cimm: 403: islamic micro finance & its product...

TRANSCRIPT

?????????????????? ????

Certified Islamic Microfinance Manager

CERTIFIED ISLAMIC MICRO FINANCE MANAGER

INTRODUCTION TO RIBA, ISLAMIC ECONOMICS & ISLAMIC MICRO FINANCE

CIMM: 403: ISLAMIC MICRO FINANCE & ITS PRODUCT MECHANISM

Simply the best Automated Learning Solution

Flexible - Elegant - Convenient & Self-Managed Study

CIMM: 403

ISLAMIC MICRO FINANCE & ITS PRODUCT MECHANISM

“There is a feeling that the way Islamic Finance is structured the lack of freedom in leveraging, the

need for real assets-- that there will be some who will find Islamic Financing Interesting.”

Noor Mohammaed Yakop, Mayalsia's Second Finance Minister

CONTENTS

Islamic Microfinance

Islamic Microfinance for Alleviating Poverty and Sustaining Peace

Islamic Modes of Microfinance

Summary, Discussion Questions, Reference Material

1

22

34

60

1

ISLAMIC MICROFINANCE

The demand for Shari'ah compatible financial products and services is increasing with the rapid progress of Islamic finance industry. The SME and microfinance are no exception to this phenomenon, especially in Muslim countries. Rather, the system of microfinance is more attuned to the principles of Islamic finance, when seen through the justice in distribution of economic and financial resources. The participants are expected to develop good understanding of Islamic modes and their application to SME and microfinance, as well as, the product development process, enabling them to effectively apply in their organizations. The course however emphasizes more the Islamic microfinance.

Conceptual Framework of Islamic Microfinance

Islamic finance, being a sub-set of Islamic Economic System, can effectively achieve the objective of distributive justice. Deriving guidance form Shari'ah (Quran and Sunnah and Fiqah), it can prove instrumental in alleviation of poverty and equitable distribution of resources and opportunities.

Islamic financial system rests on the principles of prohibition of Riba, risk sharing, asset based financing, prohibition of excessive uncertainty and speculative behavior, sanctity of contracts, and operations in Shari'ah approved activities. Islamic financial System provides a set of rules and laws governing economic, social, political, and cultural aspects of Islamic societies. The principles underlying the philosophy of Islamic finance are discussed briefly:

Prohibition of Riba

The prohibition of Riba is the core which is based on argument of social justice and equality. Islam encourages the earning of profits but forbids the charging of interest because profits, determined once the business has succeeded (ex-post), are legitimate socially (meeting justice) and economically (creation of additional assets/wealth) whereas interest, determined before hand (ex-ante), is a cost that is accrued irrespective of the outcome of business operations i.e. Business may not create assets/wealth if there are losses. Social justice demands that borrowers and lenders share rewards as well as losses in an equitable fashion and that the process of wealth accumulation and distribution in the economy be fair and representative of true productivity.

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

The system of microfinance is

more attuned to the principles of Islamic finance,

when seen through the justice in

distribution of economic and

financial resources.

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

Keep In Mind

Social justice demands that borrowers and lenders share rewards as well as losses in an equitable fashion and that the process of wealt h accumulation and distribution in the economy be fair and representative of true

productivity.

Rights and Responsibilities of the Owner of the Capital Risk Sharing Principle

In an interest-based debt contract, the borrower has to service his debt irrespective of the performance of the project he engages in, even if poor performance obtains through no fault of the borrower. Accordingly the lender and borrower do not share in the risk of the venture. In Islam, ownership is based on two interrelated characteristics.

The owner is entitled to all earnings, returns, increments, etc., which are generated out of the owned asset (generally the financial capital in business financing). Simultaneously, ownership makes the owner the sole bearer of all responsibilities and risks regarding the loss of asset.

The principle has been expressed in the Prophet (PBUH)'s saying "al kharaj bi al daman "and in the general Fiqah axiom "al ghurm bi al ghunm", which means entitlement of gain is linked to the responsibility for loss. Because the interest is prohibited, suppliers of funds become investors instead of creditors. The provider(s) of financial capital and the entrepreneur share business risksin return for right of profits.

Business Risk: The possibility that a company will have lower than anticipated profits, or that it will experience a loss rather than a profit. Business risk is influenced by numerous factors, including sales volume, per-unit price, input costs, competition, and overall economic climate and government regulations.

___________________

Glossary:

Islam encourages the earning of

profits but forbids the charging of

interest

2

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

Asset Backed Financing

A financial transaction needs to end up in asset creation i.e. it is directly or indirectly linked to a real economic transaction. Conventional finance deals in money and financial papers only, which is prohibited in Islam. Financing in Islam is always based on illiquid assets which create real assets and inventories as result of trade and production in the economy.

Prohibition of Excessive Uncertainty and Speculative Behavior/gambling

Known as Gharar means exposing oneself to excessive risk and danger in a business transaction as a result of uncertainty about the price, the quality and the quantity of the counter-value, the date of delivery, the ability of either the buyer or the seller to fulfill the commitment, or ambiguity in the terms of the deal; thereby, exposing either of the two parties to unnecessary risks. Maisir refers to un-productive speculation/un-earned income and Qimar refers to gambling.

Sanctity of Contracts

Islam upholds contractual obligations and the disclosure of information as a sacred duty. This feature is intended to reduce the risk of asymmetric information and moral hazard.

Shari'ah-Approved Activities

Only those business activities that do not violate the rules of Shari'ah qualify for investment. For example, any investment in businesses dealing with alcohol, gambling, and casinos would be prohibited. It is general rule of Shari'ah that what ever is not prohibited is permitted.

Maisir refers to un-productive

speculation/un-earned income and

Qimar refers to gambling.

Conventional

finance deals in

money and financial

papers only, which is

prohibited in Islam.

Keep In Mind

Only those business activities that do not violate the rules of Shari’ah qualify for investment. For example, any investment in businesses dealing with alcohol, gambling, and casinos would be prohibited. It is general rule of

Shari’ah that what ever is not prohibited is permitted.

3

TIP

4

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

Islamic Microfinance: An Effective Tool for Poverty Alleviation and Social Development

Introduction

Islam is not only a religion but a complete code of life. Islam is a practical religion to be implemented in our daily life since it covers all facets of human life. As such, when implemented honestly and correctly, Islam provides solutions to all problems that are faced by humanity. One of the most widespread and dangerous problems faced by humanity is that of poverty, hunger and starvation. Millions of human beings on this planet are living under severe poverty and very brutal conditions.

The issue of poverty has been a focus of international community. Everybody is talking about poverty reduction and different measures are being suggested for the purpose. Different instruments are being tried with different levels of success. However situation has not improved to such a level where it can be claimed that this Anti poverty drive has paid its dividends. However, it is widely accepted that microfinance is the most effective tool for alleviation of poverty and uplifting the living standards of poor through real economic activities in society but as per market research, conventional micro financial system could not serve potentially as was expected due to the few deficiencies in the system. So, it is an immediate need to develop substitute financial products for microfinance institutions.

During the latest research on Microfinance sector, it is evaluated that Islamic financial system provides the best solutions for Poverty alleviation and Social sustainability, it is not only providing opportunity to utilize a sustainable system but also offers good rate of return & ideal performance compare to conventional microfinance system. Islamic Microfinance is a sub-set of Islamic Economic & Financial System.

This article is written by “Muhammad Zubair Mughal”, CEO of AlHuda CIBE.

___________________Reference:

Islam is not only a religion but a

complete code of life.

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

“Islamic microfinance basically refers to a system of localized finance arrangements set up as an alternative source of funds for small, low-income Islamic clients. Typically, users of Islamic microfinance have little or no collateral, as they do not possess significant assets, and would therefore be excluded from other forms of financing, including Islamic bank financing. Thus, Islamic microfinance provides a means of accessing funds for those who are unlikely to qualify for other forms of finance, yet are still seeking full compliance with Islamic law and the Islamic way of life.”

Sources of Islamic Microfinance

Islamic Microfinance products are basically derived from the four main sources of Fiqah. The first source is Quran-e-Pak, which is the Holy Book of Muslims. It is the constitution of the Muslims from which they derive the teachings which organize both their religious and everyday affairs. Many Islamic Microfinance products like Ijarah, Bai etc. have been derived from Quran-e-Pak. The Second source of Islamic Microfinance is Sunnah, the sayings and practices of the Holy Prophet Hazrat Muhammad (SAWW). Many Islamic Microfinance Products such as Mudarabah, Istisna, Wakalah, etc. have been derived from Sunnah. The third source of Islamic microfinance is Ijma'a which is the consensus among Jurists. Some Microfinance Products derived from Ijma'a like late payments charity mechanism etc. are being utilized in Islamic Microfinance Sector. The last source is Ijtihad & Qiyas (Analogy). Ijtihad refers to making a decision in Shari'ah by personal effort, independently of any school of jurisprudence as opposed to taklid, copying or obeying without question whereas Qiyas is the process of deductive analogy in which the teachings of the Hadiths are compared and contrasted with those of the Qur'an, in order to apply a known injunction to a new circumstance and create a new injunction. Takaful or Micro Takaful is an example of Ijtihad.

