cliffside research · this research report reflects the opinions of cliffside research. we have...

TRANSCRIPT

Cliffsideresearch.com

1

Corindus Vascular Robotics, Inc. (CVRS) Status Report Rating: Strong Sell Price Target: 46c Date: October 19th, 2017 This research report reflects the opinions of Cliffside Research. We have based our opinions on facts and evidence collected and analyzed, all of which we set out in our research reports to support our opinions. This is not an offer to sell or a solicitation of an offer to buy any security. We strongly recommend that you do your own due diligence before buying or selling any security, and each investor must make any investment decision based on his/her judgment of the market and based upon all available information. At any time, you should presume that the principals of Cliffside Research and/or Cliffside Research clients and/or investors hold trading positions in the securities profiled on the site and therefore stands to realize significant gains in the event that the price of the stocks covered herein rises or declines in conjunction with our investment opinion. See our important full disclaimer titled “Terms of Service” at the bottom of this report.

CLIFFSIDE Research

2

➢ We thoroughly evaluated 4 primary selling points for CorPath and conclude

none of them are compelling reasons for healthcare providers to purchase the system.

➢ We find the PRECISE study vastly over exaggerates CorPath’s radiation

reduction to the physician.

➢ An alternative solution called the Zero-Gravity costs a fraction of a CorPath, provides nearly equivalent radiation protection, and relieves physicians of orthopedic strain & fatigue.

➢ The difference in radiation exposure between CorPath and Zero-Gravity is so

small that it can literally be measured with 4 bananas.

➢ CorPath simply can’t perform many complex procedures on its own that represent ~80% of PCI procedures.

➢ CorPath lacks haptic feedback that physicians find important in complex

cases

➢ CorPath lacks reimbursement and compelling clinical data showing improvement in patient outcomes vs. traditional procedures.

➢ Data indicates physicians are only conducting 2 procedures per month on

average using CorPath.

➢ We see only marginal improvements to CorPath GRX and believe the company will again fall woefully short of analyst expectations.

➢ With cash burn of nearly $30mil per year, CVRS is on pace to raise additional

funds around the middle of 2018, likely diluting shareholders.

➢ We see downside of over 60% to the stock and if CVRS can’t increase adoption of CorPath the company may be worthless.

Corindus Vascular Robotics, Inc. (CVRS)

We are providing a status report on Corindus Vascular Robotics, Inc. (CVRS) with a STRONG SELL rating and a target of 46c.

Cliffsideresearch.com

3

You Might Want To Sit Down For This

The Problem: Corindus Vascular Robotics, Inc. (CVRS) was originally an Israeli company founded in 2002 that currently resides in Waltham, MA. The company achieved FDA approval for its CorPath 200 robotic Percutaneous Coronary Intervention (PCI) system in 2012. PCI, formerly known as coronary angioplasty, is a nonsurgical procedure that improves blood flow to the heart by opening stenotic (narrowed or blocked) coronary arteries. Despite FDA approval, the company has only installed 51 CorPath systems in the past 5 years. Recently the stock had significantly outperformed the market based on expectations for increased adoption of the next gen system, CorPath GRX. Based on our analysis, we believe analyst estimates remain wildly optimistic and will ultimately have to be revised downward. In addition, because the company continues to burn a substantial amount of cash, we believe they will be forced to tap the equity market around Q3 of next year and will substantially dilute the shareholder base again. In the following pages we thoroughly examine the company, analysts overly optimistic assumptions and provide evidence that strongly suggests shares of CVRS are overvalued by more than 60%.

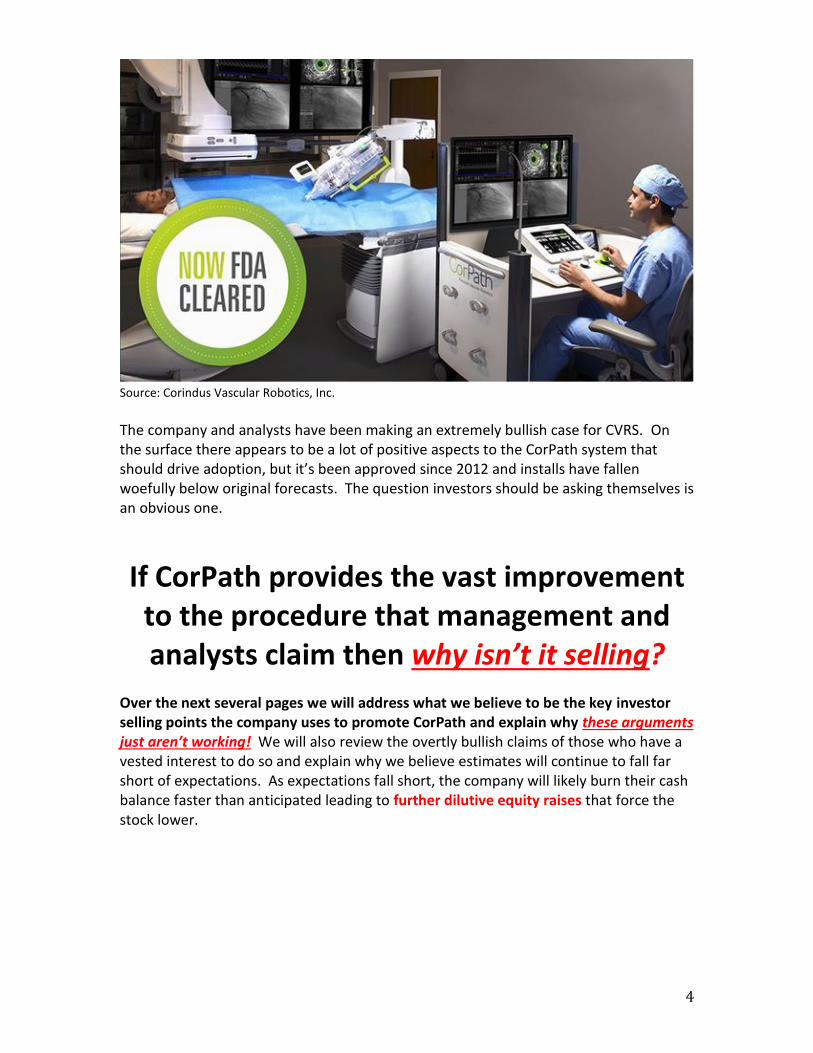

Enter CorPath: The CorPath vascular robotic system consists of an arm loaded with a disposable cassette that holds instruments (guidewire, balloon/stent) used in PCI procedures and a station where the IC can view and control the instruments. The CorPath robotic system costs $350k to $650k per unit and each procedure requires a cassette that costs $550 to $650. According to CVRS, one of the primary advantages to the CorPath system is the ability to perform the procedure at a station that reduces radiation exposure to the interventional cardiologist (IC) by over 95% without wearing heavy protective gear.

4

Source: Corindus Vascular Robotics, Inc.

The company and analysts have been making an extremely bullish case for CVRS. On the surface there appears to be a lot of positive aspects to the CorPath system that should drive adoption, but it’s been approved since 2012 and installs have fallen woefully below original forecasts. The question investors should be asking themselves is an obvious one.

If CorPath provides the vast improvement

to the procedure that management and analysts claim then why isn’t it selling?

Over the next several pages we will address what we believe to be the key investor selling points the company uses to promote CorPath and explain why these arguments just aren’t working! We will also review the overtly bullish claims of those who have a vested interest to do so and explain why we believe estimates will continue to fall far short of expectations. As expectations fall short, the company will likely burn their cash balance faster than anticipated leading to further dilutive equity raises that force the stock lower.

Cliffsideresearch.com

5

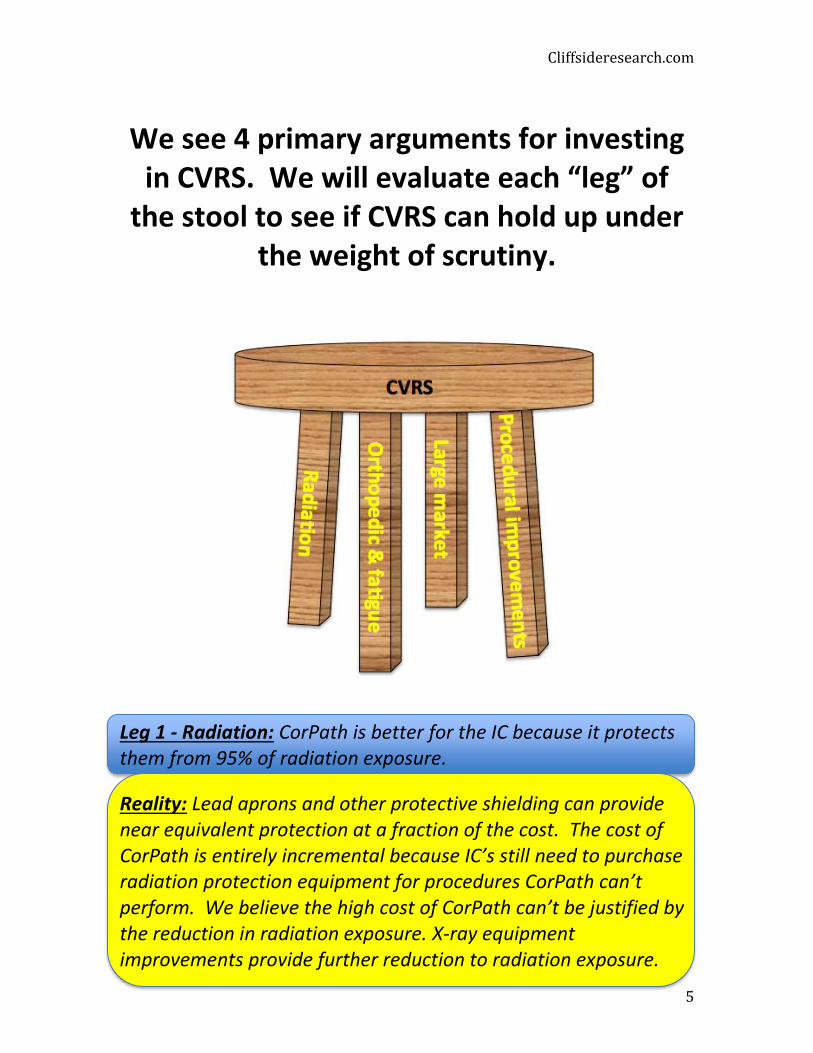

We see 4 primary arguments for investing in CVRS. We will evaluate each “leg” of

the stool to see if CVRS can hold up under the weight of scrutiny.

Leg 1 - Radiation: CorPath is better for the IC because it protects them from 95% of radiation exposure.

Reality: Lead aprons and other protective shielding can provide near equivalent protection at a fraction of the cost. The cost of CorPath is entirely incremental because IC’s still need to purchase radiation protection equipment for procedures CorPath can’t perform. We believe the high cost of CorPath can’t be justified by the reduction in radiation exposure. X-ray equipment improvements provide further reduction to radiation exposure.

