city of aurora, illinois -...

TRANSCRIPT

SOME PAGES REQUIRE ADDITIONAL INFORMATION.

CITY OF AURORA, ILLINOIS

ADMINISTRATOR’S GUIDELINESPublished 7-19-13

(revisions shown on page 3)

! ! ! ! ! ! ! ! !

TABLE OF CONTENTS

TO BE COMPLETED FOR FINAL EDITION

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 2

LIST OF REVISIONS

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 3

Date

THE CITY OF AURORA, IL ASSIST HOMEOWNERSHIP TEAM

City of Aurora, IllinoisCreates the first mortgage program and, if applicable, down payment assistance or second mortgage

programs, sets the rate, term and points, and may market the program

Participating Lenders Take applications, reserve in their own systems, process, underwrite,

approve, fund, close and sell qualified loans to the program. Check with your company on how to reserve a program loan rate in your own system so that you have funds available for closing. Your company may have their own

codes. Lenders are responsible for servicing first mortgages in accordance with Agency requirements until they’re purchased by the Master Servicer.

U S BankMaster Servicer

Provides information on acceptable loan products and delivery and funding, trains, receives all mortgage files, reviews mortgage files, notifies lenders of

mortgage file exceptions, approves mortgage files, purchases first mortgage loans, pools and delivers loans, delivers certificate to Trustee.

eHousingPlus Program Administration

Maintains the program reservation system, websites, and posts guides, forms, training materials, provides training on compliance

issues and system, answers compliance questions for the first mortgage and approves compliance file.

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 4

PROGRAM PRODUCTS

All applicants in this program may receive a first mortgage loan and down payment assistance as a percentage of the full Note amount. Descriptions of the products follow:

FIRST MORTGAGEThe current program interest rate is shown on the Issuer’s web page in the system at www.ehousingplus.com. PLEASE NOTE THAT RATES ARE SUBJECT TO CHANGE AT ANY TIME. With respect to reserved loans, the rate and assistance will not change as long as loans are delivered according to the timetable included in this Guide.

Borrowers qualifying for the first mortgage receive a grant for down payment/closing cost assistance.

DOWN PAYMENT ASSISTANCE GRANTThe Down Payment Assistance Grant is available ONLY with the Assist Homeownership first mortgage loan. Assistance amount is subject to change at any time. Check the eHousingPlus system. Currently, the Assistance is 3.00%.

The Assistance is calculated on the Note amount. The Assistance may be used for down payment or closing costs and prepaids. While there is no cash back in this program, the borrower may be reimbursed for any overpayment of escrow. Because the Assistance is a fixed percentage of the original principal amount of the mortgage loan, any remaining Assistance must be applied as a principal reduction. Assistance is in the form of a non-repayable grant. It is not repayable under any circumstances with the exception of fraud or similar circumstances. When you reserve the first mortgage, the Assistance is automatically reserved. There is no additional reservation necessary. When you close the loan there are not second mortgages, second notes, deed restrictions or liens.

The Assistance will be funded by the lender at closing. Lenders will be reimbursed by US Bank at loan purchase.

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 5

PROGRAM REQUIREMENTS

• Eligible buyers and anyone secondarily liable on the Note must be first-time buyers and must provide the past three years tax transcripts.

• Non-permanent residents follow applicable Agency (FHA, VA, etc) guidelines. • Buyers must live in the property they purchase as their principal residence. • All applicants must be considered irrespective of age, race, color, religion, national origin, sex,

marital status, military status or physical handicap. • Buyers must occupy the property purchased within 60 days of closing. • The past three years tax transcripts are NOT required for Targeted Area buyers or those utilizing

the Veteran’s Exception.

Veterans Exception For the Veterans Exception, “veteran” is defined as "a person who served in the active military, naval, or air service, and who was discharged or released therefrom under conditions other than dishonorable." The Mortgagor Affidavit has a checkbox that states: “Mortgagor(Comortgagor) meets the requirements to qualify as a “veteran” as defined in 38 U.S.C. Section 101 and has not previously obtained a loan financed by single family mortgage revenue bonds utilizing the veteran exception to the first-time homebuyer requirement set forth in Section 416 of the Tax Relief and Health Care Act of 2006. Attached hereto are true and correct copies of my discharge or release papers, which demonstrate that such discharge or release was other than dishonorable.

Homebuyer Education The Mortgagor shall have received appropriate homebuyer education pursuant to a homebuyer education program approved by the Lender. Also, approved is an online course using Neighborworks curriculum and provided by eHomeAmerica. Go to http://www.ehomeamerica.org to find the local provider.

Minimum Credit Score A minimum credit score of 640 is required. (the mid score must be 640 or above).

Maximum Debt to Income Ratio The maximum Debt to Income Ratio (DTI) is 45%.

Income LimitsInclude income of borrower(s) and who is secondarily liable on the loan. Program income is not averaged. It is annualized. That’s different from income used for credit underwriting. More detailed guidelines for calculating program income are in the Underwriter’s Program Income Calculation Guide included in this Guide

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 6

Household Income LimitsMUNICIPALITY NONTARGETED AREANONTARGETED AREA TARGETED AREATARGETED AREA

Familyof 1/2 ($)

Family of 3or More ($)

Familyof 1/2 ($)

Family of 3or More ($)

City of Aurora, Kane, DuPage, Will and Kendall Counties, Illinois

Kane, DuPage and Will Counties, Illinois 87,015 100,068 90,480 105,560Kendall County, Illinois 86,500 99,475 103,800 121,100

Village of Bartonville, Peoria County, Illinois 69,400 79,810 83,280 97,160

City of Belleville, St. Clair County, Illinois 69,400 79,810 83,280 97,160

City of Belvidere, Boone County, Illinois 69,400 79,810 83,280 97,160The County of Boone, Illinois 69,400 79,810 83,280 97,160Village of Bridgeview, Cook County,

Illinois 87,015 100,068 90,480 105,560City of Champaign, Champaign County,

Illinois 69,400 79,810 83,280 97,160The County of Champaign, Illinois 69,400 79,810 83,280 97,160City of Charleston, Coles County, Illinois 69,400 79,810 83,280 97,160The County of Coles, Illinois 69,400 79,810 83,280 97,160City of Collinsville, Madison and St.

Clair Counties, Illinois 69,400 79,810 83,280 97,160The County of Cook, Illinois 87,015 100,068 90,480 105,560City of Crest Hill, Will County, Illinois 87,015 100,068 90,480 105,560Village of Creve Coeur,

Tazewell County, Illinois 69,400 79,810 83,280 97,160City of Decatur, Macon County, Illinois 69,400 79,810 83,280 97,160The County of DeKalb, Illinois 87,255 100,344 89,040 103,880City of East Moline, Rock Island County,

Illinois 69,400 79,810 83,280 97,160City of East Peoria, Tazewell County,

Illinois 69,400 79,810 83,280 97,160City of Edwardsville, Madison County,

Illinois 69,400 79,810 83,280 97,160Village of Godfrey, Madison County,

Illinois 69,400 79,810 83,280 97,160City of Joliet, Will and Kendall Counties,

IllinoisWill County, Illinois 87,015 100,068 90,480 105,560Kendall County, Illinois 86,500 99,475 103,800 121,100

Village of Justice, Cook County, Illinois 87,015 100,068 90,480 105,560The County of Kankakee, Illinois 69,400 79,810 83,280 97,160The County of Kendall, Illinois 86,500 99,475 103,800 121,100The County of Lake, Illinois 87,015 100,068 90,480 105,560

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 7

MUNICIPALITY NONTARGETED AREANONTARGETED AREA TARGETED AREATARGETED AREA

Familyof 1/2 ($)

Family of 3or More ($)

Familyof 1/2 ($)

Family of 3or More ($)

City of LaSalle, LaSalle County, Illinois 69,400 79,810 83,280 97,160City of Lockport, Will County, Illinois 87,015 100,068 90,480 105,560City of Loves Park, Winnebago County,

