compendium of ifrs publications 2011 - adaa - … the beginning of the compendium is a list of the...

TRANSCRIPT

Compendium of IFRS Publications 2011

Foreword Welcome to ADAA’s first “Compendium of IFRS publications.” The Compendium comprises ADAA’s IFRS monthly Digests for the year 2011 and the accounting briefing papers on “Related Part Disclosures,” “Impairment of assets” and “Transactions with Government.” At the beginning of the Compendium is a list of the topics covered and a cross reference to the original publication and the page of the Compendium where you will find the topic. In addition, if you want to research a topic a little further, we have provided web links to articles and publications provided by the Accounting Profession. We hope that you find this Compendium useful and would welcome any feedback you might wish to provide.

ADAA’s IFRS Compendium editorial team (from left to right) Steven Ralls: [email protected] (Tel:02-6107467) Head of Accounting and Auditing Standards Richard Wright: [email protected] Nader Chatila: [email protected] Muhammad Shabbir: [email protected] Mahmoud Shahin: [email protected] Ahmed Al Meleegy: [email protected] Ashraf Sawiries: [email protected]

The Abu Dhabi Accountability Authority IFRS Compendium is written by the Accounting and Auditing Standards Desk of the Financial Audit and Professional Regulations Group of the Abu Dhabi Accountability Authority (ADAA). All rights reserved.

The Compendium considers recent IFRS content, updates, amendments and exposure drafts issued by the IASB and the accounting profession. All content is intended as information for the reader only and none of the content is intended as accounting advice. Entities should refer to ADAA direct if advice is required for a particular issue.

Any references to third party articles or websites are only intended for information purposes and should not be considered as an ADAA endorsement.

The Abu Dhabi Accountability Authority Compendium is intended primarily for the use of the clients of Abu Dhabi Accountability Authority, and it is issued in line with the terms of use that govern the Abu Dhabi Accountability Authority’s use of the International Accounting Standards Board (IASB) Website and its relationship with the International Accounting Standards Committee Foundation (IASCF).

Abu Dhabi Accountability Authority accepts no responsibility for loss or damage caused to any party who acts or refrains from acting in reliance on this publication, whether such loss is caused by negligence or otherwise.

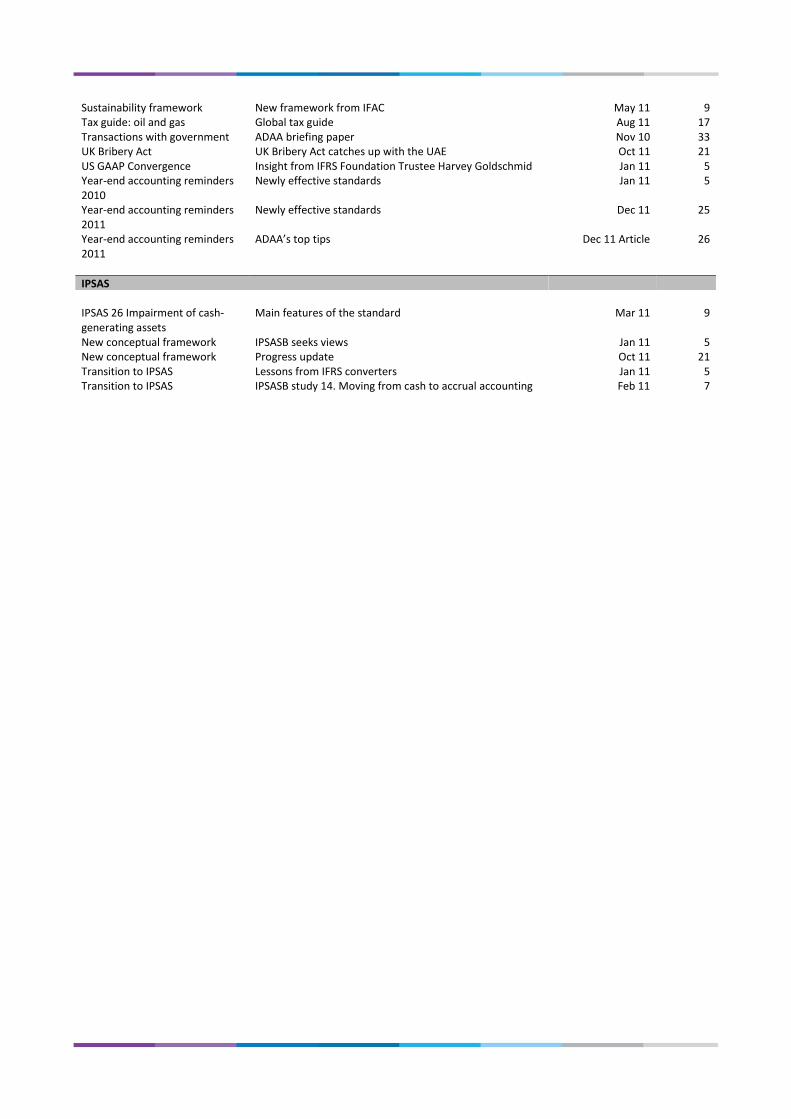

Topic Issue Publication Page

IFRS Banks Proposed changes to accounting Aug 11 17 Chemical and performance technology companies

Application of IFRS Dec 11 25

Consolidation issues Insight with reference to IFRS 3, IAS 27, IAS 38, IAS 40, SIC 12, IFRS 10, IFRS 11

Nov 11 Article 24

IASB hot topics New standards expected in 2011 Feb 11 7 IASB hot topics Updates from IASB/FASB joint sessions May 11 13 IASB update July 2011 updates Aug 11 17 IASB update IFRS 9 date delayed, changes to IAS 19 Sep 11 19 IAS 1. Presentation of financial statements

Changes to presentation of OCI Aug 11 17

IAS 24 Related party disclosures ADAA briefing paper Feb 11 27 IAS 36 Impairment of assets What do the regulators want to see Oct 11 21 IAS 36 Impairment of assets ADAA briefing paper Mar 11 30 IAS 40. Investment property Survey highlighting accounting issues Mar 11 9 IFRS 1. First-time adopters Relief for first-time adopters as available before revision to

IAS 20 Nov 11 23

IFRS 8. Segment Reporting Benefits of segment reporting Jan 11 Article 6 IFRS 8. Segment Reporting Disclosures clarified by IASB Dec 11 25 IFRS 9 Hedge accounting Exposure draft Jan 11 5 IFRS 9 Hedge accounting Developments in hedge accounting Sep 11 19 IFRS 10 Consolidated financial statements

New standard issued Jun 11 15

IFRS 11 Joint arrangements New standard issued Jun 11 15 IFRS 11 Joint arrangements Effect analysis from IASB Sep 11 19 IFRS 11 Joint arrangements Insight on new standard Oct 11 Article 22 IFRS 12 Disclosure of interests in other entities

New standard issued Jun 11 15

IFRS 13 Fair value measurement New standard issued Jun 11 15 IFRSs 2011 New IFRSs in 2011, a practical guide Apr 11 11 IFRIC 20 Stripping costs Clarification issued by IASB Nov 11 23 IFRIC update Update Nov 2011 Dec 11 25 Financial crisis Address by Hans Hoogervorst Oct 11 21 Financial crisis Address by Harvey Goldsmith Oct 11 21 Financial reporting Benefits of timely reporting Mar 11 Article 10 Financial reporting Complexity issues from IFAC Apr 11 11 Financial reporting Current economic conditions Sep 11 19 Financial reporting Illustrative financial statements Nov 11 23 Financial reporting Improving financial reporting Feb 11 Article 8 Financial reporting Recommendations for improving risk disclosures Dec 11 25 Financial reporting Non-technical summaries from IFRS Foundation Apr 11 11 Financial reporting Objectives of financial reporting from IASB Chair Mar 11 9 Goodwill Insight into goodwill referring to IFRS 3, IAS 36 & IAS 12 Apr 11 Article 12 Investment entities Exposure draft Oct 11 21 Lease accounting Latest updates to project Apr 11 11 Lease accounting Latest developments May 11 13 Lease accounting Latest updates to project Nov 11 23 Management commentary Transparency and corporate governance Sep 11 Article 20 Offsetting financial assets and liabilities

Exposure draft Feb 11 7

Professional scepticism Key focus of the accountancy profession Aug 11 Article 18 Revenue New standard, insight into revenue referring to IAS 18, IAS

11 & IFRIC 15 May 11 Article 14

Revenue Latest updates to project May 11 13 Revenue New standard proposes five steps to revenue recognition Nov 11 23 Revenue, leasing and financial instruments

Proposed new and revised standards Mar 11 9

Sustainability framework New framework from IFAC May 11 9 Tax guide: oil and gas Global tax guide Aug 11 17 Transactions with government ADAA briefing paper Nov 10 33 UK Bribery Act UK Bribery Act catches up with the UAE Oct 11 21 US GAAP Convergence Insight from IFRS Foundation Trustee Harvey Goldschmid Jan 11 5 Year-end accounting reminders 2010

Newly effective standards Jan 11 5

Year-end accounting reminders 2011

Newly effective standards Dec 11 25

Year-end accounting reminders 2011

ADAA’s top tips Dec 11 Article 26

IPSAS IPSAS 26 Impairment of cash-generating assets

Main features of the standard Mar 11 9

New conceptual framework IPSASB seeks views Jan 11 5 New conceptual framework Progress update Oct 11 21 Transition to IPSAS Lessons from IFRS converters Jan 11 5 Transition to IPSAS IPSASB study 14. Moving from cash to accrual accounting Feb 11 7

January 2011

Compendium of IFRS Publications is issued by ADAA. All rights reserved.

