in recent months. Restructuring efforts are providing a supportive

backdrop that in many ways resembles the progress of North

American financial stocks following the U.S. savings and loan crisis.

We have sold some positions as they reached our target prices, but we

continue to be optimistic about the longer-term prospects for our

holdings. The situation is more mixed in North America and Europe,

where financial stocks are trading at loftier valuations and no longer

have the support of steep yield curves. Credit conditions have been

benign, though we are concerned about the massive amounts of debt

in the system and the fragility of consumer confidence based on the

wealth effect derived from buoyant property prices.

We continue to have meaningful positions in North American

insurance stocks, including Ambac and Torchmark, but we have

become increasingly drawn to the opportunities among European

insurers. One example is Allianz of Germany, where restructuring

has strengthened the balance sheet, shed non-core assets, and boosted

the underlying return on equity. However, there remains meaningful

underlying value to be released in Allianz’s operations and in holdings

in other listed companies and real estate.

We also have significant exposure to consumer stocks, with more

emphasis on consumer staples over cyclicals. Our largest positions

are in a handful of high-quality multinationals, including Diageo,

Heineken and Nestlé. Among cyclical names, we have modest

positions primarily in U.K. advertising and retail stocks.

Our Japanese property holdings have had very strong runs as 15 years

of property deflation came to end. One of our larger holdings, Daiwa

House, is one of Japan’s largest homebuilders. Consumers have excess

cash, mortgage rates are low, prices for homes in major metropolitan

areas are stabilizing, and young buyers have pent-up demand.

Health-care stocks generally lagged the overall market again in 2005.

An inability of “big pharma” to sufficiently develop innovative new

drugs to drive revenue growth has weighed on the sector. Sub-sectors

such as medical devices and biotechnology have been more

rewarding. We see opportunity among the unloved drug stocks and

have meaningful positions in Wyeth and GlaxoSmithKline, which

has a pipeline that is vastly undervalued by the market. A $400-billion

US Medicare plan to pay for seniors’ drugs also begins in 2006.

Elsewhere in the sector we have positions in Healthsouth, Tenet

Healthcare, and ImClone Systems.

Telecommunications stocks performed miserably in 2005 because of

increased mobile competition and higher capital spending. Our

holdings are concentrated in special situations in France, such as

Bouygues and Vivendi. The French mobile market is attractive

because just three players control the market. We also hold

SprintNextel of the U.S.

Industrial and materials stocks continued to deliver strong

performance during the fourth quarter, supported by expectations for

continuing strong demand growth from China. However, we believe

most stocks in these sectors have priced in peak margin and demand

conditions. We acquired shares in Lafarge, the world’s largest cement

producer, because of its exposure to North American and European

markets, where limited supply has come on stream over the past

decade. Our exposure to the energy sector is slightly underweight, as

stock prices are discounting underlying commodity prices that may

be difficult to sustain.

We believe that the environment for global investing is favourable,

but investors should be prepared for greater uncertainty and volatility

in 2006.

ALTRINSIC GLOBAL ADVISORS, LLC

John Hock

John DeVita

Andrew Waight

December 31, 2005

– 3 –

A Message from Harbour Advisors

2005 Annual Report as at December 31, 2005

Harbour Fund and Harbour Growth & Income Fund

At year-end 2005, Harbour Fund had roughly 85% of its assets

invested in common stocks (Canadian common, 62.8% and foreign

common, 22.3%), while the fund’s cash and equivalent position

amounted to 14.9%, down roughly seven percentage points from one

year ago. The number of companies held in the portfolio has risen to

37 from 33 at year-end 2004. In the case of Harbour Growth &

Income Fund, 67.4% was invested in common stocks (Canadian

common, 50.7% and foreign common, 16.7%), 5.9% in Government

of Canada bonds, while cash and equivalents represented 26.7%.

The past year was another highly successful one, with both funds

earning strong returns. Specific companies that contributed to the

two funds’ strong results over the past year were chiefly found within

the natural resource sector and include names such as Cameco,

Falconbridge, Goldcorp, Canadian Oil Sands, EnCana, Ensign Energy

Services, Petro-Canada, Suncor and Talisman. Notable non-resource

companies that performed strongly include IPSCO, Royal Bank,

Toronto-Dominion Bank and Yellow Pages Income Fund. Portfolio

holdings that fared poorly last year include Alcan, Jones Apparel,

Potash Corporation and TJX Cos.

Significant, but fairly brief, market weakness in the latter part of the

year created a number of attractive buying opportunities, which

resulted in us boosting equity positions meaningfully in both portfolios.

We continue to be comfortable with our holdings in stocks such as

those cited previously that recorded healthy gains over the past year,

since their fundamentals remain favourable and we believe that their

valuations are still attractive. For similar reasons, we have purchased

additional shares in the four companies cited that performed poorly

in 2005. Also, we are currently doing intensive research on a handful

of new companies that we are hoping to see fit to add to our

portfolios. At this juncture, we envision that most of the new names

will be companies domiciled outside Canada.

In contrast to the strong performance recorded within the equity

sphere, as we expected the bond market continued to produce lacklustre

returns over the past year. This is shown by the fact that benchmark

10-year Government of Canada bonds yielded 3.97% as at December

31, 2005, versus 4.08% at year-end 2004 – virtually unchanged. At the

4% level, investors continue to be poorly compensated for growing

inflation risks; hence, we expect to continue to maintain minimal

bond positions in the period ahead. Simply put, we expect to earn

more favourable returns in carefully selected equities.

Harbour Foreign Equity Corporate Class and Harbour Foreign

Growth & Income Corporate Class

The equity weighting of our two foreign portfolios continued to

increase as we moved into the final quarter of the year. Broad market

weakness provided opportunities to add to many of our existing

holdings during October. At year-end, Harbour Foreign Equity

Corporate Class had 87.6% of its assets invested in foreign equities,

while the remaining 12.4% of assets were held in Government of

Canada T-bills or cash. Geographically, the fund ended the year with

50.5% of its assets in Europe (26.9% Continental Europe, 23.6%

U.K. and Ireland.), 27.6% in the U.S., and 9.5% in the Asia Pacific

region. In the case of the Harbour Foreign Growth & Income

Corporate Class, the year-end asset mix was as follows: 70% in foreign

equities, 7% in foreign bonds, and 23% in Government of Canada

T-bills or cash.

In terms of portfolio activity, we took advantage of some short-term

price weakness early in the quarter to further build our position in

Alcoa, which is now a meaningful holding within the portfolio. Other

positions that were bolstered during the quarter include Citigroup,

Australia-based Macarthur Coal, and U.K. companies Travis Perkins

and Signet Group.

Outlook

As we enter a new year, we are optimistic about the outlook for the

Habour portfolios. For 2005, it was clearly a year where there was a

definite premium on both sector and individual stock selection –

if you were invested in the right stocks, you earned very handsome

returns, and 2006 may well bring more of the same. Indications are

that the economic and financial market backdrop will remain

favourable as we move through the New Year and we feel confident

about the way that our portfolios are currently structured.

CI INVESTMENTS INC.

HARBOUR ADVISORS

Gerald Coleman

Stephen Jenkins

December 31, 2005

– 4 –

A Message from Signature Advisors

2005 Annual Report as at December 31, 2005

To varying degrees, global equity markets benefited from the continued

economic expansion and relatively low interest rate environment

of the past 12 months. For investors in Canadian markets, 2005 was

a particularly rewarding year, as financial, energy, and materials stocks

led the S&P/TSX Composite Index to a 24% advance. The continued

strength of the Canadian dollar, however, dampened returns from

U.S. and other international investments.

The dominance of commodities in the Canadian market started early

in the year and continued in the fourth quarter, with oil, some base

metals and gold all posting record highs. Higher unit prices have

refocused the global energy sector on higher-cost projects such as

oil sands, as well as alternative energy sources such as thermal coal,

nuclear and hydro (all sectors in which we have invested).

Within the oil industry, we see more upside in the capacity-constrained

drilling and service companies that are in a position to raise prices

further. Within the metals and mining sector, continued strong

demand from developing countries and tight capacity will likely keep

prices high. Many companies are in very strong positions with healthy

balance sheets, and we expect consolidation in this industry to intensify.

Inflows for income trusts remained robust through the first half of

the year, but investors were roused from complacency over the summer

months as tax uncertainty dragged the asset class down markedly.

This was a valuable lesson for investors who believed trusts are less

risky than stocks, and brought some temporary sobriety to the market.

That wore off quickly, however, when the tax cloud was lifted and

trusts were included in the S&P/TSX Composite Index in the fourth

quarter. Trusts were bid back up to their previously heady levels

by year-end.

