cloud accounting evaluation guide

TRANSCRIPT

COPYRIGHT 2012 – TECHVENTIVE, INC. – ALL RIGHTS RESERVED

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

Cloud Accounting Evaluation

Guide

2012 Edition

COPYRIGHT 2012 – TECHVENTIVE, INC. – ALL RIGHTS RESERVED

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

Table of Contents

Table of Contents ................................................................................................ 1

Introduction .......................................................................................................... 2

When to Replace Your Accounting System ...................................................... 5

Getting Organized ............................................................................................... 9

Macro Selection Considerations ...................................................................... 14

Selection Process Today .................................................................................. 23

Short Listing ....................................................................................................... 30

Software Demonstration ................................................................................... 33

Decision Making ................................................................................................ 40

Selling the Decision........................................................................................... 47

Appendix ............................................................................................................ 49

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 2

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

Introduction

A Very Different Choice in Financial Accounting Software

Accounting software has been around for decades. Functional areas such as accounts payable, accounts receivable, fixed asset accounting and general ledger accounting have been using automated financial accounting software to greatly improve the productivity of their functions and to better protect and manage key assets of an organization. Prior to the mid-1960s, many organizations often spent approximately 4% of total corporate revenue on back-office functions such as financial accounting and payroll. Today, most large organizations spend approximately 1% of total revenues on such functions with some, remarkably, spending even less. These incredible productivity improvements have helped businesses and local economies improve their gross domestic product.

These solutions have continued to improve in capability over the years and are now some of the most mature and technically sophisticated applications that an organization may utilize. Users of these solutions expect these products to not only provide the basics of financial accounting (e.g., double entry accounting, trial balances, etc.) but to also support sophisticated managerial and operational accounting requirements. As a result, core financial accounting software functions have been supplemented over the years with more robust budgeting, planning, forecasting, analytic, etc. functions.

Today, the newest financial accounting solutions are powered by cloud technology and the myriad of complementary technologies that are enabled and enhanced by cloud computing platforms. These new solutions have significant functionality to support mobile computing devices such as cell phones and tablet computers. Collaboration software is another exciting dimension being incorporated into new financial accounting solutions. Likewise, powerful platform computing environments are propelling the development of new financial accounting solutions as well as thousands of complementary add-on functional applications built by all-new armies of independent software developers.

Cloud computing changes the landscape for financial accounting software -- of that, there is no doubt. In fact, the leader board for accounting software is changing dramatically. Old guard names are being displaced by newer firms such as FinancialForce.com (a joint venture between salesforce.com and UNIT4) and Workday, to name two.

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 3

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

Buyers of accounting software are becoming savvier also. They see significant differences between the products being marketed today and those from previous generations. They are being bombarded with a veritable lexicon of new product names, architectural and technological attributes and other software characteristics that may confuse them for a time. Yet underneath all of the buzzwords and marketing hype, there truly are pioneering firms with radically new and impressive products that are reshaping the financial accounting software space.

The challenge, today, is learning how to separate the innovative and future leaders of the financial accounting software space from the also-rans and charlatans trying to pass off old technology with new marketing buzzwords.

Because of these changes in the market, we have crafted this quick buyer’s guide for cloud-based financial accounting software. Our goal is to help the reader understand the very different choices, decisions and considerations they may need to make when deciding on their next financial accounting software solution. Because the average financial accounting software solution is often utilized for close to a decade, these are not decisions to be entered into lightly. We have defined some useful guidance within these pages to help you make a decision that serves your organization well for many years to come.

This Buyer’s Guide

We have laid out this Cloud Accounting Evaluation Guide to follow a multi-step process. We believe this process will allow your organization to becomes more aware of the new accounting software marketplace and determine a new software solution partner.

Each section of this guide highlights many of the major issues your organization should consider in making a cloud accounting software selection decision.

We hope this guide will:

- help your organization get productive quickly - collapse many of the best ideas in accounting software solutions into one, easy-to-read,

structured publication - accelerate the selection team’s learning curve - define and structure the cloud accounting vendor selection process - preemptively address many of the issues the selection team will encounter in choosing a

cloud accounting solution

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 4

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

- provide practical guidance to making a cloud accounting software solution choice - make you, the reader, more self-sufficient and successful

This Buyers Guide is not a detailed methodology as it trades completeness for brevity. It does, however, serve as a quick reference guide for the selection team and provides a common framework for communicating with them. Be sure to adapt the contents of this guide to your organization. Smaller organizations may not require as formal of a selection team, for example. Larger organizations may need additional personnel, review points, etc.

Enjoy.

COPYRIGHT 2012 – TECHVENTIVE, INC.

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

5

When to replace your Accounting System

Do You Need a New Financial Accounting System?

In our three decades of analyzing the ERP marketplace, we have assisted hundreds of companies, large and small, in choosing new software. In the course of those initiatives, we have learned a lot about why companies change their financial accounting software. Our analysis of the application software marketplace indicates that 8-10% of the financial accounting software market, on average, turns over annually. Approximately 4% of the market requires a new solution because the company has experienced extraordinary growth or contraction. This change in business size often requires new solutions to reflect the increased or diminished business and functional requirements of the organization. The remaining 4-6% of the installed base for application software changes for more strategic or discretionary reasons. Businesses may decide to embark on new global or vertical market expansions. These critical product or geographic alterations to the company's business may require significant upgrades or outright changes to the ERP solution that has served the company to-date. Overall, there are five major categories of change that drive ERP software purchases. These are:

- business driven decisions

- technology driven decisions

- corporate decisions

- business combination decisions

- vendor driven decisions

Let's look at each of these in more detail.

Business driven decisions

1) The business, or parts thereof, may desire new process efficiencies, operational

efficiencies and/or productivity gains. When companies have a smattering of non-

integrated or diverse software solutions, their business may be operating at a sub-

optimal and uncompetitive level. For example, if your organization is still taking data

from one system, entering it into a spreadsheet, reformatting the information, keying it

Section

1

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 6

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

into other systems, etc., you are likely encountering significant errors and needless

costs. Better organizations recognize these inefficiencies and seek newer solutions that

are better integrated and better able to deliver more reliable information at significantly

lower cost and with little or no delay.

2) External entities, like bankers or auditors, may insist that better systems and controls

be put in place at the company. Whether their rationale is to reduce risk, improve

governance or better control business activities, the net effect may often require the

replacement or significant upgrade of the business solutions in use at the organization.

3) The business may desire new automation solutions in previously non-automated

areas. For example, if your organization implemented an automated accounting system

more than 10 years ago, it may not have contained a critical function that is available in

new solutions today (e.g., collaboration software). Businesses frequently add new

capabilities to their IT portfolio.

4) The company may decide to move to a more centralized or decentralized management

style. When such a shift occurs, the business may find that its current solutions are

either under or over powered by the new business model requirements. This can

frequently trigger the need for new accounting software.

5) The business needs new insights into its operations. Today, many organizations desire

newer financial accounting solutions that come equipped with advanced business

analytics, business intelligence and collaborative technologies.

Technology driven decisions

1) Some financial accounting solutions are not technically current and must be replaced.

