cima c1 unit 3 2012

DESCRIPTION

It's Chartered Institute of Management Accountants Course: C-01 Fundamentals of Management Accounting ,Class LSBF Manchester ,Q's By Sir Ian Wilson.TRANSCRIPT

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 1/49

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 2/49

CIMA C1Fundamentals Of Management Accounting

Overheads & Absorption Costing

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 3/49

CIMA C1Fundamentals of Management Accounting

Class Slides – Ian Wilson

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 4/49

• Consider what overheads are how the! areallocated to product unit costs & themethods emplo!ed

•

Calculate Overhead Absorption• "repare cost statements for allocation &

apportionment of overheads includingreciprocal departments

Learning Aims (CIMA)

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 5/49

• Calculate direct variable & full costs ofproducts services & activities usingoverhead absorption rates

•

Appl! information to pricing decisions

Learning Aims (CIMA)

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 6/49

We have seen that business costs can be andneed to be #classi$ed% b! t!pe & behaviour

'irect Materials 'irect (abour 'irect )*penses + Prime Cost "roduction Overheads ,OA-.

+ Total Production (Absorbed Cost) /on0"roduction Overheads + Total Cost

Context & Link to Session1

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 7/49

Costs #behave% in a variet! of wa!s1 2he classi$cations are1 3ariable Costs

Semi03ariable Costs Step Costs Fi*ed Costs Once costs t!pes & behaviour is 4nown

what happens ne*t5 Wh! did we collect this information5

Context & Link to Session1

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 8/49

Ke !m"#asis in $ areas o% use1

6 Stoc4 3aluations what is the value7cost ofinventor!5

8 "lanning future forecasts9 Control actual against planned

performance

: 'ecision Ma4ing the #right% outcome in

terms of cost7pro$t for the business

Context & Link to Session1

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 9/49

'irect Costs are #eas!% to deal with the!relate to #cost units%

;ut what about #indirect% costs or

#overheads%5 ;! their ver! nature the! cannot be traced'I-)C2(< to a cost unit

We have to $nd a wa! to #charge% theses

#indirect% costs to a #cost unit%

Context & Link to Session1

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 10/49

2he method Accountants used to chargeindirect costs to cost unit is called#A;SO-"2IO/ COS2I/=%

CIMA denition o% an 'er#ead1

An overhead is #expenditure on labour,materials, or services that cannot beeconomically identifed with a specifc

saleable cost unit %

Context & Link to Session

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 11/49

Absorption Costing is a method of sharingOverheads ,Indirect Costs7)*penses.between a number of di>erent Finished"roducts on a #%Fair%% basis

<ou will have to consider the 9 A%s1

6 Allocation

8 Apportionment ,& re0apportionment.

9 Absorption: "oint 9 leads to Over7?nder Absorption

'er#ead Costing & Absor"tion

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 12/49

It ma! be useful to s4etch out how costs areallocated apportioned and $nall! absorbedinto a single product cost per unit

2his is a useful summar! I alwa!s use togive !ou a #map% to follow & remember

Ma4e sure !ou note this down1

Absor"tion Cost *iagram

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 13/49

A Compan! will have a 2otal "roductionOverhead spend in mind sa! @BB

If it has 8 'epartments Cutting & Finishinghow much does it charge to each of these'epartments5

'ividing up Overheads is a critical processas the! will drive Absorption rates as we

have alread! seen We follow a 9 stage process1

Allocation &A""ortionment

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 14/49

6 Allocation

8 Apportionment

9 -e0Apportionment

. <ou must be able to tac4le all 91

Allocation &A""ortionment

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 15/49

Allocation1 Means1 Charging cost centres with Overheads that

are incurred solely in that centre

eg1 a salar! of a supervisor in a particularcost centre

Allocation &A""ortionment

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 16/49

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 17/49

A""ortionment+ Means+ Some costs relate to a business as a whole

#%Splitting%% shared Overheads between costcentres using some form of #%fair%% basis

eg1 using Door area for rent & rates 1 using number of emplo!ees for canteen

costs 1 using value of assets for 'epreciation

charges

Allocation &A""ortionment

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 18/49

,e-A""ortionment Means+ -e0splitting Overheads from #service% cost

centres to #production% cost centres eg1 moving service costs for sa! Canteen &

Maintenance centres to production costcentres based on bene$t & use of those

service centres

Allocation &A""ortionment

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 19/49

)*ercise 6 page 9E We can complete this e*ercise to practice

the theor! $rst lets get our details right

Indirect Wages & Materials have alread!been A((OCA2)' to the various cost centres Machining 0 "roduction Assembl! 0 "roduction