6

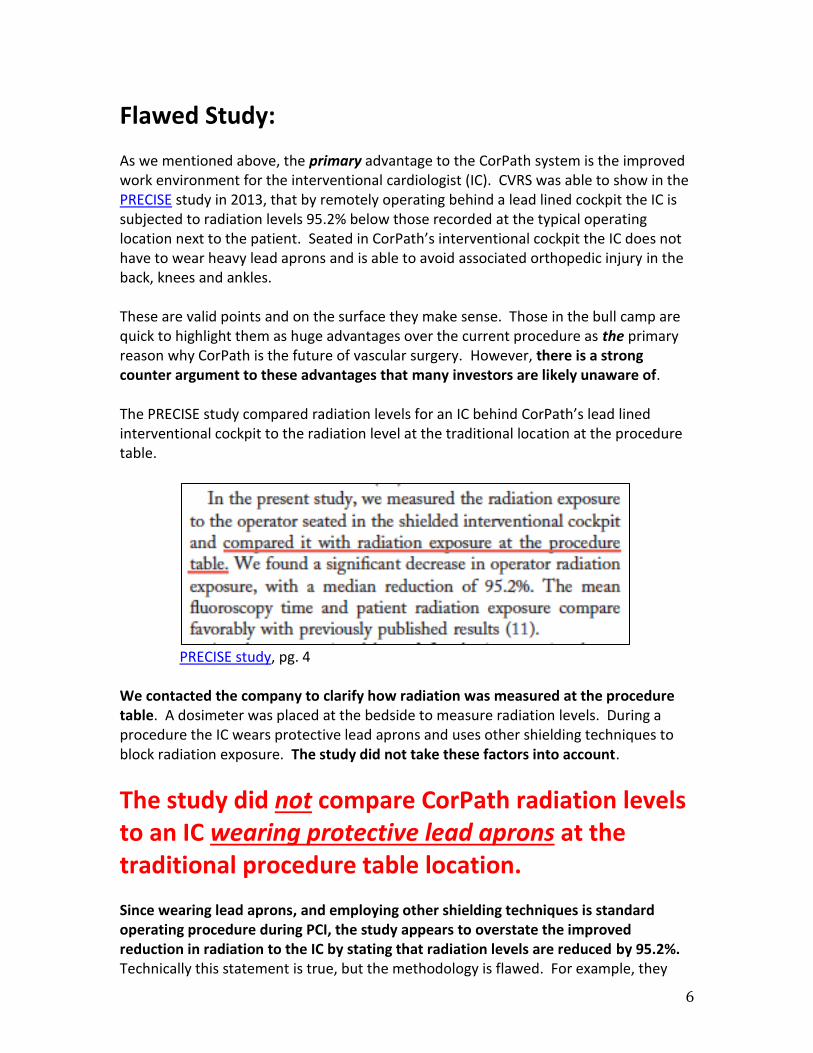

Flawed Study: As we mentioned above, the primary advantage to the CorPath system is the improved work environment for the interventional cardiologist (IC). CVRS was able to show in the PRECISE study in 2013, that by remotely operating behind a lead lined cockpit the IC is subjected to radiation levels 95.2% below those recorded at the typical operating location next to the patient. Seated in CorPath’s interventional cockpit the IC does not have to wear heavy lead aprons and is able to avoid associated orthopedic injury in the back, knees and ankles. These are valid points and on the surface they make sense. Those in the bull camp are quick to highlight them as huge advantages over the current procedure as the primary reason why CorPath is the future of vascular surgery. However, there is a strong counter argument to these advantages that many investors are likely unaware of. The PRECISE study compared radiation levels for an IC behind CorPath’s lead lined interventional cockpit to the radiation level at the traditional location at the procedure table.

PRECISE study, pg. 4

We contacted the company to clarify how radiation was measured at the procedure table. A dosimeter was placed at the bedside to measure radiation levels. During a procedure the IC wears protective lead aprons and uses other shielding techniques to block radiation exposure. The study did not take these factors into account.

The study did not compare CorPath radiation levels to an IC wearing protective lead aprons at the traditional procedure table location. Since wearing lead aprons, and employing other shielding techniques is standard operating procedure during PCI, the study appears to overstate the improved reduction in radiation to the IC by stating that radiation levels are reduced by 95.2%. Technically this statement is true, but the methodology is flawed. For example, they

Cliffsideresearch.com

7

also could have compared the radiation levels at the procedure table to the levels experienced by the operator while eating lunch in the hospital cafeteria and they should have similar, if not better results.

The question that the PRECISE study should have asked is, “How much does CorPath reduce radiation dosage to the IC in comparison to manual procedures using lead aprons and protective shielding techniques?”

Remember, this is one of the biggest selling points for CorPath.

The answer to that question is basically 0%. The two methods block roughly an equivalent amount of radiation.

8

Source: SCAI; Charles E. Chambers, MD, Kenneth A. Fetterly,PhD, Ralf Holzer,MD, Pei-Jan Paul Lin,PhD, James C. Blankenship,MD, Stephen Balter,PhD, and Warren K. Laskey,MD

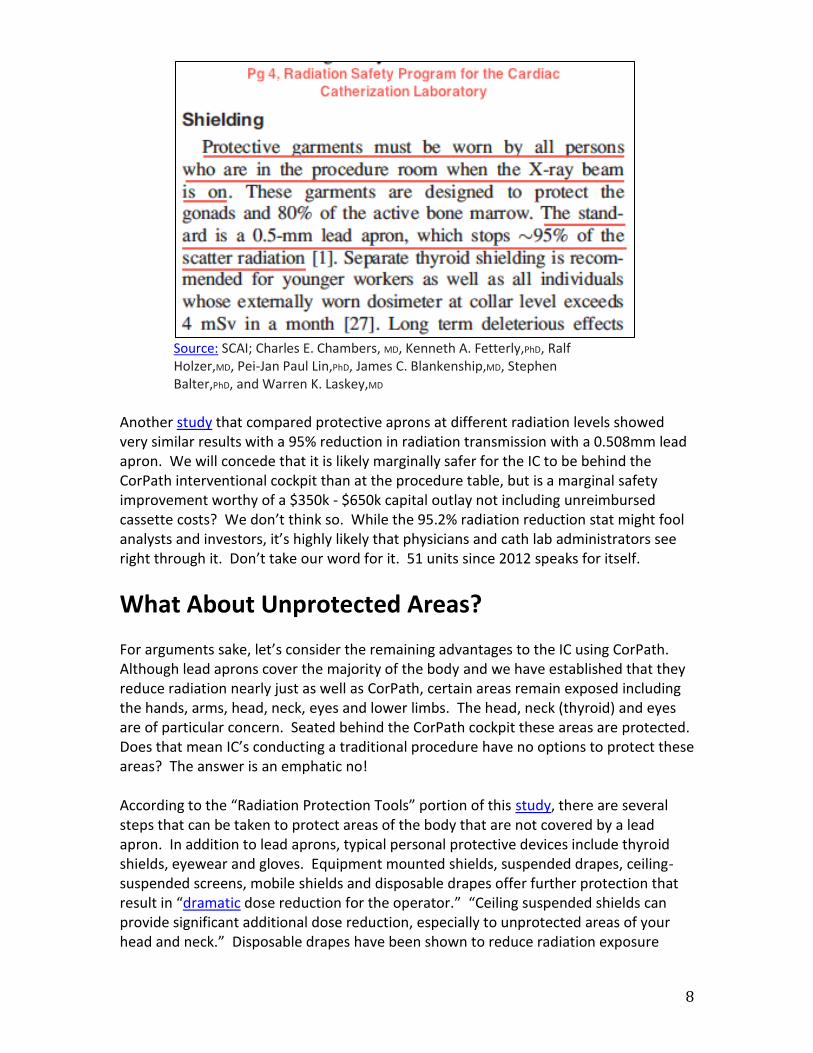

Another study that compared protective aprons at different radiation levels showed very similar results with a 95% reduction in radiation transmission with a 0.508mm lead apron. We will concede that it is likely marginally safer for the IC to be behind the CorPath interventional cockpit than at the procedure table, but is a marginal safety improvement worthy of a $350k - $650k capital outlay not including unreimbursed cassette costs? We don’t think so. While the 95.2% radiation reduction stat might fool analysts and investors, it’s highly likely that physicians and cath lab administrators see right through it. Don’t take our word for it. 51 units since 2012 speaks for itself.

What About Unprotected Areas? For arguments sake, let’s consider the remaining advantages to the IC using CorPath. Although lead aprons cover the majority of the body and we have established that they reduce radiation nearly just as well as CorPath, certain areas remain exposed including the hands, arms, head, neck, eyes and lower limbs. The head, neck (thyroid) and eyes are of particular concern. Seated behind the CorPath cockpit these areas are protected. Does that mean IC’s conducting a traditional procedure have no options to protect these areas? The answer is an emphatic no! According to the “Radiation Protection Tools” portion of this study, there are several steps that can be taken to protect areas of the body that are not covered by a lead apron. In addition to lead aprons, typical personal protective devices include thyroid shields, eyewear and gloves. Equipment mounted shields, suspended drapes, ceiling-suspended screens, mobile shields and disposable drapes offer further protection that result in “dramatic dose reduction for the operator.” “Ceiling suspended shields can provide significant additional dose reduction, especially to unprotected areas of your head and neck.” Disposable drapes have been shown to reduce radiation exposure

Cliffsideresearch.com

9

substantially “with reported reductions of 12-fold for the eyes, 26-fold for the thyroid and 29-fold for the hands.” There’s also a product for head protection called the No Brainer. The No Brainer is a light, lead free cap made of radiation blocking bismuth and barium that blocks up to 95% of radiation exposure to the brain. The cap weighs 100 grams, or approximately 1/10th the weight of a lead cap. In a study that utilized a lead drape over the patient and a No Brainer cap for patients undergoing PCI, radiation exposure to the IC was reduced by over 70% compared to usual care. The studies lead investigator, Sanjit S. Jolly, MD, MSc noted that the cost of the lead drape and No Brainer “is actually quite small.” He noted that most IC’s use each cap for months at a time before throwing them away. “Wearing a lead cap that weighs a kilogram is very cumbersome, whereas you barely notice a cap that weighs 100 grams,” he said. There are plenty of protective devices and gear that offer substantial protection to the IC and staff at a fraction of the cost of a CorPath.

RADPAD No Brainer cap

It is also important to understand PCI is only one way in which IC’s are exposed to radiation. They still need this additional protective equipment for diagnostic angiograms, other more complex procedures, or in the event of a CorPath failure that forces them to complete the procedure manually. Even when everything goes as planned with CorPath, the IC must place the catheter into the patient manually at the beginning of the procedure exposing them to typical procedure radiation.

CorPath does not eliminate the need to purchase protective gear for the IC and staff, which means the cost of CorPath and the cassettes is entirely incremental.

10

X-Ray Equipment Improvements: At the same time that radiation protection equipment is improving, the x-ray equipment that is the source of the radiation is also being improved to reduce the amount of radiation required for interventional procedures. Philips, a market leader in interventional cardiology imagery, claims that their new AlluraClarity x-ray equipment reduces radiation by up to 50% for therapeutic interventions. The FDA approved AlluraClarity in 2013. This also happens to be the last year that Philips was the exclusive worldwide distributor of CorPath. Siemens, Toshiba and GE are also keenly focused on radiation dose reduction as procedure complexity is leading to increased fluoroscopy time. In many cases these are the same complex procedures that CorPath cannot conduct. If a hospital is looking to reduce radiation exposure, we believe administrators are far more likely to consider capital outlays for new, low dose x-ray equipment. After all, it is the x-ray equipment that is the very source of the radiation and the equipment can be used across a broad range of procedures, including complex procedures that CorPath cannot.

Leg 2 - Orthopedic & fatigue: CorPath is better for the IC because it protects them from orthopedic injury. Stationed safely behind the cockpit, the IC can conduct PCI procedures with reduced fatigue.

