conference report - inclusiveinsuranceasia.com report_microtakaful...2014 microtakaful conference...

TRANSCRIPT

2014 Microtakaful

Conference Indonesia

24 April 2014 / Jakarta

Conference Report

Hosted by

Conference report edited by

AFC Consultants International, Bonn / Germany

Table of content

1. Acknowledgements .................................................................................................... 4

2. Profile of speakers ..................................................................................................... 4

3. Introduction ...............................................................................................................12

4. Overview of the Conference Agenda .........................................................................12

5. Opening Address ......................................................................................................14

6. Keynote Address .......................................................................................................15

7. Session 1: Rationale and regulatory basis of microtakaful market development ........15

8. Session 2: Key findings and recommendations of microtakaful market study in

Indonesia ..................................................................................................................17

9. Session 3: Response to the market study – industry’s perspective and current

practice .....................................................................................................................21

10. Session 4: Response to the market study – role of support institutions .....................23

11. Session 5: Response to the market study – regulators’ perspective ..........................24

12. Synthesis ..................................................................................................................25

13. Closing Address ........................................................................................................31

List of Abbreviations

AASI Asosiasi Asuransi Syariah Indonesia engl.: Indonesian Shariah Insurance Association

BCBS Basel Committee on Banking Supervision BMT Baittul Maal wa Tamwil BMZ Das Bundesministerium für wirtschaftliche Zusammenarbeit

und Entwicklung engl.: Federal Ministry for Economic Cooperation and Deve-lopment

CSR Corporate Social Responsibility FISC Financial Inclusion Subcommittee GDP Gross Domestic Product GIZ Deutsche Gesellschaft für Internationale Zusammenarbeit

engl.: German Society for International Cooperation IAIS International Association of Insurance Supervisors IFSB Islamic Financial Services Board IOSCO International Organization of Securities Commissions JAMKESMAS Jaminan Kesihatan Masyarakat MFI Microfinance Institution MIS Management Information System MoU Memorandum of Understanding MUI Majlis Ulama Indonesia

engl.: Indonesian Ulema Council NBFI Non-bank financial institutions NGO Non-governmental organization OJK Otoritas Jasa Keuangan

engl.: (Indonesian) Financial Services Authority PPP Private Public Partnership RFPI Asia Regulatory Framework Promotion of Pro-poor Insurance

Markets in Asia SAC Sharia Advisory Council UAE United Arab Emirates

4

1. Acknowledgements

The Microtakaful conference was proud to

unveil the findings of the „Market Assess-

ment on Microtakaful in Indonesia“ com-

missioned by the GIZ RFPI Asia. We sincere-

ly thank and appreciate the ongoing commit-

ment of OJK in proactively engaging stake-

holders in developing the market of inclusive

insurance for the poor and Muslim population

in Indonesia. We equally thank AASI for the

unwavering effort in convincing a broad num-

ber of (micro)takaful providers and intermedi-

aries that participated in the market assess-

ment.

Our heartfelt appreciation to Muliaman D.

Hadad and Shaifie Zein, respective chairman

of OJK and AASI, for gracing the conference

and putting across the message that the

highest officials of OJK and AASI are behind

the initiatives of promoting inclusive insur-

ance in Indonesia.

We are thrilled to express our thanks and

appreciation to Mr. Moch Muclasin of OJK

and Ms. Srikandi Utami of AASI who are fully

supportive and who accompanied GIZ-RFPI

Asia in the content and logistics preparations

which lead to the successful implementation

of the market study and the conference; both

events are considered very important mile-

stones in Indonesia.

Some of the feedback of the conference were

„there was a good mix of resources persons“

and „all were fully engaged and enthusiastic

to share knowledge and experience“. We

deeply thank all the moderators, speakers

and panel of reactions whose names are

prominently identified in the conference

agenda on page 5. Thank you all for your

unselfish contributions in making the 1st Mi-

crotakaful Conference Indonesia a big suc-

cess.

Our sincere appreciation goes also to the

GIZ-RFPI team and the admin staff of GIZ

Jakarta office for the efficient logistical sup-

port. And finally a special thank you goes to

Dr. Antonis Malagardis, GIZ-RFPI Program

Director, for his leadership and patience in

making this conference successful with high

quality.

2. Profile of speakers

Antonis Malagardis

Program Director, RFPI

Asia

Deutsche Gesellschaft

für Internationale Zu-

sammenarbeit (GIZ) GmbH Opening

Address and Panel Reactor Session 1

Dr. Antonis Malagardis joined GIZ in 2009 as

program manager of the Microinsurance In-

novations Program for Social Security

(MIPSS) in the Philippines. In January 2013

he was nominated Program Director of a

BMZ funded regional Program on Regulatory

Framework Promotion of Pro-poor lnsurance

Markets in Asia' (RFPI Asia), which aims to

advice insurance regulators/supervisors in

selected countries in Asia on inclusive insur-

ance, strengthen the capacity development of

their staff and enhance knowledge sharing on

insurance for the low-income persons with

the support of the ADB and the global part-

nership of 'Access to lnsurance Initiative'

(A2ii) among other institutions. His assign-

ments as advisor in 19 countries covered risk

management, social insurance, pension fi-

nance, health finance, public-private partner-

ships (PPP), microfinance and microinsur-

ance and lately climate finance schemes at

the policy design, supervision and product

development level.

Born in Athens Greece, studied law and eco-

nomics at the University of Athens and re-

ceived his PhD in Berlin in the field of Institu-

5

tional Economics on the topic of 'Sovereign

risk and insolvency of states' (1989).

Dante Oliver Portula

Senior Advisor- Regional

Policy, RFPI Asia Deut-

sche Gesellschaft für In-

ternationale Zusammen-

arbeit (GIZ) GmbH

Mr. Portula has been working closely with the

Department of Finance, the lnsurance Com-

mission and other financial regulators in the

Philippines for more than five years. His sup-

port to these government agencies led to the

development of microinsurance regulatory

framework and the microinsurance national

strategy, including the establishment of a

roadmap to financial literacy on microinsur-

ance and alternative dispute resolution

mechanisms for microinsurance. Currently,

Portula collaborates with various Philippine

associations of insurance companies and the

MFls in developing innovative Microinsurance

products and on setting up risk-based capital

framework and microinsurance perforrnance

standards.

As senior advisor in GIZ, with more than 18

years of microfinance experience in countries

in Southeast Asia , Portula also handles poli-

cy engagements in Nepal, Indonesia and

Mongolia on inclusive insurance market de-

velopment with insurance supervisors and

insurance associations . Portula has intensive

experience in public and private stakeholders'

collaboration. His recent training is on Stake-

holders' Dialogue from the Collective Leader-

ship Institute (CLI), Germany.

Nick Thornton.

Lead Consultant, Mi-

crotakaful Market Study in

lndonesia Speaker

Session 2

Mr. Thomton's expertise is in microfinance

and economic development. Recent work

have brought him to areas surrounding Ban-

da Aceh with the local partner IP2M (Institut

Pelatihan & Pengembangan Masyarakat), or

Institute for Training & Community Develop-

ment. He managed the local microfinance

program, integration of economic develop-

ment activities, and developing financial liter-

acy training modules.

Mr. Thornton has completed the lslamic Mi-

crofinance Manager course through the Al-

Huda Center of lslamic Banking & Economics

of Pakistan, and a course on SCA promotion

through the Chalmers Center for Economic

Development.

Mr. Thornton graduated with honors from

Covenant College in Georgia, USA with a

double major in Economics & Community

Development.

Zuriah Abdul Rahman

Microtakaful Expert and

Consultant to RFPI Asia /

AFC Consultants Interna-

tional Presenter Session 2,

Panel Reator Session 5 and

Synthesis

A professor, researcher, author and consult-

ant, Rahman is well educated and experi-

enced in Islamic insurance and risk manage-

ment both in local and international contexts.

Her appointments include program head for

lnsurance & Risk Management, head for Risk

6

Management Center, and director of the Ar-

shad Ayub Graduale Business School, UiTM.

She also serves in the accreditation panel for

Finance Accreditation Agency in Malaysia.

She has authored and published several

books and Journals such as Takaful: 'The

21st Century lnsurance Innovation', Wealth

Management in Islam.

Ms Abdul Rahman completed her Ph.D. in

Risk Management from Universiti Utara Ma-

laysia/ University of Memphis, USA. She fin-

ished her MBA and bachelor's degree in

Business Administration in Insurance from

Bowling Green State University, Ohio, USA.

Moch Muchlasin

HeadDirectorate of Sharia

NBFls, OJK

Moderator Session 2 and

Panel Reactor Session 5

Mach Muchlasin graduated from the Universi-

tas lndonesia with a Bachelor of Economics

degree in Accounting. He studied manage-

ment and employment relation in School of

lndustrial Relations and Organization Behav-

iour (IROB) at the University of New South

Wales (UNSW}-Sydney, Australia and com-

pleted his Master of Commerce degree in

2004.

