commercial refrigeration - refrigerated display and ... · product profile: commercial...

TRANSCRIPT

A joint initiative of Australian, State and Territory and New Zealand

Governments

Commercial Refrigeration -

Refrigerated Display and

Storage Cabinets

Product Profile: Commercial Refrigeration - Refrigerated Display and Storage Cabinets ii

This work is licensed under the Creative Commons Attribution 3.0 Australia Licence. To view a copy of this

license, visit http://creativecommons.org/licences/by/3.0/au

The Department of Resources, Energy and Tourism on behalf of the Equipment Energy Efficiency Program

asserts the right to be recognised as author of the original material in the following manner:

© Commonwealth of Australia (Department of Resources, Energy and Tourism) 2013.

The material in this publication is provided for general information only, and on the understanding that the

Australian Government is not providing professional advice. Before any action or decision is taken on the

basis of this material the reader should obtain appropriate independent professional advice.

This document is available at www.energyrating.gov.au

While reasonable efforts have been made to ensure that the contents of this publication are factually correct,

E3 does not accept responsibility for the accuracy or completeness of the content, and shall not be liable for

any loss or damage that may be occasioned directly or indirectly through the use of, or reliance on, the

contents of this publication.

ISBN 978-1-921516-08-5

Product Profile: Commercial Refrigeration - Refrigerated Display and Storage Cabinets iii

Contents

EXECUTIVE SUMMARY ............................................................................................................................................ I Background ........................................................................................................................................................... i The Refrigerated Display Cabinet and Refrigerated Storage Cabinet Market ................................................. ii Proposed Standards ............................................................................................................................................ ii The Possible Case for Regulation ....................................................................................................................... ii Market Barriers .................................................................................................................................................. iii Policy Options..................................................................................................................................................... iii Market Size and Energy Use .............................................................................................................................. iii Conclusion .......................................................................................................................................................... iv Consultation on this Product Profile .................................................................................................................. v Key Questions ..................................................................................................................................................... vi

1. INTRODUCTION ........................................................................................................................................... 1 What is a Product Profile? .................................................................................................................................. 1 Outline of the Product Profile ............................................................................................................................. 1 The Policy Context............................................................................................................................................... 2 History of E3 Regulation .................................................................................................................................... 3

2. REFRIGERATED DISPLAY CABINETS AND REFRIGERATED STORAGE CABINETS .......................... 4 Equipment Covered by this Product Profile ...................................................................................................... 4 Design of RDCs and RSCs ................................................................................................................................... 6 Trends in Energy Performance ........................................................................................................................... 9 Energy Efficiency Potential ................................................................................................................................ 11

3. THE RDC AND RSC MARKET ................................................................................................................... 16 Characteristics of the Market ............................................................................................................................ 16 Energy Use ......................................................................................................................................................... 19 Stock and Sales .................................................................................................................................................. 22 Registrations for Refrigerated Display Cabinets in Australia and New Zealand ........................................... 25 Forecast Energy Use and Stock ........................................................................................................................ 29 Modelling Business as Usual Energy Use and Stock ....................................................................................... 31 Modelling Greenhouse Gas Emissions from Energy Use ................................................................................ 32

4. TESTING AND PERFORMANCE STANDARDS ....................................................................................... 34 Current Test and Performance Standards ....................................................................................................... 34 Summary of Commercial Refrigeration Energy Efficiency Regulation .......................................................... 36 Future Developments ........................................................................................................................................ 37

5. POLICY OPTIONS TO ADDRESS MARKET FAILURES .......................................................................... 40 Barriers to Investment in Energy Efficient Commercial Refrigerated Cabinets ............................................ 40 Policy Responses to Identified Market Failures .............................................................................................. 42 Addressing Information Barrier Failures: Consumer Education and Information Dissemination .............. 44

6. REFERENCES ............................................................................................................................................ 47

Product Profile: Commercial Refrigeration - Refrigerated Display and Storage Cabinets iv

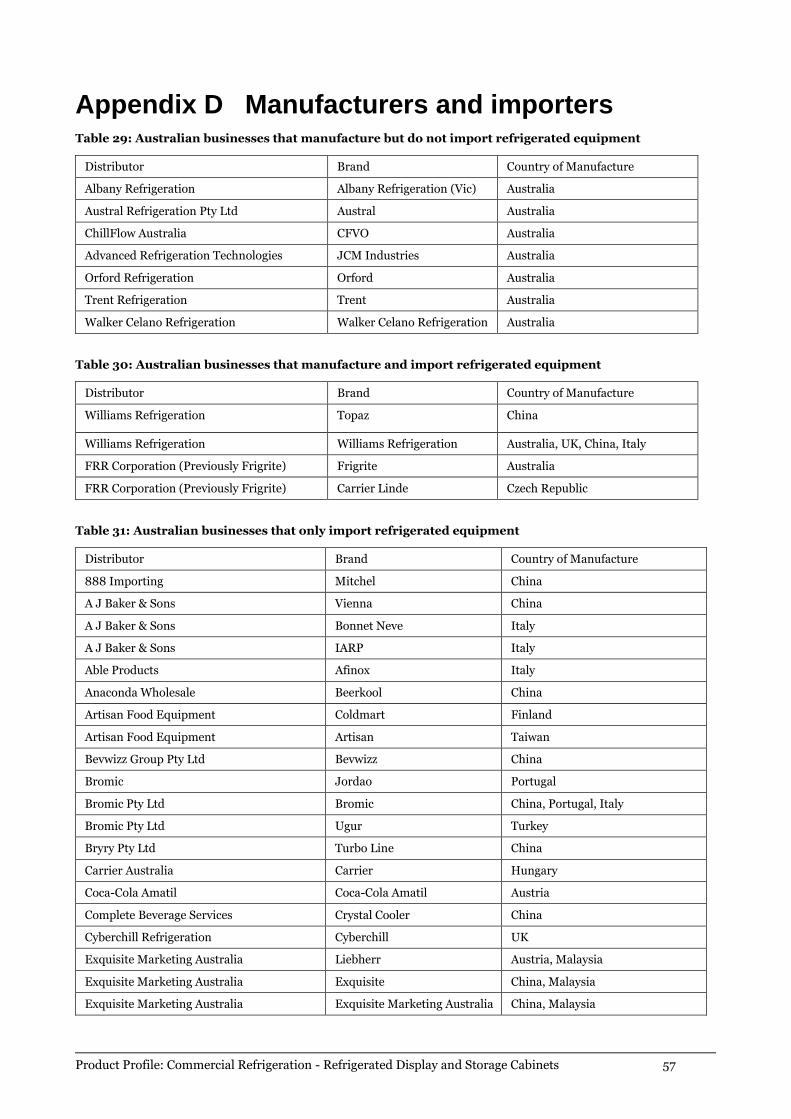

APPENDICES .......................................................................................................................................................... 49 Appendix A List of assumptions used in document ..................................................................................... 49 Appendix B Data tables supporting energy and greenhouse modelling ..................................................... 51 Appendix C Summary of classification system............................................................................................. 54 Appendix D Manufacturers and importers .................................................................................................. 57 Appendix E Australian and New Zealand RDC MEPS and HEPS levels .................................................... 61 Appendix F Summary of Test Methods ........................................................................................................ 63

