cloud computing indonesia market what are customers looking for

TRANSCRIPT

CLOUD COMPUTING

INDONESIA MARKET: WHAT CUSTOMER LOOKING FOR

JAKARTA

DECEMBER 6TH, 2011

COMPUTRADE TECHNOLOGY INTERNATIONAL'S GOLDEN CIRCLE CLUB ROUND

TABLE DISCUSSION

IWAN RACHMAT – SENIOR CONSULTANT

Recent Research on Cloud We Have Done in Q2-2011

• Survey done with IT Managers and CIOs in Australia, Hong Kong, China, India,

Singapore and Malaysia in Q2 2011

• 64% with >500 employees and 36% with 200 to 499 employees

• The public cloud is differentiated from private cloud set ups in that public clouds are

typically owned by third party providers

• Hardware is also located externally in the providers premises and they provide

clients leased use of their cloud data centres on tap as a utility service

Public

Cloud

• Private clouds on the other hand are private data centres that are owned by

companies themselves

• What makes them more cloud like than the regular data centre is that they are

upgraded with virtualised servers and can cater for fluctuating bandwidth

needs compared with the traditional server which would flounder in the face of

sudden spikes in computing demands

Private

Cloud

“Persists the opinion among local enterprises that cloud computing

– especially public cloud – is not secure”

• 40 percent of respondents said they felt that public clouds were less secure

• Cloud adoption is set to grow at CAGR of 39% through to 2015

• The research indicates fear around public clouds has been spread by vendors selling

their private cloud offerings

• Managing a cloud means securing a centralised network and allowing end points such

as PCs and mobiles to connect to it at the edges

• “Data Lock-in Model” where it is difficult getting data out of the Web customer

relationship management CRM vendor s database once it is in

• “Potential hidden-cost” as it will need upfront cost for integration with own

infrastructure & application with Cloud

• Investment in application architecture online – e.g. when google increases price of

using its App Engine caused a panic on the apps community due to cost surge

• Dependability of QoS, Performance, & reliability – that has to fully rely on the

providers’ promise

Some

Cautions

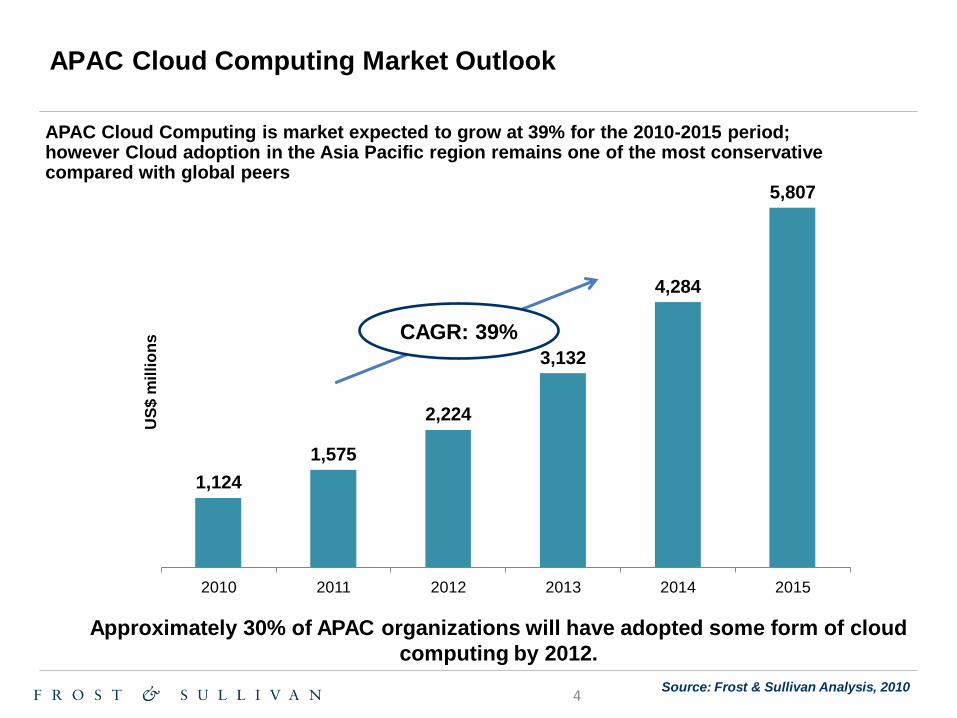

APAC Cloud Computing Market Outlook

Source: Frost & Sullivan Analysis, 2010

APAC Cloud Computing is market expected to grow at 39% for the 2010-2015 period; however Cloud adoption in the Asia Pacific region remains one of the most conservative compared with global peers

1,124

1,575

2,224

3,132

4,284

5,807

2010 2011 2012 2013 2014 2015

US

$ m

illi

on

s CAGR: 39%

Approximately 30% of APAC organizations will have adopted some form of cloud

computing by 2012.

4

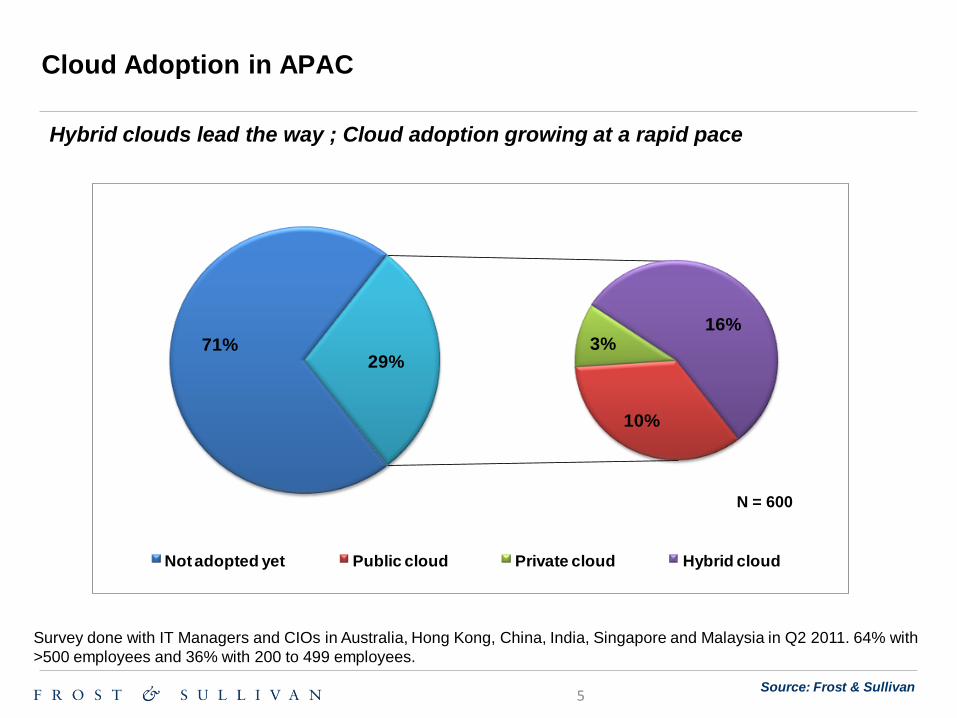

Cloud Adoption in APAC

Hybrid clouds lead the way ; Cloud adoption growing at a rapid pace

Source: Frost & Sullivan

71%

10%

3%16%

29%

Not adopted yet Public cloud Private cloud Hybrid cloud

Survey done with IT Managers and CIOs in Australia, Hong Kong, China, India, Singapore and Malaysia in Q2 2011. 64% with

>500 employees and 36% with 200 to 499 employees.

N = 600

5

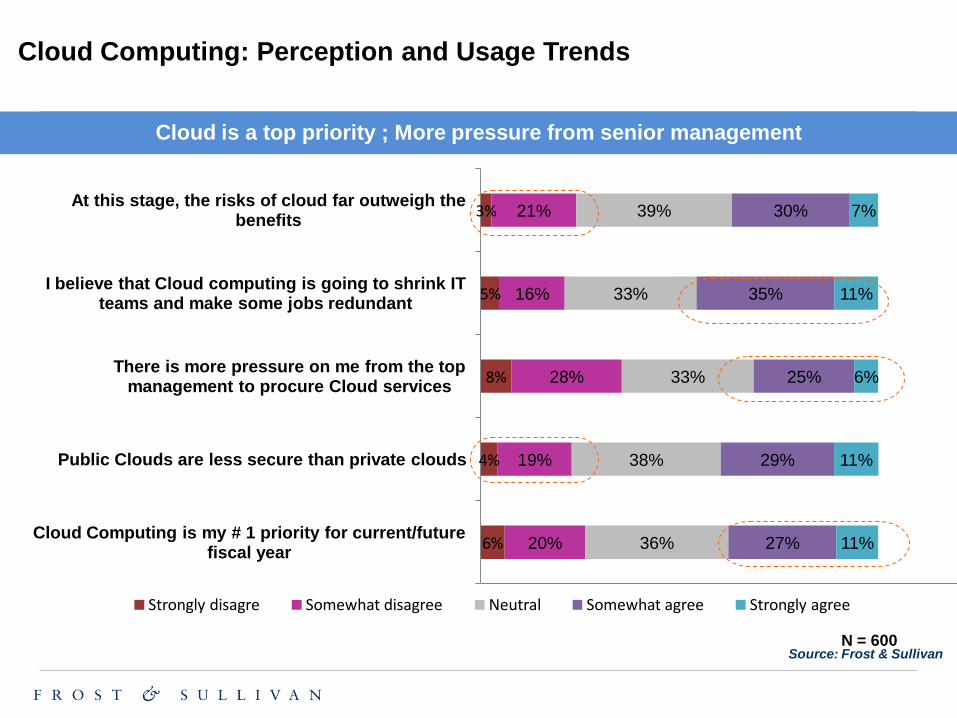

Cloud Computing: Perception and Usage Trends

Cloud is a top priority ; More pressure from senior management

Source: Frost & Sullivan N = 600

6%

4%

8%

5%

3%

20%

19%

28%

16%

21%

36%

38%

33%

33%

39%

27%

29%

25%

35%

30%

11%

11%

6%

11%

7%

Cloud Computing is my # 1 priority for current/future fiscal year

Public Clouds are less secure than private clouds

There is more pressure on me from the top management to procure Cloud services

I believe that Cloud computing is going to shrink IT teams and make some jobs redundant