He worked in Directorate General of Financial

lnstitutions - Ministry of Finance on various

roles as analyst, examiner and enforcement

officer between 1994 and 2006 prior to the

establishment of Capital Market and Financial

lnstitutions Supervisory Agency

(BapepamLK) in 2006. He has been involved

in government guarantee scheme project

(2004-2005) !hat lead to the establishment of

lndonesian Deposit lnsurance Corporation

(IDIC) in 2005.Also,he was

involved in drafting process of OJK Law in

2006-2011.

Currently, Muchlasin is the director of Sharia

Non-Bank Financial lnstitutions, lndonesia

Financial Services Authority. He is responsi-

ble for coordinating Task Force on Microin-

surance Development since 2013 with the

main task to develop and promote microin-

surance and microtakaful in lndonesia.

Muliaman D. Hadad

Chairman of Board of

Commissioners OJK

Keynote Address

Muliaman D. Hadad,

PhD, currently serves as

Member of Board of Commissioners - lndo-

nesia Financial Services Authority (OJK) as

well as Chairman of Board of Commissioners.

Previously, he was the Bank Indonesia Depu-

ty Governor in 2006 and was re-elected for

the second term in 2011.

He graduated from Faculty of Economics at

University of Indonesia in and continuing his

Master's degree at John F. Kennedy School

of Government of Harvard University in Mas-

sachusetts, USA and earned a Master of

Public Administration degree one year later.

He has a Ph.D. degree in Business and Eco-

nomics from Monash University in Melbourne,

Australia.

Hadad is active as Head of Indonesian Sharia

Economic Community and is a lecturer at

several universities, and was once in charge

as Head of Alumni Association of Faculty of

Economics in 2007-2010. He is the former

Secretary General of Central Committee for

Indonesian Association of Economists or ISEI

(2003-2006 and 2006-2009)

7

Muhammad Faried

Head Statistics Depart-

ment AASI

Moderator Session 3

Faried is the product owner

and head product Underwriter of Sharia Busi-

ness at PT Asuransi Central Asia since 2004.

From 1997, he held significant post at PT

Asuransi Central Asia. Also, he is the head of

Statistics Department at AASI. Faried com-

pleted short course of Asia Future Leadership

at NUS Singapore in 2013.

Mohammad Shaifie Zein

Chief Executive Officer - PT

Reasuransi Nasional lndo-

nesia Chairman, Asosiasi

Asuransi Syariah lndonesia

(AASI)

Opening Address

Zein is the current chairman of Asosiasi

Asuransi Syariah Indonesia (AASI). His wide

range of experience in banking and insurance

include respected posts in PT Binagriya

Upakara General lnsurance and PT Reasur-

ansi Nasional lndonesia as CEO. Further-

more, he is a trainer and speaker in fields of

finance and banking. He has taken eligibility

from lslamic lnsurance Program and Financial

Planning Standards Board (FPSB).

Zein graduated from Glasgow Caledonian

University, Scotland-UK.

Srikandi Utami, Vice-

chairperson, AASI Vice

President and Head of

Shariah

PT Sun Life Financial

lndonesia

Moderator Session 3

Utami has worked in the life insurance indus-

try for more than 20 years, with a particular

focus on marketing management. The past

eight years were spent gaining experience in

developing takaful business in several multi-

national companies .

As Vice President and Head of Shariah at PT

Sun Life Financial Indonesia, Utami is re-

sponsible for developing individual and

bancassurance takaful business through the

distribution channels of agency and partner

distribution and build brand takaful image.

She is also responsible for developing and

delivering innovative products for each distri-

bution channel, standard of procedures and

services .

Utami is active in the lndonesia Shariah

lnsurance Association, task force micro in-

surance Indonesia, lslamic Center Forums of

Indonesia to develop economic and business

to lslamic center communities across Indone-

sia and in Shariah Economy Society to build

standard of competency of human resources

for Islamic institution. Her education back-

ground includes Marketing Management and

professional degrees in insurance and taka-

ful.

8

Kartina Md Ariffin, member of

the Secretariat Technical &

Research

lslamic Financial Services

Board (IFSB)

Speaker Session 1 and Panel

Reactor Session 5

Kartina Md Ariffin has 15 years of experience

in the takaful industry. Currently, she is the

project manager for the IFSB's Working

Group for Guiding Principles for Retakaful

(lslamic Reinsurance) Undertakings as well

as the IFSB's Microtakaful Joint Working

Group with the International Association of

lnsurance Supervisors (IAIS). She is respon-

sible for the development of a takaful pruden-

tial framework and facilitated the implementa-

tion of the takaful standards and guidance

notes.

Kartina was attached to Malaysia's Etiqa

lnsurance & Takaful (previously known as

Takaful Nasional) and Syarikat Takaful Ma-

laysia Berhad, and gained vast experience in

corporate planning initiatives. She has shared

her wide range experience as speaker in in-

ternational takaful-related conferences and

seminars. Kartina graduated with a bachelor's

degree in Actuarial Science from University of

Wisconsin, Madison, United States in 1998.

She received her Master in lslamic Finance

(MIF) INCEIF from The Global University of

lslamic Finance in 2013.

Agus Haryadi,

Commissioner, TAKMIN

(network of Mfls distributing

takaful) and ASyKi

(microtakaful broker)

Panel Reactor Session 3

Haryadi, a takaful expert, is a recognized

fellow of lslamic lnsurance Society (FllS), an

associate of Society of Actuaries of lndonesia

(ASAI) and the Ajun Ahli Asuransi lndonesia -

Jiwa (AAAl-J).

He has vast experience in microtakaful insur-

ance and presently involved in distinguished

posts as microtakaful advisor for PT. AJS

Amanahjiwa Giri Artha, as part of the lslamic

lnsurance Working Group, National Shariah

Board - MUI, as member of Shariah Supervi-

sory Board of BNI Life, Shariah Supervisory

Board of Capitalinc Multifinance, and Shariah

Supervisory Board of Amanah Multifinance.

Haryadi is the current chairman of Tazkia

Cendekia 1 foundation/Sekolah Tinggi

Ekonomi Islam Tazkia. His work is balanced

with further training and workshops, with re-

cent participation to ICMIF DEVELOPMENT

WORKSHOP "Microinsurance", Eureka Con-

ference Centre, in Zeist, Netherlands

He completed his bachelor's degree in Math-

ematics from the Institute Technology Ban-

dung in 1988.

lbnu Hasyim

Director of Operation and

Actuary PT Avrist

Panel Reactor Session 4

Mr. Hasyim is currently re-

sponsible for Actuary, Oper-

ation and Product development in Avrist As-

surance, lndonesia as part of Board of Direc-

tors. He has worked intensively to develop

takaful business in AVRIST with some of

strategies in product development, building

distribution channels and the operational ac-

tivities.

He has more than 14 years in industry, in-

cluding some experienced in multinational

actuarial consultant. He has mostly spent the

experienced in life insurance industry. He has

certified as fellowship actuary by Society of

Actuary in lndonesia (PAI). He completed his

Actuarial studies at the University of Indone-

sia.

9

Zainal Abidin Mohd. Kas-

sim,

FIA, FASM, ASA Senior

Partner

Actuarial Partners Malay-

sia

Panel Reactor Session 4

Zainal is the Senior Partner at Actuarial Part-

ners Consulting Sdn Bhd. He has been a

consulting actuary with the company since

1982.• His consulting experience spans the

full spectrum of actuarial services including

life and P&C and health insurance consulting,

family and P&C and health takaful consulting,

retirement benefit consulting, social security

consulting and investment consulting.

Zainal' s experience in Takaful started in

1985 when he was appointed as actuary to

the first Takaful Operator in Malaysia. He has

extensive experience in the design and pric-

ing of takaful products, including family, P&C

and health takaful. He has been involved in

strategic analysis and setup of takaful and

retakaful operators in Asia, Africa and Eu-

rope. As one of the first of the small number

actuaries working in takaful and retakaful, he

has been on the forefront of the technical

development of various takaful contracts and

has interacted with many Sharia scholars on

the practice of takaful.

He has written many articles and spoken at

numerous conferences globally on his expe-

rience with the development of takaful. He is

a Fellow of the Institute of Actuaries of the

UK, Fellow of the Actuarial Society of Malay-

sia and an Associate of the Society of Actuar-

ies in the USA and is a past president of the

Acturial Society of Malaysia.

lsmi Kushartanto

Executive Director

Economic Shariah Com-

munication Center

Panel Reactor Session 4

Kushartanto is the current

executive director of Economic Shariah

Communication Center - Pusat Komunikasi

Ekonomi Syariah (PKES). PKES has an

lslamic Economic Movement program, the

Gerakan Ekonomi Syariah (Gres!) a national

movement and lslamic economic socialization

icon in Indonesia. Through partnerships, he

develops his own business in the field of Fi-

nancial Advisory, Green Energy and New

Media.