Illinois 69,400 79,810 83,280 97,160Village of Machesney Park, Winnebago

County, Illinois 69,400 79,810 83,280 97,160The County of Macon, Illinois 69,400 79,810 83,280 97,160The County of Madison, Illinois 69,400 79,810 83,280 97,160City of Marquette Heights, Tazewell

County, Illinois 69,400 79,810 83,280 97,160City of Mattoon, Coles County, Illinois 69,400 79,810 83,280 97,160The County of McLean, Illinois 75,500 86,825 90,600 105,700City of Mendota, LaSalle County, Illinois 69,400 79,810 83,280 97,160Village of Minooka, Kendall, Grundy

and Will Counties, IllinoisKendall County, Illinois 86,500 99,475 103,800 121,100Grundy County, Illinois 86,835 99,861 91,560 106,820Will County, Illinois 87,015 100,068 90,480 105,560

Village of Montgomery, Kane and Kendall Counties, Illinois

Kane County, Illinois 87,015 100,068 90,480 105,560Kendall County, Illinois 86,500 99,475 103,800 121,100

City of Naperville, DuPage and Will Counties, Illinois 87,015 100,068 90,480 105,560

The County of Ogle, Illinois 69,400 79,810 83,280 97,160City of Pekin, Tazewell and Peoria

Counties, Illinois 69,400 79,810 83,280 97,160City of Peoria, Peoria County, Illinois 69,400 79,810 83,280 97,160The County of Peoria, Illinois 69,400 79,810 83,280 97,160Village of Peoria Heights,

Peoria County, Illinois 69,400 79,810 83,280 97,160City of Peru, LaSalle County, Illinois 69,400 79,810 83,280 97,160Village of Plainfield, Kendall and Will

Counties, IllinoisKendall County, Illinois 86,500 99,475 103,800 121,100Will County, Illinois 87,015 100,068 90,480 105,560

City of Princeton, Bureau County, Illinois 69,400 79,810 83,280 97,160

City of Rochelle, Ogle County, Illinois 69,400 79,810 83,280 97,160The County of Rock Island, Illinois 69,400 79,810 83,280 97,160City of Rockford, Winnebago County,

Illinois 69,400 79,810 83,280 97,160

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 8

MUNICIPALITY NONTARGETED AREANONTARGETED AREA TARGETED AREATARGETED AREA

Familyof 1/2 ($)

Family of 3or More ($)

Familyof 1/2 ($)

Family of 3or More ($)

Village of Rockton, Winnebago County, Illinois 69,400 79,810 83,280 97,160

Village of Romeoville, Will County, Illinois 87,015 100,068 90,480 105,560

Village of Schaumburg, Cook and DuPage Counties, Illinois 87,015 100,068 90,480 105,560

Village of Shorewood, Will County, Illinois 87,015 100,068 90,480 105,560

City of South Beloit, Winnebago County, Illinois 69,400 79,810 83,280 97,160

City of Springfield, Sangamon County, Illinois 69,400 79,810 83,280 97,160

The County of Tazewell, Illinois 69,400 79,810 83,280 97,160City of Urbana, Champaign County,

Illinois 69,400 79,810 83,280 97,160City of Washington, Tazewell County,

Illinois 69,400 79,810 83,280 97,160The County of Winnebago, Illinois 69,400 79,810 83,280 97,160City of Wood River, Madison County,

Illinois 69,400 79,810 83,280 97,160United City of Yorkville, Kendall

County, Illinois 86,500 99,475 103,800 121,100

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 9

PROGRAM AREA(LENDERS ARE RESPONSIBLE FOR DETERMING THAT PROPERTIES ARE LOCATED IN THE PROGRAM AREA.)

City of Aurora, Kane, DuPage, Will and Kendall Counties, IllinoisVillage of Bartonville, Peoria County, IllinoisCity of Belleville, St. Clair County, IllinoisCity of Belvidere, Boone County, IllinoisVillage of Bridgeview, Cook County, IllinoisCity of Champaign, Champaign County, IllinoisCity of Charleston, Coles County, IllinoisCity of Collinsville, Madison and St. Clair Counties, IllinoisCity of Crest Hill, Will County, IllinoisVillage of Creve Coeur, Tazewell County, IllinoisCity of Decatur, Macon County, IllinoisCity of East Moline, Rock Island County, IllinoisCity of East Peoria, Tazewell County, IllinoisCity of Edwardsville, Madison County, IllinoisVillage of Godfrey, Madison County, IllinoisCity of Joliet, Will County, IllinoisVillage of Justice, Cook County, IllinoisCity of LaSalle, LaSalle County, IllinoisCity of Lockport, Will County, IllinoisCity of Loves Park, Winnebago County, IllinoisVillage of Machesney Park, Winnebago County, IllinoisCity of Marquette Heights, Tazewell County, IllinoisCity of Mattoon, Coles County, IllinoisCity of Mendota, LaSalle County, IllinoisVillage of Minooka, Grundy, Kendall and Will Counties, IllinoisVillage of Montgomery, Kane and Kendall Counties, IllinoisCity of Naperville, DuPage and Will Counties, IllinoisCity of Pekin, Tazewell and Peoria Counties, IllinoisCity of Peoria, Peoria County, IllinoisVillage of Peoria Heights, Peoria County, IllinoisCity of Peru, LaSalle County, IllinoisVillage of Plainfield, Kendall and Will Counties, IllinoisCity of Princeton, Bureau County, IllinoisCity of Rochelle, Ogle County, IllinoisCity of Rockford, Winnebago County, IllinoisVillage of Rockton, Winnebago County, IllinoisVillage of Romeoville, Will County, IllinoisVillage of Schaumburg, Cook and DuPage Counties, IllinoisVillage of Shorewood, Will County, IllinoisCity of South Beloit, Winnebago County, IllinoisCity of Springfield, Sangamon County, IllinoisCity of Urbana, Champaign County, IllinoisCity of Washington, Tazewell County, IllinoisCity of Wood River, Madison County, IllinoisUnited City of Yorkville, Kendall County, IllinoisThe County of Boone, Illinois

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 10

The County of Champaign, IllinoisThe County of Coles, IllinoisThe County of Cook, IllinoisThe County of DeKalb, IllinoisThe County of Kankakee, IllinoisThe County of Kendall, IllinoisThe County of Lake, IllinoisThe County of Macon, IllinoisThe County of Madison, IllinoisThe County of McLean, IllinoisThe County of Ogle, IllinoisThe County of Peoria, IllinoisThe County of Rock Island, IllinoisThe County of Tazewell, IllinoisThe County of Winnebago, Illinois

About the Property• Properties purchased in the program must be residential units. • New or existing, one to four unit, detached or attached, condos, townhomes. Existing two-to-four

unit residences must be at least 5 years old. New construction can be no more than a one-unit residence unless in a Targeted Area where two units are permitted. No more than 13.3% of the aggregate amount of Mortgage Loans may be made for two-to-four family residences. Mortgagor/MCC Recipient must reside in one unit of a multi-unit property as their principal residence

• Manufactured homes must meet servicer/insurer/guarantor requirements. See US Bank Bulletin on their AllRegs site.

• Mobile, recreational, seasonal or other types of vacation or non-permanent homes are not permitted.

• Land may not exceed the size required to maintain basic livability. • No more than 15% of the square footage of the home being purchased may be used in connection

with a trade or business including Child Care services (other than incidental rental from eligible two-to-four unit residences).

