commercial - blominvestbank.com invest... · 2 commercial banking in the mena region chairman’s...

TRANSCRIPT

2

Commercial Banking in the MENA Region

Chairman’s letter

Dear Clients,

It is with pleasure that I present to you the first in a series of new research products BLOMINVEST Bank will publish as we continue our expansion inthe Middle East.

Our region is poised for an increasingly relevant, impactful, and exciting role on the world stage. Further, growing interdependence between MENAnations calls for a better understanding of both our existing similarities and differences. In this context, BLOMINVEST Bank is launching a series ofresearch papers that comprehensively detail economic and financial issues in the MENA region. In parallel, we shall work to provide both countryspecific reports and other focused studies.

At BLOMINVEST, we have a strong commitment to providing our clients with the context to derive a complete and timely understanding of marketevents. Our existing research portfolio, which shall now be supplemented by these research products on a monthly basis, is a demonstration of thiscommitment. As you know, BLOMINVEST has undertaken a significant expansion and now serves clients across Egypt, Jordan, Dubai, Abu Dhabi,Sharjah, Saudi Arabia, Syria, and Qatar. As we continue to broaden this presence, we shall augment our efforts with additional research and support.

In the midst of the current global financial turmoil, we have chosen to launch this report on commercial banking. As a critical sector that is drivinggrowth in economies across the MENA region, and one which is being buffeted by an international crisis, commercial banking is highly relevant to theimmediate and near term future of MENA countries.

I look forward to sharing additional reports in the future and trust that you will find this paper insightful. I encourage you to contact the researchdepartment for additional information and to assist you with any queries that you may have.

Best Regards,

Saad Azhari

3

Commercial Banking in the MENA Region

For your queries

Research Department

Marwan Mikhael Head of Research [email protected] Tel: +961 1 737 247 Fax: +961 1 737 414

Alexandre Mouradian Deputy Head of Research [email protected] Tel: +961 1 743 300 Ext: 1414 Fax: +961 1 737 414

Cynthia Zeilah Analyst [email protected] Tel: +961 1 743 300 Ext: 1413 Fax: +961 1 737 414

Rebecca Nakhoul Analyst [email protected] Tel: +961 1 743 300 Ext: 1418 Fax: +961 1 737 414

Yasmina Merhi [email protected]: +961 1 743 300 Ext: 1410

Fax: +961 1 737 414

Jean Claude Cherfane Analyst [email protected]

Tel: +961 1 743 300 Ext: 1416 Fax: +961 1 737 414

Research Department [email protected] Tel: +961 1 747 802 +961 1 747 812 Fax: +961 1 737414

4

Commercial Banking in the MENA Region

Table of Contents

Chairman’s letter .......................................................................................................................................................... 2

For your queries ........................................................................................................................................................... 3

Table of Contents ......................................................................................................................................................... 4

Executive Summary ...................................................................................................................................................... 6

1 Global Commercial Banking Overview..................................................................................................................... 8

1.1 Recent Central Bank and Government actions .............................................................................................................. 92 Regional Overview – Middle East and North Africa ................................................................................................11

2.1 Economic Overview..................................................................................................................................................... 112.1.1 Comparative Economic Landscape ....................................................................................................................... 13

2.2 Banking Industry Overview ......................................................................................................................................... 142.2.1 Banking Industry Drivers....................................................................................................................................... 142.2.2 Performance Indicators......................................................................................................................................... 15

2.3 Market Dynamics and Industry Structure.................................................................................................................... 182.4 Competitive landscape................................................................................................................................................ 20

2.4.1 Metrics for listed banks in the region ................................................................................................................... 202.4.2 Multiples Comparison ........................................................................................................................................... 22

2.5 Recent Developments in the region ............................................................................................................................ 222.5.1 Impact of the Economic crisis in the MENA region ............................................................................................... 242.5.2 Recent projects hit by the crisis............................................................................................................................. 242.5.3 Direct Impact – Write downs in the region ........................................................................................................... 242.5.4 Government moves to face the credit crunch....................................................................................................... 24

3 Country wise Commercial Banking Overview .........................................................................................................26

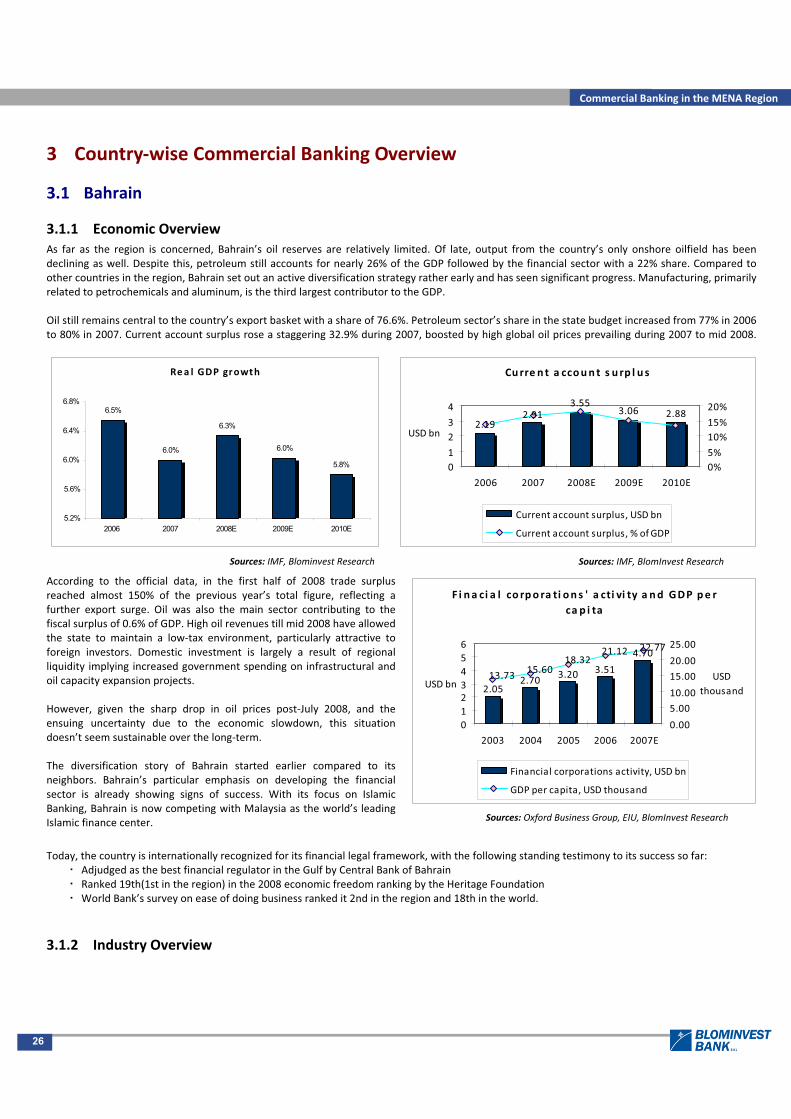

3.1 Bahrain ....................................................................................................................................................................... 263.1.1 Economic Overview............................................................................................................................................... 263.1.2 Industry Overview ................................................................................................................................................. 26

3.2 Egypt ........................................................................................................................................................................... 283.2.1 Economic Overview............................................................................................................................................... 283.2.2 Industry Overview ................................................................................................................................................. 29

3.3 Jordan ......................................................................................................................................................................... 293.3.1 Economic Overview............................................................................................................................................... 293.3.2 Industry Overview ................................................................................................................................................. 30

3.4 Kuwait......................................................................................................................................................................... 323.4.1 Economic Overview............................................................................................................................................... 323.4.2 Industry Overview ................................................................................................................................................. 32

3.5 Lebanon ...................................................................................................................................................................... 343.5.1 Economic Overview............................................................................................................................................... 343.5.2 Industry Overview ................................................................................................................................................. 34

3.6 Oman .......................................................................................................................................................................... 353.6.1 Economic Overview............................................................................................................................................... 353.6.2 Industry Overview ................................................................................................................................................. 36

3.7 Qatar........................................................................................................................................................................... 373.7.1 Economic Overview............................................................................................................................................... 373.7.2 Industry Overview ................................................................................................................................................. 38

3.8 Saudi Arabia................................................................................................................................................................ 403.8.1 Economic Overview............................................................................................................................................... 40

5

Commercial Banking in the MENA Region

3.8.2 Industry Overview ................................................................................................................................................. 403.9 United Arab Emirates .................................................................................................................................................. 42

3.9.1 Economic Overview............................................................................................................................................... 423.9.2 Industry Overview ................................................................................................................................................. 43

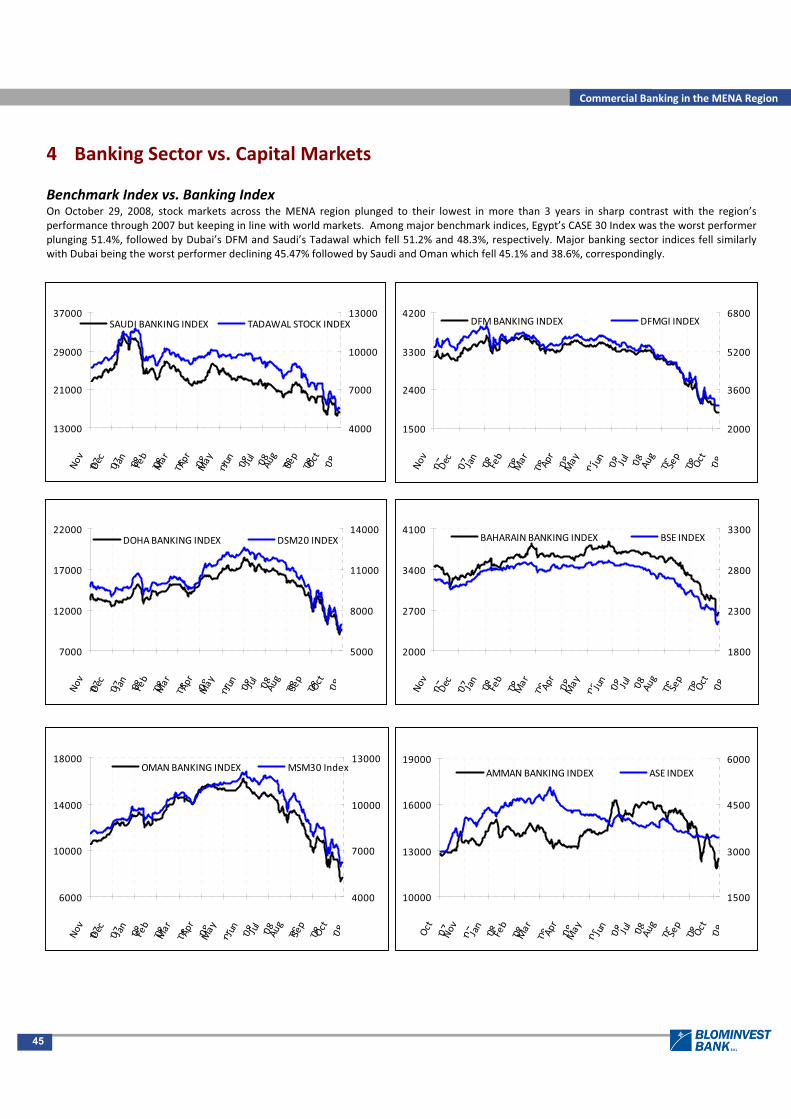

4 Banking Sector vs. Capital Markets ........................................................................................................................45