Chances are, if your current accounting software was designed before there was an

Internet, it probably isn’t current. If your organization uses a solution that cannot

support mobile applications, office automation suites or other critical technologies your

organization utilizes, then you will need to replace your system. Continuing with

obsolete technology is risky as it could leave the organization vulnerable to security

risks, inopportune hardware or software failures and an inability to find appropriately

skilled personnel to support the obsolete products.

2) Newer solutions may be acquired to replace older, custom software applications.

Businesses may decide that it is no longer cost effective to support and maintain

applications when similar or more functionality may now be available through a package

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 7

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

software choice. Likewise, the company’s dependency on a few critical programmers

that know the software may be coming to an end (e.g., due to upcoming retirements)

thus precipitating a need for a new solution.

Corporate Decisions

1) A change in the top leadership in the company could trigger changes in the software in

use at your organization. Frequently, new executives, such as a CFO, CIO or Controller,

are brought in to drive just this sort of change.

2) The company's move into new geographic markets may trigger the need for more or

better financial accounting software. If a company has been using a local software

solution but now has decided to enter into new markets in other parts of the world, the

old solution will likely fail to meet the new business requirements.

3) Should a company add or drop product lines or business units, a change in financial

accounting software may be required. If an organization finds itself with new business

partners, joint ventures, offshore entities, etc., then new financial accounting systems

may be necessary.

Business Combination Driven Decisions

1) Mergers, acquisitions and divestitures drive a significant number of application software changes. Companies often must choose a new financial accounting solution that can handle the increased scale and demands of the combined business. In the case of a divestiture, the newly spun out business may lack any information technology solutions and may require a new solution implemented in record time.

Vendor Driven Decisions

1) Sometimes, software customers want a product's direction to go one way and the

vendor takes it in a completely different direction. While each side may feel it

possesses strong business rationale for choosing their respective paths, the customer

may nonetheless need to seek a better long-term ERP solution from another firm.

2) Should a software vendor be acquired or go out of business, customers may have no

choice but to acquire new technology elsewhere. Customers must make changes if the

product they use daily is no longer supported. This is particularly true with applications

that require frequent tax and regulatory updates.

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 8

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

3) A product upgrade may require a full re-implementation of the software. Some

software upgrades are so radical that they dictate a complete re-install of the software.

This happens when file formats, core functionality, technical architecture or other major

solution aspects are altered. When customers have to undertake such a large upgrade

effort on their software, they may want to consider a different solution at that time.

Most every company will find itself responding to one of these software change requirements every few years. What distinguishes the best companies from others is the way they handle these software change requirements so that the organization is better positioned competitively, strategically and economically for years to come.

COPYRIGHT 2012 – TECHVENTIVE, INC.

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

9

Getting Organized

Guidelines for Getting Organized

Three distinct groups must be convened in most software technology selections: organization executives, functional users and IT. Many other participants may also serve important functions during some or all of the selection effort:

Section

2

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 10

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

Most every successful software selection has a core selection team. Smaller organizations may not require more than this group. In fact, the core team size should be commensurate with the size and complexity of your organization. Larger, more complex entities will want more input, more consensus and more guidance.

The following text illustrates the team composition a large entity may utilize.

A large organization will likely need a core selection team, a steering committee and input from several business unit users.

The core selection team will likely contain senior executives from:

- Finance - IT - Procurement - Legal - Operations

These individuals are responsible for articulating the organization’s strategic vision, identifying potential organization changes (that could affect a software selection decision), developing the parameters for a shortlisted cloud accounting solution, performing much of the due diligence and, making the key recommendations to the executive and/or steering committee. In sales parlance, this group represents decision makers and influencers.

The core selection team should also be supplemented with critical subject matter experts (SMEs) that intimately understand the affected accounting and finance functions. These persons know the unique organization issues/requirements, accounting nuances, regulatory requirements, integration concerns, needs of the broader user community and other factors that must be considered when evaluating new accounting software solutions. These individuals will likely be major contributors to the deeply functional aspects of the selection documents, selection process and detailed evaluation of the long and short-listed vendors.

A Finance executive is needed for several important roles. This individual should:

- analyze the effect of the proposed solutions on the capital and operating budget of the organization

- document the effect that any solution has on the free cash flow of the organization

- assess the process impacts of any new solution on different finance/accounting personnel

- ensure adequate controls will be in place

- assess any solution specific (or implementation specific) risks that could expose the organization to unwanted harm

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 11

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

Finance also has a critical role to play during due diligence. A careful review of the corporate health and viability must be undertaken for each of the short-listed providers. Equally important, Finance will want to examine the security, controls and risk mitigation efforts of the cloud computing environment where the solutions will be housed.

Finance will also be the key liaison between the selection team and the internal and external auditors.

IT representation is needed as the finance solutions will need to be integrated with the other IT systems within an organization (e.g., office automation, front office, HR, etc.). IT should provide technical due diligence in investigating the shortlisted providers’ systems.

Procurement personnel can efficiently and effectively manage the procurement process. Typically, Procurement will control communications with potential solution providers and guide the negotiations.

Legal needs to be involved in any cloud accounting selection. Their role will be to review proposed software contracts.

The Steering Committee is a group of the organization’s most senior executives. They should be apprised periodically as to the core selection team’s progress. These briefings should occur at the completion of key milestones (e.g., Getting Organized, Shortlisting and Decision Making steps). In some situations (i.e., when the scope and importance of the deal are significant), the Board of Directors will also need to be briefed.

Key Information to Collect

The best selections occur when the core selection team is quite aware of the market. We recommend the selection team gather market intelligence from a variety of resources that include:

- Analyst firm research reports (e.g., IDC, Forrester) on the cloud accounting market - Key blogs that cover the ERP market space (e.g., AccManPro, various ZDNet titles,

DealArchitect, Financial Systems News) - Traditional IT media

Whenever possible, we also recommend that the selection team visit key software shows (e.g., Dreamforce), software vendor headquarters and other opportunities where the team can access those on the vanguard of technology change.

Additionally, the project team should collect a number of critical documents that will aid it in its selection efforts. These include (but are not limited to):

- sample reports produced by the current system

- examples of spreadsheet reports the current system cannot complete

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 12

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

- a listing and flow diagram of all systems that must be integrated with the core financial software products (e.g., customer relationship management)

- quantities and roles of all current accounting system users

- inventory of all significant software modifications made to the current system

- inventory of known functional shortfalls with the current system

- inventory of difficult accounting issues (e.g., average costing for inventory accounting) that the current system struggles with

- any communications from the external auditors regarding systems and control deficiencies in the current system

- excerpts from the IT strategic plan that indicate future technical direction for the organization and more specifically for certain enabling technologies such as mobile computing

Software Selection Project Charter

A critical component of this phase should be the creation of a project charter. This document is meant to help the selection team crystallize its selection decision. It also helps the team agree on and communicate its key project requirements, value drivers and other business needs to prospective software providers. What goes in the project charter? Formats and content can vary from company to company, but essentially, a project charter should contain:

- Prioritized project objectives - what are the top 3 – 5 business priorities that the organization wants to address through this software initiative? (e.g., materially reducing the cost of the financial accounting software; modernizing the technical infrastructure that staff accountants utilize; and, freeing up IT personnel to work on more strategic initiatives).