LIST OF TABLES

Table 1: Common refrigerant gases .................................................................................................................................. 8 Table 2: Characteristics of registered refrigerated display cabinet models 2006-2012 .............................................. 10 Table 3: Energy efficiency improvement options for refrigerated display and storage cabinets ................................ 14 Table 4: European estimates of improvement potential and costs for energy saving technologies in refrigerated

display and storage cabinets ........................................................................................................................................... 15 Table 5: Proportion of cabinets by end-use, Australia and New Zealand combined ................................................... 18 Table 6: Estimated stock and sales of refrigeration products in Australia ................................................................... 19 Table 7: Electricity used by commercial refrigeration ................................................................................................... 20 Table 8: Energy used by refrigerators in supermarkets and other food service providers .......................................... 21 Table 9: Summary of energy used by commercial refrigeration as reported ............................................................... 22 Table 10: Baseline energy use by the equipment (2008) .............................................................................................. 22 Table 11: Stock and sales of refrigerated display cabinets reported in 2000 ............................................................... 23 Table 12: EU-25 stock of products .................................................................................................................................. 23 Table 13: Comparison of EU-25 and Australia stock levels ........................................................................................... 24 Table 14: Data used to estimate stock and sales ............................................................................................................ 24 Table 15: Estimated stock and sales of RDCs in Australia and New Zealand in 2013 (units) ..................................... 25 Table 16: Commercial refrigeration equipment annual demand growth by region ..................................................... 30 Table 17: Worldwide commercial refrigeration equipment annual demand growth ................................................... 30 Table 18: Summary of International Energy Efficiency Programs ............................................................................... 36 Table 19: RDC market sectors and their current purchasing drivers ........................................................................... 43 Table 20: List of assumptions used in this document ................................................................................................... 49 Table 21: Emissions intensity and electricity cost forecast data ................................................................................... 50 Table 22: Integral Cabinets – Business as usual model ................................................................................................ 51 Table 23: Remote Cabinets – Business as usual model ................................................................................................. 52 Table 24: Refrigerated Storage Cabinets – Business as usual model ........................................................................... 53 Table 25: Types of Remote Refrigerated Cabinets (Medium Temperature) Table A1 of AS 1731.14:2003 ................ 54 Table 26: Types of Remote Refrigerated Cabinets (Low Temperature) Table A2 of AS 1731.14:2003 ....................... 55 Table 27: Types of Integral Refrigerated Cabinets Table A3 of AS 1731.14:2003 ........................................................ 56 Table 28: M-package Temperature Classes ................................................................................................................... 56 Table 29: Australian businesses that manufacture but do not import refrigerated equipment .................................. 57 Table 30: Australian businesses that manufacture and import refrigerated equipment ............................................ 57 Table 31: Australian businesses that only import refrigerated equipment .................................................................. 57 Table 32: New Zealand businesses that manufacture but do not import refrigerated equipment ............................. 59 Table 33: New Zealand businesses that manufacture and import refrigerated equipment ........................................ 59 Table 34: New Zealand businesses that only import refrigerated equipment ............................................................. 60 Table 35: MEPS: Maximum energy consumption – Remote cabinets ......................................................................... 61 Table 36: MEPS: Maximum energy consumption – Integral cabinets ......................................................................... 62 Table 37: Maximum energy consumption for ‘High Efficiency’ integral display cabinets .......................................... 62 Table 38: Summary of common test methods ............................................................................................................... 63

Product Profile: Commercial Refrigeration - Refrigerated Display and Storage Cabinets v

LIST OF FIGURES

Figure 1: Examples of Refrigerated Display Cabinets ...................................................................................................... 5 Figure 2: Examples of Refrigerated Storage Cabinets ..................................................................................................... 6 Figure 3: Major components and energy flows of the refrigeration cycle ...................................................................... 7 Figure 4: Long-term trends in domestic refrigerator volume, energy use and unit price, Australia ........................... 11 Figure 5: Overview of the Australian and New Zealand markets for refrigerated cabinets..........................................17 Figure 6: Cabinet trade between Australia and New Zealand ....................................................................................... 18 Figure 7: Electricity used by commercial refrigerators in Australia and New Zealand ............................................... 21 Figure 8: Registered sales of remote RDCs in New Zealand ......................................................................................... 25 Figure 9: Registered sales of integral RDCs in New Zealand ........................................................................................ 26 Figure 10: Registered remote RDCs from the E3 Registration Database ..................................................................... 27 Figure 11: Registered integral RDCs from the E3 Registration Database..................................................................... 27 Figure 12: Share of registered RDCs registered as high efficiency ................................................................................ 28 Figure 13: VC4 - Glass door cabinet registrations.......................................................................................................... 28 Figure 14: Cabinets registered for MEPS that could be registered for HEPS ............................................................... 29 Figure 15: Business as usual energy use forecast for Australia ..................................................................................... 31 Figure 16: Business as usual energy use forecast for New Zealand .............................................................................. 32 Figure 17: Greenhouse gas emissions from electricity use forecast, Australia ............................................................. 33 Figure 18: Greenhouse gas emissions from electricity use forecast, New Zealand ...................................................... 33

Product Profile: Commercial Refrigeration - Refrigerated Display and Storage Cabinets vi

GLOSSARY AND ABBREVIATIONS

AGO Australian Greenhouse Office

AS/NZS Australian Standards and New Zealand Standards

BAU Business-as-usual

CO2-e Carbon dioxide equivalent units

COAG Council of Australian Governments

DCCEE Department of Climate Change and Energy Efficiency

DRET Department of Resources, Energy and Tourism

E3 Equipment Energy Efficiency

ECM Electronically Commutated Motor

EEO Energy Efficiency Opportunities

EUP Energy Using Products

GEMS Greenhouse and Energy Minimum Standards

GEMS Act Greenhouse and Energy Minimum Standards Act 2012

GHG Greenhouse Gas

GWh Giga Watt hour – 1 million kilo Watt hours

GWP Global warming potential

HEPS High Efficiency Performance Standards

HFC Hydrofluorocarbons

HFO Hydrofluoroolefins

ICs Integral Cabinets

Kt Kilo tonnes – 1 thousand tonnes

kWh Kilo Watt hour – 1 thousand Watt hours

LED Light Emitting Diode

MCE Ministerial Council for Energy

MEPS Minimum Energy Performance Standards

Mt Mega tonnes – 1 million tonnes

NFEE National Framework on Energy Efficiency

NPV Net Present Value

NSEE National Strategy on Energy Efficiency

NZ New Zealand

NZEECS New Zealand Energy Efficiency and Conservation Strategy 2011-2016

NZES New Zealand Energy Strategy

NZMBIE New Zealand Ministry of Business, Innovation and Employment

PID Proportional Integral Differential

RCs Remote Cabinets

RDCs Refrigerated Display Cabinets

RDC Determination

Greenhouse and Energy Minimum Performance Standards (Refrigerated Display Cabinets) Determination 2012

RIS Regulatory Impact Statement

RSCs Refrigerated Storage Cabinets

RECs Renewable Energy Certificates

SCER Standing Council on Energy and Resources

Product Profile: Commercial Refrigeration - Refrigerated Display and Storage Cabinets vii

TEC/TDA Total Energy Consumption/Total Display Area. The standard metric for energy consumption for RDCs, which balances energy use per unit of area display

The equipment RDCs and RSCs

TTMRA Trans-Tasman Mutual Recognition Arrangement

VSD Variable Speed Drive

Product Profile: Commercial Refrigeration - Refrigerated Display and Storage Cabinets i

Executive Summary

Background

This Product Profile was prepared for the Equipment Energy Efficiency (E3) Committee to analyse the case for

altering the minimum energy performance standards (MEPS) for commercial refrigeration in Australia and

New Zealand.

Energy consumed by appliances and equipment is a major source of energy consumption and greenhouse gas

(GHG) emissions in Australia and New Zealand; non-domestic or commercial refrigeration is estimated to account

for 4% of emissions from Australia’s energy sector and 6% of emissions in New Zealand (E3 2011). The

governments of both countries have recognised that substantial reductions in energy use can be achieved by

improving the efficiency of non-domestic refrigeration.

To achieve this reduction in energy use, the E3 Program develops, amongst other things, the regulations for MEPS

and energy labelling for appliances and equipment. The aim is to improve the energy efficiency of products sold on

the Australian and New Zealand markets. MEPS already apply to a range of electrical products such as three-phase

motors, distribution transformers and three-phase air conditioners, and other domestic appliances, such as

refrigerators, lighting, and air conditioners also have mandatory energy labelling.

