completing test on sales and collection cycles: account receivable

DESCRIPTION

completing test on sales and collection cycles: account receivableTRANSCRIPT

16 - 1©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Completing the Tests in the Sales and Collection Cycle:

Accounts Receivable

ATIKAH GALUH WILANDRA

1210534013

16 - 2©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

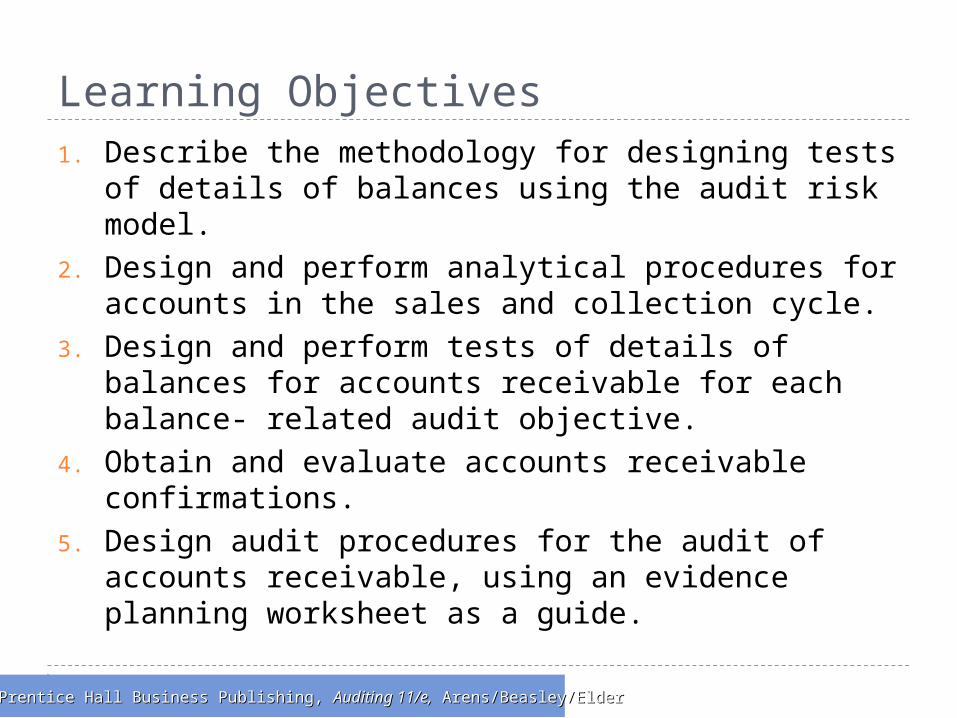

Learning Objectives 1. Describe the methodology for designing tests of

details of balances using the audit risk model.2. Design and perform analytical procedures for

accounts in the sales and collection cycle.3. Design and perform tests of details of balances

for accounts receivable for each balance- related audit objective.

