college planning essentials - j.p. morgan asset · pdf filecollege planning essentials ......

TRANSCRIPT

College Planning EssentialsA comprehensive guide to saving and investing

INVESTMENTS ARE NOT FDIC INSURED | NO BANK GUARANTEE | MAY LOSE VALUE

2015–2016

Section 1 College matters

Section 5 Appendix

Section 4 Saving and investing

Section 3 Financial aid

4 Higher education pays

5 More education, less unemployment

6 Return on a college investment

7 “Major” differences in salaries

8 Good intentions, unexpected consequences

41 Sources of financial aid

42 Financial aid: Types of applications

43 Federal aid methodologies

44 Federal student aid: A sample of grant programs

45 Federal student aid: Loan programs

46 College-related tax breaks

47 Comparing college savings options

48 The 529 plan advantage

49 Checklist: Choosing a 529 plan

50 529 plans: State tax benefits

51 Index definitions

52 Disclosures

26 Comparing college savings vehicles

27 Current saving and investing trends

28 Investing for long-term growth

29 Investing versus borrowing

30 The benefits of compounding

31 Performance pays

32 Invest more, pay less

33 Tax-efficient investing

34 Making college savings a family affair

35 Don’t pay for college with retirement funds

36 Staying diversified over 18 years

37 The power of diversification

38 Asset allocation provided a smoother ride

39 College planning checklist

Section 2 College costs

10 Tuition inflation

11 Rising college costs

12 Future four-year college costs

13 The real cost of college

14 How college costs affect behavior

16 Financial aid overview

17 Financial aid reality check

18 Federal financial aid eligibility

19 Estimating Expected Family Contribution

20 The effect of savings on financial aid

21 Student loan landscape

22 Private loans

23 The burden of debt

24 How college loans affect retirement

2

COLL

EGE

MAT

TER

S

Myth: “ College is too expensive.”

Fact: The return on an investment in college is nearly $1 million more in lifetime earnings.Page 4

College mattersThe value of a college education is growing faster than the cost. Today, a college diploma has become a necessity for anyone seeking increased earning potential, job security and career opportunity.

Common myths and facts

SECTION 1

College Planning Essentials: A comprehensive guide to saving and investing

Myth: “ Not even college graduates can fi nd a job in this economy.”

Fact: The unemployment rate among college graduates is currently just 2.5%.Page 5

Myth: “ College just isn’t worth the student loan debt.”

Fact: A college graduate earns 38% more than a high school graduate, even after factoring in student loans.Page 6

Source: Georgetown University, Failure to Launch: Structural Shift and the New Lost Generation, 2013.

By 2020, 65% of U.S. jobs will require a degree beyond high school, up from 28% in 1973.

65%

20201973

28%

COLL

EGE

MAT

TER

SCO

LLEG

E CO

STS

FIN

AN

CIA

L A

IDSA

VIN

G &

INV

ESTI

NG

4

APP

END

IX

• Bachelor’s degree holders earn nearly $1 million more over a lifetime than high school graduates. Those with doctorate degrees earn nearly $2 million more.1

• People who attend college but don’t receive a degree earn only 11% more than high school graduates.2

Higher education pays

A college diploma opens the door to a lifetime of higher earnings.

1. Bureau of Labor Statistics, 2014 dollars, based on 2014 earnings projected over a typical work life of ages 25 through 64.

2. Current Population Survey, U.S. Bureau of Labor Statistics, 2014 dollars, U.S. Department of Labor. J.P. Morgan Asset Management. Data are for persons age 25 and over. Earnings are for full-time wage and salary workers.

Average annual earnings by highest degree earned2

DEGREES OF DIFFERENCE $100,000

$60,000

$80,000

$40,000

$20,000

$0

HIGH SCHOOL GRADUATE BACHELOR’S DEGREE PROFESSIONAL DEGREE

$34,736 $57,252 $85,228

65%GREATER

PAY

145%GREATER

PAY

COLL

EGE

MAT

TER

SCO

LLEG

E CO

STS

FIN

AN

CIA

L A

IDSA

VIN

G &

INV

ESTI

NG

5

APP

END

IX

More education, less unemployment

College graduates enjoy much better job security and opportunity, especially during economic downturns.

BRIGHT JOB PROSPECTS

• The number of college-educated Americans with jobs has increased 18.2% since the beginning of the recession.1

• The unemployment rate for high school graduates aged 20 to 24 was 18.9% in 2014, nearly triple the rate for graduates with a bachelor’s degree or higher.2

• A shortage of 5 million college-educated workers is projected by 2020.3

1. Bureau of Labor Statistics Employment Situation Report, September 2015.2. National Center for Education Statistics, November 2014.3. Georgetown University Center on Education and Workforce, June 2013. Based on current production rate.4. J.P. Morgan Asset Management, Bureau of Labor Statistics, FactSet. Unemployment rates shown are for civilians

aged 25 and older. Data are as of 9/30/15.

Unemployment rates by education levelas of September 20154

19930%

2%

4%

8%

6%

10%

12%

14%

16%

18%

1995 2015201320112009200720052003200119991997

LESS THAN HIGH SCHOOL DIPLOMAHIGH SCHOOL, NO COLLEGE

SOME COLLEGECOLLEGE OR GREATER

7.9%Less than high school diploma

5.2%High school, no college

4.3%Some college

2.5%College or greater

COLL

EGE

MAT

TER

SCO

LLEG

E CO

STS

FIN

AN

CIA

L A

IDSA

VIN

G &

INV

ESTI

NG

6

APP

END

IX

Return on a college investment

Even students who borrow for college can expect a signifi cant long-term return on their investment.

Estimated cumulative earnings minus student loan repaymentBachelor’s degree versus high school diploma

CUM

ULA

TIV

E N

ET E

AR

NIN

GS

AGE

18 22 26 30 34 38 42 46 50 54 58 62 64$0

$200,000

$1,200,000

$1,000,000

$800,000

$600,000

$400,000

BACHELOR’S DEGREE

HIGH SCHOOL DIPLOMA

38% RETURN ON INVESTMENT

In this scenario, a college diploma pays for itself by age 36.

The college graduate earns 38% more over a lifetime than the high school graduate, even when factoring in loan repayment of full tuition costs.

Source: College Board, Education Pays 2013. Based on median 2011 earnings for individuals working full-time year-round at each education level and each age. Includes only students who complete degrees; excludes bachelor’s degree recipients who earn advanced degrees. Assumes college graduates borrow $14,352 to cover total first-year tuition and fee charges for 2011–2012 (weighted average of $8,256 average public four-year in-state and $27,883 private nonprofit four-year tuition and fees) for the first year and 5% more each of the next three years. Tuition payments and earnings are discounted at 3%, compounded every year beyond age 18.

36years old

COLL

EGE

MAT

TER

SCO

LLEG

E CO

STS

FIN

AN

CIA

L A

IDSA

VIN

G &

INV

ESTI

NG

7

APP

END

IX

“Major” differences in salaries

$0 $10,000 $20,000 $30,000 $40,000 $50,000 $60,000

Choice of college major has a signifi cant impact on a graduate’s starting salary.

SALARIES ON THE RISE

• On average, starting salaries for the class of 2015 are 5.2% higher than for the class of 2014.

• If salaries continue rising at this pace, the average child born today would earn roughly $91,700 in the fi rst year after college.

All degrees $48,707

Math and Sciences $44,299

Humanities and Social Sciences $38,049

Engineering $62,891

Computer Science $62,103

Communications $48,253

Business $57,229

Education $40,267

Average yearly starting salaryby college major for the class of 2015

Source: National Association of College and Employers (NACE) Salary Survey Executive Summary, Fall 2015.

COLL

EGE

MAT

TER

SCO

LLEG

E CO

STS

FIN

AN

CIA

L A

IDSA

VIN

G &

INV

ESTI

NG

8

APP

END

IX

Good intentions, unexpected consequences

Saving for college is one of a family’s top fi nancial priorities, but common mistakes can keep them from achieving goals.

Why save for college

College degree is more important now

STRONGLY AGREE SOMEWHAT AGREE

Source: Sallie Mae, How America Saves for College, 2015.

Part of the American dream

Possible reasons why:

Child will earn more money

An investment in child’s future

53% 31%

52% 26%

89%

84%

49% 34%

83%

78%

59%of parents are not

confi dent about meeting college costs.

• Not having a plan

• Investing too conservatively

• Starting too late

• Using taxable or retirementaccounts

• Overestimating fi nancial aid

• Underestimating college costs

• Not getting others involved

64% 25%

COLL

EGE

COST

S

Myth: “ I know how expensive college is.”

Fact: Many families underestimate just how much college costs and how quickly prices rise.Pages 11 and 12

Common myths and facts

College Planning Essentials: A comprehensive guide to saving and investing

Myth: “ I’m not concerned about college infl ation. It has to slow down at some point.”

Fact: Tuition continues to rise at a much faster rate than other expenses, so your savings need to keep pace.Page 10

Myth: “ I’ll just make a few compromises to help pay for college.”

Fact: Non-savers often don’t realize the sacrifi ces needed to make college affordable.Page 14

Source: Sallie Mae, How America Pays for College, 2015.

College costsSaving for college starts with a plan. And a plan starts with a goal. It’s important to understand college costs so you know how much to save by enrollment time.