Keep In Mind

During the latest research on Microfinance sector, it is evaluated that Islamic financial system provides the best solutions for Poverty alleviation and Social sustainability, it is not only providing opportunity to utilize a sustainable system but also of fers good rate of return & ideal performance compare to conventional microfinance system. Islamic Microfinance is a sub -set of

Islamic Economic & Financial System.

Islamic Microfinance products are

basically derived from the four

main sources of Fiqah.

5

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

Islamic Microfinance Products Mechanism

Islamic Microfinance products can be segregated into four categories: the partnership Mode, Trade based Mode, Rental based mode and other Models like, Qard-e-Hasan, Waqf & Zakah, Islamic Cooperatives etc. In partnership Mode, MFIs & their clients enter into Partnership agreement for a business venture on profit and Lose sharing Mechanism. We have two Products in Partnership based mode, Musharakah & Mudarabah. In Trade based Mode, MFIs & their Clients enter into trading agreements . The products of Trade based Modes are Murabaha, Musawamah, Salam and Istisna. There are two products in Rental based mechanism; Ijarah (a Shari'ah Compliant mode of leasing) and Diminishing Musharakah. Qard e hasana is an Islamic financing, a loan, which under Islamic law is always free of profit. Zakah is one of the five Pillars of Islam which is the giving of a fixed portion of one's wealth to charity, generally to the poor and needy.

Basic Principle of Shari'ah Based Microfinance

Shari'ah based Microfinancing is based upon several principles like Prohibition of Interest and Gharar (Speculative Behavior), Asset Based Financing, Risk Sharing, Sanctity of contracts and financing in Halal/Shari'ah Complaint activities.Prohibition of interest is an important principle of Islamic Microfinance. Interest is forbidden in all the divine religions but Islam have strict verdict on it. Therefore Muslims hesitate to utilize Conventional financial system and remain excluded from financial access. Islam also prohibits speculative behaviors (Gharar) because in Islamic finance, any transaction entered into should be free from excessive uncertainty and speculation.

Keep In Mind

In partnership Mode, MFIs & their clients enter into Partnership agreement for a business venture on profit and Lose sharing Mechanism. In Trade based

Mode, MFIs & their Clients enter into trading agreements.

Prohibition of interest is an

important principle of Islamic

Microfinance.

6

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

Care for the poor and poverty alleviation are the religious obligations in Islam. In Islam, Zakah, Sadqa (Donation), Tabbrumm, Fitrana, Usher etc. are dedicated for financial well being of Poor people. Islam always encourages asset based financing, we have seen the recent international financial crisis and learned a lesson that financing without the backing of assets is always risky. One of the fundamental principles of Islamic Microfinance is Risk Sharing. Risk is shared in order to compensate the loss occurred. Islamic Microfinance emphasizes the Sanctity of Contracts. Micro Takaful is a Shari'ah Compliant System of Risk Mitigation.

The Products in Islamic Microfinance

There are different products in Islamic Microfinance which are as follows:

Murabaha - Cost Plus Sale

Literally it means a sale on mutually agreed profit which is also known as cost plus sale. It is one of the most widely used instruments for short-term financing where the Microfinance Institutes undertake to supply specific goods or commodities, incorporating a mutually agreed contract for resale to the client at a mutually negotiated margin. It can be utilize for purchase of raw material, equipment, agri. Inputs, Consumer goods, Vehicle, Houses etc. in Microfinance Sector.

Musharakah - Partnership

Musharakah means a relationship established under a contract by the mutual consent of the parties for sharing of profits and losses in the joint business. Musharakah can be used for Microenterprise setup, Small productive projects, Working capital financing etc.

Islam always encourages asset

based financing

Keep In Mind

Prohibition of interest is an important principle of Islamic M icrofinance. Interest is forbidden in all the divine religions but Islam have strict verdict on it. Therefore Muslims hesitate to utilize Conventional financial system and remain excluded from financial access. Islam also prohibits speculative behaviors (Gharar) because in Islamic finance, any transaction entered into

should be free from excessive uncertainty and speculation.

Murabaha literally

means a sale on

mutually agreed

profit which is also

known as cost plus

sale.

7

TIP

8

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

Mudarabah - Partnership

A trustee-type finance contract under which one party (MFI) provides the capital for a project and the other party (Client) provides the labor/Skill. Profit sharing is agreed between the two parties to the Mudarabah contract and the losses are borne by the provider of funds.

Salam Forward Sale

Salam means a contract in which advance payment is made for goods to be delivered later on. The seller undertakes to supply some specific goods to the buyer at a future date in exchange of an advance price fully paid at the time of contract. Salam is ideal product for Agricultural Financing.

Istisna - Manufacturing contract

A pre-delivery financing instrument used to finance projects where commodity is transacted before it comes into existence. It is an order to manufacture a specific commodity and payment of price, unlike Salam is flexible, where price may be paid in advance, or in installments or on delivery of goods. Istisna may be utilized in small manufacturing Business, for production use and entrepreneur Development sectors etc.

Ijarah Islamic Lease

Ijarah means letting on lease. It is a sale of a definite usufruct of any asset in exchange of definite reward. It is an arrangement under which the Islamic

Keep In Mind

Musharakah means a relationship established under a contract by the mutual consent of the parties for sharing of profits and losses in the joint business. Musharakah can be used for Microenterprise setup, Small

productive projects, Working capital financing etc.

Salam means a contract in which

advance payment is made for goods to be delivered later

on.

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

Microfinance Institution lease equipments, light Vehicles, Instruments, buildings or other facilities to a client, against an agreed rental.

Diminishing Musharakah Diminishing Partnership

Diminishing Musharakah is a form of Musharakah where the financier and his client participate in a joint commercial enterprise or property. This attains the form of undivided ownership of both the financier and the client. Over certain period the equity of financier is purchased by the client. This is an ideal product for Housing Finance sector, but can also be utilized for other ventures as well.Some other Models of Islamic Microfinance are Qard-e-Hasan Model, Waqf Model, Zakah Model, Cooperative Model and Micro Takaful (Islamic Micro insurance) etc.

Factors to be considered while doing IMF

There are several factors which should be considered while doing Islamic Microfinance. There is a misconception that Islamic Microfinance is only for Muslims but basically Islamic Microfinance is a system not a Religion so it can be utilized & operated by both Muslim and Non-Muslim Communities for Poverty Alleviation, Social & Economic Development.

As discussed earlier, Islamic Microfinance is Shari'ah compliant microfinance which is free from Riba and Gharar. It takes into consideration Shari'ah compliant funding as it is necessary for Islamic Microfinance Institutions to have Shari'ah complaint fund in Asset side & liability side. Islamic Microfinance deals in Shari'ah vetted Products according to AAOIFI standards. There should be trainings and Quality HR in this field and it is a very important element for Islamic Microfinance Institutions. There should be qualified Shari'ah Advisors, Shari'ah Review etc. in MFIs. One of the examples of Islamic Microfinance Products is Micro takaful which is the mechanism of Shari'ah compliant insurance

Ijarah means letting on lease. It is a sale

of a definite usufruct of any asset in

exchange of definite reward.

9

CIMM: 403: Islamic Microfinance & Its Products Mechanism

Compatibility of Islamic Microfinance Products with MF Models

Islamic Microfinance Products are quite compatible with all the other Conventional Microfinance Products and it can work with almost all the Conventional Microfinance models. One of the Conventional Microfinance Models is Grameen Model which is centrally managed, dedicated microfinance institution, consists of groups of five and has highly disciplined organizational structure. The focus is primarily on lending but every group member must save a certain amount. Amna Iftikhar Malaysia, Islamic Bank, Bangladesh Limited etc. use Grameen Model. Second model is Village Bank Model which is a microcredit methodology whereby financial services are administered locally rather than centralized in a formal bank. This Model is being used by Sanadiq program -Jabal al-Hoss, Syria, FINCA - Afghanistan etc.

Another Microfinance Model is Credit Union Model in which members of a target community gather their money and make loans to one another at low interest rates. Credit unions are smaller and non-profit oriented, charging interest rates that merely allow sustainability. Muslim Credit Union (Tobago), The Amwal, Credit Union etc. use Credit Union Model. The more recent phenomena of microcredit and microfinance are often based on a cooperative model which focuses on small business lending. Cooperative Model is being used by AlBaraka MPCS Mauritius, Al-Khair Coop. India, Muslim Community Coop. Australia and Karakorum Cooperative Bank Pakistan. In India, the most popular model is Self-help groups. SHGs are groups of between 15-20 people. Scheduled banks provide the loans and manage the savings for the group but the banks do not directly interact with the SHGs. Aameen Society - India is an example of entity using SHG.