- The rationale why each objective is needed (e.g., our inability to ___ is hurting us economically. It is causing significant non-value added time being spent by accounting staff who must manually roll-up metrics or submit status reports in error-ridden, costly spreadsheets.).

- Key metrics that substantiate the need (i.e., what value would a new solution bring to the company?).

- Key capabilities the company needs (i.e., what are some of the key functional abilities that the solution must address?).

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 13

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

Cloud Accounting Selection Readiness Checklist

(Check all that apply) ______ A core selection team has been convened

______ The core selection team contains appropriate representation

commensurate with the size and complexity of your organization

______ The steering committee has been established

______ The organization has held preliminary discussions with potential outside experts

______ The project has been funded

______ Top management has signed off on the initiative. ______ The core selection team has undertaken considerable research on

the new cloud accounting market. ______ Critical project documentation has been assembled ______ The project has a charter that is agreed upon by all core selection

team members

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 14

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

Macro Selection Concerns

Prepare for a Very Different Selection

A software selection today is a different experience. The vendors, the offerings, and even the sales approaches are different. In fact, most of what you may remember from the last time your organization selected a new financial accounting solution has changed.

If your organization has an accounting software solution, it probably is an on-premise software product. These solutions are licensed for use on your organization’s computers. Your staff has to maintain these products. They have to apply upgrades, patches and fixes. Your organization has to have its own computing hardware, systems software, databases and more to operate this software.

On-premise software products are yielding market share to cloud software products as these newer solutions are scalable, require little to no capital expenditures, and, when the solution is a multi-tenant cloud product, are maintained by the software vendor (not your organization). As a general rule, these newer solutions are often less expensive to use and maintain.

When evaluating cloud accounting solutions, the selection team will likely notice:

- A different sales experience – Cloud software vendors can’t spend as much time on site doing in-person demonstrations. The expense of these sales cannot be justified with the reduced fees these vendors charge customers. More precisely, the monthly usage fees are often a fraction of the large upfront license fees that on-premise vendors charge. What your organization will likely experience is a sales environment that utilizes more web-enabled demonstrations. The selection

Section

3

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 15

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

team will still get the personalized attention they need/deserve except that the pre-sales vendor professionals will likely use internet video technologies from a remote location.

- That you will be able to use more of a product’s standard capabilities – Tailoring of application software has been getting progressively easier and less expensive. The newest products today are often built using powerful platform-as-a-service (PaaS) technologies. These PaaS environments permit users to tailor their usage of the software in powerful ways. Better products will let the organization tailor workflows, processes, field names, etc. They will also permit the addition of new functionality without impairing the vendor’s ability to maintain the application. However, very large scale or radical alterations to the core application software design may not be possible with many cloud applications as they may produce unacceptable or unplanned side effects.

- A very different set of parameters when calculating the ROI (return on investment) and TCO (total cost of ownership) of the new solution – Successive generations of accounting software have delivered diminishing benefits. The first automated accounting solution your organization implemented probably did a phenomenal job of improving the entity’s productivity, efficiency and effectiveness.

Manual

Ben

efi

ts

Time1st

Generation2nd

Generation3rd

Generation

Where Prior Benefits Were Captured

4th Generation

Batch,

ProprietaryOnline

Real-TimeUnix, Client

Server

Internet

Enabled

5th Generation

Cloud

?????

Where New Incremental Benefits Can Be Attained

The Drag On Software SalesDiminishing Benefits Curve for On-Premise Application Software

- Recently, when some on-premise solutions were hosted on cloud platforms (in a single tenant format), they were on track to deliver a small incremental improvement in productivity and some savings in hardware & capital expenditures. The scalability of these new SaaS solutions allowed firms to avoid large upfront costs. Multi-tenant cloud solutions may also bring additional savings beyond those from single-tenant solutions. Multi-tenant solutions can deliver substantial cost savings to organizations by transferring the cost of application maintenance to the software vendor. Multi-tenancy is a key departure to this past savings experience curve. Multi-tenancy

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 16

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

can reduce annual maintenance costs to such a degree that large enterprises we interviewed experienced a 41-60% reduction in the TCO over an 8 year time horizon.

Manual

Ben

efi

ts

Time1st

Generation2nd

Generation3rd

Generation

Where Prior Benefits Were Captured

4th Generation

Batch,

ProprietaryOnline

Real-TimeUnix, Client

Server

Internet

Enabled

5th Generation

Cloud

?????

Where New Incremental Benefits Can Be Attained

The Drag On Software SalesNew Benefit Curves for Cloud Application Software

IT savings via Multi-tenancy

Capital savings via Hosted SaaS

- A shorter implementation cycle – Cloud solutions often have shorter implementation timeframes. Frequently, organizations may be able to shave 3 months off their implementation time (and the costs associated with this) simply because the users do not have to incur the order, shipping, setup and other costs associated with the acquisition, configuration, patching, integrating, etc. of hardware, systems software, database, security and other products. Some cloud applications can be ‘installed’ in a manner of minutes or hours.

- You need to spend more time thinking through deployment options and functional choices –Very early in the implementation of a cloud solution, the project team will need to plan how they want the software to work. They will need to make decisions about chart of accounts design, inventory methods, etc. much earlier in the process. These decisions may trigger software configuration options that could get hard to reverse later on.

- That you have some interesting post-implementation decisions to make regarding your IT team – If typical, your IT team spends a significant amount of time every year patching, upgrading and maintaining your current on-premise accounting solution. In a multi-tenant cloud accounting solution, the workload on IT is substantially reduced. Be prepared to unleash this new found time on more strategic IT initiatives (e.g., in-memory analytic application development, mobile workforce connectivity, etc.). Freeing IT from low/non-value added activity may be one of the best benefits your organization may derive from a new solution.

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 17

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

Technology Factors to Consider

There are many kinds of cloud accounting solutions. The next few pages will attempt to highlight some of the choices your organization must make.

Hosted on-premise applications (also called Hosted SaaS or Single-Tenant SaaS) – Some vendors of on-premise software have struck deals with cloud providers to place their software on these environments. Each customer, generally, gets their own copy of the software and has their data in a separate database. This approach often allows the customer to acquire new software on a monthly subscription basis without acquiring new hardware, systems software or a new software license. While these products are marketed as SaaS (software-as-a-service) solutions, they are at their core an on-premise product that runs on a third party’s data center.

Providers of these solutions point out the following benefits to this approach:

- No upfront capital expenditures are required - The customer can decide when, or if, they want to upgrade or patch the software - The customer can make major modifications to the software, if desired - Each customer’s code and data can be logically and physically separated

There are other points to consider regarding these products. These include:

- The cost to maintain, upgrade and patch the software usually remains the responsibility of the licensee. Even if the vendor performs this maintenance, the single-tenant architecture requires the vendor to upgrade each individual implementation separately. This approach generally does not result in maintenance savings for the customer. Given this is one of the most expensive aspects of software TCO (total cost of ownership), this is a relevant issue to consider.