Finishing 0 "roduction Maintenance – Service (ets calculate an answer1

Allocation &A""ortionment

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 20/49

/ot all departments are "-O'?C2IO/ based

Some departments provide #Services% toproduction departments

2hese departments are called S)-3IC) departments

Secondar! apportionment is therefore

apportioning service centre costs toproduction cost centres

Secondar A""ortionment

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 21/49

What happens when service centres provideservices for each other5

2his is #service% to #service%

2here are 8 wa!s to deal with this issue16 )limination

8 -epeated 'istribution

.)*amples 8 provides the answer

,eci"rocal Sericing

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 22/49

aving allocated7apportioned our overheadsto a Cost centre we need to add them to orabsorb these costs in to the Cost of Sales

"roduction Overheads are added to the#"rime Cost% seen earlier in the course

2he OA- ,Overhead Absorption -ate. can beseen as a #charge out rate% for Overheads

Authors also call this #;OA-% ;udgeted Overhead Absorption -ate

'er#ead Absor"tion ,ates('A,)

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 23/49

2here are 9 common wa!s to achieve this1

6 A -ate per ?nit ,identical units.

8 A -ate per (abour our ,human time

intensive.9 A -ate per Machine our ,machine time

intensive.

All of the above are set at a pre0determined

rate using ;udgets or e*pected estimates ofproduction costs ,#;OA-%.

'A,

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 24/49

-ates of Overhead A3) to be available atthe S2A-2 of the production period

2he business CA//O2 wait until the end ofthe accounting period to see what theAC2?A( production overhead costs were

2he ;?'=)2 $gures for Overheads are used

OA- + ;udgeted Overheads for "roduction ;udgeted (evel of Activit!

'A,

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 25/49

We will wor4 out )*ercises : & Ma4e sure !ou practice this at home It is vital for A(( CIMA Management

Accounting papers !ou ta4eG /ote1 OA- -ates can be1

6 ;lan4etHor

8 'epartmental

.See page :67:8 of !our notes.)*ercise : &

'A, .lanket &*e"artmental

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 26/49

2r! )*ercise "age :9 2his is a t!pical #e*am st!le% Juestion <ou are given : answersG

Which is correct5

!/AM 0'CS

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 27/49

2he OA- is based on estimates 2hisestimate is Juanti$ed in the #;?'=)2%

Overhead Costs & Output Activit! (evels areestimated7;udgeted for a given period

One or both estimates ma! be di>erent towhat AC2?A((< ta4es place

Actual Overheads are li4el! to be greater or

less than the overheads absorbed into thecost of production & production ma! di>er

in volume also

'er & nder Absor"tion

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 28/49

In Sim"le Terms1

Over Absorbed1

Absorbed Overhead K Actual Overhead

?nder Absorbed1 Absorbed Overhead L Actual Overhead

'er & under Absor"tion

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 29/49

A possible la!out for !our calculation1 I call this the 9 ;o* approach – !ou need 9

$gures1

Absorbed Overhead1 *** ,Actual activit! * OA-.

Actual Overhead1 ***

?nder7Over Absorption1 **

nder & 'er Absor"tion

;O 6

;O 8

;O 9

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 30/49

Aurricula (td "age ::

We can practice over7under absorption

calculations for this problem

2r! & use the la!out I suggested for thisJuestion -emember the #9 bo* approach%

!xercise 2

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 31/49

N6 ;udgeted Fi*ed O7 for =reen N8 Actual number of hours wor4ed N9 reciprocal servicing

N: apportioned to 'ept (ets wor4 these e*amples through

!nd o% C#a"ter 3uestions(4)

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 32/49

We have seen that Costs can be used for16 3aluing Stoc4

8 "lanning

9 'ecision ma4ing: Control.What else will product7service costs be used

for5

Costs

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 33/49

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 34/49

As a Management Accountant !ou will beas4ed to #price% products based on their costvalue 2his means setting the Sales "rice

<ou will have to consider1

6 Mar40up ,pro$t e*pressed as a P of cost.

8 Margin ,pro$t e*pressed as a P of price.

2r! the e*ample )*ercise page Q of !ournotes

Pricing

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 35/49

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 36/49

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 37/49

Marginal Costing

5#at is Marginal Costing5 2his ta4es place where Overhead Costs are

written o> in full to the period in which the!occur

"roduction Overheads under this methodare /O2 added to "rime Cost as is the casewith Absorption Costing

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 38/49

'irect Materials 'irect (abour 3ariable Costs 'irect )*penses

+ "rime Cost "roduction Overheads 0 Fi*ed Costs via OA-

+ 2otal "roduction ,Absorbed Cost.