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 11

Purchase Price Limits (Acquisition Limits)In determining the Purchase Price, please include everything paid by the buyer or on the buyer’s behalf. Current limits are listed below and revised amounts as may be effective from time to time:

MUNICIPALITY NONTARGETED AREA TARGETED AREA

City of Aurora, Kane, DuPage, Will and Kendall Counties, Illinois 349,024 426,585

Village of Bartonville, Peoria County, IllinoisVillage of Bartonville, Peoria County, Illinois 258,690 316,177City of Belleville, St. Clair County, IllinoisCity of Belleville, St. Clair County, Illinois 258,690 316,177City of Belvidere, Boone County, IllinoisCity of Belvidere, Boone County, Illinois 323,780 395,731The County of Boone, IllinoisThe County of Boone, Illinois 323,780 395,731Village of Bridgeview, Cook County, IllinoisVillage of Bridgeview, Cook County, Illinois 349,024 426,585City of Champaign, Champaign County,

IllinoisCity of Champaign, Champaign County,

Illinois 258,690 316,177The County of Champaign, IllinoisThe County of Champaign, Illinois 258,690 316,177City of Charleston, Coles County, IllinoisCity of Charleston, Coles County, Illinois 258,690 316,177The County of Coles, IllinoisThe County of Coles, Illinois 258,690 316,177City of Collinsville, Madison and St. Clair

Counties, IllinoisCity of Collinsville, Madison and St. Clair

Counties, Illinois 258,690 316,177The County of Cook, IllinoisThe County of Cook, Illinois 349,024 426,585City of Crest Hill, Will County, IllinoisCity of Crest Hill, Will County, Illinois 349,024 426,585Village of Creve Coeur,

Tazewell County, IllinoisVillage of Creve Coeur,

Tazewell County, Illinois 258,690 316,177City of Decatur, Macon County, IllinoisCity of Decatur, Macon County, Illinois 258,690 316,177The County of DeKalb, IllinoisThe County of DeKalb, Illinois 349,024 426,585City of East Moline, Rock Island County,

IllinoisCity of East Moline, Rock Island County,

Illinois 258,690 316,177City of East Peoria, Tazewell County, IllinoisCity of East Peoria, Tazewell County, Illinois 258,690 316,177City of Edwardsville, Madison County, IllinoisCity of Edwardsville, Madison County, Illinois258,690 316,177Village of Godfrey, Madison County, IllinoisVillage of Godfrey, Madison County, Illinois 258,690 316,177City of Joliet, Will and Kendall Counties,

IllinoisCity of Joliet, Will and Kendall Counties,

Illinois 349,024 426,585Village of Justice, Cook County, IllinoisVillage of Justice, Cook County, Illinois 349,024 426,585The County of Kankakee, IllinoisThe County of Kankakee, Illinois 258,690 316,177The County of Kendall, IllinoisThe County of Kendall, Illinois 349,024 426,585The County of Lake, IllinoisThe County of Lake, Illinois 349,024 426,585City of LaSalle, LaSalle County, IllinoisCity of LaSalle, LaSalle County, Illinois 258,690 316,177City of Lockport, Will County, IllinoisCity of Lockport, Will County, Illinois 349,024 426,585City of Loves Park, Winnebago County,

IllinoisCity of Loves Park, Winnebago County,

Illinois 323,780 395,731Village of Machesney Park, Winnebago

County, IllinoisVillage of Machesney Park, Winnebago

County, Illinois 323,780 395,731The County of Macon, IllinoisThe County of Macon, Illinois 258,690 316,177The County of Madison, IllinoisThe County of Madison, Illinois 258,690 316,177

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 12

MUNICIPALITY NONTARGETED AREA TARGETED AREA

City of Marquette Heights, Tazewell County, Illinois

City of Marquette Heights, Tazewell County, Illinois 258,690 316,177

City of Mattoon, Coles County, IllinoisCity of Mattoon, Coles County, Illinois 258,690 316,177The County of McLean, IllinoisThe County of McLean, Illinois 258,690 316,177City of Mendota, LaSalle County, IllinoisCity of Mendota, LaSalle County, Illinois 258,690 316,177Village of Minooka, Will, Kendall and Grundy

Counties, IllinoisVillage of Minooka, Will, Kendall and Grundy

Counties, Illinois 349,024 426,585Village of Montgomery, Kane and Kendall

Counties, IllinoisVillage of Montgomery, Kane and Kendall

Counties, Illinois 349,024 426,585City of Naperville, DuPage and Will Counties,

IllinoisCity of Naperville, DuPage and Will Counties,

Illinois 349,024 426,585The County of Ogle, IllinoisThe County of Ogle, Illinois 258,690 316,177City of Pekin, Tazewell and Peoria Counties,

IllinoisCity of Pekin, Tazewell and Peoria Counties,

Illinois 258,690 316,177The County of Peoria, IllinoisThe County of Peoria, Illinois 258,690 316,177City of Peoria, Peoria County, IllinoisCity of Peoria, Peoria County, Illinois 258,690 316,177Village of Peoria Heights,

Peoria County, IllinoisVillage of Peoria Heights,

Peoria County, Illinois 258,690 316,177City of Peru, LaSalle County, IllinoisCity of Peru, LaSalle County, Illinois 258,690 316,177Village of Plainfield, Kendall and Will

Counties, IllinoisVillage of Plainfield, Kendall and Will

Counties, Illinois 349,024 426,585City of Princeton, Bureau County, IllinoisCity of Princeton, Bureau County, Illinois 258,690 316,177City of Rochelle, Ogle County, IllinoisCity of Rochelle, Ogle County, Illinois 258,690 316,177The County of Rock Island, IllinoisThe County of Rock Island, Illinois 258,690 316,177City of Rockford, Winnebago County, IllinoisCity of Rockford, Winnebago County, Illinois 323,780 395,731Village of Rockton, Winnebago County,

IllinoisVillage of Rockton, Winnebago County,

Illinois 323,780 395,731Village of Romeoville, Will County, IllinoisVillage of Romeoville, Will County, Illinois 349,024 426,585Village of Schaumburg, Cook and DuPage

Counties, IllinoisVillage of Schaumburg, Cook and DuPage

Counties, Illinois 349,024 426,585Village of Shorewood, Will County, IllinoisVillage of Shorewood, Will County, Illinois 349,024 426,585City of South Beloit, Winnebago County,

IllinoisCity of South Beloit, Winnebago County,

Illinois 323,780 395,731City of Springfield, Sangamon County, IllinoisCity of Springfield, Sangamon County, Illinois 258,690 316,177The County of Tazewell, IllinoisThe County of Tazewell, Illinois 258,690 316,177City of Urbana, Champaign County, IllinoisCity of Urbana, Champaign County, Illinois 258,690 316,177City of Washington, Tazewell County, IllinoisCity of Washington, Tazewell County, Illinois 258,690 316,177The County of Winnebago, IllinoisThe County of Winnebago, Illinois 323,780 395,731City of Wood River, Madison County, IllinoisCity of Wood River, Madison County, Illinois 258,690 316,177United City of Yorkville, Kendall County,

IllinoisUnited City of Yorkville, Kendall County,

Illinois 349,024 426,585

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 13

TARGETED AREAS Targeted Areas are economically distressed areas as determined from the most recent census data or designated by the state. LENDERS ARE RESPONSIBLE FOR DETERMINING THAT PROPERTIES ARE LOCATED IN TARGETED AREAS.)