5 Opportunities and Challenges ................................................................................................................................46

5.1 Penetration of Insurance............................................................................................................................................. 465.2 Microfinance ............................................................................................................................................................... 465.3 Remittances ................................................................................................................................................................ 475.4 Small and Medium Enterprises.................................................................................................................................... 475.5 Internet based banking services .................................................................................................................................. 485.6 Continuation of the reform process ............................................................................................................................ 495.7 Political and economic uncertainties........................................................................................................................... 495.8 Islamic Banking ........................................................................................................................................................... 495.9 Banking infrastructure and Risk Management ............................................................................................................ 50

6 Future Outlook ......................................................................................................................................................51

7 Appendix ...............................................................................................................................................................54

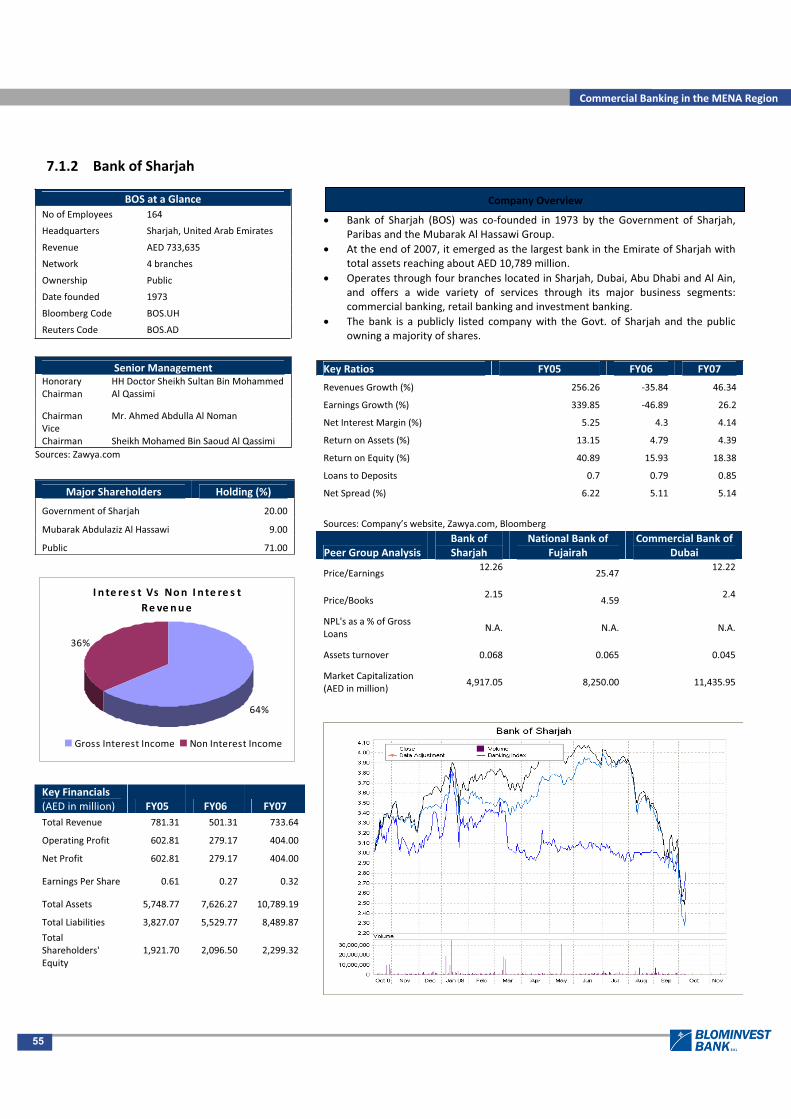

7.1 Appendix 1 Major Banking players in the region ....................................................................................................... 547.1.1 Bank Muscat ......................................................................................................................................................... 547.1.2 Bank of Sharjah..................................................................................................................................................... 557.1.3 Banque Saudi Fransi.............................................................................................................................................. 567.1.4 National Bank of Bahrain...................................................................................................................................... 577.1.5 Ahli United Bank ................................................................................................................................................... 587.1.6 Commercial International Bank (Egypt)................................................................................................................ 597.1.7 Societe Arabe Internationale De Banque .............................................................................................................. 607.1.8 Arab Bank ............................................................................................................................................................. 617.1.9 Jordan Kuwait Bank .............................................................................................................................................. 627.1.10 National Bank of Kuwait ..................................................................................................................................... 637.1.11 Commercial Bank of Kuwait................................................................................................................................ 647.1.12 Bank Audi SAL ..................................................................................................................................................... 657.1.13 BLOM Bank ......................................................................................................................................................... 667.1.14 Commercial Bank of Qatar.................................................................................................................................. 677.1.15 National Bank of Fujairah ................................................................................................................................... 687.1.16 National Bank of Oman....................................................................................................................................... 697.1.17 Qatar National Bank ........................................................................................................................................... 707.1.18 Riyad Bank .......................................................................................................................................................... 71

7.2 Appendix 2 – Acronyms............................................................................................................................................... 727.3 ............................................................................................................................................................................................ 737.4 ............................................................................................................................................................................................ 73

6

Commercial Banking in the MENA Region

Executive Summary

The Middle East and North Africa (MENA) region accommodates a diversity of people, economies and resources. Religion is the most common of themany threads that connect the region, but from an economic standpoint, the area can be broadly categorized into two main subgroups. On one handare the OPEC member countries like Saudi Arabia, UAE, and Kuwait which together hold a major chunk of the total world’s oil reserves. On the otherhand, nations such as Lebanon and Jordan are relatively scarce in oil or gas, making services and real estate the major contributors to GDP. Betweenthe two is Egypt, where the largest share of GDP comes from gas, and yet is not sufficient to join the category of resource rich nations. Giveneconomic and commodity cycles, there are times of plenty in the region and times of relative hardship. GDP growth for the region is forecastedbetween 5 6% and is expected to remain healthy despite the dampening effect of recent lower oil prices and the global economic slowdown.

Another clear result that emerges from the distribution of natural resources across the region is the linkage and interdependence between differentgroups of countries. The availability of oil driven cash flows acts as a strong intra regional development and investment opportunity. This is supportedby large populations in some countries and lesser populations in others. This diversity also forms the basis of people moving across the region andultimately resulting in a redistribution of wealth across the region.

The strong cash flows into the region provide opportunities for long term growth and trade development within the region. These are the majordrivers of a thriving commercial banking industry coupled with strong banking regulation. The commercial banking industry as in most other regions iscentrally regulated by the country’s central banks and/or the monetary authorities. Certain steps have been taken to arrest the impact of the crisisand continue the momentum built till mid 2008. Apart from the regulator’s role, some other factors as follows, have helped mitigate the impact ofthe global crisis on the banking system:(i) a not very expansive focus of the commercial banks in the region,(ii) high growth forecasts and therefore vast banking opportunities in the region,(iii) the industry as a whole still in evolving stage with minimal presence of sophisticated instruments like derivatives,(iv) the Islamic banking structure not yet comfortable with derivatives and similar products.

Religion plays an important role in the region and in fact has helped develop two different banking methodologies, the conventional system and theIslamic system. The latter however is still relatively new and continues to evolve further. It remains to be seen though how the two coexist in themarket as independent commercial systems geared towards economic profit and growth. The region is clearly aware of the need for world classbanking supervision, whether it covers Conventional or Islamic banking, and Bahrain is a good example of such thought and practice. The duality ofConventional and Islamic banking can only in the long run complement each other and be beneficial to the region.

High global oil prices during the first half of 2008 have helped the oil rich countries shore up handsome surplus which is being channeled into largescale developmental projects initiated by the governments. Extensive reforms undertaken by the regional governments and a strategy of activelydiversifying the economies away from oil is pumping capital to develop other sectors like manufacturing and financial services. The region has seentrade tariffs coming down from 20% in 2000 to 13% in 2007. With many countries now joining the World Trade Organization, it is only a matter oftime that non trade barriers and logistics will move favorably.

The industry should remain resilient to the global crisis due to the relatively strong assets compared to other developed countries. The oil richcountries withstand the global slowdown with relative ease, though at the cost of slowing down development activities. However, the region has seenhigh levels of construction activity fuelled by easy borrowing, and these ventures are likely to feel the impact. This in turn will lead to a trickle downeffect on the financiers, service providers and employees related to this business.

The banking system will benefit from the economic slowdown in many ways. There will be a period to look back, consolidate and learn many lessonsfrom this current crisis for bankers, regulators and borrowers alike.

The banking industry in the region has much to look forward to, despite the global turmoil. The primary factors that should spur future growth arefavorable demographics and low banking penetration. Most countries have large populations in the employable age of 15 to 60 years. Creation ofspecial economic zones like the six cities in Saudi Arabia, the finance centers in Qatar and Bahrain are expected to create opportunities foremployment. Moreover, the movement of expatriates will also further demand and credit growth. The penetration of banking still remains low in theregion. While part of this is due to the industry’s stage of evolution, part of it is because of an inclination towards branch based banking. Penetrationof internet based services is low as well, with most local banks only following initiatives taken by international players.

As the industry matures and the financial sector develops, need for insurance is likely to rise, helping banks increase their share of fee based incomeas against interest related income. Banks with ample infrastructure and distribution mechanisms are likely to do well in capturing the up sell/crosssell opportunity. Large intra regional movement of capital and people between oil exporting and importing countries has always kept the remittancemarket strong. The conventional money transfer bureaus are likely to face difficult times owing to high fees and emergence of internet and phone

7

Commercial Banking in the MENA Region

based channels. Banks can play a vital role in providing the last mile linkage to the transfer process and add yet another significant fee based revenuestream.

Most oil based economies have been traditionally run by large monopolistic giants, with most support services outsourced to specialized vendors.Diversification of the economy is expected to bring about the emergence of many small and medium enterprises engaged in support activities andspill into basic manufacturing and other service sectors. The ability to provide credit and business banking solutions to this space will help banksexpand portfolios away from the large wholesale and plain retail segments, as well as being a more active part of the diversification success story.

The ongoing global crisis has brought banking in most countries under scrutiny. In times of sophisticated financial instruments, cross border linkagesand economic and financial interdependence; it is unreasonable to believe that the region would remain immune. The extent of damage however issomething that only time will tell. Given the fundamentals of the regional economies, and the positioning of the industry, it is plausible to expectshort term shock waves, but the long term outlook remains optimistic and geared for growth.

