coal-to-liquids - an alternative oil supply? energy agency coal industry advisory board...

TRANSCRIPT

INTERNATIONAL ENERGY AGENCY

COAL INDUSTRY ADVISORY BOARD

COAL–TO–LIQUIDS

an alternative oil supply?

WORKSHOP REPORT

IEA Coal Industry Advisory Board workshop IEA Headquarters in Paris, 2 November 2006

IEA – 9, rue de la Fédération – 75739 Paris Cedex 15

2

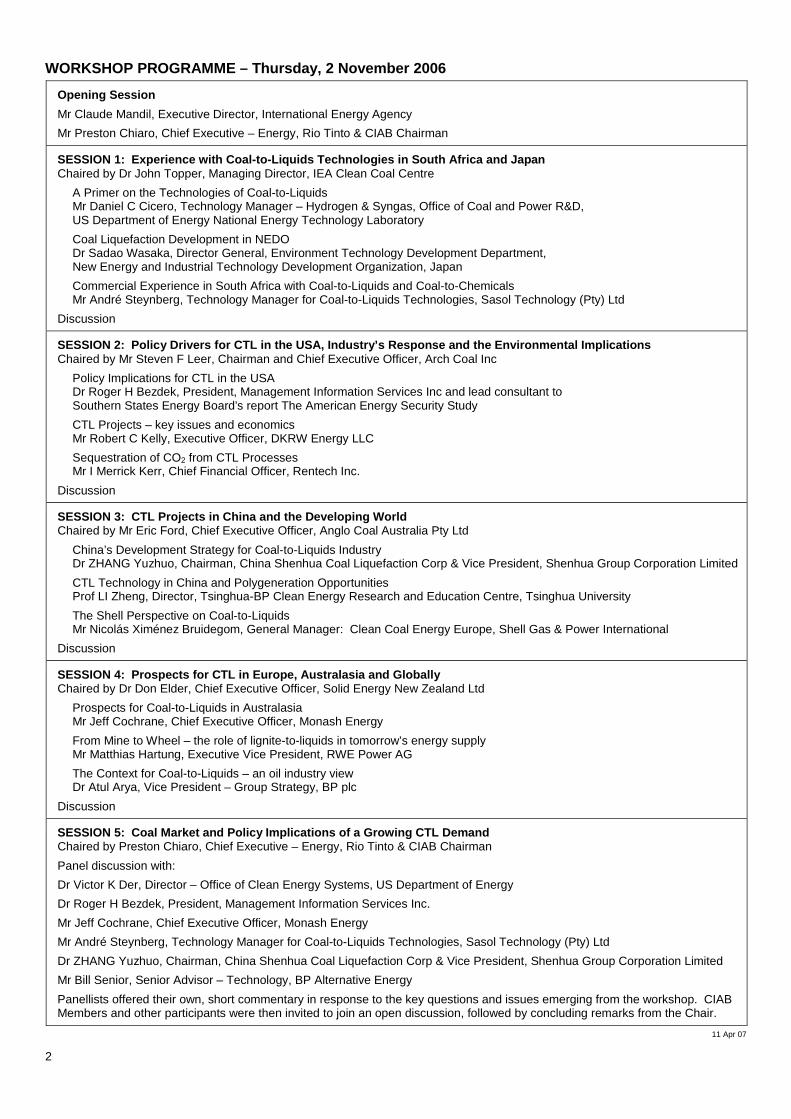

WORKSHOP PROGRAMME – Thursday, 2 November 2006

Opening Session

Mr Claude Mandil, Executive Director, International Energy Agency

Mr Preston Chiaro, Chief Executive – Energy, Rio Tinto & CIAB Chairman

SESSION 1: Experience with Coal-to-Liquids Technologies in South Africa and Japan Chaired by Dr John Topper, Managing Director, IEA Clean Coal Centre

A Primer on the Technologies of Coal-to-Liquids Mr Daniel C Cicero, Technology Manager – Hydrogen & Syngas, Office of Coal and Power R&D, US Department of Energy National Energy Technology Laboratory

Coal Liquefaction Development in NEDO Dr Sadao Wasaka, Director General, Environment Technology Development Department, New Energy and Industrial Technology Development Organization, Japan

Commercial Experience in South Africa with Coal-to-Liquids and Coal-to-Chemicals Mr André Steynberg, Technology Manager for Coal-to-Liquids Technologies, Sasol Technology (Pty) Ltd

Discussion

SESSION 2: Policy Drivers for CTL in the USA, Industry’s Response and the Environmental Implications Chaired by Mr Steven F Leer, Chairman and Chief Executive Officer, Arch Coal Inc

Policy Implications for CTL in the USA Dr Roger H Bezdek, President, Management Information Services Inc and lead consultant to Southern States Energy Board’s report The American Energy Security Study

CTL Projects – key issues and economics Mr Robert C Kelly, Executive Officer, DKRW Energy LLC

Sequestration of CO2 from CTL Processes Mr I Merrick Kerr, Chief Financial Officer, Rentech Inc.

Discussion

SESSION 3: CTL Projects in China and the Developing World Chaired by Mr Eric Ford, Chief Executive Officer, Anglo Coal Australia Pty Ltd

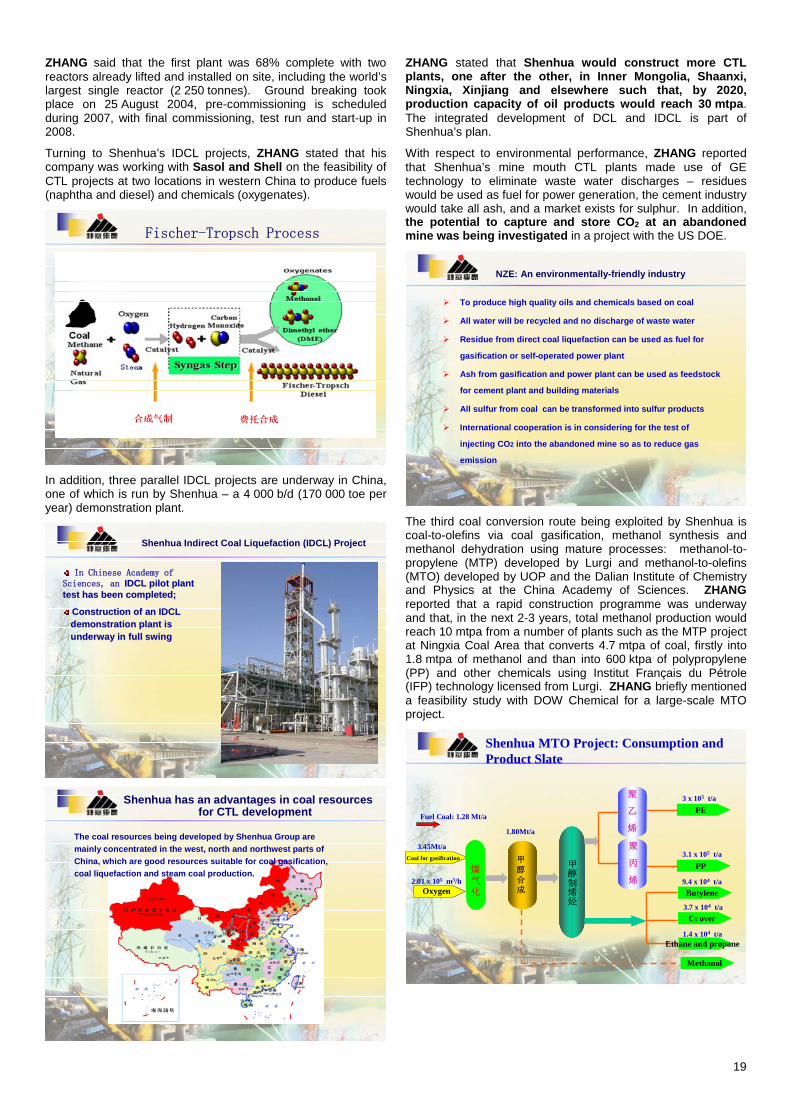

China’s Development Strategy for Coal-to-Liquids Industry Dr ZHANG Yuzhuo, Chairman, China Shenhua Coal Liquefaction Corp & Vice President, Shenhua Group Corporation Limited

CTL Technology in China and Polygeneration Opportunities Prof LI Zheng, Director, Tsinghua-BP Clean Energy Research and Education Centre, Tsinghua University

The Shell Perspective on Coal-to-Liquids Mr Nicolás Ximénez Bruidegom, General Manager: Clean Coal Energy Europe, Shell Gas & Power International

Discussion

SESSION 4: Prospects for CTL in Europe, Australasia and Globally Chaired by Dr Don Elder, Chief Executive Officer, Solid Energy New Zealand Ltd

Prospects for Coal-to-Liquids in Australasia Mr Jeff Cochrane, Chief Executive Officer, Monash Energy

From Mine to Wheel – the role of lignite-to-liquids in tomorrow’s energy supply Mr Matthias Hartung, Executive Vice President, RWE Power AG

