commercial law: deposit accounts and cash proceeds

TRANSCRIPT

Commercial Law: Deposit Accounts and Cash Proceeds

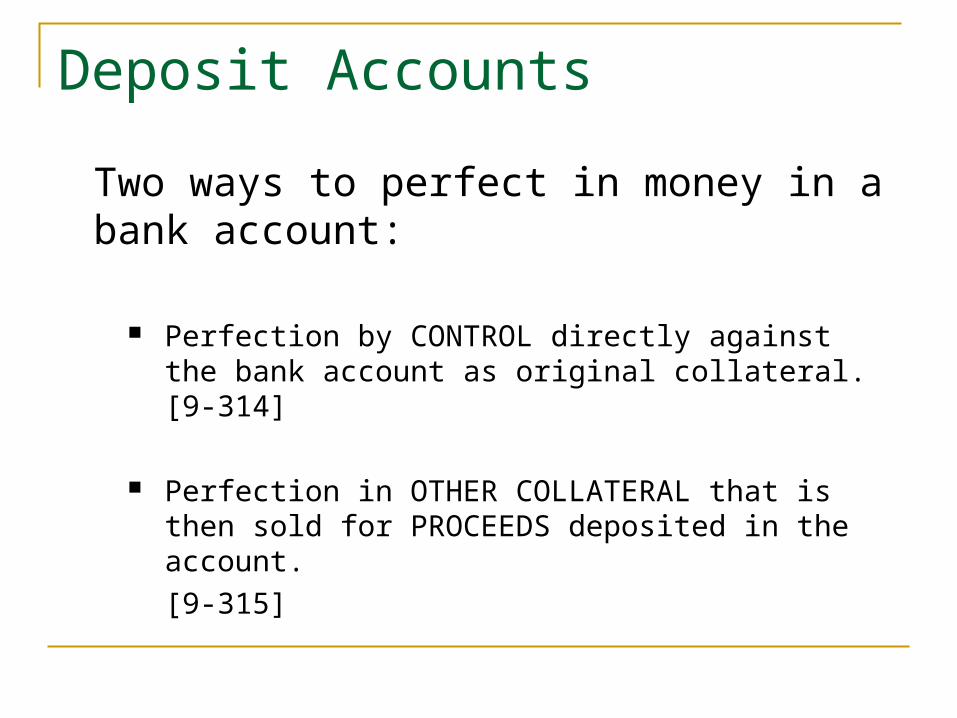

Deposit Accounts

Two ways to perfect in money in a bank account:

Perfection by CONTROL directly against the bank account as original collateral. [9-314]

Perfection in OTHER COLLATERAL that is then sold for PROCEEDS deposited in the account.

[9-315]

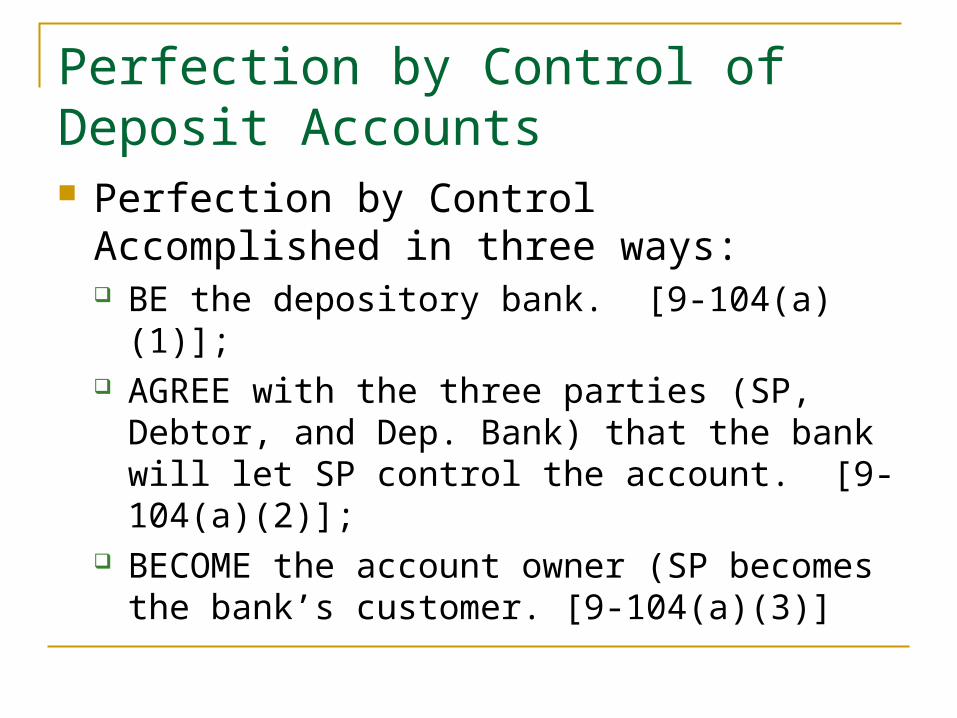

Perfection by Control of Deposit Accounts Perfection by Control Accomplished in three

ways: BE the depository bank. [9-104(a)(1)]; AGREE with the three parties (SP, Debtor, and

Dep. Bank) that the bank will let SP control the account. [9-104(a)(2)];

BECOME the account owner (SP becomes the bank’s customer. [9-104(a)(3)]