The following census tracts located within the Program Area have been designated as Targeted Areas:

City of Aurora, Kane, DuPage, Will and Kendall Counties, Illinois8535*, 8536*, 8537.00

Village of Bartonville, Peoria County, IllinoisNoneCity of Belleville, St. Clair County, Illinois5017*

City of Belvidere, Boone County, IllinoisNone

The County of Boone, IllinoisNone

Village of Bridgeview, Cook County, IllinoisNone

City of Champaign, Champaign County, Illinois0001.00, 0003.00, 0007.00, 0053.00

The County of Champaign, Illinois0001.00, 0003.00, 0007.00, 0052.00, 0053.00, 0054(BG1)*, 0055(BG 5, 6, 7)*, 0060.00City of Charleston, Coles County, IllinoisNone

The County of Coles, IllinoisNone

City of Collinsville, Madison and St. Clair Counties, IllinoisNone

The County of Cook, Illinois

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 14

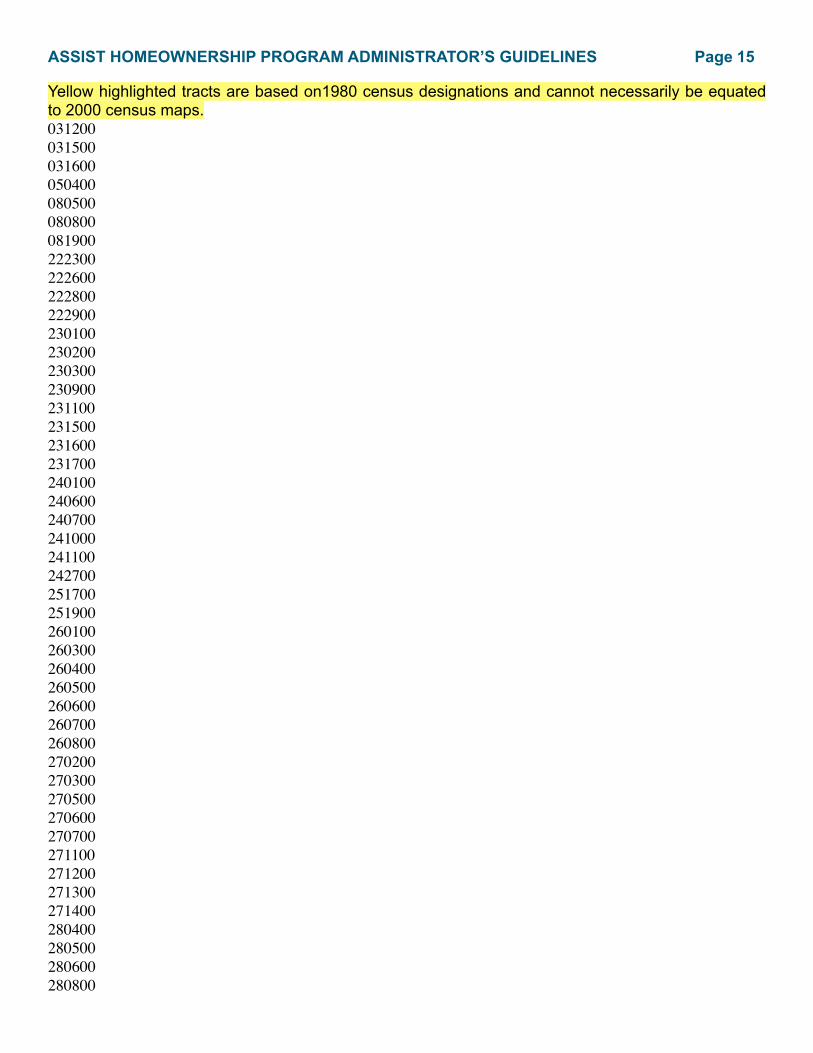

Yellow highlighted tracts are based on1980 census designations and cannot necessarily be equated to 2000 census maps.031200031500031600050400080500080800081900222300222600222800222900230100230200230300230900231100231500231600231700240100240600240700241000241100242700251700251900260100260300260400260500260600260700260800270200270300270500270600270700271100271200271300271400280400280500280600280800

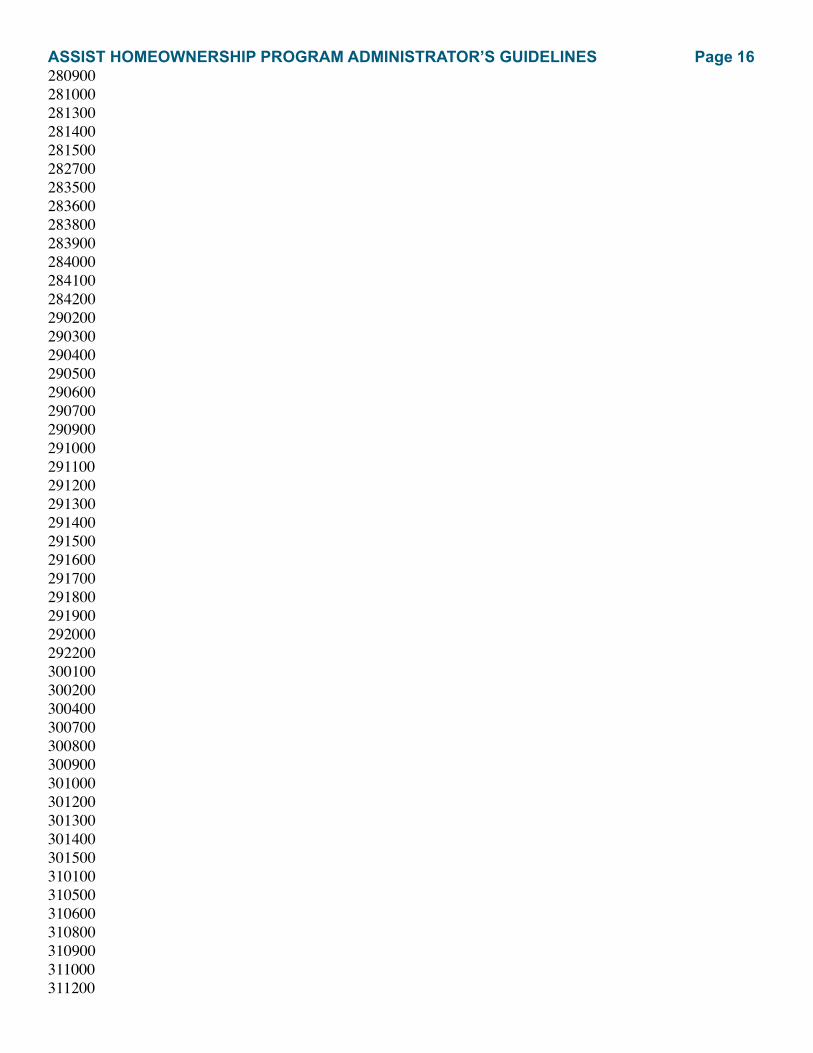

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 15

280900281000281300281400281500282700283500283600283800283900284000284100284200290200290300290400290500290600290700290900291000291100291200291300291400291500291600291700291800291900292000292200300100300200300400300700300800300900301000301200301300301400301500310100310500310600310800310900311000311200

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 16

320400330300340400340600350200350400350600351100351400351500360100360200360300360400370100370200370400380100380200380500380600380700380800381300381400381500381600381700381800382000390300390400400100400200400300400500400600400700400800410400420400420500420600420700420800420900421100430300430500430700

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 17

431300440100440800460100460200460600460700460800460900461000490200491400500200540100560200610200610300610400610500610600611100611200611300611400611700611800611900612000612100630100670200670300670600670800670900671000671100671200671500671700680100680200680300680400680500680600680700680900681000681100

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 18

6812006813006901006902006903006907007101007102007109008215008268008269018269028290008291000101*0317*0311*0512*0514*0515*0607*0611*0623*0625*0626*0703*0704*0705*0708*0709*0710*0711*0718*0719*0720*0806*1401*1402*2006*2201*2202*2203*2204*2205*2210*2211*2209*2212*2213*

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 19

2215*2214*2216*2218*2219*2220*2221*2222*2229*2304*2224*2227*2306*2307*2308*2402*2312*2404*2409*2403*2412*2419*2421*2415*2416*2417*2420*2422*2423*2424*2425*2428*2429*2430*2511*2431*2432*2436*2512*2514*2515*2516*2519*2517*2520*2521*2522*2609*2807*2817*