8

Commercial Banking in the MENA Region

1 Global Commercial Banking Overview

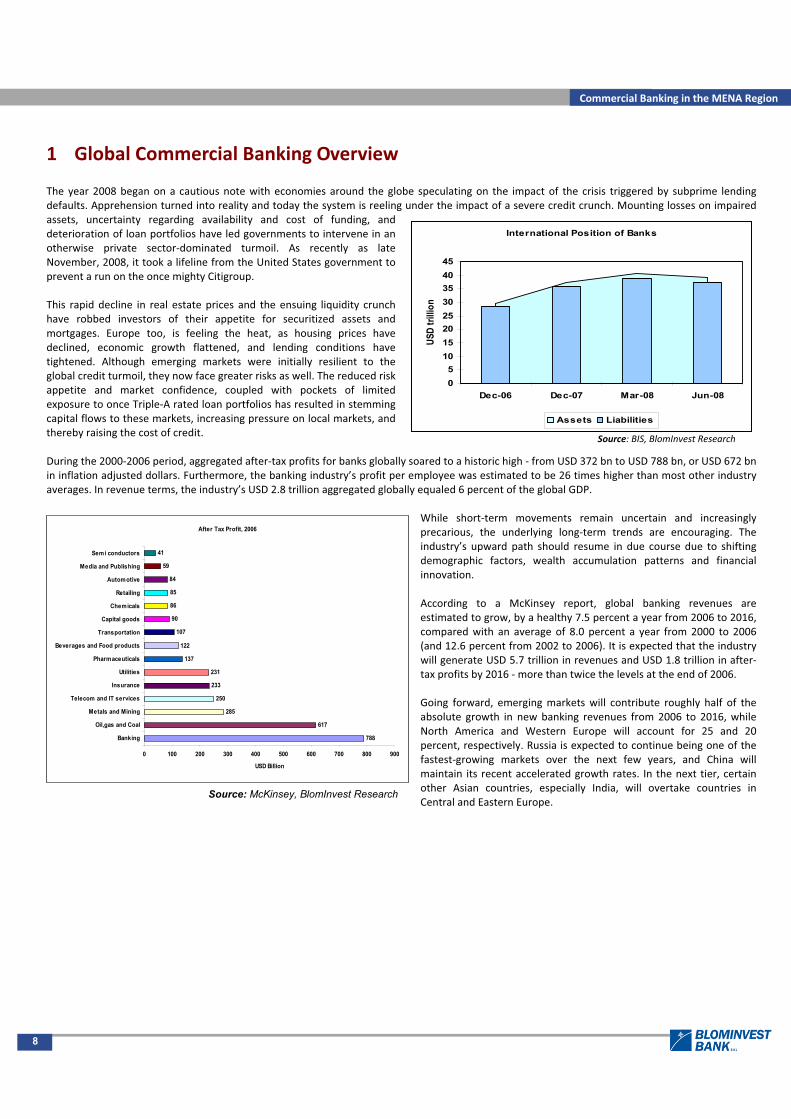

The year 2008 began on a cautious note with economies around the globe speculating on the impact of the crisis triggered by subprime lendingdefaults. Apprehension turned into reality and today the system is reeling under the impact of a severe credit crunch. Mounting losses on impairedassets, uncertainty regarding availability and cost of funding, anddeterioration of loan portfolios have led governments to intervene in anotherwise private sector dominated turmoil. As recently as lateNovember, 2008, it took a lifeline from the United States government toprevent a run on the once mighty Citigroup.

This rapid decline in real estate prices and the ensuing liquidity crunchhave robbed investors of their appetite for securitized assets andmortgages. Europe too, is feeling the heat, as housing prices havedeclined, economic growth flattened, and lending conditions havetightened. Although emerging markets were initially resilient to theglobal credit turmoil, they now face greater risks as well. The reduced riskappetite and market confidence, coupled with pockets of limitedexposure to once Triple A rated loan portfolios has resulted in stemmingcapital flows to these markets, increasing pressure on local markets, andthereby raising the cost of credit.

During the 2000 2006 period, aggregated after tax profits for banks globally soared to a historic high from USD 372 bn to USD 788 bn, or USD 672 bnin inflation adjusted dollars. Furthermore, the banking industry’s profit per employee was estimated to be 26 times higher than most other industryaverages. In revenue terms, the industry’s USD 2.8 trillion aggregated globally equaled 6 percent of the global GDP.

While short term movements remain uncertain and increasinglyprecarious, the underlying long term trends are encouraging. Theindustry’s upward path should resume in due course due to shiftingdemographic factors, wealth accumulation patterns and financialinnovation.

According to a McKinsey report, global banking revenues areestimated to grow, by a healthy 7.5 percent a year from 2006 to 2016,compared with an average of 8.0 percent a year from 2000 to 2006(and 12.6 percent from 2002 to 2006). It is expected that the industrywill generate USD 5.7 trillion in revenues and USD 1.8 trillion in aftertax profits by 2016 more than twice the levels at the end of 2006.

Going forward, emerging markets will contribute roughly half of theabsolute growth in new banking revenues from 2006 to 2016, whileNorth America and Western Europe will account for 25 and 20percent, respectively. Russia is expected to continue being one of thefastest growing markets over the next few years, and China willmaintain its recent accelerated growth rates. In the next tier, certainother Asian countries, especially India, will overtake countries inCentral and Eastern Europe.

Source: BIS, BlomInvest Research

International Position of Banks

05

1015202530354045

Dec-06 Dec-07 Mar-08 Jun-08

USD

trilli

onAssets Liabilities

Source: McKinsey, BlomInvest Research

After Tax Profit, 2006

788

617

285

250

233

231

137

122

107

90

86

85

84

59

41

0 100 200 300 400 500 600 700 800 900

Banking

Oil,gas and Coal

Metals and Mining

Telecom and IT services

Insurance

Utilities

Pharmaceuticals

Beverages and Food products

Transportation

Capital goods

Chemicals

Retailing

Automotive

Media and Publishing

Semi conductors

USD Billion

9

Commercial Banking in the MENA Region

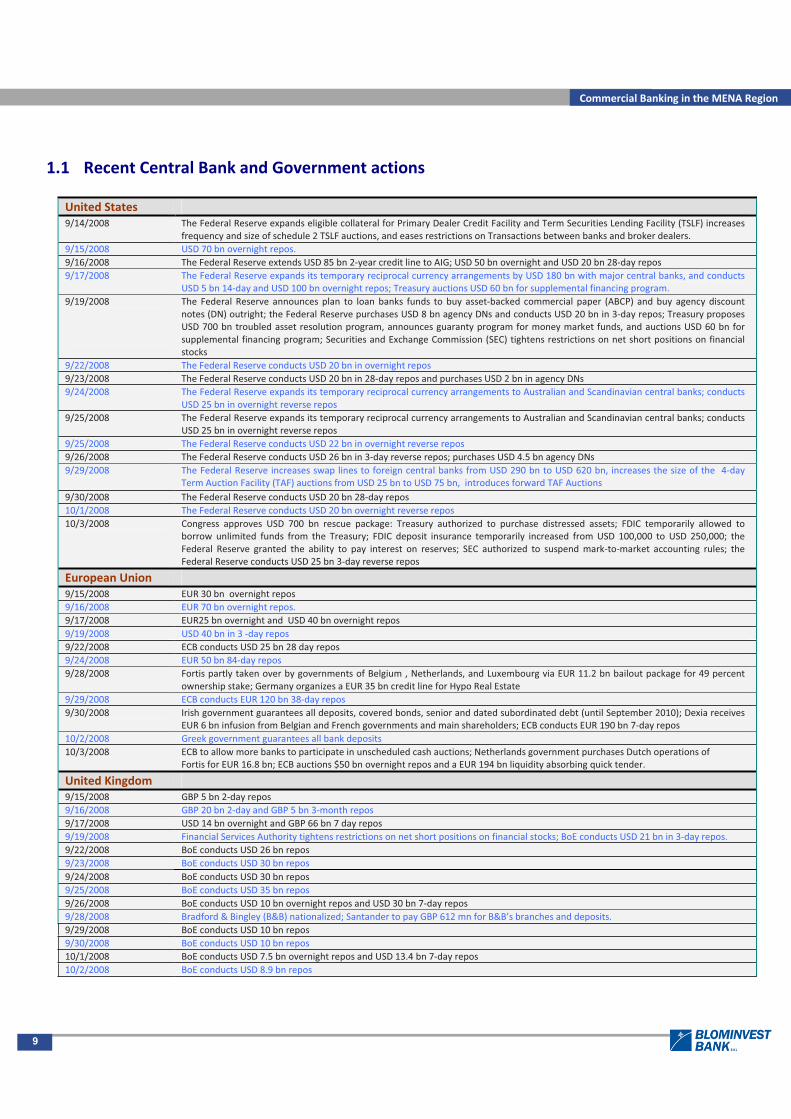

1.1 Recent Central Bank and Government actions

United States9/14/2008 The Federal Reserve expands eligible collateral for Primary Dealer Credit Facility and Term Securities Lending Facility (TSLF) increases

frequency and size of schedule 2 TSLF auctions, and eases restrictions on Transactions between banks and broker dealers.9/15/2008 USD 70 bn overnight repos.9/16/2008 The Federal Reserve extends USD 85 bn 2 year credit line to AIG; USD 50 bn overnight and USD 20 bn 28 day repos9/17/2008 The Federal Reserve expands its temporary reciprocal currency arrangements by USD 180 bn with major central banks, and conducts

USD 5 bn 14 day and USD 100 bn overnight repos; Treasury auctions USD 60 bn for supplemental financing program.9/19/2008 The Federal Reserve announces plan to loan banks funds to buy asset backed commercial paper (ABCP) and buy agency discount

notes (DN) outright; the Federal Reserve purchases USD 8 bn agency DNs and conducts USD 20 bn in 3 day repos; Treasury proposesUSD 700 bn troubled asset resolution program, announces guaranty program for money market funds, and auctions USD 60 bn forsupplemental financing program; Securities and Exchange Commission (SEC) tightens restrictions on net short positions on financialstocks

9/22/2008 The Federal Reserve conducts USD 20 bn in overnight repos9/23/2008 The Federal Reserve conducts USD 20 bn in 28 day repos and purchases USD 2 bn in agency DNs9/24/2008 The Federal Reserve expands its temporary reciprocal currency arrangements to Australian and Scandinavian central banks; conducts

USD 25 bn in overnight reverse repos9/25/2008 The Federal Reserve expands its temporary reciprocal currency arrangements to Australian and Scandinavian central banks; conducts

USD 25 bn in overnight reverse repos9/25/2008 The Federal Reserve conducts USD 22 bn in overnight reverse repos9/26/2008 The Federal Reserve conducts USD 26 bn in 3 day reverse repos; purchases USD 4.5 bn agency DNs9/29/2008 The Federal Reserve increases swap lines to foreign central banks from USD 290 bn to USD 620 bn, increases the size of the 4 day

Term Auction Facility (TAF) auctions from USD 25 bn to USD 75 bn, introduces forward TAF Auctions9/30/2008 The Federal Reserve conducts USD 20 bn 28 day repos10/1/2008 The Federal Reserve conducts USD 20 bn overnight reverse repos10/3/2008 Congress approves USD 700 bn rescue package: Treasury authorized to purchase distressed assets; FDIC temporarily allowed to

borrow unlimited funds from the Treasury; FDIC deposit insurance temporarily increased from USD 100,000 to USD 250,000; theFederal Reserve granted the ability to pay interest on reserves; SEC authorized to suspend mark to market accounting rules; theFederal Reserve conducts USD 25 bn 3 day reverse repos

European Union9/15/2008 EUR 30 bn overnight repos9/16/2008 EUR 70 bn overnight repos.9/17/2008 EUR25 bn overnight and USD 40 bn overnight repos9/19/2008 USD 40 bn in 3 day repos9/22/2008 ECB conducts USD 25 bn 28 day repos9/24/2008 EUR 50 bn 84 day repos9/28/2008 Fortis partly taken over by governments of Belgium , Netherlands, and Luxembourg via EUR 11.2 bn bailout package for 49 percent

ownership stake; Germany organizes a EUR 35 bn credit line for Hypo Real Estate9/29/2008 ECB conducts EUR 120 bn 38 day repos9/30/2008 Irish government guarantees all deposits, covered bonds, senior and dated subordinated debt (until September 2010); Dexia receives

EUR 6 bn infusion from Belgian and French governments and main shareholders; ECB conducts EUR 190 bn 7 day repos10/2/2008 Greek government guarantees all bank deposits10/3/2008 ECB to allow more banks to participate in unscheduled cash auctions; Netherlands government purchases Dutch operations of

Fortis for EUR 16.8 bn; ECB auctions $50 bn overnight repos and a EUR 194 bn liquidity absorbing quick tender.

