concurrent session 1b: trends in p&c

TRANSCRIPT

Trends in P&CConcurrent Session 1B

25th Annual Insurance ConferenceWednesday, December 7, 2016

Partner and Business Leader, Property and Casualty Actuarial

Pierre Lepage

President and CEO, MSA Research Inc.

Joel Baker

Partner, Deal Advisory – M&A

Georges Pigeon

Senior Manager, Consulting Actuary

Houston Cheng

3© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Your thoughts on current trends that are likely to shape the future

Short Term Trends

Joel BakerPresident and CEO (MSA Research Inc.)

KPMG’s 25th Annual Insurance Issues Conference Dec 7, 2016

Overview of Trends, Opportunities and Challenges in the Canadian P&C insurance/reinsurance industry.

Joel Baker, CEO,MSA Research Inc. & CatIQ Inc.

WHO WE ARE AND WHAT WE DOMSA Research Inc. is a Canadian-owned, independent and impartial analytical research firm focused on the Canadian Insurance industry. MSA commenced operations in 2004.

De f in i t i ve i nsu rance i n fo rma t ion f o r i n te l l i gen t bus iness dec i s ions

PRODUCTS & SERVICES

2016 MSA Report P&C

MSA P&C and L&H Researcher SoftwareRelied on by the overwhelming majority of

players involved in the CDN market.

2016 MSA Benchmark Report P&C

2016 MSA Market Share Report P&C

2016 MSA Quarterly Report

CONFERENCESMSA organizes several significant insurance focused events throughout the year.

An intensive one-day financial conference focused on issues affecting actuarial, accounting, finance, analysis and investment professionals in the Canadian P&C insurance industry.

Bringing together an unparalleled gathering of professionals, expertise and timely content that represents the broad spectrum of the global cyber risk challenge.

Canada’s pre-eminent annual property & casualty insurance conference.

May 24, 2017Metro Toronto Convention

Centre

March 2-3, 2017Allstream Centre, Toronto

October 1-3, 2017Quebec City

OUTLINE

• Growth? Haves and Have Nots• Results before and after FMM• A Consolidating Market with Quirks• A Look at the Reinsurance Scene• CatIQ and a deeper look at Fort Mac• Summary and Discussion

OUTLINE

• Growth? Haves and Have Nots• Results before and after FMM• A Consolidating Market with Quirks• A Look at the Reinsurance Scene• CatIQ and a deeper look at Fort Mac• Summary and Discussion

WHERE’S THE GROWTH?

OUTLINE

• Growth? Haves and Have Nots• Results before and after FMM• A Consolidating Market with Quirks• A Look at the Reinsurance Scene• CatIQ and a deeper look at Fort Mac• Summary and Discussion