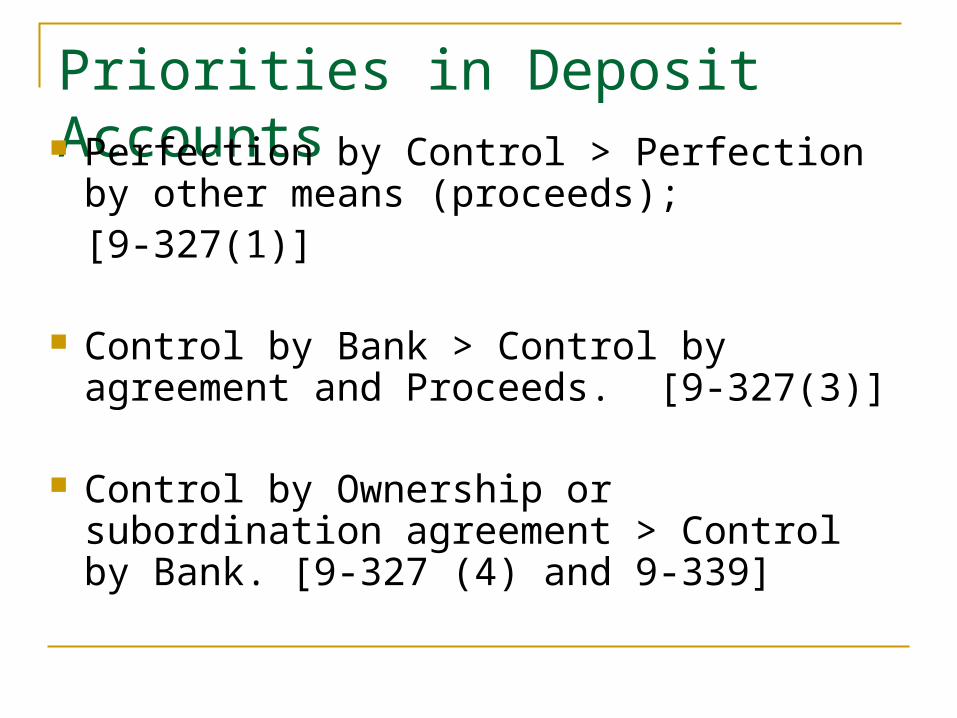

Priorities in Deposit Accounts Perfection by Control > Perfection by other

means (proceeds); [9-327(1)]

Control by Bank > Control by agreement and Proceeds. [9-327(3)]

Control by Ownership or subordination agreement > Control by Bank. [9-327 (4) and 9-339]

Advanced Priority in Deposit Accounts Control > Control in order of TIME. [9-327(2)]

Proceeds > Proceeds in order of priorities in original security interest.

Moving Money in Deposit Accounts

What to do about money that LEAVES the bank account (can you go get it back?)

What to do about money that STAYS and is COMMINGLED in the bank account (whose money is whose?)

Part I: Transfers Out of Bank Accounts Money (proceeds OR original collateral) that is transferred to

someone else out of a bank account is free and clear once it is transferred. [9-332]

Example: I sell inventory, deposit proceeds in a bank account. I then write a check on the bank account to pay for groceries. The grocery store is free and clear.

Collusion standard: If the transferee COLLUDES with the debtor to transfer the money, the court can undo the payment. [9-332(a), (b)]

Part II: Commingling and Tracing

What about money that stays in the bank account?

The problem: money that is proceeds of sales of collateral gets mixed with non-proceeds money in the same account.

USUAL case: merchant mixes proceeds from sales of inventory in with everything else in his general operating account.

Commingling (con’t)

Commingling isn’t a problem if the SP has a DIRECT interest, secured by control, in the bank account. Then, all the money that comes into that account is collateral.

Commingling IS a problem for proceeds of sales of collateral.

Tracing

Most common tracing rule is Lowest Intermediate Balance. (non-Code law). [9-315(b)(2)]

This is a rule of logic: if the account balance drops below the amount of proceeds deposited, then that amount of proceeds logically MUST have been dissipated.

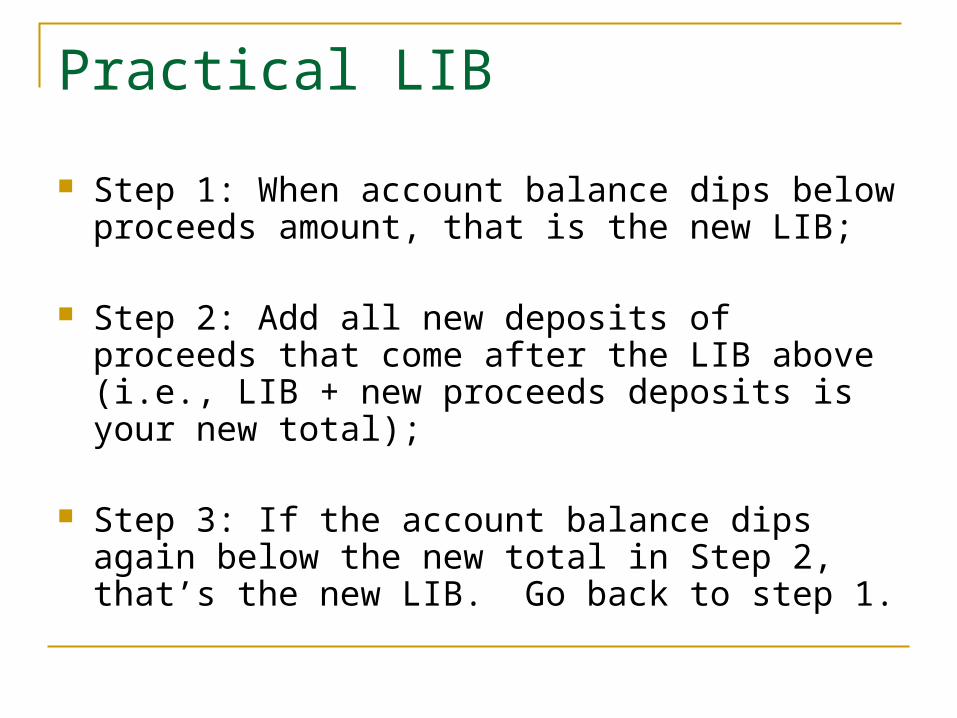

Practical LIB

Step 1: When account balance dips below proceeds amount, that is the new LIB;

Step 2: Add all new deposits of proceeds that come after the LIB above (i.e., LIB + new proceeds deposits is your new total);

Step 3: If the account balance dips again below the new total in Step 2, that’s the new LIB. Go back to step 1.

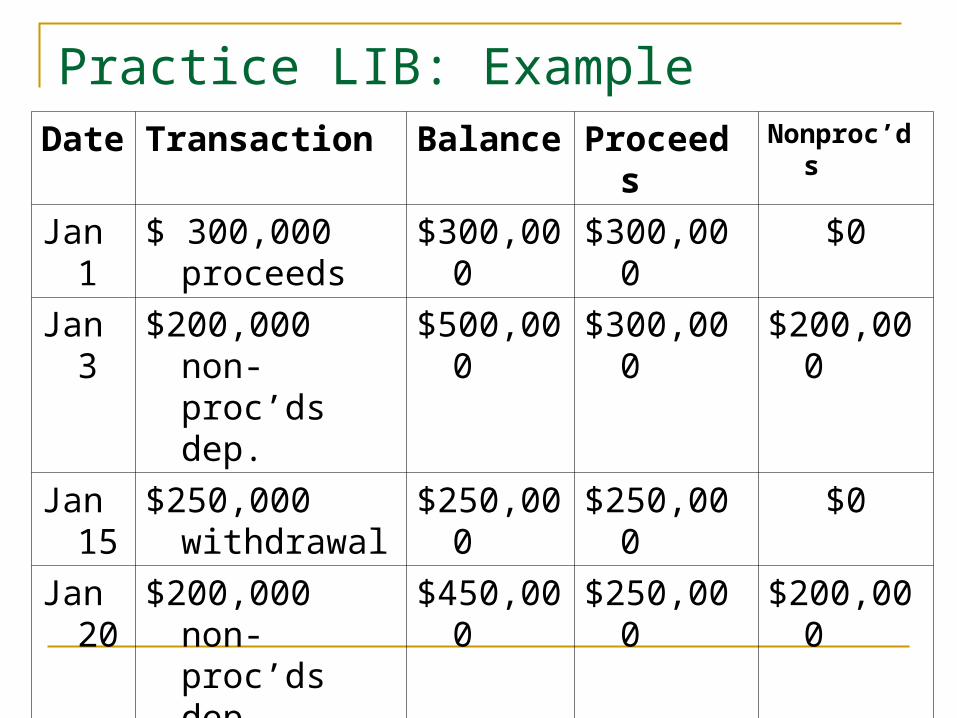

Practice LIB: ExampleDate Transaction Balance Proceeds Nonproc’ds

Jan 1

$ 300,000 proceeds

$300,000 $300,000 $0

Jan 3

$200,000 non-proc’ds dep.

$500,000 $300,000 $200,000

Jan 15

$250,000 withdrawal

$250,000 $250,000 $0

Jan 20

$200,000 non- proc’ds dep.