At this stage, the risks of cloud far outweigh the benefits

Strongly disagre Somewhat disagree Neutral Somewhat agree Strongly agree

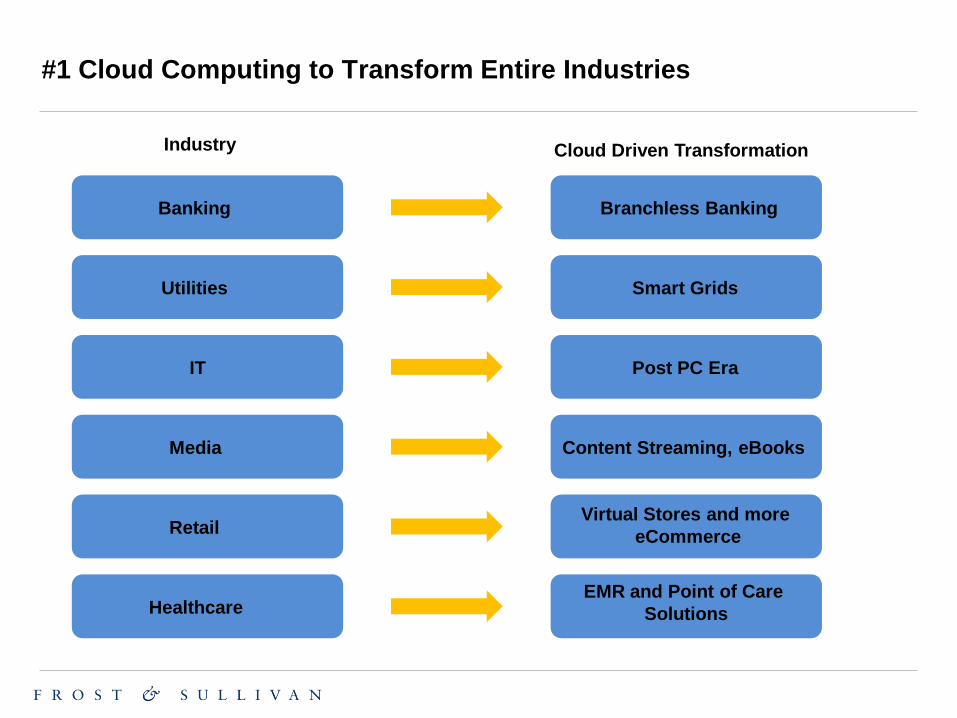

Banking

Utilities

IT

Media

Retail

Healthcare

Smart Grids

Post PC Era

Content Streaming, eBooks

Virtual Stores and more

eCommerce

EMR and Point of Care

Solutions

Branchless Banking

Industry Cloud Driven Transformation

#1 Cloud Computing to Transform Entire Industries

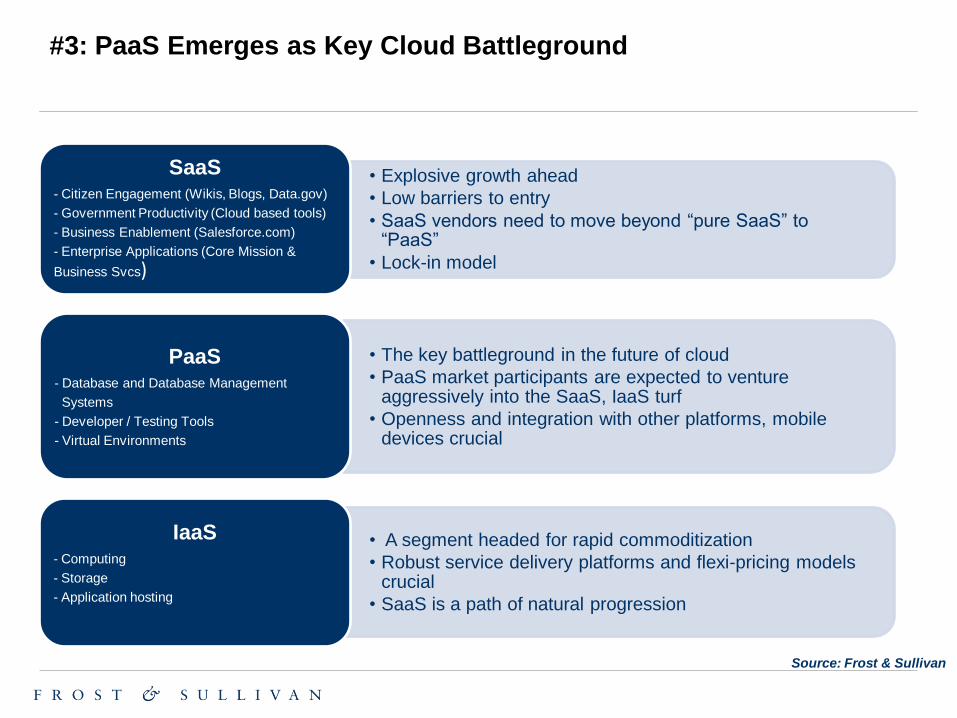

#3: PaaS Emerges as Key Cloud Battleground

Source: Frost & Sullivan

• Explosive growth ahead

• Low barriers to entry

• SaaS vendors need to move beyond “pure SaaS” to “PaaS”

• Lock-in model

SaaS - Citizen Engagement (Wikis, Blogs, Data.gov)

- Government Productivity (Cloud based tools)

- Business Enablement (Salesforce.com)

- Enterprise Applications (Core Mission &

Business Svcs)

• The key battleground in the future of cloud

• PaaS market participants are expected to venture aggressively into the SaaS, IaaS turf

• Openness and integration with other platforms, mobile devices crucial

PaaS - Database and Database Management

Systems

- Developer / Testing Tools

- Virtual Environments

• A segment headed for rapid commoditization

• Robust service delivery platforms and flexi-pricing models crucial

• SaaS is a path of natural progression

IaaS - Computing

- Storage

- Application hosting

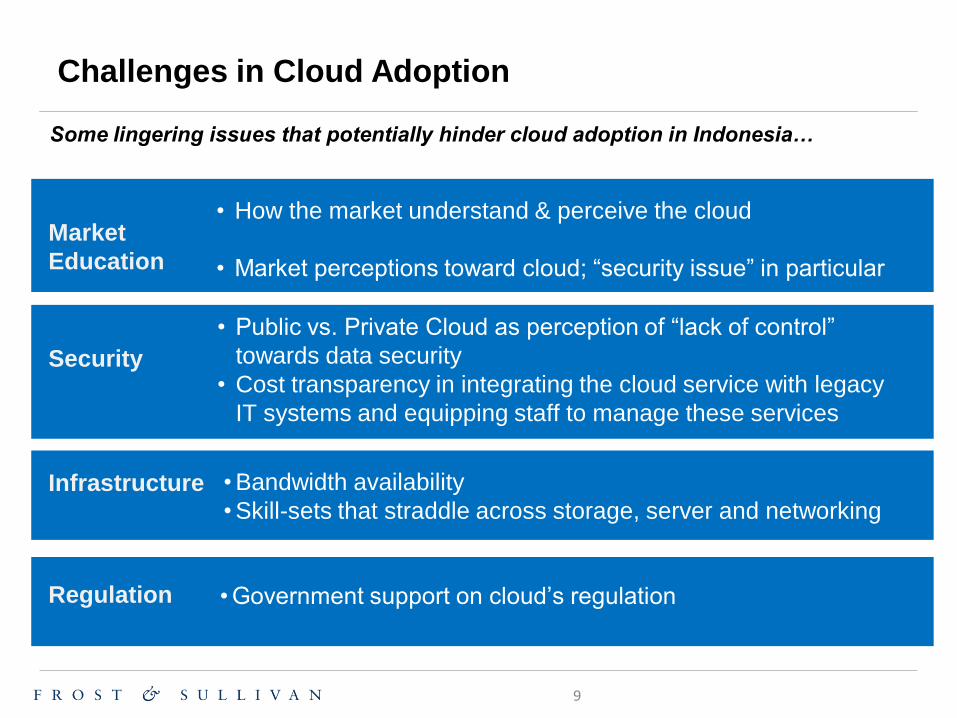

Challenges in Cloud Adoption

• How the market understand & perceive the cloud

• Market perceptions toward cloud; “security issue” in particular

Market

Education

• Public vs. Private Cloud as perception of “lack of control”

