combating financial fraud “the perfect … financial fraud “the perfect storm” plenary 2:...

TRANSCRIPT

Labuan Conference 2016

COMBATING FINANCIAL FRAUD

“The Perfect Storm”

Plenary 2: Transformation of International Financial Centres – Legislation & Governance

Presentation by - Lim Hsin Ying, Deputy Director, FIU 1, FIED

1

Labuan Conference 2016

LEARNING OBJECTIVES

Understand role of RIs in prevention of money

laundering (ML), terrorism financing (TF) & proliferation financing (PF) Implementation of reporting obligations as

effective deterrence against being made a conduit Global Scrutiny on Offshore Financial Centres and

Intermediaries

2

Labuan Conference 2016 3

Widening Income Gap + Tightening Budgets, Fiscal Conditions + Despots, Dictators, Drug Lords…Tax Dodgers + Profiteering, Unethical Intermediaries + Boundless Internet, Activist Hackers, Whistle-blowers

= LEAKS!

Source: www.forbes.com

YIKES! …as if the hackers aren’t bad

enough, there’s talk of establishing

public registries of

corporate ownership

now!

Labuan Conference 2016 4

Traditional safe havens under siege…

Date Case Details Nov. 2014

Lux Leaks

• Over 28,000 pages of documents (4.4 GB) on tax rulings between Luxembourg tax authorities and more than 340 companies worldwide aiming to reduce their tax payments, with 548 tax rulings from 2002 to 2010 leaked to the public.

• Impact: Spotlight on tax avoidance schemes in Luxembourg and other tax havens, and complicity of consultancy firms. Contributed to implementation of measures aimed at reducing tax dumping and regulating tax avoidance schemes beneficial to MNCs.

Feb. 2015

Swiss Leaks

• Over 3.3 GB of secret documents relating to accounts worth over $100 billion purportedly maintained for criminals, traffickers, tax dodgers, politicians and celebrities by HSBC Private Bank (Suisse)

• Key Findings: Many of the client accounts were held in the name of companies located in offshore tax havens such as BVI, Panama, Niue etc., rather than by the individuals who owned the money; thousands more used de-identified numbered accounts / aliases to obscure identities of ultimate beneficial owners

April 2016

Panama Leaks

• Over 11.4 million files, 2.6 TB of secret documents covering a period of almost 40 years leaked from internal database of Mossack Fonseca & Co., a Panama-based law firm

• Links up direct and indirect offshore holdings of some 140 current and former world leaders, billionaires, former spy chiefs, relatives of politicians, public officials

• Key Findings: o Use of anonymous shell companies whose real owners hide behind hired “nominees” serving as

“getaway cars” for tax dodgers, launderers and crooked public officials o Professional Advisers - Unwitting agent or accomplice? Major banks referenced by ICIJ responsible for

data creation of over 15,000 companies in BVI, Panama and other offshore locations.

Sources: www.icij.org; www.wsj.com; www.economist.com; www.forbes.com

Labuan Conference 2016 5

AUSTRAC Case Study: Complex tax avoidance scheme hid funds in Samoa & New Zealand

• Individual A and B were family members who owned and controlled a group of Australia-based companies (motor vehicle repairs and sale of automotive products in Australia

• Arrangement 1 – International transfers made to an offshore superannuation fund and rapid return of these funds to Australia

Company 1 subsequently claimed deductions for the AUD200,000 offshore superannuation contribution in its tax returns and was assessed as liable for less tax than it should have been >> Deductions later disallowed and deemed not deductible

Labuan Conference 2016 6

AUSTRAC Case Study: Complex tax avoidance scheme hid funds in Samoa & New Zealand

• Arrangement 2 (Years 1 to 10 of the scheme) – On-going international transfers of funds under a fictitious loan arrangement over ten years.

Complex ‘round robin’ tax avoidance arrangement aimed at disguising the fund movements as legitimate transactions associated with the loan. In reality, any funds sent overseas ultimately returned to the original beneficiary, either Company 1 or other related companies in Australia

Labuan Conference 2016 7

AUSTRAC Case Study: Complex tax avoidance scheme hid funds in Samoa & New Zealand

• Arrangement 3 (Years 11 to 10 of the scheme) – Transfer of loan arrangement to another Australian company when the original company went into liquidation.

i. Company 1 changed its name and subsequently went into liquidation, forcing the Australian Taxation Office (ATO) to write-off a tax debt of AUD800,000 which had accrued on the income tax account of the company.

ii. The ‘fictitious’ loan liability for Company 1 transferred to Company 2, which was incorporated in Australia and associated with Company 1 and Individuals A and B. Loan liability approximately AUD3 million at the time.

iii. Company 2 continued to utilize tax avoidance arrangement by making interest payments on the loan to the Samoa-based private bank via its subsidiary with a bank account in New Zealand. Upon receipt of these ‘interest-payment’, the bank’s subsidiary subsequently transferred funds into Company 2’s bank accounts in Australia, describing them these transfers as ‘loan draw downs’.

iv. Company 2 claimed the funds received as ‘loan draw downs’ were lent to companies in the Australian group of companies by way of interest-free loans.