In the fixed-income markets, interest rates rose several times in the

U.S. and Canada in 2005, but the U.S. Federal Reserve now appears

to be very close to the end of its tightening cycle. We expect rates

to peak sometime toward mid-2006. We have been increasing holdings

of investment-grade corporate bonds where the outlook has been

favourable. Bond market turbulence through last April and May also

represented opportunity to buy high-yield bonds and we added to

our positions throughout that period in several funds.

The fundamental outlook for the economy remains fairly good.

Company earnings and balance sheets remain very healthy, even

with the slowdown in earnings growth. Given the extraordinary

availability of capital at unprecedentedly low rates, mergers and

acquisition activity gathered pace both at home and abroad over 2005,

and is likely to continue into 2006. Many large Canadian companies

such as Dofasco, Placer Dome and Falconbridge were the subject

of takeover bids in 2005, narrowing the breadth of the Canadian

marketplace.

While we maintain confidence in many segments of the Canadian

market, we expect to make greater investments in global markets

over the coming quarters. Signature’s strength across capital markets

allows us to use the knowledge of our existing positions to make strategic

investments in global companies. For example, our investment in a

number of Japanese banks are already beginning to bear fruit, and

we are expanding our main investment themes to include companies

in the U.S., South America and Europe.

As we head into 2006, we remain positive on equities, which we still

believe offer better value than fixed-income investments. At the same

time, we are growing more cautious in the face of higher energy prices,

rising interest rates and somewhat slower economic growth.

CI INVESTMENTS INC.

SIGNATURE ADVISORS

Eric Bushell

Robert Lyon

James Dutkiewicz

Matt Shandro

December 31, 2005

– 5 –

A Message from Synergy Asset Management

2005 Annual Report as at December 31, 2005

Despite various shocks to the economic system, the year 2005 proved

to be a surprisingly positive year for equity markets. Rising interest

rates, a 45% rise in oil prices and unprecedented disasters such as

Hurricane Katrina could not hold stocks back and most major markets

finished higher. The Canadian stock market was especially strong

with the S&P/TSX Composite Index generating a total return of

24.1%. This outpaced almost every other country’s major composite

index, in Canadian dollar terms. The large majority of our Synergy

funds finished in the first or second quartile in their respective

categories.

We have been bullish on the outlook for equity markets for some

time now due to their low valuations relative to interest rates, high

levels of corporate profitability and the generally negative investor

sentiment that existed towards stocks following the collapse of the

Internet/technology bubble. We felt the catalyst for a “Goldilocks”

rally in this cycle would be a growing sense that the U.S. Federal

Reserve was nearing the end of its interest rate tightening cycle.

Given the strong markets in the fourth quarter, it appears that

investors are embracing this scenario to some degree.

As we enter the fourth year of this bull market cycle, we remain

cautiously optimistic that 2006 will be another profitable year for

equity investors. On a free cash flow and earnings basis, markets seem

to have priced in a significant slowdown. Profit growth, especially in

the U.S., has exceeded stock market appreciation for a number of

years now, leaving price/earnings ratios attractive in the context of low

long-term interest rates. These relatively low expectations lend us

confidence in solid stock market returns when the interest rate

tightening cycle ends. At this point, the economy seems to be settling

into a “Goldilocks” trajectory (not too hot and not too cold, but just

right), suggesting that the end of the Fed interest rate tightening cycle

is near and stocks will climb again this year.

However, we are keenly aware that as time passes and further interest

rate increases occur, the weight of history starts to weigh against our

bullish stance and we have to be prepared to become more

conservative in our outlook for equity prices around the world.

We are not monetary policy experts or Fed watchers, but history

has told us that you need to be more careful when the Fed is hiking

rates. There can really only be two results from tighter monetary

policy: a recession or a “soft landing” for the economy. The first is bad

for stock markets, while the second is usually good.

Through 2005, we felt the perception of a soft landing occurring

would be positive for equities. The rally in November and December

suggests the market is now beginning to adapt this mindset.

Therefore, we believe 2006 will be about whether the perception of a

soft landing occurring can actually become reality. In other words,

the markets will likely come under pressure if U.S. interest rate hikes

continue beyond the next quarter and/or the economy begins to

weaken considerably. We will be vigilant in monitoring both of these

trends and adjusting our portfolios’ bullish positioning if necessary.

Within our earnings momentum based portfolios, we have begun to

slowly transition them away from more cyclical sectors such as energy

and consumer-discretionary into areas that show steadier growth.

Our rationale is that in the backdrop of a decelerating environment,

companies that exhibit positive fundamental change and/or that are

better able to sustain their earnings growth will command a scarcity

premium. We remain overweight materials stocks, but much less so

than this time last year. In spite of our long-term belief in energy

prices, we have reduced our energy weightings as well. Sectors where

we are increasing weightings include health care and financials.

SYNERGY ASSET MANAGEMENT

David Picton

Michael Mahoney

December 31, 2005

– 6 –

A Message from Trilogy Advisors, LLC

2005 Annual Report as at December 31, 2005

Global equity markets were a mixed picture in 2005, with the U.S.

market posting a lacklustre gain of only 3.8% in U.S. dollars, while

many other markets posted strong double-digit gains in local currency

terms. That said, higher interest rates in the U.S. and Canada

triggered strength in both the U.S. and Canadian dollars that muted

the impact of foreign stock price increases for North American

investors. As a result, the MSCI World Index posted a gain for the

year of only 7.6% in U.S. dollars and 4.9% in Canadian dollars.

For Canadian investors, 2005 turned out to be another year best spent

at home. In Canadian dollars, Canada’s equity market provided the

best returns among all the developed markets with a 24.1% return.

Other areas that provided exciting returns were the emerging markets

and Japan, which were up 27.0% and 21.0% in Canadian dollar

terms. Remarkable strength in energy and other commodity markets

turned out to be a major plus for both Canada and the emerging

markets in 2005.

Looking ahead, we anticipate another year of global economic

growth, which should create a constructive backdrop for equity

markets – even as the composition of growth and relative market

performance is likely to shift. The U.S. continues to be a good news-

bad news story. The good news is that the Federal Reserve may be

getting close to the end of its monetary tightening cycle, and markets

have historically done well after the Fed stops tightening. The bad

news is that the yield curve is now extremely flat (and inverted across

some maturities), which suggests that earnings growth could turn out

to be more disappointing than many company analysts now expect.

We would not be surprised to see foreign markets continue to outpace

the U.S. market in 2006. Valuations remain more attractive in many

foreign markets compared to the U.S. And even thought interest rates

may rise this year in Europe and Japan, monetary policy in those

regions is likely to remain more accommodative than in the U.S. for

some time to come, since growth has been more subdued. There is

also a good chance, in our opinion, that U.S. dollar weakness may

resume if the Fed stops tightening and currency markets refocus on

the need for a weaker dollar to correct large U.S. trade and current

account imbalances.

Equity valuations remain quite reasonable, with the MSCI World

Index trading at about 14.5 times next year’s estimated earnings.

Markets in Europe and non-Japan Asia are trading at around 12 to 13

times, while many emerging market stocks still trade on single-digit

multiples. With government bond yields still quite low in most

nations, comparisons of bond yields to equity earnings yields still

suggest that equities on average are still more than 40% undervalued

relative to bonds. Accordingly, we continue to favour equities in

CI International Balanced Fund, which maintains a target of 70%

equities/30% fixed income.

In our global equity portfolios, we currently have exposure of

approximately 44% to the U.S., 29% to Europe, 15% to Japan, and

8% to emerging markets and non-Japan Asian markets. Our strongest

sector tilts are toward the consumer discretionary and technology

sectors, which should benefit from continued global growth and an

end to Fed tightening. We are tilted away from highly defensive

sectors like consumer staples and utilities, as well as away from energy

and materials, which we believe may be vulnerable to a downshift in

U.S. growth. We are not currently employing any currency hedges,

although we may consider hedging U.S. dollar exposure if interest

rate differentials begin to provide less support for the U.S. currency.

