company presentation - s21.q4cdn.com · this presentation, ... credit card rev. cash rev. monthly...

TRANSCRIPT

Company Presentation

March 2015

Forward-Looking Statements

2

This presentation, including the accompanying oral presentation (collectively, this “presentation”), does not constitute an offer to sell or the solicitation of an offer to buy anysecurities. This presentation is provided by On Deck Capital, Inc. (“OnDeck”) for informational purposes only. No representations express or implied are being made byOnDeck or any other person as to the accuracy or completeness of the information contained herein.

This presentation contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 and other legal authority. Forward-looking statements include statements about scalability, growing distribution channels, credit predictability and information concerning our future financial performance,business plans and objectives, potential growth opportunities, financing plans, competitive position, industry environment and potential market opportunities. Forward-looking statements can also be identified by words such as "will," "enables," "expects," "allows," "continues," "believes," "anticipates," "estimates" or similar expressions.Forward-looking statements are neither historical facts nor assurances of future performance. They are based only on our current beliefs, expectations and assumptionsregarding the future of our business, anticipated events and trends, the economy and other future conditions. Moreover, we do not assume responsibility for the accuracyand completeness of forward-looking statements. As such, they are subject to inherent uncertainties, changes in circumstances, known and unknown risks and otherfactors that are difficult to predict and in many cases outside our control.

As a result, you should not rely on any forward-looking statements. Our expected results may not be achieved, and actual results may differ materially from ourexpectations. Important factors that could cause actual results to differ from our forward-looking statements are the risks that we may not be able to manage our anticipatedor actual growth effectively, that our credit models do not adequately identify potential risks, and other risks, including those in documents that we file with the Securitiesand Exchange Commission, or SEC, from time to time which are available on the SEC website at www.sec.gov. We undertake no obligation to publicly update any forward-looking statements for any reason after the date of this presentation to conform these statements to actual results or to changes in our expectations, except as required bylaw.

In addition to the U.S. GAAP financial information, this presentation includes certain non-GAAP financial measures. We believe that non-GAAP measures can provideuseful supplemental information for period-to-period comparisons of our core business and is useful to investors and others in understanding and evaluating our operatingresults. These non-GAAP measures have not been calculated in accordance with U.S. GAAP. You should not consider them in isolation or as a substitute for an analysis ofour results under U.S. GAAP. There are a number of limitations related to the use of these non-GAAP measures versus their nearest GAAP equivalents. For example,neither Adjusted EBITDA nor Adjusted Net (Loss) Income is a substitute for Net (Loss) Income. In addition, other companies may calculate non-GAAP financial measuresdifferently or may use other measures to evaluate their performance, all of which could reduce the usefulness of our non-GAAP financial measures as tools for comparison.Adjusted EBITDA excludes some recurring costs, including interest expense associated with debt used for corporate purposes, non-cash stock-based compensation,depreciation and amortization expense and fair value adjustment for our warrant liability. Therefore Adjusted EBITDA does not reflect interest expense, the non-cashimpact of stock-based compensation or working capital needs that will continue for the foreseeable future. Adjusted Net (Loss) Income excludes stock-based compensationexpense and warrant liability fair value adjustment which will continue for the foreseeable future and therefore will generally be more favorable than Net (Loss) Incomedetermined in accordance with GAAP. Please refer to the Non-GAAP Reconciliations at the end of this presentation for a description of these non-GAAP measures and areconciliation to Net (Loss) Income.

OnDeck Powers the Growth of Small Businesses Through Lending and Technology Innovation

3

Card Quest Inc.

Shannon Schofield

Mojito Maintenance

Dan Gonzalo

Furry Tales Doggy Daycare

Lena Botwright

J.a.m.b.s Jewelry

Mark S. Desrochers

Seasons

Gerald Palumbo

$2 Billion+ total originations

Scalable financial model

5th Generation proprietary credit scoring model

30,000+ small business served

73 net promoter score

150%+ y-o-y originations growth

A Leading Online Platform for Small Business Lending

4

459

1,158

168369

2013 2014 Q4 '13 Q4 '14

Originations$MM

65

158

2350

2013 2014 Q4'13 Q4'14

Gross Revenue$MM

Investment Highlights

5

Massive and underserved market

Proprietary analytics and scoring models

Integrated and scalable technology platform

Diversified customer acquisition channels

Robust funding platform

Experienced management team

Attractive financial profile

Small Business Lending Market is Massive and Underserved

6

Sources: U.S. SBA, FDIC, Oliver Wyman, How “New-Form Lending” Will Shape Banks’ Small Business Strategies, 2013

1. As of 12/31/2014; Loans under management represents the unpaid principal balance plus the amount of principal outstanding for loans held for sale, excluding net deferred origination costs, and the amount of principal outstanding of term loans the company serviced for others, each at the end of the period.