5 of 34

Abu Dhabi Accountability Authority monthly digest

ADAA Highlights IFRS news, IPSAS and updates from the IASB, IFAC and the Accounting Profession

ADAA’s hot topics

What’s new this month?

The benefits of segment reporting – on the back page ADAA’s Muhammad Shabbir highlights how IFRS 8 provides management with a unique opportunity to convey to shareholders how they review and monitor business performance.

IFRS at critical crossroads? IFRS Foundation trustee Harvey Goldschmid increases the pressure on FASB and the SEC to let go of USGAAP and adopt IFRS. Harvey explains his concerns that the quality of accounting standards might diminish.

Hedge accounting under IFRS — Good news! The IASB has released an exposure draft to substantially simplify hedge accounting. This is the third phase of the IASB’s project to replace IAS 39.

Mastering the transformation to IPSAS Time, knowledge, resources are limited so how best to approach the transfer from cash accounting to accruals and to full IPSAS? IPSASB seeks views on the new Conceptual Framework: Alongside the IASB’s program IPSASB is updating its framework that sets out the principles of IPSAS. If there isn’t a standard to apply accountants turn to the framework. If there is a standard but applying it is not clear, accountants turn to the framework. You have an opportunity to have your say. Year-end accounting reminders

Reminder: effective dates of IFRSs for interim and annual periods ending 31 December 2010. ADAA suggests the new standard on IAS 24 Related Parties is adopted early.

The IASB is located in Cannon Street in London The IPSASB is located on the 5th Avenue in New York

What’s new from the IASB? What’s new from the IPSASB?

IFRS at critical crossroads?

Foundation trustee Harvey Goldschmid expresses his concerns If the US SEC comes to a negative decision on IFRS adoption:

That the coalition of nations supporting IFRS could break apart and nations return to pre-2000 fragmentation of many national accounting systems.

That the coalition in support of IFRS could hold, the US becomes isolated and the quality of IFRS accounting standards suffers as a result.

The full article is available here

Mastering the transformation to IPSAS a few thoughts on the lessons learned from IFRS converters;

Start early – there is never enough time.

It is a change project, people, processes and systems will change and this can be uncomfortable.

Short-term solutions are only short-term.

Do not underestimate the need to train people well.

Two documents that may help can be accessed

from Deloitte’s website here and here.

IPSASB seeks views on the new Conceptual Framework: Key principles are: Relevance, Faithful Representation, Understandability, Timeliness, Comparability and Verifiability. The

ED can be read here.

Please turn the page for ADAA’s monthly accounting insight…

What’s new from the Accounting Profession?

Hedge accounting under IFRS — Good news! Actually it’s not all good news. The IASB’s theme of “through the eyes of management” continues and hedge effectiveness will be driven by an entity’s risk management strategy. The 80-125% rule goes but mandatory discontinuance of a hedge relationship remains if the relationship no longer qualifies. There are changes to what goes to Other Comprehensive Income. There are new rules for groups of hedges and significant new disclosures. EY’s publication may be accessed here

Year-end accounting reminders For 31 December 2010 reporters here is a reminder of the newly effective standards (and of standards issued and not effective). Access

KPMG’s publication here. A major change is for leases of land that may result in operating leases being reclassified as finance leases. Reclassification is retrospective.

Access KPMG’s publication here. ADAA suggests the new standard on IAS 24 Related Parties is adopted early. Our September

article can be accessed here.

January 2011

Compendium of IFRS Publications is issued by ADAA. All rights reserved.

6 of 34

Abu Dhabi Accountability Authority monthly digest

ADAA Highlights IFRS news, IPSAS and updates from the IASB, IFAC and the Accounting Profession

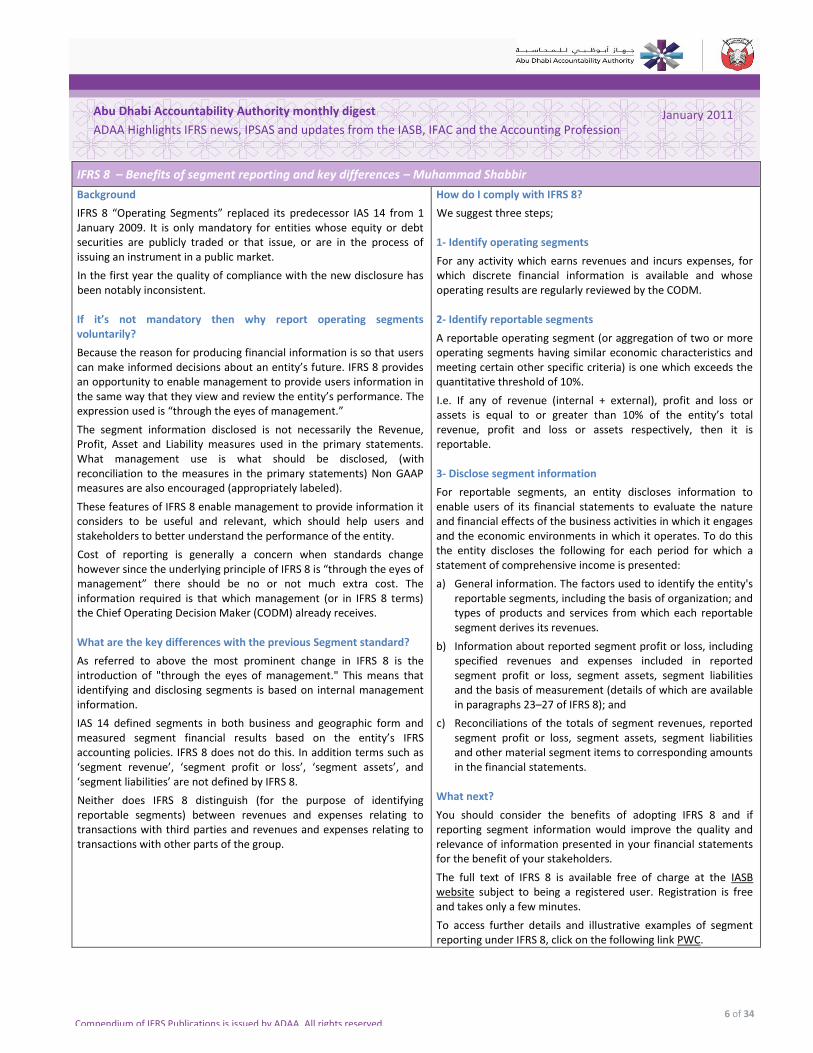

IFRS 8 – Benefits of segment reporting and key differences – Muhammad Shabbir

Background

IFRS 8 “Operating Segments” replaced its predecessor IAS 14 from 1 January 2009. It is only mandatory for entities whose equity or debt securities are publicly traded or that issue, or are in the process of issuing an instrument in a public market.

In the first year the quality of compliance with the new disclosure has been notably inconsistent. If it’s not mandatory then why report operating segments voluntarily?

Because the reason for producing financial information is so that users can make informed decisions about an entity’s future. IFRS 8 provides an opportunity to enable management to provide users information in the same way that they view and review the entity’s performance. The expression used is “through the eyes of management.”

The segment information disclosed is not necessarily the Revenue, Profit, Asset and Liability measures used in the primary statements. What management use is what should be disclosed, (with reconciliation to the measures in the primary statements) Non GAAP measures are also encouraged (appropriately labeled).

These features of IFRS 8 enable management to provide information it considers to be useful and relevant, which should help users and stakeholders to better understand the performance of the entity.

Cost of reporting is generally a concern when standards change however since the underlying principle of IFRS 8 is “through the eyes of management” there should be no or not much extra cost. The information required is that which management (or in IFRS 8 terms) the Chief Operating Decision Maker (CODM) already receives. What are the key differences with the previous Segment standard?

As referred to above the most prominent change in IFRS 8 is the introduction of "through the eyes of management." This means that identifying and disclosing segments is based on internal management information.

IAS 14 defined segments in both business and geographic form and measured segment financial results based on the entity’s IFRS accounting policies. IFRS 8 does not do this. In addition terms such as ‘segment revenue’, ‘segment profit or loss’, ‘segment assets’, and ‘segment liabilities’ are not defined by IFRS 8.

Neither does IFRS 8 distinguish (for the purpose of identifying reportable segments) between revenues and expenses relating to transactions with third parties and revenues and expenses relating to transactions with other parts of the group.

How do I comply with IFRS 8?

We suggest three steps; 1- Identify operating segments

For any activity which earns revenues and incurs expenses, for which discrete financial information is available and whose operating results are regularly reviewed by the CODM. 2- Identify reportable segments

A reportable operating segment (or aggregation of two or more operating segments having similar economic characteristics and meeting certain other specific criteria) is one which exceeds the quantitative threshold of 10%.

I.e. If any of revenue (internal + external), profit and loss or assets is equal to or greater than 10% of the entity’s total revenue, profit and loss or assets respectively, then it is reportable.

