coal insghts, august 2015

DESCRIPTION

“NCL should be benchmarked against global biggies” It may not be the largest coal producer in India, but Northern Coalfields enjoys a unique position in the coal matrix. The only CIL arm to achieve its entire production through departmental means, NCL enjoys the very best in mining conditions, infrastructure and manpower. CMD T K Nag talks to Coal Insights about his dream of taking NCL to the big league of global giants Also read: ● In focus: Material handling set to ride power projects to growth ● In focus: Time to tighten the belt (spotlight on conveyor belting industry) ● In focus: Return of the reactor (spotlight on nuclear energy) ● Special feature Read interviews of key conveyor belting and material handling players ● Feature: India’s Q1 coal production at 20% of annual target ● Logistics: Dighi aims to handle 10 mt of coal by 2019 -20 Plus, our regular coverage of international coal prices, India's coal production updates, corporate, social buzz and muchTRANSCRIPT

4 Coal Insights, August 2015

COnTEnTs

22 Yuan devaluation weighs on steam coal offers in August

24 Coking coal offers continue fall in August

26 India’s Q1 coal production at 20% of annual target

32 India’scoalimportsshowflattrendtillJuly

36 Coal stocks scenario improves at 100 TPPs y-o-y

37 India’s cement output slipped back to 23-mt level in June

38 Material handling set to ride power projects to growth

44 Oriental rides the MAXX wave

50 Aim is to reduce the cost of ownership

53 CBC India bets big on bulk consumers

54 SCBL geared up to double its market share

58 Return of the reactor

62 Coal washing: Understanding critical issues

64 Jaypee Cement bags Majra mine at Rs 1,230/t

65 Tata Hitachi launches EX110 ‘Super’ series hydraulic excavator

67 Newton Weighing gets 40% repeat orders

68 Corporate updates

70 US power sector coal consumption may drop 7%

71 Electricity holds key to coal in ASEAN

77 N Korea top anthracite supplier in July

80 Thermal coal handling by major ports up 5.8% in April-July

81 Annexure

84 Supply data

86 E-auction data

86 Port data

66 | CoRpoRAtEAdani Enterprises targets coking coal, pet coke marketsCompany has opened a new business unit and is in talks with Australian miners.

42 | IN FoCUStime to tighten the belt The material handling industry bullish on long term, but short term challenges remain.

78 | LogIStICSDighi aims to handle 10 mt of coal by 2019 -20 Cargo handling capacity to go up to 18 mt by end of 2015, says Vijay Kalantri.

34 | FEAtURERIL gasifiers not likely to dry up pet coke suppliesIndustry believes RIL will not be out of market and consumers need not panic.

6 | CoVER StoRY“NCL should be benchmarked against global biggies”Equipped with best mines, NCL is capable to play in the big league, says T K Nag.

6 Coal Insights, August 2015

COvER sTORy

“NCL should be benchmarked against global biggies”

It may not be the largest producer of coal in the country, but Northern Coalfields Ltd (NCL) enjoys a unique

position in India’s coal matrix. The only subsidiary of Coal India Ltd to achieve its entire coal production through departmental means, NCL enjoys the very best mining conditions, infrastructure and perhaps the best manpower too. There is hardly any major hurdle on despatches either, as more than 90 percent of coal produced is consumed by pit-head thermal power plants. That gives T K Nag, chairman-cum-managing director (CMD) of NCL, enough space to aspire for bigger achievements. In a wide-ranging interview, Nag (the first full-time CMD of the company in a pretty long time) tells Rakesh Dubey and Arindam Bandyopadhyay about his ambitious plans to go for the next phase of mines modernisation via implementation of IT-enabled systems, and shares his dream of taking NCL to the big league of global mining giants.

Coal Insights, August 2015 7

COvER sTORy

Excerpts:

It has been nearly a year since you took over as CMD of NCL. How would you describe your experience so far in a company that did not have a full-time CMD for a pretty long period? What do you think the company’s major strengths are?

NCL has its own strengths. There are big opencast mines and no underground (UG) projects, unlike other subsidiaries of Coal India Limited (CIL). I would say this is a compact company having mining areas almost adjacent to each other.

The other unique feature is that it is totally a worker-oriented company, in the sense that hundred percent coal production comes through departmental means. It is the only subsidiary to do so, though in overburden removal, outsourcing is there. Overall, the literacy rate of operators or workers is quite high as we do not have piece-rated workers here. The mine workers understand the problems and the engineers are quite efficient because they have been working in such highly productive mines.