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 20

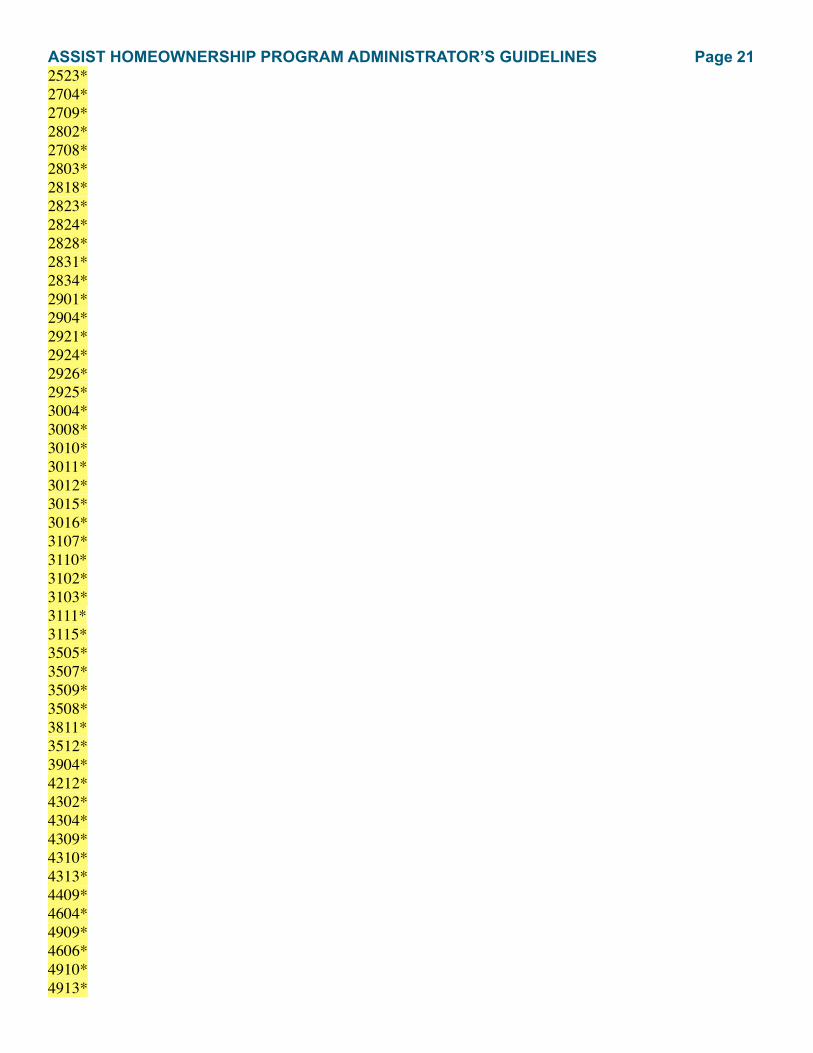

2523*2704*2709*2802*2708*2803*2818*2823*2824*2828*2831*2834*2901*2904*2921*2924*2926*2925*3004*3008*3010*3011*3012*3015*3016*3107*3110*3102*3103*3111*3115*3505*3507*3509*3508*3811*3512*3904*4212*4302*4304*4309*4310*4313*4409*4604*4909*4606*4910*4913*

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 21

4914*5105*5301*5302*6003*6009*6101*6103*6109*6110*6701*6121*6704*6705*6706*6709*6713*6714*6715*6717*6718*6719*6720*6808*6814*6909*7106*7107*6911*7109*7110*8092*8173*AND PARTS OF:8237*8175*8243*8271*8272*0301*0306*0307*0313*0314*0501*0601*0706*0803*0818*2004*

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 22

2101*2513*2801*2820*2821*2822*2835*3005*3113*3114*4201*4301*4312*4404*4502*4601*4602*4603*4605*4701*4909*5305*6004*6114*6914*7101*7102*7103*7105*7108*7111*7305*7306*7501*7502*7506*8141*8260*

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 23

TO BE UPDATED PENDING MORE INFORMATION

City of Crest Hill, Will County, IllinoisNone

Village of Creve Coeur, Tazewell County, IllinoisNone

City of Decatur, Macon County, Illinois0001.00, 0002*, 0003.00, 0006.00, 0007.00, 0008.00, 0009.00, 0010.00

The County of DeKalb, Illinois0010.00, 0011.00, 0012.00

City of East Moline, Rock Island County, Illinois0206.00, 0207(BG1)*

City of East Peoria, Tazewell County, Illinois0202*

City of Edwardsville, Madison County, Illinois4030.02(BG1)*

Village of Godfrey, Madison County, IllinoisNone

City of Joliet, Will and Kendall Counties, Illinois8812(BG1)*, 8813*, 8819.00, 8820.00, 8821*, 8824*, 8825*

Village of Justice, Cook County, IllinoisNone

The County of Kankakee, Illinois0110.00, 0116.00, 0117.00(BG4)*, 0123.00

The County of Kendall, IllinoisNone

The County of Lake, Illinois8613*, 8622*, 8623.00, 8624*, 8626.05, 8627.00, 8629(BG1)*, 8629.02

City of LaSalle, LaSalle County, IllinoisNone

City of Lockport, Will County, IllinoisNone

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 24

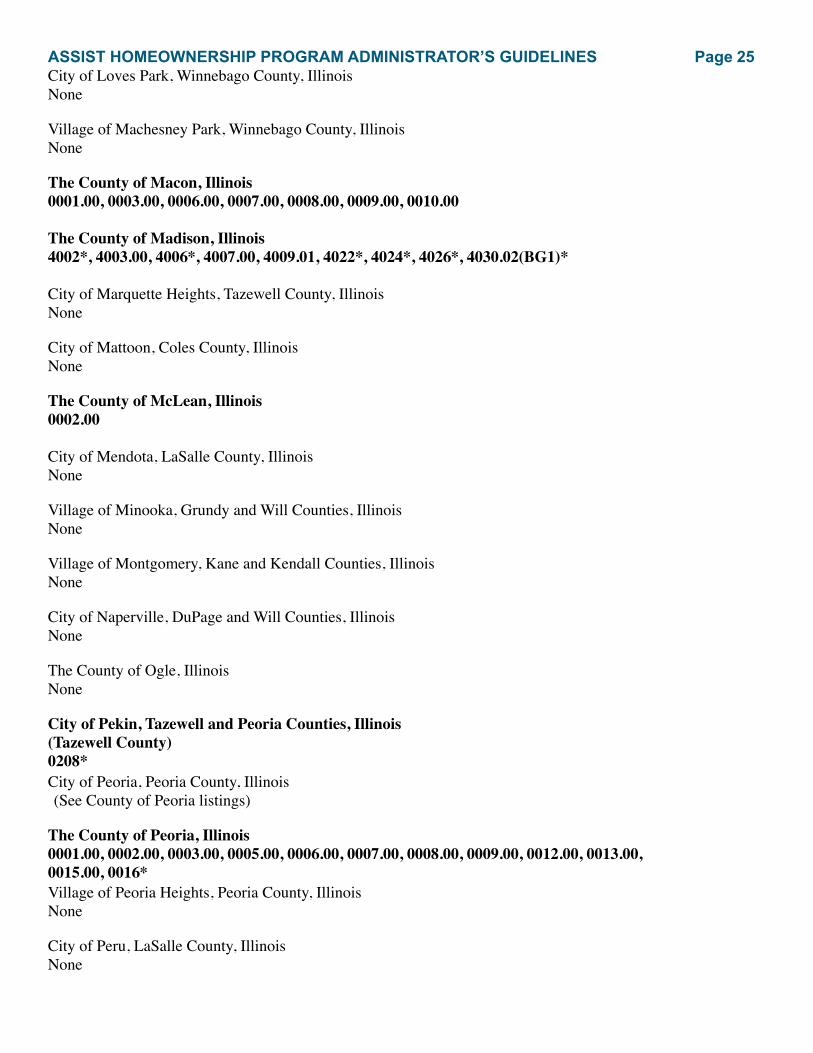

City of Loves Park, Winnebago County, IllinoisNone

Village of Machesney Park, Winnebago County, IllinoisNone

The County of Macon, Illinois0001.00, 0003.00, 0006.00, 0007.00, 0008.00, 0009.00, 0010.00

The County of Madison, Illinois4002*, 4003.00, 4006*, 4007.00, 4009.01, 4022*, 4024*, 4026*, 4030.02(BG1)*