Australia and New Zealand introduced MEPS and high efficiency performance standards (HEPS) for refrigerated

display cabinets in 2004, as specified in AS 1731. The potential for further energy savings was investigated by the

E3 Committee in 2009 through producing ‘In From The Cold - a 10-year strategic plan for non-domestic

refrigeration’.

This Product Profile provides an overview of the market in Australia and New Zealand for non-domestic

refrigerated display and storage cabinets (RDCs and RSCs). It identifies what products are available, efficiency

trends in the market, major suppliers and the available information on the sales and installed stock of the

equipment. It seeks feedback on whether energy efficiency improvements are possible and reasons why more

efficient models aren’t dominating the market.

Excluded from the scope of AS 1731 and this Product Profile are:

• Refrigerated vending machines;

• Ice-makers; and

• Cabinets intended for use in catering and similar non-retail application.

None of the documents related to the development of these standards provide definitive reasons for the current

exclusion of RSCs. However, consultation with stakeholders who were involved in the early stages of developing

AS 1731 suggest the contribution of RSCs was considered too small to include at that time.

This document does not propose policy but rather indicates a variety of options for feedback from stakeholders,

and for the governments of Australia and New Zealand to consider. MEPS and voluntary labelling are included in

the short list of possible options, along with education measures. Any proposals for regulation will need to have

further analysis and public consultation through a Regulatory Impact Statement (RIS).

Product Profile: Commercial Refrigeration - Refrigerated Display and Storage Cabinets ii

The Refrigerated Display Cabinet and Refrigerated Storage Cabinet Market

The market for RDCs in Australia and New Zealand is complex and diverse. AS 1731, the standard which defines

the current MEPS, captures over 50 different products, across four temperature classes. These include units

ranging in size from multi-door cabinets in large supermarkets to counter-top glass cabinets designed to display

cakes.

Historic growth in the overall volume of refrigerated food, frozen foods and chilled beverages sold in supermarkets,

food retail and service establishments in Australia and New Zealand is expected to continue. As a result the total

estimated stock of RDCs is estimated to grow from 775,000 units in 2011 to approximately 1.4 million units in

2030. Data for the RSC market is less certain but is believed to be in the order of 10% of the RDC market.

Proposed Standards

The performance metrics in AS 1731 have not been changed since 2004, and there is concern that these standards

no longer represent a suitable minimum requirement for manufacturers. Energy intensity in the refrigeration

sector has trended down since 2004 and revisiting the standards could lead to cost effective outcomes for

consumers.

There was comment by some stakeholders questioned during the preliminary consultation phase of this project

that if AS 1731 is updated, Australia and New Zealand could adopt a standard aligned with the international

standard, ISO 23953, which is currently being developed. This new standard would set MEPS for RDCs, using

classes analogous to the current AS 1731. ISO 23953 is expected to be released in 2015, which gives some scope for

Australia and New Zealand representatives to contribute to its development.

Harmonising with ISO 23953 could provide two principle benefits to consumers in Australia and New Zealand.

Both Australia and New Zealand receive a significant proportion of their imports from China, in excess of two-

thirds in recent years. Importers questioned during the preliminary consultation phase suggested that many of the

Chinese factories manufacture for Europe in the same facility as Australia and New Zealand. As the Australian and

New Zealand market is relatively small these importers do not believe that they would manufacture different units

for any future Australian and New Zealand standard. Aligning with the ISO standard increases the certainty that

the standard will be met, but also that these businesses will continue servicing this market. Secondly, using the

ISO standard will reduce the compliance cost which is a component of current units. Rather than engineer and test

units to a standard intended for a small market, the testing and engineering costs will be spread across the whole

European and Australian-New Zealand markets.

The Possible Case for Regulation

Introducing more stringent MEPS will mostly benefit RDC users in small businesses, the cohort currently most

likely to make purchasing decisions based on just the capital costs. Preliminary analysis suggests that purchasing

more efficient equipment could be cost effective for periods greater than two years; however, in the absence of

more stringent MEPS, few small businesses are willing to spend the additional upfront capital required for the

more efficient equipment.

Large corporations in the supermarket sector, who have dedicated energy professionals, high operational certainty

and significant capital expenditure, have demonstrated that installing more efficient equipment is cost effective, by

installing units which exceed the current standards significantly. Updating the MEPS will have less impact on these

market participants than on small corporations where significant market barriers remain.

The outcomes in the RSC sector are less certain as the data is more uncertain. However, it is assumed that the RSC

market roughly shadows the integral RDC market: informed consumers with adequate capital are making

informed purchasing decisions, while less informed consumers are not. Again it is the consumers experiencing

information barriers that will benefit most from the possible application of MEPS to RSCs.

Separating the market into three cohorts, remote RDCs, integral RDCs and RSCs, the case for regulation is

strongest for integral RDCs and weakest for remote RDCs. Integral units contain both the condenser and

evaporator in the same case. Any regulations would only slightly impact smaller businesses who do not have the

resources to research and plan their purchases of cooling equipment.

Product Profile: Commercial Refrigeration - Refrigerated Display and Storage Cabinets iii

Market Barriers

The RDC sector is affected by the common barriers to improved energy efficiency; principle-agent and information

barriers. The RSC sector is also affected by similar barriers albeit to a lesser extent.

Principle-agent barriers occur when the equipment purchaser does not pay the operating costs for the equipment

and so has little incentive to select the most efficient equipment. In the RDC sector, this is most often associated

with the provision of promotional drinks and frozen confectionary cabinets, and also occurs when franchisees

purchase equipment through a franchise, or a service technician purchases equipment on another’s behalf.

However, some promotional equipment suppliers have recognised the market differentiation available from

providing best-in-class units; they are now providing what are considered by industry stakeholders to be some of

the most efficient units available worldwide. Therefore, the principle-agent barrier is declining in the RDC sector

due to competition in the market.

The most prevalent information barrier in the sector is the lack of consideration or understanding of on-going

running costs when making purchasing decisions; these decisions are generally based purely on capital cost.

Raising MEPS could address this to some degree by removing less efficient units from the market. However,

raising MEPS only impacts energy use when new units are purchased; as the typical lifetime of a cabinet is around

ten years, it will take considerable time to improve the efficiency of all RDCs in use across Australia and

New Zealand. Due to this, complimentary action could include an education program for RDC users on reducing

the energy use of existing RDCs.

Policy Options

Chapter 5 discusses in detail the policy options which could be used to address the barriers to improved energy

efficiency. These are outlined below.

1. Update MEPS, either through updating AS 1731 or by adopting or harmonising with the pending

ISO 23953 standard

2. Extend MEPS to RSCs, using a volume rather than total energy consumption/total display area metric

3. Introduce a ‘bottom-up” MEPS, where units assembled ‘on-site’ demonstrate compliance with MEPS

based on their components

4. Make mandatory or voluntary comparative labelling and product information available through

energyrating.gov.au

5. Explore ways to inform market participants of existing energy efficiency information, through industry

publications, membership bodies and suppliers

Market Size and Energy Use

Data on the number of units in use, their size and cost are difficult to determine accurately without significant

input from distributors operating in Australia and New Zealand. Stakeholders are invited to provide any

additional information which would enhance the understanding of the market size and energy use.

A number of data sources, the details of which are discussed in chapter 3, are currently available that provide

broad indications of the size of the market. There are estimated to be 192,000 remote RDCs in operation across

Australia and New Zealand in 2013, and as many as 900,000 integral RDCs.

These units are responsible for significant energy use and greenhouse gas emissions from the indirect emissions

associated with electricity production. Remote RDCs in Australia and New Zealand use about 5,300 GWh of

electricity each year and emit around 4 million tonnes of CO2-e. Integral units use almost 2,400 GWh each year,

contributing about 2 million tonnes of CO2-e.

The RSC market is the smallest of the three, using around 440 GWh of electricity across Australia and

New Zealand, and emitting around 300,000 tonnes of CO2-e each year.

