comprehensive annual financial report … annual report consists of a series of financial...

TRANSCRIPT

COMPREHENSIVE ANNUAL FINANCIAL REPORT

OF THE

TOWN OF LANTANA, FLORIDA

FOR THE FISCAL YEAR ENDED

SEPTEMBER 30, 2009

PREPARED BY THE FINANCE AND ADMINISTRATIVE SERVICES DEPARTMENT

TOWN OF LANTANA, FLORIDA

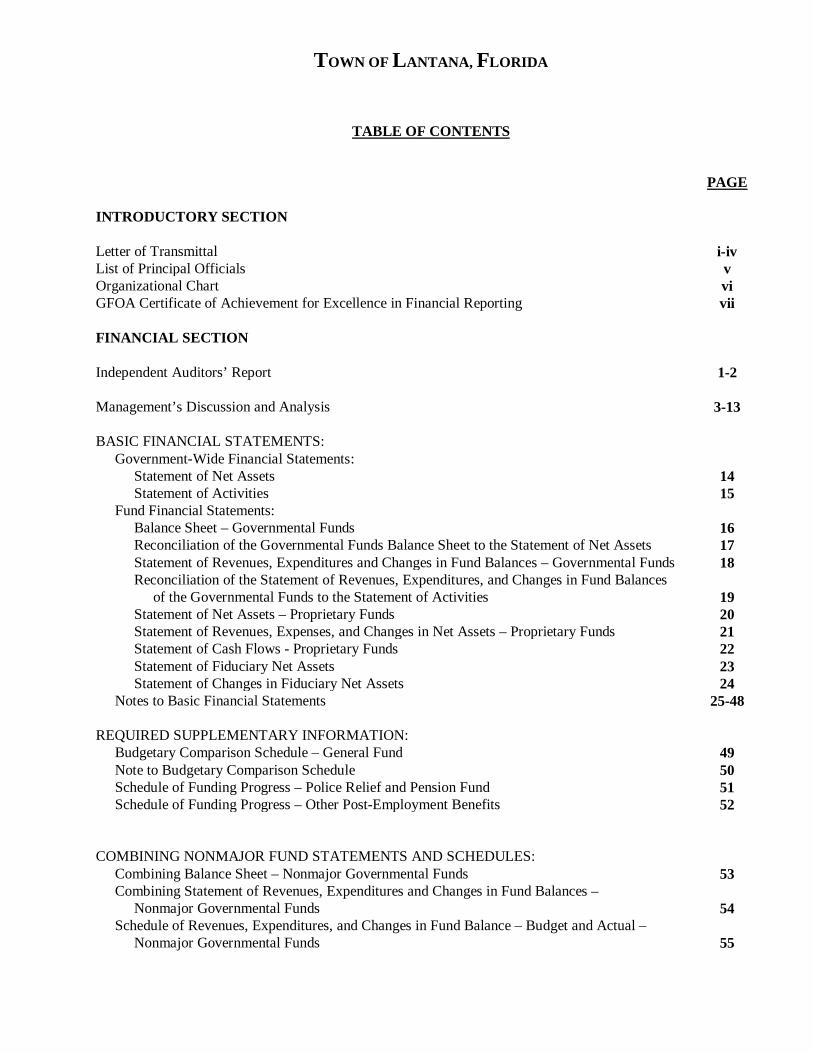

TABLE OF CONTENTS PAGE INTRODUCTORY SECTION Letter of Transmittal i-iv List of Principal Officials v Organizational Chart vi GFOA Certificate of Achievement for Excellence in Financial Reporting vii FINANCIAL SECTION Independent Auditors’ Report 1-2 Management’s Discussion and Analysis 3-13 BASIC FINANCIAL STATEMENTS: Government-Wide Financial Statements: Statement of Net Assets 14 Statement of Activities 15 Fund Financial Statements: Balance Sheet – Governmental Funds 16 Reconciliation of the Governmental Funds Balance Sheet to the Statement of Net Assets 17 Statement of Revenues, Expenditures and Changes in Fund Balances – Governmental Funds 18 Reconciliation of the Statement of Revenues, Expenditures, and Changes in Fund Balances of the Governmental Funds to the Statement of Activities

19

Statement of Net Assets – Proprietary Funds 20 Statement of Revenues, Expenses, and Changes in Net Assets – Proprietary Funds 21 Statement of Cash Flows - Proprietary Funds 22 Statement of Fiduciary Net Assets 23 Statement of Changes in Fiduciary Net Assets 24 Notes to Basic Financial Statements 25-48 REQUIRED SUPPLEMENTARY INFORMATION: Budgetary Comparison Schedule – General Fund 49 Note to Budgetary Comparison Schedule 50 Schedule of Funding Progress – Police Relief and Pension Fund 51 Schedule of Funding Progress – Other Post-Employment Benefits 52 COMBINING NONMAJOR FUND STATEMENTS AND SCHEDULES: Combining Balance Sheet – Nonmajor Governmental Funds 53 Combining Statement of Revenues, Expenditures and Changes in Fund Balances – Nonmajor Governmental Funds

54

Schedule of Revenues, Expenditures, and Changes in Fund Balance – Budget and Actual – Nonmajor Governmental Funds

55

TOWN OF LANTANA, FLORIDA

TABLE OF CONTENTS (Continued)

PAGE STATISTICAL SECTION Net Assets by Component – Last Seven Fiscal Years 56 Changes in Net Assets – Last Seven Fiscal Years 57-58 Fund Balances of Governmental Funds – Last Seven Fiscal Years 59 Changes in Fund Balances of Governmental Funds – Last Seven Fiscal Years 60 Net Assessed Value and Estimated Actual Value of Taxable Property – Last Ten Fiscal Years 61 Property Tax Rates – Direct and Overlapping Governments – Last Ten Fiscal Years 62 Principal Property Taxpayers – Current Year and Nine Years Ago 63 Property Tax Levies and Collections – Last Ten Fiscal Years 64 Ratios of Outstanding Debt by Type – Last Ten Fiscal Years 65 Direct and Overlapping Governmental Activities Debt 66 Sports Complex Bonds Pledged Revenue Coverage – Last Ten Fiscal Years 67 Streets and Highways Note Pledged Revenue Coverage – Last Ten Fiscal Years 68 1998 Water and Sewer Bonds Pledged Revenue Coverage – Last Ten Fiscal Years 69 Demographic and Economic Statistics – Last Ten Fiscal Years 70 Principal Employers – Palm Beach County – Current Year and Nine Years Ago 71 Principal Employers – Town of Lantana 71 Full-Time Equivalent Town Government Employees by Function 72 Operating Indicators by Function/Program 73 Capital Asset Statistics by Function/Program 74 Miscellaneous Statistics 75-76 Schedule of Insurance in Force 77 COMPLIANCE SECTION Independent Auditors’ Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards

78-79 Management Letter in Accordance with the Rules of the Auditor General of the State of Florida 80-82

INTRODUCTORY SECTION

v

TOWN OF LANTANA, FLORIDA

LIST OF PRINCIPAL OFFICIALS

SEPTEMBER 30, 2009

TITLE NAME Mayor David J. Stewart Vice Mayor Thomas Deringer Vice Mayor Pro Tem Cindy Austino Council Member ElizabethTennyson Council Member Dr. Lynn Moorhouse Town Manager Michael Bornstein Town Attorney R. Max Lohman Town Engineers Mathews Consulting, Inc. Keith & Shnars, P.A. Kimley-Horn & Assoc., Inc.

Engenuity Group Inc. Town Auditors MarcumRachlin, a division of

Marcum LLP Utilities Director Jerry Darr Town Clerk Crystal Gibson Operations Director Michael Greenstein Finance and Administrative Services Director Stephen Kaplan Police Chief Richard Lincoln Library Director Sid Patchett Development Services Director David Thatcher

vi

TOWN OF LANTANA ORGANIZATIONAL CHART

vii

FINANCIAL SECTION

-3-

MANAGEMENT’S DISCUSSION AND ANALYSIS The purpose of financial reporting, in general, is to provide the readers of the financial statements with information that will help them make decisions and draw conclusions about an entity. As management of the Town of Lantana (Town), Florida, we offer readers of the Town’s financial statements this narrative overview and analysis of the financial activities of the Town for the fiscal year ended September 30, 2009. We encourage readers to consider the information presented here in conjunction with information that we have furnished in our accompanying transmittal letter beginning on Page i, and the accompanying basic financial statements.

FINANCIAL HIGHLIGHTS • The Town’s net assets at September 30, 2009 were $17.47 million, excluding the amount

invested in capital assets. Of this amount, $17.4 million (unrestricted net assets) may be used to meet the Town’s ongoing obligations to citizens and creditors.

• Governmental activities net assets were $28.2 million, of which, $10.8 million were unrestricted.

• The total revenues from all sources were $14.16 million.

• The total costs of all Town programs were $14.2 million.

• During the year, the Town’s governmental activity expenses exceeded revenues by $393,156.