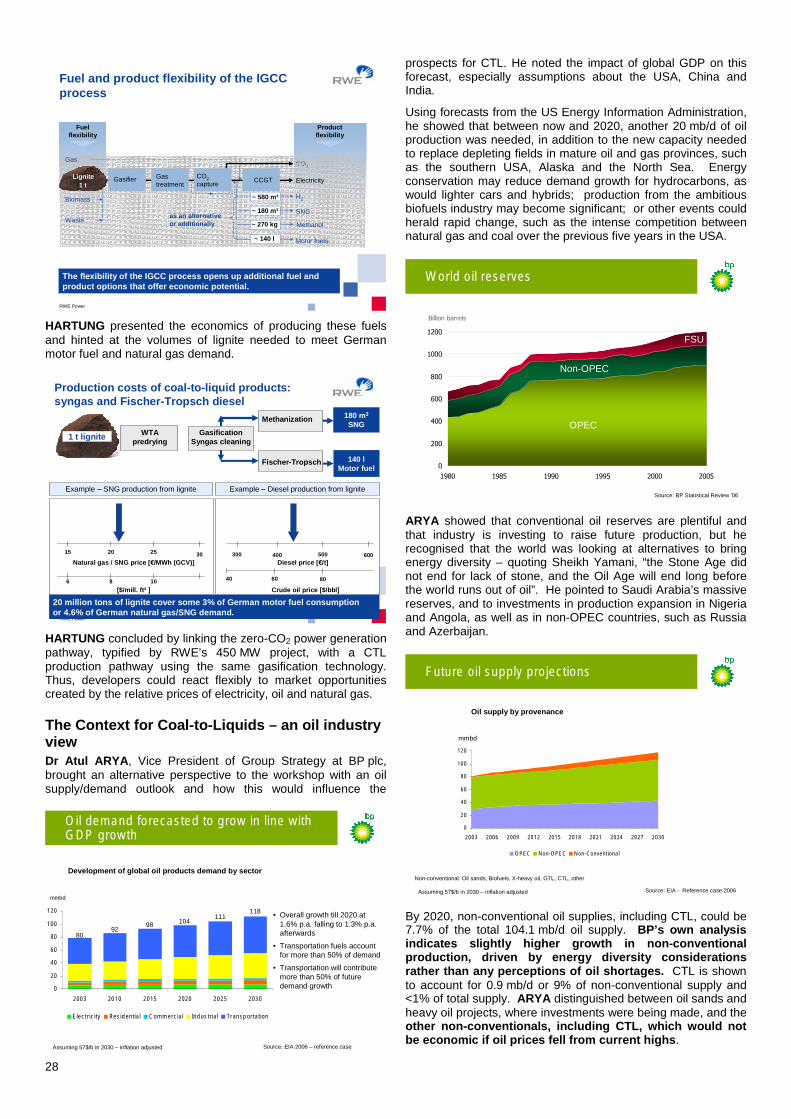

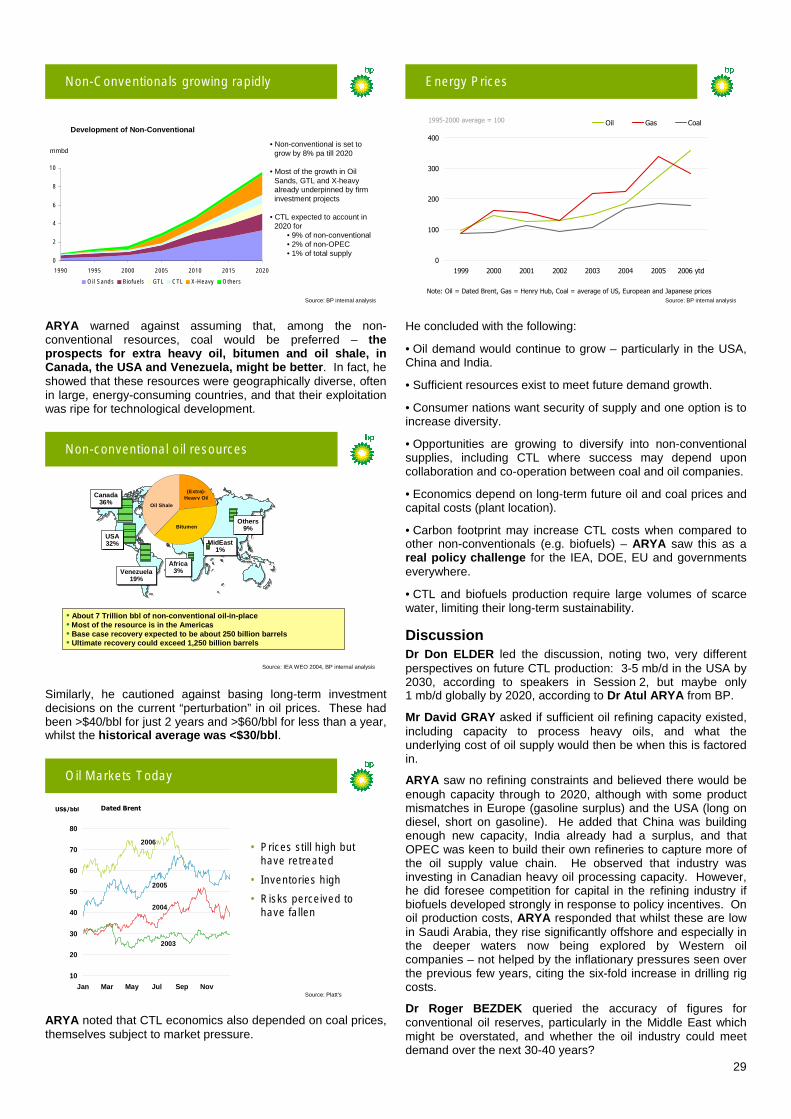

The Context for Coal-to-Liquids – an oil industry view Dr Atul Arya, Vice President – Group Strategy, BP plc

Discussion

SESSION 5: Coal Market and Policy Implications of a Growing CTL Demand Chaired by Preston Chiaro, Chief Executive – Energy, Rio Tinto & CIAB Chairman

Panel discussion with:

Dr Victor K Der, Director – Office of Clean Energy Systems, US Department of Energy

Dr Roger H Bezdek, President, Management Information Services Inc.

Mr Jeff Cochrane, Chief Executive Officer, Monash Energy

Mr André Steynberg, Technology Manager for Coal-to-Liquids Technologies, Sasol Technology (Pty) Ltd

Dr ZHANG Yuzhuo, Chairman, China Shenhua Coal Liquefaction Corp & Vice President, Shenhua Group Corporation Limited

Mr Bill Senior, Senior Advisor – Technology, BP Alternative Energy

Panellists offered their own, short commentary in response to the key questions and issues emerging from the workshop. CIAB Members and other participants were then invited to join an open discussion, followed by concluding remarks from the Chair.

11 Apr 07

3

Background Oil supply security and price concerns have led to a renewed interest in coal as an alternative feedstock for the production of transport fuels and chemicals. By using coal conversion technologies, such as coal-to-liquids (CTL), the world’s vast coal resources could become an important alternative to crude oil.

CTL describes both coal gasification, combined with Fischer-Tropsch (F-T) synthesis to produce liquid fuels, and the less developed, direct coal liquefaction technologies. Coal gasification is applied widely in the production of chemicals and fertilisers, notably in China where 8 000 coal gasifiers are operating. Fischer-Tropsch synthesis, first developed in Germany during the early decades of the 20th century, has been further developed and improved in South Africa by Sasol.

In the past, CTL has substituted for imported oil: during the 1930s and 1940s, when coal-rich Germany needed a secure source of transport fuels; and, since the 1950s in South Africa, where 40 million tonnes of coal per year are still converted into 160 000 barrels per day (b/d) of crude oil equivalent. Following the oil price shocks of the 1970s, significant coal liquefaction R&D was undertaken in the USA, Europe, Japan and Australia, although much of this development work was subsequently put on hold as oil prices stabilised from the mid-1980s and through the 1990s.

Today, with the return of high oil prices, China is constructing a 60 000 b/d CTL plant and, with plans for further projects, aims to produce one million barrels per day (mb/d) by 2020. In the USA, new incentives have been introduced for coal-based transport fuels and coal companies are now assessing the commercial viability of new projects as one component of a wider vision to make greater use of the country’s vast coal resource1.

Technical Background2 Coal may be used to produce liquid fuels suitable for transportation applications by the removal of carbon or addition of hydrogen, either directly or indirectly. The first approach is usually known as carbonisation or pyrolysis and has low yields; the second is called liquefaction. As the cost of converting coal into useful liquid fuels is higher than the cost of refining crude oil, it is the relatively low price of the raw coal feedstock that provides the main incentive to pursue the technology.

Direct liquefaction is potentially the most efficient route currently available, yielding in excess of 70% by weight of the dry, ash-free (daf) coal feed, under favourable conditions. Although many different direct processes exist, common features are the dissolution of a high proportion of the coal in a solvent at elevated temperature and pressure followed by catalysed hydrocracking of the dissolved coal with hydrogen gas. The overall energy efficiencies of the very best modern processes are generally in the range 60-70% and the technology has been demonstrated at large pilot plants. Although no commercial plants yet exist, Shenhua Group’s first CTL facility is under construction in China using direct liquefaction technology.

The less efficient, but commercially proven, indirect liquefaction process relies on the gasification of coal to produce synthesis gas (a mixture of carbon monoxide and hydrogen) which is then reacted over a catalyst at temperature and pressure to produce the desired liquid products. It is this indirect process, using well-established Fischer-Tropsch synthesis, that has been commercialised by Sasol in South Africa and will be used in several new projects proposed in China. For modern plant, overall energy efficiency is typically >40%.

Summary This workshop, “Coal-to-Liquids – an alternative oil supply?”, was held in conjunction with the annual Plenary meeting of the IEA Coal Industry Advisory Board. Coal industry leaders from IEA member countries joined their counterparts from South Africa, China, Russia and Poland to debate developments in a field that has attracted renewed attention because of recent high oil prices and concerns over the security of energy supplies. Coal-to-liquids (CTL) has a long history in South Africa and Sasol now converts 40 million tonnes of raw coal per year to produce 160 000 barrels per day (b/d) of crude oil equivalent using the commercially-proven indirect liquefaction process. In the USA, companies are moving ahead with projects that seek to reduce the country’s dependence on imported oil, encouraged by a variety of Federal and state government incentives. However, it is in China where new projects are being developed in earnest, with a major construction project underway in Inner Mongolia. This plant, using newly-developed direct liquefaction technology and scheduled for commissioning in 2008, will produce one million tonnes of oil products each year (20 000 b/d) with a planned expansion to 100 000 b/d. Dr ZHANG Yuzhuo, Chairman of China Shenhua Coal Liquefaction Corporation, explained that this project formed one component of a strategy that would limit oil imports to below 50% of China’s demand by 2020 when direct and indirect coal liquefaction plants are expected to meet 10-15% of the forecast 450 million tonnes (9 million b/d) annual oil demand. The global abundance of coal means that CTL could play an important future role, especially if greater experience leads to improved economics. However, as in other energy sectors, the scarcity of capital and skills was considered to be a major hurdle. NGOs, industrialists and policy advisors were all agreed that using coal as an alternative to oil for producing transport fuels will require carbon dioxide capture and storage (CCS), if significant increases in carbon dioxide (CO2) emissions are to be avoided. In OECD countries, the need for CCS was taken as a given by project developers. In China, it is not a priority, but participants at the workshop heard a clear willingness to apply the technology if some way could be found to cover the economic cost. The CIAB will consider this challenge over the coming year within the broader context of how clean coal technologies can be more widely deployed.

Opening Session Mr Claude MANDIL, Executive Director of the International Energy Agency, welcomed delegates from around the world. He saw CTL as an important topic, framing his comments in terms of the “3 E’s” of good energy policy: security of energy supply, economic development and environmental protection. In explaining why alternatives to oil were desirable for energy security reasons, he referred to President Bush’s 2006 State of the Union Address in which the President stated, “America is addicted to oil”. MANDIL agreed that the transport sector was too dependent upon oil, so the IEA needed to understand the potential for alternatives, including biofuels, coal-to-liquids, gas-to-liquids and biomass-to-liquids, not to replace oil, but as part of a diverse mix. However, he queried if CTL would be cost effective enough to contribute to economic growth; he looked forward to the workshop’s findings on this point and cautioned against government subsidies. MANDIL noted with concern that CTL may add to pollution and CO2 emissions, unless abatement measures were taken (e.g. CO2 capture and storage). With the coal industry enjoying stronger demand growth than previously expected, he briefly mentioned that World Energy Outlook 2006 would raise serious questions about the sustainability of this growth. To conclude, MANDIL said that bold steps were needed to achieve the “3 E’s”, because the world was not on a pathway to sustainable energy supplies.

Mr Preston CHIARO, Chief Executive – Energy at Rio Tinto and CIAB Chairman also welcomed delegates and oversaw the day’s proceedings.

4

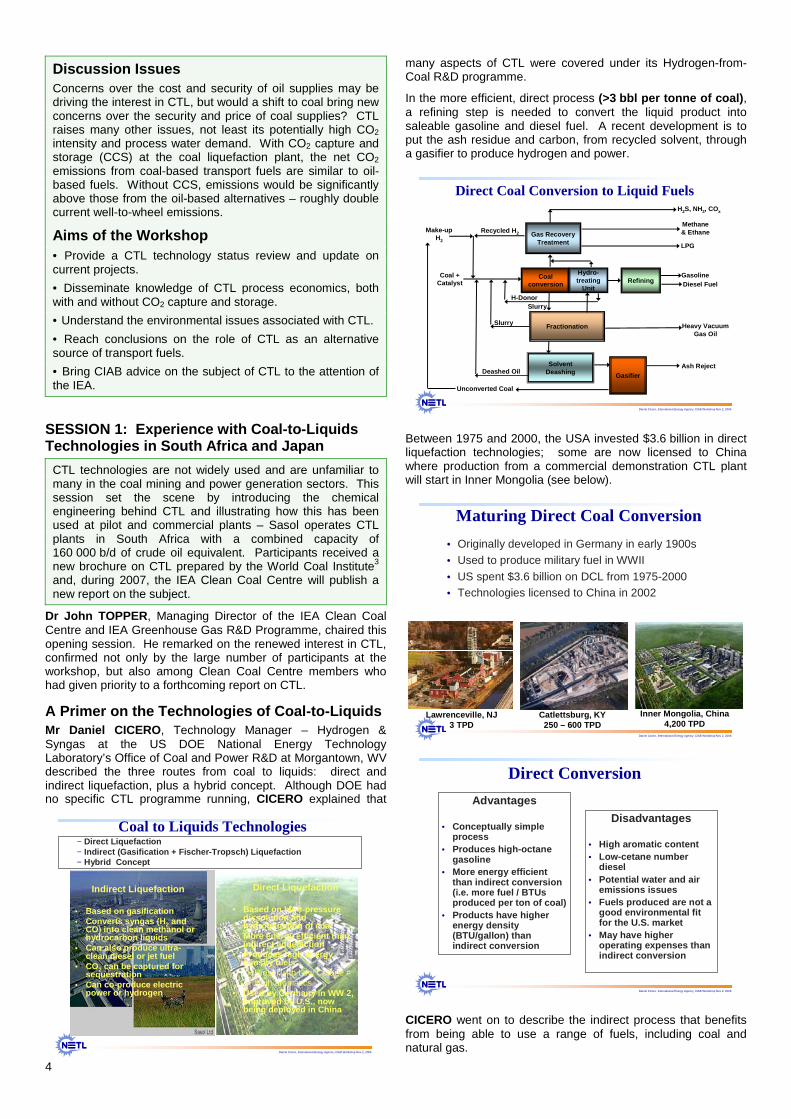

Discussion Issues Concerns over the cost and security of oil supplies may be driving the interest in CTL, but would a shift to coal bring new concerns over the security and price of coal supplies? CTL raises many other issues, not least its potentially high CO2 intensity and process water demand. With CO2 capture and storage (CCS) at the coal liquefaction plant, the net CO2 emissions from coal-based transport fuels are similar to oil-based fuels. Without CCS, emissions would be significantly above those from the oil-based alternatives – roughly double current well-to-wheel emissions.

Aims of the Workshop • Provide a CTL technology status review and update on current projects.

• Disseminate knowledge of CTL process economics, both with and without CO2 capture and storage.