Reality: Innovative lead-free protective garments can reduce the weight of traditional lead aprons by 40%. Mobile weightless suspended curtains can also be utilized that provide increased protection and in our opinion virtually eliminate the orthopedic advantages of CorPath at a fraction of the cost.

Lighter Equipment: The other primary advantage to CorPath is that the IC doesn’t have to wear heavy lead aprons. Again, from this study in the “Personal Protective Devices” section we find that, “because of the ergonomic hazards of personal protective devices (particularly lead aprons), attempts to reduce the fatigue and injury associated with wearing heavy protective apparel have been made.” We found several alternatives to pure lead aprons including lead hybrids and lead-free options that offer near equivalent protection at up to a 40% reduction to the weight of traditional lead aprons. Although CorPath does relieve the IC from the weight of heavy lead aprons, that advantage is substantially diminished with lighter equipment.

Cliffsideresearch.com

11

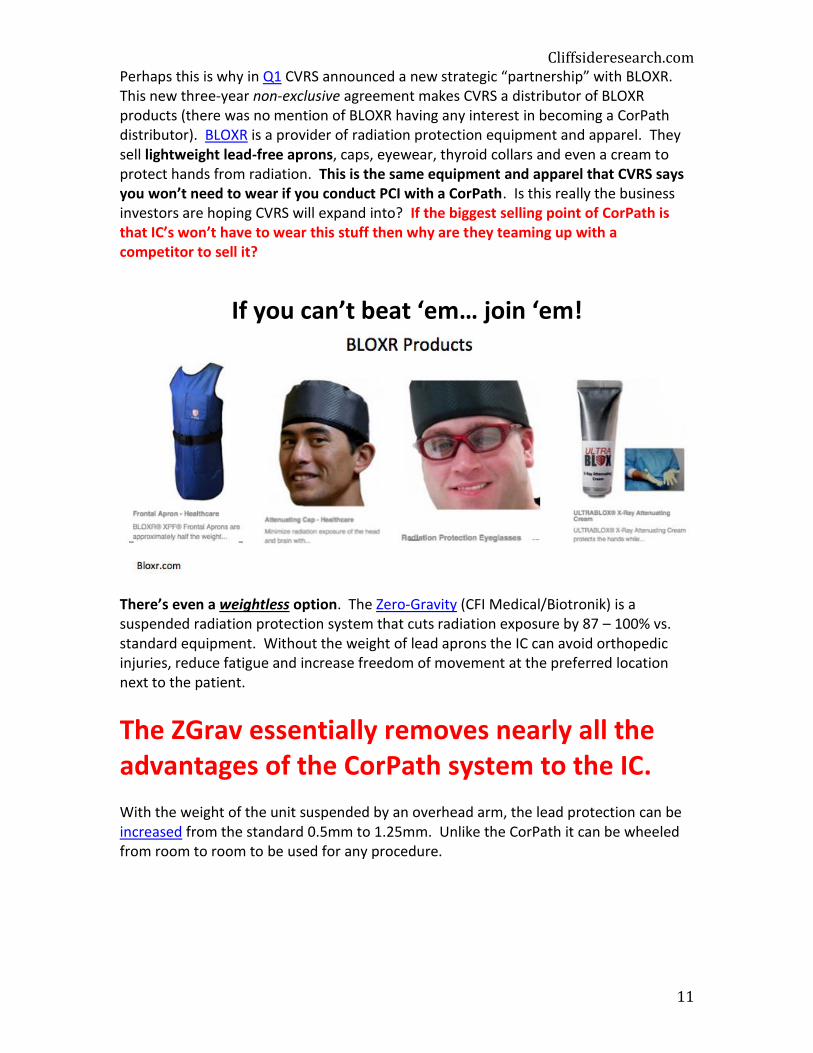

Perhaps this is why in Q1 CVRS announced a new strategic “partnership” with BLOXR. This new three-year non-exclusive agreement makes CVRS a distributor of BLOXR products (there was no mention of BLOXR having any interest in becoming a CorPath distributor). BLOXR is a provider of radiation protection equipment and apparel. They sell lightweight lead-free aprons, caps, eyewear, thyroid collars and even a cream to protect hands from radiation. This is the same equipment and apparel that CVRS says you won’t need to wear if you conduct PCI with a CorPath. Is this really the business investors are hoping CVRS will expand into? If the biggest selling point of CorPath is that IC’s won’t have to wear this stuff then why are they teaming up with a competitor to sell it?

If you can’t beat ‘em… join ‘em!

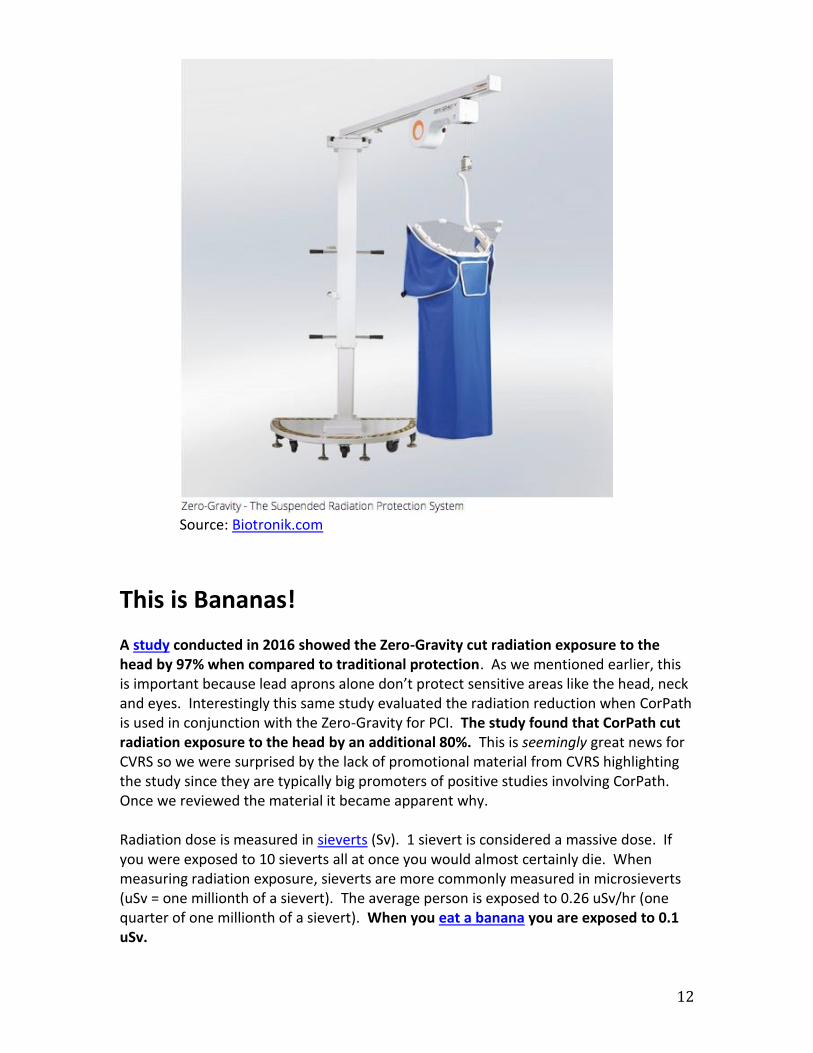

There’s even a weightless option. The Zero-Gravity (CFI Medical/Biotronik) is a suspended radiation protection system that cuts radiation exposure by 87 – 100% vs. standard equipment. Without the weight of lead aprons the IC can avoid orthopedic injuries, reduce fatigue and increase freedom of movement at the preferred location next to the patient.

The ZGrav essentially removes nearly all the advantages of the CorPath system to the IC. With the weight of the unit suspended by an overhead arm, the lead protection can be increased from the standard 0.5mm to 1.25mm. Unlike the CorPath it can be wheeled from room to room to be used for any procedure.

12

Source: Biotronik.com

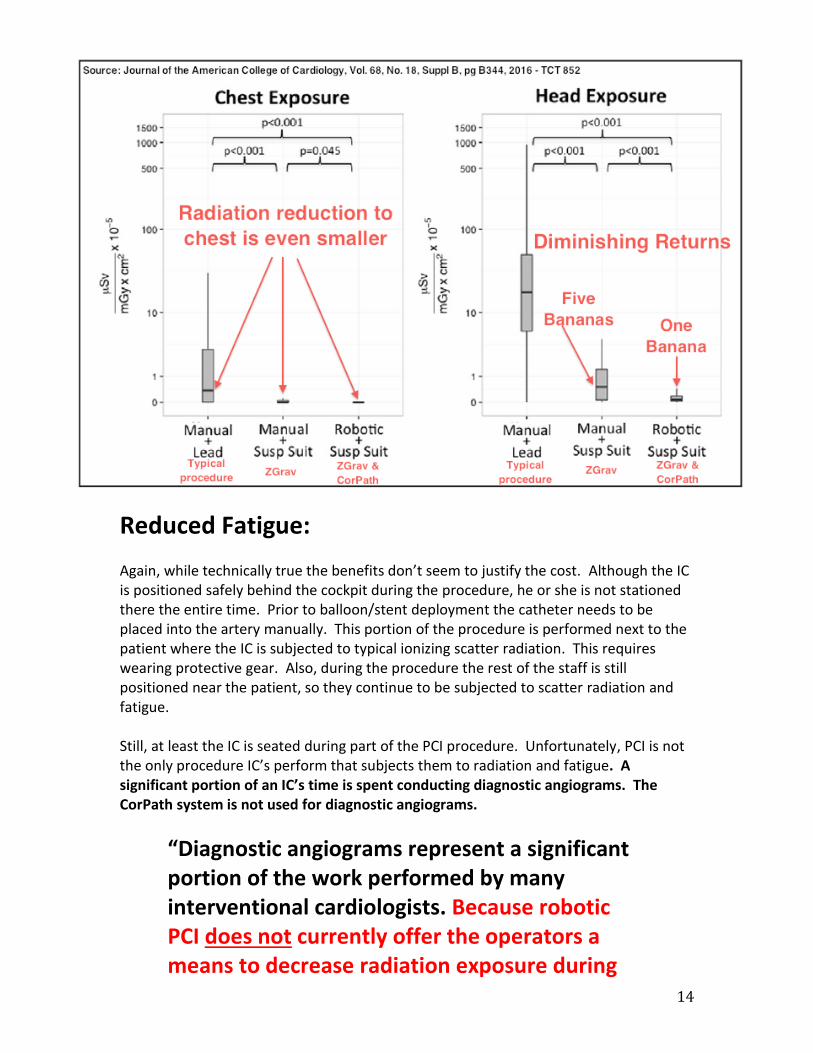

This is Bananas! A study conducted in 2016 showed the Zero-Gravity cut radiation exposure to the head by 97% when compared to traditional protection. As we mentioned earlier, this is important because lead aprons alone don’t protect sensitive areas like the head, neck and eyes. Interestingly this same study evaluated the radiation reduction when CorPath is used in conjunction with the Zero-Gravity for PCI. The study found that CorPath cut radiation exposure to the head by an additional 80%. This is seemingly great news for CVRS so we were surprised by the lack of promotional material from CVRS highlighting the study since they are typically big promoters of positive studies involving CorPath. Once we reviewed the material it became apparent why. Radiation dose is measured in sieverts (Sv). 1 sievert is considered a massive dose. If you were exposed to 10 sieverts all at once you would almost certainly die. When measuring radiation exposure, sieverts are more commonly measured in microsieverts (uSv = one millionth of a sievert). The average person is exposed to 0.26 uSv/hr (one quarter of one millionth of a sievert). When you eat a banana you are exposed to 0.1 uSv.