Keep In Mind

As discussed earlier, Islamic Microfinance is Shari’ah compliant microfinance which is free from Riba and Gharar. It takes into consideration Shari’ah compliant funding as it is necessary for Islamic Microfinance Institutions to have Shari’ah complaint fund in Asset side & liability side. Islamic Microfinance deals in Shari’ah vetted Products according to AAOIFI standards.

10

11

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

Demand for Islamic Micro Finance - Research Studies by International Institutions

Some research studies were conducted by International Institutions which shown an appetite of Islamic Microfinance Products especially in Muslim Majority countries. According to CGAP Survey in 2008 in Jordan, Algeria and Syria, the 20%40% respondents gave preference to Islamic Microfinance. In 2007 the PlaNet Finance Survey in West bank and Gaza showed that 35%-60% respondents were in favor of Islamic Microfinance. The same situation resulted from other surveys like USAID conducted a survey in 2002 in Jordan which has shown that 24.9% of respondents who were in favor of Islamic Microfinance. IFC/FINCA conducted a survey in 2006 in Jordan in which 32% of respondents preferred Islamic Microfinance. Frankfurt School of Finance and Management conducted a survey in 2006 in Algeria which showed that 20.7% respondents favored IMF. IFC 2007 showed 43%-46% respondents in Syria and Bank Indonesia Survey showed 49% respondents in Indonesia who preferred Islamic Microfinance over conventional microfinance. AlHuda Centre of Islamic Banking and Economics has conducted a survey in 4 districts of Pakistan in which 99% of the respondents preferred Islamic Microfinance. These results show that Islamic Microfinance has a great demand in both Muslim and Non-Muslim Countries.

Research studies showed an

appetite of Islamic Microfinance

Products especially in Muslim Majority

countries.

Keep In Mind

AlHuda Centre of Islamic Banking and Economics has conducted a survey in 4 districts of Pakistan in which 99% of the respondents preferred Islamic Microfinance. These results show that Islamic Microfinance has a great

demand in both Muslim and Non-Muslim Countries.

12

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

Islamic Microfinance Institutions Worldwide

There are about 250 Islamic Microfinance Institutions which are working globally in 32 countries. There are 14 Islamic Microfinance Institutions in Pakistan whereas Yemen Sudan, Bangladesh, Afghanistan, UK, Malaysia have 11, 13, 9, 9, 5 and 11 Islamic Microfinance Institutions respectively. This shows that Islamic Microfinance Institutions exist worldwide not only in Muslim Countries but also in Non-Muslims Countries. The names of the countries along with the institutions providing Islamic Microfinance are shown in the below table:

Research studies showed an appetite

of Islamic Microfinance

Products especially in Muslim Majority

countries.

Countries

Indonesia BPRS, Islamic Financial Cooperatives referred as bait Maal wat Tamwil (BMT)

Bangladesh Islamic Bank Bangladesh, Social and Investment Bank,Al

Afghanistan FINCA (Qard Hasan), WOCCU, Ariana Financial Services , IFIC, etc.

Pakistan Akhuwat , Farz Foundation, ASASAH, Muslim Aid, Islamic Relief, CWCD, ,HHRD , NRSP, NRDP, Naymet etc.

Malaysia Amina Iftikhar, Tabung Haji etc

India AICMEU, BASIX, Sahulat, Bait-un-Nasr , Al-Khair Co- operative, Marwar Shariah Credit

Azerbaijan Bait –un Nasr

Egypt Mit Ghamar Project

Syria Sanadiq project Jabal al Hoss

Lebanon Mu’assat Bayat Al-Mal

Yemen Hodeidah Microfinance Program, Al- Amal Microfinance Bank

South Africa Awqaf South Africa

U.K Faith Matters, Islamic Relief, Muslim Aid, HSBC Amanah

Jordan Jordan Islamic Bank

CIMM: 403: Islamic Microfinance & Its Products Mechanism

A glimpse of Demand for Islamic Microfinance Worldwide

13

14

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

Pakistan as Leader of Islamic Microfinance Industry

Pakistan is considered to be a leader of Islamic Microfinance Industry. Islamic Microfinance Institutions operating in Pakistan are Akhuwat, Centre for Women Co-operative Development (CWCD), Narowal Rural Support Program (NRSP) KPK, Farz Foundation, Islamic Relief, KKCB, Helping Hand for Relief and Development, Muslim Aid, Deep Foundation, NGO World, Al-Noor Foundation etc. the product wise detail of Islamic Microfinance Institutions operating in Pakistan are:

Pakistan is considered to be a

leader of Islamic Microfinance

Industry.

Institution

Akhuwat Qaraz-e-Hasna, MicroTakaful, Grants

CWCD Murabaha, Ijarah, Salam & Istisna MicroTakaful

NRSP –K PK Murabaha Mudarabah with BOK for funding Source

Farz Foundation Murabaha, Musharakah, Livestock

CIMM: 403: Islamic Microfinance & Its Products Mechanism

Institution

Islamic Relief Murabaha and Qarz-e-Hassan

KKCB b a icr fMura ah and M oTaka ul

Helping Hand for RD Murabaha, Mudarabah

Muslim Aid Murabaha

NRDP, Deep Foundation, NGO world, Al Noor Foundation 5 MicroTakaful Co, 5 Full fledge Islamic Banks, 13 SAIBB

15

16

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

Need Assessment of Islamic Microfinance

Islamic Microfinance is an emerging Market worldwide. Approximately 44% conventional microfinance clients worldwide reside in Muslim countries. Research shows that almost one-half of the 56 IDB member countries in Asia and Africa are classed as United Nations Least Developed Countries (LDCs). Islamic Asset-based Financing can prevent diversion of funds for consumption. For Muslim majority countries, great need for Islamic Microfinance exists and large target segment is averse to the interest based microfinance products. Islamic Microfinance have proven track record that its deals with long lasting & Complete solutions for Sustainability.

When we look for need assessment of Islamic Microfinance in Central Asia, the Caucasus and South Asia, we see a great demand. Total Population of South Asia, Central Asia, West Africa and MENA Region & Caucasus are 2.4 Billion , out of them 1.12 Billion are Muslims which are 47.3%, and shows a big Demand of Islamic Microfinance Products for Financial Inclusion because Muslim are reluctant to move Interest based MF System. IMF is beneficial for Muslim as well as for Non-Muslims. According to World Bank, South Asia is home to half the world's poor, where Muslim population is 33.2% of total population, which shows immediate need of Islamic Microfinance there and shows a great potential and requirement for Islamic Microfinance in these regions.

Keep In Mind

Islamic Asset -based Financing can prevent diversion of funds for consumption. For Muslim majority countries, great need for Islamic Microfinance exists and large target segment is averse to the interest based microfinance products. Islamic Microfinance have proven track record that

its deals with long lasting & Complete solutions for Sustainability.

Islamic Microfinance is an emerging Market

worldwide

17

CIMM: 403: Islamic Microfinance & Its Products Mechanism

CIMM: 403: Islamic Microfinance & Its Products Mechanism

Need Assessment of Islamic Microfinance in Different Continents

118

19

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

Challenges faced by Islamic Microfinance

Islamic Microfinance Institutions are facing some challenges which are needed to be addressed. The biggest challenge which is now faced by Islamic Microfinance Industry is the non-availability of donors and Shari'ah Compliant Sources of Funds which is also a hurdle in the way to scale it up. There is a need to develop a uniform regulatory and legal framework for Islamic Microfinance Institutions. Due to limited Islamic microfinance institutions, this sector is also facing the shortage of quality HR. There is a big need to develop Shari'ah expertise towards the growth of Islamic Microfinance. If we see the product mix of Islamic Microfinance industry, it is seen that only Murabaha is covering almost 80% Microfinance Industry so there is an immediate need of research on other Islamic Microfinance Products for product diversification. In short, standardization of Islamic Microfinance Products is very much needed.

Opportunities for Islamic Microfinance

Many opportunities exist for Islamic Microfinance sector. International Islamic Microfinance Network (IMFN) was established in 2009 by Islamic Microfinance institutions to strengthen and support the Islamic Microfinance Institutions. It is an effective platform for coordination and harmony among Islamic Microfinance Institutions. One should try to expand the market of Islamic Microfinance where conventional Microfinance Institutions face limitations especially in Muslim Majority Countries. AlHuda Centre of Islamic Banking and Economics, Pakistan has established an Islamic Microfinance Help desk for advisory, trainings and capacity building for Microfinance Institutions. It provides complete solutions in the field of Islamic Microfinance.