- Some hosted, SaaS solutions are essentially the same products vendors have been selling for a decade or more. While the applications may have been designed for web interaction, they generally lack one or more of the following components:

- An Integration-as-a-Service (IaaS) capability to make connections between on-premise, cloud, mobile, social and other applications

- A Platform-as-a-Service (PaaS) capability to allow the user to easily tailor and extend the application

- A rich PaaS ecosystem that contains hundreds, if not thousands, of applications that can extend, enrich and leverage the base software solution

Multi-tenant SaaS products – These solutions are akin to many consumer websites (e.g., Google search engine). There is one copy of the software but all customers use it. Each customer’s data is

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 18

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

kept ‘logically’ separated from other customers’ data. It may or may not be ‘physically’ segregated though.

Because there is only one copy of software, all customers are essentially using the same version of the software. Moreover, every customer is running on the most current version of the software.

There are some significant benefits that multi-tenant solutions offer. These include:

- Application maintenance is primarily the responsibility of the vendor. This capability is a major TCO savings. Yes, customers can sandbox new releases and test them prior to their go-live date.

- The software permits each user to tailor the application. These tailoring changes are carried forward from one release to the next.

- New, added functionality is often delivered via a setting that a customer must consciously enable. If your organization does not want to use a new feature/function, it generally will not be required to do so.

Multi-tenant applications are not for everyone. Some buyers may balk at:

- The inability to do radical programming changes to the software. If your organization’s functional requirements are so unique and cannot be satisfied by the tailoring capabilities of the cloud solution, an on-premise or hosted SaaS product may be a better fit.

Private cloud solutions – Private cloud solutions are essentially on-premise applications that are being run on an organization’s internal cloud infrastructure. In this situation, an IT group has created a cloud-like environment for use by their organization. Software, hardware, etc. are running much like they would in a public cloud environment except that their organization is generally the only entity with access to these systems and data.

The advantage of a private cloud solution is that the organization can control every aspect of the solution set. They decide when, or if, they upgrade the solutions. They limit access to the solutions. They can add additional layers of technology or can modify applications to their choosing. Like a hosted SaaS solution, this flexibility comes at a price as these systems require their own hardware, systems software, database licenses, staff to maintain the hardware and software, etc.

Financial Factors to Consider

Cloud solutions, whether single or multi-tenant, are generally good at reducing an organization’s upfront capital costs in IT. Figure 3 provides an illustrative view of different cost categories your organization should consider in evaluating any cloud solution.

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 19

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

050

100150200250300350

Maintenance - Hardware

Maintenance - Systems Software

Maintenance -Applications

Implementation - Services

Implementation -Hardware

Implementation -Applications

Illustrative Cost Differential

There are other financial considerations to evaluate as well. These include:

- Cash flow – While the current economy is producing record low interest rates in many parts of the world, access to capital is still difficult. Be sure to evaluate each solution based on its impact on free cash flow. Often, cloud solution vendors will offer discounts should users pre-pay 1-3 year’s worth of usage up-front. Measure these discounts against your organization’s cash on-hand, borrowing capability and cost of capital.

- Operating Expense – A key component of the cash flow analysis will be to understand how the new solution will impact current and future accounting period operating budgets. If a monthly subscription pricing method is being used, be sure to understand how many users will be accessing the system. Also, be sure to understand exactly how monthly charges will be calculated (e.g., based on users, modules, etc.) so that accurate operating funds estimates can be created.

- Capital Expenditure – This remains a significant cost item for on-premise solutions but not so much for most cloud solutions. The vendor is responsible for the acquisition, deployment, maintenance, etc. of the computing equipment and systems software used on the cloud platform. These costs are generally amortized and included in the monthly operation fee. Also note that on-premise hardware is seldom as scalable as that found on cloud services. Should your on-premise solution need more storage, computing power,etc., your organization may have no choice but to acquire new servers and acquire new usage licenses for critical systems software.

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 20

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

- Implementation costs - Implementation costs of cloud solutions are generally less than those for a comparable on-premise product. Why? The solutions are often ‘installed’ in minutes or hours on the cloud provider’s site. This effort alone could take weeks or months to complete on-premise. Some solutions come pre-supplied with specific processes, sample charts of accounts, reports, etc. These further reduce implementation costs. If the product is part of a family of solutions in a robust PaaS ecosystem, there may also be specific integration tools, add-on products, etc. that will also shorten implementation times and costs. No matter what cloud computing solution type your organization chooses though, some activities, like change management, will be needed in all implementations.

Security Factors to Consider

Placing one’s accounting transactions, sales data, etc. in a third party’s data center requires a measure of trust. Security and risk concerns regarding cloud solutions are appropriate concerns to have and your organization should undertake a measure of due diligence to ensure that specific risks have been mitigated to an appropriate level.

Most cloud accounting solution providers have implemented relatively strong security measures. They need to have these controls as their company’s reputation is dependent on having the highest standards of reliability and security. Cloud accounting software vendors should:

- protect the integrity of their customers’ data - minimize the possibility of a hostile hack into this information - maintain segregation of customer data from that of other customers’ data

Additionally, these firms should have well-planned disaster recovery plans that include:

- failover data centers - automated backup and recovery

When evaluating a cloud accounting software vendor, be sure the vendor has:

- a SAS 70 Part II/SSAE 16/ISAE 3402 certification - ISO 27001 certification

These certifications indicate the level of security controls/measures in effect at a point in time. We recommend that any organization considering a cloud accounting solution examine their own current level of security to develop a relative comparison of capabilities and concerns.

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 21

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

Beyond the certifications, we recommend a technical team develop and complete a technology review checklist with each vendor. This team should develop comfort with each vendor’s approach to:

- Data encryption - Data segregation - Intrusion detection & notification - Backup and recovery protocols - Privacy management - Disposal, destruction and redaction of personal information - Protection of personal information - Information quality standards - Monitoring and enforcement programs - Security safeguards testing - Security to/from portable media and telephony - Physical access controls - Controls re: transmission of personal information - Logical access controls - Etc.

How transparent each cloud system is can vary from one vendor to another. Some are quite open about system uptime, disruptions, etc. Some will publish information about the security (physical and technology) utilized at their cloud centers (e.g., http://trust.salesforce.com/trust/status/).