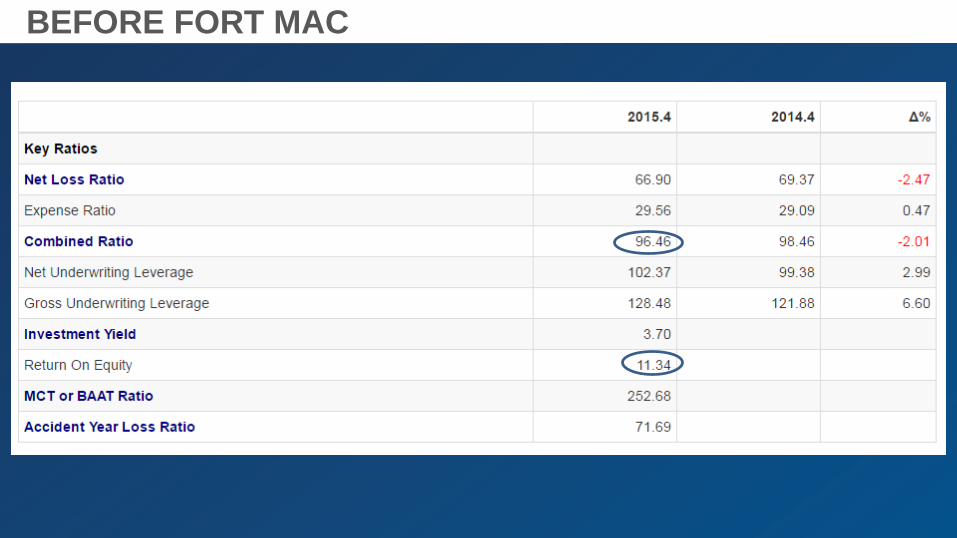

BEFORE FORT MAC

• DPW up 5.9%

• Claims Down 1%

• U/W Income up 137%

• Inv Inc. down 8%

• Net Income up 10%

BEFORE FORT MAC

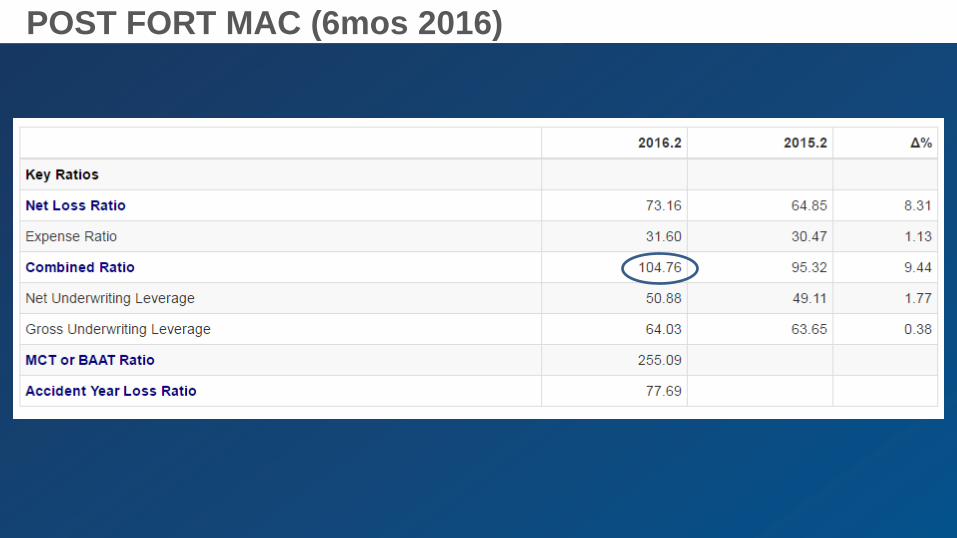

POST FORT MAC (6mos 2016)

• Claims Up 14%

• U/W Income $2+ billion negative swing.

• Inv Inc. down 30%

• Income wiped out.

POST FORT MAC (6mos 2016)

OUTLINE

• Growth? Haves and Have Nots• Results before and after FMM• A Consolidating Market with Quirks• A Look at the Reinsurance Scene• Regional Players Vs. National Writers• CatIQ and a deeper look at Fort Mac• Summary and Discussion

MARKET SHAREShifts since 2006

Lumpy consolidation

41.7

64.4

82.8

35.4

55.1

79.6

0

10

20

30

40

50

60

70

80

90

Top 5 Top 10 Top 20

2015 2006

TOP 5 COMPANIES

Companies Market Share Companies Market Share

Intact 13.9 Intact 9.8

ICBC 8.1 ICBC 8.3

Aviva 7.2 Aviva 7.5

Desjardins 7.2 Co-operators 5.1

TD 5.4 Economical 4.7

Total 41.7 Total 35.4

2015 2006

109 IS A CROWDParticipants in the Commercial Market

Intact Financial Corp First American Group Estrie-Richelieu Legacy General Ins. Co.Lloyd's Underwriters Lawyers' Professional Ind Red River Valley Mutual PEI MutualAviva Canada Group RBC Heartland Farm Mutual Electric Insurance Co.AIG Ins. Co. Can Old Republic Ins. Co. EGI Financial Holdings American Road Ins. Co.RSA Canada Stewart Title Guaranty Co Co-operative Hail Ins Co Industrial AllianceNorthbridge Financia Trisura Guarantee Ins. Co AEGIS MAX Canada Insurance CoZurich Ins Co Ltd. Millennium Ins Corp. COFACE Sompo Japan NipponkoaCo-operators Group Gore Mutual Ins Co Chicago Title Ayr Farmers' Mutual Ins. Genworth Fin Mort Ins Can TD Insurance Triton Insurance Company Jewelers Mutual Ins. Co.EIG Wynward Ins Group Sunderland Marine Ins Co Cherokee Ins CoChubb Canada Group Motors Ins Corp Portage la Prairie Mutual Omega General Ins CoICBC Ecclesiastical Ins. Commonwell Mutual Mennonite Mutual Fire InsTravelers Group Everest Tokio Marine and Nichido Poultry Ins Exch RecipGreen Shield Canada Arch Insurance Canada Ltd Western Surety Co. Protective Ins CoFM Global Peace Hills General Virginia Surety Co. Sentry InsWawanesa Mutual Ins. Co. Berkley Ins Co Allstate Canada Grp Kings Mutual Ins CoAllianz Global Risks US BCAA Mitsui Sumitomo Ins Algoma Mutual Ins CoLiberty Mutual Group Optimum General Grp Allied World Specialty Antigonish Farmers'American Bankers of FLA Axis Reinsurance Co. Ironshore Insurance Ltd. Clare Mutual Ins CoSGI CANADA Group HDI Global DAS Legal Protection Promutuel ReGuarantee Co of NA Great American Ins Co Sask Mutual Ins. Co. T.H.E. Ins CoCanada Guaranty Mortgage EULER Hermes Amer Credit Hartford Fire Ins Co Pictou County Farmers'Desjardins Group Int Ins Co Hannover Atradius Credit Insurance InnovAssurContinental Cas. Co. Mutual Fire Ins Co of B.C Technology Insurance Comp First North American InsMunich Re Canada OSBIE MEARIE CorePointe Ins CoCapitale Group NLFIC SSQ, Societe D'AssurancesXL Group Starr Insurance & Reinsurance Aspen InsuranceSwiss Re Canada Group BI&I Trillium Mutual Ins Co.