$80-120Bn

Unmet

Demand for Small

Business Lines

of Credit

$0.6Bn

OnDeck Loans Under

Management1

$80-120BnUnmet

Demand for Small

Business Lines

of Credit

$178BnBusiness Loan

Balances Under

$250,000 in

the U.S.

in Q3 ꞌ14

28MMU.S. Small Businesses

OnDeck Unique Small

Businesses Served

30K

Credit Card Rev. Cash Rev. Monthly Exp. Inventory & Payroll

Landscaping Rev. Snow Removal Rev. Monthly Exp. Fuel & Payroll

Repair Rev. Subcontractor Rev. Monthly Exp. Supplies & Payroll

• Diverse businesses require

manual underwriting

• Technology and data

limitations

• Lack of standardized small

business credit score

Diversity of Small Businesses Creates Challenges for Traditional Lenders…

CHALLENGES FOR

TRADITIONAL LENDERS

Cash Flow ProfileRestaurant

Landscaping Company

Plumbing Company

7

Q1 Q2 Q3 Q4

…Leading to a Frustrating Borrowing Experience for Small Businesses

FRUSTRATIONS FOR

SMALL BUSINESSES

• Time consuming offline process

• Non-tailored credit assessment

• Product mismatch

• Rigid collateral requirements

8

The OnDeck Score®

Proprietary and Purpose Built for Small Business

100+ external data sources

5th Generationproprietary credit scoring model

10 Million+ small businesses in proprietary database

2,000+ data points per application

9

Score

A

B

C

D

E

Ris

k G

rad

ing

• Probabilistic record linkage

• Dimensionality reduction

• Ensemble learning

• Exhaustive cross validation

• Feature engineering

• Adaptive learning

Proprietary Data

Analysis Platform

Public

RecordsCredit

Data

Social

Data

Proprietary

Data

Transactional

Data

Accounting

DataF

Acceptance Rate (%)

The OnDeck Score Personal Credit Score Random

Resulting in Funding Significantly More

Loans for the Same Risk…

More Accurate than the Personal Credit Score

at Predicting Bad Credit Risk1…

We Rely on the OnDeck Score for Greater Accuracy, Predictability and Access

10

1. Analysis on OnDeck Score v5 using actual OnDeck loan performance data.

90%

100%

0%

100% 40% 20% 10% 0%

% o

f D

efa

ults E

limin

ate

d

10%

10

20

40

Random Personal CreditScore

OnDeck Score

Online Minutes1

Automated Review As Fast As Immediately3

As Fast As Same Day

The OnDeck Solution for Small Business Lending

11

1. Application time depends on customer having the required documentation available.

2. Source: Small business survey conducted by the Federal Reserve Bank of New York, Spring 2014

3. Approximately 1/3 of customers are subjected to secondary, manual review process.

FundApproveApply

Offline33 Hours2

Manual ReviewWeeks or Months

Several Days

Traditional

Lending

Use Case

Size $5,000 – $250,000 $5,000 – $25,000

Term 3 – 24 months 6 months

Pricing1 Average monthly “cents-on-dollar” of 2.23¢

Average 52% APRAverage 36% APR

Payment Automated daily or weekly payments Automated weekly payments

Availability Renewal opportunity at ~50% paid down Draw on-demand

Tailored Products for Small Businesses

1. Based on Q4 ꞌ14.

Term Loan(Launched in 2007)

Line of Credit(Launched in September 2013)

HiringNewStaff

Buying Inventory

Marketing Managing Cash Flow

12

7.5 YearsMedian Time in Business

$569,000Median Annual Revenue

700+Industries

30,000+Small Businesses Served

in all 50 U.S. states

Established and Diverse Customer Base

13

Online

Customer

Experience

Data

Aggregation,

Analytics

and Scoring

Technology

Powered

Servicing &

Collections

Integrated and Scalable Technology Platform

14

$2 Billion+Total Originations

52,000+Total Loans

5.3 Million+Customer Payments

Diversified and Growing Distribution Channels

Numbers represent loan units.

15

1,276

5,758

14,920

2012 2013 2014

Direct

3,7315,955

8,131

2012 2013 2014

Funding

Advisors

Strategic

Partners

55%

30%

14%

Direct Funding Advisors Strategic Partners

Channel Mix 2014

4371,346

3,870

2012 2013 2014

Robust Funding Platform

16

Funding mix is shown as of December 31, 2014 based on unpaid principal balance on loans and line of credit with the exception of OnDeck-funded loans.

Securitization

Warehouse

Lines

OnDeck

Marketplace® Diversified

Scalable

Durable

Low-cost

Capital-efficient

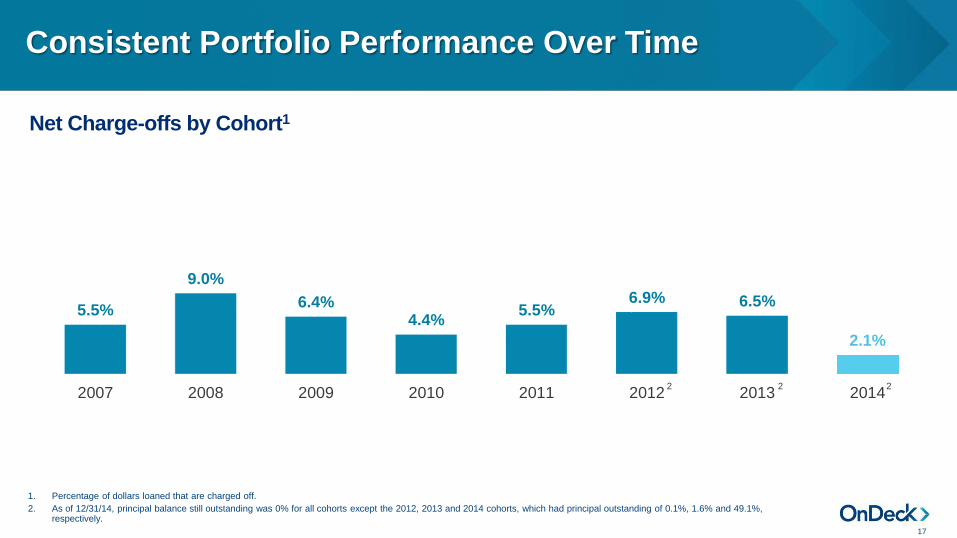

5.5%

9.0%

6.4%4.4%

5.5%6.9% 6.5%

2.1%

2007 2008 2009 2010 2011 2012 2013 2014

Net Charge-offs by Cohort1

Consistent Portfolio Performance Over Time

17

1. Percentage of dollars loaned that are charged off.

2. As of 12/31/14, principal balance still outstanding was 0% for all cohorts except the 2012, 2013 and 2014 cohorts, which had principal outstanding of 0.1%, 1.6% and 49.1%, respectively.

222

Growth Strategy

Brand and direct

marketing

Strategic partnerships

Data and analytics

Product expansion

Extend customer

lifetime value

International expansion

18

Industry Leading Management Team and Investors

Noah

Breslow

CEO

James

Hobson

COO

Paul

Rosen

Sales

Howard

Katzenberg

CFO

Zhengyuan

Lu

Capital Markets

Krishna

Venkatraman

Data & Analytics

Pamela

Rice

Technology

Cynthia

Chen

Risk

Andrea

Gellert

Marketing

Management Team Team Experience

19

Board of Directors

James Robinson IIIRRE VenturesAmerican Express

David HartwigSapphire Ventures

Sandy MillerInstitutional Venture Partners

Jane J. ThompsonWalmart Financial ServicesCFPB Advisory Board

Neil WolfsonSF Capital Group

Ron VerniSage Software

Financial Highlights

20

Capital light funding model

Compelling customer lifetime value

Rapid growth

Demonstrated operating leverage

Rapid Originations Growth

21

$28 $34$50 $61

$75$93

$122

$168

$227$248

$313

$369

Q1 '12 Q2 '12 Q3 '12 Q4 '12 Q1 '13 Q2 '13 Q3 '13 Q4 '13 Q1 '14 Q2 '14 Q3 '14 Q4 '14

($MM)

2012

The sum of the quarters may not exactly match the annual numbers due to rounding.