• Total expenditures and other financing uses in the General Fund exceeded revenues and other financing sources by $1,278,461.

• At the end of the current fiscal year, unreserved and undesignated fund balance for the General Fund was $8.9 million, or 91% of total General Fund expenditures. However, of this balance, $3.3 was accumulated due to the sale of Town property from prior years, of which, $1,737,300 remains available after the construction of the seawall explained in further detail on page 10. Council has recommended that this amount remain as unreserved and undesignated fund balance, and it is not to be used to finance the Town’s operations in future years.

OVERVIEW OF THE FINANCIAL STATEMENTS This annual report consists of a series of financial statements. The three components of the basic financial statements are: (1) Government-wide financial statements, which include the Statement of Net Assets and the Statement of Activities. These statements provide information about the activities of the Town as a whole. (2) Fund financial statements illustrate how these services were financed in the short term, as well as what remains for future spending. Fund financial statements also report the Town’s operations in more detail

-4-

than the government-wide statements by providing information about the Town’s most significant funds. (3) Notes to the financial statements. Other information such as budgetary comparisons, statements of the non-major governmental funds, and the statistical section contains data such as financial trends, debt capacity, and demographic, economic and operating information to assist the reader in better understanding the operations of the Town. This report also contains other supplementary information in addition to the basic financial statements. The financial statement focus is on both the Town as a whole (government-wide) and on the major individual funds. The following graph shows the relationship between the CAFR and the basic financial statements and Required Supplementary Information (“RSI”).

General Information on the government structure, services and environment

Introductory Section

Management's Discussion and Analysis

Government-wide Financial Statements

Governmental Fund Financial StatementsCAFR

Proprietary Fund Financial Statements FinancialSection

Fiduciary Fund Financial Statements

Notes to the Financial Statements

Additional Required Supplementary Information

Information on non-major individual funds, budgetary comparisons and other supplementary information

Trend data and non-financial dataStatistical Section

Supplementary Information (RSI)

Basic Financial statements and RSI

Relationship Between Comprehensive AnnualFinancial Report (CAFR)

AndBasic Financial Statements and Required

-5-

GOVERNMENT-WIDE FINANCIAL STATEMENTS A frequently asked question regarding the Town’s financial health is whether the year’s activities contributed positively to the overall financial well-being. The Statement of Net Assets and the Statement of Activities report information about the Town as a whole and about its activities in a way that helps answer this question. These statements include all assets and liabilities using the accrual basis of accounting, which is similar to the accounting used by most private-sector companies. All of the current year’s revenues and expenses are taken into account, regardless of when cash is received or paid. These two statements report the Town’s net assets and changes therein. Net assets, the difference between assets and liabilities, are one way to measure the Town’s financial health, or financial position. Over time, increases or decreases in net assets are an indicator of whether the financial health is improving or deteriorating. The Statement of Net Assets and the Statement of Activities present information about the following: • Governmental activities – All of the Town’s basic services are considered to be governmental activities, including general government, community development, public safety, public services, library, and recreation. Property taxes, sales taxes, utility taxes, and franchise fees finance most of these activities. • Proprietary activities/Business-type activities – The Town charges a fee to customers to cover all or most of the cost of the services provided.

FUND FINANCIAL STATEMENTS The fund financial statements provide detailed information about the most significant funds – not the Town as a whole. Some funds are required to be established by State law. However, management establishes other funds, which aid in the management of money for particular purposes or meet legal responsibilities associated with the use of certain taxes, grants, and other monies. The Town’s three kinds of funds, governmental, proprietary, and fiduciary use different accounting approaches as explained below: • Governmental funds – Most of the Town’s basic services are reported in governmental funds. Governmental funds focus on how resources flow in and out, with the balances remaining at year-end that are available for spending. These funds are reported using an accounting method called the modified accrual accounting method, which measures cash and all other financial assets that can readily be converted to cash. The governmental fund statements provide a detailed short-term view of the Town’s general governmental operations and the basic services it provides. Governmental fund information shows whether there are more or less financial resources that can be spent in the near future to finance the Town’s programs. The basic governmental fund financial statements can be found on pages 16-19 of this report.

-6-

• Proprietary funds – These fund financial statements consist of a Statement of Net Assets, Statement of Revenues, Expenses, and Changes in Net Assets and Statement of Cash Flows. These statements are prepared on an accounting basis that is similar to the basis used to prepare the government-wide financial statements.

The Town uses Enterprise Funds to account for business-type activities that charge fees to customers for the use of specific goods or services. These funds are used to report the same functions presented as business-type activities in the government-wide financial statements. Internal Service Funds are used to account for services provided and billed on an internal basis. The Town uses Internal Service Funds to account for its workers compensation and general liability expenses. The basic proprietary fund financial statements can be found on pages 20-22 of this report.

• Fiduciary funds – Fiduciary funds are used to account for resources held for the benefit of parties outside the government. Fiduciary funds are not reflected in the government-wide financial statement because the resources of those funds are not available to support the Town’s own programs. The accounting used for fiduciary funds is much like that used for proprietary funds. The basic fiduciary fund financial statements can be found on pages 23 and 24 of this report.

GOVERNMENT-WIDE FINANCIAL ANALYSIS

As noted earlier, net assets may serve over time as a useful indicator of a government’s financial position. In the case of the Town, assets exceeded liabilities by $37.9 million, which is approximately the same amount as the previous fiscal year. The largest portion of the Town’s net assets (53.8%) reflects its investment in capital assets (e.g., land, buildings, machinery, and equipment), less any related debt used to acquire those assets that are still outstanding. The Town uses these capital assets to provide services to citizens; consequently, these assets are not available for future spending. Although the Town’s investment in its capital assets is reported net of related debt, it should be noted that the resources needed to repay this debt must be provided from other sources since the capital assets themselves cannot be used to liquidate these liabilities.

2009 2008 2009 2008 2009 2008Assets: Current and other assets 12,261,750$ 13,360,947$ 7,676,765$ 7,318,293$ 19,938,515$ 20,679,240$ Capital assets 20,214,469 19,614,632 11,724,512 12,163,275 31,938,981 31,777,907 Total assets 32,476,219 32,975,579 19,401,277 19,481,568 51,877,496 52,457,147 Liabilities: Long term debt outstanding 3,528,166 3,758,778 8,788,545 9,356,124 12,316,711 13,114,902 Other liabilities 705,800 581,392 975,851 814,235 1,681,651 1,395,627 Total liabilities 4,233,966 4,340,170 9,764,396 10,170,359 13,998,362 14,510,529 Net Assets: Invested in capital assets, net of related debt 17,338,103 16,428,650 3,067,301 2,948,454 20,405,404 19,377,104 Restricted 80,105 186,222 - - 80,105 186,222 Unrestricted 10,824,045 12,020,537 6,569,580 6,362,755 17,393,625 18,383,292 Total net assets 28,242,253$ 28,635,409$ 9,636,881$ 9,311,209$ 37,879,134$ 37,946,618$

Activities Business-type

ActivitiesTotal

Activities

Town of LantanaNet Assets

Governmental

-7-

A portion of the Town’s unrestricted net assets ($1.7 million) represents resources that are requested by the Town Council to be set aside as this amount was acquired due to the sale of Town owned property in prior years. The remaining balance of unrestricted net assets ($15.7 million) may be used to meet the government’s ongoing obligations to citizens and creditors. The decrease in the government’s net assets for the fiscal year ended September 30, 2009 was $67,484 compared to an increase of $366,828 for the previous fiscal year. Business-type activities accounted for a $325,672 increase, while the governmental activities accounted for a $393,156 decrease. Details of these changes are explained later in the analysis. For both fiscal years presented, the Town was able to report positive balances in all three categories of net assets, as well as for its separate governmental and business-type activities.

GOVERNMENTAL ACTIVITIES Listed below is a schedule that illustrates the revenues, expenses, and changes in net assets.