towards data security

• Cost transparency in integrating the cloud service with legacy

IT systems and equipping staff to manage these services

Security

• Bandwidth availability

• Skill-sets that straddle across storage, server and networking

Infrastructure

• Government support on cloud’s regulation Regulation

Some lingering issues that potentially hinder cloud adoption in Indonesia…

9

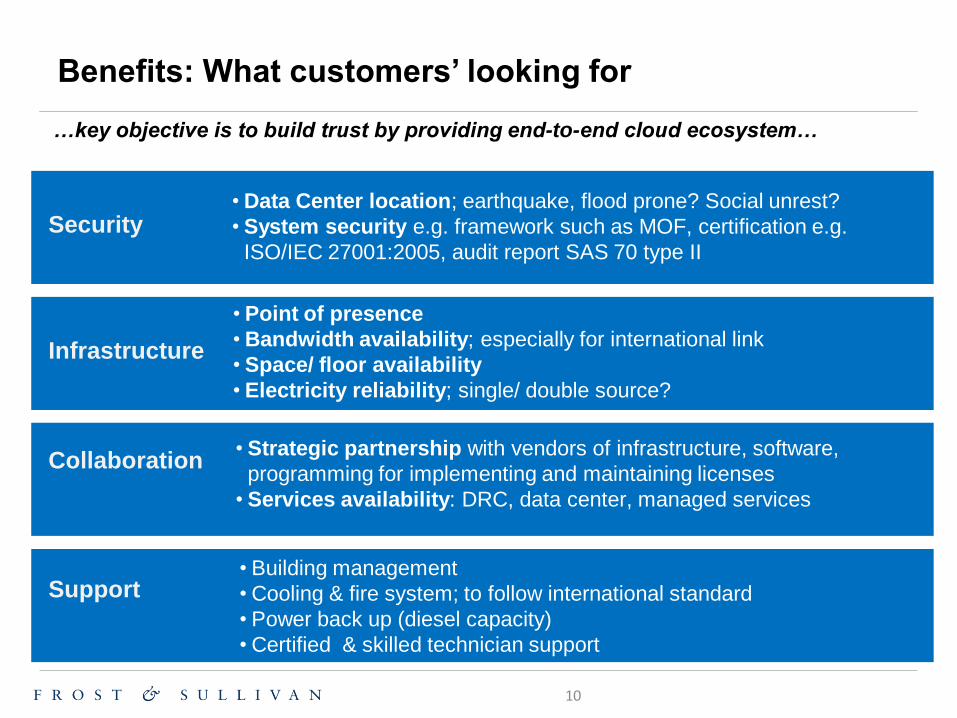

Benefits: What customers’ looking for

• Data Center location; earthquake, flood prone? Social unrest?

• System security e.g. framework such as MOF, certification e.g.

ISO/IEC 27001:2005, audit report SAS 70 type II

Security

• Point of presence

• Bandwidth availability; especially for international link

• Space/ floor availability

• Electricity reliability; single/ double source?

Infrastructure

• Building management

• Cooling & fire system; to follow international standard

• Power back up (diesel capacity)

• Certified & skilled technician support

Support

• Strategic partnership with vendors of infrastructure, software,

programming for implementing and maintaining licenses

• Services availability: DRC, data center, managed services

Collaboration

…key objective is to build trust by providing end-to-end cloud ecosystem…

10

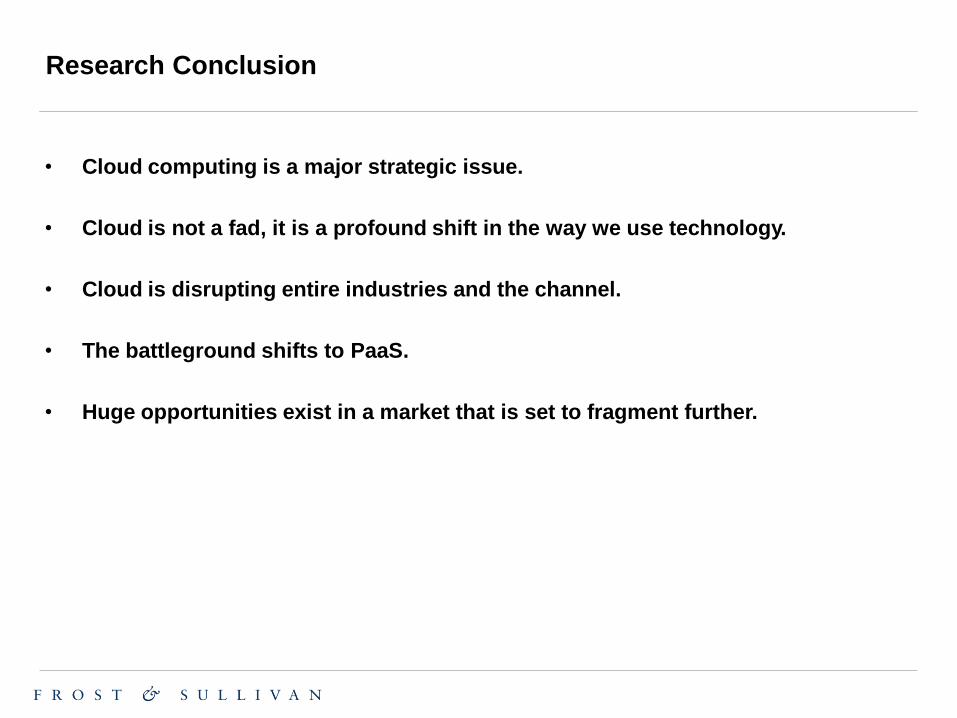

Research Conclusion

• Cloud computing is a major strategic issue.

• Cloud is not a fad, it is a profound shift in the way we use technology.

• Cloud is disrupting entire industries and the channel.

• The battleground shifts to PaaS.

• Huge opportunities exist in a market that is set to fragment further.

For your kind references

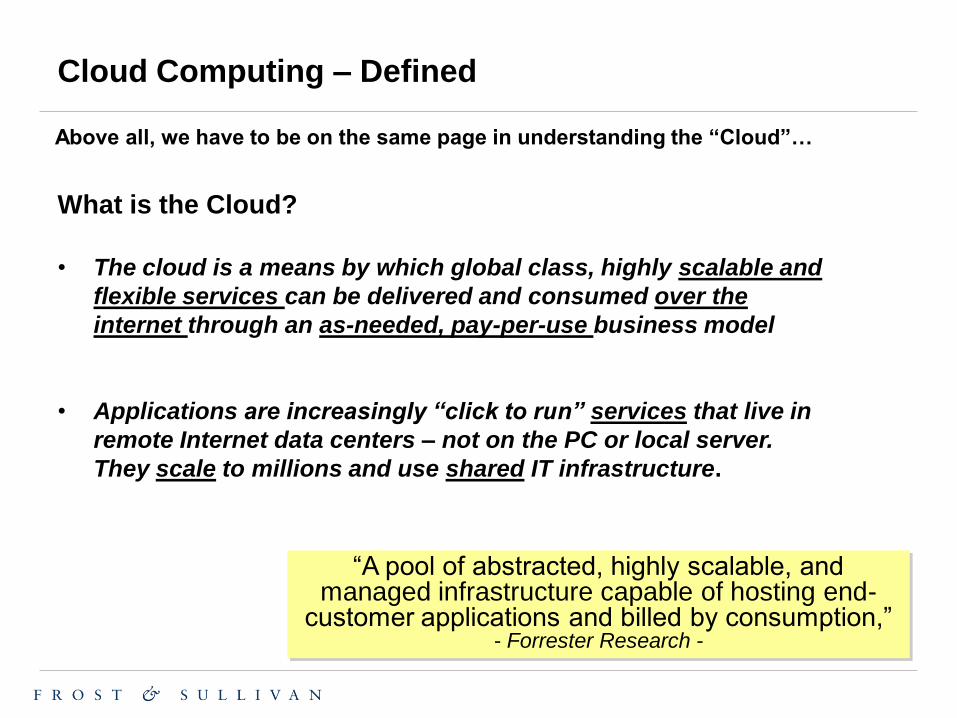

• The cloud is a means by which global class, highly scalable and

flexible services can be delivered and consumed over the

internet through an as-needed, pay-per-use business model

• Applications are increasingly “click to run” services that live in

remote Internet data centers – not on the PC or local server.

They scale to millions and use shared IT infrastructure.

Cloud Computing – Defined

What is the Cloud?