TRILOGY ADVISORS, LLC

William Sterling

Greg Gigliotti

Robert Beckwitt

André Desautels

Richard Gluck

François Campeau

Bradley Wilds

Pablo Salas

December 31, 2005

– 7 –

CI Global Segregated FundUnderlying Fund Information (Unaudited)

CIG - 025

Top 25 Holdings of Underlying Fund

No. of Shares/ Average MarketFace Amount Investment Cost ($) Value ($)

1,188,600 Microsoft Corp. 45,137,701 36,137,531 686,800 General Electric Co. 35,863,477 27,987,839 795,646 Comcast Corp., Class A 27,856,626 23,977,612 200,900 Everest Re Group Ltd. 22,053,079 23,439,501 842,815 Pfizer Inc. 32,018,226 22,851,350 402,099 Citigroup Inc. 25,928,010 22,687,902

1,135,200 Cisco Systems Inc. 23,835,807 22,595,773 334,000 Exxon Mobil Corp. 23,634,747 21,812,324 877,400 Continental Airlines Inc., Class B 13,608,211 21,728,427

1,060,400 News Corp Inc., B-shares 20,233,058 20,478,135 267,700 Lockheed Martin Corp. 18,601,690 19,804,384

2,128,116 Liberty Media Corp., Class A 28,795,997 19,472,472 1,054,700 AES Corp. 14,547,669 19,411,581

293,600 Morgan Stanley 22,384,014 19,368,520 50,200 Samsung Electronics Co. Ltd., GDR 9,447,891 19,231,368

581,350 IAC/InterActive Corp. 19,459,235 19,135,006 1,127,300 Diageo PLC 18,841,757 18,998,425

320,171 Credit Suisse Group 14,536,819 18,980,735 501,100 AXA SA 15,954,773 18,803,235

7,467,176 Vodafone Group PLC 26,251,238 18,745,986 1,175 Mitsubishi Tokyo Financial Group Inc. 12,731,567 18,542,520

256,400 Fisher Scientific International Inc. 18,532,322 18,440,767 964,300 Saipem SpA 12,658,106 18,397,453

1,982 Mizuho Financial Group Inc. 12,475,851 18,297,444 510,800 Commerzbank AG 15,406,654 18,295,340

Underlying Portfolio Exposure

Country Allocation (%)

Long Positions:U.S.A. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37.0Japan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15.3U.K. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5.8Germany . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5.4France . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5.3Switzerland . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4.6Cash & Equivalents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4.4Bermuda . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3.7Italy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.6Norway . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.4South Korea . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.8Singapore . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.8Hong Kong . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.6Taiwan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.1Indonesia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.0Denmark . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.0Ireland . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.9Thailand . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.9Liberia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.7Sweden . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.7Brazil . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.6Greece . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.6Malaysia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.4Belgium . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.1Russia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.1Israel . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.1Argentina . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.1Peru . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.1

Short Positions:U.S.A. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . -0.1

2005 Annual Report as at December 31, 2005

– 8 –

IncomeInterestIncome distribution from investments

Expenses (Management expense ratios – Schedule 3)Management fees (Note 4)Administrative (Note 4)CustodyLegalAuditGoods and services tax

Net income (loss) for the year

Realized and unrealized gain (loss) on investments Realized gain (loss) on investments (a)Capital gain distribution from investmentsChange in unrealized appreciation

(depreciation) of investmentsNet gain (loss) on investmentsIncrease (decrease)

in net assets from operations(Earnings per unit – Schedule 4)

(a) Realized gain (loss) on investmentsProceeds from sale of investments Investments at cost, beginning of yearInvestments purchased

Investments at cost, end of yearCost of investments soldRealized gain (loss) on investments

CI Global Segregated FundFinancial Statements

AssetsInvestments at market valueCashReceivable for unit subscriptionsReceivable for securities soldDividends and accrued interest receivable

LiabilitiesPayable for securities purchased Payable for unit redemptions

Net assets and unitholders’ equity

Net asset value per unit – Schedule 1

Number of units outstanding (Unit transactions – Schedule 2)

Statements of Operations for the years ended December 31 ($000’s)

2005 2004

11,379 13,88817 22

- -- 37- -

11,396 13,947

- 292 -2 29

11,394 13,918

12.55 11.81

907,927 1,178,612

Statements of Net Assets as at December 31 (in $000’s except for per unitamounts and units outstanding)

Statements of Changes in Net Assets for the years ended December 31 ($000’s)

2005 2004

1 1- -1 1

9 11114 138

- 1- -- -1 1

124 151(123) (150)

(348) (372)- -

1,185 1,112837 740

714 590

3,356 2,38815,657 18,352

9 6515,666 18,41711,962 15,6573,704 2,760(348) (372)

Net assets, beginning of year

Capital transactionsProceeds from units issued Amounts paid for units redeemed

Increase (decrease) in net assetsfrom operations

Net assets, end of year

2005 2004

13,918 15,529

402 384(3,640) (2,585)(3,238) (2,201)

714 59011,394 13,918

Investment Portfolio as at December 31, 2005

No. of Average MarketUnits/Shares Investment Cost ($) Value ($)

893,841 CI Global Fund (Class A) 11,962,359 11,378,593

Total Investments (99.9%) 11,962,359 11,378,593

Other Assets (net) (0.1%) 15,061

Total Net Assets (100.0%) 11,393,654

The accompanying notes are an integral part of these financial statements. Percentages shown in brackets relate investments at market value to total net assets of the fund.

2005 Annual Report as at December 31, 2005

– 9 –

CI Global Segregated FundFinancial Statements – Supplementary Schedules (for the years ended December 31)

2005 Annual Report as at December 31, 2005

Schedule 1

Net asset value per unit, end of year ($)

Schedule 2

Unit transactions Balance, beginning of yearUnits issued for cash Units redeemedBalance, end of year

Schedule 3

Management expense ratios 1, 2 (%)Management and operating expensesGoods and services tax expensesTotal management expense ratio

Schedule 4

Earnings per unit 3 ($)

2005 2004 2003 2002 2001

3.34 3.29 3.40 3.37 3.420.17 0.23 0.18 0.17 0.183.51 3.52 3.58 3.54 3.60

2005 2004

1,178,612 1,369,86533,709 33,068

(304,394) (224,321)907,927 1,178,612

2005 2004 2003 2002 2001

12.55 11.81 11.34 9.51 11.93

2005 2004

0.69 0.45

1 Management expense information is calculated based on expenses charged directly to the fund plus, if applicable, expenses of the underlying funds, calculated on a weighted average basis on the percentageweighting of underlying fund and is expressed as an annualized percentage of average net assets for the year.

2 The fiscal year end of the underlying funds changed from December 31 to March 31. As a result, the MER of the underlying fund is based on the most recent audited MER at December 31, 2004. It is expectedthat the MER of the underlying funds at December 31, 2005 would be slightly less than the prior year MER due to a decline in fees that occurred in September 2005.

3 Earnings per unit is calculated by dividing the increase (decrease) in net assets from operations of the fund by the weighted average number of units outstanding during the year.

For inception date for the fund, please refer to note 1 in the Notes to the Financial Statements. The accompanying notes are an integral part of these financial statements.

– 10 –

CI Global Value Segregated FundUnderlying Fund Information (Unaudited)

CIG - 024

Top 25 Holdings of Underlying Fund

No. of Shares/ Average MarketFace Amount Investment Cost ($) Value ($)

116,600 ImClone Systems Inc. 5,661,714 4,641,767 370,810 Sumitomo Trust & Banking Co. Ltd. 2,851,825 4,407,064 73,430 Wyeth 3,898,219 3,933,171 42,900 AMBAC Financial Group Inc. 3,540,436 3,843,593 76,600 Noble Energy Inc. 3,240,732 3,589,094

268,100 Daiwa Securities Group Inc. 2,197,502 3,535,405 105,020 Tyco International Ltd. 3,484,600 3,523,866 73,400 J.P. Morgan Chase & Co. 3,497,320 3,387,102

113,900 GlaxoSmithKline PLC 3,179,065 3,346,984 32,800 Sanofi-Aventis 3,004,144 3,341,088 87,150 Heineken NV 3,546,674 3,212,627 79,634 ING Groep NV 2,881,449 3,211,800 49,600 Torchmark Corp. 2,642,778 3,206,325 29,500 Lafarge SA 3,349,746 3,086,156

111,800 Bristol-Myers Squibb Co. 4,186,256 2,987,053 8,590 Nestle SA, Registered Shares 2,882,054 2,987,046

85,000 Royal Bank of Scotland Group PLC 2,952,777 2,984,037 608,439 Kingfisher PLC 3,724,149 2,887,563 168,519 Diageo PLC 2,968,491 2,840,056 77,400 Vivendi Universal SA 2,186,954 2,819,117 31,200 Altria Group Inc. 1,717,258 2,710,457 34,410 Molson Coors Brewing Co. (USD) 2,604,442 2,680,067 97,900 Sprint Corp., FON Group 2,448,079 2,658,928

134,300 ATI Technologies Inc. (USD) 2,045,097 2,652,897 207,900 WPP Group PLC 2,698,375 2,615,853

Underlying Portfolio Exposure

Country Allocation (%)

