cnb community bancorp, inc. - county national bank€¦ · · 2013-06-18cnb community bancorp,...

TRANSCRIPT

2012 Annual Report

CNB Community Bancorp, Inc.

Banking that Starts in Your Communityand Stays in Your Community

Front (L to R)

Stephen J. Maddalena, General Manager, Kentwood Office Furniture Judy R. Gabriele, Director of Development, Hillsdale Community Health Center Craig S. Connor, President & Chief Executive Officer, County National Bank John E. Barrett, President, Eagle Funeral Homes, Inc.

Back (L to R)

David W. Pope, Chairman, Powers Clothing, Inc.

John P. Lovinger, Attorney, Parker, Hayes & Lovinger, P.C.

Claude J. Rowley, President, Rowley, Inc.

Steven A. Wells, President, Wells Equipment Sales, Inc.

County National Bank | 2012 Board of Directors

Banking that Starts in Your Communityand Stays in Your Community

[ 2 ]

County National Bank | Banking that Starts in Your Community and Stays in Your Community

CountyNationalBank.com

TABLE OF CONTENTS

Board of Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Inside Cover

Company Profile . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Page 1

Financial Highlights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Page 2

Executive Letter . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Page 3 - 11

Officer Photos . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Back Cover

CountyNationalBank .com

[ 1 ]

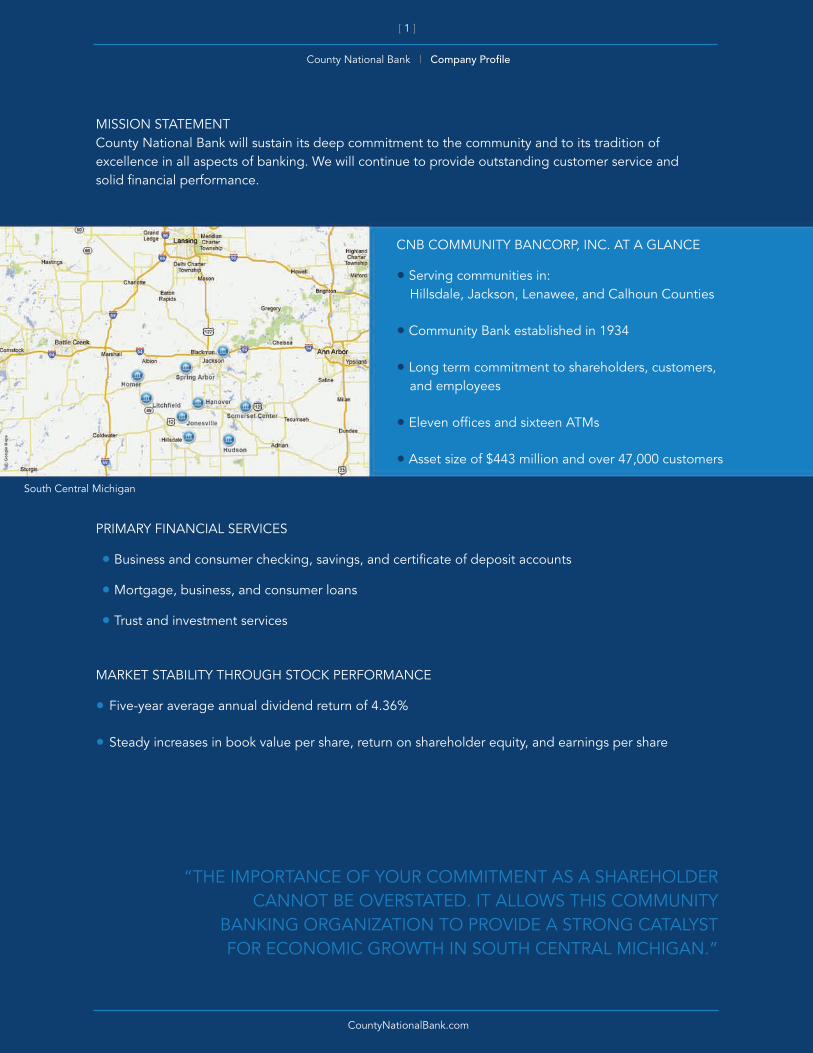

County National Bank | Company Profile

CNB COMMUNITY BANCORP, INC . AT A GLANCE

• Serving communities in: Hillsdale, Jackson, Lenawee, and Calhoun Counties

• Community Bank established in 1934

• Long term commitment to shareholders, customers, and employees

• Eleven offices and sixteen ATMs

• Asset size of $443 million and over 47,000 customers

PRIMARY FINANCIAL SERVICES

• Business and consumer checking, savings, and certificate of deposit accounts

• Mortgage, business, and consumer loans

• Trust and investment services

MARKET STABILITY THROUGH STOCK PERFORMANCE

• Five-year average annual dividend return of 4 .36%

• Steady increases in book value per share, return on shareholder equity, and earnings per share

MISSION STATEMENT County National Bank will sustain its deep commitment to the community and to its tradition of excellence in all aspects of banking . We will continue to provide outstanding customer service and solid financial performance .

South Central Michigan

“THE IMPORTANCE OF YOUR COMMITMENT AS A SHAREHOLDER CANNOT BE OVERSTATED . IT ALLOWS THIS COMMUNITY

BANKING ORGANIZATION TO PROVIDE A STRONG CATALYST FOR ECONOMIC GROWTH IN SOUTH CENTRAL MICHIGAN .”

CountyNationalBank.com

[ 2 ]

County National Bank | Financial Highlights

2012 COMPARISON HIGHLIGHTSFOR THE YEAR: 2012 2011 Income before federal income taxes $ 5,220,688 $ 4,958,271 Net income 3,711,938 3,434,678 Basic and diluted earnings per share 1 .84 1 .71 Cash dividends declared 1,733,438 1,682,106 Per share 0 .86 0 .84

AT YEAR END: Investment securities $ 25,917,557 $ 18,845,340 Loans held for sale 1,445,018 1,519,328 Net portfolio loans 316,578,540 307,912,951 Total assets 443,213,566 382,271,281 Deposits 391,246,000 324,600,177 Shareholders’ equity 34,953,806 32,771,743 Book value per share 17 .31 16 .35 Number of shares outstanding 2,018,703 2,004,003 Number of shareholders 360 368

2012 FIVE YEAR COMPARATIVE FINANCIAL SUMMARY In thousands, except per share data

2012 2011 2010 2009 2008ASSETS Cash and due from banks $ 70,298 $ 33,446 $ 21,270 $ 31,103 $ 17,308 Federal funds sold 440 263 470 322 879 Certificates of deposit 9,515 487 1,718 1,707 - U .S . Treasury and agency securities 3,909 6,462 3,966 8,076 8,394** State, municipal and other securities 22,009 12,383 18,194 15,760 10,354** Loans held for sale 1,445 1,519 1,316 194 553 Net loans 316,579 307,913 285,602 258,464 252,967 Other assets 19,019 19,798 14,411 14,730 12,685 TOTAL $ 443,214 $ 382,271 $ 346,947 $ 330,356 $ 303,140

LIABILITIES AND SHAREHOLDERS’ EQUITY Noninterest-bearing demand $ 72,323 $ 60,037 $ 49,199 $ 46,814 $ 36,904 Interest-bearing 318,923 264,563 253,878 237,852 219,351 Total deposits 391,246 324,600 303,077 284,666 256,255 FHLB advances and line of credit 15,495 22,531 10,328 13,490 16,050 Line of credit note payable 650 750 836 961 961 Other liabilities 869 1,618 1,764 1,639 997 Total shareholders’ equity 34,954 32,772 30,942 29,600 28,877 TOTAL $ 443,214 $ 382,271 $ 346,947 $ 330,356 $ 303,140

Book value per share $ 17 .31 $ 16 .35 $ 15 .50 $ 14 .88 $ 14 .55

Total interest and dividend income $ 17,953 $ 17,904 $ 17,057 $ 16,513 $17,225 Total interest expense 1,607 1,974 2,480 3,600 4,867 Net interest income 16,346 15,930 14,577 12,913 12,358 Provision for loan losses 1,245 1,915 1,945 1,579 661 Net interest income after provision for loan losses 15,101 14,015 12,632 11,334 11,697 Noninterest income 5,242 4,345 4,257 5,077 3,826 Noninterest expenses 15,122 13,402 12,775 12,770 13,038 Income before federal income taxes 5,221 4,958 4,114 3,641 2,485 Federal income taxes 1,509 1,523 1,184 1,252 954 Net income $ 3,712 $ 3,435 $ 2,930 $ 2,389 $ 1,531

Basic and diluted earnings per share $ 1 .84 $ 1 .71 $ 1 .47 $ 1 .20 $ 0 .77 Return on shareholders’ equity * 11 .3% 11 .1% 9 .9% 8 .1% 5 .1% Cash dividends per share $ 0 .86 $ 0 .84 $ 0 .82 $ 1 .00 $ 0 .91

* Based on shareholders’ equity at beginning of year . ** There was a reclassification in 2008 to conform to the 2009 presentation .