United Kingdom9/15/2008 GBP 5 bn 2 day repos9/16/2008 GBP 20 bn 2 day and GBP 5 bn 3 month repos9/17/2008 USD 14 bn overnight and GBP 66 bn 7 day repos9/19/2008 Financial Services Authority tightens restrictions on net short positions on financial stocks; BoE conducts USD 21 bn in 3 day repos.9/22/2008 BoE conducts USD 26 bn repos9/23/2008 BoE conducts USD 30 bn repos9/24/2008 BoE conducts USD 30 bn repos9/25/2008 BoE conducts USD 35 bn repos9/26/2008 BoE conducts USD 10 bn overnight repos and USD 30 bn 7 day repos9/28/2008 Bradford & Bingley (B&B) nationalized; Santander to pay GBP 612 mn for B&B’s branches and deposits.9/29/2008 BoE conducts USD 10 bn repos9/30/2008 BoE conducts USD 10 bn repos10/1/2008 BoE conducts USD 7.5 bn overnight repos and USD 13.4 bn 7 day repos10/2/2008 BoE conducts USD 8.9 bn repos

10

Commercial Banking in the MENA Region

10/3/2008 BoE extends eligible collateral for its weekly long term repo operations to include AAA rated ABS and highly rated ABCP; conductsUSD 8.2 bn overnight repos and USD 30 bn 7 day repos.

Others9/15/2008 Other central banks provide liquidity, including Japan (YEN 1.5 tril.) and Australia (AUD 2.1 bn, among others.9/16/2008 Other central banks provide liquidity, including Japan (YEN 2.5 tril.), Switzerland (SF726.4 mn) and Australia (AUD1.7 bn), among

others

9/17/2008 Other central banks provide liquidity, including Japan (YEN 2.5 tril.), and Australia (AUD2.8 bn), among others.

9/19/2008 Other central banks provide liquidity, including Japan (YEN 3 tril.), Switzerland (USD 10 bn), and Australia (AUD1.9 bn), among others;several regulatory institutions impose restrictions on equity short sales

9/29/2008 Iceland’s government takes 75 percent stake in Glitnir Bank10/2/2008 Brazilian central bank eases reserve requirements10/3/2008 Russian central bank extends unsecured loans to qualified banks for up to six months and introduces other measures

11

Commercial Banking in the MENA Region

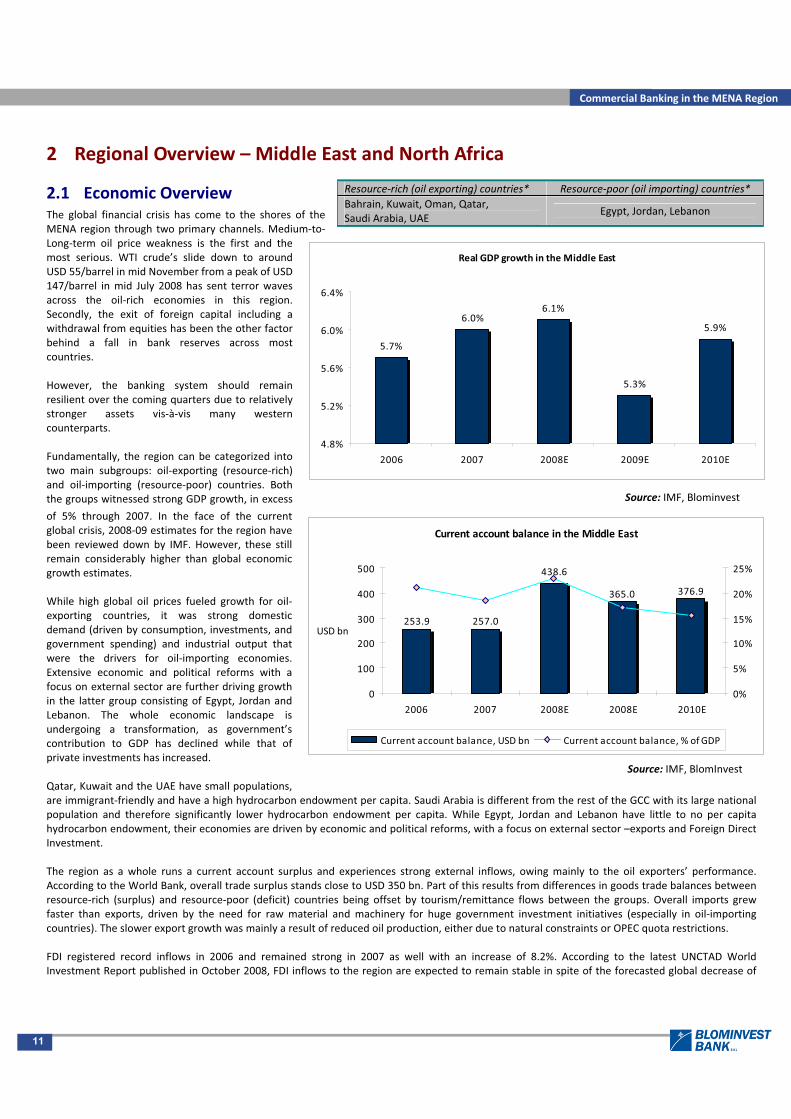

2 Regional Overview – Middle East and North Africa

2.1 Economic OverviewThe global financial crisis has come to the shores of theMENA region through two primary channels. Medium toLong term oil price weakness is the first and themost serious. WTI crude’s slide down to aroundUSD 55/barrel in mid November from a peak of USD147/barrel in mid July 2008 has sent terror wavesacross the oil rich economies in this region.Secondly, the exit of foreign capital including awithdrawal from equities has been the other factorbehind a fall in bank reserves across mostcountries.

However, the banking system should remainresilient over the coming quarters due to relativelystronger assets vis à vis many westerncounterparts.

Fundamentally, the region can be categorized intotwo main subgroups: oil exporting (resource rich)and oil importing (resource poor) countries. Boththe groups witnessed strong GDP growth, in excess

of 5% through 2007. In the face of the currentglobal crisis, 2008 09 estimates for the region havebeen reviewed down by IMF. However, these stillremain considerably higher than global economicgrowth estimates.

While high global oil prices fueled growth for oilexporting countries, it was strong domesticdemand (driven by consumption, investments, andgovernment spending) and industrial output thatwere the drivers for oil importing economies.Extensive economic and political reforms with afocus on external sector are further driving growthin the latter group consisting of Egypt, Jordan andLebanon. The whole economic landscape isundergoing a transformation, as government’scontribution to GDP has declined while that ofprivate investments has increased.

Qatar, Kuwait and the UAE have small populations,are immigrant friendly and have a high hydrocarbon endowment per capita. Saudi Arabia is different from the rest of the GCC with its large nationalpopulation and therefore significantly lower hydrocarbon endowment per capita. While Egypt, Jordan and Lebanon have little to no per capitahydrocarbon endowment, their economies are driven by economic and political reforms, with a focus on external sector –exports and Foreign DirectInvestment.

The region as a whole runs a current account surplus and experiences strong external inflows, owing mainly to the oil exporters’ performance.According to the World Bank, overall trade surplus stands close to USD 350 bn. Part of this results from differences in goods trade balances betweenresource rich (surplus) and resource poor (deficit) countries being offset by tourism/remittance flows between the groups. Overall imports grewfaster than exports, driven by the need for raw material and machinery for huge government investment initiatives (especially in oil importingcountries). The slower export growth was mainly a result of reduced oil production, either due to natural constraints or OPEC quota restrictions.

FDI registered record inflows in 2006 and remained strong in 2007 as well with an increase of 8.2%. According to the latest UNCTAD WorldInvestment Report published in October 2008, FDI inflows to the region are expected to remain stable in spite of the forecasted global decrease of

Resource rich (oil exporting) countries* Resource poor (oil importing) countries*Bahrain, Kuwait, Oman, Qatar,Saudi Arabia, UAE

Egypt, Jordan, Lebanon

Real GDP growth in the Middle East

5.7%

6.0%6.1%

5.3%

5.9%

4.8%

5.2%

5.6%

6.0%

6.4%

2006 2007 2008E 2009E 2010E

Source: IMF, Blominvest

Current account balance in the Middle East

438.6

253.9 257.0

365.0 376.9

0

100

200

300

400

500

2006 2007 2008E 2008E 2010E

USD bn

0%

5%

10%

15%

20%

25%

Current account balance, USD bn Current account balance, % ofGDP

Source: IMF, BlomInvest

12

Commercial Banking in the MENA Region

10%. The intra regional capital flows have witnessed two major trends. On the demand side, public sectors have opened up and announced a seriesof structural reforms, including progress on Basel II implementation in most countries; whereas on the supply side, booming oil prices till mid 2008have brought in ample liquidity.

Resource poor economies are more diversified,with trading and manufacturing being the largeGDP contributors. Oil exporting countries aregradually realizing the importance ofdiversification as a means to reducing overalleconomic risk. Bahrain commenced thediversification process earlier compared to othercountries and has tasted early success, as a resultof which its dependence on oil has come down.The financial sector now amounts to 22% of GDP,just marginally behind oil which has a share of26%. On the other hand, Saudi Arabia with 54.4%of GDP still being accounted for by petroleumneeds to diversify further. A seemingly commonapproach among the countries is to focus on theindustrial sector, especially energy intensivemanufacturing like petrochemicals and metals.Further confirming this trend, the GulfOrganization for Industrial Consulting estimatesinvestments worth USD 120 bn in the GCC countries towards the chemicals and petrochemical industries over the next 5 years. At the same time,Saudi Arabia is leading the way in steel industry, with projects worth over USD 460 bn, including steel railway linking its east and west.

A liquidity surge on account of high hydrocarbon prices will be a trigger to inter regional investment and attract workers from poorer countries, whileeasing pressure on labor markets. On the otherhand, a decline in oil prices like the one in mid2008 may affect the region’s economicdevelopment. Saudi Arabia, which in Septemberapproved aluminum projects worth well over USD17 bn, is now reviewing one of the projects, whichwas due to start production in 2012. The Kingdomis also reviewing or adjusting contracts acrossmultiple other industry segments, from oil servicesto real estate development.

All countries in the region, regardless ofdependence on hydrocarbons, are net importers offood and industrial inputs. Hence, highinternational commodity prices exert inflationarypressures on most regional economies. Forcountries which have their currencies pegged tothe United States Dollar, any expansionarymonetary policy move by the Fed accentuates thedanger of imported inflation.