2013 2014

$5 $5 $7$9

$11$14

$18

$23

$29

$36

$44

$50

Q1 '12 Q2 '12 Q3 '12 Q4 '12 Q1 '13 Q2 '13 Q3 '13 Q4 '13 Q1 '14 Q2 '14 Q3 '14 Q4 '14

($MM)

Strong Gross Revenue Growth

22

The sum of the quarters may not exactly match the annual numbers due to rounding.

2012 2013 2014

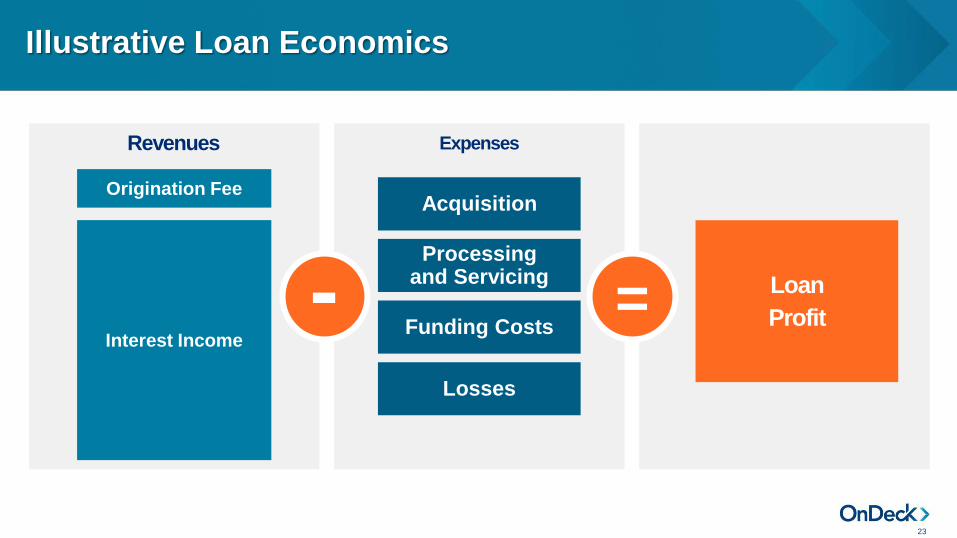

Loan

Profit

Revenues Expenses

–

Illustrative Loan Economics

23

=

Origination Fee

Interest Income

Losses

Funding Costs

Processing and Servicing

Acquisition

-

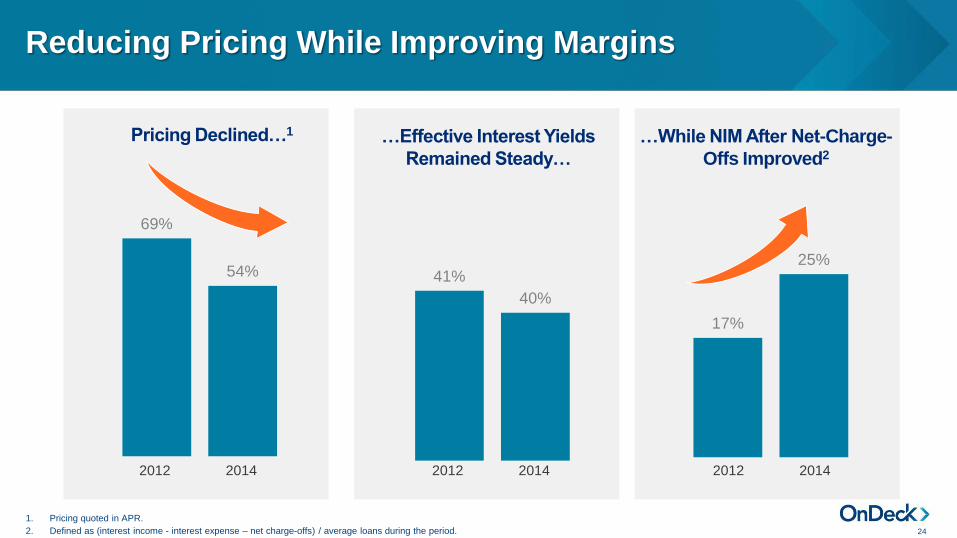

Reducing Pricing While Improving Margins

24

69%

54% 41%

40%

17%

25%

Pricing Declined…1 …Effective Interest Yields

Remained Steady…

…While NIM After Net-Charge-

Offs Improved2

2012 2014 2012 2014 2012 2014

1. Pricing quoted in APR.

2. Defined as (interest income - interest expense – net charge-offs) / average loans during the period.

Customers Acquired in Q1 ꞌ13

• Average 2.3 loans per customer in 8 quarters

• $4.1MM in interest still outstanding

($MM)