Keep In Mind

There is a big need to develop Shari’ah expertise towards the growth of Islamic Microfinance. If we see the product mix of Islamic Microfinance industry, it is seen that only Murabaha is covering almost 80% Microfinance Industry so there is an immediate need of research on other Islamic Microfinance Products for product diversification. In short, standardization of Islamic Microfinance Products is very much needed.

There is a need to develop a uniform

regulatory and legal framework for Islamic

Microfinance Institutions.

20

CIMM: 403: Islamic Microfinance & Its Products Mechanism

A perfectly sustainable system with goal of poverty alleviation is needed to expand Islamic Microfinance. Islamic Banking and Finance is emerging in South Asia and MENA region which will strengthen the Islamic Microfinance effectively.

A Case Study from Pakistan: AKHUWAT Pakistan

Akhuwat is a big name in Islamic Microfinance Market in Pakistan. It was established in 2001. Akhuwat is basically using Qarz-e-Hassan Model in order to promote Qard-e-Hassan as a viable model and a broad-based solution for poverty alleviation. It provides interest free microfinance services to poor families enabling them to become self reliant. Akhuwat has 63 branches in 38 cities and towns of Pakistan. As of January 31, 2012, 132867 families are its borrowers in which 89890 loans are utilized by female borrowers. It has distributed the amount of PKR 1664821742. The recovery rate of the loans granted is 99.85% and no. of active loans is 45297. It is indeed a decay of hope.

Keep In Mind

One should try to expand the market of Islamic Microfinance where conventional Microfinance Institutions face limitations especially in Muslim Majority Countries. AlHuda Centre of Islamic Banking and Economics, Pakistan has established an Islamic Microfina nce Help desk for advisory, trainings and capacity building for Microfinance Institutions which provides complete solutions in the field of Islamic Microfinance.

21

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

Compatibility of Microfinance with Islamic Modes

Microfinance is a proven tool for increased access to the financial services by the disadvantaged people. The communities which reject the conventional interest based financial instruments, are excluded from benefit of the only available vent to redress their miseries of poverty and powerlessness. Microfinance Institutions (MFIs) can increase their penetration by introducing the Islamic financial instruments both for Microcredit and Microsavings. The compatibility of the principles of Islamic finance with the best practices of microfinance provides sufficient convenience to devise the operational mechanism for introducing Islamic modes of financing and expanding the outreach.

Ideally, the microfinance works through the principle of joint liability (peer groups), providing short maturity graduating cycles of small loans, repayments conforming to the business cash flow, as well as, promoting saving habits to cope with the unforeseen adversity and maintaining liquidity. These characteristics provide strong nexus with the Islamic finance. Social collateral, an important invention of microfinance, facilitates providing collateral free loans, yet achieving very high recovery rates (close to 100%). Islamic modes of sharing profit and loss also minimizes the need for collateral, as surveillance of MFI being partner in the results of business does not leave any room for acquiring collateral. Even the deferred payment in sale transaction is more secured in peer groups. Further, Islamic insurance (takaful) and the surety-ship/mutual guarantee (Kafalah) reflect collective responsibility and fulfill requirement of group lending. Working with the client brings comparative advantage of procuring supplies at competitive rates and fetching better prices and sharing of profits at source.

Microcredit: An extremely small loan given to impoverished people to help them become

self employed.

Microsavings: A branch of microfinance, consisting of a small deposit account offered to

lower income families or individuals as an incentive to store funds for future use.

Microsavings accounts work similar to a normal savings account, however, are designed

around smaller amounts of money.

_____________________Glossary:

Islamic modes of sharing profit and

loss also minimizes the need for

collateral

Microfinance

Institutions (MFIs)

can increase their

penetration by

introducing the

Islamic financial

instruments both for

Microcredit and

Microsavings.

TIP

22

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

ISLAMIC MICROFINANCE FOR ALLEVIATING POVERTY AND SUSTAINING PEACE

Introduction

Peace is humanity's highest values, its prized possession; the most sought after and yet the most elusive. Peace encompasses a broad array of social, political and

economic aspects. Peace is threatened by unjust economic, social and political order, absence of democracy, environmental degradation and absence of human rights. Every single individual has the potential and the right to live a decent life.

Peace is interlinked with poverty. Poverty can unsettle peace. Poverty is a concept with many facets. It is the individuals' lack of freedom and ability to meet daily needs for themselves and their dependents. Poverty encompasses failure to attain minimum living levels, welfare attributes as well as the resources that may enable people to improve their conditions. The root causes of poverty cannot be solved by a short-term infusion. It requires the building of systems, structures, capacity. A Vatican communiqué states “The scandal of poverty reveals the inadequacy of current systems of human coexistence in promoting the realization of the common good. This imposes the need for reflection on the deep roots of material poverty and, consequently, also on spiritual poverty that makes man indifferent to the suffering of others”. In fact the frustrations, hostility and anger spawned by poverty cannot sustain peace in any society. For building stable peace, society must find ways to provide opportunities for people to live with dignity. The society must ensure the fulfillment of basic needs.

More than a billion people live on less than a dollar a day. The moral test of a society is how it treats its most vulnerable members. The poor have the most urgent moral claim on the conscience of the nation and it should look at its policies that affect the poor.

The Article “Islamic Microfinance for Alleviating Poverty and Sustaining Peace” is written by Tanim Laila, Director, Economics Division, Institute of Hazrat Muhammad SAW.

___________________Glossary:

Peace is interlinked with poverty.

Poverty can unsettle peace.

23

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

Deprivation and powerlessness of the poor wounds the whole community. On the other hand, a healthy community can be achieved only the able members of society accords proper addresses the needs of the poor. This includes proving the poor the opportunity and tools too work their way out of poverty. People have a right to economic initiative and private property, but these rights have limits. No one is allowed to amass excessive wealth when others lack the basic necessities of life. Peace is the fruit of justice and is dependent upon right order among human beings. Peace is more than end of violence. Peace is unity and harmony. Peace upholding the rights of others and fulfillment of basic human needs.

A Crisis that Disrupted Economic Wellbeing

The world is slowly recovering from the worst financial crisis ever. The crisis has undone major strides in the millennium development goals. Analyst believe the world's pledge to achieve the MDGsby 2014 may not be achievable. People round the world are poorer and hungrier than in the recent past. The socio-economic problems facing people today have emanated from the unbridled creation of fictitious assets, particularly reserve currencies, and the unhindered forces of demand and supply with exploitative tools in the financial system.

MDGs: MDGs stand for Millennium Developed Goals. The MDGs are eight international development goals that all 193 United Nations Member states and at least 23 international organizations have agreed to achieve by the year 2015. They include eradicating extreme poverty, reducing child mortality rates, fighting disease epidemics such as AIDs and developing a global partnership for development.

_________________Glossary:

Keep In Mind

The root causes of poverty cannot be solved by a short -term infusion. It requires the building of systems, structures, capacity. A Vatican communiqué states “The scandal of poverty reveals the inadequacy of current systems of human coexistence in promoting the realization of the common good. This imposes the need for reflection on the deep roots of material poverty and, consequently, also on spiritual poverty that makes man indifferent to the

suffering of others”.

Deprivation and powerlessness of the poor wounds

the whole community.

24

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

John Perkins, in the preface to his book, Confessions of an Economic Hitman, while analysing the dangerous world situation, writes: “The idea that all economic growth benefits humankind and that the greater the growth, the more widespread the benefits, _ _ _ is of course erroneous _ _ _ It benefits only a small portion of the population _ _ _ may result in increasingly desperate circumstances for the majority _ _ _ When men and women are rewarded for greed, greed becomes a corrupting motivator.”

Islamic economists (e.g., Siddiqui, 2009; Chapra, 2009, Bagsiraj, 2009) continually refer to the global economic crisis as a result of interest rates (Riba) from the great depression to the crisis in the western countries. Huge budgetary imbalances, excessive monetary expansion, large balance of paymentsdeficits, insufficient foreign aid, and inadequate international cooperation can all be related to flaws in the theory of interest - the root of the crisis. If the value of an Islamic bank's liabilities were determined by the performance of its assets, there would be no sub-prime crisis. Unfortunately, risk-sharing techniques do not predominate in the world of modern finance.

Economic well being is the primary goal of development. It is one thing to be a wealthy nation but unless that wealth is spread medium/ long term stability cannot be guaranteed. A modern welfare state performs four economic functions, viz. establishing the legal framework for the economy; directing allocation of resources to improve economic efficiency; establishing programmes to improve distribution of income and stabilizing the economy through macroeconomic policies.

Goals of macroeconomic policy are full employment, price stability, economic growth and comfortable Balance of Payment situation. Money, credit & finance are the life blood of the economic system. Wealth creation involves using goods and services (wealth) already available in the economy. Money or finance makes it possible to cycle existing wealth to create further wealth.