3- Disclose segment information

For reportable segments, an entity discloses information to enable users of its financial statements to evaluate the nature and financial effects of the business activities in which it engages and the economic environments in which it operates. To do this the entity discloses the following for each period for which a statement of comprehensive income is presented:

a) General information. The factors used to identify the entity's reportable segments, including the basis of organization; and types of products and services from which each reportable segment derives its revenues.

b) Information about reported segment profit or loss, including specified revenues and expenses included in reported segment profit or loss, segment assets, segment liabilities and the basis of measurement (details of which are available in paragraphs 23–27 of IFRS 8); and

c) Reconciliations of the totals of segment revenues, reported segment profit or loss, segment assets, segment liabilities and other material segment items to corresponding amounts in the financial statements.

What next?

You should consider the benefits of adopting IFRS 8 and if reporting segment information would improve the quality and relevance of information presented in your financial statements for the benefit of your stakeholders.

The full text of IFRS 8 is available free of charge at the IASB website subject to being a registered user. Registration is free and takes only a few minutes.

To access further details and illustrative examples of segment reporting under IFRS 8, click on the following link PWC.

February 2011

Compendium of IFRS Publications is issued by ADAA. All rights reserved.

7 of 34

Abu Dhabi Accountability Authority monthly digest

ADAA Highlights IFRS news, IPSAS and updates from the IASB, IFAC and the Accounting Profession

ADAA’s hot topics

What’s new this month?

Offsetting Financial Assets and Financial Liabilities –your opportunity to shape the rules to determine the basis for offsetting financial assets and financial liabilities by commenting on Exposure Draft 2011/1. Hot topics from the IASB this year - It is going to be a busy year for the IASB (and us). Ten new (or updated) standards are expected this year. Public Private Partnerships (PPP) challenged. State owned entities (SOEs) rise Having rescued the private sector with state investments and citizen taxes, the idea that the private sector model is always the best model for creating wealth and improving public services is being doubted by many policy-makers.

Transition to the Accrual Basis of Accounting – Public Sector – Additional guidance from IPSASB to help Government entities moving from cash accounting to accruals accounting. Does your corporate business plan harness the growth prospects of emerging markets - PWC survey 1,201 business leaders and CEOs in 69 countries during the last quarter of 2010. This publication highlights where they see growth coming from, and how to achieve it. Raising the Bar - On the back page ADAA’s Steve Ralls provides an insight into improving financial reporting.

The IASB is located in Cannon Street in London The IPSASB is located on the 5

th

Avenue in New York

What’s new from the IASB? What’s new from the IPSASB?

Offsetting Financial Assets and Financial Liabilities Offsetting will only be allowed when there exists a right enforceable at all times. Comments to be received by 28 April 2011. Click the link for the Full text of Exposure Draft 2011/1 Hot topics from the IASB this year - It is going to be a busy year for the IASB and us so if you are thinking of retiring….! We expect ten new (or updated) standards in 2011.

Financial institutions will be particularly affected by the change to IAS 39/IFRS 9, impairment and hedge accounting.

Conglomerates will need to reconsider entities that they control and SPEs.

All of us will need to consider the new leasing and revenue standards. If you are entering into new leases now we suggest you test the accounting under the proposed revised IAS 37. Click the link to View IASB Work Plan

Transition to the Accrual Basis of Accounting – Public Sector. IPSASB released study 14 “Transition to the accrual basis accounting: Guidance for Governments and Government entities (Third Edition)”. The publication is a “must read” for Public Sector entities this quarter. It runs to more than 300 pages so it will take a while to work through it! Study 14 is structured into four parts.

Part I address the logistics of the transition process.

Part II deals with the selection, development, and approval of accounting policies, and issues associated with the definition and identification of reporting entities.

Part III outlines the broad steps required for the identification, recognition, measurement, and disclosure of assets, liabilities, revenues, and expenses.

Part IV highlights implementation issues associated with specific IPSASs. Get Study 14

Please turn the page for ADAA’s monthly accounting insight…

What’s new from the Accounting Profession?

Public Private Partnerships (PPP) challenged. State owned entities (SOEs) rise - SOEs can outperform private companies if they possess four key factors: governance, strategy, innovation and corporate social responsibility. Evidence is found in many of the fastest-growing economies – particularly China. EY surveyed over 12,000 citizens in 24 countries they reported they had largely positive feelings about the state-owned companies of their own countries. The full article is available in this link. Get Government as Best in Class Shareholder

Does your corporate business plan harness the growth prospects of emerging markets - Chief executives are nearly as confident of growth this coming year as in the boom years before the financial crisis. Big emerging markets like China, India and Indonesia are growing much faster than the world economy. This multi-speed recovery will have a big impact on strategies going forward. Get the 14th Annual Global CEO Survey from PWC.

February 2011

Compendium of IFRS Publications is issued by ADAA. All rights reserved.

8 of 34

Abu Dhabi Accountability Authority monthly digest

ADAA Highlights IFRS news, IPSAS and updates from the IASB, IFAC and the Accounting Profession

“Raising the bar” – Steve Ralls

Raising the bar

It is a favourite expression of mine. Every day we try to improve the quality of what we do and the outputs we provide. We can’t all be as innovative as entities such as Apple and change industries (after all we are accountants!) but we can innovate in improving our financial reporting. So how to raise the bar?

If one enters “quality” into an internet search engine, the results show there are two aspects to quality;

Quality Control, and

Quality Assurance. Quality control procedures ensure the quality of reporting and quality assurance procedures affirm or “attest” the quality achieved. So what can be done to improve these? For the Auditors

For the Auditing profession the IAASB has published “Audit Quality an IAASB perspective” access it here. Their focus is on the new clarity International Auditing Standards (IASs) which particularly cover;

Instilling a thinking audit and the importance of professional scepticism

Focussing on higher risk areas; estimates, fair value and related party transactions

Quality of evidence – external third party compared to management representations

For group audits is it appropriate to rely on the work of others

Communicating important matters in a clear and meaningful way The words in the ISAs might be aimed at the auditors but they seemingly apply to accountants in preparing financial statements too. For the Accountants

The IASB continues its programme to enhance and improve International Financial Standards. In May 2010 they published the annual “Improvements to IFRS,” in November IAS 24 Related party disclosures and in October the first of the amendments to financial instruments. They are going to be busy this year too and so will we! Topics will include; the remaining changes to financial instruments, fair value measurement guidance, control and SPE’s, Presentation, Revenue, Post employment benefits and liabilities.

The growing consensus is that to achieve high quality financial reporting entities should apply IFRS (or in the Public Sector IPSAS). US GAAP continues to align with the IASB as evidenced by their latest project on offsetting financial assets and liabilities which will result in offsetting only where there exists a right enforceable at all tImes. Click here to visit the web page, review the project and listen to the web cast.

For Management

Quality in financial reporting is demonstrated by doing more than just compliance. High quality financial statements tell a story and they enhance the understanding of the reader by answering the questions as they arise. They are easy to read, deal with the key risks and judgments and have a logical flow. Here are four ideas to consider;

Investor studies confirm that increasing the transparency of an organization increases its value. The IASB has recently published a non-mandatory practice statement to help entities present a narrative report. This information helps management to explain to users of financial statements management’s objectives, their strategies for achieving them and how they affect financial performance and financial position.

IFRS 8 segment reporting is not mandatory unless an entity is listed. However for non-listed entities the application of IFRS 8 is a huge opportunity to improve the transparency of their reporting and when combined with a high quality management commentary is of great benefit to users of the financial statements.

Adopt standards early. Every standard or amendment to a standard has a date by when it must be implemented. However, the standards also normally encourage early adoption. Why? Because the new treatment is better, so why do something that is not so good? There are a series of amendments to standards that are not effective until 2011 or 2012. But why leave them until then? Is the accounting treatment less favorable? Or is the cost too much or the change too difficult? Are any of these good reasons not to implement the change early?

IPSAS 24 – presentation of budget information in financial statements. Just in case you thought we had forgotten our Public Sector friends! IPSAS 24 is only mandatory if budgets are published – most aren’t and neither are the financial statements either – IPSAS 24 arguably gives a better opportunity to explain the results than Management commentary gives to IFRS reporters.

As you close your 31 December 2010 reporting we wish you well with your financial close and encourage you to continue on your path “raising the bar.”

March 2011

Compendium of IFRS Publications is issued by ADAA. All rights reserved.

9 of 34

Abu Dhabi Accountability Authority monthly digest

ADAA Highlights IFRS news, IPSAS and updates from the IASB, IFAC and the Accounting Profession

ADAA’s hot topics

What’s new this month?

The benefits of timely financial information: on the back page ADAA’s Richard Wright provides an insight. The objectives of financial reporting. The incoming Chair of the IASB addresses the European Commission’s conference “Financial Reporting and auditing – A time for change?” Big changes coming soon will you be ready? Proposed new and revised standards on accounting for revenue, leasing and financial instruments. We show you where you can learn more.

IFRS for real estate. This survey of nearly 40 property companies including two from the UAE highlights the issues around accounting for investment properties. The continuing uncertainty in the sector has led to an increase in demand for greater transparency in accounting and reporting, seemingly a greater number of companies have improved the quality of their disclosure. IPSAS 26—Impairment of Cash-Generating Assets. To help Government Agencies in their transition to IPSAS, we highlight the main features of the standard.