SECTION 2

of families have to rule out colleges because of cost.62%

10

COLL

EGE

MAT

TER

SCO

LLEG

E CO

STS

FIN

AN

CIA

L A

IDA

PPEN

DIX

SAV

ING

& IN

VES

TIN

G

Tuition infl ation

College tuition costs have increased faster than any other household expense in recent decades.

• Colleges are spending more to attract the best students.

• Colleges are hiring more to reduce student-to-faculty ratios.

• Colleges are receiving less fi nancial support from cash-strapped states.

WHY COSTS ARE RISING

Source: BLS, Consumer Price Index, J.P. Morgan Asset Management. Data represents cumulative percentage price change from January 1983–August 2015.

108%

128%

143%

186%

356%

722%

28%

47%

0% 100% 200% 300% 400% 500% 600% 700% 800%

Sweets

Apparel

Cars

Coffee

Gas

Housing

Medical Care

Tuition

Tuition versus other expensesCumulative percent price change since 1983

11

COLL

EGE

MAT

TER

SCO

LLEG

E CO

STS

FIN

AN

CIA

L A

IDA

PPEN

DIX

SAV

ING

& IN

VES

TIN

G

Rising college costs

College savings need to grow at a healthy rate to match or exceed rapidly rising costs.

KEEPING PACE

• During the 2014-15 academic year, families spent an average of $24,164 on college – up 16% from the previous year. This has been the largest increase since 2009-10.1

• If prices increase 5% each year, the cost of college will more than double by 2034.

1. Sallie Mae, How America Pays for College, 2015.2. J.P. Morgan Asset Management using The College Board, 2015 Trends in College Pricing.

Future college costs estimated to inflate 5% per year. Average tuition and fees for the public sector reflect four-year, in-state charges.

2034

Tuition, fees and room and board expenses2

Private

Private

Public

Public

$105,701

$47,045

$43,921

$19,548

TUITION AND FEES

PROJECTED ANNUAL COSTS for 2034

Private$105,701

Public$47,045

ROOM AND BOARD2016

$20,000$0 $40,000 $60,000 $80,000 $100,000

12

COLL

EGE

MAT

TER

SCO

LLEG

E CO

STS

FIN

AN

CIA

L A

IDA

PPEN

DIX

SAV

ING

& IN

VES

TIN

G

Future four-year college costs

Source: J.P. Morgan Asset Management, using The College Board, 2015 Trends in College Pricing. Future college costs estimated to inflate 5% per year.

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

$500,000

Projected cost of a four-year college educationbased on child’s current age

$124,482$112,909

$102,412$92,890$84,254

$279,690

$253,687

$230,101

$208,709$189,305

PUBLIC

PRIVATE

$308,358

$137,241

$339,965

$151,309

$374,811

$166,818

$413,229

$183,917

$455,585

$202,768

The younger the child, the more college is likely to cost. Add up four years per child, and it equals one of a family’s largest expenses.

NewbornAge 18 Age 16 Age 14 Age 12 Age 10 Age 8 Age 6 Age 4 Age 2

13

COLL

EGE

MAT

TER

SCO

LLEG

E CO

STS

FIN

AN

CIA

L A

IDA

PPEN

DIX

SAV

ING

& IN

VES

TIN

G

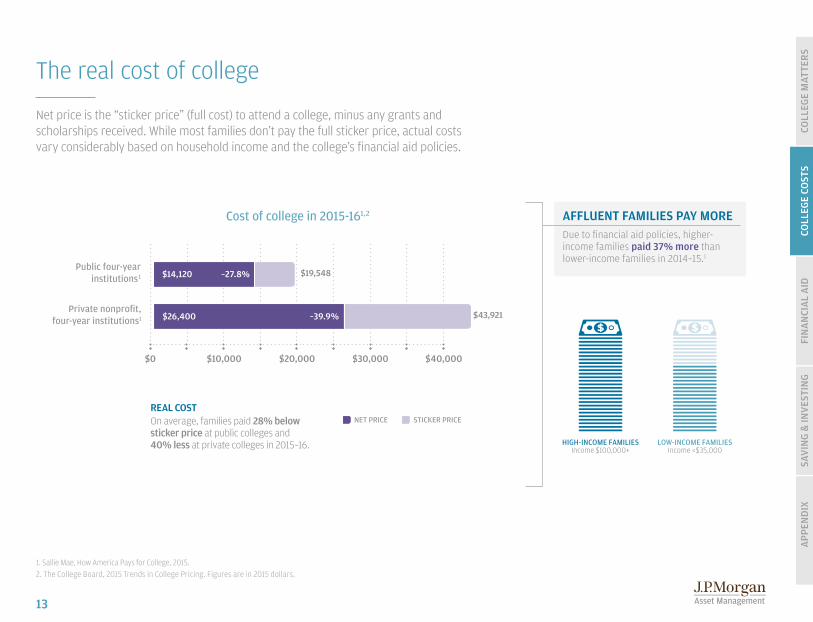

AFFLUENT FAMILIES PAY MOREDue to fi nancial aid policies, higher-income families paid 37% more than lower-income families in 2014–15.1

The real cost of college

Net price is the “sticker price” (full cost) to attend a college, minus any grants and scholarships received. While most families don’t pay the full sticker price, actual costs vary considerably based on household income and the college’s fi nancial aid policies.

1. Sallie Mae, How America Pays for College, 2015.2. The College Board, 2015 Trends in College Pricing. Figures are in 2015 dollars.

NET PRICE STICKER PRICE

REAL COSTOn average, families paid 28% below sticker price at public colleges and 40% less at private colleges in 2015–16. HIGH-INCOME FAMILIES

Income $100,000+LOW-INCOME FAMILIES

Income <$35,000

$0 $10,000 $20,000 $30,000 $40,000

$14,120 –27.8% $19,548

$43,921 $26,400 –39.9%

Public four-year institutions1

Private nonprofi t, four-year institutions1

Cost of college in 2015-161,2

14

COLL

EGE

MAT

TER

SCO

LLEG

E CO

STS

FIN

AN

CIA

L A

IDA

PPEN

DIX

SAV

ING

& IN

VES

TIN

G

42%

Student works more

45%

Parent reduces

spending

How college costs affect behavior

To better afford college, many families must choose less expensive schools or change their daily lifestyles.

Source: Sallie Mae, How America Pays for College, 2015.

Actions taken to make college more affordablePercentage of people taking each action

Parent works more

22%

Student changes

major

16%

Student accelerates education

25%

Student reduces

spending

60%48%

Student lives at home

STUDENT ACTIONS PARENT ACTIONS

Elimination of colleges based on cost

0% 20% 40% 60% 80% 100%

OFF THE LISTAfter reviewing their fi nancial aid package, 62% of families ruled out some colleges based on cost, up from 56% in 2009.

2015 62%

FIN

AN

CIA

L A

ID

Financial aidSECTION 3

Financial aid can help pay for college, but not all aid is free, and not everyone qualifi es. The more you save now, the less you may have to borrow later.

Myth: “Financial aid is free money.”

Fact: 34% of all aid comes from loans that must be paid back with interest.Page 16

Common myths and facts

College Planning Essentials: A comprehensive guide to saving and investing

Myth: “ I don’t need to save because my child will receive a scholarship.”

Fact: Only 0.3% of college students actually get a full ride. Page 17

Myth: “ Saving for college will hurt my chances for fi nancial aid.”

Fact: Savings generally have little impact on fi nancial aid eligibility when the funds are held in parents’ names.Pages 18 and 20

Source: Edvisors, MarketWatch, "Class of 2015 has the most student debt in U.S. history," May 2015.

7 in 10 college seniors graduated with student loan debt in 2015.

16

COLL

EGE

COST

SFI

NA

NCI

AL

AID

APP

END

IXSA

VIN

G &

INV

ESTI

NG

COLL

EGE

MAT

TER

S

TOTAL AID IN 2013–14

$184.5 billion

Financial aid overview

Most college students require fi nancial assistance of some kind, but 34% of all aid comes in the form of loans that must be paid back with interest.

AID IS DOWN, TUITION IS UP

• From 2008 to 2014, state and local fi nancing per student declined 23% nationally.

• From 2003 to 2015, tuition and fees increased 69% at state colleges and nearly 31% at non-profi t private institutions.

Undergraduate student aid by source and typein billions, 2013–14

Borrowed

Free money

$62.9

(34%)

(26%)

(21%)

(8%)

(6%)

$47.1

$37.9

$15.6

$10.8

Federal loans

State grants

Private and employer grants

Federal work study$0.9 (<1%)

Federal grants including Pell

Institutional grants

Educationtax benefi ts

Source: The College Board, November 2014 Trends in Student Aid. Percentages may not total 100% due to rounding.

Average aid packagefor full-time undergraduate

students, 2013–14

Federal loans$4,840

Tax credits, deductions and federal work study$1,260

Grant aid from all sources$8,080

Average total aid package

$14,180

(5%)$9.3

17

COLL

EGE

COST

SFI

NA

NCI

AL

AID

APP

END

IXSA

VIN

G &

INV

ESTI

NG

COLL

EGE

MAT

TER

S

1. Sallie Mae, How America Pays for College, 2015.2. Finaid.org. Based on full-time students at four-year colleges.3. Sallie Mae, How America Saves for College, 2015.