Keep In Mind

Huge budgetary imbalances, excessive monetary expansion, large balance of payments deficits, insufficient foreign aid, and inadequate international cooperation can all be related to flaws in the theory of interest - the root of the crisis. If the value of an Islamic bank’s liabilities were determined by the performance of its assets, there would be no sub-prime crisis. Unfortunately,

risk-sharing techniques do not predominate in the world of modern finance.

Deprivation and powerlessness of the poor wounds

the whole community.

25

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

The global financial may have been avoided had the use of fictitious monetary assets not been so easy and widespread. The solution lies in disciplining the creation of money, limiting self-interest with social interest and business ethics, and transforming the corrupt financial system to make it free from exploitation and games of chance, thus enabling mankind to optimally use the resources for benefits on a larger scale. Islamic finance provides a solid basis for these reformatory measures; it is up to human beings how they realize the potential.

In the midst of such an unprecedented crisis, Islamic banking and finance is witnessing phenomenal growth, with the global value of Islamic finance approaching $1 trillion. According to an estimate by the Asian Development Bank, the average annual growth of the Islamic banking and financial sector is more than 15 percent. Islamic banking and finance is now among the fastest-growing financial segments in the international financial system. This has lead to much research and interest.

Characteristics of Islamic Finance and Islamic Microfinance

The Islamic economics system is based on justice, equity and welfare. Islamic economics seeks to establish a broad-based economic well-being with full employment and optimum rate of economic growth. It will bring socio-economic justice and equitable distribution of income and wealth. Islamic economics will also ensure the stability in the value of money to enable the medium of exchange to be a reliable unit of account and a stable store of value.

The system strikes a balance between flexibility and oversight. The proponent of Islamic banking system expect that credit cruch could not happen in the Islamic financial institutions, because this system operates based on partnership between the client and the banks. There is a social commitment within the Islamic banking and finance. This crisis has stunned both the left and the right of the political spectrum and the different economic schools of thought. Many economists and policy makers have suggested more regulation and transparency, with only a few highlighting the role greed and speculation played. Islamic finance provides moral injunctions on accountability to the Creator to check human vices such as greed. It also enforces market discipline through limits on leverage, excessive lending and derivatives.

Islamic finance provides a solid

basis for the reformatory

measures; it is up to human beings how they realize

the potential.

26

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

The Islamic economic system is based on the Shari'ah Law. The Shari'ah is derived from two primary Sources of Islamic law, namely the divine revelations set forth in the Qur'an, and the sayings and example set by the Islamic Prophet Muhammad in the Sunnah. Islamic Jurisprudence interprets and extends the application of Shari'ah to questions not directly addressed in the primary sources by including secondary sources.

These secondary sources usually include the consensus of the religious scholars embodied in ijma, and analogy from the Qur'an and Sunnah through qiyas.

Islamic economics, in fact, can promote a balance between the social and economic aspects of human society, the self and social interests and between the individual, family, society and the State. It can effectively address issues like income distribution and poverty alleviation, which capitalism has not been able to address. At the global level, it may be helpful in eliminating the sources of instability, thus making the world a happier place with harmony among followers of various religions. In the words of Dr Zeti Akhtar Aziz, ex Governor of Bank Negara Malaysia, 'Islamic finance is a corporate, social responsibility movement of the educated, enlightened Muslim middle classes'.

Traditional vs. Islamic Microfinance

In traditional bank loans secured by collateral substantially detaches bankers from the risks faced by their clients. In fact it even creates conflicts of interest. Traditional banks are also biased towards the rich. Poor people with good ideas but no collateral often fail to attract finance under this system, with the result that wealth inequality increases from one generation to the next. The risk-sharing financing of Islamic Banks has the potential to do away with conflicts of interest and usher in greater economic stability.

Islamic Economics system strikes a

balance between flexibility and

oversight.

Keep In Mind

The Islamic economics system is based on justice, equity and welfare. Islamic economics seeks to establish a broad -based economic well -being with full employment and optimum rate of economic growth. It will bring socio -economic justice and equitable distribution of income and wealth. Islamic economics will also ensure the stability in the value of money to enable the medium of exchange to be a reliable unit of account and a stable store of

value.

The Shari’ah is

derived from two

primary Sources of

Islamic law, namely

the Quran and the

Sunnah.

TIP

27

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

Entrepreneurs and conventional bankers like to increase excessive risk, and then insulate themselves from it, in order to increase their return on capital. In this way, an entrepreneur can borrow from a bank at fixed interest and then invest in a business that makes profit. The entrepreneur retains profit out of the borrowed money. Such incentive encourages entrepreneurs to borrow heavily and grow their business operations. One consequence of this approach is that a few large organizations have come to dominate the business landscape.

The heavy indebtedness of such corporations means that a moderate rise in interest rates combined with a moderate fall in revenues can quickly erode an entire profit margin. This is one reason that share prices can change so dramatically over relatively short periods. Furthermore, interest charges on bank finance are a cost item in the production process and, therefore, act to increase the price of goods and services. The interest payments that society receives from the conventional banking system are funded by society itself.

Islam has a completely different philosophy for the economy that results in a very different society from a capitalist one. The overall direction of the Islamic economic system is to secure the satisfaction of all basic needs for every individual completely, and to enable them to satisfy their needs as much as possible. From this perspective, Islam looks at people individually rather than the whole of society. This means economic polices will look to cater for all rather than just leaving satisfaction to the market. This may be achieved by a host of rules Islam has to ensure wealth distribution and by government involvement in the economy to ensure that it moves in the direction Islam has designated.

Qiyas: Literally it means measure, example, comparison or analogy. Technically, it means a

derivation of the law on the analogy of an existing law if the basis of the two is the same. It is

one of the sources of Islamic law.

________________-Glossary:

Entrepreneurs and

conventional

bankers like to

increase excessive

risk, and then

insulate themselves

from it, in order to

increase their return

on capital.

Most Islamic scholars enjoin

that money should be fully backed by

real assets.

Keep In Mind

Islam looks at people individually rather than the whole of society. This means economic polices will look to cater for all rather than just leaving satisfaction to the market. This may be achieved by a host of rules Islam has to ensure wealth distribution and by government involvement in the economy to ensure that it moves in the direction Islam has designated.

TIP

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

While both systems accept money to be a store of value and a medium of exchange, the financial market-based economic system permits money to be treated like any other commodity which can be traded for a profit/interest. In contrast, most Islamic scholars enjoin that money should be fully backed by real assets. It is not permissible for money to be traded for money except at par. From the Islamic perspective, a key consequence of permitting both creation of credit money and interest-based lending is to allow banks and other financial institutions to generate massive amounts of wealth at the expense of the rest of society, especially the poor, resulting in the inevitable charge that the economic system persistently favors the rich over the poor.

Inequity has become the hallmark and the most serious problem facing mankind in all societies. Masses of people in almost all emerging/developing, Islamic and non-Islamic, and even developed and industrialized economies are facing the same fate. The interest-based financial system is a major hurdle in achieving distributive justice. It is creating un-repayable debt making a class of people richer and leaving others poorer and oppressed. Excessive debt and its servicing are the striking features of the interest-based mechanism: yesterday's debt can be repaid by taking out more debt today. The economic problems of developing countries are the result of excessive debt accumulation. The cost incurred in the form of interest has to be paid by successive governments through increasing rates, taxes and charges on consumption goods and utilities. For servicing the debts, governments raise taxes without providing any socioeconomic amenities. Their foreign exchange earnings, including export proceeds and remittances of expatriates, are also consumed by debt servicing.

Leaving aside the poor and developing countries, even the developed countries have become accustomed to the bane of debt. The real story of modern empire, writes John Perkins, is that it “exploits desperate people and is executing history's most brutal, selfish and ultimately self-destructive resource-grab.”

Experience has shown that micro-enterprises have generally proved to be viable institutions with respectable rates of return and low default rates. They have also proved to be a successful tool in the fight against poverty and unemployment. The experience of the International Fund for Agricultural Development (IFAD) is that credit provided to the most enterprising of the poor is quickly repaid by them from their higher earnings.

Debt Service: The cash that is required for a particular time period to cover the repayment of

interest and principal on a debt. Debt service is often calculated on a yearly basis.

___________________-Glossary:

Inequity has become the

hallmark and the most serious

problem facing mankind in all

28

CIMM: 403: Islamic Microfinance & Its Products Mechanism

A number of countries have, accordingly, established special institutions to grant credit to the poor and lower middle class entrepreneurs. Even though these have been extremely useful, there are two major problems that need to be resolved. One of these is the high cost of finance in the interest-oriented microfinance system. A timely study by Dr. Qazi Kholiquzzaman Ahmed, President of the Bangladesh Economic Association, has revealed that the effective rate of interestcharged by microfinance institutions, including the Grameen Bank, turns out to be as high as 30 to 45 percent. This causes serious hardship to the borrowers in servicing their debt. They are often constrained to not only sacrifice essential consumption but also borrow from money-lenders. This engulfs them unwittingly into an unending debt cycle which will not only perpetuate poverty but also ultimately lead to a rise in unrest and social tensions.