The IASB is located in Cannon Street in London The IPSASB is located on the 5

th Avenue in

New York

What’s new from the IASB? What’s new from the IPSASB?

The objectives of financial reporting. The incoming Chair of the IASB Hans Hoogervorst considers that the overall objective of financial reporting standards must be transparency.

Speaking on the financial crisis Hans considers that a lack of focus on transparency by banks resulted in risks being kept out of the balance sheet.

Hans notes that there is still much for the IASB to consider but accounting standards improving.

Hans cites “OCI as a pragmatic way of shielding the P&L from volatility” as being one of the successes. His full speech can be accessed here

IPSAS 26—Impairment of Cash-Generating Assets

The Standard provides the requirements for the identification of assets that may be impaired.

IPSAS 26 is drawn primarily from IAS 36. The main differences between the standards are:

IPSAS 26 does not apply to cash-generating assets carried at revalued amounts, IAS 36 does.

IPSAS 26 does not apply to intangible assets that are regularly revalued to fair value, IAS 36 does.

Goodwill is outside the scope of IPSAS 26. It is inside the scope of IAS 36.

IPSAS 26 does not consider a forced sale to be a reflection of fair value less costs to sell. IAS 36 does if management is compelled to sell immediately.

The full text of IPSAS 26 and further details on IAS 36 differences are on the IFAC website here

Please turn the page for ADAA’s monthly accounting insight…

What’s new from the Accounting Profession?

Big changes coming soon will you be ready?

The proposed new and revised standards on accounting for revenue, leasing and financial instruments will have a major impact on the financial statements of almost every entity. KPMG has produced a series of publications “New on the horizon” that showcase an exposure draft’s requirements and provides background and comment. If you want to get ahead of the competition on a host of topics click here.

IFRS for real estate: current issues and financial statements survey. The survey undertaken by EY concludes;

90% of entities use fair value rather than the cost model in IAS 40.

Disclosure of assumptions and valuation methods has greatly improved.

The number of companies providing sensitivity analysis is now nearly half.

The survey includes ALDAR Properties and EMAAR Properties. Full access to the survey is available here

March 2011

Compendium of IFRS Publications is issued by ADAA. All rights reserved.

10 of 34

Abu Dhabi Accountability Authority monthly digest

ADAA Highlights IFRS news, IPSAS and updates from the IASB, IFAC and the Accounting Profession

The benefits of timely financial information – Richard Wright

Before you leave home do you check the weather forecast?

Before leaving for the airport do you check the website to see if your flight is on time?

Before you drive, do you check the traffic news?

Before you invest do you check a company’s financial performance?

Before we make any decision we seek information to check our decision is the ‘best.’ Critical to the decision is the timeliness of that information.

Yesterday’s weather forecast will not tell you whether you can leave your umbrella behind in London although it does in Abu Dhabi! Why timely financial information is important?

IAS 1.9 states “the objective of financial statements is to provide information about the financial position, performance and cash flows of an entity that is useful.” The IFRS Framework notes “The usefulness of financial information is enhanced if it is timely. Timeliness means available in time to influence decisions. The older the information is the less useful it is”. The US Government (Accounting) Standards Board stated “the passage of time diminishes the usefulness that the information otherwise would have had". It is hard to think of any benefit old financial information has. Why a last minute rush reduces quality

When a deadline approaches a disproportionate amount of time can be required by management, finance teams and statutory auditors to get the reporting finished. Sometimes quality suffers. Timely financial reporting improves quality, improves efficiency and enables management to focus on telling the financial story. Timely reporting must be balanced against reliable reporting since there is no point in reporting wrong information. Most entities should be capable of reporting within 6 months from the end of their financial year. How to achieve timely reporting?

Finance management, statutory auditors and non-finance management all need to be committed, enthusiastic, well briefed and working as one team. Fail to plan, plan to fail. The team needs a well thought through agreed project plan. Making the year-end just another month (or just another quarter); there really should not be anything ‘special’ that happens at the year-end.

Users of timely information

Public entities have many user groups; employees, shareholders, suppliers, customers and government. All need information to consider how they will interact with an entity and to assess how effective the entity is in achieving its objectives. Timely financial information is naturally more relevant and useful in these respects. Improved financial management

Timely reporting helps entities to identify and correct weaknesses in their financial systems. There is a clear link between excellence in financial management and the ability to prepare financial information in a timely manner. Entities can use the financial reporting process as an iterative learning and quality enhancing cycle such that the quality of the financial systems continually improves and timelines of reporting becomes a by-product of effective financial management. Improving use of resources

Automating processes, improving controls, removing blocks, streamlining, enhancing and refining the flow of information improves the use of resources and balances the demands placed on finance departments throughout the year. Timely reporting promotes good governance

Timely reporting evidences and enhances good governance because it enhances an entity's ability to plan for the future by spotting opportunities and avoiding threats. It clearly also helps with budget setting discussions! What is timely?

Most listed entities report within 3 months of their year-end date. Many private and government entities report within 6 months of their year-end date. In Abu Dhabi listed entities report within 3 months and the Government plans to report within 6 months. Government entities will therefore need to report within 5 months i.e. May 31

st for 31

December reporters. A timely conclusion!

Timely financial reporting is a positive response to the objectives of the Abu Dhabi Government. It demonstrates managerial capability, accountability and transparency. Timely reporting builds trust and confidence and improves relevance and usefulness of information. Timely financial reporting is a key characteristic for all standard setters. Timely financial information enhances quality, makes effective use of resources, promotes good governance and strengthens the relevance of information to users.

April 2011

Compendium of IFRS Publications is issued by ADAA. All rights reserved.

11 of 34

Abu Dhabi Accountability Authority monthly digest

ADAA Highlights IFRS news, IPSAS and updates from the IASB, IFAC and the Accounting Profession

ADAA’s hot topics

What’s new this month?

IFRS resources directly from IASB Briefing for Chief Executives, Audit Committees and Boards of Directors

Forward looking or just want to stay ahead of competition, listen to what standard setter has to say: A bank of valuable insights and tools from the accounting profession

A Practical guide to new IFRSs for 2011. More on lease project – lease term and variable lease payments simplified.

Sharing deal insight PwC reviews deal activity in EMEA. Rethinking the role of government in the 21

st century -

to respond to change in the economic climate, and the onset of public sector recessions in many countries.

Financial statements face complexity issues Business leaders demand a new form of business reporting which integrates an entity’s social and environmental performance with its economic performance. How profound are the required changes to financial reporting?

US CPA exam in UAE His Excellency Riyad Al Mubarak, Chairman of ADAA noted: “We are very pleased at Abu Dhabi Accountability Authority with the news; it is overwhelming to see that our efforts have been successful and our initiative becoming a reality. It has been a long journey since our first contact with the Illinois Board of Examiners proposing to administer the exam in Abu Dhabi.”

Goodwill – is it good? On the back page ADAA’s Ahmed El Meleegy provides an insight.

The IASB is located in Cannon Street in London The IPSASB is located on the 5

th Avenue in

New York

What’s new from the IASB? What’s new from the IPSASB?

Briefing for Chief Executives, Audit Committees and Boards of Directors: The IFRS Foundation of IASB has published concise and easy to use briefing notes which provide summaries of all IFRS in non-technical language. Briefing notes are specially prepared to provide a broad overview of IFRS and of the business implications of implementing them. For a nominal charge it can be accessed here.

Forward looking or just want to stay ahead of competition, listen to what standard setter has to say: Podcast provides short summary of the main topics and projects discussed at IASB Board and Interpretations Committee meetings. This month’s summaries also include discussions on IFRIC 15 “Agreement for the Construction of Real Estate” and can be accessed here.

Financial statements face complexity issues IFAC interviewed business leaders and published a report titled “Integrating the Business Reporting Supply Chain”. They expressed the need for profound changes to financial reporting.

'Elemental changes to the current format of financial reporting need to be made to increase its relevance and stakeholder value and stem the increasing complexity that has plagued financial reporting in recent years', IFAC’s report says.

Please turn the page for ADAA’s monthly accounting insight…

What’s new from the Accounting Profession?

A practical guide to new IFRSs for 2011 This 24-page guide by PwC provides a high-level outline of the key requirements of new IFRS standards and interpretations that come into effect in 2011, in question and answer format. Get started here.

More on lease project - lease term and variable lease payments simplified E&Y publication highlights the latest updates to IASB and FASB joint lease project. Get hold of the proposed changes here.

Sharing deal insight PwC reviews the financial services deal activity in EMEA. To get the recent trends and future developments, including analysis of latest transactions and insights into emerging investment opportunities click here.

Rethinking the role of the government in the 21st century With the change in the economic climate, and the onset of public sector recessions in many countries, governments are now being called on to rethink their roles and develop policies to achieve ‘good growth’ and tackle their deficits by doing things very differently, as well as doing fewer (and different) things. This PwC report assesses the changing relationship between government and business as the world emerges from the depths of global recession.

Good news! CPA Exam in UAE ADAA hosted a press conference at the Emirates Palace to announce the beginning of the international administration of the Uniform CPA Examination this coming August in the UAE, Bahrain, Kuwait and Lebanon. For full press coverage and many other useful links click here.

April 2011

Compendium of IFRS Publications is issued by ADAA. All rights reserved.