CASH DIVIDENDS PER SHARE BOOK VALUE PER SHARE

CountyNationalBank .com

[ 3 ]

County National Bank | Executive Letter

2012 WAS A VERY GOOD YEAR FOR CNB Community Bancorp, Inc . Our financial perfor-mance, shareholder return, growth in deposits and loans, and our commitment to providing financial services to the communities in which we do business all represent characteristics of a high performing community bank . I think as you look over the pages that follow you will be pleased with the results of our Bank’s efforts and your return on investment .

The importance of your commitment as a share-holder cannot be overstated . It allows this community banking organization to provide a strong catalyst for economic growth in south central Michigan and in turn, helps to elevate the quality of life for people in our market . Our Board, employees and customers thank you deeply for the financial investment you have made as a shareholder . Our Board and employ-ees pledge to use prudent and profitable management of our Bank’s capital resources so you will be rewarded for that investment .

Our efforts during 2012 produced the best earnings year in the Bank’s 78-year history . Earning $3,712,000 after tax was an outstanding accomplishment . The main drivers of improved net income were: increased mortgage loan activity made possible by the record low mortgage loan rates, a reduction in provision for loan loss expense, and continued good management of the spread between interest income and interest expense .

2012 net profit represents per share earnings of $1 .84, an 8% increase from 2011 . Return on average equity was 11 .3%, up from 11 .1% for 2011 . Book value per share increased 96¢ to $17 .31, and the real dollar amount of capital growth after dividends was $2,182,000 . Our dividend payout was 86¢ per share or 47% of earnings . Our provision for loan loss account now stands at $5,503,000 or 1 .70% of loans outstanding . Net charge-offs for the year were $1,355,000, or .43% of average loans outstand-ing . The retention of earnings is very important as it helps build capital, which is needed to support the growth in our balance sheet .

“OUR EFFORTS DURING 2012

PRODUCED THE BEST EARNINGS YEAR

IN THE BANK’S 78-YEAR HISTORY .”

DIVIDEND YIELD:Based on Annual Cash Dividend DeclaredYield based on four quarter weighted average trading price at the end of each year

EARNINGS PER SHARE

11.1%

RETURN ON EQUITY Based on shareholders’ equity at beginning of year

11.1%

CountyNationalBank.com

[ 4 ]

County National Bank | Executive Letter

Organizational growth was outstanding during 2012 . Total assets under management grew to $829,376,000 from $745,752,000, up 11 .2% . Bank assets grew 16% to $443,214,000 . Loans serviced were $270,964,000, up $19,262,000 for the year . Trust assets ended the year at $107,261,000 with several million dollars in new trust accounts opened . Other assets being managed through sweep accounts and CDARS were $7,937,000 at year end .

LOAN PORTFOLIO Our loan portfolio is performing well . The increase of $8,723,000 in loan balances for 2012 helped to produce interest income of $17,246,000 . Increased competitive forces required us to lower interest rates charged to our borrowers in order to remain competitive . With this prolonged low rate environ-ment, we faced another year of decreasing yields on our loan and investment portfolio; however, our growth in loans allowed us to hold interest income to about where it was for 2011 .

Many of our customers were able to refinance their mortgages with us lowering our interest income . We compensated for this loss in revenue by grow-ing commercial real estate loans by $28,558,000 . Many banks in Michigan are seeing weak loan demand, as was the case last year, so they are actively seeking to purchase loan participations . We now have over $14,000,000 in commercial loans sold to other community banks, and this helps us to meet the needs of more commercial customers while utilizing less bank capital and deposits .

MORTGAGE LENDINGThe mortgage department had an outstand-ing year of mortgage production and growth . The residential mortgage serviced portfolio, those loans we have sold to Freddie Mac and to Federal Home Loan Bank of Indianapolis, grew to 2,581 mortgages totaling $256,313,000; this is a 5% increase over year end 2011 consist-ing of 2,486 mortgages totaling $244,314,000 .Our mortgage loan originations increased from 523 mortgages totaling $65,829,000 in 2011, to 773 mortgages totaling $102,065,000 in 2012; this is a 55% increase in originations from 2011 .Total income related to mortgage origination was $2,733,000, a record year for the mortgage area .

Jackson Advisory BoardExecutive Committee

Front Row, L to R: Sharon L. Burns, 2nd Vice President – C.F.O., Dorene M. Shaw, Vice President – Chief Auditor,

Lois E. Howard, Vice President – Commercial Loans, Mary P. Marshall, Vice President – Senior Trust OfficerBack Row, L to R:

Scott E. Evans, Vice President – Senior Mortgage Officer, Cindy Dwyer, Vice President – Technology, John R. Waldron, Senior Vice President – Senior Loan Officer, Diane K. Clow, Vice President – Director of Human Resources,

Spencer D. Swank, Executive Vice President & C.F.O., Craig S. Connor, President & C.E.O., Not pictured: Kelly D. Jensen, 2nd Vice President – Branch Administrator

Front Row, L to R: Donald J. Calbert, Richard M. CraftBack Row, L to R: Kurt J. Parker, Robert L. Simmons, Stephen J. Maddalena

CountyNationalBank .com

[ 5 ]

County National Bank | Executive Letter

LOSS MITIGATION As of year end 2012, we had seven properties in Other Real Estate Owned (OREO) with a balance of $779,000 . During the year, we sold eleven acquired properties with three pending sales in 2013 . Through this latest economic downturn, our staff has done a very good job keeping our OREO numbers very manageable .

Our loss mitigation department currently has processed 39 HAMPs (Home Affordable Modi-fication Program) . This is a federally sponsored program to help homeowners avoid foreclosure and stay in their homes by providing payment relief through lower interest rates and extended terms . In addition, the borrower can earn certain principal reductions by honoring the modification terms . In 2012, we completed 47 modifications that have kept families in their homes . Of these modifications, 76% of them are current or less than 30 days past due .

To benefit the Bank and our borrowers, the loss mitigation department has utilized the Michigan’s “Hardest Hit” program, Step Forward Michigan . These are federal dollars administered by the State of Michigan designed to help people avoid foreclosure because of delinquency . The borrower must apply and qualify for this program and our role has been one of a consultant, ushering the borrower through the process . Once qualified, these funds are paid on the loans and do not have to be repaid to the State of Michigan . The program assisted our distressed borrowers in receiving an aggregate of $71,000 in relief funds, which were used to bring their delinquent loans current .

“THE SMARTEST MOVE I MADE .” — JOHN HOOVER, CNB CUSTOMER

(L to R) John Hoover and Pistol – Owner, Wolverine Steel & WeldingBerry Malek, CRC, CTFA – Assistant Vice President – Trust Officer – CNB

CountyNationalBank.com

[ 6 ]

County National Bank | Executive Letter

CONSUMER LENDING In 2012, we originated 599 new loans totaling $14,000,000, down from the prior year . An extremely competitive rate environment in 2012 presented the challenge of balancing the Bank’s desire to offer competitive rates while maintaining our net interest margin .

We are excited to report that in 2013 the consumer lending department will begin to utilize a more dynamic loan software program to keep up with the ever-changing compliance and technology demands in today’s lending environment .

TRUST AND INVESTMENTS Our trust and investment group led by Mary Marshall saw good growth in both new accounts and assets under management . During the year, 64 new accounts were opened and the assets under management grew from $98,788,000 to $107,261,000 .

We continue to promote the benefits of doing business with a trust department of a local community bank . We have expertise in invest-ment management and this makes us a popular choice with those customers needing help with investing IRA, pension or 401(k) rollover dollars . Additionally, we are trying to bring awareness to the many benefits of fee for investment manage-ment services that we offer, compared to commission based investment management services many of our competitors offer .