2009 2008 2009 2008 2009 2008Revenues: Program revenues: Charges for services 2,304,471$ 2,426,559$ 4,834,025$ 4,599,751$ 7,138,496$ 7,026,310$ Operating grants and contributions 491,802 453,677 - - 491,802 453,677 Capital grants and contributions 38,872 18,034 145,735 - 184,607 18,034

General revenues: Property taxes 3,166,215 6,575,098 - - 3,166,215 6,575,098 Utility taxes 918,889 935,562 - - 918,889 935,562 Franchise fees based on gross receipts 772,731 804,092 - - 772,731 804,092 Communication services tax 409,214 493,392 - - 409,214 493,392 Sales and use tax 605,504 693,442 - - 605,504 693,442 State revenue sharing - unrestricted 289,023 323,426 - - 289,023 323,426 Investment income (loss) - unrestricted 73,451 393,206 (14,847) 109,918 58,604 503,124 Miscellaneous 125,749 98,366 - - 125,749 98,366 Gain from sale of capital assets - - - 27,375 - 27,375

Total revenues 9,195,921 13,214,854 4,964,913 4,737,044 14,160,834 17,951,898

Expenses: Program expenses: General government 802,674 675,795 - - 802,674 675,795 Physical environment 3,407,583 2,894,199 - - 3,407,583 2,894,199 Public safety 4,854,172 7,277,120 - - 4,854,172 7,277,120 Culture and recreation 406,927 1,799,145 - - 406,927 1,799,145 Interest on long-term debt 117,721 131,221 - - 117,721 131,221 Utility - Water & Sewer - - 4,639,241 4,807,590 4,639,241 4,807,590

Total expenses 9,589,077 12,777,480 4,639,241 4,807,590 14,228,318 17,585,070

Increase (decrease) in net assets (393,156) 437,374 325,672 (70,546) (67,484) 366,828

Net assets - October 1 28,635,409 28,198,035 9,311,209 9,381,755 37,946,618 37,579,790

Net assets - September 30 28,242,253$ 28,635,409$ 9,636,881$ 9,311,209$ 37,879,134$ 37,946,618$

Activities Activities Activities

Town of LantanaChanges in Net Assets

Governmental Business-type Total

-8-

The net assets of the Town’s governmental activities for the year ended September 30, 2009 decreased by $393,156 compared to an increase of $437,374 in the prior year. Significant variances from the prior year are as follows: • Property taxes decreased by $3.4 million during the year. However, in fiscal year 2009,

Palm Beach County began charging a separate tax rate relating to the Municipal Service Taxing Unit (MSTU) for Fire/Rescue services. In previous years, the property tax rate charged by the Town, included this rate and was then paid to the County for services rendered. As such, since the Town did not collect the revenue, there was no expense to pay which is the reason Public Safety recognized a significant decrease.

• Investment income decreased by $319,755 due to reduced rates of return on Town investments and the unrealized loss in the State-run Local Governmental Investment Pool.

• Due to a significant reduction of consumer spending, revenues such as State revenue sharing and sales and use tax were lower than the previous year.

• The Operations Department was created in fiscal year 2009 within the Physical

Environment category. Some of the divisions within Culture and Recreation were transferred under the Operations Department causing a reduction in Culture and Recreation and an increase in Physical Environment.

The Town’s programs include General Government, Physical Environment, Public Safety and Culture and Recreational services. General Government contains the following departments: Legislative, Executive, Finance, and Legal. Physical Environment contains Public Works and Utilities and Operations. Public Safety contains Police and Development Services. Culture and Recreation contains Library and Special Events. Each program’s net cost (total cost, less revenues generated by the activities) is presented below. The net cost demonstrates the extent to which the Town’s general taxes support each of the Town’s programs.

2009 2008 2009 2008 2009 2008

General government 802,674$ 675,795$ (511,352)$ (597,033)$ 291,322$ 78,762$ Physical environment 3,407,583 2,894,199 (1,161,466) (1,071,323) 2,246,117 1,822,876 Public safety 4,854,172 7,277,120 (975,802) (1,000,267) 3,878,370 6,276,853 Culture and recreation 406,927 1,799,145 (186,525) (229,647) 220,402 1,569,498 Interest on long-term debt 117,721 131,221 - - 117,721 131,221

Total 9,589,077$ 12,777,480$ (2,835,145)$ (2,898,270)$ 6,753,932$ 9,879,210$

of Servicesof Services

Town of LantanaGovernmental Activities

Total Cost of Services Net Cost of ServicesProgram Revenuesof Services

-9-

The cost of all governmental activities this year was $9.6 million. As shown on the Statement of Activities, those who directly benefited from the programs paid for $2.8 million of this cost, and $6.36 million was financed through general revenues.

Business-Type Activities Business-type activities increased the Town’s net assets by $325,672 for fiscal year 2009. Net assets of the proprietary fund at September 30, 2009, were $9.6 million. The cost of providing all proprietary (business-type) activities this year was $4.6 million compared to $4.8 million in the prior year. As shown in the Statement of Activities, amounts paid by users of service were $4.8 million in fiscal year 2009. A few factors contributed to the increase in net assets in 2009. First, revenue increased from the previous year due to a Council-approved 5% rate increase in June 2009 and a 3% increase in water consumption. While investment income recognized a decrease of $95,071, the increase in rates and consumption exceeded this decrease. Additionally, in fiscal year 2009, large capital projects began which are classified as capital assets, whereas, in the previous fiscal year, there were more projects focused on repairs and maintenance.

FINANCIAL ANALYSIS OF THE TOWN’S FUNDS As noted earlier, the Town uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements. Governmental Funds – The focus of the Town’s governmental funds is to provide information on near-term inflows, outflows, and balances of spendable resources. Such information is useful in assessing the Town’s financing requirements. In particular, unreserved fund balance may serve as a useful measure of a government’s net resources available for spending at the end of the fiscal year. As of the end of the current fiscal year, the Town’s governmental funds reported combined ending fund balances of $10.7 million, compared to $12 million in the prior fiscal year, a decrease of approximately $1.3 million. This decrease is due to a storm event that occurred within the first month of the fiscal year – October 2008. Most of the sand from the municipal beach was washed away due to strong water erosion. With three buildings on the dune about to fall into the Atlantic Ocean, the Town Council issued an emergency order and directed the Town Manager to construct a seawall. Working diligently with engineers, the Florida Department of Environmental Protection, Palm Beach County’s Department of Environmental Resources Management and the Florida Game and Fish Commission, staff coordinated the construction of a seawall spanning approximately 600 out of the 750 feet of beach at a cost of $1.56 million. Due to State requirements, the final phase to complete the full seawall could not be completed during this time. The funding for this project came from $3.3 million of the General Fund’s undesignated fund balance that Council had set aside many years ago from the sale of Town property.

-10-

Approximately 88% or $9.4 million of the combined ending fund balances (Governmental Funds) of $10.7 million constitutes unreserved and undesignated fund balance, which is available for spending at the government’s discretion. Of the $9.4 million, $503,011 is derived from the Special Revenue funds’ undesignated and unreserved fund balances. These funds will be used towards each fund’s intended purpose. Additionally, the Town Council has stated that the remaining $1.7 million of the original $3.3 million acquired from the sale of Town-owned property be earmarked for future programs to be decided on at a later time. The remainder of fund balance is reserved or designated to indicate that it is not available for new spending because it has already been committed. The General Fund is the chief operating fund for the Town. At the end of the current fiscal year, unreserved and undesignated fund balance in the General Fund was $8.9 million, while total fund balance was $9.6 million. As a measure of the General Fund’s liquidity, it may be useful to compare both unreserved fund balance and total fund balance to the total fund expenditures. Unreserved and undesignated fund balance represents 91% of total General Fund expenditures, while total fund balance represents 98% of that same amount.

General Fund Budgetary Highlights Differences between the original budget and the final amended budget were $2,981,819 and can be briefly summarized as follows: • Increase for the purchase of a communication system which includes police radios that

are interoperable with other agencies for $249,616. • Increase in various capital outlay expenditures carried over from the previous fiscal

year in the amount of $1,107,148. • Increase in capital outlay specific to the construction of the seawall at Lantana’s

municipal beach park by $1,563,000. The most significant variances between the final budget and actual were as follows: • Revenues for the 2009 fiscal year were $267,145 less than the final budget. While

State revenue sharing, sales tax, and building permits were less than anticipated, other revenues such as taxes (local communications services tax, water utility tax, and franchise fees) exceeded expectations. The net effect of these revenues comes very close to the final budget. The sole revenue that accounts for the variation between budget and actual is investment income which is derived from surplus funds the Town has deposited at Qualified Public Depositors (QPD) and the State Board of Administrations Local Governmental Investment Pool (Florida PRIME), all of which earned considerably less than projected when preparing budget estimates the year before. The rates received from investments have decreased considerably since 2007 due to the current economic climate.

-11-

• Expenditures were $1.9 million less than the final budget for the 2009 fiscal year. About

65% of the difference is attributed to projects that were not fully completed by the end of the fiscal year. The remainder of the reduction was due to the combination of departments closely monitoring all expenditures, as well as lower than expected fuel costs.

CAPITAL ASSET AND DEBT ADMINISTRATION

Capital Assets The capital assets of the Town are those assets that are used in the performance of Town functions. Capital assets include equipment, buildings, land, park facilities, etc. The Town has elected to retroactively apply the capitalization requirements of GASB Statement No. 34 to major general infrastructure assets. • The Town’s investment in capital assets for its governmental and business-type

activities as of September 30, 2009, amounts to $31.9 million (net of accumulated depreciation).

