cmp 153 fy19e pe 9 -...

TRANSCRIPT

Kirloskar Brothers Ltd BUY

- 1 - Tuesday, 20th September, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

ST

OC

K P

OIN

TE

R

Target Price ` 317 CMP ` 153 FY19E PE 9.4X

Index Details Kirloskar Brothers Ltd (KBL) faced a rough patch in 2016. The sharp

sell off in crude oil prices disrupted the business model of its most

profitable operations (SPP Pumps Ltd, UK). Further the prolonged

drought and challenges of working with Indian Government bodies

sharply impacted its domestic operations. For FY16, The company

reported a net loss of Rs 32.2 crore, which came as a wakeup call for

the management. With a view to stem losses and turnaround its

business operations, the company has undertaken a massive

restructuring exercise across all verticals. This in our opinion is a

favourable move and should restore KBL back to profitability. In

addition the Government’s thrust on agriculture and infrastructure

augurs well for growth, and KBL being the largest pump player is

expected to be the biggest beneficiary.

We expect consolidated sales to grow at a CAGR of 6.6% over FY17-

19 from Rs 2,594 cr in FY16 to Rs 3,139 cr by FY19 on the back of

healthy growth in the product business (expected CAGR growth of

8.6% to Rs 2,770 cr by FY19). While EBITDA is expected to grow at a

CAGR of 57.9% from Rs 65.3 cr in FY16 to Rs 257 cr by FY19,

earnings are expected to grow at a faster clip of 263.1% CAGR to Rs

139.7 cr over the same period.

We Initiate coverage on KBL Brothers as a BUY with the price

objective of Rs 317- representing a potential upside of 107% from

the CMP of Rs 153. At the CMP of Rs 153 the stock is trading at

12.7X and 9.0X its estimated earnings for FY18 and FY19. We have

assigned a PE multiple of 18X (average PE multiple of 18X) on FY19

EPS of Rs 17.6 to arrive at the target price

We are optimistic about the company’s prospects given that:

1. The share of the unorganized sector in the pump market has fallen from 60% in FY10 to 44% in FY15. We expect the share to further fall to 35% by FY18. This shift is expected to drive revenue growth for the products business of KBL.

Sensex 28,634

Nifty 8,808

Industry Industrial Machinery

Scrip Details

MktCap (` cr) 1,217.7

BVPS (`) 121.8

O/s Shares (Cr) 7.94

AvVol 76,167

52 Week H/L 219/113

Div Yield (%) 0.3

FVPS (`) 2.0

Shareholding Pattern

Shareholders %

Promoters 65.4

Public 34.6

Total 100.0

KBL vs. Sensex

0

50

100

150

200

250

300

350

0

5000

10000

15000

20000

25000

30000

35000

Sep

-13

Dec-1

3

Mar-

14

Ju

n-1

4

Sep

-14

Dec-1

4

Mar-

15

Ju

n-1

5

Sep

-15

Dec-1

5

Mar-

16

Ju

n-1

6

Sep

-16

KBL Sensex

Key Financials (` in Cr)

Y/E Mar Net

Sales EBITDA PAT

EPS

(`)

EPS

Growth (%)

RONW

(%)

ROCE

(%)

P/E

(x)

EV/EBITDA

(x)

2016 2,594.4 65.3 (33.2) -4.2 -180.9 -3.4 1.4 NA 24.6 2017E 2,756.5 125.4 35.8 4.5 207.6 3.6 6.5 36.6 12.6 2018E 2,914.0 204.0 98.9 12.5 176.7 9.2 12.5 13.2 7.3 2019E 3,139.2 256.9 139.7 17.6 41.2 11.7 16.3 9.4 5.4

- 2 - Tuesday, 20th September, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

2. In the medium term, monsoon 2016 being at par with Long Period

Average (LPA) augurs well for the standard pumps segment. With rainfall projected at 94-104% of the LPA, we expect renewed vigor in enquiries for pumps

3. The Government’s focus on creating 100 smart cities and its

thrust on affordable housing for all (11 crore dwelling units) is a Rs 13.3 lac cr opportunity. KBL being the market leader is expected to be the biggest beneficiary.

4. KBL has undertaken a restructuring exercise across all business verticals -

The company is diversifying its UK operations from predominately Offshore Oil and Gas to downstream and desalination projects which are much more stable and carry a far lower risk. This is expected to drive the order book going forth.

Non performance of the projects business has prompted KBL to limit its exposure to this segment. Instead, it has decided to refocus on its stronghold i.e the products segment. This should restore profitability in the future.

To complete the range of product offerings of Kirloskar Ebara, KBL has acquired Rodelta, whose products are a strategic fit.

KBL has initiated talks with state Government bodies to revive stalled projects. This should clear dead inventories and clean up its balance sheet. It is also looking at alternatives to boost the off-take of its manufactured equipment.

- 3 - Tuesday, 20th September, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Company Background

KBL Brothers Limited (KBL) is a global pump manufacturing company with

expertise in engineering and the manufacture of systems for fluid

management. The company provides complete solutions for large

infrastructure projects in the areas of water supply, power plants, irrigation, oil

& gas and marine & defence.

