cle cours banking law for general practitioner

TRANSCRIPT

Banking Law for the General Practitioner

National Academy of Continuing Legal Education

Kathleen A. Scott, Esq.

Senior Counsel

Norton Rose Fulbright US LLP

Introduction

• Banks are not ordinary business corporations organized under the general business corporation laws of the various states; there are specialized state and federal banking statutes

• A bank may be chartered by either the U.S. Government or a state banking department, and is subject to the banking laws of the chartering authority, oftentimes with a federal overlay of regulation and supervision

• Liquidation of a bank is done according to federal or state bank liquidation laws, not federal bankruptcy laws

• Banks vs. “investment banks”

• Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank) made major changes to the federal banking laws

2

Bank regulators – Federal

Board of Governors of the Federal Reserve System (“Federal Reserve Board”)

• Monetary policy and bank supervisory responsibilities

• In the bank supervisory area, has jurisdiction over:

• Bank holding companies and savings and loan holding companies

• State-chartered banks that are member banks of the Federal Reserve System

• Non-U.S. banks with operations in the United States

Office of the Comptroller of the Currency (“OCC”)

• Charters and supervises national banks and federal thrifts

• Licenses and supervises offices of non-U.S. banks that choose the OCC as licensing authority

3

Primary federal bank regulatory agencies (cont’d)

Federal Deposit Insurance Corporation (“FDIC”)

• Provides federal deposit insurance for state and national banks, and state and federal thrifts

• If a bank has deposits subject to federal deposit insurance, federal deposit insurance is required

• During the economic crisis, deposit insurance temporarily was raised to $250,000 per ownership category; Dodd-Frank made it permanent

• Primary federal regulator of state non-member banks and state-chartered thrifts

Office of Thrift Supervision (“OTS”) previously had chartered and supervised federal thrifts and holding companies and some state-chartered thrifts, but was abolished by Dodd-Frank and jurisdiction divided among Federal Reserve Board, OCC and FDIC

4

Consumer Financial Protection Bureau

Bureau of Consumer Financial Protection (“CFPB”)

• Established as part of Dodd-Frank reform bill

• Most consumer laws and regulations transferred to CFPB, such as:

• Mortgage regulations

• Remittance regulations

• Equal credit opportunity

• Privacy

• SEC, CFTC and FTC also have jurisdiction in certain areas

• Adds federal level of supervision over large banks and certain nonbank financial institutions

• “Larger participants” in the automobile financing market, consumer debt collection, international money transfers, and student loan servicing market

5

Banking Statutes and Regulations - Federal

Bank Holding Company Act (12 USC 1841 et seq.)

• Regulates the activities of bank holding companies and financial holding companies

• What makes a company a “bank holding company”

• Bank holding companies can engage in banking and activities closely related to banking (limited insurance and securities underwriting authority, and restricted ability to engage in, or invest in companies that engage in, non-banking-related activities)

• In 1999, the Gramm Leach Bliley Act authorized bank holding companies to become “financial holding companies” (FHCs)

• FHCs can engage in activities considered financial in nature or incidental or complementary to a financial activity (insurance and securities underwriting authority, merchant banking)

• 12 CFR Part 225, Regulation Y

6

Principal federal statutes and regulations (cont’d)

National Bank Act (12 USC 21 et seq.)

• Provides for the chartering of national banks

• Regulates activities of national banks

• 12 CFR Chapter 1, starting with Part 1 and following

Federal Reserve Act (12 USC 221 et seq.)

• Provides for membership of state banks in the Federal Reserve System (national banks must become member banks)

• Regulates certain activities of member banks

• Establishes the Federal Reserve Bank system

• 12 CFR Part 208, Regulation H

7

Principal federal statutes and regulations (cont’d)

Federal Deposit Insurance Act (12 USC 1811 et seq.)

• Establishes a system of federal deposit insurance

• Regulates at the Federal level the activities of state-chartered insured banks that are not member banks of the Federal Reserve system

• Establishes the procedures for conservatorship, receivership and liquidation of insured banks

• 12 CFR Parts 303-369

8

Principal federal statutes and regulations (cont’d)

International Banking Act (12 USC 3101 et seq.)

• Provides authority for the Federal Reserve Board to approve or revoke the ability of a non-U.S. bank to establish a branch, agency, representative office or commercial lending company in the United States

• Provides that the non-banking activities in the United States of non-U.S. banks that have banking operations in the United States must conform to the activities in which a U.S. bank holding company (or FHC, if the non-U.S. bank qualifies to be treated as such) may engage

• 12 CFR Part 211, Regulation K

9

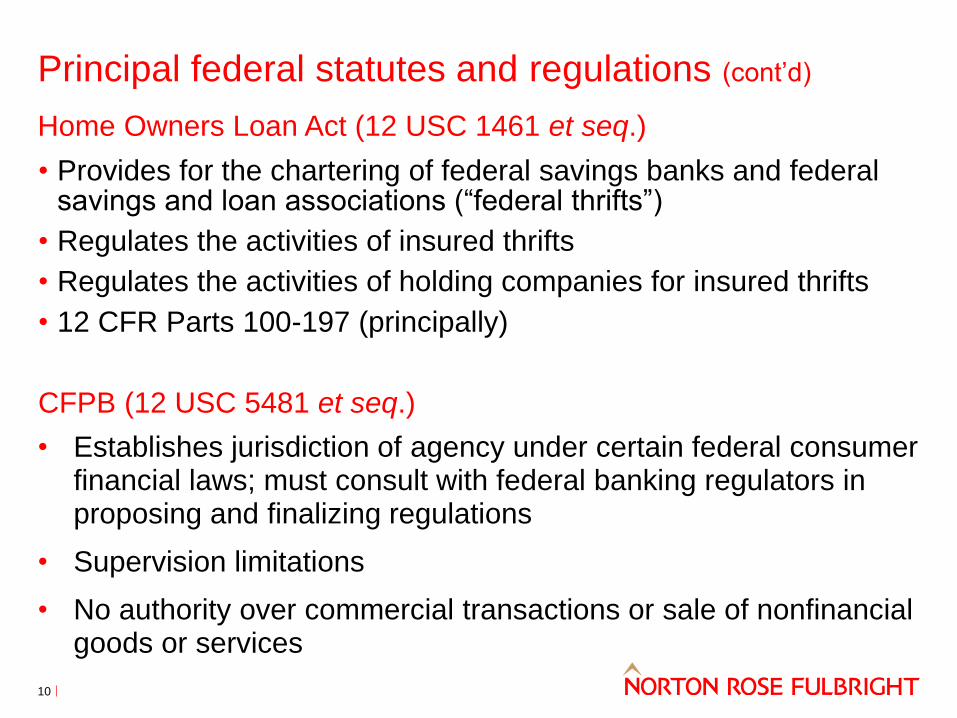

Principal federal statutes and regulations (cont’d)

Home Owners Loan Act (12 USC 1461 et seq.)

• Provides for the chartering of federal savings banks and federal savings and loan associations (“federal thrifts”)

• Regulates the activities of insured thrifts

• Regulates the activities of holding companies for insured thrifts

• 12 CFR Parts 100-197 (principally)

CFPB (12 USC 5481 et seq.)

• Establishes jurisdiction of agency under certain federal consumer financial laws; must consult with federal banking regulators in proposing and finalizing regulations

• Supervision limitations

• No authority over commercial transactions or sale of nonfinancial goods or services

10

State banking laws and agencies

• Banks can be chartered by the OCC or by a state; each state allows banking organizations to be formed

• The state code will authorize the categories of banking institutions permitted to be organized in the state, set forth the authorized activities and requirements for each category and prescribe the supervisory oversight of the state regulator

• The types of banking organizations authorized are similar to those chartered at the federal level, although there are some differences

11

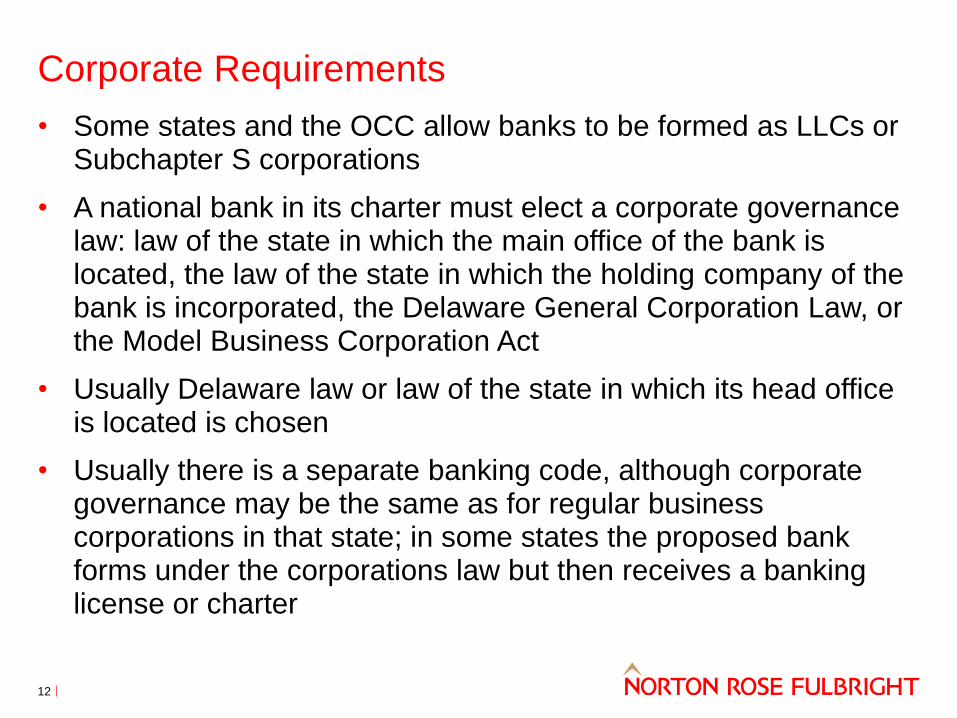

Corporate Requirements

• Some states and the OCC allow banks to be formed as LLCs or Subchapter S corporations

• A national bank in its charter must elect a corporate governance law: law of the state in which the main office of the bank is located, the law of the state in which the holding company of the bank is incorporated, the Delaware General Corporation Law, or the Model Business Corporation Act

• Usually Delaware law or law of the state in which its head office is located is chosen

• Usually there is a separate banking code, although corporate governance may be the same as for regular business corporations in that state; in some states the proposed bank forms under the corporations law but then receives a banking license or charter

12

State vs. federal charter?

• Why choose a state or a federal charter?

• Ultimately it is a business choice in line with business plan

• Pre-emption of state law for national banks and federal thrifts

• History at OCC and OTS of aggressive pre-emption determinations

• Controversial pre-emption decisions included pre-emption of state laws dealing with “predatory” lending and bank sales of insurance to customers

• Dodd-Frank Act restricted use of preemption, including eliminating it for operating subsidiaries of national banks and federal thrifts

• Laws generally not preempted: contracts; torts; criminal law; rights to collect debts; acquisition and transfer of property; taxation; zoning; and any other laws as determined by the OCC

13

Capital requirements

Banks must abide by certain capital and liquidity requirements

Risk-based capital requirements

• The more risky the asset, the more capital that needs to be reserved

International standards developed by the Basel Committee of the Bank for International Settlements – international group of regulators

Basel I: assigned risk weights

Basel II: more reliance on internal models

• Standard option similar to Basel I

• Models need to be approved by regulators

• Needed to be adopted by each country, but implementation in the United States was delayed

14

Capital requirements: post-economic crisis

Basel III: Changes made after the recent economic crisis

• Capital standards strengthened

• Leverage ratio

• Strengthened liquidity requirements

• Capital surcharge on large systemically significant banks

• Supplementary leverage ratio

• New proposal Total Loss-Absorbing Capacity (TLAC)

Additional Dodd-Frank Act changes to capital rules

• Collins Amendment directed federal banking agencies to establish, on a consolidated basis, minimum leverage capital and risk-based capital requirements not be less than what would be applicable to insured depository institutions

• Applicable to insured depository institutions and their holding companies and SIFIs

