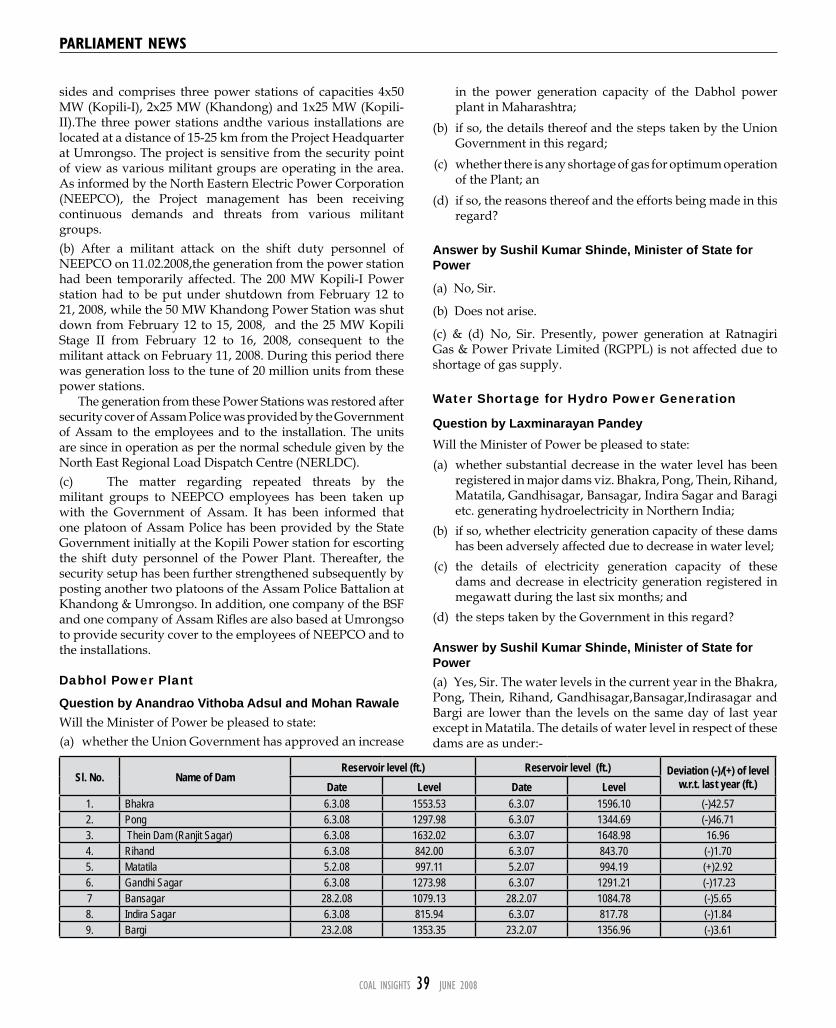

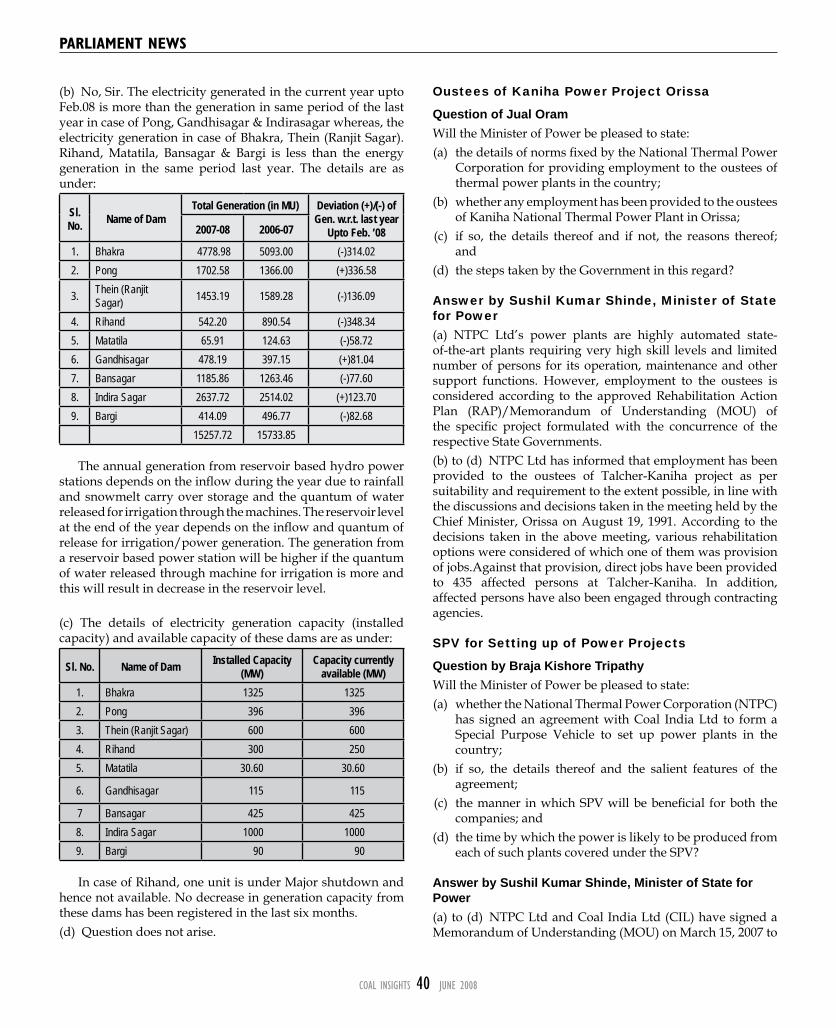

coal insights june08

TRANSCRIPT

EDITORIALChief EditorKohinoor Mandal, Tel: +91 92310 23166Email: [email protected]

EditorRakesh Dubey, Tel: +91 92310 02087Email: [email protected]

AdvertisingSoumitra Bose, Tel: +91 92310 00232Email: [email protected]

SubscriptionAnustup Lahiri, Tel: +91 92310 25872Email: [email protected]

DesignDebal RayShibu KarmakarFor suggestions, feedback and queries, please write to [email protected]

Copyright: All rights reserved. No part of Coal Insights can be reproduced or copied in any form or by any means without the prior permission of mjunction services limited. Please inform us if any copyright has been inadvertently infringed.

Disclaimer: This document is for information purpose only. Certain information herein has been acquired from various external sources believed to be reliable. While we have taken reasonable care to compile this report, we in no way assume any responsibility for any error or discrepancy in regards to information contained herein. Readers are requested to make appropriate judgment without any prejudice or compulsion.

Registered & Corporate Officemjunction services limited, Tata Centre, 43 Jawaharlal Nehru Road, Kolkata 700 071, Tel: +91 33 6610 6100/2288 2606, Fax: +91 33 2288 2078Kolkata: mjunction services limited, Bells House, 7th Floor, 21 Camac Street, Kolkata 700 016, Tel: +91 33 6610 0100, Fax: +91 33 2289 5983/84 Bokaro: mjunction services limited, Room 19, Old Admin Building, Bokaro Steel Plant, Bokaro 827 001, Tele/Fax: + 91 654 2226 132 Jamshedpur: mjunction services limited, Armoury Road, Bistupur, Jamshedpur 831 001, Tel: +91 657 6519 985/86/90/91, Tele/Fax: +91 657 2424 432 Durgapur: mjunction services limited, Room 618, Ispat Bhavan, Durgapur Steel Plant, Durgapur 713 203, Tel: +91 343 6510 185, Tele/Fax: +91 343 2586 946 Rourkela: mjunction services limited, Administrative Building, Room 624, 6th Floor, Rourkela Steel Plant, Rourkela 769 011, Tel: +91 661 6514 142, Fax: +91 661 2513 072 Mumbai: mjunction services limited, Jolly Bhavan II, 403, 4th Floor, 7 New Marine Lines, opp. Nirmala Niketan Home Science College, Mumbai 400 002, Tel: +91 22 6651 0662 Delhi: mjunction services limited, C127, 2nd Floor, Rex House, Naraina Industrial Area, Phase I, New Delhi 110 028, Tel: +91 11 2589 6900/2589 7000/6566 1774, Tele/Fax: +91 11 2589 6100 Bhilai: mjunction services limited, Room 321, 3rd Floor, Ispat Bhavan, Bhilai Steel Plant, Bhilai 490 001, Tel: +91 788 6451 066, Tele/Fax: +91 788 2227 136 Chennai: mjunction services limited, 2nd Floor, Begum Ishpani Complex, Old 44 (New 91) Armenian Street, Chennai 600 001, Tel: +91 44 4216 7417, Tele/Fax: +91 44 4205 1417

www.mjunction.inwww.metaljunction.in www.coaljunction.in www.buyjunction.in

www.autojunction.in www.straightline.in

Dear Readers,

At a time when leading coal mining companies world over, including those in China, have gone for stock exchange listing to raise funds, the Finance Ministry’s suggestion for considering an Initial Public Offering for Coal India Ltd (CIL) is a welcome step. Experience suggests that all companies have benefited after going public and the move by the Indian government will indeed benefit CIL as well.

Incidentally, at least four Chinese coal companies, China National Coal Group Corp., Shenhua Group, China’s largest coal mining firm, Yanzhou Coal Mining Co. Ltd, Heilongjiang Longmei Mining (Group) Co., Ltd., among others, had gone for overseas listing to raise funds in the last two years.

The move had not only benefited the companies, but also helped China increase its coal production capacity in a big way to match the growing demand. Even a majority of coal miners in the US, the UK, Australia, South Africa as well as in Indonesia are listed in stock exchanges.

In such circumstances, the listing in stock exchanges of India’s national coal producer, CIL, which is also the world’s single largest coal company, much bigger than the likes of BHP, Xstrata and Peabody, will improve its status and also bring it at par with well known names. Incidentally, the world’s second largest coal mining company is based out of China and its annual production is slightly less than 200 million tons.

In this issue of Coal Insights, we have covered the implications of proposed stock exchange listing of CIL at a time when it will have to increase its production to a staggering 521 million tons per annum by 2011-12 in order to meet domestic demand, compared with nearly 380 million tons produced in 2007-08.

The production plan has been revised recently by the new minister of state for coal and it is expected that the revised target would be over 550 million tons by 2011-12.

According to the revised production plan, CIL will have to increase its coal output at a CAGR of nearly 10 percent against the earlier growth plan of 6 percent. To meet the target, it is necessary that CIL starts implementing some innovative ideas and many feel IPO will be handy in achieving the target.

It is expected that an IPO will lead to increased professionalism and CIL will become more responsible to address the requirements of all the stakeholders, who quite often complain about the service quality of the company.

However, there seems to be some uncertainty regarding Coal India coming out with the proposed IPO as not only there is likely to be opposition from the Left, which is known to be against any move to dilute stake in any of the government companies, but even the company itself is not that keen on going ahead with the issue before getting the “Navratna” status.

The company first wants to get the coveted status and then go for IPO, but this strategy may not work in view of opposition by the Left, which feels that not only there should not be any kind of dilution in stake in any government company, but ‘Navratna’ companies should be specially exempted. So if CIL gets ‘Navratna’ status, the IPO plans may take a back seat.

Best regards,Editor

COAL INSIGHTS � JUNE 2008

COnTEnTs

Coal MaRKet FunDaMentals 8 Thermal coal prices touch record high 12 Coking coal prices likely to keep

soaring

CoveR stoRy

27 WCI suggests strategy for sustainable energy future

28 Essar to start CBM project in Durgapur

29 CVIfundsinsufficienttoacquireglobal assets

29 SECL against giving coal block part to private player

30 HIsmelt technology reduces dependence on coking coal

31 Coalministryfinalisingblueprintforregulator

32 MMTC invites bids for supply of coke and steam coal

33 New Coal Act planned for captive mining

CoRpoRate upDate

14 Coal India IPO plan hangs in balance16 Why should CIL go for the IPO?18 No IPO before Navratna: CIL chief

FeatuRe19 CoalblockidentifiedforCTLproject20 RioTintofilesfordiamondmining

lease in India21 Tata Power arm wins global honour21 PFC to invite proposals for Jharkhand