2009 2008 2009 2008 2009 2008

Land 110,367$ 110,367$ 4,300$ 4,300$ 114,667$ 114,667$ Construction-in-progress 49,427 - 356,392 - 405,819 - Roads and streets 22,799,727 22,779,860 - - 22,799,727 22,779,860 Buildings and improvements 6,943,964 5,409,569 11,475,383 11,507,245 18,419,347 16,916,814 Infrastructure - - 8,679,737 8,764,853 8,679,737 8,764,853 Furniture, equipment & vehicles 4,731,584 4,477,245 983,219 981,271 5,714,803 5,458,516 Intangible assets, net - - 1,097,878 1,221,727 1,097,878 1,221,727 Total assets 34,635,069$ 32,777,041$ 22,596,909$ 22,479,396$ 57,231,978$ 55,256,437$

Less accumulated depreciation (14,420,600) (13,162,409) (10,872,397) (10,316,121) (25,292,997) (23,478,530)

Total 20,214,469$ 19,614,632$ 11,724,512$ 12,163,275$ 31,938,981$ 31,777,907$

Capital AssetsTown of Lantana

Activities ActivitiesTotal

ActivitiesGovernmental Business-type

Additional information on the Town’s capital assets can be found in Note 6 beginning on page 36 of this report.

-12-

Long-Term Debt

Currently, the Town uses debt financing on an as-needed basis each year. At the end of the current fiscal year, the Town had total debt of $11.5 million. None of this amount comprises debt backed by the full faith and credit of the government. Gas tax, utility tax and water and sewer revenues secure the bond and notes. During periods where capital leases are utilized, the equipment secures the debt.

2009 2008 2009 2008 2009 2008

Bonds and loans payable 2,876,366$ 3,185,982$ 8,657,211$ 9,214,821$ 11,533,577$ 12,400,803$

Total 2,876,366$ 3,185,982$ 8,657,211$ 9,214,821$ 11,533,577$ 12,400,803$

Activities Activities Activities

Town of LantanaOutstanding Debt

Governmental Business-type Total

Additional information on the Town’s debt can be found in Note 7 beginning on page 37 of this report.

NEXT YEAR’S BUDGET AND ECONOMIC FACTORS During the current fiscal year, unreserved and undesignated fund balance in the General Fund decreased from $9.7 million to $8.9 million. The Town Council has recommended that $1.7 million of this amount remain in the General Fund and not be used to balance future year’s budgets. The remaining fund balance’s use changes from year to year. In some years, large capital equipment is purchased; in other years, it has been Council’s direction not to use any of the Town’s fund balance. Finally, as the economy continues on by either shrinking or remaining static, fund balance may assist future years of declining revenues due to lower property values and other revenues that reduce with the economy. In considering the Town’s budget for fiscal year 2009-2010, the Town’s Council and management were conservative as to the growth of revenues and expenditures.

-13-

CONTACTING THE TOWN’S FINANCIAL MANAGEMENT

This financial report is designed to provide our citizens, taxpayers, customers, investors, and creditors with a general overview of the Town’s finances and to show the Town’s accountability for the money it receives and spends. If you have questions about this report or need additional financial information, contact the Town’s Finance Department, at the Town of Lantana, 500 Greynolds Circle, Lantana, Florida 33462.

BASIC FINANCIAL STATEMENTS

Governmental Business-typeActivities Activities Total

ASSETSCash and cash equivalents 11,409,720$ 5,223,207$ 16,632,927$ Investments 111,465 105,633 217,098 Receivables, net 637,489 442,477 1,079,966 Inventories 15,752 - 15,752 Restricted assets:

Cash and cash equivalents - 1,840,299 1,840,299 Investments - 21,978 21,978

Deferred charges - 43,171 43,171 Net pension asset 87,324 - 87,324 Capital assets not being depreciated 159,794 360,692 520,486 Capital assets being depreciated and amortized, net 20,054,675 11,363,820 31,418,495

Total assets 32,476,219 19,401,277 51,877,496

LIABILITIESAccounts payable and accrued liabilities 424,929 243,267 668,196 Retainages payable - 420,060 420,060 Unearned revenue 262,070 - 262,070 Meter deposits payable - 157,929 157,929 Accrued interest payable 18,801 154,595 173,396 Noncurrent liabilities:

Due within one year 583,222 679,203 1,262,425 Due in more than one year 2,944,944 8,109,342 11,054,286

Total liabilities 4,233,966 9,764,396 13,998,362

NET ASSETSInvested in capital assets, net of related debt 17,338,103 3,067,301 20,405,404 Restricted for public safety 80,105 - 80,105 Unrestricted 10,824,045 6,569,580 17,393,625

Total net assets 28,242,253$ 9,636,881$ 37,879,134$

TOWN OF LANTANA, FLORIDA

STATEMENT OF NET ASSETS

SEPTEMBER 30, 2009

See notes to basic financial statements.-14-

Charges Operating Capitalfor Grants and Grants and Governmental Business-type

Function/Program Activities Expenses Services Contributions Contributions Activities Activities Total

Governmental activities:General government 802,674$ 511,352$ -$ -$ (291,322)$ -$ (291,322)$ Physical environment 3,407,583 813,309 327,073 21,084 (2,246,117) - (2,246,117) Public safety 4,854,172 798,668 159,346 17,788 (3,878,370) - (3,878,370) Culture and recreation 406,927 181,142 5,383 - (220,402) - (220,402) Interest on long-term debt 117,721 - - - (117,721) - (117,721)

Total governmental activities 9,589,077 2,304,471 491,802 38,872 (6,753,932) - (6,753,932)

Business-type activities: Utility - water and sewer 4,639,241 4,834,025 - 145,735 - 340,519 340,519

Total business-type activities 4,639,241 4,834,025 - 145,735 - 340,519 340,519 Total government 14,228,318$ 7,138,496$ 491,802$ 184,607$ (6,753,932) 340,519 (6,413,413)

General revenues:Property taxes 3,166,215 - 3,166,215 Utility taxes 918,889 - 918,889 Franchise fees based on gross receipts 772,731 - 772,731 Communications services tax 409,214 - 409,214 Sales and use tax 605,504 605,504 State revenue sharing - unrestricted 289,023 - 289,023 Investment income (loss) - unrestricted 73,451 (14,847) 58,604 Miscellaneous 125,749 - 125,749

Total general revenues 6,360,776 (14,847) 6,345,929

Change in net assets (393,156) 325,672 (67,484)

Net assets, beginning of year 28,635,409 9,311,209 37,946,618

Net assets, end of year 28,242,253$ 9,636,881$ 37,879,134$

TOWN OF LANTANA, FLORIDA

STATEMENT OF ACTIVITIES

YEAR ENDED SEPTEMBER 30, 2009

Program Revenues Changes in Net AssetsNet Expense (Revenue) and

See notes to basic financial statements.-15-

Nonmajor TotalGovernmental Governmental

General Funds FundsASSETS

Cash and cash equivalents 9,511,770$ 1,168,499$ 10,680,269$ Investments 101,822 9,643 111,465 Receivables: Accounts, net of allowance for uncollectible amounts 309,451 - 309,451 Intergovernmental 249,186 78,852 328,038 Inventories 15,752 - 15,752

Total assets 10,187,981$ 1,256,994$ 11,444,975$

LIABILITIES AND FUND BALANCES

Liabilities:Accounts payable and accrued liabilities 300,135$ 124,794$ 424,929$ Deferred revenue 34,326 - 34,326 Unearned revenue 262 070 262 070

TOWN OF LANTANA, FLORIDA

BALANCE SHEETGOVERNMENTAL FUNDS

SEPTEMBER 30, 2009

See notes to basic financial statements.-16-

Unearned revenue 262,070 - 262,070

Total liabilities 596,531 124,794 721,325

Fund balances:Reserved:

Reserved for inventories 15,752 - 15,752 Unreserved, designated for: -

Subsequent year's expenditures - 53,990 53,990 Capital improvements 642,912 575,199 1,218,111

Unreserved and undesignated, reported in:General fund 8,932,786 - 8,932,786 Special revenue funds - 503,011 503,011

Total fund balances 9,591,450 1,132,200 10,723,650 Total liabilities and fund balances 10,187,981$ 1,256,994$ 11,444,975$

See notes to basic financial statements.-16-

Total governmental fund balances (page 16) 10,723,650$

Amounts reported for governmental activities in the statement of net assets are different because:

Capital assets used in governmental activities are not financial resources and therefore are not reported in the governmental funds:

Cost of assets 34,635,069$ Less accumulated depreciation (14,420,600) 20,214,469

Other long-term assets are not available to pay for current period expenditures and therefore are deferred in the fund. 34,326

Net pension assets for defined benefit pension plans are reported in the statement of net assets. They are not reported in the governmental fund statements because they do not represent available spendable resources. 87,324

Long-term liabilities, including bonds and notes payable, are not due and payable in the current period and therefore are not reported in the funds:

Accrued interest payable (18,801)$ Bonds and notes payable (2,876,366) Compensated absences payable (600,800) Other post-employment benefits (51,000) (3,546,967)

Internal service funds are used by management to charge the costs of certain activities such as insurance to individual funds. The assets and liabilities of the internal service funds are included in governmental activities in the statement of net assets.