Entity-wise performance of KBL

Particulars (Rs in crores) Country Stake (%) Sales (Mar 16) PBT (Mar 16) PAT (Mar 16)

PARENT COMPANY

Kirloskar Brothers Ltd India 1,680.0 6.0 12.0

SUBSIDIARY COMPANIES

Kirloskar Brothers International B V Netherland 100 873.0 (16.0) (15.0)

The Kolhapur Steel Ltd. India 96 39.0 (5.0) (5.0)

Kirloskar Corrocoat Pvt Ltd. India 65* 46.0 5.0 3.0

Kirloskar Systech India 100 22.0 7.0 5.0

Karad Projects & Motors Ltd. India 100 263.0 5.0 5.0

JOINT VENTURE COMPANIES

Kirloskar Ebara Pumps India 45# 71.0 (13.0) (12.0)

TOTAL 2,994.0 (10.0) (8.0)

Less: Intra Group Transactions (372.0) (17.0) (17.0)

Goodwill Amortisation (7.0) (7.0)

TOTAL (KBL) 2,622.0 (34.0) (32.0)

Source: KBL, Ventura Research # 45% held by Ebara Corp * 35% held by Corrocoat UK

- 4 - Tuesday, 20th September, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Key Investment Highlights

Indian pumps sector set for robust growth

Estimates on the size of the Indian pump market vary from Rs 8,500-12,000 cr

as not much data is available [as bulk of the market ~44% is unorganized]. In

comparison to the global market, which is pegged to grow at a 6% CAGR to

USD 56 bn in CY 2017 from USD 47 bn in CY 2014, the Indian market is

expected to grow at a robust rate of 10-12% CAGR by FY19.

The Indian pump industry can be classified on the basis of user segments as

shown below.

Agriculture: The demand for pumps from the agri sector was disrupted over

the last couple of years due to severe drought. The demand from this segment

diminishes when rainfall is excessive or exceedingly low, while it thrives best

when rainfall is reasonable. With rainfall projected at 94-104% of the LPA, we

expect renewed vigor in enquiries for pumps. The central allocation of Rs

20,000 cr to irrigation & water conservation will keep demand elevated for

pumps. Further, the GOI is increasingly focusing on off grid solar pumps for

agri use. This is expected to propel demand for the high margin solar pumps.

Sector wise market share of Pumps in India

Agriculture, ̀ 2295, 27%

Building services, `1615,

19%

Waste & Wastewater,

`1445, 17%

Power generation, `1020,

12%

Oil and Gas,

`680, 8%

Metals and Mining, `340,

4%

Others, `1105, 13%

Source: FICCI report, Ventura Research

Highly fragmented

retail market

- 5 - Tuesday, 20th September, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Modi Govt’s thrust on irrigation & energy efficient pumps to further fuel

demand

The central government has clearly spelt out its aim to increase the irrigation

penetration domestically. In the Union Budget FY16-17, the Government

allocated Rs 5,840 cr to irrigation. Moreover it has laid emphasis on fast

tracking of 89 irrigation projects under the Accelerated Irrigation Benefit

Programme (outlay of ~Rs 17,000 crore in FY17) and a further Rs 86,500

crore has been earmarked to be spent over the next five years. This should

propel demand going ahead for KBL.

Building Services: Increasing urbanization has led the horizontal expansion

of India's cities, putting stress on their infrastructure. However with

urbanization expected to only accelerate, vertical growth is the only option.

This should foster the growth of Building services. Further the Govt is focused

on creating 100 smart cities and affordable housing for all (expected to lead to

the construction of 11 crore dwelling units) by 2022. This massive

infrastructure push would need investments to the tune of Rs 13.3 lac crore.

With pumps being an integral part of building services, the demand is only

expected to be strong. And KBL, by virtue of being the largest player, is

expected to be the biggest beneficiary.

Water & Wastewater: The ambitious Smart Cities project, Swacch Bharat

Mission and the emphasis on better sanitation, safe disposal of waste/sewage,

clean water for all is expected to propel the demand for pumps.

Power Generation: The installed capacity for power is projected to grow to

463.54 GW by 2022 from the current 275 GW. Increased usage of washed

coal and expansion of nuclear power should boost the demand for pumps.

KBL’s market share dominance in the pump sector to continue

KBL, by virtue of its century old experience in pumps, commands the highest

market share of 12%. Considering the fact that ~44% of the pump market is

unorganized, KBL has a 21.5% market share within the organized sector. We

expect KBL to retain its market leadership position in the domestic pump

business due to its wide product range and superior distribution network.

- 6 - Tuesday, 20th September, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Best placed to take advantage of the shift in the pump business

from the unorganized to organized sector

The unorganized sector is mainly dominated by assemblers, cheap imports or

SME players who do not have much expertise in manufacturing cost efficient

pumps. The unorganized sector has dominated purely on the basis of cheap

pricing. Our channel checks suggest that the unorganized sector pumps are

~30-40% cheaper than pumps offered by the organized sector. However this

cheap pricing is purely optical. The maintenance cost & power consumption

costs (~85-90% of the cost over the life of the pump) of these inefficient

pumps far outweigh the cost of procurement. Increased awareness has led to

a gradual shift away from the unorganized sector towards organized players.

As a result the share of the unorganized sector has tumbled from 60% in 2010

to 45% in 2014 and is expected to further fall to 35% in FY18

KBL has the highest market share in the pump industry in India

Unorganised, 44%

Kirloskar Bros, 12%

CRI, 11%

KSB Pumps, 8%

Crompton Greaves, 7%

Texmo, 6%

Grundfos, 4%

WPIL, 3%V Guard, 2% Others, 3%

Source: KBL, Ventura Research

- 7 - Tuesday, 20th September, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Restructuring across territories after a rough FY16

KBL ran into a rough patch during FY16 on the back of slow order off take

and orders put on hold in its contracting business, which accounted for ~25%

of its consolidated business.