15

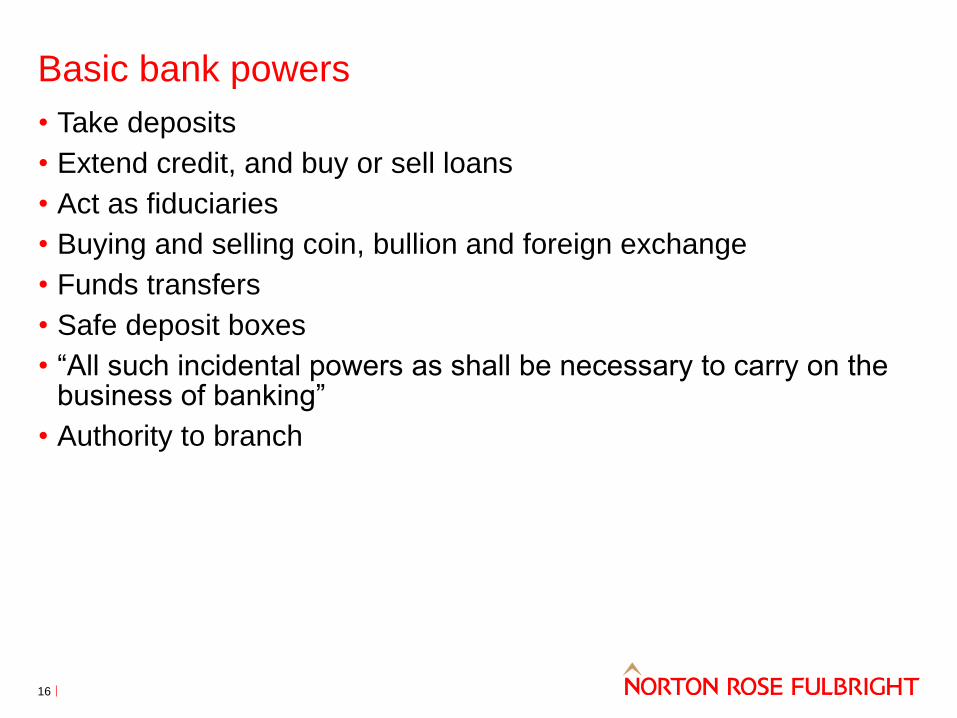

Basic bank powers

• Take deposits

• Extend credit, and buy or sell loans

• Act as fiduciaries

• Buying and selling coin, bullion and foreign exchange

• Funds transfers

• Safe deposit boxes

• “All such incidental powers as shall be necessary to carry on the business of banking”

• Authority to branch

16

Restrictions on bank transactions with affiliate

Sections 23A and 23B of the Federal Reserve Act and Federal Reserve Board Regulation W (12 CFR Part 223)

• Statutory quantitative and qualitative restrictions on a bank’s ability to do business with its affiliates; Regulation W focuses on insured bank’s transactions

• Legislative intent was to try to ensure that a transaction by a bank with its affiliate would not drag the bank down

• Transactions with affiliates generally have to be on an arm’s-length basis

• Extensions of credit to affiliates also must collateralized at least at 100% collateralization,

• Only certain types of collateral are acceptable

• “Affiliate” is broadly defined and includes mutual funds advised by banks

• Transactions by a bank with a non-affiliate for the benefit of an affiliate of the bank also are covered

• There are some exemptions from requirements, but narrowly drawn

17

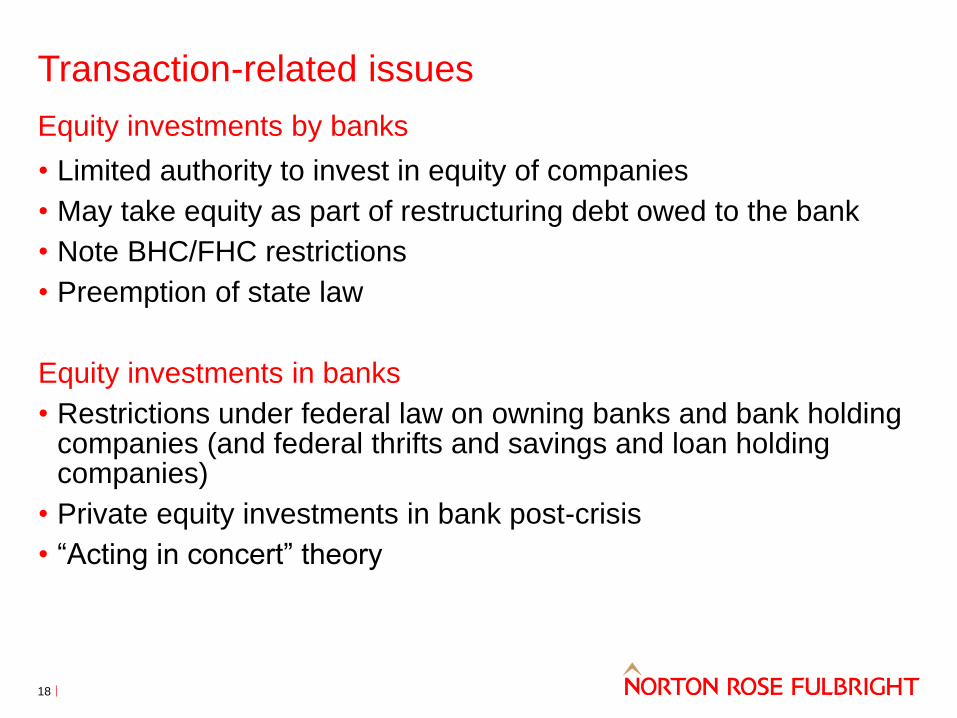

Transaction-related issues

Equity investments by banks

• Limited authority to invest in equity of companies

• May take equity as part of restructuring debt owed to the bank

• Note BHC/FHC restrictions

• Preemption of state law

Equity investments in banks

• Restrictions under federal law on owning banks and bank holding companies (and federal thrifts and savings and loan holding companies)