12 of 34

Abu Dhabi Accountability Authority monthly digest

ADAA Highlights IFRS news, IPSAS and updates from the IASB, IFAC and the Accounting Profession

Goodwill – is it good? ADAA’s Ahmed El Meleegy provides a view

Goodwill is a good intangible

In a merger or acquisition management will focus on the percentage of the purchase price accounted for by goodwill. Generally speaking, the higher this figure, the better! Goodwill is good, because it is not amortised. As a result it doesn’t hurt earnings, unlike other intangible and tangible assets

Perhaps this is why the IASB updated IFRS 3 and increased in the focus on intangibles.

Often very little information is disclosed by entities about their goodwill, even at the time of an acquisition. It is just the residual.

IFRS 3R now places even more emphasis on management looking much more closely at transactions for specific intangibles, even if the result is more amortisation of intangibles to earnings. Goodwill should be definable

Goodwill is the residual in a business combination after recognising all of an acquiree’s identifiable assets, liabilities, and contingent liabilities. This results in the illusion that goodwill is not measurable. It is just the last number standing, with no basis for it.

IFRS 3R does not accept this. Goodwill is definable and an acquirer should understand what the residual un-definable goodwill represents.

Appendix B to the standard requires disclosure of a description of the factors that make up goodwill. Goodwill often comes down to a combination of one or more of the following four factors:

Workforce value.

Going-concern value.

Payment of anticipated synergies between the merging organisations.

Overpayment! Effect of IFRS 3R on the measurement of Goodwill

Goodwill continues to be a residual but It is likely a different residual compared to the previous standard.

IFRS 3R provides additional clarity that may result in more intangibles being recognised reducing the residual goodwill.

All consideration, including any previously held interest, is measured at fair value. Changing the residual.

IFRS 3R provides an option, on each transaction to measure non-controlling interests at full fair value or at the fair value of their proportion of identifiable assets and liabilities (same as previous standard). The first option, will result in higher goodwill.

Goodwill Impairment principle

The principle of impairment under IFRS is to impair an asset (or a group of assets) when the entity is not able to recover the carrying value either through use or the sale of the asset (or group of assets).

Goodwill created by applying IAS 12

Goodwill may be created due to the requirement of IAS 12 to measure deferred tax based on the difference between the carrying amount of an asset or liability and its tax base rather than measuring the deferred tax based on its fair value, which could be tiny or even zero.

For the purpose of impairment assessment, IAS 36 explicitly requires tax to be excluded from the estimate of future cash flows and therefore deferred taxes are also excluded in determining the value of the cash generating unit. This causes a problem and there has been some debate in the accounting profession as to the intention of IAS 36 to require an immediate impairment of goodwill caused by the recognition of deferred tax liabilities in excess of their fair value.

To avoid this impairment it has been suggested that the deferred tax liability in excess of the fair value may be offset against the goodwill and the net amount only to be tested to determine whether that goodwill is impaired. ADAA does not subscribe to this view and considers that if Fair Value Less Cost To Sell is used to test the goodwill then the problem of IAS 12 interacting with IAS 36 is avoided.

The IASB have issued an amendment to IAS 12 (effective 2011) which deals specifically with this problem where it relates to investment properties. Goodwill Impairment and the crisis

The results of the latest study by Houlihan Lokey. (European Goodwill Impairment Study 2010-2011) on the goodwill impairment recorded by the 600 largest European companies listed in the STOXX Europe 600 Index surprisingly indicates that overall reported levels of goodwill have not really been affected by the financial crisis. This is reflected in the reported goodwill impairment from 2005 to 2009 of Euro 2 trillion, of which only Euro 0.1 trillion was booked during the crisis period of 2008 to 2009.

The situation appears dramatically different in the USA. Duff & Phelps (2010 Goodwill Impairment Study) on 5,175 U.S companies indicates a substantial goodwill impairment in 2005–2009 which occurred just as the financial crisis was reaching its peak. Reported goodwill impairment of US$ 227 billion from 2005 to 2009, of which US$ 188 billion was booked in 2008 and US$ 26 billion in 2009.

This huge variance between the goodwill impairment reported in

Europe (IFRS adopter) and USA (US GAAP adopter) could raise a question about the effectiveness of impairment testing under IFRS compared to US GAAP. However, the standards are pretty similar. Perhaps more likely is that the assumptions that rest behind the assessments came under greater challenge and scrutiny in the USA.

May 2011

Compendium of IFRS Publications is issued by ADAA. All rights reserved.

13 of 34

ABU DHABI ACCOUNTABILITY AUTHORITY MONTHLY DIGEST

ADAA Highlights IFRS news, IPSAS and updates from the IASB, IFAC and the Accounting Profession

ADAA’s hot topics

What’s new this month?

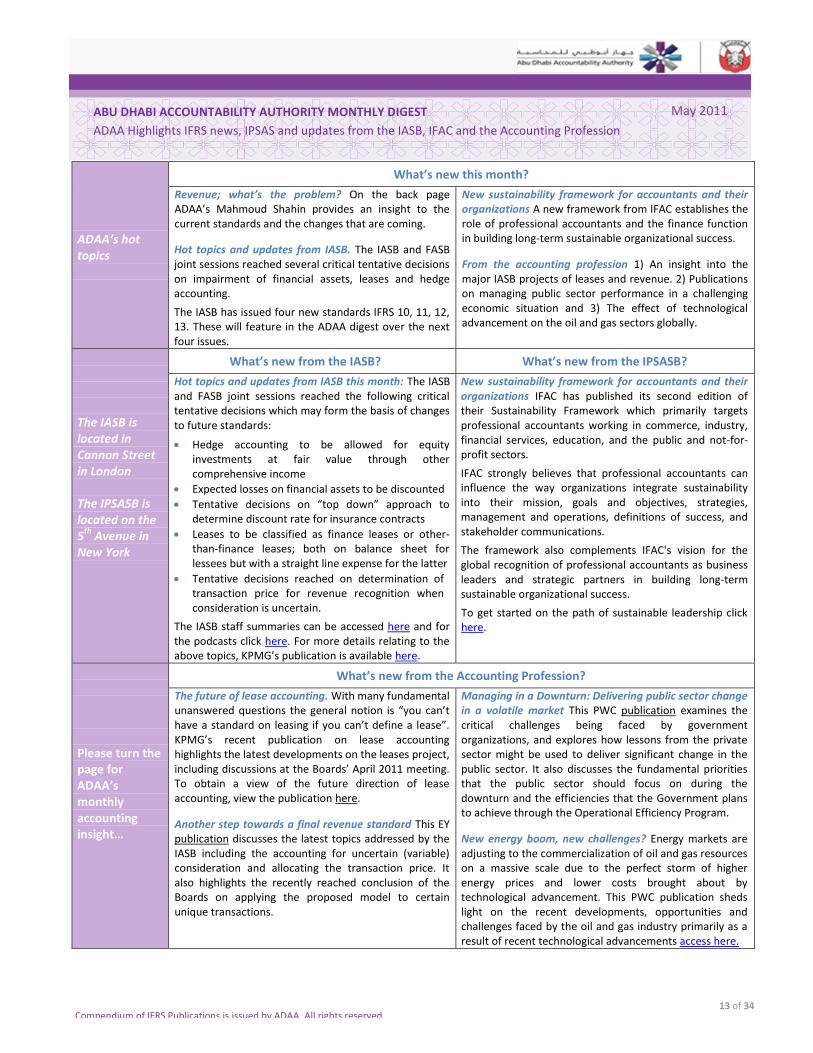

Revenue; what’s the problem? On the back page ADAA’s Mahmoud Shahin provides an insight to the current standards and the changes that are coming.

Hot topics and updates from IASB. The IASB and FASB joint sessions reached several critical tentative decisions on impairment of financial assets, leases and hedge accounting.

The IASB has issued four new standards IFRS 10, 11, 12, 13. These will feature in the ADAA digest over the next four issues.

New sustainability framework for accountants and their organizations A new framework from IFAC establishes the role of professional accountants and the finance function in building long-term sustainable organizational success.

From the accounting profession 1) An insight into the major IASB projects of leases and revenue. 2) Publications on managing public sector performance in a challenging economic situation and 3) The effect of technological advancement on the oil and gas sectors globally.

The IASB is located in Cannon Street in London The IPSASB is located on the 5

th Avenue in

New York

What’s new from the IASB? What’s new from the IPSASB?

Hot topics and updates from IASB this month: The IASB and FASB joint sessions reached the following critical tentative decisions which may form the basis of changes to future standards:

Hedge accounting to be allowed for equity investments at fair value through other comprehensive income

Expected losses on financial assets to be discounted

Tentative decisions on “top down” approach to determine discount rate for insurance contracts

Leases to be classified as finance leases or other-than-finance leases; both on balance sheet for lessees but with a straight line expense for the latter

Tentative decisions reached on determination of transaction price for revenue recognition when consideration is uncertain.

The IASB staff summaries can be accessed here and for the podcasts click here. For more details relating to the above topics, KPMG’s publication is available here.

New sustainability framework for accountants and their organizations IFAC has published its second edition of their Sustainability Framework which primarily targets professional accountants working in commerce, industry, financial services, education, and the public and not-for-profit sectors.