We continue outreach to local Attorneys and CPAs in both Jackson and Hillsdale markets with special seminars, lunch and learn events, and telephone briefings . Our trust officers are regular guests on the bank-sponsored radio programs, and Tim Sullivan, AVP and trust officer, hosts a weekly radio show on WCSR Hillsdale .

BRANCH PERFORMANCE Each of our eleven branch offices experienced significant deposit growth in 2012, resulting in an average growth per office of 14 .7% . From 2011 through 2012, total bank deposits grew from

$324,600,000 to $391,246,000, or 20 .5% . As shown in the Bank Deposit Growth graph below, a comparison between total bank deposits in 2008 to total bank deposits in 2012 reveals an impressive 52 .7% increase .

We continue to look for ways to increase our market share, which includes improving the products and services we offer, as well as improvements to our delivery method . In 2012, we streamlined our checking account product offering to include e-Checking – a free checking account with the benefits of electronic statement delivery, online banking, bill payment service, and more . This account has appealed to many of our customers who appreciate the convenience of banking online .

Our branch officers and branch managers participated in an in-depth leadership training program in 2012 . They were able to quickly put into action some of the ideas learned, leading to better communication among the branch staff and facilitating an improved ability to meet the financial needs of our customers . Plans are in place to extend the program to other managers and supervisors in 2013 .

TECHNOLOGY Technology plays an important role helping us to stay competitive in the market place and allowing our employees to become more efficient in their day to day activities . Our commitment to investing

BANK DEPOSIT GROWTH

CountyNationalBank .com

[ 7 ]

County National Bank | Executive Letter

in technology continued during 2012 with several projects completed .

Throughout the year, we purchased and installed 16 ATMs and cash machines that included more user-friendly features, including the American Disability Act features . The cost of this invest-ment in technology was $436,000 with the expense spread out over three to five years . In addition, all of our ATMs are now online, which allows for account information to be updated in real time, whereby withdrawals and deposits show immediately . This gives our customers better information and also helps to better control and prevent fraud .

Over the course of two years, we completed the replacement of 162 personal computers with a

comprehensive virtual desktop system, using technology that improves portability, manage-ability, and compatibility allowing us to become more efficient .

MARKETING Our community banking message of reinvesting in our markets is core to our culture, so we continued with the marketing focus of recycling deposits into loans to businesses and individuals . We expanded on that message through advertis-ing by talking about recycling some of our earnings into donations and contributions to a great many non-profit organizations, schools, events, and projects . All of which helps to make our communities better places in which to live .

“IT’S BANKING THAT STARTS IN YOUR COMMUNITY AND STAYS IN YOUR COMMUNITY”

Vermeulen’s Furniture:(L to R) Nate Vermeulen – Vice President, Bill Jors – 2nd VP Commercial Loan Officer, CNB, Lynn Vermeulen – President

CountyNationalBank.com

[ 8 ]

County National Bank | Executive Letter

“WE HAVE WORKED HARD OVER MANY YEARS TO DEVELOP A POSITIVE REPUTATION AND IMAGE…”

Our message was also supported by some of our great customers through testimonial ads, some of which are featured in this report . We hosted several luncheons for realtors, accountants, and attorneys to provide product and service information we thought would be of benefit to those groups . Additionally, we participated in many school and community events, promoting and supporting their efforts and taking advan-tage of the opportunity to meet with many community members .

We partnered with a number of area schools to present information to students about the American Bankers Association programs called “Get Smart about Credit” and “Teach Children to Save” . We also participated in the “Lights, Camera, Save!” program and worked with one area school that entered several videos in this contest . As part of our participation in the “Payback for Education” event, we hosted several Hillsdale County students at the bank and exposed them to various banking careers, in a hands-on setting .

For our efforts in the area of financial literacy, we were asked by the Michigan Bankers Association to make a presentation to the House Banking Committee in Lansing . We are proud of our efforts and equally proud to have been given the opportunity to report to this group .

We introduced a new product called Insured Cash Sweep (ICS), which allows for large deposits to be eligible for multi-million-dollar FDIC insurance . We have had success with introducing this product to businesses, municipalities, and school districts . We continue to promote our products and services, events, and financial information through our website, electronic newsletter, radio programs, and newspaper columns . As a community bank, we believe it is vitally important to truly be a part of our community – our staff members continue to serve through memberships on school boards and committees, service organizations, retail and economic development groups, churches, and non-profits .

CNB staff members participate in the Hillsdale County Fair Parade.

Craig Connor, CNB President & C.E.O, with Eric Macy & Richard Moore from the Hillsdale Rotary Club, and Sharon Bisher, Executive Director of the Hillsdale County Community Foundation, at Baw Beese Lake’s Sandy Beach. CNB is one of the donors of the Sandy Beach Renovation Project.

CountyNationalBank .com

[ 9 ]

County National Bank | Executive Letter

EMPLOYEE DEVELOPMENT AND RECRUITMENT Following our introduction in 2011 of providing training in “Service Excellence”, in 2012 we contin-ued this training to our branch officers and manag-ers focusing on “Leadership Training” . Plans are in place to extend this training to our lenders in 2013 .

On Veterans Day, arrangements were made to close the offices for this traditional banking holi-day in order to provide the Bank’s first ever staff-wide Training Day . Training took place at the local Michindoh Conference Center where employees received the required annual regulatory training, were updated on the Bank’s 2013 Marketing Plan, and reviewed the upcoming year’s employee benefit plans . While all training was an important part of this day, providing the staff with a day to reacquaint, reunite and refresh was an equally important benefit .

We are pleased to report the addition of two new officers to the Bank:

Stacey L . Clemens joined the Bank on January 9th as the Bank’s assistant vice president – compliance officer . Stacey brought over eight years of profes-sional experience, working in all areas of regulatory compliance and risk management . Stacey has an associate degree from Northwest State Community College and attended Defiance College . She is a Certified Regulatory Compliance Manager (CRCM), which she received from the Institute of Certified Bankers .

Chad E . Rumsey joined the Bank on January 9th as a commercial loan officer for the Jackson market area . Chad brings over 13 years of banking experience, including branch manager, treasury management and commercial lending . Chad has a B .A . in business administration from Grand Valley

Legacy Assisted Living Center:(L to R) Chad Rumsey – Commercial Loan Officer, CNB, Lloyd Ganton – C.E.O, Ganton Retirement Centers, Paul Buchholz – President & CFO, Ganton Retirement Centers

CountyNationalBank.com

[ 10 ]

County National Bank | Executive Letter

State University . Chad is a native of the Jackson area, and his knowledge of this market and the market’s commercial customers has been very productive for the Bank .

We also had several internal promotions within the officer group in 2012:

John R . Waldron was promoted from vice president – senior loan officer to senior vice president – senior loan officer on October 10th . John has been with the Bank since 2002, bringing previous commercial loan experience . He also worked with the U .S . Department of Treasury as a national bank examiner . John has a BBA in finance and a minor in accounting from Western Michigan University . John’s leadership and knowledge are instrumental to the success of our Bank . Considering the many regulatory challenges and high level of production and growth of the Bank’s loan areas, his contributions have been vitally important to our accomplishments .

Sharon L . Burns was promoted from second vice president – controller to second vice president and CFO on December 3rd . Sharon has been with the Bank since 2010, as well as having previously worked with a well-known area CPA firm . Sharon will have the overall responsibility for the financial accounting for the Bank . Sharon has a bachelor’s degree in accounting and a master’s degree in organizational management from Spring Arbor University . Sharon’s guidance to the Bank as CFO will be critical to the continued solid reputation of the Bank .

Kelly D . Jensen was promoted from assistant vice president – branch officer to second vice president – branch administrator on December 3rd . Kelly has over 35 years of banking experience in branch management as well as lending . Kelly will have responsibility of branch operations, with all branch managers and officers reporting directly to him . Kelly attended JCC focusing on business and also attended the American Institute of Banking . He has completed the Michigan Banker’s Association

Commercial Lending School and various other courses through the MBA . Kelly’s new leadership role for the branch offices will provide focused direction for the growth and development of the branch market .

Kelly L . Lantis was promoted to commercial credit officer on September 3rd . Kelly has over 24 years of service with County National Bank in the credit department and as a consumer loan officer . In 1993, Kelly made the decision to continue her service with the Bank in a part-time capacity while raising her family . She has returned as a full-time commercial credit officer . Kelly has a B .A . in finance from Hillsdale College, and has continued her education attending various work-related courses and seminars . Kelly’s knowledge has been key to the increased demands of credit administration .