Compelling Customer Lifetime Value

25

1. Includes upfront internal and external commissions as well as direct marketing expenses.

2. Contribution is defined to include interest income and fees collected on initial and repeat loans, less acquisition costs for repeat loans, less the following items for both initial and repeat loans: estimated third party processing and servicing expenses, estimated funding costs (excluding any cost of equity capital) and charge offs. For this purpose, processing and servicing expenses are estimated based on the mix of new and renewal originations and outstanding principal balances.

3. Figures may not foot due to rounding.

3.0x+ROI

after

8 quarters

$15.4Return3

or

$5.0Investment

Q1 ꞌ13

$5.0

$2.8

$1.9

$1.5

$1.1

$1.4

Acquisition

Cost1Contribution2 Q2 ꞌ13 Q3 ꞌ13 Q4 ꞌ13 Q1 ꞌ14 Q2 ꞌ14

$1.6

Q3 ꞌ14

$3.7

$1.4

Q4 ꞌ14

81%

61%

54%

2012 2013 2014

Cost of Revenue Operating Expenses

84%

68%

51%

2012 2013 2014

Provision for Loan LossesFunding CostsSales & Marketing Technology & Analytics

Processing & Servicing General & Administrative

Demonstrated Operating Leverage

Figures are based on a percentage of gross revenue.

26

Adjusted EBITDA and Adjusted Net Loss

See appendix for a reconciliation of these non-GAAP measures.

($16.3)

($0.2)($2.1)

$0.6

($20.2)

($4.6)($3.2)

($0.8)

Adjusted EBITDA Adjusted Net Loss

2013 2014 Q4 ꞌ13 Q4 ꞌ14

27

Investment Highlights

28

Massive and underserved market

Proprietary analytics and scoring models

Integrated and scalable technology platform

Diversified customer acquisition channels

Robust funding platform

Experienced management team

Attractive financial profile

APPENDIX

1

Adjusted EBITDAYear Ended

December 31,

Three Months Ended

December 31,

(000s) 2013 2014 2013 2014

Net (Loss) Income ($24,356) ($18,708) ($5,607) ($4,291)

Adjustments:

Corporate Interest Expense 1,276 398 206 124

Income Tax Expense – – – –

Depreciation and Amortization 2,645 4,071 881 1,223

Stock-Based Compensation Expense 438 2,842 171 1,395

Warrant Liability Fair Value Adjustment 3,739 11,232 2,243 2,110

Adjusted EBITDA ($16,258) ($165) ($2,106) $561

Appendix: Non-GAAP Adjusted EBITDA Reconciliation

Adjusted EBITDA represents our net income (loss), adjusted to exclude interest expense associated with debt used for corporate purposes (rather than funding costs associated with lending activities), income tax expense, depreciation and amortization, stock-based compensation expense and warrant liability fair value adjustment. EBITDA is impacted by changes from period to period in the fair value of the liability related to preferred stock warrants. Management believes that adjusting EBITDA to eliminate the impact of the changes in fair value of these warrants is useful to analyze the operating performance of the business, unaffected by changes in the fair value of preferred stock warrants which are not relevant to the ongoing operations of the business. All such preferred stock warrants converted to common stock warrants upon initial our initial public offering in December 2014.

30

Adjusted Net LossYear Ended

December 31,

Three Months Ended

December 31,

(000s) 2013 2014 2013 2014

Net Loss ($24,356) ($18,708) ($5,607) ($4,291)

Adjustments:

Stock-Based Compensation Expense 438 2,842 171 1,395

Warrant Liability Fair Value Adjustment 3,739 11,232 2,243 2,110

Adjusted Net Loss ($20,179) ($4,634) ($3,193) ($786)

Appendix: Non-GAAP Adjusted Loss Reconciliation

Adjusted net loss represents our net income (loss) adjusted to exclude stock-based compensation expense and warrant liability fair value adjustment, each on the same basis and with the same limitations as described before for Adjusted EBITDA.

31