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 22

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

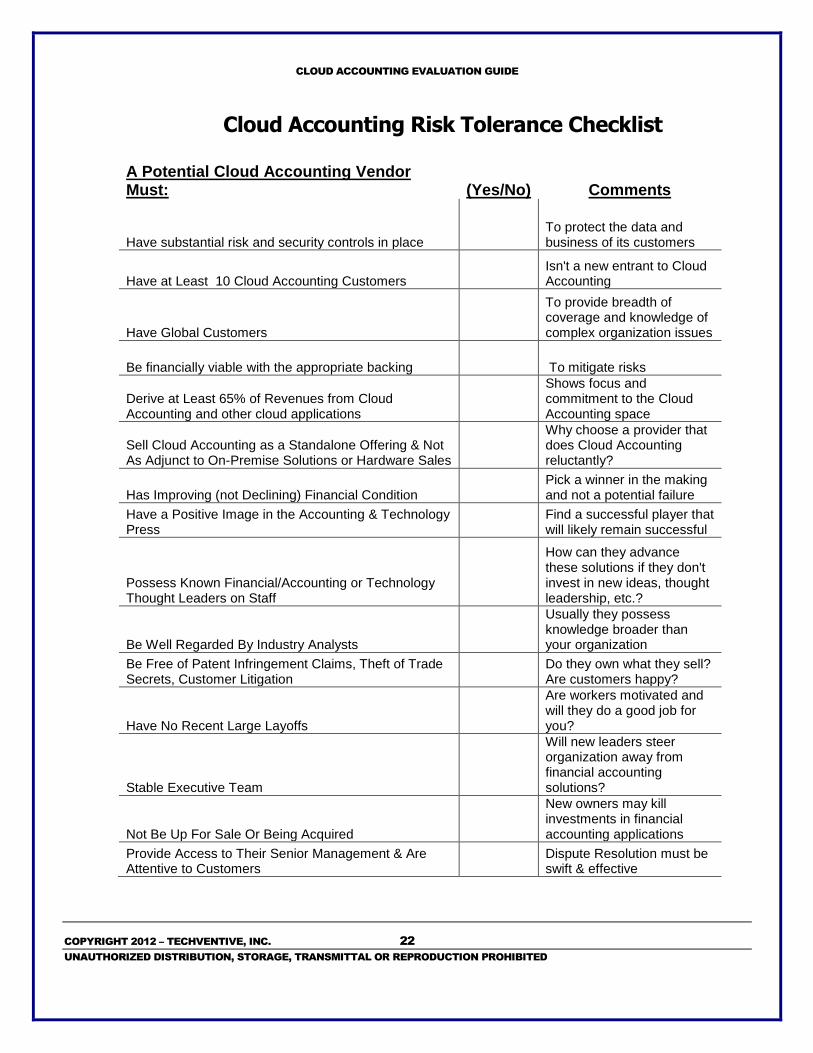

Cloud Accounting Risk Tolerance Checklist

A Potential Cloud Accounting Vendor Must: (Yes/No) Comments

Have substantial risk and security controls in place To protect the data and business of its customers

Have at Least 10 Cloud Accounting Customers Isn't a new entrant to Cloud Accounting

Have Global Customers

To provide breadth of coverage and knowledge of complex organization issues

Be financially viable with the appropriate backing To mitigate risks

Derive at Least 65% of Revenues from Cloud Accounting and other cloud applications

Shows focus and commitment to the Cloud Accounting space

Sell Cloud Accounting as a Standalone Offering & Not As Adjunct to On-Premise Solutions or Hardware Sales

Why choose a provider that does Cloud Accounting reluctantly?

Has Improving (not Declining) Financial Condition Pick a winner in the making and not a potential failure

Have a Positive Image in the Accounting & Technology Press

Find a successful player that will likely remain successful

Possess Known Financial/Accounting or Technology Thought Leaders on Staff

How can they advance these solutions if they don't invest in new ideas, thought leadership, etc.?

Be Well Regarded By Industry Analysts

Usually they possess knowledge broader than your organization

Be Free of Patent Infringement Claims, Theft of Trade Secrets, Customer Litigation

Do they own what they sell? Are customers happy?

Have No Recent Large Layoffs

Are workers motivated and will they do a good job for you?

Stable Executive Team

Will new leaders steer organization away from financial accounting solutions?

Not Be Up For Sale Or Being Acquired

New owners may kill investments in financial accounting applications

Provide Access to Their Senior Management & Are Attentive to Customers

Dispute Resolution must be swift & effective

COPYRIGHT 2012 – TECHVENTIVE, INC.

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

23

Selection Process Today

The Ever-Evolving Software Selection

Software selection activities have evolved over the years. A critical driver behind this evolution has been the increasing maturation and evolution of package software. Years ago, software buyers had no choice but to develop lengthy, highly detailed functional checklists with which to compare one application software product to another. These software buyers did this as the earliest applications often lacked significant but critical chunks of functionality. Only through an exhaustive review of most every function and feature could a buyer ascertain which solution best met their needs. In fact, the software marketplace of yore was so imperfect that buyers often did not choose the best product but rather the one that was missing the fewest critical functional components. Over time, as software products matured, function/ feature checklists gave way to more process or scenario-based evaluation techniques. While the checklists contained thousands of features, many of these functions would never be utilized by a prospective buyer. For example, did it really matter that one package could permit users to allocate a general ledger balance five different ways while another only possessed four? The answer, obviously, was no. Product maturity alone was not enough to decide the best business fit. Instead, users put vendors and their products through drills where vendors had to demonstrate the software's ability to perform specific processes or solve particularly thorny business problems (e.g., complex subsidiary intercompany accounting). The goal in these process/scenario driven selections was to surface the degree of difficulty in implementing or using each product. Subsequent accounting software evolutionary changes are prompting another change in how organizations acquire application software. Today, most any reputable application software vendor

Section

4

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 24

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

can deliver core accounting functionality. Where the differentiation may lie now rests in how well the solution accommodates future business change, future technology innovations, current and future business tailoring requirements and other needs. Some readers may wonder what is wrong with continuing to use a function/ feature checklist approach to selecting their next cloud accounting-based solution. They may argue that function/ feature approaches have worked for them in the past and that this should work again going forward. Should they choose this approach, they may well find that all evaluated products have remarkable similarities, functions, features and capabilities. As a result, a meaningful comparison of the products may not occur thus complicating the final decision-making process. Worse, users may be confused as to the real evaluation considerations they should be putting at the top of their priority list. The biggest danger lies in developing a function/ feature checklist that mirrors the current solution. Buyers in this instance often make a new software choice that will deliver no additional value to the organization as the new solution represents merely a lateral change in technology. The next several pages address a number of evaluation tasks and activities your organization should consider. Hopefully, many of these suggestions will sharpen the focus of the selection team around more critical differentiators in today's software market.

Avoid a Non-Value Added Replacement

Earlier in this buyers guide, we identified a number of reasons that an organization may have for choosing a new accounting software solution. For example, we discussed how technical obsolescence may force an organization to acquire a new solution. Yet, no matter what the reason for the change, the software selection team should be focused on bringing additional value to the organization. A simple replacement of one technology product with another generic solution will not result in new value being added to the organization. To maximize the value that may be possible from a new accounting solution, the selection team needs to understand how the new technologies (i.e., not just the accounting functionality) will impact other operational aspects of the company, other users of the information, the workload of the company’s IT organization, etc. The selection team should evaluate how any new solution impacts:

- the organization's total cost of ownership (TCO) over a multi-year timeframe (e.g., 8-10 years)

- key ROI metrics such as inventory turns, top line revenue growth, net margins, free cash flow, return on assets employed, and, of course, shareholder equity

- the efficiency and effectiveness of both accounting and non-accounting workers - potential improvements in accounting and non-accounting processes