power project22 Indian steel cos close coal deals for

FY0922 RINL coking coal tie-ups23 CILconfidentofmeetingsteelcos

demand24 Coal as a fuel set to remain strong

globally26 State power utilities demand revision

in coal unloading norms

34 Coal India should try to create brand image: Ranganath

paRliaMent news37 Legislators’ coal queries

logistiCs44 Paradip Port to double coal handling

capacity

46 MCLconfidentofachieving15%output rise

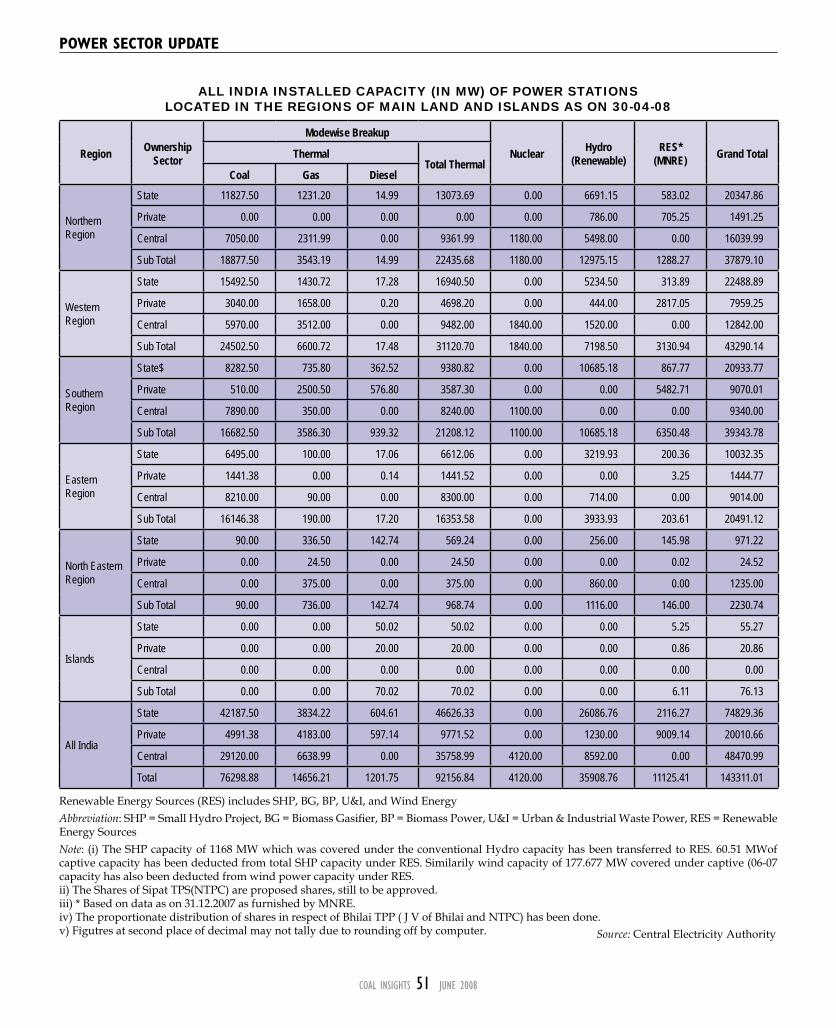

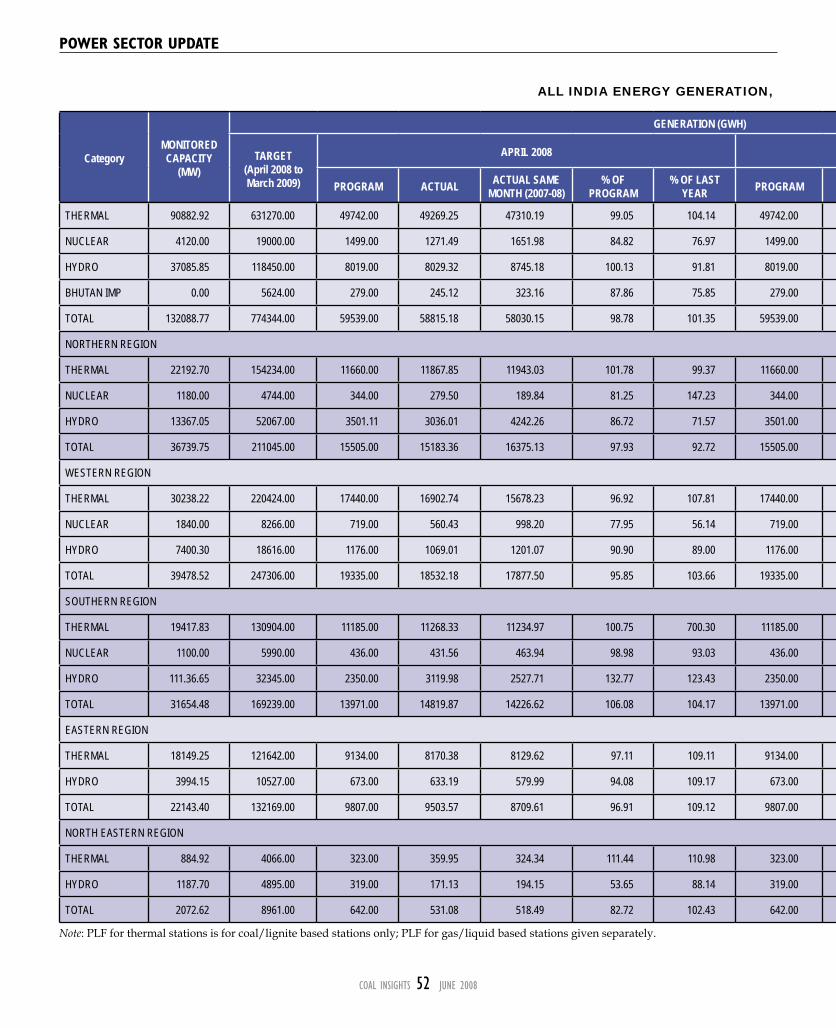

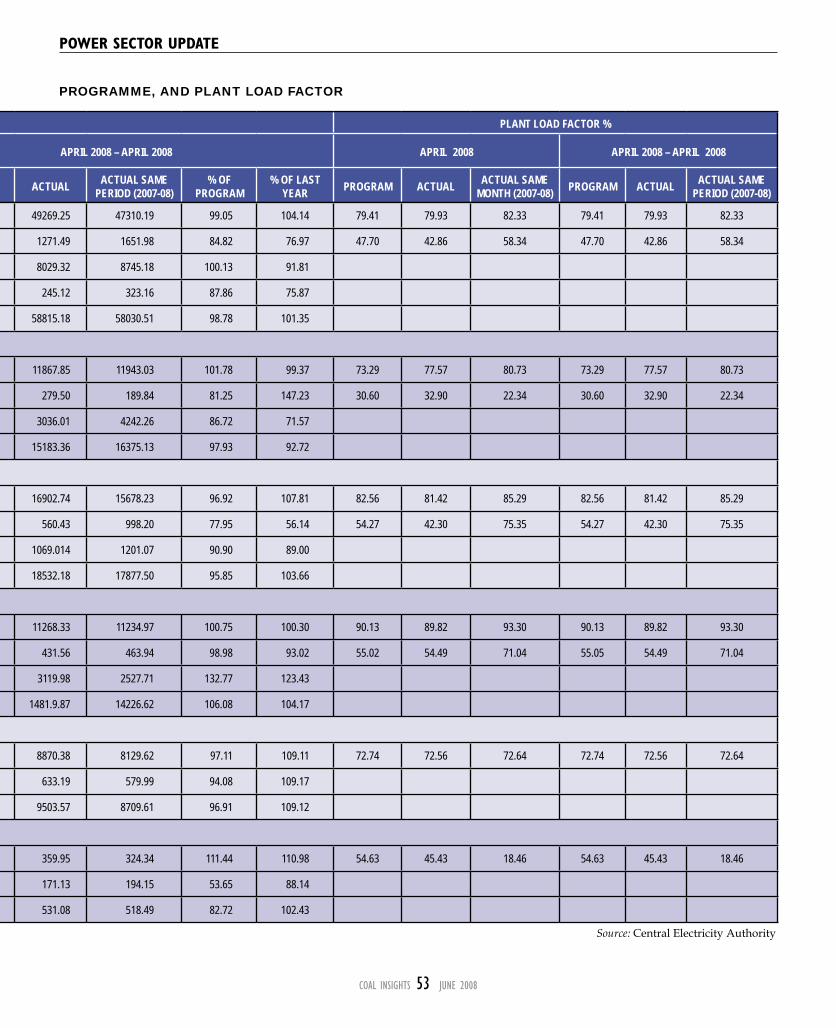

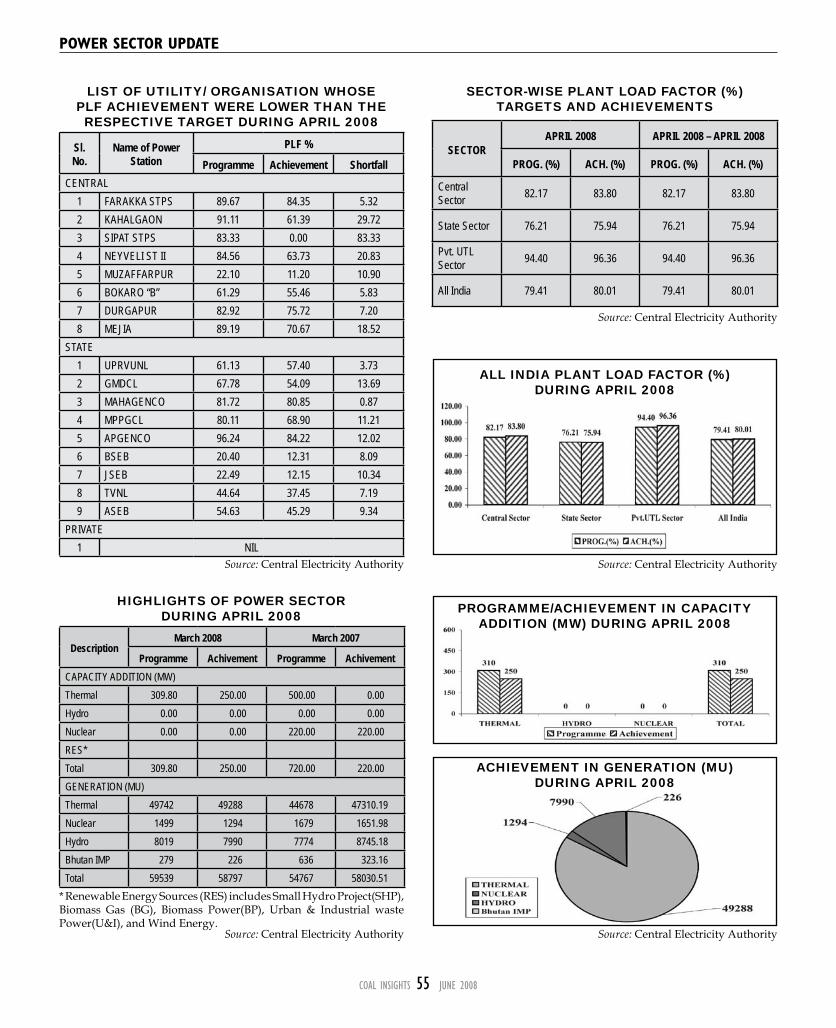

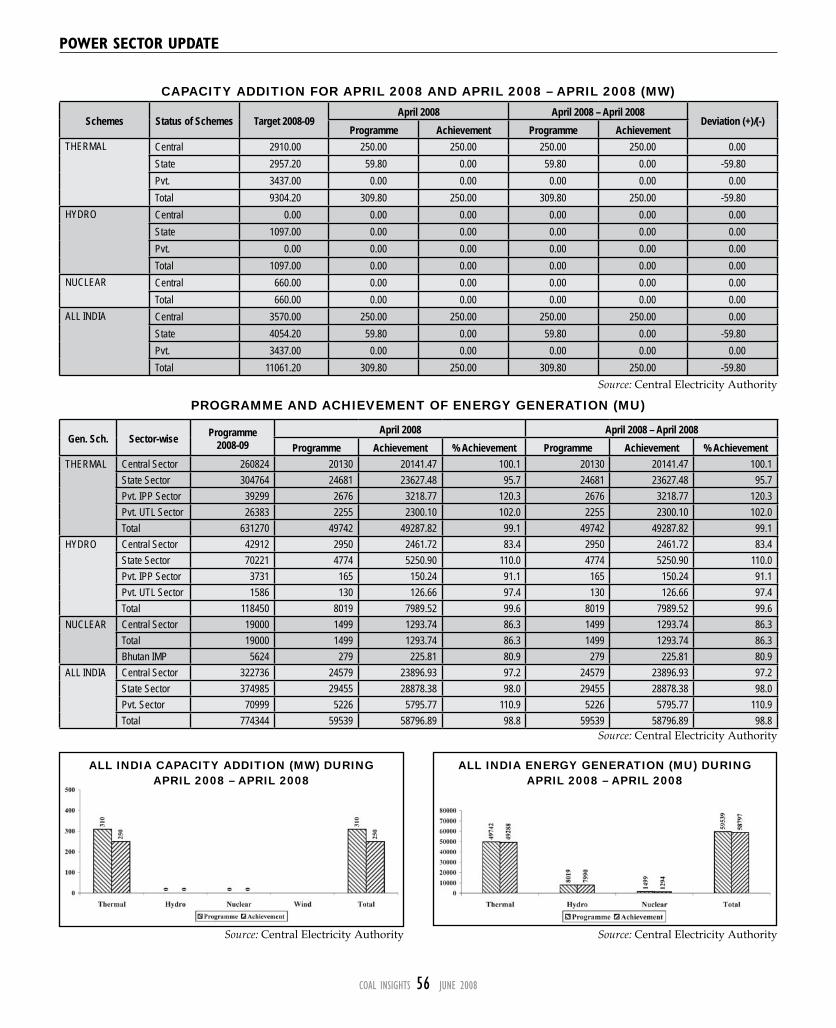

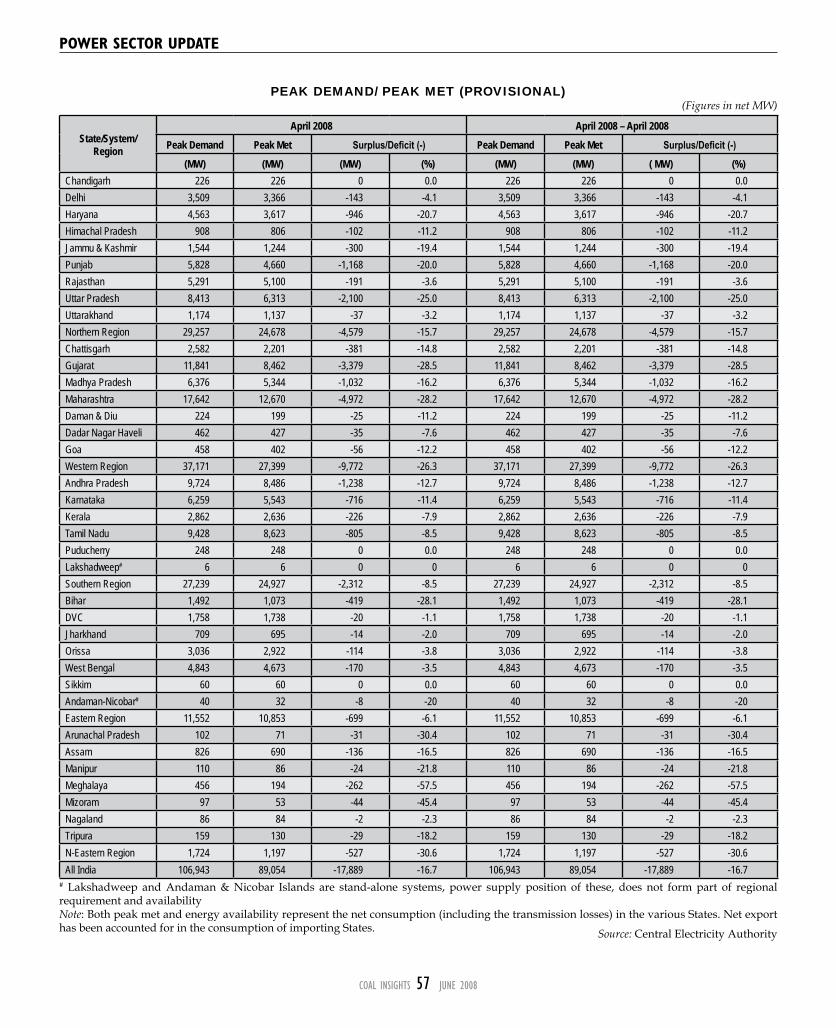

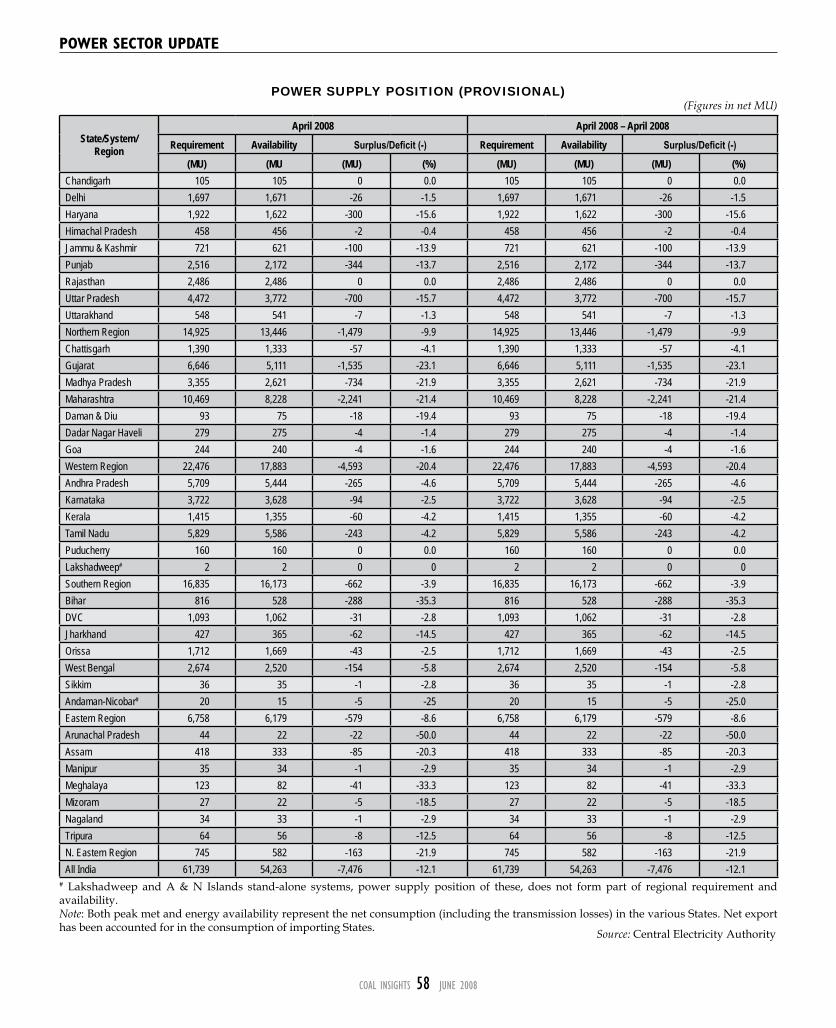

poweR seCtoR upDate51 All India installed capacity52 All India energy generation

programme 57 Peak Demand/ Peak Met

(Provisional) 58 Power Supply Position (Provisional)