4. Obtain and evaluate accounts receivable confirmations.

5. Design audit procedures for the audit of accounts receivable, using an evidence planning worksheet as a guide.

16 - 3©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

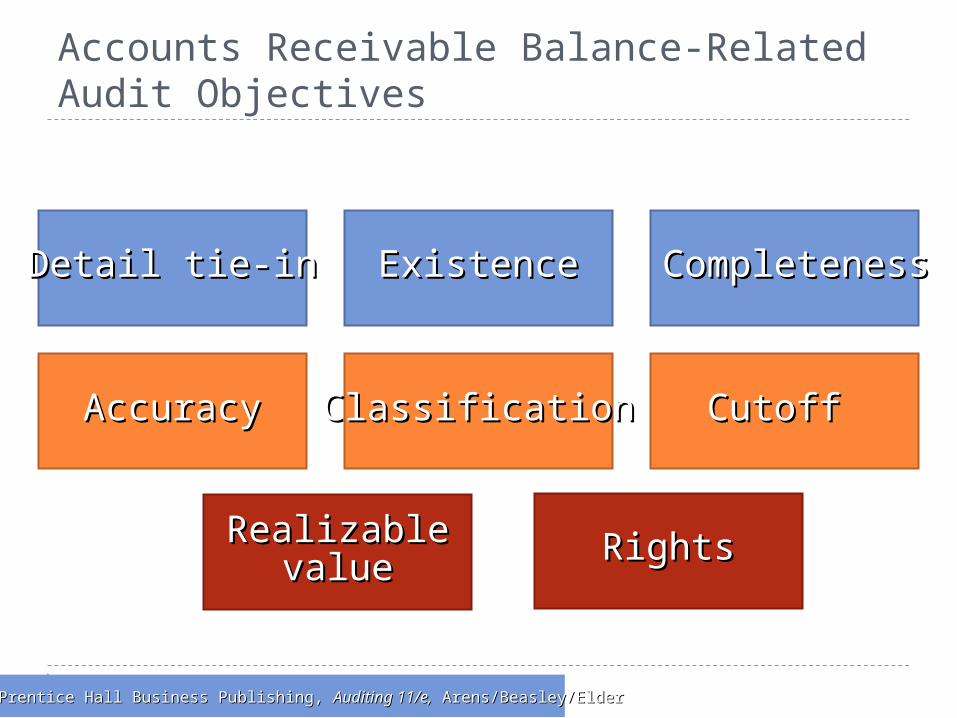

Accounts Receivable Balance-Related Audit Objectives

Detail tie-inDetail tie-in

RealizableRealizablevaluevalue

ClassificationClassificationAccuracyAccuracy

ExistenceExistence

RightsRights

CompletenessCompleteness

Cutoff Cutoff

16 - 4©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

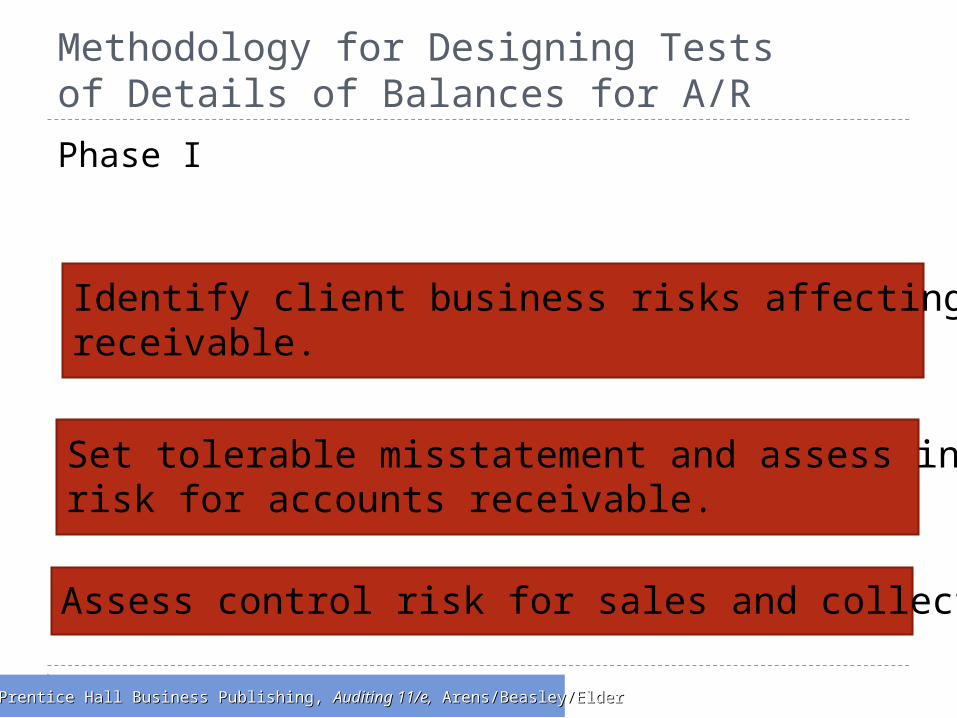

Methodology for Designing Testsof Details of Balances for A/R

Phase I

Set tolerable misstatement and assess inherentrisk for accounts receivable.

Assess control risk for sales and collection cycle.

Identify client business risks affecting accountsreceivable.

16 - 5©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Methodology for Designing Testsof Details of Balances for A/R

Phase II

Design and perform tests of controls andsubstantive tests of transactions for thesales and collection cycle.