So, all that I needed to do was put a little effort to streamline things. And I think I have been able to stabilise whatever deficiencies were there. As I said, the compactness of the mines is a definitive advantage for us. Also, there are a sufficient number of equipment to work with. You can introduce new technologies here as people are quite adaptable. The trade union is by and large very cooperative. Law and order is also good compared to some other subsidiaries, as Madhya Pradesh is by and large a peaceful state. These are our plus points. So, a little effort helped in streamlining things.

What, according to you, are the areas where NCL needs improvement?

Frankly speaking, there are not many areas where the company requires significant improvement. Nevertheless, since NCL has larger mines, it should be benchmarked against the best mining practices adopted by other similar big mines in the global arena.

One area of improvement is the introduction of more IT technologies

Advantage NCL

♦ Technologically advanced, highly mechanised mines; has maximum number of draglines (21) in CIL

♦ Huge coal reserves (balance reserves as on April 1, 2014 are 9.66 billion tons) mostly amenable to opencast mining, which help to meet the country’s power grade coal requirements; currently, NCL supplies coal to about 12 percent of the country’s total installed capacity of coal-based power stations

♦ Has highly skilled workforce for HEMM operations and maintenance

♦ High customer satisfaction; More than 90 percent coal is supplied to pithead power plants

♦ International Certifications like ISO 9001 (Quality Management System, since 2009), ISO 14001 (Environment Management System, since 2001) and OHSAS 18001 (Occupational health and safety)

Areas of improvement

♦ Meeting the challenge of reduction in skilled/semi-skilled manpower arising on account of superannuation

♦ Expediting the procurement process

♦ Employees’ healthcare

1 Planned production from NCL projects during 2015-16 and onwards is attached as Annexure–I on Pg 81-82.

and systems in our mining operations. To that end, we are trying to take some initiatives, but we have a long way to go. There is much scope for IT in maintenance, operations, operator- independent systems etc. so that the entire processes could be monitored seamlessly and there is complete coordination between various areas of work.

Talking about IT, CIL had taken a decision to introduce the GPS system in mining operations, but now it is said the move has not really helped much. What has been NCL’s experience in this regard?

GPS technology is used in the Operator Independent Truck Despatch System (OITDS) system that has been deployed in 5 of our mines. We have recently introduced operator-independent systems in four mines (we already had it in Jayant) where GPS is the main tool.

So far as the use of GPS in coal transportation is concerned, we have done it in one of the mines. There is not much scope here as the majority of coal goes by MGR and silo. However, in two-three mines, we are going to implement it by September. GPS helps in preventing coal pilferage. In situations where a truckload of coal is being de-routed, you can do

Geo-fencing by way of GPS. Mahanadi Coalfields Ltd (MCL) has done it very successfully.

So, I don’t think GPS doesn’t help. At the end of the day you will derive the benefits. As I said, the IT-enabled systems deployed globally in the mining sector use GPS. You can’t do away with that.

Coming to the production front, what was NCL's coal output in 2014-15 and what is the number expected this year?

NCL achieved coal production of 72.48 million tons (mt) during 2014-15. We have planned to produce 80 mt of coal during FY15-161.

The mega projects of NCL like Amlohri, Nigahi, Dudhichua and Jayant are all geared up to meet their respective coal production targets this fiscal. Till July 2015, these projects have achieved more than 98 percent of their target in production.

In 2015-16, we are also going to achieve the despatch target of 79.5 mt. Till now, we are hovering around 100 percent achievement.

26 Coal Insights, August 2015

fEATuREfEATuRE

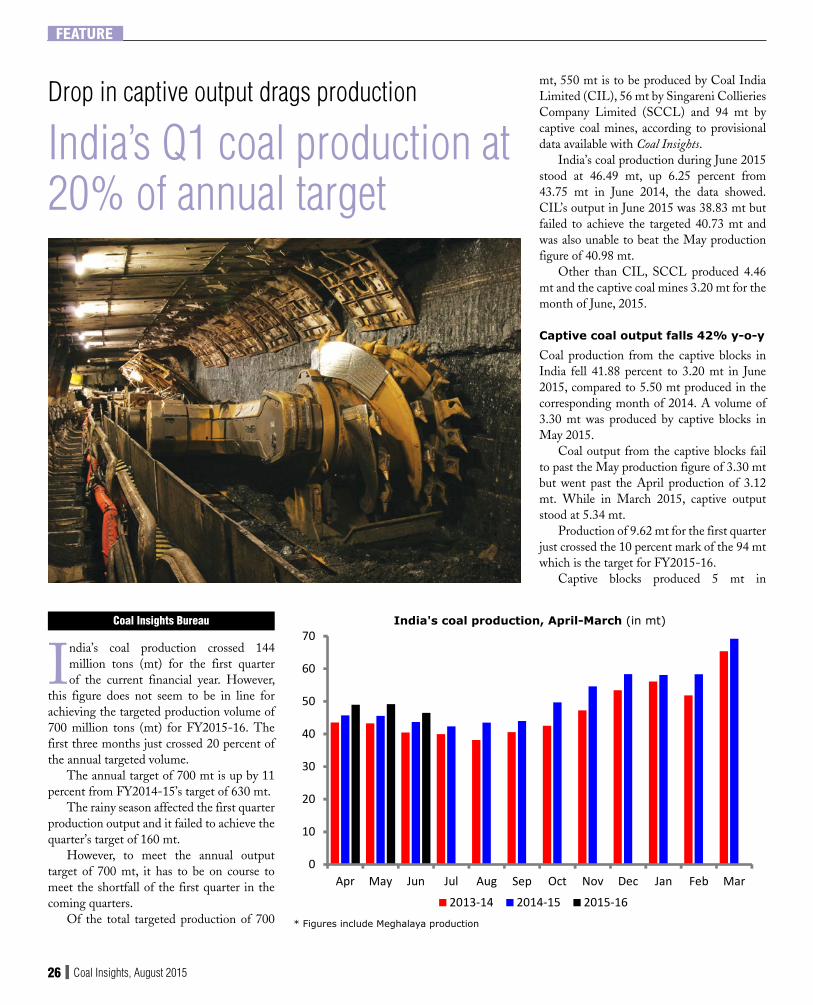

Drop in captive output drags production

India’s Q1 coal production at 20% of annual target

Coal Insights Bureau

India’s coal production crossed 144 million tons (mt) for the first quarter of the current financial year. However,

this figure does not seem to be in line for achieving the targeted production volume of 700 million tons (mt) for FY2015-16. The first three months just crossed 20 percent of the annual targeted volume.

The annual target of 700 mt is up by 11 percent from FY2014-15’s target of 630 mt.

The rainy season affected the first quarter production output and it failed to achieve the quarter’s target of 160 mt.

However, to meet the annual output target of 700 mt, it has to be on course to meet the shortfall of the first quarter in the coming quarters.

Of the total targeted production of 700

mt, 550 mt is to be produced by Coal India Limited (CIL), 56 mt by Singareni Collieries Company Limited (SCCL) and 94 mt by captive coal mines, according to provisional data available with Coal Insights.

India’s coal production during June 2015 stood at 46.49 mt, up 6.25 percent from 43.75 mt in June 2014, the data showed. CIL’s output in June 2015 was 38.83 mt but failed to achieve the targeted 40.73 mt and was also unable to beat the May production figure of 40.98 mt.

Other than CIL, SCCL produced 4.46 mt and the captive coal mines 3.20 mt for the month of June, 2015.

Captive coal output falls 42% y-o-y

Coal production from the captive blocks in India fell 41.88 percent to 3.20 mt in June 2015, compared to 5.50 mt produced in the corresponding month of 2014. A volume of 3.30 mt was produced by captive blocks in May 2015.

Coal output from the captive blocks fail to past the May production figure of 3.30 mt but went past the April production of 3.12 mt. While in March 2015, captive output stood at 5.34 mt.

Production of 9.62 mt for the first quarter just crossed the 10 percent mark of the 94 mt which is the target for FY2015-16.

Captive blocks produced 5 mt in

0

10

20

30

40

50

60

70

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

2013-14 2014-15 2015-16

India's coal production, April-March (in mt)