IFAC strongly believes that professional accountants can influence the way organizations integrate sustainability into their mission, goals and objectives, strategies, management and operations, definitions of success, and stakeholder communications.

The framework also complements IFAC's vision for the global recognition of professional accountants as business leaders and strategic partners in building long-term sustainable organizational success.

To get started on the path of sustainable leadership click here.

Please turn the page for ADAA’s monthly accounting insight…

What’s new from the Accounting Profession?

The future of lease accounting. With many fundamental unanswered questions the general notion is “you can’t have a standard on leasing if you can’t define a lease”. KPMG’s recent publication on lease accounting highlights the latest developments on the leases project, including discussions at the Boards’ April 2011 meeting. To obtain a view of the future direction of lease accounting, view the publication here.

Another step towards a final revenue standard This EY publication discusses the latest topics addressed by the IASB including the accounting for uncertain (variable) consideration and allocating the transaction price. It also highlights the recently reached conclusion of the Boards on applying the proposed model to certain unique transactions.

Managing in a Downturn: Delivering public sector change in a volatile market This PWC publication examines the critical challenges being faced by government organizations, and explores how lessons from the private sector might be used to deliver significant change in the public sector. It also discusses the fundamental priorities that the public sector should focus on during the downturn and the efficiencies that the Government plans to achieve through the Operational Efficiency Program.

New energy boom, new challenges? Energy markets are adjusting to the commercialization of oil and gas resources on a massive scale due to the perfect storm of higher energy prices and lower costs brought about by technological advancement. This PWC publication sheds light on the recent developments, opportunities and challenges faced by the oil and gas industry primarily as a result of recent technological advancements access here.

May 2011

Compendium of IFRS Publications is issued by ADAA. All rights reserved.

14 of 34

ABU DHABI ACCOUNTABILITY AUTHORITY MONTHLY DIGEST

ADAA Highlights IFRS news, IPSAS and updates from the IASB, IFAC and the Accounting Profession

Revenue; what’s the problem? - ADAA’s Mahmoud Shahin provides a view

A potted history

IAS 11 ‘Construction Contracts’ was issued in 1993 alongside the updated IAS 18 ‘Revenue’ (previously ‘Revenue Recognition’ issued in 1982!) The standards have been collectively updated a total of 18 times since then. The major update being IFRIC 15 ‘Agreements for the construction of Real Estate’ which some see as bridging the gap between the two standards. So what’s the problem?

Put simply the standards have different core principles and IAS 18 is inconsistent within itself. Neither are the standards truly in line with the IFRS Framework. The Framework refers to “increases in economic benefits.” IAS 11 requires revenue to be recognized by reference to the stage of completion of a contract at the end of a reporting period. IAS 18 for the sale of goods requires that revenue is recognized only when effective control and the risks and rewards of ownership of the goods are transferred to the customer, and IAS 18 for the sale of services refers to the stage of completion. So IAS 11 and IAS 18 for services focuses on the amount of work (or service) undertaken by an entity and then smoothes the recognition of profit over the work done (or service) plus or minus any generous or ungenerous provision for contingencies! Whilst IAS 18 for the sale of goods focuses on the customer taking control and receiving the economic benefits of receiving control of an asset. Do the different principles make a real difference?

Put simply – YES because the differences result in reporting different (and sometimes hugely different) revenue and profit numbers. IFRIC 15 bridging the gap

IFRIC 15 ‘Agreements for the Construction of Real Estate’ changed things. The IFRIC intended to address diversity in practice in the real estate industry however the IFRIC can also be applied by analogy to other industries.

The IFRIC set out to put contracts clearly into either IAS 11 or IAS 18 by focusing on which of the contracting parties has the ability to control what happens to the asset. The result in the Real Estate sector was that entities engaged in delivering a standard property to a customer stopped using IAS 11 and started using IAS 18. Why? Because IFRIC 15 follows a continuous control concept. Paragraph 17 states “The entity may transfer to the buyer control and the significant risks and rewards of ownership of the work in progress in its current state as construction progresses. In this case if all the criteria (for the sale of goods in IAS 18.14) are met continuously as construction progresses….revenue shall be recognised according to the stage of completion.) In practice it appears it has been too difficult to identify when this continuous control concept should apply and the IFRIC appears to have achieved its objective of putting contracts into IAS 11 or IAS 18. So will a new Revenue standard deal with the problem?

Well certainly the answer the IASB and the FASB are looking for is YES! What are the key features of the new standard

We expect to see it in its final form in Q4 this year. Its core principle is to ‘recognise revenue to depict the transfer of goods or services in an amount that reflects the consideration expected to be received in exchange for those goods or services.’ The IASB has developed 5 steps to apply the principle;

1. Indentify the contract(s) with the customer 2. Indentify the separate performance obligations 3. Determine the transaction price 4. Allocate the transaction price 5. Recognise revenue when a performance obligation is satisfied. In practice, for simple revenue transactions there will be no change. Where there are multiple contracts and multiple performance obligations, there may be little change or there may be quite a big change. What do I need to do?

Entities will need to review their revenue recognition policies as soon as the standard is issued in Q4 2011. More information may be accessed on the IASB’s website here

Compendium of IFRS Publications is issued by ADAA. All rights reserved.

June 2011

15 of 34

Abu Dhabi Accountability Authority monthly digest

ADAA Highlights IFRS news, IPSAS and updates from the IASB, IFAC and the Accounting Profession

ADAA’s hot topics IFRS 10 IFRS 11 IFRS 12 IFRS 13 ADAA’s Muhammad Shabbir explains

What’s new this month? Four new standards!

Four new standards effective for annual periods beginning on or after 1 January 2013. Earlier application is permitted as long as IFRS 10, 11, 12, IAS 27 (2011) and IAS 28 (2011) are adopted at the same time. Although IFRS 12 may be adopted early by itself.

IFRS 10 Consolidated Financial Statements introduces a single model for assessment of control.

IFRS 11 Joint Arrangements. Joint control does not exist unless contractually agreed.

IFRS 12 Disclosure of Interests in Other Entities combines the disclosures in IAS 27, 28, 31 and adds new disclosures on top.

IFRS 13 Fair Value Measurement. A unified definition and measurement is published for fair value.

IFRS 10 - Consolidated Financial Statements IFRS 11 - Joint Arrangements

Why another standard on consolidation? IFRS 10 deals with divergent control models in IAS 27 and SIC 12. IAS 27 defines control as the “power to govern.” SIC-12 places greater emphasis on risks and rewards.

So what will happen to IAS 27 and SIC 12? SIC 12 is replaced entirely as the issues raised by it are addressed in IFRS 10. What remains in IAS 27 is the accounting for subsidiaries, jointly controlled entities, and associates in separate financial statements.

Concurrent with issuing IFRS 10, the IASB also issued IAS 27 (revised 2011) and IAS 28 (revised 2011).

What you need to know about IFRS 10. Consolidation is based on “control.” The control model applies to all entities including ‘special purpose entities.’ Control has three elements:

Power over an investee

Exposure or rights to variable returns of the investee and

Ability to use power over the investee to affect the investor’s return.

IFRS 10 contains detailed guidance on applying the control principle.

Power can exist over a portion of an investee (silos) which can become a “deemed entity” and consolidated.

Control is reassessed if there is a change in facts and circumstances.

The standard introduces new terminology in its control model, like the term “investor” to refer to a reporting entity that potentially controls another entity and “investee” to refer to an entity that is, or may be a subsidiary of a reporting entity.

Will IFRS 10 replace IFRS 3 also? No. IFRS 10 only changes who or what to consolidate not how.

A final thought. IFRS 10 is deliberately written to bring entities that are structured to be off balance sheet onto the balance sheet and it applies retrospectively.

Further reading Access Deloitte’s detailed commentary on IFRS 10 here.

IFRS 11 replaces IAS 31 Interests in Joint Ventures and SIC-13 Jointly controlled Entities — Non-monetary Contributions. It addresses two aspects of IAS 31:

1) That the structure of the arrangement was the only determinant of the accounting and,

2) That an entity had a choice of accounting treatment.

IFRS 11 improves on IAS 31 by establishing principles that are applicable to the accounting for all joint arrangements.

Key requirements and changes Defines joint control as “the contractually agreed sharing of control of an arrangement, which exists only when decisions about the relevant activities require the unanimous consent of the parties sharing control”.

Where there is joint control, IFRS 11 address only two forms of joint arrangements (joint operations and joint ventures). Whereas IAS 31 identified three forms of joint ventures (i.e., jointly controlled operations, jointly controlled assets and jointly controlled entities).

A Joint operation exists when parties have joint control over assets and liabilities.

A Joint venture exists when parties have joint control of the arrangement that has the rights to assets and liabilities.

The determination whether a joint arrangement is a joint operation or a joint venture is based on the parties’ rights and obligations under the arrangement. The existence of a separate vehicle is a necessary, but not sufficient condition for a joint arrangement to be considered a joint venture.

Accounting for joint arrangements Proportional consolidation has gone. Not many entities used it and it doesn’t make accounting sense to keep it.

Joint ventures are equity accounted under IAS 28 (revised 2011)

Joint arrangements are accounted by recognizing the share of the assets, liabilities, revenues and expenses.

Another key consideration Due to the differences in the way joint arrangements are assessed and now proportionate consolidation has gone, entities may need to restate their financial statements. Detailed transitional guidance is available in IFRS 11.