/on0production Overheads + 2otal Cost

Absor"tion Costingtem"late

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 39/49

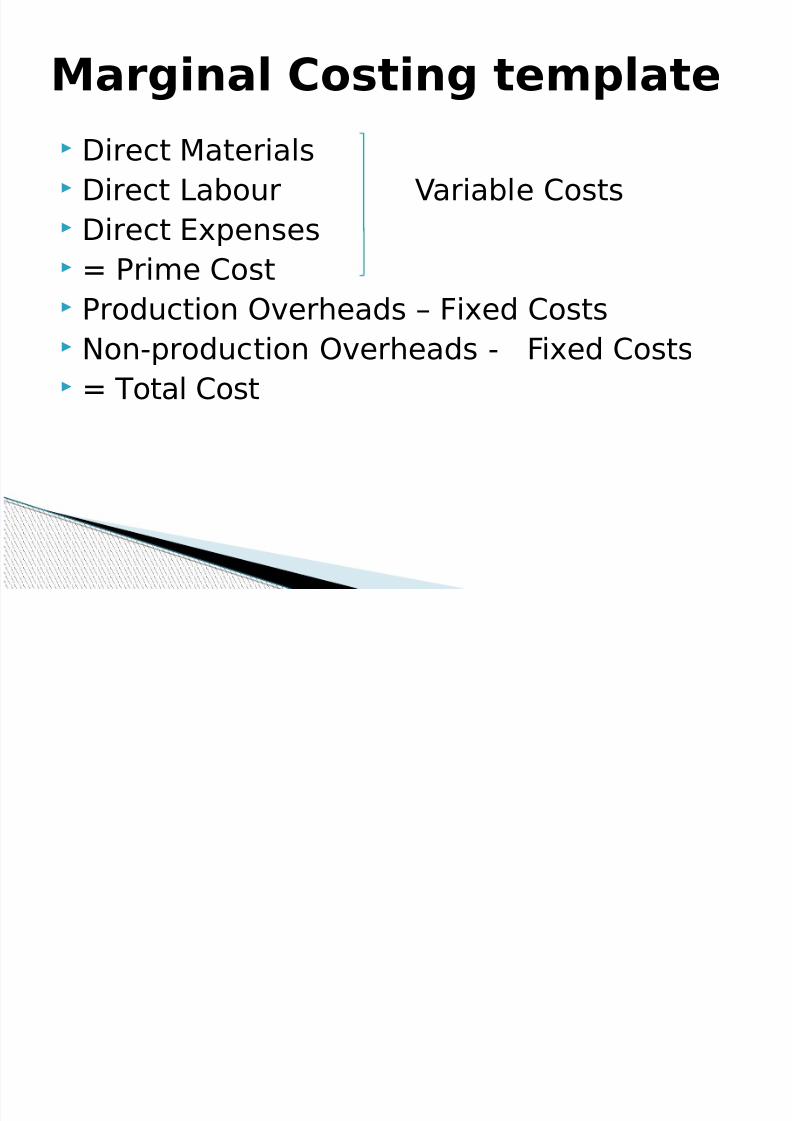

'irect Materials 'irect (abour 3ariable Costs 'irect )*penses

+ "rime Cost "roduction Overheads – Fi*ed Costs /on0production Overheads 0 Fi*ed Costs + 2otal Cost