UK subsidiary- highest profit maker turning red

Historically the debt free UK business was the highest profit generating entity

of KBL and alone contributed Rs ~55 cr of the consolidated PBIT of the

company. However the UK operations of KBL took an ugly turn in FY16 and

posted a net loss of Rs 8 cr.

What went wrong?

About 40% of the UK’s order book comes from the offshore Oil and Gas sector

to which KBL was one of the three suppliers. However as the crude oil

collapsed to below $50 per barrel, the operations of all the North Sea offshore

industries were rendered unviable (Break-even of $65). This has severely

affected order flows and no revival is anticipated given the bleak outlook for oil

prices. Restructuring measures undertaken

On the back of several restructuring measures, the management expects that

the operations in 2017 would not be a replica of 2016 and the company will

not lose cash. However it will be an uphill task to attain the operational levels

of 2013/2014.

Power cost forms a major portion of pump cost over its life cycle

Maintenance Cost, 15%

Power Cost, 70%

Initial Cost, 15%

Source: KBL , Ventura Research

Steady fall in contribution of unorganized sector expected to continue

40%

56%65%

60%

44%35%

FY10 FY15 FY18

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Organised Unorganised

Source: KBL, Ventura Research

- 8 - Tuesday, 20th September, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

In order to revive the UK operations the management has pivoted from the

offshore Oil and Gas industry to the downstream Oil and Gas segment and

desalination projects. These businesses are much more stable and carry far

lower risk. KBL has been receiving favourable enquiries from players in the

downstream and desalination industry. These could convert into sales

considering the rich expertise of KBL in complex pumps, which require a lot of

commissioning support.

Acquisition of Rodelta temporarily dented bottomline for FY16

KBL acquired Rodelta in July 2015, when it was in receivership mode

(equivalent of a BIFR case in India).The Acqusition of Rodelta is strategically

very important as it is an almost exact fit to the missing products in KBL

Ebara’s (Indian Subsidiary of KBL) portfolio. Further Rodelta also holds

approvals from Statoil and Shell and this was something KBL Ebara was

seeking since long. The acquisition is strategic not only from the customer

access perspective but from the angle of completion of KBL Ebara's portfolio

as well.

Rodelta’s order book was zero on the date of acquisition as the company had

gone into receivership seven months prior to it. The company had

accumulated losses of ~ Rs 7.5 cr for 2015 which were absorbed by KBL in its

consolidated numbers.

Shifting focus from the less certain project business to the steady

products segment

KBL which historically was only into the products business, forayed into the

project business sighting the high margins. The lack of execution experience

and inability to deal with the vagaries of Govt methods of working and

changing policies took its toll on the profitability of KBL. Slower economic

growth, unavailability of land, unviable projects initiated by contractees and

customers’ inability to take delivery due to the liquidity crunch further

hampered the projects business.

Restructuring of business operation to stem losses from the project

business

KBL has consciously chosen to avoid projects which entail considerable

amount of civil works. Further as a policy it has chosen to focus strictly on its

skills set and supply systems to existing EPC players. These contracts are

entered only if they fall in the framework of their terms and conditions.

- 9 - Tuesday, 20th September, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