• Private equity investments in bank post-crisis

• “Acting in concert” theory

18

Transaction-related issues (cont’d)

Margin Lending Regulations

• “Margin stock” defined

• Banks are restricted in the amount they may lend for the purpose of buying or carrying margin stock if the credit is secured by margin stock

• When any loan is collateralized by margin stock, a form must be signed by the borrower and placed in the loan file

• Secured by margin stock also includes indirectly secured, such as a negative pledge

• Special rules when margin stock is part of a larger group of collateral

• Nonbank lenders must register with local Federal Reserve Bank

19

Transaction-related issues (cont’d)

Tying Restrictions and Exceptions

• Bank prohibited from extending credit, leasing or selling property of any kind, or furnishing any service, or fixing or varying the consideration for any of the foregoing, on the condition or requirement that the customer obtain or provide some additional credit, property, or service from such bank (or its holding company or nonbank subsidiary of the bank holding company) other than a traditional banking service (loan, discount, deposit, or trust service) or that the customer not obtain some other credit, property, or service from a competitor of the bank, its bank holding company or nonbank subsidiary of the bank holding company, other than a condition or requirement that such bank shall reasonably impose in a credit transaction to assure the soundness of the credit

20

Transaction-related issues (cont’d)

Flood Insurance

• Applies to loans secured by buildings or mobile homes located or to be located in areas determined by the Federal Emergency Management Agency to have special flood hazards

• Requires that the building, mobile home or personal property securing the loan be covered by flood insurance for the term of the loan; extremely limited exceptions

• Coverage is limited to the overall value of the property securing the designated loan minus the value of the land on which the property is located

• If borrower fails to maintain the required amount of coverage, bank must obtain the insurance for the borrower and can charge the borrower for the premiums and fees incurred in purchasing the insurance

• Civil penalties for violations

21

Transaction-related issues (cont’d)

FIRREA appraisal requirements

• Appraisals by licensed or certified appraisers are required when a bank makes a loan taking real estate as collateral

• There are several exceptions, including:

• Lien on real estate is taken as collateral in an abundance of caution

• Lien on real estate has been taken for purposes other than the real estate’s value

• Bank is acting in a fiduciary capacity and is not required to obtain an appraisal under other law

• Bank staff may do appraisal but staff appraiser must be independent of the lending, investment, and collection functions and not otherwise involved with the transaction

• Outside appraisers must be engaged directly by the bank or the bank’s agent, not the borrower

• Bank regulators periodically issue guidance

22

Representations and warranties

• Capital

• Dodd-Frank

• Anti-money laundering laws and regulations

• Economic sanctions laws and regulations

• Awareness of anti-money laundering and economic sanctions laws increased post 9/11, and you now see related reps and warranties in credit documents

• Since the passage of Dodd-Frank, you are starting to see reps and warranties related to regulatory changes

Transaction-related issues (cont’d)

23

Other regulatory issues

Anti-Money Laundering (“AML”) (Financial Crimes Enforcement Network, “FinCEN’)

• Cash reporting and recordkeeping requirements

• AML Compliance Program

• Customer Identification Program

• Suspicious Transaction Reporting

• Applicable to a broad array of businesses classified as “financial institutions”

• New proposal to cover investment advisers

• Identification requirement of “beneficial owner” of entity pending

24

Other regulatory issues (cont’d)

Economic Sanctions (Office of Foreign Assets Control, “OFAC”)

• U.S. persons are prohibited from doing business with “Specially Designated Nationals”

• Separate economic sanctions imposed against countries or certain property

• Each of these programs is covered by its own set of regulations

25

Other regulatory issues (cont’d)

Consumer Lending: Community Reinvestment Act

Consumer Protection Regulations and Disclosure

• Truth in Lending (Regulation Z) – credit cards, consumer lending

• Regulation B (Equal Credit Opportunity) – nondiscriminatory access to credit

• Regulation E (Electronic Funds Transfer Act) – debit cards, gift cards, fund transfers