It is, therefore, important that, while the group lending method adopted by the Grameen bank and other microfinance institutions for ensuring repayment is retained, microcredit is provided to the very poor on a humane interest-free basis. This may be possible if the microfinance system is integrated with zakah and awqaf institutions. For those who can afford to bear the cost of microfinance, it would be better to popularize the Islamic modes of profit-and-loss sharing and sales-and lease-

Effective Rate of Interest: An investment's annual rate of interest when compounding

occurs more often than once a year. Calculated as the following:

_____________________Glossary:

Keep In Mind

Experience has shown that micro -enterprises have generally proved to be viable institutions with respectable rates of return and low default rates. They have also proved to be a successful tool in the fight against poverty and unemployment. The experience of the International Fund for Agricultural Development (IFAD) is that credit provided to the most enterprising of the

poor is quickly repaid by them from their higher earnings.

29

30

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

based modes of finance in Muslim countries not only to avoid interest but also to prevent the misuse of credit for personal consumption. Moreover, availability of resources at the disposal is an issue faced by of microfinance institutions. This problem may be difficult to solve unless the microfinance sector is scaled up by integrating it with the commercial banks in order to enable the use of a significant proportion of their vast financial resources for actualizing a crucial socio-economic goal.

The risk arises from the inability of micro-enterprises to provide acceptable collateral. One way of reducing the risk is to use the group lending method which has already proved its effectiveness. Another way is to establish the now-familiar loan guarantee scheme which has been introduced in a number of countries. To reduce the burden on the loan guarantee scheme it may be possible to cover the losses arising from the default of very small micro-enterprises from the zakah fund provided that the loan has been granted on the basis of Islamic modes of finance and does not involve interest. A third way is to minimize the use of credit for personal consumption by providing credit in the form of tools and equipment through the ijarah (lease) mode of Islamic finance rather than in the form of cash. The raw materials and merchandise needed by them may be provided on the basis of Murabaha, Salamand Istisna modes. If they also need some working capital, it may be provided as Qard Hasan (interest-free loan) from the zakah fund.

Salam: Salam means a contract in which advance payment is made for goods to be delivered

later on. The seller undertakes to supply some specific goods to the buyer at a future date in

exchange of an advance price fully paid at the time of contract.

Istisna: It is a contractual agreement for manufacturing goods and commodities, allowing

cash payment in advance and future delivery or a future payment and future delivery. A

manufacturer or builder agrees to produce or build a well described good or building at a

given price on a given date in the future.

Ijarah: Letting on lease. It refers to the sale of a definite usufruct of any asset in exchange of definite reward. It is an arrangement under which the Islamic banks lease equipments, buildings or other facilities to a client, against an agreed rental.

-____________________Glossary:

Availability of resources at the

disposal is an issue faced by of

microfinance institutions.

31

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

Poverty Alleviation through Zakat and Waqf

The institution of microfinance was developed to create access to funds for the poor and unbanked population. However, Conventional microfinance is not for the poorest of the poor. There is a sizeable substratum within the rural poor whose lives are unlikely to be touched, let alone improved by financial services. They are not "bankable" in their own or their neighbour's eyes, even when the bank is exclusively for poor people. Yet they desperately need some sort of assistance. In addition, traditional microfinance institutions based on compounding interest causes serious hardship on the borrowers in servicing their debt. It is, therefore, important th at access to credit is provided to the poor on more humane, interest-free basis. This may be possible if the microfinance system is integrated with Zakah and Waqf institutions.

An Islamic microfinance system, on the other hand, identifies being the poorest of the poor as the primary criterion of eligibility for receiving zakah. It is geared towards eliminating abject poverty through its institutions based on zakah and sadaqah. Zakah and sadaqah as instruments of charity occupy a central position in the Islamic scheme of poverty alleviation. Zakah is the third among five pillars of Islam and payment of zakah is an obligation on the wealth of every Muslim based on clear-cut criteria. Zakah has been variously described by scholars as a tool of redistribution of income, a tool of public finance, and of course, as a mechanism of development and poverty alleviation. Rules of Shari'ah are fairly clear and elaborate in defining the nature of who are liable to pay zakah and who can benefit from zakah. The first and foremost category of potential beneficiaries is the poor and the destitute. A greater degree of flexibility exists with respect to beneficiaries of sadaqah.

Traditional microfinance

institutions based on compounding

interest causes serious hardship on

the borrowers in servicing their debt.

32

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

The primary issue with zakah and sadaqah-dependent institutions is the issue of sustainability as they are essentially rooted in voluntarism. Funds mobilized through charity could fluctuate from time to time and may not lend themselves to careful planning and implementation.

The issue of sustainability is addressed in the institution of awqaf through creation of permanent and income-generating physical assets. Awqaf has historically been the major vehicle for creating community assets. On the flip side, the restrictions on development and use of assets under waqf for pre-specified purposes introduce rigidity into the system. Undoubtedly, it is important to preserve and develop assets under waqf to add to productive capacity and create capabilities for wealth creation. Awqaf may also be created specifically to impart knowledge and skills in entrepreneurship development among the poor as microfinance alone cannot create wealth unless combined with entrepreneurial skills. Indeed all technical assistance programs can be organized as awqaf.

While zakah funds must be distributed to the destitute and poorest of poor, this institution could be integrated with microfinance. This may be attempted by seeking to push such individuals through zakah distribution out of dire poverty to levels, where they are no longer regarded as “un-bankable” by MFIs. A linkage if established between the MFIs and zakah funds would enhance the effectiveness of microfinance towards achieving poverty alleviation.

Zakah is a cornerstone of the values that govern Islamic economics. It created the first universal welfare system in human history. It specifies the manner in which zakah revenue is to be raised and who pays it. On the expenditure side it set forth the uses of zakat revenue. Like a modern budget it describes the economic order that it attempts to establish and express the ideals and aspirations of society. As a fiscal mechanism zakat performs some of the major functions of public finance

Sadaqah: Charitable giving

____________________Glossary:

Keep In Mind

A greater degree of flexibility exists with respect to beneficiaries of sadaqah. The primary issue with zakah and sadaqah-dependent institutions is the issue of sustainability as they are essentially rooted in voluntarism. Funds mobilized through charity could fluct uate from time to time and may not lend themselves to careful planning and implementation.

Zakah funds must be distributed to

the destitute and poorest of poor, this institution could be

integrated with microfinance.

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

which deal with social security entitlement system like food subsidy, education, health care etc. Thus Islam discourages accumulation of personal assets and encouraging eradication of poverty.

Zakah is Free Money. It is a grant for the poor It may be reiterated that zakah is an Islamic charitable fund and therefore, no form of interest or profit can be made from it. It is free money and it a right of the poor and hence may be used in Islamic microfinance. Although traditional interestbased microcredit has evolved as an important tool for poverty alleviation, it is failing to attain desired effects for many reasons:

§ A major portion of loan disbursed to the poor is diverted to fulfill their basic consumption needs that leaves them with smaller investable fund and hampers business profitability.

§ Traditional microfinance institutions (MFIs) charge higher interest rate than banks that may lead to credit rationing problem as only higher return projects being selected and overall social welfare not being maximized.

§ Similar projects in different locations may differ in their profitability. But MFIs usually charge standard fixed interest rates for similar projects.

Because of these three reasons non-graduation from poverty for conventional MFIs is falling. In addition to zakah funds in Islamic Microfinance Shari'ah based and profit and loss sharing or equity participation modes may also be utilized to give the poor access to funds. The bank's sharing of risk and the return is undoubtedly more beneficial for the poor. Conclusion

The major objective of economic policy has been to promote growth in the overall pursuit of development and happiness of the population. However, it has been observed that because of rising inequality, growth alone is not a reliable indicator of socio-economic development. Despite growth in many parts of the world, a large number of people are unemployed, half-fed and ill-treated as a result of unhindered market forces. A growing population who are marginalized in terms of economic opportunities due to the omnipresence of interest and an economic system that does fulfill their basic needs poses a threat to peace. To quote the words on ILO headquarter “If you want peace, cultivate justice”. Socio-economic justice is essential for lasting peace and harmony in any and all nations.

In the aftermath of the global financial crisis, rising inequality and an ever growing population under the poverty line, it is imperative for adopting an economic system concerned with fulfilling basic human needs and creating opportunities for the poor. The Islamic economic system is essentially such a system with a fine blend of community welfare, ethics and morality and investments in the real economy.