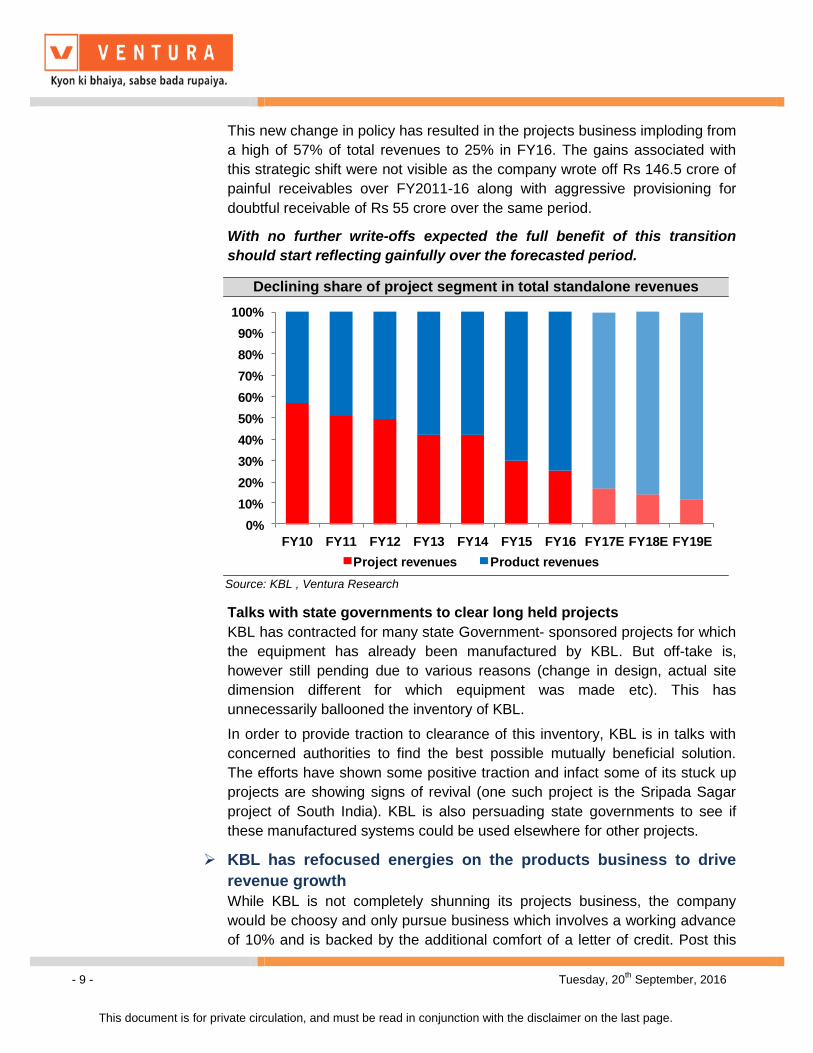

This new change in policy has resulted in the projects business imploding from

a high of 57% of total revenues to 25% in FY16. The gains associated with

this strategic shift were not visible as the company wrote off Rs 146.5 crore of

painful receivables over FY2011-16 along with aggressive provisioning for

doubtful receivable of Rs 55 crore over the same period.

With no further write-offs expected the full benefit of this transition

should start reflecting gainfully over the forecasted period.

Talks with state governments to clear long held projects

KBL has contracted for many state Government- sponsored projects for which

the equipment has already been manufactured by KBL. But off-take is,

however still pending due to various reasons (change in design, actual site

dimension different for which equipment was made etc). This has

unnecessarily ballooned the inventory of KBL.

In order to provide traction to clearance of this inventory, KBL is in talks with

concerned authorities to find the best possible mutually beneficial solution.

The efforts have shown some positive traction and infact some of its stuck up

projects are showing signs of revival (one such project is the Sripada Sagar

project of South India). KBL is also persuading state governments to see if

these manufactured systems could be used elsewhere for other projects.

KBL has refocused energies on the products business to drive

revenue growth

While KBL is not completely shunning its projects business, the company

would be choosy and only pursue business which involves a working advance

of 10% and is backed by the additional comfort of a letter of credit. Post this

Declining share of project segment in total standalone revenues

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

Project revenues Product revenues

Source: KBL , Ventura Research

- 10 - Tuesday, 20th

September, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

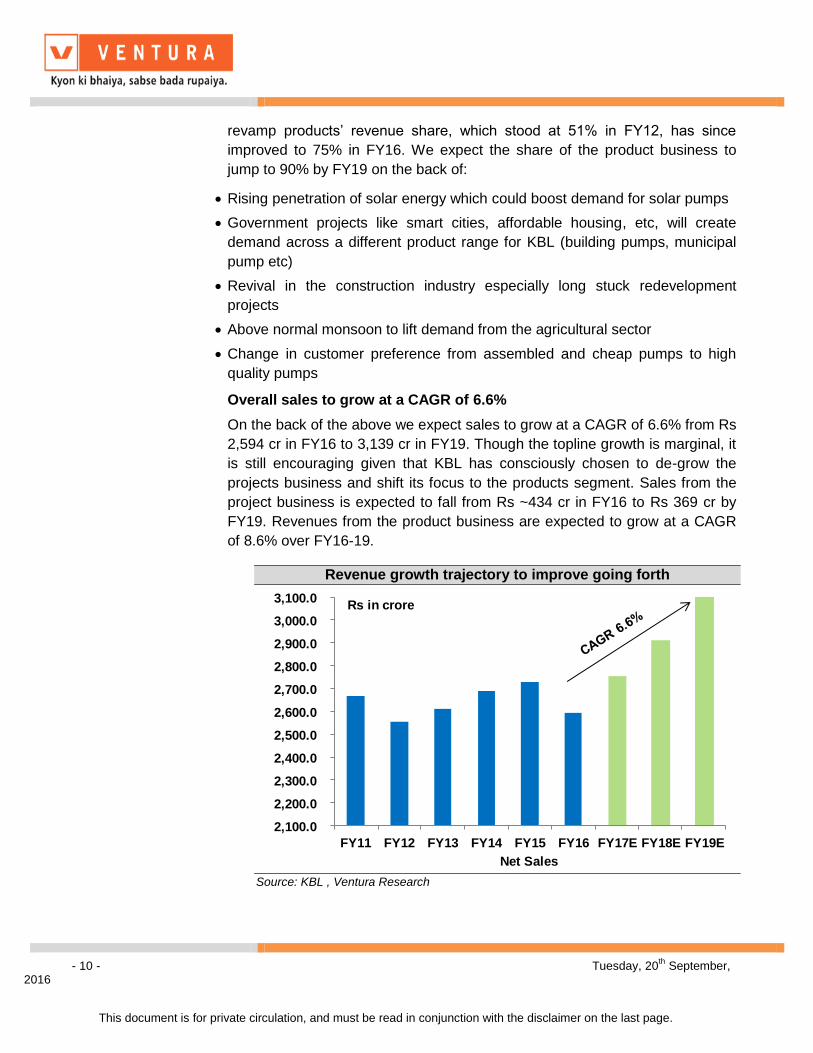

revamp products’ revenue share, which stood at 51% in FY12, has since

improved to 75% in FY16. We expect the share of the product business to

jump to 90% by FY19 on the back of:

Rising penetration of solar energy which could boost demand for solar pumps

Government projects like smart cities, affordable housing, etc, will create

demand across a different product range for KBL (building pumps, municipal

pump etc)

Revival in the construction industry especially long stuck redevelopment

projects

Above normal monsoon to lift demand from the agricultural sector

Change in customer preference from assembled and cheap pumps to high

quality pumps

Overall sales to grow at a CAGR of 6.6%

On the back of the above we expect sales to grow at a CAGR of 6.6% from Rs

2,594 cr in FY16 to 3,139 cr in FY19. Though the topline growth is marginal, it

is still encouraging given that KBL has consciously chosen to de-grow the

projects business and shift its focus to the products segment. Sales from the

project business is expected to fall from Rs ~434 cr in FY16 to Rs 369 cr by

FY19. Revenues from the product business are expected to grow at a CAGR

of 8.6% over FY16-19.