Labuan Conference 2016 8

AUSTRAC Case Study: Complex tax avoidance scheme hid funds in Samoa & New Zealand

• Arrangement 4 (Years 15 to 16 of the scheme) – Introduction of an Australian charitable organization, which was unrelated to the main group of companies, to facilitate transfer of funds between the bank’s New Zealand subsidiary and the Australian group of companies

Company 2 subsequently claimed deductions for interest expenses and fees paid to the Samoa-based private bank, hence reducing its taxable income and was assessed as liable for less tax than it should have been, thereby avoiding its tax obligations.

Labuan Conference 2016

Reporting Institutions are the first line of defence

Criminals & Criminal Proceeds

Financial Institutions

Law Enforcement

Agencies (LEAs)

Non-bank FIs

DNFBPs

• Obscure ultimate BOs

• Cleansing of illicit proceeds through intermediaries

FIs - Supervisory authorities

LFSA, BNM, SC

Financial Intelligence Unit

FIED, BNM Submit CTRs &STRs

Collect, analyse,

disseminate financial intel

Feedback on effectiveness of financial

intel.

Prevent on-boarding of criminals through effective risk profiling, CDD, verification and transaction monitoring

Early detection of illicit/suspicious activities and prompt reporting to FIU

Monitor & enforce AML/CTF

requirements

AML/CFT PREVENTIVE MEASURES • ML/TF Risk Assessment, Client Risk Profiling, CDD, Enhanced CDD & On-going Monitoring of Clients & Transactions • Promptly Detect & Report Suspicious Transactions, CTRs • Effective Sanctions Monitoring and Implementation of Sanctions Regime

DNFBPs - Supervisory authorities

BNM in collab. with Ministries

& SROs

1 2 3

4 5

9

Labuan Conference 2016 10

Relevant AML/CFT Act and Guidelines

AML/CFT Guidelines for Labuan RIs are imposed pursuant to the AMLA 2001 and LFSAA 1996

Labuan FSA serves as the AML/CFT regulator and supervisor of Labuan RIs, and have issued AML/CFT Guidelines for RIs licensed to operate in the following sectors: o Banking o Capital Markets & Other Businesses o Insurance & Takaful o Trust Company

For all other DNFBPs that operate in Labuan i.e. gaming, lawyers, real estate, accountants, dealers in precious metals and stones, these RIs are subject to BNM’s Sector 5 AML/CFT Policy Document for DNFBPs and come under the AML/CFT supervision of FIED, BNM.

Relevant AML/CFT Law, Regulations & Guidelines for Labuan RIs

International Expectations on Implementation of AML/CFT obligations by Ris

Immediate Outcome 4 from FATF Methodology 2013 FIs & DNFBPs adequately apply AML/CFT preventive measures commensurate with their risks, and report suspicious transactions, with RIs expected to:

• Understand the nature and level of ML/TF risks;

• Develop and apply AML/CFT policies, internal controls and programmes to adequately mitigate identified risks;

• Apply appropriate CDD measures to identify and verify customers and BOs and conduct ongoing monitoring;

• Adequately detect and report suspicious transactions; and

• Comply with other AML/CFT requirements.

www.labuanibfc.com/guideline-main/2230/guideline-main.html

amlcft.bnm.gov.my/AMLCFT07.html

Labuan Conference 2016 11

Consequences of Non-Compliance

1. Enforcement action can be taken against a reporting institution and/or on individual directors, officers and employees for serious non-compliance with AML/CFT requirements;

2. Penalties upon breach of AMLA 2001 include:

• General Offence (section 86) – Fine not exceeding RM1.0 million e.g. for failure to conduct CDD and failure to adopt, develop and implement AML/CFT compliance programme;

• Lapse in Record Keeping – Fine not exceeding RM3.0 million or imprisonment for a term not exceeding five (5) years or both

• Opening Account in False Name – Fine not exceeding RM3.0 million or imprisonment for a term not exceeding five (5) year or both

Labuan Conference 2016 12

All countries are expected to comply with the international standards

UN Conventions and Security Council Resolutions

Financial Action Task Force (FATF), Headquartered in Paris Malaysia Accepted as FATF Member Country in February 2016

All countries are members of a FRSB (except DPRK, Iran - Observer in EAG)

Vienna Convention Palermo Convention

Security Council Resolution 1267 and its Successors

Security Council Resolution 1373

International Convention for the Suppression of the Financing of Terrorism

FATF serves as Secretariat; Issues & Ensures compliance by jurisdictions to 40 Recommendations & Technical Compliance / Effectiveness Methodology