2-year Public22%

4-yearPublic 10%

Private 13%

2-year Public

8%

Private 26%

4-yearPublic13%

Financial aid reality check

Many families expect more free money from grants and scholarships than they are likely to receive.

MORE APPLICATIONS, LESS AID

• Financial aid applicants include 86% of middle-income families and 76% of high-income families. The more people applying, the less aid there is to go around.1

Financial aid expectations3

61%

Grant reality 2014–15 (need-based)

Scholarship reality 2014–15 (merit-based)

45%

46%

Percent of total costs covered by grants

Percent of total costs covered by scholarships

of parents who are not yet saving for college expect

scholarships or grants to cover

the costs.

of families received grants averaging $7,1141

of families received scholarships averaging $8,8431

of college students receive enough grants

and scholarships to cover all costs.2

0.3%

18

COLL

EGE

COST

SFI

NA

NCI

AL

AID

APP

END

IXSA

VIN

G &

INV

ESTI

NG

COLL

EGE

MAT

TER

S

1. Sallie Mae, How America Pays for College 2015.2. Based on federal methodology for 2016–17 school year.3. Protected amount for parents is dependent upon a number of factors, including household size and number of students in college.

Federal fi nancial aid eligibility

The Department of Education processes the Free Application for Federal Student Aid (FAFSA) to determine the Expected Family Contribution (EFC). This is the amount colleges use to determine how much federal aid you’re eligible to receive.

FEDERAL AID

In 2013–14, 82% of families with a college-bound child applied for federal aid.1

TOTAL COLLEGECOSTS EACH YEAR

EXPECTED FAMILYCONTRIBUTION (EFC)

FINANCIAL AID ELIGIBILITY

GRANDPARENTS/OTHERS

0%of income and assets considered in federal fi nancial aid

formulas. However, withdrawals for college by grandparents or others may be considered student income and must be reported on the following year’s fi nancial aid forms. Such

income can reduce the amount of aid by 50%.

PARENTS

Income

Up to 5.64%

of non-retirement assets above

protected amount, including 529 plans,

investments and savings

Assets

+ 50%of income

above protected amount of $6,400

20%of all assets in bank accounts, CDs, UGMAs/

UTMAs and any other savings

Income

STUDENTS

+

Assets

EFC is not the amount your family will pay for college or

get in federal aid. It’s a number used by schools to calculate how much aid a student is

eligible to receive.

TOTAL EFCHOW EFC IS CALCULATED2

A family’s annual income, including the student’s, counts far more in the formula than savings and investments, especially when held in the parents’ names.

of adjusted gross income above the protected

amount3

22%–47%

19

COLL

EGE

COST

SFI

NA

NCI

AL

AID

APP

END

IXSA

VIN

G &

INV

ESTI

NG

COLL

EGE

MAT

TER

S

Estimating Expected Family Contribution

1. Based on two-parent household with one child attending college, one child living at home. Assuming no income or assets for each dependent and age 49 for eldest parent. Protected amounts for assets vary based on age and income. These are estimates provided for illustrative purposes only, and they may not be representative of your personal situation and circumstances.

Expected Family ContributionEstimates based on income and assets1

ASSETS (EXCLUDING PRIMARY RESIDENCE AND RETIREMENT ACCOUNTS)

$0

$2,364

$7,200

$15,170

$22,517

$30,257

$37,988

$45,391

$52,741

$60,091

$25,000

$2,364

$7,200

$15,170

$22,517

$30,257

$37,988

$45,391

$52,741

$60,091

$50,000

$75,000

$100,000

$125,000

$150,000

$175,000

$200,000

$225,000

$250,000

$50,000

$2,863

$8,108

$16,236

$23,583

$31,323

$39,054

$46,457

$53,807

$61,157

$150,000

$6,060

$13,666

$21,876

$29,223

$36,963

$44,694

$52,097

$59,447

$66,797

$200,000

$8,299

$16,486

$24,696

$32,043

$39,783

$47,514

$54,917

$62,267

$69,617

$250,000

$11,071

$19,306

$27,516

$34,863

$42,603

$50,334

$57,737

$65,087

$72,437

$300,000

$13,891

$22,126

$30,336

$37,683

$45,423

$53,154

$60,557

$67,907

$75,257

COM

BIN

ED IN

COM

E

Example: If you earn $150,000 in income and have $100,000 of savings, your estimated EFC is $34,143.

$100,000

$4,282

$10,846

$19,056

$26,403

$34,143

$41,874

$49,277

$56,627

$63,977

The Department of Education provides the Expected Family Contribution (EFC) as guidance to colleges on fi nancial aid eligibility in order to help determine the amount a family should pay. Use the chart below to estimate your EFC based on combined income and assets.

20

COLL

EGE

COST

SFI

NA

NCI

AL

AID

APP

END

IXSA

VIN

G &

INV

ESTI

NG

COLL

EGE

MAT

TER

S

The effect of savings on fi nancial aid

Savings actually count far less than income when calculating your Expected Family Contribution (EFC) for federal fi nancial aid purposes.

529 PLAN ADVANTAGE

• When a 529 account is owned by parents, it has much less impact on federal fi nancial aid eligibility than custodial accounts.

Maximum parental savings considered in federal fi nancial aid formulas.

5.64%

Big difference in college savings, little difference in fi nancial aidFederal fi nancial aid for two families earning the same income and sending a

child to the same college costing $30,000 per year

EXPECTED FAMILY CONTRIBUTION

FEDERAL FINANCIAL AID

$30,000

$20,000

$10,000

$0Smiths

$75,000 saved in 529 plan

WilsonsNo savings

$18,152$16,229

$11,848 $13,771

The Smiths have $75,000 more in savings but get just $1,923 less in financial aid.

Source: J.P. Morgan Asset Management and finaid.org. Assumes both families earn $100,000 annually and 529 plan is owned by the parents. Does not include non-federal financial aid opportunities such as scholarships.

21

COLL

EGE

COST

SFI

NA

NCI

AL

AID

APP

END

IXSA

VIN

G &

INV

ESTI

NG

COLL

EGE

MAT

TER

S

Student loan landscape

Student loan debt has soared in recent years, putting an increased fi nancial burden on college graduates and their parents.

Subsidized Stafford LoansFor undergraduate students with documented fi nancial need. The government pays interest while the student is in college.

Unsubsidized Stafford Loans For undergraduate and graduate students regardless of fi nancial need. The government does not pay interest while the student is in college.

Grad PLUS For graduate students only.

Parents PLUS For parents only.

Perkins For students with high need at some institutions.

Private Education Loans2 Offered by private lenders, they can either supplement or replace federally guaranteed loans.

$0 $10 $20 $30 $40 $50 $60 $70 $80 $90 $100 $110 $120

2005–06

2009–10

2013–14 t$105.8

t$117.7

t$90.4

Issuance of federal and private loansSelected years, 2013 dollars in billions1

1. The College Board, 2014 Trends in Student Aid.2. Private education includes loans to students from states and from institutions, in addition to private loans by banks, credit unions and Sallie Mae.3. Edvisors.com, May 2015.4. New York Federal Reserve, Wall Street Journal, “5 Things About Grad-School Debt,” August 2015.

Americans carrying at least $100,000 in student loan debt have more than quintupled in the past decade to just over 1.8 million.4

The class of 2015 is the most indebted in history, with an average of $35,051 owed per student.3

22

COLL

EGE

COST

SFI

NA

NCI

AL

AID

APP

END

IXSA

VIN

G &

INV

ESTI

NG

COLL

EGE

MAT

TER

S

Private loans

With college costs rising faster than the availability of federal aid, many families are choosing to fi ll the growing gap with private loans.

PRIVATE LOANS AT A GLANCE

Private loan defaultsas of 20122

$8 billionin defaulted private loans

850,000distinct loans in default

• Americans currently owe $91 billion in outstanding private student loan debt.1

• Private loans make up 7.2% of the $1.27 trillion student loan market.

• Private student loans tend to have higher interest rates and less flexible repayment options than federal loans.

1. MeasureOne Private Student Loan Performance Report – Q1 2015.2. Private Student Loan Report 2012, Consumer Finance Protection Bureau.

Federal vs. private student loansOutstanding balances (in billions)1

Federal $1,174.492.8%

Private $91.07.2%

23

COLL

EGE

COST

SFI

NA

NCI

AL

AID

APP

END

IXSA

VIN

G &

INV

ESTI

NG

COLL

EGE

MAT

TER

S

The burden of debt Debt balancesby type of consumer loan (in trillions)2

• Student loan debt more than tripled to $1.2 trillion between 2004 and 2014.2

• The average student borrower graduates with $35,051 in loans.3

• Student loan defaults are at a 20-year high, affecting over 7 million borrowers.4

DROWNING IN DEBT

$0.4

$0.6

$0.8

$1.0

$1.2

’04 ’05 ’06 ’07 ’08 ’09 ’10 ’11 ’12 ’13 ’14 ’15

STUDENT LOAN

CREDIT CARD

AUTO LOAN

HOME-EQUITY LOAN

In 2010, student loan debt surpassed credit card debt for

the fi rst time in history.