U.S.A. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35.8Japan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14.4U.K. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10.9France . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7.0Germany . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6.2Italy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6.0Netherlands . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4.5Switzerland . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.4South Korea . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.1Bermuda . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.8Cash & Equivalents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.8Canada . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.4Hong Kong . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.0Sweden . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.8Finland . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.7Taiwan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.7Mexico . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.7Thailand . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.6Singapore . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.5Cayman Islands . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.4Croatia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.3

2005 Annual Report as at December 31, 2005

– 11 –

IncomeInterestIncome distribution from investments

Expenses (Management expense ratios – Schedule 3)Management fees (Note 4)Administrative (Note 4)CustodyLegalAuditGoods and services tax

Net income (loss) for the year

Realized and unrealized gain (loss) on investments Realized gain (loss) on investments (a)Capital gain distribution from investmentsChange in unrealized appreciation

(depreciation) of investmentsNet gain (loss) on investmentsIncrease (decrease)

in net assets from operations(Earnings per unit – Schedule 4)

(a) Realized gain (loss) on investmentsProceeds from sale of investments Investments at cost, beginning of yearInvestments purchased

Investments at cost, end of yearCost of investments soldRealized gain (loss) on investments

CI Global Value Segregated FundFinancial Statements

AssetsInvestments at market valueCashReceivable for unit subscriptionsReceivable for securities soldDividends and accrued interest receivable

LiabilitiesPayable for securities purchased Payable for unit redemptions

Net assets and unitholders’ equity

Net asset value per unit – Schedule 1

Number of units outstanding (Unit transactions – Schedule 2)

Statements of Operations for the years ended December 31 ($000’s)

2005 2004

3,098 4,71930 38

- -- -- -

3,128 4,757

- 2231 -31 22

3,097 4,735

11.16 10.98

277,567 431,364

Statements of Net Assets as at December 31 (in $000’s except for per unitamounts and units outstanding)

Statements of Changes in Net Assets for the years ended December 31 ($000’s)

2005 2004

1 -21 -22 -

3 436 47

- 1- -- -- 1

39 53(17) (53)

175 90- -

(129) 31446 404

29 351

1,694 9474,218 4,844

26 2314,244 5,0752,725 4,2181,519 857

175 90

Net assets, beginning of year

Capital transactionsProceeds from units issued Amounts paid for units redeemed

Increase (decrease) in net assetsfrom operations

Net assets, end of year

2005 2004

4,735 5,041

165 383(1,832) (1,040)(1,667) (657)

29 3513,097 4,735

Investment Portfolio as at December 31, 2005

No. of Average MarketUnits/Shares Investment Cost ($) Value ($)

244,491 CI Global Value Fund (Class A) 2,725,173 3,097,702

Total Investments (100.1%) 2,725,173 3,097,702

Other Assets (net) (-0.1%) (1,110)

Total Net Assets (100.0%) 3,096,592

The accompanying notes are an integral part of these financial statements. Percentages shown in brackets relate investments at market value to total net assets of the fund.

2005 Annual Report as at December 31, 2005

– 12 –

CI Global Value Segregated FundFinancial Statements – Supplementary Schedules (for the years ended December 31)

2005 Annual Report as at December 31, 2005

Schedule 1

Net asset value per unit, end of year ($)

Schedule 2

Unit transactions Balance, beginning of yearUnits issued for cash Units redeemedBalance, end of year

Schedule 3

Management expense ratios 1, 2 (%)Management and operating expensesGoods and services tax expensesTotal management expense ratio

Schedule 4

Earnings per unit 3 ($)

2005 2004 2003 2002 2001

3.34 3.30 3.42 3.41 3.440.17 0.23 0.18 0.17 0.183.51 3.53 3.60 3.58 3.62

2005 2004

431,364 491,81115,286 36,229

(169,083) (96,676)277,567 431,364

2005 2004 2003 2002 2001

11.16 10.98 10.25 8.82 10.58

2005 2004

0.08 0.75

1 Management expense information is calculated based on expenses charged directly to the fund plus, if applicable, expenses of the underlying funds, calculated on a weighted average basis on the percentageweighting of underlying fund and is expressed as an annualized percentage of average net assets for the year.

2 The fiscal year end of the underlying funds changed from December 31 to March 31. As a result, the MER of the underlying fund is based on the most recent audited MER at December 31, 2004. It is expectedthat the MER of the underlying funds at December 31, 2005 would be slightly less than the prior year MER due to a decline in fees that occurred in September 2005.

3 Earnings per unit is calculated by dividing the increase (decrease) in net assets from operations of the fund by the weighted average number of units outstanding during the year.

For inception date for the fund, please refer to note 1 in the Notes to the Financial Statements. The accompanying notes are an integral part of these financial statements.

– 13 –

CI Harbour Segregated FundUnderlying Fund Information (Unaudited)

CIG - 021

Top 25 Holdings of Underlying Fund

No. of Shares/ Average MarketFace Amount Investment Cost ($) Value ($)

3,100,000 Suncor Energy Inc. 65,715,748 227,292,000 2,800,000 Talisman Energy Inc. 45,675,803 172,480,000 1,800,000 Royal Bank of Canada 80,146,085 163,458,000 2,500,000 Toronto-Dominion Bank 98,525,308 152,825,000 3,300,000 Bank of Nova Scotia 81,072,330 152,262,000 7,500,000 BHP Billiton Ltd. 127,283,085 145,480,202 3,000,000 Alcan Inc. 125,319,141 143,280,000 1,500,000 Canadian National Railway Co. 65,638,767 139,710,000 4,000,000 Falconbridge Ltd. 82,815,185 138,000,000 2,500,000 EnCana Corp. 64,736,730 131,400,000 2,600,000 Ensign Energy Services Inc. 35,393,270 121,992,000 2,000,000 Citigroup Inc. 116,983,262 112,847,343 2,300,000 Petro-Canada 38,246,725 107,295,000 1,150,000 Potash Corp. of Saskatchewan 60,804,184 107,065,000 1,400,000 Canadian Imperial Bank of Commerce 75,851,815 106,974,000 1,000,000 IPSCO Inc. 25,351,183 96,710,000 5,600,000 Yellow Pages Income Fund 77,778,624 91,280,000 1,200,000 Cameco Corp. (USD) 17,350,544 88,548,000

680,000 Canadian Oil Sands Trust 27,411,252 85,680,000 2,200,000 Ross Stores Inc. 65,069,260 73,921,637

500,000 Total SA, ADR 61,572,963 73,479,828 4,200,000 Diageo PLC 66,764,417 70,782,741 2,600,000 TJX Co. Inc. 68,943,599 70,222,067 1,000,000 Morgan Stanley 68,292,951 65,969,073

260,000 Air Liquide 48,665,622 58,157,942

Underlying Portfolio Exposure

Sector Allocation (%)

Energy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26.5Materials . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23.7Financials . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20.8Cash & Equivalents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15.0Consumer Discretionary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6.7Industrials . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3.6Consumer Staples . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3.5Health Care . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.1Warrants . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.1

2005 Annual Report as at December 31, 2005

– 14 –

IncomeInterestIncome distribution from investments

Expenses (Management expense ratios – Schedule 3)Management fees (Note 4)Administrative (Note 4)CustodyLegalAuditGoods and services tax

Net income (loss) for the year

Realized and unrealized gain (loss) on investments Realized gain (loss) on investments (a)Capital gain distribution from investmentsChange in unrealized appreciation

(depreciation) of investmentsNet gain (loss) on investmentsIncrease (decrease)

in net assets from operations(Earnings per unit – Schedule 4)

(a) Realized gain (loss) on investmentsProceeds from sale of investments Investments at cost, beginning of yearInvestments purchased

Investments at cost, end of yearCost of investments soldRealized gain (loss) on investments

CI Harbour Segregated FundFinancial Statements

AssetsInvestments at market valueCashReceivable for unit subscriptionsReceivable for securities soldDividends and accrued interest receivable

LiabilitiesPayable for securities purchased Payable for unit redemptions

Net assets and unitholders’ equity

Net asset value per unit – Schedule 1

Number of units outstanding (Unit transactions – Schedule 2)

Statements of Operations for the years ended December 31 ($000’s)

2005 2004

29,671 28,75919 60

- -- -- -

29,690 28,819

- 101 101 20

29,689 28,799

21.84 17.84

1,359,338 1,614,547

Statements of Net Assets as at December 31 (in $000’s except for per unitamounts and units outstanding)

Statements of Changes in Net Assets for the years ended December 31 ($000’s)

2005 2004

2 2- -2 2

22 21230 225

- 11 -1 13 3

257 251(255) (249)

2,207 1,216- -

3,949 2,9066,156 4,122

5,901 3,873

5,774 4,86718,755 22,099

530 30719,285 22,40615,718 18,7553,567 3,6512,207 1,216

Investment Portfolio as at December 31, 2005

No. of Average MarketUnits/Shares Investment Cost ($) Value ($)

1,570,723 Harbour Fund (Class A) 15,718,100 29,670,963

Total Investments (99.9%) 15,718,100 29,670,963

Other Assets (net) (0.1%) 18,528

Total Net Assets (100.0%) 29,689,491

Net assets, beginning of year

Capital transactionsProceeds from units issued Amounts paid for units redeemed

Increase (decrease) in net assetsfrom operations

Net assets, end of year

2005 2004

28,799 29,297

2,296 1,368(7,307) (5,739)(5,011) (4,371)

5,901 3,87329,689 28,799

The accompanying notes are an integral part of these financial statements. Percentages shown in brackets relate investments at market value to total net assets of the fund.