$450,000 $250,000 $200,000

(LIB) $250,000

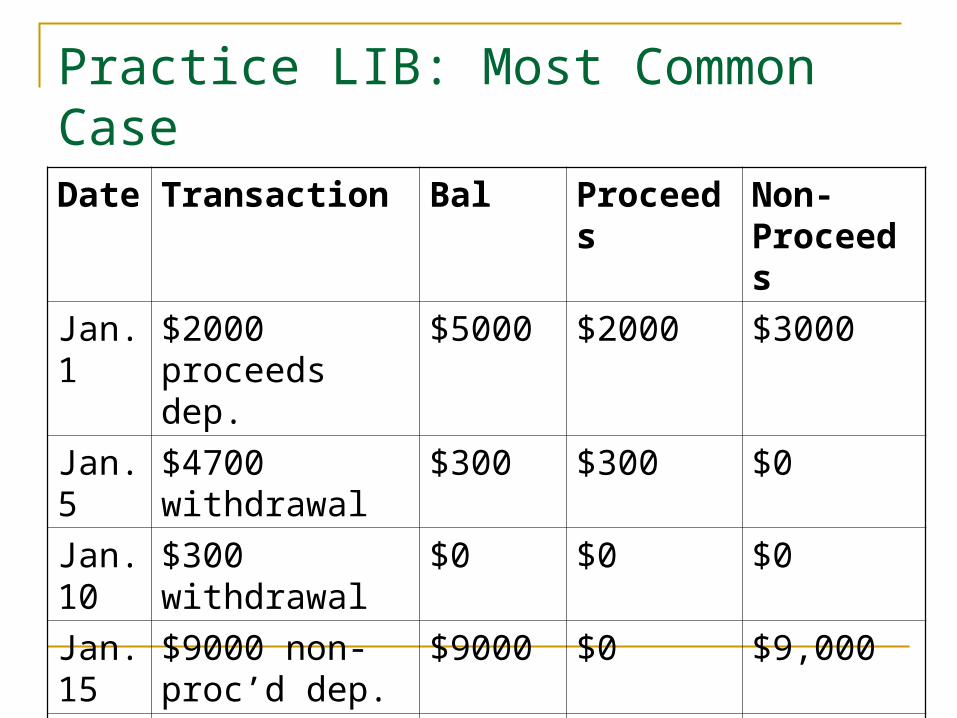

Practice LIB: Most Common CaseDate Transaction Bal Proceeds Non-

Proceeds

Jan. 1

$2000 proceeds dep.

$5000 $2000 $3000

Jan. 5

$4700 withdrawal

$300 $300 $0

Jan. 10

$300 withdrawal

$0 $0 $0

Jan. 15

$9000 non-proc’d dep.

$9000 $0 $9,000

LIB: $0

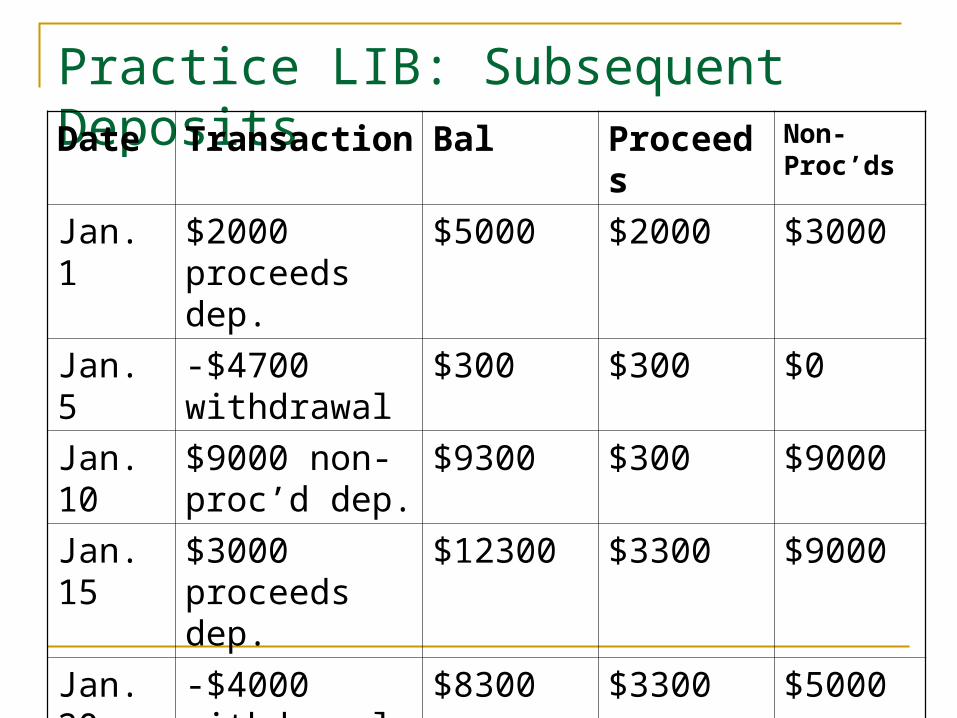

Practice LIB: Subsequent DepositsDate Transaction Bal Proceeds Non-

Proc’ds

Jan. 1 $2000 proceeds dep.

$5000 $2000 $3000

Jan. 5 -$4700 withdrawal

$300 $300 $0

Jan. 10

$9000 non-proc’d dep.

$9300 $300 $9000

Jan. 15

$3000 proceeds dep.