Kushartanto has 17 years of work experience

in the Bank Ekspor lmpor lndonesia (after a

merger Bank Mandiri). He held significant

posts in credit field plantation, corporate cred-

it, and credit recovery. Furthermore, he

worked in some of the lslamic Bank, Bank

Syariah Mandiri as a director, Bank lnter-

nasional lndonesia (Bll), Perrnata Bank and

Bank (BNI) with the position as head for the

past eleven years.

Kushartanto completed his MBA from the

University of Colorado, Denver, USA in 1993

and graduated from the Faculty of Agricul-

ture, Bogor Agricultural University, Depart-

ment of Agronomy in 1982.

Abdul Majid - Panelist

Director of Cooperative

BMT UGT Sidogiri Pasuru-

an

Panel Reactor Session 3

For almost nine years, Mr

Abdul Majid has managed and developed

the Islamic microfinance institutions namely

Cooperative UGT Sidogiri BMT which offers

10

Islamic saving and loan products . His is ex-

perienced in the field of Islamic microfinance

in general, but especially in the field of sav-

ings and loans.

He has worked as sharia supervisor of

INKOPSYAH (Parent Cooperative Sharia) /

Jakarta from 2008 to 2014, as well as coordi-

nator of Partners Bank Financial Consultant

(KKMB) BI in Malang since 2004.

In 2008 Mr Majid graduated from law faculty

of Al Aqeedah University Jakarta and Eco-

nomic Education at Islamic University of Ma-

lang. Furthermore Mr Majid completed sever-

al Islamic finance trainings among others an

Islamic banking training conducted by LPPI

Jakarta.

Ir. Dumoly F Pardede,

Deputy Commissioner,

Non-Bank Financial lnstitu-

tions Supervision lndone-

sia FSA

Closing Address

Pardede began his career as a government

official in the Directorate of Investment

Funds, Directorate General of Monetary Af-

fairs- Ministry of Finance in 1989. During the

25 years of his career, he held many posi-

tions in the Directorate General of Financial

Institutions and in Capital Market and Finan-

cial lnstitutions Supervisory Board - Ministry

of Finance, the predecessor of currently Fi-

nancial Services Authority (OJK).

His various roles span from as examiner,

reviewer power development financial institu-

tions and most recently as head of the bu-

reau.

In addition, he also serves as chairman of the

audit committee in PN Gas and Deposit

lnsurance Agency . He currently serves as

Chief of the Bureau of Pension Funds, Capi-

tal Market Supervisory Agency and Financial

Institution.

He has a Master Business Administration

(MBA) for Finance & Accountancy from

Cleveland State University (CSU).

Aprillina Triyono - Panelist

Technical Director

PT Asuransi Tri Pakarta

Ms Aprillina has been active in

the Indonesian Insurance In-

dustry for more than 30 years. Starting her

career in Tugu Pratama Indonesia Insurance

Company in 1982, she has been responsible

for various classes of insurance business.

She left her position in Tugu Pratama Indo-

nesia as the Head of Reinsurance Division

before she was appointed Director of PT.

Asuransi Dharma Bangsa in 2001.

In 2003, she joined PT. Asuransi Tri Pakarta

which gave her responsibilities to handle

technical matters. The Company then ap-

pointed her as Technical Director until pre-

sent. Together with other members of the

Board of Directors, Ms Aprillina has success-

fully transformed the company to one of best

insurance companies in Indonesia.

During her career, Mrs. Lina has attended

various either local or international insurance

courses, workshops and seminars. She is

also active in the Indonesian Insurance Asso-

ciation. She was appointed as the keynote

speaker for several workshops and seminar

with various topics.

11

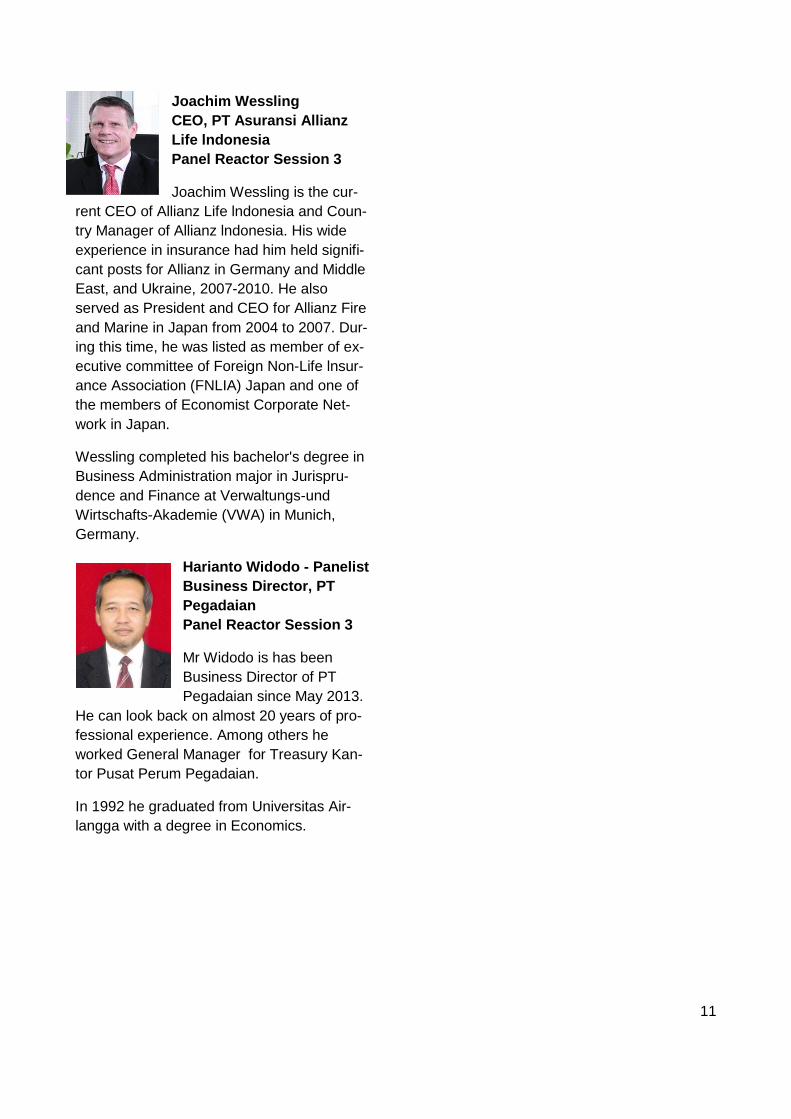

Joachim Wessling

CEO, PT Asuransi Allianz

Life lndonesia

Panel Reactor Session 3

Joachim Wessling is the cur-

rent CEO of Allianz Life lndonesia and Coun-

try Manager of Allianz lndonesia. His wide

experience in insurance had him held signifi-

cant posts for Allianz in Germany and Middle

East, and Ukraine, 2007-2010. He also

served as President and CEO for Allianz Fire

and Marine in Japan from 2004 to 2007. Dur-

ing this time, he was listed as member of ex-

ecutive committee of Foreign Non-Life lnsur-

ance Association (FNLIA) Japan and one of

the members of Economist Corporate Net-

work in Japan.

Wessling completed his bachelor's degree in

Business Administration major in Jurispru-

dence and Finance at Verwaltungs-und

Wirtschafts-Akademie (VWA) in Munich,

Germany.

Harianto Widodo - Panelist

Business Director, PT

Pegadaian

Panel Reactor Session 3

Mr Widodo is has been

Business Director of PT

Pegadaian since May 2013.

He can look back on almost 20 years of pro-

fessional experience. Among others he

worked General Manager for Treasury Kan-

tor Pusat Perum Pegadaian.

In 1992 he graduated from Universitas Air-

langga with a degree in Economics.

12

3. Introduction

In many Islamic countries, significant portions of the population live in poverty and lack ac-cess to financial services, such as insurance, that can help prevent the further worsening of their economic situations and living condi-tions. In such countries as Indonesia, the creation of an appropriate market for insur-ance that is compliant with Islamic laws and that will cater to the low-income sector – a microtakaful market- is a need that is slowly gaining attention and priority. But while initial efforts have led to the development and offer of some microtakaful products, the pace of development needs speed and the approach needs concerted collaboration between the government and the industry. The current situation needs to be understood to inform the future progress and to pave the way for the formal establishment of the microtakaful market. As one of the steps to improve that understanding GIZ (through the RFPI Asia program), OJK, AASI invited insurance regu-lators, Islamic finance standard setting body, insurance providers and takaful operators, finance intermediaries, insurance support institutions such as actuaries and academia, development organizations and international (micro)takaful and microinsurance experts to the 2014 Microtakaful Conference Indonesia, that took place on 24 of April 2014 in Jakarta. Around 170 people participated in the event.