2005 Annual Report as at December 31, 2005

– 15 –

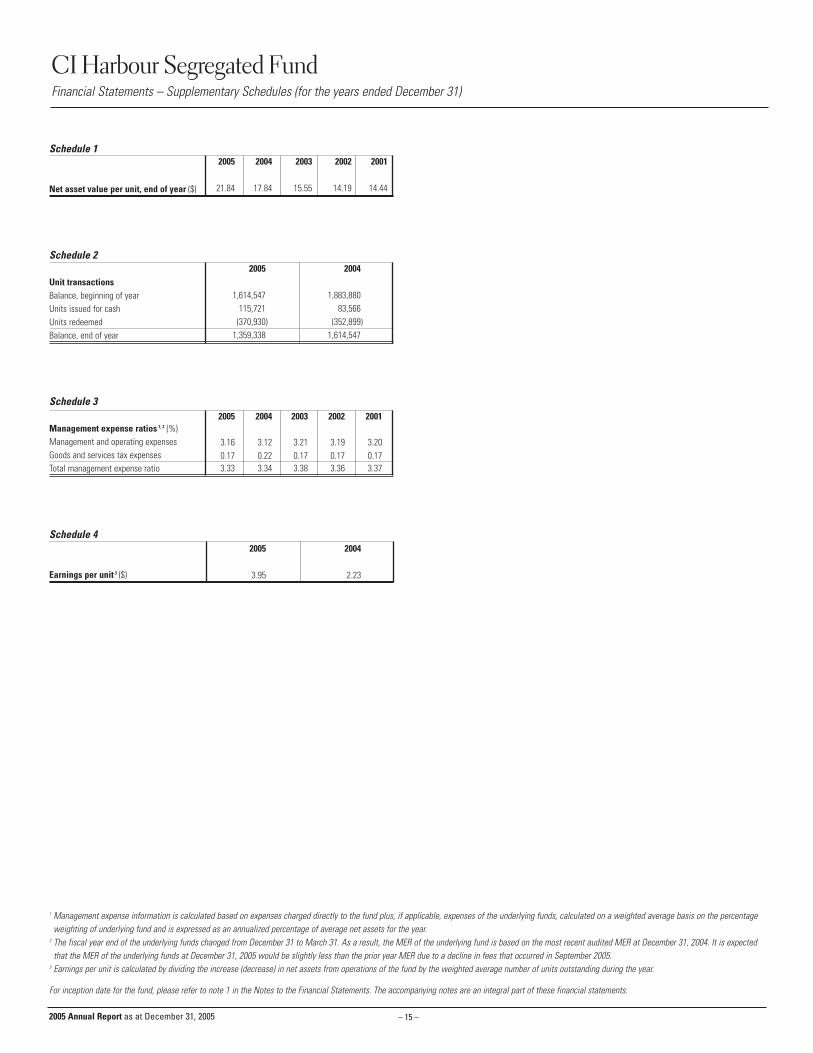

CI Harbour Segregated FundFinancial Statements – Supplementary Schedules (for the years ended December 31)

2005 Annual Report as at December 31, 2005

Schedule 1

Net asset value per unit, end of year ($)

Schedule 2

Unit transactions Balance, beginning of yearUnits issued for cash Units redeemedBalance, end of year

Schedule 3

Management expense ratios 1, 2 (%)Management and operating expensesGoods and services tax expensesTotal management expense ratio

Schedule 4

Earnings per unit 3 ($)

2005 2004 2003 2002 2001

3.16 3.12 3.21 3.19 3.200.17 0.22 0.17 0.17 0.173.33 3.34 3.38 3.36 3.37

2005 2004

1,614,547 1,883,880115,721 83,566(370,930) (352,899)

1,359,338 1,614,547

2005 2004 2003 2002 2001

21.84 17.84 15.55 14.19 14.44

2005 2004

3.95 2.23

1 Management expense information is calculated based on expenses charged directly to the fund plus, if applicable, expenses of the underlying funds, calculated on a weighted average basis on the percentageweighting of underlying fund and is expressed as an annualized percentage of average net assets for the year.

2 The fiscal year end of the underlying funds changed from December 31 to March 31. As a result, the MER of the underlying fund is based on the most recent audited MER at December 31, 2004. It is expectedthat the MER of the underlying funds at December 31, 2005 would be slightly less than the prior year MER due to a decline in fees that occurred in September 2005.

3 Earnings per unit is calculated by dividing the increase (decrease) in net assets from operations of the fund by the weighted average number of units outstanding during the year.

For inception date for the fund, please refer to note 1 in the Notes to the Financial Statements. The accompanying notes are an integral part of these financial statements.

– 16 –

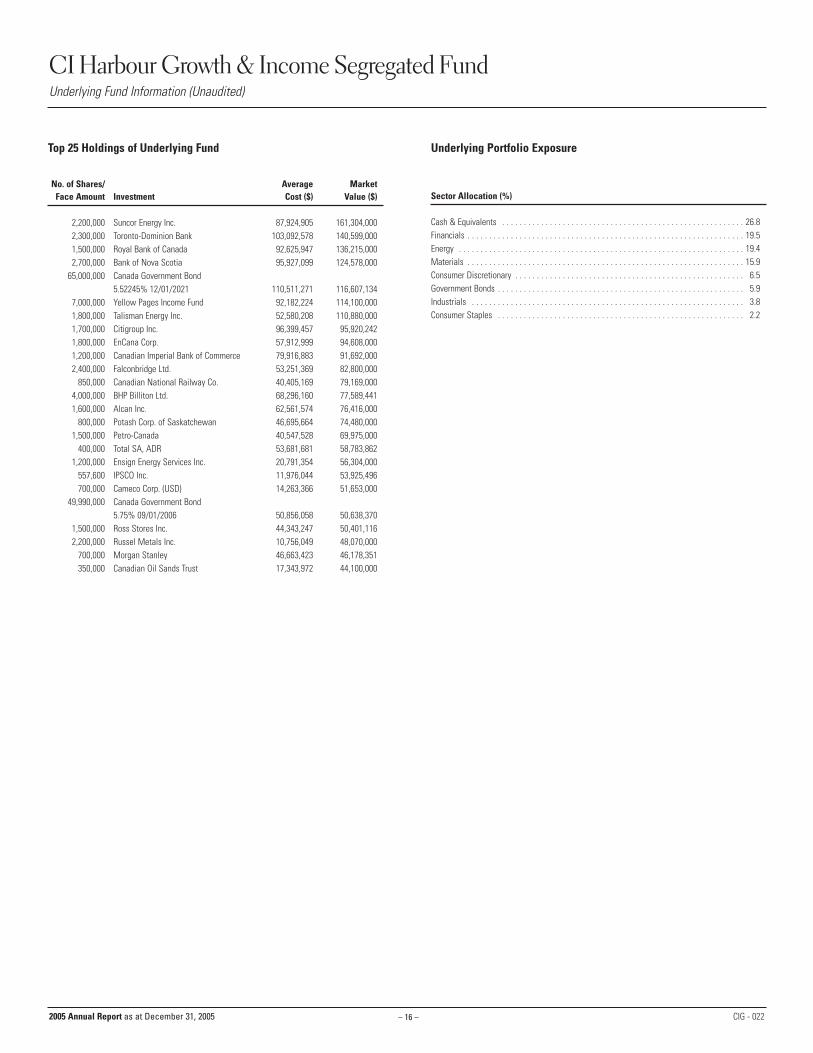

CI Harbour Growth & Income Segregated FundUnderlying Fund Information (Unaudited)

CIG - 022

Top 25 Holdings of Underlying Fund

No. of Shares/ Average MarketFace Amount Investment Cost ($) Value ($)

2,200,000 Suncor Energy Inc. 87,924,905 161,304,000 2,300,000 Toronto-Dominion Bank 103,092,578 140,599,000 1,500,000 Royal Bank of Canada 92,625,947 136,215,000 2,700,000 Bank of Nova Scotia 95,927,099 124,578,000

65,000,000 Canada Government Bond 5.52245% 12/01/2021 110,511,271 116,607,134

7,000,000 Yellow Pages Income Fund 92,182,224 114,100,000 1,800,000 Talisman Energy Inc. 52,580,208 110,880,000 1,700,000 Citigroup Inc. 96,399,457 95,920,242 1,800,000 EnCana Corp. 57,912,999 94,608,000 1,200,000 Canadian Imperial Bank of Commerce 79,916,883 91,692,000 2,400,000 Falconbridge Ltd. 53,251,369 82,800,000

850,000 Canadian National Railway Co. 40,405,169 79,169,000 4,000,000 BHP Billiton Ltd. 68,296,160 77,589,441 1,600,000 Alcan Inc. 62,561,574 76,416,000

800,000 Potash Corp. of Saskatchewan 46,695,664 74,480,000 1,500,000 Petro-Canada 40,547,528 69,975,000

400,000 Total SA, ADR 53,681,681 58,783,862 1,200,000 Ensign Energy Services Inc. 20,791,354 56,304,000

557,600 IPSCO Inc. 11,976,044 53,925,496 700,000 Cameco Corp. (USD) 14,263,366 51,653,000

49,990,000 Canada Government Bond 5.75% 09/01/2006 50,856,058 50,638,370

1,500,000 Ross Stores Inc. 44,343,247 50,401,116 2,200,000 Russel Metals Inc. 10,756,049 48,070,000

700,000 Morgan Stanley 46,663,423 46,178,351 350,000 Canadian Oil Sands Trust 17,343,972 44,100,000

Underlying Portfolio Exposure

Sector Allocation (%)

Cash & Equivalents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26.8Financials . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19.5Energy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19.4Materials . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15.9Consumer Discretionary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6.5Government Bonds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5.9Industrials . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3.8Consumer Staples . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.2

2005 Annual Report as at December 31, 2005

– 17 –

IncomeInterestIncome distribution from investments

Expenses (Management expense ratios – Schedule 3)Management fees (Note 4)Administrative (Note 4)CustodyLegalAuditGoods and services tax

Net income (loss) for the year

Realized and unrealized gain (loss) on investments Realized gain (loss) on investments (a)Capital gain distribution from investmentsChange in unrealized appreciation

(depreciation) of investmentsNet gain (loss) on investmentsIncrease (decrease)

in net assets from operations(Earnings per unit – Schedule 4)

(a) Realized gain (loss) on investmentsProceeds from sale of investments Investments at cost, beginning of yearInvestments purchased

Investments at cost, end of yearCost of investments soldRealized gain (loss) on investments

CI Harbour Growth & Income Segregated FundFinancial Statements

AssetsInvestments at market valueCashReceivable for unit subscriptionsReceivable for securities soldDividends and accrued interest receivable

LiabilitiesPayable for securities purchased Payable for unit redemptions

Net assets and unitholders’ equity

Net asset value per unit – Schedule 1

Number of units outstanding (Unit transactions – Schedule 2)

Statements of Operations for the years ended December 31 ($000’s)

2005 2004

24,843 25,19159 60

- -- 6- -

24,902 25,257

13 1- 4

13 524,889 25,252

17.54 15.08

1,419,158 1,675,116

Statements of Net Assets as at December 31 (in $000’s except for per unitamounts and units outstanding)

Statements of Changes in Net Assets for the years ended December 31 ($000’s)

2005 2004

2 275 -77 2

19 19178 175

- 1- -- 12 2

199 198(122) (196)

1,776 95721 -

2,135 1,9123,932 2,869

3,810 2,673

5,091 3,94117,095 19,206

832 87317,927 20,07914,612 17,0953,315 2,9841,776 957

Investment Portfolio as at December 31, 2005

No. of Average MarketUnits/Shares Investment Cost ($) Value ($)

1,468,246 Harbour Growth & Income Fund (Class A) 14,612,291 24,842,714

Total Investments (99.8%) 14,612,291 24,842,714

Other Assets (net) (0.2%) 46,348

Total Net Assets (100.0%) 24,889,062

Net assets, beginning of year

Capital transactionsProceeds from units issued Amounts paid for units redeemed

Increase (decrease) in net assetsfrom operations

Net assets, end of year

2005 2004

25,252 25,354

2,928 1,743(7,101) (4,518)(4,173) (2,775)

3,810 2,67324,889 25,252

The accompanying notes are an integral part of these financial statements. Percentages shown in brackets relate investments at market value to total net assets of the fund.

2005 Annual Report as at December 31, 2005

– 18 –

CI Harbour Growth & Income Segregated FundFinancial Statements – Supplementary Schedules (for the years ended December 31)

2005 Annual Report as at December 31, 2005

Schedule 1

Net asset value per unit, end of year ($)

Schedule 2

Unit transactions Balance, beginning of yearUnits issued for cash Units redeemedBalance, end of year

Schedule 3

Management expense ratios 1, 2 (%)Management and operating expensesGoods and services tax expensesTotal management expense ratio

Schedule 4

Earnings per unit 3 ($)

2005 2004 2003 2002 2001

3.07 3.04 3.12 3.10 3.120.17 0.21 0.17 0.17 0.173.24 3.25 3.29 3.27 3.29

2005 2004

1,675,116 1,873,895179,010 123,548(434,968) (322,327)

1,419,158 1,675,116

2005 2004 2003 2002 2001

17.54 15.08 13.53 12.62 12.56

2005 2004

2.44 1.51

1 Management expense information is calculated based on expenses charged directly to the fund plus, if applicable, expenses of the underlying funds, calculated on a weighted average basis on the percentageweighting of underlying fund and is expressed as an annualized percentage of average net assets for the year.

2 The fiscal year end of the underlying funds changed from December 31 to March 31. As a result, the MER of the underlying fund is based on the most recent audited MER at December 31, 2004. It is expectedthat the MER of the underlying funds at December 31, 2005 would be slightly less than the prior year MER due to a decline in fees that occurred in September 2005.

3 Earnings per unit is calculated by dividing the increase (decrease) in net assets from operations of the fund by the weighted average number of units outstanding during the year.

For inception date for the fund, please refer to note 1 in the Notes to the Financial Statements. The accompanying notes are an integral part of these financial statements.

– 19 –

CI Synergy American Segregated FundUnderlying Fund Information (Unaudited)

CIG - 023

Top 25 Holdings of Underlying Fund

No. of Shares/ Average MarketFace Amount Investment Cost ($) Value ($)

107,500 Burlington Northern Santa Fe Corp. 5,992,117 8,851,471 71,000 Aetna Inc. 5,431,317 7,785,153

125,600 Bank of America Corp. 7,064,127 6,739,263 85,700 CB Richard Ellis Group Inc., Class A 3,200,851 5,863,789 59,300 Wells Fargo & Co. 4,438,503 4,331,844 68,700 Freeport-McMoRan Copper & Gold Inc., Class B 3,297,126 4,297,245 79,100 Advance Auto Parts Inc. 2,958,332 3,996,845

124,700 CVS Corp. 4,001,983 3,830,455 74,600 QUALCOMM Inc. 3,566,278 3,736,505 55,700 Medtronic Inc. 3,747,354 3,728,228

100,500 Chesapeake Energy Corp. 2,120,902 3,707,551 136,400 Sprint Corp., FON Group 3,774,355 3,704,574 44,000 Genzyme Corp. 3,221,695 3,620,881

102,300 Alcoa Inc. 3,370,229 3,517,046 75,300 J.P. Morgan Chase & Co. 3,212,224 3,474,779 89,500 Coach Inc. 2,685,255 3,469,283 44,000 Merrill Lynch & Co. Inc. 3,360,976 3,464,853

186,800 News Corp Inc., A-Shares 3,981,059 3,377,212 53,900 Teck Cominco Ltd., Class B 1,770,508 3,344,495 45,900 Devon Energy Corp. 2,314,666 3,337,503

128,300 MEMC Electronic Materials Inc. 2,146,714 3,307,070 97,700 Hewlett-Packard Co. 3,174,400 3,252,123

122,400 Motorola Inc. 2,624,495 3,214,761 51,100 Allstate Corp. 3,251,347 3,212,390 66,600 Cintas Corp. 3,505,502 3,184,813

Underlying Portfolio Exposure

Sector Allocation (%)

Consumer Discretionary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17.7Financials . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17.7Information Technology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16.8Health Care . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12.6Industrials . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10.4Energy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8.8Materials . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8.7Consumer Staples . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3.1Cash & Equivalents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.5Telecommunication Services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.7

2005 Annual Report as at December 31, 2005

– 20 –

IncomeInterestIncome distribution from investments

Expenses (Management expense ratios – Schedule 3)Management fees (Note 4)Administrative (Note 4)CustodyLegalAuditGoods and services tax

Net income (loss) for the year

Realized and unrealized gain (loss) on investments Realized gain (loss) on investments (a)Capital gain distribution from investmentsChange in unrealized appreciation

(depreciation) of investmentsNet gain (loss) on investmentsIncrease (decrease)

in net assets from operations(Earnings per unit – Schedule 4)

(a) Realized gain (loss) on investmentsProceeds from sale of investments Investments at cost, beginning of yearInvestments purchased

Investments at cost, end of yearCost of investments soldRealized gain (loss) on investments

CI Synergy American Segregated FundFinancial Statements

AssetsInvestments at market valueCashReceivable for unit subscriptionsReceivable for securities soldDividends and accrued interest receivable

LiabilitiesPayable for securities purchased Payable for unit redemptions

Net assets and unitholders’ equity

Net asset value per unit – Schedule 1

Number of units outstanding (Unit transactions – Schedule 2)

Statements of Operations for the years ended December 31 ($000’s)

2005 2004

3,443 4,75446 24

- -- -- -

3,489 4,778

- -29 829 8

3,460 4,770

10.56 10.19

327,624 468,049

Statements of Net Assets as at December 31 (in $000’s except for per unitamounts and units outstanding)

Statements of Changes in Net Assets for the years ended December 31 ($000’s)

2005 2004

1 -- -1 -

3 435 42

- 1- -- -- -

38 47(37) (47)

(621) (551)- -

792 839171 288

134 241

1,481 1,0026,853 8,337

- 696,853 8,4064,751 6,8532,102 1,553(621) (551)

Investment Portfolio as at December 31, 2005

No. of Average MarketUnits/Shares Investment Cost ($) Value ($)

279,730 Synergy American Fund (Class A) 4,751,200 3,443,479

Total Investments (99.5%) 4,751,200 3,443,479

Other Assets (net) (0.5%) 16,976

Total Net Assets (100.0%) 3,460,455

Net assets, beginning of year

Capital transactionsProceeds from units issued Amounts paid for units redeemed

Increase (decrease) in net assetsfrom operations

Net assets, end of year

2005 2004

4,770 5,407

123 296(1,567) (1,174)(1,444) (878)

134 2413,460 4,770

The accompanying notes are an integral part of these financial statements. Percentages shown in brackets relate investments at market value to total net assets of the fund.

2005 Annual Report as at December 31, 2005

– 21 –

CI Synergy American Segregated FundFinancial Statements – Supplementary Schedules (for the years ended December 31)

2005 Annual Report as at December 31, 2005

Schedule 1

Net asset value per unit, end of year ($)

Schedule 2

Unit transactions Balance, beginning of yearUnits issued for cash Units redeemedBalance, end of year

Schedule 3

Management expense ratios 1, 2 (%)Management and operating expensesGoods and services tax expensesTotal management expense ratio

Schedule 4

Earnings per unit 3 ($)

2005 2004 2003 2002 2001

3.23 3.20 3.30 3.27 3.340.17 0.22 0.17 0.17 0.183.40 3.42 3.47 3.44 3.52

2005 2004

468,049 560,26512,024 31,037

(152,449) (123,253)327,624 468,049

2005 2004 2003 2002 2001

10.56 10.19 9.65 8.41 12.21

2005 2004

0.33 0.46

1 Management expense information is calculated based on expenses charged directly to the fund plus, if applicable, expenses of the underlying funds, calculated on a weighted average basis on the percentageweighting of underlying fund and is expressed as an annualized percentage of average net assets for the year.

2 The fiscal year end of the underlying funds changed from December 31 to March 31. As a result, the MER of the underlying fund is based on the most recent audited MER at December 31, 2004. It is expectedthat the MER of the underlying funds at December 31, 2005 would be slightly less than the prior year MER due to a decline in fees that occurred in September 2005.

3 Earnings per unit is calculated by dividing the increase (decrease) in net assets from operations of the fund by the weighted average number of units outstanding during the year.

For inception date for the fund, please refer to note 1 in the Notes to the Financial Statements. The accompanying notes are an integral part of these financial statements.

– 22 –

CI Money Market Segregated FundUnderlying Fund Information (Unaudited)

CIG - 020

Top 25 Holdings of Underlying Fund

No. of Shares/ Average MarketFace Amount Investment Cost ($) Value ($)

47,800,000 Province of Ontario T-Bill 3.58% 06/02/2006 47,095,181 47,095,181 42,200,000 Province of Ontario 5.9% 03/08/2006 42,529,160 42,511,858 32,000,000 Government of Canada T-Bill

3.16% 01/03/2006 31,991,680 31,991,680 30,300,000 Royal Bank of Canada BA 3.2% 02/03/2006 30,210,452 30,210,452 29,551,000 Greater Toronto Airport Authority

3.52286% 05/18/2007 29,561,661 29,551,000 29,400,000 Province of Quebec T-Bill 3.34% 03/03/2006 29,234,464 29,234,464 28,100,000 Bank of Montreal BDN 3.39% 03/06/2006 27,931,923 27,931,923 27,800,000 Province of New Brunswick T-Bill

3.35% 03/06/2006 27,635,563 27,635,563 27,600,000 GE Capital Canada Funding Co.

3.29% 02/13/2006 27,491,386 27,491,386 27,400,000 Government of Canada T-Bill

3.21% 01/03/2006 27,392,783 27,392,783 27,200,000 ASIF II 3.58714% 06/15/2007 27,156,315 27,180,960 27,000,000 Deutschebank Canada TD 3.25% 01/03/2006 27,002,404 27,002,404 24,600,000 HSBC Bank Canada BDN 3.24% 02/08/2006 24,515,552 24,515,552 24,500,000 HSBC Bank Canada BDN 3.3% 02/14/2006 24,401,138 24,401,138 24,500,000 Province of Ontario T-Bill 3.33% 02/28/2006 24,369,024 24,369,024 23,400,000 Citibank N.A. 3.65% 06/01/2006 23,050,769 23,050,769 21,500,000 McCain Finance Canada Ltd.

3.34% 01/23/2006 21,454,877 21,454,877 21,100,000 Bank of Nova Scotia BDN 3.32% 02/15/2006 21,012,430 21,012,430 21,000,000 CIBC BA 3.41% 03/10/2006 20,865,851 20,865,851 19,100,000 Government of Canada T-Bill

3.24% 02/23/2006 19,009,279 19,009,279 19,100,000 Government of Canada T-Bill

3.42% 05/04/2006 18,881,487 18,881,487 18,600,000 Toronto Dominion Bank BDN

3.44% 03/14/2006 18,473,075 18,473,075 18,500,000 Government of Canada T-Bill

3.23% 04/06/2006 18,345,129 18,345,129 17,900,000 Province of Ontario 3.25% 01/20/2006 17,900,062 17,900,000 17,400,000 Bank of Montreal 3.39571% 09/14/2007 17,400,000 17,400,000

Underlying Portfolio Exposure

Allocation (%)

Short Term Notes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81.9Bonds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17.8Cash & Equivalents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.3

2005 Annual Report as at December 31, 2005

– 23 –

IncomeInterestIncome distribution from investments

Expenses (Management expense ratios – Schedule 3)Management fees (Note 4)Administrative (Note 4)CustodyLegalAuditGoods and services tax

Net income (loss) for the year

Realized and unrealized gain (loss) on investments Realized gain (loss) on investments (a)Capital gain distribution from investmentsChange in unrealized appreciation

(depreciation) of investmentsNet gain (loss) on investmentsIncrease (decrease)

in net assets from operations(Earnings per unit – Schedule 4)

(a) Realized gain (loss) on investmentsProceeds from sale of investments Investments at cost, beginning of yearInvestments purchased

Investments at cost, end of yearCost of investments soldRealized gain (loss) on investments

CI Money Market Segregated FundFinancial Statements

AssetsInvestments at market valueCashReceivable for unit subscriptionsReceivable for securities soldDividends and accrued interest receivable

LiabilitiesPayable for securities purchased Payable for unit redemptions

Net assets and unitholders’ equity

Net asset value per unit – Schedule 1

Number of units outstanding (Unit transactions – Schedule 2)