109 IS A CROWDParticipants in the Commercial Market

Intact Financial Corp First American Group Estrie-Richelieu Legacy General Ins. Co.Lloyd's Underwriters Lawyers' Professional Ind Red River Valley Mutual PEI MutualAviva Canada Group RBC Heartland Farm Mutual Electric Insurance Co.AIG Ins. Co. Can Old Republic Ins. Co. EGI Financial Holdings American Road Ins. Co.RSA Canada Stewart Title Guaranty Co Co-operative Hail Ins Co Industrial AllianceNorthbridge Financia Trisura Guarantee Ins. Co AEGIS MAX Canada Insurance CoZurich Ins Co Ltd. Millennium Ins Corp. COFACE Sompo Japan NipponkoaCo-operators Group Gore Mutual Ins Co Chicago Title Ayr Farmers' Mutual Ins. Genworth Fin Mort Ins Can TD Insurance Triton Insurance Company Jewelers Mutual Ins. Co.EIG Wynward Ins Group Sunderland Marine Ins Co Cherokee Ins CoChubb Canada Group Motors Ins Corp Portage la Prairie Mutual Omega General Ins CoICBC Ecclesiastical Ins. Commonwell Mutual Mennonite Mutual Fire InsTravelers Group Everest Tokio Marine and Nichido Poultry Ins Exch RecipGreen Shield Canada Arch Insurance Canada Ltd Western Surety Co. Protective Ins CoFM Global Peace Hills General Virginia Surety Co. Sentry InsWawanesa Mutual Ins. Co. Berkley Ins Co Allstate Canada Grp Kings Mutual Ins CoAllianz Global Risks US BCAA Mitsui Sumitomo Ins Algoma Mutual Ins CoLiberty Mutual Group Optimum General Grp Allied World Specialty Antigonish Farmers'American Bankers of FLA Axis Reinsurance Co. Ironshore Insurance Ltd. Clare Mutual Ins CoSGI CANADA Group HDI Global DAS Legal Protection Promutuel ReGuarantee Co of NA Great American Ins Co Sask Mutual Ins. Co. T.H.E. Ins CoCanada Guaranty Mortgage EULER Hermes Amer Credit Hartford Fire Ins Co Pictou County Farmers'Desjardins Group Int Ins Co Hannover Atradius Credit Insurance InnovAssurContinental Cas. Co. Mutual Fire Ins Co of B.C Technology Insurance Comp First North American InsMunich Re Canada OSBIE MEARIE CorePointe Ins CoCapitale Group NLFIC SSQ, Societe D'AssurancesXL Group Starr Insurance & Reinsurance Aspen InsuranceSwiss Re Canada Group BI&I Trillium Mutual Ins Co.

OUTLINE

• Intro to MSA• Growth? Haves and Have Nots• Results before and after FMM• A Consolidating Market with Quirks• A Look at the Reinsurance Scene• CatIQ and a deeper look at Fort Mac• Summary and Discussion

LICENSED REINSURERS RANKED BY GPW

Swiss Re General Reinsurance Corporation

Munich Re XL Reinsurance America Inc.

Hannover Rück SE Aspen Insurance UK Limited

Everest Re Toa Reinsurance Company of America

Promutuel Réassurance Caisse Centrale de Réassurance

SCOR Canada Reinsurance Company Mapfre Re Compania de Reaseguros, S.A.

Farm Mutual Reinsurance Plan Inc.American Agricultural Insurance Company

Partner Reinsurance Company of the U.S. Sirius America Insurance Company

Odyssey Reinsurance Company Munich Reinsurance America, Inc.

Transatlantic Reinsurance Company Catalina General Insurance Co.