Product Profile: Commercial Refrigeration - Refrigerated Display and Storage Cabinets iv

Conclusion

There are numerous policy options available to remove the market barriers impacting on the promotion of energy

efficiency in commercial refrigeration. The policy options considered most appropriate within this product profile

involve the removal of information barriers. There appears to be little evidence of principal-agent failures in the

market, as some suppliers view energy efficient units as a way to distinguish themselves in the market.

There is evidence that the current MEPS for RDCs are outdated and should be amended to better reflect the

efficiency of products in the market. Preliminary consultation indicates that industry stakeholders favour

harmonising the Australian and New Zealand standard with the International standard ISO 23953, currently

under review with an expected release during 2015. Harmonising with the International standard minimises the

compliance cost on manufacturers. Harmonisation may also have wider benefits due to the Australian and

New Zealand markets being are relatively small, so there is a risk that manufacturers may not be inclined to

manufacture specific models for the region if local requirements substantially differ from international

requirements.

Product Profile: Commercial Refrigeration - Refrigerated Display and Storage Cabinets v

Consultation on this Product Profile

Readers are asked to comment on a number of aspects of this document, particularly market data and modelling

assumptions, to assist with the formulation of a preferred policy option in the future. While we welcome comments

on all aspects of the Product Profile, comments responding to the questions listed under the heading, ‘Key

Questions’ would be of particular assistance.

Consultation workshops will be held in Melbourne, Sydney and Auckland. These will be coordinated by the New

Zealand project leader from the Energy Efficiency and Conservation Authority (EECA) on behalf of E3. Feedback

from the meetings and submissions will also be coordinated by EECA.

Written comments should be emailed, and received by Friday 4th October 2013.

Email: [email protected] and also [email protected]. Subject: Commercial refrigeration – RDCs and RSCs.

The evidence in this Product Profile will be reviewed and supplemented in light of any written submissions made

by stakeholders and/or issues raised at stakeholder meetings.

The Equipment Energy Efficiency Committee will make a decision on whether to proceed with a proposal to

improve the efficiency of commercial/non-domestic refrigerated display and storage cabinets and what the

preferred options should be.

If the preferred options involve regulation, a Regulation Impact Statement will be prepared to analyse the costs,

benefits, and other impacts of the proposal. Further consultation with industry will be carried out prior to any

final decisions being made.

Product Profile: Commercial Refrigeration - Refrigerated Display and Storage Cabinets vi

Key Questions

Standards

1. Should the MEPS and HEPS detailed in AS 1731 be updated?

2. If the MEPS and HEPS are updated, to what level should they be increased?

3. Do you agree that MEPS and HEPS should be extended to include RSCs? If so, do you consider that the

use of energy consumption per unit net volume is the appropriate metric for the measurement of energy

efficiency? If not, please describe alternatives.

4. Do you agree that there is scope to reduce the complexity of the existing classification of RDCs

(e.g. 36 categories of remote display cabinets with 12 categories having no MEPS or HEPS)? What would

be the benefits and are there any potential costs or disadvantages from moving to a simpler system?

5. Do you agree that the international test method ISO 23953 would be appropriate for measuring the energy

performance of regulated RDCs and RSCs for MEPS in Australia and New Zealand? Is there a case for

moving to this standard?

6. If Australia and New Zealand were to adopt an international standard, is there a case for aligning our

MEPS/HEPS with international levels? If not, please provide a case.

7. What impact would updating the MEPS have on Australian and New Zealand manufacturers? Are there

instances where increased MEPS would adversely affect sales? If not, please provide evidence that can be

shared and discussed with other stakeholders.

8. Are there any shortcomings with the Australian or international standards which are creating a barrier to

energy efficient innovations?

Market data

1. Do you agree with the market data presented for Australia and New Zealand? In particular, do you agree

with the estimates of current and projected stock and sales of RDCs and RSCs? If not, please provide your

assumptions.

2. Do you agree with the category breakdown of commercial refrigerated cabinets between display and

storage cabinets, and between medium and low temperature products?

3. Do you agree with the assumptions on product lifespan, capital and installation costs and efficiency

presented in the BAU scenario? If not, please provide evidence.

4. Do you agree with the claim that over 97% of sales are for units imported into Australia and New Zealand?

If not, please provide evidence.

5. Is there a case for regulating other related devices like ice-makers, refrigerated vending machines and

wine fridges?

6. Do you agree with the barriers to improved energy efficiency identified in this product profile and that

they are limiting the uptake of higher efficiency RDCs and RSCs in the Australian and New Zealand

markets? Are you aware of other issues which impact on the sale of more efficient products?

7. Could you contribute to a survey to determine the size and cost of the RDC and RSC market in Australia

and New Zealand?

Policy issues

1. Do you think a comparative labelling scheme would improve the quality of energy use information in the

market? Are there alternate options which could achieve the same aim?

2. Should mandatory ‘star’ rating labels be used for these products, as for domestic refrigerators, or do you

think that voluntary endorsement labels, such as Energy Star, would work better?

3. What additional costs do you think mandatory star rating labels and / or voluntary endorsement labels

would place on industry compared to the current situation? What impact do you think they would have on

competition and consumer choice? Please provide evidence to support your case.

Product Profile: Commercial Refrigeration - Refrigerated Display and Storage Cabinets vii

4. If a voluntary label was applied, how would you ensure all industry players contributed to energy use

information on products on the market?

5. Do you believe the ‘Deemed to comply’ policy option is both feasible and desirable?

6. Are there any additional measures which the E3 program could consider to increase the efficiency of RDCs

and RSCs?

Product Profile: Commercial Refrigeration - Refrigerated Display and Storage Cabinets 1

1. Introduction

What is a Product Profile?

Energy consumed in the operation of equipment is a major contributor to Australian and New Zealand energy use

and a source of greenhouse gas emissions. In recognition of this, the Council of Australian Governments (COAG)

and the New Zealand Government initiated the Equipment Energy Efficiency (E3) Program. The E3 Program

develops, amongst other things, Minimum Energy Performance Standards (MEPS) and Energy Rating Labels

(ERLs) for appliances and equipment, with the aim of improving the energy efficiency of products sold in Australia

and New Zealand.

Product Profiles are developed for the E3 Program under the direction of the E3 Committee. The E3 Committee

comprises representatives of government agencies that promote energy efficiency in the Commonwealth, State,

Territory and New Zealand governments. A Product Profile outlines the factors impacting the energy performance

of an equipment or technology type and explores the case for targeted government intervention to improve energy

efficiency of the equipment type across the Australian and New Zealand economies.

Outline of the Product Profile

This Product Profile provides a technology and market assessment of commercial refrigerated display cabinets

(RDCs) and refrigerated storage cabinets (RSCs) in Australia and New Zealand. It is intended to review the energy

efficiency and energy consumption trends for these products under a business-as-usual (BAU) scenario, to identify

scope for improvement and to investigate options to help improve the efficiency of RDCs and RSCs. This first

chapter provides some of the relevant history of the Australian Greenhouse and Energy Minimum Standards

(GEMS) legislation and its interaction with MEPS and Australian Standards.

The second chapter defines the equipment and processes covered by this Product Profile. It describes RDCs and

RSCs, including what equipment types are regulated or covered by standards, the energy using processes in

refrigeration and the typical application of RDCs. The chapter concludes with a discussion of energy efficiency

trends in the market and their impact on unit performance.

The third chapter examines the Australian and New Zealand market for RDCs and RSCs. It begins by defining the

characteristics of the market, including trade figures and discussion of the relationships between suppliers,

manufacturers and consumers. This is followed by an estimate of the energy used by the equipment and the

businesses which use this energy. The chapter concludes by estimating the current number of RDCs and RSCs in

use and the amount of energy they use.

Chapter four discusses the test and performance standards which apply to RDCs and RSCs, both locally and

internationally. This includes discussion of energy efficiency programs which apply to this equipment. This is

followed by summaries of registration data for MEPS units and discussion of options for updating the MEPS.