Above all, we have to be on the same page in understanding the “Cloud”…

“A pool of abstracted, highly scalable, and managed infrastructure capable of hosting end-

customer applications and billed by consumption,” - Forrester Research -

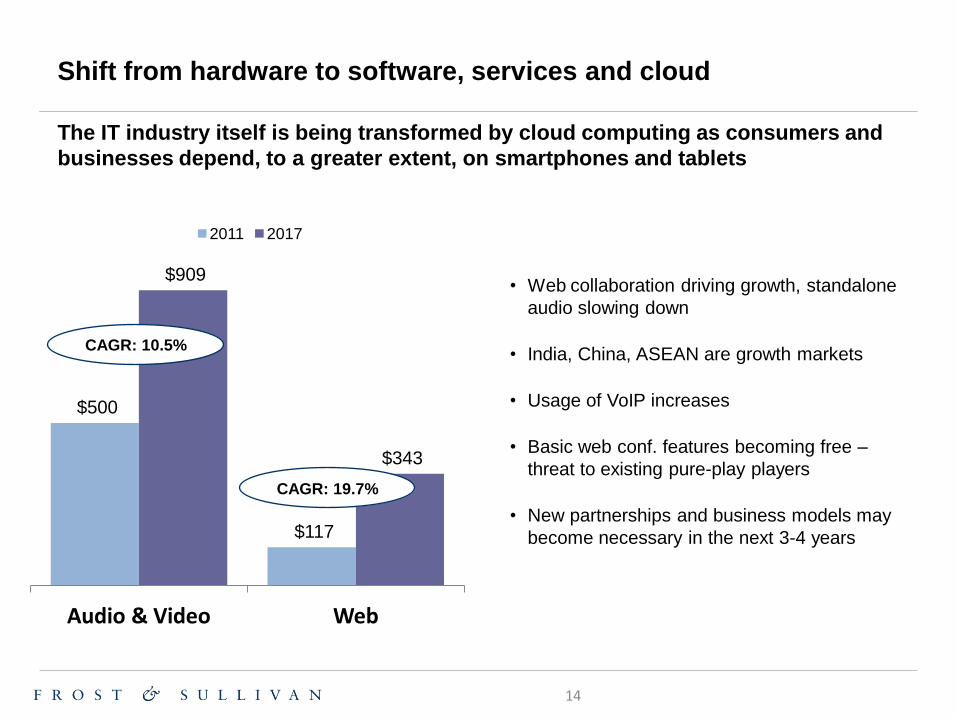

Shift from hardware to software, services and cloud

• Web collaboration driving growth, standalone

audio slowing down

• India, China, ASEAN are growth markets

• Usage of VoIP increases

• Basic web conf. features becoming free –

threat to existing pure-play players

• New partnerships and business models may

become necessary in the next 3-4 years

$500

$117

$909

$343

Audio & Video Web

2011 2017

CAGR: 10.5%

CAGR: 19.7%

The IT industry itself is being transformed by cloud computing as consumers and

businesses depend, to a greater extent, on smartphones and tablets

14

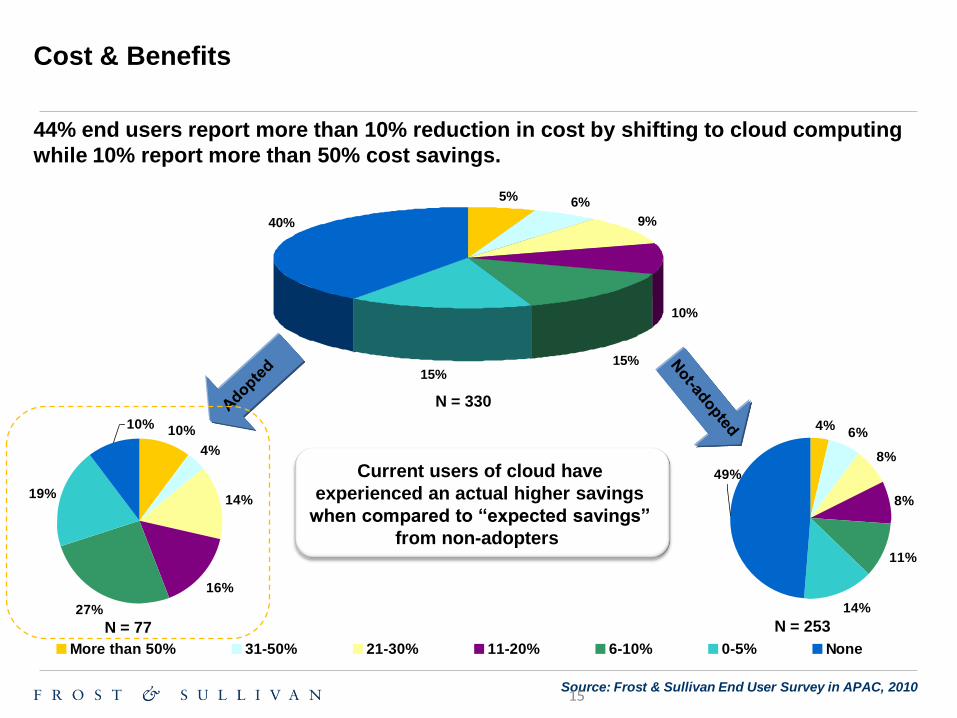

Source: Frost & Sullivan End User Survey in APAC, 2010

5% 6%

9%

10%

15%15%

40%

10%

4%

14%

16%

27%

19%

10%

More than 50% 31-50% 21-30% 11-20% 6-10% 0-5% None

4%6%

8%

8%

11%

14%

49%

N = 77 N = 253

N = 330

Current users of cloud have

experienced an actual higher savings

when compared to “expected savings”

from non-adopters

44% end users report more than 10% reduction in cost by shifting to cloud computing

while 10% report more than 50% cost savings.

Cost & Benefits

15

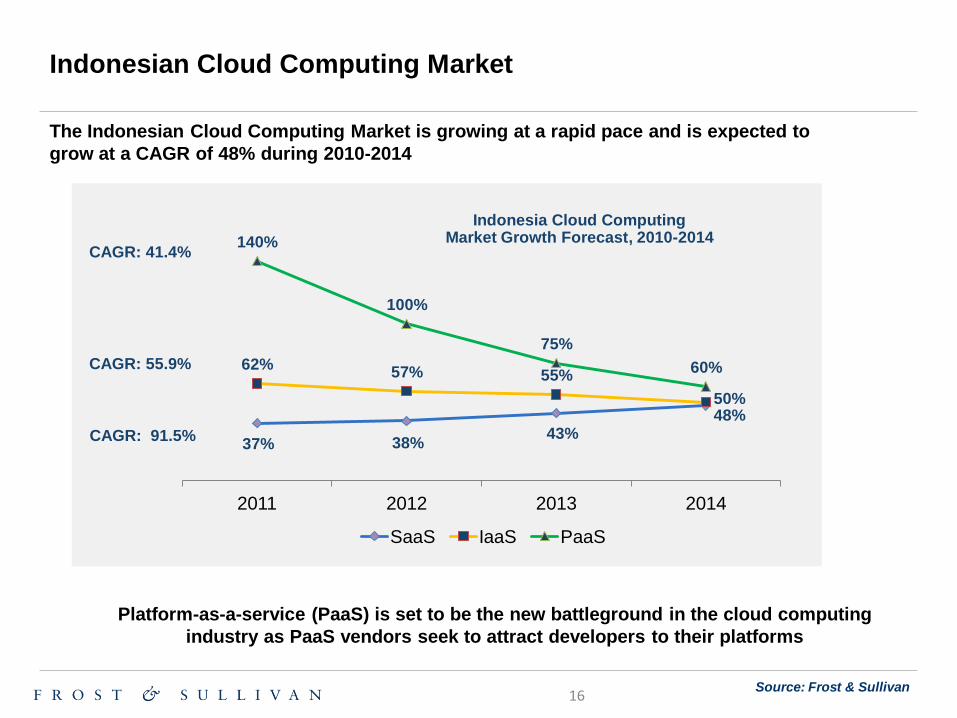

Indonesian Cloud Computing Market

37% 38% 43%

48%

62% 57% 55%

50%

140%

100%

75%

60%

2011 2012 2013 2014

SaaS IaaS PaaS

Indonesia Cloud Computing Market Growth Forecast, 2010-2014

Platform-as-a-service (PaaS) is set to be the new battleground in the cloud computing

industry as PaaS vendors seek to attract developers to their platforms

Source: Frost & Sullivan

CAGR: 41.4%

CAGR: 55.9%

CAGR: 91.5%

The Indonesian Cloud Computing Market is growing at a rapid pace and is expected to