4. Overview of the Conference Agenda

The conference should give the possibility to discuss the microtakaful market assessment in Indonesia commissioned and funded by GIZ in the first quarter of 2014. In order to gather input and opinions from the different stakeholders five consecutive sessions have been planned, followed by the synthesis and the Closing address. The conference started with an Opening Address and a Keynote Speech. The detailed agenda for the confer-ence is as follows:

13

Time Activity

8:00 AM Registration

9:00 AM

Opening Address:

Shaifie Zein, Chairman, AASI

Antonis Malagardis, Program Director, GIZ RFPI Asia

9:45 AM

Keynote address:

Muliaman D. Hadad, Chairman of Board of Commissioners, OJK

10:05 AM

Session 1: Rationale and regulatory basis of microtakaful market development Speaker: Kartina Md Ariffin, member of the Secretariat, Technical & Research, Islamic Financial Services Board (IFSB) Panel of reactors:

Dumoly F Pardede, Deputy Commissioner for NBFI, OJK

Zuriah Rahman, Takaful expert and consultant to GIZ-RFPI Asia/AFC

Antonis Malagardis, Program Director, GIZ RFPI Asia

Moderator: Dante Portula, Senior Advisor, GIZ RFPI Asia

10:45 AM

Session 2: Key findings and recommendations of microtakaful market study in Indonesia Presenters:

Nick Thornton, Lead consultant, Microtakaful market study in Indonesia

Zuriah Rahman, Takaful expert and consultant to GIZ-RFPI Asia/AFC

Moderator: Moch Muchlasin, Head, Directorate of Sharia NBFIs, OJK

11:30 AM

Session 3: Response to the market study – industry’s perspective and current practice Panel of reactors:

Joachim Wessling, CEO, PT Asuransi Allianz Life Indonesia (takaful window)

Aprillina Triyono, Technical Director, PT Asuransi Tri Pakarta (takaful window)

Agus Haryadi, Commissioner, TAKMIN (network of MFIs distributing takaful) and for ASyKi (mi-crotakaful broker)

Abdul Majid, BMT Sidogiri (an Islamic cooperative)

Harianto Widodo, Business Director, PT. Pegadaian (Persero)

Moderator: Srikandi Utami, Vice-chairperson, AASI

12:30 PM Lunch Break

1:30 PM

Session 4: Response to the market study – role of support institutions Panel of reactors:

Ibnu Hasyim, Director of Operation and Actuary, PT Avrist

Ismi Kushartanto, Executive Director, Economic Shariah Communication Center

Zainal Kassim, Actuarial Partners Malaysia

Moderator: Muhammad Faried, Head Statistics Department, AASI

2:30 PM

Session 5: Response to the market study – regulators’ perspective Panel of reactors:

Moch Muchlasin, Head, Directorate of Sharia NBFIs, OJK

Kartina Md Ariffin, member of the Secretariat, Technical & Research, Islamic Financial Services Board (IFSB)

Zuriah Rahman, Takaful expert and consultant to GIZ-RFPI Asia/AFC

Moderator: Antonis Malagardis, Program Director, GIZ RFPI Asia

3:30 PM

Synthesis:

Zuriah Rahman, Takaful expert and consultant to GIZ-RFPI Asia/AFC

Closing address:

Moch Muchlasin, Head, Directorate of Sharia NBFIs, OJK

4:00 PM Coffee, networking

14

5. Opening Address

The opening of the 2014 microtakaful confer-ence was officiated by the honorable Mr Shaifie Zein, Chairman of AASI, who gave insights into the status of takaful and mi-crotakaful in Indonesia.

Currently the takaful market is still dominated by individual insurance companies and the lack of capacity of the industry is still compar-atively high. Although the market penetration of 5 percent of the insurance market, repre-senting 1 % of the GDP, is quite low, Indone-sia has a huge potential for a strong market growth due to its large and mostly Muslim population. Looking to other developing and emerging countries some promising and comprehensive examples and success sto-ries can be found and allow to look forward for a comparable positive development in Indonesia.

In the Indonesian context, microinsurance, respectively microtakaful, is still mostly seen as a corporate social responsibility (CSR) activity by most of insurance companies, hence a mind shift in this respect is neces-sary, combined with measures to increase the persisting low level of awareness among the low and middle income population, the primary target group of microtakaful products.

A consequence, AASI, OJK and GIZ RFPI Asia initiated in 2013 a cooperation to en-hance the development of the microtakaful market in Indonesia. One outcome of this cooperation is the microtakaful market as-sessment commissioned by GIZ in early 2014 which will be discussed in the framework of that conference. The market assessment, as well as the conference will give the opportuni-ty to share best practices for microtakaful.

As final remark Mr Zein expressed his grati-tude to OJK for the good cooperation estab-lished by the tripartite agreement.

Dr Antonis Malagardis, Program Director of the GIZ RFPI ASIA, takes the opportunity to explain GIZ’s role in the cooperation with AASI and OJK. The implementing agency of the German Ministry of Economic Coopera-tion and Development (BMZ for its German acronym) GIZ has the mandate to enhance and broaden inclusive insurance. Therefore the GIZ RFPI Asia is currently supporting 6

countries: Indonesia, Thailand, Philippines, Nepal. Vietnam and Mongolia in establishing policy frameworks and regulations for micro-insurance. In Indonesia the newly established Grand Design provides a comprehensive regulatory framework and strategy for micro-insurance, furthermore a nationwide financial literacy campaign has been launched to im-prove the population’s awareness for financial products, in this respect it has also to be highlighted that all market players play im-portant roles, and the task is not limited only to the regulator.

GIZ follows an approach directed to different implementation levels. On the macro level, GIZ cooperates closely with regulators, e.g. as mentioned earlier, for the development of the Grand Design in Indonesia. On the meso level the cooperation focuses primarily on training institutions and associations. The activities dedicated to the third level, the mi-cro level, focus on the clients’ awareness and appropriate products and distribution chan-nels.

An important role will and should be played by private public partnerships (PPP) to achieve a sound and broad development of the microinsurance market. This development should happen under the dogma of affordabil-ity, accessibility and awareness / trust of the products and aimed towards the relevant stakeholders and players. Currently the mi-croinsurance market is still dominated with a share of around 60% by credit-life insurance products, often even without the awareness of the benefi-ciaries. Never-theless there is a high need for microin-surance against loss of property, for health issues and so called crop insur-ance. Hence a very crucial aspect is the usage of adequate distribution channels to keep the price low and to reach effectively and efficiently the target customers.

15

Additionally to achieve an inclusive mi-crotakaful the stakeholders should clearly differentiate the meanings and intention be-tween financial education and marketing as well as between advocacy and policy making.

For the proper measurement of such achievements impact assessments have to be conducted. It should always be taken into account that such measures will need some time to have a visible and measurable effect and in consequence it is necessary to con-duct long-term impact assessments.

Mr Malagardis emphasizes that Indonesia will have in this respect a double responsibility to create a national microinsurance market and specifically an experience for microtakaful.

6. Keynote Address

The keynote address by the honourable Mr Muliaman D. Hadad, Chairman of Board of Commissioners from OJK, highlights the fac-tors for a sustainable growth of the microtaka-ful market.

Although the market for takaful is emerging, it still remains quite small, growth comes pre-dominantly from an increasing demand among the low and middle income popula-tion. Thus microtakaful can substantially con-tribute to the sustainable growth of the market by broadening access to such services. It should be taken into account that especially among that segment of population, religion and culture play a crucial role and they con-sequently need to be served and approached differently. To achieve that and to ensure a sustainable growth, several factors need to be identified. Among the most important fac-tors is the sharia compliance of the offered products. Potential beneficiaries should be aware and be informed that the offered prod-ucts fulfill all the relevant features to be con-sidered sharia compliant. The overall product design shall be demand-driven and be char-acterized by its relative simplicity; this will lead to a high acceptance among the target population and their willingness to consume microtakaful which finally leads to economies of scales, including a more efficient delivery of the microtakaful services. For a proper product design and pricing the availability of appropriate and sufficient data is indispensa-

ble, hence efforts have to be done to improve the database building and the implementation of Management Information Systems (MIS). The product price shall eventually reflect the considerable risks and cover the cost of ex-pected claims, but ensure the availability and affordability among the low income custom-ers.

On the other side, consumer protection and awareness raising can overcome the still pre-vailing lack of confidence in the market. But also the unrestricted availability for non-muslim persons should be addressed in this context. Appropriate measures need to be implemented nationwide.