Becky J . Wiley was promoted from human resource specialist and staff development to human resource specialist and staff development officer on October 10th . Becky joined the Bank in 2011 . Her background and 22 years of experience in the H .R . arena in a manufacturing setting has transitioned smoothly to the Bank . Becky has an associate degree from Northwest State Community College . She is a certified Professional in Human Resources (PHR) .

Branch Officer Linda Cavasin making a Teach Children to Save presentation.

CountyNationalBank .com

[ 11 ]

County National Bank | Executive Letter

In addition to her knowledge of the law governing H .R ., Becky is an innovative trainer and has developed programs to continue educating and building the skill sets of our staff .

RETIREMENT Spencer D . Swank announced his plans to retire as of January 31, 2013 . Spencer joined the Bank in March of 1998, as vice president and CFO, and is retiring from the banking business after a very successful career spanning 43 years . Spencer’s title of CFO and executive vice president did not do justice to the role he played at County National Bank these past 14 years . Spencer was the chief financial officer, branch administrator, chairman of the investment committee and the ALCO committee, risk man-agement officer, cashier of the Bank and had the overall responsibility for marketing, facilities and information technology . County National Bank has consistently performed very well through the years, but especially noteworthy is the Bank’s performance through the latest economic downturn . Spencer’s countless management contributions are in large part the reason behind

the Bank’s success and solid reputation . Spencer will be missed by our customers, Directors and staff; however, he has developed a very capable team of internal successors . We thank Spencer for many years of dedicated service to our organization, and wish him the best in his retirement years .

THE FUTURE Our future continues to be bright with growth opportunities in the markets in which we do business . We have worked hard over many years to develop a positive reputation and image; seeing this effort develop into so many quality referrals is very rewarding . We will continue to focus on providing you, the shareholders, with a very good return on your investment through the payment of dividends and the increase in equity . We plan to stay with the conservative banking business model that has served us so well, keeping us a safe and sound bank . Once again, we all, Directors and employees, would like to thank you for continued support of your locally owned community bank .

Craig S. Connor President & CEO

[ 2 ]

County National Bank | Banking that Starts in Your Community and Stays in Your Community

CountyNationalBank.com

L to R: Craig S. Connor, President & Chief Executive Officer,

Spencer D. Swank, Executive Vice President & Chief Financial Officer

Front, L to R: Suzanne L. Decker, Mortgage Officer, Brenda L. Carpenter, Mortgage Officer, Luann J. Crowley, 2nd Vice President – Mortgage Loans

Back, L to R: Debra K. Storer, Underwriter Operations Officer, Craig D. Talbert, Mortgage Officer, Jeffrey S. Jackson, Consumer Loan Officer, Phyllis J. Brooks, 2nd Vice President – Consumer Loans,

Scott E. Evans, Vice President – Senior Mortgage Officer, Randall L. Tate, Loss Mitigation Officer

Front, L to R: Stacey L. Clemens, Assistant Vice President – Compliance Officer, Dorene M. Shaw, Vice President – Chief Auditor, Debra S. Smith, 2nd Vice President – Accounting

Back, L to R: Sharon L. Burns, 2nd Vice President – CFO, Rae A. Organ, Assistant Vice President – Bank Secrecy & Security Officer

Front, L to R: Wendora K. Broesamle, Hillsdale Branch Officer, Linda C. Cavasin, Spring Arbor Branch Officer, Gwenda J. Ripley, Cortland/Jackson Branch Officer Back, L to R: Donald W. Germann, Jonesville Branch Officer, Michelle L. Caldwell, Litchfield Branch Officer,

Kelly D. Jensen, 2nd Vice President – Branch Administrator, Robin G. Pelham, Somerset Center Branch Officer, Craig R. Burlingame, Homer Branch Officer

Front, L to R: Timothy P. Sullivan, Assistant Vice President – Trust Officer, Mary P. Marshall, Vice President – Senior Trust Officer Back, L to R: Christine L. Walworth, Assistant Vice President – Trust Operations Officer, Barry A. Malek, Assistant Vice President – Trust Officer

Seated, L to R: David J. Kreger, Assistant Vice President – Commercial Loan Officer, Eric A. Potes, Commercial Loan Officer, William C. Jors, 2nd Vice President – Commercial Loan Officer Standing, L to R: John R. Waldron, Senior Vice President – Senior Loan Officer, Kelly L. Lantis, Commercial Credit Officer, Lois E. Howard, Vice President – Commercial Loans,

Ronald J. Haber, 2nd Vice President – Commercial Loans, Chad E. Rumsey, Commercial Loan Officer

Seated, L to R: Jill A. Taylor, Marketing & Public Relations Officer, Sandra K. Grimm, Assistant Vice President – Data Processing, Rebecca J. Wiley, Human Resources & Staff Development Officer Standing, L to R: Diane K. Clow, Vice President – Director of Human Resources, L. Michelle Heminger, 2nd Vice President – Administration, Cindy Dwyer, Vice President – Technology

County National Bank | 2012 Officers

Banking that Starts in Your Communityand Stays in Your Community

CountyNationalBank.com

Member FDICPrinted on 10% post consumer recycled paper

CNB Community Bancorp,

Inc.

Hillsdale, Michigan

Years Ended December 31, 2012 and 2011

Consolidated Financial

Statements

CNB COMMUNITY BANCORP, INC. TABLE OF CONTENTS PAGE

Independent Auditors’ Report 1 Consolidated Financial Statements for the Years Ended December 31, 2012 and 2011 Consolidated Balance Sheets 2 Consolidated Statements of Income 3 Consolidated Statements of Comprehensive Income 4 Consolidated Statements of Shareholders’ Equity 5 Consolidated Statements of Cash Flows 6 Notes to Consolidated Financial Statements 7-29

Rehmann Robson

675 Robinson Rd. Jackson, MI 49203 Ph: 517.787.6503 Fx: 517.788.8111

www.rehmann.com

1

INDEPENDENT AUDITORS’ REPORT March 1, 2013 Board of Directors and Shareholders CNB Community Bancorp, Inc. Hillsdale, Michigan We have audited the accompanying consolidated financial statements of CNB Community Bancorp, Inc. (the Corporation), which comprise the consolidated balance sheets as of December 31, 2012 and 2011, and the related consolidated statements of income, comprehensive income, shareholders’ equity and cash flows for the years then ended, and the related notes to the consolidated financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to fraud or error. Independent Auditors’ Responsibility Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free of material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on auditor judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the Corporation’s preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Corporation’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the consolidated financial position of CNB Community Bancorp, Inc. as of December 31, 2012 and 2011, and the consolidated results of their operations and their cash flows for the years then ended in accordance with accounting principles generally accepted in the United States of America.

CNB COMMUNITY BANCORP, INC.

CONSOLIDATED BALANCE SHEETS

December 31

2012 2011

Cash and due from banks 70,298,373$ 33,446,034$

Federal funds sold 440,187 262,961

Cash and cash equivalents 70,738,560 33,708,995

Certificates of deposit 9,515,000 487,000

Investment securities 25,917,557 18,845,340

Net portfolio loans 316,578,540 307,912,951

Loans held for sale 1,445,018 1,519,328

Accrued interest receivable 1,128,349 1,177,310

Premises and equipment, net 4,630,776 4,097,920

Bank-owned life insurance 4,167,285 4,051,082

Goodwill 2,590,750 2,590,750

Other assets 6,501,731 7,880,605

Total assets 443,213,566$ 382,271,281$

Deposits

Noninterest-bearing demand 72,323,190$ 60,037,273$

NOW, MMDA, and other interest-bearing deposits 172,055,368 121,528,286

Savings 72,987,097 64,572,430

Time 73,880,345 78,462,188

Total deposits 391,246,000 324,600,177

FHLB advances and line-of-credit 15,495,465 22,531,296

Other line-of-credit borrowings 650,000 750,000

Accrued interest payable 84,866 120,620

Other liabilities 783,429 1,497,445

Total liabilities 408,259,760 349,499,538

Commitments and contingencies (Notes 11, 12, 13 and 14)

Shareholders' equity

Common stock, no par value; 4,000,000 shares authorized,

2,018,703 shares issued and outstanding (2,004,003 at

December 31, 2011) 10,989,445 10,709,851

Unearned restricted stock awards (368,262) (251,713)

Retained earnings 24,171,693 22,193,193

Accumulated other comprehensive income 160,930 120,412

Total shareholders' equity 34,953,806 32,771,743

Total liabilities and shareholders' equity 443,213,566$ 382,271,281$

ASSETS

LIABILITIES AND SHAREHOLDERS' EQUITY

The accompanying notes are an integral part of these consolidated financial statements.