snapshot63 Lack of funds plague Tanzania coal

sector

Coal wiRe64 Domestic News70 International News

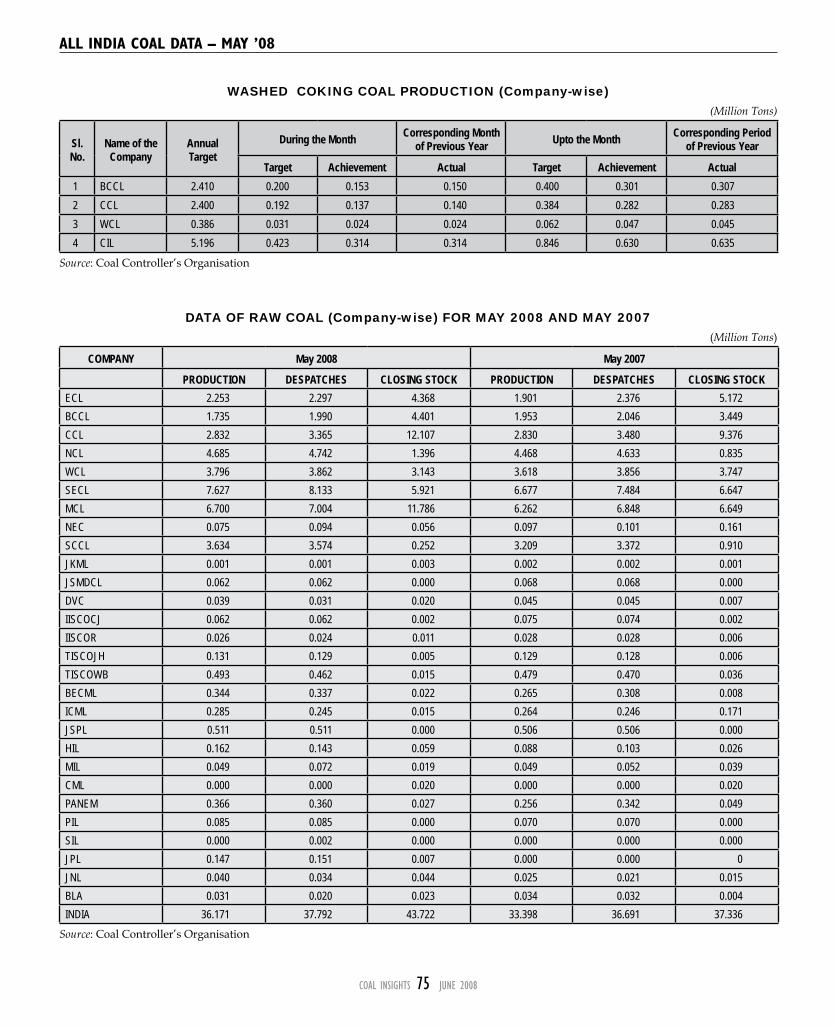

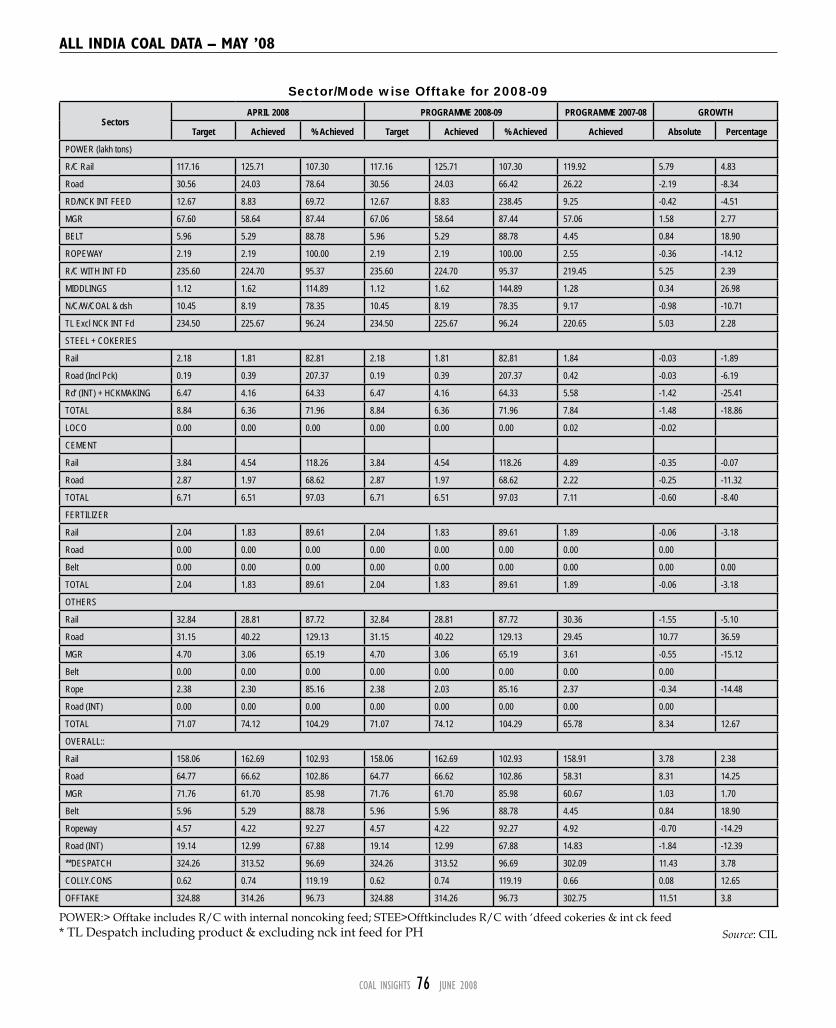

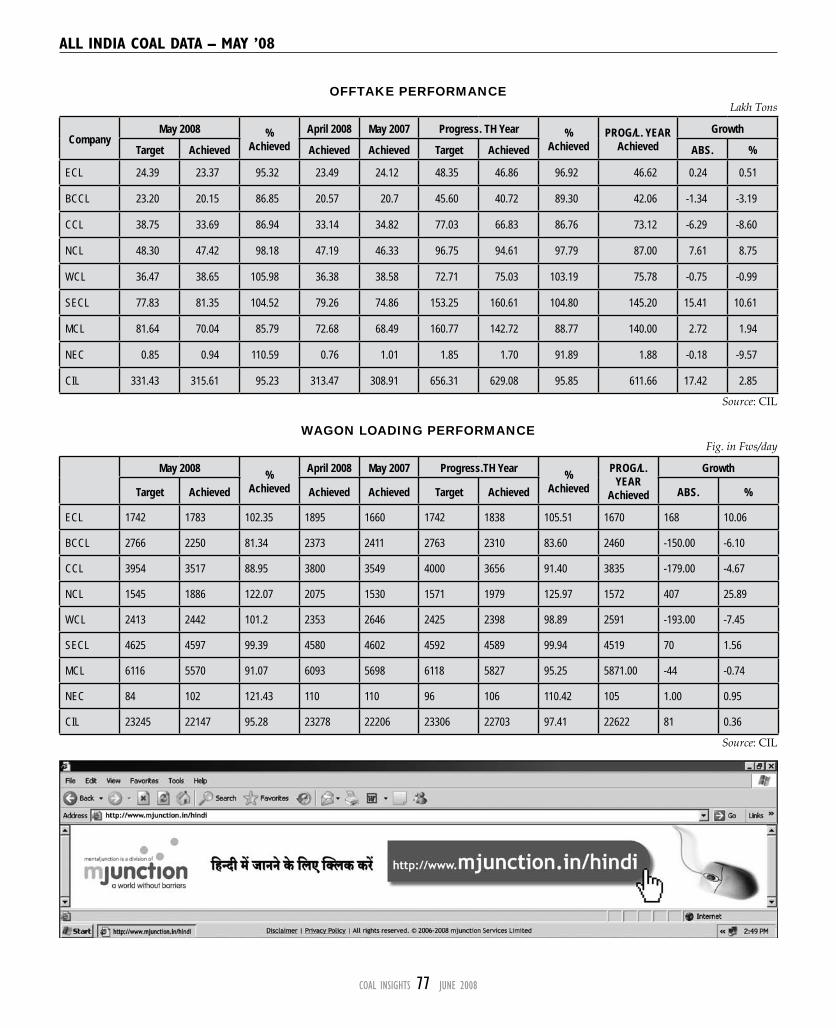

all inDia Coal Data 73 Coal Production Data

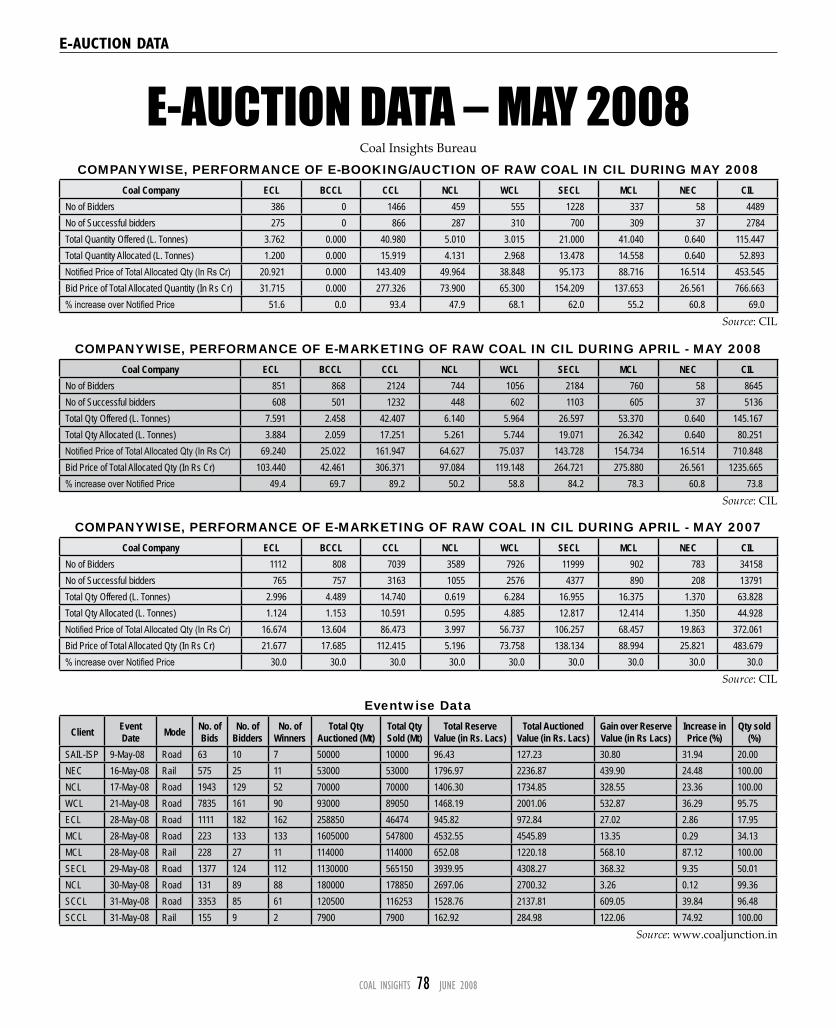

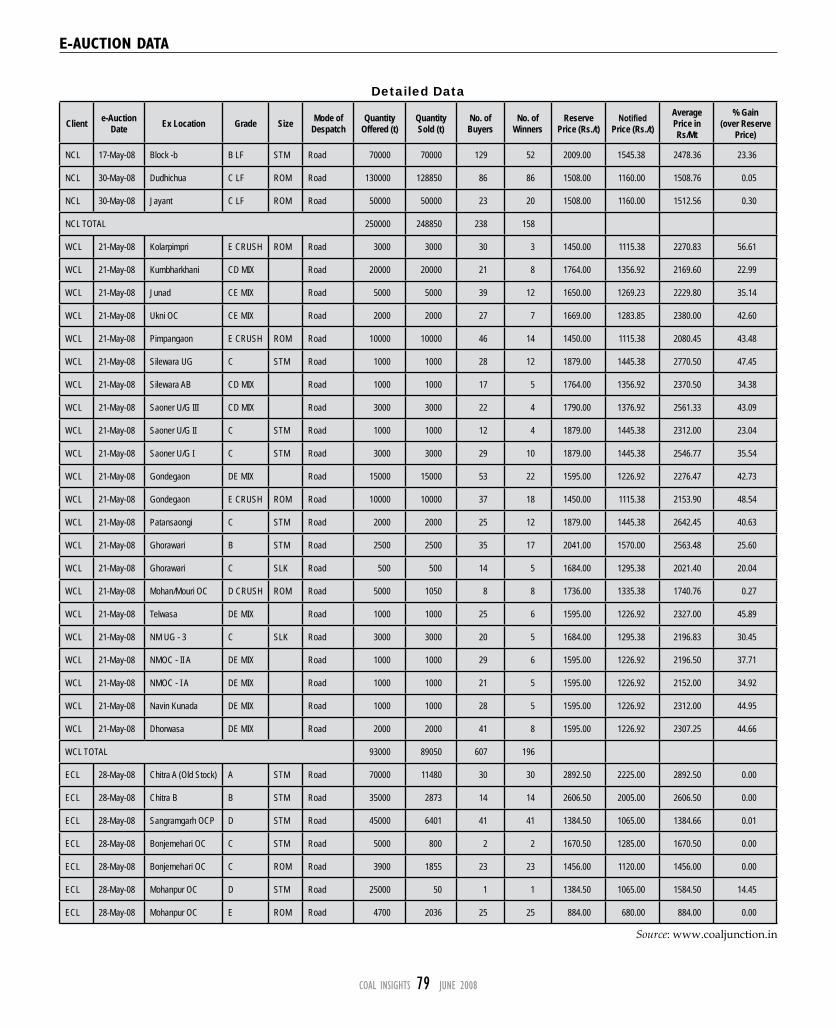

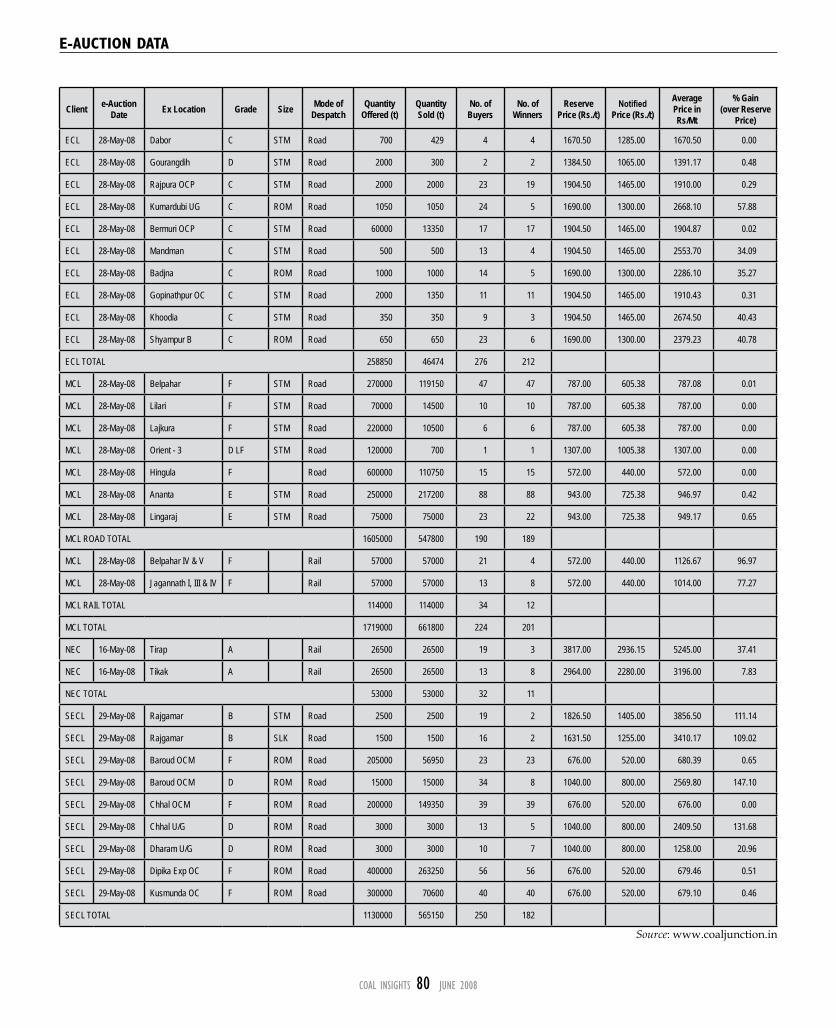

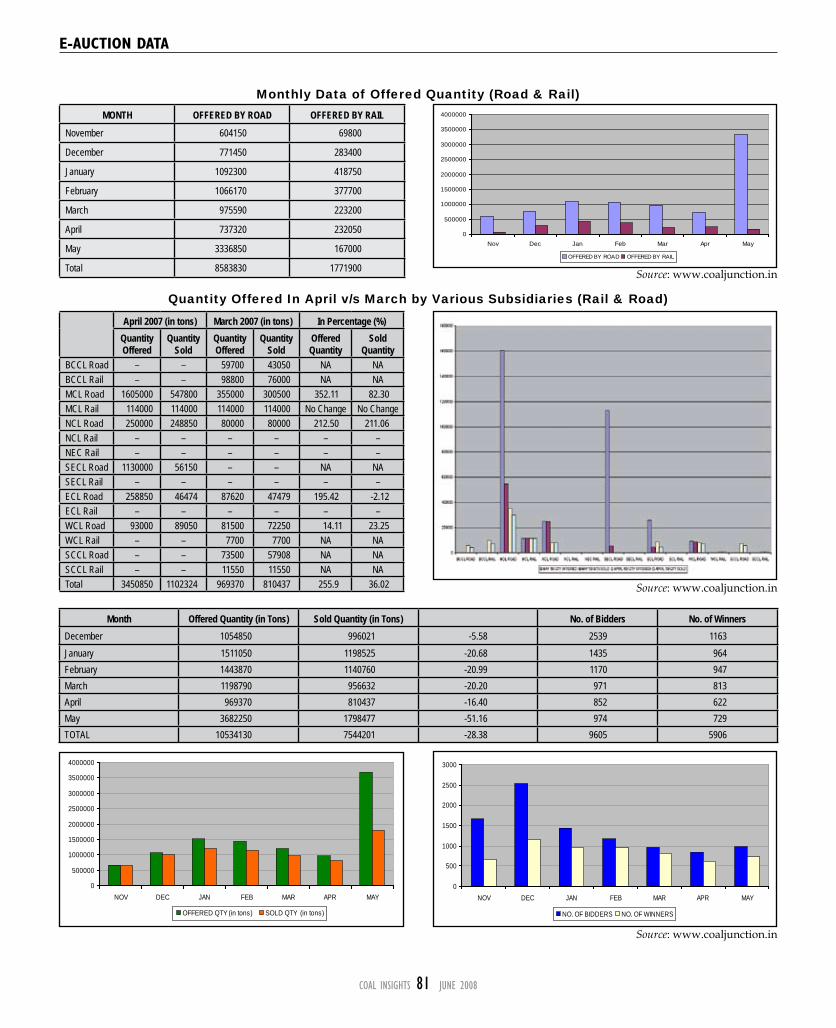

e-auCtion Data 78 E-auction details of CIL 79 E-auction by coaljuntion

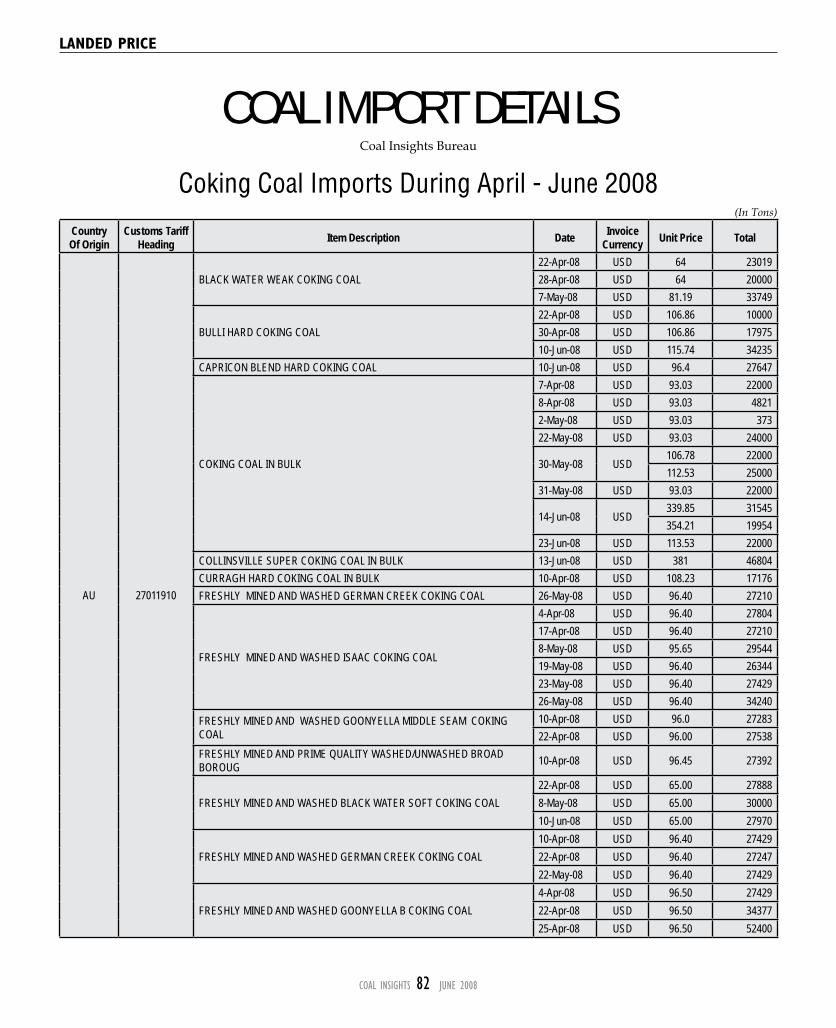

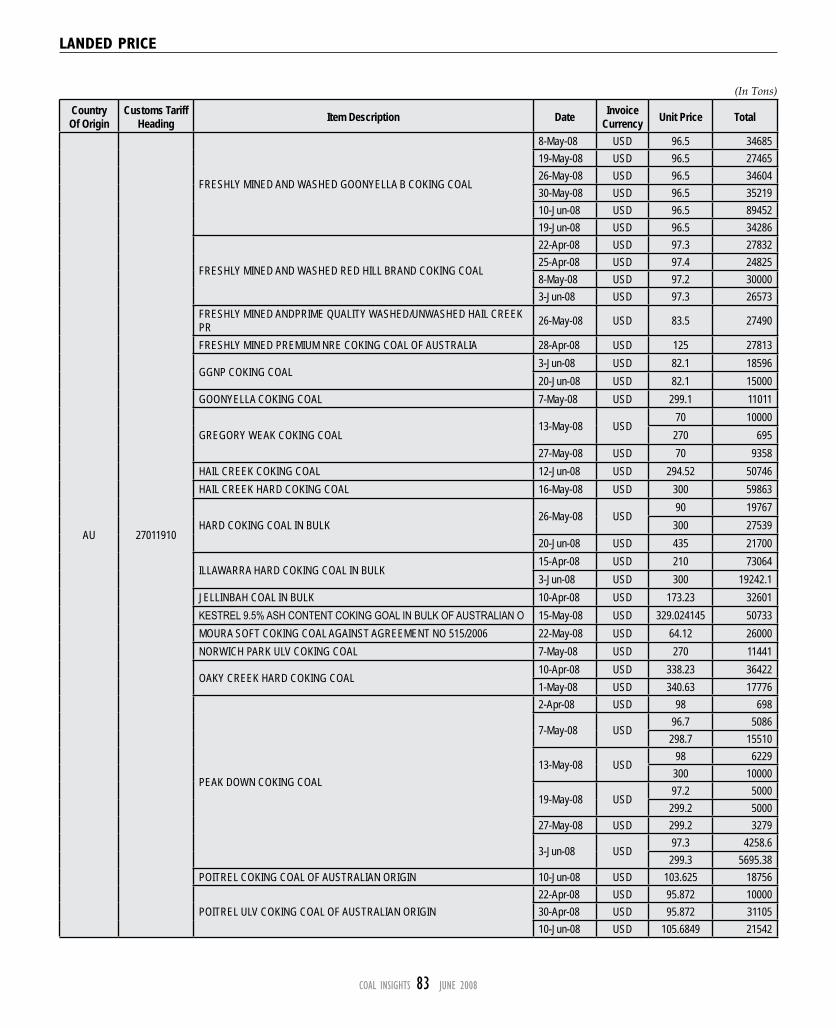

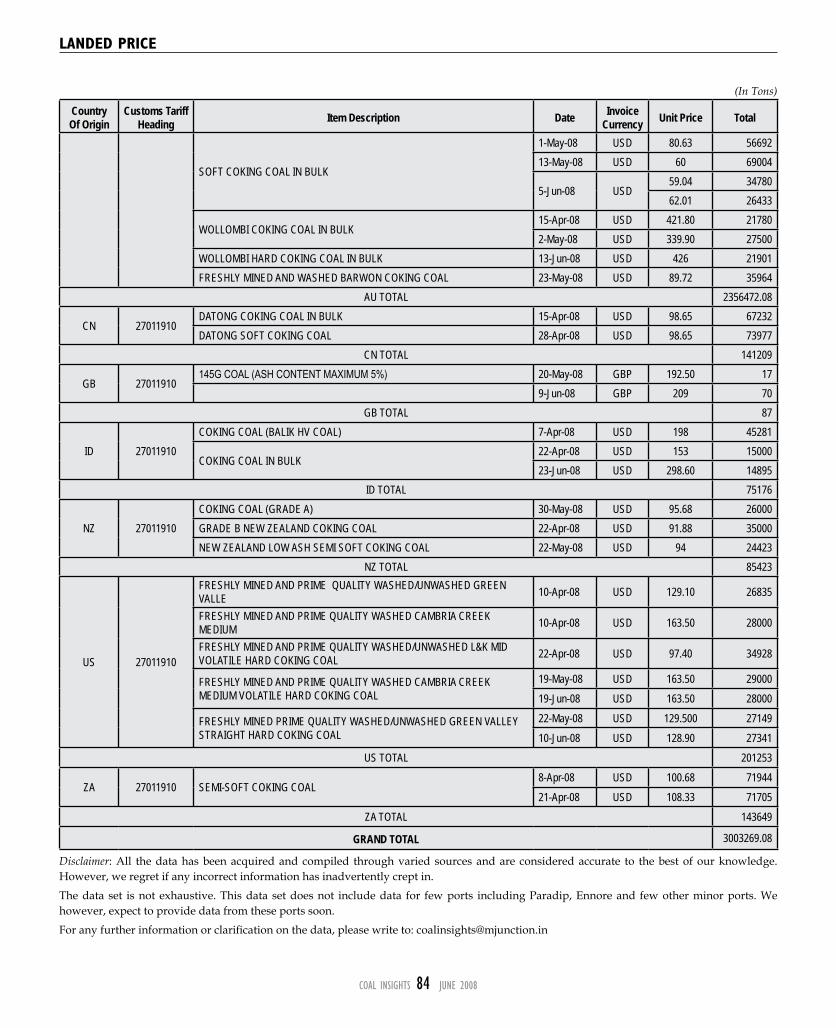

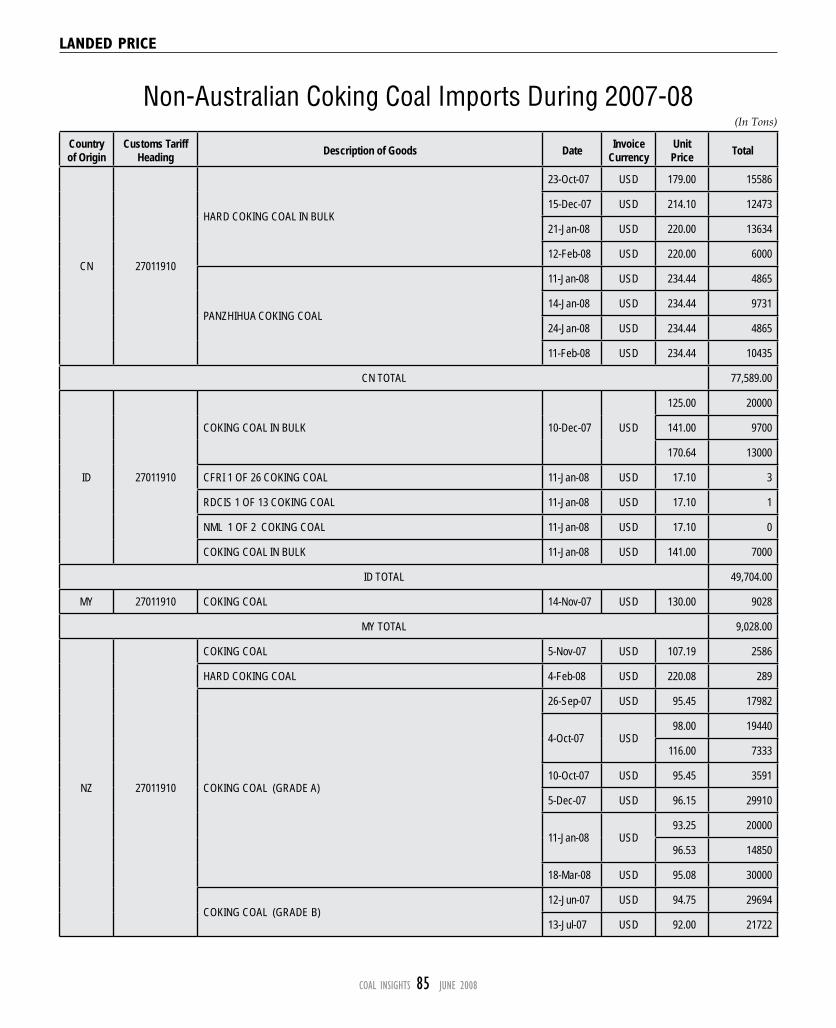

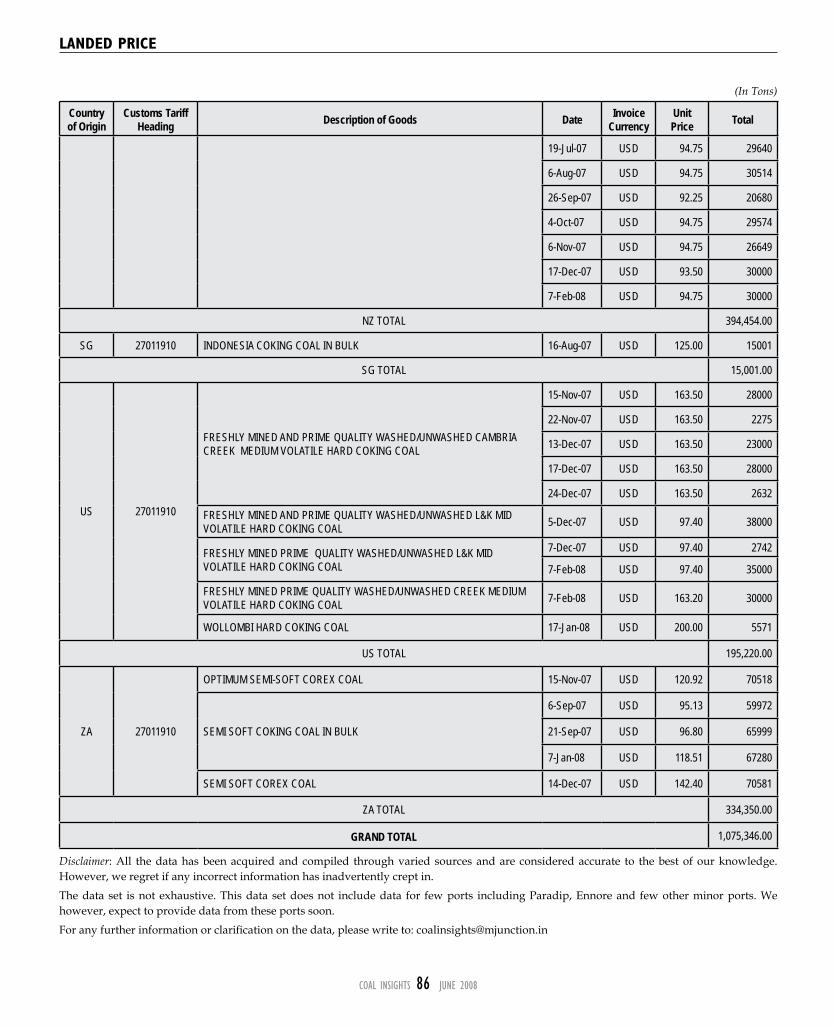

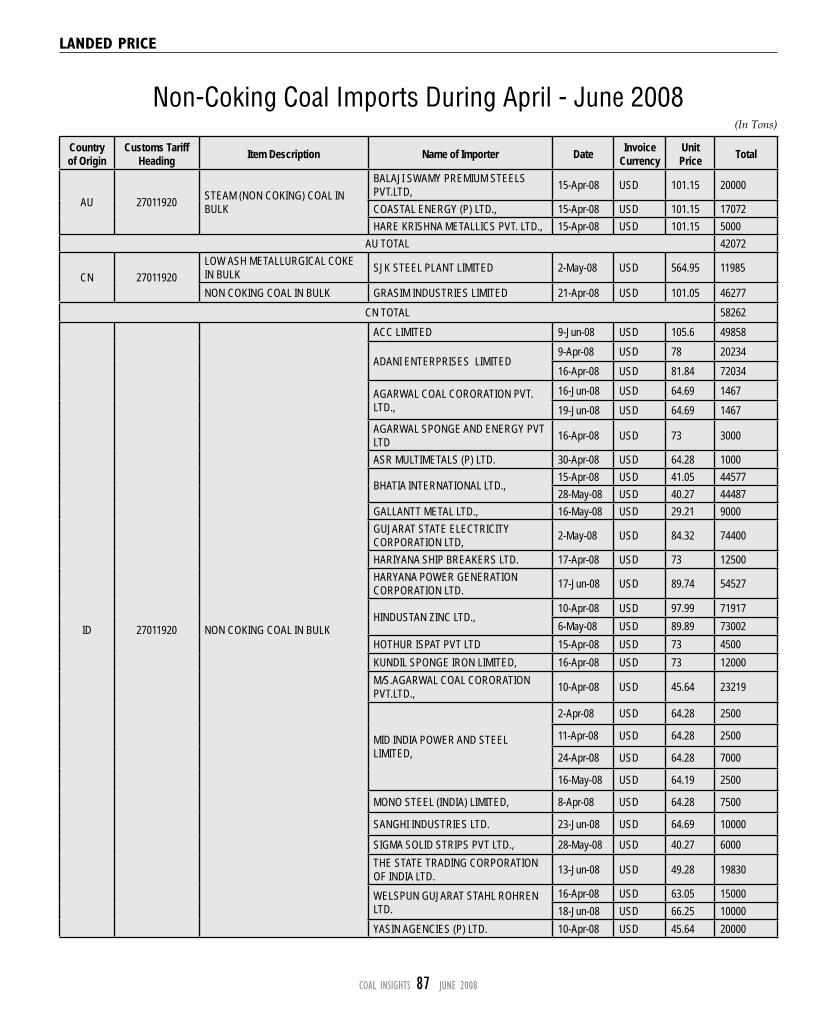

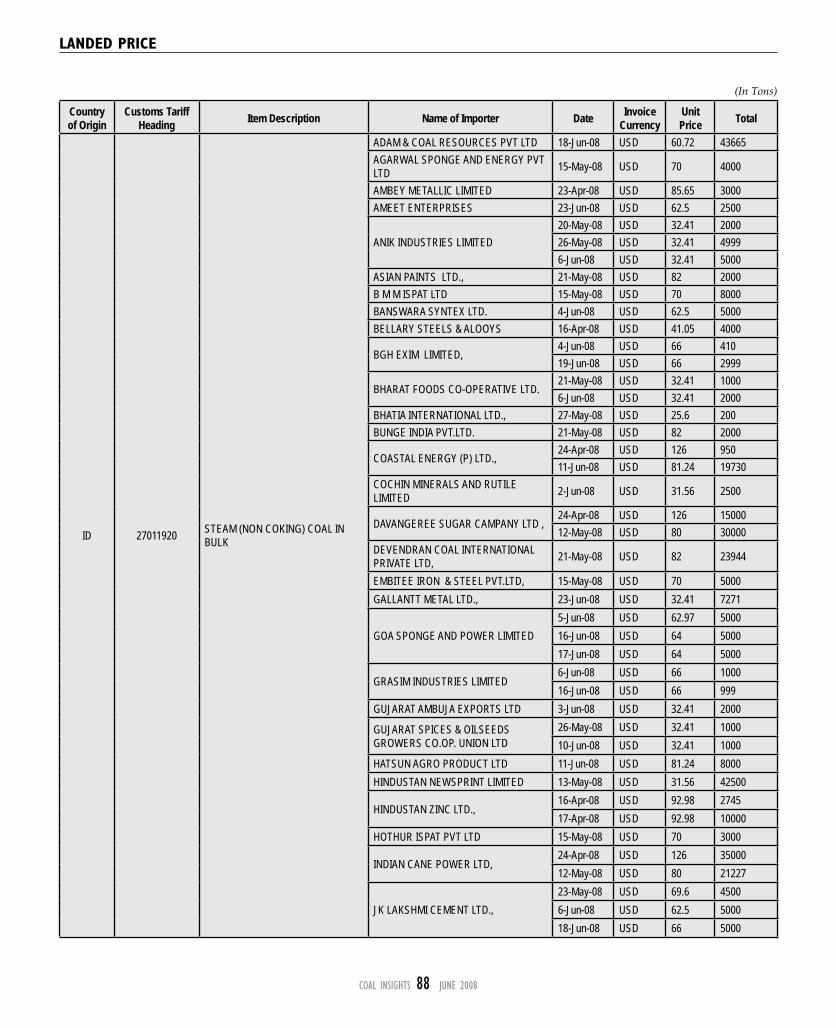

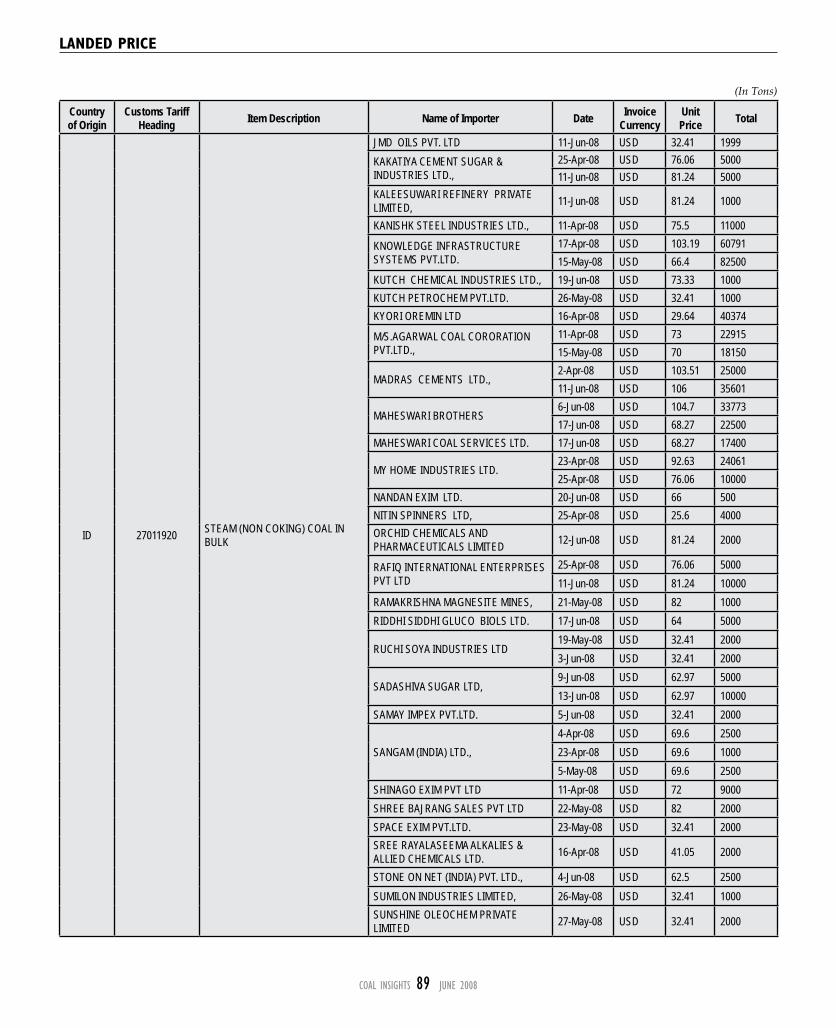

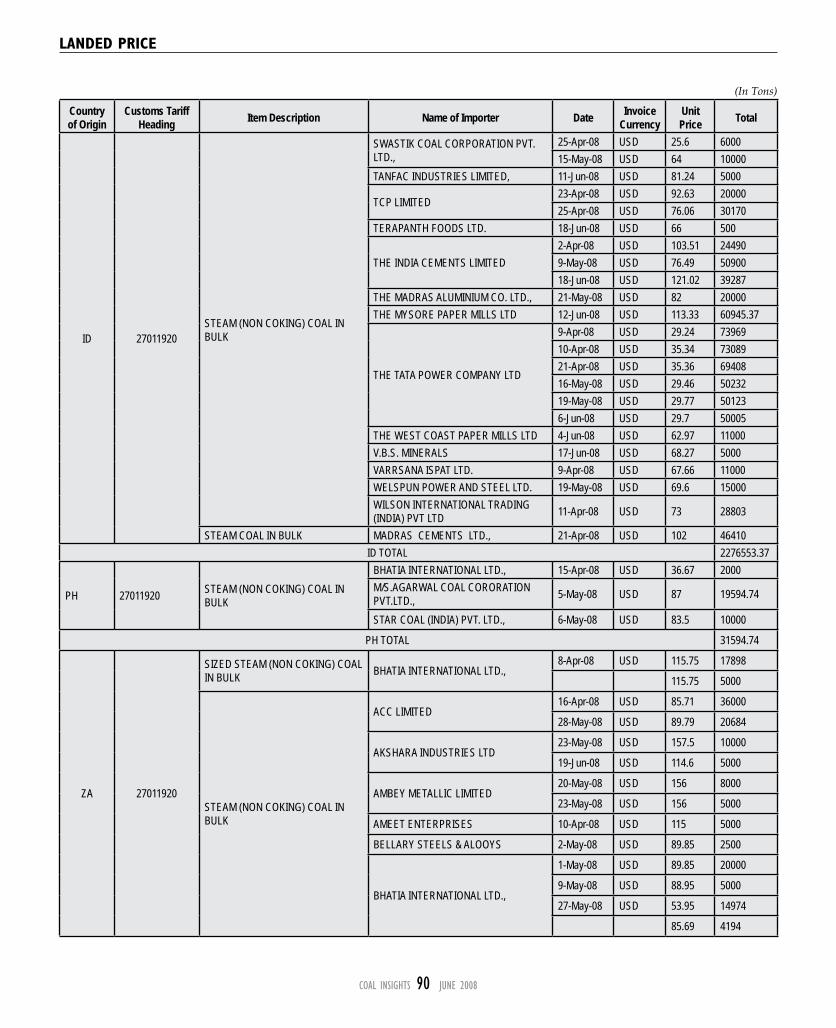

Coal iMpoRt Data 82 Coking coal during April - June 200885 Non-Australian Coking Coal Imports

During 2007-08 87 Non-coking coal during April - June

2008

COAL INSIGHTS � JUNE 2008

LETTERs TO EDITOR

EditorCoal Insights

14 June 08

Your May issue of Coal Insights, which handled the issue of land acquisition in India with great sensitivity and in great detail, was thought provoking, to say the least.

Land acquisition has become a critical impediment in the industrialisation of India, and there is little doubt that uncertainties on land acquisition are costing the nation dearly both in terms of time and money. Very few realise that precious opportunities are being lost, which may not again come India’s way.

It may be misconstrued that I am only voicing the industry perspective, without any insight into the trials and tribulations of landowners who have to give up their land. Here, I would like to present my personal experience on the matter.

As the managing director of the then Ipitata Sponge Iron Ltd, which is now Tata Sponge Iron Ltd, a joint sector undertaking between the Orissa government and Tata Steel, I was personally involved in acquiring 310 acres of largely agricultural land in Bilaipada near Joda in the Keonjhar District of Orissa. This was done as far back as in 1980-82. Things may have been different 25 years ago, but the lessons that I learned are perhaps valid even today.

No amount of policy making and legislation can resolve the issue of acquiring the land belonging to farmers and villagers who have been living in an area for generations together. It is an emotional bonding, and emotions inevitably do not know logic. In Orissa for example, there is a tradition in some villages that they bury their dead within their premises, i.e. in the courtyard of their own residence. For them, to give up land for industrialisation becomes an extremely difficult emotional decision because of obvious reasons.

Yet, my own experience was that everything can be won over by faith and trust. It is possible to make them feel a part of the development and then acquire their land. In Ipitata’s case, more than 80 percent of the land was farmland in which paddy was grown. All that we promised was that irrespective of how much land was being acquired from any individual landowner, Ipitata would provide one job for the family. We kept our word and more than 200 wards or nominees of landowners were given jobs in Ipitata either before or soon after the plant commenced operation in 1986-87.