The debt impacton students and their parents

42% 65% 75% $208,000of recent college graduates

currently live with their parents5of parents expect to support their children for up to five

years after graduation6

of student borrowers say loan payments make it harder

to buy a home7

loss in lifetime wealth due to student loan debt8

1. Pew Research Center. Young Adults, Student Debt and Economic Well-Being Report, May 2014. Households headed by a person younger than 40.

2. New York Federal Reserve, Household Debt and Credit Report, Q2 2015.

3. Edvisors.com, May 2015. 4. U.S. Department of Education, FY 2014, Q3. 5. Accenture, 2014 College Graduate Employment Survey. 6. Upromise by Sallie Mae, 2015.

7. American Student Assistance, “Life Delayed: The Impact of Student Debt on the Daily Lives of Young Americans,” 2013.

8. Demos, “At What Cost? How Student Debt Reduces Lifetime Wealth,” August 2013.

Families that don’t save enough for college often have no other choice than to borrow. Today, a record four in 10 households owe student debt.1

• The interest rate on federal parental college loans is 6.84%.1

DID YOU KNOW?

How college loans affect retirement

Parents who borrow for college often spend their critical pre-retirement years paying off loans instead of funding 401(k)s, IRAs and other retirement accounts.

1. Interest rates apply to loans first disbursed between July 1, 2015, and July 1, 2016. 2. Edvisors, U.S. Department of Education, National Postsecondary Student Aid Study, May 2015.3. J.P. Morgan Asset Management. Assumes a 6.84% interest rate and 10-year loan repayment period.4. J.P. Morgan Asset Management. Illustration assumes $356 monthly investments over 10 years and an annual investment return of 6%, without the effects of taxes. This example does not

represent the performance of any particular investment. Different assumptions will result in outcomes different than this example. Your results may be more or less that the figures shown. Investment losses could affect the relative tax-deferred investment advantage. Each investor should consider his or her current and anticipated investment horizon and income tax bracket when making an investment decision, as the illustration may not reflect these factors. These figures do not reflect any management fees or expenses. Such costs would lower performance. This chart is shown for illustrative purposes only. Past performance is no guarantee of future results.

If this money were invested for retirement insteadGrowth of $356 monthly investments made over 10 years4

$59,687$42,720 $106,890 $191,424

10 years 20 years 30 years

INVESTMENT GROWTHTOTAL INVESTMENT

Average parental debt at college graduation

$30,867 $356 $42,720Total debt2 Monthly loan payment3 Total cost with interest3

While in an account, 0% of parents’ retirement assets are considered in federal fi nancial aid formulas.

Withdrawals taken to pay for college are treated as student income, half of which may count against federal aid packages.

0 %

50 %

The relationship between retirement savings and college fi nancial aid

24

COLL

EGE

COST

SFI

NA

NCI

AL

AID

APP

END

IXSA

VIN

G &

INV

ESTI

NG

COLL

EGE

MAT

TER

S

SAV

ING

& IN

VES

TIN

G

Saving and investingSECTION 4

Choosing the right savings plan and following time-tested investment strategies can help you reduce taxes, increase growth potential and accumulate more for college.

Myth: “ All college savings plans are the same.”

Fact: College savings plans differ in a variety of ways, including investments, tax benefi ts and fl exibility. Pages 26 and 33

Common myths and facts

College Planning Essentials: A comprehensive guide to saving and investing

Myth: “ I’ll just take out a loan if I don’t save enough.”

Fact: It costs more to borrow and pay interest than to invest and earn interest. Page 29

Myth: “ It’s too early to start saving for college.”

Fact: Starting early and saving regularly helps you maximize the power of compounding. Page 30

Source: Sallie Mae, How America Saves for College, 2015.

of families saving for college invest in 529 plans.Only 27%

26

COLL

EGE

COST

SFI

NA

NCI

AL

AID

SAV

ING

& IN

VES

TIN

GA

PPEN

DIX

COLL

EGE

MAT

TER

S

27%

Comparing college savings vehicles

Understanding the different tax benefi ts and features of college savings vehicles can help you choose the right one for your needs.

of parents own 529 plans

Source: Sallie Mae, How America Saves for College, 2015.1. Earnings on non-qualified withdrawals may be subject to federal income tax and a 10% federal penalty tax, as well as state and local income taxes.

529 college savings plan Custodial account (UGMA/UTMA) Coverdell Education Savings Account

• Tax-free investing and withdrawals for any qualifi ed higher education expense1

• Account owner control for the life of the account

• No income limits on contributors

• High contribution maximums

• Low impact on fi nancial aid eligibility

• Funds must be used for the child’s benefi t, not necessarily for college

• Portion of investment earnings taxed at child’s and parents’ rates

• Child assumes control at age of majority, usually 18 or 21

• High impact on fi nancial aid eligibility

• Tax-free investing and withdrawals for any level of education1

• Income limits on contributors

• Age limits on benefi ciaries

• Maximum contribution of $2,000 annually per benefi ciary

• Low impact on fi nancial aid eligibility

of parents own UGMA/UTMA accounts9% of parents own

Coverdell accounts11%

27

COLL

EGE

COST

SFI

NA

NCI

AL

AID

SAV

ING

& IN

VES

TIN

GA

PPEN

DIX

COLL

EGE

MAT

TER

S

14%U.S. Savings Bonds

Current saving and investing trends

Half of U.S. families aren’t saving for college. The other half often choose vehicles that don’t maximize their growth potential, such as savings accounts, CDs and taxable investments.

Percentage of families using:

15%CDs

48%General Savings Accounts

27%529 College Savings Plan

17%Investments

11%Trust Fund

12%Prepaid State Plan

23%Checking Account

11%Coverdell Education Savings Accounts

Source: Sallie Mae, How America Saves for College, 2015.

0% 50%10% 20% 30% 40%

9%UGMA/UTMA

FAMILIES DON’T FULLY MAXIMIZE GROWTH POTENTIALMore parents—48%—save for college with low-yielding savings accounts than any other method.

FAMILIES USING A 529 PLAN

FAMILIES USING A TRADITIONAL

SAVINGS ACCOUNT

On average, those parents with a 529 plan save 89% more than those simply using a savings account.

28

COLL

EGE

COST

SFI

NA

NCI

AL

AID

SAV

ING

& IN

VES

TIN

GA

PPEN

DIX

COLL

EGE

MAT

TER

S

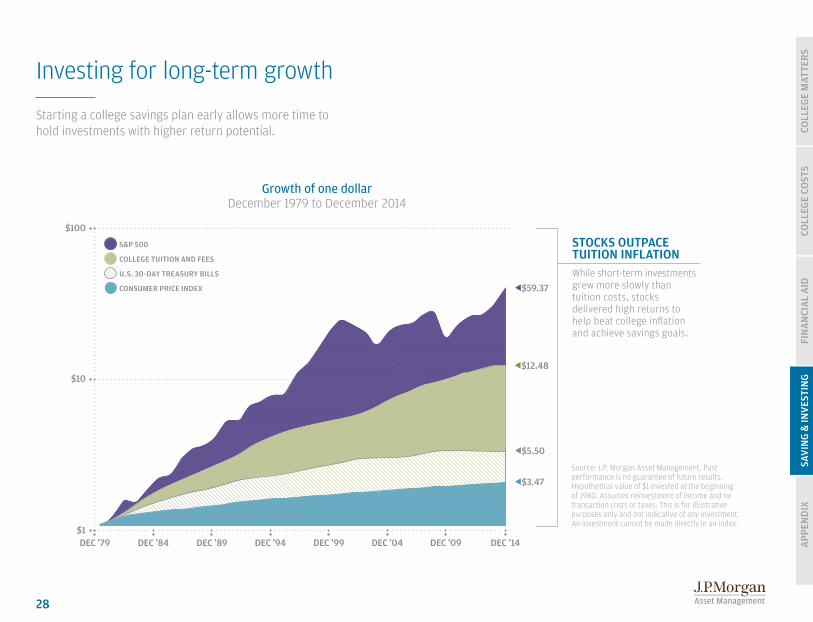

S&P 500

U.S. 30-DAY TREASURY BILLS

CONSUMER PRICE INDEX

COLLEGE TUITION AND FEES

Investing for long-term growth

Starting a college savings plan early allows more time to hold investments with higher return potential.

$100

$10

$1DEC ’79 DEC ’14DEC ’09DEC ’04DEC ’99DEC ’94DEC ’89DEC ’84

Growth of one dollarDecember 1979 to December 2014

Source: J.P. Morgan Asset Management. Past performance is no guarantee of future results. Hypothetical value of $1 invested at the beginning of 1980. Assumes reinvestment of income and no transaction costs or taxes. This is for illustrative purposes only and not indicative of any investment. An investment cannot be made directly in an index.

STOCKS OUTPACE TUITION INFLATIONWhile short-term investments grew more slowly than tuition costs, stocks delivered high returns to help beat college infl ation and achieve savings goals.

t$59.37

t$12.48

t$5.50

t$3.47

Investing versus borrowing

It costs less to invest now than to borrow later. When you borrow for college, you pay interest. When you invest, you earn interest and other forms of investment returns.