Statements of Operations for the years ended December 31 ($000’s)

2005 2004

2,141 2,5582 6- -- -5 2

2,148 2,566

- -- -- -

2,148 2,566

12.04 11.89

178,444 215,810

Statements of Net Assets as at December 31 (in $000’s except for per unitamounts and units outstanding)

Statements of Changes in Net Assets for the years ended December 31 ($000’s)

2005 2004

1 136 3937 40

2 27 10- 1- -- -- -9 13

28 27

- -- -

- -- -

28 27

2,504 2,1882,558 3,3242,087 1,4224,645 4,7462,141 2,5582,504 2,188

- -

Investment Portfolio as at December 31, 2005

No. of Average MarketUnits/Shares Investment Cost ($) Value ($)

214,140 CI Money Market Fund (Class A) 2,141,402 2,141,402

Total Investments (99.7%) 2,141,402 2,141,402

Other Assets (net) (0.3%) 6,425

Total Net Assets (100.0%) 2,147,827

Net assets, beginning of year

Capital transactionsProceeds from units issued Amounts paid for units redeemed

Increase (decrease) in net assetsfrom operations

Net assets, end of year

2005 2004

2,566 3,336

3,124 1,723(3,570) (2,520)

(446) (797)

28 272,148 2,566

The accompanying notes are an integral part of these financial statements. Percentages shown in brackets relate investments at market value to total net assets of the fund.

2005 Annual Report as at December 31, 2005

– 24 –

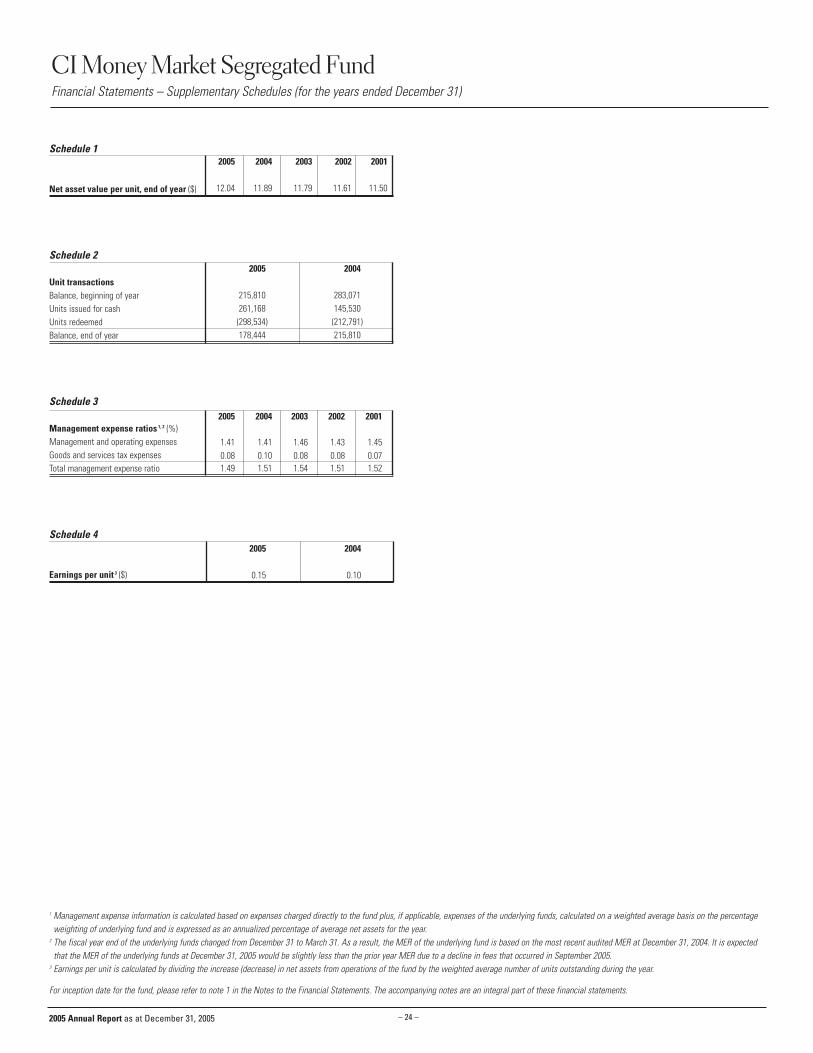

CI Money Market Segregated FundFinancial Statements – Supplementary Schedules (for the years ended December 31)

2005 Annual Report as at December 31, 2005

Schedule 1

Net asset value per unit, end of year ($)

Schedule 2

Unit transactions Balance, beginning of yearUnits issued for cash Units redeemedBalance, end of year

Schedule 3

Management expense ratios 1, 2 (%)Management and operating expensesGoods and services tax expensesTotal management expense ratio

Schedule 4

Earnings per unit 3 ($)

2005 2004 2003 2002 2001

1.41 1.41 1.46 1.43 1.450.08 0.10 0.08 0.08 0.071.49 1.51 1.54 1.51 1.52

2005 2004

215,810 283,071261,168 145,530(298,534) (212,791)178,444 215,810

2005 2004 2003 2002 2001

12.04 11.89 11.79 11.61 11.50

2005 2004

0.15 0.10

1 Management expense information is calculated based on expenses charged directly to the fund plus, if applicable, expenses of the underlying funds, calculated on a weighted average basis on the percentageweighting of underlying fund and is expressed as an annualized percentage of average net assets for the year.

2 The fiscal year end of the underlying funds changed from December 31 to March 31. As a result, the MER of the underlying fund is based on the most recent audited MER at December 31, 2004. It is expectedthat the MER of the underlying funds at December 31, 2005 would be slightly less than the prior year MER due to a decline in fees that occurred in September 2005.

3 Earnings per unit is calculated by dividing the increase (decrease) in net assets from operations of the fund by the weighted average number of units outstanding during the year.

For inception date for the fund, please refer to note 1 in the Notes to the Financial Statements. The accompanying notes are an integral part of these financial statements.

2005 Annual Report as at December 31, 2005 – 25 –

1. THE FUNDS

The following funds were created by board resolution of Unity Life of Canada.

Fund Names (the “Fund”) Dated

CI Global Segregated Fund October 28, 1997

CI Global Value Segregated Fund October 28, 1997

CI Harbour Segregated Fund October 28, 1997

CI Harbour Growth & Income Segregated Fund October 28, 1997

CI Synergy American Segregated Fund October 28, 1997

CI Money Market Segregated Fund October 28, 1997

Each Fund invests all of its net assets in a CI mutual fund (the “Underlying Funds”).

CI Investments Inc. is the manager of each Fund and Underlying Fund.

The Investment Portfolio for each Fund is shown as at December 31, 2005 and the Statements of

Net Assets are as at December 31, 2005 and 2004. The Statements of Operations and Changes

in Net Assets for each Fund are for the years ended December 31, 2005 and 2004. The

Supplementary Schedules on the Financial Statements for each Fund are for each of the most

recent five years for schedules 1 and 3, and two years for schedules 2 and 4 ended December 31.

Effective December 31, 2000, the Funds were closed to new or additional contributions.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

These financial statements have been prepared in accordance with Canadian generally

accepted accounting principles.

The following is a summary of significant accounting policies of the Funds:

(a) Valuation of Investments

Mutual funds are valued on each business date at their closing net asset value.

(b) Foreign Exchange

Foreign currency amounts are translated into Canadian dollars as follows: market value of

investments, forward currency contracts, other assets and liabilities at the closing rate of

exchange on each business day; income, expenses and purchases, sales and settlements of

investments at the rate of exchange prevailing on the respective dates of such transactions.

(c) Investment Transactions and Income Recognition

Investment transactions are accounted for on the trade date and any realized gains and

losses from such transactions are calculated on an average cost basis. Distributions from

Underlying Funds are recorded on the ex-distribution date and interest income is accrued on

a daily basis.

(d) Net Asset Value Per Unit

Net asset value per unit is calculated at the end of each day on which the Toronto Stock

Exchange is open for business by dividing the net assets of each Fund by its outstanding units.

(e) Use of Estimates

The preparation of financial statements in accordance with Canadian generally accepted

accounting principles requires management to make estimates and assumptions that

affect the reported amounts of assets and liabilities at the reporting date and the reported

amounts of income and expenses during the reporting period. Actual results could differ

from those estimates.

3. INCOME TAXES

The Funds are deemed to be inter-vivos trusts under the provisions of the Income Tax Act

(Canada) and are deemed to have allocated their income to the beneficiaries. Each Fund’s net

capital gains (losses) are deemed to be those of the beneficiaries. Accordingly, the Funds are