In the interim period, we also made sure that the landowner nominees were given jobs matching their skills by the contractors involved in erection of the plant. As the CEO, I faced no problem at all with the villagers during the five years that I was involved with Ipitata. I think it was the trust that the villagers had in me was responsible for the largely smooth stint.

One of the articles in your issue correctly focuses on trust as the key factor in acquisition of land. If the intentions of the

company involved are clear and honest, it is not very difficult to get the trust of innocent and simple villagers.

What spoils the whole atmosphere is the interference of politicians and other agencies that are busy looking after their own small gains and selfish interests. I am afraid no amount of R & R Policy initiated by CIL and other big agencies can get around this issue. Whether it is the Tata Motor’s project in Singur, or the Enron project in Maharashtra, or several other projects throughout India, the common thread in all land disputes is interference from politicians.

I was lucky that when I was in Orissa, the authorities were able to rise above their own immediate gains. I admit that things are not as easy as they sound. Simply offering compensation money, for instance, is no solution. Ours is a poor country, and here we are talking of dealing with often the poorest of the poor. Among a lot of other procedural problems, one is the sudden emergence of “relatives” after compensation money has already been paid!

I thought I should communicate my views as land acquisition is becoming a painful but a real obstacle to the industrialisation of India, and pertinent experience can always be helpful for policymakers. Amartya Sen himself pointed out that, “Manchester was once a village.” If we want to create many Manchesters in India, we cannot let these issues spoil the party.

I would also like to take this opportunity to say that all the publications of mjunction look great and maintain very high standards in their presentation and designing, as well as the quality of their content. I congratulate the Chief Editor, Kohinoor Mandal, and his entire team for this.

This is indeed a true reflection of the work culture at mjunction, which has been carefully nurtured by your Managing Director, Viresh Oberoi.

I feel proud that you are a part of the Tata family, with which I have been associated for the last 36 years. Kudos to all of you at mjunction.

Amit Chatterjee,Adviser to the MD,Tata Steel

I read Coal Insights regularly and thoroughly, and I feel it covers the coal industry extensively and effectively.

However, I would like to put in a word on how I feel the magazine can be improved further. I suggest you should highlight the expectations and perceptions of people in the country from coal companies. In fact, it would be really good if you can cover the expectations and perceptions of the common man who is in no way related to the coal business.

The general perception of Coal India now is not very encouraging. I feel Coal Insights can play a big role in improving the public perception of Coal India, whose contribution in India’s energy generation is enormous.