IT TAKES A PLAN

• Without a plan, families run the risk of not saving enough and borrowing too much. Yet 36% of high-income families and 60% of middle-income families don’t have a plan to pay for college.1

529 college savings plan versus student loanInitial investment of $1,000 plus monthly investments of $3002

$200,000

$150,000

$100,000

$50,000

$0College savings plan

over 18 yearsCollege loan:principal and

interest

$119,143

INVESTMENT GROWTH

OUT-OF-POCKET COST

$167,553

$65,800

lower out-of-pocket costwith 529 plan

$101,753

Average parental loan debt at graduation3

$10,000

$17,577

$30,867

$7,799

$0

1994-95

2004-05

2014-15

$20,000 $40,000$30,000

A BURDEN FOR EVERYONEThe average parental debt load has almost doubled in a decade to nearly $31,000 in 2014-15, while the average debt faced by students was more than $35,000 in 2015.4

1. Sallie Mae, How America Pays for College, 2015.2. J.P. Morgan Asset Management. The investing illustration

assumes an initial lump-sum investment of $1,000, subsequent monthly investments of $300 thereafter for 18 years, and assumes an annual investment return of 6% and federal tax rate of 28%. Investment losses could affect the relative tax-deferred investment advantage. Each investor should consider his or her current and anticipated investment horizon and income tax bracket when making an investment decision, as the illustration may not reflect these factors. The borrowing illustration assumes an interest rate of 7.21% and a payback period of 10 years. This hypothetical illustration is not indicative of any specific investment and does not reflect the impact of fees or expenses. The chart is shown for illustrative purposes only. Past performance is no guarantee of future results.

3. Edvisors, U.S. Department of Education, National Postsecondary Student Aid Study, May 2015.

4. Wall Street Journal, “Congratulations Class of 2015. You’re the Most Indebted Ever (For Now),” May 2015, and MarketWatch, “Class of 2015 has the most student debt in U.S. history,” May 2015.

29

COLL

EGE

COST

SFI

NA

NCI

AL

AID

SAV

ING

& IN

VES

TIN

GA

PPEN

DIX

COLL

EGE

MAT

TER

S

30

COLL

EGE

COST

SFI

NA

NCI

AL

AID

SAV

ING

& IN

VES

TIN

GA

PPEN

DIX

COLL

EGE

MAT

TER

S

The benefi ts of compounding

The sooner you start saving, the more time you may have to grow your college fund through the power of long-term compounding. Even small contributions add up over time.

Total accumulation

in 6 years

Total accumulationin 12 years

Total accumulationin 18 years

$50,000

$100,000

$150,000

$200,000

$0

$100 MONTHLY CONTRIBUTIONS

$250 MONTHLY CONTRIBUTIONS

$500 MONTHLY CONTRIBUTIONS

Start early, small savings add upTotal amounts accumulated over 6, 12 and 18 years

If you start saving $500 per month when a child is born, you’ll earn

$84,214 morethan if you start at age 6.

$8,3

70 $20

,926

$41,

852

$50

,610

$10

1,22

0

$37,

087

$92,

717

$185

,434

$20

,24

4

Source: J.P. Morgan Asset Management. This hypothetical example illustrates the future values of different regular monthly investments for different time periods. Chart also assumes an annual investment return of 6%. Investment losses could affect the relative tax-deferred investing advantage. This hypothetical illustration is not indicative of any specific investment and does not reflect the impact of fees or expenses. Such costs would lower performance. Each investor should consider his or her current and anticipated investment horizon and income tax bracket when making an investment decision, as the illustration may not reflect these factors. A plan of regular investment cannot assure a profit or protect against a loss in a declining market. The chart is shown for illustrative purposes only. Past performance is no guarantee of future results.

Start early, accumulate more

31

COLL

EGE

COST

SFI

NA

NCI

AL

AID

SAV

ING

& IN

VES

TIN

GA

PPEN

DIX

COLL

EGE

MAT

TER

S

Performance pays

Even small increases in investment returns can make a big difference when it comes time to pay for college.

SEEKING HIGHER RETURNS

• Be an investor, not just a saver in low-yielding bank accounts.

• Stay invested for the long haul to avoid the risk of being out of markets during upswings.

• Reduce taxes to keep more of what you earn.

Source: J.P. Morgan Asset Management using The College Board 2015 Trends in College Pricing. This hypothetical assumes an investment of $100,000 over an 18-year period. Different assumptions will result in outcomes different from this example. Investment losses could affect the relative tax-deferred investing advantage. This hypothetical illustration is not indicative of any specific investment and does not reflect the impact of fees or expenses. Such costs would lower performance. Each investor should consider his or her current and anticipated investment horizon and income tax bracket when making an investment decision.

Investment growth over 18 yearsCalculations assume an initial investment of $100,000 at birth

$350,000

$300,000

$250,000

$200,000

$150,000

$100,00010 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

t$337,993

of $100,000covers a full year’s cost at

public college (in-state)

covers a full year’s cost at

private college

covers a full year’s cost at

Ivy League college

covers two full years’ cost at

private college

initial investment

Slightly higher returns can pay for a full year of college

+$21,485$240,662 +$44,772 +$70,004 +$97,3315.5%5.0% 6.0% 6.5% 7.0%

Difference of

$97,331

t$240,662

6.5% ANNUAL RETURN

6.0% ANNUAL RETURN

7.0% ANNUAL RETURN

5.5% ANNUAL RETURN

5.0% ANNUAL RETURN

32

COLL

EGE

COST

SFI

NA

NCI

AL

AID

SAV

ING

& IN

VES

TIN

GA

PPEN

DIX

COLL

EGE

MAT

TER

S

Invest more, pay less

Some savings vehicles, such as 529 plans, allow large contributions that can help you pay for much of college from your investment earnings instead of your pocket.

Source: College Board, 2015 Trends in College Pricing. Based on tuition, fees and room/board costs for 2015–2016 school year. Costs estimated to inflate 5% per year. This example is hypothetical and assumes a 6% annual rate of return and an annual lump-sum contribution of $18,749 over a 12-year period. This example does not represent the performance of any particular investment. Different assumptions will result in outcomes different from this example. Your results may be more or less than the figures shown. Investment losses could affect the relative tax-deferred investing advantage. Each investor should consider his or her current and anticipated investment horizon and income tax bracket when making an investment decision, as the illustration may not reflect these factors. These figures do not reflect any management fees or expenses that would be paid by a 529 plan participant. Such costs would lower performance.

$200,000$0 $100,000 $300,000

Average private college cost

$339,965

Lump-sum investment

Annual investments

Out-of-pocketpayment

INVESTMENT GROWTHOUT-OF-POCKET COST

Investing versus paying out of pocketAmounts needed to fund four years of private college in 12 years

$165,776

$232,952

$339,965

Save 31% on out-of-pocket costs

Save 0% on out-of-pocket costs

Save 51% on out-of-pocket costs

33

COLL

EGE

COST

SFI

NA

NCI

AL

AID

SAV

ING

& IN

VES

TIN

GA

PPEN

DIX

COLL

EGE

MAT

TER

S

Tax-effi cient investing

A tax-advantaged account, such as a 529 plan, has the potential to grow faster for college than a taxable investment earning the exact same returns.

$15,477 more

with a tax-free 529 plan

$90,000 $120,000$60,000$30,000$0

Taxableaccount

Tax-free529 plan

Lower taxes equal a larger college fundInvestment growth over 18 years2

1. Earnings on non-qualified withdrawals may be subject to federal income tax and a 10% federal penalty tax, as well as state and local income taxes.

2. J.P. Morgan Asset Management. Illustration assumes an initial $1,000 investment and monthly investments of $300 for 18 years. Chart also assumes an annual investment return of 6% and a federal tax rate of 28%. Investment losses could affect the relative tax-deferred investing advantage. This hypothetical illustration is not indicative of any specific investment and does not reflect the impact of fees or expenses. Each investor should consider his or her current and anticipated investment horizon and income tax bracket when making an investment decision, as the illustration may not reflect these factors. These figures do not reflect any management fees or expenses that would be paid by a 529 plan participant. Such costs would lower performance. The chart is shown for illustrative purposes only. Past performance is no guarantee of future results.

$103,666

$119,143

STATE TAX BENEFITS

• Many 529 plans offer state tax benefits in addition to federal tax-free investing.1 See the Appendix on page 50 for more information.

34

COLL

EGE

COST

SFI

NA

NCI

AL

AID

SAV

ING

& IN

VES

TIN

GA

PPEN

DIX

COLL

EGE

MAT

TER

S

Making college savings a family affair

Getting family, friends and students involved in college savings can increase the size of your account and reduce your share of the expenses.

TALK TO CHILDREN

• Over half (54%) of college savers have discussed education costs with children, compared to just 28% of non-savers.1

Don’t go it aloneParents expect only 5% of college costs to be paid with contributions

from grandparents, friends and family.1

1. Sallie Mae, How America Saves for College, 2015.2. J.P. Morgan Asset Management. This hypothetical example illustrates the future values of regular

monthly investments by the account owner and annual investment by other contributors over an 18-year period. Investment losses could affect the relative tax-deferred investing advantage. This hypothetical illustration is not indicative of any specific investment and does not reflect the impact of fees or expenses. Such costs would lower performance. Each investor should consider his or her current and anticipated investment horizon and income tax bracket when making an investment decision, as the illustration may not reflect these factors. A plan of regular investment cannot assure a profit or protect against a loss in a declining market. The chart is shown for illustrative purposes only. Past performance is no guarantee of future results.

More contributors create a larger college fundInvestment growth over 18 years2

$36,906

$72,264

$185,434

Family and friends $1,000 annually

Total

Parents $6,000 annually

Grandparents $2,500 annually

$294,604

5%

35

COLL

EGE

COST

SFI

NA

NCI

AL

AID

SAV

ING

& IN

VES

TIN

GA

PPEN

DIX

COLL

EGE

MAT

TER

S

Don’t pay for college with retirement funds

Every dollar withdrawn from 401(k)s and IRAs for college can mean several dollars less for retirement, due to years of lost investment earnings and compounding.

A DANGEROUS DECISION

Nearly one in three parents either plans to use or would consider using retirement

funds for college.1

How college withdrawals can jeopardize retirement security2

Pay 10% penalty if under age 59½3

Penalties

Financial aid

Withdrawal treated as student income

More drawbacks of using retirement funds for college

Taxes

Taxes due on amount withdrawn

1. Sallie Mae, How America Saves for College, 2015.2. J.P. Morgan Asset Management. This illustration assumes that assets would have remained in a tax-advantaged retirement account instead of being withdrawn for college, earning 6% annual investment

returns for 20 years. This example does not represent the performance of any particular investment. Different assumptions will result in outcomes different from this example. Your results may be more or less than the figures shown. Investment losses could affect the relative tax-deferred investing advantage. Each investor should consider his or her current and anticipated investment horizon and income tax bracket when making an investment decision, as the illustration may not reflect these factors. These figures do not reflect any management fees or expenses. Such costs would lower performance. Shown for illustrative purposes only. Past performance is no guarantee of future results.

3. Distributions from retirement accounts may not be subject to the 10% penalty if used for qualified higher education expenses. Refer to IRS Publication 970 or your 401(k) plan provider for details.

$10,000

$32,071

$25,000

$80,178

$50,000

$160,357

Amount withdrawn for college:

Retirement account reduced by:

36

COLL

EGE

COST

SFI

NA

NCI

AL

AID

SAV

ING

& IN

VES

TIN

GA

PPEN

DIX

COLL

EGE

MAT

TER

S

Staying diversifi ed over 18 years

Compare the best, worst and average annual returns for different investments over rolling 18-year periods.

WHY DIVERSIFY?

• A balanced portfolio delivered higher returns than bonds with lower volatility than stocks.

• Even in its worst 18-year period, the balanced portfolio outperformed average tuition infl ation.

• Even in its best 18-year period, short-term cash underperformed average tuition infl ation.

Source: Barclays Capital, FactSet, Robert Shiller, Strategas/Ibbotson, Federal Reserve, BLS, J.P. Morgan Asset Management. Rolling returns shown are based on calendar-year returns from 1978 to 2014. Data are as of 12/31/14. Past performance is not indicative of future results. Diversification does not guarantee investment returns and does not eliminate the risk of loss.

8%

16%

20%

6%

14%

18%

4%

12%

2%

10%

0%

Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual Average annual tuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflationtuition inflation

11.9%

10.9%

3.9%

7.0%

17.4%

14.8%

6.7%

7.2%7.9%

1.5%

18-year rolling returnsAverage annual returns, 1978–2014

Stocks

Bonds

Cash

50-50Portfolio

9.3%

12.2%

6.9%

AverageAverageAverageAverageAverageAverageAverageAverageAverage

Lowest Lowest Lowest Lowest Lowest Lowest Lowest returnreturnreturnreturnreturnreturnreturn

Highest Highest Highest Highest Highest Highest Highest Highest ReturnReturnReturnReturnReturnReturnReturn

37

COLL

EGE

COST

SFI

NA

NCI

AL

AID

SAV

ING

& IN

VES

TIN

GA

PPEN

DIX

COLL

EGE

MAT

TER

S

The power of diversifi cation

A more diversifi ed portfolio has historically provided higher returns with lower risk.

S&P 500

MSCI EAFE

Barclays Agg. 55%

15%

30%

Traditional portfolio

27%

22%

13%

9%

8%

8%8%

8%4%4%

S&P 500

Russell 2000

Barclays Agg.

MSCI EAFE

REIT

Equity Mkt. Neutral

MSCI EM

Commodities

Return

Standard Deviation

4.81%

10.74%

Return

Standard Deviation

6.19%

10.19%

More diversifi ed portfolio

Source: J.P. Morgan Asset Management. Indexes and weights of the traditional portfolio are as follows: U.S. stocks: 55% S&P 500, U.S. bonds: 30% Barclays Capital Aggregate, International stocks: 15% MSCI EAFE. Portfolio with 25% in alternatives is as follows: U.S. stocks: 22.2% S&P 500, 8.8% Russell 2000; International Stocks: 4.4% MSCI EM, 13.2% MSCI EAFE; U.S. Bonds: 26.5% Barclays Capital Aggregate; Alternatives: 8.3% CS/Tremont Equity Market Neutral, 8.3% DJ/UBS Commodities, 8.3% NAREIT Equity REIT Index. Return and standard deviation calculated using Morningstar Direct. Charts are shown for illustrative purposes only. Past returns are no guarantee of future results. Diversification does not guarantee investment returns and does not eliminate risk of loss. Data as of December 31, 2014.

Portfolio risks and returns2000-2014

38

COLL

EGE

COST

SFI

NA

NCI

AL

AID

SAV

ING

& IN

VES

TIN

GA

PPEN

DIX

COLL

EGE

MAT

TER

S

Asset allocation provided a smoother ride

A diversifi ed portfolio of many different asset classes fl uctuated less than any one on its own.

Cash

1.0%

AssetAlloc.13.3%

AssetAlloc.14.9%

REITs

25.9%

Volatil

ity

Annualized

FixedIncome

3.2%

Comdty.

20.5%

HighYield

12.8%

Small Cap

20.5%

DMEquity16.2%

EMEquity18.8%

Large Cap

16.2%

EMEquity–2.3%

Small Cap

38.8%

DMEquity23.3%

2013

REITs

2.9%

Cash

0.0%

FixedIncome–2.0%

HighYield7.3%

Large Cap

32.4%

Comdty.

–9.5%

EMEquity34.5%

EMEquity39.8%

EMEquity79.0%

REITs

35.1%

REITs

27.9%

REITs

8.3%

REITs

19.7%

FixedIncome

5.2%

Small Cap

26.9%

AssetAlloc.

-25.4%

HighYield3.1%

Comdty.

21.4%

Comdty.

16.2%

Comdty.

–35.6%

HighYield

59.4%

DMEquity14.0%

DMEquity26.9%

DMEquity11.6%

EMEquity18.6%

EMEquity32.6%

HighYield

19.6%

20052007

20092006

20102011

20122008

REITs

12.2%

REITs

–37.7%

REITs

–15.7%

Cash

1.8%

Cash

0.1%

Cash

4.8%

Cash

3.0%

Cash

0.1%

FixedIncome

6.5%

HighYield3.2%

Cash

0.1%

FixedIncome

7.8%

Large Cap

5.5%

Comdty.

18.9%

FixedIncome

2.4%

FixedIncome

4.3%

DMEquity8.2%

AssetAlloc.12.2%

DMEquity32.5%

EMEquity19.2%

EMEquity-53.2%

EMEquity–18.2%

HighYield3.6%

Small Cap

–1.6%

Small Cap

18.4%

Small Cap

–33.8%

DMEquity17.9%

Small Cap

–4.2%

REITs

28.0%

AssetAlloc.7.1%

Large Cap

4.9%

HighYield

13.7%

FixedIncome5.9%

Cash

0.1%

FixedIncome4.2%

HighYield

–26.9%

Large Cap

26.5%

HighYield

14.8%

AssetAlloc.–0.7%

Large Cap

16.0%

AssetAlloc.15.3%

AssetAlloc.8.1%

FixedIncome

7.0%

Comdty.

16.8%

Large Cap

2.1%

Small Cap

4.6%

Cash

4.8%

Small Cap

27.2%

Large Cap

15.1%

Small Cap

16.3%

AssetAlloc.13.3%

DMEquity–43.1%

DMEquity–11.7%

Comdty.

2.1%

Comdty.

–1.1%

AssetAlloc.25.0%

Comdty.

–13.3%

AssetAlloc.5.2%

DMEquity–4.5%

REITs

28.0%

FixedIncome6.0%

2014

Cash

0.0%

HighYield0.0%

EMEquity–1.8%

Small Cap

4.9%

Large Cap

13.7%

Comdty.

–17.0%

Large Cap

15.8%

Large Cap

–37.0%

Small Cap

7.8%

Cash

1.5%

EMEquity8.8%

HighYield8.0%

AssetAlloc.5.8%

DMEquity4.9%

FixedIncome

4.7%

Large Cap

7.7%

REITs

8.3%

Comdty.