• Understand the environmental issues associated with CTL.

• Reach conclusions on the role of CTL as an alternative source of transport fuels.

• Bring CIAB advice on the subject of CTL to the attention of the IEA.

SESSION 1: Experience with Coal-to-Liquids Technologies in South Africa and Japan

CTL technologies are not widely used and are unfamiliar to many in the coal mining and power generation sectors. This session set the scene by introducing the chemical engineering behind CTL and illustrating how this has been used at pilot and commercial plants – Sasol operates CTL plants in South Africa with a combined capacity of 160 000 b/d of crude oil equivalent. Participants received a new brochure on CTL prepared by the World Coal Institute3 and, during 2007, the IEA Clean Coal Centre will publish a new report on the subject.

Dr John TOPPER, Managing Director of the IEA Clean Coal Centre and IEA Greenhouse Gas R&D Programme, chaired this opening session. He remarked on the renewed interest in CTL, confirmed not only by the large number of participants at the workshop, but also among Clean Coal Centre members who had given priority to a forthcoming report on CTL.

A Primer on the Technologies of Coal-to-Liquids Mr Daniel CICERO, Technology Manager – Hydrogen & Syngas at the US DOE National Energy Technology Laboratory’s Office of Coal and Power R&D at Morgantown, WV described the three routes from coal to liquids: direct and indirect liquefaction, plus a hybrid concept. Although DOE had no specific CTL programme running, CICERO explained that

Daniel Cicero, International Energy Agency, CIAB Workshop Nov 2, 2006

Coal to Liquids Technologies

Indirect Liquefaction

• Based on gasification• Converts syngas (H2 and

CO) into clean methanol or hydrocarbon liquids

• Can also produce ultra-clean diesel or jet fuel

• CO2 can be captured for sequestration

• Can co-produce electric power or hydrogen

Direct Liquefaction

• Based on high-pressure dissolution and hydrogenation of coal

• More energy efficient than indirect liquefaction

• Produces high energy density fuels− Diesel with Low Cetane #− High aromatics

• Used by Germany in WW 2, improved by U.S., now being deployed in China

− Direct Liquefaction− Indirect (Gasification + Fischer-Tropsch) Liquefaction− Hybrid Concept

many aspects of CTL were covered under its Hydrogen-from-Coal R&D programme.

In the more efficient, direct process (>3 bbl per tonne of coal), a refining step is needed to convert the liquid product into saleable gasoline and diesel fuel. A recent development is to put the ash residue and carbon, from recycled solvent, through a gasifier to produce hydrogen and power.

Daniel Cicero, International Energy Agency, CIAB Workshop Nov 2, 2006

Direct Coal Conversion to Liquid Fuels

Gas RecoveryTreatment

Refining

Fractionation

SolventDeashing

Hydro-treating

Unit

Coalconversion

Ash Reject

Heavy VacuumGas Oil

Diesel FuelGasoline

LPG

Methane& Ethane

H2S, NH3, COx

H-DonorSlurry

Slurry

Deashed Oil

Recycled H2Make-upH2

Coal +Catalyst

Gasifier

Unconverted Coal

Between 1975 and 2000, the USA invested $3.6 billion in direct liquefaction technologies; some are now licensed to China where production from a commercial demonstration CTL plant will start in Inner Mongolia (see below).

Daniel Cicero, International Energy Agency, CIAB Workshop Nov 2, 2006

Maturing Direct Coal Conversion

• Originally developed in Germany in early 1900s• Used to produce military fuel in WWII

• US spent $3.6 billion on DCL from 1975-2000• Technologies licensed to China in 2002

Lawrenceville, NJ3 TPD

Catlettsburg, KY250 – 600 TPD

Inner Mongolia, China4,200 TPD

Daniel Cicero, International Energy Agency, CIAB Workshop Nov 2, 2006

Direct Conversion

Advantages

• Conceptually simple process

• Produces high-octane gasoline

• More energy efficient than indirect conversion (i.e. more fuel / BTUs produced per ton of coal)

• Products have higher energy density (BTU/gallon) than indirect conversion

Disadvantages

• High aromatic content• Low-cetane number

diesel• Potential water and air

emissions issues• Fuels produced are not a

good environmental fit for the U.S. market

• May have higher operating expenses than indirect conversion

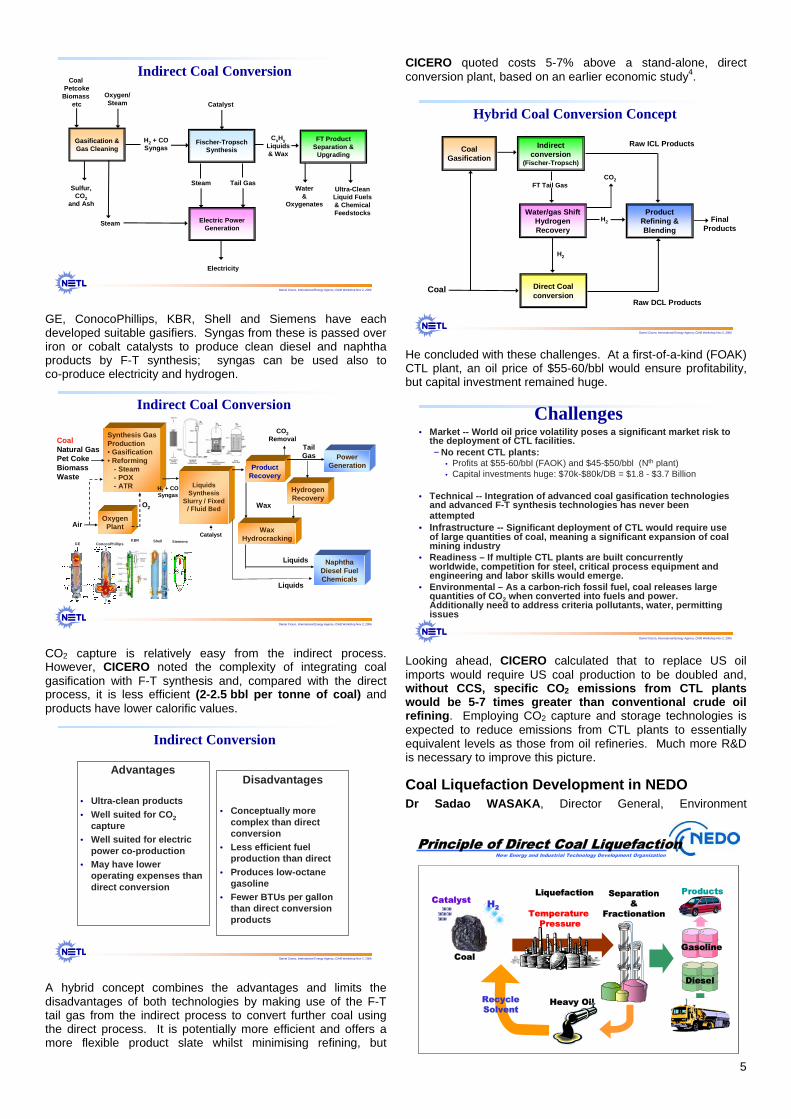

CICERO went on to describe the indirect process that benefits from being able to use a range of fuels, including coal and natural gas.

5

Daniel Cicero, International Energy Agency, CIAB Workshop Nov 2, 2006

Indirect Coal Conversion

Gasification & Gas Cleaning

Fischer-TropschSynthesis

FT ProductSeparation &

Upgrading

Electric PowerGeneration

Oxygen/Steam

CoalPetcoke

Biomassetc

Sulfur,CO2

and Ash

Steam

Electricity

Steam Tail Gas

H2 + COSyngas

CxHyLiquids& Wax

Water&

Oxygenates

Ultra-CleanLiquid Fuels& ChemicalFeedstocks

Catalyst

GE, ConocoPhillips, KBR, Shell and Siemens have each developed suitable gasifiers. Syngas from these is passed over iron or cobalt catalysts to produce clean diesel and naphtha products by F-T synthesis; syngas can be used also to co-produce electricity and hydrogen.

Daniel Cicero, International Energy Agency, CIAB Workshop Nov 2, 2006

LiquidsSynthesis

Slurry / Fixed / Fluid Bed

Indirect Coal Conversion

CoalNatural Gas Pet CokeBiomassWaste

Synthesis GasProduction• Gasification• Reforming

- Steam- POX- ATR

OxygenPlantAir

O2

ProductRecovery

NaphthaDiesel FuelChemicals

TailGas Power

Generation

HydrogenRecovery

WaxHydrocracking

Liquids

Wax

Liquids

CO2Removal

GE ConocoPhillipsKBR Shell Siemens

H2 + COSyngas

Catalyst

CO2 capture is relatively easy from the indirect process. However, CICERO noted the complexity of integrating coal gasification with F-T synthesis and, compared with the direct process, it is less efficient (2-2.5 bbl per tonne of coal) and products have lower calorific values.

Daniel Cicero, International Energy Agency, CIAB Workshop Nov 2, 2006

Indirect Conversion

Advantages

• Ultra-clean products• Well suited for CO2

capture• Well suited for electric

power co-production• May have lower

operating expenses than direct conversion

Disadvantages

• Conceptually more complex than direct conversion

• Less efficient fuel production than direct

• Produces low-octane gasoline

• Fewer BTUs per gallon than direct conversion products

A hybrid concept combines the advantages and limits the disadvantages of both technologies by making use of the F-T tail gas from the indirect process to convert further coal using the direct process. It is potentially more efficient and offers a more flexible product slate whilst minimising refining, but

CICERO quoted costs 5-7% above a stand-alone, direct conversion plant, based on an earlier economic study4.

Daniel Cicero, International Energy Agency, CIAB Workshop Nov 2, 2006

Hybrid Coal Conversion Concept

CoalGasification

Product Refining & Blending

Direct Coal conversion

Water/gas Shift Hydrogen Recovery

Indirect conversion

(Fischer-Tropsch)

H2 FinalProducts

Raw DCL Products

Raw ICL Products

Coal

FT Tail Gas

H2

CO2

He concluded with these challenges. At a first-of-a-kind (FOAK) CTL plant, an oil price of $55-60/bbl would ensure profitability, but capital investment remained huge.

Daniel Cicero, International Energy Agency, CIAB Workshop Nov 2, 2006

Challenges• Market -- World oil price volatility poses a significant market risk to

the deployment of CTL facilities.− No recent CTL plants:

• Profits at $55-60/bbl (FAOK) and $45-$50/bbl (Nth plant)• Capital investments huge: $70k-$80k/DB = $1.8 - $3.7 Billion

• Technical -- Integration of advanced coal gasification technologies and advanced F-T synthesis technologies has never been attempted

• Infrastructure -- Significant deployment of CTL would require use of large quantities of coal, meaning a significant expansion of coal mining industry

• Readiness – If multiple CTL plants are built concurrently worldwide, competition for steel, critical process equipment andengineering and labor skills would emerge.

• Environmental – As a carbon-rich fossil fuel, coal releases large quantities of CO2 when converted into fuels and power. Additionally need to address criteria pollutants, water, permitting issues

Looking ahead, CICERO calculated that to replace US oil imports would require US coal production to be doubled and, without CCS, specific CO2 emissions from CTL plants would be 5-7 times greater than conventional crude oil refining. Employing CO2 capture and storage technologies is expected to reduce emissions from CTL plants to essentially equivalent levels as those from oil refineries. Much more R&D is necessary to improve this picture.