$12300 $3300 $9000

Jan. 20

-$4000 withdrawal

$8300 $3300 $5000

LIB: $3300

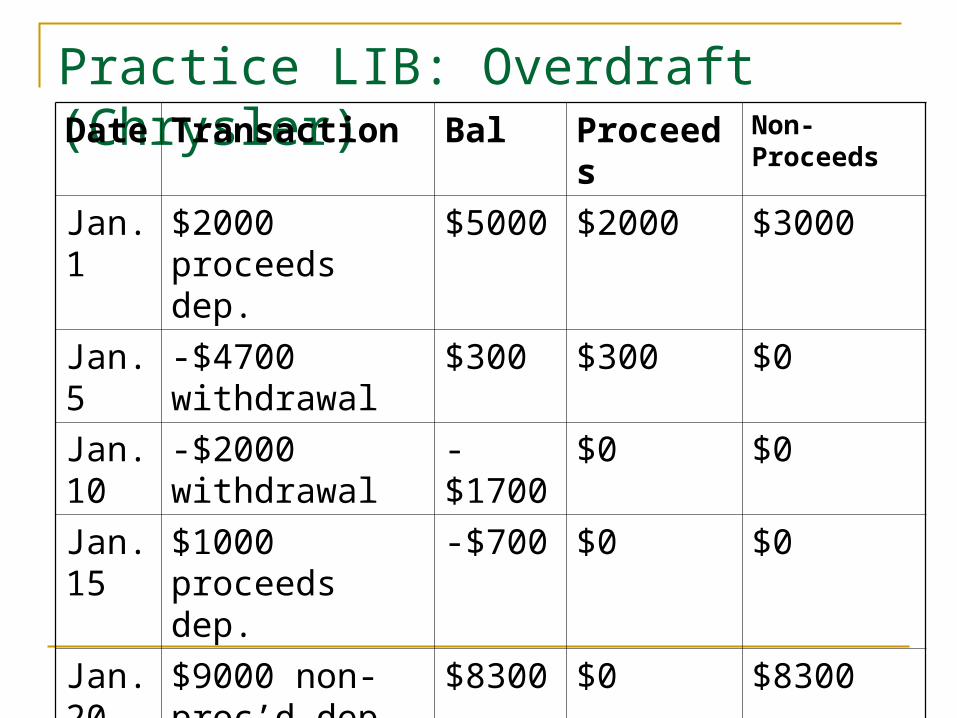

Practice LIB: Overdraft (Chrysler)Date Transaction Bal Proceeds Non-

Proceeds

Jan. 1

$2000 proceeds dep.

$5000 $2000 $3000

Jan. 5

-$4700 withdrawal

$300 $300 $0

Jan. 10

-$2000 withdrawal

-$1700 $0 $0

Jan. 15

$1000 proceeds dep.

-$700 $0 $0

Jan. 20

$9000 non-proc’d dep.

$8300 $0 $8300

LIB: $0

So What do Sophisticated Parties Do? Perfect in pledgeable collateral (chattel

paper, notes) by possession, to prevent sales to third parties;

Create lock-box accounts that limit the debtor’s ability to commingle and transfer proceeds.