–1.9%

Asset class performanceRanked in order of annual returns, 2005–14

Source: Barclays Capital, Bloomberg, FactSet, MSCI, NAREIT, Russell, Standard & Poor’s, J.P. Morgan Asset Management. Large cap: S&P 500, Small cap: Russell 2000, EM Equity: MSCI EME, DM Equity: MSCI EAFE, Comdty: Bloomberg Commodity Index, High Yield: Barclays Global HY Index, Fixed Income: Barclays Capital Aggregate, REITs: NAREIT Equity REIT Index. The “Asset Allocation” portfolio assumes the following weights: 25% in the S&P 500, 10% in the Russell 2000, 15% in the MSCI EAFE, 5% in the MSCI EME, 25% in the Barclays Capital Aggregate, 5% in the Barclays 1-3m Treasury, 5% in the Barclays Global High Yield Index, 5% in the Bloomberg Commodity Index and 5% in the NAREIT Equity REIT Index. Balanced portfolio assumes annual rebalancing. All data represents total return for stated period. Past performance is not indicative of future returns. Data are as of 9/30/15. Annualized 10-yr returns represent period of 12/31/04–12/31/14. Please see disclosure page at end for index definitions.

39

COLL

EGE

COST

SFI

NA

NCI

AL

AID

SAV

ING

& IN

VES

TIN

GA

PPEN

DIX

COLL

EGE

MAT

TER

S

College planning checklist

Set a goal

Review and adjustCreate your plan

What type of college should we consider?

What costs should I expect?

What is my family’s fi nancial outlook?

How much of total costs do I want to pay?

What can I afford to save?

What does my fi nancial advisor recommend?

Review plan annually

Make adjustments based on life changes

Compare and choose college savings options

Understand my risk tolerance

Get startedOpen an account and select investments

Set up a schedule of monthly contributions

APP

END

IX

College Planning Essentials: A comprehensive guide to saving and investing

AppendixSECTION 5

College Planning Essentials: A comprehensive guide to saving and investing

fafsa.ed.gov

fi naid.org

irs.govIRS Publication 970, Tax Benefi ts for Education

ed.gov/fi naid.html

collegeconfi dential.com

collegesavings.org savingforcollege.com

iefa.org

How to apply for federal fi nancial aid

Guide to grants, scholarships, loans and other aid

Guide to federal income tax benefi ts for education

Information from U.S. Department of Education

Resources to help pay for college

Information about 529 plans

Comprehensive guide to college funding

Aid for students studying in a foreign country

Parents and others can learn more about obtaining fi nancial aid for college through the following websites:

Financial aid resources

41

COLL

EGE

COST

SFI

NA

NCI

AL

AID

APP

END

IXSA

VIN

G &

INV

ESTI

NG

COLL

EGE

MAT

TER

S

Sources of fi nancial aid

U.S. federal government

TYPES OF FINANCIAL AID DETAILS

Grants and scholarships

Loans

Work study

Allows qualifi ed students to earn money for college expenses

In addition to aid from the U.S. Department of Education, scholarships and loan repayment may be available to qualifi ed students through additional government entities.

Grants and scholarships

May be available even if families aren’t eligible for federal aid

Example: New York offers a Math and Science Teaching Incentive Scholarship to eligible students in approved programs that lead to math or science teaching careers.

Grants and scholarshipsAid may be available for attending a particular college and/or studying specifi c majors.

Grants and scholarships

Private loans

Possible sources include charitable foundations, religious and community organizations, local businesses, ethnicity-based organizations, students’ and parents’ employers, and civic groups and professional associations related to a fi eld of study.

Tend to have higher interest rates and less fl exible repayment options than federal loans.

States

Colleges

Non-profi t or private organizations

Banks, credit unions or other lenders

Source: www.studentaid.ed.gov (U.S. Department of Education).

TYPES OF FINANCIAL AIDGrants and scholarships are free gifts that generally don’t have to be repaid. Grants are typically need-based while scholarships are merit-based. Loans must be paid back with interest.

42

COLL

EGE

COST

SFI

NA

NCI

AL

AID

APP

END

IXSA

VIN

G &

INV

ESTI

NG

COLL

EGE

MAT

TER

S

Financial aid: Types of applications

There are over 200 institutions that require students to submit the CSS/Financial Aid PROFILE in addition to the FAFSA.1 The PROFILE is an online application that is administered by the College Scholarship Service, the fi nancial aid division of the College Board. The PROFILE is used to determine students’ eligibility for need-based institutional scholarships, grants or loans and is a more detailed assessment of the student’s and parents’ income and assets when calculating EFC.

1. College Board, Participating Institutions and Programs.2. See financial aid office or net price calculator at your desired institution for more information about what is used to calculate awards.

FAFSACSS/FINANCIAL AID PROFILE2

Need-based institutional aid Need-based institutional aid

Standard, universal application

Required by every institution

Looks at assets and income at a high level and uses a standard EFC formula for every applicant.

College-specifi c application

Considers a deeper level of income and assets when calculating EFCApplicants may be asked to report additional assets or income such as home equity, business income and assets under a sibling’s name.

Required by over 200 institutions in addition to the FAFSAMajority of schools tend to be specialized,

highly selective or private schools.

43

COLL

EGE

COST

SFI

NA

NCI

AL

AID

APP

END

IXSA

VIN

G &

INV

ESTI

NG

COLL

EGE

MAT

TER

S

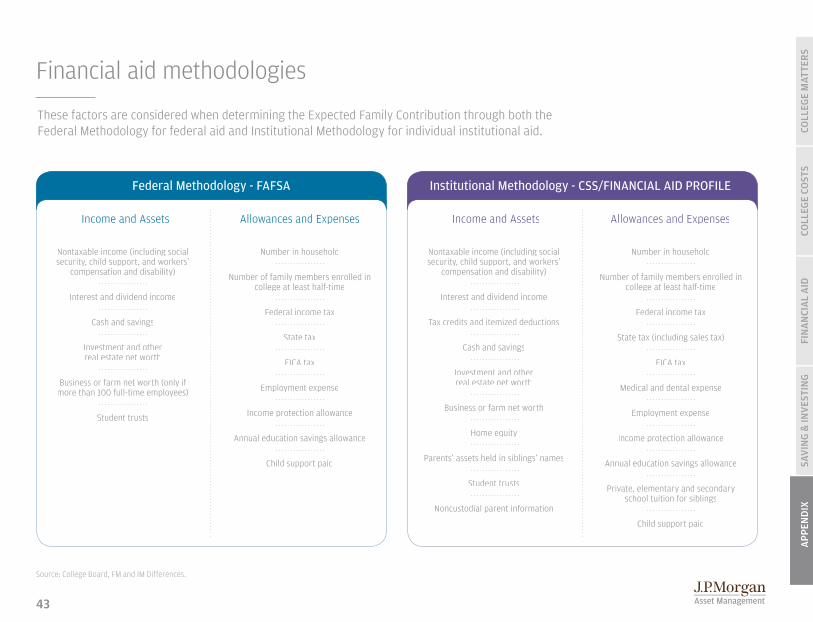

Financial aid methodologies

These factors are considered when determining the Expected Family Contribution through both the Federal Methodology for federal aid and Institutional Methodology for individual institutional aid.

Federal Methodology - FAFSA Institutional Methodology - CSS/FINANCIAL AID PROFILE

Income and Assets Income and AssetsAllowances and Expenses Allowances and Expenses

Nontaxable income (including social security, child support, and workers’

compensation and disability)

Nontaxable income (including social security, child support, and workers’

compensation and disability)

Number in household Number in household

Number of family members enrolled in college at least half-time

Number of family members enrolled in college at least half-time

Federal income tax Federal income tax

State tax State tax (including sales tax)

FICA tax FICA tax

Employment expense

Employment expense

Medical and dental expense

Income protection allowance

Income protection allowanceAnnual education savings allowance

Annual education savings allowance

Private, elementary and secondary school tuition for siblings

Child support paid

Child support paid

Interest and dividend income Interest and dividend income

Tax credits and itemized deductionsCash and savings

Cash and savingsInvestment and other real estate net worth

Investment and other real estate net worthBusiness or farm net worth (only if

more than 100 full-time employees)

Business or farm net worth

Home equity

Parents’ assets held in siblings’ names

Noncustodial parent information

Student trusts

Student trusts

Source: College Board, FM and IM Differences.