Internal service fund net assets 729,451

Total net assets (page 14) 28,242,253$

TOWN OF LANTANA, FLORIDA

RECONCILIATION OF THE GOVERNMENTAL FUNDS BALANCE SHEETTO THE STATEMENT OF NET ASSETS

SEPTEMBER 30, 2009

See notes to basic financial statements.-17-

Nonmajor TotalGovernmental Governmental

General Funds FundsRevenues:

Taxes 5,312,145$ 259,712$ 5,571,857$ Licenses and permits 389,827 - 389,827 Intergovernmental 1,642,493 75,653 1,718,146 Charges for services 1,227,443 8,827 1,236,270 Fines and forfeitures 96,680 4,459 101,139 Investment income 72,207 1,244 73,451 Miscellaneous 121,765 600 122,365

Total revenues 8,862,560 350,495 9,213,055

Expenditures:Current:

General government 763,636 - 763,636 Physical environment 2,157,125 228,686 2,385,811 Public safety 4,563,517 67,202 4,630,719 Culture and recreation 201,539 - 201,539

Capital outlay 1,983,247 141,509 2,124,756 Debt service:

Principal 90,880 218,736 309,616 Interest and fiscal charges 31,077 88,842 119,919

Total expenditures 9,791,021 744,975 10,535,996

Deficiency of revenues over expenditures (928,461) (394,480) (1,322,941)

Other financing sources (uses):Transfers in - 350,000 350,000 Transfers out (350,000) - (350,000)

Total other financing sources (uses) (350,000) 350,000 - Net change in fund balances (1,278,461) (44,480) (1,322,941)

Fund balances, beginning 10,869,911 1,176,680 12,046,591

Fund balances, ending 9,591,450$ 1,132,200$ 10,723,650$

YEAR ENDED SEPTEMBER 30, 2009

TOWN OF LANTANA, FLORIDA

STATEMENT OF REVENUES, EXPENDITURES AND CHANGES IN FUND BALANCESGOVERNMENTAL FUNDS

See notes to basic financial statements.-18-

Net change in fund balances - total governmental funds (page 18) (1,322,941)$

Amounts reported for governmental activities in the statement of activities are different because:

Governmental funds report capital outlays as expenditures. However, in the statement of activities, the cost of capital assets is allocated over their estimated useful lives and reported as depreciation expense:

Expenditures for capital assets 2,124,756$ Less current year depreciation (1,552,881) 571,875

Donated capital assets used in governmental activities are not financial resources and, therefore, are not reported in the funds. 27,962

Revenues in the statement of activities that do not provide current financial resources are not reported as revenue in the funds. (45,096)

Repayment of debt principal is an expenditure in the governmental funds, but the payment reduces long-term liabilities in the statement of net assets.

Principal payments on bonds and notes 309,616

Some expenses in the statement of activities do not require the use of current financial resources and therefore are not reported in the governmental funds:

Net pension asset (9,580)$ Accrued interest payable 2,198 Compensated absences payable (28,004) Other post-employment benefits (51,000) (86,386)

Internal service funds are used by management to charge the cost of certain activities, such as insurance, to individual funds. The net revenue (expense) of internal service funds is reported with governmental activities.

Internal service fund change in net assets 151,814

Change in net assets (page 15) (393,156)$

TOWN OF LANTANA, FLORIDA

RECONCILIATION OF THE STATEMENT OF REVENUES, EXPENDITURES AND CHANGES INFUND BALANCES OF THE GOVERNMENTAL FUNDS TO THE STATEMENT OF ACTIVITIES

YEAR ENDED SEPTEMBER 30, 2009

See notes to basic financial statements.-19-

Business-type GovernmentalActivities Activities

InternalWater & Service

Sewer FundASSETS

Current assets:Cash and cash equivalents 5,223,207$ 729,451$ Investments 105,633 - Receivables:

Accounts receivable, net of allowance for uncollectible amounts 335,242 - Intergovernmental 107,235 - Total current assets 5,771,317 729,451

Noncurrent assets:Restricted assets:

Cash and cash equivalents 1,840,299 - Investments 21,978 -

Deferred charges 43,171 - Capital assets, net of accumulated depreciation and amortization 11,724,512 -

Total noncurrent assets 13,629,960 - Total assets 19,401,277 729,451

LIABILITIES Current liabilities:

Accounts payable and accrued liabilities 243,267 - Retainages payable 420,060 - Meter deposits payable 157,929 - Accrued interest payable 154,595 - Compensated absences payable, current portion 57,113 - Bonds payable, current portion 622,090 -

Total current liabilities 1,655,054 - Noncurrent liabilities:

Compensated absences payable 74,221 - Bonds payable 8,035,121 -

Total noncurrent liabilities 8,109,342 -

Total liabilities 9,764,396 -

NET ASSETSInvested in capital assets, net of related debt 3,067,301 - Unrestricted 6,569,580 729,451

Total net assets 9,636,881$ 729,451$

TOWN OF LANTANA, FLORIDA

STATEMENT OF NET ASSETSPROPRIETARY FUNDS

SEPTEMBER 30, 2009

See notes to basic financial statements.-20-

Business-type GovernmentalActivities Activities

InternalWater & ServiceSewer Fund

Operating revenues:Charges for services 4,820,424$ 613,800$ Miscellaneous revenues 13,601 -

Total operating revenues 4,834,025 613,800

Operating expenses:Personal services 1,369,310 - Cost of sales and services 1,825,289 - General and administrative - 461,986Depreciation 846,565 - Amortization 166,974 -

Total operating expenses 4,208,138 461,986

Operating income 625,887 151,814

Nonoperating revenues (expenses):Investment loss (14,847) - Interest expense (431,103) - Grants 145,735 -

Total nonoperating revenues (expenses) (300,215) -

Change in net assets 325,672 151,814

Net assets, beginning 9,311,209 577,637

Net assets, end of year 9,636,881$ 729,451$

TOWN OF LANTANA, FLORIDA

STATEMENT OF REVENUES, EXPENSES AND CHANGES IN NET ASSETSPROPRIETARY FUNDS

YEAR ENDED SEPTEMBER 30, 2009

See notes to basic financial statements.-21-

Business-type GovernmentalActivities Activities

InternalWater & Service

Sewer FundCash flows from operating activities:

Cash received from customers 4,857,408$ -$ Cash paid to employees for services (1,382,349) - Cash received from interfund services provided - 613,800 Cash paid to suppliers for goods and services (1,659,943) (464,424) Other receipts 13,601 -

Net cash provided by operating activities 1,828,717 149,376

Cash flows from capital and related financing activities:Acquisition and construction of capital assets (531,652) - Principal repayments (597,021) - Interest paid (439,002) - Grants received 38,500 -

Net cash used in capital and related financing activities (1,529,175) -

Cash flows from investing activities: Proceeds from sale of investments 401,526 - Purchase of investments (127,611) -

Interest received 28,234 - Net cash provided by investing activities 302,149 -

Net increase in cash and cash equivalents 601,691 149,376

Cash and cash equivalents, beginning 6,461,815 580,075 Cash and cash equivalents, ending 7,063,506$ 729,451$

Cash and cash equivalents:Unrestricted 5,223,207$ 729,451$ Restricted 1,840,299 -

7,063,506$ 729,451$

Reconciliation of operating income to net cash provided by operating activities:Operating income 625,887$ 151,814$ Adjustments to reconcile operating income to net

cash provided by operating activities:Depreciation 846,565 - Amortization 166,974 - Changes in assets and liabilities:

Decrease in accounts receivable 29,745 - Decrease in prepaid items - 6,641 Decrease in accounts payable and accrued liabilities (113,572) (9,079) Increase in retainages payable 275,847 - Increase in meter deposits payable 7,240 - Decrease in compensated absences (9,969) -

Total adjustments 1,202,830 (2,438) Net cash provided by operating activities 1,828,717$ 149,376$

Noncash investing activities - Change in fair value of investments (43,081)$ -$

TOWN OF LANTANA, FLORIDA

STATEMENT OF CASH FLOWSPROPRIETARY FUNDS

YEAR ENDED SEPTEMBER 30, 2009

See notes to basic financial statements.-22-

PensionTrustFund

ASSETS

Accounts receivable 43,172$ Prepaid items 3,178 Investments:

U.S. Government obligations 146,806 U.S. Government agencies 581,689 Corporate obligations 936,826 Domestic stocks 3,692,462 Temporary investment funds 760,229

Total investments 6,118,012

Total assets 6,164,362

LIABILITIES

Accounts payable 49,830

NET ASSETS

Net assets held in trust for pension benefits 6,114,532$

TOWN OF LANTANA, FLORIDA

STATEMENT OF FIDUCIARY NET ASSETS

SEPTEMBER 30, 2009

See notes to basic financial statements.-23-

PensionTrustFund

Additions:Contributions:

Employer 331,310$ State of Florida 97,987Plan members 111,040

Total contributions 540,337

Investment income:Interest and dividends 141,139 Net appreciation in fair value of investments 640,815 Investment expenses (33,420)

Net investment income 748,534 Total additions 1,288,871

Deductions:Participant benefit payments 150,272 Administrative expenses 29,832

Total deductions 180,104

Net increase 1,108,767

Net assets, beginning 5,005,765

Net assets, ending 6,114,532$

TOWN OF LANTANA, FLORIDA

STATEMENT OF CHANGES IN FIDUCIARY NET ASSETS

YEAR ENDED SEPTEMBER 30, 2009

See notes to basic financial statements.-24-

NOTES TO BASIC FINANCIAL STATEMENTS

TOWN OF LANTANA, FLORIDA

NOTES TO BASIC FINANCIAL STATEMENTS

YEAR ENDED SEPTEMBER 30, 2009

-25-

NOTE 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The Town of Lantana, Florida (the Town) was originally incorporated in 1921 pursuant to Chapter 8998, Laws of Florida. It was re-incorporated in 1931 by Chapter 15302, Laws of Florida. The Town operates under a Council-Manager form of government. The Town is governed by an elected Mayor and a four-member Town Council (the “Council”), which appoints a Town Manager. The Town provides the following services: public safety, recreation, sanitation, streets and roads, planning and zoning, water and sewer, and general administrative services.

The basic financial statements of the Town have been prepared in conformity with accounting principles generally accepted in the United States (GAAP) as applied to governmental units. The Governmental Accounting Standards Board (GASB) is the accepted standard-setting body for establishing governmental accounting and financial reporting principles. The following is a summary of the Town’s more significant policies:

a. Reporting Entity

Under governmental accounting and financial reporting standards, the Town’s reporting entity consists of the Town, organizations for which the Town is financially accountable and other organizations for which the nature and significance of their relationship with the Town are such that exclusion would cause the Town’s financial statements to be misleading or incomplete. The Town government is considered financially accountable if it appoints a voting majority of an organization’s governing body and it is able to impose its will on that organization. The Town may also be financially accountable if an organization is fiscally dependent on the primary government regardless of the authority of the organization’s governing board. Legally separate organizations outside of the primary government that meet the criteria for financial accountability are considered component units. Based upon the application of these criteria, there were no organizations that met the criteria described above.

b. Government-Wide and Fund Financial Statements

The government-wide financial statements (i.e., the statement of net assets and the statement of activities) report information on all of the non-fiduciary activities of the Town. For the most part, the effect of interfund activity has been removed from these statements. Governmental activities, which normally are supported by taxes and intergovernmental revenues, are reported separately from business-type activities, which rely to a significant extent on fees and charges for support. The statement of activities demonstrates the degree to which the direct expenses of a given function are offset by program revenues. Direct expenses are those that are clearly identifiable with a specific function or segment. Program revenues include 1) charges to customers or applicants who purchase, use, or directly benefit from goods, services or privileges provided by a given function or segment and, 2) grants and contributions that are restricted to meeting the operational or capital requirements of a particular function or segment. Taxes and other items not properly included among program revenues are reported instead as general revenues.

TOWN OF LANTANA, FLORIDA

NOTES TO BASIC FINANCIAL STATEMENTS (Continued)

-26-

NOTE 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

b. Government-Wide and Fund Financial Statements (Continued) Separate financial statements are provided for governmental funds, proprietary funds and fiduciary funds, even though the latter are excluded from the government-wide financial statements. Major individual governmental funds are reported as separate columns in the fund financial statements. All remaining nonmajor governmental funds are aggregated and reported as nonmajor funds.

c. Measurement Focus, Basis of Accounting and Financial Statement Presentation

The government-wide financial statements are reported using the economic resources measurement focus and the accrual basis of accounting, as are the proprietary fund and fiduciary fund financial statements. Revenues are recorded when earned and expenses are recorded when a liability is incurred, regardless of the timing of related cash flows. Property taxes are recognized as revenues in the year for which they are levied. Grants and similar items are recognized as revenue as soon as all eligibility requirements imposed by the provider have been met.

Governmental fund financial statements are reported using the current financial resources measurement focus and the modified accrual basis of accounting. Revenues are recognized as soon as they are both measurable and available. Revenues are considered to be available when they are collectible within the current period or soon enough thereafter to pay liabilities of the current period. For this purpose, the Town considers revenues to be available if they are collected within 60 days of the end of the current fiscal period. Expenditures generally are recorded when a liability is incurred, as under accrual accounting. However, debt service expenditures, as well as expenditures related to compensated absences, are recorded only when payment is due.

Property taxes, franchise fees, other taxes, licenses, and interest associated with the current fiscal period are all considered to be susceptible to accrual and so have been recognized as revenues of the current fiscal period. Revenues for expenditure driven grants are recognized when the qualifying expenditures are incurred. All other revenue items are considered to be measurable and available only when cash is received by the Town.

The Town reports the following major governmental fund:

General Fund – The General Fund is the primary operating fund of the Town and is used to account for all financial resources applicable to the general operations of the Town government, except those required to be accounted for in another fund.

The Town reports the following major enterprise fund:

Water and Sewer – The Water and Sewer Fund is used to account for the provision of water and sewer services to residents of the service area. All activities to provide such services are accounted for in this fund, including administration, generation, transmission, distribution, collection, pumping, treatment, disposal and customer service.

TOWN OF LANTANA, FLORIDA

NOTES TO BASIC FINANCIAL STATEMENTS (Continued)

-27-

NOTE 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

c. Measurement Focus, Basis of Accounting and Financial Statement Presentation (Continued)

Additionally, the Town reports the following fund types:

Internal Service Fund – The Internal Service Fund is used to account for insurance premiums and deductibles which are funded by other Town funds on a cost reimbursement basis. Pension Trust Fund – The Pension Trust Fund accounts for the activities of the Police Relief and Pension Fund, which accumulates resources for pension benefit payments to qualified employees.

Private-sector standards of accounting and financial reporting issued prior to December 1, 1989, generally are followed in both the government-wide and proprietary fund financial statements to the extent that those standards do not conflict with or contradict guidance of the Governmental Accounting Standards Board. The Town has the option of following subsequent private-sector guidance for their business-type activities and enterprise funds, subject to this same limitation. The Town has elected to not follow subsequent private-sector guidance.

As a general rule, the effect of interfund activity has been eliminated from the government-wide financial statements. Exceptions to this general rule are charges between the Town’s utility functions and various other functions of the Town. Elimination of these charges would distort the direct costs and program revenues reported for the various functions concerned.

Amounts reported as program revenues include 1) charges to customers or applicants for goods, services, or privileges provided, 2) operating grants and contributions, and 3) capital grants and contributions. Internally dedicated resources are reported as general revenues rather than as program revenues. Likewise, general revenues include all taxes.

Proprietary funds distinguish operating revenues and expenses from non-operating items. Operating revenues and expenses generally result from providing services and producing and delivering goods in connection with a proprietary fund’s principal ongoing operations. The principal operating revenues of the Water and Sewer Fund and the Internal Service Fund are charges to customers for sales and services. Operating expenses for the Water and Sewer Fund and the Internal Service Fund include the cost of sales and services, general and administrative expenses, depreciation and amortization. All revenues and expenses not meeting this definition are reported as non-operating revenues and expenses.

When both restricted and unrestricted resources are available for use, it is the Town’s policy to use restricted resources first, then unrestricted resources as needed.

TOWN OF LANTANA, FLORIDA

NOTES TO BASIC FINANCIAL STATEMENTS (Continued)

-28-

NOTE 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

d. Assets, Liabilities, and Net Assets or Equity

1. Deposits and Investments

Cash and cash equivalents include cash on hand, time and demand deposits. The Town maintains a cash pool that is available for use by all funds. Interest earned on pooled cash is allocated to each of the funds based on the fund’s average equity balance on a monthly basis.

All investments, except the Florida PRIME and Fund B, are reported at fair value, which is based on quoted market prices. The Florida PRIME is recorded at the value of the pool shares (2a-7 like pool), which is fair value. Fund B is a fluctuating NAV pool and is reported based on the fair value factor. Cash and cash equivalents, for purposes of the statement of cash flows, includes pooled cash and investments which are defined as short-term, highly liquid investments with original maturities of three months or less.

2. Interfund Receivables and Payables

Activity between funds that is representative of lending/borrowing arrangements outstanding at the end of the fiscal year is referred to as either due to/from other funds. Any residual balances outstanding between the governmental activities and business-type activities are reported in the government-wide financial statements as internal balances.

3. Receivables

Receivables include amounts due from other governments and others for services provided by the Town. Receivables are recorded and revenues are recognized as earned or as specific program expenditures/expenses are incurred. Allowances for uncollectible receivables are based upon historical trends and the periodic aging of receivables.

4. Inventories

Inventories consist principally of materials and supplies held for consumption and are recorded at cost using the first-in first-out method. In the governmental funds, the cost of inventories are recorded as expenditures at the time of purchase, while in the proprietary funds, the cost of inventories are recorded as expenses when consumed. In the governmental funds, reported inventories are offset by a fund balance reserve which indicates that they do not constitute available spendable resources.

5. Restricted Assets

Restricted assets of the enterprise fund consist of bond proceeds restricted for debt service and renewal and replacements under the terms of the outstanding revenue bonds, as well as capacity charges and other revenues of the Water and Sewer System restricted for capital improvements to the facility.

TOWN OF LANTANA, FLORIDA

NOTES TO BASIC FINANCIAL STATEMENTS (Continued)

-29-

NOTE 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

d. Assets, Liabilities, and Net Assets or Equity (Continued)

6. Capital Assets

Capital assets, which include property, plant, equipment, and infrastructure assets (e.g., roads, bridges, sidewalks, and similar items) are reported in the applicable governmental or business-type activities columns in the government-wide financial statements. Capital assets are defined by the Town as assets with an initial individual cost of $1,000 or more and an estimated useful life in excess of one year. Purchased or constructed assets are recorded at actual cost or estimated historical cost if actual cost is unavailable. Donated capital assets are recorded at estimated fair market value at the date of donation. The Town has elected to retroactively apply the capitalization requirements of GASB Statement No. 34 to major general infrastructure assets acquired since 1980. Infrastructure assets include roads, bridges, sidewalks, lighting and drainage systems and similar assets that are immovable and of value only to the Town. The costs of normal maintenance and repairs that do not add to the value of the asset or materially extend the asset’s life are not capitalized. Major outlays for capital assets and improvements are capitalized as projects are constructed.

Tangible capital assets of the Town are depreciated using the straight-line method over the following useful lives:

Asset Years

Buildings and improvements 25-50 yearsRoads and streets 25 yearsFurniture, equipment and vehicles 5-10 yearsWater and sewer system 7-50 years

Intangible capital assets which consist of a right of use of the City of Lake Worth wastewater facilities are amortized over periods ranging between 13 and 40 years.

7. Unearned Revenue

Unearned revenue is recorded for governmental fund receivables that are not both measurable and available. In addition, inflows that do not yet meet the criteria for revenue recognition, such as occupational licenses collected in advance, are recorded as unearned revenue in the government-wide and the fund statements.

TOWN OF LANTANA, FLORIDA

NOTES TO BASIC FINANCIAL STATEMENTS (Continued)

-30-

NOTE 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

d. Assets, Liabilities, and Net Assets or Equity (Continued)

8. Compensated Absences

It is the Town's policy to permit employees to accumulate, within certain limits, earned but unused vacation time, sick leave, and compensatory time, which will be paid to employees upon separation from Town service. All vacation and sick leave pay and compensatory time is accrued when incurred in the government-wide and proprietary fund financial statements. A liability for those amounts is reported in the governmental funds only if they have matured, for example, as a result of employee resignations and retirements.

9. Long-Term Obligations

In the government-wide financial statements and the proprietary fund types in the fund financial statements, long-term debt and other long-term obligations are reported as liabilities in the applicable governmental activities, business-type activities or proprietary fund type statement of net assets. Bond premiums and discounts, as well as issuance costs, are deferred and amortized over the life of the bonds using the straight line method. Bonds are reported net of the applicable bond premium or discount. Bond issuance costs are reported as deferred charges and amortized over the term of the related debt.

In the fund financial statements, governmental fund types recognize bond premiums and discounts, as well as bond issuance costs, during the current period. The face amount of debt issued is reported as other financing sources. Premiums received on debt issuances are reported as other financing sources while discounts on debt issuances are reported as other financing uses. Issuance costs, whether or not withheld from the actual debt proceeds received, are reported as debt service expenditures.

10. Net Assets

Net assets of the government-wide and proprietary funds are categorized as invested in capital assets, net of related debt; restricted or unrestricted. Invested in capital assets, net of related debt, is that portion of net assets that relates to the Town’s capital assets reduced by accumulated depreciation and by any outstanding debt incurred to acquire, construct or improve those assets, excluding unexpended proceeds. Restricted net assets is that portion of net assets that has been restricted for general use by external parties (creditors, grantors, contributors, or laws or regulations of other governments) or imposed by law through constitutional provisions or enabling legislation. Unrestricted net assets consist of all net assets that do not meet the definition of either of the other two components.

TOWN OF LANTANA, FLORIDA

NOTES TO BASIC FINANCIAL STATEMENTS (Continued)

-31-

NOTE 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

d. Assets, Liabilities, and Net Assets or Equity (Continued)

11. Fund Equity

In the fund financial statements, governmental funds report reservations of fund balance to indicate the portion of fund balance that is not appropriable for expenditures or is legally segregated by outside parties for a specific purpose. Designations indicate tentative managerial plans or intent to use financial resources in a future period. Undesignated fund balance indicates the portion of fund balance which is available for future use.

12. Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements. Estimates also affect the reported amounts of revenues and expenditures/expenses during the reporting period. Actual results could differ from those estimates.

NOTE 2. DEPOSITS AND INVESTMENTS

Deposits

All of the Town’s deposits are held in qualified public depositories pursuant to State of Florida Statutes, Chapter 280, Florida Security for Public Deposits Act. Under the Act, every qualified public depository shall deposit with the Treasurer eligible collateral of the depository to be held subject to his or her order. The Treasurer, by rule, shall establish minimum required collateral pledging levels. The pledging level may range from 25% to 125% of the average monthly balance of public deposits depending upon the depository’s financial condition and establishment period. All collateral must be deposited with an approved financial institution. Any potential losses to public depositors are covered by applicable deposit insurance, sale of securities pledged as collateral and, if necessary, assessments against other qualified public depositories of the same type as the depository in default.

Investments – Town

The Town has adopted an investment policy in accordance with Florida Statutes to establish guidelines for the efficient management of its cash reserves. The Town is authorized to invest in obligations of the U.S. Treasury, its agencies and instrumentalities, certificates of deposit, the State Board of Administration investment pool, any intergovernmental investment pools authorized pursuant to Chapter 163 of the Florida Statutes, SEC registered money market funds with the highest credit quality rating from a nationally recognized rating agency, and securities of any interest in any open-end or closed-end management type investment company or investment trust registered under the Investment Company Act of 1940, provided that the portfolio is limited to obligations of the U.S. government, its agencies and instrumentalities and to repurchase agreements fully collateralized by such U.S. government obligations and provided that such investment company or investment trust takes delivery of such collateral either directly or through an authorized custodian.

TOWN OF LANTANA, FLORIDA

NOTES TO BASIC FINANCIAL STATEMENTS (Continued)

-32-

NOTE 2. DEPOSITS AND INVESTMENTS (Continued)

Investments – Town (Continued) The State Board of Administration (SBA) administers the Florida PRIME, (formally known as the Local Government Surplus Funds Trust Fund (LGIP), and the Fund B Surplus Funds Trust Fund. (Fund B), both of which are governed by Chapter 19-7 of the Florida Administrative Code and Chapters 218 and 215 of the Florida Statutes. These rules provide guidance and establish the policies and general operating procedures for the administration of the Florida PRIME and Fund B. The Florida PRIME is not a registrant with the Securities and Exchange Commission (SEC); however, the Board has adopted operating procedures consistent with the requirements for a 2a-7 fund, which permits money market funds to use amortized cost to maintain a constant net asset value (NAV) of $1 per share. The fair value of the position in the Florida PRIME is equal to the value of the pool shares. The Fund B is accounted for as a fluctuating NAV pool. As of September 30, 2009, the fair value factor for Fund B was $ .54915 per share. The Fund B is not subject to participant withdrawal requests. Distributions from Fund B, as determined by the SBA, are effected by transferring eligible cash or securities to the Florida PRIME, consistent with the pro rata allocation of pool shareholders of record at the creation of Fund B. One hundred percent of such distributions from Fund B are available as liquid balance within the Florida PRIME. The investments in the Florida PRIME and Fund B are not insured by FDIC or any other governmental agency. As of September 30, 2009, the Town had the following investments:

WeightedFair Average

Value Maturity

Florida PRIME 24,891$ 33 daysFund B 214,185 6.69 years

239,076$ Interest Rate Risk The Town has an investment policy of structuring the investment portfolio so that the securities mature to meet cash requirements for ongoing operations, thereby avoiding the need to sell securities on the open market prior to maturity and investing operating funds primarily in short-term securities, money market mutual funds, or similar investment pools unless it is anticipated that long-term securities can be held to maturity without jeopardizing the liquidity requirements. The Town’s investment policy limits the maturities on individual investments to no more than five years.

Credit Risk The Town’s investment policy limits investments to the highest ratings issued by a nationally recognized statistical rating organization (NRSRO). The Florida PRIME is rated AAAm by Standard and Poors. The Fund B is not rated by an NRSO.

TOWN OF LANTANA, FLORIDA

NOTES TO BASIC FINANCIAL STATEMENTS (Continued)

-33-

NOTE 2. DEPOSITS AND INVESTMENTS (Continued)

Investments – Town (Continued) Concentration of Credit Risk The Town’s investment policy states that assets shall be diversified to control the risk of loss resulting from concentration of assets to a specific maturity, instrument, issue, dealer, or bank through which these securities are bought and sold. As of September 30, 2009, the value of each position held in the Town’s portfolio is less than 5% in any one issuer.