City of Marquette Heights, Tazewell County, IllinoisNone

City of Mattoon, Coles County, IllinoisNone

The County of McLean, Illinois0002.00

City of Mendota, LaSalle County, IllinoisNone

Village of Minooka, Grundy and Will Counties, IllinoisNone

Village of Montgomery, Kane and Kendall Counties, IllinoisNone

City of Naperville, DuPage and Will Counties, IllinoisNone

The County of Ogle, IllinoisNone

City of Pekin, Tazewell and Peoria Counties, Illinois(Tazewell County)0208*City of Peoria, Peoria County, Illinois (See County of Peoria listings)

The County of Peoria, Illinois0001.00, 0002.00, 0003.00, 0005.00, 0006.00, 0007.00, 0008.00, 0009.00, 0012.00, 0013.00, 0015.00, 0016*Village of Peoria Heights, Peoria County, IllinoisNone

City of Peru, LaSalle County, IllinoisNone

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 25

Village of Plainfield, Kendall and Will Counties, IllinoisNone

City of Princeton, Bureau County, IllinoisNone

City of Rochelle, Ogle County, IllinoisNone

The County of Rock Island, Illinois0206.00, 0207 (BG1)*, 0223.00, 0226.00, 0233*, 0235*, 0236.00

City of Rockford, Winnebago County, Illinois0010.00, 0011.00, 0013.00, 0021.00, 0024.00, 0025.00, 0026.00, 0027*, 0028.00, 0031(BG4, 5)*

Village of Rockton, Winnebago County, IllinoisNone

Village of Romeoville, Will County, IllinoisNone

Village of Schaumburg, Cook and DuPage Counties, IllinoisNone

Village of Shorewood, Will County, IllinoisNone

City of South Beloit, Winnebago County, IllinoisNone

City of Springfield, Sangamon County, Illinois0002(BG1)*, 0007(BG3)*, 0008.00, 0009.00, 0014.00, 0015.00, 0016.00, 0017.00, 0018(BG1, 2, 3, 4, 6, 7)*, 0024.00, 0026 (BG1,4)*, 0028.02The County of Tazewell, Illinois0208*

City of Urbana, Champaign County, Illinois (Urbana)0052.00, 0053.00, 0054(BG1)*, 0055(BG5, 6, 7)*, 0060.00

City of Washington, Tazewell County, IllinoisNone

The County of Winnebago, Illinois0010.00, 0011.00, 0013.00, 0021.00, 0024.00, 0025.00, 0026.00, 0027*, 0028.00, 0031(BG4, 5)*

City of Wood River, Madison County, IllinoisNone

United City of Yorkville, Kendall County, IllinoisNone

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 26

FINANCING FACTSIt’s expected that lenders have reviewed some preliminary documentation and believe that applicants will also qualify for credit. Excessive cancellations will be reviewed to assure that allocation is not being utilized inappropriately.

Appraisal The Appraisal must indicate that the home has at least a 30 year remaining useful life.

Cash Back Cash Back to the borrower is not permitted. However, borrowers are permitted a reimbursement of overage of prepaids and earnest money deposit to the extent any minimum contribution has been satisfied and permitted by Agency guidelines. Document such transactions.

Construction to permNot permitted in the program.

CosignersFor credit underwriting: Permitted for FHA loans under very specific conditions. Follow FHA guidelines for credit purposes only. Treat cosigner income as directed by FHA. For program purposes: Cosigners are allowable in an FHA transaction when meeting the following conditions (1) a cosigner cannot have any ownership interest in the property (they cannot be on the Mortgage/Deed) and (2) the cosigner cannot reside in the property being purchased. A cosigner’s income is not considered for program purposes, tax returns are not required and cosigners do not sign any program documents.

Manufactured Housing See U S BANK bulletin on their web page .

Minimum Loan Amount There is no minimum loan amount in this program.

Prepayments The first mortgage may be prepaid at any time without penalty.

Refinances of existing mortgage loansThis program is intended for new mortgage financing. Refinances of existing mortgage loans are not permitted. However, temporary, construction or bridge financing with a term of 2 years or less may be taken out with a program loan. Remaining reservesNot established by the program. If any, these are determined by the type of financing used (i.e. FHA, VA.).

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 27

PROGRAM PROCESS SUMMARY

TRAIN Lender training is provided by the Administrator and Servicer -- See TRAINING tab located on the ?? ADD LINK eHP University program training is offered 24/7, upon completion certificate prints and directions provided for username and password credentials. For underwriting, delivery and funding information --US Bank also offers ongoing training.

LENDER PORTAL USER CREDENTIALSFollowing eHP University training, Lenders apply for User Credentials on the ehousingplus website with instructions received in an email the Wednesday following training.

QUALIFY Lenders qualify applicants for the program. Lenders may pre-qualify and complete application process in their own internal systems using their internal codes. For the program, buyers must present an executed sales agreement before being entered into the program reservation system.

RESERVE To reserve funds in program’s online system click here to reserve ?? New construction, short sales or any other known delayed loans must be reserved no sooner than 15 days prior to closing.

TIMELINE REMINDERLenders process the loan normally and consider program requirements Remember 15 day lock only extended with Underwriter Certification or cancels.

UNDERWRITE AND CERTIFY Lenders underwrite & are responsible for credit decisions of the loans in the program. Servicer does not re-underwrite loans. Following credit approval, Underwriter completes the online Underwriter Certification form. THIS STEP MUST BE COMPLETED WIHTIN 15 DAYS OF LOAN RESERVATION. The Underwriter Certification is available within the eHousingPlus Lender Portal.

CLOSE AND VERIFY It’s important to provide accurate closing instructions to closing agents. All program docs must be returned to you. At closing have borrower and seller execute (and have notarized) the Affidavits/ Certification form. Other forms may be required if using down payment assistance. This form may be found within the eHousingPlus Lender Portal in the area titled LOAN FORMS.

SHIP / SUBMITUse the Compliance Checklist to assemble the compliance file. Forms may be found within the secure eHousingPlus Lender Portal in the area titled LOAN FORMS. THE COMPLIANCE FILE IS SENT DIRECTLY TO EHOUSINGPLUS. The mortgage file with credit package is submitted to U S Bank.

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 28

PROGRAM TIMELINEBuyers MUST HAVE A FULLY- EXECUTED SALES CONTRACT FOR A SPECIFIC PROPERTY in order to have funds reserved or be on a waiting list. The contract may be dated prior to the date of the loan application. (Buyers may be prequalified. However, if the buyer does not have a contract on a property, PROGRAM FUNDS MAY NOT BE HELD for the buyer until such time as the buyer presents a valid contract.)

Program funds are locked for a buyer when a reservation is submitted on and accepted by the system and a loan number is obtained.

All loans must be registered through the eHousing Website. Complete the reservation form online and submit it via the Internet. Reservations submitted correctly receive a confirmation that the loan has been accepted and a loan number. If submitted incorrectly, there is instant online feedback identifying non-compliance and/or missing information issues. Lenders may choose to print confirmation from “Loan Detail” screen.

Loan Processing, Delivery and Purchase Timetable: New Construction and Short Sales cannot be reserved until 15 days before closing. Reservation to Underwriter Certification = 15␣days (no extensions) Reservation to Closed & Delivered First Mortgage Loan = 50 days (no extensions)Reservation to Exceptions Cleared &␣1st & 2nd mortgage Loans Purchased = 70 daysLoans not meeting the timetable cancel automatically without notice. Lenders may not automatically replace a loan in this first-come, first-served program. There is no reinstatement of canceled loans.

Extension Extension requests must be made prior to exceeding 70 days to Purchase. The extension grants up to 30 additional days for loans to be purchased by the Servicer at a cost of $375. The extension fee will be netted when loans are purchased for loans that are delivered. For loans that are not purchased, the Issuer will bill the lender for the fee.

There is a link to the extension request form on the program page within the ehousingplus system. Look for the SUMMARY tab. Click on and scroll down to Extension verbiage and click.

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 29

PROGRAM FEES

FIRST MORTGAGE FEESThere are no Origination or Discount Fees charged in this program.