2

CNB COMMUNITY BANCORP, INC.

CONSOLIDATED STATEMENTS OF INCOME

Year Ended December 31

2012 2011

Interest and dividend income

Loans (including fees) 17,246,240$ 17,216,187$

Debt securities

Taxable 228,943 195,181

Tax-exempt 384,204 417,534

Dividends and other 93,780 74,654

Total interest and dividend income 17,953,167 17,903,556

Interest expense

Deposits 1,220,914 1,584,989

Borrowed funds 385,870 388,869

Total interest expense 1,606,784 1,973,858

Net interest income 16,346,383 15,929,698

Provision for loan losses 1,245,000 1,914,430

Net interest income, after provision for loan losses 15,101,383 14,015,268

Noninterest income

Service charges on deposit accounts 980,604 922,011

Trust fees 578,817 532,860

Net gain on loans sold 1,907,871 1,047,828

ATM service charges 901,533 803,989

Net loan servicing fees 99,163 191,774

Other 773,503 846,996

Total noninterest income 5,241,491 4,345,458

Noninterest expenses

Compensation and benefits 9,406,715 8,266,783

Occupancy and equipment 2,006,343 1,814,990

Professional fees 386,455 347,402

Printing, stationery and supplies 171,793 167,216

Other 3,150,880 2,806,064

Total noninterest expenses 15,122,186 13,402,455

Income before federal income taxes 5,220,688 4,958,271

Federal income taxes 1,508,750 1,523,593

Net income 3,711,938$ 3,434,678$

Net income per basic share of common stock 1.84$ 1.71$

The accompanying notes are an integral part of these consolidated financial statements.

3

CNB COMMUNITY BANCORP, INC.

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

Year Ended December 31

2012 2011

Unrealized holding gain (loss) on available-for-sale securities

arising during the year 61,518$ (64,063)$

Income tax (expense) benefit related to unrealized gain (loss) on

available-for-sale securities arising during the year (21,000) 22,000

Other comprehensive income (loss) 40,518 (42,063)

Net income 3,711,938 3,434,678

Comprehensive income 3,752,456$ 3,392,615$

The accompanying notes are an integral part of these consolidated financial statements.

4

CNB COMMUNITY BANCORP, INC.

CONSOLIDATED STATEMENTS OF SHAREHOLDERS' EQUITY

Unearned Accumulated

Restricted Other Total

Stock Retained Comprehensive Shareholders'

Shares Amount Awards Earnings Income Equity

Balances, January 1, 2011 1,996,673 10,566,140$ (226,628)$ $20,440,621 162,475$ 30,942,608$

Comprehensive income - - - 3,434,678 (42,063) 3,392,615

Restricted stock awards, net of

forfeitures (Note 15) 7,330 143,711 (25,085) - - 118,626

Dividends declared - $0.84

per share of common stock - - - (1,682,106) - (1,682,106)

Balances, December 31, 2011 2,004,003 10,709,851 (251,713) 22,193,193 120,412 32,771,743

Comprehensive income - - - 3,711,938 40,518 3,752,456

Restricted stock awards, net of

forfeitures (Note 15) 14,700 279,594 (116,549) - - 163,045

Dividends declared - $0.86

per share of common stock - - - (1,733,438) - (1,733,438)

Balances, December 31, 2012 2,018,703 10,989,445$ (368,262)$ 24,171,693$ 160,930$ 34,953,806$

Common Stock

The accompanying notes are an integral part of these consolidated financial statements.

5

CNB COMMUNITY BANCORP, INC.

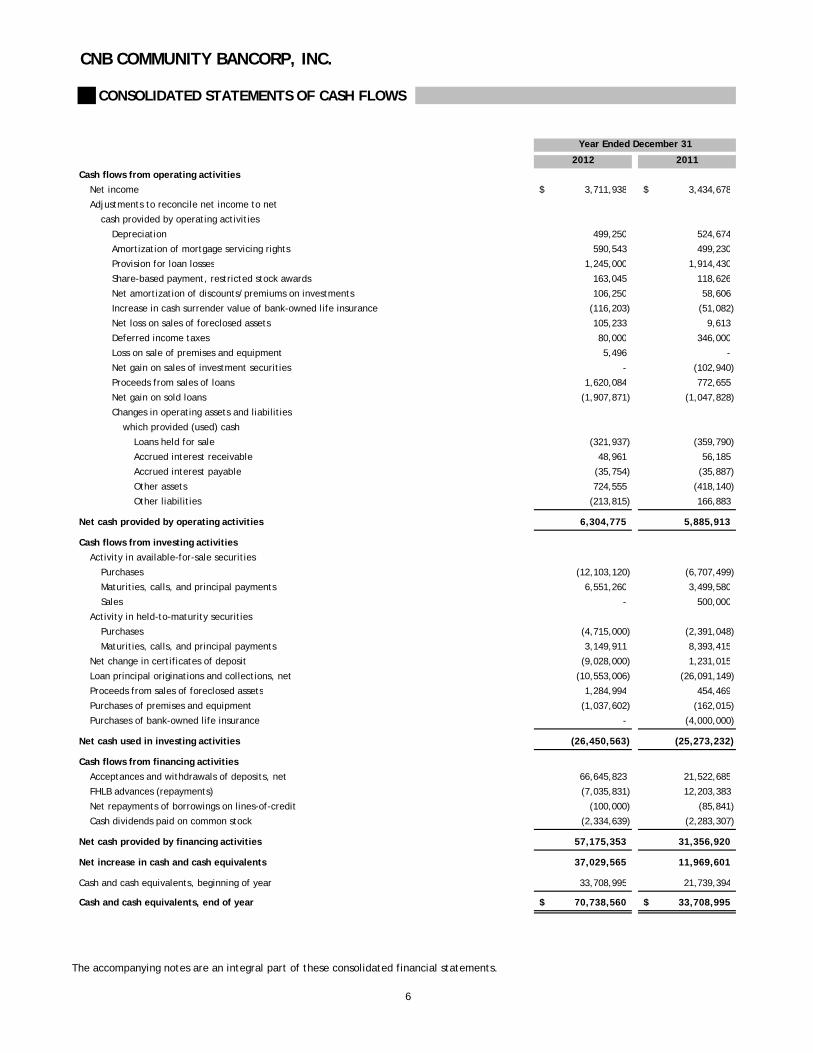

CONSOLIDATED STATEMENTS OF CASH FLOWS

Year Ended December 31

2012 2011

Cash flows from operating activities

Net income 3,711,938$ 3,434,678$

Adjustments to reconcile net income to net

cash provided by operating activities

Depreciation 499,250 524,674

Amortization of mortgage servicing rights 590,543 499,230

Provision for loan losses 1,245,000 1,914,430

Share-based payment, restricted stock awards 163,045 118,626

Net amortization of discounts/premiums on investments 106,250 58,606

Increase in cash surrender value of bank-owned life insurance (116,203) (51,082)

Net loss on sales of foreclosed assets 105,233 9,613

Deferred income taxes 80,000 346,000

Loss on sale of premises and equipment 5,496 -

Net gain on sales of investment securities - (102,940)

Proceeds from sales of loans 1,620,084 772,655

Net gain on sold loans (1,907,871) (1,047,828)

Changes in operating assets and liabilities

which provided (used) cash

Loans held for sale (321,937) (359,790)

Accrued interest receivable 48,961 56,185

Accrued interest payable (35,754) (35,887)

Other assets 724,555 (418,140)

Other liabilities (213,815) 166,883

Net cash provided by operating activities 6,304,775 5,885,913

Cash flows from investing activities

Activity in available-for-sale securities

Purchases (12,103,120) (6,707,499)

Maturities, calls, and principal payments 6,551,260 3,499,580

Sales - 500,000

Activity in held-to-maturity securities

Purchases (4,715,000) (2,391,048)

Maturities, calls, and principal payments 3,149,911 8,393,415

Net change in certificates of deposit (9,028,000) 1,231,015

Loan principal originations and collections, net (10,553,006) (26,091,149)

Proceeds from sales of foreclosed assets 1,284,994 454,469

Purchases of premises and equipment (1,037,602) (162,015)

Purchases of bank-owned life insurance - (4,000,000)

Net cash used in investing activities (26,450,563) (25,273,232)

Cash flows from financing activities

Acceptances and withdrawals of deposits, net 66,645,823 21,522,685

FHLB advances (repayments) (7,035,831) 12,203,383

Net repayments of borrowings on lines-of-credit (100,000) (85,841)

Cash dividends paid on common stock (2,334,639) (2,283,307)

Net cash provided by financing activities 57,175,353 31,356,920

Net increase in cash and cash equivalents 37,029,565 11,969,601

Cash and cash equivalents, beginning of year 33,708,995 21,739,394

Cash and cash equivalents, end of year 70,738,560$ 33,708,995$

The accompanying notes are an integral part of these consolidated financial statements.