Inflation in the MENA Region

10.6% 11.3%

15.8%

7.0%

14.4%

0%

5%

10%

15%

20%

2006 2007 2008E 2009E 2010E

Source: IMF, BlomInvest

Share of the hydrocarbon sector in the GDP ofGCC countries

39.0%

54.4%

26.0%

45.3%

52.1%56.6%

0%

10%

20%

30%

40%

50%

60%

UAE Saudi Arabia Bahrain Oman Kuwait Qatar

Source: Central Banks, BlomInvest

13

Commercial Banking in the MENA Region

2.1.1 Comparative Economic Landscape

All figures as per latest releases viz. 2006 07* Assuming 100 for the year 2000, except Egypt where 2001/2002=100** For Egypt, data given is for fiscal year 2007 2008*** Oil and gas sector combined

Sources: IMF World Economic Outlook Report 10/2008, CIA World Factbook, The Economist Intelligence Unit, Bank Audi, The Gulf Times, Central Bank of the UnitedArab Emirates, United Arab Emirates Ministry of Economy, Saudi Arabian Monetary Agency, Central Bank of Bahrain, Bahrain Ministry of Finance, Central Bank of Oman,Central Bank of Kuwait, Qatar Central Bank, Central Bank of Jordan, Jordan Department of Statistics, Banque du Liban, Central Bank of Egypt

Rank GDP growth Investments/GDP Current account/GDP Money supply/GDP Fiscal balance/GDP Employment

1 Qatar Qatar Kuwait Egypt Kuwait Qatar

2 UAE Jordan Saudi Arabia UAE UAE Kuwait

3 Egypt Lebanon UAE Bahrain Qatar UAE

4 Bahrain Saudi Arabia Bahrain Lebanon Saudi Arabia Saudi Arabia

5 Jordan Egypt Qatar Kuwait Bahrain Egypt

6 Oman UAE Oman Saudi Arabia Oman Jordan

7 Kuwait Oman Egypt Qatar Jordan Oman

8 Saudi Arabia Kuwait Lebanon Oman Egypt Bahrain / Lebanon

9 Lebanon Bahrain Jordan Jordan Lebanon

UAE KSA Bahrain Oman Kuwait Qatar Jordan Lebanon Egypt**

GDP (USD bn)* 117.99 247.86 13.37 28.32 67.57 31.20 13.27 21.31 96.13

GDP per capita(current prices, USD ‘000)

42.501 15.724 22.771 15.714 33.687 78.754 2.766 6.569 1.739

Inflation (%) 11.1% 4.11% 3.4% 5.50% 4.98% 13.76% 5.4% 9.3% 8.81%

Investment (USD bn) 40.44 83.28 3.48 8.13 22.05 29.34 4.47 5.42 33.12

Current a/c balance (USD bn) 37.01 95.12 2.90 4.0 47.47 10.45 2.98 2.63 0.9

Money supply(USD bn)

154.04 177.97 14.92 15.88 66.80 32.32 2.11 16.44 141.60

Interest rate (%) 4.25 5.5 5.3 6.02 6.25 5.55 7 12 10

Velocity of money circulation 1.02 2.11 1.32 2.52 1.65 2.10 7.58 1.50 1.12

Fiscal balance(USD bn)

30.21 47.15 0.11 104.45 32.81 10.46 0.87 2.56 12.04

Fiscal balance to GDP ratio (%) 15.69 12.3 0.6 0.14 29.83 14.7 5.25 10.39 7.5

Population (mn) 4.49 24.24 0.76 2.7 3.40 1.2 5.72 3.75 75.05

Unemployment rate (%) 2.4 5.63 20 15 1.5 0.5 13.5 20 9.1

Contribution of oil to economy (%) 38.6 54.4 26.0 45.3 52.1*** 56.6*** n/a n/a n/a

14

Commercial Banking in the MENA Region

2.2 Banking Industry OverviewAt a time when global growth is under pressure, the time is ripe to look at banks in the emerging markets of the MENA region. These have escapedthe ongoing crisis primarily due to limited global exposure and absence of sophisticated derivatives with underlying toxic assets. Economicfundamentals have remained strong across the region and are likely to remain so for the coming few years. Banks have been among the majorbeneficiaries of the strong nominal GDP growth, which has translated into annual asset growth exceeding 20% for most MENA countries.

Boosted by the huge fiscal surplus buildup through mid 2008, governments in the region are actively looking toward diversification, in turn investingin multiple large scale development projects. The banking sector has been a key beneficiary and facilitator of this investment spree, and creditdemand on account of this is likely to be a key growth driver in short term. For Egypt, Lebanon and Jordan however the nascent consumer financesegment is expected to drive growth owing to an underserved potential target market. Despite strong loan growth over the last 3 years, bankingsector penetration is still low, and is supportive of strong and sustained loan growth over the next few years.

Banks are gradually moving toward balance sheet driven fee income as against non recurring investment returns. This is furthered by an increasingimpetus to penetrate the retail consumer and SME segments.

2.2.1 Banking Industry Drivers

Strong economic fundamentals and reform driven growthReal GDP is expected to grow in the range of 5 6% during 2008 (Source: IMF) and remain in mid single digit range during 2009.

The year’s high global oil prices enabled countries to build significant cash reserves that are now being channeled toward large investments acrossmultiple sectors. Previous high prices have also helped increase capital flows and remittances into countries like Jordan, Lebanon and Egypt.

With the exception of Kuwait, the pegging of local currencies to the US Dollar has pushed interest rates down facilitating credit expansion implyingample liquidity in the system.

Bahrain’s success in developing non oil sectors like manufacturing and finance make it less prone to oil price fluctuations. Proven oil and gas reservesstood at 125 mn barrels and 3.25 trillion cubic feet respectively as of January 2008 (Source: Energy Information Administration).

The authorities recognize the importance of effective regulation in their ability to attract investment toward the development of financial servicesand have taken strong steps to bring rules and supervision close to leading international standards. The GCC also expects to streamline licensingregulations and creation of a single regulatory regime for the financial services sector.

Favorable demographicsA large part of the population in most countries is in the age group of 15 64years with the majority being under 35 years of age. The population beingclose to or at a working age implies high consumer spending and in turndemand for retail banking services, both on the deposits and credit sides.Qatar seems to be the most favorably placed followed by Bahrain and Kuwait.

The creation of huge employment pockets like the six economic cities in SaudiArabia and the financial centers in Qatar and Bahrain is attracting hugeexpatriate population. While it directly pushes up banking requirements, italso indirectly facilitates capital flow through remittances to countries likeEgypt, Jordan and Lebanon. Such demographic factors are a strong enabler fortighter economic integration among regional countries.

The GCC population has accumulated USD 1.5 trillion in personal wealth.Clients increasingly prefer wealth and asset management services providedlocally rather than offshore, by regionally respected and trusted institutions,leading to strong growth in these sectors.

Government’s focus on diversificationOver recent years, MENA countries have become increasingly aware of the importance of building a diversified and sustainable economy. This isparticularly true in case of the Gulf States that have hydrocarbon based economies. Part of the diversification strategy is also to support the SMEsector, and for the broader private sector which is still relatively underdeveloped in many MENA countries. The Omani government, with its recent

Source: CIA, EIU & BlomInvest Research

Demographic Profile 2008

Bahrain

Oman

Kuwait

Qat ar

SaudiU.A.E

Egypt LebanonJordan

Egypt

0.00%

5.00%

10.00%

15.00%

15 18 21 24 27 30 33 36

Median Age

Working

agepo

pulation

grow

th(200

812

)

15

Commercial Banking in the MENA Region

aggressive incentive program to encourage small businesses to employ itscitizenry is a good case example of a program that is expected to deliver goodreturns.

With USD 2.76 trillion worth of developments either under way or in thepipeline, the GCC is now the world’s largest project finance market. Theinvestments span leisure, residential, infrastructure and industrialdevelopments as the governments seek to forge stronger and more diversifiedeconomic future. Many news outlets have remarked on the presence ofbetween 15 and 20% of the world’s cranes in Dubai alone.

Simultaneously, most of the countries are pursuing liberalization. Trade tariffshave been reduced from a simple average of 20% in 2000 to 13% by 2007,which was the fastest reduction across the world. All the countries in thisstudy, excluding Lebanon (currently in negotiation stage), are now members ofthe World Trade Organization. Many are members of regional or bilateral trade agreements (including with EU or the United States). This success ishowever balanced by hidden trade barriers and poor trade logistics. A few countries have started reducing non tariff barriers like the complexity ofdocumentation needed (mainly Egypt, Lebanon and Jordan). However, a lot still needs to be done.

Low banking penetrationOverall, banking penetration is relatively low in the MENA region incomparison with its Western counterpart specially in countries likeEgypt, Saudi Arabia, Kuwait, and Jordan, with each branch servicing anaverage of roughly 24,000, 18,000, 11,000 and 10,000 customersrespectively. This compares with double to triple that number inWestern economies.

Cross border coordinationAccording to a recent World Bank study, the region offers avenues forintegration, which could definitely enhance its overall competitiveness.However, the opportunity has not been fully exploited, even thoughthere have been a number of attempts at cross border coordination, thelatest one being Pan Arab Free Trade Agreement. The region as a whole,however, is still more integrated through labor mobility than throughtrade or capital flows, and the infrastructural coordination is still in itsinitial stages.

Intra regional trade is at single digit levels, which is low by global standards. For most countries, its ratio to overall trade has increased over the pasttwo decades; only in Syria and Jordan the ratio exceeds 15%. Trade in the region is rendered difficult due to a lack of coordinated tariffs and existenceof non trade barriers. Trade in services has not been included in most of the existing free trade agreements, and is thus rather constrained within theregion. Nevertheless, Kuwait is an exception having followed an export strategy for telecommunication services and has become one of the world’slargest providers, connecting 27 mn mobile subscribers in the ME and Sub Saharan Africa.

Despite investors’ willingness to invest in other countries of the region, there are barriers to capital flows. The situation is better in countries likeEgypt, where the sector is relative more liberalized. Lebanese banks are opening or acquiring branches across the region. In Jordan, a large part ofprivate banks is owned by GCC investors. At the moment, there are stock markets in almost every MENA country, and increasing numbers of investorsare trading in stock markets (for example, Gulf investors are particularly active on Egyptian and Jordanian stock markets). Still, there are a lot ofhidden or legal restrictions on capital inflows and outflows, which restrict intra regional stock trading. However, the situation is gradually changingdue to the region’s willingness to ensure access to the high liquidity in the Gulf States. Regional capital flows are also helped by increasingdevelopment investments and improving business environment in most of the countries.