Axis Reinsurance Company

CESSIONS TO NON-AFFILIATED AS A % OF GPW

6.66.2

5.6 5.7

6.5

5.9 5.85.6

5.4

7.7

4.94.6

4.2 4.34.6

3.93.7

3.53.3 3.2

1.7 1.61.4 1.4

1.82 2.1 2.1 2.1

4.5

1

2

3

4

5

6

7

8

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Total Registered UnRegistered

OUTLINE

• Intro to MSA• Growth? Haves and Have Nots• Results before and after FMM• A Consolidating Market with Quirks• A Look at the Reinsurance Scene• Regional Players Vs. National Writers• CatIQ and a deeper look at Fort Mac• Summary and Discussion

CATIQ INC.

Catastrophe Indices and Quantification Inc. delivers detailed analytical and meteorological information on Canadian natural and man-made catastrophes. Launched with the support of the Canadian insurance and reinsurance industry in 2014.

2016/2017 ADVISORY COMMITTEECatIQ is guided by an advisory committee

Joel BakerPresident & CEO,MSA Research Inc. & CatIQ

Michael BriseboisGlobal Head of Reinsurance,TD Insurance

Paul CutbushSVP Catastrophe Management,Aon Benfield Analytics

Cara LowVP, Corporate Actuarial andAppointed Actuary, WawanesaMutual Insurance Company

Paul A. MacDonaldSVP & Chief Claims Officer,RSA Insurance Group

Glenn McGillivrayManaging Director,ICLR

Balz GrollimundHead Treaty Underwriting,Swiss Reinsurance Company Canada

Carolyn RennieManaging Director,CatIQ

Sean RussellManaging Director,Guy Carpenter & Company Ltd.

Eric SteenEVP, Reinsurance,JLT Re

Chris RolSenior Policy Advisor, IBC

Rebecca WagnerAssociate Director, PredictionServices Operations - Central Region, MSC, Environment and Climate Change Canada

© 2016 Catastrophe Indices and Quantification Inc. (CatIQ). Not for redistribution.

$-

$1,000.00

$2,000.00

$3,000.00

$4,000.00

$5,000.00

$6,000.00

2008 2009 2010 2011 2012 2013 2014 2015 2016

Mill

ions

CatIQ’s Estimated Annual Insured Catastrophe Losses in Canada(2016 Data Includes CATs up to September 30, 2016 - Subject to Change)

NE EstimatedLosses

CAT Losses

Notable Event (NE) losses are

estimated between $10-$25M

An average event loss of $17.5M is

used

Canadian CAT Loss Estimates

Fort McMurray Wildfire – During (May 3rd)• 4:00 pm - Evacuations continue – only major road (absolute chaos). Unofficial reports of

fire spreading into Absand Heights area destroying homes and flames in industrial areas south of Fort McMurray

• 5:00 pm – Premier Rachel Notley addressed situation– Biggest fire-related evacuation in AB history – Potential impact greater than Slave Lake

• 5:30 pm – Reports of buildings, gas stations, hotels, trailers & homes on fire > local wind gusts 50 km/h + still SSW similar situations forecast Wed.

• 6:49 pm – Northern edge of fire growing fast, all of Fort McMurray under MANDATORY Evac. Except MacDonald Island, Saprae Creek & Airport

• 88,000 + people successfully evacuated• No fire related injuries or fatalities• Media frenzy

© 2016 Catastrophe Indices and Quantification Inc. (CatIQ). Not for redistribution. 27

Fort McMurray Wildfire ~ $3.8 B (CAD)

© 2016 Catastrophe Indices and Quantification Inc. (CatIQ). Not for redistribution. 28

May 2, 20160815 MDT

May 3, 20160715 MDT

May 4, 20160715 MDT

May 5, 20160815 MDT

May 6, 20160715 MDT

May 19, 20161245 MDT

© 2016 Catastrophe Indices and Quantification Inc. (CatIQ). Not for redistribution. 29

© 2016 Catastrophe Indices and Quantification Inc. (CatIQ). Not for redistribution.

CatIQ’s 90 Day FMM Wildfire Loss Estimate180 day update released on Dec 1 to CatIQ subscribers

© 2016 Catastrophe Indices and Quantification Inc. (CatIQ). Not for redistribution. 31

~$3.8 B (CAD)

BACK OF NAPKIN LOGIC

• Assume $2 billion of FMM losses borne by reinsurers. • Years for reinsurance market to ‘earn’ this back assuming COR of

90:• Licensed NPE in 2015 $1.65B -> U/W income @90CR = $165

Million• Proportion of reinsurance business in AB = 10.3%. Ie $17 Million

Years to ‘Earn Back FMM’ :Canada: 12Alberta: 117.6FMM: Next Ice Age

Global Leaders’ Panel

Peter HearnPresident & CEO,Guy Carpenter &

Company Ltd.