Cliffsideresearch.com

13

The study found that manual PCI with traditional lead protection exposes the head to 14.9 uSv per procedure. Radiation exposure to the head of IC’s using the Zero-Gravity was 0.5 uSv per PCI procedure. Radiation exposure to the head of IC’s using the Zero-Gravity in conjunction with CorPath was reduced by an additional 80%...to 0.1 uSv.

Another way of saying this is that CorPath reduced radiation exposure to the head by

4 bananas!

CorPath’s radiation reduction to the chest, which is typically covered by lead aprons, was also evaluated and the improvements were even smaller. What we have here is a case of diminishing returns where the incremental radiation reduction benefit of CorPath cannot be justified by its price tag. Lead investigator of the study Andrew LaCombe summed it up best by stating that, “given the large reductions in cranial radiation exposure with the suspended lead curtain (Zero-Gravity), some might question why the robotic system would even be needed, especially given the cost and learning curve.” A Zero-Gravity costs about $75 - $85k or approximately 80% less than the cost of the CorPath. Now that’s a lot of bananas!

14

Reduced Fatigue: Again, while technically true the benefits don’t seem to justify the cost. Although the IC is positioned safely behind the cockpit during the procedure, he or she is not stationed there the entire time. Prior to balloon/stent deployment the catheter needs to be placed into the artery manually. This portion of the procedure is performed next to the patient where the IC is subjected to typical ionizing scatter radiation. This requires wearing protective gear. Also, during the procedure the rest of the staff is still positioned near the patient, so they continue to be subjected to scatter radiation and fatigue. Still, at least the IC is seated during part of the PCI procedure. Unfortunately, PCI is not the only procedure IC’s perform that subjects them to radiation and fatigue. A significant portion of an IC’s time is spent conducting diagnostic angiograms. The CorPath system is not used for diagnostic angiograms.

“Diagnostic angiograms represent a significant portion of the work performed by many interventional cardiologists. Because robotic PCI does not currently offer the operators a means to decrease radiation exposure during

Cliffsideresearch.com

15

diagnostic catheterizations, scattered radiation risks will remain a problem, even at centers where robotic PCI is available.”

~Journal of the American Heart Association IC’s also perform other procedures like atherectomy and percutaneous mitral valve repair that also subjects the physician to radiation and fatigue. The CorPath is not approved to perform these procedures.

Leg 3 - Procedural improvements: CorPath improves PCI because of the increased control of the guidewire, precise placement of the balloon/stent and improved stent selection in comparison to the manual method. It’s easy to learn and IC’s conduct faster PCI’s after only 3 cases.

Reality: The jury is out. On the subject of improved efficacy, clinical data is lacking. At best CorPath has shown equivalent efficacy to manual PCI for fairly simple coronary lesions. The truth is CorPath is incapable of completing PCI in many complex cases. We find CorPath improves PCI in some ways and makes it worse in other ways. For example, when using CorPath the IC lacks haptic feedback. In some cases procedure times have been extended.

Simple vs. Complex PCI: CVRS lacks compelling clinical study evidence of improvement in CorPath patient outcomes versus traditional manual PCI patient outcomes. No randomized trials have been completed for either CorPath 200 or GRX. Most of the data that has been presented showing equivalent outcomes to manual PCI has been from highly selected patients with fairly simple coronary lesions. CVRS has not been able to show improved efficacy based on enhanced guidewire dexterity or stent placement. While there is some evidence that CorPath enhances stent selection over visual methods, in our view this alone is not compelling enough to justify the system cost and additional disposable costs. Growth in PCI procedures is primarily in the form of complex (type C) lesions due to an aging population, equipment & technique improvements, and a decrease in inappropriate PCI. Inappropriate PCI associated with stable coronary artery disease is

16

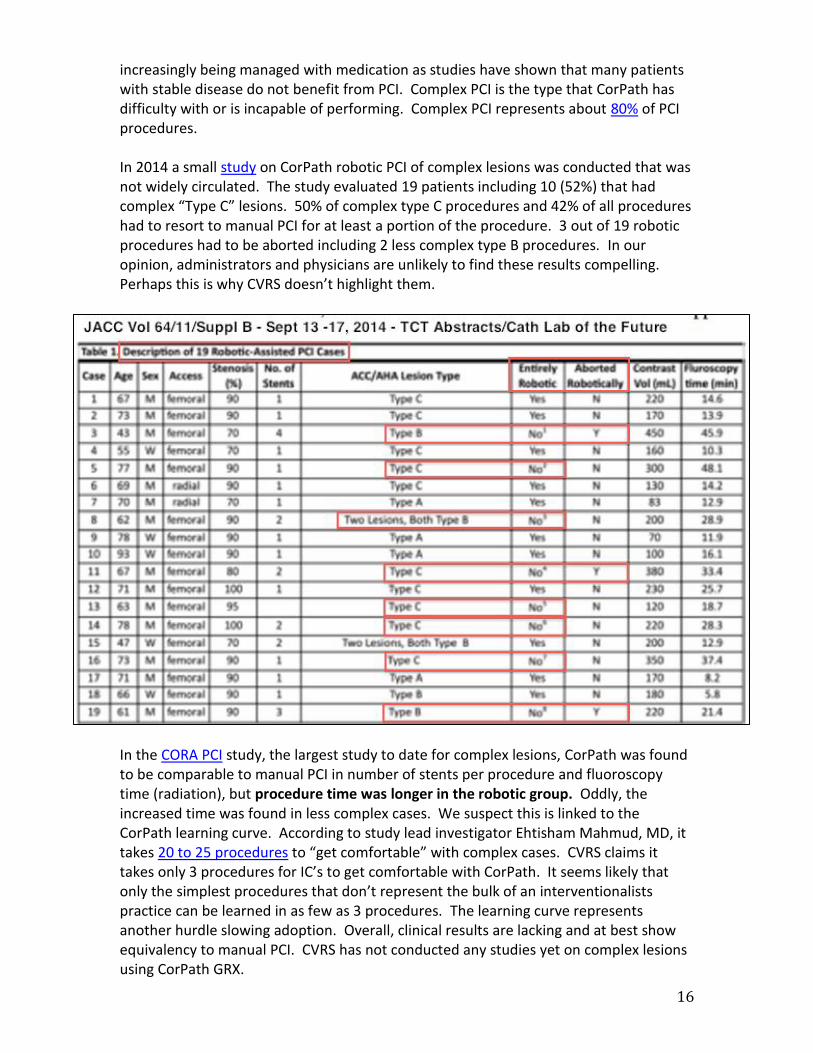

increasingly being managed with medication as studies have shown that many patients with stable disease do not benefit from PCI. Complex PCI is the type that CorPath has difficulty with or is incapable of performing. Complex PCI represents about 80% of PCI procedures. In 2014 a small study on CorPath robotic PCI of complex lesions was conducted that was not widely circulated. The study evaluated 19 patients including 10 (52%) that had complex “Type C” lesions. 50% of complex type C procedures and 42% of all procedures had to resort to manual PCI for at least a portion of the procedure. 3 out of 19 robotic procedures had to be aborted including 2 less complex type B procedures. In our opinion, administrators and physicians are unlikely to find these results compelling. Perhaps this is why CVRS doesn’t highlight them.

In the CORA PCI study, the largest study to date for complex lesions, CorPath was found to be comparable to manual PCI in number of stents per procedure and fluoroscopy time (radiation), but procedure time was longer in the robotic group. Oddly, the increased time was found in less complex cases. We suspect this is linked to the CorPath learning curve. According to study lead investigator Ehtisham Mahmud, MD, it takes 20 to 25 procedures to “get comfortable” with complex cases. CVRS claims it takes only 3 procedures for IC’s to get comfortable with CorPath. It seems likely that only the simplest procedures that don’t represent the bulk of an interventionalists practice can be learned in as few as 3 procedures. The learning curve represents another hurdle slowing adoption. Overall, clinical results are lacking and at best show equivalency to manual PCI. CVRS has not conducted any studies yet on complex lesions using CorPath GRX.

Cliffsideresearch.com

17

“Looking at the bulk of the evidence, it appears the benefits of robotic PCI are mostly for the physician, with some spill over to the rest of the cath lab staff and hints, but not waves, of benefit for patients themselves.”

~American College of Cardiology, August 3rd, 2017

Do You Feel Me? CorPath does not provide haptic feedback. Haptic feedback is a combination of force and tactile feedback that IC’s rely on particularly in more complex PCI procedures like chronic total occlusion (CTO). With CorPath, when a guidewire meets resistance the IC has no tactile sense to guide him. Without haptic feedback the IC risks complications like vessel perforation. According to a review of robotic PCI by the Journal of the American Heart Association, haptic feedback is important to IC’s during PCI.

“Although the PRECISE registry reported procedural success of 98%, many interventionalists feel that tactile sensation of wires and catheters is important for procedural success in challenging cases.”

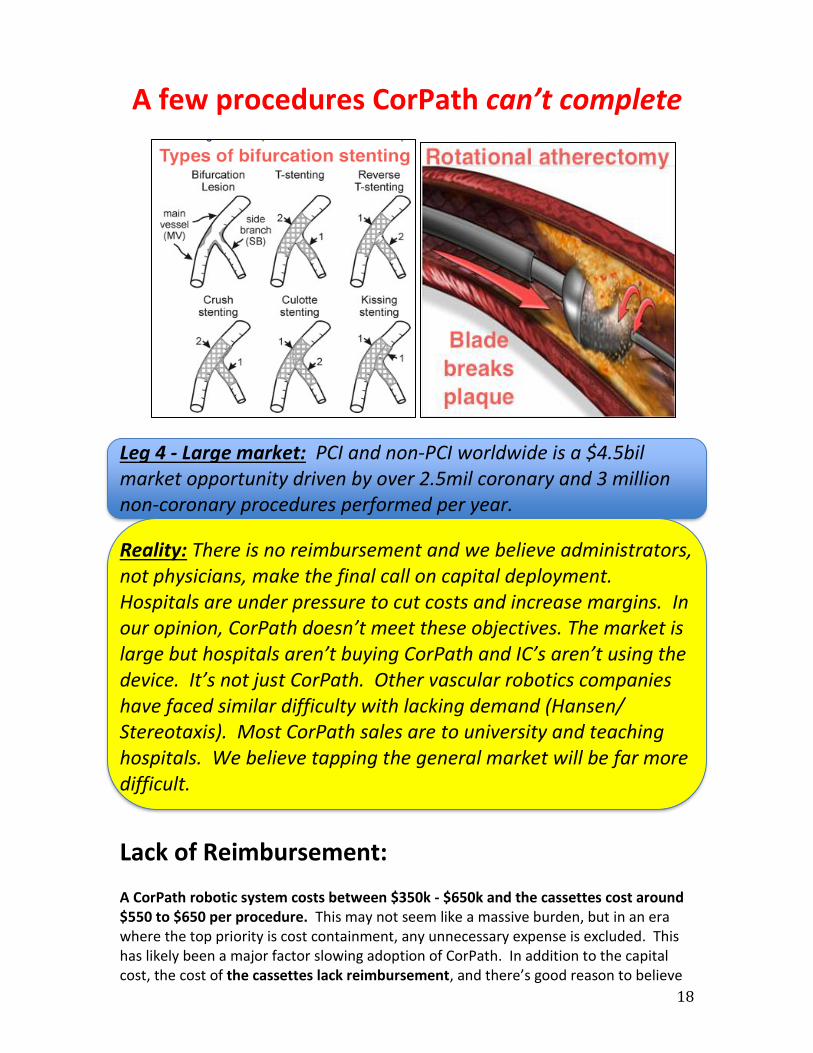

~American Heart Association In addition to lack of haptic feedback, the Journal of the American Heart Association review highlights several other shortcomings that will be difficult for CorPath GRX to overcome. CorPath does not support over-the-wire coronary interventions like microcatheters for CTO, and aspiration devices used during heart attacks. CorPath cannot complete rotational atherectomy for calcified lesions or bifurcation stenting with a two-stent approach without resorting to traditional manual techniques. In these cases IC’s must revert to the manual approach to complete a major portion of complex PCI cases that are becoming more common. CorPath has only been validated using a 0.014-inch guidewire and rapid balloon and stent systems. CorPath’s incompatibility with 0.018 and 0.035 guidewires, over-the-wire balloon catheters, drug-coated balloons, and intravascular imaging catheters represent other hurdles to increased adoption. In the end, CorPath’s limited utility simply doesn’t justify the additional cost in our opinion.