6

CNB COMMUNITY BANCORP, INC. NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

7

1. BUSINESS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Consolidation and Nature of Business The consolidated financial statements include the accounts of CNB Community Bancorp, Inc., a registered bank holding company (the “Corporation”), and its wholly-owned subsidiary Hillsdale County National Bank (the “Bank”). All significant intercompany transactions and balances have been eliminated in consolidation. The Bank is an independently owned community bank engaged in the business of retail and commercial banking services through its 11 full-service branches located in Hillsdale, Jackson, Lenawee and Calhoun Counties in Michigan. Active competition, principally from other commercial banks, savings banks, and credit unions, exists in the Bank’s primary markets. The Bank’s results of operations can be significantly affected by changes in interest rates or changes in the automotive and agricultural industries which comprise a significant portion of the local economic environment. Concentration Risks The Bank’s primary deposit products are interest and noninterest-bearing checking accounts, savings accounts, and time deposits, and its primary lending products are residential and commercial real estate mortgages, commercial and consumer loans. The Bank does not have any significant concentrations with respect to any one industry, customer, or depositor. The Bank also provides trust services. The Bank is a federally chartered bank and is a member of the Federal Deposit Insurance Corporation (“FDIC”) Bank Insurance Fund. The Bank is subject to the regulations of the FDIC and the supervision of the Office of the Comptroller of the Currency (“OCC”) and undergoes periodic examinations by these regulatory authorities. The Corporation is further subject to regulations of the Federal Reserve Board governing bank holding companies. Use of Estimates The preparation of consolidated financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities as of the date of the consolidated balance sheet and reported amounts of income and expenses during the year. Actual results could differ from those estimates. Significant estimates include but are not limited to the determination of the allowance for loan losses, the fair value of certain investment securities, the carrying values of intangible assets, and the fair values of financial instruments. Summary of Significant Accounting Policies Accounting policies used in the preparation of the accompanying consolidated financial statements are in conformity with accounting principles generally accepted in the United States. The principles which materially affect the determination of the financial position or results of operations of the Corporation and the Bank are summarized below. Cash and Cash Equivalents For the purposes of the consolidated statements of cash flows, cash and cash equivalents include cash and balances due from banks and federal funds sold. Generally, federal funds are sold for a one-day period. The Corporation maintains deposit accounts in various financial institutions which generally exceed federally insured limits or are not insured. Management does not believe the Corporation is exposed to any significant interest, credit, or other financial risk as a result of these deposits. Certificates of Deposit Certificates of deposit are held with other financial institutions and are carried at cost. Maturities range from within one year to five years. Fair Value Measurements Fair value refers to the price that would be received to sell an asset or paid to transfer a liability (an exit price) in an orderly transaction between market participants in the market in which the reporting entity transacts such sales or transfers based on the assumptions market participants would use when pricing an asset or liability. Assumptions are developed based on prioritizing information within a fair value hierarchy that gives the highest priority to quoted prices in active markets (Level 1) and the lowest priority to unobservable data, such as the reporting entity’s own data (Level 3). A description of each category in the fair value hierarchy is as follows:

Level 1: Valuation is based upon quoted prices for identical instruments traded in active markets. Level 2: Valuation is based upon quoted prices for similar instruments in active markets, quoted prices for identical or similar instruments in markets that are not active, and model-based valuation techniques for which all significant assumptions are observable in the market. Level 3: Valuation is generated from model-based techniques that use at least one significant assumption not observable in the market. These unobservable assumptions reflect the estimates of assumptions that market participants would use in pricing the asset or liability.

CNB COMMUNITY BANCORP, INC. NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

8

For a further discussion of Fair Value Measurements, refer to Note 2 to the consolidated financial statements. Investment Securities Debt securities that management has the ability and positive intent to hold to maturity are classified as held-to-maturity and are recorded at amortized cost. All other investment securities are classified as available-for-sale and recorded at fair value, with unrealized gains and losses, net of the effect of deferred income taxes, recorded in other comprehensive income. Purchase premiums and discounts are recognized in interest income using the interest method over the terms of the investment securities. Realized gains or losses on the sale of the available-for-sale securities are recorded in investment income on the trade date and are determined using the specific identification method. Investment securities are reviewed at each reporting period for possible other-than-temporary impairment (“OTTI”). In determining whether an other-than-temporary impairment exists for debt securities, management must assert that: (a) it does not have the intent to sell the security; and (b) it is more likely than not it will not have to sell the security before recovery of its cost basis. If these conditions are not met, the Corporation separates the total impairment into the credit loss component and the amount of the loss related to other factors. In order to determine the amount of the credit loss for a debt security, the Corporation calculates the recovery value by performing a discounted cash flow analysis based on the current cash flows and future cash flows management expects to recover. The amount of the total other-than-temporary impairment related to the credit risk is recognized in earnings and is included in noninterest income. The amount of the total other-than-temporary impairment related to other risk factors is recognized as a component of other comprehensive income. For debt securities that have recognized an other-than-temporary impairment through earnings, if through subsequent evaluation there is a significant increase in the cash flow expected, the difference between the amortized cost basis and the cash flows expected to be collected is accreted as interest income. Available-for-sale equity securities are reviewed for other-than-temporary impairment at each reporting date. This evaluation considers a number of factors including, but not limited to, the length of time and extent to which the fair value has been less than cost, the financial condition and near term prospects of the issuer, and management’s ability and intent to hold the securities until fair value recovers. If it is determined that management does not have the ability and intent to hold the securities until recovery or that there are conditions that indicate that a security may not recover in value then the difference between the fair value and the cost of the security is recognized in earnings and is included in noninterest income. No such losses were recognized in 2012 or 2011. Restricted Investments The Bank is a member of the Federal Home Loan System and is required to invest in capital stock of the Federal Home Loan Bank of Indianapolis (“FHLBI”). The amount of the required investment is based upon the available balance of the Bank’s advances from the FHLBI and is carried at cost plus the value assigned to stock dividends. The Bank is also a member of the Federal Reserve Bank System (“FRB”). The FRB determines the amount of the required investment at the time the Bank becomes a member. The amount is carried at cost. Loans Loans that management has the positive intent and ability to hold for the foreseeable future or until maturity or pay-off are generally reported at their outstanding unpaid principal balances adjusted for charge-offs, the allowance for loan losses, and any deferred fees or costs on originated loans. Interest income is accrued on the unpaid principal balance. Loan origination fees, net of certain direct loan origination costs, are deferred and recognized as an adjustment of the related loan yield using the interest method. The accrual of interest on mortgage and commercial loans is discontinued at the time the loan is 90 days past due unless the credit is well-secured and in process of collection. Personal loans are typically charged-off no later than 180 days past due. Past due status is based on contractual terms of the loan. In all cases, loans are placed on nonaccrual or charged-off at an earlier date if collection of principal or interest is considered doubtful. All interest accrued in the current year but not collected for loans that are placed on nonaccrual or are charged-off, is reversed against interest income while interest accrued but not collected in prior years is reversed against the allowance for loan losses. The interest income on these loans is accounted for on the cash-basis or cost-recovery method, until qualifying for return to accrual. Loans are returned to accrual status when all principal and interest amounts contractually due are brought current and future payments are reasonably assured. For impaired loans not classified as nonaccrual, interest income is recognized daily as it is earned according to the terms of the loan agreement. Nonperforming loans of the loan portfolio are comprised of those loans accounted for on a nonaccrual basis, accruing loans contractually past due 90 days or more as to interest or principal payments (120 days or more past due on real estate residential loans) and loans modified under troubled debt restructurings (nonperforming originated loans). Allowance for Loan Losses The allowance for loan losses (“allowance”) is an estimate of loan losses inherent in the Bank's loan portfolio. The allowance is established through a provision for loan losses which is charged to expense. Additions to the allowance are expected to maintain the appropriateness of the total allowance after loan losses. Loan losses are charged-off against the allowance when the Bank determines the loan balance to be uncollectible. Cash received on previously charged-off amounts is recorded as a recovery to the allowance.