John CharmanChairman & CEO,

Endurance Speciality Holdings Ltd.

Mark CloutierGroup CEO,

Brit Insurance Ltd.

Mike SapnarCEO,

Transatlantic Re

Laura TaylorManaging Partner & CFO,

Nephila Capital

Quoting VJ Dowling –Is it Diversification or Diworseification?

• Fort Mac may have put paid to Canada’s vaunted status as a safe diversifier for the global reinsurance market.

• https://youtu.be/uSHhkXiA8ZU

OUTLINE

• Growth? Haves and Have Nots• Results before and after FMM• A Consolidating Market with Quirks• A Look at the Reinsurance Scene• CatIQ and a deeper look at Fort Mac• Summary

CHALLENGES & IMBALANCES

• Volatility brought on by Cats and challenges in auto lines. • Heavy reliance on the $27 billion auto line (47%+ of

primary volume) – a losing game in the long run. • Primary rates not keeping pace w/escalating cat losses. • Consumers dangerously underinsured for EQ/Flood.• Extreme competition – battle for distribution• No formal federal backstop yet

OPPORTUNITIES

• Increasing need for property coverages, reinsurance and ILS solutions to cope with increasing frequency and severity; coverage gaps; public sector challenges.

• Growth of flood insurance

• Growth of Cyber

• Explosion of InsurTech

Thank You

Joel [email protected]. 416-368-0777 x21C. 416-577-6557@Joel_Baker1

www.msaresearch.comwww.catiq.com

Medium Term Trends

Houston ChengConsulting Actuary and Senior Manager (KPMG)

6© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

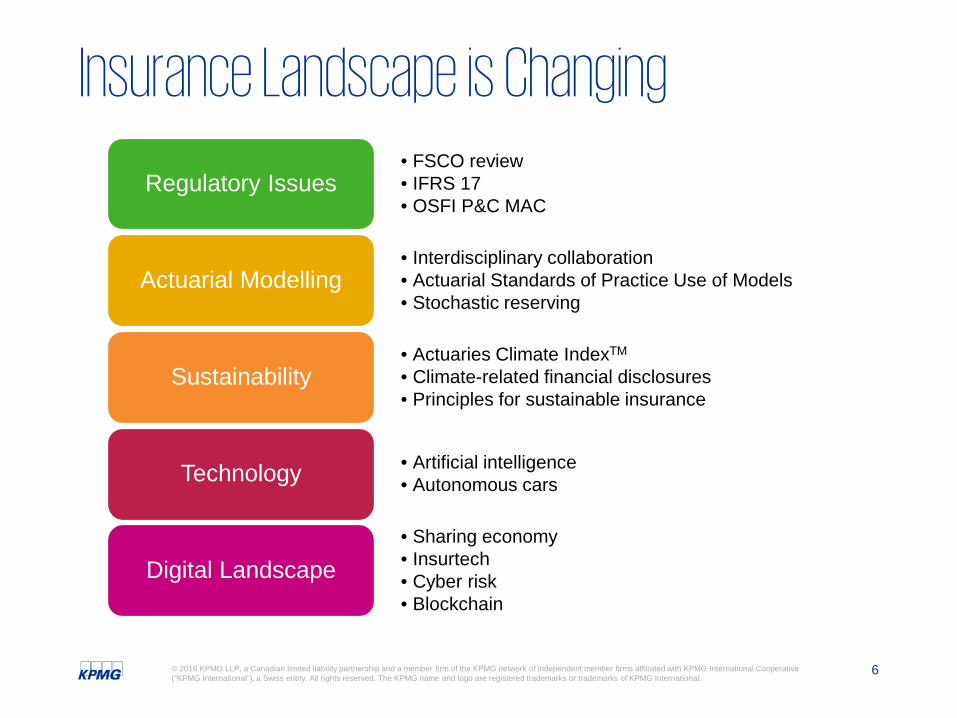

Insurance Landscape is Changing• FSCO review• IFRS 17• OSFI P&C MAC

Regulatory Issues

• Interdisciplinary collaboration• Actuarial Standards of Practice Use of Models• Stochastic reserving

Actuarial Modelling

• Actuaries Climate IndexTM

• Climate-related financial disclosures• Principles for sustainable insurance

Sustainability

• Artificial intelligence• Autonomous carsTechnology

• Sharing economy• Insurtech• Cyber risk• Blockchain

Digital Landscape

7© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Regulatory Issues

• Recommended new, independent and integrated regulator called the Financial Services Regulatory Authority (FSRA)