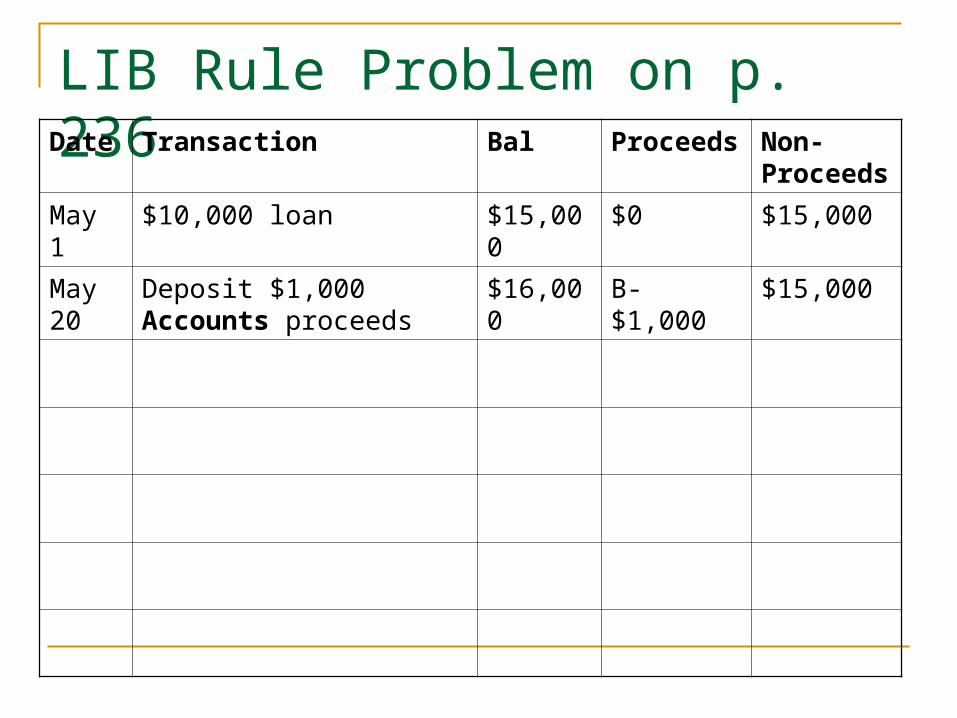

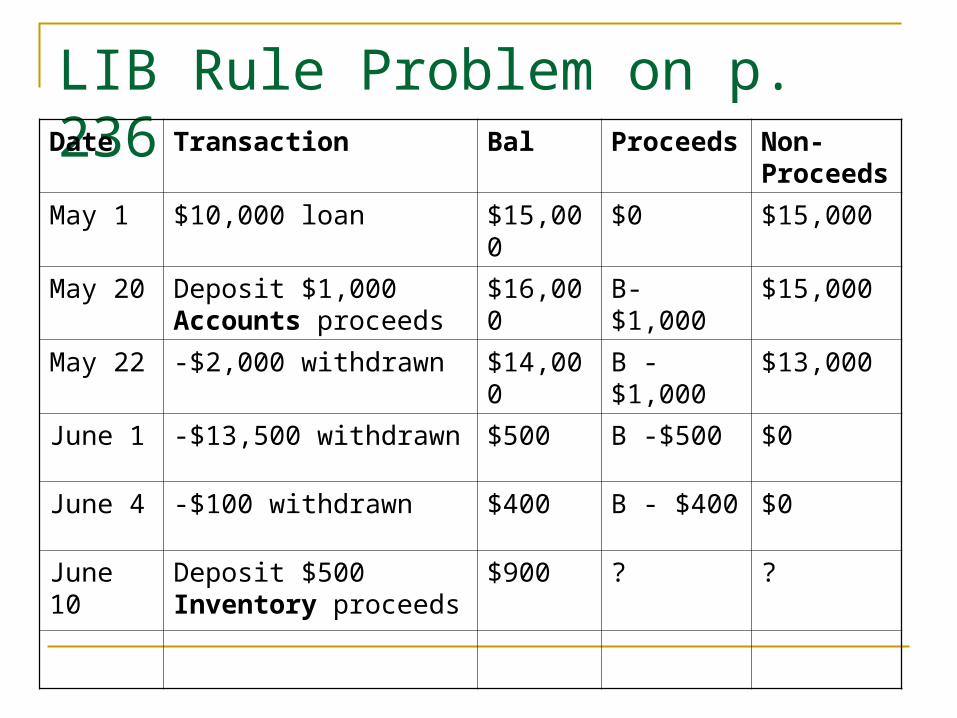

LIB Rule Problem on p. 236Date Transaction Bal Proceeds Non-

Proceeds

May 1 $10,000 loan $15,000 $0 $15,000

May 20

Deposit $1,000 Accounts proceeds

$16,000 B- $1,000 $15,000

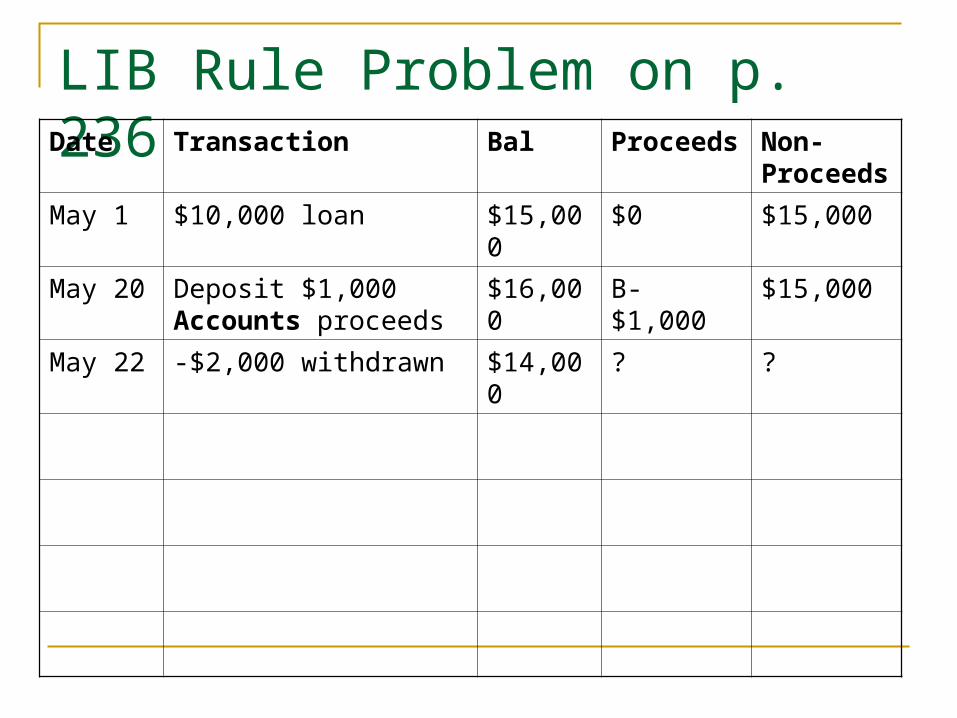

LIB Rule Problem on p. 236Date Transaction Bal Proceeds Non-

Proceeds

May 1 $10,000 loan $15,000 $0 $15,000

May 20 Deposit $1,000 Accounts proceeds

$16,000 B- $1,000 $15,000

May 22 -$2,000 withdrawn $14,000 ? ?