2.2.2 Performance Indicators

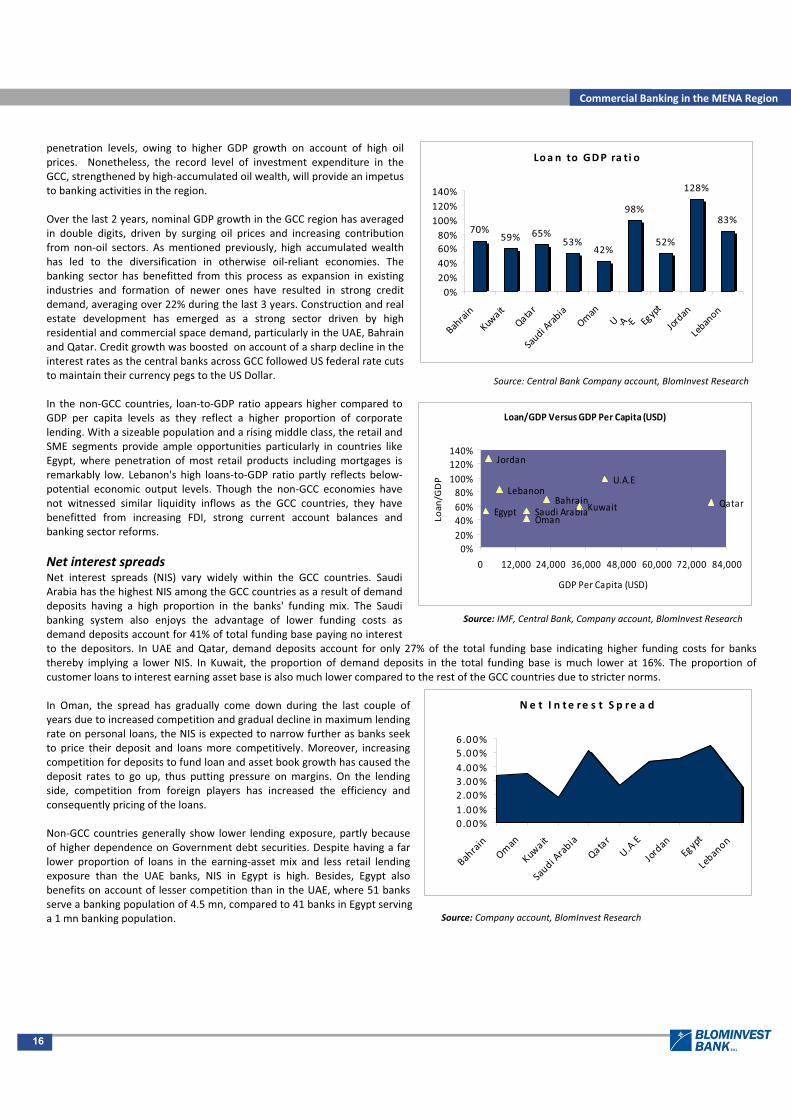

Credit growthLoans to GDP ratio is a key metric indicating the penetration level of the banking sector. In the MENA region, lower banking penetration impliessustained loan demand. However, the current loan to GDP ratio in the GCC states provides a somewhat distorted picture of the banking sector

Source: Zawya, EIU, Central Bank & BlomInvest Research

Bra nch Se rvi ce Ra ti o 2007

1970

11,150

6040 6549 7725

17,960

10,529

23,789

5431

05000

10000150002000025000

Bahrain

Kuwait

Qatar

Oman

U.A.E

Saudi Arabia

Jordan

Egypt

Lebanon

Peop

leserved

perbranch

Gulf P rojec ts B y S ec to rs

59.90%

21.20%

6.7 0%

6 .60%

2.00%

3.6 0%

Constru ction O i l & G as P e troc hemica l P ower W a te r & Wa stewa ter O the r

Source:Meed

16

Commercial Banking in the MENA Region

N e t I n te re s t S p re a d

0.00%1.00%2.00%3.00%4.00%5.00%6.00%

Bahrain

Oman

Kuwait

Saudi Arabia

Qatar

U.A.E

Jordan

Egypt

Lebanon

Source: Company account, BlomInvest Research

penetration levels, owing to higher GDP growth on account of high oilprices. Nonetheless, the record level of investment expenditure in theGCC, strengthened by high accumulated oil wealth, will provide an impetusto banking activities in the region.

Over the last 2 years, nominal GDP growth in the GCC region has averagedin double digits, driven by surging oil prices and increasing contributionfrom non oil sectors. As mentioned previously, high accumulated wealthhas led to the diversification in otherwise oil reliant economies. Thebanking sector has benefitted from this process as expansion in existingindustries and formation of newer ones have resulted in strong creditdemand, averaging over 22% during the last 3 years. Construction and realestate development has emerged as a strong sector driven by highresidential and commercial space demand, particularly in the UAE, Bahrainand Qatar. Credit growth was boosted on account of a sharp decline in theinterest rates as the central banks across GCC followed US federal rate cutsto maintain their currency pegs to the US Dollar.

In the non GCC countries, loan to GDP ratio appears higher compared toGDP per capita levels as they reflect a higher proportion of corporatelending. With a sizeable population and a rising middle class, the retail andSME segments provide ample opportunities particularly in countries likeEgypt, where penetration of most retail products including mortgages isremarkably low. Lebanon's high loans to GDP ratio partly reflects belowpotential economic output levels. Though the non GCC economies havenot witnessed similar liquidity inflows as the GCC countries, they havebenefitted from increasing FDI, strong current account balances andbanking sector reforms.

Net interest spreadsNet interest spreads (NIS) vary widely within the GCC countries. SaudiArabia has the highest NIS among the GCC countries as a result of demanddeposits having a high proportion in the banks' funding mix. The Saudibanking system also enjoys the advantage of lower funding costs asdemand deposits account for 41% of total funding base paying no interestto the depositors. In UAE and Qatar, demand deposits account for only 27% of the total funding base indicating higher funding costs for banksthereby implying a lower NIS. In Kuwait, the proportion of demand deposits in the total funding base is much lower at 16%. The proportion ofcustomer loans to interest earning asset base is also much lower compared to the rest of the GCC countries due to stricter norms.

In Oman, the spread has gradually come down during the last couple ofyears due to increased competition and gradual decline in maximum lendingrate on personal loans, the NIS is expected to narrow further as banks seekto price their deposit and loans more competitively. Moreover, increasingcompetition for deposits to fund loan and asset book growth has caused thedeposit rates to go up, thus putting pressure on margins. On the lendingside, competition from foreign players has increased the efficiency andconsequently pricing of the loans.

Non GCC countries generally show lower lending exposure, partly becauseof higher dependence on Government debt securities. Despite having a farlower proportion of loans in the earning asset mix and less retail lendingexposure than the UAE banks, NIS in Egypt is high. Besides, Egypt alsobenefits on account of lesser competition than in the UAE, where 51 banksserve a banking population of 4.5 mn, compared to 41 banks in Egypt servinga 1 mn banking population.

Source: IMF, Central Bank, Company account, BlomInvest Research

Loan/GDP VersusGDP Per Capita (USD)

BahrainKuwait Qatar

Saudi ArabiaOman

U.A.E

Egypt

Jordan

Lebanon

0%20%40%60%80%

100%120%140%

0 12,000 24,000 36,000 48,000 60,000 72,000 84,000

GDP Per Capita (USD)

Loan/GDP

Loa n to GDP ra ti o

70%59% 65%

53%42%

98%

52%

128%

83%

0%20%40%60%80%

100%120%140%

Bahrain

Kuwait

Qatar

Saudi Arabia

Oman

U .A . E Egypt

Jordan

Lebanon

Source: Central Bank Company account, BlomInvest Research

17

Commercial Banking in the MENA Region

Non Interest Income/ Total Operating Income

49%

29%

48%

33%

41% 42%

35%

52%

33%

0%

10%

20%

30%

40%

50%

60%

Bahrain

Oman

Kuwait

Saudi Arabia

Qatar

U .A .E Jordan

Egypt

Lebanon

Source: Company account, Blominvest Bank

Provisons/Total loan

0.59%

0.42%

0.34%0.32%

0.08%

0.22%0.29%

0.38%0.39%

0.10%

0.04%

0.18%

0.32%

0.46%

0.60%

Bahrain

Oman

Kuwait

Saudi Arabia

Qatar

U .A . E Jordan

Egypt

Lebanon

Source: Company account, BlomInvest Research

Source: Company account, Blominvest Bank

Cos t to I n come

50% 49%42% 41% 42%

33%45%

57%

69%

0%10%20%30%40%50%60%70%80%

Bahrain

Oman

Kuwait

Saudi Arabia

Qatar

U.A.E

Jordan

Egypt

Lebanon

CostIn the MENA region, the costs of doing business have been surging due to risinginflation. In the GCC, spiraling rentals and demand for qualified staff arepushing up costs for the banking sector. However, Saudi Arabia is an exception,witnessing a declining trend in the cost to income ratio. A focus shift towardcorporate loans is likely to lead to higher volumes and net interest incomegrowth in medium term.

Cost efficiency at Bahraini banks compares well with international standards,with typical ratios around 50%. Cost/income ratios improved in part due torising pre impairment operating revenues in a favorable environment.However, the cost efficiency of Bahraini banks is weaker than that of Kuwaiti,Saudi or UAE banks, reflecting fewer potential economies of scale from arelatively smaller domestic market.

Qatari banks have managed to maintain moderate cost to income levels amidrising staff costs due to rising inflation and competition.

Kuwait’s cost income ratio is very low by both regional and internationalstandards. Over the past few years, banks have invested heavily in IT (85% of transactions are executed on line) and have also expanded their branchoutreach.

In the non GCC countries, cost to income ratio has increased as a result of rising inflation, increasing competition and aggressive branch expansionplans.

Non interest incomeIn the past, GCC banks achieved relatively high levels of non interest incomedriven mainly by volatile sources of income, particularly, higher investmentreturns (real estate & equity market). In many cases, these volatile sources ofincome have largely dissipated leaving a pool of steady balance sheet relatedfee income, particularly in Qatar and Saudi Arabia. For the GCC economies,much of this has been on account of a shift toward more specialized lending. Inthe UAE, non interest income is expected to grow due to an increase in corebusiness volumes.

Within the GCC, the contribution of non interest income is lower for SaudiArabia, partly due to diminishing returns on retail equity broking business. Onthe whole, the quality of non interest income is likely to improve as volatilenon interest income is replaced with steadier balance sheet driven fee income.

For the North African and Levant banks, the non interest income of thebanking sector has been primarily fueled by fee income from higher tradeactivity and corporate lending. Rising retail penetration in Egypt is projected tobe a key driver of recurring non interest income growth. In Jordan, the

contribution of non interest income to total income increased sharply duringthe past couple of years, mainly on the back of unsustainable brokeragerevenues and market related gains. This trend reversed during 2007 asbrokerage volume declined and market related gains dried up

ProvisioningThe provisioning efforts in the GCC region have been particularly low,averaging below 0.6% of loan, helped by buoyant economies, substantialwrite backs and increased corporate lending. However, revaluations may leadto increase in provisioning, particularly in a sluggish property market. In SaudiArabia, the positive trend in provisioning is supported by the shift in mixtoward the corporate sector.

18

Commercial Banking in the MENA Region

ROE Vs Capital Adequacy ratio

0.00%

14.00%

28.00%

42.00%

Bahrain

Oman

Kuwait

Saudi Arabia

Qatar

U .A .E Jordan

Egypt

Lebanon

ROE CAR

Source: Company account, BlomInvest Research

In Kuwait, provisioning for loan losses has been declining as a result of denominator effect, given strong loan growth. Meanwhile, this would befurther propelled by a decline in general provisioning requirement.

Provisioning for loan losses in North Africa remain normal, averaging below0.4% of total loans. However, NPL coverage is relatively low compared to theGCC, with the exception of Egypt where provisioning costs are increasing dueto amplified retail activities and general economic slowdown.

Return on equity and capital adequacyThe return on equity (ROE) for a majority of MENA banks, except in Bahrainand Lebanon, is in excess of 13%. Lebanese banks have a significant exposureto government debt and inter bank assets, which earn lower spreads, therebyimplying a reduced ROE. Whereas for Bahraini bank, ROE were impacted by itsinvestment in structured investment vehicles (SIV) exposure and also impactedby impairment charges.

Banks in the MENA region are well capitalized by international standards, withsector wide capital adequacy ratio (CAR) of 18.1% in 2007 vs. a CARrequirement of 10% by major monetary authorities in the region. This is dueto strong internal capital generation, providing capital for future growth aswell as strong shareholder support and increasing access to international capital markets

High ROE in Qatar, Saudi Arabia and UAE is because of high net interest spreads due to high percentage of non interest bearings deposits, low cost /income ratio as well as low provisioning levels in 2007

The higher CARs in the GCC region demonstrate the banks' ability to earn exceptionally high returns from excess equity, primarily from investmentand capital gains. Moreover, in the absence of the tax shield advantage, debt capital becomes more expensive than equity, which implies that MENAbanks have a marginal debt related Tier II capital. Moreover, the banking sector is aiming at Basel II compliance.