If you give the truth to people, at least Coal India will be projected correctly, as a company which supplies 80 percent of coal to fire all the thermal power stations in the country.

S.R. UpadhyayChairman cum Managing Director,Mahanadi Coalfields Ltd.

COAL INSIGHTS 8 JUNE 2008

COAL mARkET funDAmEnTALs

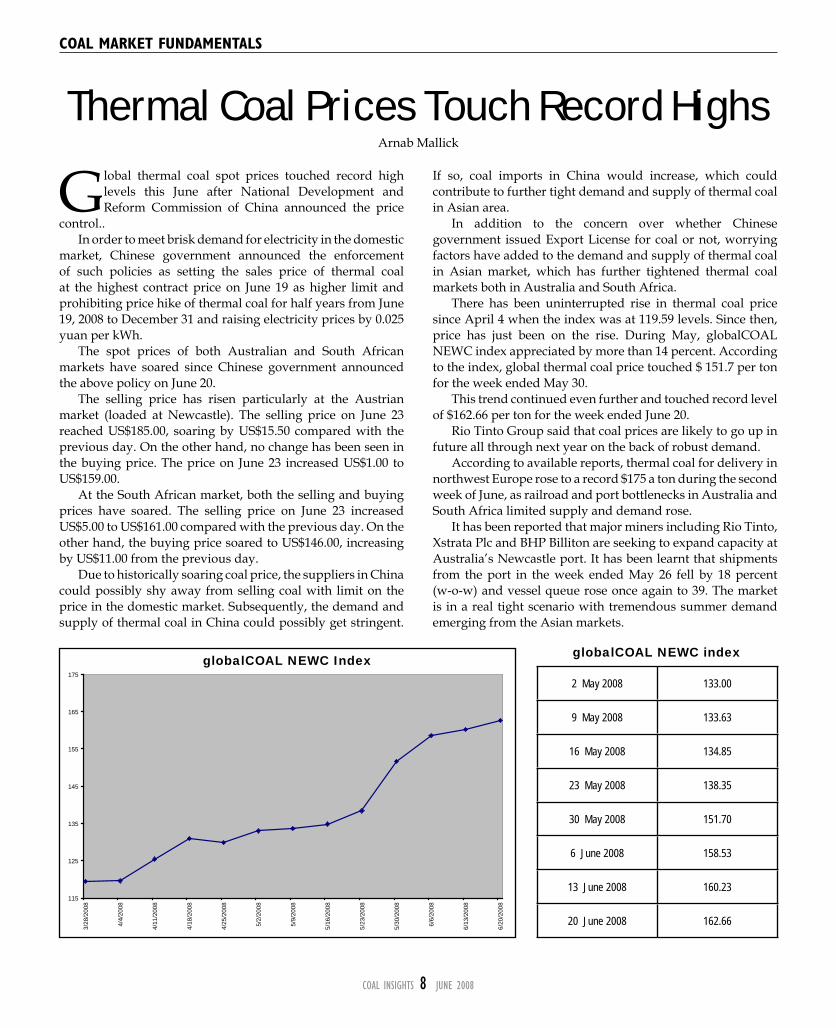

Global thermal coal spot prices touched record high levels this June after National Development and Reform Commission of China announced the price

control.. In order to meet brisk demand for electricity in the domestic

market, Chinese government announced the enforcement of such policies as setting the sales price of thermal coal at the highest contract price on June 19 as higher limit and prohibiting price hike of thermal coal for half years from June 19, 2008 to December 31 and raising electricity prices by 0.025 yuan per kWh.

The spot prices of both Australian and South African markets have soared since Chinese government announced the above policy on June 20.

The selling price has risen particularly at the Austrian market (loaded at Newcastle). The selling price on June 23 reached US$185.00, soaring by US$15.50 compared with the previous day. On the other hand, no change has been seen in the buying price. The price on June 23 increased US$1.00 to US$159.00.

At the South African market, both the selling and buying prices have soared. The selling price on June 23 increased US$5.00 to US$161.00 compared with the previous day. On the other hand, the buying price soared to US$146.00, increasing by US$11.00 from the previous day.

Due to historically soaring coal price, the suppliers in China could possibly shy away from selling coal with limit on the price in the domestic market. Subsequently, the demand and supply of thermal coal in China could possibly get stringent.

If so, coal imports in China would increase, which could contribute to further tight demand and supply of thermal coal in Asian area.

In addition to the concern over whether Chinese government issued Export License for coal or not, worrying factors have added to the demand and supply of thermal coal in Asian market, which has further tightened thermal coal markets both in Australia and South Africa.

There has been uninterrupted rise in thermal coal price since April 4 when the index was at 119.59 levels. Since then, price has just been on the rise. During May, globalCOAL NEWC index appreciated by more than 14 percent. According to the index, global thermal coal price touched $ 151.7 per ton for the week ended May 30.

This trend continued even further and touched record level of $162.66 per ton for the week ended June 20.

Rio Tinto Group said that coal prices are likely to go up in future all through next year on the back of robust demand.

According to available reports, thermal coal for delivery in northwest Europe rose to a record $175 a ton during the second week of June, as railroad and port bottlenecks in Australia and South Africa limited supply and demand rose.

It has been reported that major miners including Rio Tinto, Xstrata Plc and BHP Billiton are seeking to expand capacity at Australia’s Newcastle port. It has been learnt that shipments from the port in the week ended May 26 fell by 18 percent (w-o-w) and vessel queue rose once again to 39. The market is in a real tight scenario with tremendous summer demand emerging from the Asian markets.

Thermal Coal Prices Touch Record HighsArnab Mallick

globalCOAL NEWC index

2 May 2008 133.00

9 May 2008 133.63

16 May 2008 134.85

23 May 2008 138.35

30 May 2008 151.70

6 June 2008 158.53

13 June 2008 160.23

20 June 2008 162.66

115

125

135

145

155

165

175

3/28

/200

8

4/4/

2008

4/11

/200

8

4/18

/200

8

4/25

/200

8

5/2/

2008

5/9/

2008

5/16

/200

8

5/23

/200

8

5/30

/200

8

6/6/

2008

6/13

/200

8

6/20

/200

8

globalCOAL NEWC Index

COAL INSIGHTS 10 JUNE 2008

COAL mARkET funDAmEnTALs

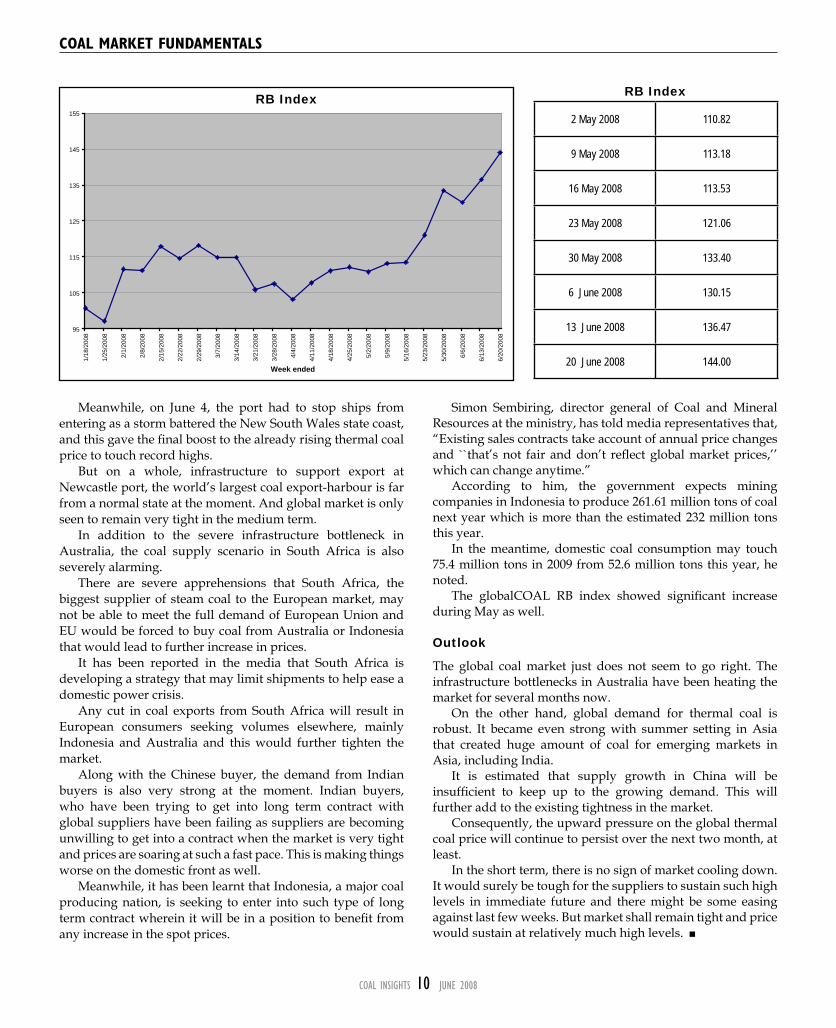

Meanwhile, on June 4, the port had to stop ships from entering as a storm battered the New South Wales state coast, and this gave the final boost to the already rising thermal coal price to touch record highs.

But on a whole, infrastructure to support export at Newcastle port, the world’s largest coal export-harbour is far from a normal state at the moment. And global market is only seen to remain very tight in the medium term.

In addition to the severe infrastructure bottleneck in Australia, the coal supply scenario in South Africa is also severely alarming.

There are severe apprehensions that South Africa, the biggest supplier of steam coal to the European market, may not be able to meet the full demand of European Union and EU would be forced to buy coal from Australia or Indonesia that would lead to further increase in prices.

It has been reported in the media that South Africa is developing a strategy that may limit shipments to help ease a domestic power crisis.

Any cut in coal exports from South Africa will result in European consumers seeking volumes elsewhere, mainly Indonesia and Australia and this would further tighten the market.

Along with the Chinese buyer, the demand from Indian buyers is also very strong at the moment. Indian buyers, who have been trying to get into long term contract with global suppliers have been failing as suppliers are becoming unwilling to get into a contract when the market is very tight and prices are soaring at such a fast pace. This is making things worse on the domestic front as well.

Meanwhile, it has been learnt that Indonesia, a major coal producing nation, is seeking to enter into such type of long term contract wherein it will be in a position to benefit from any increase in the spot prices.

Simon Sembiring, director general of Coal and Mineral Resources at the ministry, has told media representatives that, “Existing sales contracts take account of annual price changes and ``that’s not fair and don’t reflect global market prices,’’ which can change anytime.”

According to him, the government expects mining companies in Indonesia to produce 261.61 million tons of coal next year which is more than the estimated 232 million tons this year.

In the meantime, domestic coal consumption may touch 75.4 million tons in 2009 from 52.6 million tons this year, he noted.

The globalCOAL RB index showed significant increase during May as well.

Outlook

The global coal market just does not seem to go right. The infrastructure bottlenecks in Australia have been heating the market for several months now.

On the other hand, global demand for thermal coal is robust. It became even strong with summer setting in Asia that created huge amount of coal for emerging markets in Asia, including India.

It is estimated that supply growth in China will be insufficient to keep up to the growing demand. This will further add to the existing tightness in the market.

Consequently, the upward pressure on the global thermal coal price will continue to persist over the next two month, at least.

In the short term, there is no sign of market cooling down. It would surely be tough for the suppliers to sustain such high levels in immediate future and there might be some easing against last few weeks. But market shall remain tight and price would sustain at relatively much high levels.

RB Index

2 May 2008 110.82

9 May 2008 113.18

16 May 2008 113.53

23 May 2008 121.06

30 May 2008 133.40

6 June 2008 130.15

13 June 2008 136.47

20 June 2008 144.00

95

105

115

125

135

145

155

1/18

/200

8

1/25

/200

8

2/1/

2008

2/8/

2008

2/15

/200

8

2/22

/200

8

2/29

/200

8

3/7/

2008

3/14

/200

8

3/21

/200

8

3/28

/200

8

4/4/

2008

4/11

/200

8

4/18

/200

8

4/25

/200

8

5/2/

2008

5/9/

2008

5/16

/200

8

5/23

/200

8

5/30

/200

8

6/6/

2008

6/13

/200

8

6/20

/200

8

Week ended

RB Index

COAL INSIGHTS 12 JUNE 2008

COAL mARkET funDAmEnTALs

With the conclusion of long term agreement (LTA) for the current fiscal between global steel leaders and coking coal producers, Indian steelmakers too

managed to finalise delivery contracts for the financial year beginning July. Following the recently set benchmark of around $300 a ton by Japanese steel makers, the Steel Authority of India Ltd (SAIL) has signed an LTA at the same price.

SAIL has signed contracts with six to seven suppliers. It is estimated that SAIL would import 13-14 million tons in 2008-09. These contracts will cover more than 90 percent of its needs. The suppliers are based in Australia, New Zealand and the US. It is learnt that another leading private steel maker has also signed LTA and the price settled was around 15 percent more than the benchmark price.

Leading coke makers have also been finalising their deals. Pike River Coal Ltd has recently announced that it has settled selling price of its premium hard coking coal with two Japanese steel mills as well as Gujarat NRE Coke Ltd and Saurashtra Fuels Pvt Ltd at $300 per ton.

Meanwhile, Australian company Wesfarmers Ltd, has more than tripled the price it charges for Curragh Mine coking coal. It is expected to get prices as high as $300 a ton. According to the company’s statement, Queensland mine output will be within the forecast of 6.1-6.5 million tons for the year ending June 30.

Amid the tightness in the supply market, the demand is pretty robust and likely to remain so in the second half of the year. But continuing infrastructure bottlenecks in Australia and natural calamities at other parts of the globe may worsen the coking coal supply scenario. However, there are growing apprehensions about the shortage of export licence (EL) from China. There are rumours that the Chinese government might release additional EL of 21.20 million tons. But at this stage, it is not known when this will be released, or whether it shall be released at all.

The Tex Report said due to EL shortage, there have already been cases of cancellation of existing contracts for low volatile PCI coal and other types to Japan and South Korea and further delay in release of additional EL might trigger many such cancellations. Consequently, things are getting even tighter.

Meanwhile, as per a recent Tex Report article, contract negotiations on hard coking coal of Australia origin for fiscal 2008 between Japanese BFs and Xstrata Coal is facing difficulties as Xstrata is asking for a steep price rise, far exceeding the contract price that has been settled with other suppliers.

Global Trade Scenario

ImportsAccording to customs clearance statistics of China, coking coal imports of the country have gone down by 9.6 percent

(y-o-y) in April 2008 at 5.31 lakh tons, against previous year’s corresponding figure of 5.88 lakh tons.

South Korea imported 2.18 million tons of coking coal in April 2008 at an average price of $148.16 a ton. In May 2008, imports fell to 1.35 million tons at an average price of $206.26 a ton. According to Japan’s finance ministry, Japan imported 2.05 million tons of coking coal in March 2008 at an average price of $111.18 a ton. However, average import price of coking coal from China during the same period stood at $210.44 per ton. Meanwhile, Taiwan imported 4.96 million tons in April 2008 registering 22.9 percent y-o-y growth.

ExportsAustralia’s hard coking coal export during January-March 2008 has recorded over 13 percent decline (y-o-y) to 17.63 million tons from previous year’s comparable figure of 20.42 million tons. In April 2008, the US exported 3.90 million tons of coking coal at an average price of $131.71 per ton.

OutlookUBS AG has revised its forecast for coking coal price upwards by 50 percent for next year. It has put the figure at $300 per ton from the previous estimate of $200 per ton, primarily on the back of slow output growth from mines in Australia and Canada, and robust growth in demand from steel makers across the globe.

A Credit Suisse group analyst has estimated coking coal price to increase to more than $350 per ton on back of similar apprehensions. Merrill Lynch & Co. has also raised its forecasts for coking coal to $320 a ton next year, 78 percent more than the previous estimate. Macquarie Group Ltd has also said in a recent report that supply of coking coal will fall short of consumption this year also.

According to a recent Dow Jones report, New World Resources NV may increase its coking coal prices by as much as 40 percent next year to match international market rates.

Dow Jones cited Executive Chairman Mike Salamon said that the company is selling at an average price of $213 ton this year compared with world prices of about $300, leaving ``a lot of room to catch up.” New World, which produces about 6.7 million tons of coking coal annually, raised prices by 61 percent this year, Dow Jones said.

In a nutshell, our outlook remains the same as it has been over the last few months. The market is in an extremely tight state with contract prices seeing record levels. Interestingly, even at these high prices steel makers are finding it difficult to finalise contracts as suppliers are trying to make the most of the optimistic mood, thanks to the severe supply crunch.

SAIL signs LTA for $300 a ton

Coking coal prices likely to keep soaringArnab Mallick

COAL INSIGHTS 1� JUNE 2008

COvER sTORy

In what is being termed as another bold move after the fuel price hike, the UPA government is pushing for disinvestment in profit-making PSUs. This time, the list

includes the world’s largest coal producing company, Coal India Ltd (CIL).

In a letter, the Department of Disinvestment under Finance Minister P. Chidambaram, has asked the Coal Ministry to seriously consider selling 10 percent stake in wholly state-owned CIL through an initial public offer (IPO).

CIL has a paid-up capital of Rs 6,316 crore and has posted aggregate profits of Rs 9,576.22 crore in 2007-08, 12 percent higher than the previous financial year.

Besides detailed financial information on CIL, the Finance Ministry is understood have also sought the Coal Ministry’s assessment of the company’s valuation in today’s market condition.

Incidentally, the idea of IPO was first floated around two years back in the beginning of 2006. There was a proposal of partial stake sale of 5 percent in CIL through an IPO, which ran into rough weather due to political reasons. The Finance Ministry has now asked the Coal Ministry to reconsider the IPO proposal.

Meanwhile, the Coal Ministry is gearing up to seek a third party opinion on valuation. The IPO could be through a combination of issue of fresh shares and part sale of government equity. Either way, Coal Ministry sources admit that the move will trigger angry reactions from its Left allies who consider coal mining areas as their traditional strongholds.

CIL is the holding company of seven coal producing companies - Northern Coalfields, South Eastern Coalfields, Western Coalfields, Mahanadi Coalfields, Eastern Coalfields, Bharat Coking Coal and Central Coalfields. It is also the holding company of Coal Mining and Development Planning Institution, a research and development arm.

It is understood that the proposed IPO will be for CIL as a whole, and the subsidiaries will not be listed separately.

CIL’s equity base comprises 63.16 million equity shares of Rs 1,000 each. The shares of Rs 1,000 face value are likely to be split to a face value of Rs 10 each before the IPO. It is expected that through the IPO, the company will be able to mobilise funds to the tune of more than Rs 7,000 crore.

While the funds raised through fresh issue of shares would be used by CIL for its own expansion plans, that mopped up through sale of government equity would accrue to the government kitty.

As of now, it appears that the Coal Ministry under Prime

Fate of Coal India IPO

Plan Hangs In BalanCeCoal Insights Bureau

Minister Manmohan Singh has not yet taken any view of its own in the issue, and is waiting for inputs from CIL.

Doubts over IPOMany in the financial market circles, however, doubt whether the proposed IPO will ultimately materialise. The last time the UPA tried to push the disinvestment agenda through an IPO of Neyveli Lignite Corporation, it had to go back on a Cabinet decision since the alliance’s southern ally, the Dravida Munnetra Kazhagam, threatened to pull out.

Meanwhile, Coal Minister Santosh Bagrodia confirmed that the finance ministry had asked for some details about the company. “We have in turn asked CIL for information,” he said. However, it is said that since the present policy does not envisage disinvestment by the government in a Navratna company — a status which CIL is expecting shortly — the finance ministry’s proposal seems to be aimed at ensuring that the IPO precedes the Navratna status.

Last month, the finance ministry was faced with a similar situation when the follow-on public offer of NTPC Ltd, a Navratna company, came up. The ministry could not agree to the proposal as it was against the disinvestment policy.

Market analysts, however, said the environment was not conducive for any large IPO at this stage. “I am sure the finance ministry will have second thoughts about the IPO because they would also like to wait to have best possible valuation for the equity,” said a Mumbai-based analyst, citing the recent slide in the Sensex and the Nifty.

“Though the move may be part of the government’s overall strategy to raise funds (through profit making PSUs) but the actual implementation will be difficult till the market stabilises,” added the analyst.

COAL INSIGHTS 1� JUNE 2008

COvER sTORy

Coal India’s initial public offering (IPO) plan has been gathering dust for more than two years now. The then chairman Sashi Kumar first floated the plan that the

company should be allowed to tap the capital market. The proposal was then shelved due to political differences.

It was argued that the IPO will help the company raise funds for future expansion, which was not acceptable to some of the political parties on various grounds.

However, after a gap of more than two years, the proposal has been raised once again. Only this time it has come from the government itself, and not from the company management. This has baffled industry insiders, as the government recently refused a follow on issue to NTPC, another public sector biggie.

At a time when there is heated debate in favour of, or opposing the IPO, Coal Insights thought it prudent to dig slightly deeper and find out what could have been the reason for the government’s sudden change of mind, especially when its major ally – the Left – is dead against any kind of divestment in PSUs.

The Prime Minister’s initiative has been welcomed by industry circles as well as the media. In fact, the popular notion is that the government should divest stake in profit making PSUs and raise capital to cut its expenses by mobilising all its resources in order to check the spiralling inflation.

It is argued that with a paid-up capital of Rs 6,316 crore and posted aggregate profits of about Rs 9,576 crore, Coal India is fairly comfortable financially, and the government would be

able to raise a fairly good amount by divesting even a small part of it.

Similarly, the government should consider divesting from other profitable PSUs and investing the capital raised in development and infrastructure projects.

Others, however, feel that the IPO move is primarily to mop up funds to tide over the country’s financial problems. They have, in fact, likened this to selling family jewels to overcome a crisis that can be done by raising other resources!

It is also being said that a stake sale in chronically sick PSUs makes sense, but to privatise profit-making PSUs is clearly not in order.

Critics also argue that in a polity like ours, the government should remain committed to a strong and effective public sector, whose social objectives are met by commercial functioning. This is especially true of some industries which are reserved for the public sector, coal mining being one.

Divestment is justified by some who claim that the government’s finances are in bad shape and need to be shored up, but that seems a bit exaggerated. And even if that is partly true is the situation so bad that the government needs to put its assets on sale?

The fact is that since Coal India is a profit-making concern, it is capable of mobilising resources for investment and expansion from its own funds. It does not need to take the route of divesting equity in order to mobilise resources for modernisation.

Having gone through some of the arguments since the government decision was made public in early June 2008, Coal Insights tried to find if there could be another explanation for the government’s decision.

We spoke to the Coal India chairman P.S. Bhattacharyya, who in the past had opposed the idea of an IPO, especially at a time when the balance sheet of the company is very healthy and it has huge cash in hand to invest on any kind of expansion and modernisation.

In favour of IPOThis time, however, Bhattacharyya came out with an extremely innovative reason for the need to come out with IPO.

According to him, Coal India has identified nearly 190 projects that would be taken up during the Eleventh Plan to reach the production target of 521 million tons per annum by 2011-12.

Why should CIlgo for the IPO?

Rakesh Dubey

COAL INSIGHTS 17 JUNE 2008

COvER sTORy

For these projects, a total of about 41,000 hectares of land would be needed. Of this, only 12,000 to 13,000 hectares of land falls under the forest area, where there is practically no need to resettle human population. For the rest and majority of the population, acquisition might become a major issue.

With the recent events in Nandigram and Singur where land acquisition process had led to severe repercussions not only from local people, but political parties as well, the acquisition of habitable land for doing mining is going to be a difficult proposition, Bhattacharyya said.

In order to pacify the project-affected people and ensure smooth acquisition of land, Coal India had recently come out with its own Resettlement and Rehabilitation (R&R) policy, taking a cue from the national R&R policy. CIL’s policy talks about total community development instead of merely acquiring land and paying a price for it.

Bhattacharyya feels that if the company goes for an IPO, it would then become easier for it to acquire land. Since it is looking at total community development, the company will be in a position to offer shares to those from whom it is going to acquire land.That will provide an ownership to the displaced people, he said.

A case in point is the recent smooth acquisition of land by Jindal Steel and Power Ltd for its mega greenfield steel project at Salboni in West Bengal, Bhattacharyya said.

Incidentally, the steel company had been able to acquire land by offering shareholding in the company to the oustees, thereby creating a sense of belonging and confidence among them. The idea was not only innovative, but also successful. Not even a single protest over land acquisition at Salboni, which is not far away Singur and Nandigram where largescale violence took place over land acquisition.

Exodus of executivesAnother important issue that the proposed IPO could help to address is the expected largescale exodus of senior executives from Coal India to private mining companies, which have been allotted blocks for captive mining.

Till now poaching of executives from Coal India by private coal companies has not been a major issue, but it is perceived that as soon as these private companies plan to start mining, they will need experienced people to supervise their mining operations.

Private companies are unlikely to get experienced mining executives from any other place other than Coal India and its subsidiary companies.

So once the IPO is in place, Coal India might be in a position to offer Employees Stock Options (ESOP) to its senior executives in order to prevent them from leaving the company.

COAL INSIGHTS 18 JUNE 2008

COvER sTORy

Contrary to expectations that Coal India will immediately jump to take advantage of the government suggestion to come out with an initial public offering, chairman P.S.

Bhattacharyya, in an exclusive interview to Rakesh Dubey, ruled out the possibility before getting the ‘Navratna’ status. Bhattacharyya also shared his views on other developments taking place in the company.

Excerpts:

You have been asked by the government to prepare for IPO. How do you intend to move forward?There is nothing to move forward on, as of now. It is just that the government has taken a general decision that large companies with net worth of more than Rs 200 crore should be listed on the stock exchange. We also feel that should happen and would like to apply with the government for listing. But in terms of priority, we would like to be listed only after getting the ‘Navratna’ status because that will have an impact on our valuation.

By when do you expect to get the ‘Navratna’ status?It should not take too long, because it has already crossed the Inter Ministerial Group stage and now it has to go to the apex committee of secretaries of various ministries. That is the last stage and once it is cleared by the apex committee, it should be through. Given the kind of strategic relevance that we have today vis-à-vis the status of other ‘Navratna’ companies, I don’t see any reason why it should be denied.

CIL is flush with funds, and it does not need to go for IPO to raise funds. So why do you still want to go for it? The biggest benefit that we perceive in IPO is governance. A listed company has to follow certain norms, and we want all our companies to be exposed to the stringent norms in terms of reporting systems.

Another very important thing is we want to issue shares to the landless people as part of the Resettlement and Rehabilitation policy. If they are losing land and gaining ownership in a company, it will help us in acquiring land. We also want to issue shares to employees. We want to build this as part of our R&R policy and that can happen only if the company’s shares are listed on stock exchanges.

You had invited expressions of interest (EOIs) for developing seven underground mines. What is the status?The response of EOI so far is extremely good and we have extended the date of submission of bids to June 27. Hopefully then we will be able to assess the actual response.

What is the status of the EOIs invited to set up washeries?We are expecting a good response. In order to elicit better response, we have removed the clause that says if bidding is done by a consortium company, every member must have experience of either having set up a washery or operating a washery in the past. Now if the consortium in totality has the

experience of setting up and operating a washery, it is enough. Even if the lead member or any member in the consortium does not have such experience, we are OK with it now.

We decided to remove the clause because there could be financers who can put the money together, but does not have the experience. Now we even plan to allow such people to bid.

By when do you expect to invite EOIs for developing abandoned mines?We will invite EOIs for developing 26 abandoned mines, and they will be floated towards the end of June. Once that comes, some of these mines can resume production if world-class technology is made available to them. It is difficult to estimate any production figure from these mines as of now.

Is it true that this plan to invite EOIs to develop abandoned mines came only after ArcelorMittal offered to developed abandoned mines of Coal India? I would say ArcelorMittal’s proposal acted as a catalyst and triggered the process to a certain extent. We took stock of all the abandoned mines and arrived at the number of mines where reserves are there to be exploited. Possibly with the help of some new technology, it should be possible to do this.

no IPO before navratna: CIl chiefGlobal mining firms bid for

CIL’s UG mining pactCompanies like XIndia Ltd, Australia’s White Mining Co, Bucyrus and UK’s Anglo Coal are among the companies who have evinced an interest to carry out an underground mining contract in seven Coal India blocks.

CIL has invited expressions of interest (EoIs) for undertaking underground mining contracts in seven mines located in West Bengal, Jharkhand, Orissa, Chhattisgarh and Maharashtra.

These would be a long-term contract for extracting anything between 2 to 5 million tons (mt) of coal annually from each of these mines. Reserves are in excess of 400 mt in all these blocks and selected parties will invest in installing machinery and equipment in these mines.

Opening up seven new underground mines is part of CIL’s plan to enhance coal production from such mines to balance the supply of coal from opencast and underground mines. Currently, coal production is heavily skewed in favour of opencast mines.

Incidentally, a few companies interested in entering into contracts with CIL for underground mining have asked for more time to participate in the process of expression of interest. Accordingly, the last date for submitting EOIs has been extended from May 25 to June 27.

COAL INSIGHTS 19 JUNE 2008

fEATuRE

The coal ministry is all set to allot blocks for coal-to-liquid (CTL) projects. This is in spite of the Minister of State for Coal, Santosh Bagrodia’s comment barely a month ago

that he was not willing to give much priority to CTL projects. However, it seems the Prime Minister’s wish has finally prevailed. This has happened came exactly a year after an amendment was made in the Coal Mines Act in July 2007, wherein a provision was made that coal would be used to produce syn gas.

Now the ministry has not only identified a block for such a purpose, but has also invited applications from interested parties on June 19, 2008, for setting up such projects. The identified block for this CTL project is Palasbani in Talcher Coalfield area of Mahanadi Coalfields Ltd. The block is situated in Angul district of Orissa and its area is about 35 sq.km. spread over 12 coal seams with estimated total indicated reserve of 1500 million tons up to a depth of 600 metres.

That India should pursue CTL projects was first mooted by an Investment Commission headed by Ratan Tata way back in March 2007. Taking note of the recommendations, the PMO formed an inter-ministerial group in the Planning Commission to examine the feasibility of converting coal to liquid fuel and gas. In its presentation, the commission had noted that CTL was a feasible proposition and should become an integral part of India’s strategy for oil security. On its part, the PMO had suggested that a time-bound action plan should be prepared in this regard for ensuring oil security.

India, the commission argued, would have to import more than 90 percent of its oil requirements in the future and as new oil finds were unlikely to reduce imports, there was a need for CTL projects to ensure oil security. It had also noted that the low-grade coal in the country would not be a constraint and the converted liquid fuel and gas would be ultra clean. The project, it said, would require captive opencast coal mines with pit-head reserves of 1.3 billion tons of coal.

The commission also pointed out that the CTL technology was a success in South Africa with a significant impact on its economy. It felt that a mechanism for Centre-State partnership would be essential for the success of such a project. Incidentally, China too is pursuing CTL projects in a big way and the world’s biggest such plant came into operation recently in that country.

It said that four to five CTL projects can double India’s domestic proven oil reserves and the proposed project will add 20 percent to it. The liquid fuel to be produced would be predominantly diesel, but will also include naphtha and LPG.

After the presentation, the commission had recommended that as a first step, it was necessary to notifiy that CTL would enable large-scale consumption of coal.

Following this, the government had made amendments in the law, then constituted an inter-ministerial group to ensure speedy allocation of blocks. This was not only to iron out any differences, but also to evolve better guidelines for the technology.

The IMG was set up under the Chairmanship of Member (Energy) Planning Commission with representatives from the department of expenditure (Ministry of Finance), department of industrial policy and promotion (Ministry of Commerce and Industry), department of science and technology, ministry of petroleum and natural gas, and ministry of coal as members.

The IMG will also undertake detailed scrutiny of applications, evaluate them and obtain feedback from stakeholders. It will make additional recommendations to the government and allocate the blocks on the basis of relative merit. It will also monitor the progress of CTL projects and suggest changes in the guidelines.

IMG has been given the right to invite experts for its assistance and the ministry of coal will provide it with secretarial assistance. A viable coal liquefaction project requires at least 20 million tons of coal per year and the proposed block identified for the project meets this criteria.

Eligibility CriteriaSince the expected investment for 3.5 million tons oil and oil products project is around $6 billion to $8 billion, the government has set certain conditions to be eligible for applying for blocks for CTL projects.

The applicant company should have minimum net worth of Rs 4000 crore. It will also have to provide details of collaborations with the proven technology providers, along with supporting documents.

Coal Block Identified For CTL Project Lokenath Tiwary

Bigwigs ready for CTL projectThe country’s top corporate houses, including the Tatas (with Sasol Group of South Africa), Mukesh Ambani-controlled Reliance Group, the Jindals along with the Adani Group and others have already evinced interest in setting up CTL projects.

With the invitation of applications for a single coal block, all these companies will now have to compete and outbid each other to secure rights for a cluster of coal blocks with estimated reserves of about 1.5 billion tons, for their proposed $8 billion CTL project in India.

With the soaring cost of crude oil, currently close to $130 a barrel, there has been a huge rush of proposals from big corporate houses for coal block for setting up CTL project.

Tata Chemicals was the first to announce a technology tie-up with South Africa’s Sasol for setting up a CTL project, which was followed by Reliance, the Jindals and Adanis submitting similar proposals along with the details of their respective technology partners.

COAL INSIGHTS 20 JUNE 2008

fEATuRE

Rio Tinto said on June 23, that it has lodged mining lease applications for its Bunder diamond project in the Bundelkhand region of Madhya Pradesh, which

is a vital step in the development of what could be the first significant world class diamond mine in India.

The company also said in a press release that it has set an exploration target for diamond mineralisation of 40 to 70 million tons at a grade of between 0.3 and 0.7 carats per ton at the Bunder project. The targeted diamond grades are at least three times greater than the grade of the Panna mine, India’s only other hard rock diamond mine.

Incidentally, the Bunder project was originally discovered as part of a regional exploration reconnaissance in 2004. A prospecting licence was executed in September 2006, which allowed exploration activities to continue, and an order of magnitude study was commenced to evaluate the economic viability of the eight diamondiferous lamproites. The results of this are expected by the end of third quarter of 2008.

“Diamonds are a significant part of the history of India and an important product for Rio Tinto. We have spent more than Rs 100 crore ($25 million) over the last six years on diamond exploration and evaluation in India, and remain excited about the prospects for the Bunder project,” managing director of Rio Tinto in India, Nik Senapati, said.

The managing director of Rio Tinto’s diamond business, Bill Champion, commented, “We are delighted with the progress of the Bunder project, which has the potential to be a world class operation.”

Currently, Rio Tinto processes the majority of its diamonds in India and independently markets the diamond productions from its Australian, Canadian and African mines, with a well established presence in all the major diamond centres of the world.

Rio Tinto’s strategic alliance with the Indian diamond industry, built over the past 25 years, has enabled it to gain a deep understanding of India as the world’s largest diamond cutting centre and as one of the key emerging markets for diamond demand.

Work on the Bunder diamond project to date includes mapping, 48 drill-holes and five surface bulk samples. Drilling is continuing and further surface bulk sampling to support diamond valuation is underway. Environmental approval for a 10 ton per hour Dense Media Separation Plant is expected soon from the Madhya Pradesh government, which allows processing of bulk samples at the project site.

Following the completion of the order of magnitude study in the second half of 2008, a pre-feasibility study would involve further social and environmental studies, including further drilling and below the surface bulk sampling.

In total, Rio Tinto has spent over Rs 75 crore ($19 million) to date on evaluation of the deposit. Plans are in place to spend around a further Rs 135 crore ($30 million) to support continued evaluation of the deposit.

The company’s release, however, said that the exploration targets are based on assessments of prospects within Rio Tinto’s Bunder project prospecting licences, which are supported by drilling, geophysics, surface bulk sampling and modelling undertaken over the last three years.

However, there may be changes during evaluation of this mineralisation, which can only be established through further work.

The potential quantity and grade is conceptual in nature, there has been insufficient exploration to define a mineral resource and it is uncertain if further exploration will result in discovery of a mineral resource.

Rio Tinto’s diamond businessRio Tinto is a leading international mining group headquartered in the UK, combining Rio Tinto Plc, a London and NYSE listed company, and Rio Tinto Ltd, which is listed on the Australian Securities Exchange.

The company has a global diamond exploration portfolio encompassing six continents and including projects in Canada, India, southern and western Africa, Brazil, Russia and Australia.

Currently, Rio Tinto produces about 16 percent of the world’s rough diamonds by volume and 8 percent by value through its 100 percent control of the Argyle mine in Australia, 60 percent of the Diavik mine in Canada and a 78 percent interest in the Murowa mine in Africa.

These three mines allow Rio Tinto to be present in all segments of the market. Rio Tinto’s share of the production from these three mines was approximately $1billion in 2007 and sold through Rio Tinto Diamonds NV in Antwerp, Belgium. About 70 percent of Rio Tinto’s diamonds are processed in India.

Rio Tinto Diamonds NV is the sales and marketing division representing the diamond mines of the Rio Tinto Group. It is a leading supporter of the Kimberley Process as well as a founding member of the Council for Responsible Jewellery Practices.

Rio Tinto Files ForDiamond Mining lease In India

Coal Insights Bureau

COAL INSIGHTS 21 JUNE 2008

fEATuRE

The North Delhi Power Limited (NDPL), a jv between Tata Power Co. Ltd and the Government of NCT of Delhi, won the Edison Award in the international category.

It is the first power utility from India to have received this award. The award was presented to NDPL, in recognition of its operational excellence in the electric industry, for innovatively utilising and integrating its Geographical Information System (GIS) with other applications for network planning, operations, commercial and asset management.

The award is given annually by the Edison Electric Institute (EEI) to honour both global and US electric companies for outstanding contributions to the power industry.

According to reports, the chairman of NDPL, Adi Engineer, said, “Distribution reforms are most critical for transformation of the power sector in India. NDPL’s trailblazing achievements over the past six years in North Delhi have finally won international recognition by way of the coveted Edison Electric Award.”

“For the first time, an Indian utility has been so acclaimed. We humbly accept it on behalf of team NDPL. We now look forward to playing a larger role in improving power distribution in other cities of India,” Engineer added.

“It’s a tremendous achievement for team NDPL to have won the prestigious international Edison award and a testimony of

commitment and dedication of our team at NDPL to provide world class services to our consumers using latest technology. GIS has been of immense help in our achieving several milestones in the power distribution operations for the benefit of all our stakeholders”, Sunil Wadhwa, CEO of NDPL said.

Innovative utilisation of GISNDPL innovatively utilised and integrated GIS with other applications for managing network planning, operations, commercial and asset management processes. NDPL’s asset base comprising over 10 lakh consumers spread over a distribution area of 510 sq km, were geospatially captured and digitised.

NDPL’s GIS was integrated with Customer Relation Management (CRM) processes which enhance stakeholder value with better connection, metering, billing and collections management. The application was also integrated with the company’s Enterprise Resource Package (ERP) for planning and execution of capital investment schemes for augmentation and extension of the distribution network.

The GIS initiatives have resulted in improvements in NDPL’s Consumer Satisfaction Index, overall system reliability, and significant reductions in aggregated technical and commercial (AT&C) losses.

Tata Power Arm Wins Global HonourCoal Insights Bureau

The Power Finance Corporation (PFC) will soon call for proposals for the 4,000-MW Tilaiya Ultra Mega Power Project (UMPP) at Jharkhand, the Power Secretary Anil

Razdan said.The project will start before the end of 2008. The ministry is

also looking into the proposal from the Government of Orissa for three new sites for setting up UMPPs, he said.

A site near Tilaiya village in Hazaribagh district of Jharkhand has been identified by the Central Electricity Authority (CEA) after consulting with the Jharkhand government.

It will be a pit head coal fired plant with the scope of future expansion. About 3,355 acres have been identified for the plant and ash dyke. State government will provide a township for the staff.

Imported coalRazdan said that if all the planned power plants go on line, then by the end of the Eleventh Plan, India will require 40 million tons (mt) of imported steam coal. Import are is around 24 mt currently. “We are in active dialogue with concerned ministries for faster handling of coal at the ports,” he added.

Land acquisitionThe process of land acquisition for UMPPs has been slow due to the opposition from the local population and huge area required for the projects.

Razdan said that in the last one year the Power Ministry, along with the CEA, has done an exercise in order to optimise the land requirement for the projects. The CEA has done a rethink on the land requirement and has come out with suggestion that would reduce land requirement by 15 to 40 percent, he said.

Razdan said that coastal UMPPs do not require a large area of land for handling coal because ash content of imported coal is less. There is a possibility of reducing land requirement, he said. “We need to keep in mind that the land requirement for UMPPs is huge and India is a densely populated country,” he added.

About the UMPP for Maharashtra that has been delayed due to change in the location of the plant, Razdan said that as soon as the ministry gets a new site duly cleared by the Maharashtra Government, the initial ground work could begin. The earlier site for the UMPP had faced opposition from the locals.

PFC to soon invite proposals for Jharkhand mega power projectCoal Insights Bureau

COAL INSIGHTS 22 JUNE 2008

fEATuRE

Leading Indian steel manufacturers have finally managed to enter into yearly contracts for supply of hard coking coal for the year 2008-09 beginning July, a top official of

a leading steel company said.While companies like Steel Authority of India Ltd and

Rashtriya Ispat Nigam Limited, have entered into contracts at a price ranging around $300 a ton, a few private companies like JSW Steel is believed to have signed the contract for the year at as high as $360 a ton range, sources said. It could not be, however, independently verified with JSW officials.

This year’s contract price is more than three times of 2007-08 price of $97 a ton. This year’s signing of annual coking coal contracts by Indian steel companies with Australian miners were delayed almost by a month. This had happened as Indian companies, which start negotiations after Japanese steel companies finalised their contracts.