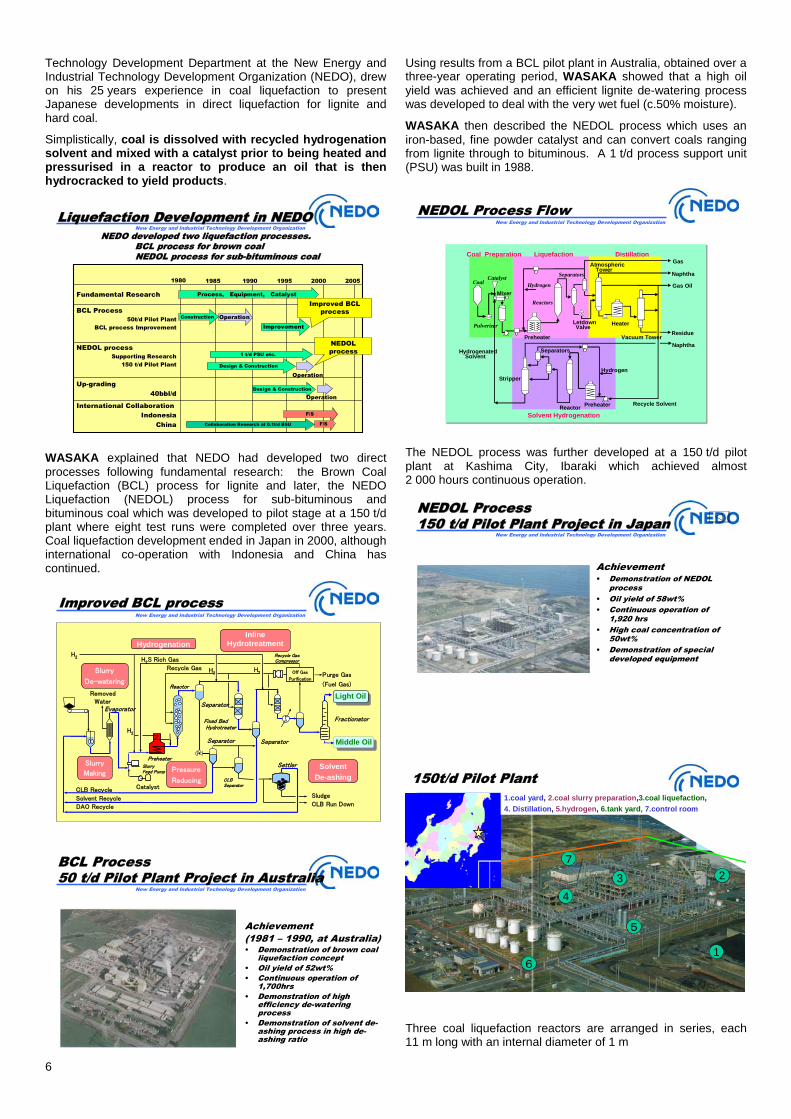

Coal Liquefaction Development in NEDO Dr Sadao WASAKA, Director General, Environment

New Energy and Industrial Technology Development Organization

Coal

RecycleSolvent

H2

Liquefaction

Heavy Oil

Separation&

Fractionation

ProductsCatalyst

Diesel

Gasoline

Temperature Pressure

Principle of Direct Coal Liquefaction

6

Technology Development Department at the New Energy and Industrial Technology Development Organization (NEDO), drew on his 25 years experience in coal liquefaction to present Japanese developments in direct liquefaction for lignite and hard coal.

Simplistically, coal is dissolved with recycled hydrogenation solvent and mixed with a catalyst prior to being heated and pressurised in a reactor to produce an oil that is then hydrocracked to yield products.

New Energy and Industrial Technology Development OrganizationLiquefaction Liquefaction Development in NEDODevelopment in NEDO

Up-grading40bbl/d

International CollaborationIndonesia

China

NEDOL processSupporting Research

150 t/d Pilot Plant

BCL Process50t/d Pilot Plant

BCL process Improvement

Fundamental Research

1980 1985 1990 1995 2000 2005

Process, Equipment, Catalyst

Construction OperationImprovement

Design & Construction

Operation

1 t/d PSU etc.

Design & Construction

Operation

F/S

F/S

Improved BCL process

NEDOL process

Collaboration Research at 0.1t/d BSU

NEDO developed two liquefaction processes.BCL process for brown coalNEDOL process for sub-bituminous coal

WASAKA explained that NEDO had developed two direct processes following fundamental research: the Brown Coal Liquefaction (BCL) process for lignite and later, the NEDO Liquefaction (NEDOL) process for sub-bituminous and bituminous coal which was developed to pilot stage at a 150 t/d plant where eight test runs were completed over three years. Coal liquefaction development ended in Japan in 2000, although international co-operation with Indonesia and China has continued.

New Energy and Industrial Technology Development Organization

Solvent Recycle

Recycle Gas

SeparatorLight OilLight Oil

Recycle GasCompressor

Fixed BedHydrotreater

HydrogenationInline

Hydrotreatment

Solvent De-ashing

Middle OilMiddle Oil

SludgeCLB Recycle

Removed Water

Evaporator

Reactor

Fractionator

Slurry

De-watering

Settler

H2

CLB Separator

CLB Run Down

Catalyst

Preheater

Pressure

Reducing

SeparatorSeparator

DAO Recycle

Slurry

Making

H2S Rich Gas

Off Gas

Purification

Slurry Feed Pump

Purge Gas

(Fuel Gas)

H2

H2

H2

Improved BCL process

New Energy and Industrial Technology Development Organization

BCL Process50 t/d Pilot Plant Project in Australia

Achievement(1981 – 1990, at Australia)• Demonstration of brown coal

liquefaction concept• Oil yield of 52wt%• Continuous operation of

1,700hrs• Demonstration of high

efficiency de-watering process

• Demonstration of solvent de-ashing process in high de-ashing ratio

Using results from a BCL pilot plant in Australia, obtained over a three-year operating period, WASAKA showed that a high oil yield was achieved and an efficient lignite de-watering process was developed to deal with the very wet fuel (c.50% moisture).

WASAKA then described the NEDOL process which uses an iron-based, fine powder catalyst and can convert coals ranging from lignite through to bituminous. A 1 t/d process support unit (PSU) was built in 1988.

New Energy and Industrial Technology Development Organization

NEDOL Process Flow

Coal

Pulverizer

Catalyst

Mixer

Preheater

Reactors

Separators

LetdownValve

AtmosphericTower

Heater

Vacuum Tower

Hydrogen

Hydrogen

Reactor

Separators

Preheater

Stripper

HydrogenatedSolvent

Recycle Solvent

Gas

Naphtha

Gas Oil

Naphtha

Residue

Coal Preparation Liquefaction Distillation

Solvent Hydrogenation

The NEDOL process was further developed at a 150 t/d pilot plant at Kashima City, Ibaraki which achieved almost 2 000 hours continuous operation.

New Energy and Industrial Technology Development Organization

NEDOL ProcessNEDOL Process150 t/d Pilot Plant Project in Japan150 t/d Pilot Plant Project in Japan

Achievement• Demonstration of NEDOL

process• Oil yield of 58wt%• Continuous operation of

1,920 hrs• High coal concentration of

50wt%• Demonstration of special

developed equipment

New Energy and Industrial Technology Development Organization

2

1

3

4

5

6

7

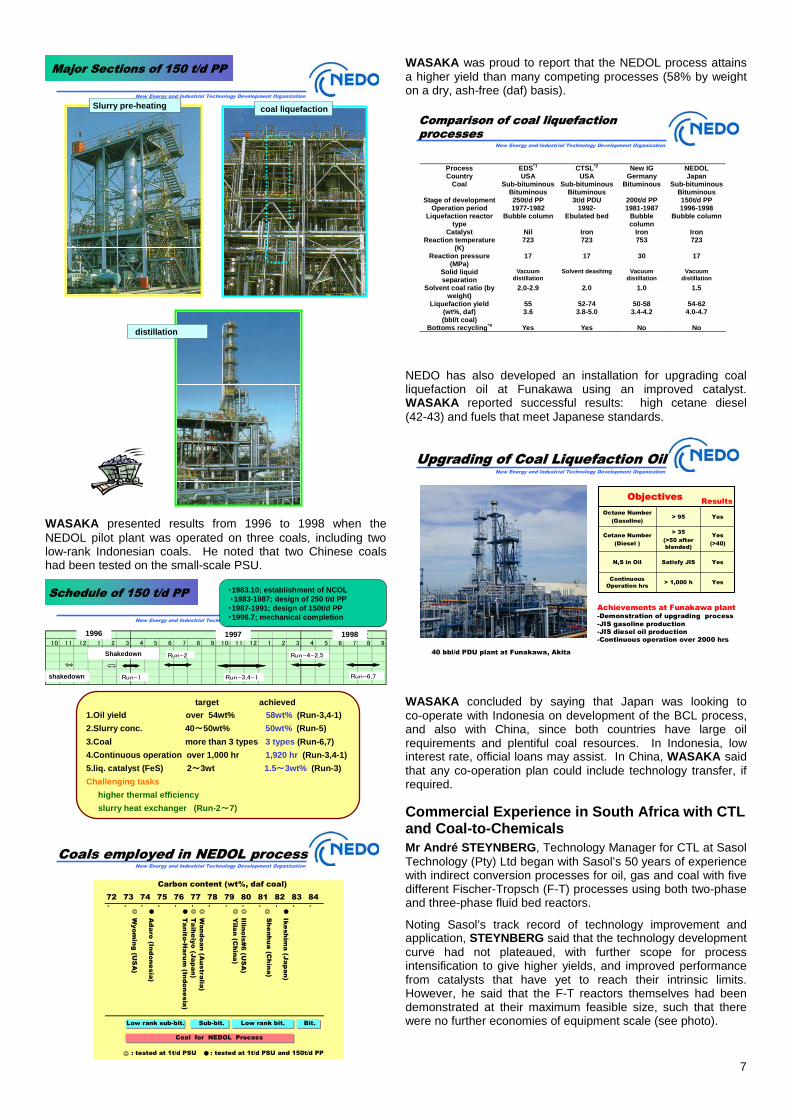

1.coal yard, 2.coal slurry preparation,3.coal liquefaction,4. Distillation, 5.hydrogen, 6.tank yard, 7.control room

150t/d Pilot Plant

Three coal liquefaction reactors are arranged in series, each 11 m long with an internal diameter of 1 m

7

New Energy and Industrial Technology Development Organization

Slurry pre-heating coal liquefaction

Major Sections of 150 t/d PPMajor Sections of 150 t/d PP

distillation

WASAKA presented results from 1996 to 1998 when the NEDOL pilot plant was operated on three coals, including two low-rank Indonesian coals. He noted that two Chinese coals had been tested on the small-scale PSU.

New Energy and Industrial Technology Development Organization

Schedule of 150 t/d PPSchedule of 150 t/d PP ・1983.10; establishment of NCOL・1983-1987; design of 250 t/d PP・1987-1991; design of 150t/d PP ・1996.7; mechanical completion

平成8年度 平成9年度 平成10年度10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9

試運転ーⅡ

試運転ーⅠ Run-1

Run-2

Run-3,4-1 Run-6,7

Run-4-2,5

target achieved

1.Oil yield over 54wt% 58wt% (Run-3,4-1)

2.Slurry conc. 40~50wt% 50wt% (Run-5)

3.Coal more than 3 types 3 types (Run-6,7)

4.Continuous operation over 1,000 hr 1,920 hr (Run-3,4-1)

5.liq. catalyst (FeS) 2~3wt 1.5~3wt% (Run-3)

Challenging tasks

higher thermal efficiency

slurry heat exchanger (Run-2~7)

Shakedown

shakedown

19981996 1997

New Energy and Industrial Technology Development OrganizationCoals employed in NEDOL processCoals employed in NEDOL process

Carbon content (wt%, daf coal)72 73 74 75 76 77 78 79 80 81 82 83 84

- - - - - - - - - - - - -

◎ ● ● ◎ ◎ ◎ ◎ ●Wyom

ing (US

A)

Adaro (Indonesia)

Tanito-H

arum (Indonesia)

Taiheiyo

(Japan)W

andoan(A

ustralia)

Yilan

(China)

Illinois#6 (US

A)

Shenhua (C

hina)

Ikeshima

(Japan)

◎ : tested at 1t/d PSU : tested at 1t/d PSU and 150t/d PP

Coal for NEDOL Process

Low rank sub-bit. Sub-bit. Low rank bit. Bit.

◎

●

WASAKA was proud to report that the NEDOL process attains a higher yield than many competing processes (58% by weight on a dry, ash-free (daf) basis).

New Energy and Industrial Technology Development Organization

Comparison of coal liquefaction processes

Process EDS*1 CTSL*2 New IG NEDOL Country USA USA Germany Japan

Coal Sub-bituminous Bituminous

Sub-bituminous Bituminous

Bituminous Sub-bituminous Bituminous

Stage of development 250t/d PP 3t/d PDU 200t/d PP 150t/d PP Operation period 1977-1982 1992- 1981-1987 1996-1998

Liquefaction reactor type

Bubble column Ebulated bed Bubble column

Bubble column

Catalyst Nil Iron Iron Iron Reaction temperature

(K) 723 723 753 723

Reaction pressure (MPa)

17 17 30 17

Solid liquid separation

Vacuum distillation

Solvent deashing Vacuum distillation

Vacuum distillation

Solvent coal ratio (by weight)

2.0-2.9 2.0 1.0 1.5

Liquefaction yield (wt%, daf) (bbl/t coal)

55 3.6

52-74 3.8-5.0

50-58 3.4-4.2

54-62 4.0-4.7

Bottoms recycling*4 Yes Yes No No

NEDO has also developed an installation for upgrading coal liquefaction oil at Funakawa using an improved catalyst. WASAKA reported successful results: high cetane diesel (42-43) and fuels that meet Japanese standards.