2.3 Market Dynamics and Industry StructureThe banking sector is one of the main beneficiaries of the improving investment climate and strong investment pickup in the GCC region, pegged bysome estimates at USD 2.76 trillion. The global credit crisis has had limited impact on the region’s credit growth as its exposure was less than USD 3bn primarily due to ongoing reforms and investment plans within various countries. The consumer finance segment in Egypt and Lebanon is in itsinitial phase of growth and is expected to retain the momentum even in the slowing global economic scenario.

The MENA market is highly concentrated compared to other regions implying healthy net interest spread. The outlook remains positive but a slightdrop is not ruled out.

The move toward relatively more stable and recurring revenue streams is prompting banks to increase focus on fee based activities. During 2007, thecombined fee based income for the banks under study stood at 13.5% of total income (gross interest + non interest income).

Entry of global players continues to fuel competition and the ensuing consolidation activity.

Retail lending in the region compared with other regions remains low. During 2007, Egypt recorded retail lending at 17.0% of total loans; lowest in theregion. The same stood at 39.9%, 35.7%, 29.3% and 27.7% in Oman, Bahrain, Qatar and UAE, respectively. One key focus area during 2008 09 will beIT spending, which is estimated to be around USD 2 bn. It is estimated that the region's institutions will continue to spend a large portion of their ITbudgets (up to 30%) toward new initiatives.

Non GCC countries have generally been slow in adopting new banking technologies in the past. However, the trend is now changing and the rush tosecure market share is prompting financial institutions to invest in state of the art systems. Furthermore, retail banking technology will attract thehighest investments over the coming years, as banks look to move beyond branch centric distribution models and improve penetration. ExtendingATMs networks, investing in online and phone banking channels, and rationalizing branch infrastructure are all on the cards. Core bankingupgrades and anti money laundering practices will also attract significant investments during 2008 2009.The banking industry in almost all thecountries in the region, with the exception of Egypt, follows the structure given below. In Egypt, the overall structure is similar except for theintervening power of the President over the monetary authority.

19

Commercial Banking in the MENA Region

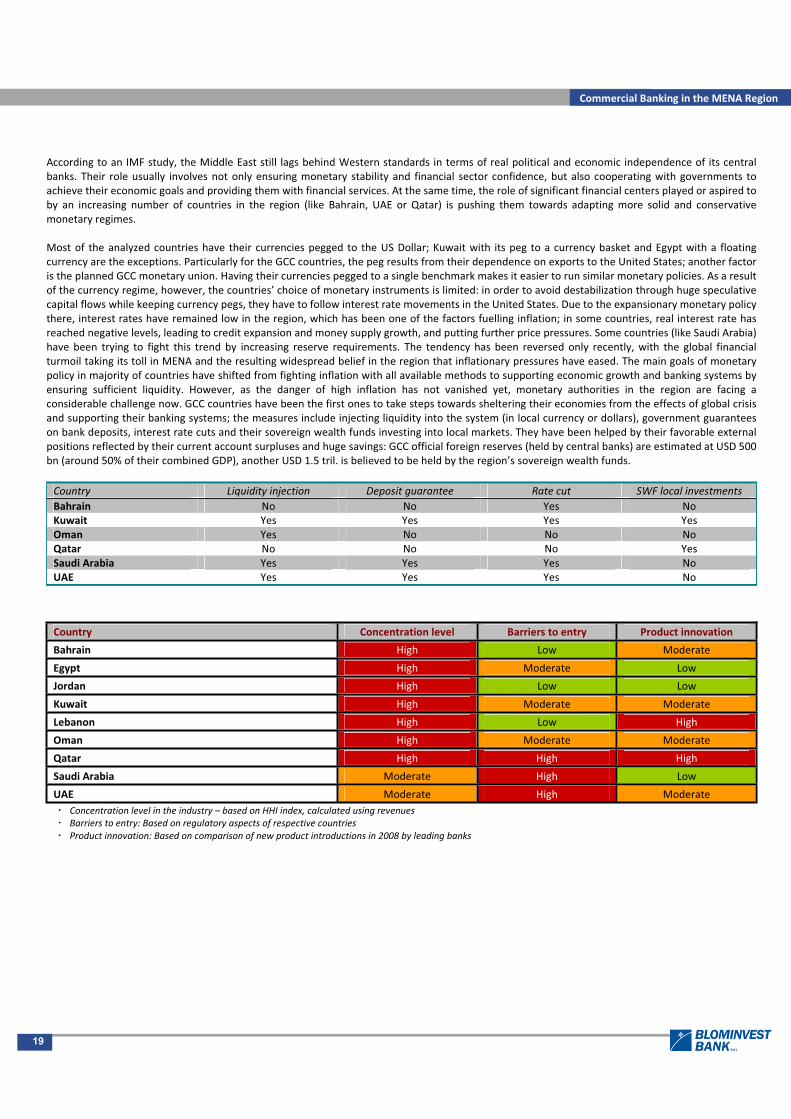

According to an IMF study, the Middle East still lags behind Western standards in terms of real political and economic independence of its centralbanks. Their role usually involves not only ensuring monetary stability and financial sector confidence, but also cooperating with governments toachieve their economic goals and providing them with financial services. At the same time, the role of significant financial centers played or aspired toby an increasing number of countries in the region (like Bahrain, UAE or Qatar) is pushing them towards adapting more solid and conservativemonetary regimes.

Most of the analyzed countries have their currencies pegged to the US Dollar; Kuwait with its peg to a currency basket and Egypt with a floatingcurrency are the exceptions. Particularly for the GCC countries, the peg results from their dependence on exports to the United States; another factoris the planned GCC monetary union. Having their currencies pegged to a single benchmark makes it easier to run similar monetary policies. As a resultof the currency regime, however, the countries’ choice of monetary instruments is limited: in order to avoid destabilization through huge speculativecapital flows while keeping currency pegs, they have to follow interest rate movements in the United States. Due to the expansionary monetary policythere, interest rates have remained low in the region, which has been one of the factors fuelling inflation; in some countries, real interest rate hasreached negative levels, leading to credit expansion and money supply growth, and putting further price pressures. Some countries (like Saudi Arabia)have been trying to fight this trend by increasing reserve requirements. The tendency has been reversed only recently, with the global financialturmoil taking its toll in MENA and the resulting widespread belief in the region that inflationary pressures have eased. The main goals of monetarypolicy in majority of countries have shifted from fighting inflation with all available methods to supporting economic growth and banking systems byensuring sufficient liquidity. However, as the danger of high inflation has not vanished yet, monetary authorities in the region are facing aconsiderable challenge now. GCC countries have been the first ones to take steps towards sheltering their economies from the effects of global crisisand supporting their banking systems; the measures include injecting liquidity into the system (in local currency or dollars), government guaranteeson bank deposits, interest rate cuts and their sovereign wealth funds investing into local markets. They have been helped by their favorable externalpositions reflected by their current account surpluses and huge savings: GCC official foreign reserves (held by central banks) are estimated at USD 500bn (around 50% of their combined GDP), another USD 1.5 tril. is believed to be held by the region’s sovereign wealth funds.

Country Liquidity injection Deposit guarantee Rate cut SWF local investmentsBahrain No No Yes NoKuwait Yes Yes Yes YesOman Yes No No NoQatar No No No YesSaudi Arabia Yes Yes Yes NoUAE Yes Yes Yes No

Country Concentration level Barriers to entry Product innovation

Bahrain High Low Moderate

Egypt High Moderate Low

Jordan High Low Low

Kuwait High Moderate Moderate

Lebanon High Low High

Oman High Moderate Moderate

Qatar High High High

Saudi Arabia Moderate High Low

UAE Moderate High ModerateConcentration level in the industry – based on HHI index, calculated using revenuesBarriers to entry: Based on regulatory aspects of respective countriesProduct innovation: Based on comparison of new product introductions in 2008 by leading banks

20

Commercial Banking in the MENA Region

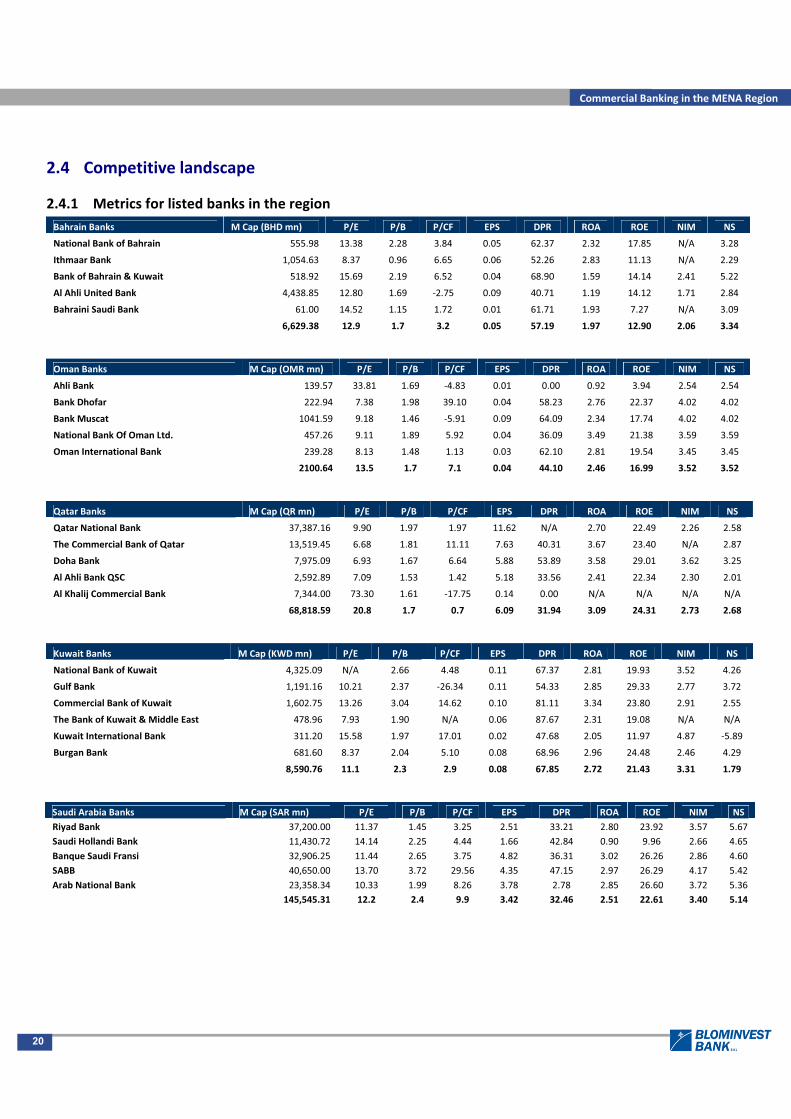

2.4 Competitive landscape

2.4.1 Metrics for listed banks in the regionBahrain Banks M Cap (BHD mn) P/E P/B P/CF EPS DPR ROA ROE NIM NS

National Bank of Bahrain 555.98 13.38 2.28 3.84 0.05 62.37 2.32 17.85 N/A 3.28

Ithmaar Bank 1,054.63 8.37 0.96 6.65 0.06 52.26 2.83 11.13 N/A 2.29

Bank of Bahrain & Kuwait 518.92 15.69 2.19 6.52 0.04 68.90 1.59 14.14 2.41 5.22

Al Ahli United Bank 4,438.85 12.80 1.69 2.75 0.09 40.71 1.19 14.12 1.71 2.84

Bahraini Saudi Bank 61.00 14.52 1.15 1.72 0.01 61.71 1.93 7.27 N/A 3.09

6,629.38 12.9 1.7 3.2 0.05 57.19 1.97 12.90 2.06 3.34

Oman Banks M Cap (OMR mn) P/E P/B P/CF EPS DPR ROA ROE NIM NS

Ahli Bank 139.57 33.81 1.69 4.83 0.01 0.00 0.92 3.94 2.54 2.54

Bank Dhofar 222.94 7.38 1.98 39.10 0.04 58.23 2.76 22.37 4.02 4.02

Bank Muscat 1041.59 9.18 1.46 5.91 0.09 64.09 2.34 17.74 4.02 4.02

National Bank Of Oman Ltd. 457.26 9.11 1.89 5.92 0.04 36.09 3.49 21.38 3.59 3.59

Oman International Bank 239.28 8.13 1.48 1.13 0.03 62.10 2.81 19.54 3.45 3.45

2100.64 13.5 1.7 7.1 0.04 44.10 2.46 16.99 3.52 3.52

Qatar Banks M Cap (QR mn) P/E P/B P/CF EPS DPR ROA ROE NIM NS

Qatar National Bank 37,387.16 9.90 1.97 1.97 11.62 N/A 2.70 22.49 2.26 2.58

The Commercial Bank of Qatar 13,519.45 6.68 1.81 11.11 7.63 40.31 3.67 23.40 N/A 2.87