Incidentally, major Australian miners had delayed the negotiation process following heavy rains in January, which had flooded a large number of mines. The miners took some time in assessing the damage caused by the flood and this had resulted in a huge spurt in spot prices for coking coal.

The spurt in spot prices had also affected long term contract

prices as miners like Xstrata, BHP Billiton etc. after assessing that there is going to be a slight shortfall in production of coking coal this year compared with demand.

Sources, however, said that delay in signing the contract was not significant as Japanese buyers, who sign contract for financial year beginning April and they had managed to seal the deals only around April 10 this year.

Compared with this, Indian companies, who enter into contracts for supply between July and June, had managed to sign the contract just towards the end of May this year, that is before the end of previous contract.

Since a large number of steel companies world over had gone for an increase in production capacity, infrastructure on mining front had not increased proportionately. While port facilities in Australia continued to be a major hazard, the situation was not much different on the Railways front in that country, industry sources said.

Meanwhile, SAIL sources said the company has tied up for almost entire quantity of expected coking coal requirement for the next year, except PCI coal. “We have signed contracts with six to seven miners spread over Australia, New Zealand and US for coking coal,” a source said.

Indian Steel Cos Close Coal Deals For FY09Coal Insights Bureau

RINL’s expansion plan which would take the hot metal production capcity to the 6.3 million ton mark by 2010, is being carried out smoothly. To

achieve this growth and ensure that there is no disruption in the supply of raw materials, the company had joined a consortium last year with SAIL, CIL, NMDC and NTPC known as the International Coal Ventures Limited (ICVL) to tap and acquire coal assets all over the world, with special emphasis on Australia and the US.

It was reported some time back that the SPV would alone invest somewhere close to Rs 5,000 crore, while a sum of close to Rs 10,000 to Rs 25,000 crore would be generated through investments. The countries which have already been identified for this purpose include Mozambique, Australia, Canada and the US. The process of setting up of a panel comprising investment bankers to take the project through is in progress.

At present, RINL imports around 4 million tons of coking coal mostly from Australia, on long term basis. According to Chairman and Managing Director, RINL,

P.K. Bishnoi, the mining companies from which RINL sources its coking coal include prominent names such as BHP Billiton, BMA, Anglo Coal and Massey Coal.

However, these companies are demanding a three-fold hike in prices for the current year. RINL wishes to add more names to the basket in the near future. Most of the coking coal required by the company is procured from Australia.

Unlike other large scale steel companies in India, RINL is not blessed with captive mines from where it can source its raw materials. This is the reason why the company has to depend heavily on external sources to feed its growing demand.

The over 200 percent hike in coking coal prices has come as a major blow. Besides this, RINL was among those big steel companies which offered to reduce its steel prices, for at least the next three months, after being requested by the steel ministry of India. In fact, Bishnoi said that the company would find it difficult to make any profits if the situation persists.

RInl Coking Coal Tie-upsNudrat Alim

COAL INSIGHTS 23 JUNE 2008

fEATuRE

It is estimated that SAIL will need around 14 million tons of coking coal to run its plants at expanded capacity and it will be importing about 90 percent of that hard coking coal from Australia and that too from BHP of Australia.

The source further said that the company is yet to start negotiation for soft coking coal and PCI coal as the same has not yet been concluded by Japanese buyers. Once the Japanese companies were through with the negotiation process for soft and PCI coal, then only Indian companies will start negotiation for those varieties.

Incidentally, Japanese companies had signed contracts with Australian buyers for supply of coking coal at various rates ranging between $280 and $300 depending on size and according to SAIL sources, the price range was almost similar for them as well.

In addition to the requirement of SAIL, RINL is likely to import around 5 million tons of coking coal this year. Considering the fact that SAIL and RINL, both public sector companies under Ministry of Steel, enter into negotiations jointly, they often manage to get a good deal compared with private steel companies.

But one disadvantage of these public sector companies is that they are required to buy at least 10 percent of their total coking coal through open global tender. In the current market scenario, because of this government condition, SAIL and RINL either do not get coal by floating global tenders, or they pay higher price, as spot price is generally more than annual contracted prices.

However, a company like Tata Steel, which had in the past acquired equity stake in a few mines in Australia, gets the coal at the cheapest rate among all companies, primarily because they had contributed to the equity of those companies.

Though many other companies, taking a cue from Tata Steel, are trying to acquire equity stake in coal mining companies of Australia, virtually none of them have so far managed to do so.

A few like JSW Steel have, however, managed some stake acquisition in mining companies, but that has taken place in countries like South Africa and Mozambique.

As Indian steel making companies increase production capacity, there is going to be an increased demand for coking coal. At present, steel companies are meeting a bulk of its coking coal requirement

through imports, but it is estimated that the country’s indigenous production is likely to increase significantly in the near future.

Of the total estimated geological reserves of 255 billion tons of coal, only around 13 billion tons is estimated to be coking coal, while the rest is steam coal. Coking coal is available in India in only one coalfield – Jharia – and a bulk of this, at present, cannot be mined due to various reasons.

Jharia, near Dhanbad in Jharkhand, is a highly inhabited place compared to other coalfields in the country, and its density of population is much higher than even some of the big cities. The coking coal reserves in the Jharia coalfields is expected to be around 3 billion tons.

Apart from the huge population, another reason why mining is not possible in Jharia is fire in a large number of blocks that happened due to unscientific mining conducted before nationalisation of coal mines in 1973.

Incidentally, nearly 640 coal blocks in Jharia is on fire and the population over the area is more than 400,000. They need to be relocated to a safe place to stop the fire and start mining, and the Jharia Action Plan was formulated a long time ago for this. The scheme, of course, could not be implemented due to various reasons.

“But now the plan is moving fast. Both the Jharkhand and West Bengal governments have taken a serious look at the plan and while the West Bengal government has approved the plan, the Jharkhand government is in the process of clearing it,” Coal India Chairman P.S. Bhattacharyya, said.

Once the Jharkhand government approves the plan, it will go to the Ministry of Coal and it is expected that the ministry will clear it by the end of this year, he said.

“Only once the plan is cleared and scientific mining takes off and mine fires are stopped, Coal India will be in a position to meet the substantial requirement of coking coal of steel industries,” Bhattacharyya said, while addressing members of Bharat Chamber of Commerce in the second week of June.

In addition, the company has identified 26 abandoned mines that would be developed in joint venture with private companies. Some of these mines have substantial amount of coking coal reserves, Bhattacharyya said.

All these measures together will ensure increased availability of coking coal to the steel industry, he added.

Incidentally, India is currently importing a total of around 50 million tons of coal, of which a majority or about 27 million tons is coking coal by steel companies, while the rest is steam coal by power companies.

Implementing Jharia Action Plan

CIL Confident Of Meeting Most Of steel Cos Demand

Coal Insights Bureau

COAL INSIGHTS 2� JUNE 2008

fEATuRE

Amid skyrocketing oil prices and increasing demand for energy, coal continues to hold its place of importance as a fuel. Though carbon dioxide emissions remain

a problem area, its importance as an energy source kept on surging. China and India have undergone rapid economic and industrial expansion with huge appetite for energy, and they are falling back on coal as oil prices soar.

Chinese coal import exceeded its export, setting off a near-doubling of prices. Japan is burning more coal since an earthquake damaged a nuclear reactor last year. In the US, coal usage increased faster than power output. While electricity use rose by 1.6 percent from 2006 to 2007, coal usage rose by 1.95 percent.

High demand for coal has driven its price even higher, to $150 per ton. China-driven coal boom has pushed up wages and created more jobs for US miners, port and rail workers. Oil consumers are forced to switch to coal, thanks to the soaring oil prices. OPEC increased its output but even that did not stabilise prices.

Economic impactThis situation has helped coal-producing states. High price and demand for coal increased the domestic demand for miners and increased wages, which in turn impacted the economy.

India and China are extensively setting up coal-fired plants. Coal is also gaining momentum in the US. Around 150 proposals for coal-fired plants were put forward in 2007.Datamonitor, the International Energy Agency, has long since projected a rise in coal usage based on energy security grounds.

There are coal reserves which can last up to 200 years and the deposits are evenly distributed in the US (27 percent), Russia (17 percent), China (13 percent) and India (10 percent).

Latest estimates suggest that coal will account for 27 percent of the global energy generation mix by 2030, up from today’s 24. It accounts for 60 percent of global energy resources. Given the abundance of resources and coal’s geographical spread a number of countries see the fuel as the only viable option to alleviate energy security concerns.

Statistical Review of World Energy 2008 The defining feature of global energy markets remains high and volatile prices, reflecting a tight balance of supply and demand. It has put issues such as energy security and alternative energies at the forefront of the political agenda worldwide, according to BP’s chief executive, Tony Hayward.

He said that the world’s fossil fuel resource base remains sufficient to support growing levels of production but the continued weakness in oil supply and increasing demand outside the OECD also highlight the challenges that industry faces in maintaining secure energy supplies.

Declining OECD oil production means that while resources are not a constraint globally, the resources within reach of

private investment by companies like BP are limited. Political factors, barriers to entry, and high taxes all play a role here.

World economic growth was strong last year, despite financial market turmoil which began in August, and this continued to support global energy consumption. And although growth in primary energy consumption slowed in 2007 to 2.4 percent it was still above the 10-year average for the fifth consecutive year.

Oil pricesOil prices are rising for over six years. BP’s data series since 1961 state it is the longest ever period of continuously rising prices. Dated Brent crude oil averaged $72.39 per barrel in 2007, an increase of 11 percent. Prices rose steadily from a low of just over $50 in mid-January to above $96 by year-end.

Global oil consumption grew by 1.1 percent in 2007, or 1 million barrels per day (bpd), slightly below the 10-year average. Consumption in the oil exporting regions of the Middle East, South and Central America, and Africa accounted for two-thirds of the world’s growth.

The Asia-Pacific region grew by 2.3 percent, even though growth in China and Japan was below average, with strong growth in a number of emerging economies. OECD consumption fell by 0.9 percent, or nearly 400,000 bpd.

Global oil production fell by 0.2 percent, or 130,000 bpd, the first decline since 2002. OPEC production dropped by 350,000 bpd due to the cumulative impact of production cuts implemented in November 2006 and February 2007. Increased output in Angola and Iraq, and growing supply of condensates/NGLs, partially offset larger cuts in other OPEC countries.

GasWorld natural gas consumption grew by 3.1 percent in 2007, although only North America, Asia-Pacific, and Africa recorded above average regional growth. The US accounted for nearly half of the world’s gas consumption growth, driven by cold winter weather and strong demand in power generation.

Coal growth fastestCoal was the fastest growing fuel in the world for the fourth consecutive year. Global consumption rose by 4.5 percent and it was spread in every region except the Middle East. Chinese coal consumption rose by 7.9 percent, the weakest since 2002. Indian consumption rose by 6.6 percent, and OECD consumption rose by 1.3 percent, both above average.

Environmental concerns Despite its advantages, it is the dirtiest carbon-based fuel accounting for 40 percent of global emissions but things may look up with global efforts to achieve clean burning of coal.

Coal As A Fuel Set To Remain Strong GloballyDhirendra Pandey

COAL INSIGHTS 2� JUNE 2008

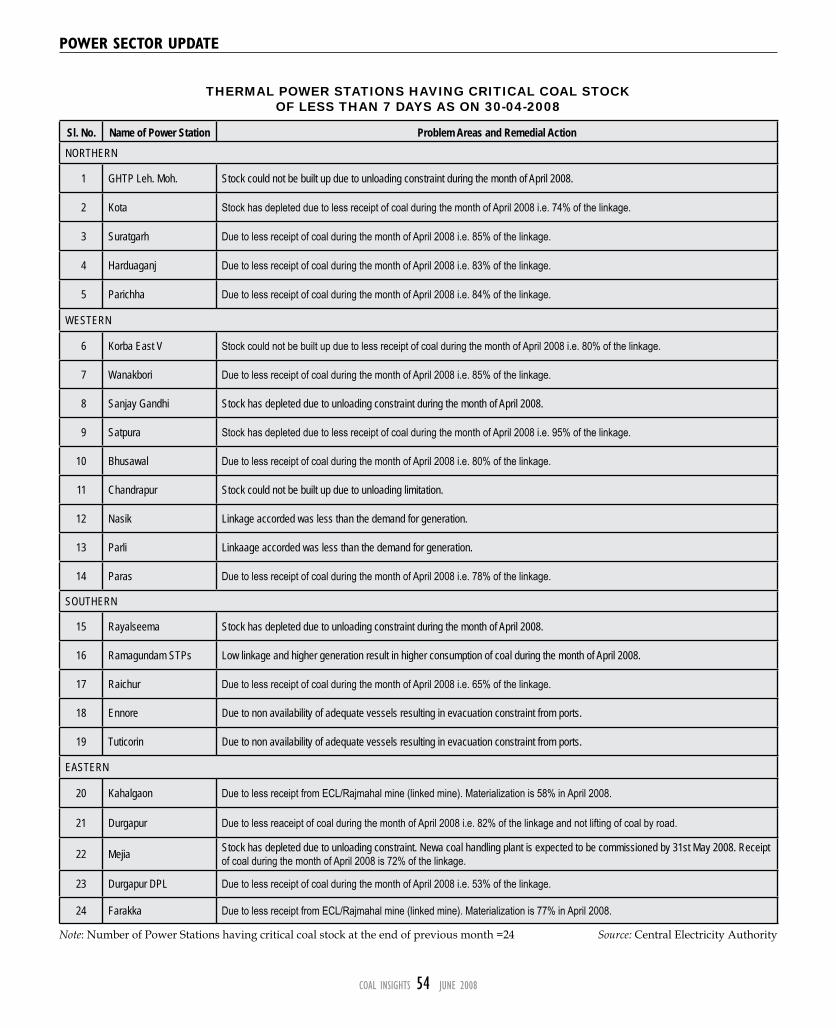

The supply of inferior grade of coal to power plants by coal companies and a cut in unloading time of rakes to seven hours from previously set 11 hours, were

the main issues raised by representatives of various power plants in an interaction with power secretary Anil Razdan recently.

The power plants lodged strong protests with the power secretary, sources who attended the meeting said.

Power utilities based in Maharashtra, Punjab, Rajasthan, Andhra Pradesh, Karnataka and Madhya Pradesh were at the forefront to bring to the power ministry’s notice that due to the bad quality coal supplied by Coal India and its subsidiaries, they are forced to consume more coal.

Besides power plants, coal consumers in the country generally feel that most of the time they do not get the correct grade of coal from the companies. “If we are promised delivery of E grade coal, we generally end up getting F grade and for F grade, we get G grade,” a member of the Indian Coal Consumers Association told Coal Insights.

The power plants also alleged that besides getting inferior grade coal which affects their generation capacity, as per New Coal Distribution Policy, which required signing of Fuel Supply Agreements, the coal companies have reduced linkages, posing a serious threat to the functioning of several plants.

“We were getting up to about 80 percent of normal requirement under linkages, but the quantity has been reduced in recent FSAs to 75 percent, and there too, the commitment is only around 60 percent of the FSAs. Now, we are effectively getting only 45 percent of our normative requirement of coal,” an official of a power company said.

A source, who attended the meeting, said that Razdan has asked the Coal Ministry and coal companies to take corrective steps as early as possible. The Railways has also been asked not to press for unloading of coal in seven hours, when power plants have the arrangement of unloading a rake within 11 hours.

The state power utilities also informed that due to heavy reduction in coal linkages by the coal companies, some of the plants were left with coal of half day or for a day.

Razdan urged all power utilities to enter into FSAs as quickly as possible as the coal market is already tight and prices are soaring.

The current price of coal in international markets is

hovering around $156 per ton. The Centre has projected coal shortfall of about 76 million tons by the end of the Eleventh Plan period and it has asked the states to take necessary steps for import of nearly 20 million tons.

Unloading constraints

Meanwhile, it has been found by the Infrastructure Constraints Review Committee (ICRC) constituted by the Government of India that some power plants like the Ropar thermal plant and Lehra Mohabatt thermal plant are unable to unload the full quantity of supplied coal rakes in one go due to infrastructural constraints.

The sub-group constituted by the ICRC to address issues connected to study the critical coal stock at some thermal plants in the country has found that the problem did not really lie with inadequate coal supply, but with the unloading constraints at the thermal plants.

At a monitoring meeting of the sub-group, the representative of the Railways informed that as per a special review conducted by them in respect of 30 power utilities to assess the impact of this special drive to supply coal, it was revealed that materialisation of linkages was only around 84 percent only.

ICRC has indicated in its report that many of those power stations were unable to unload the full quantity of supplied rakes in one go, resulting in high detention time and demurrage charges.

The detention time was found to be very high in Ropar, Lehra Mohabatt Panipat Suratgarh, Yamuna Nagar, Gandhi Nagar, Bhusawal, Durgapur, Mejia, DTPS and Mettur power plants. ICRC has observed in its report that unless unloading performance of power stations improved, stock building would be very difficult.

fEATuRE

state Power Utilities DemandRevision In Coal Unloading norms

Lokenath Tiwary

For Classified Advertisements,please contact

Soumitra Bose, +91 92310 000232or [email protected]

COAL INSIGHTS 27 JUNE 2008

fEATuRE

Despite recent reports that developed countries are slightly hesitant to provide funds for developing carbon capture and storage (CCS) technology because