Further reading Access Deloitte’s detailed commentary on IFRS 11 here.

Compendium of IFRS Publications is issued by ADAA. All rights reserved.

June 2011

16 of 34

Abu Dhabi Accountability Authority monthly digest

ADAA Highlights IFRS news, IPSAS and updates from the IASB, IFAC and the Accounting Profession

IFRS 12 - Disclosure of Interests in Other Entities IFRS 13 - Fair Value Measurement

IFRS 12 is a disclosure standard. It applies to entities that have an interest in subsidiaries, joint arrangements, associates or unconsolidated structured entities. All of the disclosure requirements of the existing IAS 27, 28 and 31 have been removed from those standards and are included in IFRS 12.

There are substantial disclosure requirements in the new standard including a number of new ones. One of the most significant is that an entity is now required to disclose the judgments made to determine when it does not control another entity.

The new disclosures will assist readers of the financial statements to make their own assessment of the financial impact were management to reach a different conclusion regarding consolidation of an entity — by providing more information about the unconsolidated entities.

The standard requires an entity to disclose information that helps users of its financial statements evaluate the nature of and risks associated with its interest in other entities and the effects of those interests on its financial statements.

Further reading. Access E&Y’s publication on implications of IFRS 12 on real estate and construction industry here.

IFRS 13 aims to improve consistency and reduce complexity by providing, for the first time, a precise definition of fair value and a single source of fair value measurement and disclosure requirements for use across IFRSs. Accordingly all fair value measurement guidance will be removed from all other standards!

Scope. The standard applies to all transactions and balances for which IFRSs require or permit fair value measurement (whether financial or non-financial), with the exception of share based transactions accounted for under IFRS 2 and leasing transactions within the scope of IAS 17.

Definition of fair value The price obtained to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

Summary of key guidance for fair value measurement; Asset or liability: Fair value considers the characteristics of the asset or liability if market participants would take those characteristics into account when pricing the asset or liability at the measurement date. Characteristics may include condition, location and restrictions on the sale and use of asset.

The transaction: Fair value assumes that the transaction will take place between market participants in the principal market or in the most advantageous market (in the absence of principal market) to sell the asset or transfer the liability.

Market participants: Fair value measurement assumes that the market participants act in their economic best interest.

Non-financial asset: For non-financial assets fair value measurement assumes highest and best use of the asset by market participants.

Liabilities and entity’s own equity instruments: Fair value is determined assuming that the instrument would be transferred on the measurement date, but would remain outstanding (i.e., it is a transfer value, not an extinguishment or settlement cost).

Non-performance risk: The fair value measurement of a liability must take account of non-performance risk, including entity’s own credit risk.

Valuation techniques: Use must be appropriate in the circumstances and sufficient data available to measure fair value, maximizing the use of relevant observable inputs and minimizing the use of unobservable inputs.

Further reading. Access E&Y’s detailed commentary on IFRS 13 here.

August 2011

Compendium of IFRS Publications is issued by ADAA. All rights reserved.

17 of 34

Abu Dhabi Accountability Authority monthly IFRS digest

ADAA Highlights IFRS news and updates from the IASB, IFAC and the Accounting Profession

ADAA’s hot topics The IASB is located in Cannon Street in London Please turn the page for ADAA’s monthly accounting insight

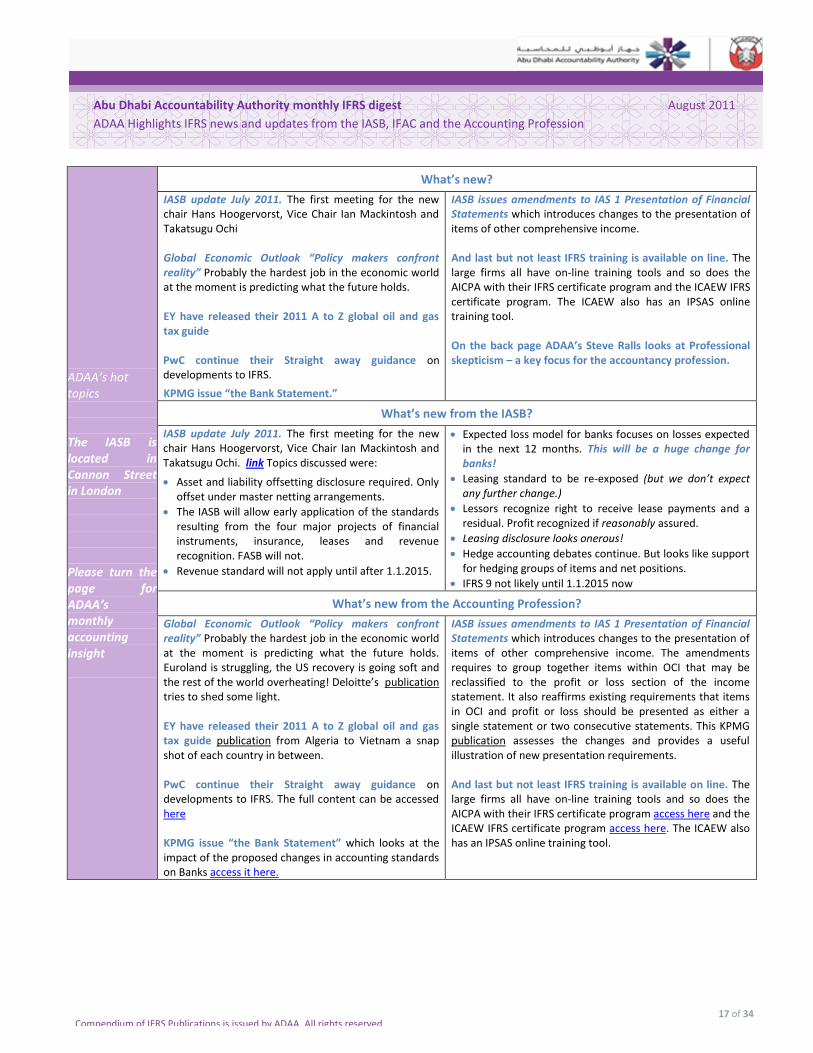

What’s new?

IASB update July 2011. The first meeting for the new chair Hans Hoogervorst, Vice Chair Ian Mackintosh and Takatsugu Ochi Global Economic Outlook “Policy makers confront reality” Probably the hardest job in the economic world at the moment is predicting what the future holds. EY have released their 2011 A to Z global oil and gas tax guide PwC continue their Straight away guidance on developments to IFRS.

KPMG issue “the Bank Statement.”

IASB issues amendments to IAS 1 Presentation of Financial Statements which introduces changes to the presentation of items of other comprehensive income. And last but not least IFRS training is available on line. The large firms all have on-line training tools and so does the AICPA with their IFRS certificate program and the ICAEW IFRS certificate program. The ICAEW also has an IPSAS online training tool. On the back page ADAA’s Steve Ralls looks at Professional skepticism – a key focus for the accountancy profession.

What’s new from the IASB?

IASB update July 2011. The first meeting for the new chair Hans Hoogervorst, Vice Chair Ian Mackintosh and Takatsugu Ochi. link Topics discussed were:

Asset and liability offsetting disclosure required. Only offset under master netting arrangements.

The IASB will allow early application of the standards resulting from the four major projects of financial instruments, insurance, leases and revenue recognition. FASB will not.

Revenue standard will not apply until after 1.1.2015.

Expected loss model for banks focuses on losses expected in the next 12 months. This will be a huge change for banks!

Leasing standard to be re-exposed (but we don’t expect any further change.)

Lessors recognize right to receive lease payments and a residual. Profit recognized if reasonably assured.

Leasing disclosure looks onerous!

Hedge accounting debates continue. But looks like support for hedging groups of items and net positions.

IFRS 9 not likely until 1.1.2015 now

What’s new from the Accounting Profession?

Global Economic Outlook “Policy makers confront reality” Probably the hardest job in the economic world at the moment is predicting what the future holds. Euroland is struggling, the US recovery is going soft and the rest of the world overheating! Deloitte’s publication tries to shed some light. EY have released their 2011 A to Z global oil and gas tax guide publication from Algeria to Vietnam a snap shot of each country in between. PwC continue their Straight away guidance on developments to IFRS. The full content can be accessed here KPMG issue “the Bank Statement” which looks at the impact of the proposed changes in accounting standards on Banks access it here.

IASB issues amendments to IAS 1 Presentation of Financial Statements which introduces changes to the presentation of items of other comprehensive income. The amendments requires to group together items within OCI that may be reclassified to the profit or loss section of the income statement. It also reaffirms existing requirements that items in OCI and profit or loss should be presented as either a single statement or two consecutive statements. This KPMG publication assesses the changes and provides a useful illustration of new presentation requirements. And last but not least IFRS training is available on line. The large firms all have on-line training tools and so does the AICPA with their IFRS certificate program access here and the ICAEW IFRS certificate program access here. The ICAEW also has an IPSAS online training tool.

August 2011

Compendium of IFRS Publications is issued by ADAA. All rights reserved.