Socio-economic justice is essential for lasting peace and harmony in any and all nations

33

34

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

ISLAMIC MODES OF MICROFINANCE

Most of the Islamic modes being used by the Islamic banks are applicable in microfinance. However, only a few most suited products should be selected in view of their suitability for microfinance, especially in the initial period. Accordingly, such instruments can be categorized as under:

Sale Contracts§ Murabaha§ Salam§ Istisna

Quasi Debt Modes§ Islamic Lease (Micro Ijarah)

Participatory Modes§ Mudarabah§ Musharakah

Hybrid Modes§ Diminishing Musharakah§ Murabaha with IstisnaIn this course, we will discuss the Trade Based

Modes of Islamic Microfinance i.e. the sale contracts.

MurabahaAlso known as cost plus sales, it is one of the most widely used instruments for short-term financing where the investor (bank/MFI) undertakes to supply specific goods or commodities, incorporating a mutually agreed contract for resale to the client at a mutually negotiated margin (necessarily the cost to be declared). In case the cost is not referred, the sale is categorized as Musawamah. On the other hand, Bai Muajjal is also a sale contract in which the price is allowed to be recovered at some later date, through installments or in lump sum, though the cost is not required to be disclosed.

Originally, Murabaha is a particular type of sale and not a mode of finance. The Shari'ah Scholars have allowed Murabaha financing on deferred payment basis subject to certain conditions to render the transaction Riba free. In modern banking system the commodity is purchased on the request of client (prior promise to purchase) that is why it is termed as banking Murabaha or Murabaha to the Purchase Orderer.

Bai Muajjal is also a sale contract in

which the price is allowed to be

recovered at some later date

35

CIMM: 403: Islamic Microfinance & Its Products Mechanism

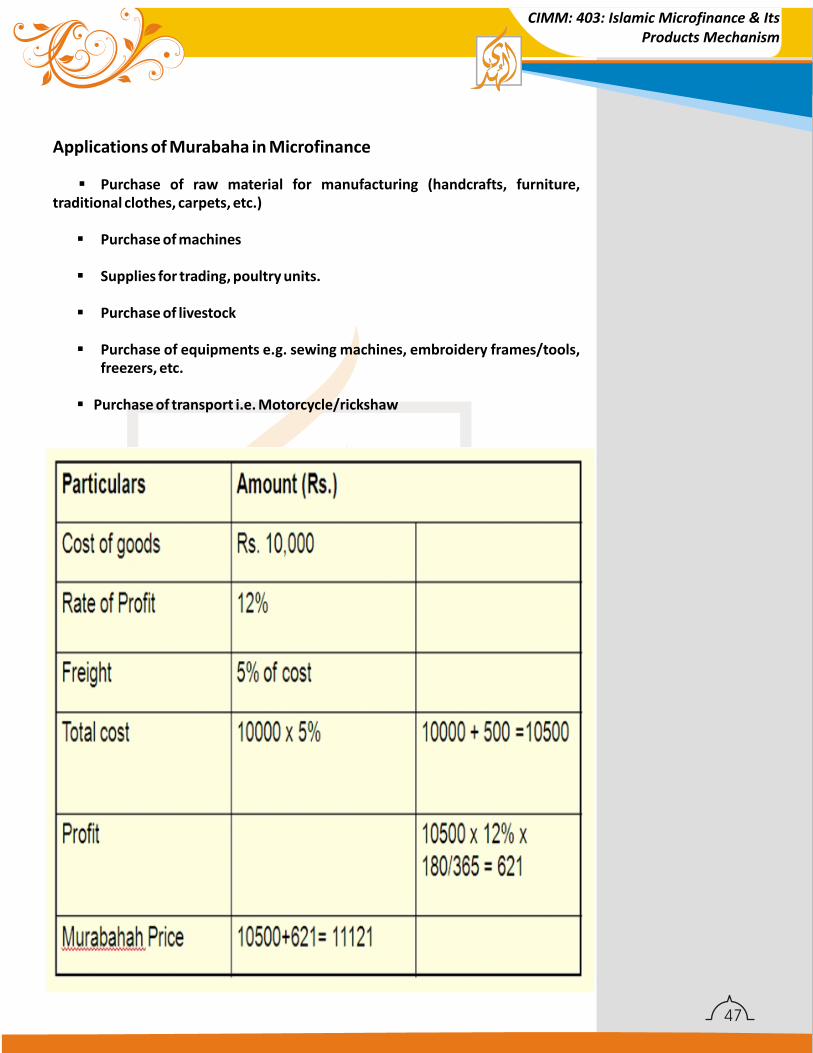

The Murabaha is widely used by the Islamic banks to satisfy various type of financing requirements in diverse sectors e.g., consumer finance for purchase of durables, purchase of machinery, equipment and raw material etc. However, the most common and the most popular application of Murabaha is in financing the short-term trade for which it is eminently suitable. More particularly, Murabaha can be used for short, medium, and long term financing in respect of the following:

§ Sale of raw material§ Sale of inventory§ Sale of equipment§ Sale of agricultural inputs§ Consumer goods financing§ House financing§ Vehicle financing§ Import and export (pre-shipment) financing, etc.

Murabaha is a particular kind of sale where the seller expressly mentions the cost of the sold commodity he has incurred, and sells it to another person by adding some profit or mark-up thereon. The profit in Murabaha can be determined by mutual consent, either in lump sum or through an agreed ratio of profit to be charged over the cost.

All the expenses incurred by the seller in acquiring the commodity like freight, custom duty etc. shall be included in the cost price and the mark-up can be applied on the aggregate cost. However, recurring expenses of the business like salaries of the staff, the rent of the premises etc. cannot be included in the cost of an individual transaction.

Keep In Mind

A greater degree of flexibility exists with respect to beneficiaries of sadaqah. The primary issue with zakah and sadaqah-dependent institutions is the issue of sustainability as they are essentially rooted in voluntarism. Funds mobilized through charity could fluctuate from time to time and may not lend themselves to careful planning and implementation.

CIMM: 403: Islamic Microfinance & Its Products Mechanism

In fact, the profit claimed over the cost takes care of these expenses. Murabaha is valid only where the exact cost of a commodity can be ascertained. If the exact cost cannot be ascertained, the commodity cannot be sold on Murabaha basis. In this case the commodity must be sold on Musawamah (bargaining) basis i.e. without any reference to the cost or to the ratio of profit / mark-up. The price of the commodity in such cases shall be determined in lump sum by mutual consent.

36

37

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

Examples:

§ “A” purchased a pair of shoes for Rs. 100/-. He wants to sell it on Murabaha with 10% mark-up. The exact cost is known. The Murabaha sale is valid.

§ “A” purchased a ready - made suit with a pair of shoes in a single transaction, for a lump sum price of Rs. 500/-. A can sell the suit including shoes on Murabaha. But he cannot sell the shoes separately on Murabaha, because the individual cost of the shoes is unknown. If he wants to sell the shoes separately, he must sell it at a lump sum price without reference to the cost or to the mark-up.

Murabaha as a Mode of Financing

Originally, Murabaha is a particular type of sale and not a mode of financing. The ideal mode of financing according to Shari'ah is Mudarabah or Musharaka which have been discussed in the first chapter. However, in the perspective of the current economic set up, there are certain practical difficulties in using Mudarabah and Musharaka instruments in some areas of financing. Therefore, the contemporary Shari'ah experts have allowed, subject to certain conditions, the use of the Murabaha on deferred payment basis as a mode of financing.

Keep In Mind

Murabaha is valid only where the exact cost of a commodity can be

ascertained. If the exact cost cannot be ascertained, the commodity cannot

be sold on Murabaha basis.

Originally, Murabaha is a

particular type of sale and not a mode

of financing.

Keep In Mind

There are certain practical difficulties in using Mudarabah and Musharaka

instruments in some areas of financing. Therefore, the contemporary

Shari’ah experts have allowed, subject to certain conditions, the use of the

Murabaha on deferred payment basis as a mode of financing.

38

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

But there are two essential points which must be fully understood in this respect:

§ It should never be overlooked that, originally, Murabaha is not a mode of financing. It is only a device to escape from "interest" and not an ideal instrument for carrying out the real economic objectives of Islam. Therefore, this instrument should be used as a transitory step taken in the process of the Islamization of the economy, and its use should be restricted only to those cases where Mudarabah or Musharaka are not practicable.

§ The second important point is that the Murabaha transaction does not come into existence by merely replacing the word of "interest" by the words of "profit" or "mark-up". Actually, Murabaha as a mode of finance has been allowed by the Shari'ah scholars with some conditions. Unless these conditions are fully observed, Murabaha is not permissible. In fact, it is the observance of these conditions which can draw a clear line of distinction between an interest-bearing loan and a transaction of Murabaha. If these conditions are neglected, the transaction becomes invalid according to Shari'ah.

Basic Features of Murabaha Financing

The basic features of Murabaha are as follows:

§ Murabaha is not a loan given on interest. It is the sale of a commodity for a deferred price which includes an agreed profit added to the cost.