Marginal Costing tem"late

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 40/49

Sales (ess "roduction Costs + =ross "ro$t

=ross "ro$t (ess )*penses ,/on0"roduction. + /et "ro$t

Absor"tion Costingtem"late

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 41/49

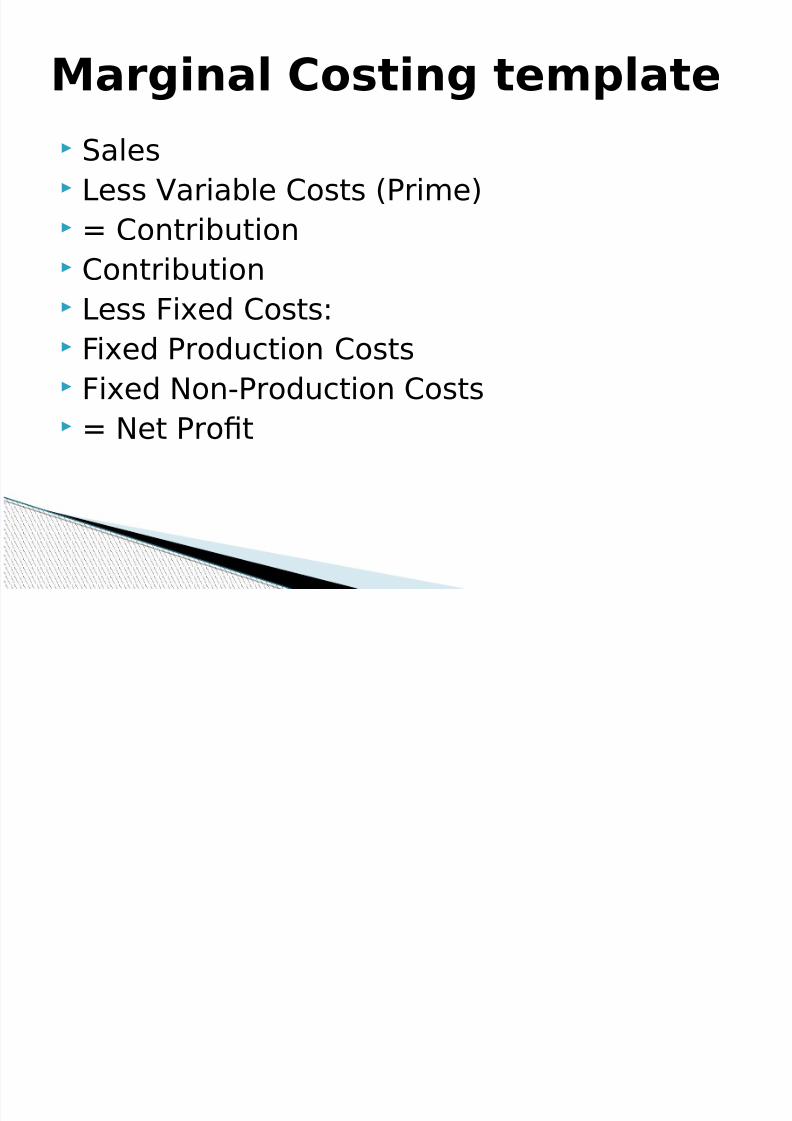

Sales (ess 3ariable Costs ,"rime. + Contribution

Contribution (ess Fi*ed Costs1 Fi*ed "roduction Costs Fi*ed /on0"roduction Costs + /et "ro$t

Marginal Costing tem"late

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 42/49

Write down the data I have we can practiceMarginal A/' Absorption Costing techniJues1

Sales "rice1 @8B 'irect Materials @ 'irect (abour @9 3ariable overheads @: All above are ")- ?/I2

Fi*ed Overheads @8BBBB ;udgeted eachmonth1

;udgeted "roduction 8BBBB units

Marginal Costing !xam"le1

i l i l

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 43/49

Actual "roduction & sales was 8BBBB ?nitsin a particular month1

Calculate1

6 Contribution per ?nit

8 2otal Contribution for the month

9 2otal "ro$t for the Month – A(( usingMA-=I/A( COS2I/=

: "ro$t for the month using AbsorptionCosting

Marginal Costing !xam"le1

i l C i l

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 44/49

In this e*ercise the "ro$ts achieved werethe same under Marginal & Absorptionmethods

Wh!5 ;ecause SA()S + "-O'?C2IO/ both

volumes are 8BBBB ?nits IF Sales & "roduction Juantities di>er the

pro$ts WI(( 'IFF)-G Accountants e*pect this & need to reconcile

the di>erence

Marginal Costing !xam"le1

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 45/49

2he reconciliation can be made simpler b!wor4ing to a method1

/ote1 2his is an e*am favourite topic (earn the ne*t slide well1 AC + Absorption Costing "ro$t MC + Marginal Costing "ro$t