Revenue growth trajectory to improve going forth

2,100.0

2,200.0

2,300.0

2,400.0

2,500.0

2,600.0

2,700.0

2,800.0

2,900.0

3,000.0

3,100.0

FY11 FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

Rs in crore

Net Sales

Source: KBL , Ventura Research

- 11 - Tuesday, 20th

September, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Revamp in the projects business to drive potential margin boost

Consolidated EBITDA margins of the company fell to an all time low of 2.5% in

FY16 mainly driven by

Cost overruns, receivable write off’s and high provisioning in the project

business

Cyclical headwinds in the UK operation

Acquisition of Rodelta

Denial of an extension of license for steam turbines, which was a highly

profitable business

In order to improve profitability, the management has taken several corrective

measures which in our opinion should be meaningfully accretive.

We expect a steady revival in the fortunes of KBL going forth as EBITDA

margins are expected to rise from the current 2.5% to 8.2% by FY19.

Consolidated PAT margins are expected to revive post FY16 from -1.3% to

4.4% by FY19.

Substantial margin improvement going forth

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

FY11 FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

EBITDA Margin PAT margin

Source: KBL, Ventura Research

- 12 - Tuesday, 20th

September, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Capacity redundancy to lead to debt reduction

Across all its manufacturing capacities, the average utilization for FY16 has

been ~50-55%. The redundancy in the system should be comfortable to cater

to the projected demand growth over the next two-three years.

Barring the maintenance capex of Rs 25-30 crores, not much further

investments in assets are foreseen and we believe that the priority use of cash

would be to pare down debt from the existing level of Rs 300 crore to Rs 150-

180 crore by FY19.

This is expected to improve the profitability materially.

Comfortable debt position going ahead

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

-

0.1

0.2

0.3

0.4

0.5

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19

Debt to Equity Interest Coverage

no of times no of times

Source: KBL, Ventura Research

Stable Debt/ EBITDA going forth

-

1.0

2.0

3.0

4.0

5.0

6.0

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19

Debt / EBITDA

no of times

Source: KBL, Ventura Research

- 13 - Tuesday, 20th

September, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Financial Performance

On a standalone basis for Q1 FY17, KBL reported a flattish trend in revenues

at Rs 357 cr (-1.5% YoY). Despite sluggish sales we are pretty upbeat as this

demonstrates agility on the part of the management to execute its strategic

shift (towards products) without degrowing the revenues. In line with its other

focus to clean up its balance sheet, KBL wrote of high receivables and cost

over runs incurred in the project business. As a result margins took a hit of 50

bps YoY to 3.3%. The bottomline slumped to report a loss of Rs 3.2 cr (in

comparison to a profit of Rs 7.7 cr posted in Q1 FY16) on the back of a steep

decline in non operating income to 2.2 cr (11.5 cr in Q1 FY16).

In FY16, KBL’s consolidated net sales stood at Rs 2,721 crore registering a

degrowth of 4.4% YoY. EBITDA slumped 65.7% YoY to Rs 65.3 cr in FY16

against Rs 190.4 cr in FY15 on the back of huge losses in the domestic

project business and a debacle of the UK operations. EBITDA margins fell to a

life time low of 2.5% as compared to 7.0% YoY. This led to a net loss of Rs

32.2 cr in FY16 as compared to a profit of Rs 45.3 cr in FY15.

Quarterly Financial Performance (Rs crores)

Description Q1FY17# Q1FY16# FY16* FY15*

Net Sales 356.8 362.4 2,594.4 2,727.9

Growth (%) (1.5) (4.9)

Total expenditure 345.1 348.6 2,529.1 2,537.4

EBITDA 11.7 13.8 65.3 190.4

Margin (%) 3.3 3.8 2.5 7.0

Depreciation 9.7 10.2 77.1 94.7

EBIT (Ex. OI) 2.0 3.6 (11.8) 95.7

Non-Operating Income 2.2 11.5 30.3 17.2

EBIT 4.2 15.1 18.5 112.9

Margin (%) 1.2 4.2 0.7 4.1

Finance Cost 7.9 8.9 52.3 50.5

Exceptional Items - -

PBT (3.7) 6.2 (33.8) 62.4

Margin (%) (1.0) 1.7 (1.3) 2.3

Provision for Tax (0.5) (1.5) (1.5) 17.1

Profit after Tax (3.2) 7.7 (32.3) 45.3

Margin (%) (0.9) 2.1 (1.2) 1.7

Source: KBL, Ventura Research (# represents standalone, * represents consolidated)

- 14 - Tuesday, 20th

September, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Financial Outlook

The strategic shift in focus from the painful projects business to the much

more stable products business is expected to bring about a revival in the

fortunes of KBL. We expect consolidated sales to grow at a CAGR of 6.6%

over FY17-19 on the back of a healthy growth in the product business; the

product segment is expected to grow at a CAGR of 8.6% from ~2160 cr in

FY16 to 2,770 cr in FY19.