grow at a CAGR of 48% during 2010-2014

16

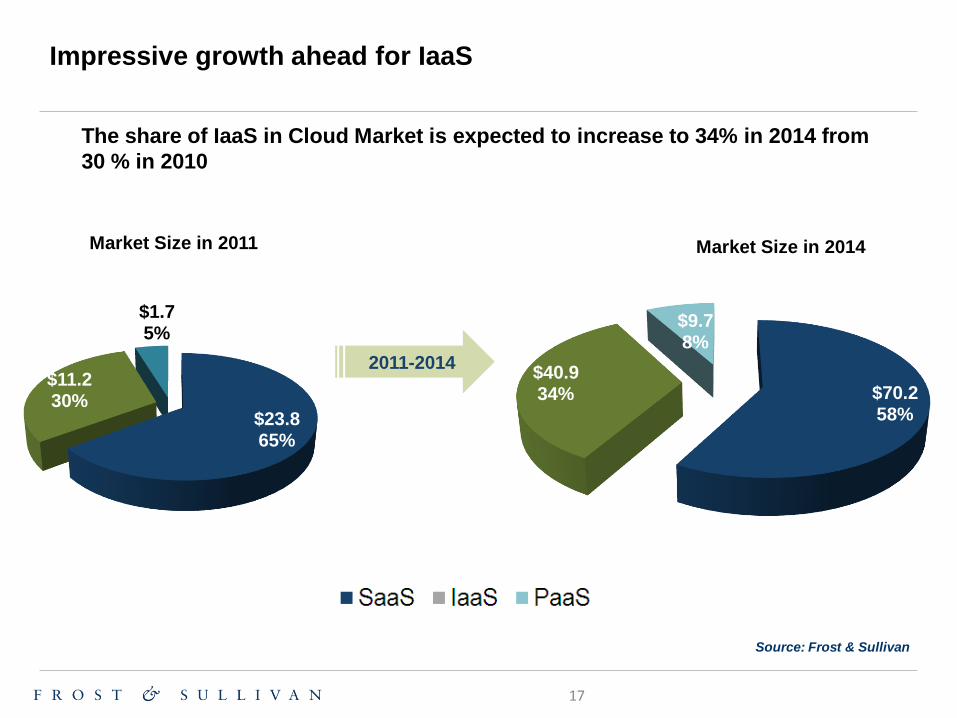

Impressive growth ahead for IaaS

The share of IaaS in Cloud Market is expected to increase to 34% in 2014 from

30 % in 2010

$23.8 65%

$11.2 30%

$1.7 5%

$70.2 58%

$40.9 34%

$9.7 8%

Source: Frost & Sullivan

Market Size in 2011 Market Size in 2014

2011-2014

17

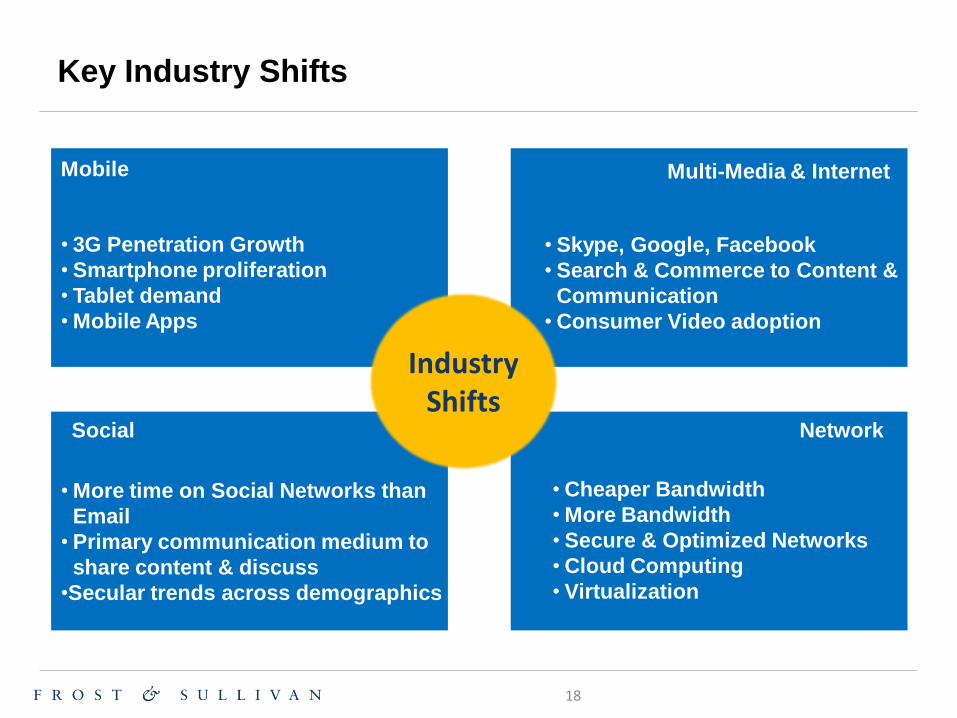

Key Industry Shifts

Social

Mobile Multi-Media & Internet

Network

• 3G Penetration Growth

• Smartphone proliferation

• Tablet demand

• Mobile Apps

• More time on Social Networks than

• Primary communication medium to

share content & discuss

•Secular trends across demographics

• Skype, Google, Facebook

• Search & Commerce to Content &

Communication

• Consumer Video adoption

• Cheaper Bandwidth

• More Bandwidth

• Secure & Optimized Networks

• Cloud Computing

• Virtualization

Industry Shifts

18

Major Trends Shaping the Indonesian Market

• Phase 1 : Basic infrastructure creation

• Phase 2 : Increasing competitiveness and connectivity

• Phase 3: Optimizing and maximizing IT

• Lot of Indonesian enterprises will go through Phase 2 and 3 at the same time forcing them to look at

the cloud

• Mobility will play a big factor in the push towards cloud – especially PaaS,and SaaS

Trend # 1: Future Shift in Adoption Patterns

• The entry of global participants, and their marketing initiatives in the form of conferences and road

shows, This is expected to drive awareness levels and adoption in the long term.

• However, enterprises continue to remain skeptical of Cloud adoption due to Security and Privacy

concerns.

Trend # 2: Increasing Awareness

• Currently nascent but huge supply side push with lots of launches in last one year

• Perceived Lack of infrastructure with regards to internet connectivity and availability.

• However maturity of service offerings, enterprises would be keener to move some of their IT spend to

Cloud.

Trend # 3: Nascent Market , growing maturity of suppliers

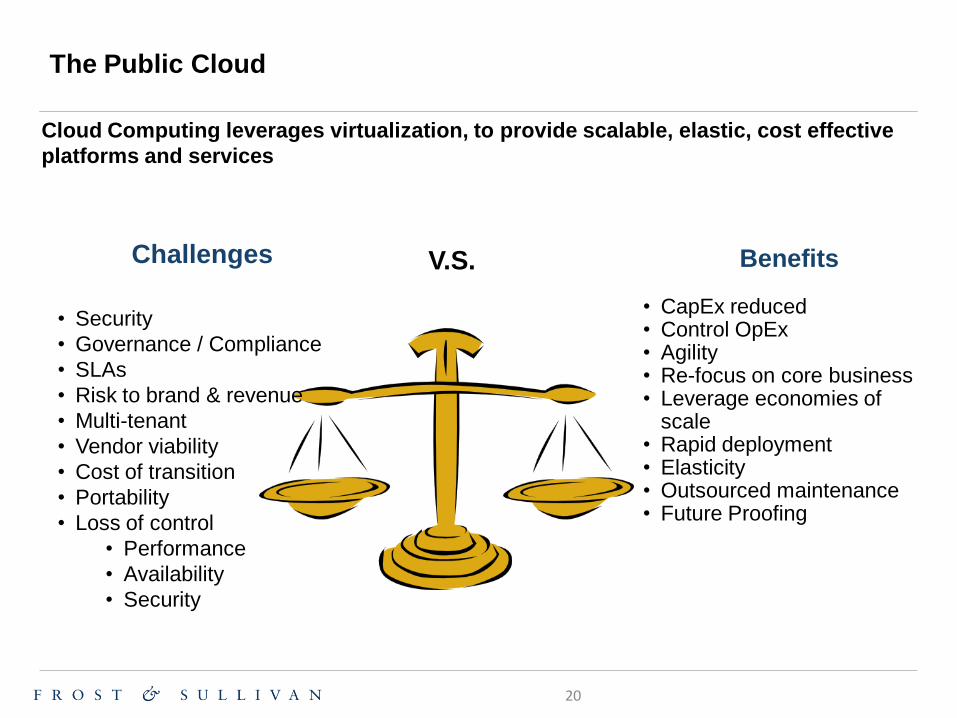

Cloud Computing leverages virtualization, to provide scalable, elastic, cost effective

platforms and services

The Public Cloud

Challenges

• Security

• Governance / Compliance

• SLAs

• Risk to brand & revenue

• Multi-tenant

• Vendor viability

• Cost of transition

• Portability

• Loss of control

• Performance

• Availability

• Security

Benefits

• CapEx reduced • Control OpEx • Agility • Re-focus on core business • Leverage economies of

scale • Rapid deployment • Elasticity • Outsourced maintenance • Future Proofing

V.S.