• Regulation CC (Funds Availability) - checks

• Regulation DD (Truth in Savings) – disclosures

• Fair Credit Reporting Act – credit reports, “adverse action”

26

Other regulatory issues (cont’d)

Privacy of Non-Public Personal Information

• Protection of confidential customer information

• Customers protected are individuals

• Privacy Policy provided at beginning of customer relationship and annually thereafter

• Banks must ensure its service providers also protect confidentiality of customer information

• Affiliate marketing issues

• Requirements in event of breach

• Model Forms

• “Interagency Guidelines Establishing Information Security Standards”

• Recent changes allow annual notices to be posted to a bank’s website

• ID Theft

27

Other regulatory issues (cont’d)

Outsourcing

• Banks often outsource services to affiliated and unaffiliated service providers

• Oftentimes used for back-office activities such as data input, clearing of transactions, back office processing, Internet-related activities

• Certain outsourcings require notice to regulators

• Contracts should include provisions for regulatory access

• Outsourcings to non-U.S. service providers can be of special concern

• Regulatory Guidance

28

Other regulatory issues (cont’d)

Cybersecurity

• Increasing concern by regulators

• Banks subject to attacks

• Safety and soundness issues

• Interagency guidance

• States also taking a stand

29

Dodd-Frank – in general

“Dodd-Frank Wall Street Reform and Consumer Protection Act” was signed into law on July 21, 2010 (Public Law 111-203)

• Major changes made to financial regulation in the United States

• Implemented through numerous regulatory rulemakings

Systemic risk a key provision in the law

• Large bank holding companies

• Nonbank financial institutions deemed to be of systemic risk

OTS eliminated

• Jurisdiction divided up among OCC, FDIC and Federal Reserve Board

30

Dodd-Frank – in general (cont’d)

Major themes of Dodd-Frank include:

• Systemic risk issues

• Consumer Financial Protection Bureau

• Volcker Rule

• Swaps and derivatives

• Credit risk retention

• Mortgage reforms

• Investor protections

31

Dodd-Frank - systemic risk regulation

Title I of the Act: Financial Stability Oversight Council (FSOC) to identify and respond to systemic risk

• Chaired by Treasury Secretary, FSOC consists of either federal or state government agencies except for an independent appointee with insurance expertise

• Responsibilities include designation of individual nonbank financial companies that are considered to pose a risk to US financial stability to be supervised and regulated by the Federal Reserve Board (SIFI – systemically important financial institution)

“Nonbank financial companies” are companies that derive:

• 85% or more of annual gross revenues from financial activities; or

• 85% or more of consolidated assets relate to financial activities

• “Financial activities” as defined in Bank Holding Company Act

• To date, four designated: AIG, Prudential, GE Capital (scaling back), Metlife (challenging definition in court)

32

Dodd-Frank - systemic risk regulation (cont’d)

Systemic Risk Test: Would company pose a risk to the US financial stability in the event of its material financial distress or failure, or because of nature, scope, size, scale, concentration, interconnectedness, and mix of company’s activities

• Large bank holding companies (US-based BHCs/FHCs and non-US banks that are treated as US BHCs or FHCs under the International Banking Act) with total consolidated assets of $50 billion or more are in effect deemed to be of systemic risk

• Large bank holding companies and nonbank financial companies deemed to be of systemic risk are subject to enhanced prudential standards on their operations

33

Dodd-Frank - systemic risk regulation (cont’d)

Comprehensive final prudential standards regulations adopted and effective June 1, 2014, but compliance dates generally move to 2015 and 2016; added to certain others adopted previously

• Prudential Standards now include:

• Enhanced risk-based capital and leverage capital requirements, resolution planning, capital planning and stress testing

• Risk Management and Risk Committee requirements

• Enhanced liquidity requirements

• Debt-to-Equity Limits

• Similar requirements for non-U.S. banks, and more

• Prudential standards on SIFIs imposed a case-by-case basis: e.g., prudential standards for GE Capital

• Federal Reserve Board also may impose stricter regulation on certain financial activities or products because the activities may pose systemic risk

34

Orderly Liquidation Authority – Title II of Dodd-Frank

• Intended to address “too big to fail” concept

• Systemic risk determination (different from Title I)

• Orderly liquidation of covered financial companies by FDIC similar to how FDIC resolves insured banks now

• Authority would be invoked if the Treasury Secretary, upon FDIC and Federal Reserve Board recommendation and in consultation with the President, determines that a failed financial company cannot be resolve under traditional means (US Bankruptcy Code) without posing a systemic risk

Dodd-Frank - systemic risk regulation (cont’d)

35

“Volcker Rule”

“Volcker Rule” imposes prohibitions and restrictions on the ability of banking entities and SIFIs to engage in proprietary trading or investing in or sponsoring a private equity fund

“Banking entities” -- insured banks and their holding companies, non-US banks that maintain branches and agencies in the US and their subsidiaries and affiliates

Final rules issued December 2013 by US federal banking agencies, SEC and CFTC

General Rule prohibits banking entities from:

• Engaging in proprietary trading: engaging as principal for the trading account of the banking entity in any purchase or sale of one or more financial instruments (securities, derivatives, commodity sale contract)

• As principal, directly or indirectly acquiring or retaining any ownership interest in or sponsoring a “covered fund” as defined (a fund exempt from certain provisions of the Investment Company Act)

36

“Volcker Rule” (cont’d)

Exemptions from the proprietary trading ban:

• Underwriting

• Market-making

• Risk-mitigating hedging

• Trading in certain domestic government obligations

• Trading as fiduciary

• Riskless principal transactions

• “Solely outside the United States”

37

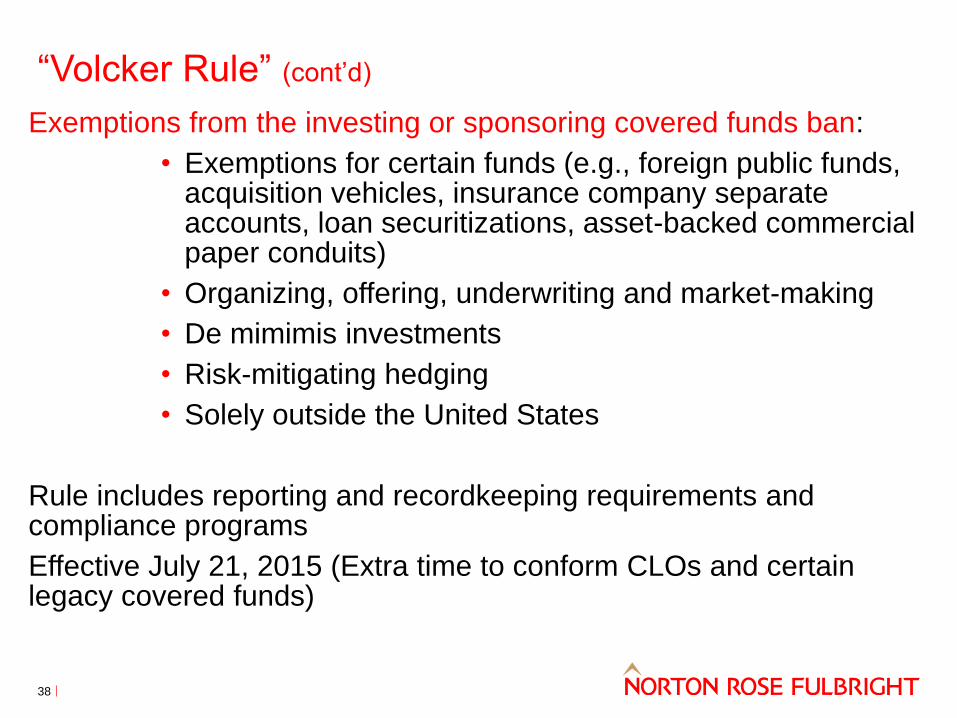

“Volcker Rule” (cont’d)

Exemptions from the investing or sponsoring covered funds ban:

• Exemptions for certain funds (e.g., foreign public funds, acquisition vehicles, insurance company separate accounts, loan securitizations, asset-backed commercial paper conduits)

• Organizing, offering, underwriting and market-making

• De mimimis investments

• Risk-mitigating hedging

• Solely outside the United States

Rule includes reporting and recordkeeping requirements and compliance programs

Effective July 21, 2015 (Extra time to conform CLOs and certain legacy covered funds)

38

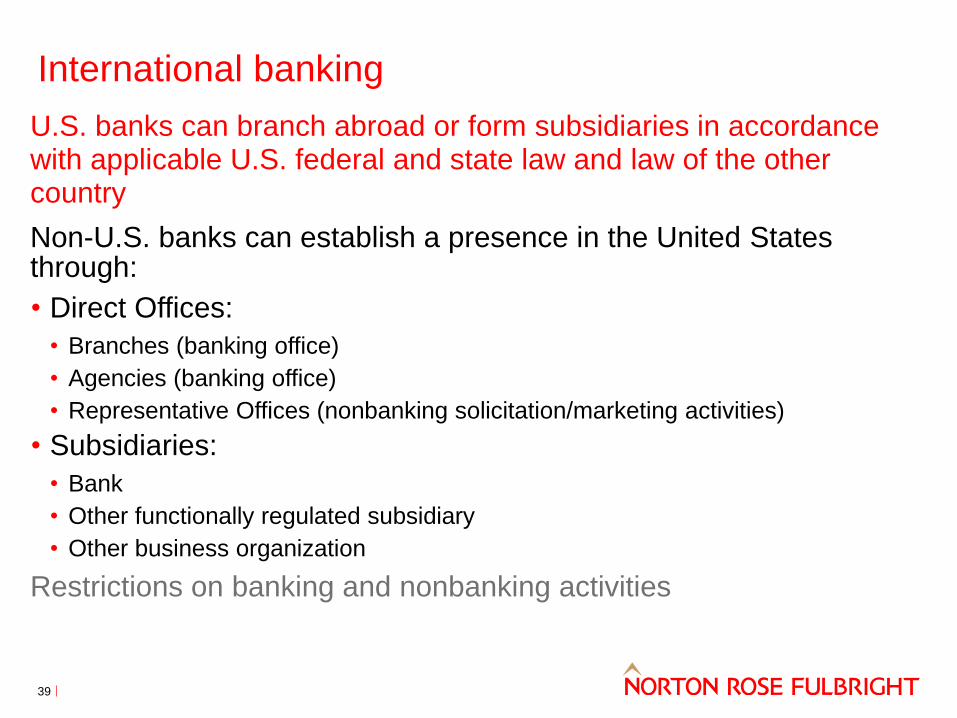

International banking

U.S. banks can branch abroad or form subsidiaries in accordance with applicable U.S. federal and state law and law of the other country

Non-U.S. banks can establish a presence in the United States through:

• Direct Offices:

• Branches (banking office)

• Agencies (banking office)

• Representative Offices (nonbanking solicitation/marketing activities)

• Subsidiaries:

• Bank

• Other functionally regulated subsidiary

• Other business organization

Restrictions on banking and nonbanking activities

39

International Banking (cont’d)

Approval from the home country regulator

Board of Governors of the Federal Reserve System (Federal Reserve Board) – gatekeeper

• Comprehensive supervision on a consolidated basis (“CCS”)

• New Dodd-Frank systemic risk consideration requirement for entry and termination

License needed to open an office is needed from either OCC or a state

Most international bank offices are state-licensed

• New York has the most international bank offices in the United States

• Other states that also have a substantial international bank presence: FL, CA, TX, IL

40

Questions:

Kathleen A. Scott, Esq. Senior Counsel Norton Rose Fulbright US LLP 666 Fifth Avenue New York, NY 10103 Telephone: (212) 318-3084

Fax: (212) 318-3400 E-mail: [email protected]

Website: www.nortonrosefulbright.com

Blog: www.regulationtomorrow.com

41

Disclaimer

Norton Rose Fulbright US LLP, Norton Rose Fulbright LLP, Norton Rose Fulbright Australia, Norton Rose Fulbright Canada LLP and Norton Rose Fulbright South Africa Inc are separate legal entities and all of them are members of Norton Rose Fulbright Verein, a Swiss verein. Norton Rose Fulbright Verein helps coordinate the activities of the members but does not itself provide legal services to clients.

References to ‘Norton Rose Fulbright’, ‘the law firm’ and ‘legal practice’ are to one or more of the Norton Rose Fulbright members or to one of their respective affiliates (together ‘Norton Rose Fulbright entity/entities’). No individual who is a member, partner, shareholder, director, employee or consultant of, in or to any Norton Rose Fulbright entity (whether or not such individual is described as a ‘partner’) accepts or assumes responsibility, or has any liability, to any person in respect of this communication. Any reference to a partner or director is to a member, employee or consultant with equivalent standing and qualifications of the relevant Norton Rose Fulbright entity.

The purpose of this communication is to provide general information of a legal nature. It does not contain a full analysis of the law nor does it constitute an opinion of any Norton Rose Fulbright entity on the points of law discussed. You must take specific legal advice on any particular matter which concerns you. If you require any advice or further information, please speak to your usual contact at Norton Rose Fulbright.

43