Inflection point for revenues going forth

-2%

0%

2%

4%

6%

8%

10%

23

24

25

26

27

28

29

30

31

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19

Net Sales EBITDA Margin PAT margin

Rs (in 000 crore)

Source: KBL , Ventura Research

Improvement in return ratios going ahead

-5

0

5

10

15

20

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19

RoCE RoE

%

Source: KBL , Ventura Research

Stable working capital days ahead

20

30

40

50

60

70

80

90

100

110

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19

Credit Days Inventory Days Debtor Days

no of days

Source: KBL , Ventura Research

- 15 - Tuesday, 20th

September, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Valuation

We Initiate coverage on KBL as a BUY with a price objective of Rs 317-

representing a potential upside of 107% from the CMP of Rs 153. At the CMP of

Rs 153 the stock is trading at 12.7X and 9.0X its estimated earnings for FY18

and FY19. We have assigned a PE multiple of 18X (average PE multiple of 18X)

on the FY19 EPS of Rs 17.6 to arrive at the target price. We are positive on the

company on account of the following factors:

Pedigree of management which deserves a higher multiple

Despite implosion of the projects business we expect the topline to show

slight growth (CAGR of 6.6%) propelled by the faster augmentation of

the products business

Margin profile to scale back to steady state levels of 7-8% from the

abysmal 2.5% clocked in FY16.

Cleaning up of the balance sheet with aggressive receivables write off

Foray into new segments of downstream Oil and Gas and desalination to

present new opportunities

Closure of decade old projects segment to lead to improved cash flow

and stem losses going forth

1-Yr Fwd P/E Band

0

100

200

300

400

500

Aug-09 Aug-10 Aug-11 Aug-12 Aug-13 Aug-14 Aug-15 Aug-16

CMP 10X 14X 18X 22X 26X

Source: KBL, Ventura Research

- 16 - Tuesday, 20th

September, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

1-Yr Fwd EV/EBITDA Band

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Aug-09 Aug-10 Aug-11 Aug-12 Aug-13 Aug-14 Aug-15 Aug-16

EV 6X 8X 10X 12X 14X

Rs in cr

Source: KBL, Ventura Research

1-Yr Fwd P/B Band

0

50

100

150

200

250

300

350

400

Aug-09 Aug-10 Aug-11 Aug-12 Aug-13 Aug-14 Aug-15 Aug-16

CMP 0.9X 1.3X 1.7X 2.1X 2.5X

Source: KBL, Ventura Research

- 17 - Tuesday, 20th

September, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

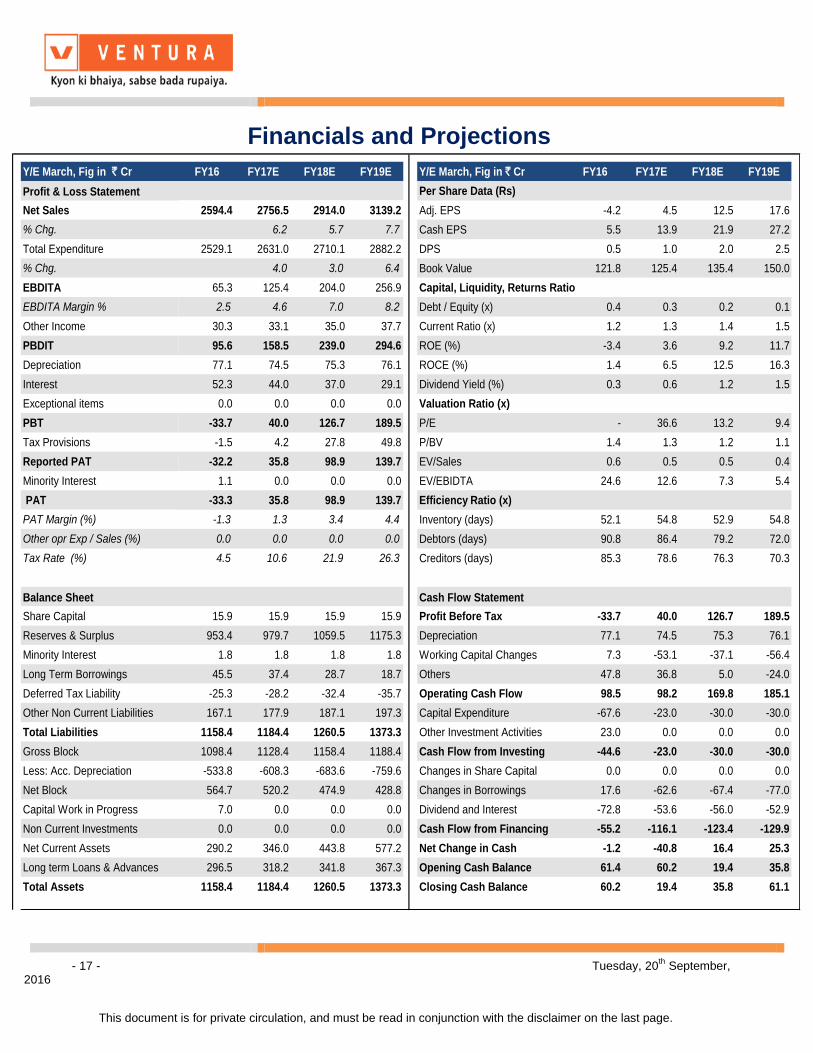

Financials and Projections

Y/E March, Fig in ` Cr FY16 FY17E FY18E FY19E Y/E March, Fig in ` Cr FY16 FY17E FY18E FY19E