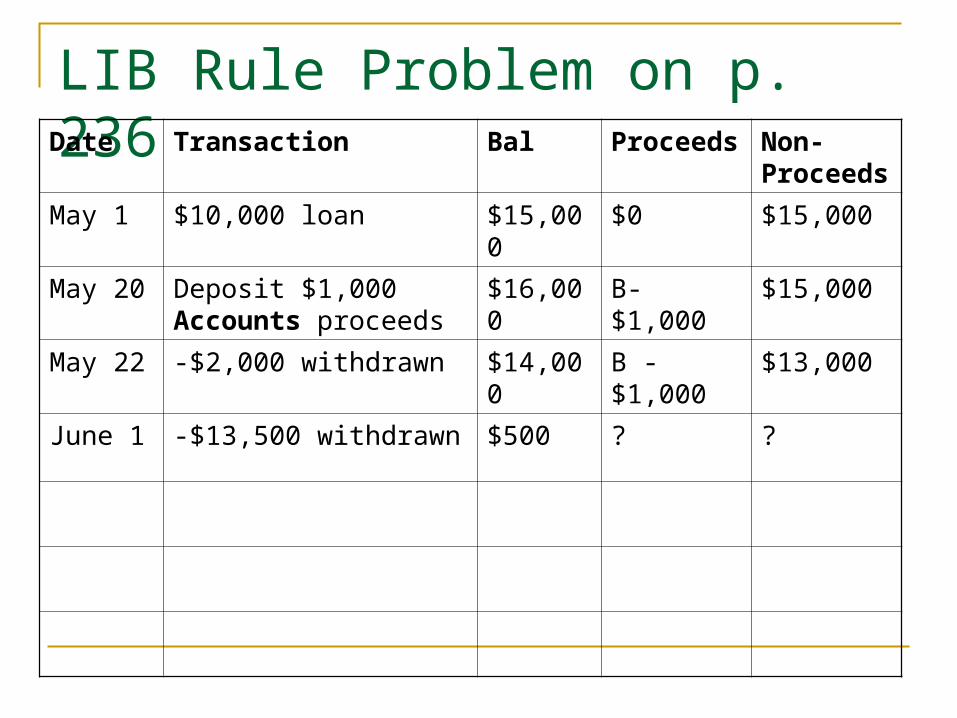

LIB Rule Problem on p. 236Date Transaction Bal Proceeds Non-

Proceeds

May 1 $10,000 loan $15,000 $0 $15,000

May 20 Deposit $1,000 Accounts proceeds

$16,000 B- $1,000 $15,000

May 22 -$2,000 withdrawn $14,000 B -$1,000 $13,000

June 1 -$13,500 withdrawn $500 ? ?

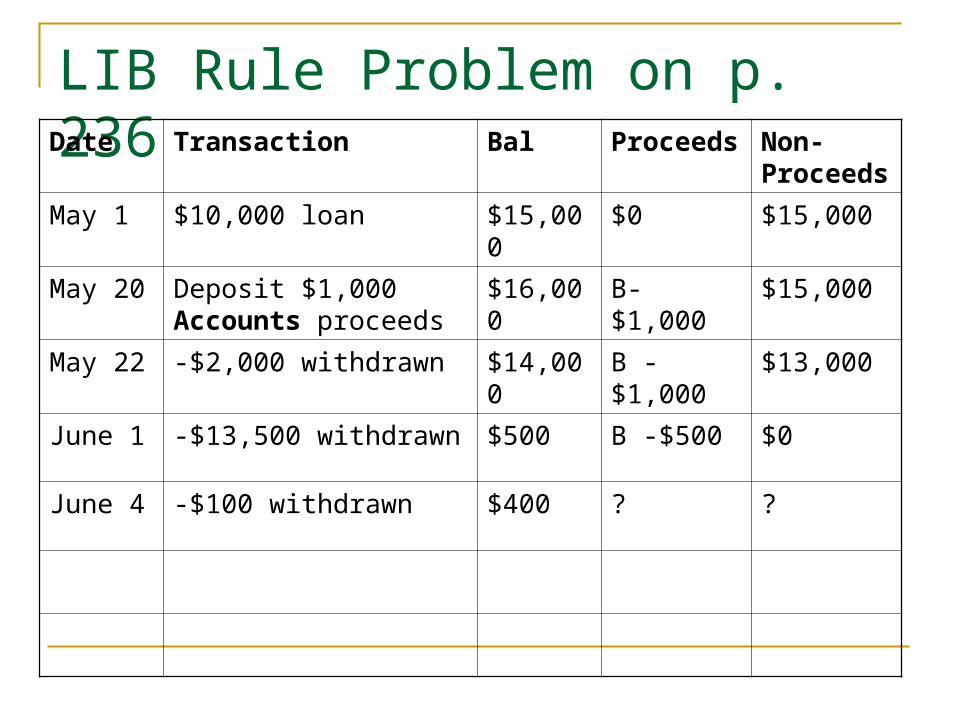

LIB Rule Problem on p. 236Date Transaction Bal Proceeds Non-

Proceeds

May 1 $10,000 loan $15,000 $0 $15,000

May 20 Deposit $1,000 Accounts proceeds

$16,000 B- $1,000 $15,000

May 22 -$2,000 withdrawn $14,000 B -$1,000 $13,000

June 1 -$13,500 withdrawn $500 B -$500 $0

June 4 -$100 withdrawn $400 ? ?

LIB Rule Problem on p. 236Date Transaction Bal Proceeds Non-

Proceeds

May 1 $10,000 loan $15,000 $0 $15,000

May 20 Deposit $1,000 Accounts proceeds

$16,000 B- $1,000 $15,000

May 22 -$2,000 withdrawn $14,000 B -$1,000 $13,000

June 1 -$13,500 withdrawn $500 B -$500 $0

June 4 -$100 withdrawn $400 B - $400 $0

June 10 Deposit $500 Inventory proceeds

$900 ? ?