New Energy and Industrial Technology Development Organization

Upgrading of Coal Liquefaction Oil

> 1,000 h

Satisfy JIS

> 35(>50 after blended)

> 95 YesOctane Number

(Gasoline)

YesContinuous Operation hrs

YesN,S in Oil

Yes(>40)

Cetane Number(Diesel )

Objectives

40 bbl/d PDU plant at Funakawa, Akita

Results

Achievements at Funakawa plant-Demonstration of upgrading process-JIS gasoline production-JIS diesel oil production -Continuous operation over 2000 hrs

WASAKA concluded by saying that Japan was looking to co-operate with Indonesia on development of the BCL process, and also with China, since both countries have large oil requirements and plentiful coal resources. In Indonesia, low interest rate, official loans may assist. In China, WASAKA said that any co-operation plan could include technology transfer, if required.

Commercial Experience in South Africa with CTL and Coal-to-Chemicals Mr André STEYNBERG, Technology Manager for CTL at Sasol Technology (Pty) Ltd began with Sasol’s 50 years of experience with indirect conversion processes for oil, gas and coal with five different Fischer-Tropsch (F-T) processes using both two-phase and three-phase fluid bed reactors.

Noting Sasol’s track record of technology improvement and application, STEYNBERG said that the technology development curve had not plateaued, with further scope for process intensification to give higher yields, and improved performance from catalysts that have yet to reach their intrinsic limits. However, he said that the F-T reactors themselves had been demonstrated at their maximum feasible size, such that there were no further economies of equipment scale (see photo).

8

Sasol Advanced Synthol (SAS)

Transport of 10.7 m SAS reactor sections

STEYNBERG outlined Sasol’s history through two periods: as a state-owned corporation and, since 1979, as a private-sector company. OPEC’s oil price hikes were an important influence during the first period and led to two large CTL plants being built with some urgency. The second period was characterised by ongoing technology improvement and diversification into higher value products for a global market.

When assessing potential CTL projects, STEYNBERG identified some key prerequisites sought by Sasol:

• Large coal deposits, sufficient to supply plants with a minimum size of 80 000 b/d.

• Stranded coal, due to its low-quality or location, making it unsuitable for alternative applications, such as electricity generation.

• Government support for the very large capital investments, on the grounds of improved energy security through decreased dependence on imported energy, and to shield developers from oil price volatility.

Key drivers for a viable CTL business

Access to:large reserves of low cost gasifiable coal (a minimum of

approximately 2 – 4 billion tons) at proposed location.

Minimum plant capacity: ≈ 80 000 barrels per day to realize economy of scale benefits.

“Stranded coal” (e.g. due to quality or location) which can

not be easily monetised in other ways.

Drive for energy security supported by current global energy dynamics

Ability and will to provide enabling support

0

10

20

30

40

50

60

70

80

1955 1960 1965 1970 1975 1980 1985 1990 1995 2000

Cru

de O

il P

rice

($/B

arr

el)

US$ of the day (Nominal) 2003 US$ (Real)

Conditions today similar to when Sasol was established….

Crude oil prices once again at 1973 levels

Sasol II was justified at current oil price levelsSasol II was justified at current oil price levels

He noted that current conditions, in respect of oil prices, favoured CTL development and were similar to those in the mid-1970s when Sasol made its decision to invest in the Sasol Two plant at Secunda.

Beginning with Sasolburg, where the reactor is still making waxes, STEYNBERG outlined Sasol’s F-T reactor development. The world’s first commercial CTL plant, initially producing about 8 000 b/d, was the Sasol One plant opened in 1955 at Sasolburg using both German and American technologies. The Sasol Two and Sasol Three plants were commissioned in 1980 and 1983 respectively and, in 1989, Sasol unveiled its Sasol Advanced Synthol (SAS) reactor at commercial scale. In general, synthesis feed gas (syngas) from a coal gasifier is passed over (in fixed bed tubular Arge reactors), or circulated with (in circulating fluidised bed (CFB) Synthol reactors), or percolated through (in Sasol Slurry Phase Distillate (SPD) reactors and Sasol Advanced Synthol (SAS) reactors) iron- or cobalt-based catalysts at between 220°C and 350°C to produce F-T liquids.

Sasol’s Fischer-Tropsch Reactor Development

2000

6500

100

3500

7500

11000

20000

500 700 100 2500

17000

0

5000

10000

15000

20000

1955 1980 1982 1983 1987 1989 1990 1991 1993 1995 1998 Oryx,2006

Year of first operation

Synthol Advanced Synthol

High Temperature

Arge Slurry

Low Temperature

Capacity per reactor (bbl/day)

Sasol produces almost 40% of South Africa’s liquid transport fuels, but STEYNBERG explained that Sasol’s business went far beyond CTL – from coal mining to chemicals (ammonia, nitrogenous fertilisers and commercial explosives, waxes, phenolics such as phenol and cresols, solvents such as alcohols and ketones, polyethylene, polypropylene, alpha olefins such as 1-hexene and 1-octene, coke, tar, sulphur and noble gases).

Variety of Industrial Processes

Coal processingSyngas production akin to MeOH and ammonia plants Hydrocarbon synthesis - gas, liquid and solid mixtures- recycles and solids separation- large volumes flammable materials at high pressure that auto-ignite

Refinery operationsChemical processing Integrated utility systems Power generationCatalyst manufacture has elements of mineral processing combined with the precision found in the pharmaceutical industry

The low temperature Sasol Slurry Phase Distillate (SPD) process, using cobalt catalyst, is now part of a three-step process to produce primarily diesel fuel and naphtha from natural gas. A full-scale, commercial slurry phase reactor was commissioned at Sasolburg by Sasol in 1993 using iron catalyst for the production of waxes and paraffins, and the proprietary technology has then been further developed for GTL plants with an advanced cobalt catalyst. During 2006, a 34 000 b/d GTL plant was commissioned in Qatar in partnership with Qatar

9

Petroleum, with another in Nigeria operating from 2010, in partnership with Chevron. The Sasol Chevron company, with its headquarters in London, was formed to further develop the global GTL business.

In 2004, the gasifiers at Sasolburg were shut down when pipeline natural gas from Mozambique replaced coal as the feedstock; natural gas also now supplements the coal feed at Secunda.

Sasol Infrachem (SCI) - Sasolburg

Rectisol

Synthesisgas

ArgeReactors

SlurryBed

Reactor

MethanolReactor

CO2

H2 to NH3Production

Dew PointCorrection

Shift

Benfield PSA

Tailgas

Towngas

ProductSeparation

ProductSeparation

ProductSeparation

Coal

Air

Gasification

AirSeparation

Oxygen

Raw gas

Sasol Synthetic Fuels, based at Secunda, operates the world’s only CTL plant, with 80 Lurgi gasifiers at the now integrated Sasol Two and Sasol Three plants.

The high temperature Sasol Advanced Synthol (SAS) reactor was developed during the 1980s as a more efficient and cost-effective successor to the CFB Synthol reactor. It operates at about 350°C with an iron-based catalyst to produce, in a single step, synthetic crude oil for downstream refining into fuels and chemicals. Nine SAS reactors (from Korea and Japan) are now operating at Secunda, having replaced the original 16 Synthol reactors in 1999, and now produce the equivalent of about 160 000 b/d of product fuels and chemicals.

Secunda

CO2 Benfield

Synthol

Fresh Feed

MethaneReforming

CryogenicSeparation

CH4 Rich

PSAH2

Propylene

Separation

C3/C4

Rectisol CO2

Raw Gas

Pure Gas

1-octene1-hexene

Pt Reformer Gasoline

CondensationDistillation

OxygenateWork-up

AlcoholKetoneAcetic Acid

Reaction Water

Diesel

Catpoly

Ethylene

Cracker

C2=/C2

Gasoline

Isomerization

C5/C6

H2 Rich

Hydrotreat Diesel

ActivatedSludge

Cooling Water

GasificationWater

The 3 different Sasol Fischer-Tropsch technologies

Cobalt low temperature Fischer -Tropsch (Co-LTFT)Iron low temperature Fischer-Tropsch (Fe-LTFT)Iron high temperature Fischer-Tropsch (Fe-HTFT)

The 3 technologies produce fundamentally different types of hydrocarbons and thus ultimately have the potential to produce different chemical products

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Co-LTFT Fe-LTFT Fe-HTFT

Olefins alkanes oxygenates aromatics

Sasol uses three, fundamentally different F-T technologies: low temperature cobalt catalyst, low temperature iron catalyst and high temperature iron catalyst.

Sasol’s Fe-HTFT technology with additional chemicalsGas

Coal

26% Propylene

33 % Diesel

Fuels Chemicals

Coal

3 % LPG

SASOLFe -HTFT

33 % Naphtha

Syngas production

Product upgrading

5 % other olefins and oxygenates

Fe-HTFT

Further processing of the streams

Ethylene

Butene and butylenes

Hexene

Octene

Nonene

Detergent alcohols

Ethanol

N and iso-propanol

N and iso-butanol

Acetone

MEK

Complex due to many different products with differed market drivers. Therefore a phased approach has proven to be successful

STEYNBERG alluded to the complexity of the CTL and F-T processes, but also pointed to opportunities for CO2 capture: at the syngas purification stage, where sulphur and CO2 are stripped using a physical organic solvent in the Rectisol process; CO2 is also removed from F-T products using the hot potassium carbonate Benfield process. CO2 is currently vented at Secunda, but STEYNBERG said that whilst CCS is not yet practiced by SASOL, the company had all the competencies needed to undertake such projects.

CO2 application and storage opportunities

Geological storage in saline aquifers and depleted oil/gas reservoirsEnhanced oil recovery Enhanced Coal Bed Methane (CBM) extractionCompetencies needed:Gas treatment and compression :

Synfuels, Sastech, SPI CPF in MozambiqueHigh pressure transmission lines :

Sastech, Sasol Gas (Rompco) Gas reservoirs, gas wells:

SPI Coal geology :

Sasol Mining Oil field development :

SPI and external

This is the type of project that Sasol can do

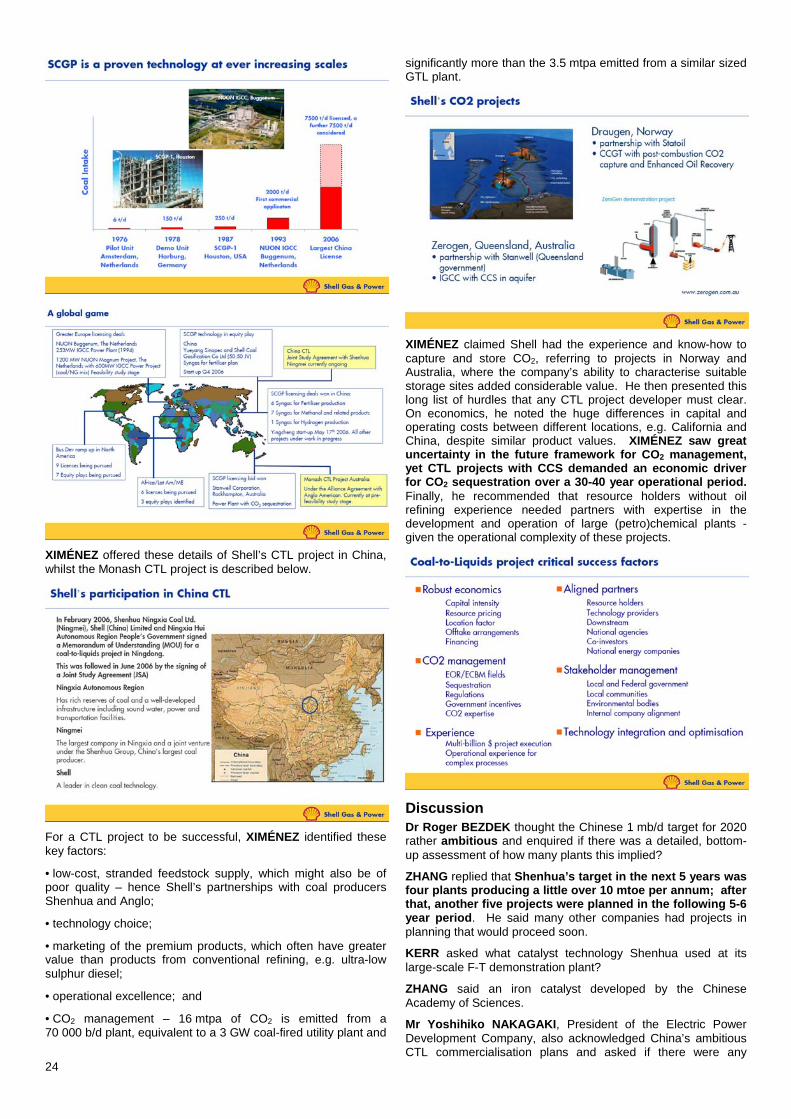

Finally, Sasol is engaged on a feasibility study for two CTL plants in China: one with Shenhua Corporation, focusing on a site in Shaanxi Province about 650 km west of Beijing; and the other with Shenhua Ningxia Coal Company, focusing on a site about 1 000 km west of Beijing.

Discussion Opening the discussion, Dr John TOPPER remarked on the continuous technical development of these complex processes that had taken place over many years, particularly in South Africa, and helped at times by timely oil price rises.

Dr Dan LASHOF, Science Director at the Natural Resource Defense Council’s Climate Center, sought clarification on the energy efficiency of direct processes (often quoted to be 58-72%) and whether the figures included for the additional refining needed beyond the liquefaction step itself, thus allowing comparison with indirect F-T processes.

WASAKA responded that the NEDO process was 60-63% efficient with higher levels possible, but not above 70%.

10

CHIARO wanted to know more about resource use, he fully understood the coal demand CTL could create, but what of the quantity and quality of water?

STEYNBERG agreed that CTL plants needed to be sited near available coal and water resources. Water provides essential hydrogen and process cooling. Whilst the latter can be minimised by making best use of air cooling, STEYNBERG replied that water consumption was typically between one and two cubic metres per tonne of coal on a dry, ash-free basis.

Mr David GRAY, former Director of the British Coal Petrol and Diesel from Coal Project, asked what the yield was from the competing processes per tonne of coal, after accounting for process energy demand, energy which itself must come from coal (i.e. how much of the coal ends up in products that can displace oil products)? He was also interested to hear how much transport fuel Sasol could produce if this were the sole focus of the company?

WASAKA indicated that around 50% of the coal (dry, ash-free basis) was converted into product after upgrading, depending on the coal, process and conditions.

STEYNBERG quoted motor fuel yields from Sasol’s indirect process of about two barrels of oil products per tonne of coal on a dry, ash-free basis6 – plants under study in China would produce about 70% diesel and 30% naphtha. He added that for gasoline production, a high temperature F-T process with iron catalyst was the best technology.

SESSION 2: Policy Drivers for CTL in the USA, Industry’s Response and the Environmental Implications

Today’s high oil prices make coal a competitive source for transport fuels, but commercial risks remain high and only those projects that are economically viable and environmentally sound are likely to proceed. Incentives, available under the recent Transportation Act, could accelerate the conversion of the vast US coal resource into transport fuels (a 50c/gal tax credit is available under the Safe, Accountable, Flexible, and Efficient Transportation Equity Act of 2005 – equivalent to c.$20/bbl – and possible loan guarantees under the Energy Policy Act of 2005). The US Department of Energy is supporting a commercial-scale project to convert waste coal into F-T diesel and power. In addition, the US Department of Defense’s concept of a single fuel for the battlefield opens up opportunities for alternative fuels; a coal-based fuel would reduce the inherent risks and vulnerabilities associated with oil-based supplies.

Mr Steven LEER, Chairman and Chief Executive Officer at Arch Coal Inc, chaired this session, noting a shift in emphasis from the technical to the economic in three presentations on CTL developments in the USA.

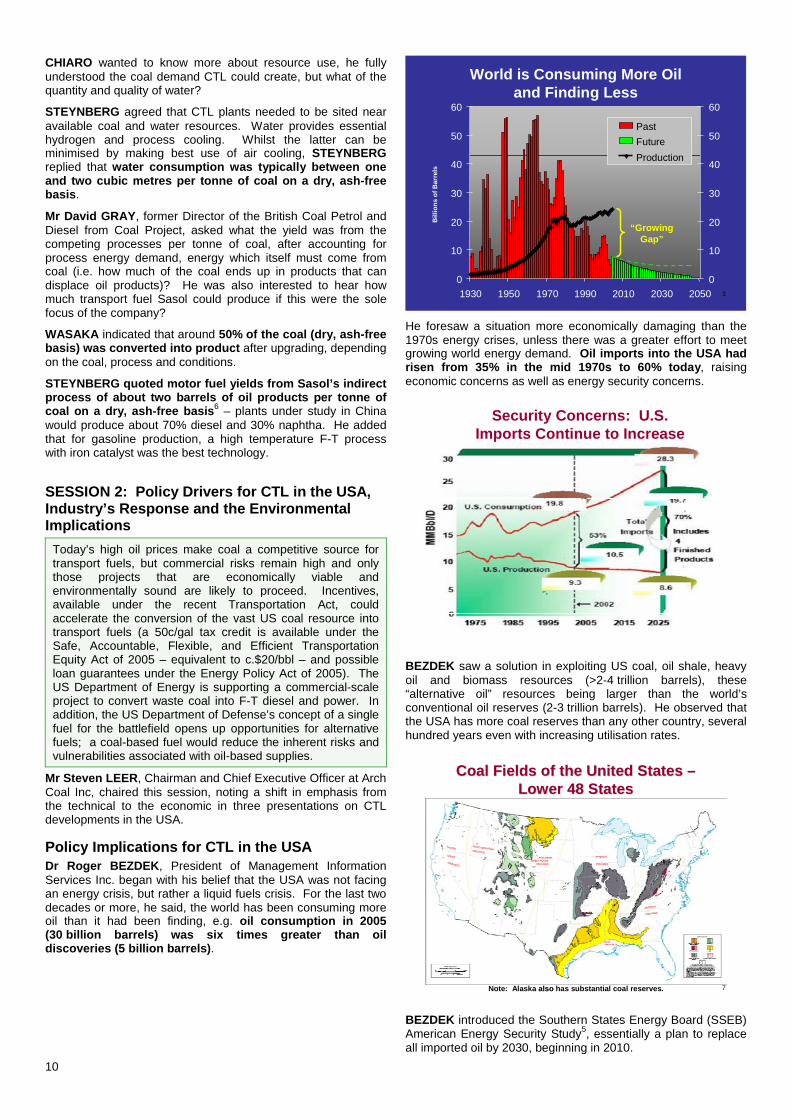

Policy Implications for CTL in the USA Dr Roger BEZDEK, President of Management Information Services Inc. began with his belief that the USA was not facing an energy crisis, but rather a liquid fuels crisis. For the last two decades or more, he said, the world has been consuming more oil than it had been finding, e.g. oil consumption in 2005 (30 billion barrels) was six times greater than oil discoveries (5 billion barrels).

3

World is Consuming More Oiland Finding Less

Past discovery by ExxonMobil

0

10

20

30

40

50

60

1930 1950 1970 1990 2010 2030 2050

Bill

ion

s o

f B

arre

ls

0

10

20

30

40

50

60

Past

Future

Production

“GrowingGap”

He foresaw a situation more economically damaging than the 1970s energy crises, unless there was a greater effort to meet growing world energy demand. Oil imports into the USA had risen from 35% in the mid 1970s to 60% today, raising economic concerns as well as energy security concerns.

Security Concerns: U.S. Imports Continue to Increase

BEZDEK saw a solution in exploiting US coal, oil shale, heavy oil and biomass resources (>2-4 trillion barrels), these “alternative oil” resources being larger than the world’s conventional oil reserves (2-3 trillion barrels). He observed that the USA has more coal reserves than any other country, several hundred years even with increasing utilisation rates.

7

____________________________________________________________________________________________________

Coal Fields of the United States Coal Fields of the United States ––Lower 48 StatesLower 48 States

Note: Alaska alsoalso has substantial coal reserves.

BEZDEK introduced the Southern States Energy Board (SSEB) American Energy Security Study5, essentially a plan to replace all imported oil by 2030, beginning in 2010.

11

REDUCTION IN U.S. OIL IMPORTS

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

U.S

. Oil

Imp

ort

s

The study:

• developed a plan for the US to establish energy security and independence through the production of alternative oil and liquid fuels;

• emphasised enhanced oil recovery using CO2 and increased transport efficiency; and,

• developed policy and legislative recommendations.

To eliminate imports would require all options: coal-to-liquids (29% in 2030), biomass (24%), efficiency measures in the transport sector (16%), oil shale (16%), and enhanced oil recovery (15%). If oil imports were held steady, at the 2005 level of 13 mb/d, BEZDEK said demand growth to 25 mb/d and declining US production would open a supply gap of 5 mb/d by 2025 – five to six times more oil than Australia currently consumes. He called for early and massive action because of the 8-10 year lead time before these options would have a major impact. To establish a programme, SSEB was working with Congress and the Administration.

10

THE PATH TO U.S. ENERGY SECURITYAND INDEPENDENCE

i

Conventional Oil Production

CTL

Biomass

Oil Shale

EOR

Import Gap

Trans.Efficiency

0

5

10

15

20

25

30

2007

2009

2011

2013

2015

2017

2019

2021

2023

2025

2027

2029

MM

bp

d

In the case of CTL, the SSEB study anticipated dozens of 20-60 000 b/d plants such that, by 2030, 5.6 mb/d would be produced. BEZDEK reported that other studies also estimated a huge potential for CTL in the USA:

• US DOE National Energy Technology Laboratory study (July 2006) – 5.1 mb/d by 2027.

• US National Coal Council Study (March 2006) – 2.6 mb/d by 2025.

• US DOE Unconventional Fuels Task Force (November 2006) – 2.5 mb/d by 2035.

BEZDEK listed the following benefits from adoption of the SSEB initiative: reduce risk and lower oil prices; foster new technology; create millions of jobs; and, revitalise the manufacturing sector. He spoke of the enhanced economic

growth that would help eliminate trade and budget deficits, quantifying the annual benefits as (2005 dollars):

• $185 billion in new investments

• $332 billion in increased industry sales

• 1.4 million new jobs

• $14 billion in profits

• $94 billion in increased federal, state and local tax revenues

• $625 billion reduction in US trade deficit

BEZDEK referred to the many policy-related actions already underway and a number of incentives aimed at CTL.

16

WHAT IS THE USA DOING?

• President Bush: U.S. is “addicted to oil” & must reduce oil imports

• Studies and plans being developed by Federal agencies: Dept. of Energy, Dept. of Defense, Unconventional Fuels Task Force, DOE labs

• Studies and plans being developed by state governments, SSEB, Western Governors Association

• Many states have passed CTL legislation & are building CTL plants

• U.S. Congress: Study mandated for GAO, Congressional Caucus formed, CTL incentives legislation passed

• Independent initiatives: National Academy of Sciences, National Coal Council, National Petroleum Council

18

U.S. FEDERAL GOVERNMENTCTL INCENTIVES

• EPACT 1992: Court orders for AFVs• EPAct 2005: Financial incentives, loans & loan

guarantees, earmarks, $1.4B in ITCs, Incentives for Innovative Technologies program

• SAFETEA-LU 2005 provides a $0.50/gal. excise tax credit for CTL products

• Legislation: Many Bills in U.S. Congress: Expensing of CTL equipment, loan guarantees, excise & investment tax credits, Trust Fund for CTL development, matching grants, require use of CTL fuel in SPR, R&D incentives, purchase agreements, production tax credits, mandate use of CTL fuels in Federal fleet, accelerated depreciation, cost-shared demonstrations

KEY ROLE OF CONGRESSIONAL LEGISLATIVE INCENTIVES

• As noted, U.S. Federal law SAFETEA-LU 2005 currently provides a $0.50/gal. excise tax credit for CTL products.

• However, this incentive is set to expire in 2009, before any major new CTL plants can come online.

• Its extension through 2020 will provide critically needed market incentives for the development of CTL plants.

• This extension is critical, because the tax credit will reduce CTL OPEX by $20/bbl.

• Legislation to extend this tax credit has been introduced in the U.S. Congress.

He called for an extension of the CTL tax credit from 2009 to 2020.

12

U.S. DEPT. OF ENERGY INITIATIVES

• Secretary Bodman has emphasized the need for CTL• DOE mandated National Coal Council and National

Petroleum Council to conduct independent studies• DOE conducting a series of studies to estimate feasibility

& impacts of rapid CTL development• Unconventional Fuels Task Force: Developing

commercialization plan, schedule, budget, and incentives for accelerated CTL development

• DOE labs conducting CTL R&D: NETL, Los Alamos, Oak Ridge, etc.

• Increased budgets for CTL programs

BEZDEK noted that the US Department of Defense itself consumes 400 000 b/d – more than most countries.

U.S. DEPT. OF DEFENSE INITIATIVES

• Office of the Secretary of Defense Clean Fuel Initiative: catalyze industry to produce CTL fuels for the military

• Battlefield Use Fuel of the Future Program-- 3 stages (evaluation, demo, implementation)-- leading to CTL F-T fuel procurement by 2010

• Total Energy Development Program-- Utilize domestic coal to produce CTL fuels-- Couple program with advanced technologies-- Focus on qualification & certification

• Naval Research Advisory Committee: Financing CTL plants viable if DOD makes long-term commitment

He saw state governments moving ahead faster than Federal government, with highly-skilled, well-paid, technical and professional jobs being the key driver in many states, especially coal-producing states.

22

STATE GOVERNMENT CTL INCENTIVES

• Many states promoting CTL development: Arizona, Colorado, Kentucky, Illinois, Mississippi, Montana, North Dakota, Ohio, Pennsylvania, South Dakota, Virginia, West Virginia, Wyoming

• State CTL incentives include: Consortia to purchase CTL fuels, tax credits, financing assistance, grants, job training, alternative fuels incentives, alternative energy portfolio standards, strategic partnerships, public vehicle fuel mandates, site assistance, accelerated permitting, public energy authorities, tax increment financing, property tax relief, alternative energy revolving loans

• Cities: Require fleets to use alternate fuels – Denver, Chicago, Oakland, Portland, San Francisco, etc.

23

STATE GOVERNMENT CTL PROJECTS

• Illinois: Rentech to convert fertilizer plant to CTL for gas and clean fuel

• Mississippi: Agreement with Rentech for $700M 10K bpd plant

• North Dakota: MOU with Headwaters and others for 10K – 50K bpd plant (5-7 yrs.) Pennsylvania: WMPI building $612M 5K bpd plant by 2008 (Sasol, Shell, and Nextant)

• South Dakota: Designing a 28K bpd plant; site planning to begin in late 2006

• Virginia: Planning a 10K bpd modular plant

In conclusion, BEZDEK referred back to the feasibility studies that indicate the USA could produce 3-5 mb/d of CTL liquids by 2030 and again noted the activity, at all levels of government, with that objective.

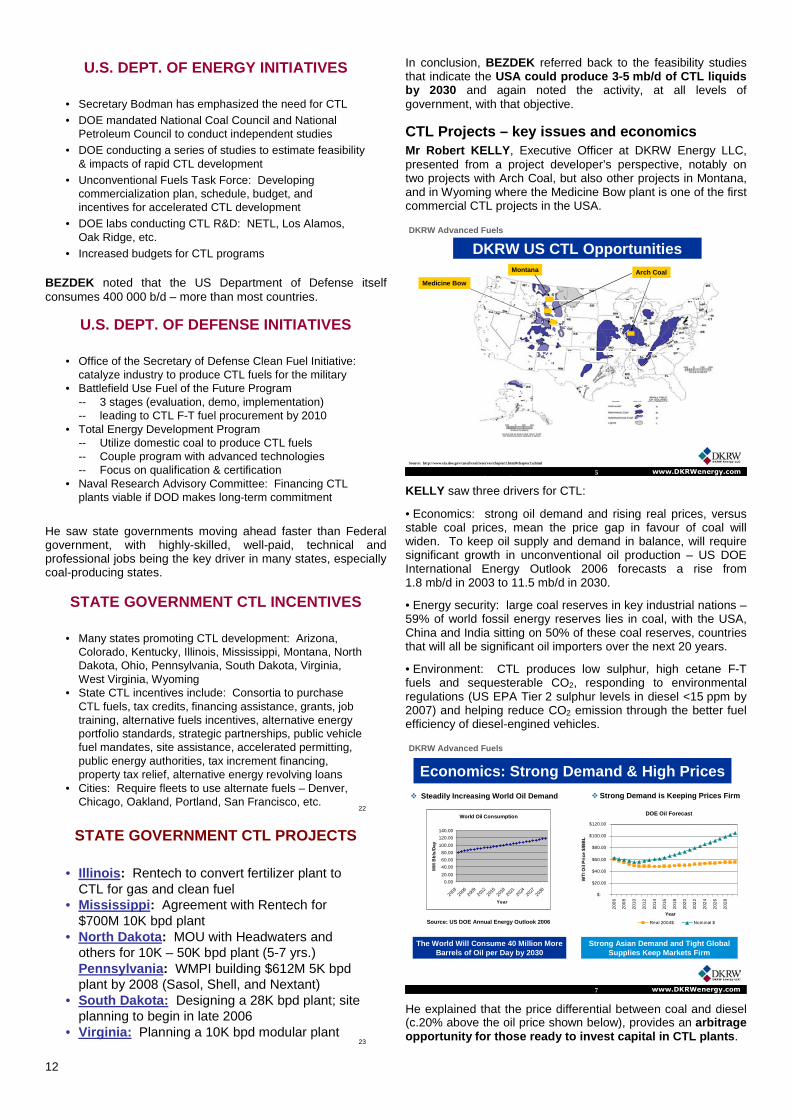

CTL Projects – key issues and economics Mr Robert KELLY, Executive Officer at DKRW Energy LLC, presented from a project developer’s perspective, notably on two projects with Arch Coal, but also other projects in Montana, and in Wyoming where the Medicine Bow plant is one of the first commercial CTL projects in the USA.

Confidential & Proprietary www.DKRWenergy.comwww.DKRWenergy.com5

Source: http://www.eia.doe.gov/cneaf/coal/reserves/chapter1.html#chapter1a.html

DKRW US CTL OpportunitiesDKRW Advanced Fuels

Medicine Bow

Arch CoalMontana

KELLY saw three drivers for CTL:

• Economics: strong oil demand and rising real prices, versus stable coal prices, mean the price gap in favour of coal will widen. To keep oil supply and demand in balance, will require significant growth in unconventional oil production – US DOE International Energy Outlook 2006 forecasts a rise from 1.8 mb/d in 2003 to 11.5 mb/d in 2030.

• Energy security: large coal reserves in key industrial nations – 59% of world fossil energy reserves lies in coal, with the USA, China and India sitting on 50% of these coal reserves, countries that will all be significant oil importers over the next 20 years.

• Environment: CTL produces low sulphur, high cetane F-T fuels and sequesterable CO2, responding to environmental regulations (US EPA Tier 2 sulphur levels in diesel <15 ppm by 2007) and helping reduce CO2 emission through the better fuel efficiency of diesel-engined vehicles.

Confidential & Proprietary www.DKRWenergy.comwww.DKRWenergy.com7

Economics: Strong Demand & High Prices

The World Will Consume 40 Million More Barrels of Oil per Day by 2030

Strong Asian Demand and Tight Global Supplies Keep Markets Firm

Strong Demand is Keeping Prices Firm

Source: US DOE Annual Energy Outlook 2006

Steadily Increasing World Oil Demand

DKRW Advanced Fuels

$-

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

200

6

200

8

201

0

201

2

201

4

201

6

201

8

202

0

202

2

202

4

202

6

202

8

Real 2004$ Nominal $

DOE Oil Forecast

Year

WT

I Oil

Pri

ce $

/BB

L

World Oil Consumption

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

2003

2006

2009

2012

2015

2018

2021

2024

2027

2030

Year

MM

Bb

ls/D

ay

He explained that the price differential between coal and diesel (c.20% above the oil price shown below), provides an arbitrage opportunity for those ready to invest capital in CTL plants.

13

Confidential & Proprietary www.DKRWenergy.comwww.DKRWenergy.com8

Economics: Low Coal Feedstock Costs

Coal is Projected to Have a Significantly Lower Cost Than Oil Over the Next 25-30 Years—Btu Arbitrage

DKRW Advanced Fuels

Source: US DOE Annual Energy Outlook 2006

DOE Fuel Price Forecasts 2003-2030

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

$18.00

$20.00

200

3

200

7

201

1

201

5

201

9

202

3

202

7

$/m

mbt

u

Oil

Coal

KELLY moved on to examine the key strategic issues when developing CTL projects:

• Scale – how big, or how small?

• Product mix – liquid fuels, power, chemicals, CO2.

• Contracts – cost and security of coal feedstock, and liquid fuel off-take agreements.

• Environmental – including CO2.

• Construction and permanent financing – EPC partner.

Confidential & Proprietary www.DKRWenergy.comwww.DKRWenergy.com14

Advantages of Scale in CTL Plants

Capex vs Capacity in CTL Plants

0.0

20.0

40.0

60.0

80.0

100.0

120.0

10000 20000 40000 80000

BPD of Capacity

Ind

ex 1

0000

BP

D =

100

DKRW Advanced Fuels

Opex vs Capacity in CTL Plants

0.0

20.0

40.0

60.0

80.0

100.0

120.0

10000 20000 40000 80000

BPD of Capacity

Ind

ex 1

000

0 B

PD

=10

0

There are capital and operating costbenefits of large scale plants

Source: Headwaters ACC Presentation

(year-2006 dollars)

Despite these clear scale economies, KELLY argued that smaller CTL projects had attractions, particularly when it came to seeking capital – large projects carry greater upfront costs (e.g. front-end engineering and design (FEED) costs and permitting costs prior to the final investment decision (FID)) and greater financial risks. Moreover, project financing is more widely available below $1 billion (i.e. 10-15 000 b/d) at a lower weighted average cost of capital (WACC) than for, say, a $5-7 billion, 80 000 b/d CTL plant. Finally, large projects need large coal reserves (e.g. 2-4 billion tonnes) such as found in the Powder River Basin and China, but few other places. Coal consumption is then typically beyond what a single mine can supply to a mine mouth CTL plant, thus increasing exposure to rail cost risks.

Confidential & Proprietary www.DKRWenergy.comwww.DKRWenergy.com15

Disadvantages of Scale in CTL Plants

DKRW Advanced Fuels

There are more opportunities, a lower cost of capital, and less development risk in smaller CTL projects

Coal Reserve Opportunities Limited

• Larger reserve position required--- 2x-8x

• Fewer mine-mouth opportunities—rail costs

Project Financing is More Difficult

• Limits to project financing --- $1B

• Higher WACC as scale increases

Development costs are larger

• Larger development costs incurred 2x-4X

• Significant financial risks before FID complete

KELLY reflected that big projects may suit a small number of big companies with access to sufficient equity, but DKRW’s business model aimed at fighting economies of scale with well-structured, smaller projects.

Confidential & Proprietary www.DKRWenergy.comwww.DKRWenergy.com16

Scale & Development Cost Risk

DKRW Advanced Fuels

Large scale plants incur significantly higher development costs prior to the FID

Scale and Development Costs

0

50

100

150

10000 20000 40000 80000

Capacity (bpd)

$MM

Source: Scully Capital Analysis for DOD 2006 2.5% Capex

KELLY presented details of the Medicine Bow CTL project which will use a low-temperature iron catalyst to produce ultra-low sulphur diesel and naphtha, with 275 MW of electric power generated from waste heat and tail gas, of which 60 MW would be exported – a true polygeneration plant. DKRW’s own intellectual property, in terms of gasifier / F-T process integration, brought unique added value to the project.

Confidential & Proprietary www.DKRWenergy.comwww.DKRWenergy.com17

Medicine Bow Fuel & Power

Coal

Entered into Option with Arch Coal to purchase coal reserves in Carbon Basin ReserveUnderground Continuous Coal Mine Owned

Mine built and operated by ArchPermits for Surface & Continuous Mining completedConstruction expected to commence QIV 2007

ConversionFacility

Coal-to-Liquids PlantCoal Mine at plant

Gasification (GE)

Fischer Tropsch (Rentech)

Hydrocracking (UOP)

Permit applications to be submitted in 2006Expected Construction start = end of 2007

Expected I.S.D. = end of 2010

Liquids & Other Products

Capacity = 10,000-15,000 barrels / day

Diesel (ultra low sulfur)

NaphthaLong-term Purchase Contract

Shipped via pipelineExport Power 60MW

CO2 (to EOR)SulfurChemicals

Secure Coal Resources Package Technology & EPC Sell Products

DKRW Advanced Fuels

CO2 can be captured, liquefied and used for EOR in Wyoming where it would remain sequestered after the tertiary recovery of crude oil at rates only slightly below the CTL plant’s

14

own output. The mine mouth design ensures a competitive coal feedstock and DKRW has acquired an option on 180 Mt of permitted bituminous coal reserves in the Carbon Basin that would support the initial plant (in-service date (ISD) end of 2010), and future expansions.

Confidential & Proprietary www.DKRWenergy.comwww.DKRWenergy.com18

Medicine Bow Project ParticipantsArch Coal: Carbon Basin Reserve Option

General Electric: Gasification License

Rentech: Fischer Tropsch License

Refiner/Marketer: Liquids Off-Take Agreement

Exploration Company: CO2 Off-Take Agreement

EPC Contractor: SNC-Lavalin

Financial Advisor: Citibank

Key Project Participants in Medicine Bow

DKRW Advanced Fuels

Financing the project, including the coal mine, will require $1.5-2.0 billion. A debt to equity ratio of 65:35 is proposed, the debt comprising loans backed by Federal loan guarantees, advances from the EPC turnkey contractor, and insurance company borrowings. Equity will come from a public offering and strategic partners – KELLY saw value in being the first CTL developer to seek capital from the market.