Investments – Lantana Relief and Pension Fund (LPRPF) The Plan’s Board of Trustees recognizes that the obligations of the Plan are long-term and that

its investment policy should be made with a view toward performance and return over a number of years. The general investment objective is to obtain a reasonable total rate of return defined as interest and dividend income plus realized and unrealized capital gains or losses that commensurate with the prudent investor rule and Chapter 185 of the Florida Statutes. Permissible investments include obligations of the U.S. Treasury and U.S. agencies, high capitalization common or preferred stocks, pooled equity funds, high quality bonds or notes and fixed income funds.

At September 30, 2009, the Plan had the following investments:

Credit Rating by Fair EffectiveInvestment Type Standard & Poor's Value Duration (Years)

U.S. Government obligations AAA 146,806$ 7.20U.S. Government agencies AAA 581,689 5.10Corporate obligations A-AAA 936,826 4.12Temporary investment funds Not rated 760,229 Daily

Total investments 2,425,550$ Interest Rate Risk Interest rate risk is the risk that changes in interest rates will adversely affect the fair value of an investment in debt securities. Generally, the longer the time to maturity, the greater the exposure to interest rate risks. Through its investment policies, the Plan manages its exposure to fair value losses arising from increasing interest rates. The Plan limits the effective duration of its investment portfolio through the adoption of the Lehman Brothers Intermediate Aggregate Bond Index bench mark. Credit Risk Credit risk is the risk that a debt issuer will not fulfill its obligations. The Plan’s investment policy addresses credit risk by limiting investments in bonds and preferred stocks to securities rated investment grade or above by a Nationally Recognized Statistical Rating Organization, unless specifically approved by the Board of Trustees. Securities which are unrated may be purchased, if in the judgment of the investment manager, they would carry an investment grade rating. Consistent with State law, the Plan’s investment guidelines limit its fixed

TOWN OF LANTANA, FLORIDA

NOTES TO BASIC FINANCIAL STATEMENTS (Continued)

-34-

NOTE 2. DEPOSITS AND INVESTMENTS (Continued)

Investments – Lantana Relief and Pension Fund (LPRPF) (Continued)

income investments to a quality rating of “A” or equivalent as rated by Moody’s or by Standard & Poor’s bond rating services at the time of purchase. Fixed income investments which are downgraded below the minimum rating must be liquidated at the earliest beneficial opportunity. The Plan’s investments were in compliance with the above at September 30, 2009. Custodial Credit Risk Custodial credit risk is defined as the risk that the Plan may not recover cash and investments held by another party in the event of a financial failure. The Plan requires all securities to be held by a third party custodian in the name of the Plan. Securities transactions between the broker-dealer and the custodian involving the purchase or sale of securities must be made on a “delivery vs. payment” basis to ensure that the custodian will have the security or money, as appropriate, in hand at the conclusion of the transaction. Concentration of Credit Risk The Plan’s investment policy establishes limitations on portfolio composition by investment type and by issuer to limit its exposure to concentration of credit risk. The Board requires that Plan assets be invested with no more than 60% in stocks and convertible securities measured at cost or 70% of the Plan assets at market (fair) value. In addition, the Plan limits investment in common stock (equity investments) as follows: • No more than three percent of the Plan’s assets may be invested in the common or capital

stock of any single corporation.

• The Plan’s investment in the common stock of any single corporation shall not exceed three percent of such corporation’s outstanding common or capital stock.

No investment represents a concentration of 5% of more of net plan assets. Risks and Uncertainties The Plan has investments in a variety of investment securities. Investment securities are exposed to various risks, such as interest rate, market and credit risk. Due to the level of risk associated with certain investment securities, and the level of uncertainty related to changes in the value of investment securities, it is a least reasonably possible that changes in risks in the near term would materially affect balances and the amounts reported in the statement of plan net assets and the statement of changes in plan net assets.

TOWN OF LANTANA, FLORIDA

NOTES TO BASIC FINANCIAL STATEMENTS (Continued)

-35-

NOTE 3. PROPERTY TAXES Ad valorem taxes on property values are assessed as of January 1st and are levied the following October. Taxes are payable on November 1st, with discounts allowed of 1% to 4% if paid prior to March 1st of the following calendar year. All unpaid taxes on real and personal property become delinquent and subject to lien on April 1st. Real and personal property taxes are collected by Palm Beach County and remitted to the Town. State law permits Florida cities to levy a maximum of $10 per $1,000 (10 mills) of assessed taxable value for general government services. The Town levied taxes at a rate of 3.2395 mills, combined with Palm Beach County’s Fire/Rescue rate for the Municipal Service Taxing Unit (MSTU) of 2.95, leaving a margin of 3.8105 mills under the maximum possible assessment of 10 mills.

NOTE 4. RECEIVABLES

Receivables for the Town’s individual major funds and nonmajor funds in the aggregate, including the applicable allowances for uncollectible accounts as of September 30, 2009, are as follows:

Water and NonmajorGeneral Sewer Governmental

Fund Fund Funds TotalReceivables:

Accounts receivable 314,131$ 350,062$ -$ 664,193$ Intergovernmental 249,186 107,235 78,852 435,273

563,317 457,297 78,852 1,099,466 Less allowance for uncollectibles (4,680) (14,820) - (19,500)

Net total receivables 558,637$ 442,477$ 78,852$ 1,079,966$

NOTE 5. INTERFUND TRANSFERS

The following is a summary of transfers for the year ended September 30, 2009:

NonmajorGovernmental

Transfers Out Funds

General Fund 350,000$

Transfers In

Transfers are used to (1) move revenues from the fund with collection authorization to the fund servicing debt as debt service principal and interest payments become due, (2) move unrestricted general fund revenues to finance various programs that the government must account for in other funds in accordance with budgetary authorizations, including amounts provided as subsidies or matching funds for various grant programs.

TOWN OF LANTANA, FLORIDA

NOTES TO BASIC FINANCIAL STATEMENTS (Continued)

-36-

NOTE 6. CAPITAL ASSETS

The following summarizes capital asset activity for the fiscal year ended September 30, 2009:

Beginning EndingBalance Additions Deletions Balance

Governmental activities:Capital assets not being depreciated:

Land 110,367$ -$ -$ 110,367$ Construction in Progress - 49,427 - 49,427

110,367 49,427 - 159,794 Capital assets being depreciated:

Roads and streets 22,779,860 19,867 - 22,799,727 Buildings and improvements 5,409,569 1,540,355 (5,960) 6,943,964 Furniture, equipment and vehicles 4,477,245 543,069 (288,730) 4,731,584

Total capital assets being depreciated 32,666,674 2,103,291 (294,690) 34,475,275

Less accumulated depreciation for:Roads and streets (8,322,342) (908,988) - (9,231,330) Buildings and improvements (1,606,602) (186,650) 5,960 (1,787,292) Furniture, equipment and vehicles (3,233,465) (457,243) 288,730 (3,401,978)

Total accumulated depreciation (13,162,409) (1,552,881) 294,690 (14,420,600) Total capital assets being depreciated, net 19,504,265 550,410 - 20,054,675 Governmental activities capital assets, net 19,614,632$ 599,837$ -$ 20,214,469$

Business-type activities:Capital assets not being depreciated:

Land 4,300$ -$ -$ 4,300$ Construction in progress - 356,392 - 356,392

Total capital assets not being depreciated 4,300 356,392 - 360,692

Capital assets being depreciated:Plant and buildings 11,507,245 - (31,862) 11,475,383 Infrastructure 8,764,853 145,714 (230,830) 8,679,737 Equipment 981,271 29,545 (27,597) 983,219

Total capital assets being depreciated 21,253,369 175,259 (290,289) 21,138,339

Less accumulated depreciation for:Plant and buildings (4,308,603) (407,409) 31,862 (4,684,150) Infrastructure (5,315,351) (362,585) 230,830 (5,447,106) Equipment (692,167) (76,571) 27,597 (741,141)

Total accumulated depreciation (10,316,121) (846,565) 290,289 (10,872,397)

Capital assets being amortized:Intangible rights 3,080,157 - - 3,080,157 Less accumulated amortization (1,858,430) (123,849) - (1,982,279)

Total capital assets being amortized, net 1,221,727 (123,849) - 1,097,878 Total capital assets being depreciated

and amortized 12,158,975 (795,155) - 11,363,820 Business-type activities capital assets, net 12,163,275$ (438,763)$ -$ 11,724,512$

TOWN OF LANTANA, FLORIDA

NOTES TO BASIC FINANCIAL STATEMENTS (Continued)

-37-

NOTE 6. CAPITAL ASSETS (Continued)

Depreciation expense for the fiscal year ended September 30, 2009 was charged to functions/programs of the Town as follows: Governmental activities:

General government 41,334$ Public safety 259,150 Physical environment 1,056,370 Culture and recreation 196,027

Total depreciation expense – governmental activities 1,552,881$