Chapter five considers the barriers to efficient energy use of RDCs and RSCs and discusses the policy options, if

any, that can be used to remove these barriers. This discussion considers the policy options to address the

identified market failures and the impact addressing these barriers may have on energy use and emissions in

Australia and New Zealand.

Product Profile: Commercial Refrigeration - Refrigerated Display and Storage Cabinets 2

The Policy Context

The E3 Program operates under national legislation and is administered by the Australian Government, with input

from state and territory governments and the New Zealand Government. E3 was established in 1992 to coordinate

the mandatory MEPS and mandatory ERLs.

The policies that support the E3 Program differ in the two nations but drive towards a common goal of improving

the energy efficiency of appliances and products in Australia and New Zealand.

Australian Policy Context

In 2009 COAG released a comprehensive 10-year National Strategy on Energy Efficiency (NSEE). The strategy

established a cooperative plan to deliver a range of energy efficiency measures across all Australian jurisdictions.

The measures in the strategy are framed around the four following themes:

• Assisting households and businesses to transition to a low-carbon future;

• Reducing impediments to energy efficiency improvements;

• Making buildings more energy efficient; and

• Government working in partnership and leading the way.

The strategy is wide-ranging in scope and includes a suite of measures to strengthen energy efficiency standards

for appliances, equipment, buildings and vehicles. A number of measures under the strategy will also provide

Australians with better information and training to assist them in making informed choices to improve their

energy efficiency.

All Australian jurisdictions have also signed a National Partnership Agreement on Energy Efficiency to deliver a

nationally-consistent approach to energy efficiency through a range of energy efficiency initiatives, including

nationally consistent energy efficiency standards for appliances and equipment and a process to enable industry to

adjust to increasingly stringent standards over time.

From October 2012, regulation of the Australian MEPS has been undertaken at a national level, under the

Greenhouse and Energy Minimum Standards Act 2012 (GEMS Act 2012). This Act harmonised state legislation

and regulations previously used for compliance, and established a consistent, national legislative footing.

Subordinate to the GEMS Act 2012 are Determinations to manage individual products (for instance the

Greenhouse and Energy Minimum Performance Standards (Refrigerated Display Cabinets) Determination 2012

(RDC Determination)).

New Zealand Policy Context

Adopted in 2011, the New Zealand Energy Strategy (NZES) 2011-2021 (New Zealand Ministry of Business,

Innovation and Employment (NZMBIE) 2013) and the New Zealand Energy Efficiency and Conservation Strategy

(NZEECS) 2011-2016, together provide the strategic direction for the energy sector and the role energy plays in the

New Zealand economy. One of the objectives of the NZEECS is “greater business and consumer uptake of energy

efficient products” with a target of “extending minimum energy performance standards, labelling and ENERGY

STAR® product coverage to remain in line with major trading partners”.

The NZEECS promotes the careful use of a mix of measures, such as information on consumer and business needs,

along with codes and standards to underpin confidence in energy efficient products and practices. It recognises

that common standards and energy labelling information supports closer economic relationships with Australia

and reduces compliance costs for product manufacturers and suppliers who are often trading in both countries.

New Zealand is committed to providing energy efficiency labelling and standards for products, in association with

Australia, to better inform consumer choice.

NZES sets out four priority areas:

• Diverse resource development;

• Environmental responsibility;

• Efficient use of energy; and

• Secure and affordable energy.

Product Profile: Commercial Refrigeration - Refrigerated Display and Storage Cabinets 3

History of E3 Regulation

The introduction of MEPS for RDCs and RSCs in Australia and New Zealand was first considered in 2000-2001

with the publication of several Technical Reports (Australian Greenhouse Office (AGO) 2000a, AGO 2000b, AGO

2001a, AGO 2001b). After consultation with stakeholders, the Australia and New Zealand Governments

implemented MEPS for RDCs only, used in Australia and New Zealand. RSCs were originally excluded from

regulation because they were estimated to contribute less to total energy consumption compared to RDCs.

Australian Standard AS 1731:2003 defined both the test methods and the MEPS requirements for RDCs. These

requirements came into force in 2004. There are currently no MEPS for RSCs. However, as many RSCs are now

supplied by manufacturers and importers of RDCs, there appears to be a case for revisiting this exemption.

AS 1731 was reviewed in 2008. Strong stakeholder support for improvements to the current MEPS for RDCs

encouraged the E3 Committee to commit to a 10-year strategy to increase the energy efficiency of commercial

refrigeration appliances. The preparatory work for the strategy was documented in the “In from the Cold” reports

(E3 2011). Specific recommendations included adopting international standards to broaden the scope of MEPS to

include RSCs, strengthening MEPS to reflect improvements in performance since 2004, and adopting the

international test method for the equipment.

Since the review undertaken in 2008, AS 1731 has not been updated to take into account any of the

recommendations from ‘In From The Cold - a 10-year strategic plan for non-domestic refrigeration’.

This current Product Profile now explores some of these options.

Product Profile: Commercial Refrigeration - Refrigerated Display and Storage Cabinets 4

Equipment Covered by this Product Profile

RDCs and RSCs are used to store and display foodstuffs and beverages in a temperature-controlled environment.

They are designed to maintain an internal temperature range suitable for the display or storage of perishable

goods, or for chilling non-perishable beverages. Food safety laws or guidelines usually dictate the temperature

requirements.

The Australian Standard AS 1731 classifies RDCs according to the intended application, location of condensing unit

or compressor, storage temperature and configuration of the cabinet. Each general classification is then identified

by a coded designation as a ‘type’ such as vertical, horizontal, open and those with glass-doors.

This Product Profile does not consider refrigerated vending machines, ice makers or cabinets intended for use in

catering and similar non-retail applications, which are excluded from AS 1731.

Refrigerated Display Cabinets

These are units that are intended to store and display for sale chilled and/or frozen foodstuffs and beverages. These

cabinets allow the stored products to be either directly viewed through an opening in the cabinet or through

transparent doors, lids or covers that:

• are normally kept closed, but can be opened to access the contents; and

• enable users to access any of the contents without stepping inside the refrigerated space.

RDCs are typically used in supermarkets, petrol stations and smaller food and beverage vendors such as ‘corner

stores’ and delicatessens. Supermarkets use RDCs to display fruit and vegetables, meat, fish and poultry and dairy

and deli items (with dedicated staff) and frozen goods. Petrol stations and smaller vendors use RDCs to display

chilled beverages and ice-confectionary.

A summary table of all cabinet types is included in Appendix C, and examples of the designations are included in

Figure 1.

Integral and Remote Units

Both RSCs and RDCs can be supplied as remote or self-contained/incorporated/integral units. In a remote unit the

condenser and compressor are in a different location to the evaporator, in a system analogous to split-system air-

conditioners. For example a supermarket might have a large bank of refrigerated cabinets, with compressors and

condensers outside to reduce space and noise on the shop floor. The use of one compressor to supply several

display cabinets (one-to-many configuration) is common in large facilities.

Integral units contain both the condenser and evaporator in the same case. The refrigeration cycles are functionally

identical, but remote units will necessarily involve more piping, and therefore a larger amount of refrigerant.

Remote cabinets are typically found in large to medium sized supermarkets with a centralised refrigeration area. In

this system, each display case is connected to an external compressor and condenser via high pressure liquid and

suction refrigerant piping with additional connections required for condensate drain lines and electricity. Cases

contain an expansion valve, one or more evaporators and evaporator fans to circulate air.

Integral cabinets are found in supermarkets, typically in addition to remote cabinets, in service stations and corner

stores. Integral cabinets can be easily moved and installed and therefore provide flexibility for large businesses and

low commitment to smaller businesses.

The designation for a remote cabinet is ‘R’ and for an integral cabinet is ‘I’. The full classification scheme for RDCs

is outlined in Appendix C.

2. Refrigerated Display Cabinets and

Refrigerated Storage Cabinets

Product Profile: Commercial Refrigeration - Refrigerated Display and Storage Cabinets 5

Each of the examples in Figure 1 could be integral or remote systems. Separating the compressor and condenser

from the display cabinet will have little influence on the appearance of the cabinet and is primarily an engineering

and system design consideration.