20

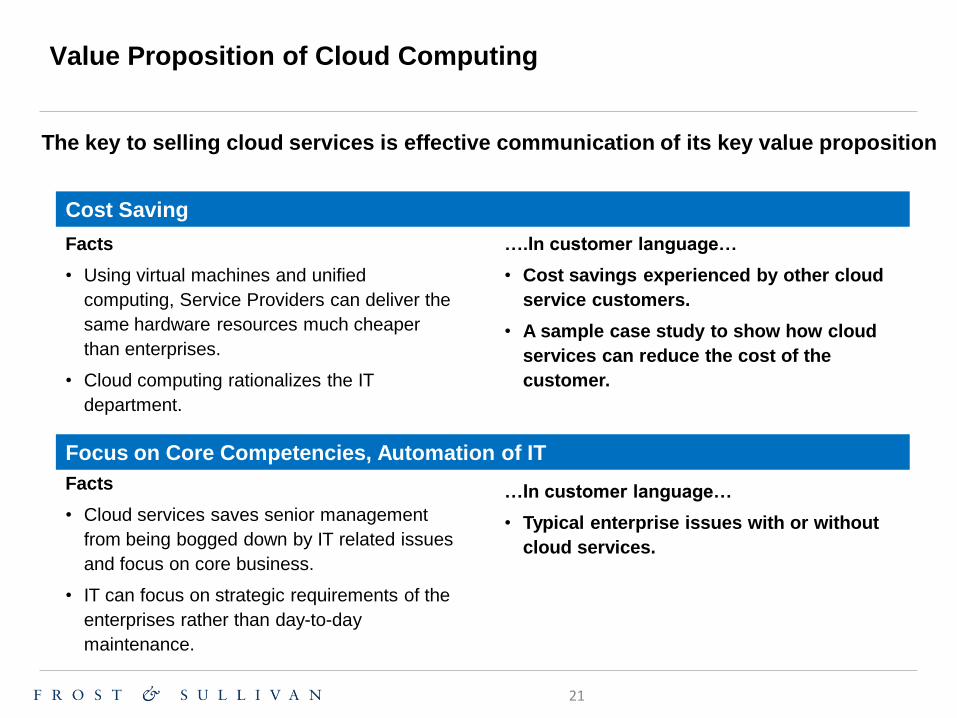

The key to selling cloud services is effective communication of its key value proposition

Facts

• Using virtual machines and unified

computing, Service Providers can deliver the

same hardware resources much cheaper

than enterprises.

• Cloud computing rationalizes the IT

department.

….In customer language…

• Cost savings experienced by other cloud

service customers.

• A sample case study to show how cloud

services can reduce the cost of the

customer.

Facts

• Cloud services saves senior management

from being bogged down by IT related issues

and focus on core business.

• IT can focus on strategic requirements of the

enterprises rather than day-to-day

maintenance.

…In customer language…

• Typical enterprise issues with or without

cloud services.

Value Proposition of Cloud Computing

Focus on Core Competencies, Automation of IT

Cost Saving

21

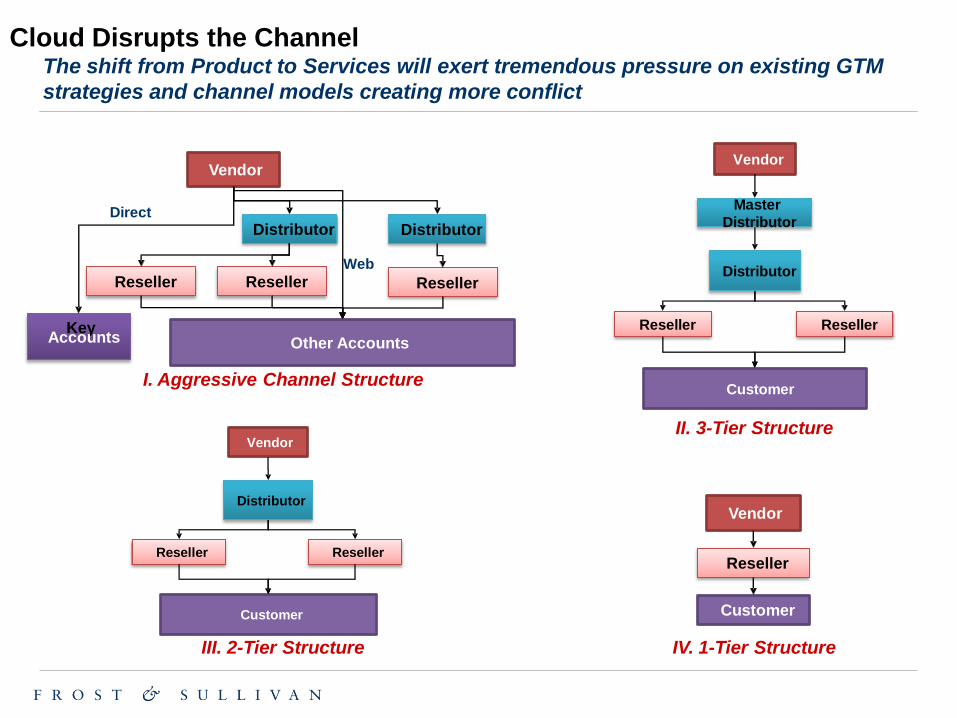

Cloud Disrupts the Channel

I. Aggressive Channel Structure

III. 2-Tier Structure

II. 3-Tier Structure

IV. 1-Tier Structure

The shift from Product to Services will exert tremendous pressure on existing GTM

strategies and channel models creating more conflict

Vendor

Key Accounts

Distributor

Reseller Reseller

Other Accounts

Distributor

Reseller

Direct

Web

Vendor

Master Distributor

Reseller Reseller

Customer

Distributor

Vendor

Reseller Reseller

Customer

Distributor

Vendor

Reseller

Customer

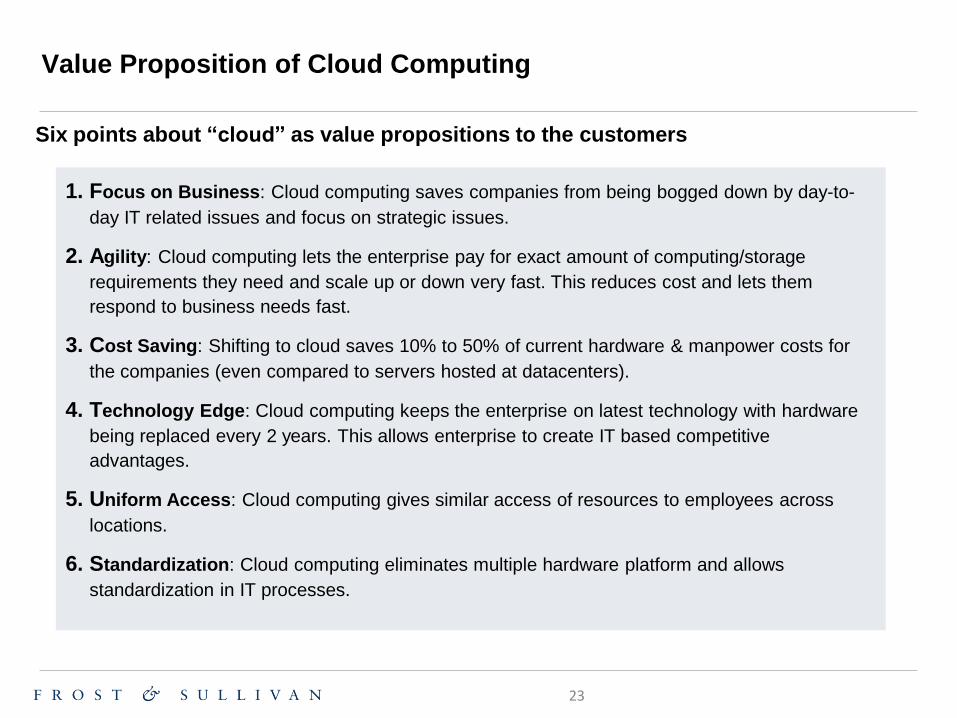

Value Proposition of Cloud Computing

Six points about “cloud” as value propositions to the customers

1. Focus on Business: Cloud computing saves companies from being bogged down by day-to-

day IT related issues and focus on strategic issues.

2. Agility: Cloud computing lets the enterprise pay for exact amount of computing/storage

requirements they need and scale up or down very fast. This reduces cost and lets them

respond to business needs fast.

3. Cost Saving: Shifting to cloud saves 10% to 50% of current hardware & manpower costs for

the companies (even compared to servers hosted at datacenters).

4. Technology Edge: Cloud computing keeps the enterprise on latest technology with hardware

being replaced every 2 years. This allows enterprise to create IT based competitive

advantages.

5. Uniform Access: Cloud computing gives similar access of resources to employees across

locations.

6. Standardization: Cloud computing eliminates multiple hardware platform and allows

standardization in IT processes.

23

Increasing Demand has Led to Entry of Global Market Participants

• Foreign investments in the Telecom sector and the expansion plans of local players into the

Broadband Wireless Access has attracted the attention of the global players, such as Google,

Amazon, NetSuite, Salesforce, RightNow, Oracle and Zoho have entered the Indonesian market,

primarily through channel partners.

• These participants currently hold a large share of the market with limited offerings from local service

providers.

• In terms of user segments, Manufacturing dominates the adoption level across verticals in

Indonesia. Further, the SMBs and Large Businesses contributed almost equally to the market in 2010,

a trend which is expected to continue in the medium term.