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 25

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

Find Full Process Support

When evaluating new solutions, the selection team should take the broadest possible view of processes. In the past, selection teams often limited the purview of their selection to discrete accounting functions such as fixed asset accounting. This functional view may be very familiar to finance and accounting users but is only part of the equation when one sees how certain financial accounting components fit in the larger enterprise process designs. For example, the process called “opportunity to cash” (OTC) often begins in the marketing department where prospects are nurtured and passed along to the appropriate sales channel for further pursuit. Sales professionals convert these opportunities to proposals and eventually to orders. This is when accounting begins to track the deal even though a significant amount of work effort has preceded the transaction so far. Accounting professionals are quite familiar with the rest of the process where the order is converted into a bill/invoice, discounts may or may not be offered and revenue will subsequently be booked to the appropriate ledger entries. The broad view of a process is important as the selection team should understand what other technologies must be integrated to deliver maximum value to the organization. In the OTC example above, the new accounting solution should also have a tight integration with CRM (customer relationship management) software, Marketing campaign software (e.g., Marketo), mobile software (i.e., if sales people want to capture orders on their iPad while meeting with prospects), etc. Viewed this way, the selection team must evaluate more than accounting functionality. It must also view the solution’s PaaS (platform-as-a-service) and the other applications and technologies within the PaaS ecosystem. Why is this larger process view so important? When an organization seeks to purchase an accounting solution, the applications will invariably need to be integrated with non-accounting but equally critical operational technology solutions. In evaluating cloud accounting vendors, the selection team must also evaluate:

- the ease with which accounting applications can be integrated with other software solutions

- the availability of other operational and accounting products that can enhance business outcomes without unduly adding to the cost and workload of the company’s IT organization

- the ability of a solution’s tailoring capabilities to support vertical and other extensions to the core product

- the ecosystem of complementary products that can be added to the core solutions set especially if some of those can be added via a simple click or download

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 26

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

Evaluate the Platform as Much as the Application

We believe the best long-term value may come from choosing a multitenant cloud accounting solution that has a strong, underlying platform-as-a-service (PaaS) as well as a robust collection of third-party add-on technologies within the PaaS ecosystem. The selection team can make this assessment of the PaaS and PaaS ecosystem relatively easy. Software buyers need only log into a vendor’s application store online and peruse the available products. We would also recommend that buyers also evaluate:

- the number of complementary products designed to work with the cloud accounting software. For example, are there manufacturing, warehouse distribution, food industry, etc. applications?

- the size of the third-party ecosystem. Some vendors have no ecosystem while others may possess tens or hundreds of thousands of products to choose from.

- the reviews that different products are receiving (including the one being considered in this evaluation)

- the breadth of the add-on technologies. For example, are there mobile, analytic, big data, social media, and other enabling technology solutions available for purchase?

- the availability of tools that will permit straightforward tailoring and extension of the applications your organization is considering

Make Flexibility a Priority

As previously mentioned, software products are generally used by organizations for

approximately 10 years. In choosing a new accounting software solution, the selection team

must plan for change and evaluate vendors on their ability to support flexibility.

Within 10 years, can your organization expect to see any of the following changes?

- new leadership/management

- entry into new markets

- launch or abandonment of particular products or services

- new regulations

- new methods of selling products or services

- corporate reorganization

- new business owners

- etc.

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 27

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

Software rigidity is a luxurythat few organizations can afford today. Rapid change and tailoring

capabilities need to be a focus area for the selection team.

There is another major attribute that the selection team can use in evaluating the flexibility or

rigidity of a particular solution. The selection team should undertake an examination of the

following:

- How long did it take each vendor to build out their core accounting solution? If this

product was originally built using a PaaS, the answer should be closer to 1-2 years. For

vendors that are trying to transition older on-premise products to the cloud or to

multitenant cloud solutions, the answer may be spelled out in 5-10 year time frames or

longer. If the vendor's product is so difficult for them to change, why should the

selection team expect it to be easier for your organization?

- What is the average age of a product on the vendor's application store? If new

products are being added to this store daily and in large numbers, then the selection

team can be fairly certain that there is a powerful and flexible PaaS toolset behind

them. If the vendor has no application store or has only a smattering of solutions

within it, the selection team may want to seriously investigate the root causes for this.

Focus on the Organization of Tomorrow

The organization that is selecting software today will likely bear little resemblance to the one using this solution years from now. While no selection team can have a perfect crystal ball that foretells the future, they nonetheless must choose a solution with flexibility for today and tomorrow. This means that rapid tailoring capabilities, which may be part of the PaaS, are very important. We believe these organizations of tomorrow will also possess certain characteristics, if successful:

- have the ability to change and grow in a nonlinear fashion - easily serve nontraditional users of organization information (e.g., shareholders,

regulators, external auditors, suppliers, customers, etc.) - receive, send and collaborate with all manner of internal and external entities via

accounting and non-accounting technologies (e.g., social media, collaboration software, video and mobile tech)

- easily alter workflows and business processes that change with changing business requirements

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 28

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

Make Accounting a Real Partner in the Organization

Finally, the selection team needs to ensure that the chosen solution does more than simply optimize the activities and results within the finance accounting organization. Our earlier comments regarding the need for a strong and expansive process view warrant continued emphasis. Accounting departments and accounting solutions work best when both are focused on delivering value for the entire organization. Make sure your selection keeps this in mind.

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 29

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

Key Selection Team Decisions

(Check all that have been adequately addressed) ______ Will the new software bring additional value to the organization?

______ Is the selection effort focused on more than the limited functional

needs of the financial accounting group?

______ Does the team have a plan as to how it will choose and evaluate each vendor’s PaaS (platform-as-a-service)?

______ Does the team have a plan as to how it will choose and evaluate each vendor’s PaaS ecosystem?

______ Is product flexibility & extensibility being built into the selection

process?

______ Will the solutions fit the organization requirements of today and tomorrow?

______ Is the selection team positioned to choose a solution that

optimizes the entirety of processes?

COPYRIGHT 2012 – TECHVENTIVE, INC.

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

30

Short Listing

Why Create a Short List

It is expensive to evaluate software applications and the vendors that make those products. For this reason, make sure that the providers that the selection team is seriously evaluating are, in fact, serious candidates for your organization.

A cloud accounting selection will require a commitment of time from several of your most senior executives. Each additional solution provider on your shortlist represents a significant additional time commitment from each of these executives. Chances are, the schedules of these executives were already full before this project started and adding more providers to the shortlist isn’t going to help. Cloud accounting software providers also want to see a small shortlist. Why? It costs software vendors a considerable amount to compete for these sales. Some organizations will engage outside legal counsel to assist them during the negotiations. They may invest hundreds or thousands of person-hours into this sales effort (depending on the complexity of your organization) and they need to see that they have at least a one in four chance of winning. Some providers will not proceed if there are more than three providers on a shortlist as it is simply not cost-effective for them to do so. When cloud accounting software providers realize a prospective client is looking at a long list of candidates, they know that this prospect is still shopping and not serious about doing a deal yet. As a result, the software vendor will only provide passing support for this sale.