ADMINISTRATOR FEE The program includes a Compliance Fee of $225 that is paid via check and submitted as part of the Compliance File. See Compliance File Checklist for additional information.

SERVICER FEESThe program includes a Tax Service Fee of $85 and a Funding Fee of $200 that will be netted by the Servicer at loan purchase. The fees must be disclosed on the HUD-1 as being paid to U S Bank.

LENDER FEESIn addition to the SRP noted below, Lenders are permitted to charge reasonable and customary charges for out of pocket expenses and costs. Other financing costs such as legal fees and underwriting fees may be charged and courier fees may be charged if such fees are normally charged. Lenders may charge the usual and reasonable settlement costs. Settlement costs include titling and transfer costs, title insurance, survey fees or other similar costs. Other allowable fees include doc prep fees, notary fees, hazard, mortgage and life insurance premiums, recording or registration charges, prepaid escrow deposits and other similar charges allowable by the insurer/guarantor. "Junk" fees are not a defined term and may not be charged. Excessive fees are not permitted in the program.

LENDER COMPENSATION Lenders receive SRP of 1.75% and reimbursement of the advanced DPA when US Bank purchases the loan.

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 30

PROGRAM COMPLIANCE UNDERWRITING Underwriters should remember that CALCULATION OF PROGRAM (COMPLIANCE) INCOME IS DIFFERENT THAN CALCULATION OF INCOME FOR CREDIT PURPOSES. The program requires that underwriters consider the income of borrowers and those who are secondarily liable on the Note (but not cosignors). Use the information below as a general guide. Because each case is different, please contact eHousingPlus Compliance if you have questions.

Unlike income that is averaged for credit underwriting, the program is concerned with actual current income. You should be reviewing the YTD income, the income of the last 4 months and the income shown on previous tax returns for consistency. You should not be averaging income. If there are not inconsistencies in earnings, use the guidelines for each loan type to determine current gross monthly income. Current gross monthly income is multiplied by remaining months in the year to determine "total current annualized income".

For the tax year in which the closing occurs, consider YTD income. First, establish current base income for the balance of the year using the guidelines for each type of income. Then consider any additional income. For assistance, contact the Compliance Office.

Gross monthly income is the sum of monthly gross pay; any additional income from overtime, part-time employment, bonuses, income from self-employment, dividends, interest, royalties, pensions, VA compensation and net rental income, other income (such as alimony, child support, public assistance, sick pay, social security benefits, unemployment compensation, income received from trusts, and income received from business activities or investments, continuation of which is probable based on foreseeable economic circumstances based upon the Mortgagor's Affidavit (to such effect), all as computed at the time of application for a mortgage loan and confirmed at the time of closing. We will check information with respect to gross monthly income obtained from the reservation form, Underwriter’s Certification and applicable certificates and affidavits executed the date of the Closing of the Mortgage Loan, provided that any gross monthly income not included for credit underwriting purposes must be included in determining gross monthly income. The limit is the limit and any amount over the limit is not acceptable. The Affidavit, executed by the borrower(s), and certified by the lender, must include the total verified annual income.

This program considers income of the borrower(s) and the income of any others who are secondarily liable on the loan who must reside in the property. Do not include the income of cosignors.

Questions regarding the calculation of income for program purposes should be directed to the Compliance office at [email protected] or 954-217-0817. There are many variables and the Compliance office will be pleased to assist. You are encouraged to ask questions in writing so that you receive a written response that may be printed and retained in your file.

“Alternate Documentation” (Alt Docs) as defined by the governing Agency (FHA, VA, etc) and other secondary market entities if acceptable to the Agency is acceptable in the program. Lender verification for compliance purposes is acceptable provided that such documentation includes the necessary, acceptable income tax transcripts. The Servicer requires a credit package as indicated on the various loan delivery checklists. However, the Servicer does not re-underwrite the loans for credit purposes. See bolded paragraph below.

Although reference is made to VOE’s and VOD’s in the guidelines below, they are not required if acceptable Agency alternate documentation is in the file. This documentation includes, but may not be limited to, current pay stubs which delineate “current period”, W-2's for all borrowers and all employers, and bank statements to verify assets. If W-2's are present in the loan file, lending personnel should verify that the total of W-2's presented equals the total income shown on borrower’s federal income tax transcripts. If a VOE is in the file, the borrower does not have to provide W-2's unless the underwriter deems this necessary for prudent underwriting. Figures shown on all documents should be consistent. See bolded paragraph below.

Because a program qualifier is “income”, even if not required for credit purposes (i.e. automated underwriting), you should be seeking the two most current paystubs with YTD. Do not include in the compliance file, keep copies for your records.

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 31

Although reference is made to the last 4 to 6 weeks income, Underwriters should be reviewing federal income tax transcriplts to verify that there are no unexplained and/or unacceptable differences current income to past income.

Examples below not intended to serve as exclusive methodology. Please contact the Compliance office [email protected] or 954-217-0817 with questions regarding individual cases.

Please note that the income reported for program income calculation CAN NEVER BE LOWER THAN THE INCOME USED TO QUALIFY FOR CREDIT PURPOSES.

Hourly Employees For the tax year in which the loan is closing, use the Year to Date base income. If consistent, utilize the base to determine the balance of the year by 1.Using last 4 to 6 weeks' pay stubs, identify hourly rate of pay and average number of regular hours worked per week. Multiply hourly rate times regular weekly hours. Multiply result times number of weeks for balance of year and add to YTD for an annualized base salary. 2.If the person has no other sources of income (for example: overtime, bonus, commissions, second jobs, interest, dividends, child support, alimony, public assistance), this will be the Current Total Annual Income. 3.Compare the total annual income in #2 above to Paystubs, VOE’s, previous year’s income per W2's and tax returns. You should not find significant differences. In some cases, the Current Total Annual Income will be higher than the previous year's income. Variances should be attributable to increases/decreases in pay or number of hours worked. You should not find significant differences. In some cases, the Current Total Annual Income will be higher than the previous year's income. Variances should be attributable to increases/decreases in pay or number of hours worked.

Salaried Employees 1. Using last 4 to 6 weeks' pay stubs, identify weekly (or other frequency) rate of pay. Multiply rate times the number of regular pay periods in the year (52 weeks, 12 months, 24 semi-months) 2. If the person has no other sources of income (for example: overtime, bonus, commissions, second jobs, interest, dividends, child support, alimony, public assistance), this will be the Current Total Annual Income. 3. Compare the total annual income in #2 above to Paystubs, VOE’s, previous year’s income per W2's and tax returns. You should not find significant differences. In some cases, the Current Total Annual Income will be higher than the previous year's income. Variances should be attributable to increases/decreases in pay or number of hours worked

Business, Self Employment 1. Use the quarterly tax returns and financial statements to identify the current NET year to date income. 2. Divide the year to date income by the number of months during which it was earned and multiply times remaining number of months in year. Add to actual YTD. ADD DEPRECIATION. 3. If the person has no other sources of income (for example: overtime, bonus, commissions, second jobs, interest, dividends, child support, alimony, public assistance), this will be the Current Total Annual Income. 4. Compare the total annual income in #2 above to the previous year's income per W2's and tax returns. You should not find significant differences.

Verified Termination of Overtime, Commission, Bonus, Seasonal, Periodic, One Time Overtime, Bonus, Commissions Using last 4 to 6 weeks' pay stubs, identify the year to date total earnings of the borrower. Subtract the Current Total Base Income (see above) to arrive at the total year to date extraordinary income. If verification of termination of overtime, commission or bonus is provided in writing (i.e. a letter from an employer) or such termination is due to a change of employment, use the current YTD overtime, commission or bonus, do not annualize and add as a lump sum to the Current Total Annual Income.