* Figures include Meghalaya production

38 Coal Insights, August 2015

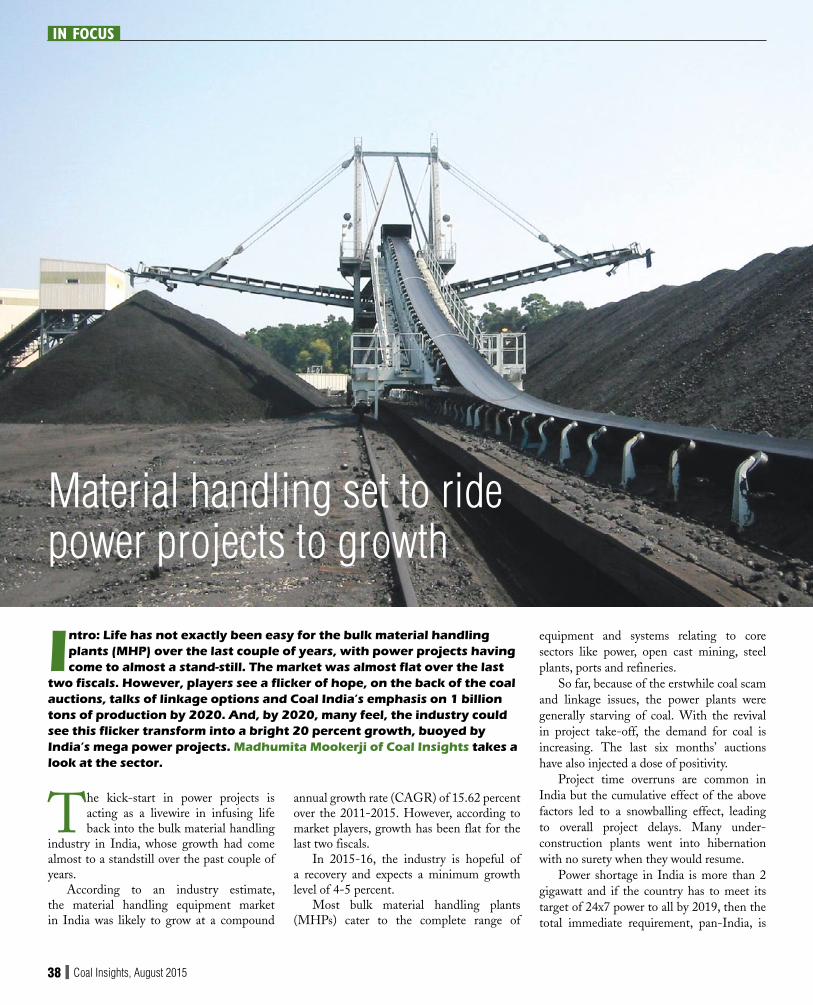

Material handling set to ride power projects to growth

The kick-start in power projects is acting as a livewire in infusing life back into the bulk material handling

industry in India, whose growth had come almost to a standstill over the past couple of years.

According to an industry estimate, the material handling equipment market in India was likely to grow at a compound

annual growth rate (CAGR) of 15.62 percent over the 2011-2015. However, according to market players, growth has been flat for the last two fiscals.

In 2015-16, the industry is hopeful of a recovery and expects a minimum growth level of 4-5 percent.

Most bulk material handling plants (MHPs) cater to the complete range of

In fOCus

equipment and systems relating to core sectors like power, open cast mining, steel plants, ports and refineries.

So far, because of the erstwhile coal scam and linkage issues, the power plants were generally starving of coal. With the revival in project take-off, the demand for coal is increasing. The last six months’ auctions have also injected a dose of positivity.

Project time overruns are common in India but the cumulative effect of the above factors led to a snowballing effect, leading to overall project delays. Many under-construction plants went into hibernation with no surety when they would resume.

Power shortage in India is more than 2 gigawatt and if the country has to meet its target of 24x7 power to all by 2019, then the total immediate requirement, pan-India, is

Intro: Life has not exactly been easy for the bulk material handling plants (MHP) over the last couple of years, with power projects having come to almost a stand-still. The market was almost flat over the last

two fiscals. However, players see a flicker of hope, on the back of the coal auctions, talks of linkage options and Coal India’s emphasis on 1 billion tons of production by 2020. And, by 2020, many feel, the industry could see this flicker transform into a bright 20 percent growth, buoyed by India’s mega power projects. Madhumita Mookerji of Coal Insights takes a look at the sector.