CNB COMMUNITY BANCORP, INC. NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

9

The allowance consists of two primary components, general reserves and specific reserves related to impaired loans. The general component covers non-impaired loans and is based on historical losses adjusted for current factors. The historical loss experience is determined by portfolio segment and is based on the actual loss history experienced by the Bank over the most recent three years. The Bank places more emphasis, or weight, on the more current quarters in the loss history period. This actual loss experience is adjusted for economic factors based on the risks present for each portfolio segment. These economic factors include consideration of the following: levels of and trends in delinquencies and impaired loans; levels of and trends in charge-offs and recoveries; trends in volume and terms of loans; effects of any changes in risk selection and underwriting standards; other changes in lending policies, procedures, and practices; experience, ability, and depth of lending management and other relevant staff; national and local economic trends and conditions; industry conditions; and effects of changes in credit concentrations. These factors are inherently subjective and are driven by the repayment risk associated with each portfolio segment. A loan is considered impaired when, based on current information and events, it is probable that the Bank will be unable to collect the scheduled payments of principal or interest when due according to the contractual terms of the loan agreement. Factors considered by management in determining impairment include payment status, collateral value, and the probability of collecting scheduled principal and interest payments when due. Loans that experience insignificant payment delays and payment shortfalls generally are not classified as impaired. Management determines the significance of payment delays and payment shortfalls on a case-by-case basis, taking into consideration all of the circumstances surrounding the loan and the borrower, including the length of the delay, the reasons for the delay, the borrower’s prior payment record, and the amount of the shortfall in relation to the principal and interest owed. Impairment is measured on a loan-by-loan basis for commercial loans by either the present value of expected future cash flows discounted at the loan’s effective interest rate, the loans obtained market price, or the fair value of the collateral, less costs to sell, if the loan is collateral dependent. A loan is collateral dependent if its repayment is expected to be provided solely by the underlying collateral. Large groups of smaller balance homogeneous loans are collectively evaluated for impairment. Accordingly, the Bank does not separately identify individual consumer and residential loans for impairment disclosures, unless such loans are the subject of a restructuring agreement. The Bank evaluates the credit quality of loans in the consumer loan portfolio, based primarily on the aging status of the loan and payment activity. Accordingly, nonaccrual loans, loans past due as to principal or interest 90 days or more and loans modified under troubled debt restructurings of the originated portfolio are considered in a nonperforming status for purposes of credit quality evaluation. Under certain circumstances, the Bank will provide borrowers relief through loan restructurings. A loan restructuring constitutes a troubled debt restructuring (“TDR”) if for economic or legal reasons related to the borrower's financial difficulties the Bank grants a concession to the borrower that it would not otherwise consider. Restructured loans typically present an elevated level of credit risk as the borrowers are not able to perform according to the original contractual terms. Loans that are reported as TDRs are considered impaired and measured for impairment as described above. The Bank assigns a risk rating to all loans that exceed $25,000 and all nonaccrual loans, and periodically performs detailed internal reviews of all loans over $300,000 and of all lines of credit. These risk ratings are also subject to examination by the Bank's regulators. During the internal reviews, management monitors and analyzes the financial condition of borrowers and guarantors, trends in the industries in which the borrowers operate and the fair values of collateral securing the loans. These credit quality indicators are used to assign a risk rating to each individual loan. The risk ratings can be grouped into five major categories, defined as follows:

Pass: A pass loan is a credit with no existing or known potential weaknesses deserving of management's close attention. Special Mention: Loans classified as special mention have a potential weakness that deserves management's close attention. If left uncorrected, this potential weakness may result in deterioration of the repayment prospects for the loan or of the Bank's credit position at some future date. Special mention loans are not adversely classified and do not expose the Bank to sufficient risk to warrant adverse classification. Substandard: Loans classified as substandard are not adequately protected by the current net worth and paying capacity of the borrower or of the collateral pledged, if any. Loans classified as substandard have a well-defined weakness or weaknesses that jeopardize the repayment of the debt. Well defined weaknesses include a borrower's lack of marketability, inadequate cash flow or collateral support, failure to complete construction on time, or the failure to fulfill economic expectations. They are characterized by the distinct possibility that the Bank will sustain some loss if the deficiencies are not corrected. Doubtful: Loans classified as doubtful have all the weaknesses inherent in those classified as substandard, with the added characteristic that the weaknesses make collection or repayment in full, on the basis of currently existing facts, conditions, and values, highly questionable and improbable. Loss: Loans classified as loss are considered uncollectible and are charged-off immediately.

CNB COMMUNITY BANCORP, INC. NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

10

The majority of the Bank’s consumer and residential loan portfolio is comprised of secured loans that are evaluated at origination on a centralized basis against standardized underwriting criteria. The ongoing measurement of credit quality of the consumer and residential loan portfolios is largely done on an exception basis. If payments are made on schedule, as agreed, then no further monitoring is performed. However, if delinquency occurs, the delinquent loans are turned over to the Bank’s loss mitigation department for resolution. Credit quality for the entire consumer and residential loan portfolio is measured by the periodic delinquency rate, nonaccrual amounts and actual losses incurred.

The Bank maintains a separate general valuation allowance for each portfolio segment. These portfolio segments include commercial, commercial real estate, residential real estate, and consumer with risk characteristics described as follows:

Commercial: Commercial loans are generally underwritten to existing cash flows of operating businesses. Debt coverage is provided by business cash flows and economic trends influenced by unemployment rates and other key economic indicators are closely correlated to the credit quality of these loans. Commercial Real Estate: Commercial real estate loans consist of owner occupied and non-owner occupied businesses, with the majority being owner occupied. Most commercial real estate loans are personally guaranteed by the owners of the real estate. Trends in vacancy rates of commercial properties impact the credit quality of these loans. Residential Real Estate: The degree of risk in residential mortgage lending depends primarily on the loan amount in relation to collateral value, the interest rate and the borrower's ability to repay in an orderly fashion. Economic trends determined by unemployment rates and other key economic indicators are closely correlated to the credit quality of these loans. For the last few years, weak economic trends indicate that the borrowers' capacity to repay their obligations had been deteriorating. Consumer: The consumer loan portfolio is usually comprised of a large number of small loans, including automobile, personal, recreational purpose, etc. Most loans are made directly for consumer purchases. Economic trends determined by unemployment rates and other key economic indicators are closely correlated to the credit quality of these loans. Strong underwriting guidelines within this portfolio remain in place.

Although management believes the allowance to be appropriate, ultimate losses may vary from its estimates. At least quarterly, the Board of Directors reviews the appropriateness of the allowance, including consideration of the relevant risks in the portfolio, current economic conditions and other factors. If the Board of Directors and management determine that changes are warranted based on those reviews, the allowance is adjusted. In addition, the Bank's primary regulator reviews the appropriateness of the allowance. The regulatory agency may require changes to the allowance based on its judgment about information available at the time of its examination. Off-Balance Sheet Credit Related Financial Instruments In the ordinary course of business, the Bank has entered into commitments to extend credit, including commitments under credit arrangements, commercial letters of credit, and standby letters of credit. Such financial instruments are recorded when they are funded. Loans Held for Sale Mortgage loans originated and intended for sale in the secondary market are carried at the lower of aggregate cost or fair value in the aggregate. Net unrealized losses, if any, are recognized through a valuation allowance of which adjustments are recognized in the consolidated statements of income. Transfers of Financial Assets Transfers of financial assets, including mortgage loans held-for-sale, as described above, are accounted for as sales when control over the assets has been surrendered. Control over transferred assets is deemed to be surrendered when 1) the assets have been legally isolated from the Bank, 2) the transferee obtains the right (free of conditions that constrain it from taking advantage of that right) to pledge or exchange the transferred assets, and 3) the Bank does not maintain effective control over the transferred assets through an agreement to repurchase them before their maturity. Other than servicing, as disclosed in Note 5, the Bank has no substantive continuing involvement related to these loans. Servicing Servicing assets are recognized as separate assets when rights are acquired through purchase or through sale of financial assets. Generally, purchased servicing rights are capitalized at the cost to acquire the rights. For sales of mortgage loans, a portion of the cost of originating the loan is allocated to the servicing right based on relative fair value. Fair value is based on market prices for comparable mortgage servicing contracts, when available, or alternatively, is based on a valuation model that calculates the present value of estimated future net servicing income. The valuation model incorporates assumptions that market participants would use in estimating future net servicing income, such as the cost to service, the discount rate, the custodial earnings rate, an inflation rate, ancillary income, prepayment speeds and default rates and losses.