Another factor, that can also be seen as unique selling point in comparison to conven-tional insurance, are the full transparency and accountability of (micro-) takaful products. Nevertheless it is important for microtakaful providers to ensure quick and straightforward claim services and practices, to maintain and increase the trust and demand among the targeted population. As Indonesia still has a large share of rural population depending on agriculture and the country’s vulnerability to natural disasters, takaful products should be designed to cope and manage better such risks.

All this efforts can only be achieved jointly with a strong involvement by all stakeholders.

7. Session 1: Rationale and regulatory basis of microtakaful market development

Ms Kartina Md Ariffin, member of the Secre-tariat of Islamic Financial Services Board

16

(IFSB), presents the key aspects necessary to establish a regulatory framework for mi-crotakaful starting with an introduction of the role of IFSB.

IFSB was inaugurated in 2002 and serves as an international standard-setting body of reg-ulatory and supervisory agencies for the Is-lamic financial services industry. The IFSB principles should be seen as complementing to standards set by Basel Committee on Banking Supervision, (BCBS), International Organization of Securities Commissions (IOSCO), and International Association of Insurance Supervisors (IAIS). The IFSB standards are followed by more than 180 national regulatory authorities and public or private entities. Besides the design of stand-ards, IFSB also provided technical support to

the different institutions.

Main aspects covered by IFSB in regards to Takaful are:

Corporate Governance

Financial and Prudential Regulation

Transparency, Reporting and Market Conduct

Supervisory Review Process

Recently the IFSB established a working group dedicated to the issue of retakaful and a joint working group with the IAIS Financial Inclusion Subcommittee. That joint working group conducts a global survey on the status of microtakaful, looking on the microtakaful regulation already adopted to collect best practices for regulatory frameworks.

The IFSB sees the following key characteris-tics/ necessities as essential for a well-designed microtakaful product:

Inclusivity

Grouping for efficiency

Simple processes

Consumer awareness

Limited (available) data (to be over-come)

Appropriate contribution collection

Suitable distribution channels

The relevant stakeholders are among others the low income / poor population, regulators, sharia scholars the government etc.

Nevertheless an essential point to clarify is the adequate definition of microtakaful; ques-tions to be discussed are among others:

Does it primarily target the rural population?

Does it serve people below a specific income level?

Is it a standardized product?

In order to further elaborate such definitions and to get a deeper insight in practices, the joint working group will sent out a question-naire to regulators, takaful providers etc. The result are intended to be published mid- 2015.

Following the presentation by Kartina Md Ariffin, the panelists have the possibility to elaborate on the regulatory issues; guided by questions from Dante Portula, GIZ RFPI Asia.

One question directed to Dumoly F Pardede, Deputy Commissioner for NBFI/ OJK, focus-es on the need for OJK to develop regula-tions and products for the Islamic community especially for the poor sectors. The compre-hensive answer was that OJK, has existed

17

just over 2 years, and he believes in the po-tential of market growth especially for mi-crotakaful and also a need for establishing a stable and reliable regulatory framework.

Another question was put forward to GIZ’s commitment to spend resources for the mi-crotakaful market development. Mr Antonis Malagardis highlights that GIZ’s considers inclusive insurance, including microtakaful, a highly important topic and is therefore com-mitted strongly to achieve this. This commit-ment has to be seen in relation to Germany’s involvement in the G20 activities to enhance the global financial inclusion. One of the 9 aspects of financial inclusion is the promotion of inclusive insurance. In order to align the activities GIZ has signed an MoU with the Islamic Development Bank of working togeth-er in the field of Islamic finance and also co-operates closely with IFSB and IAIS through the attendance of meetings of the Financial Inclusion Subcommittee (FISC).

In regards to lessons and experience Indone-sia can learn from other countries more ad-vanced in the area of microtakaful. Ms Zuriah Abdul Rahman, AFC Consultants Interna-tional, stresses the importance of education for all stakeholders including regulators and takaful providers.

Furthermore the takaful providers should not only stick to financial performance but include non-financial performance indicators to as-sess the quality of their business activities. Also the companies should revise their corpo-rate governance principles and their product should be profitable. Directing to the regula-tors Ms Abdul Rahman sees the need to es-tablish a regulatory framework for the distri-bution channels of microtakaful and a special need for a recognizable logo stating the halal / sharia compliance of the microtakaful prod-uct.

8. Session 2: Key findings and recommendations of microtakaful market study in Indonesia

This second session of the day was held jointly by Mr Nick Thornton, independent consultant and Ms Zuriah Abdul Rahman, AFC Consultants International, both respon-sible for the market assessment for mi-crotakaful in Indonesia. The market assess-

ment is based on the extensive meetings and discussions with different stakeholders, with a certain focus to the customers (e.g. in total Nick Thornton conducted over one dozen of Focus Group Discussion) in the first quarter of 2014.

The findings of the market assessment can be summarized in 12 key messages.

1) Great need for awareness: The tar-get population is not aware of the concepts of takaful or shariah compli-ant insurance.

2) Context matters: To reach the cus-tomers effectively and also increase the level of awareness among them, it is necessary to address them in their regional/ local languages.

3) Appropriate distribution channels and networks: For an efficient distri-bution it is necessary to identify ap-propriate distribution channels, possi-ble channels are among others the post offices and Islamic cooperatives.

4) Shared surplus is helpful: Depend-ing on the type of takaful model used, there is a prospect for profit sharing between the contributor and the oper-ator.

5) Preference for traditional distribu-tion channels and payment meth-ods: The majority of the population prefers traditional methods against modern methods like mobile pay-ments and use of cellphones.

6) Risk priorities have not changed: The top risks against which the low income population primarily wants to protect are illness, education (not be-ing able to afford education of their children), death (life insurance).

7) There is ability and willingness to pay: Low income people are able to make regular contributions, often higher amounts than previously thought.

8) Flexibility in contribution collec-tion: It is important for takaful provid-ers to offer to their customers certain flexibilities in the contribution collec-

18

tion; this can decrease the barriers to microtakaful services and potential lapse of the policy.

9) Bundling could increase coverage: A possibility to increase coverage of microtakaful is the bundling with other (Islamic) financial services.

10) Complementarity for national health insurance: Although Indone-sia has established a national health insurance the target population has a preference to receive an add-on cov-erage with a health microtakaful.

11) Ta‘awuni: This concept of mutual as-sistance makes also the difference with conventional insurance and should be highlighted when targeting the target population.

12) Differentiate takaful from conven-tional insurance: Also other unique features have to be communicated to the target population especially on the Sharia compliance.

Nick Thornton stressed the importance of partnerships among takaful providers and MFIs, cooperatives for a broad outreach of microtakaful. The MFIs and cooperatives will have to play a double role, first of all as dis-tributors but also as institutions that contrib-ute actively to takaful literacy and awareness raising among the target population. Such activities can support the existing willingness to implement microtakaful into concrete activi-ties, as many potential customers prefer taka-ful against conventional insurance if the price is adequate.

Zuriah Abdul Rahman, AFC Consultants International, starts her presentation with a comprehensive explanation of the basic con-cepts of takaful. In her opinion the successful promotion of takaful also depends on the clear description of the characteristics of takaful and the differences from conventional insurance.

The key concept of takaful is risk sharing, not risk transfer as with using conventional insur-ance. When raising awareness it is essential to explain to potential customers that takaful is based on mutual help and solidarity, as well as shared responsibility. The amount of

money paid to takaful operator is a contribu-tion rather than a premium. This contribution can be seen as voluntary alms, in the form of sadaqa, to the “brothers and sisters” being a member of the takaful scheme. Contributing the form of sadaqa makes it easier for the potential clients to understand why they will not get back anything/or only a profit share if they have not been exposed to a certain risk

and have not made any claim.

Referring to the findings of the market stud-ies, Ms Abdul Rahman highlights that Indo-nesia has already a well-established infra-structure of potential distribution channels (e.g. rural banks, cooperatives), building a good foundation for achieving a high out-reach. Potentials on the medium term per-spective lie in the cooperation with post offic-es and money transfer agents and commer-cial banks. In the long term perspective con-cepts of bancatakaful and of employer deduc-tion should also be initiated.

Ms Abdul Rahman provided additional gen-eral overview on takaful products being of-fered in different Islamic countries. Being from Malaysia, she gives deeper insights of that national takaful market. Having a small market share for takaful, Malaysia does not have a very huge potential for microtakaful, because of the income distribution among the Malaysian population, with relatively less people living under the poverty line.

Other countries offering microtakaful products are Sudan (as pioneer country, where the first takaful product was offered roughly 35 years

19

ago), Lebanon and Sri Lanka, the United Ar-ab Emirates among others.