18

A few procedures CorPath can’t complete

Leg 4 - Large market: PCI and non-PCI worldwide is a $4.5bil market opportunity driven by over 2.5mil coronary and 3 million non-coronary procedures performed per year.

Reality: There is no reimbursement and we believe administrators, not physicians, make the final call on capital deployment. Hospitals are under pressure to cut costs and increase margins. In our opinion, CorPath doesn’t meet these objectives. The market is large but hospitals aren’t buying CorPath and IC’s aren’t using the device. It’s not just CorPath. Other vascular robotics companies have faced similar difficulty with lacking demand (Hansen/ Stereotaxis). Most CorPath sales are to university and teaching hospitals. We believe tapping the general market will be far more difficult.

Lack of Reimbursement: A CorPath robotic system costs between $350k - $650k and the cassettes cost around $550 to $650 per procedure. This may not seem like a massive burden, but in an era where the top priority is cost containment, any unnecessary expense is excluded. This has likely been a major factor slowing adoption of CorPath. In addition to the capital cost, the cost of the cassettes lack reimbursement, and there’s good reason to believe

Cliffsideresearch.com

19

it may never be reimbursed according to Lloyd W. Klein, MD, professor of medicine at Rush Medical College in Chicago.

“I don’t think [the cassettes] will ever be reimbursed. Third-party payors are trying not to pay for what we are doing now, let alone for additional costs. I don’t see it happening. They would demand proof of better efficacy and more safety, and that’s not very likely, at least not right away. You’re talking about a procedure that is keeping a number of hospitals afloat. So administrators are watching profit margin of these procedures and the idea that you are going to cut into profit margin for disposables and you need a large capital outlay would be a very tough sell for most hospitals in the country right now.”

~Lloyd W. Klein, MD Under the fee-for-service model that dominates reimbursement today, physicians are reimbursed based on a fee schedule for any identifiable procedure. But third-party payors (Medicare/Medicaid/insurers) are moving away from the fee-for-service model because it increases unnecessary testing and procedures leading to spiraling healthcare costs. Today, payors and regulators are pushing providers (hospitals, etc.) to increase value-based (fee-for-value) service where reimbursement is based on the quality of patient outcomes as an alternative to fee-for-service. In a value-based system reimbursement payment risk is pushed to the provider (cath lab) and cost containment becomes paramount. Administrators, not physicians, decide where to allocate capital. In an era that is increasingly focused on cutting costs and improving patient outcomes, administrators are highly sensitive to unnecessary capital expense. Since healthcare costs and the pressure to move to a value-based reimbursement model will only increase, hospital administrators will continue to look to contain unnecessary costs like CorPath.

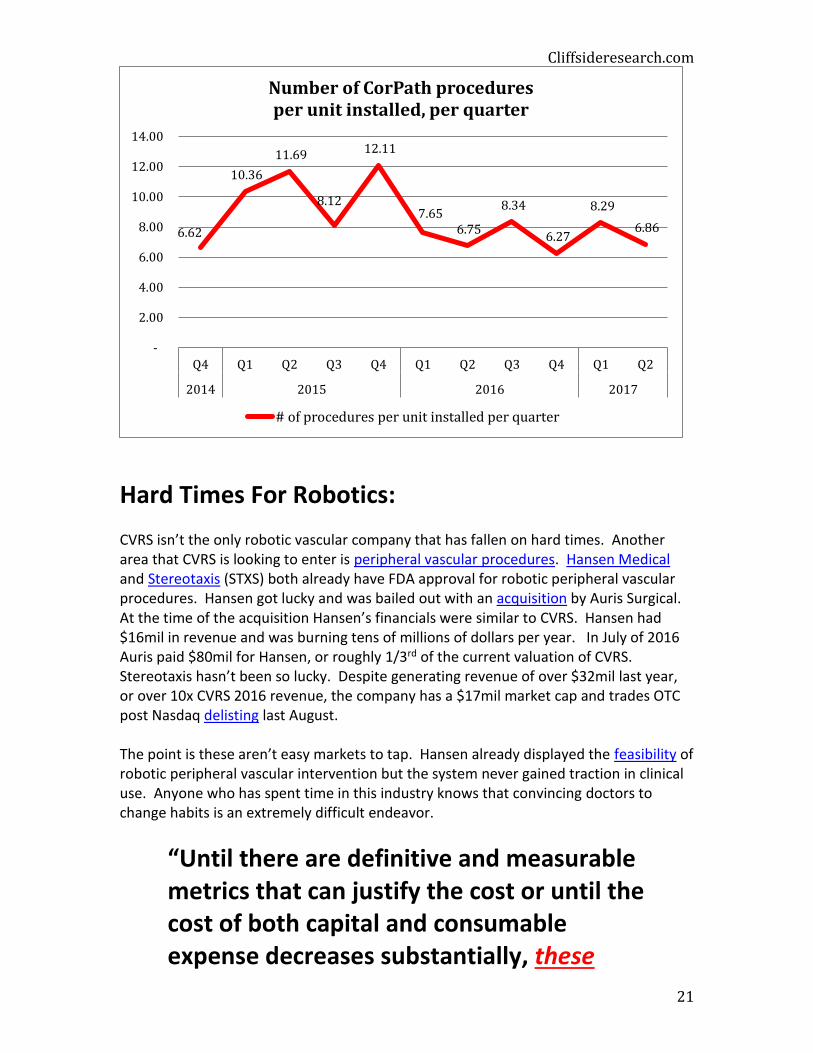

IC’s Aren’t Using It: Since 2012 CVRS has only installed 51 units including the new CorPath GRX. Each time an IC conducts a PCI procedure they must use a new cassette. The more procedures completed, the more cassettes are required. As the install base grows and more physicians are trained to use the device with increasing confidence we would expect the number of procedures per unit to grow meaningfully. But that’s not what is happening. As you can see below, despite the (slow) growth of the install base, the utilization of CorPath is declining. In the most recent quarter cassette revenue per installed units was only $3,431. If we annualize the recent quarter’s results this equates to only $13,724 per year. With cash burn of just over $28mil for the past two years it will be a very long time before CVRS is able to breakeven without massive adoption of the CorPath system and increased utilization.

20

Cassettes typically cost $550 to $650 per procedure. To be conservative we’ll assume the cost per procedure is $500 per cassette. Based on that assumption we calculated the number of CorPath PCI procedures per installed units per quarter. The data again reveals that utilization is on the decline and in the most recent quarter IC’s conducted fewer than 7 procedures per unit per quarter, or roughly two procedures per month per unit. If we assumed a higher price per cassette the results would have been even worse. According to Stifel, the typical US cath lab conducts 24.1 PCI procedures per month. If even the hospitals that install the device aren’t using them, how can new customers justify paying upwards of a half a million dollars for one?

IC’s are only conducting roughly two procedures per month using CorPath!

2628

3234

3840 40 41

4548

51

$3.31

$5.18

$5.84

$4.06

$6.05

$3.83

$3.38

$4.17

$3.13

$4.15

$3.43

0

10

20

30

40

50

60

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2014 2015 2016 2017

$-

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

CorPath install base slowly increases, but utilization decreases

Total install base Cassette revenue (000) per unit installed

Cliffsideresearch.com

21

Hard Times For Robotics: CVRS isn’t the only robotic vascular company that has fallen on hard times. Another area that CVRS is looking to enter is peripheral vascular procedures. Hansen Medical and Stereotaxis (STXS) both already have FDA approval for robotic peripheral vascular procedures. Hansen got lucky and was bailed out with an acquisition by Auris Surgical. At the time of the acquisition Hansen’s financials were similar to CVRS. Hansen had $16mil in revenue and was burning tens of millions of dollars per year. In July of 2016 Auris paid $80mil for Hansen, or roughly 1/3rd of the current valuation of CVRS. Stereotaxis hasn’t been so lucky. Despite generating revenue of over $32mil last year, or over 10x CVRS 2016 revenue, the company has a $17mil market cap and trades OTC post Nasdaq delisting last August. The point is these aren’t easy markets to tap. Hansen already displayed the feasibility of robotic peripheral vascular intervention but the system never gained traction in clinical use. Anyone who has spent time in this industry knows that convincing doctors to change habits is an extremely difficult endeavor.

“Until there are definitive and measurable metrics that can justify the cost or until the cost of both capital and consumable expense decreases substantially, these

6.62

10.36

11.69

8.12

12.11

7.65 6.75

8.34

6.27

8.29

6.86

-

2.00

4.00

6.00

8.00

10.00

12.00

14.00

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2014 2015 2016 2017

Number of CorPath proceduresper unit installed, per quarter

# of procedures per unit installed per quarter

22

solutions will remain of interest mostly to high-end university and teaching institutions rather than a mainstream solution for all healthcare providers.”

~Tom Watson, MD Buyline

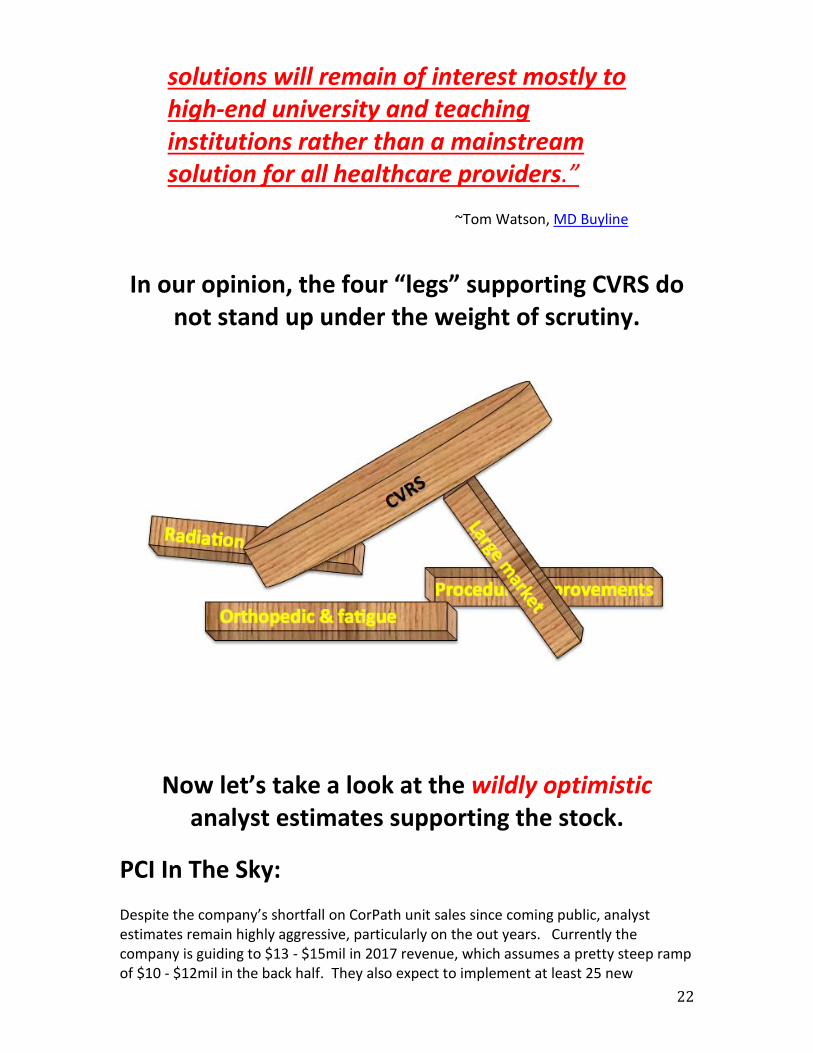

In our opinion, the four “legs” supporting CVRS do not stand up under the weight of scrutiny.

Now let’s take a look at the wildly optimistic analyst estimates supporting the stock.

PCI In The Sky: Despite the company’s shortfall on CorPath unit sales since coming public, analyst estimates remain highly aggressive, particularly on the out years. Currently the company is guiding to $13 - $15mil in 2017 revenue, which assumes a pretty steep ramp of $10 - $12mil in the back half. They also expect to implement at least 25 new

Cliffsideresearch.com

23

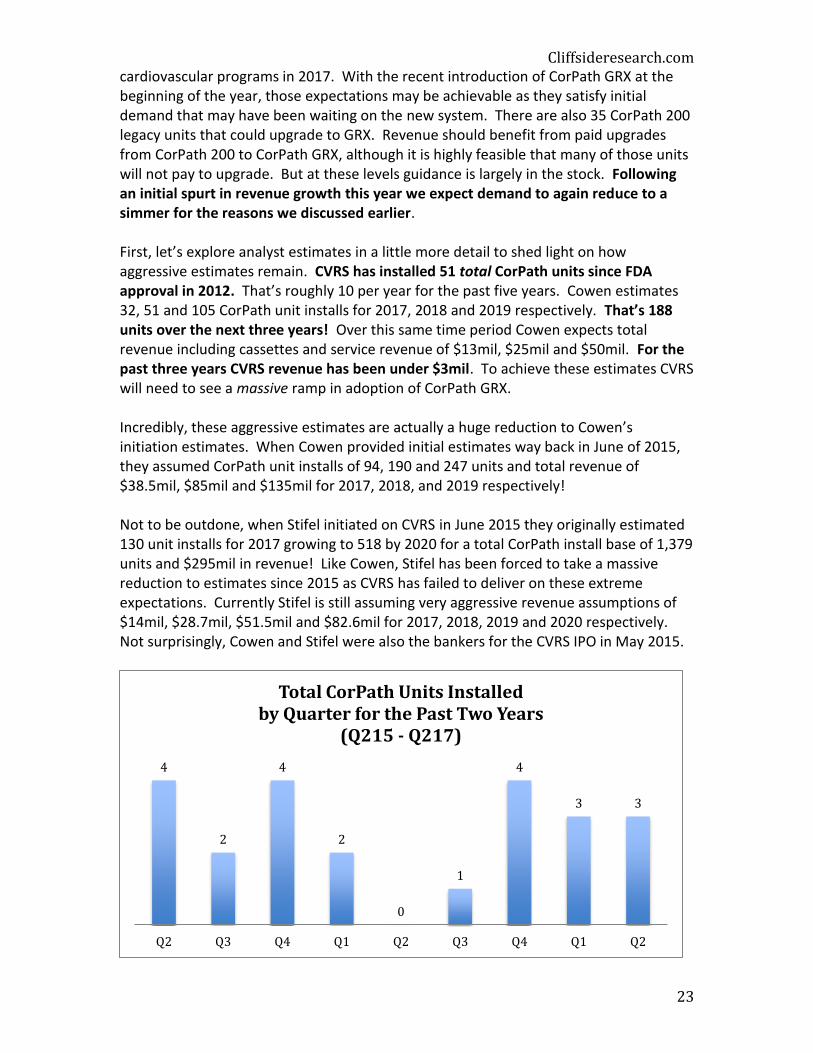

cardiovascular programs in 2017. With the recent introduction of CorPath GRX at the beginning of the year, those expectations may be achievable as they satisfy initial demand that may have been waiting on the new system. There are also 35 CorPath 200 legacy units that could upgrade to GRX. Revenue should benefit from paid upgrades from CorPath 200 to CorPath GRX, although it is highly feasible that many of those units will not pay to upgrade. But at these levels guidance is largely in the stock. Following an initial spurt in revenue growth this year we expect demand to again reduce to a simmer for the reasons we discussed earlier. First, let’s explore analyst estimates in a little more detail to shed light on how aggressive estimates remain. CVRS has installed 51 total CorPath units since FDA approval in 2012. That’s roughly 10 per year for the past five years. Cowen estimates 32, 51 and 105 CorPath unit installs for 2017, 2018 and 2019 respectively. That’s 188 units over the next three years! Over this same time period Cowen expects total revenue including cassettes and service revenue of $13mil, $25mil and $50mil. For the past three years CVRS revenue has been under $3mil. To achieve these estimates CVRS will need to see a massive ramp in adoption of CorPath GRX. Incredibly, these aggressive estimates are actually a huge reduction to Cowen’s initiation estimates. When Cowen provided initial estimates way back in June of 2015, they assumed CorPath unit installs of 94, 190 and 247 units and total revenue of $38.5mil, $85mil and $135mil for 2017, 2018, and 2019 respectively! Not to be outdone, when Stifel initiated on CVRS in June 2015 they originally estimated 130 unit installs for 2017 growing to 518 by 2020 for a total CorPath install base of 1,379 units and $295mil in revenue! Like Cowen, Stifel has been forced to take a massive reduction to estimates since 2015 as CVRS has failed to deliver on these extreme expectations. Currently Stifel is still assuming very aggressive revenue assumptions of $14mil, $28.7mil, $51.5mil and $82.6mil for 2017, 2018, 2019 and 2020 respectively. Not surprisingly, Cowen and Stifel were also the bankers for the CVRS IPO in May 2015.

4

2

4

2

0

1

4

3 3

Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

Total CorPath Units Installed by Quarter for the Past Two Years

(Q215 - Q217)

24

So What’s So Great About GRX Anyway? The extremely aggressive assumptions for CorPath 200 never materialized. For the bullish case currently being laid out by analysts to come true you have to believe the new upgrades to CorPath GRX are going to massively accelerate adoption. Based on a review of the upgrades, we do not believe they are enough to overcome the significant headwinds that foiled CorPath 200’s market entry. The headwinds that foiled CorPath 200’s market adoption are still in place and we feel are highly likely to continue hampering the company’s attempt to gain meaningful market share. So what are the massive improvements that are going to drive huge adoption of CorPath GRX?

• Ability to control the catheter for more complex cases (not clinically validated)

• New extended reach arm allows for positioning of radial or femoral access

• New touchscreen display on the arm streamlines workflow

• Bigger screen in the cockpit We believe the improvements are primarily marginal in nature and more significant developments in the past have not led to increased CorPath adoption. For example, historically most PCI procedures have been performed via femoral (leg) access. Increasingly PCI procedures are being conducted via radial (arm) access. Prior to October 2015 CorPath was only approved for femoral access. According to CVRS, radial access represents approximately 40% of all PCI procedures in the US and is the predominant approach abroad. That means that prior to approval, CorPath couldn’t market the radial approach representing over 40% of the PCI market.

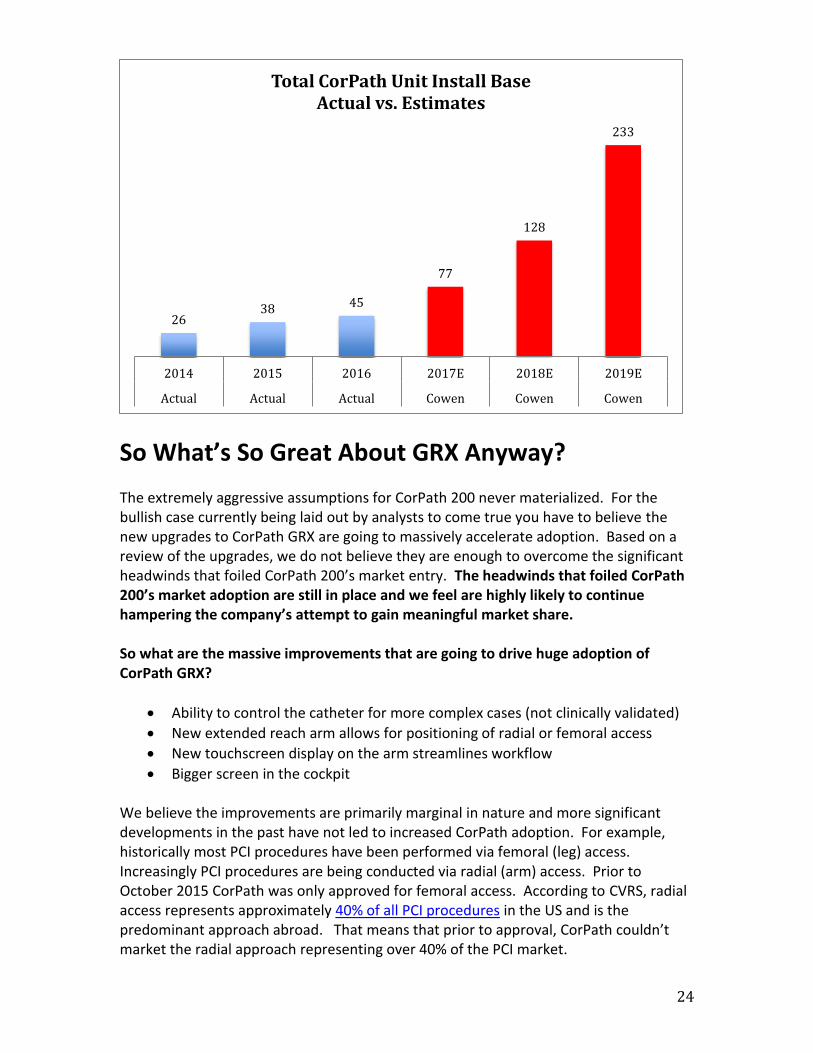

2638 45

77

128

233

2014 2015 2016 2017E 2018E 2019E

Actual Actual Actual Cowen Cowen Cowen

Total CorPath Unit Install Base Actual vs. Estimates

Cliffsideresearch.com

25

In October 2015 CVRS received CorPath FDA approval for radial access. At the time the company stated that, “the FDA’s clearance for radial access PCI with the CorPath System is a significant step in the adoption of robotic PCI.” Following radial access approval CVRS only installed 11 units over the five quarters preceding GRX approval. This was very much inline with the install pace prior to radial access approval. If increasing the addressable market by over 40% didn’t spur increased adoption, why would the marginal improvements of GRX spur it?