44

COLL

EGE

COST

SFI

NA

NCI

AL

AID

APP

END

IXSA

VIN

G &

INV

ESTI

NG

COLL

EGE

MAT

TER

S

DETAILS ANNUAL AWARD LIMIT1

Federal student aid: A sample of grant programs

Awarded to undergraduate students with exceptional fi nancial need

Federal Pell Grant recipients receive priority

Not all colleges participate

Funds depend on availability at the college; apply by college’s deadline

For undergraduate, post-baccalaureate or graduate students who are taking or will be taking coursework necessary to become elementary or secondary teachers

Must attend a participating college and meet certain academic achievement requirements

Must agree to serve for a minimum of four years as a full-time teacher in a high-need fi eld, serving low-income students

Failure to complete the teaching service commitment results in grant funds being converted to a Federal Direct Unsubsidized Stafford Loan that must be repaid

Non-need based, this grant is available to any undergraduate student who is not eligible for the Pell Grant and whose parent or guardian died as a result of performing military service in Iraq or Afghanistan after the events of 9/11

Must have been less than 24 years old or enrolled at least part-time at the time of the parent’s or guardian’s death

Generally awarded to undergraduate students in fi nancial need

2015–16 award year

Federal Supplemental Educational Opportunity Grant (FSEOG)

Federal Pell Grant

Teacher Education Assistance for College and Higher Education (TEACH) Grant

Iraq and Afghanistan Service Grant

1. Awards are subject to availability of funds, and recipients must meet certain eligibility requirements. This is for informational purposes only.

up toup to

$5,775$5,775up toup to

$5,775up toup to

up toup to

$5,775$5,775up toup to

$5,775up toup to

up toup to

$4,000$4,000up toup to

$4,000up toup to

up toup to

$4,000$4,000up toup to

$4,000up toup to

45

COLL

EGE

COST

SFI

NA

NCI

AL

AID

APP

END

IXSA

VIN

G &

INV

ESTI

NG

COLL

EGE

MAT

TER

S

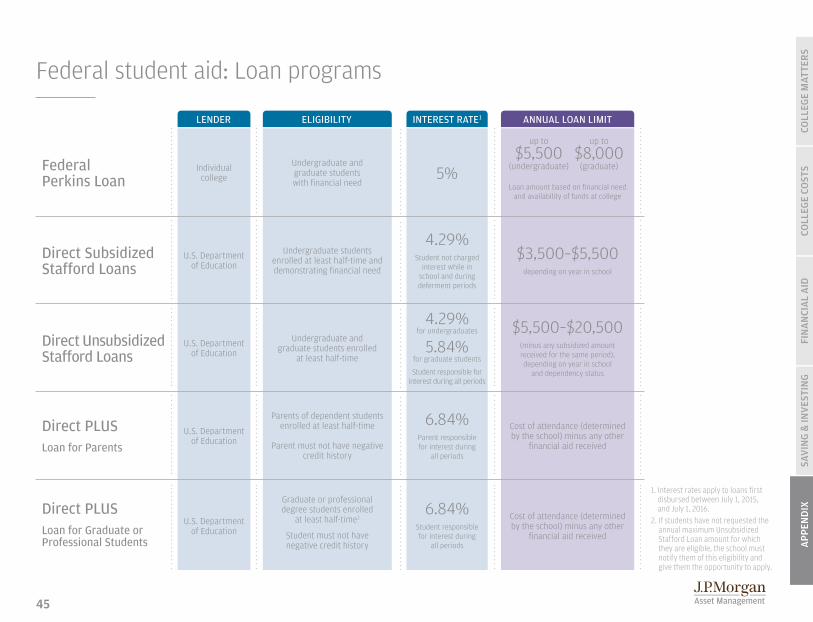

Loan amount based on fi nancial need and availability of funds at college

up to

$5,500(undergraduate)

up to

$8,000(graduate)

$3,500–$5,500 depending on year in school

$5,500–$20,500 (minus any subsidized amount received for the same period), depending on year in school

and dependency status

Cost of attendance (determined by the school) minus any other

fi nancial aid received

Cost of attendance (determined by the school) minus any other

fi nancial aid received

5%

4.29%Student not charged

interest while in school and during deferment periods

4.29%for undergraduates

5.84%for graduate students

Student responsible for interest during all periods

6.84%Student responsible for interest during

all periods

6.84%Parent responsible for interest during

all periods

Federal student aid: Loan programs

FederalPerkins Loan

ELIGIBILITY INTEREST RATE1LENDER ANNUAL LOAN LIMIT

Undergraduate and graduate students with fi nancial need

Individualcollege

Undergraduate students enrolled at least half-time and demonstrating fi nancial need

U.S. Department of Education

Undergraduate and graduate students enrolled

at least half-time

U.S. Department of Education

Parents of dependent students enrolled at least half-time

Parent must not have negative credit history

Graduate or professional degree students enrolled

at least half-time2

Student must not have negative credit history

U.S. Department of Education

U.S. Department of Education

Direct Subsidized Stafford Loans

Direct Unsubsidized Stafford Loans

1. Interest rates apply to loans first disbursed between July 1, 2015, and July 1, 2016.

2. If students have not requested the annual maximum Unsubsidized Stafford Loan amount for which they are eligible, the school must notify them of this eligibility and give them the opportunity to apply.

Direct PLUSLoan for Parents

Direct PLUSLoan for Graduate or Professional Students

46

COLL

EGE

COST

SFI

NA

NCI

AL

AID

APP

END

IXSA

VIN

G &

INV

ESTI

NG

COLL

EGE

MAT

TER

S

College-related tax breaks¹

1. Must meet certain eligibility requirements. Information as of August 2015. Please consult a tax advisor for additional details.2. Taxpayers cannot claim both credits for the same student in the same year.3. See page 50 for more information.

Some states allow contributions to a 529 college savings plan to be deductible for state income tax purposes. Rules and deductible amounts vary by state.

The maximum deduction is

$2,500 per year.

• The American Opportunity Credit allows eligible taxpayers to claim up to $2,500 in qualifi ed expenses per student per year for the fi rst four years of college.

• The Lifetime Learning Credit allows eligible taxpayers to claim up to $2,000 in qualifi ed expenses per student per year for an unlimited number of years of college.

Contributions to 529 plans, Coverdell Education Savings Accounts, qualifying U.S. savings bonds and other college accounts are not typically deductible from federal taxes. However, they grow on a tax-deferred basis, and withdrawals are generally tax free for qualifi ed expenses.

You can claim a federal tax deduction forthe interest paid on student loans taken out for yourself, your spouse or your dependents. This benefi t applies to all loans used to pay higher education expenses, not just federal student loans.

• You can deduct up to $4,000 for tuition and fees on your tax return. To qualify, your income cannot be over $80,000 if single and $160,000 if married.

• This is available for an unlimited number of years for higher education, and the student must be enrolled in at least one class at an eligible school.

Federal tax credits2 Student loan interest deduction Tuition and fees deduction

Tax-deferred college savings plans State tax deductions3

47

COLL

EGE

COST

SFI

NA

NCI

AL

AID

APP

END

IXSA

VIN

G &

INV

ESTI

NG

COLL

EGE

MAT

TER

S

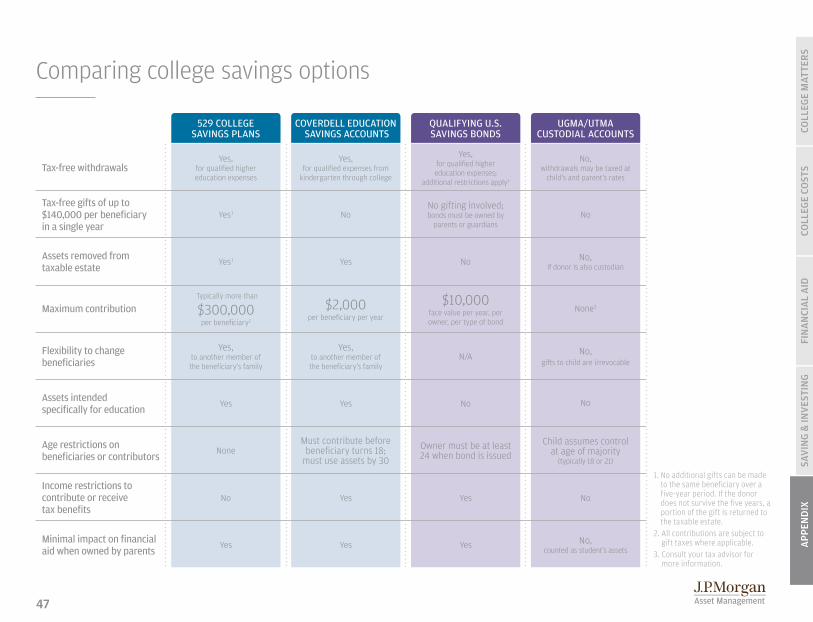

Yes

Yes

Yes, to another member of the benefi ciary’s family

Must contribute before benefi ciary turns 18;

must use assets by 30

COVERDELL EDUCATION SAVINGS ACCOUNTS

Yes, for qualifi ed expenses from

kindergarten through college

No

Yes

Yes

No

Yes

Yes, to another member of the benefi ciary’s family

None

529 COLLEGE SAVINGS PLANS

Yes, for qualifi ed higher education expenses

Yes1

Yes1

Yes

Typically more than

$300,000per benefi ciary2

$2,000per benefi ciary per year

Yes

Yes

N/A

Owner must be at least 24 when bond is issued

QUALIFYING U.S. SAVINGS BONDS

Yes, for qualifi ed higher education expenses;

additional restrictions apply3

No gifting involved; bonds must be owned by

parents or guardians

No

No

No

No, counted as student’s assets

No

UGMA/UTMACUSTODIAL ACCOUNTS

No, withdrawals may be taxed at

child’s and parent’s rates

No, if donor is also custodian

None3

Child assumes control at age of majority

(typically 18 or 21)

Comparing college savings options

Tax-free gifts of up to $140,000 per benefi ciary in a single year

Assets intended specifi cally for education

Maximum contribution

Income restrictions to contribute or receive tax benefi ts

Minimal impact on fi nancial aid when owned by parents

Tax-free withdrawals

Flexibility to change benefi ciaries

Assets removed from taxable estate

Age restrictions on benefi ciaries or contributors

1. No additional gifts can be made to the same beneficiary over a five-year period. If the donor does not survive the five years, a portion of the gift is returned to the taxable estate.

2. All contributions are subject to gift taxes where applicable.

3. Consult your tax advisor for more information.

$10,000face value per year, per owner, per type of bond