Also in countries where National Health Scheme are established, health takaful prod-ucts are frequently used as add-on to such securities as those often cover only the basic treatments and do not cover sufficiently the costs and services in case of serious illness.

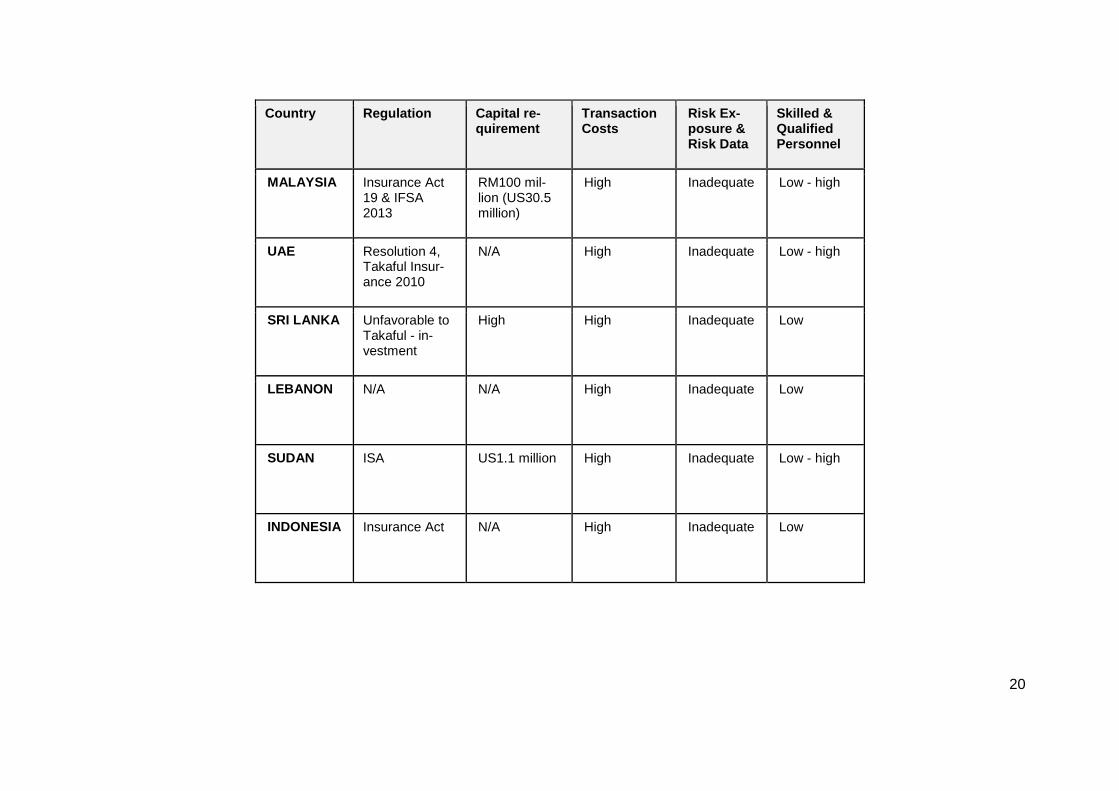

Having a closer look on the regulation on takaful in other countries, Ms Abdul Rahman confirms that in even more developed takaful markets there is ongoing need to establish accurate regulation and standards for mi-crotakaful. Even in Sudan, being a pioneer in respect to takaful, risk exposure and available data are inadequate. A further concern is the inadequate level of knowledge/or high dis-parities in the knowledge level among differ-ent players (e.g. operators, regulators) even in countries like Malaysia, Lebanon or Sudan.

The following table gives an overview on the comparison among different countries where microtakaful products are offered:

20

Country Regulation Capital re-quirement

Transaction Costs

Risk Ex-posure & Risk Data

Skilled & Qualified Personnel

MALAYSIA Insurance Act 19 & IFSA 2013

RM100 mil-lion (US30.5 million)

High Inadequate Low - high

UAE Resolution 4, Takaful Insur-ance 2010

N/A High Inadequate Low - high

SRI LANKA Unfavorable to Takaful - in-vestment

High High Inadequate Low

LEBANON N/A N/A High Inadequate Low

SUDAN ISA US1.1 million High Inadequate Low - high

INDONESIA Insurance Act N/A High Inadequate Low

21

Ms Zuriah appeal for more education among all stakeholders (from regulators to custom-ers) in a different manner for a positive and sustainable takaful experience in Indonesia.

9. Session 3: Response to the market study – industry’s perspective and current practice

This session gives the insurance industry the opportunity to react to the market study and its findings. Ms Srikandi Utami, AASI; invited the representatives of different takaful opera-tors (full-fledged / takaful window) to intro-duce their institutions and to explain to what extend these findings are reflected in their daily business activities. As first speaker Mr Joachim Wessling, PT Asuransi Allianz Life Indonesia, explains the company’s experi-ence operating as a takaful provider with a takaful window. The company has been work-ing for six years in the field of takaful and clearly follows a business approach with the goal to generate profits. Nevertheless Allianz as a global insurance company is also con-cerned about the reputation in the different markets. Therefore a clear statement was given that the profit goals stay at reasonable and sustainable level. Allianz considers up to 4 percent of profit margin as a fair share and has currently a profit margin of around 3 per-cent.

Following the business approach means for Allianz as well to attain the best skilled em-ployees in the field of takaful and is conse-quently willing to pay to takaful experts in their company equal salaries in comparison to other employees having comparable re-sponsibilities and skills in other divisions.

To reach its customers Allianz is working with more than 90 MFIs, the share of takaful is around 40%. Mr Wessling sees a specific challenge in the adequate training of the dis-tributors and sellers, as well-trained agents and distributors also contribute to the trans-parency of the market.

Ms Aprilina Triyono, PT Asuransi Tri Pakar-ta, confirms this opinion expressed by Mr Wessling, that one of the biggest challenges

is the training and education of employees and agents.

PT Asuransi Tri Pakarta operates under a takaful window and has opened 30 branch offices and 52 offices in small cities. The company offers microtakaful products such as, Personal Accident, Fire and Motor takaful. Almost 20 percent of income was generated from microtakaful segment.

Mr Agus Haryadi, Commissioner TAKMIN (network of MFIs distributing microtakaful products) and for ASyKi (microtakaful broker), mentioned that the TAKMIN group had signed an MoU with the NGO PERAMU in 1993 and later established the ASyKi to moni-tor the activities of its members. TAKMIN was established as a cooperative combining sev-eral Islamic institutions and each individual member holds a 10 percent share from the cooperative. In 2005 PERAMU entered into a partnership with MFIs and IFIs to offer mi-crotakaful products. One of the products of-fered was Mikro Sakinah, a credit life product with an option to add additional lives (e.g. spouse of borrower), and another unique product called the Tabungan Qurban, a Sacri-fice Savings Plan for the BMT to provide the sacrificial goat or cow to the family of the saver in the event that the participant dies. This plan was well received because the members do not feel the pinch due to the direct deduction from the monthly dues. In 2012 TAKMIN has another partner in the form of BMT Sidogiri to act as an Assurance Bro-ker for microtakaful and licensed by OJK. From this arrangement, the entity managed to reap Rp150 million contributions per month with the support of more than 100,000 mem-bers. BMT members admitted to the im-portance of asuransi, hence the very encour-aging performance of the business.

22

Question from the audience:

“How does the TAKMIN group tackle the is-sue of approaching the market given their vast outreach?”

Answer from Mr Haryadi

The establishment of ASyKi has greatly facili-tated the role of TAKMIN as a leading NGO taking the market’s interest at heart. Because TAKMIN is such a large organization and the market is equally large, hence the promotion and education of microtakaful has been un-dertaken by ASyKi and this resulted in more microtakaful customers taken in by the prod-uct and concept it serves which is in line with Islam, after its establishment.

Mr. Abdul Majid, representing BMT Sidogiri and ASyKi (takaful broker), which is an entity operating as a cooperative using the ta’awuni concept, that is mutual sharing of benefits and losses. It comprises of 14,000 small business owners, and more than 400,000 credit and savings members.

Mr. Abdul Majid explained that members, due to their low education level had a misconcep-tion that the life is worth only Rp2-5 million (that is the sums assured). He also stressed that members are keen on coverage for edu-cation to their family members and also to cover natural disasters that occur quite fre-quently in Indonesia. Asuransi Shariah as it is widely known among its members faced competition from other distribution channel, hence, he appeals for price to be kept as low as possible for the sake of retention.

In 2012 they launched the Program Asuransi which includes financing with microtakaful

and the pricing increased accordingly with the increased in benefits.

Question from the audience:

“The majority of the cooperative members are Muslims, while most are small income earn-ers, how does BMT Sidogiri retain its mi-crotakaful customers and their membership to the cooperative?”