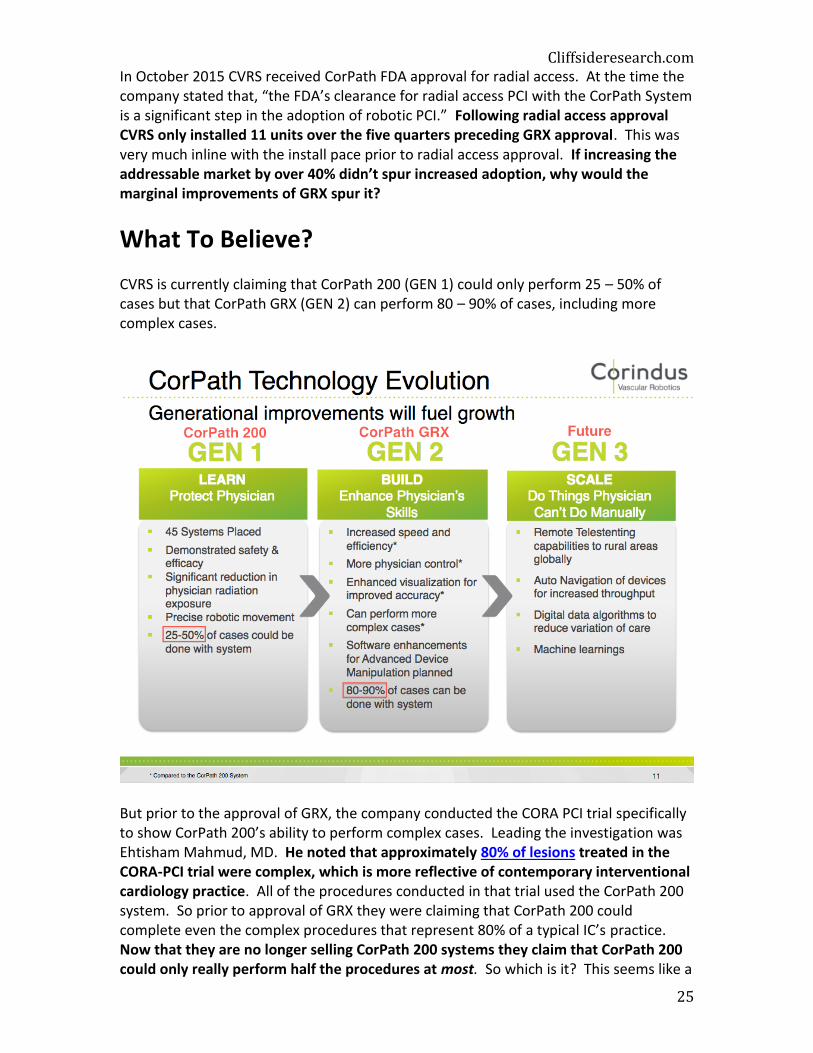

What To Believe? CVRS is currently claiming that CorPath 200 (GEN 1) could only perform 25 – 50% of cases but that CorPath GRX (GEN 2) can perform 80 – 90% of cases, including more complex cases.

But prior to the approval of GRX, the company conducted the CORA PCI trial specifically to show CorPath 200’s ability to perform complex cases. Leading the investigation was Ehtisham Mahmud, MD. He noted that approximately 80% of lesions treated in the CORA-PCI trial were complex, which is more reflective of contemporary interventional cardiology practice. All of the procedures conducted in that trial used the CorPath 200 system. So prior to approval of GRX they were claiming that CorPath 200 could complete even the complex procedures that represent 80% of a typical IC’s practice. Now that they are no longer selling CorPath 200 systems they claim that CorPath 200 could only really perform half the procedures at most. So which is it? This seems like a

26

convenient way to promote the capabilities of the new system at the expense of the old system. GRX may marginally increase the addressable market, but we find the figures above highly promotional.

Conclusion: CVRS consistently burns substantial amounts of cash, has never been profitable and has an accumulated deficit of $165mil. For the past two years the company has burned over $28mil in cash per year and is on pace to burn at least as much this year. It will likely be several years before the company is cash flow positive, if ever. Post the most recent raise in February they had $35.2mil in cash on the balance sheet. At the current burn rate the company will be out of cash around Q3 of next year. Prior to that we suspect they will once again go back to the equity well for another highly dilutive raise. Since 2015 shares outstanding have nearly doubled from 105mil to 197mil shares. Since they are burning around $30mil per year it seems reasonable to assume they will raise at least this amount on a future round. Using the past two equity raises of $46mil and $45mil respectively as a proxy, we feel it’s safe to say they’ll likely raise at least $45mil some time next year. This is a scenario the company’s bankers are likely well aware of. The bankers also understand that the lower the stock is, the more dilutive the deal will be. Goosing the stock higher to a less dilutive price would help the company. Thus there is substantial incentive for analysts to put forward highly aggressive estimates and expectations in hopes of securing a banking deal. Based on our analysis of the company and the difficulties facing CorPath GRX, we believe analyst estimates are highly speculative and should not be relied upon. While it is possible that GRX will result in an initial short-term boost to unit sales for the reasons we explained, we do not believe a temporary increase in activity will lead to a sustainable increase in adoption. Growth in PCI is primarily from complex cases. GRX still lacks certain capabilities for complex cases and has not been clinically validated for complex PCI. We argue that GRX’s incompatibility with larger guidewires, over-the-wire interventions, and lack of support for bifurcation stenting with a 2-stent approach represent significant hurdles to increased adoption. We evaluated the company’s pitch to investors and found several issues that we feel explain the extremely limited adoption of CorPath to date. Going forward the company will face most of these concerns for GRX as well. The pitch to investors essentially boils down to four main topics:

1) Reduced radiation We started with radiation reduction because we believe this is the selling point that CVRS has emphasized as the largest benefit to the IC over all others. We were able to show that CorPath does not reduce radiation exposure as much as they claim vs. conventional protective gear. In one clinical trial the radiation

Cliffsideresearch.com

27

exposure between CorPath and protective gear was so little that it equated to the difference in radiation exposure between someone eating 5 bananas versus someone eating 1 banana. Based on the lack of demand it appears that hospitals are not convinced that the additional radiation protection from CorPath justifies the cost. Conventional protective gear can be used for any procedure and costs a fraction of a $350k - $650k CorPath, which has only been validated primarily for less complex procedures.

2) Reduced orthopedic strain and fatigue Historically IC’s have worn heavy lead aprons that cause orthopedic strain and fatigue. Today IC’s have several lead hybrid and lead-free options that can reduce the weight of protective gear by up to 40%. There is even a weightless curtain called the Zero-Gravity. Importantly, the curtain also protects the IC’s head, eyes and thyroid with a transparent lead shield. Zero-Gravity essentially eliminates the lead weight related orthopedic and fatigue advantages to CorPath at a fraction of the cost. This also allows the IC to operate in the preferred position next to the patient.

3) Improved procedural control and stent selection CorPath lacks clinical data demonstrating improved efficacy. At best CorPath has shown equivalence to traditional manual PCI. CorPath lacks haptic feedback that IC’s find important, especially in complex cases. According to the American College of Cardiology most of the benefits to CorPath appear to be for the physician, not the patient.

4) Large Market If the market were truly as large as they believe then they would be selling more units. The disposable cassettes lack reimbursement and without compelling evidence showing improved efficacy for robotic PCI over manual PCI, that is not likely to change. The $550 to $650 cassette cost per procedure is entirely incremental and cuts into procedure profits. Increasingly hospitals are being pressured to reduce costs and improve patient outcomes to justify reimbursement. CorPath does not meet these objectives. Even in cases where administrators have been able to justify the expense, IC’s aren’t utilizing CorPath as much as expected with installed units averaging only two procedures per month. The company will have to show they can meaningfully penetrate PCI before they can seriously consider other indications like peripheral vascular, neurovascular and structural heart.

CVRS remains a “show me” stock. Until the company can demonstrate the type of monstrous growth that analysts are forecasting we have no faith in the ability of the company to succeed. Even with a strong revenue ramp it will be years before profitability could be reached, if ever. As we’ve laid out in explicit detail above, we believe there are several hurdles that will continue to trip them up. It appears inevitable that the company will be back to the equity market next year for another dilutive raise.

28

Ultimately we believe CVRS will follow the lead of other vascular robotic companies that have tried and failed to gain traction in the space, racking up massive losses for investors in the process. The $165mil in accumulated losses for CVRS pales in comparison to the $470mil accumulated loss for Stereotaxis. Prior to Hansen Medical’s buyout at 1/3rd the current valuation of CVRS, they had accumulated losses of $463mil. We believe CVRS will continue to burn cash and add to their accumulated losses for the foreseeable future. Ultimately, companies that can’t turn a profit are worth zero. We can’t see a path to profitability for CVRS. A year from now the cash will be gone (again). Given this backdrop we do not believe current valuation is justified. We feel the closest proxies to CVRS are Stereotaxis (STXS) and Hansen Medical. Inclusive of preferred shares the enterprise value of STXS is about $39mil. Prior to Hansen’s acquisition its enterprise value was about $75mil as a standalone company. CVRS continues to face significant barriers to increased CorPath adoption. Therefore we feel a valuation somewhere in the middle of this range around $57mil for CVRS is entirely justified.

Including net cash of $33.7mil we arrive at a $90.7mil market cap, or 46c per share

representing over 60% downside for CVRS.

Longer-term, if CorPath is unable to gain traction the company may be worthless.

FULL DISCLOSURE: Cliffside Research and our affiliates invest in the companies we cover. We spend great effort in our due diligence process. We make investments based on our conviction in our due diligence process. You should assume at the time of publication we hold a short position in securities of the company discussed in this report. Please see our full “Terms of Service” at the bottom of this report or at cliffsideresearch.com.