§ Being a sale, and not a loan, the Murabaha should fulfill all the conditions necessary for a valid sale, especially those enumerated earlier in this chapter.

§ Murabaha cannot be used as a mode of financing except where the client needs funds to actually purchase some commodities. For example, if he wants funds to purchase cotton as a raw material for his ginning factory, the Bank can sell him the cotton on the basis of Murabaha. But where the funds are required for some other purposes, like paying the price of commodities already purchased by him, or the bills of electricity or other utilities or for paying the salaries of his staff, Murabaha cannot be affected, because Murabaha requires a real sale of some commodities, and not merely advancing a loan.

§ The financier must have owned the commodity before he sells it to his client.

Murabaha should fulfill all the

conditions necessary for a

valid sale

39

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

§ The commodity must come into the possession of the financier, whether physical or constructive, in the sense that the commodity must be in his risk, though for a short period.

§ The best way for Murabaha, according to Shari'ah, is that the financier himself purchases the commodity and keeps it in his own possession, or purchases the commodity through a third person appointed by him as agent, before he sells it to the customer. However, in exceptional cases, where direct purchase from the supplier is not practicable for some reason, it is also allowed that he makes the customer himself his agent to buy the commodity on his behalf. In this case the client first purchases the commodity on behalf of his financier and takes its possession as such. Thereafter, he purchases the commodity from the financier for a deferred price. His possession over the commodity in the first instance is in the capacity of an agent of his financier. In this capacity he is only a trustee, while the ownership vests in the financier and the risk of the commodity is also borne by him as a logical consequence of the ownership. But when the client purchases the commodity from his financier, the ownership, as well as the risk, is transferred to the client.

§ As mentioned earlier, the sale cannot take place unless the commodity comes into the possession of the seller, but the seller can promise to sell even when the commodity is not in his possession. The same rule is applicable to Murabaha.

§ It is also a necessary condition for the validity of Murabaha that the commodity is purchased from a third party. The purchase of the commodity from the client himself on 'buy back' agreement is not allowed in Shari'ah. Thus Murabaha based on 'buy back' agreement is nothing more than an interest based transaction. The above mentioned procedure of the Murabaha financing is a complex transaction where the parties involved have different capacities at different stages.

The sale cannot take place unless the

commodity comes into the possession

of the seller

40

Tip

CIMM: 403: Islamic Microfinance & Its Products Mechanism

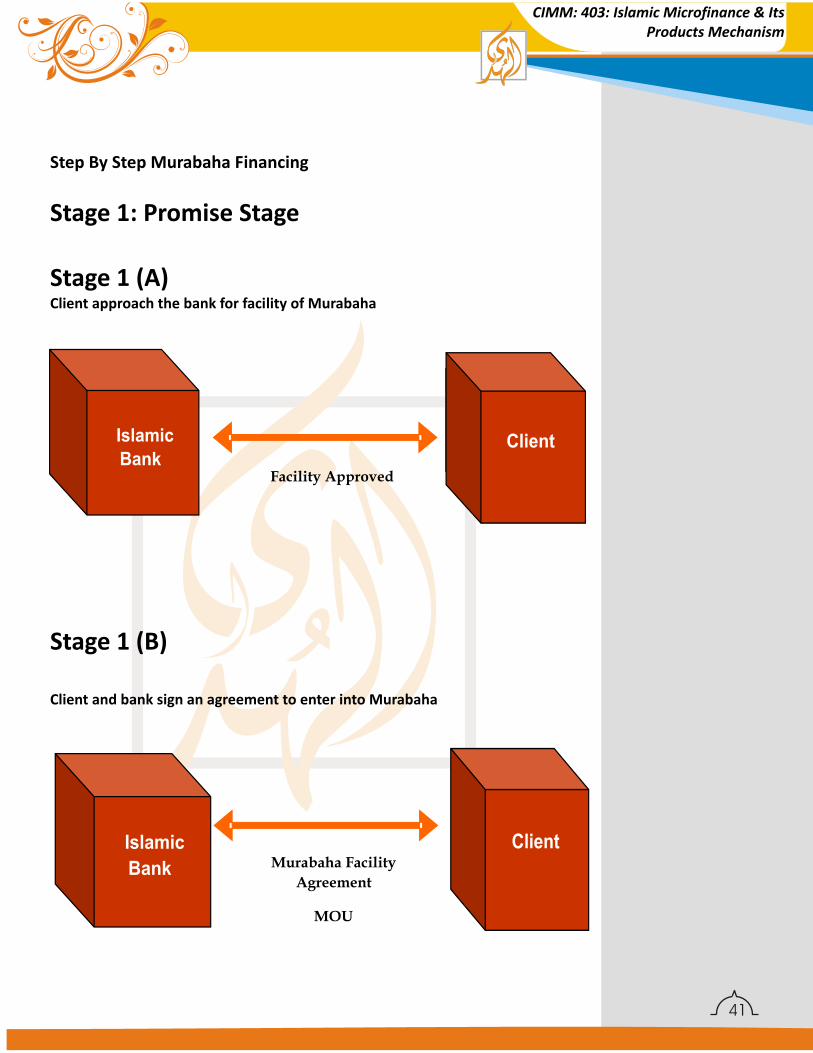

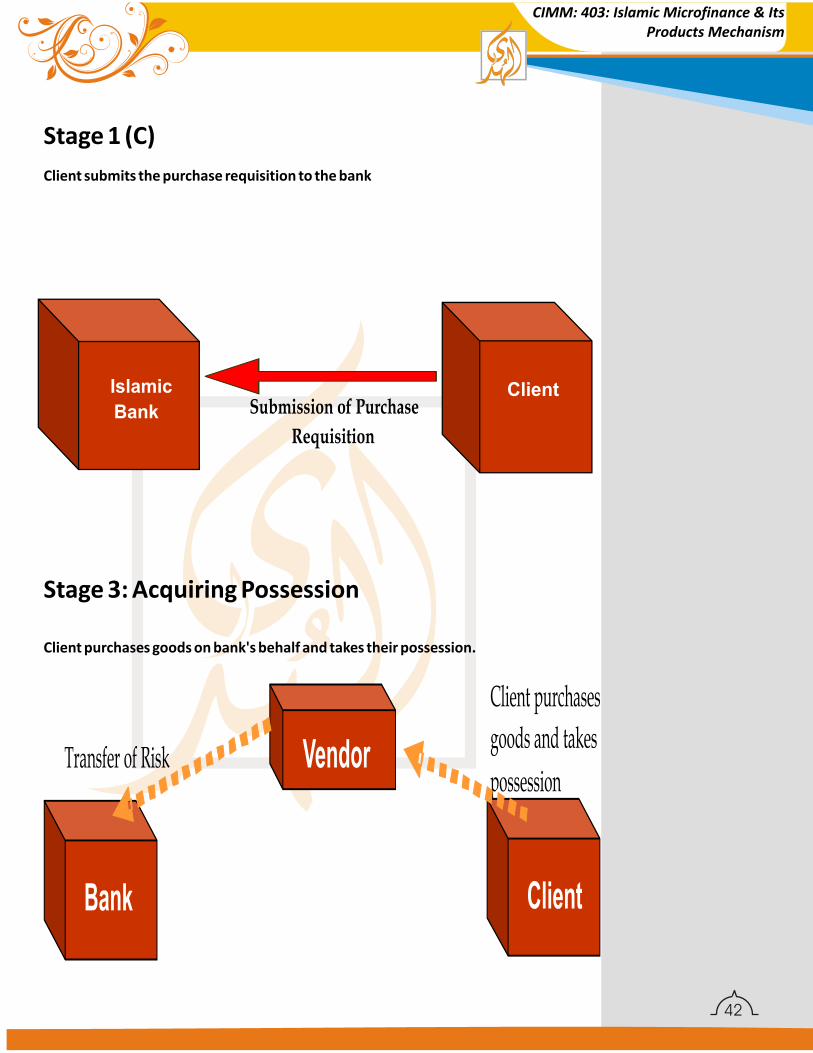

Steps Involved in Murabaha

In the light of the aforementioned principles, a financial institution can use the Murabaha as a mode of finance by adopting the following procedure:

Firstly: The client and the institution sign an over-all agreement whereby the institution promises to sell and the client promises to buy the commodities from time to time on an agreed ratio of profit added to the cost. This agreement may specify the limit up to which the facility may be availed.

Secondly: When a specific commodity is required by the customer, the institution appoints the client as his agent for purchasing the commodity on its behalf, and an agreement of agency is signed by both the parties.

Thirdly: The client purchases the commodity on behalf of the institution and takes its possession as an agent of the institution.

Fourthly: The client informs the institution that he has purchased the commodity on his behalf, and at the same time, makes an offer to purchase it from the institution.