Answer from Mr. Abdul Majid:

“The concept used is very simple, in mi-crotakaful, the promotion is via infaq or dona-tion, whether you live or die during the course of the policy either way you will be rewarded, on this earth or in the hereafter. So there is nothing to lose. Members are taken in due to the simple explanation and the alignment with their religious beliefs. Most of the members quipped that they are happy to be a coopera-tive member, besides getting the benefits of microtakaful, they do not feel the pinch when it comes to contributing to the microtakaful fund because it is deducted from members’ subscription. On top of that each member gets a 10 percent share of the cooperative and its profits.”

The next speaker, Mr. Harianto, from Perga-daian (Pawnshops) mentioned that their dis-tribution channel has started microtakaful offerings after an MoU was signed recently with the members of the AASI; 10 percent of their business is Shariah compliant. The pro-file of their customers are:

60% - householders and professionals

80% - women

70% - possess higher education

Their target market is suitable for microtakaful products, and according to him, it is easy to market and the customers understand the benefits of microtakaful products quite well. On top of that it is distinguishable from insur-ance, while delivery is made simple, handling collection of contribution is easy to maintain a low cost structure. Most of their microtakaful products are bundled with the financing that is offered.

For the future IT systems will be needed

which match with IT systems in pawnshops to support product selling.

23

10. Session 4: Response to the market study – role of support institutions

After lunch, that allowed the participants to exchange their opinion and knowledge on the topic of microtakaful, besides also to get in contact with each other and to initiate new cooperation opportunities, representatives from the supporting institutions have the pos-sibility to comment on the market study and to express their opinion about the status of microtakaful in Indonesia.

Mr Muhammad Faried, gave an introduction to the different panelists and asked Mr Zainal Kassim to start elaborating on the role of support institutions.

Mr Zainal Kassim, Actuarial Partners Malay-sia, outlines some of the most crucial chal-lenges in providing takaful services. First of all he sees the necessary message to be transmitted in regards to takaful is the dogma of solidarity to the potential customers.

Looking to product design of a takaful prod-uct, the contribution of a microtakaful client has a risk and savings component. Essential for the adequate management, especially of the savings component is the existence of sukuk (bond) markets (shariah compliant in-vestment markets). But also the adequate estimation of the risk component bears some challenges as takaful customers usually ex-pect the takaful product to be cheaper than a comparable conventional insurance product. Another challenge can be seen in the admin-istration costs of a takaful fund, especially in the case of a microtakaful fund. Usually ad-ministration costs per client / claim do not vary heavily between the costumers contrib-

uting the multiple amount for a takaful product and microtakaful customers, but obviously the share of administration costs is much higher in the microtakaful contribution compared to a takaful contribution.

In general Mr Zainal sees a huge protection gap for takaful but also insurance in general. Giving as an example Australia where around 98% of the population is aware of the benefits (and risks) of insurance, but only around 50% are insured adequately. Closing such protec-tion gaps requires also addressing the right person. For instance in Saudi Arabia, most of the women are responsible for the household budgeting and are in consequence primarily addressed by takaful providers for taking the decision to insure against risks the entire family could face.

Mr Zainal suggestions for the future devel-opment of microtakaful are among others is to make the microtakaful membership com-pulsory. In this way adverse selection can be avoided, the massive clustering of “bad” risks, as primarily those with a relatively high risk decide to be member in a takaful if the sys-tem remains voluntary. In a compulsory sys-tem the risk can be better pooled and is di-versified.

In general Mr Zainal advocates for a “back to the basics” approach of providing microtaka-ful. First of all he recommends using already existing cooperatives to create takafuls. In that manner no conflict with sharia compli-

ance can arise, as takaful is just an Islamic cooperative insurance. By applying this ap-proach distribution costs can significantly be reduced. The compulsory takaful product should be simple and cover risks against

24

death and disability. In Mr Zainal opinion this can lead as well to lower regulatory costs.

In his concluding remarks Mr Zainal says that the takaful pro-viders should stop giving guarantees for claim pay-ments, and refi-nancing a takaful fund with a qard loan, if there is insufficient fund-ing. More promis-ing concepts are the retakaful and wakala concept.

Mr Ismi Kushar-tanto, Economic

Shariah Committee Center, a government promotional agency, elaborated on the role of the center, partly to educate the public, ex-plaining the role of the regulator, socialization of the mass through its involvement in takaful in GRES! activity.

The center also has a dedicated website and TV program emphasizing on muamalat (busi-ness transaction the Islamic way). They have recently published a book, organized a ba-zaar and a Shariah Economic Writing Com-petition. Another important function was the awareness program of the standard logo (GRES!) used in the culture and system adopted by the center. The center also works with 14 associations including the Majlis Ula-mak Indonesia (MUI), AASI, BMT and others.

They have also created the Program Sejuta, created for those who are characteristically non-creditworthy and for financial inclusivity. These individuals are grouped and trained to be financially literate. They also created a number of self-help programs such as Susu Ibu (the importance of breast feeding), for the coffee growers to increase their savings and for the Red Group (those below the poverty line) to be eligible for emergency programs under the Zakat Institutions. The Yellow Group, those that had crossed the poverty line, but still dependent on financial support is encouraged to be independent through vari-ous self-help activities. The next target groups is the Green Group who has crossed the poverty while the Blue Group comprises

those living under more or less proper eco-nomic conditions, and are ready to move for-ward. These are the masses of whom their financial and physical welfare need to be pre-served against all risks.

Most of their events are partnered and devel-oped with BMTs and several microtakaful channels to enable acceleration of the BMT growth, opening lines of communication and banking services.

GRES! Logo, can be seen as a standard and accepted by the microtakaful industry and is in compliance with the MUI.

Mr Ibnu Hashim from PT Avrist, a life insur-ance company was established in 1975. They have a 7,000 strong agent support and more than 500 employees. The company’s Shariah asset growth is increasing and 40 percent of their individual customers are Non-muslims. Microtakaful contributed 5 percent to their total profit. The Micro Tabbarru’ fund contrib-uted a great deal to their business and it pro-vided small loans for women amounting to Rp 800,000 with a premium contribution of Rp 3,000. They have in total 19,000 members (contributors).

11. Session 5: Response to the market study – regulators’ perspective

During this Session especially the Head, Di-rectorate of Sharia NBFIs of OJK, Mr Moch Muchlasin, had the chance to express his opinion and outlook in regards to the market

study. Asked on the main challenges to be envisaged, he says that the first step would be to accept and learn from the findings. By improving the regulatory standards the con-sumer protection can be enhanced. An im-proved regulatory framework will neverthe-less allow the continuation of useful informal

25

self-insurance schemes. A comprehensive and working regulatory framework can only be established when a frequent exchange with the different stakeholders and the market is maintained. In his opinion “learning by do-

ing” seems to be the best approach to develop a functioning regulatory framework. The need for support, not only from GIZ; in product design, pricing and awareness raising / and consumer protec-tion.

Question from the audience:

Is OJK going to take the lenient approach to the microtakaful industry given that the pro-vider and the distribution channel is all set to go?

Answer from Mr Moch Muchlasin:

Every regulator has an important role to play and their position is more critical because it has to promote the industry while at the same time protect the consumer. Leniency will not guarantee that the industry and the market will prosper. It however has to strike a bal-ance between being too leni-ent and too strict. This can be achieved by learning from others.

Ms Zuriah Abdul Rahman emphasizes that awareness raising and education of all the stakeholders is the key for a sound mi-crotakaful market. This can be achieved for example with close cooperation with the Eco-nomic Shariah Communication Center, through the GRES!, that executes awareness raising campaign also via mass media. Also mosques and mushallahs, as well as zakat centers, can play a very important role in the promotion of microtakaful. They can provide the necessary infrastructure and usually are also close to the targeted population. “Time is crucial”, as Indonesia is currently still at a premature stage, the market has to grow and the regulation has to improve in a long way.

Mr Antonis Malgardis, having the task as session moderator, takes the opportunity to

give a summary on behalf of Ms Kartina MdArrifin, from IFSB, as she had to leave unfortunately before she could participate personally in that session. To get a better overview IFSB will conduct an all embracing worldwide survey on microtakaful, covering the aspects of definition of microtakaful, gov-ernance, prudential regulation, market con-duct and supervision.

Question from the audience:

How long will it take for OJK or the Shariah Board to approve a microtakaful product? Can the time taken be reduced?

Answer from MrMoch Muchlasin:

With speed comes a price, because without careful consideration of many factors, Shari-ah risk may occur and as a result a non-Shariah compliant product is offered to the market. Therefore the Shariah council has to deliberate and take many aspects of religious edicts to determine whether a microtakaful product can be released to the market.

12. Synthesis

In the last session Ms Zuriah Abdul Rah-man, AFC Consultants International, gave a synthesis on the topics discussed sessions hold during the day:

Session 1: Rationale and regulatory basis of microtakaful market development.