APG (M’sia also Member) MENAFATF GIABA CFATF MONEYVAL GAFISUD EAG

Implementation by FATF-Styled Regional Bodies (FSRBs)

Principles from these Resolutions embedded in FATF Recommendations & Methodology

Labuan Conference 2016 13

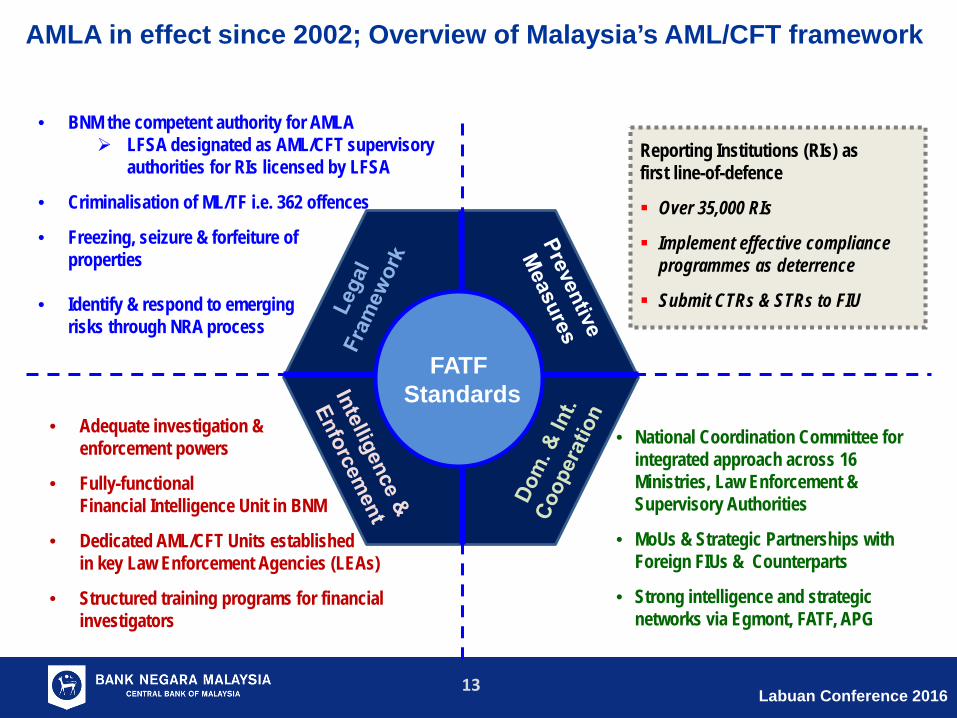

AMLA in effect since 2002; Overview of Malaysia’s AML/CFT framework

FATF Standards

• BNM the competent authority for AMLA LFSA designated as AML/CFT supervisory

authorities for RIs licensed by LFSA

• Criminalisation of ML/TF i.e. 362 offences

• Freezing, seizure & forfeiture of properties

• Identify & respond to emerging risks through NRA process

• Adequate investigation & enforcement powers

• Fully-functional Financial Intelligence Unit in BNM

• Dedicated AML/CFT Units established in key Law Enforcement Agencies (LEAs)

• Structured training programs for financial investigators

• National Coordination Committee for integrated approach across 16 Ministries, Law Enforcement & Supervisory Authorities

• MoUs & Strategic Partnerships with Foreign FIUs & Counterparts

• Strong intelligence and strategic networks via Egmont, FATF, APG

Reporting Institutions (RIs) as first line-of-defence

Over 35,000 RIs

Implement effective compliance programmes as deterrence

Submit CTRs & STRs to FIU

Labuan Conference 2016 14

Key Findings from Mutual Evaluation Exercise 2014

• On-site visit by APG & FATF Assessors from 13/11 to 25/11/2014;

• Assessment made based on Technical Compliance and Effectiveness of Malaysia’s AML/CFT regime in line with FATF Recommendations & Methodology;

• Outcome – Malaysia has achieved high levels of technical compliance. But, significant improvements needed in: a. Effectiveness of international cooperation for

cross-border crime prevention and ML/TF investigations;

b. Conduct of parallel ML/TF investigations and prosecution;

c. Identification and assessment of foreign-sourced threats, institutional vulnerabilities, TF, inter-connectedness of organized crimes and other categories of crime on Malaysia’s National ML/TF Risk Assessment; and

d. Improved understanding on ML/TF risks and adoption of a risk-based approach in implementation of AML/CFT preventive measures by onshore and offshore FIs and DNFBPs.

Labuan Conference 2016

Thank You Please visit BNM’s AML/CFT Microsite

for more information.

http://amlcft.bnm.gov.my

15