FSCO review

• Expected effective date of January 1, 2021• There will be impact to P&C insurers

IFRS 17

• Guidance provisionally entitled Criteria for the Use of Internal Models in the Determination of Regulatory Capital for Insurance Companies

• OSFI anticipates issuing guidance for consultation in 2017

OSFI P&C MAC

8© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Actuarial Modelling

• With advancements in data analytics and technology, actuaries will need to collaborate with professionals from different backgrounds

Interdisciplinary collaboration

• Comments on exposure draft closed• Expected to be adopted early 2017

Actuarial Standards of Practice on Use of Models

• Will play a role in IFRS 17

Stochastic reserving

9© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

SustainabilityActuaries Climate IndexTM

Joint effort by various North American actuarial organizations

Objective quarterly measure of changes in extreme weather frequency and sea level

Help educate public, policymakers, and actuaries about increased frequency of climate extremes

Actuaries Climate IndexTM

Ref

eren

ce P

erio

d S

tand

ard

Dev

iatio

ns

Source: www.actuariesclimateindex.org

10© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

SustainabilityFinancial Stability Board: Task Force on Climate-related Financial Disclosures

• G20 asked FSB to review how financial sector can take account of climate-related issues

Why

• Task Force chaired by Michael Bloomberg

Who

• Provide clear recommendations for preparers to disclose consistent information on climate-related financial risks

What

Physical Risks•Financial impacts of physical effects of climate change

Liability Risks•Financial impacts of legislation to limit carbon emissions, and potential for liability from contributing or failing to act on climate change

Transitional Risks•Financial impacts of failing successfully transition to low carbon economy

Additional Information: www.fsb-tcfd.org

11© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

SustainabilityPrinciples for Sustainable Insurance

The United Nations Principles for Sustainable Insurance (PSI) serve as a global framework for theinsurance industry to address environmental, social and governance (ESG) risks and opportunities.

• Embed in decision-making ESG issues relevant to insurance business1

• Work with clients and business partners to raise awareness of ESG issues, manage risk and develop solutions2

• Work with governments, regulators and other key stakeholders to promote widespread action across society on ESG issues3

• Demonstrate accountability and transparency in regularly disclosing publicly progress in implementing the Principles4

Additional Information: www.unepfi.org/psi/

12© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

TechnologyArtificial Intelligence

Improve efficiency

• Beyond textual data• Use Multimedia data• e.g., analyze

customer interactions

Reducecosts

• Increase automation• Improve accuracy• e.g., reduce claims

processing time

Gain competitive advantage

• Provide better customer service

• Simplify claim and underwriting process

Machine learning has changed other industries – insurance is primed to betransformed by deep learning

13© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

TechnologyAutonomous Cars – Potential Business Models

Illustrative Future State Business Models

Entity Scenario A Scenario B Scenario C Scenario D

Provide driving and vehicle data to insurers

Become distributor of insurance for a selected set of carriers

Act as an insurance company with many functions outsourced

Become a fully integrated insurance company

Strategic Angle Telemetry data Brand, customerconnectivity Product advantage Product advantage

Revenue Model Fees Commissions

Underwriting profit and investment income (annuity)

Vehicle and parts sales

Underwriting profit and investment income (annuity)

Vehicle and parts sales

License data fromOEMs to underwrite policies

Form alliances with OEMs

Serve as third-party administrators - for example, current insurers could process the claims of the OEMs

Transform business model to compete with new entrants

Expand into new products and services

OEM

sIn

sure

r

14© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Digital Landscape

Digital

Sharing Economy• Possessions• Trading• Knowledge/experience• Services• Lending/funding

Insurtech•Underwriting•Claim handling•Distribution• Internet of Things• Peer-to-peer

Cyber Risk•Risk to insurers•Risk to policyholders• Large and small scale•Organized attack

Blockchain

15© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Digital LandscapeBlockchain – Relevance to key insurance trends

Insurance trend/ topic Blockchain relevance

1 Insurance industry ripe for disruption Blockchain is a technology that could drive / enable disruption

2 Rise of automation and shift to a digital labor force

Blockchain raises the question of whether a paradigmshift in transaction processing is better than automating an existing process

3 Demographic changes with less understanding and lower demand for insurance products among millennial generation

Blockchain can help lower transaction costs, reducing cost of insurance for cost-conscious buyers

4 Customer expectations driven by experiences with platforms like Amazon, Apple, Uber, etc.

Blockchain can help drive quicker transaction processing for claim payment, etc. that can enable a better customer experience. Blockchain-enabled platforms can reduce barriers to entry for new competitors

5 Rise of the on-demand economy with new entrants already capturing market share

Blockchain can further enable low-cost transactions with near real-time confirmation

6 Rise of “social insurance” and peer-to-peer insurance

Blockchain helps eliminate the need for intermediaries to enable financial transactions

7 Legacy infrastructure and process challenges where transaction costs continue to comprise a large portion of premiums

Blockchain could drive a complete overhaul of existing transaction processing, driving down transaction costs

Mergers and Acquisition

Georges PigeonPartner, Deal Advisory (KPMG)

17© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Why undertake M&A?

Enter a new geographic market 1

Provide a new product and service 2Access a new distribution channel to reach customers 3

Equip operations with new tools 4

Capture new customers5

18© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

The Canadian perspective Sustained number of transactions in insurance

Includes as targets:

– Underwriters

– Brokers/MGAs

Based on information extracted from KPMG’s Financial Services M&A Digest January 2013 to October 2016

– Insurance services: loss adjustors / claims management

– Employee / HR benefit distributors and servicers

12 12 13 1311 11

15 14

19

26

12 11

16

8

16

0

5

10

15

20

25

30

Q1-13 Q2-13 Q3-13 Q4-13 Q1-14 Q2-14 Q3-14 Q4-14 Q1-15 Q2-15 Q3-15 Q4-15 Q1-16 Q2-16 Q3-16

19© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

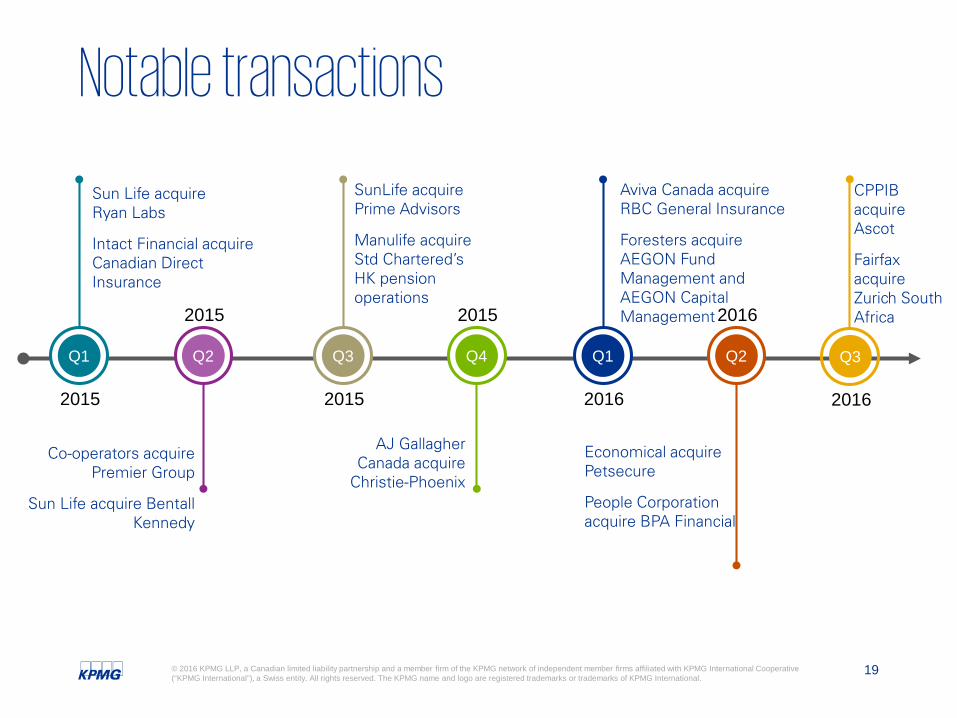

Notable transactions

SunLife acquire Prime Advisors

Manulife acquire Std Chartered’sHK pension operations

Sun Life acquire Ryan Labs

Intact Financial acquire Canadian Direct Insurance

Co-operators acquire Premier Group

Sun Life acquire BentallKennedy

AJ Gallagher Canada acquire

Christie-Phoenix

Q1 Q2 Q3 Q4 Q1 Q2

2015

2015

2015

2015 2016

2016

Aviva Canada acquire RBC General Insurance

Foresters acquire AEGON Fund Management and AEGON Capital Management

Economical acquire Petsecure

People Corporation acquire BPA Financial

Q3

2016

CPPIB acquire Ascot

Fairfax acquire Zurich South Africa

20© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Profile of buyer remains concentrated…

Underwriters:– Aviva Canada– Fairfax Holdings, mostly overseas– Sun Life Canada

Distributors:– Hub International – Brokerlink– People Corporation– Co-Operators Group

…with non-traditional buyer profiles increasingly present

Private Equity/pension plan

5%

15%Service Provider25%

Underwriter

55%Distributor

Source: KPMG’s Financial Services M&A Digest January 2016 to October 2016

21© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Profile of targets remains concentrated…

Underwriters:– 67% cross-border– Continued consolidation in

Canada RBC General Insurance Petsecure

Distributors:– Local and regional players

…heavily focused on distribution

Source: KPMG’s Financial Services M&A Digest January 2016 to October 2016

Asset Management

7%

18%Service Provider

20%Underwriter

55%Distributor

22© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

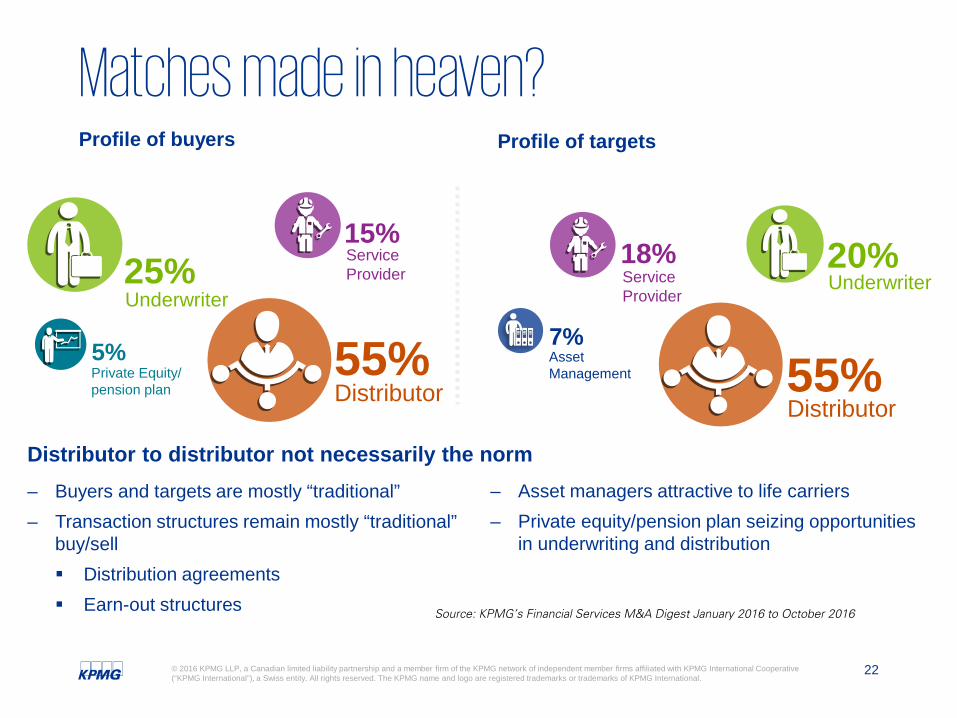

Matches made in heaven?Profile of buyers Profile of targets

– Buyers and targets are mostly “traditional”– Transaction structures remain mostly “traditional”

buy/sell Distribution agreements Earn-out structures

– Asset managers attractive to life carriers– Private equity/pension plan seizing opportunities

in underwriting and distribution

Distributor to distributor not necessarily the norm

Asset Management

7%

18%Service Provider

20%Underwriter

55%Distributor

Private Equity/pension plan

5%

15%Service Provider25%

Underwriter

55%Distributor

Source: KPMG’s Financial Services M&A Digest January 2016 to October 2016

23© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Drivers & catalysts of Canadian M&A activity

Succession planning01

Capital deployment / redeployment02

Suboptimal market positioning and/or profitability03

Wealth management04

05 Fintech / InsurTech

Questions and Answers

25© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Questions and Answers (1)

From the trends discussed by Houston, do you see any that could influence the level

of M&A activities?

26© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Questions and Answers (2)

How are smaller / regional players coping with recent and future challenges?

27© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Questions and Answers (3)

Many executives think it is very important to “keep pace” in order for their

companies to stay relevant.

Can you tell us how some companies are approaching the need to “keep pace”?

28© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Final Thought

If you were a member of a management team or of a Board, what would be the

P&C Industry trend you would follow the most in the next year?

Contact usPierre LepagePartner and Business Leader, Property and Casualty [email protected] 777 3630

Georges PigeonPartner, Deal Advisory – M&[email protected] 840 2178

Houston ChengSenior Manager, Property and Casualty [email protected] 777 8364

kpmg.ca

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. 13673

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.