Doha Bank 7,975.09 6.93 1.67 6.64 5.88 53.89 3.58 29.01 3.62 3.25

Al Ahli Bank QSC 2,592.89 7.09 1.53 1.42 5.18 33.56 2.41 22.34 2.30 2.01

Al Khalij Commercial Bank 7,344.00 73.30 1.61 17.75 0.14 0.00 N/A N/A N/A N/A

68,818.59 20.8 1.7 0.7 6.09 31.94 3.09 24.31 2.73 2.68

Kuwait Banks M Cap (KWDmn) P/E P/B P/CF EPS DPR ROA ROE NIM NS

National Bank of Kuwait 4,325.09 N/A 2.66 4.48 0.11 67.37 2.81 19.93 3.52 4.26

Gulf Bank 1,191.16 10.21 2.37 26.34 0.11 54.33 2.85 29.33 2.77 3.72

Commercial Bank of Kuwait 1,602.75 13.26 3.04 14.62 0.10 81.11 3.34 23.80 2.91 2.55

The Bank of Kuwait & Middle East 478.96 7.93 1.90 N/A 0.06 87.67 2.31 19.08 N/A N/A

Kuwait International Bank 311.20 15.58 1.97 17.01 0.02 47.68 2.05 11.97 4.87 5.89

Burgan Bank 681.60 8.37 2.04 5.10 0.08 68.96 2.96 24.48 2.46 4.29

8,590.76 11.1 2.3 2.9 0.08 67.85 2.72 21.43 3.31 1.79

Saudi Arabia Banks M Cap (SAR mn) P/E P/B P/CF EPS DPR ROA ROE NIM NSRiyad Bank 37,200.00 11.37 1.45 3.25 2.51 33.21 2.80 23.92 3.57 5.67Saudi Hollandi Bank 11,430.72 14.14 2.25 4.44 1.66 42.84 0.90 9.96 2.66 4.65Banque Saudi Fransi 32,906.25 11.44 2.65 3.75 4.82 36.31 3.02 26.26 2.86 4.60SABB 40,650.00 13.70 3.72 29.56 4.35 47.15 2.97 26.29 4.17 5.42Arab National Bank 23,358.34 10.33 1.99 8.26 3.78 2.78 2.85 26.60 3.72 5.36

145,545.31 12.2 2.4 9.9 3.42 32.46 2.51 22.61 3.40 5.14

21

Commercial Banking in the MENA Region

Egypt Banks M Cap (EGP mn) P/E P/B P/CF EPS DPR ROA ROE NIM NS

Al Watany Bank of Egypt 3,940.00 16.17 3.69 12.44 2.44 19.82 0.97 11.39 3.14 6.84

Crédit Agricole Egypt 2,870.00 5.48 1.50 7.51 1.83 0.00 2.81 31.59 3.20 8.10

Piraeus Bank Egypt 655.65 62.20 0.99 2.10 0.18 N/A 0.17 1.60 1.72 4.84

Commercial International Bank (Egypt) 8,555.63 6.65 1.95 3.08 4.40 15.17 3.00 33.07 3.38 6.34

BLOM Bank Egypt 1,875.00 14.79 2.34 n/a 1.69 N/A 1.43 9.75 2.30 0.61

Ahli United Bank of Egypt 1,260.00 8.59 1.88 12.28 2.45 N/A 0.01 0.04 3.38 6.75

Export Development Bank of Egypt 1,100.00 3.54 0.80 5.78 3.11 N/A 3.04 28.36 2.37 4.97

20,256.28 16.8 1.9 3.1 2.30 11.66 1.63 16.54 2.78 5.49

Jordan Banks M Cap (JOD mn) P/E P/B P/CF EPS DPR ROA ROE NIM NS

Bank of Jordan 237.00 9.72 1.47 1.47 0.24 61.51 1.72 16.17 N/A 6.40

Jordan Commercial Bank 171.85 13.84 2.11 2.11 0.18 25.47 2.34 15.84 4.35 4.44

Arab Banking Corporation 9,078.00 15.14 1.78 1.78 1.43 14.00 2.15 12.11 N/A N/A

Arab Jordan Investment Bank 191.00 22.89 1.62 1.62 0.08 73.14 1.15 7.31 2.17 N/A

Jordan Kuwait Bank 627.00 N/A 3.87 3.87 0.44 33.80 2.42 21.94 N/A 4.21

Union Bank Limited 295.45 N/A 1.35 1.35 0.15 68.96 1.41 8.69 N/A 3.21

10,600.30 15.4 2.0 2.0 0.42 46.15 1.87 13.68 3.26 4.57

Lebanon Banks M Cap (LP mn) P/E P/B P/CF EPS DPR ROA ROE NIM NSBLC Bank 77.37 5.11 4.6 N/A 446.25 0 0.38 N/A N/A N/A

BLOM Bank 3,070,031.58 N/A N/A 1.68 1,266.16 434.38 1.31 15.71 3.05 3.05

Bank Audi 2,573.64 11.88 1.31 N/A 7,994.00 34.24 1.22 11.39 3.19 3.19

Bank of Beirut 1,140.37 16.13 2.45 N/A 1,637.73 31.57 0.81 12.67 2.43 2.43

Banque Bemo 64.64 N/A N/A N/A 750.87 N/A 0.79 11.32 1.79 1.79

Byblos Bank 752.24 7.98 1.08 1.16 340.63 46.36 1.05 13.61 2.76 2.76

3,074,639.84 10.3 2.4 1.4 2,072.61 109.31 0.93 12.94 2.64 2.64

UAE Banks M Cap (AED mn) P/E P/B P/CF EPS DPR ROA ROE NIM NS

Commercial Bank of Dubai 10,334.71 8.82 2.13 8.50 0.67 36.20 3.81 21.84 4.65 4.41

Mashreq Bank 39,524.50 19.12 3.76 2.38 12.98 0.00 2.63 22.37 2.76 4.94

Abu Dhabi Commercial Bank 13,323.70 6.65 1.12 1.79 0.42 60.38 2.12 18.10 2.80 3.12

Bank of Sharjah 5,142.92 9.07 1.36 7.81 0.32 77.35 4.39 18.39 6.31 5.14

Commercial Bank International 2,943.02 8.93 1.76 13.64 0.27 17.22 3.45 23.74 3.24 3.07

First Gulf Bank 16,775.00 5.79 1.07 301.52 1.46 12.45 3.32 21.02 N/A N/A

Invest Bank 3740.00 13.20 2.21 6.22 0.26 34.44 3.89 18.03 3.82 4.52

National Bank of Abu Dhabi 24,015.85 7.21 1.70 8.50 1.31 25.41 2.08 24.78 2.62 4.41

National Bank of Fujairah 8,250.00 25.41 4.62 14.05 0.29 50.95 3.10 19.19 4.24 4.54

National Bank of Umm Al Qaiwain 7,682.40 18.83 2.77 2.98 0.34 0.00 5.00 21.28 7.77 6.02

National Bank Of Ras Al Khaima 5,143.17 8.72 2.60 N/A 0.54 N/A 4.05 28.43 6.80 N/A

United Arab Bank 6,823.36 28.16 5.11 9.96 0.27 37.04 3.85 17.79 5.14 4.84

Union National Bank 7,968.75 4.75 1.06 4.86 0.62 26.75 2.41 18.70 2.99 3.49

151,667.38 12.7 2.4 30.8 1.52 31.52 3.39 21.05 4.43 4.41

Sources: Zawya, Bloomberg and BlomInvest Research

22

Commercial Banking in the MENA Region

2.4.2 Multiples ComparisonKuwaiti banks offer the maximum value in the region. Listed Kuwaiti banks are currently trading at 11.1x earnings and 2.3x book value multiples – aclear discount to other regional peers.

Saudi and UAE banks follow next given the prevailing numbers. While Saudi banks are trading at 12.2x and 2.4x book value, UAE banks are trading at12.7x earnings and 2.4x book value multiples, respectively.

The Omani banking sector, despite years of strong growth, remains rather under penetrated. Similar to Bahrain, however, the sector suffers fromsmall market capitalizations and low trading volumes. In this respect, the Kuwaiti banks fare better, with three stocks trading above USD 10 mn a dayand seven trading USD 5 mn or more a day. Qatar is a preferred banking sector in terms of economic fundamentals and banking asset growth, Qataribanks are trading at a significant PE premium to most MENA banks for a given earnings growth rate.

Bahrain is likely to be less attractive from a long term growth perspective, given high sector penetration, limited oil and gas reserves and a smallpopulation. Furthermore, the banking stocks have relatively small market capitalizations and are rather illiquid from a volume and value tradedperspective.

Among the non GCC countries, Lebanese banks are the most attractive, while the Egyptian and Jordanian counterparts are the most unattractivegiven their expensive valuation and lower earnings growth relative to most MENA banking stocks. Banks in Lebanon are trading at 10.3x earnings and2.4x book value multiples, a clear discount to Egypt and Jordan. This can be primarily attributed to lower banking penetration indicated by the lowerloan to GDP ratio. Structural reforms in Lebanon and the impact of the global crisis on the region are likely to be the critical factors to watch out for.

2.5 Recent Developments in the regionSaudi Arabia12 Oct 08

17 Oct 08

21 Oct 08

30 Oct 08

23 Nov 08

Saudi Arabia Monetary Agency (SAMA) cuts its Repo Rate by 50 bps, to 5.00% from 5.50%. Deposit rate on hold at2.00%SAMA lowers the reserve requirement, to 10% from 13%

The Kingdom of Saudi Arabia guarantees all bank deposits

SAMA injects USD2 3 bn into the banking system in the form of US Dollar deposits.

SAMA cuts its repo rate cut by 100 bps, to 4.00% from 5.00%, leaving the reverse repo unchanged at 2.00%.