Cliffsideresearch.com

29

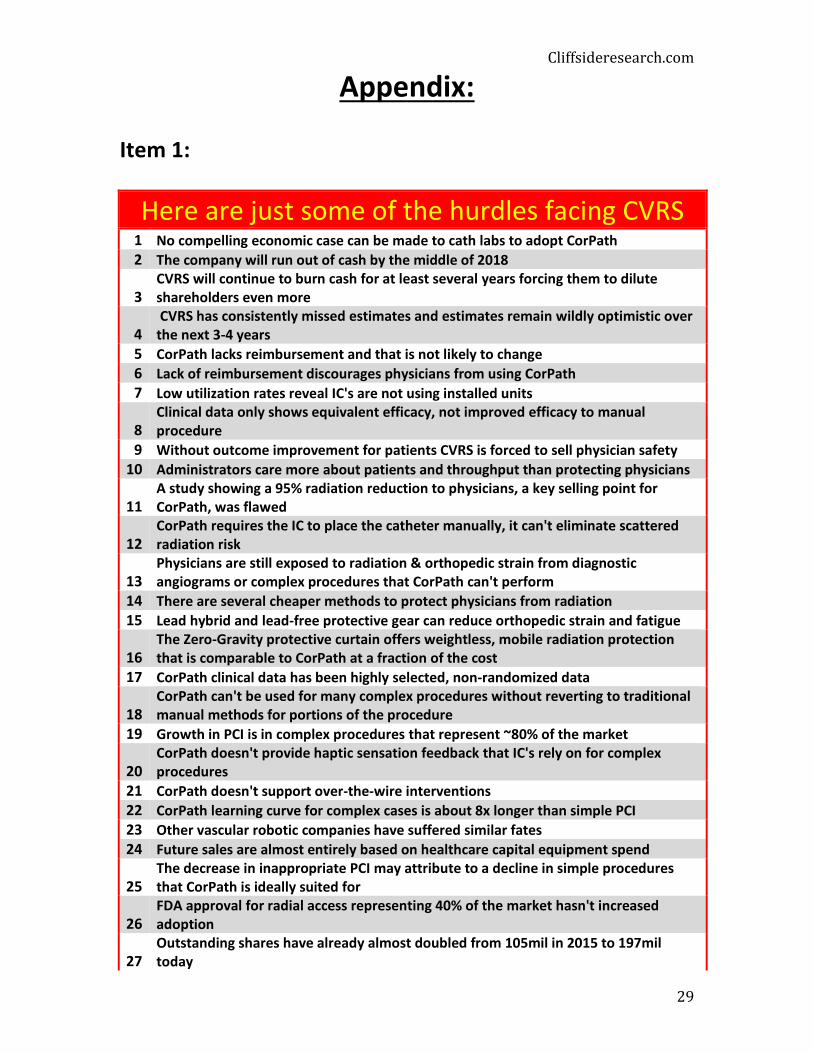

Appendix: Item 1:

Here are just some of the hurdles facing CVRS 1 No compelling economic case can be made to cath labs to adopt CorPath

2 The company will run out of cash by the middle of 2018

3 CVRS will continue to burn cash for at least several years forcing them to dilute shareholders even more

4 CVRS has consistently missed estimates and estimates remain wildly optimistic over the next 3-4 years

5 CorPath lacks reimbursement and that is not likely to change

6 Lack of reimbursement discourages physicians from using CorPath

7 Low utilization rates reveal IC's are not using installed units

8 Clinical data only shows equivalent efficacy, not improved efficacy to manual procedure

9 Without outcome improvement for patients CVRS is forced to sell physician safety

10 Administrators care more about patients and throughput than protecting physicians

11 A study showing a 95% radiation reduction to physicians, a key selling point for CorPath, was flawed

12 CorPath requires the IC to place the catheter manually, it can't eliminate scattered radiation risk

13 Physicians are still exposed to radiation & orthopedic strain from diagnostic angiograms or complex procedures that CorPath can't perform

14 There are several cheaper methods to protect physicians from radiation

15 Lead hybrid and lead-free protective gear can reduce orthopedic strain and fatigue

16 The Zero-Gravity protective curtain offers weightless, mobile radiation protection that is comparable to CorPath at a fraction of the cost

17 CorPath clinical data has been highly selected, non-randomized data

18 CorPath can't be used for many complex procedures without reverting to traditional manual methods for portions of the procedure

19 Growth in PCI is in complex procedures that represent ~80% of the market

20 CorPath doesn't provide haptic sensation feedback that IC's rely on for complex procedures

21 CorPath doesn't support over-the-wire interventions

22 CorPath learning curve for complex cases is about 8x longer than simple PCI

23 Other vascular robotic companies have suffered similar fates

24 Future sales are almost entirely based on healthcare capital equipment spend

25 The decrease in inappropriate PCI may attribute to a decline in simple procedures that CorPath is ideally suited for

26 FDA approval for radial access representing 40% of the market hasn't increased adoption

27 Outstanding shares have already almost doubled from 105mil in 2015 to 197mil today

30

28 CVRS is a one product company with very little revenue

29 CorPath isn't mobile and it takes up space

30 The rest of the staff is still exposed to harmful radiation, orthopedic strain and fatigue

31 PIPE shares are now registered and holders can sell

Item 2:

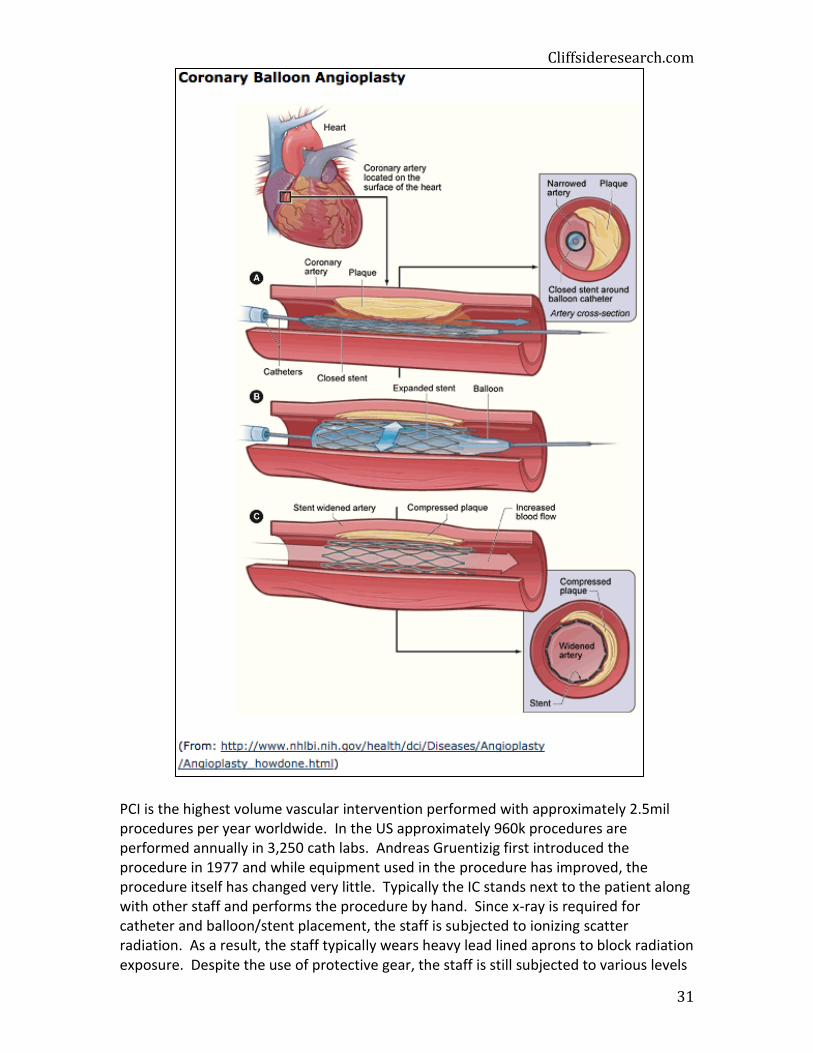

PCI Overview: Percutaneous Coronary Intervention (PCI), formerly known as coronary angioplasty, is a nonsurgical procedure that improves blood flow to the heart by opening stenotic (narrowed or blocked) coronary arteries. In the procedure, an interventional cardiologist (interventionalist or IC) accesses the patient’s heart percutaneously via the femoral or radial artery. Using x-ray guidance, a catheter is advanced through the artery to the aorta and finally to the blockage in the coronary artery. The catheter allows the IC to deploy several different devices including guidewires, balloons, stents and cutting devices. The IC inserts and inflates a balloon in the blocked area to restore blood flow and simultaneously deploys a stent to hold the artery open.

Cliffsideresearch.com

31

PCI is the highest volume vascular intervention performed with approximately 2.5mil procedures per year worldwide. In the US approximately 960k procedures are performed annually in 3,250 cath labs. Andreas Gruentizig first introduced the procedure in 1977 and while equipment used in the procedure has improved, the procedure itself has changed very little. Typically the IC stands next to the patient along with other staff and performs the procedure by hand. Since x-ray is required for catheter and balloon/stent placement, the staff is subjected to ionizing scatter radiation. As a result, the staff typically wears heavy lead lined aprons to block radiation exposure. Despite the use of protective gear, the staff is still subjected to various levels

32

of radiation. Increasingly studies are showing that continuous exposure to radiation can lead to health concerns including cancer, cataracts and carotid atherosclerosis. In addition, the weight of the lead can lead to orthopedic injury to the IC and staff.

Cliffsideresearch.com

33

Terms of Service

By viewing this material you agree to the following Terms of Service. You agree that use of this report and any report downloaded from Cliffside Research (cliffsideresearch.com) is at your own risk. In no event will you hold Cliffside Research, or any affiliated party liable for any direct or indirect trading losses caused by any information provided by Cliffside Research. You further agree to do your own research and due diligence before making any investment decision with respect to securities covered herein. You represent that you have sufficient investment sophistication to critically assess the information, analysis and opinion on this report. You further agree that you will not communicate the contents of this report to any other person unless that person has agreed to be bound by these same terms of service. If you download or receive the contents of this report as an agent for any other person, you are binding your principal to these same Terms of Service. You should assume that as of the publication date of our reports and research, Cliffside Research (possibly along with or through our members, partners, affiliates, employees, and/or consultants) along with our clients and/or investors and/or their clients and/or investors has a short position in all stocks (and/or options, swaps, and other derivatives related to the stock) and bonds covered herein, and therefore stands to realize significant gains in the event that the price of either declines. We intend to continue transacting in the securities of issuers covered on this site for an indefinite period after our first report, and we may be long, short, or neutral at any time hereafter regardless of our initial position and views as stated in our research. This is not an offer to sell or a solicitation of an offer to buy any security. Cliffside Research is not registered as an investment advisor in any jurisdiction. If you are in the United Kingdom, you confirm that you are accessing research and materials as or on behalf of: (a) an investment professional falling within Article 19 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “FPO”); or (b) high net worth entity falling within Article 49 of the FPO. Our research and reports express our opinions, which we have based upon generally available information, field research, inferences and deductions through our due diligence and analytical process. To the best of our ability and belief, all information contained herein is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable, and who are not insiders or connected persons of the stock covered herein or who may otherwise owe any fiduciary duty or duty of confidentiality to the issuer. However, such information is presented “as is,” without warranty of any kind, whether express or implied. Cliffside Research makes no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use. Further, this report contains a very large measure of analysis and opinion. All expressions of opinion are subject to change without notice, and Cliffside Research does not undertake to update or supplement any reports or any of the information, analysis and opinion contained in them. You agree that the information is copyrighted, and you therefore agree not to distribute this information (whether the downloaded file, copies / images / reproductions, or the link to these files) in any manner other than by providing the following link: http://www.cliffsideresearch.com/research. If you have obtained Cliffside Research reports in any manner other than by download from that link, you

34

may not read such research without going to that link and agreeing to the Terms of Service. You further agree that any dispute arising from your use of this report and / or the Cliffside Research website or viewing the material hereon shall be governed by the laws of the State of California, without regard to any conflict of law provisions. You knowingly and independently agree to submit to the personal and exclusive jurisdiction of the superior courts located within the State of California and waive your right to any other jurisdiction or applicable law, given that Cliffside Research has offices in California. The failure of Cliffside Research to exercise or enforce any right or provision of these Terms of Service shall not constitute a waiver of this right or provision. If any provision of these Terms of Service is found by a court of competent jurisdiction to be invalid, the parties nevertheless agree that the court should endeavor to give effect to the parties’ intentions as reflected in the provision and rule that the other provisions of these Terms of Service remain in full force and effect, in particular as to this governing law and jurisdiction provision. You agree that regardless of any statute or law to the contrary, any claim or cause of action arising out of or related to use of this report or the material herein must be filed within one (1) year after such claim or cause of action arose or be forever barred.