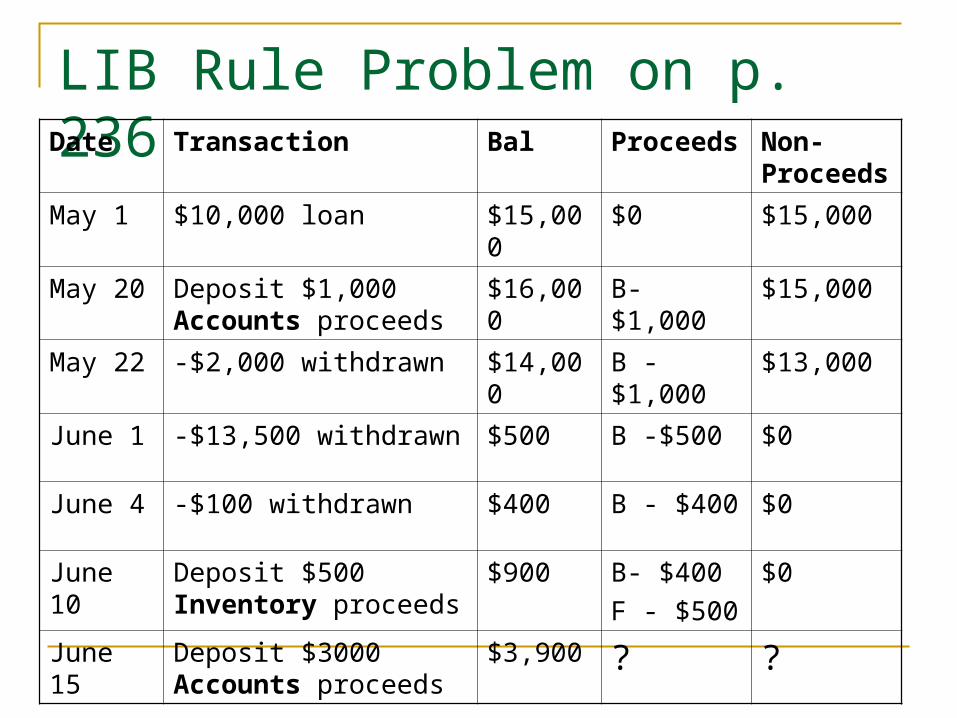

LIB Rule Problem on p. 236Date Transaction Bal Proceeds Non-

Proceeds

May 1 $10,000 loan $15,000 $0 $15,000

May 20 Deposit $1,000 Accounts proceeds

$16,000 B- $1,000 $15,000

May 22 -$2,000 withdrawn $14,000 B -$1,000 $13,000

June 1 -$13,500 withdrawn $500 B -$500 $0

June 4 -$100 withdrawn $400 B - $400 $0

June 10 Deposit $500 Inventory proceeds

$900 B- $400

F - $500

$0

June 15 Deposit $3000 Accounts proceeds

$3,900 ? ?

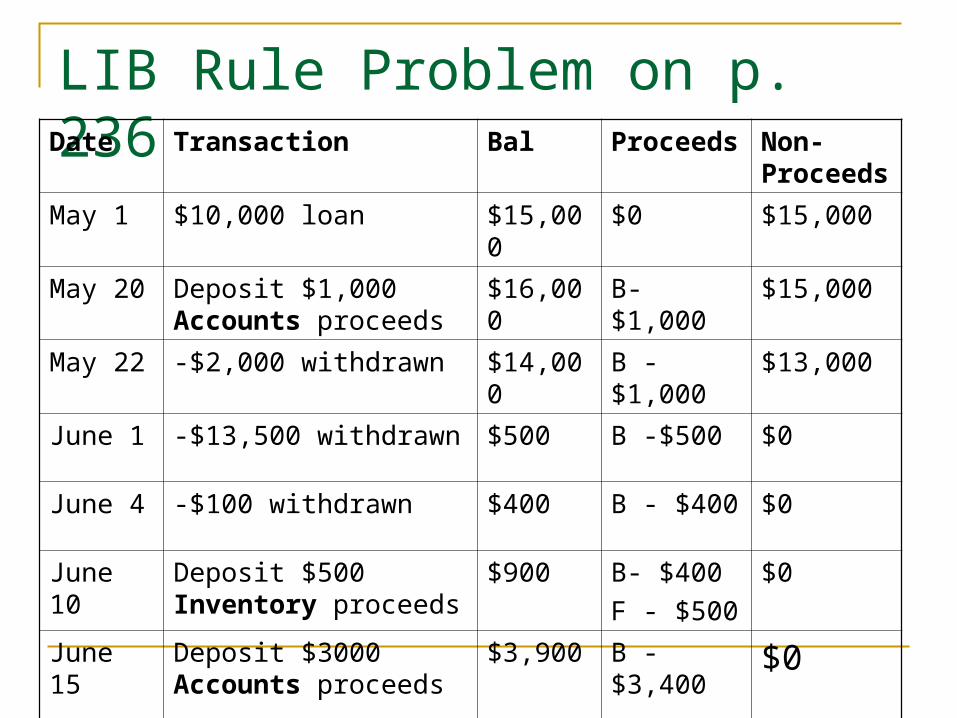

LIB Rule Problem on p. 236Date Transaction Bal Proceeds Non-

Proceeds

May 1 $10,000 loan $15,000 $0 $15,000

May 20 Deposit $1,000 Accounts proceeds

$16,000 B- $1,000 $15,000

May 22 -$2,000 withdrawn $14,000 B -$1,000 $13,000

June 1 -$13,500 withdrawn $500 B -$500 $0

June 4 -$100 withdrawn $400 B - $400 $0

June 10 Deposit $500 Inventory proceeds

$900 B- $400

F - $500

$0

June 15 Deposit $3000 Accounts proceeds

$3,900 B -$3,400

F -$500 $0