16 - 6©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Methodology for Designing Testsof Details of Balances for A/R

Phase III

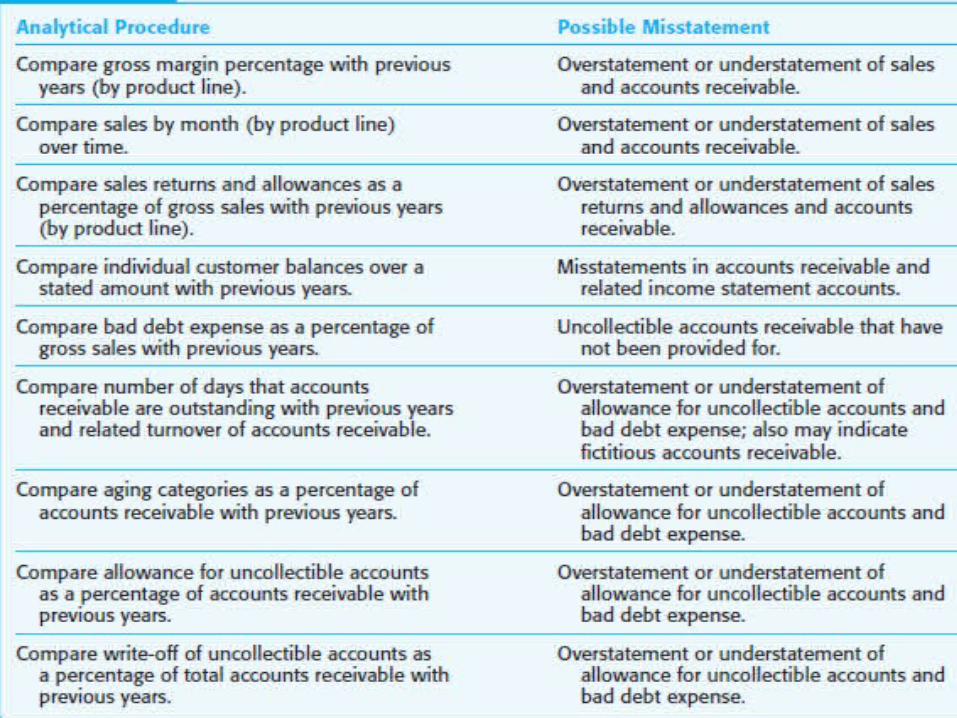

Design and perform analytical procedures foraccounts receivable balance.

16 - 7©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

16 - 8©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Methodology for Designing Testsof Details of Balances for A/R

.Design tests of details of accounts receivablebalance to satisfy balance-related audit objectives.

TimingTimingItems toItems toselectselect

SampleSamplesizesize

AuditAuditproceduresprocedures

16 - 9©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Designing Tests of Details of Balances Aged Trial BalanceAged Trial Balance Recorded Accounts Receivable ExistRecorded Accounts Receivable Exist Existing Accounts Receivable Are IncludedExisting Accounts Receivable Are Included Cutoff for Accounts Receivable Is CorrectCutoff for Accounts Receivable Is Correct Accounts Receivable Is Stated at Realizable Accounts Receivable Is Stated at Realizable