Horizontal, frozen, open-top, island cabinet

Vertical, chilled, open, multi-deck cabinet

Semi-vertical, chilled, multi-deck cabinet

Vertical, refrigerated, glass-door cabinet

Horizontal, chilled service-counter

Horizontal, chilled, glass-door display cabinet

Figure 1: Examples of Refrigerated Display Cabinets

Product Profile: Commercial Refrigeration - Refrigerated Display and Storage Cabinets 6

Refrigerated Storage Cabinets

These are products that are specifically designed to store, but not to display for sale, chilled and/or frozen

foodstuffs. They are not currently covered by MEPS and are not captured under any existing Australian or

New Zealand Standards. They are generally defined by the storage volume and any extra features, such as food

preparation areas, lighting and materials.

They predominantly have solid faced lids, drawers or doors that:

• are normally kept closed, but can be opened to access the contents;

• obscure the majority of the contents of the cabinet from view when closed; and

• allow users to access the contents of any part of the interior without stepping inside the refrigerated space.

Examples of RSCs are shown in Figure 2.

Refrigerated storage cabinet

Vertical refrigerated storage cabinet

Figure 2: Examples of Refrigerated Storage Cabinets

Design of RDCs and RSCs

RDCs and RSCs are special purpose refrigerators. This section presents a brief overview of the design of the

equipment. Special attention is paid to the components that make up the refrigerators as they are responsible for

most of the energy use. A more comprehensive description of the equipment can be found in ‘In From The Cold - a

10-year strategic plan for non-domestic refrigeration’.

The Refrigeration Cycle

In general, refrigeration equipment uses energy, or work, to move heat from a cold space to a hot space. A typical

refrigeration process operates by continuously heating and cooling a refrigerant gas in a closed loop, as shown in

Figure 3. This process includes the following steps:

• The refrigerant gas is sucked into the electrically driven compressor. The gas is compressed, causing it to

heat up

• The hot gas enters an air- or water-cooled condenser (the first heat exchanger) where it is cooled and

condensed into a liquid at high pressure

• The cooled high-pressure liquid flows through an expansion valve into a low-pressure evaporator

• The lower pressure causes the liquid to boil, which draws heat from the area surrounding the evaporator

coil (the second heat exchanger).

In an RDC or RSC, the evaporator coil is inside the cabinet, which is therefore cooled to the desired temperature.

The performance of both heat exchangers - the condenser and evaporator - can be enhanced with the addition of

electric fans.

Product Profile: Commercial Refrigeration - Refrigerated Display and Storage Cabinets 7

Figure 3: Major components and energy flows of the refrigeration cycle

The efficiency of this process is referred to as the Coefficient of Performance (COP), which is usually expressed as a

ratio of the amount of electricity used to move each unit of heat. A refrigeration system with a COP of three uses

1 kW of electricity for every 3 kW of heat moved. It is a system characteristic and is the product of the efficiencies

of each individual component and their interactions. Typical COPs in this market range from three to about five.

Refrigerant Gases

The choice of gas in the refrigerator is driven by the target temperature inside the cabinet and the ambient

temperature. A range of gases are available to designers and the selection of the refrigerant gas can influence the

efficiency of the refrigerator. Several of these gases have a high Global Warming Potential (GWP) (IPCC 2007).

Others have been banned under the Montreal Protocol, which sought to eliminate the ozone depleting gases. It is

the responsibility of each participating country to implement the guidelines set out in the Montreal Protocol.

Table 1 lists several common refrigerant gases.

Refrigerant gases can be made from either a single chemical compound or a blend of multiple compounds. Blended

gases have the disadvantage that the components may leak at different rates, meaning that they cannot be topped-

up in the event of a leak and that the whole refrigerant charge may have to be discarded.

Product Profile: Commercial Refrigeration - Refrigerated Display and Storage Cabinets 8

Table 1: Common refrigerant gases

Designation Applications GWP Strengths and weaknesses

R22

Chlorodifluoro-methane

Wide range of refrigeration

1,810 Montreal Protocol gas, with ozone depletion potential of 0.055

R134A

1,1,1,2-Tetrafluoro-ethane

Air-conditioning and higher temperature refrigeration

1,430 High global warming potential

R407F

Blend of R32, R125 and R134a

Wide range of refrigeration. Designed as a swap for ozone-depleting R22

1,705 Blended gas

Straight-swap for R22, however, may reduce performance

R404A Mainly used for low temperature

3,784 Blended gas

High global warming potential

R290

Propane

Typical in ice cream freezers, but appropriate for wide range

3.3 Flammable. International laws limit charge of hydrocarbon refrigerants to less than 150g per unit. This means that the most common application is in small, integral units

Frequently used as a replacement for R22

R600a

Isobutane

Small cabinets and refrigerators

3 Flammable, so subject to safety restrictions

Low GWP replacement for R12 and R134a but size limited due to flammability

R744

Carbon dioxide

Wide range of refrigeration

1 Cheap and easily obtained. Requires higher pressure than other gases, requiring more robust components. Toxic in some situations

Note: GWP is a relative measure of how much heat a greenhouse gas traps in the atmosphere, relative to a similar mass of carbon

dioxide.

The refrigeration loop is a closed system, but some leakage will occur and need to be refilled over time. This creates

safety issues with the gases which are flammable or poisonous, such as R290 or R744. Further, leakage is a

problem with the higher GWP gases, like R134A and R404A.

With the introduction of a price on greenhouse gas emissions in Australia, a restructuring of the refrigerants

market is underway. This will have some potential consequences for the energy performance of refrigerated

cabinets. The additional cost of using synthetic greenhouse gases with high GWPs, such as hydrofluorocarbons

(HFCs), is putting more focus on alternative refrigerants with lower GWPs including ‘natural’ refrigerants such as

hydrocarbons, carbon dioxide and ammonia. However all of these alternatives possess characteristics that require

special design considerations to ensure safety.

Very low GWP refrigerants such as hydrofluoroolefins (HFOs) and the hydrocarbons, are flammable gases and

therefore have specific safety requirements. Ammonia (NH3 or R 717) is toxic and mildly flammable and again

requires certain precautions to ensure safety. Carbon dioxide (CO2 or R 744) operates at relatively high pressures

when compared to HFCs and this needs to be taken into account in the refrigeration system design.

Compressors

The largest energy using component in any refrigeration system is the compressor, typically driven by electricity.

Compressors are chosen for a given application based on the refrigerant to be used, the desired pressure range and

the cost. Other mechanisms are possible to compress the fluid but these are generally experimental.

Fans

Fans increase air flow over the heat exchangers, leading to higher heat-transfer rates per unit of area. Typical

systems will include an electric fan on both the evaporator and condenser. As with any electrical device, any fan

motor contained within the refrigerated space will contribute to the heat load.

Product Profile: Commercial Refrigeration - Refrigerated Display and Storage Cabinets 9

Internal Lighting

Many RDCs incorporate lights to illuminate the contents. The technology used has evolved from incandescent to

fluorescent tubes, and more recently compact fluorescents and light emitting diodes (LEDs). Through this

progression the energy used in lighting has decreased, leading to a reduction in the related heat-load. Lights within

the refrigerated compartment contribute heat to the compartment, which typically needs to be removed by the

refrigeration cycle.

Refrigerator Controls

To maintain a constant temperature in the refrigerated compartment, electrical controllers must operate the

compressor. A basic system might use a simple thermostat in the cold compartment, which switches off the

compressor once the desired temperature is achieved. More complex systems might employ thermostats on the

heat exchangers, which operate fans to increase the rate of heat transfer. Modern systems might use a

microprocessor to control all system aspects and use sophisticated control devices like Proportional Integral

Differential (PID) controllers to achieve accurate temperature control.

Low temperature and some medium temperature evaporators require periodic defrosting to remove water that

condenses and/or freezes on the evaporator surface. This can be done with electric heating, hot refrigerant gas or

air defrosts. All defrosting methods add to the energy usage of the system.

Air Curtains

These devices are used on open display cabinets, blowing air across the opening of the refrigerated compartment.

They are intended to reduce infiltration of warm, ambient air into the refrigerated compartment and therefore

improve the refrigeration efficiency. However, their operation uses electricity to drive a fan, so the efficiency

improvement is the improved refrigeration efficiency, less the energy consumed to drive the fan. While they are

effective in some applications, if not properly designed they can actually decrease performance. As the barrier is

simply a barrier of moving air, it is susceptible to disruption by obstructions caused by improper stacking of

products, pedestrian traffic or air gusts through the store.

Insulation

Good insulation is central to the performance of all refrigerators. Many different materials can be used for this

task, but broadly speaking thicker insulation equates to less heat flow into the refrigerator. This includes all design

and material choices which reduce heat-flow, and also includes thermal-breaks and seal materials. Early RDCs

used single panes of glass for their doors, but new designs sometimes use double or triple glazed doors and some

utilise low-e (heat reflecting) glass as well.

Component Energy Use

In a typical RDC or RSC, the compressor will use the most energy of any system part, at around 50%, with fans

consuming about 33% and the ancillary systems 17%. The compressor and electric motor driving it are effectively

one energy using unit. As a guide, the compressor accounts for about half the system energy use.

The operation of both the evaporator and condenser are typically enhanced by employing electric fans, one, or

more, for each heat exchanger. These fans together draw about a third of the system energy use.

The balance of energy use is spread across a number of ancillary systems, the energy uses of which will be

determined by the system configuration and can vary widely depending on the application. These systems may

include the electronic control unit, cabinet lighting, air-curtains and defrost heaters.

This energy breakdown differs for freezer cases which incorporate defrost heaters. These are included in the

Ancillary Systems, and can shift this distribution, depending on operating characteristics.

Trends in Energy Performance

This section presents some information on the trends in the energy performance of the equipment. Through the

actions of the market, in some cases aided by policy measures, the performance of RDCs has been improving over

time. While there is no data available on the performance improvements of RSCs it is assumed that their efficiency

has improved in parallel with RDCs, as they share much of the same components.

Product Profile: Commercial Refrigeration - Refrigerated Display and Storage Cabinets 10

The performance trend of RSCs throughout time is not as well documented. However, the major energy using

processes in RSCs are identical to RDCs and so will demonstrate the same improvements over the same time

period. The principle differences arise in the door materials, which will be solid and hence better insulating than in

RDCs, and in lighting, which will only operate when the door is open. Thus RSCs will use slightly less energy than

RDCs of comparable size, and follow the improvement trend in unit performance.

Table 2 shows the average performance of all the RDC models registered for MEPS in Australia and New Zealand

for the period 2006 to 2012. Over this time, the number of registrations has increased by 23% per annum, and the

total average energy consumption has dropped by 1.6%, mainly in the 2006-2007 period. Some of this fall in

energy consumption is due to a small shift in the proportion of registrations towards medium temperature cabinets

between 2006 and 2012. The average display area per model has grown slightly (+0.6%) to around 2m2 per unit in

2012, resulting in an overall energy efficiency improvement of 2.2% between 2006 and 2012.

Under both the Australian/New Zealand and international standards (AS 1731 and ISO 23953:2005) energy

efficiency of RDCs is measured by the Total Energy Consumption / Total Display Area (TEC/TDA). Calculation of

the TDA takes into account a number of factors including:

• The horizontal projection of the RDC;

• The vertical projection of the RDC;

• Cabinet length including both horizontal and vertical open length;

• Length of glazing, both horizontal and vertical; and

• The light transmission through the glazing surface, or the vertical or horizontal projection.

It should be noted that these figures are drawn from the values for individual models and the averages are

therefore ‘model-weighted’. They have not been combined with data on sales or stock here, to provide an indication

of the average performance of products sold each year, or the average performance of products in use. This is due

to the fact that no sales data is available.

Table 2: Characteristics of registered refrigerated display cabinet models 2006-2012

Date Registrations Average display area (m2)

Average energy consumption (kWh/day)

Average TEC/TDA (kWh/day/m2)

Jan 2006 423 1.9 24.5 12.9

Jan 2008 658 1.9 22.1 11.7

Jan 2010 929 2.0 22.4 11.3

Jan 2012 1447 2.0 22.3 11.3

Source: E3 Registration database

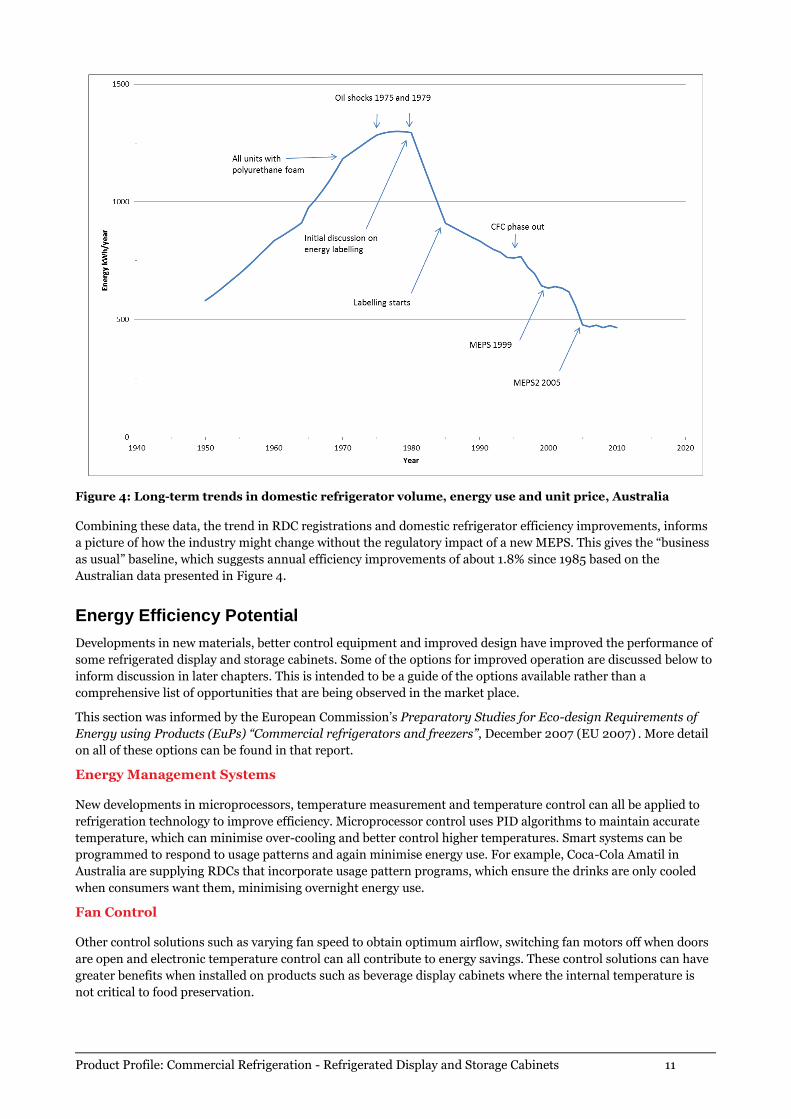

The improvement over time of domestic refrigerators is much better known, and may point to similar

improvements in commercial equipment. Figure 4 shows how the energy efficiency of residential refrigerators used

in Australia has improved (DCCEE 2013). Importantly, the figure highlights the influence of targeted performance

regulations. Similar trends have been reported for the United States (ASE 2011).

Product Profile: Commercial Refrigeration - Refrigerated Display and Storage Cabinets 11

Figure 4: Long-term trends in domestic refrigerator volume, energy use and unit price, Australia

Combining these data, the trend in RDC registrations and domestic refrigerator efficiency improvements, informs

a picture of how the industry might change without the regulatory impact of a new MEPS. This gives the “business

as usual” baseline, which suggests annual efficiency improvements of about 1.8% since 1985 based on the

Australian data presented in Figure 4.

Energy Efficiency Potential

Developments in new materials, better control equipment and improved design have improved the performance of

some refrigerated display and storage cabinets. Some of the options for improved operation are discussed below to

inform discussion in later chapters. This is intended to be a guide of the options available rather than a

comprehensive list of opportunities that are being observed in the market place.

This section was informed by the European Commission’s Preparatory Studies for Eco-design Requirements of

Energy using Products (EuPs) “Commercial refrigerators and freezers”, December 2007 (EU 2007) . More detail

on all of these options can be found in that report.

Energy Management Systems

New developments in microprocessors, temperature measurement and temperature control can all be applied to

refrigeration technology to improve efficiency. Microprocessor control uses PID algorithms to maintain accurate

temperature, which can minimise over-cooling and better control higher temperatures. Smart systems can be

programmed to respond to usage patterns and again minimise energy use. For example, Coca-Cola Amatil in

Australia are supplying RDCs that incorporate usage pattern programs, which ensure the drinks are only cooled

when consumers want them, minimising overnight energy use.

Fan Control

Other control solutions such as varying fan speed to obtain optimum airflow, switching fan motors off when doors

are open and electronic temperature control can all contribute to energy savings. These control solutions can have

greater benefits when installed on products such as beverage display cabinets where the internal temperature is

not critical to food preservation.

Product Profile: Commercial Refrigeration - Refrigerated Display and Storage Cabinets 12

High Efficiency Compressors

Most RDC compressors are “hermetically sealed” to contain refrigerant losses from the compressor, which means

the compressor and motor must be considered together. High efficiency compressors use less energy to compress

the working fluid, enhanced by design and materials improvements.

The energy savings for this type of improvement vary with the application and type of compressor, but for a typical

beverage cooler, changing to a high-efficiency compressor will save about 5% of the total electricity consumption.

Variable Speed Drive Compressors

Variable speed drives (VSD) accurately control the power to electric motors, making low speed operation possible

and efficient. The benefits of VSDs are two-fold; allowing low-speed operation means the compressor can be run

closer to its best-efficiency-point (BEP), which in turn reduces the number of compressor on-off cycles, reducing

current spikes. This reduces energy cost and can also improve compressor life. VSDs are not compatible with all

motors and are generally bought as a motor and VSD pair.

Energy savings associated with VSDs are linked to the reduction of refrigerant mass flow. Lower refrigerant flow

reduces the condensing pressure and in turn, compressor energy consumption. VSDs draw some power, so will not

always yield energy savings. As a general rule, if the compressor works at a full load less than 80% of the time the

addition of a VSD will save energy.

Efficient Fan Motors

In a similar manner to compressor improvements discussed above, fan efficiency can be improved with either a

more efficient fan, motor or both. Computer modelling and material improvements continue to deliver

incrementally more efficient fans, and fans designed for specific applications.

Electronically commutated motors (ECMs) are high-efficiency direct current motors which use permanent

magnets and a built in inverter. They are significantly more efficient than common alternative current (AC) motors

and easier to control. ECMs achieve approximately 70% efficiency across their operating range, compared to 35%

for a standard AC fan motor. ECMs also report operating lives of 90,000 hours, approximately double that of a

standard AC motor.

In addition, high efficiency fan blades could have an application in some situations such as optimising air curtains

in open deck cabinets.

Motor efficiency has improved with the introduction of ECMs. Stakeholder consultation sessions indicate these are

the most likely retrofit opportunity, with pay-back periods of less than two years reported on straight motor swaps.

High Efficiency Lighting

Lighting technology has moved from traditional incandescent lights, to fluorescent tubes with magnetic ballasts,

then to fluorescent tubes with electronic ballasts and most recently to LEDs.

Each improvement has increased the luminous efficiency by decreasing the heat load associated with light output.

Luminous efficacy indicates how much light a lamp generates from the electricity it uses, with small numbers

meaning more efficient lights. This lowers the overall energy use of the unit through two different mechanisms;

electrical demand for lighting is reduced, and the heat load into the cabinet is reduced. Test standards require the

cabinet lights be run during testing, to reflect real life conditions so both of these mechanisms are captured.

Most new cabinets are now supplied with LEDs as standard and there are many retrofit LED products available to

replace fluorescent and incandescent lamps.

Light Control

Cabinets which are used intermittently, such as those in take-away food outlets, may include lighting controls

which turn off the cabinet lights when not required. These could be either a simple timer which runs the lights

during business hours or motion sensors which turn the lights on as a customer approaches.

These controllers could be retrofitted in some circumstances.

Product Profile: Commercial Refrigeration - Refrigerated Display and Storage Cabinets 13

Insulation

There are many ways to reduce heat flow into the refrigerated compartment; these can be broadly lumped together

as insulation improvements. The most typical example is the insulation material around the cooled compartment;

making this thicker or using a higher r-value material will improve the unit performance. Other simple actions like

moving cabinets out of direct sunlight or from under heating vents will improve the unit performance.

New cabinets benefit from modern insulation materials, though are still limited by the overall cabinet size to

chilled compartment ratio, which will be reduced as thicker insulation is included. Customers often select cabinets

by external size and so the reduction in internal volume required by using thicker insulation is not detected.

Changes to Heat Ingress

The four technology options listed below (advanced glazing, air curtains, night blinds and physical barriers such as

doors and lids) can be retrofitted to existing units and are all designed to reduce heat entering the cooled space.

However, their application can have mixed results as they can significantly reduce the cooling load required by the

compressor. If the compressor or the unit controls cannot adapt to this change, the cabinet can be over-cooled,

leading to frozen products. For this reason, these modifications should be tested thoroughly before widespread

implementation.

Advanced Glazing

Heat ingress to RDCs with glass doors can be reduced with advanced glazing, such as double-glazing or heat

reflective glass. Double-glazing is becoming common in integral RDCs, demonstrated in particular in the units

supplied by Coca-Cola Amatil in Australia.

Retrofitting advanced glazing is plausible in some situations, but there are limits on physical installation. Most

RDCs with glass doors use metal frames, designed for a single pane of glass; thus a thicker glazing unit, such as a

double-glazed unit will be difficult to install. Some of the laminated and coated glass products avoid this problem.

Alternatively, some existing RDCs could have their whole door replaced with a more efficiently glazed unit.

Air Curtains

With open display cases, energy can be wasted by allowing refrigerated air to spill into the store. The effect of the

spillage can be minimised with air curtains where air is blown over the open section of the case, which separates

cooled food from the warmer store air. The use of air curtains must be carefully monitored as they may actually

lead to increased energy use if incorrectly operated.

Retrofitting an air-curtain is unlikely to be plausible and will require a large degree of testing to decrease energy

use.

Night Blinds

Night blinds are similar to roller-blinds used for windows and offer energy savings for open display cabinets,

particularly in applications where use varies greatly between day and night. They are inexpensive when compared

to other physical barriers, such as solid coverings, though they are also less effective.

Night blinds can be retrofitted fairly easily, but their interaction with the refrigeration system should be carefully

monitored, as freezing can occur. Night blinds decrease the heat flow into the cabinet overnight, significantly

reducing the cooling requirements. If the compressor cannot be run at low loads it will over-cool the compartment,

and in some cases freeze the product.

Night blinds can be mechanised and automated to open and close on a timer, ensuring gains are achieved without

reliance on manual operations.

Physical Barriers / Doors and Lids

Using RDCs with doors or lids will save energy when compared to open units and many supermarkets are already

applying this change. Some businesses have been reluctant to implement this change due to a perception that the

extra barrier of a door or lid would lead to a reduction in sales and permanent switching of customer allegiance.

However research on doors on RDCs suggests the impact of this mechanism on sales is exaggerated (ASHRAE

2010).

Currently there is a small trial underway in New Zealand to retrofit doors to cabinets containing processed dairy