Section

5

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 31

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

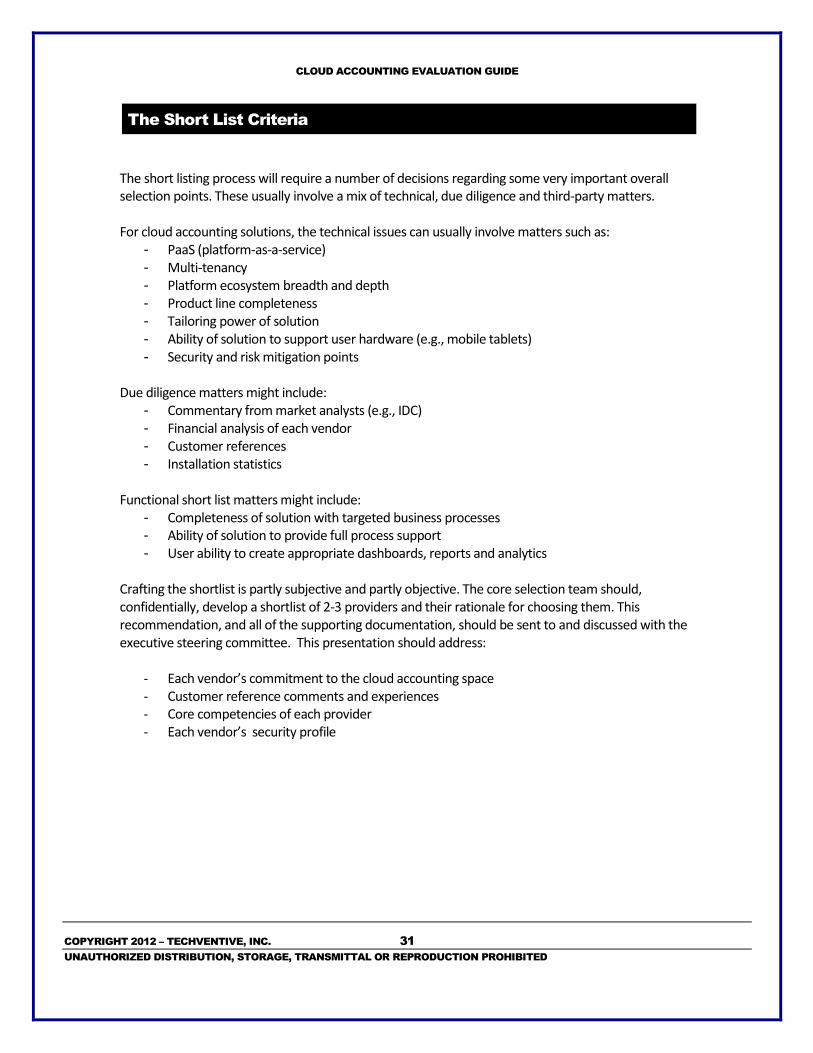

The Short List Criteria

The short listing process will require a number of decisions regarding some very important overall selection points. These usually involve a mix of technical, due diligence and third-party matters. For cloud accounting solutions, the technical issues can usually involve matters such as:

- PaaS (platform-as-a-service) - Multi-tenancy - Platform ecosystem breadth and depth - Product line completeness - Tailoring power of solution - Ability of solution to support user hardware (e.g., mobile tablets) - Security and risk mitigation points

Due diligence matters might include:

- Commentary from market analysts (e.g., IDC) - Financial analysis of each vendor - Customer references - Installation statistics

Functional short list matters might include:

- Completeness of solution with targeted business processes - Ability of solution to provide full process support - User ability to create appropriate dashboards, reports and analytics

Crafting the shortlist is partly subjective and partly objective. The core selection team should, confidentially, develop a shortlist of 2-3 providers and their rationale for choosing them. This recommendation, and all of the supporting documentation, should be sent to and discussed with the executive steering committee. This presentation should address:

- Each vendor’s commitment to the cloud accounting space - Customer reference comments and experiences - Core competencies of each provider - Each vendor’s security profile

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 32

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

Key Shortlisting Long List Vendor

Criteria (Y/N) Criteria 1 2 3 4 5 6

Y Product built with a PaaS Y Y Y Y Y Y

Y

Product is multi-tenant cloud

SaaS product Y Y Y Y Y Y

Y

Product part of large, relevant

ecosystem Y Y Y Y Y Y

Y

Vendor has at least 10 cloud

accounting software deals in

production Y Y N N N N

Y

Cloud accounting software is

the firm's core competency Y N N Y Y N

N

Key executives have strong

cloud and accounting

credentials Y N N N Y N

Y

Vendor possesses deep,

relevant intellectual property

(e.g., best practices,

benchmarks, methodologies,

global requirements, etc.) Y N Y N N N

Y

Vendor uses a quality

improvement program

internally Y N Y Y N N

Y

Vendor committed to SAE 16

or other security protocols Y N N N N N

N

Vendor has positive media

coverage re: its cloud

accounting software business Y Y N N Y N

N

Existing clients are equal to

or larger than our firm Y N Y n/a n/a N

Y

Vendor has a broad cloud

accounting software offering Y Y Y N Y N

Y

Vendor has exemplary client

references Y Mostly Y n/a n/a Y

Keep this Vendor? Yes No No No Yes No

If no, why not?

Cloud

acctg

software

commitm

ent really

lacking in

this firm

No real

client

base

no IP, no

quality

program

and no

credentials

good

credentials

but new in

this space

COPYRIGHT 2012 – TECHVENTIVE, INC.

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

33

Software Demonstration

Demonstration Guidelines

The software demonstration has been a staple of accounting software selections for decades. Prospective buyers would invite a vendor to their offices so that the vendor could answer questions and illustrate, often with access to a demonstration version of the software, the capabilities of the product.

Software vendors originally traveled to customer locations because on premise software did not lend itself well to remote demonstrations. Many years ago, demonstrations required a considerable amount of technical wizardry to get the solutions to operate remotely in the days of slow modems and spotty Internet access. When the live demonstration was not possible, vendor salespeople often fell back upon their tried-and-true method of using slideshows to illustrate a product's capabilities.

Today, most businesses have access to the Internet with many having high speed connections. The need for vendors to be physically present to demonstrate products has been diminished considerably by advancements in telecommunications capabilities and the ubiquitous nature of this telecommunication infrastructure.

But there are new economics involved with cloud accounting software. Many of today's most modern products are sold on a subscription basis, not up-front licenses. As a consequence, cloud software vendors do not receive the same large cash payment that frequently occurred with older on-premise sales. As result, cloud accounting software vendors generally cannot spend as much on selling to your organization as prior generations of vendors did.

But that is turning out to be a good thing anyway. Software vendors that have a lower cost of sales can also deliver lower-cost solutions to their customers. Moreover, today's software vendors take

Section

6

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 34

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

advantage of webinar, telecommunication, video, Internet and other technological innovations to make the software sales and demonstration experience better.

Today, vendors frequently place user videos, software demonstrations and replays of demonstrative webinars on their website for software buyers to peruse at their own leisure. As result, each member of your selection team can perform much of the selection effort, pre-shortlist, at home, at all hours and independently.

The days of tying up each vendor for days on end at your organization are fading away. The selection team should embrace the shopping and education tools vendors make available online to make your selection process more efficient, effective and responsive.

Step One – Getting Very Familiar

Software vendors today display a tremendous amount of information regarding their products available on the Internet. Some of these materials include:

- Role-based (e.g., accounts payable clerk) videos. These are often 3-5 minute videos showing how a particular user would interact with and get value from the software. These are especially useful in helping users visualize the new solution and to verify that critical core functionality is already present in the application.

- Pre-recorded webinars. These are longer format video productions that often run up to one hour in length. Webinars usually cover a specific issue (e.g., subsidiary accounting) or process area (e.g., opportunity to cash) in detail. Webinars often include a mix of presentations, voiceover and, sometimes, live video. As with role-based videos, webinars can provide insights into the product's functionality, its completeness and its look and feel.