18 of 34

Abu Dhabi Accountability Authority monthly IFRS digest

ADAA Highlights IFRS news and updates from the IASB, IFAC and the Accounting Profession

ADAAs Steve Ralls explains

Professional skepticism is a key focus for the Accountancy Profession - Steve Ralls

The Audit Inspection Unit (AIU) of the UK’s Professional Oversight Board published its 2011 report in July. The key issues and concerns it identifies are; Professional skepticism, Audit quality, Auditor Independence, Group audits, reporting to Audit Committee and audit of disclosures. link

The Chairman of the Public Company Accounting Oversight Board (PCAOB) in a speech to the SEC and Financial Reporting Institute 30

th Annual Conference,

June 2011 said; “auditors must approach their jobs with independence and skepticism.” link

The Institute of Chartered Accountants in England and Wales (ICAEW) in their May 2011 publication on the clarified ISA’s say: “The need for professional skepticism under clarified ISAs is more important than ever. ISA 200.13 defines professional skepticism as an attitude that includes a questioning mind, being alert to conditions which may indicate possible misstatement due to error or fraud, and a critical assessment of audit evidence. ” link

Section 290.6 of the International Federation of Accountants (IFAC) April 2010 handbook of the Code of Ethics for Professional Accountants states; “Independence of Mind. The state of mind that permits the expression of a conclusion without being affected by influences that compromise professional judgment, thereby allowing an individual to act with integrity and exercise objectivity and professional skepticism.” link

Why are the AIU, PCAOB, ICAEW and IFAC focusing on professional skepticism? Is not professional skepticism a key tool for all accountants, be they in audit, or industry? All fully paid up members of the professional bodies are signed up to IFAC and its code of ethics. At the heart of the code it states; “A distinguishing mark of the accountancy profession is its acceptance of the responsibility to act in the public interest. Therefore a professional accountant’s responsibility is not exclusively to satisfy the needs of an individual client or employer.”

The IFAC code emphasizes integrity, objectivity professional confidence and due care. So clearly there is an emphasis on all professional accountants to apply professional skepticism at all times.

However it is difficult to maintain skepticism when market information is telling you something else.

If something seems too good to be true then it usually is! History highlights the need for skepticism. For example the tulip craze and the 2008 financial crisis, the South Sea bubble and Madoff, arguably all had the same root cause – a lack of skepticism.

In the year 1634 in Amsterdam tulip bulbs were traded as a means of exchange and a store of value. Black bulbs being highest in value. The craze lasted 4 years before the market burst and the price of bulbs fell in days to a fraction of their previous worth.

In October 2008 many of the world’s largest financial institutions nearly collapsed, needed financial support or went under as a result of risks arising in the USA from home loans, mortgages and imaginative lending standards which had been passed to the world market’s through credit default instruments.

In 1720 shares in the South Sea Company chartered a boom and bust path, created by market misinformation and some rather unscrupulous practices of the UK aristocracy.

In December 2008 the Madoff investment scandal broke when former NASDAQ chairman Bernie Madoff admitted his wealth management business was an elaborate Ponzi scheme. It took in new capital to fund above market returns to investors.

There does seem to be a difference between the tulip scandal and the 2008 financial crisis, and the South Sea bubble and Madoff. In the tulip scandal and the 2008 financial crisis investors lost sight of the risks. In the South Sea bubble and Madoff investors were bewitched by the impossible (as it turned out) returns.

Professional skepticism is making a welcome return. This can be seen in the focus of the IASB’s projects. Bringing prudence back into accounting by moving to an expected loss model for financial instruments, bringing leases onto the balance sheet and challenging the valuation and impairment models and disclosures with the new standard IFRS 13, which greatly emphasizes the use of market observable inputs. (A discounted cash flow is just accountants playing with the numbers).

It can also be seen in the AIU “…findings continue to identify the need for firms to ensure that both partners and staff exercise appropriate professional skepticism, particularly in respect of key areas of audit judgment such as the valuation of assets and the impairment of goodwill and other intangibles.”

Compendium of IFRS Publications is issued by ADAA. All rights reserved.

September 2011

19 of 34

Abu Dhabi Accountability Authority monthly IFRS digest

ADAA Highlights IFRS news and updates from the IASB, IFAC and the Accounting Profession

ADAA’s hot topics

What’s new?

IASB issues effect analysis of IFRS 11 Joint Arrangements. A “must read” for all entities dealing with IAS 31. Hedge accounting; Another step forward. Explaining the developments in hedge accounting. Stay informed; listen to what the standard setter has to say. Useful podcast summaries Including discussions on IFRS 11. IASB update, Exposure draft issued to delay the mandatory date for IFRS 9 and investors’ perspective on key changes to IAS 19 explained.

Current economic conditions — financial reporting considerations. What you need to know regarding the impact of the current economic crisis on financial reporting. Still some good news? Opportunities in adversity. Probabilities for global banking growth, including the emerging markets of the world. Management Commentary boosts transparency and enhances corporate governance - On the back page ADAA’s Nader Chatila looks at the role of management commentary in achieving transparency and enhancing corporate governance.

The IASB is located in Cannon Street in London

What’s new from the IASB?

IASB issues effect analysis of IFRS 11 Joint Arrangements; analyze the expected effect on your financial statements.

With proportionate consolidation gone and significant changes to the definition of joint control, IFRS 11 Joint Arrangements is expected to have a significant impact on how these arrangements are accounted for. For this reason IASB has published an effect analysis of IFRS 11. Besides discussing JV activity overview and other details, the analysis provides useful info on the financial statements effect of IFRS 11.

The standard becomes mandatory for annual periods beginning on or after 1 January 2013. Get hold of this important analysis here.

Stay informed; listen to what standard setter has to say. The recent podcast from the Interpretation Committee includes discussions on IFRS 11 and the Board podcast covers critical topics of lease, revenue and hedge accounting and can be accessed here. IASB update. IFRS 9 delayed; proposed effective date postponed to 1 January 2015. To read and comment on the exposure draft, access the project page here and PWC’s discussion paper here.

Addressing the investors’ perspective, IASB published an article on key changes relating to presentation of net pension liabilities or assets and net pension cost. Access it here and PWC’s practical guide here.

Please turn the page for ADAA’s monthly accounting insight

What’s new from the Accounting Profession?

Hedge accounting; Another step forward The Board has tentatively decided that:

A cash flow hedge of a net position can be an eligible hedged item even if the individual forecast transactions within the net position affect profit or loss in different periods.

The proposed accounting for forward points will allow financial institutions to better reflect the economic yield achieved in funding swap transactions.

An aggregated exposure qualifies as a hedged item.

The fair value option is extended to ‘own use’ contracts. To access full publication from E&Y, click here.

Current economic conditions — financial reporting considerations. The recent downgrade by Standard & Poor’s (S&P) of the long-term credit rating of the US and current economic conditions raise a number of financial reporting considerations. Key highlights are;

Notwithstanding S&P’s downgrade, the US Treasury rates can continue to be used as the “risk-free interest rate”.

All movements in US treasury rates represent movements of the “benchmark interest rate.”

Companies should continue to monitor ongoing developments and consider their potential financial reporting effects. To access the full publication click here.

Still some good news? Opportunities in adversity KPMG’s report explains why some senior banking executives are still optimistic about global banking growth.

Compendium of IFRS Publications is issued by ADAA. All rights reserved.

September 2011

20 of 34

Abu Dhabi Accountability Authority monthly IFRS digest

ADAA Highlights IFRS news and updates from the IASB, IFAC and the Accounting Profession

ADAAs Nader Chatila explains

Management Commentary boosts transparency and enhances corporate governance - Nader Chatila

The global economic crisis and corporate collapses in the last few years had a severe impact on capital markets. Investors perhaps believe they were misguided by entities’ financial information and management commentaries that did not properly explain the risks. Improving communication between the corporate community and investors is key to restoring confidence in the capital markets.

In recent years, disclosure requirements regarding capital structure, liquidity and cash flows have become the focus of standard setters whom consider that a good management commentary can complement the financial statements by providing; an explanation of the amounts presented in the financial statements, an understanding of management’s strategy, objectives and actions and a commentary on future performance.

The SEC has proposed extensive new Management Discussion & Analysis (MD&A) requirements for the disclosure of short term borrowings throughout reporting periods to reduce the potential for window dressing of liquidity positions.

In Australia an association of senior finance executives has produced the G100 guidance to assist the preparation of management commentary on an entity’s operations and financial condition (G 100 Guidance).

In December 2010 the International Accounting Standards Board (IASB) acknowledged inconsistencies in international reporting and released a Practice Statement on Management Commentary. This non-binding publication provides practical guidance on how entities can enhance their Management Commentary. (IASB Practice Statement)

The practice statement considers the following areas for management commentary to consider:

1. The nature of the business;

2. Management’s objectives and strategies for meeting those objectives;

3. The entity’s most significant resources, risks and relationships;

4. The results of operations and prospects; and

5. The critical performance measures and indicators that management uses to evaluate the entity’s performance against stated objectives.

We enclose an example of (Rio Tinto Management Commentary 2010)

1. Nature of the business: This covers a discussion of the entity’s main markets, its competitive position within those markets and the significant features of the legal, regulatory and macro-economic

1. environment that influences the entity and the markets in which the entity operates.

2. Objectives and strategies. Here management disclose their objectives and strategies in a way that enables users of the financial statements to understand the priorities for action as well as to identify the resources that must be managed to deliver results in a manner that provides users with insight that may shape their expectations about the entity’s future performance.