Profit & Loss Statement Per Share Data (Rs)

Net Sales 2594.4 2756.5 2914.0 3139.2 Adj. EPS -4.2 4.5 12.5 17.6

% Chg. 6.2 5.7 7.7 Cash EPS 5.5 13.9 21.9 27.2

Total Expenditure 2529.1 2631.0 2710.1 2882.2 DPS 0.5 1.0 2.0 2.5

% Chg. 4.0 3.0 6.4 Book Value 121.8 125.4 135.4 150.0

EBDITA 65.3 125.4 204.0 256.9 Capital, Liquidity, Returns Ratio

EBDITA Margin % 2.5 4.6 7.0 8.2 Debt / Equity (x) 0.4 0.3 0.2 0.1

Other Income 30.3 33.1 35.0 37.7 Current Ratio (x) 1.2 1.3 1.4 1.5

PBDIT 95.6 158.5 239.0 294.6 ROE (%) -3.4 3.6 9.2 11.7

Depreciation 77.1 74.5 75.3 76.1 ROCE (%) 1.4 6.5 12.5 16.3

Interest 52.3 44.0 37.0 29.1 Dividend Yield (%) 0.3 0.6 1.2 1.5

Exceptional items 0.0 0.0 0.0 0.0 Valuation Ratio (x)

PBT -33.7 40.0 126.7 189.5 P/E - 36.6 13.2 9.4

Tax Provisions -1.5 4.2 27.8 49.8 P/BV 1.4 1.3 1.2 1.1

Reported PAT -32.2 35.8 98.9 139.7 EV/Sales 0.6 0.5 0.5 0.4

Minority Interest 1.1 0.0 0.0 0.0 EV/EBIDTA 24.6 12.6 7.3 5.4

PAT -33.3 35.8 98.9 139.7 Efficiency Ratio (x)

PAT Margin (%) -1.3 1.3 3.4 4.4 Inventory (days) 52.1 54.8 52.9 54.8

Other opr Exp / Sales (%) 0.0 0.0 0.0 0.0 Debtors (days) 90.8 86.4 79.2 72.0

Tax Rate (%) 4.5 10.6 21.9 26.3 Creditors (days) 85.3 78.6 76.3 70.3

Balance Sheet Cash Flow Statement

Share Capital 15.9 15.9 15.9 15.9 Profit Before Tax -33.7 40.0 126.7 189.5

Reserves & Surplus 953.4 979.7 1059.5 1175.3 Depreciation 77.1 74.5 75.3 76.1

Minority Interest 1.8 1.8 1.8 1.8 Working Capital Changes 7.3 -53.1 -37.1 -56.4

Long Term Borrowings 45.5 37.4 28.7 18.7 Others 47.8 36.8 5.0 -24.0

Deferred Tax Liability -25.3 -28.2 -32.4 -35.7 Operating Cash Flow 98.5 98.2 169.8 185.1

Other Non Current Liabilities 167.1 177.9 187.1 197.3 Capital Expenditure -67.6 -23.0 -30.0 -30.0

Total Liabilities 1158.4 1184.4 1260.5 1373.3 Other Investment Activities 23.0 0.0 0.0 0.0

Gross Block 1098.4 1128.4 1158.4 1188.4 Cash Flow from Investing -44.6 -23.0 -30.0 -30.0

Less: Acc. Depreciation -533.8 -608.3 -683.6 -759.6 Changes in Share Capital 0.0 0.0 0.0 0.0

Net Block 564.7 520.2 474.9 428.8 Changes in Borrowings 17.6 -62.6 -67.4 -77.0

Capital Work in Progress 7.0 0.0 0.0 0.0 Dividend and Interest -72.8 -53.6 -56.0 -52.9

Non Current Investments 0.0 0.0 0.0 0.0 Cash Flow from Financing -55.2 -116.1 -123.4 -129.9

Net Current Assets 290.2 346.0 443.8 577.2 Net Change in Cash -1.2 -40.8 16.4 25.3

Long term Loans & Advances 296.5 318.2 341.8 367.3 Opening Cash Balance 61.4 60.2 19.4 35.8

Total Assets 1158.4 1184.4 1260.5 1373.3 Closing Cash Balance 60.2 19.4 35.8 61.1