A business can have opening & closing stoc4s Stoc4 levels MA< di>er We can then tac4le a second Juestion1

Marginal Costing

Ab i & M i l

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 46/49

If Op Stoc4 K Close Stoc4

If Op Stoc4 + Close Stoc4

If Op Stoc4 L Close Stoc4

Absor"tion & MarginalCosting+

MC "ro$t K AC "ro$t

MC "ro$t + AC "ro$t

MC "ro$t L AC "ro$t

2hese are )< -ules1 remember them –

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 47/49

Sales "rice @6B 'irect Materials @9 'irect (abour @8

3ariable overheads @6 Fi*ed Overheads @6BBBB per month ;udgeted "roduction BBB units per month Actual "roduction & Sales + :EBB units

-eJuired1 Wor4 out Marginal & Absorption "ro$ts

!xercise

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 48/49

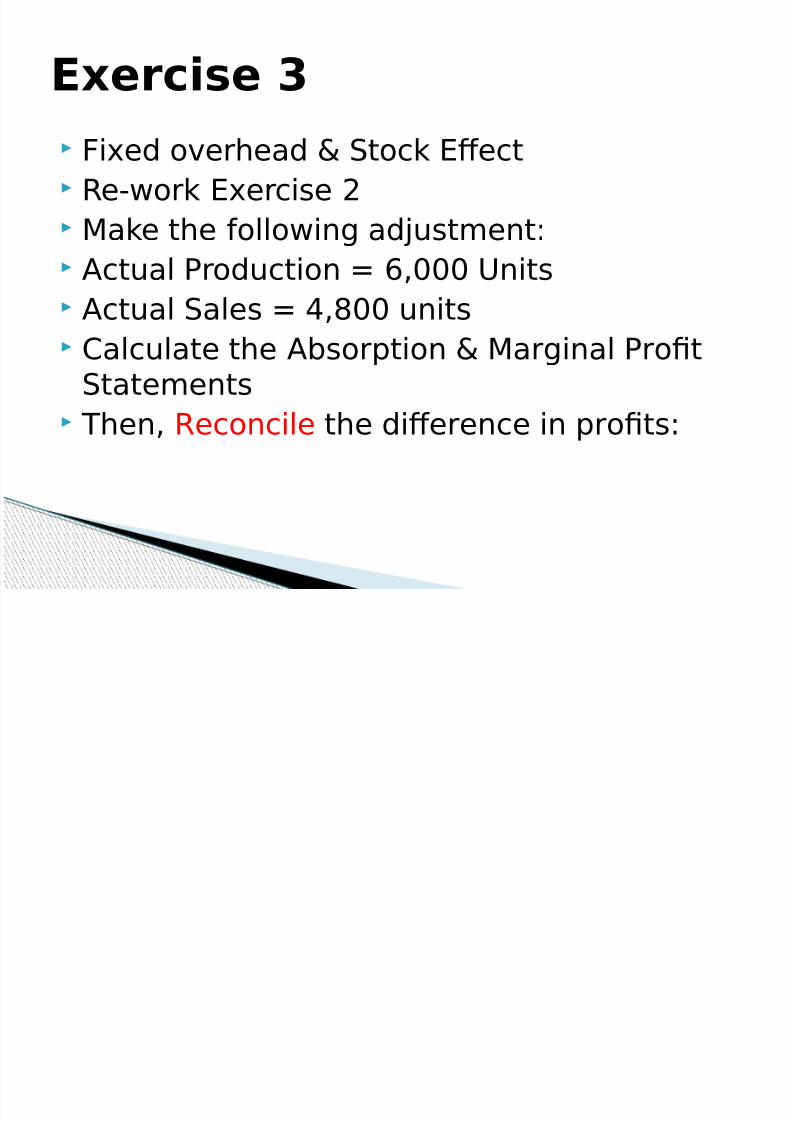

Fi*ed overhead & Stoc4 )>ect -e0wor4 )*ercise 8 Ma4e the following adRustment1

Actual "roduction + BBB ?nits Actual Sales + :EBB units Calculate the Absorption & Marginal "ro$t

Statements

2hen -econcile the di>erence in pro$ts1

!xercise 4

7/17/2019 CIMA C1 Unit 3 2012

http://slidepdf.com/reader/full/cima-c1-unit-3-2012 49/49