By engineering a smaller plant with a good initial return, KELLY explained that the potential then existed for greater economies of scale to be achieved during two later expansions of the project up to 30 000 b/d. He anticipated capital cost reductions of up to 25%, as experience was gained with CTL plants, and higher income from more diverse and valuable chemical products over time.

KELLY concluded by outlining the features of a successful CTL project: well structured debt/equity, key technologies and coal reserves secured early, on competitive terms, and positive public policy incentives. However, he stressed that if CTL was to succeed, then projects had to be commercially viable without state support. KELLY was optimistic of future growth prospects in a huge global market.

Sequestration of CO2 from CTL Processes Mr Merrick KERR, Chief Financial Officer at Rentech Inc., presented his company’s long history of F-T catalyst technology development, culminating in the first, fully-integrated CTL pilot plant of 10 b/d at Commerce City, Colorado.

2

Synhytech Plant, Pueblo, CO

(1992-1993)

Boulder, CO Catalyst Plant

(1990-1991)

Pueblo / Denver, CO (1993-Present)

Sterling, CO Plant

(1982-1987)

Zuni, CO Plant (1988-1989)

Commerce City, CO (2007)

La Porte, TX

(1998-2003)

Then largest FT slurry reactors in the world Verified Rentech Process at full scale

Developed Rentech’s proprietary and patented iron catalyst

Used syngas gas as feedstock to produce FT diesel for engine testing

Produced over 22,000 pounds of Rentech’s catalyst

Proved the technology using different operating conditions, and feedstocks, including coalStill serving as Rentech’s R&D facilities

Exclusive CTL license / non-exclusive GTL licenseTested Rentech FT catalyst technology in DOE joint industry effort

First fully integrated domestic CTL facility will be located at Rentech’s new R&D center

25 years of Technology Development

2

This product development unit (PDU) will be used to train operators, validate Rentech process designs and supply fuels for testing, including to the US DoD.

3

Architect’s Rendering of the PDU

►First Fully Integrated CTL Production Unit in the US

Advances Rentech capabilities 10 bpd of finished product

►Facility DeliverablesActual products in volume available for end user testing and evaluation

Ability to refine FT reactor performance parametersFeedstock analysis and validation of CO2 variables based on syngas quality and process design

Training of facility operators

3

On-line: 2007Commerce City, Colorado

Product Development Unit

Rentech’s strategic plan is to develop a repeatable and scaleable CTL process up to 50 000 b/d, building on its patented iron catalyst for F-T synthetic diesel production, and thus jump-start CTL production in the USA. To that end, KERR reported that Rentech had acquired an ammonia fertiliser plant for conversion from natural gas to coal. An oversized gasifier will feed excess syngas to a 1 500-1 800 b/d CTL plant and 55% of the CO2 removed prior to F-T synthesis can be used for urea production. Interestingly, the fertiliser plant economics support 50% debt, whilst the CTL plant is entirely funded with equity.

66

U.S. Coal Supply Regions

► Coal is the primary US domestic energy resource:

265 billion tons of proven, developed coal reserves

►At Rentech, we:

Develop energy solutions

Work to protect the environment

Are carbon-capture ready

Evaluate every project for maximum carbon capture potential

Utilizing Rentech’s technology to convert just 5% of U.S. coal reserves would double the known domestic oil reserves.

Strategies for Energy and the Environment

5

►High Performance

►Usable in Today’s Engines, Pipelines

►Ultra-low in Sulfur

►Significant Environmental Advantages

5

(1) HC = Hydrocarbon, CO = Carbon Monoxide, C02 = Carbon Dioxide, N0x = Nitrogen Oxide, PM = Particulate Matter. Data from U.S. Military testing.

FT Fuel Emissions Reductions (1) Relative to EPA Low Sulfur Diesel

(55%)

(13%)(4%)

(45%)

(62%)

(52%)

(15%)(17%)

(60%)

(72%)

HC CO CO2 NOx PM

Cruise Idle

Rentech’s Premium Synthetic Diesel

15

KERR turned to CO2 capture where he saw three alternatives in descending order of attractiveness:

• Revenue-generating options: food-grade CO2, capture into other products (e.g. urea), EOR, and enhanced coal bed methane recovery (ECBM).

• Sequestration alternatives: salt domes, saline reservoirs, and geological strata.

• Theoretical possibilities: algae gasification, fast-growth forests, and deep-sea entrapment.

Using results from work with the State of Wyoming, KERR said that ECBM needs a $5/tCO2 credit to be profitable at current natural gas prices.

8

►Inject CO2 into coal seams to enhance gas production

Coal has up to 10 times the affinity to absorb CO2 over methane

Methane is chased out and produced

►Evaluation:

Not profitable given current conditions even at $6/Mscf gas and zero cost CO2 (due to time and volume of CO2 required before gas begins to flow)

Potential to be profitable with a carbon credit of $5/ton

Fischer-Tropsch Coal-

to-Liquids Plant

Gas Productto 3rd Party

Compressionand Dehydration

CO 2 To

Injection Well

Product fromProduction Well

2000-psi 1500-psi

CO 2

Pipeline

Coal Depth = 1,260 feet

Enhanced Coal Bed Methane Recovery

In contrast, he quoted a CO2 value of $10-20/tCO2 when used in EOR projects compared with a cost of production of $7-15/tCO2, noting that this data was site specific to Wyoming.

9

Water Product

Fischer-TropschCoal-

to-Liquids Plant

Gas/Oil/

WaterSep.

CO2

RecycleFacility

EORCO 2

Compressor OilProduct

GasProduct

CO2 ToInjectionWell

Product fromProductionWell

2000-psi 1500-psi

2500-psiCO2

Pipeline

Fischer-TropschCoal-

to-Liquids Plant

CO2 ToInjectionWell

Product fromProductionWell

2000-psi

CO2

Pipeline

Well Depth = 9,500 feet

Enhanced Oil Recovery

►Inject CO2 into existing oil fields to extract additional production

►Evaluation: Highly attractive project economics

Investment required for well development, distribution and re-injection is approximately $165 million for a 1,400 tpd CO2 project

Breakeven CO2 value:$10 - 20 / ton (depending on market oil price)

Gas Product to 3rd party compression & dehydration

10

►Significant CAPEX required

To capture and clean CO2 stream

Gas separation and clean-up costs for syngas prior to entering the FT reactor are inherent to CTL costs (unlike IGCC, where CO2 separation is not required by process and is an additional cost)

Compression costs are significant to reach liquid phase at 2,000 psifrom separation pressures of 1 atm

►Total cost: $7 - $15 / ton

To provide pipeline quality CO2 at the plant fence

Includes return on capital for compression

Impacts of CO2 Capture on Wyoming Project

KERR concluded with a list of Rentech’s current projects, including at East Dubuque, Illinois, where Rentech hopes that a CO2 pipeline, proposed in the Governor’s energy plan for EOR in southern Illinois, will run close enough to allow 100% sequestration. At Natchez, Mississippi, coal and petcoke would be converted, and two joint development projects with Peabody Energy in Illinois and Montana, both include CO2 capture-ready designs for EOR and ECBM.

1111

Peabody Energy JointDevelopment Agreement► 2 projects under study

Sited at or nearby Peabody minesInitial project sizes: 10,000 and 30,000 Bbl/dScalable, repeatable design

► Projects engineered to be carbon-capture ready

► Phase 1One-year Scoping and feasibilitySites under consideration in Montana and Illinois Basin

Rentech Process Licensee► DKRW and Arch Coal

Medicine Bow, Wyoming

► Working with oil and gas company to incorporate carbon capture

East Dubuque►Strategic Location

On the Mississippi RiverExisting Ammonia PlantConversion to Illinois coal feedstock

►CO2 sequestration alternatives Food grade for carbonated beveragesTrapped in Urea, a fertilizer productProposed CO2 pipeline for Enhanced Oil Recovery

►First US commercial scale CTL & FT plantCurrently in Front End Engineering & Design

Natchez►Strategic Location

On the Mississippi RiverNear existing oil fields with Enhanced Oil Recovery

►Ideal CO2 sequestration location Enhanced Oil Recovery

►Currently in feasibility and scoping study

Rentech Projects

Discussion Dr Stephan SINGER, Head of the European Climate and Energy Policy Unit at WWF, wondered if CTL would survive in a post-Bush, carbon-constrained world, because it failed to reduce CO2 emissions. He asked if the SSEB study had considered alternatives, such as coal-to-hydrogen and electric cars, and whether improving vehicle efficiency had been factored in?

BEZDEK replied that efficiency improvements did lead to a substantial demand reduction in the study. Whilst electric vehicles and hydrogen raised their own difficulties and had not been studied, he was aware of other work. BEZDEK returned to the win-win opportunity that CTL with CCS coupled to EOR offered in terms of energy supply.

KERR observed that the efficiency of new vehicle technologies was not necessarily an improvement: he quoted 55 mpg for diesel vehicles and 50 mpg for electric hybrids.

Mr David GRAY, former Director of the British Coal Petrol and Diesel from Coal Project, asked if consumers would consider CTL fuels to be environmentally acceptable, whether oil refiners would permit blending of coal products for distribution, and whether manufacturers would guarantee vehicle engines used with coal-based fuels? He thought that the proposal to produce 5 mb/d in the USA was incredible – requiring, he believed, a doubling of US coal output.

BEZDEK agreed that the supply gap was indeed challenging at 5 mb/d, but would be bridged by energy efficiency measures, oil shale, biomass, biodiesel and electric hybrid vehicles, with coal playing a part through CTL.

KELLY confirmed that oil refiners would accept blending of F-T fuels – DKRW had spent the previous year negotiating detailed specifications and commercial terms with major refiners and marketers in the Rocky Mountain area to allow pipeline shipment to Denver of F-T fuels where they would go into commercial batch.

KERR referred to the September 2006 announcement by the US Department of Defense following the successful trials of a synthetic jet fuel (50:50 F-T:JP 8) in two engines of a B-52 Stratofortress bomber. Produced from natural gas for these trials, but with the stated aim of moving to coal-based fuels by 2009/10.

16

Mr Matthias HARTUNG, Executive Vice President at RWE Power AG, asked if the coal industry was engaged and contributing to the efforts to mitigate CO2 including through CO2 storage?

LEER explained that the industry was putting money into projects jointly supported by government, projects at utility companies and projects at national laboratories. Under almost any scenario, he saw a significant increase in coal use, in the USA, China, India and elsewhere, such that the key question was to find ways of safely storing CO2. LEER was convinced that technology would provide the answers; the developed countries had a responsibility to develop the technologies and to share these with developing countries. This would take time, but with the forecast energy demand growth to 2030, all options would be needed including coal with CCS. He said that to exclude particular energy sources was not good public policy and that it was unrealistic to expect that any country would not exploit its indigenous coal resource.

KELLY spoke as a US-focussed project developer who, like others, was assuming that carbon would have a price in the future and that CO2 would have to be sequestered, even though there was no current policy constraint on CO2 emissions. Developers were motivated not only by the economic potential of projects linked to EOR, but also by the longer term need to deal with CO2. He saw better energy efficiency as an inherent driver – developers sought the maximum output from CTL plants.

Dr Atul ARYA, Vice President of Group Strategy at BP plc, suggested that given the scale and complexity of future CO2 management, the coal industry should collaborate with the oil industry, although he was unsure on precisely how. He thought it better to incentivise energy diversity rather than energy independence. ARYA then posed this dilemma: if the USA achieved greater energy independence through successful CTL projects, then oil prices would presumably fall, making the projects uneconomic.

BEZDEK believed the goal of energy independence was worthy, if only to reduce the rate of growth of imports. It would require many diverse measures, including a commitment to energy efficiency, demand reduction and alternative fuels, and other measures not yet considered. The impact on world oil markets would be positive, but with Chinese demand growth, he thought the price impact might be relative modest.

Dr Don ELDER asked if the Rentech project economics treated CO2 as a credit of $5/tCO2 or as an avoided cost? He also asked a more fundamental question on the feasibility of constructing as many as one hundred 50 000 b/d CTL projects in the USA. Had the economic analysis considered the inflationary pressures of such a large programme on costs of materials, labour, technology, coal, water, etc.?

KERR responded that the CO2 credit assumed a plant already running with an established baseline such that the avoided CO2 would have a value.

BEZDEK replied that Nth plant costs had been assessed with different capital costs assumptions. However, he believed that there would be huge demand from all energy sectors which would therefore all be faced with similar inflationary pressures. He did have a concern about a shortage of labour, especially following the downsizing during the 1990s when the US oil and gas industry lost half a million people.