CNB COMMUNITY BANCORP, INC. NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

11

Servicing assets or liabilities are amortized in proportion to and over the period of net servicing income or net servicing loss and are assessed for impairment or increased obligation based on fair value of rights compared to amortized cost at each reporting date. Impairment is determined by stratifying rights into tranches based on predominant risk characteristics, such as interest rate, loan type, and investor type. Impairment is recognized through a valuation allowance for an individual tranche, to the extent that fair value is less than the capitalized amount for the tranche. If the Bank later determines that all or a portion of the impairment no longer exists for a particular tranche, a reduction of the allowance may be recorded as an increase to income. Capitalized servicing rights are reported in other assets on the consolidated balance sheets. Servicing fee income is recorded for fees earned for servicing loans for others. The fees are based on a contractual percentage of the outstanding principal, or a fixed amount per loan and are recorded as income when earned. The amortization of mortgage servicing rights is netted against loan servicing fee income, a component of noninterest income. Foreclosed Assets Assets acquired through, or in lieu of, loan foreclosure are held for sale and are initially recorded at fair value, less costs to sell, on the date of transfer, establishing a new cost basis. Subsequent to foreclosure, valuations are periodically performed by management and the assets are carried at the lower of the carrying amount or fair value less costs to sell. Revenue and expenses from operations and changes in the valuation allowance are included in other noninterest expenses on the consolidated statements of income. Premises and Equipment Land is carried at cost. Premises and equipment are carried at cost, less accumulated depreciation which is computed principally by the straight-line method based upon the estimated useful lives of the related assets, which range from 3 to 40 years. Major improvements are capitalized and appropriately amortized based upon the useful lives of the related assets or the expected terms of the leases, if shorter, using the straight-line method. Maintenance, repairs, and minor alterations are charged to current operations as expenditures occur. Management annually reviews these assets to determine whether carrying values have been impaired. FDIC Insurance Premium (Included in Other Assets) The Corporation was required to prepay quarterly FDIC risk-based assessments for the fourth quarter of 2009 and each of the quarters in the years ending December 31, 2010, 2011, 2012, and 2013. The assessments for subsequent years have been deferred on the accompanying December 31, 2012 and 2011 consolidated balance sheets as a prepaid asset of approximately $426,000 and $704,000, respectively, and are expected to be expensed on a ratable basis quarterly through December 31, 2013. Bank-Owned Life Insurance (BOLI) The Corporation holds life insurance policies purchased on the lives of key members of management. In the event of death of one of these individuals, the Corporation, as beneficiary of the policies, would receive a specified cash payment equal to the face value of the policy. Such policies are recorded at their cash surrender value, or the amount that can be currently realized as of the consolidated balance sheet date. The change in cash surrender value is an adjustment of premiums paid in determining the net expense or income recognized under the contracts for the year and is included in noninterest expenses or income. Goodwill Goodwill consists of amounts paid in excess over the fair value of identifiable net assets acquired. Goodwill is not amortized but is assessed at least annually for impairment or on an interim basis if an event occurs or circumstances change that would more likely than not reduce the fair value of the reporting unit below the carrying value. Income Taxes Deferred income tax assets and liabilities are determined using the liability (or balance sheet) method. Under this method, the net deferred tax asset or liability is determined based on the federal income tax effects of the temporary differences between the book and tax bases of the various balance sheet assets and liabilities and gives current recognition to changes in tax rates and laws. Valuation allowances are established, where necessary, to reduce deferred tax assets to the amount expected more likely than not to be realized. Income tax expense is the tax payable or refundable for the year plus or minus the change during the year in deferred tax assets and liabilities. The Corporation analyzes its filing positions in the jurisdictions where it is required to file income tax returns, as well as all open tax years in these jurisdictions. The Corporation also treats interest and penalties attributable to income taxes, and reflects any charges for such, to the extent they arise, as a component of its noninterest expenses. Net Income Per Share Basic earnings per share represents income available to common stockholders divided by the weighted-average number of common shares outstanding during the year, which was 2,013,522 and 2,001,495 during 2012 and 2011, respectively. Diluted earnings per share reflects additional common shares that would have been outstanding if dilutive potential common shares had been issued, as well as any adjustments to income that would result from the assumed issuance.

CNB COMMUNITY BANCORP, INC. NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

12

Reclassifications Certain amounts as reported in the 2011 consolidated financial statements have been reclassified to conform with the 2012 presentation. Subsequent Events In preparing these consolidated financial statements, the Corporation has evaluated, for potential recognition or disclosure, significant events or transactions that occurred during the period subsequent to December 31, 2012, the most recent consolidated balance sheet presented herein, through March 1, 2013, the date these consolidated financial statements were available to be issued. No such significant events or transactions were identified.

2. FAIR VALUE MEASUREMENTS

The Corporation utilizes fair value measurements to record fair value adjustments to certain assets and liabilities and to determine fair value disclosures. Marketable securities available-for-sale are recorded at fair value on a recurring basis. Additionally, from time to time, the Corporation may be required to record at fair value other assets on a nonrecurring basis, such as impaired loans, loans held for sale, foreclosed assets, mortgage servicing rights, held-to-maturity securities, and certain other assets and liabilities. These nonrecurring fair value adjustments typically involve the application of lower of cost or market accounting or write downs of individual assets. Following is a description of the valuation methodologies and key inputs used to measure financial assets and liabilities recorded at fair value, as well as a description of the methods and significant assumptions used to estimate fair value disclosures for financial instruments not recorded at fair value in their entirety on a recurring basis. For financial assets and liabilities recorded at fair value, the description includes an indication of the level of the fair value hierarchy in which the assets or liabilities are classified.

Cash and Cash Equivalents The carrying value of cash and short-term instruments, including Federal funds sold, approximates fair values. Certificate of Deposits Fair value of certificates of deposit are estimated using discounted cash flow analysis based on current rates for similar types of deposit. Investment Securities Held-to-maturity securities are recorded at fair value on a nonrecurring basis, unless an other-than-temporary impairment is recorded. Investment securities classified as available-for-sale are recorded at fair value on a recurring basis. Fair value measurement is based upon quoted prices, if available. If quoted prices are not available, fair values are measured using independent pricing models or other model based valuation techniques such as the present value of future cash flows, adjusted for the security’s credit rating, prepayment assumptions and other factors such as credit loss and liquidity assumptions. Level 1 securities include those traded on an active exchange, such as the New York Stock Exchange, that are traded by dealers or brokers in active over-the-counter markets and money market funds. Level 2 fair value measurement is based upon quoted prices, if available. If quoted prices are not available, fair values are measured using independent pricing models or other model based valuation techniques such as the present value of future cash flows, adjusted for the security’s credit rating, prepayment assumptions and other factors such as credit loss and liquidity assumptions. Level 2 securities include mortgage-backed securities issued by government-sponsored entities, municipal bonds and corporate debt securities in active markets. The Corporation did not have Level 3 investment securities valued on a recurring basis at December 31, 2012 or 2011. Federal Reserve Bank and Federal Home Loan Bank Stock The carrying value of Federal Reserve Bank and Federal Home Loan Bank of Indianapolis Stock approximates fair value based on the redemption provisions of the Federal Reserve Bank and Federal Home Loan Bank of Indianapolis. Loans Held for Sale Loans held for sale are carried at the lower of cost or fair value. The fair value of loans held for sale is based on what secondary markets are currently offering for portfolios with similar characteristics. As such, the Corporation classifies loans held for sale subjected to nonrecurring fair value adjustments as Level 2. At December 31, 2012 and 2011, there was no impairment recorded for loans held for sale and, therefore, no loans held for sale were recorded at fair value on a nonrecurring basis. Loans For variable-rate loans that reprice frequently and with no significant change in credit risk, fair values are based on carrying values. Fair values for fixed interest rate loans are estimated using discounted cash flow analyses, using interest rates currently being offered for loans with similar terms to borrowers of similar credit quality. The resulting amounts are adjusted to estimate the effect of declines, if any, in the credit quality of borrowers since the loans were originated. Fair values for nonperforming loans are estimated using discounted cash flow analyses or underlying collateral values, where applicable.

CNB COMMUNITY BANCORP, INC. NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

13