Some of the basic issues facing microtakaful is unique as attested by the IFSB representa-tive, especially on the definition of microtaka-ful itself, and rules relating to Corporate Gov-ernance, Financial and Prudential Regulation, Transparency, Reporting and Market Conduct and Supervisory Review Process.

However, with the existence of various laws and rules on takaful found in many countries it will be easier to adopt and adapt the current practice to suit the Indonesian scenario. What has been practiced now as elaborated in the Grand Design for Microinsurance is suitable for reference for microtakaful except for the issues mentioned above. The current part-nerships of the industry with various distribu-tion channel and community self-help should

26

proceed and given the encouragement while at the same time to work on improving the regulatory framework.

These established partnerships have shown to save cost, products are designed to suit

the target market, typically the co-operative mem-bers, must be easy to under-stand, affordable in terms of pric-ing, simple in procedures and fast in claims settlement. With the desirable features, it is en-visaged that re-tention level will remain high. Ad-

ditionally, corporate governance and Supervi-sory Review Process needed to be strength-ened with the inclusion of the Sharia Re-quirements especially on the establishment of Sharia Advisory Council (SAC) under the purview of OJK and the Sharia Committee of each microtakaful provider. With the exist-ence of the SAC, issues relating to transpar-ency, solvency requirements, risk manage-ment and Shariah compliancy will be ade-quately addressed.

On the Reporting and Market Conduct, the key issue to be addressed is Consumer Pro-tection due to their vulnerability and this could be tackled by educating the public on mi-crotakaful through various media and chan-nels which could reach the rural and urban population. The existing Economic Shariah Communication Center, Masjid (mosques), Zakat Centers, IFIs and MFIs are focal points where microtakaful providers could reach out to the target market. On the other hand, mi-crotakaful providers also need to be aware of the various measures undertaken by various regulatory authorities around the world in addressing, solvency standards, underwriting guidelines, reserves and minimum paid up capital to ensure they remain a financially viable entity.

On the topic of inclusivity, to date, no regula-tion has provided a definition of who should

be the target market for microtakaful due to the diversity and diverse characteristics of its consumers. What is known however, they are the selected poor, included are the low in-come; group is preferred to individuals, the underwriting process needs to take into ac-count their demographic profile however, this may be hindered by lack of appropriate data-base to look into their financial capacity to make regular contributions.

Session 2: Key Findings and recommen-dations of microtakaful market study in Indonesia

The market survey concluded that 12 factors are critical in addressing this sector. They are:

Awareness, since the majority of the respondents could not differentiate between sharia compliant products and conventional insurance.

Context matters, because low level of education and very little exposure to financial literacy programs makes them less knowledgeable on mi-crotakaful, therefore it is best that promotional materials, intermediaries and the cooperatives or existing community based structure be used and supported with the language that is understood by them.

Existing distribution channels have created demand for microtakaful though various financial support pro-grams, both MFIs and IFIs need to be strengthened and regulated.

Image on microtakaful is positive as attested by members of MFIs and this need to be enhanced.

Preferred choice for delivery and payment (contribution) are rural and agriculture banks, cooperatives, agents and post office.

Risk priorities are those pertaining to health, education, family (life) and basic general takaful such as motor (motorcycles).

Allocation of part of their earnings for microtakaful seemed real, because majority could spare more than the desired amount for coverage.

Flexibility is greatly emphasized due to their unpredictable income, hence,

27

must take into account cyclical nature of jobs, informal workers, and the like.

Bundling of microtakaful products with other financial products seemed the best way to offer microtakaful to the poor, because the majority of re-spondents are already subscription members of cooperatives and re-ceived various types of financing for various needs.

Complementary product, microtakaful is considered an add-on to existing coverage National Health Insurance Scheme, the Jaminan Kesihatan Masyarakat (JAMKESMAS) providing basic medication and outpatient treatment.

Ta’awuni (cooperative) is a powerful concept creating and binding rela-tionship between Muslim communi-ties. The existence of mutual help, brotherhood and solidarity falls in line with the teaching of Islam.

Perception of National Health Insur-ance Scheme and insurance is nega-tive, so a Shariah compliant product bodes well with the consumers.

In comparison with other countries, except for inadequate regulatory framework, Indonesia fared equally well with other microtakaful markets such as, in Malaysia, Sri Lanka, Lebanon, and UAE. With a large poor popula-tion of more than 114 million poor, Indonesia could create a critical mass at a faster rate than the other countries. However, 3 critical factors need to be enhanced, they are, edu-cation, training of Sharia and technical ex-perts, a well-established regulatory frame-work.

Session 3: Response to the market study – industry’s perspective and current prac-tice

Views and comments made by various indus-try experts found microtakaful business hav-ing a huge potential in Indonesia. Based on the various initiatives and partnerships to strengthen and to create delivery channels, the microtakaful providers, the cooperatives, the microtakaful broker and pawnshop own-ers have reported positive income from their respective microtakaful business. Profits ranged from 3-5 percent depending on who is their target market and what products are offered. The common sought product is the bundled credit life and microtakaful. Mi-crotakaful is sought by Muslims due to the Sharia compliancy and their trust in the prod-uct, although it is not exclusively for Muslims as microtakaful is also open to non-Muslim population as well.

Session 4: Response to the market study – role of support institutions

Despite microtakaful being different in con-cept from microinsurance requiring a different approach in its promotion and marketing, the product design takes into account both the risk cost and savings component plus the other costs (administrative and so forth), simi-lar to insurance. Product pricing requires ac-tuarial calculation to ensure sustainability of the fund. Underwriting should also be less complex and desirably be a compulsory scheme to weed out adverse selection or moral hazard. In the microtakaful market there should be less competition on pricing but more on service. Adequacy of pricing will help build and develop a fund big enough to ensure viability of the business.

The government agency entrusted to dissem-inate information, financial and takaful literacy and financial inclusivity of the poor into the takaful market is the Economic Shariah Communication Center. It has both physical and visual images that help to support the industry and augurs well for the business. GRES! and the logo of Asuransi Mikro Shari-ah provide confidence to the public and to a certain extent consumer protection is assured by the regulators.

28

Session 5: Response to the market study – regulators’ perspective

Indonesian regulators are open to new ideas, concepts, practices and standards in order to achieve the objectives of financial and takaful inclusion for the poor and low income. In this regards, international standards and practices are highly regarded. Learning from other countries’, adopting and adapting to the Indo-nesian market takes precedence in order to avoid making mistakes.

In the words of the regulator, something to this effect, “let it be known that we have done something for the poor, lest we will be ques-tion by the Almighty that no effort was made to improve their lot.”

In summarizing the outcome of the confer-ence based on the market assessment and input from the various organizations, the fol-lowing were accomplished:

Objective 1 of conference was present the key findings and recommendations of the microtakaful study and draw the commitment of regulators and the industry to support the advocacy on mi-crotakaful market develop-ment.

Supply-Side

1. Findings from the market assessment indi-cated that there are both formal and informal microtakaful providers:

Formal:

Full-fledged takaful providers: 5

Takaful windows: 40

New takaful providers: 8 (to launch new products in 2 years)

Informal:

– IMFIs and Cooperatives

2. Distribution channels featured both tradi-tional and non-traditional:

Traditional:

Brokers and agents

Banks

MFIs and IMFIs

Cooperatives (BMT, BTM)

Direct selling

Working Group (TAKMIN)

Non-traditional:

Retail outlets (scratch off vouchers ac-tivated by cell phone)

Telecommunication Companies

School Groups

Post Offices

3. Microtakaful Network Highlights

TAKMIN – has 43 MFIs in Jakarta & West Java

Sidogiri Group and BT Sidogiri–branches in 10 provinces, Java, Kalimantan, Sumatra and Bali - outreach 500,000 people

Allianz – insures 2 million people nationwide through distribution partners

4. Microtakaful Products

Plan Cost/Contribution Af-

fordable

Life & Personal

Accident (PA)

IDR 15,000 to

25,000/year

Life, PA, Disabil-

ity, Accidents and

related healthcare

account

IDR 175,000/year with

savings IDR 100,000

Dengue Fever IDR 59,000/year

Motorcycle IDR 200,000/year

5. Microtakaful Structure or Model

Partner-Agent Model

MOU between Insurance and Takaful Indus-try and distribution channels resulting in:

Dual role of MFIs and IMFIs

Dual role of Zakat Funds

Industry cooperation

29

Company cooperation (general insurance & takaful window)

Regulatory Environment Issues:

AAJI requests to OJK include the following and deemed to be

Challenges to Regulators:

Less stringent solvency requirements

Speed up product registration

Standardized regulations to avoid difficulties in regional differ-ences in interpretation of in-surance and microtakaful regulations