- Case studies. Case studies document the implementation and/or experience that specific companies have gained through utilization of the solution. Case studies are often delivered in PDF documents that can be downloaded from the vendor's website. Prospective buyers will find case studies of interest as they provide clues as to the ROI others have received. Case studies also highlight a product's ability to solve some particularly onerous business problems.

- Product guides. Product guides often contain the most detailed information regarding specific product functions and features. Some product guides also provide insight into the solution’s applicability in specific verticals.

- Technical specification sheets. Tech sheets are instrumental in understanding technical architecture, extensibility tools, PaaS (platform-as-a-service) components, ecosystem characteristics and more.

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 35

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

Your selection team should amass and review all of this information prior to any direct vendor contact. From this information alone, the selection team should be able to eliminate several long list vendors from further consideration.

Step Two – Consider a Trial

Some software vendors have a trial solution option that your selection team should take advantage of whenever possible. The key here is that not all vendors offer this. Why? Unlike an inexpensive functionally limited application that anyone may download to their mobile phone, accounting applications often require some measure of coaching to configure initially. For example, you may need to configure the software for your chart of accounts, currency requirements or repeat payments. If this initial configuration is done incorrectly or with the wrong parameters, the user of the trial software may come away with an incorrect perception of what the software can and cannot do. This is not necessarily a fault of the vendor but rather a realization of the power and complexity that may reside in some of the solutions.

Some vendors will only permit a trial usage of their software subject to your organization meeting certain provisos. For example, will the selection team:

- Agree to some level of training before activating the trial software?

- Complete the trial within a defined time period?

- Provide the vendor with some documented use cases or other functional/process requirement documentation prior to the launch of the trial?

- Be willing to pay some nominal fee for the use of the trial software and the prep/training time the vendor invests in your organization?

Software vendors want to see some quid pro quo from your organization before they “invest” their time and expensive pre-sales personnel in helping the selection team through the trial experience. These are expensive undertakings on their part and they need to be sure that your organization is actually a serious buyer of new accounting technology. The selection team therefore must be ready to prove to the vendor that it is a relevant, focused and ready buyer of this type of software. Your organization is, in effect, qualifying for the right to earn a trial usage.

Please note that some trial software may be: free, low-cost, of a limited or unlimited duration. There is no industry standard for this. The number of users may or may not be constrained. Please check into these and other details before committing to any trial period.

Also note that some vendors may provide full access to their solution’s functionality while others may offer just a “taste.” Be sure the selection team knows what they are reviewing as a highly limited version of the product may give them an incorrect perception of the solution’s true capabilities.

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 36

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

One last point regarding trials. Not every vendor offers them and, of those that do, they may not offer them to every prospective customer. Whether a vendor will offer a trial solution should not be a deal breaker. It may, though, put that vendor’s solution at a disadvantage when it comes to making a final selection decision.

Step Three – Document What You Saw

While there can be significant similarities from one software product to the next, there should also be some very notable differences, too. Software selection teams can often become distracted by some of the bells and whistles present within any given package. And since selections often occur over a matter of weeks, there is often a tendency for teams to forget what they saw from one vendor's solution to the next. It is for this reason that most vendors want to be the last vendor your team will evaluate as it will be the one your team will remember the best.

Documenting what each team member saw is crucial to making an informed decision. It is not enough to simply document what one personally liked or disliked. Each team member needs to methodically review the same capabilities across multiple products and document at a minimum whether each solution possessed, satisfactorily met or exceeded their needs/expectations. Any time a particular product outright failed to meet expectations (or materially exceeded them), a selection team member should document exactly what they did or did not see. THIS DOCUMENTATION SHOULD OCCUR WHILE THE PRODUCT IS BEING REVIEWED – NOT DAYS OR WEEKS LATER.

From our vantage point at Vital Analysis, we have reviewed hundreds and hundreds of products and can attest to the difficulty in any one human being’s ability to adequately recall every nuance of every product we have seen. The problem is compounded when the team that was charged with a selection decision realizes that no one maintained adequate documentation.

Failure to document each vendor's solution will likely result in:

- rework for the selection team and the vendors involved

- dissatisfaction among the team and the vendors involved

- the potential for an incorrect selection decision

- inability to defend the selection decision before the executive committee

Does the documentation effort have to be onerous? No. In fact, the selection team can often stipulate that many core functions and features are present in most packages. The documentation the team must produce should be focused around significant departures from common functionality or capabilities. Done this way, the team can avoid the generation and completion of function/ feature checklists.

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 37

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

Step Four – Platform & Integration Review

Functions and features are not all that must be reviewed. A cloud accounting software selection must, in our opinion, include a review of the PaaS (platform-as-a-service) and other technologies. In particular, the team should evaluate the:

- robustness of the platform and its technical capabilities

- ability of the platform to develop additional, complementary applications

- size of the platform ecosystem

- number of developers and integrators building on this platform

- ease with which these applications can be integrated to:

o other cloud applications within the platform ecosystem

o other non-vendor cloud applications

o mobile devices on premise solutions

o analytic, business intelligence and other data-driven technologies

o social media

o collaboration technologies

o and more

This exercise can be quite telling as the selection team may encounter products that:

- have no PaaS

- have little or no third-party products in their PaaS ecosystem

- may be difficult to integrate with third-party cloud or on-premise applications

- integrate to a specific social media tool but not in a easy to extend manner

- etc.

Reviewing the technical platform and the integration opportunities available under each solution may produce some of the greatest differentiation the selection team will encounter. It is for this reason that we strongly advise readers to undertake this step and give it serious evaluation time and consideration.

CLOUD ACCOUNTING EVALUATION GUIDE

COPYRIGHT 2012 – TECHVENTIVE, INC. 38

UNAUTHORIZED DISTRIBUTION, STORAGE, TRANSMITTAL OR REPRODUCTION PROHIBITED

Step Five – Call in the Vendors

After the selection team has completed the first four steps, they are ready to engage directly with the software vendor. Be prepared for some interesting activity at this juncture.

First of all, be prepared that many of your interactions with the vendor will occur on teleconferences, webinars and other collaborative media. As stated previously, modern software vendors will utilize every technology possible to respond to deals in a more virtual aspect. Unless your organization is significantly large in size and scope and presents an outsized revenue opportunity for the vendor, your organization will likely deal with the vendor in a virtual manner throughout most, if not all, of the sales process.

One of the first things the selection team and the vendor must do is clarify their understanding of the product's capabilities as well as those of its PaaS. Be sure to share with the vendor the team’s assessment of their product’s strengths and weaknesses. Some of their assumptions regarding the vendor’s product could be based on the viewing of obsolete information or simply due to a lack of information involving critical needs that your organization has.

Once the selection team has corrected this information for all vendors, they should make any adjustments to the short list and move the selection forward.

At this stage, the selection team should notify each vendor of the organization’s most complex, thorny or difficult business problems and process issues. Vendors should be given a few days to contemplate solutions for these and be prepared to provide an Internet-based demonstration of how these issues will be resolved.

The selection team needs to take copious notes for all of these vendor solution suggestions. At the end of each proposed solution, one selection team member should play back their understanding of the solution to the vendor to ensure it has been correctly recorded. This information will be especially important in:

- guiding any future implementation team

- estimating the work effort required for the implementation

- assessing the solution’s impact on process owners and their organization