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 32

Regular Overtime, Bonus, Commissions 1. Using last 4 to 6 weeks' pay stubs, identify the year to date total earnings of the borrower. Subtract the Current Total Base Income (see above) to arrive at the total year to date extraordinary income. 2. Divide the year to date extraordinary income by the number of pay periods during which it was earned (to obtain an average). Multiply times the appropriate factor (Balance of year weeks, months, semi- months, etc.) for balance of year figure and add to actual YTD extraordinary income for annual income.3. If the person has no other sources of income (for example: second jobs, interest, dividends, child support, alimony, public assistance), this will be the Current Total Annual Income. 4. Compare the total annual income in #2 above to Paystubs, VOE’s, previous year’s income per W2's and tax returns. You should not find significant differences. In most cases, the Current Total Annual Income will be higher than the previous year's income. It will also generally be higher than the annualized year to date income. The variances should be attributable to increases/decreases in pay.

Interest, Dividends 1. Use current earnings statements issued by the bank, investment broker or agent. Identify the year to date interest or dividend earnings. Divide by the investment term year to date (for an average) and multiply times appropriate factor to annualize the earnings.2. If statements are not available, and the terms of the investment agreement are available, multiply the principal amount of the asset times the annual interest yield factor for a projected interest earnings amount. 3. If neither are available, use the previous year's earnings statements or tax returns to identify total annual interest and dividend income. If the assets are still invested in the same instruments, use the previous year's figure. 4. Add the result of the computation in either #1, #2 or #3 above to the Current Total Annual Income.

Alimony, Child Support 1. Use the monthly amount appearing in the divorce decree, separation agreement or other support document. 2. If the borrower receives more than the amount stipulated in the agreements, use the monthly figure that the borrower declares and can be verified. 3. If the borrower receives less than the amount stipulated in the agreements and there is a verifiable history of the underpayments for at least 2 years (as evidenced by Court records), then use the past 2 years' historical monthly earnings. If there is no such history that can be verified, use the amount stipulated in #1 above. 4. Multiply the monthly amount of alimony or child support times 12. Add to the Current Total Annual Income (plus any other income sources).

Pensions, Temporary Payments 1. Use the benefits statement issued by the benefits provider (pensions, workers compensation, disability compensation, social security, AFDC, etc.) to identify the amount of the benefit, payment frequency and expected term of the benefit. 2. Multiply the amount of the benefit times the payment frequency for the balance of year and add to actual YTD for an annualized amount. Add to the Current Total Annual Income (plus any other income sources). 3. If the benefit is absolutely not payable to the recipient beyond a given date (that means a complete and permanent stop of benefits without extensions, exceptions, waivers or other conditions) and such date is within 12 calendar months of the anticipated closing date, then calculate the benefits expected through the end of the benefits term. That will be the total annual income amount from the specific benefits source. Add to the Current Total Annual Income (plus any other income sources).

Boarder’s Income and Rental Income in One Unit Properties The Boarder’s wages/income and rental income paid to the borrower must be included in the program calculation of income.

Rental Income from 2-4 Unit Properties Anticipated rental income from the property being purchased is not included in the program calculation of income but may be treated as detailed in Agency (FHA, VA, Freddie, etc) guidelines. If the borrower’s own other rental property from which income is derived, that income must be included in the program calculation of income.

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 33

PROGRAM FORMS This topic addresses the specific program forms required for the program for originating, processing, closing and loan delivery. All forms are found on the ehousingplus program page behind security as they are auto-fill.

A complete Mortgage File to US Bank must include all standard Agency (i.e. FHA, VA, etc. forms).

While forms may be downloaded on your PC or laptop, going to the Website for forms each time you need them assures that the most current version is being used.

The simple rule of who signs program forms – if the person is named on the Mortgage/Deed, they sign the program forms. If they are not on the Mortgage/Deed, they do not sign the program forms. Also, remember cosigners cannot live in property, do not sign program documents or take title. Having people sign documents who should not sign is as incorrect as not having all sign who should. Under no circumstances may a cosigner’s name appear on title or warranty deed, only those on credit sign the 1003 and HUD-1.

Original, personal signatures of all borrowers and sellers are required and must match on all documents associated with the transaction.

Whenever a party is known in any of the documents by more than a single name, a Name Affidavit Will Be Required.

Powers of Attorney and/or Personal Representatives for the Borrower Are Not Acceptable. Exception: Active Duty Military Personnel may provide an “Alive and Well” letter.

COMPLIANCE FORMS There are no forms signed prior to closing. Prior to closing, the Lender’s Underwriter completes the online Underwriter’s Certification. After the Certification is submitted online, Lenders may access program forms that are auto-fill. There are four forms used on every loan -- Affidavits/Certification Form that contains (3 sections as noted below), Lender Commitment Form and Award Letter (required for all loans) and the Compliance File Checklist. In cases where there is a cosignor, there is a Cosignor Affidavit.

At closing, the borrower(s) and those secondarily liable on the Note (but not cosignors) sign the Mortgagor’s Affidavit. Sellers sign the Builder/Seller Affidavit and Lender’s sign the Lender’s Certification that are part of the Affidavits-Certification form. Cosignors do sign the Cosignor Affidavit.

There are two letters required in response to ML 2013-14 -- Lender Commitment Form and Award Letter. Follow distribution shown on bottom of Award Letter. The Commitment Form is printed and retained by lender, a copy in the FHA Case Binder and a copy to US Bank with US Bank form USB-002. Provided by US Bank.

The Compliance Checklist should be used to ship the Compliance File to eHousingPlus.

Delivery/Funding FormsThe Servicer provides checklists on their site for submission of the Mortgage File. There is a link on the eHousingPlus website for this program to U S Bank’s website.

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 34

OTHER DOCUMENTS REQUIRED FOR COMPLIANCE FILE

Tax Transcripts (Tax transcripts for the preceding year are due April 15 of the current year.) The past three years tax transcripts are required for borrowers and spouses. Not required for those buying in Targeted Areas or those purchasing under the Veteran’s Exception. Requests for Extensions are not acceptable in lieu of tax transcripts.

Real Estate Purchase Contract The full address of the property, full names of all sellers and buyers, total purchase price of the property must be included. If there is not an address for new construction, a lot number and subdivision name are required. All named persons must sign. Include the name and title whenever a representative is signing for a corporation.

Final Loan Application (1003) The typed application signed and dated by all parties is required. Loan interviewer must complete and sign page 3 of 4 of the 1003. If this is not possible, then an Officer must sign in place of the interviewer. All persons taking title to the property must execute all program documents. The income disclosed on the Affidavit must be the same or more than that shown on the 1003. The purchase price, loan amount, and other financial details must be the same as shown on all other documents.

HUD-1 Settlement Statement Buyer, seller and closing agent must fully execute the HUD-1. Borrowers on the HUD-1 must be all persons taking title to the property and match the Affidavit and application. Persons not taking title to the property may not appear or sign the HUD-1. The Tax Service Fee and Funding Fee must be shown as being payable to Servicer. Please do not bundle charges. Itemize all charges to the transaction. Payoffs of other debt must appear on Page 1 under Section 100 of the HUD-1 as part of "Settlement Costs".

Warranty Deed A copy of the Warranty Deed is required.

Homebuyer Education Certificate Required of all named on the Warranty Deed.

Discharge or Release Papers for VetsFor those qualifying for the Veteran’s Exception, a copy of Discharge or Release papers is required.

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 35

??US BANK WEB SITE INFORMATION

For information on how to find the US Bank checklists, bulletins and guidelines please see below.

1. Click on this link: http://www.mrbp.usbank.com/thirdParty/goOffsiteConfirm.cfm?BL=USB&ID=1006

2. You will be prompted with a pop-up message, click Continue.

3. Click on Housing Finance Authority folder,

4. Within the folder, you will find the Product Descriptions, US Bank Checklists and Fee Sheet for this program.

5. Other important information can be found on this site as well such as Closing & Funding information, RESPA manual and the US Bank Bulletins.

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 36

??SAMPLES OF FORMS

ASSIST HOMEOWNERSHIP PROGRAM ADMINISTRATOR’S GUIDELINES Page 37