The Indonesian Cloud Computing market has been witnessing increasing traction

from local enterprises as they learn more and more about the delivery model and the

opportunity to decrease costs and bring in efficiencies.

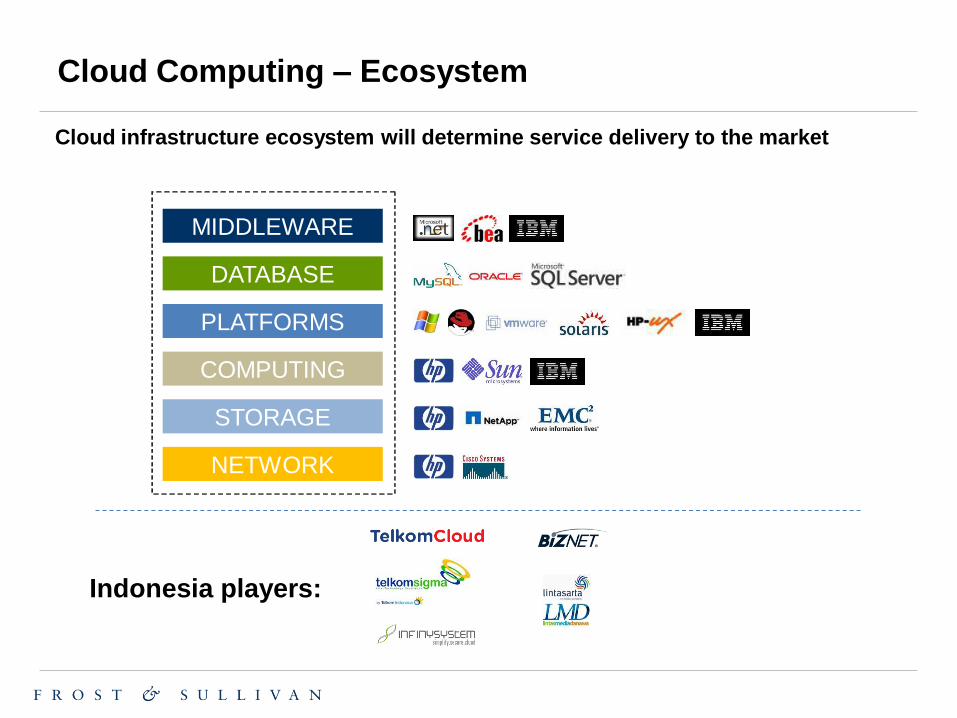

Cloud Computing – Ecosystem

MIDDLEWARE

DATABASE

PLATFORMS

STORAGE

COMPUTING

NETWORK

Cloud infrastructure ecosystem will determine service delivery to the market

Indonesia players:

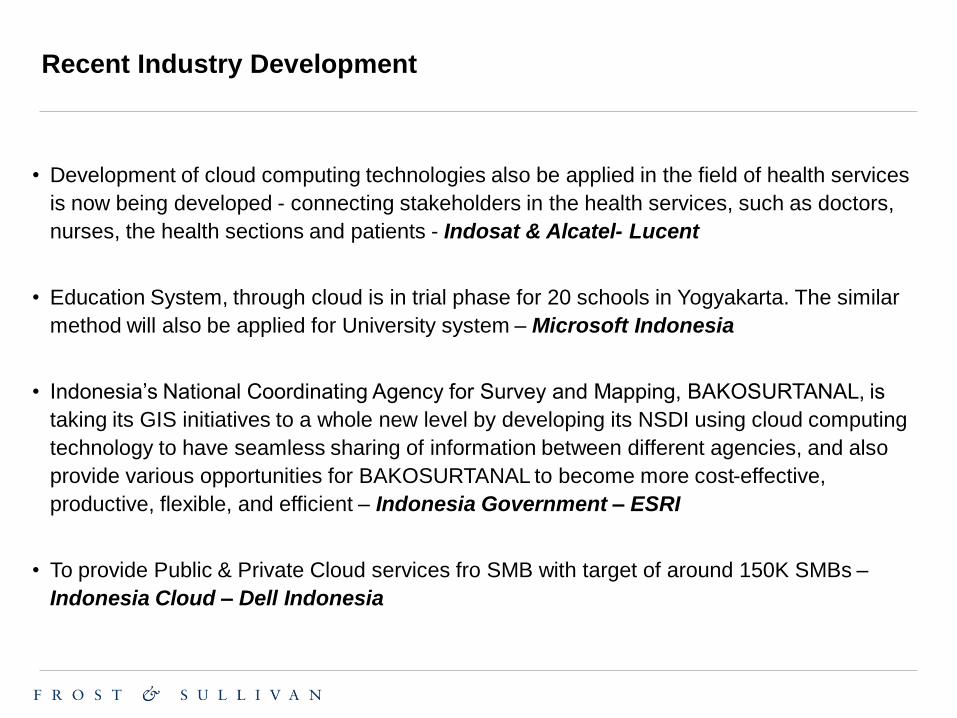

Recent Industry Development

• Development of cloud computing technologies also be applied in the field of health services

is now being developed - connecting stakeholders in the health services, such as doctors,

nurses, the health sections and patients - Indosat & Alcatel- Lucent

• Education System, through cloud is in trial phase for 20 schools in Yogyakarta. The similar

method will also be applied for University system – Microsoft Indonesia

• Indonesia’s National Coordinating Agency for Survey and Mapping, BAKOSURTANAL, is

taking its GIS initiatives to a whole new level by developing its NSDI using cloud computing

technology to have seamless sharing of information between different agencies, and also

provide various opportunities for BAKOSURTANAL to become more cost-effective,

productive, flexible, and efficient – Indonesia Government – ESRI

• To provide Public & Private Cloud services fro SMB with target of around 150K SMBs –

Indonesia Cloud – Dell Indonesia

Key Takeaways

• Significant market potential within the next 5 years with projected CAGR of 39%

• Communication & education to the market is key initial step in introducing

“Cloud” to alleviate general issues of security & privacy of public cloud

• Some industry trend that create market pull & to the cloud development incl.

booming on smartphone & tablet demand, fast adoption on social network, and

pressure on high CAPEX for telecom

• Some issues that can hinder development of cloud going forward; in area of

market education, security, infrastructure, & regulation – to be solved in order for

the industry to be fully taking off

• To identify what customers looking for in subscribing to the “cloud”; from

security issues up to support & certification i.e. to provide them with trust &

security

• To communicate to customer using their language & to forward cloud’s value

propositions

The Frost & Sullivan Story

30

Pioneered Emerging Market & Technology Research

• Global Footprint Begins

• Country Economic Research

• Market & Technical Research

• Best Practice Career Training

• MindXChange Events

Partnership Relationship with Clients

• Growth Partnership Services

• GIL Global Events

• GIL University

• Growth Team Membership™

• Growth Consulting

Visionary Innovation

• Mega Trends Research

• CEO 360 Visionary Perspective

• GIL Think Tanks

• GIL Global Community

• Communities of Practice

What Makes Us Unique

31

All services aligned on growth to help clients develop and implement

innovative growth strategies

Continuous monitoring of industries and their convergence, giving

clients first mover advantage in emerging opportunities

More than 40 global offices ensure that clients gain global perspective

to mitigate risk and sustain long term growth

Proprietary Team Methodology integrates 7 critical research

perspectives to optimize growth investments

Career research and case studies for the CEOs’ Growth Team to ensure

growth strategy implementation at best practice levels

Close collaboration with clients in developing their research based

visionary perspective to drive GIL

Focused on Growth

Industry Coverage

Global Footprint

Career Best Practices

360 Degree Perspective

Visionary Innovation Partner

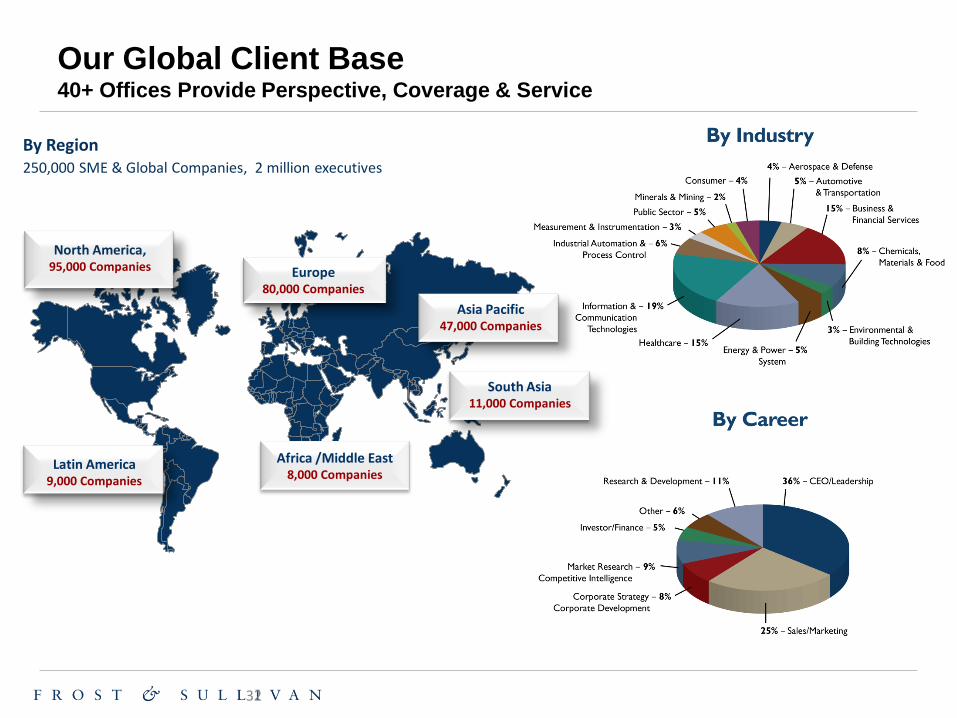

Our Global Client Base 40+ Offices Provide Perspective, Coverage & Service

32

Others, 40.0%

By Region 250,000 SME & Global Companies, 2 million executives

North America, 95,000 Companies Europe

80,000 Companies

Latin America 9,000 Companies

South Asia 11,000 Companies

Africa /Middle East 8,000 Companies

Asia Pacific 47,000 Companies

Our Industry Coverage

33

Automotive &

Transportation

Aerospace & Defense Measurement & Instrumentation

Information & Communication Technologies

Healthcare Environment & Building Technologies

Energy & Power Systems

Chemicals, Materials & Food

Electronics & Security

Industrial Automation & Process Control

Automotive Transportation & Logistics

Consumer Technologies

Minerals & Mining

Our Research Methodology Integration of Research Methodologies Provide 360 Degree Perspective

34

Idea Generation for Growth Pipeline

Comprehensive Evaluation of Opportunities

Reduced Risk and Enhanced Accuracy

Best Practices in Strategy Implementation

Foundation for Visionary Perspective

Innovative Growth Strategies

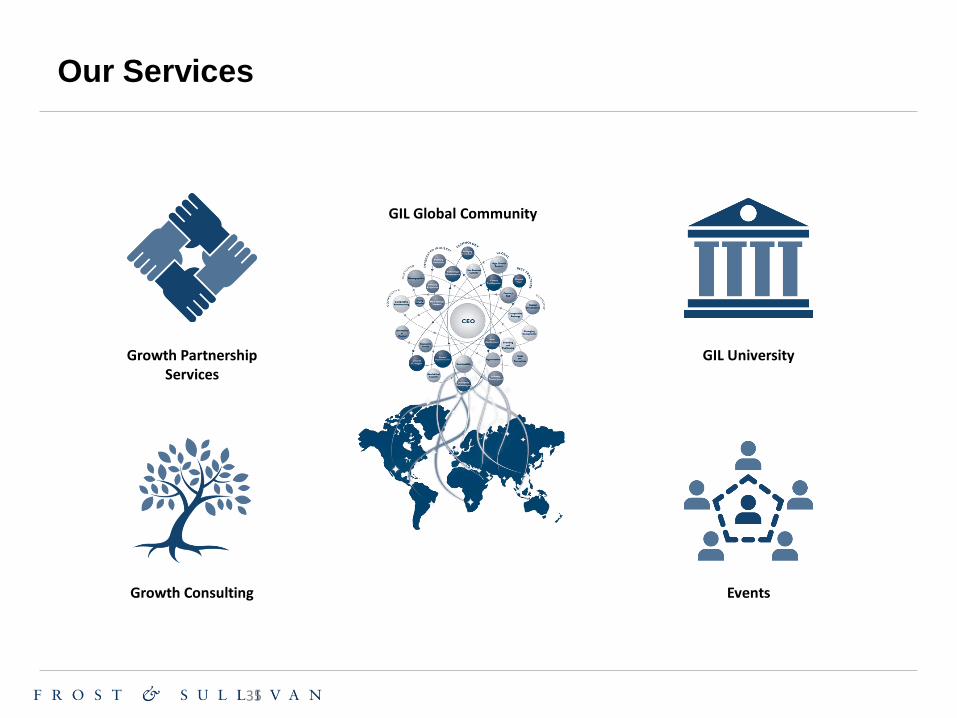

Our Services

35

Growth Partnership Services

Growth Consulting

GIL University

Events

GIL Global Community

GIL Global Community: Growth, Innovation and Leadership

36

• CEO Roundtables

• Best Practice Research

• Mega Trends

• Analyst Briefings

• Webinars

• GIL Events

• Newsletters

• Growth Workshops.

• Networking

• Community Forums

• Blogs and Wikis

• Visionary Scenarios

• Think Tanks

• Solution Wheels

• Industry Thought Leaders

• Career Tracks

• Benchmarking

GIL Event Schedule

GIL Middle East, FEBRUARY

GIL Thailand, MARCH

GIL APAC, APRIL

GIL Europe, MAY

GIL Russia, MAY

GIL Japan, JUNE

GIL Korea, JUNE

GIL Continental Europe, JULY

GIL South Africa, AUGUST

GIL Silicon Valley, SEPTEMBER

GIL India, OCTOBER

GIL Indonesia, OCTOBER

GIL China, NOVEMBER

GIL Australia, NOVEMBER

GIL Latin America, DECEMBER

Growth Team Membership™: GTM Application of Best Practices Career Research

37

Deliverables

• Interactive Events

• Best Practices Guidebooks

• Career Toolkits

• Case Histories

• Growth Workshops

• Think Tanks

Impact

• Faster Implementation Speed

• Avoidance of Mistakes Already Made

• Elimination of Reinventing the Wheel

• Acceleration of Problem Solving

• Continuous Problem Solving

• Continuous Productivity Improvement

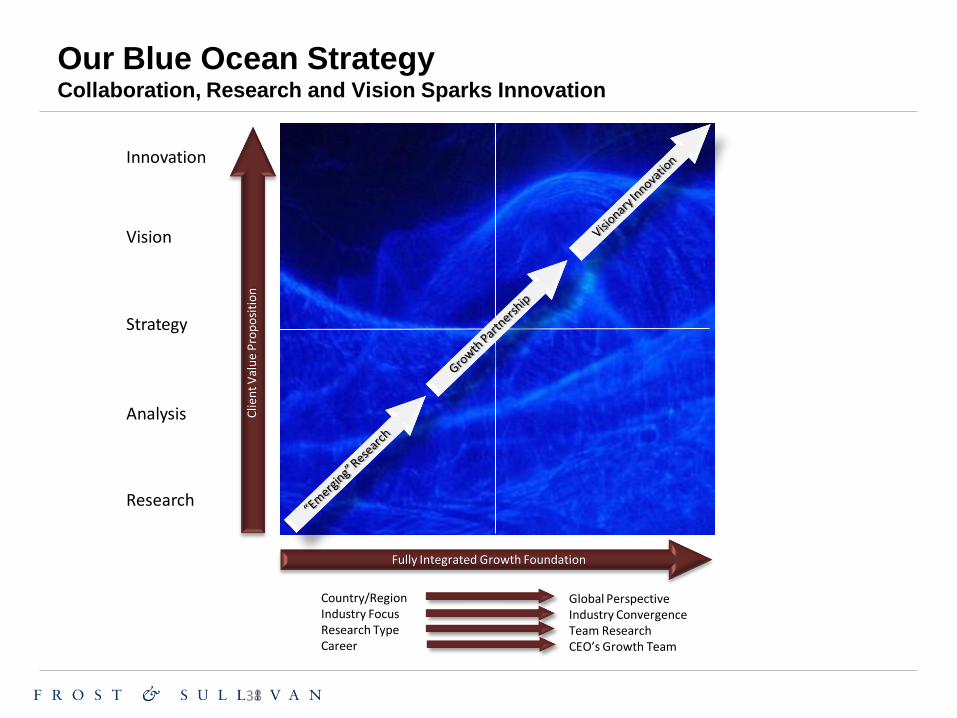

Our Blue Ocean Strategy Collaboration, Research and Vision Sparks Innovation

38

Research

Analysis

Strategy

Vision

Innovation

Country/Region Industry Focus Research Type Career

Global Perspective Industry Convergence Team Research CEO’s Growth Team

Clie

nt

Val

ue

Pro

po

siti

on

Fully Integrated Growth Foundation

Frost & Sullivan, the Growth Partnership Company, enables clients to accelerate growth and achieve best-in-class positions in growth, innovation and leadership. The company's Growth Partnership Service provides the CEO and the CEO's Growth Team with disciplined research and best-practice models to drive the generation, evaluation, and implementation of powerful growth strategies. Frost & Sullivan leverages 50 years of experience in partnering with Global 1000 companies, emerging businesses and the investment community from more than 40 offices on six continents. To join our Growth Partnership, please visit http://www.frost.com

Contact:

Dewi Nuraini

Corporate Communications, Frost & Sullivan

Phone : (+6221) 571.0838 / 571.3246

Email : [email protected]

About Frost & Sullivan

http://www.facebook.com/pages/Frost-Sullivan/

http://www.linkedin.com/companies/4506

http://www.slideshare.net/FrostandSullivan

http://twitter.com/frost_sullivan

http://twitter.com/FROST_ID