- 18 - Tuesday, 20th

September, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Disclosures and Disclaimer Ventura Securities Limited (VSL) is a SEBI registered intermediary offering broking, depository and portfolio management services to clients. VSL is member of BSE, NSE and MCX-SX. VSL is a depository participant of NSDL. VSL states that no disciplinary action whatsoever has been taken by SEBI against it in last five years except administrative warning issued in connection with technical and venial lapses observed while inspection of books of accounts and records. Ventura Commodities Limited, Ventura Guaranty Limited, Ventura Insurance Brokers Limited and Ventura Allied Services Private Limited are associates of VSL. Research Analyst (RA) involved in the preparation of this research report and VSL disclose that neither RA nor VSL nor its associates (i) have any financial interest in the company which is the subject matter of this research report (ii) holds ownership of one percent or more in the securities of subject company (iii) have any material conflict of interest at the time of publication of this research report (iv) have received any compensation from the subject company in the past twelve months (v) have managed or co-managed public offering of securities for the subject company in past twelve months (vi) have received any compensation for investment banking merchant banking or brokerage services from the subject company in the past twelve months (vii) have received any compensation for product or services from the subject company in the past twelve months (viii) have received any compensation or other benefits from the subject company or third party in connection with the research report. RA involved in the preparation of this research report discloses that he / she has not served as an officer, director or employee of the subject company. RA involved in the preparation of this research report and VSL discloses that they have not been engaged in the market making activity for the subject company. Our sales people, dealers, traders and other professionals may provide oral or written market commentary or trading strategies to our clients that reflect opinions that are contrary to the opinions expressed herein. We may have earlier issued or may issue in future reports on the companies covered herein with recommendations/ information inconsistent or different those made in this report. In reviewing this document, you should be aware that any or all of the foregoing, among other things, may give rise to or potential conflicts of interest. We may rely on information barriers, such as "Chinese Walls" to control the flow of information contained in one or more areas within us, or other areas, units, groups or affiliates of VSL. This report is for information purposes only and this document/material should not be construed as an offer to sell or the solicitation of an offer to buy, purchase or subscribe to any securities, and neither this document nor anything contained herein shall form the basis of or be relied upon in connection with any contract or commitment whatsoever. This document does not solicit any action based on the material contained herein. It is for the general information of the clients / prospective clients of VSL. VSL will not treat recipients as clients by virtue of their receiving this report. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of clients / prospective clients. Similarly, this document does not have regard to the specific investment objectives, financial situation/circumstances and the particular needs of any specific person who may receive this document. The securities discussed in this report may not be suitable for all investors. The appropriateness of a particular investment or strategy will depend on an investor's individual circumstances and objectives. Persons who may receive this document should consider and independently evaluate whether it is suitable for his/ her/their particular circumstances and, if necessary, seek professional/financial advice. And such person shall be responsible for conducting his/her/their own investigation and analysis of the information contained or referred to in this document and of evaluating the merits and risks involved in the securities forming the subject matter of this document. The projections and forecasts described in this report were based upon a number of estimates and assumptions and are inherently subject to significant uncertainties and contingencies. Projections and forecasts are necessarily speculative in nature, and it can be expected that one or more of the estimates on which the projections and forecasts were based will not materialize or will vary significantly from actual results, and such variances will likely increase over time. All projections and forecasts described in this report have been prepared solely by the authors of this report independently of the Company. These projections and forecasts were not prepared with a view toward compliance with published guidelines or generally accepted accounting principles. No independent accountants have expressed an opinion or any other form of assurance on these projections or forecasts. You should not regard the inclusion of the projections and forecasts described herein as a representation or warranty by VSL, its associates, the authors of this report or any other person that these projections or forecasts or their underlying assumptions will be achieved. For these reasons, you should only consider the projections and forecasts described in this report after carefully evaluating all of the information in this report, including the assumptions underlying such projections and forecasts. The price and value of the investments referred to in this document/material and the income from them may go down as well as up, and investors may realize losses on any investments. Past performance is not a guide for future performance. Future returns are not guaranteed and a loss of original capital may occur. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice. We do not provide tax advice to our clients, and all investors are strongly advised to consult regarding any potential investment. VSL, the RA involved in the preparation of this research report and its associates accept no liabilities for any loss or damage of any kind arising out of the use of this report. This report/document has been prepared by VSL, based upon information available to the public and sources, believed to be reliable. No representation or warranty, express or implied is made that it is accurate or complete. VSL has reviewed the report and, in so far as it includes current or historical information, it is believed to be reliable, although its accuracy and completeness cannot be guaranteed. The opinions expressed in this document/material are subject to change without notice and have no obligation to tell you when opinions or information in this report change. This report or recommendations or information contained herein do/does not constitute or purport to constitute investment advice in publicly accessible media and should not be reproduced, transmitted or published by the recipient. The report is for the use and consumption of the recipient only. This publication may not be distributed to the public used by the public media without the express written consent of VSL. This report or any portion hereof may not be printed, sold or distributed without the written consent of VSL. This document does not constitute an offer or invitation to subscribe for or purchase or deal in any securities and neither this document nor anything contained herein shall form the basis of any contract or commitment whatsoever. This document is strictly confidential and is being furnished to you solely for your information, may not be distributed to the press or other media and may not be reproduced or redistributed to any other person. The opinions and projections expressed herein are entirely those of the author and are given as part of the normal research activity of VSL and are given as of this date and are subject to change without notice. Any opinion estimate or projection herein constitutes a view as of the date of this report and there can be no assurance that future results or events will be consistent with any such opinions, estimate or projection. This document has not been prepared by or in conjunction with or on behalf of or at the instigation of, or by arrangement with the company or any of its directors or any other person. Information in this document must not be relied upon as having been authorized or approved by the company or its directors or any other person. Any opinions and projections contained herein are entirely those of the authors. None of the company or its directors or any other person accepts any liability whatsoever for any loss arising from any use of this document or its contents or otherwise arising in connection therewith. The information contained herein is not intended for publication or distribution or circulation in any manner whatsoever and any unauthorized reading, dissemination, distribution or copying of this communication is prohibited unless otherwise expressly authorized. Please ensure that you have read “Risk Disclosure Document for Capital Market and Derivatives Segments” as prescribed by Securities and Exchange Board of India before investing in Securities Market. Ventura Securities Limited

Corporate Office: 8th Floor, ‘B’ Wing, I Think Techno Campus, Pokhran Road no. 02, Off Eastern Express Highway , Thane (West) 400 607.

- 19 - Tuesday, 20th

September, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.