Coal Insights, August 2015 71

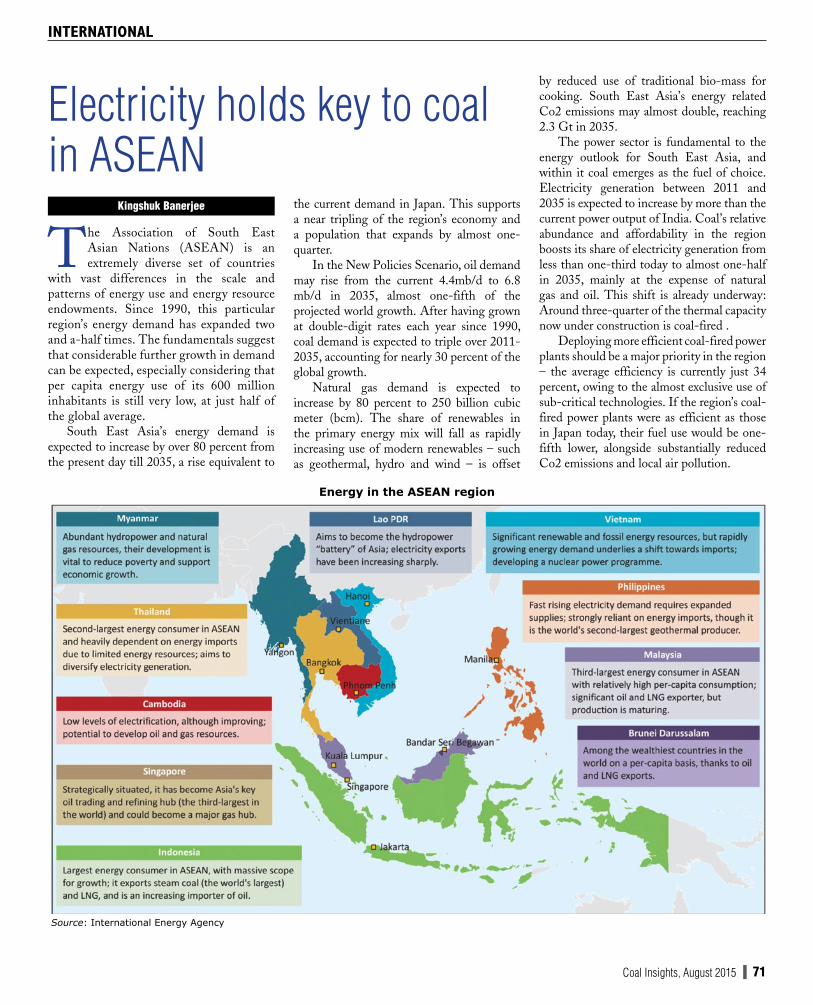

Electricity holds key to coal in ASEAN

Kingshuk Banerjee

The Association of South East Asian Nations (ASEAN) is an extremely diverse set of countries

with vast differences in the scale and patterns of energy use and energy resource endowments. Since 1990, this particular region’s energy demand has expanded two and a-half times. The fundamentals suggest that considerable further growth in demand can be expected, especially considering that per capita energy use of its 600 million inhabitants is still very low, at just half of the global average.

South East Asia’s energy demand is expected to increase by over 80 percent from the present day till 2035, a rise equivalent to

the current demand in Japan. This supports a near tripling of the region’s economy and a population that expands by almost one-quarter.

In the New Policies Scenario, oil demand may rise from the current 4.4mb/d to 6.8 mb/d in 2035, almost one-fifth of the projected world growth. After having grown at double-digit rates each year since 1990, coal demand is expected to triple over 2011-2035, accounting for nearly 30 percent of the global growth.

Natural gas demand is expected to increase by 80 percent to 250 billion cubic meter (bcm). The share of renewables in the primary energy mix will fall as rapidly increasing use of modern renewables – such as geothermal, hydro and wind – is offset

by reduced use of traditional bio-mass for cooking. South East Asia’s energy related Co2 emissions may almost double, reaching 2.3 Gt in 2035.

The power sector is fundamental to the energy outlook for South East Asia, and within it coal emerges as the fuel of choice. Electricity generation between 2011 and 2035 is expected to increase by more than the current power output of India. Coal’s relative abundance and affordability in the region boosts its share of electricity generation from less than one-third today to almost one-half in 2035, mainly at the expense of natural gas and oil. This shift is already underway: Around three-quarter of the thermal capacity now under construction is coal-fired .

Deploying more efficient coal-fired power plants should be a major priority in the region – the average efficiency is currently just 34 percent, owing to the almost exclusive use of sub-critical technologies. If the region’s coal-fired power plants were as efficient as those in Japan today, their fuel use would be one-fifth lower, alongside substantially reduced Co2 emissions and local air pollution.

InTERnATIOnAL

Energy in the ASEAN region

Source: International Energy Agency

Tear

alo

ng th

e do

tted

line

Tear

alo

ng th

e do

tted

line

90 Coal Insights, August 2015