ValueValue The Client Has Rights to Accounts The Client Has Rights to Accounts

ReceivableReceivable

16 - 10©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

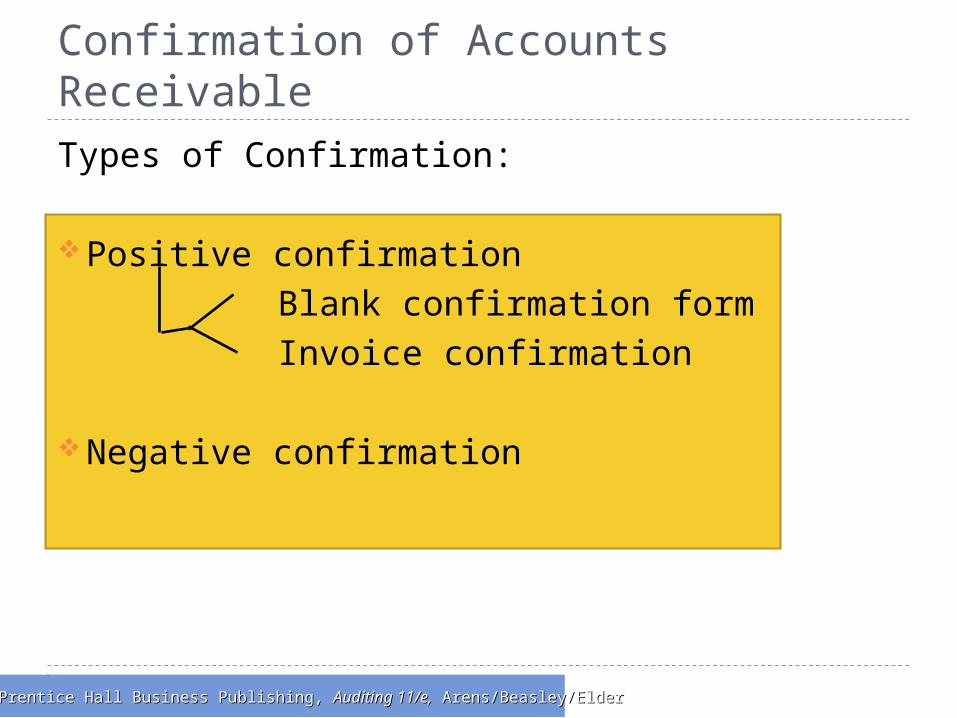

Confirmation of Accounts ReceivableTypes of Confirmation: Positive confirmation

Blank confirmation formInvoice confirmation

Negative confirmation

16 - 11©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

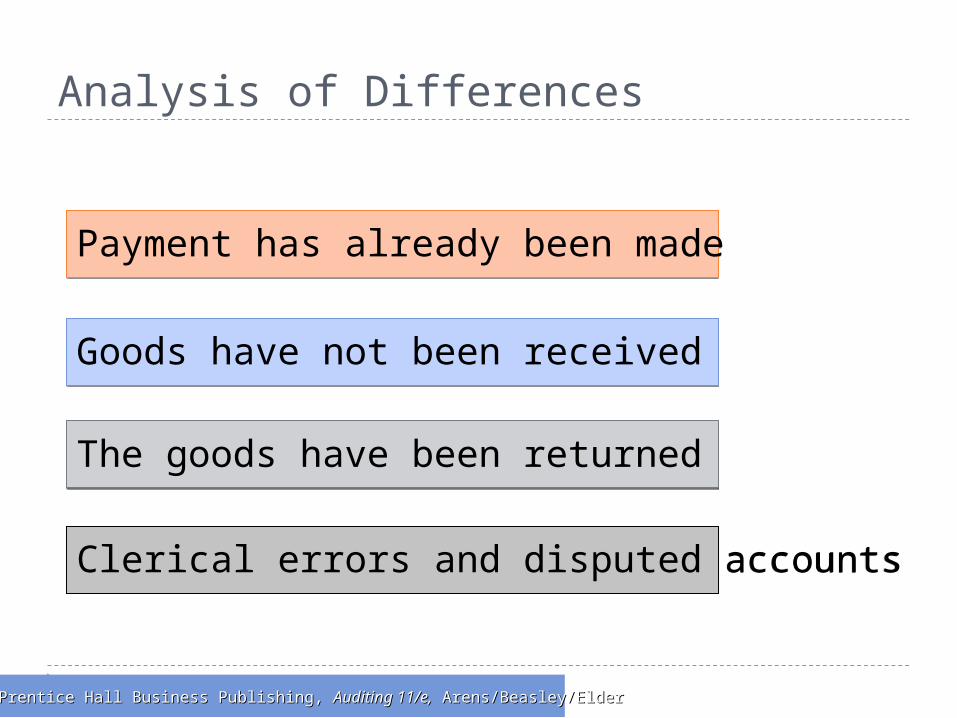

Analysis of Differences

Payment has already been madePayment has already been made

Goods have not been receivedGoods have not been received

The goods have been returnedThe goods have been returned

Clerical errors and disputed accountsClerical errors and disputed accounts

16 - 12©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Drawing Conclusions

Reevaluate internal control.

Evaluate the qualitative nature ofmisstatements.

Determine whether sufficient evidencewas obtained.

16 - 13©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Source of Each Row in the Evidence Planning Worksheet

Tolerable misstatementTolerable misstatement Acceptable audit riskAcceptable audit risk Inherent riskInherent risk Control riskControl risk Substantive tests of transactions resultsSubstantive tests of transactions results Analytical proceduresAnalytical procedures Planned detection risk and planned audit Planned detection risk and planned audit evidenceevidence

16 - 14©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder