connecting strengths, - national university of...

TRANSCRIPT

LeedenThe Integration Specialist for Welding, Gas and Safety

Connecting Strengths, Catalysing Growth

Annual Report 2008Leeden Limited

01

02

05

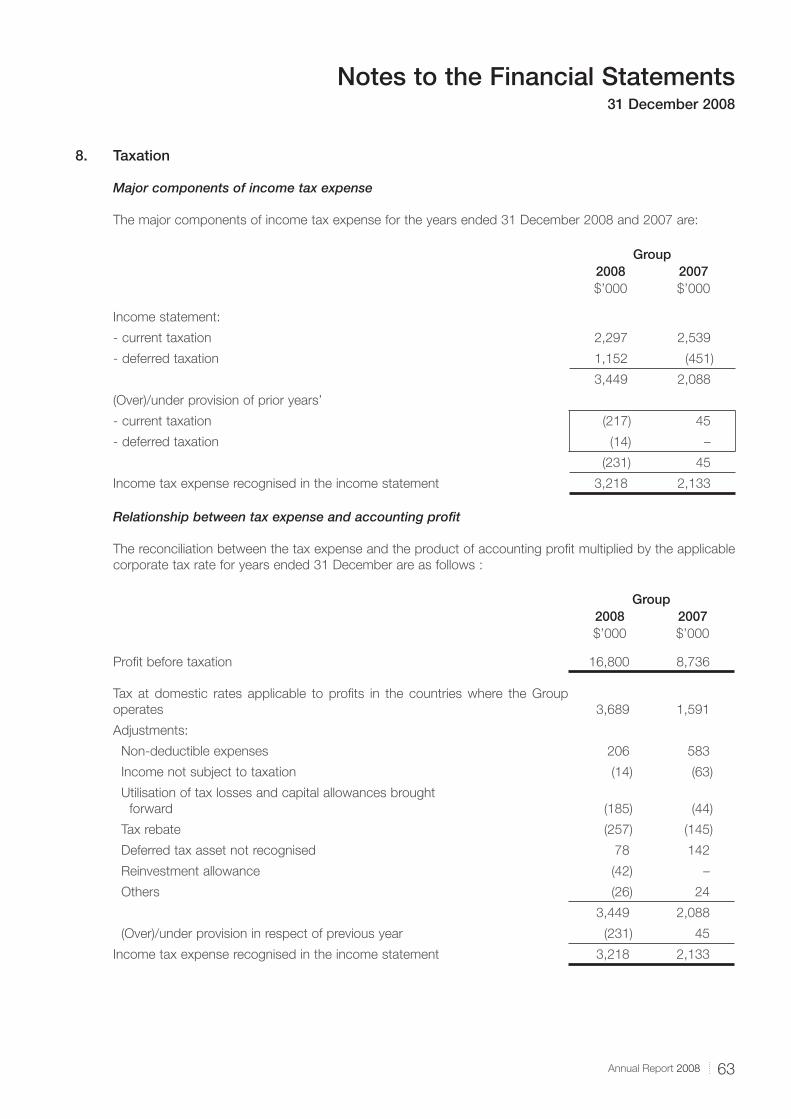

08

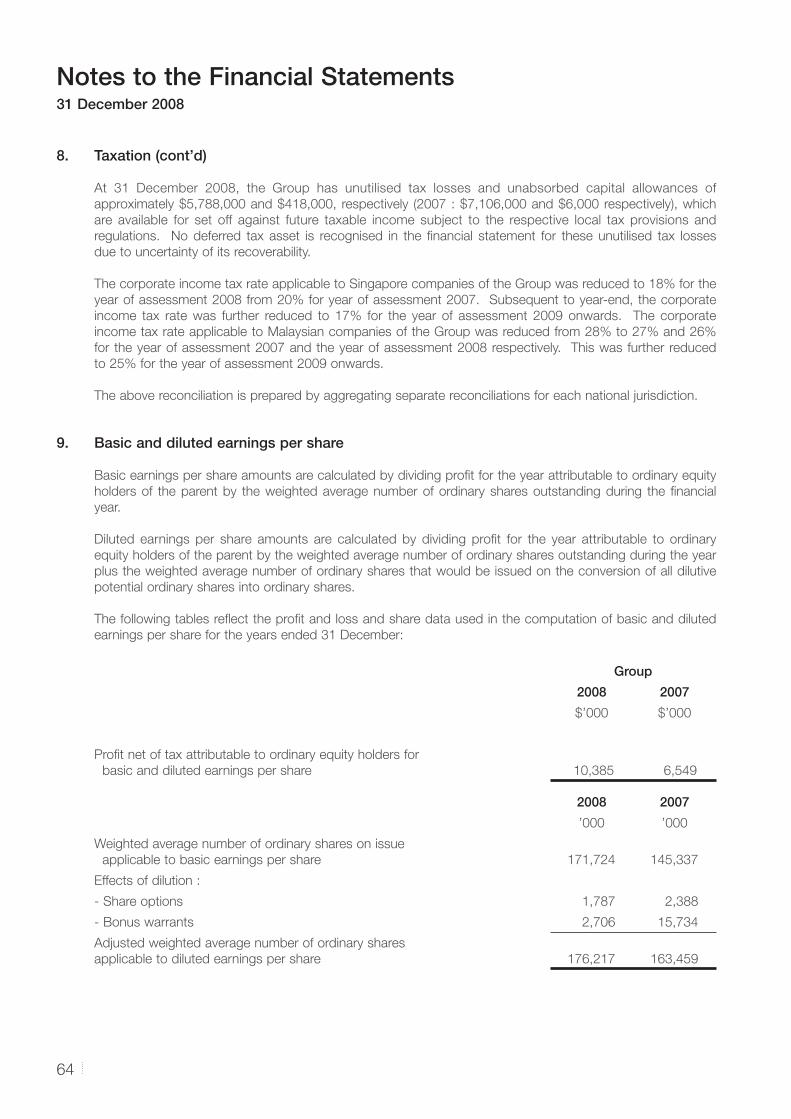

09

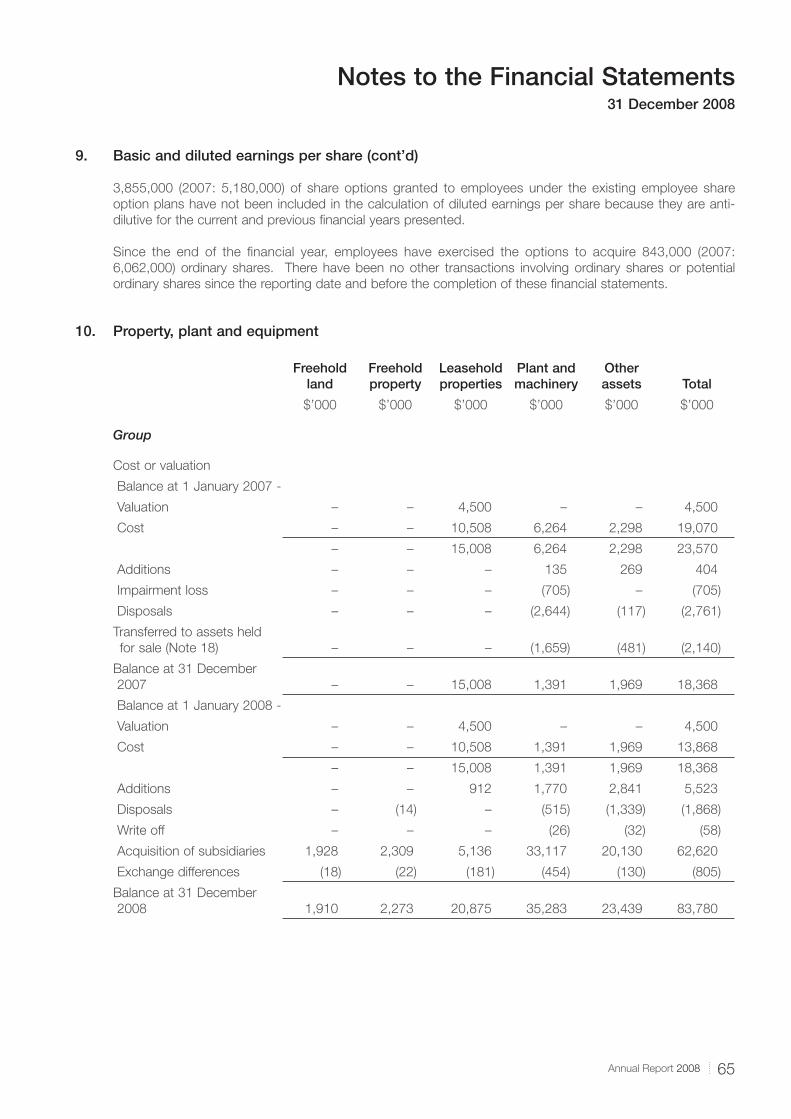

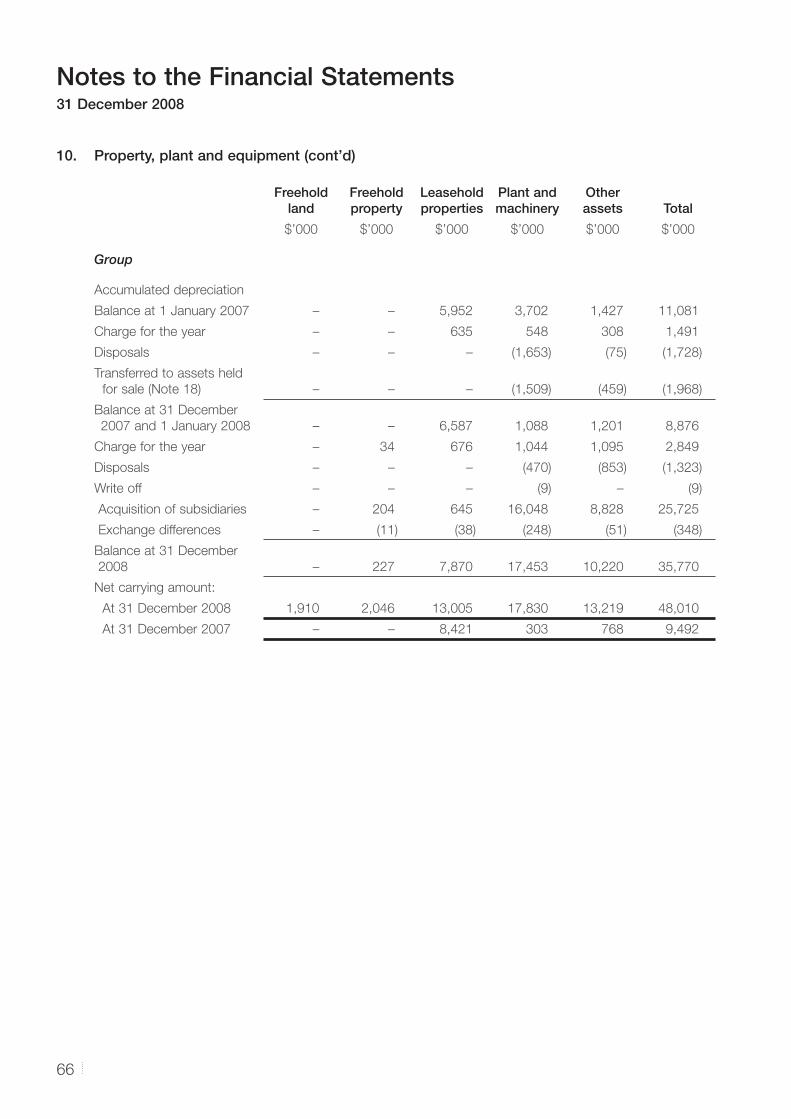

10

12

13

22

29

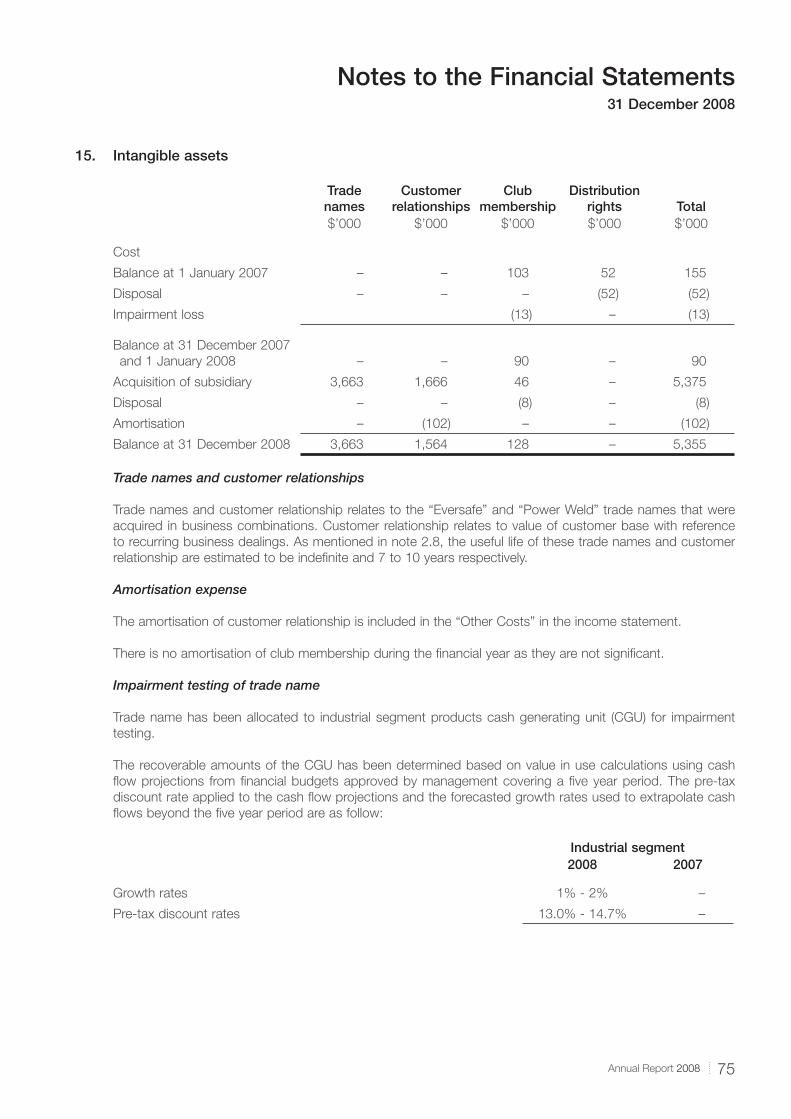

30

31

32

34

37

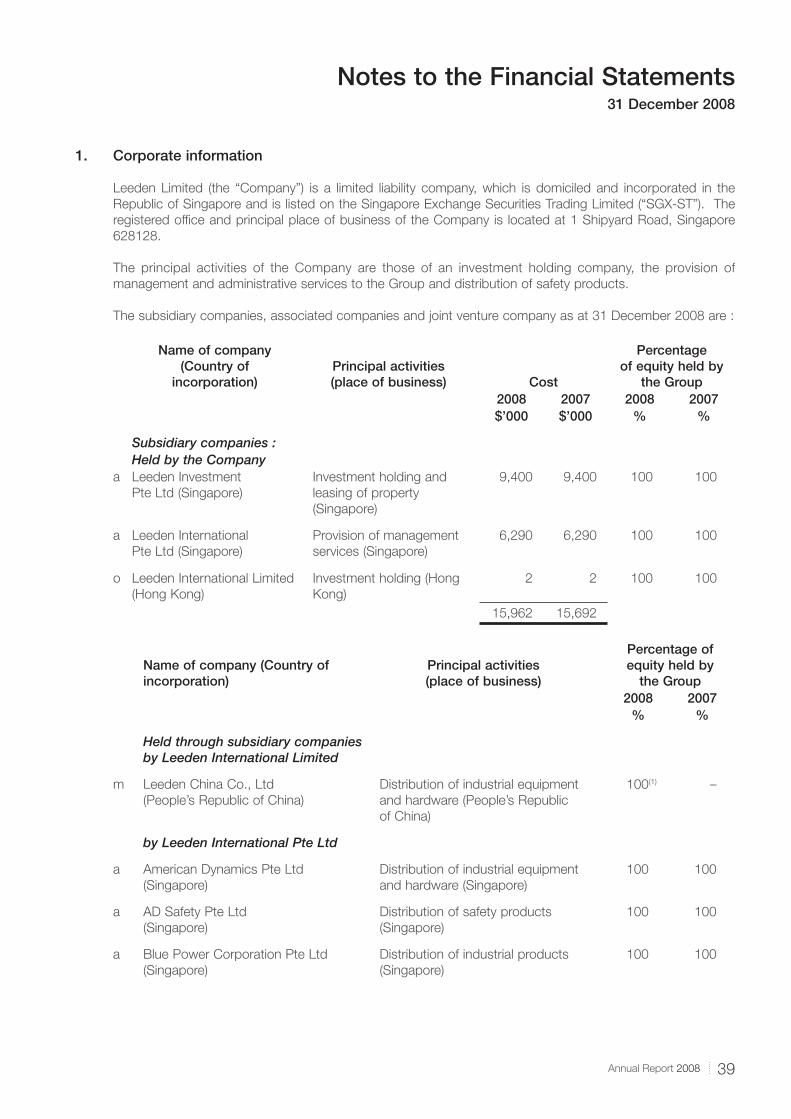

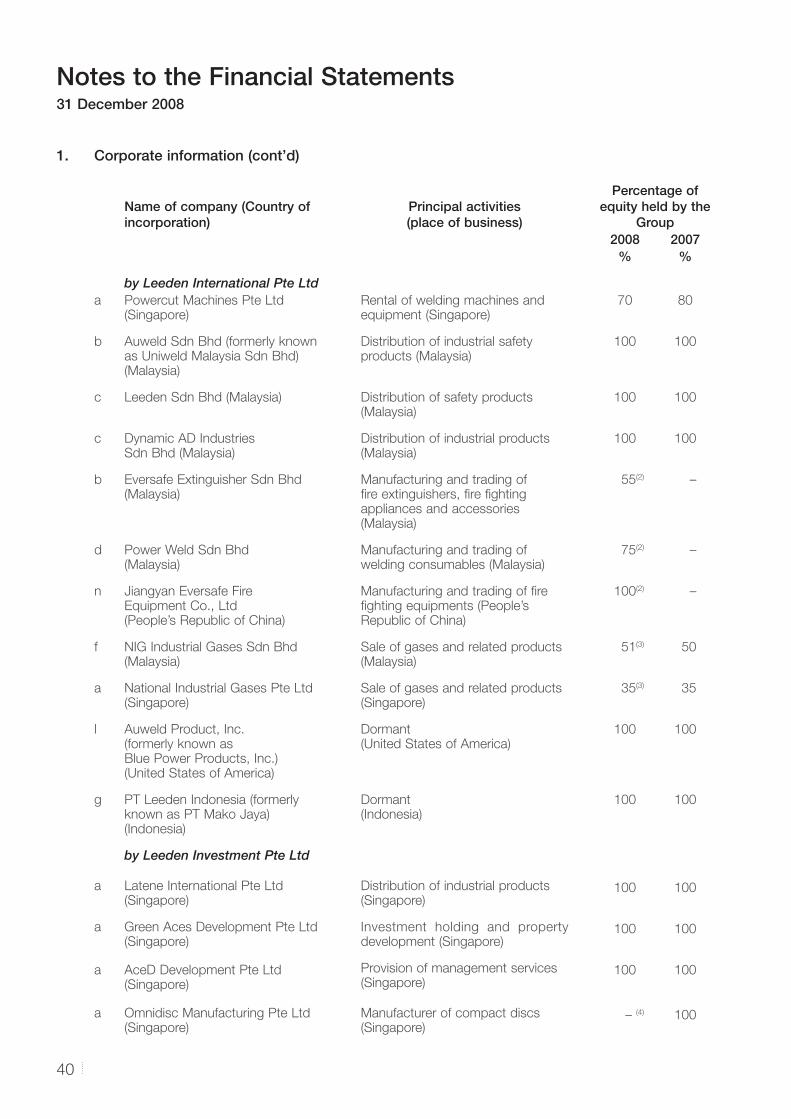

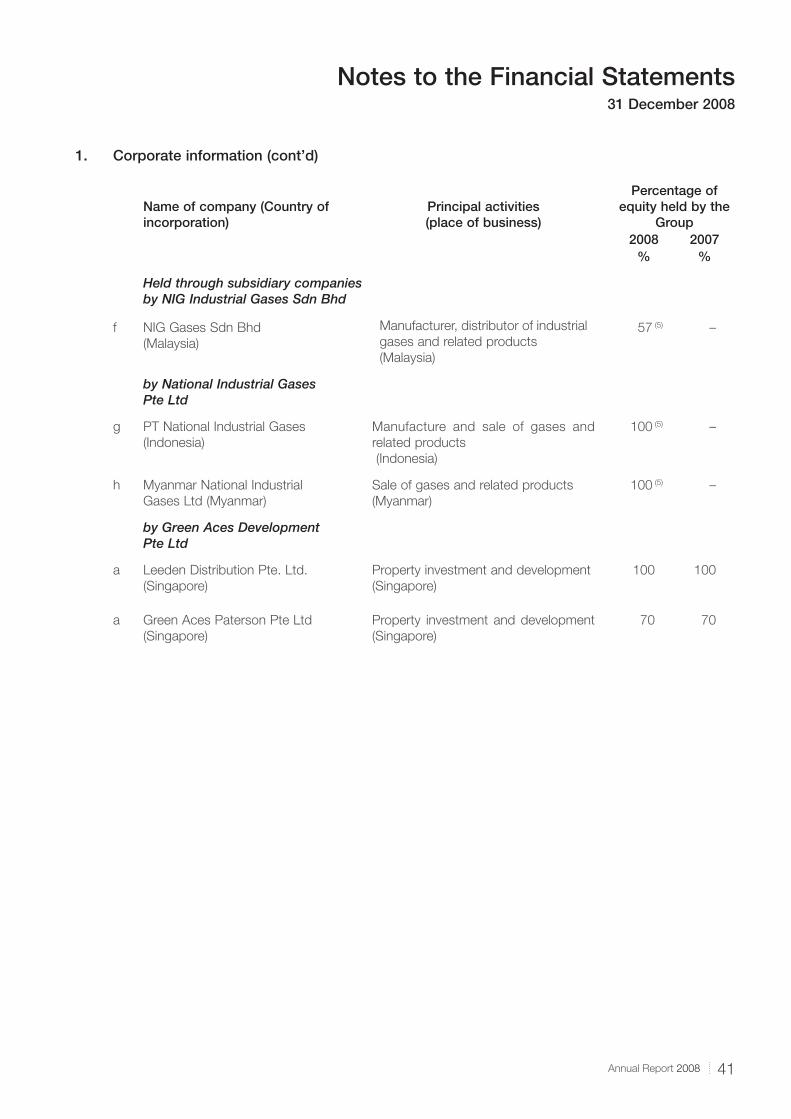

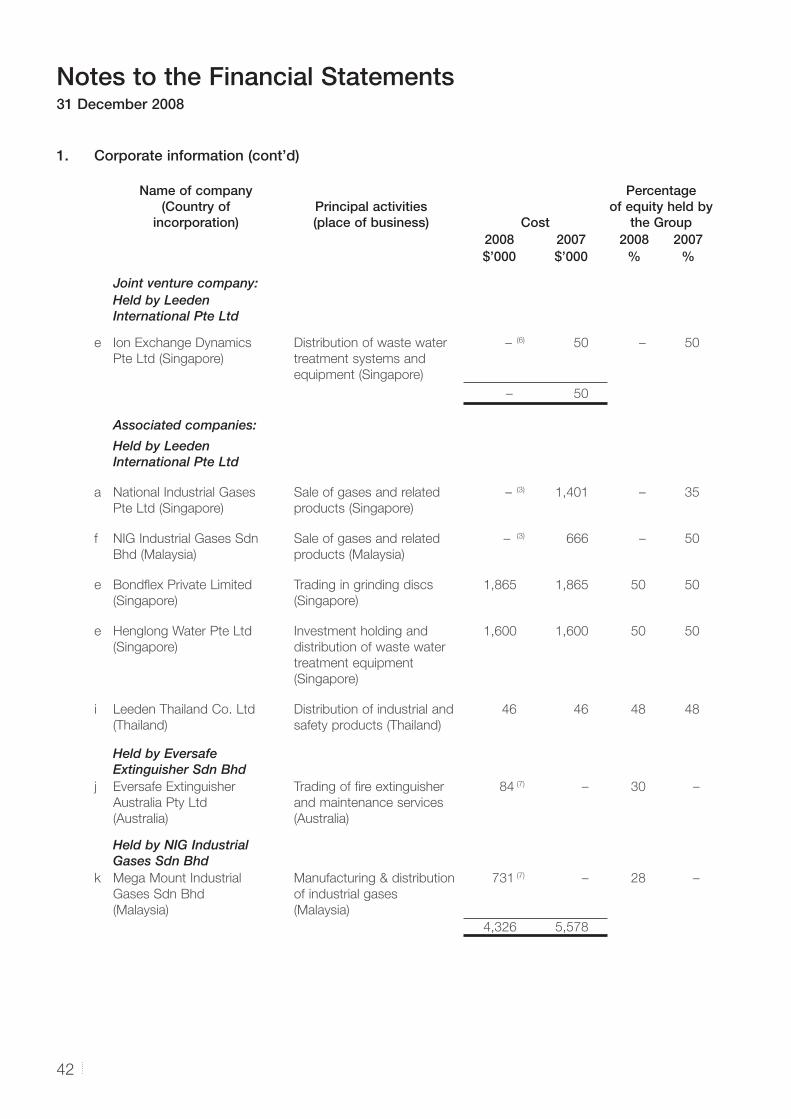

39

100

101

102

103

To be accepted as Asia’s foremost integration

specialist in welding, gas and safety

Achieve market leadership in Asia’s marine, oil & gas industries

Ensure customer value by providing integrated services & solutions for welding, gas and safety

Build a company of repute to attract and nurture people of high performance

Our Vision

Our Mission

About Us

Chairman & CEO’s Message

Operations Review

Financial Highlights

Financial Overview

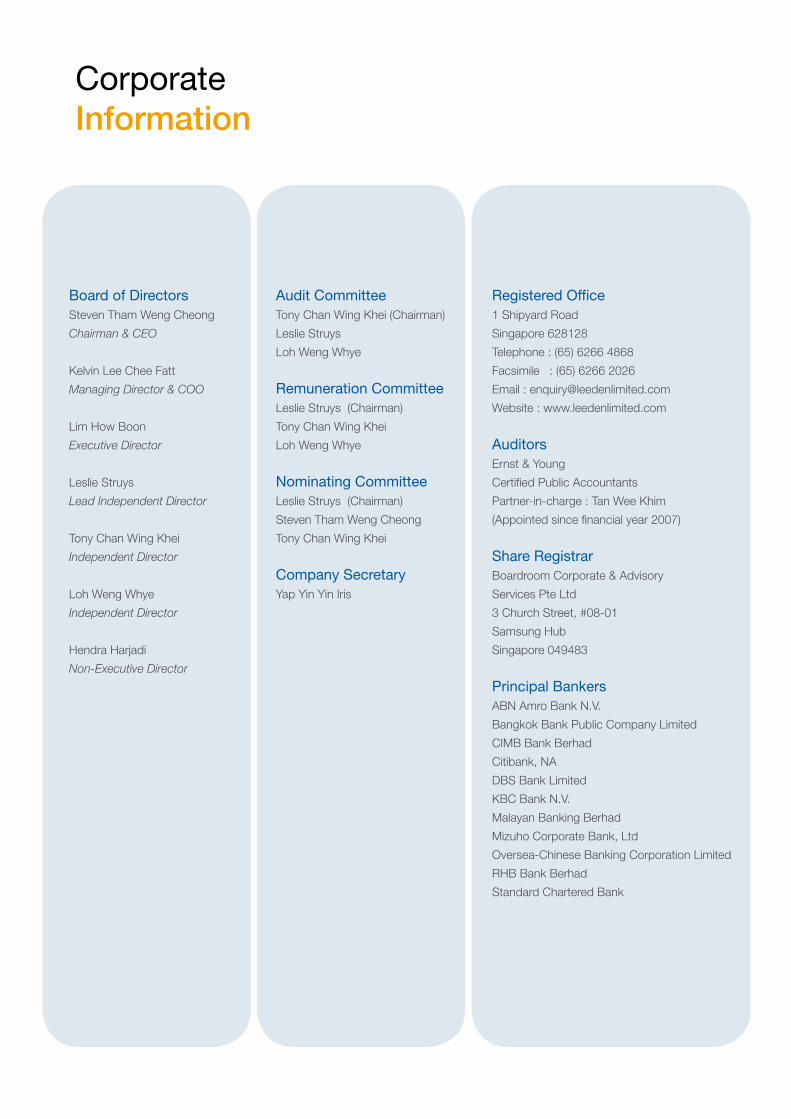

Board of Directors

Management Team

Corporate Governance Report

Directors’ Report

Statement by Directors

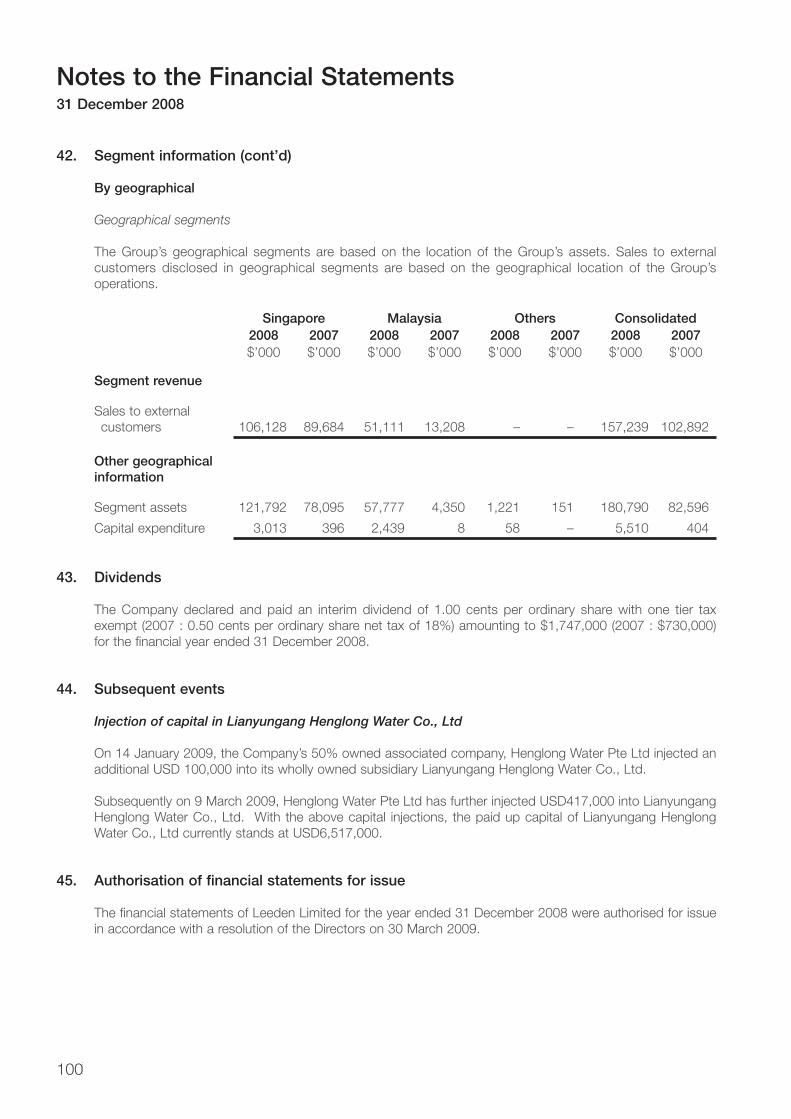

Independent Auditors’ Report

Consolidated Income Statement

Balance Sheets

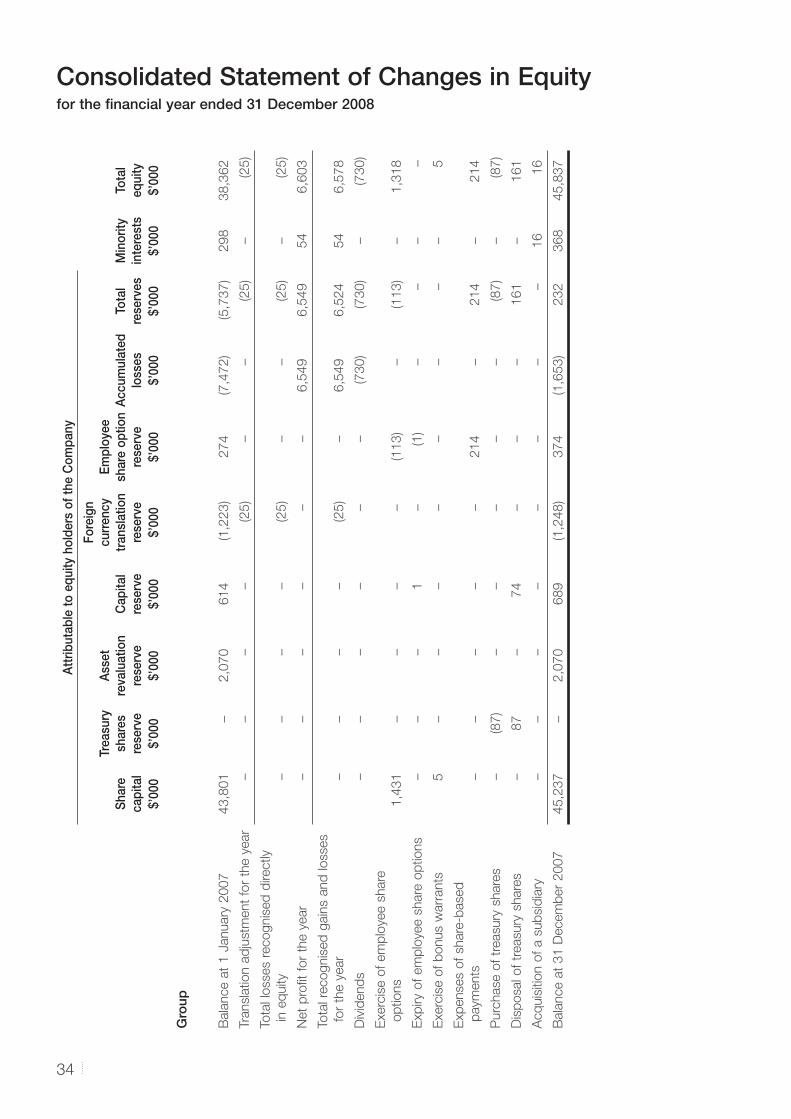

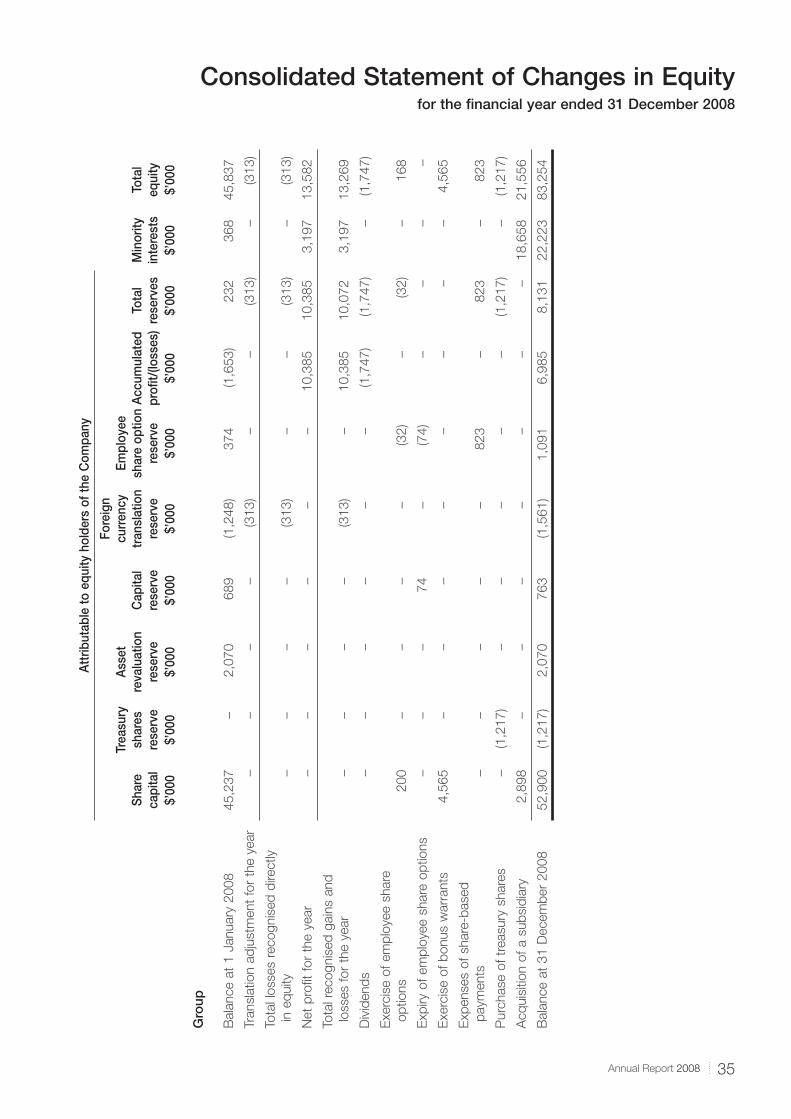

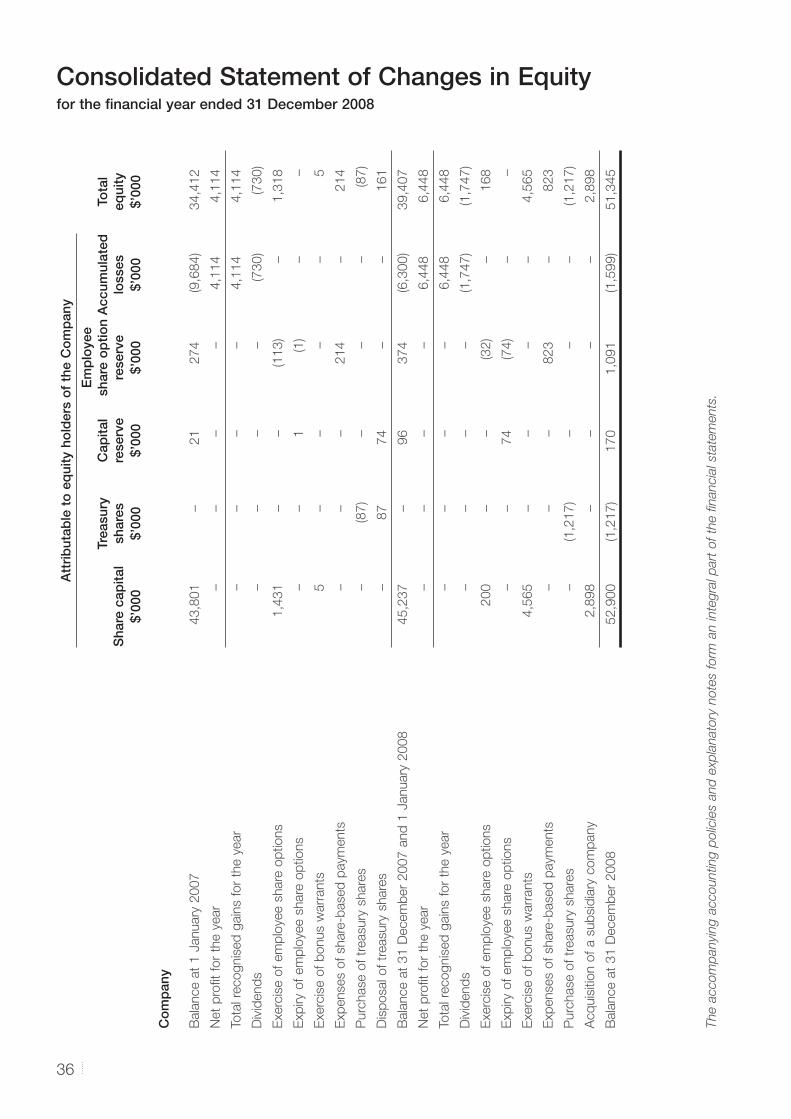

Consolidated Statements of Changes in Equity

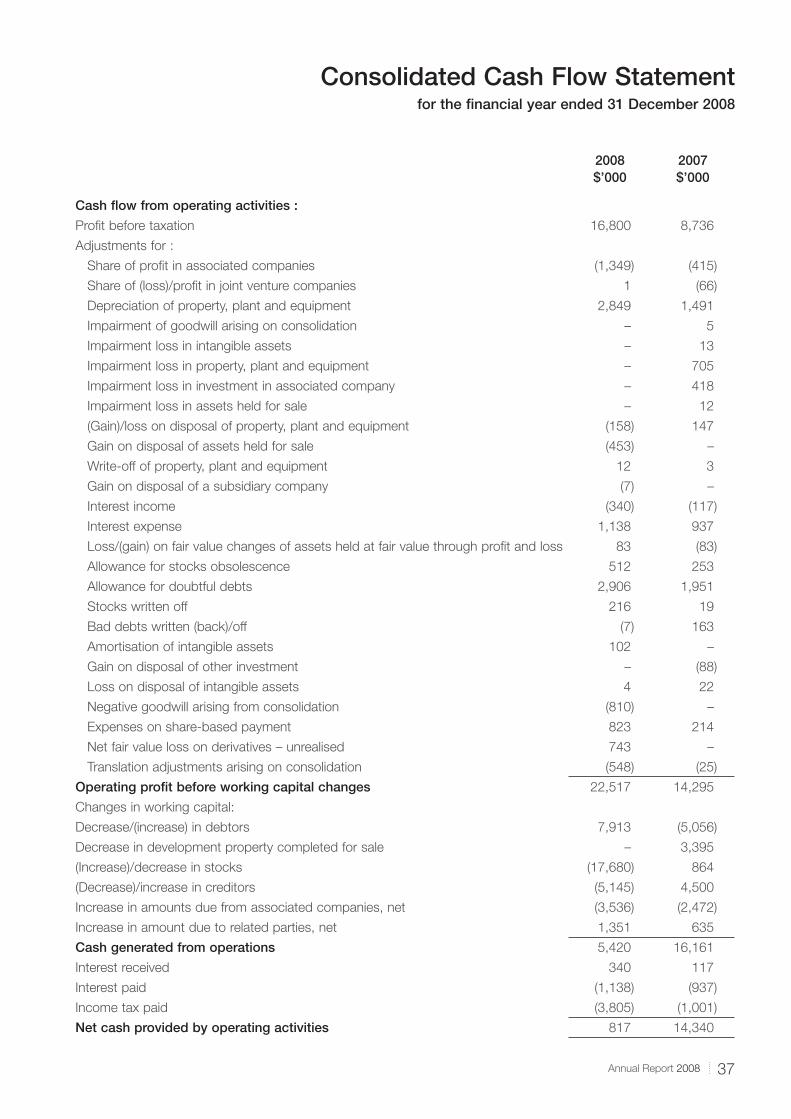

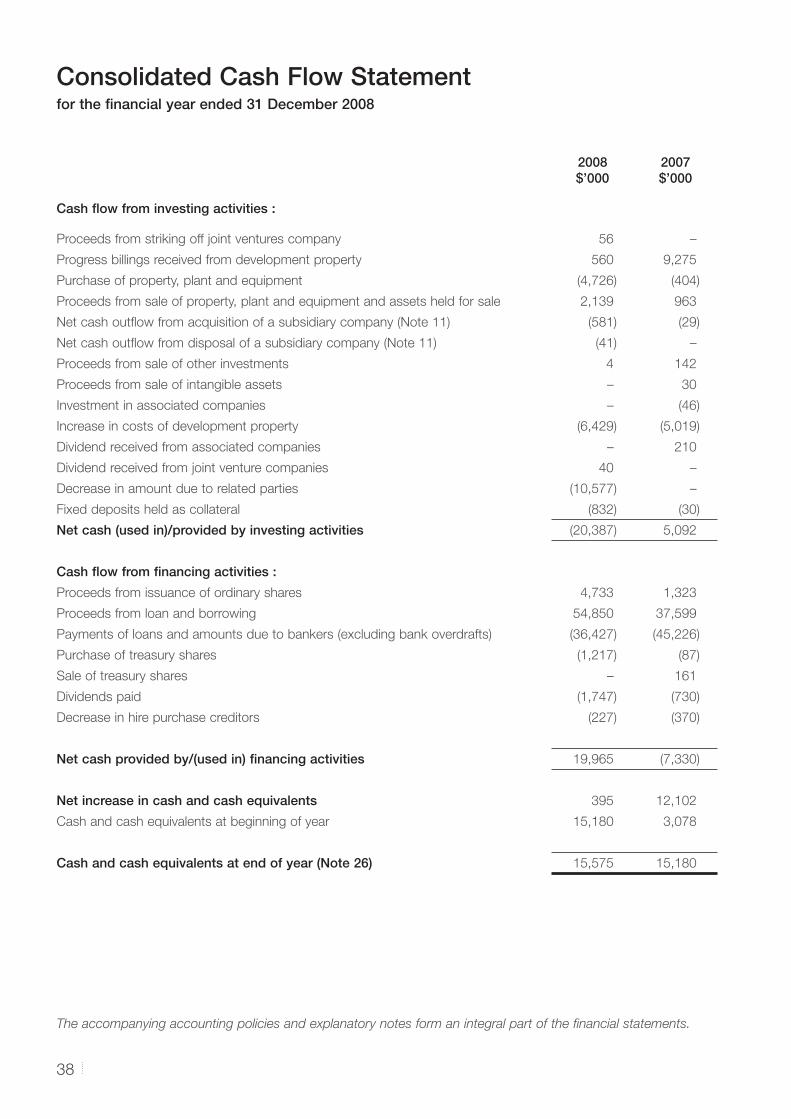

Consolidated Cash Flow Statement

Notes to the Financial Statements

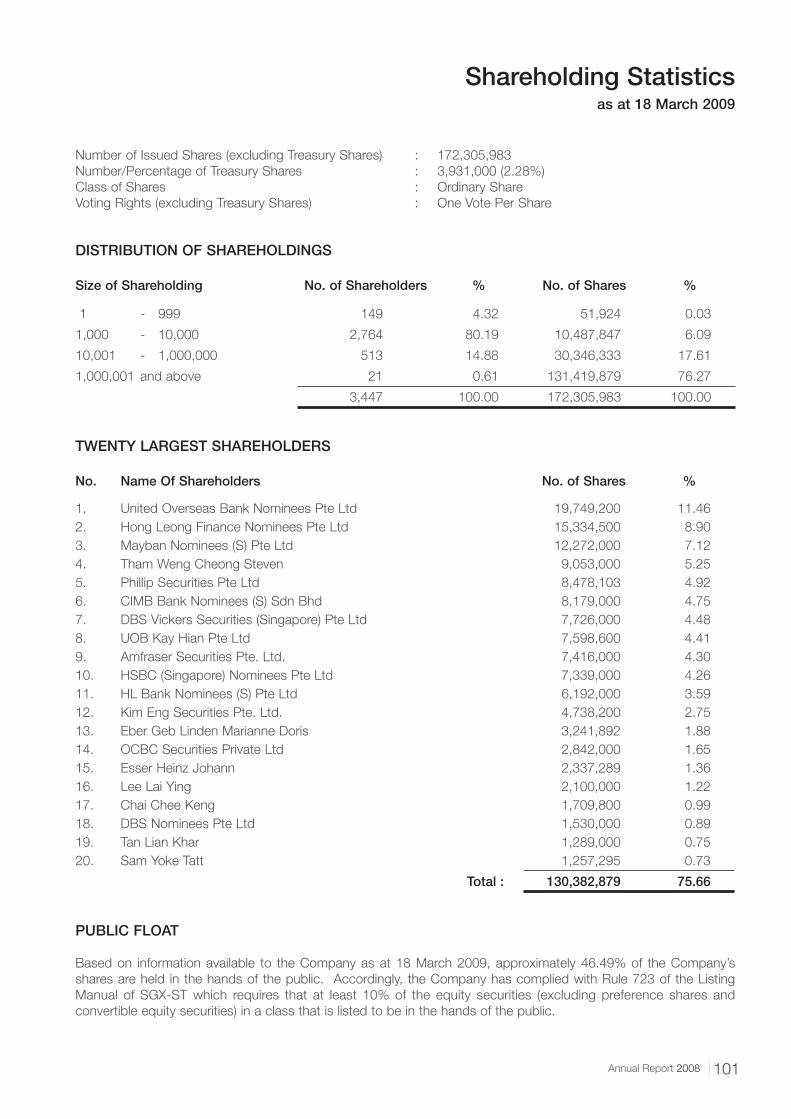

Shareholding Statistics

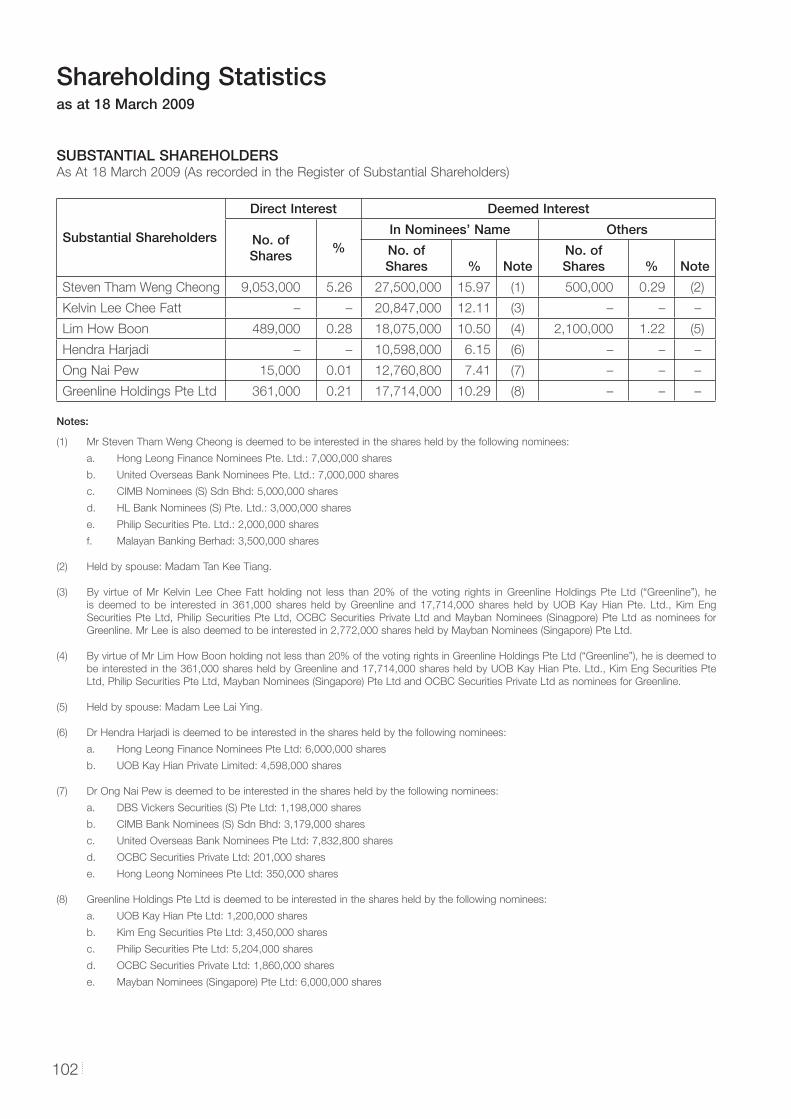

Substantial Shareholders

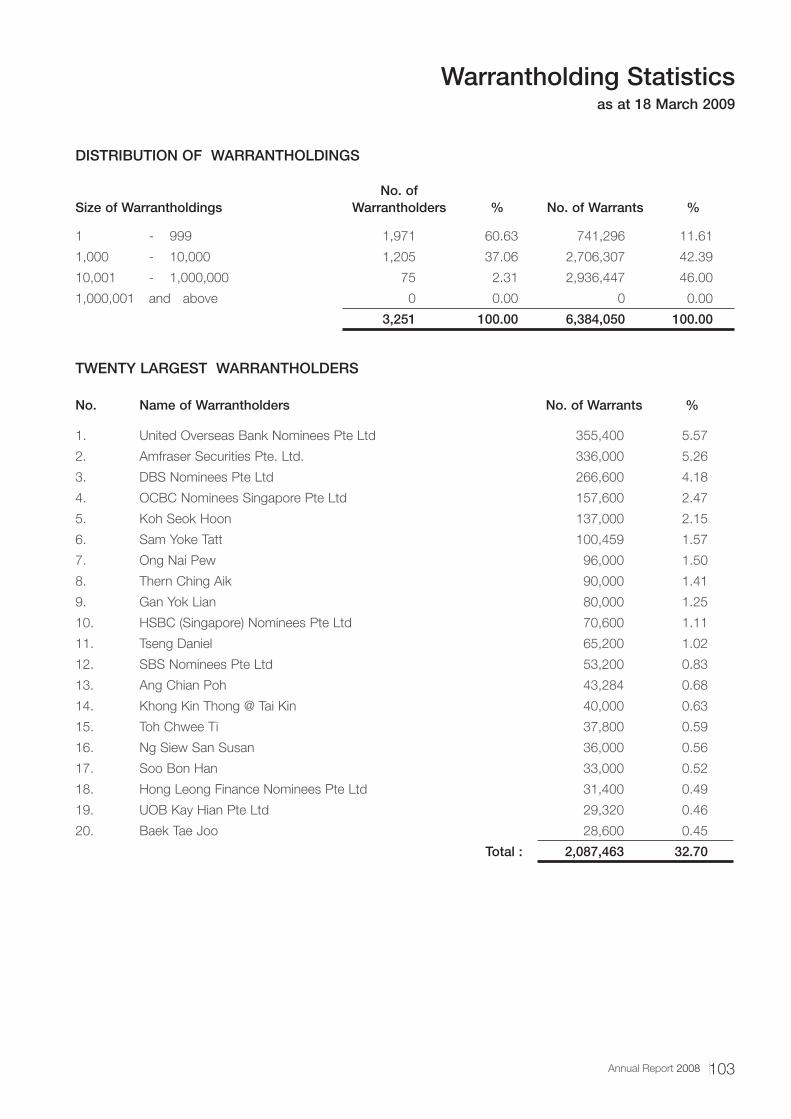

Warrantholding Statistics

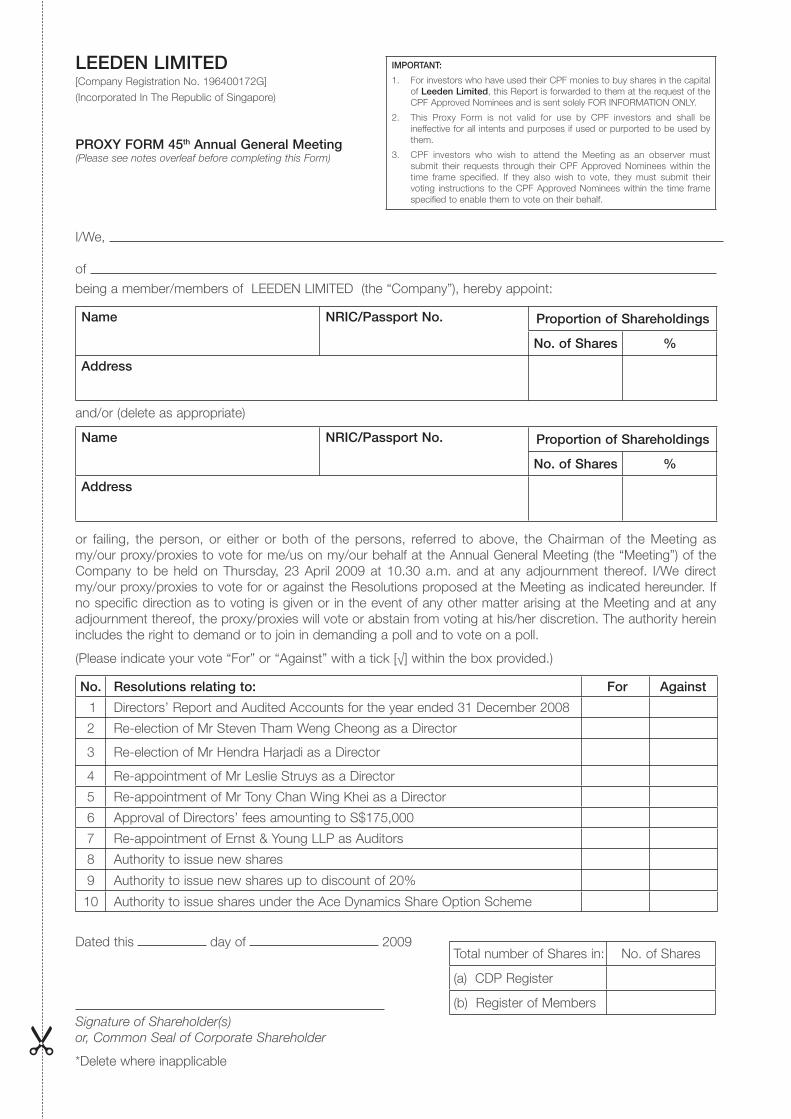

Notice of Annual General Meeting

Proxy Form

Contents

01Annual Report 2008

Since our incorporation in 1964, we have progressed from a reputable distributor of welding and safety products as well as

downstream industrial gas manufacturer and distributor to become a value added integration specialist for our customers in the

marine, oil & gas industries.

Our customers include major oil and gas companies and contractors, shipbuilding and ship repair yards, oil rig, platform, jacket

and floating production storage offloading (FPSO) systems as well as steel and pipeline fabricators from across Asia.

Our customers’ success is fundamental to the way we conduct our business. In fulfilling and anticipating the dynamic business

needs of our customers, we expertly strategise to ensure success in our partnerships. We believe that through proximity to our

customers, premium quality service can be delivered at all times.

Our achievements attest to our consistent delivery of product quality, value and service excellence. We’ve received the Spring

Singapore National Model Company award and accreditations like ISO9001:2000. We’ve also garnered recognition from the

brands we represent, including:

• Evac International Pte Ltd (Licensed Distributor 2006 – 2009)

• Red Wing International (Exclusive Distributor)

• DBI SALA By Capital Safety Group Asia (Top Asia Distributor Award 2008)

• Weiler (Sales Excellence Award 2008)

• Hobart (Outstanding Sales Achievement 2008)

• Miller (Outstanding Sales Achievement 2008)

• OTC Daihen (Sales Achievement Award for OTC XD-500 Welding Machine and OTC Arc Welding Robot 2007 and

First Half 2008)

• Bortech Corporation (Top Performance Award – Number One Distributor in the Asia Pacific Region)

We continue to be a strong and progressive Welding, Gas and Safety integration company; one that cares for the success of its

customers, business partners, staff and shareholders.

About Us

Dear Shareholders

In spite of the global slow down as foreshadowed in my previous

Annual Peport, Leeden Limited achieved its fourth consecutive year of

unprecedented earnings growth in 2008 on the back of strong marine

and offshore, oil and gas activities. The Group’s turnover jumped 53%

to a record of S$157.2 million in FY2008 while the net profit after tax

more than doubled to S$13.6 million in FY2008.

I would like to emphasize that, FY2008 was a challenging year to

operate in as the sub-prime crisis escalated into a full blown global

recession and news of order book cancellations and delays plagued

the marine and offshore industries. Nevertheless, I am very happy to

report that through careful planning and strategic M&A activities, the

Group has successfully navigated through the storm and emerged to

achieve all time high sales and profits.

Our success to date would not have been possible without human

capital, an extremely important element in our business model. I would

like to take the opportunity to applaud our management, marketing

communications, technical product and sales teams who have done

a fantastic job in their consistent efforts to build the ‘Leeden’ brand by

delivering quality customized integrated solutions in our core business

of welding, gas and safety.

...through careful planning and strategic M&A activities, the

Group has successfully navigated through the storm and

emerged to achieve all time high sales and profits. Our success

to date would not have been possible without human capital,

an extremely important element in our business model.

“ “

02

Chairman and CEO’sMessage

03

The Group also made some strategic acquisitions during

the year to enhance its presence in the region and further

complement its industrial operations. Leeden acquired a 55%

stake in Eversafe Extinguisher Sdn Bhd, a well established

Malaysian company which specializes in fire protection

products. The Group also acquired a 75% stake in Power

Weld Sdn Bhd, which is in the business of manufacturing

and distributing quality welding electrodes and welding wires.

By leveraging on Leeden’s established distribution network,

Leeden and its subsidiaries can benefit from mutual synergies

to effectively increase the Group’s presence in Asia.

During the year, the Group also increased its stake in strategic

associate companies, making them subsidiaries, notably

National Industrial Gases Pte Ltd and NIG Industrial Gases Sdn

Bhd.

Moving ForwardAs the global recession deepens, market conditions have

never been more uncertain and trying. However, we still see

opportunities amidst the crisis and have formulated plans and

strategies to face the new challenging environment.

With worries of dwindling global demand, flow of work for new

builds in the offshore and marine segment may see a slow

down. On the other hand, we anticipate yards to do more

conversion and repair jobs and we will tailor our product range

accordingly to service this segment while adding mid-range

products to help customers save costs. Riding on this, we will

continue to penetrate new and existing markets, while growing

our geographical reach in Thailand, Vietnam and Indonesia.

With the recent spate of announcements on fiscal stimulus

plans, the budget for infrastructure spending by governments

across the region has increased tremendously. Hence, we will

expand our revenue streams by broadening our sales channels

to penetrate the infrastructure industry as well. Currently, 40%

of our revenue is derived from our safety and gas products, out

of which, 50% is servicing industries outside the marine and

offshore.

As mentioned, our rich human capital has helped the Group to

grow over the years. Consequently, we will continue to build

the team at Leeden and intend to increase the current team

of management, sales and technical product executives in

line with our expansion plans. On top of this, the Group will

set up new training facilities to upgrade skills of staff to ensure

the provision of world class customer service pertinent to our

success.

Besides working on organic growth, we will also be on the

lookout for more M&A opportunities which may arise amidst

the economic turmoil. Leeden will continue to focus on its core

competencies to be Asia’s leading integration specialist for

welding, gas and safety. At the same time, creating value for

its customers through more comprehensive ‘one-stop’ solution

for welding, gas and safety product needs.

As part of our efforts to focus on what we do best, the property

business will be discontinued subsequent to the completion of

the Paterson Linc project by early 2010.

In AppreciationIn appreciation of the support shown by shareholders, an

interim dividend of net 1 cent per share was declared and

paid on 10 September 2008, doubling the dividend amount

declared and paid in FY2007. The Board does not recommend

a final dividend to be declared for the year ended 31 December

2008.

I would like to thank our longstanding stakeholders, namely

our shareholders, our business associates, loyal customers,

my colleagues on the Board, the management and staff, for

their dedication and support. I sincerely look forward to your

continuous support as we march into the Leeden era with

renewed focus and zeal in the industrial business.

Steven ThamChairman & Chief Executive Officer

7 April 2009

Annual Report 2008

Connecting Expertise and Experience At Leeden, our wealth of expertise and experience gives us the competitive edge as we continue to provide our clients with excellent one-stop services and solutions. The delivery of integrated solutions, together with our commitment towards client satisfaction, has contributed not only to the growth of Leeden, but also to the progress of our customers.

With the winning synergy of expertise and experience, we are able to strengthen Leeden’s foothold in the marine, oil and gas industries.

Welding DivisionOver the years, Leeden has established itself as a leading

integrated solutions provider and consultant in the welding,

gas and safety arena. The Group’s competitive position is

maintained through its provision of value-added welding

products and services, making the business more resilient

through economic downturn.

In spite of the negative business sentiments, the Group

has recognized the crisis as an opportunity to expand its

presence in the region. During the year, Leeden acquired

Power Weld, a leading electrode manufacturer in Malaysia

to further expand its filler metal product range, providing the

Group with an assured source of supply for quality welding

electrodes and welding wires.

The Group has also been awarded a number of new agencies,

one of which is from the FSH Welding Group, specifically

for its welding electrodes under the SelectArc Industries

brand. Other new agencies obtained during the year include

CompAir, a leading manufacturer of compressors in the UK,

Procut, a supplier of high quality carbide burrs and ATA

Tools for it’s range of air and pneumatic tools.

The sale of welding equipments and consumables will

continue to play a major role in the Group’s core business.

Notwithstanding the challenges ahead, the Group will

continue to leverage on its strengths and develop synergies

from its acquisitions in order to better serve our customers.

05

Operations Review

Gas DivisionThe right mix of gases ensures effective welding solutions.

That is why Leeden’s Gas Division is a vital component to

Leeden’s integrated welding solutions. The Group’s gas

business in Singapore, Malaysia and Batam is operated

through the National Industrial Gases Group (NIG Group), a

joint venture with National Oxygen Pte Ltd, which is a wholly

owned subsidiary of Taiyo Nippon Sanso Corporation.

In FY2008, Leeden increased its stake in NIG resulting in the

group of companies operating the gas business, becoming

indirect subsidiaries of the Leeden Group.

As one of the largest downstream industrial gas

manufacturers and distributors in Singapore, Malaysia and

Batam, NIG Group provides the most comprehensive range

of gas and gas-related products and services, including

specialized industrial gases, gas cylinders, gas control

apparatus and gas systems & engineering consultancy

services.

The NIG Group has the largest dissolved acetylene

production capabilities in Singapore, Malaysia and Batam

region. In Malaysia, the NIG Group has an extensive

distribution network with branches spanning from Penang

to Johor Bahru, offering NIG operations in Malaysia

the business agility and efficiency as a key competitive

advantage over other competitors.

Annual Report 2008

06

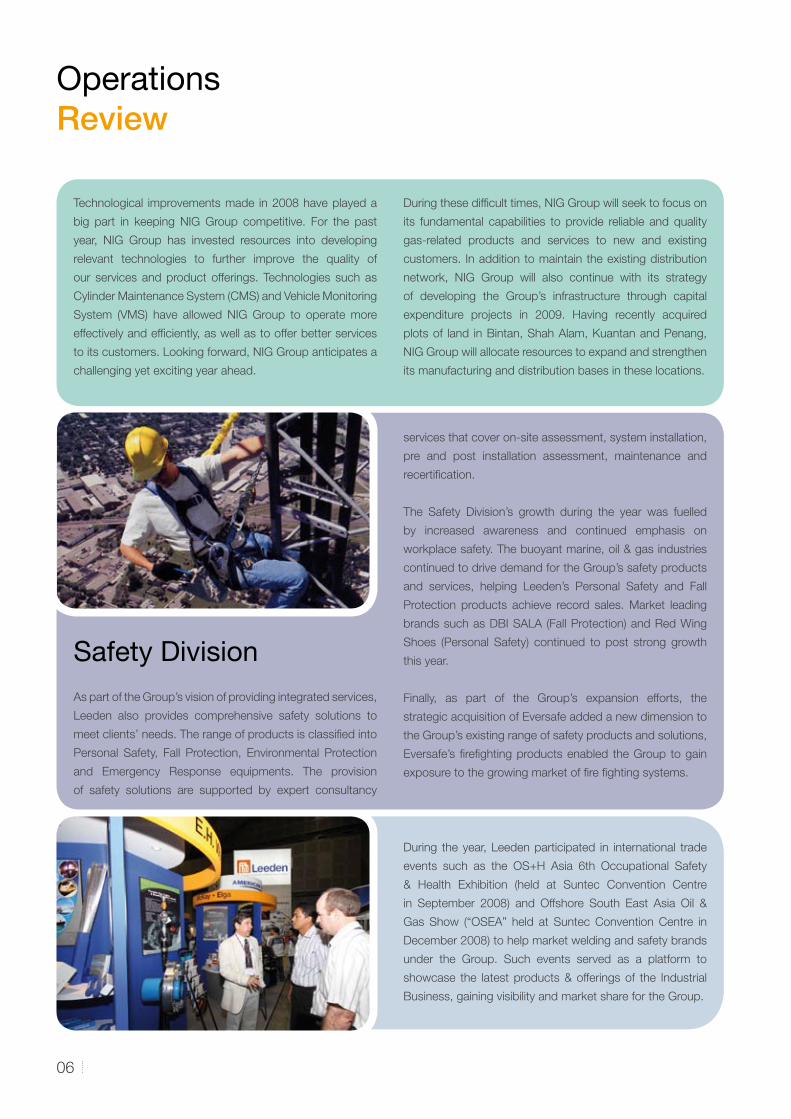

Safety DivisionAs part of the Group’s vision of providing integrated services,

Leeden also provides comprehensive safety solutions to

meet clients’ needs. The range of products is classified into

Personal Safety, Fall Protection, Environmental Protection

and Emergency Response equipments. The provision

of safety solutions are supported by expert consultancy

services that cover on-site assessment, system installation,

pre and post installation assessment, maintenance and

recertification.

The Safety Division’s growth during the year was fuelled

by increased awareness and continued emphasis on

workplace safety. The buoyant marine, oil & gas industries

continued to drive demand for the Group’s safety products

and services, helping Leeden’s Personal Safety and Fall

Protection products achieve record sales. Market leading

brands such as DBI SALA (Fall Protection) and Red Wing

Shoes (Personal Safety) continued to post strong growth

this year.

Finally, as part of the Group’s expansion efforts, the

strategic acquisition of Eversafe added a new dimension to

the Group’s existing range of safety products and solutions,

Eversafe’s firefighting products enabled the Group to gain

exposure to the growing market of fire fighting systems.

Technological improvements made in 2008 have played a

big part in keeping NIG Group competitive. For the past

year, NIG Group has invested resources into developing

relevant technologies to further improve the quality of

our services and product offerings. Technologies such as

Cylinder Maintenance System (CMS) and Vehicle Monitoring

System (VMS) have allowed NIG Group to operate more

effectively and efficiently, as well as to offer better services

to its customers. Looking forward, NIG Group anticipates a

challenging yet exciting year ahead.

During these difficult times, NIG Group will seek to focus on

its fundamental capabilities to provide reliable and quality

gas-related products and services to new and existing

customers. In addition to maintain the existing distribution

network, NIG Group will also continue with its strategy

of developing the Group’s infrastructure through capital

expenditure projects in 2009. Having recently acquired

plots of land in Bintan, Shah Alam, Kuantan and Penang,

NIG Group will allocate resources to expand and strengthen

its manufacturing and distribution bases in these locations.

Operations Review

During the year, Leeden participated in international trade

events such as the OS+H Asia 6th Occupational Safety

& Health Exhibition (held at Suntec Convention Centre

in September 2008) and Offshore South East Asia Oil &

Gas Show (“OSEA” held at Suntec Convention Centre in

December 2008) to help market welding and safety brands

under the Group. Such events served as a platform to

showcase the latest products & offerings of the Industrial

Business, gaining visibility and market share for the Group.

Catalysing Growth and ExcellenceAt Leeden, we constantly seize opportunities to enhance our business segments and deepen our regional network, thus maintaining our position as one of the leading solutions provider in Asia. Alongside growth opportunities, synergistic acquisitions made in FY2008 will continue to boost growth and excellence for Leeden, as well as accelerate progress for our customers.

By making the most of every opportunity, Leeden is able to catalyse growth and excellence.

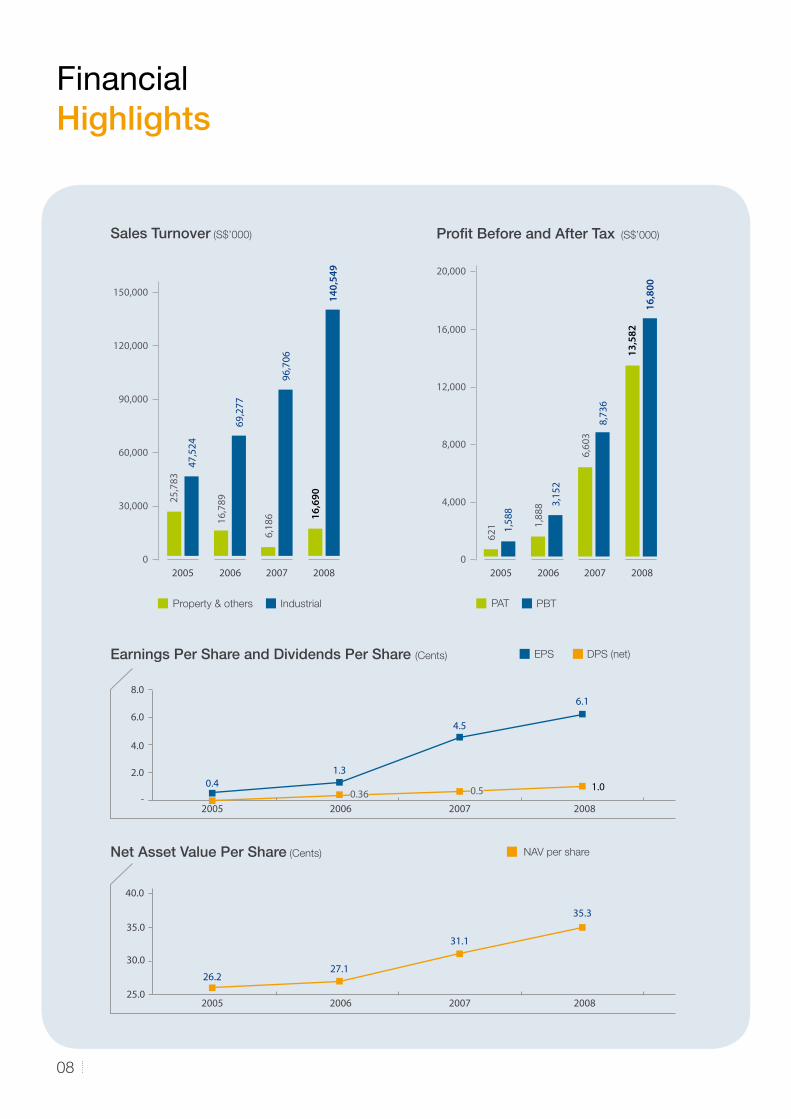

FinancialHighlights

Profit Before and After Tax (S$’000)Sales Turnover (S$’000)

Earnings Per Share and Dividends Per Share (Cents)

8.0

6.0

4.0

2.0

-2005 2006 2007 2008

0.41.3

4.5

6.1

EPS DPS (net)

0.36 0.5 1.0

Net Asset Value Per Share (Cents)

40.0

35.0

30.0

25.0

26.227.1

31.1

35.3

NAV per share

2005 2006 2007 2008

PBTPAT

1,58

8

621

3,15

2

1,88

8

8,73

6

6,60

3

16,800

13,582

200720062005 2008

08

Property & others Industrial

47,524

25,783

69,277

16,789

140,54

9

16,690

96,706

6,18

6

200720062005 20080

30,000

60,000

90,000

120,000

150,000

0

4,000

8,000

12,000

16,000

20,000

In 2008, the Leeden Group continued its growth momentum

to register another year of excellent performance. The Group

achieved a record turnover of S$157.2 million in FY2008, which

is a 53% jump from FY2007 turnover of S$102.9 million.

The Group’s Industrial Business (made up of the welding,

gas, and safety divisions) registered a significant increase in

turnover of 45% from S$96.7 million in FY2007 to S$140.5

million in FY2008 on the back of strong marine and offshore

activities and contribution of S$45.1 million from newly

acquired subsidiaries. Turnover from other businesses, mainly

property development, grew from S$6.2 million in FY2007 to

S$16.7 million in FY2008.

In spite of the challenging economic conditions, overall gross

profit margin remained strong at 28%, with overall gross profit

increasing 49% to S$44.1 million in FY2008.

In line with increased sales revenue, distribution costs grew

38% from S$12.5 million in FY2007 to S$17.2 million. However,

distribution costs as a percentage of sales decreased from 12%

to 11% as a result of economies of scale. While administrative

costs grew 55% from S$5.8 million in FY2007 to S$9.0 million

in FY2008, administrative costs remained constant at 6% of

sales over both years.

Other costs increased by S$1.0 million to S$4.5 million in

FY2008 as the Group adopted a conservative stance on

its profitability and provided a higher allowance for doubtful

debts and stock obsolescence of S$1.8 million in FY2008

as compared to S$0.3 million in FY2007. In addition, there

was an unrealized derivative loss of S$0.7 million recorded in

FY2008, out of which S$0.5 million relates to a USD option

contract that has expired in January 2009 and the unrealized

losses have since been reversed. Other costs as a percentage

of sales remained constant at 3% in both years.

A negative goodwill of S$0.8 million was recognized due to

the acquisition of Eversafe Extinguisher Sdn Bhd (“Eversafe”)

and Power Weld Sdn Bhd (“Power Weld”). Share of profits

from associated companies was 225% higher in FY2008 at

S$1.3 million.

Leeden achieved another year of record earnings with a 106%

jump in profit after taxation to S$13.6 million in FY2008. Profit

attributable to equity holders of the Company grew 59% to

S$10.4 million.

Balance SheetWith the acquisition of new subsidiaries Eversafe, Power

Weld, National Industrial Gas Ptd Ltd (“NIG”), and NIG

Industrial Gases Sdn Bhd (“NIB”), there was a consolidation

of the Group’s balance sheet items as of 31 December 2008,

whereas revenue from these new subsidiaries were recognized

only for the remaining period of the financial year after the

acquisitions.

The Group’s non-current assets grew from S$19.1 million as

at 31 December 2007 to S$60.0 million as at 31 December

2008 mainly due to the acquisition of new subsidiaries which

resulted in higher property, plant and equipment, intangible

assets and goodwill.

Current assets also increased from S$63.5 million as at

31 December 2007 to S$120.8 million as at 31 December

2008 due to a higher stock level which grew from S$17.7

million as at 31 December 2007 to S$46.2 million as at 31

December 2008. The increase in stocks was due to S$12.2

million of stocks held by newly acquired subsidiaries and higher

stock holding was also necessary to provide better services

and prompt deliveries to customers. As such, stock turnover

increased from 93 days in FY2007 to 123 days in FY2008.

Trade debtors also increased from S$28.8 million as at

31 December 2007 to S$48.5 million as at 31 December 2008

due to the acquisition of new subsidiaries which accounted for

S$20.7 million of the trade debts. Trade debtors’ turnover days

improved from 102 days in FY2007 to 86 days in FY2008.

The Group’s current liabilities grew from S$33.3 million as

at 31 December 2007 to S$81.0 million as at 31 December

2008, while non-current liabilities increased from S$3.5 million

as at 31 December 2007 to S$16.5 million as at 31 December

2008. The increase in total liabilities was mainly due to the

consolidation of newly acquired subsidiaries which resulted in

higher amount due to bankers and long-term loans by S$40.8

million to S$51.9 million as at 31 December 2008.

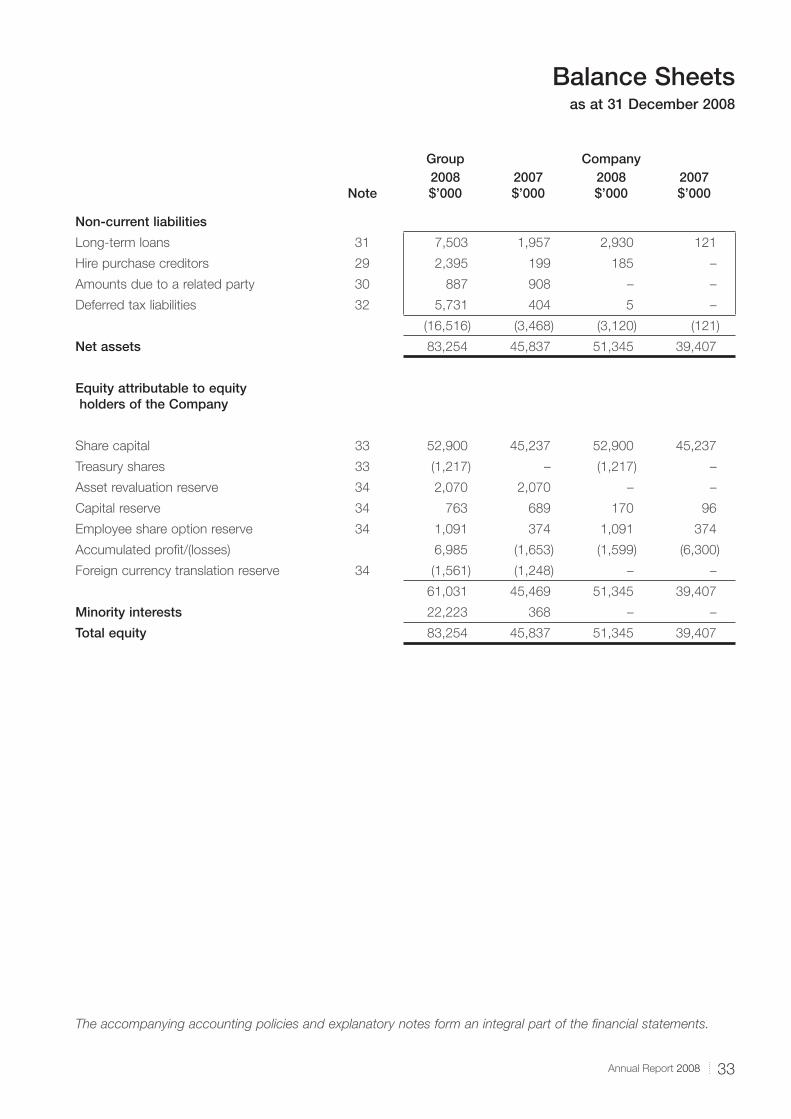

Leeden’s total equity improved from S$45.8 million as at

31 December 2007 to S$83.3 million as at 31 December 2008.

Cash FlowAs at 31 December 2008, the Group had cash and cash

equivalents of S$15.6 million, a 3% improvement from 31

December 2007. As the Group stocked up during the year

to ensure better service and prompt delivery to customers,

net cash provided by operating activities declined from S$14.3

million in FY2007 to S$0.8 million in FY2008.

Due to the Group’s acquisition activities, net cash provided by

financing activities rose to S$20.0 million, while net cash used

in investing activities was S$20.4 million.

FinancialReview

09Annual Report 2008

Board of Directors

Mr Steven Tham appointed on the

Board on 30 June 2000, has been the

Group’s Executive Chairman and Chief

Executive Officer since 27 March 2001.

He was last re-elected on 27 April 2007.

Mr Tham has over 30 years of working

experience in the industrial, banking,

trading, retail and property industries.

He holds a BBA (Hons) and M. Sc

(Real Estate) Degree from the University

of Singapore. He is also a member of

the Chartered Institute of Management

Accountants and the Singapore Institute

of Directors (MSID).

Mr Kelvin Lee was appointed

as Executive Director on 12 August

2004 and has been promoted to the

position of Managing Director & Chief

Operating Officer on 1 October 2007.

He was last re-elected on 25 April 2008.

Mr Lee has over 33 years of experience

in the chemical, metallurgy, welding

and industrial gases industries. He is

currently appointed as a council member

of the board of Singapore Welding

Society and a committee member of

the Asian Industrial Gases Association

and the Industrial Gases Association of

Singapore. He is also a member of the

Singapore Institute of Directors (MSID).

Mr Lee holds a Bachelor of Science

Degree from the University of London.

Mr Lim How Boon is our Executive

Director and has joined the Board since 1

February 1999. He was last re-elected on

25 April 2008. Mr Lim is an accountant

by profession and is a Fellow (FCPA)

of the Institute of Certified Public

Accountants of Singapore (ICPAS). He

has accumulated more than 40 years

of working experience covering the

insurance, hotel, leisure, retail, property,

building and construction industries.

Mr Lim is also an active community

leader and has been commended twice

by the Singapore Government, having

being awarded the Public Service Medal

(PBM) and Public Service Star (BBM)

in 1980 and 1990 respectively. He is

currently a member of the Singapore

Institute of Directors (MSID).

Mr Leslie Struys has served on

the Board as a Non-Executive and

Independent Director since 30 June

1993. Mr Struys was appointed as the

Lead Independent Director on 1 January

2006. He was last re-elected onto the

Board on 25 April 2008. He is currently

the Chairman of both the Remuneration

Committee and Nominating Committee

and a member of the Audit Committee.

Mr Struys graduated from the University

of Malaya in 1960 with a Bachelor of

Arts Degree in Economics. He also

sits on the Board of Fraser & Neave

Holdings Bhd, a Malaysian Company

listed on the Bursa Malaysia Securities

Berhad, as the Senior Independent and

Non-Executive Director.

10

Mr Tony Chan Wing Khei was

appointed as a Non-Executive and

Independent Director since 1 March

1997. He was last re-elected on 28 April

2006. He serves as the Chairman of

the Audit Committee and is a member

of the Remuneration Committee and

Nominating Committee. Mr Chan has

over 30 years of experience in the

construction and property industries

both in Singapore and Malaysia. Mr Chan

is a civil engineer having graduated

from the Royal Melbourne Institute of

Technology.

Mr Loh Weng Whye was appointed

as an Independent Director on 7

February 2005 and last re-elected on 27

April 2007. He is a member of both the

Audit and Remuneration Committees.

Mr Loh is a veteran in infrastructure

development and energy business in

Singapore and the region, with over

35 years of experience in senior and

corporate-level appointments with

the civil service, government-linked

companies and the private sector.

Under the Public Utilities Board, he

headed Generation Projects responsible

for the management and commissioning

of power station projects worth more

than S$3 billion. He was also the

founding General Manager (Projects) of

Tuas Power Ltd. Mr Loh was formerly

President of ST Energy Pte Ltd and

SembCorp Energy Pte Ltd. He was

appointed Advisor to Green Dot Capital,

an investment and holding company

under Temasek Holdings. Currently,

Mr Loh sits on the boards of four SGX

mainboard-listed companies. He was

appointed Senior Adivisor by YTL Power

International for the bidding for the three

Singapore gencos and the S$3.8 billion

acquisition of PowerSeraya Ltd. He also

holds advisory appointments in external

councils and institutions of tertiary

education. Holding MSc. (Industrial Eng.)

and B Eng. (Mechanical) Degree, he is

a Professional Engineer (Singapore), a

Member of the Singapore Institute of

Directors, and was elected a Fellow of

the Institution of Engineers Singapore in

1995.

Mr Hendra Harjadi was appointed as

Non-Executive Director on 3 May 2004.

He was last re-elected on 27 April 2007.

Mr Harjadi is the Managing Director of

various companies in Indonesia and has

over 30 years of experience managing

companies in the oil and gas and retail

industries. Mr Harjadi holds a Bachelor

of Arts Degree from the Universitas

Methodist Indonesia.

11Annual Report 2008

From Left

Mr Steven Tham

Mr Kelvin Lee

Mr Lim How Boon

Mr Leslie Struys

Mr Tony Chan

Mr Loh Weng Whye

Mr Hendra Harjadi

12

Management Team

Mr Edwin Chow joined American

Dynamics Pte Ltd in January 2008 as

General Manager in charge of Welding

Business in the Singapore, Malaysia

and Batam. Mr Chow holds a Diploma

in Marketing and also a Diploma in

Marine Engineering. He has over

20 years of experience in marketing

welding equipment and consumables

in the shipbuilding and oil & gas related

industries.

Mr Robert Goh has been with the

Group since 1978 and is currently the

General Manager of National Industrial

Gases Pte Ltd, heading the Gas

Business in Singapore and Batam. Mr

Goh has over 30 years of operations

and sales experience in the oil and gas

related industries.

Mr Philip Chan is the Assistant

General Manager in charge of the Safety

Business in Singapore as well as in the

Asia region. He has been with the Group

since 1990. Mr Chan holds a Master

of Business Administration Degree from

the University of Birmingham. He is

responsible for increasing sales and

profitability of the Safety Business in the

region.

Mr Alex Ong joined the Company

in February 2008 as Head of Welding

Consumables, Market Development

Division. Mr Ong holds a Bachelor of

Science in Business Administration from

TUE, Philippines with extensive regional

sales and marketing exposure over the

past 25 years. He is responsible for

developing the Asia market for welding

consumables.

Mr Tan Kean Hooi has been the

General Manager of NIG Gases Sdn

Bhd since 1993 and is responsible

for the Gas Business in the central

region of Malaysia. He holds a Bachelor

Degree in Architecture from University

of Strathclyde, and a Housing, Building

Planning Degree from University Science

Malaysia (USM).

Mr Cheang Fook Sam is the

General Manager of Hercules Machinery

Gases Sdn Bhd and NIG Utara Sdn Bhd.

With more than 30 years of industrial

sales experience, he is responsible for

the gas and equipment sales activities in

the northern region of Malaysia.

Mr Tan Lian Khar is the Managing

Director and one of the co-founders

of Eversafe Extinguisher Sdn Bhd

(“Eversafe”). He is responsible for the

overall growth and profitability of

Eversafe.

Mr Dennis Teo is the Operations

Director of Power Weld Sdn Bhd and

has more than 20 years of experience

in the manufacturing and marketing of

welding electrodes and consumables in

Malaysia.

Ms Fang Lee Wei is the Group

Financial Controller. She joined the

Group in 2006 and has more than

10 years of experience in financial

management and accounting. Ms

Fang holds a Master of Commerce in

International Business Degree from the

University of New South Wales and is a

member of the Institute of Certified Public

Accountants of Singapore (ICPAS).

She is responsible for all aspects of

financial and accounting management

of the Group, including treasury, internal

control and tax matters.

Ms Iris Yap is the Senior Manager

of Corporate Services and the Group’s

Company Secretary. She has been

with the Group for over 20 years and

oversees the corporate secretarial,

legal and general administration of

the Group. Ms Yap holds a Bachelor in

Business Administration Degree from La

Trobe University, Australia. She is Fellow

(FCIS) of the Institute of Chartered

Secretaries and Administrators (ICSA)

and the Singapore Associations of the

Institute of Chartered Secretaries and

Administrators (SAICSA).

13Annual Report 2008

Corporate Governance Report

Leeden Limited (the “Company” or “Leeden” or “Group”) continues to be committed to observing high standards

of corporate governance by complying with the Singapore Code of Corporate Governance (the “Code”).

For effective corporate governance, the Company has put in place various self-regulatory and monitoring

mechanisms. This Report outlines the Company’s corporate governance practices and structures that were in

place for the fi nancial year 2008.

BOARD OF DIRECTORS

Principle 1 : Board’s Conduct of its Affairs

The Board of Directors (the “Board”) holds at least two scheduled meetings a year with ad-hoc meetings being

convened as and when necessary. During the year, the Board met four times.

The principal roles of our Board are as follows:-

Formulating and approving the Group’s policies, strategies and fi nancial objectives;

Approving annual budgets, major funding proposals, investment and divestment proposals;

Overseeing the processes for evaluating the adequacy of risk management, internal controls, fi nancial

reporting and compliance;

Reviewing and approving any interested person transactions;

Approving the nomination of board members and the appointment of key executives;

Reviewing and endorsing the recommended framework of remuneration for the Board and key executives;

Setting values and standards of the Company and ensuring that obligations to shareholders are understood;

and

Assuming responsibilities for compliance with Corporate Governance.

The Board of Directors is obliged to act in good faith and will consider at all times, the interest of the Company.

The Company has adopted a set of Approving Authority & Limit, setting out the level of authorization required for

specifi ed transactions, including those that require Board approval.

To assist the Board in executing its responsibilities, the Board is supported by the Audit Committee, Nominating

Committee and Remuneration Committee. These Committees function within clear defi ned terms of reference,

which are reviewed on a regular basis, to ensure effectiveness of each Committee.

Upon appointment of a director, orientation program is organized for the newly appointed director to ensure that

incoming director is familiar with the Company’s business activities and directions of the Group. The Company will

consider relevant training for the directors, from time to time. Relevant courses include seminars conducted by the

Singapore Institute of Director or other training institute. During the year under review, the Directors visited one of

the overseas plants to understand the operations and provide strategic guidance.

A formal letter is provided to each newly-appointed Director, explaining their statutory and other duties and

responsibilities as a director.

Corporate Governance Report

14

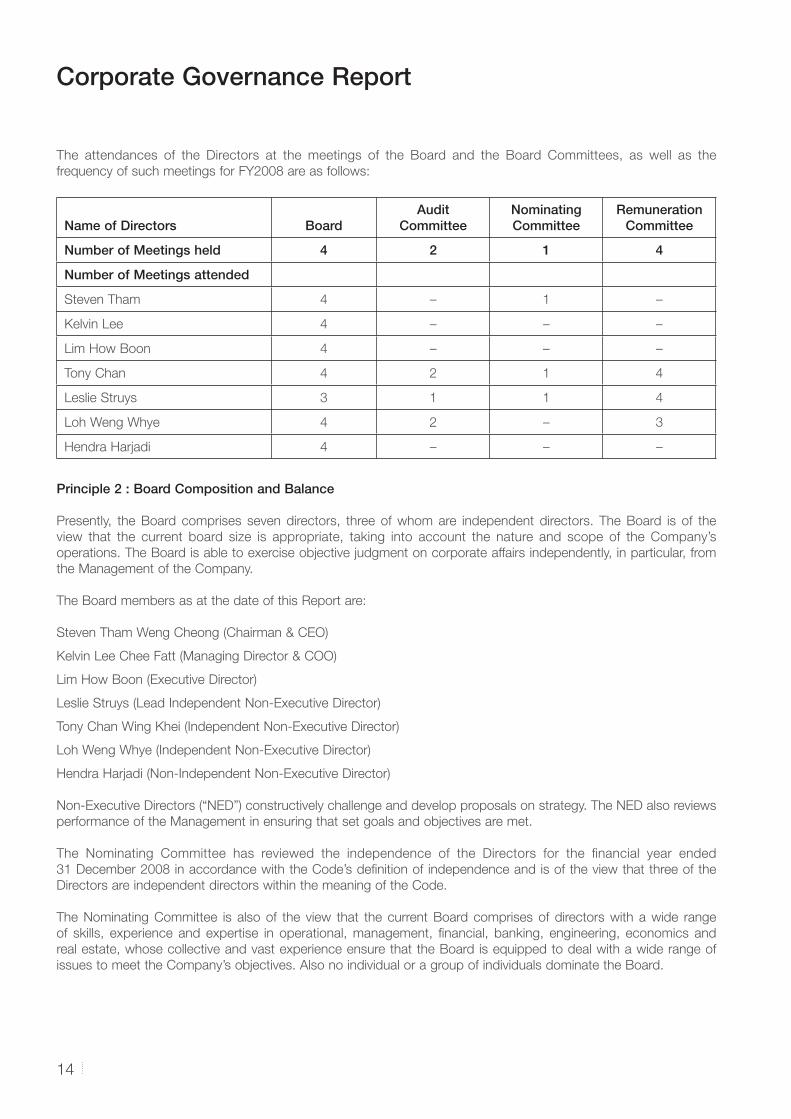

The attendances of the Directors at the meetings of the Board and the Board Committees, as well as the

frequency of such meetings for FY2008 are as follows:

Name of Directors BoardAudit

CommitteeNominating Committee

Remuneration Committee

Number of Meetings held 4 2 1 4

Number of Meetings attended

Steven Tham 4 – 1 –

Kelvin Lee 4 – – –

Lim How Boon 4 – – –

Tony Chan 4 2 1 4

Leslie Struys 3 1 1 4

Loh Weng Whye 4 2 – 3

Hendra Harjadi 4 – – –

Principle 2 : Board Composition and Balance

Presently, the Board comprises seven directors, three of whom are independent directors. The Board is of the

view that the current board size is appropriate, taking into account the nature and scope of the Company’s

operations. The Board is able to exercise objective judgment on corporate affairs independently, in particular, from

the Management of the Company.

The Board members as at the date of this Report are:

Steven Tham Weng Cheong (Chairman & CEO)

Kelvin Lee Chee Fatt (Managing Director & COO)

Lim How Boon (Executive Director)

Leslie Struys (Lead Independent Non-Executive Director)

Tony Chan Wing Khei (Independent Non-Executive Director)

Loh Weng Whye (Independent Non-Executive Director)

Hendra Harjadi (Non-Independent Non-Executive Director)

Non-Executive Directors (“NED”) constructively challenge and develop proposals on strategy. The NED also reviews

performance of the Management in ensuring that set goals and objectives are met.

The Nominating Committee has reviewed the independence of the Directors for the fi nancial year ended

31 December 2008 in accordance with the Code’s defi nition of independence and is of the view that three of the

Directors are independent directors within the meaning of the Code.

The Nominating Committee is also of the view that the current Board comprises of directors with a wide range

of skills, experience and expertise in operational, management, fi nancial, banking, engineering, economics and

real estate, whose collective and vast experience ensure that the Board is equipped to deal with a wide range of

issues to meet the Company’s objectives. Also no individual or a group of individuals dominate the Board.

15Annual Report 2008

Corporate Governance Report

Principle 3 : Role of Chairman and Chief Executive Offi cer (“CEO”)

The Board is of the view that it is in the best interest of the Group to adopt a single leadership structure,

whereby the CEO and Chairman of the Board is the same person, so as to ensure that the decision-making

process of the Group would be unnecessarily hindered. Mr Steven Tham continues to be the Chairman and CEO

of the Group. The Board is of the opinion that suffi cient checks and safeguards are in place to ensure that the

process of decision making is independent and based on collective decisions without any individual exercising

any considerable power or infl uence. As the Chairman, Mr Tham is responsible for the workings of the Board

and ensuring compliance with the Group’s guidelines on corporate governance. He exercises control over the

accuracy and timeliness of the information that the Directors receive. He facilitates effective contributions of the

NEDs in particular and encourages constructive relationships between Executive Directors and NEDs. As the CEO,

Mr Tham plays a pivotal role in the development and execution of policies and strategies and the day-to-day

management of the Group.

With the appointment of Mr Leslie Struys as the Company’s lead independent director, shareholders will have an

alternative avenue to raise their concerns, especially when contacts through the normal channels of the Chairman/

CEO have failed or when such contact is inappropriate.

BOARD COMMITTEES

Principle 4 : Board Membership

Nominating Committee (NC)

The NC comprises of three Directors, majority of whom are independent and non-executive. In addition, the

Chairman of the NC is not, and not directly associated with, a substantial shareholder.

The members of the NC as at the date of this report are:-

Mr Leslie Struys Chairman (Independent Non-Executive)

Mr Tony Chan (Independent Non-Executive)

Mr Steven Tham

The NC met once during the fi nancial year to evaluate Board’s performance as guided by the Terms of Reference

adopted by the NC on 11 August 2006.

The principal duties and responsibilities include:

Making recommendations to the Board on the appointment of new executive and non-executive Directors;

Determining annually whether or not a Director is independent as well as put in place plans for succession,

in particular for the Chairman and Chief Executive Offi cer;

Recommending Directors who are retiring by rotation to be put forward for re-election;

Deciding whether or not a Director is able to and has been adequately carrying out his duties as a Director

of the Company; and

Evaluating the performance and effectiveness of the Board as a whole.

Corporate Governance Report

16

In accordance with the Company’s Articles of Association, one-third of the Board is subject to re-election annually.

For this forthcoming Annual General Meeting, Mr Steven Tham Weng Cheong and Mr Hendra Harjadi will retire by

rotation. Mr Leslie Struys and Mr Tony Chan Wing Khei will retire pursuant to S153(6) of the Companies Act, Cap.

50. The NC had recommended Mr Steven Tham Weng Cheong, Mr Hendra Harjadi, Mr Leslie Struys and Mr Tony

Chan Wing Khei for re-election at the forthcoming Annual General Meeting.

Having considered their performance and contributions, the Board accepted the NC’s recommendation and

accordingly, Mr Steven Tham Weng Cheong, Mr Hendra Harjadi, Mr Leslie Struys and Mr Tony Chan Wing Khei

will be offering themselves for re-election at the forthcoming Annual General Meeting.

When the need for a new director arises, Nominating Committee will review the expertise, skills and attributes on

the Board, identify its needs and shortlist candidates with appropriate profi le for nomination and re-nomination.

The search will be through search companies, contacts and recommendation.

Principle 5 : Board Performance

The NC, in considering the re-appointment of any Director, evaluates the performance of the Director. Subsequent

to fi nancial year-end, the Board initiated an evaluation to assess the effectiveness of the Board as a whole in

FY2008 which requires the completion of a questionnaire. The assessment parameters include attendance record

at meetings of the Board and Board Committees, participation at meetings and contributions. Board performance

criteria will not change from year to year unless circumstances deem it necessary. The Board would continue the

evaluation into this fi nancial year and address the fi ndings accordingly. While the NC has continued monitoring the

contribution of individual Directors (such as meeting attendance, performance during meetings and how much

effort and time devoted etc), a more formal and appropriate/acceptable process of doing so would take some time

to evolve.

Principle 6 : Access to Information

Board members are provided with quarterly fi nancial reports and are furnished with relevant information from

time to time on material transactions to enable them to make informed decision. Board papers are circulated for

meetings of the Board and Committees in advance, to enable the Directors to review the information and obtain

further explanations, where necessary.

Directors have the discretion, whether as a group or individually, to obtain independent professional advice on any

matter in the furtherance of their duties as directors, at the Company’s expenses.

The Directors have separate and independent access to the Company Secretary and senior management of the

Company at all times. The Company Secretary attends the board meetings and assists the Board in ensuring

that established Board procedures are followed and all relevant statutes and regulations that are applicable to the

Company are complied with.

The Board is accountable to the shareholders and oversees the management of the business and affairs of the

Group.

17Annual Report 2008

Corporate Governance Report

Principle 7 : Procedures for Developing Remuneration PoliciesPrinciple 8 : Level of Mix of RemunerationPrinciple 9 : Disclosure on Remuneration

Remuneration Committee

The Remuneration Committee (RC) comprises of three independent non-executive members. Mr Leslie Struys is

the Chairman for the RC. The members of the RC as at the date of this Report are as follows:

Mr Leslie Struys Chairman (Independent Non-Executive)

Mr Tony Chan (Independent Non-Executive)

Mr Loh Weng Whye (Independent Non-Executive)

The primary role of RC, guided by the Terms of Reference adopted on 11 August 2006, is to review and approve

recommendations on remuneration including but not limited to directors’ fees, salaries, allowances, bonuses, share

options and benefi ts-in-kind. The RC met 4 times last year. The RC has access to professional advice both from

the internal human resource personnel and external remuneration professionals. The RC does not participate in

any decisions concerning their own remuneration package.

RC has adopted a framework for reviewing the remuneration of non-executive directors. It consists of a base fee,

membership fee for Board Committee as well as fees for being the Chairman of Board Committee. Amount of

time and level of responsibilities are taken into account when reviewing the remuneration. Fees for non-executive

Directors are subject to shareholders’ approval at the Company’s Annual General Meeting. Executive Directors are

not entitled to base fees or fees for membership of Board Committee. The remuneration packages for Executive

Chairman and Executive Directors consist of a performance bonus based on the Group’s profi tability. The RC

also ensures that the remuneration of the Executive Chairman and Executive Directors is on par with the industrial

standards and comparable companies.

The RC’s principle functions are to:

1. Review and recommend to the Board in consultation with the Chairman and CEO a remuneration framework

so as to determine a specifi c remuneration package and employment terms for each of the executive

directors and key management executives of the Group;

2. Recommend to the Board in consultation with the Chairman and CEO a share option scheme or long term

incentive schemes from time to time;

3. Ensure that all aspects of remunerations are covered which include directors’ fee, salaries, allowances,

bonuses, share options and benefi ts-in-kind; and

4. Compare the remuneration packages of directors within the industry and comparable companies so as

to fi nd a meaningful way of assessing the performance of individual executive directors. The remuneration

packages shall include a performance-related element.

The RC administers the Ace Dynamics Share Option Scheme and Leeden Share Option Scheme 2007, which

were approved by shareholders on 19 February 2000 and 8 August 2007, respectively.

Corporate Governance Report

18

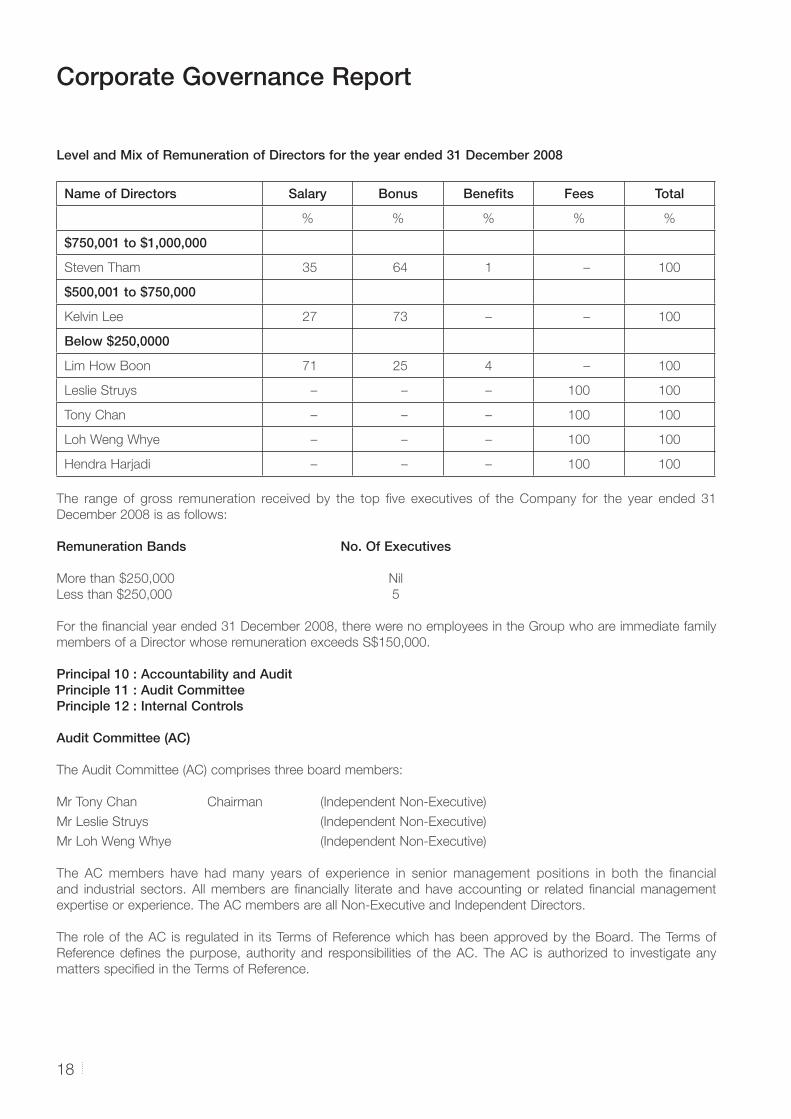

Level and Mix of Remuneration of Directors for the year ended 31 December 2008

Name of Directors Salary Bonus Benefi ts Fees Total

% % % % %

$750,001 to $1,000,000

Steven Tham 35 64 1 – 100

$500,001 to $750,000

Kelvin Lee 27 73 – – 100

Below $250,0000

Lim How Boon 71 25 4 – 100

Leslie Struys – – – 100 100

Tony Chan – – – 100 100

Loh Weng Whye – – – 100 100

Hendra Harjadi – – – 100 100

The range of gross remuneration received by the top fi ve executives of the Company for the year ended 31

December 2008 is as follows:

Remuneration Bands No. Of Executives

More than $250,000 Nil

Less than $250,000 5

For the fi nancial year ended 31 December 2008, there were no employees in the Group who are immediate family

members of a Director whose remuneration exceeds S$150,000.

Principal 10 : Accountability and AuditPrinciple 11 : Audit CommitteePrinciple 12 : Internal Controls

Audit Committee (AC)

The Audit Committee (AC) comprises three board members:

Mr Tony Chan Chairman (Independent Non-Executive)

Mr Leslie Struys (Independent Non-Executive)

Mr Loh Weng Whye (Independent Non-Executive)

The AC members have had many years of experience in senior management positions in both the fi nancial

and industrial sectors. All members are fi nancially literate and have accounting or related fi nancial management

expertise or experience. The AC members are all Non-Executive and Independent Directors.

The role of the AC is regulated in its Terms of Reference which has been approved by the Board. The Terms of

Reference defi nes the purpose, authority and responsibilities of the AC. The AC is authorized to investigate any

matters specifi ed in the Terms of Reference.

19Annual Report 2008

Corporate Governance Report

During the fi nancial year, the AC met twice and performed the following key functions:

Reviews with the internal auditors, the scope and the results of internal audit procedures and their evaluation

of the overall internal control systems and any signifi cant fi ndings;

Reviews with the external auditors, their audit plan, risk assessment, fi ndings for the external audit process

and any other relevant matters;

Reviews signifi cant fi nancial reporting issues and judgments to ensure the integrity of the fi nancial

statements and any formal announcements in relation to fi nancial performance;

Reviews the interim and annual fi nancial statements before submission to the Board for release to SGX-ST;

Reviews and makes recommendations to the Board on the appointment of external auditors;

Reviews interested person transactions, if any, as set out in the Listing Rules of SGX-ST; and

Reviews all non-audit services provided by the fi rm of external auditors, if any, to determine if the provision

of such services would affect the independence of the external auditors.

The AC has the express power to conduct or authorize investigations into any matters within its terms of reference,

has full access to and co-operation by the Management and full discretion to invite any Director or executive

offi cer to attend its meetings. All major fi ndings and recommendations are brought to the attention of the Board of

Directors.

In performing its functions, the AC also meets with external auditors without the presence of the Company’s

management at least once annually. Such meetings allow for a more open discussion on any issues of concerns.

During the year, AC has reviewed the effectiveness of the Group’s material internal controls, including fi nancial and

operational compliance controls, and risk management. The processes used by the AC to review the effectiveness

of the system of internal control and risk management include discussions with management and auditors on the

risks identifi ed and the review of signifi cant issues arising there from.

The AC, having reviewed all non-audit services provided by the external auditors to the Group, is satisfi ed that the

nature and extent of such services would not affect the independence of the external auditors.

The Directors are of the opinion that, in the absence of any evidence to the contrary, the system of internal controls

provides reasonable, but not absolute, assurance that the Group will not be adversely affected by any event that

could reasonably be foreseen as it strives to achieve its business objectives.

Whistle Blowing Policy

The Company has adopted a Policy and Procedure on Whistle Blowing. The Company has provided employees

with well-defi ned and accessible channels within the Group to raise concerns about possible improprieties in

matters of fi nancial reporting such as fraud, corruption or other matters. Upon receipt of such complaint, the AC

would exercise discretion on how to proceed with the investigation, thereafter recommend necessary actions to be

taken.

The AC has received no complaints as at the date of this report.

Corporate Governance Report

20

Principle 13 : Internal Audit

The Company has outsourced its internal audit function to a certifi ed public accounting fi rm. The internal auditors

plan its internal audit schedules in consultation with, but independent of the Management. The audit plan is

submitted to the AC for approval prior to the commencement of the internal audit. With the assistance of the

AC, the Board reviews the effectiveness of the Company’s internal control on an on-going basis, provides its

perspective on management control and ensures appropriate actions when required.

The internal auditors comply with the Standards for the Professional Practice of Internal Auditing developed by the

Institute of Internal Auditors.

COMMUNICATION WITH SHAREHOLDERS

Principle 14 : Communication with ShareholdersPrinciple 15 : Promoting Greater Participation by Shareholders

In complying with the Code:-

All information as required under the Singapore Exchange’s disclosure policy is disseminated to shareholders

through the SGXNET on a timely basis and the Company does not practice selective disclosure;

Price sensitive announcement including interim and full-year results are released through SGXNET within the

mandatory period;

The Annual Report is sent to all shareholders of the Company at least 14 days before the meeting and the

Notice of Annual General Meeting (“AGM”) is made available on SGX-ST’s website;

Members of the Board and various Board committees together with the External Auditor are present and

available to address questions at the AGM;.

Members of the Company are encouraged to attend the AGM and in the event that the member cannot

attend the AGM, the Articles of Association of the Company allow a member to appoint one or two proxies

to attend and vote on behalf of the member. At the AGM, shareholders are given the opportunity to voice

their constructive views and direct questions regarding the Group to the Management or the Directors,

including the Chairmen of the Audit Committee, Remuneration Committee and Nominating Committee; and

All the resolutions at the AGM are single item resolutions.

DEALINGS WITH SECURITIES[SGX-ST Listing Rule 1207 (18)]

The Company has adopted an internal code to provide guidance with regards to dealings in the Company’s

securities by Directors and senior offi cers of the Group.

The guideline sets out window periods where trading in the Company’s securities are not allowed. Directors and

senior offi cers are also expected to observe insiders trading laws at all times even when dealing in securities

outside the window periods. They are also discouraged from dealing in the Company’s share on short-term

considerations. Directors and senior offi cers are required to report to the Company Secretary whenever they deal

in the Company’s shares.

21Annual Report 2008

Corporate Governance Report

RISK MANAGEMENT

Although the Board does not have a risk management committee, the management reviews the Company’s

business and operational activities on a regular basis to identify areas of business risks as well as appropriate

control measures to mitigate these risks. Any signifi cant matters detected by the management are reported to the

Directors. The Group continues to review on an on-going basis, succession plans and other employees-related

issues in an effort to recruit and retain skilled and experienced workforce necessary for its operation The Group’s

fi nancial risk management is discussed under Note 39 to the Notes to the Financial Statements on pages 92 to

97.

MATERIAL CONTRACTS[SGX-ST Listing Rule 1207 (8)]

No material contracts were entered into between the Company or any of its subsidiaries involving the interest of

the CEO or any director or controlling shareholder of the Company or their associates, either still subsisting by end

of the fi nancial year or if not then subsisting, entered into since the end of the previous fi nancial year.

INTERESTED PERSON TRANSACTIONS

The Company has adopted an internal policy governing procedures for the identifi cation, approval and monitoring

of transactions with interested persons. All interested person transaction is subject to review by the AC.

During the fi nancial year, there was no interested person transactions entered into by the Group.

Directors’ Report

22

The Directors are pleased to present their report to the members together with the audited consolidated fi nancial

statements of Leeden Limited (the “Company”) and its subsidiary companies (collectively, the “Group”) and the

balance sheet and statement of changes in equity of the Company for the fi nancial year ended 31 December

2008.

Directors

The Directors of the Company in offi ce at the date of this report are :

Steven Tham Weng Cheong

Kelvin Lee Chee Fatt

Lim How Boon

Leslie Struys

Tony Chan Wing Khei

Loh Weng Whye

Hendra Harjadi

Arrangements to enable Directors to acquire shares and debentures

Other than Leeden Share Option Scheme 2007 and Ace Dynamics Share Option Scheme, neither at the end of

nor at any time during the fi nancial year, was the Company a party to any arrangement whose objects are, or one

of whose object is, to enable the Directors of the Company to acquire benefi ts by means of the acquisition of

shares or debentures of the Company or any other body corporate.

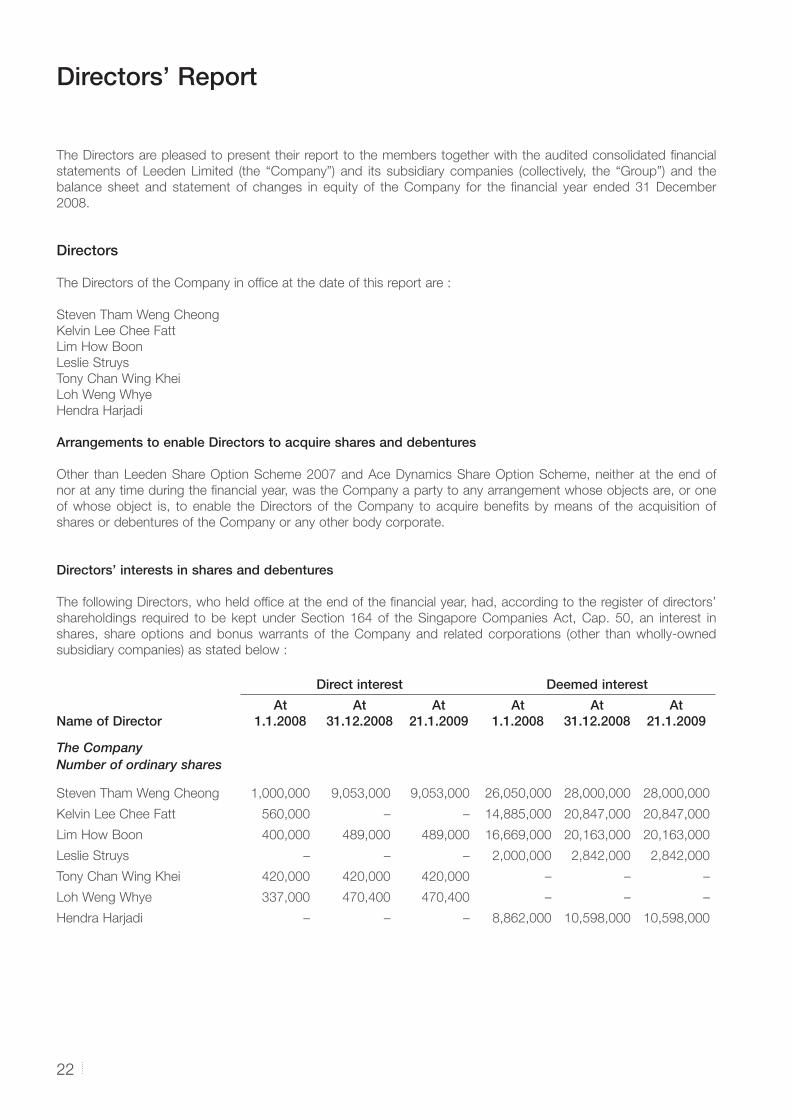

Directors’ interests in shares and debentures

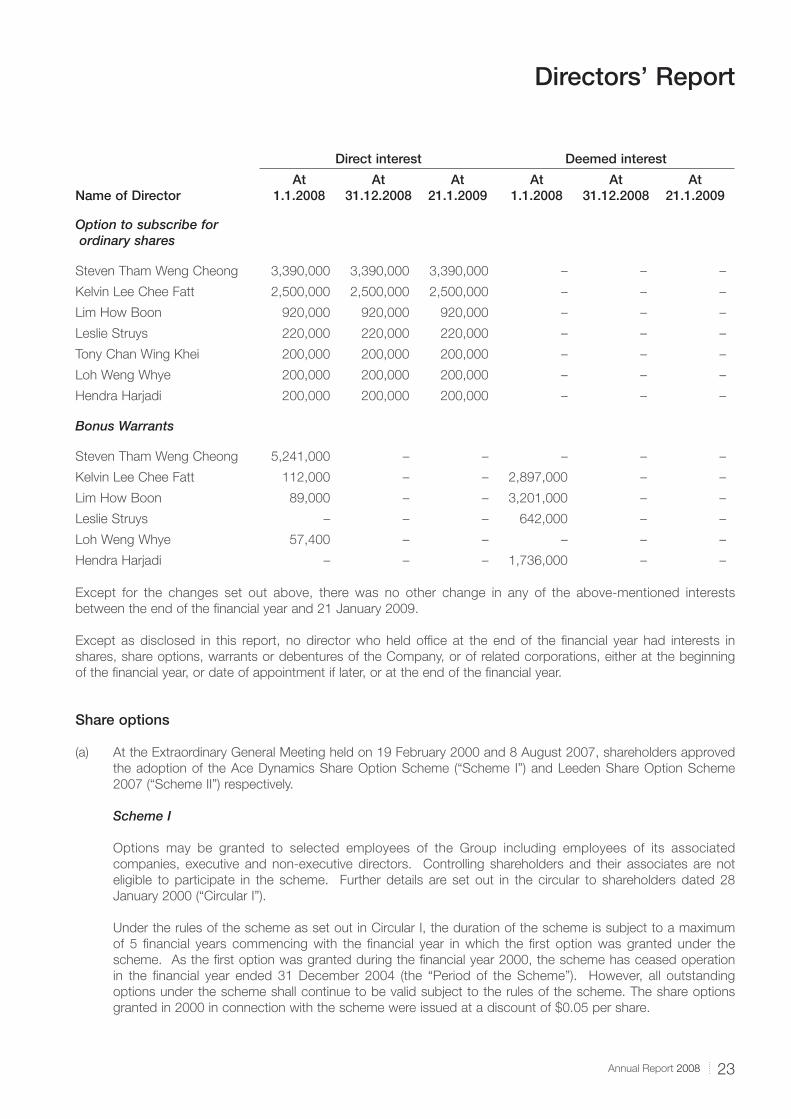

The following Directors, who held offi ce at the end of the fi nancial year, had, according to the register of directors’

shareholdings required to be kept under Section 164 of the Singapore Companies Act, Cap. 50, an interest in

shares, share options and bonus warrants of the Company and related corporations (other than wholly-owned

subsidiary companies) as stated below :

Direct interest Deemed interest

Name of DirectorAt

1.1.2008At

31.12.2008At

21.1.2009At

1.1.2008At

31.12.2008At

21.1.2009

The CompanyNumber of ordinary shares

Steven Tham Weng Cheong 1,000,000 9,053,000 9,053,000 26,050,000 28,000,000 28,000,000

Kelvin Lee Chee Fatt 560,000 – – 14,885,000 20,847,000 20,847,000

Lim How Boon 400,000 489,000 489,000 16,669,000 20,163,000 20,163,000

Leslie Struys – – – 2,000,000 2,842,000 2,842,000

Tony Chan Wing Khei 420,000 420,000 420,000 – – –

Loh Weng Whye 337,000 470,400 470,400 – – –

Hendra Harjadi – – – 8,862,000 10,598,000 10,598,000

23Annual Report 2008

Directors’ Report

Direct interest Deemed interest

Name of DirectorAt

1.1.2008At

31.12.2008At

21.1.2009At

1.1.2008At

31.12.2008At

21.1.2009

Option to subscribe for ordinary shares

Steven Tham Weng Cheong 3,390,000 3,390,000 3,390,000 – – –

Kelvin Lee Chee Fatt 2,500,000 2,500,000 2,500,000 – – –

Lim How Boon 920,000 920,000 920,000 – – –

Leslie Struys 220,000 220,000 220,000 – – –

Tony Chan Wing Khei 200,000 200,000 200,000 – – –

Loh Weng Whye 200,000 200,000 200,000 – – –

Hendra Harjadi 200,000 200,000 200,000 – – –

Bonus Warrants

Steven Tham Weng Cheong 5,241,000 – – – – –

Kelvin Lee Chee Fatt 112,000 – – 2,897,000 – –

Lim How Boon 89,000 – – 3,201,000 – –

Leslie Struys – – – 642,000 – –

Loh Weng Whye 57,400 – – – – –

Hendra Harjadi – – – 1,736,000 – –

Except for the changes set out above, there was no other change in any of the above-mentioned interests

between the end of the fi nancial year and 21 January 2009.

Except as disclosed in this report, no director who held offi ce at the end of the fi nancial year had interests in

shares, share options, warrants or debentures of the Company, or of related corporations, either at the beginning

of the fi nancial year, or date of appointment if later, or at the end of the fi nancial year.

Share options

(a) At the Extraordinary General Meeting held on 19 February 2000 and 8 August 2007, shareholders approved

the adoption of the Ace Dynamics Share Option Scheme (“Scheme I”) and Leeden Share Option Scheme

2007 (“Scheme II”) respectively.

Scheme I

Options may be granted to selected employees of the Group including employees of its associated

companies, executive and non-executive directors. Controlling shareholders and their associates are not

eligible to participate in the scheme. Further details are set out in the circular to shareholders dated 28

January 2000 (“Circular I”).

Under the rules of the scheme as set out in Circular I, the duration of the scheme is subject to a maximum

of 5 fi nancial years commencing with the fi nancial year in which the fi rst option was granted under the

scheme. As the fi rst option was granted during the fi nancial year 2000, the scheme has ceased operation

in the fi nancial year ended 31 December 2004 (the “Period of the Scheme”). However, all outstanding

options under the scheme shall continue to be valid subject to the rules of the scheme. The share options

granted in 2000 in connection with the scheme were issued at a discount of $0.05 per share.

Directors’ Report

24

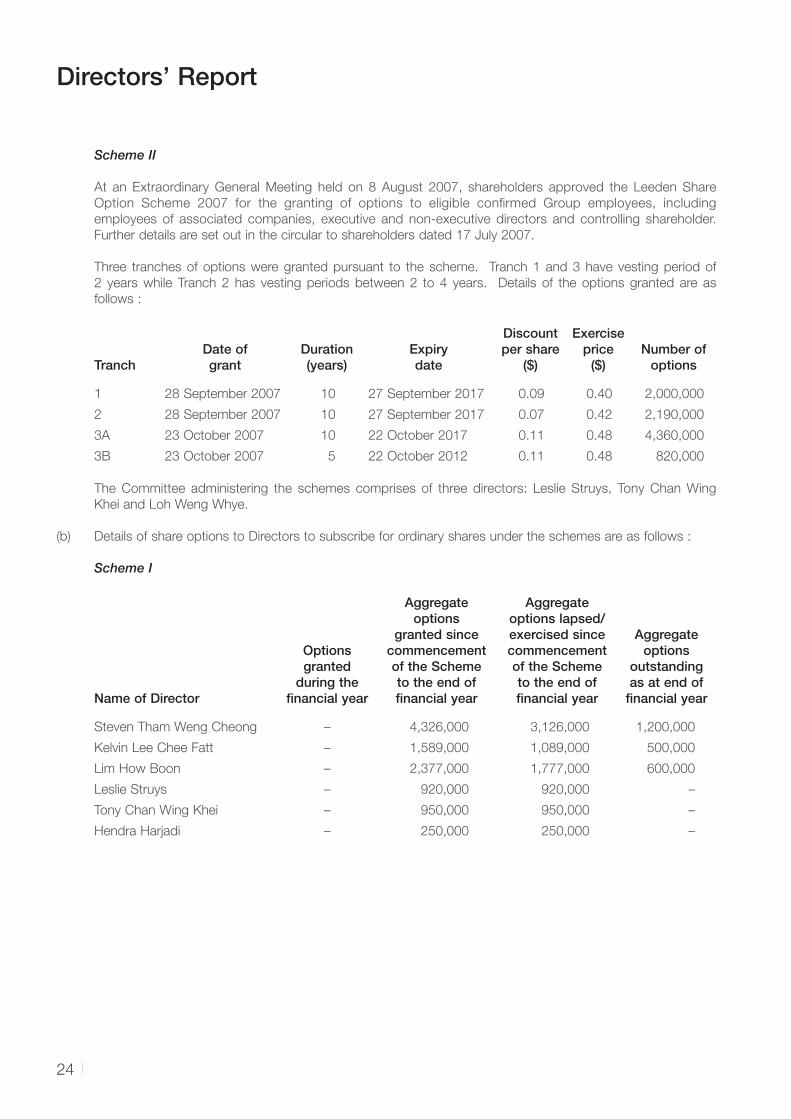

Scheme II

At an Extraordinary General Meeting held on 8 August 2007, shareholders approved the Leeden Share

Option Scheme 2007 for the granting of options to eligible confi rmed Group employees, including

employees of associated companies, executive and non-executive directors and controlling shareholder.

Further details are set out in the circular to shareholders dated 17 July 2007.

Three tranches of options were granted pursuant to the scheme. Tranch 1 and 3 have vesting period of

2 years while Tranch 2 has vesting periods between 2 to 4 years. Details of the options granted are as

follows :

TranchDate ofgrant

Duration(years)

Expirydate

Discount per share

($)

Exerciseprice

($)Number of

options

1 28 September 2007 10 27 September 2017 0.09 0.40 2,000,000

2 28 September 2007 10 27 September 2017 0.07 0.42 2,190,000

3A 23 October 2007 10 22 October 2017 0.11 0.48 4,360,000

3B 23 October 2007 5 22 October 2012 0.11 0.48 820,000

The Committee administering the schemes comprises of three directors: Leslie Struys, Tony Chan Wing

Khei and Loh Weng Whye.

(b) Details of share options to Directors to subscribe for ordinary shares under the schemes are as follows :

Scheme I

Name of Director

Optionsgranted

during the fi nancial year

Aggregateoptions

granted since commencement of the Scheme to the end of fi nancial year

Aggregate options lapsed/ exercised since commencement of the Scheme to the end of fi nancial year

Aggregateoptions

outstandingas at end of

fi nancial year

Steven Tham Weng Cheong – 4,326,000 3,126,000 1,200,000

Kelvin Lee Chee Fatt – 1,589,000 1,089,000 500,000

Lim How Boon – 2,377,000 1,777,000 600,000

Leslie Struys – 920,000 920,000 –

Tony Chan Wing Khei – 950,000 950,000 –

Hendra Harjadi – 250,000 250,000 –

25Annual Report 2008

Directors’ Report

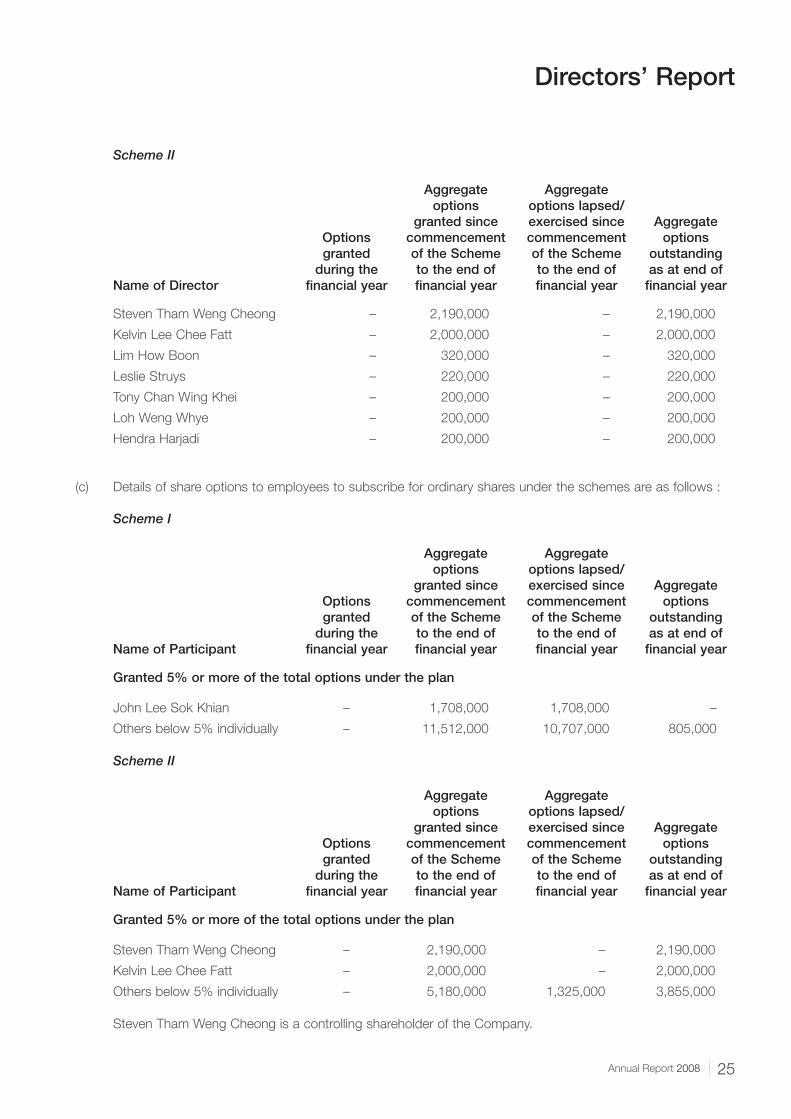

Scheme II

Name of Director

Optionsgranted

during the fi nancial year

Aggregateoptions

granted since commencement of the Scheme to the end of fi nancial year

Aggregate options lapsed/ exercised since commencement of the Scheme to the end of fi nancial year

Aggregateoptions

outstandingas at end of

fi nancial year

Steven Tham Weng Cheong – 2,190,000 – 2,190,000

Kelvin Lee Chee Fatt – 2,000,000 – 2,000,000

Lim How Boon – 320,000 – 320,000

Leslie Struys – 220,000 – 220,000

Tony Chan Wing Khei – 200,000 – 200,000

Loh Weng Whye – 200,000 – 200,000

Hendra Harjadi – 200,000 – 200,000

(c) Details of share options to employees to subscribe for ordinary shares under the schemes are as follows :

Scheme I

Name of Participant

Optionsgranted

during the fi nancial year

Aggregateoptions

granted since commencement of the Scheme to the end of fi nancial year

Aggregate options lapsed/ exercised since commencement of the Scheme to the end of fi nancial year

Aggregateoptions

outstandingas at end of

fi nancial year

Granted 5% or more of the total options under the plan

John Lee Sok Khian – 1,708,000 1,708,000 –

Others below 5% individually – 11,512,000 10,707,000 805,000

Scheme II

Name of Participant

Optionsgranted

during the fi nancial year

Aggregateoptions

granted since commencement of the Scheme to the end of fi nancial year

Aggregate options lapsed/ exercised since commencement of the Scheme to the end of fi nancial year

Aggregateoptions

outstandingas at end of

fi nancial year

Granted 5% or more of the total options under the plan

Steven Tham Weng Cheong – 2,190,000 – 2,190,000

Kelvin Lee Chee Fatt – 2,000,000 – 2,000,000

Others below 5% individually – 5,180,000 1,325,000 3,855,000

Steven Tham Weng Cheong is a controlling shareholder of the Company.

Directors’ Report

26

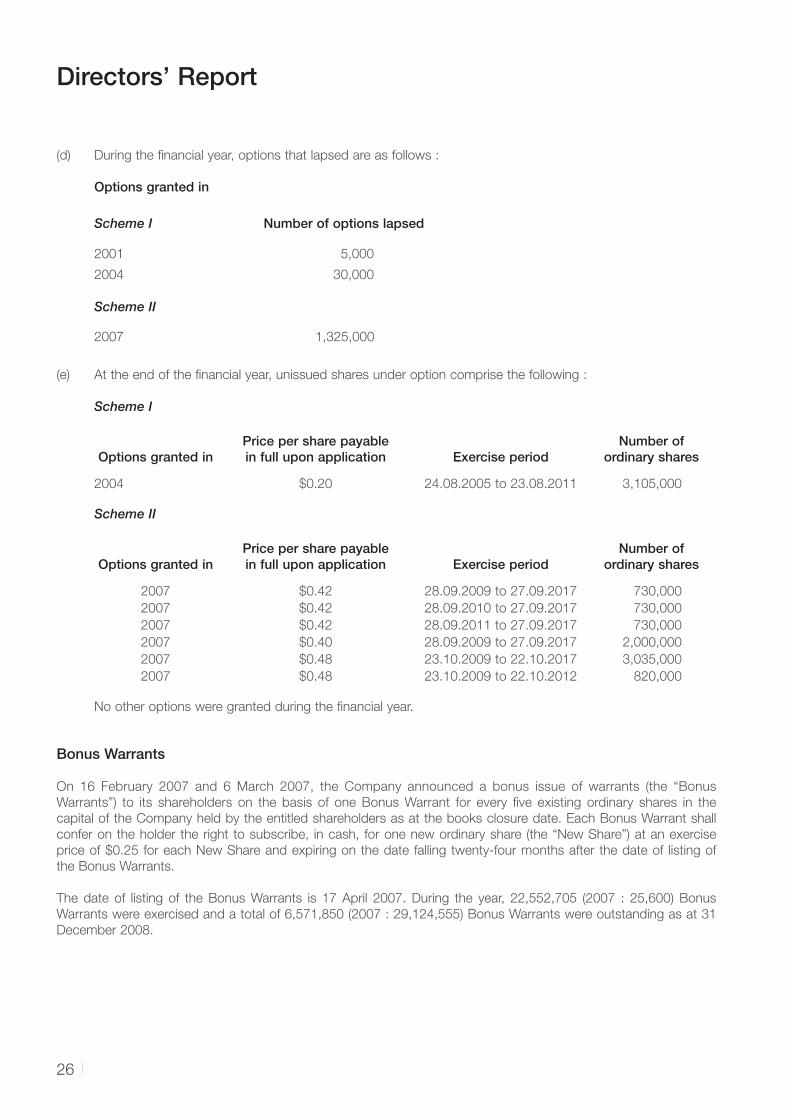

(d) During the fi nancial year, options that lapsed are as follows :

Options granted in

Scheme I Number of options lapsed

2001 5,000

2004 30,000

Scheme II

2007 1,325,000

(e) At the end of the fi nancial year, unissued shares under option comprise the following :

Scheme I

Options granted in Price per share payablein full upon application Exercise period

Number ofordinary shares

2004 $0.20 24.08.2005 to 23.08.2011 3,105,000

Scheme II

Options granted in Price per share payablein full upon application Exercise period

Number ofordinary shares

2007 $0.42 28.09.2009 to 27.09.2017 730,000

2007 $0.42 28.09.2010 to 27.09.2017 730,000

2007 $0.42 28.09.2011 to 27.09.2017 730,000

2007 $0.40 28.09.2009 to 27.09.2017 2,000,000

2007 $0.48 23.10.2009 to 22.10.2017 3,035,000

2007 $0.48 23.10.2009 to 22.10.2012 820,000

No other options were granted during the fi nancial year.

Bonus Warrants

On 16 February 2007 and 6 March 2007, the Company announced a bonus issue of warrants (the “Bonus

Warrants”) to its shareholders on the basis of one Bonus Warrant for every fi ve existing ordinary shares in the

capital of the Company held by the entitled shareholders as at the books closure date. Each Bonus Warrant shall

confer on the holder the right to subscribe, in cash, for one new ordinary share (the “New Share”) at an exercise

price of $0.25 for each New Share and expiring on the date falling twenty-four months after the date of listing of

the Bonus Warrants.

The date of listing of the Bonus Warrants is 17 April 2007. During the year, 22,552,705 (2007 : 25,600) Bonus

Warrants were exercised and a total of 6,571,850 (2007 : 29,124,555) Bonus Warrants were outstanding as at 31

December 2008.

27Annual Report 2008

Directors’ Report

Directors’ contractual benefi ts

Except as disclosed in the fi nancial statements, since the end of the previous fi nancial year, no Director of the

Company has received or become entitled to receive a benefi t by reason of a contract made by the Company or a

related corporation with the Director, or with a fi rm of which the Director is a member, or with a company in which

the Director has a substantial fi nancial interest.

Audit Committee

The Audit Committee at the date of this report comprises of the following three members who, are independent

Directors :

Tony Chan Wing Khei (Chairman)

Leslie Struys

Loh Weng Whye

The Audit Committee (“AC”) carried out its functions in accordance with Section 201B(5) of the Singapore

Companies Act, Cap. 50, including the following:

Reviews the audit plans of the internal and external auditors of the Company and reviews the internal

auditors’ evaluation of the adequacy of the Company’s system of internal accounting controls and the

assistance given by the Company’s management to the external and internal auditors;

Reviews the interim and annual fi nancial statements and the auditors’ report on the annual fi nancial

statements of the Company before their submission to the Board of Directors;

Reviews effectiveness of the Company’s material internal controls, including fi nancial, operational and

compliance controls and risk management via reviews carried out by the internal auditors;

Meets with the external auditors, other committees, and management in separate executive sessions to

discuss any matters that these groups believe should be discussed privately with the AC;

Reviews legal and regulatory matters that may have a material impact on the fi nancial statements, related

compliance policies and programmes and any reports received from regulators;

Reviews the cost effectiveness and the independence and objectivity of the external auditors;

Reviews the nature and extent of non-audit services provided by the external auditors;

Recommends to the board of directors the external auditors to be nominated, approves the compensation

of the external auditors, and reviews the scope and results of the audit;

Reports actions and minutes of the AC to the board of directors with such recommendations as the AC

considers appropriate; and

Reviews interested person transactions in accordance with the requirements of the Singapore Exchange

Securities Trading Limited (“SGX-ST”)’s Listing Manual.

Directors’ Report

28

The AC, having reviewed all non-audit services provided by the external auditors to the Group, is satisfi ed that the

nature and extent of such services would not affect the independence of the external auditors. The AC has also

conducted a review of interested person transactions.

The AC convened two meetings during the year. The AC has also met with internal and external auditors, without

the presence of the Company’s management, at least once a year.

Further details regarding the AC are disclosed in the Report on Corporate Governance.

Auditors

Ernst & Young LLP have expressed their willingness to accept reappointment as auditors.

On behalf of the Board of Directors,

Steven Tham Weng CheongDirector

Kelvin Lee Chee FattDirector

Singapore

30 March 2009

29Annual Report 2008

Statement by Directors

We, Steven Tham Weng Cheong and Kelvin Lee Chee Fatt, being two of the Directors of Leeden Limited, do

hereby state that, in the opinion of the Directors :

(i) the accompanying balance sheets, consolidated income statement, statements of changes in equity, and

consolidated cash fl ow statement together with notes thereto are drawn up so as to give a true and fair

view of the state of affairs of the Group and of the Company as at 31 December 2008 and the results of the

business, changes in equity and cash fl ows of the Group and the changes in equity of the Company for the

year ended on that date, and

(ii) at the date of this statement, there are reasonable grounds to believe that the Company will be able to pay

its debts as and when they fall due.

On behalf of the Board of Directors,

Steven Tham Weng CheongDirector

Kelvin Lee Chee FattDirector

Singapore

30 March 2009

Independent Auditors’ ReportTo the Members of Leeden Limited

30

We have audited the accompanying fi nancial statements of Leeden Limited (the “Company”) and its subsidiary

companies (collectively, the “Group”) set out on pages 31 to 100, which comprise the balance sheets of the Group

and the Company as at 31 December 2008, the statements of changes in equity of the Group and the Company,

and the income statement and cash fl ow statement of the Group for the year then ended, and a summary of

signifi cant accounting policies and other explanatory notes.

Management’s responsibility for the fi nancial statements

Management is responsible for the preparation and fair presentation of these fi nancial statements in accordance

with the provisions of the Singapore Companies Act, Cap. 50 (the Act) and Singapore Financial Reporting

Standards. This responsibility includes devising and maintaining a system of internal accounting controls suffi cient

to provide a reasonable assurance that assets are safeguarded against loss from unauthorised use or disposition;

and transactions are properly authorised and that they are recorded as necessary to permit the preparation of true

and fair profi t and loss account and balance sheet and to maintain accountability of assets; selecting and applying

appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances.

Auditors’ responsibility

Our responsibility is to express an opinion on these fi nancial statements based on our audit. We conducted our

audit in accordance with Singapore Standards on Auditing. Those standards require that we comply with ethical

requirements and plan and perform the audit to obtain reasonable assurance whether the fi nancial statements are

free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the

fi nancial statements. The procedures selected depend on the auditor’s judgement, including the assessment of

the risks of material misstatement of the fi nancial statements, whether due to fraud or error. In making those risk

assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the

fi nancial statements in order to design audit procedures that are appropriate in the circumstances, but not for

the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes

evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made

by management, as well as evaluating the overall presentation of the fi nancial statements.

We believe that the audit evidence we have obtained is suffi cient and appropriate to provide a basis for our audit

opinion.

Opinion

In our opinion,

(i) the consolidated fi nancial statements of the Group, and the balance sheet and statement of changes in

equity of the Company are properly drawn up in accordance with the provisions of the Act and Singapore

Financial Reporting Standards so as to give a true and fair view of the state of affairs of the Group and of

the Company as at 31 December 2008 and the results, changes in equity and cash fl ows of the Group and

the changes in equity of the Company for the year ended on that date; and

(ii) the accounting and other records required by the Act to be kept by the Company and by those subsidiary

companies incorporated in Singapore of which we are the auditors have been properly kept in accordance

with the provisions of the Act.

Ernst & Young LLP

Public Accountants and Certifi ed Public Accountants

Singapore

30 March 2009

31Annual Report 2008

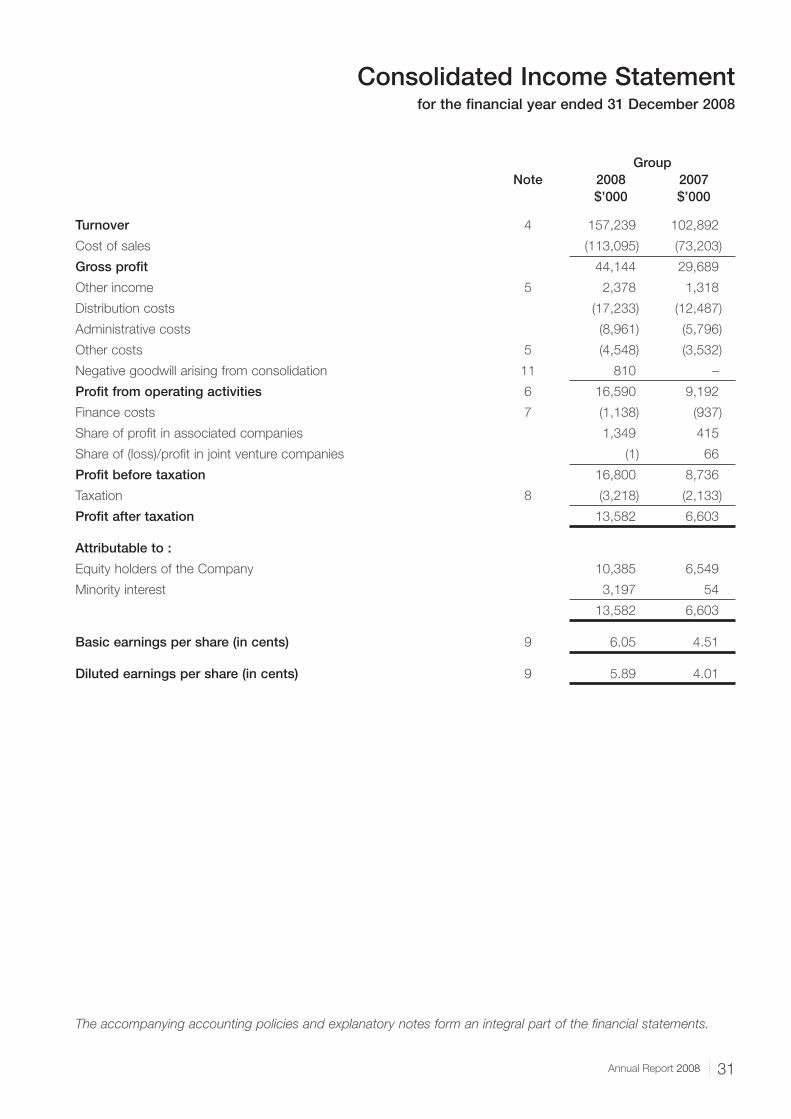

Consolidated Income Statementfor the fi nancial year ended 31 December 2008

GroupNote 2008 2007

$’000 $’000

Turnover 4 157,239 102,892

Cost of sales (113,095) (73,203)

Gross profi t 44,144 29,689

Other income 5 2,378 1,318

Distribution costs (17,233) (12,487)

Administrative costs (8,961) (5,796)

Other costs 5 (4,548) (3,532)

Negative goodwill arising from consolidation 11 810 –

Profi t from operating activities 6 16,590 9,192

Finance costs 7 (1,138) (937)

Share of profi t in associated companies 1,349 415

Share of (loss)/profi t in joint venture companies (1) 66

Profi t before taxation 16,800 8,736

Taxation 8 (3,218) (2,133)

Profi t after taxation 13,582 6,603

Attributable to :

Equity holders of the Company 10,385 6,549

Minority interest 3,197 54

13,582 6,603

Basic earnings per share (in cents) 9 6.05 4.51

Diluted earnings per share (in cents) 9 5.89 4.01

The accompanying accounting policies and explanatory notes form an integral part of the fi nancial statements.

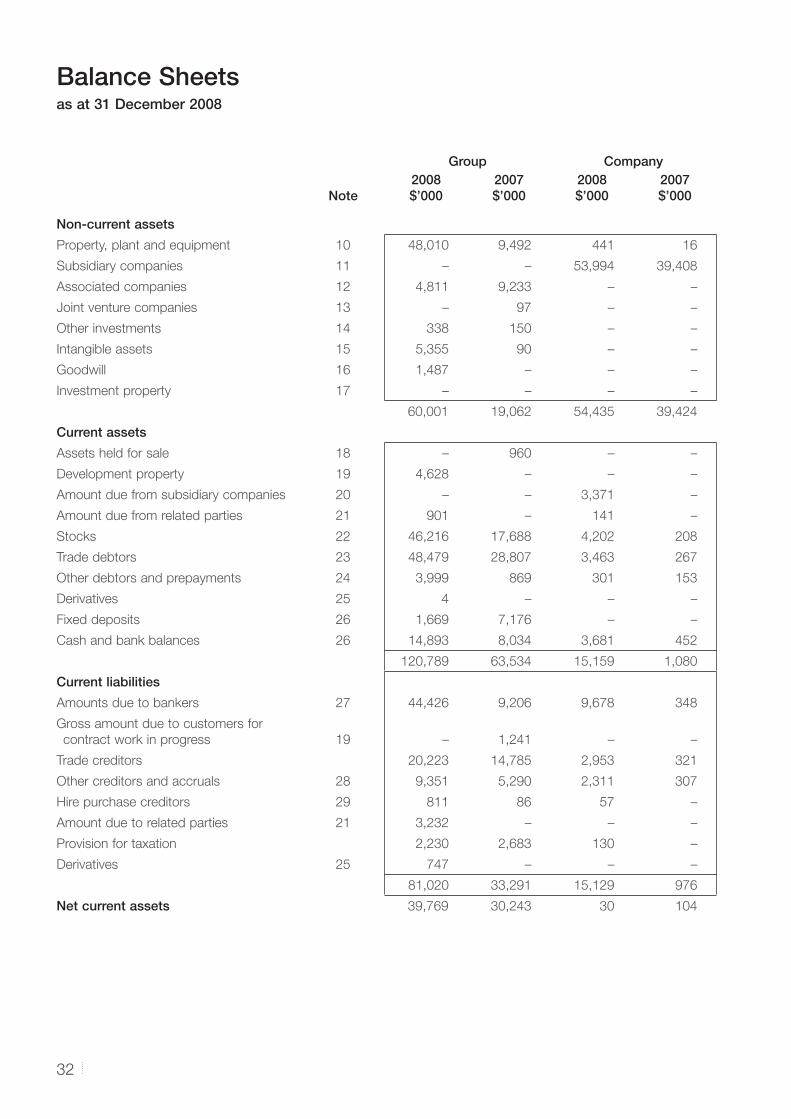

Balance Sheetsas at 31 December 2008

32

Group Company

Note2008$’000

2007$’000

2008$’000

2007$’000

Non-current assets

Property, plant and equipment 10 48,010 9,492 441 16

Subsidiary companies 11 – – 53,994 39,408

Associated companies 12 4,811 9,233 – –

Joint venture companies 13 – 97 – –

Other investments 14 338 150 – –

Intangible assets 15 5,355 90 – –

Goodwill 16 1,487 – – –

Investment property 17 – – – –

60,001 19,062 54,435 39,424

Current assets

Assets held for sale 18 – 960 – –

Development property 19 4,628 – – –

Amount due from subsidiary companies 20 – – 3,371 –

Amount due from related parties 21 901 – 141 –

Stocks 22 46,216 17,688 4,202 208

Trade debtors 23 48,479 28,807 3,463 267

Other debtors and prepayments 24 3,999 869 301 153

Derivatives 25 4 – – –

Fixed deposits 26 1,669 7,176 – –

Cash and bank balances 26 14,893 8,034 3,681 452

120,789 63,534 15,159 1,080

Current liabilities

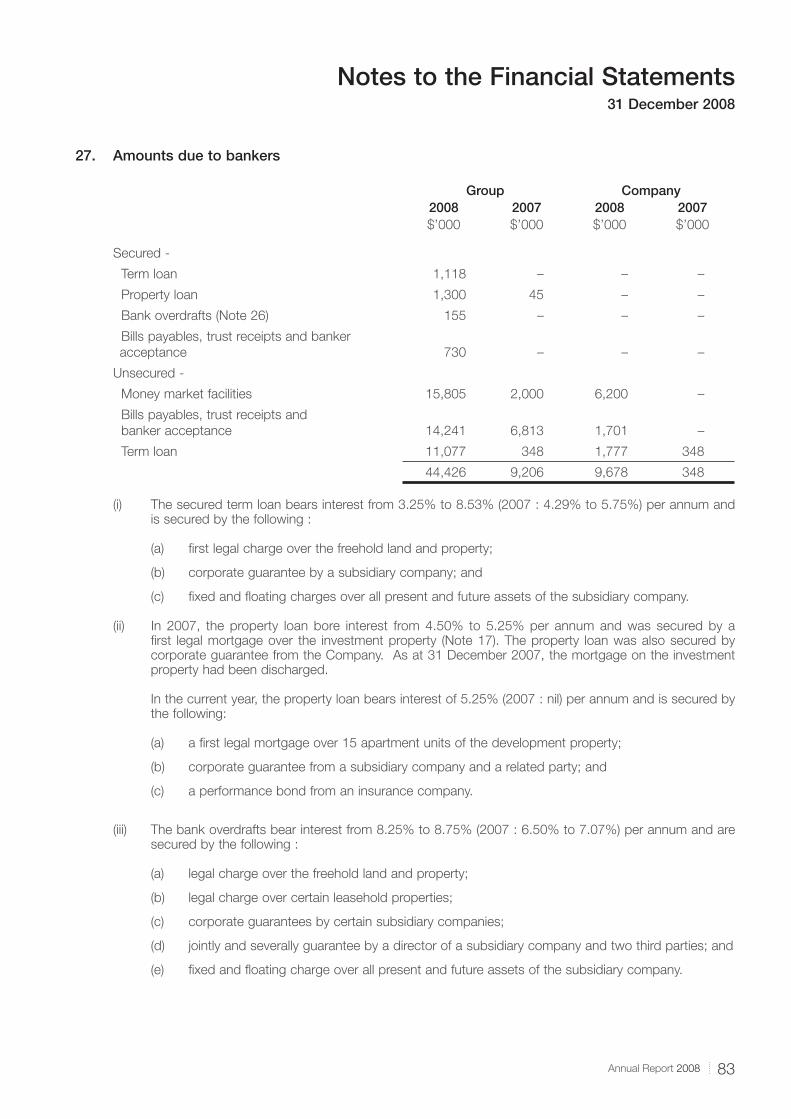

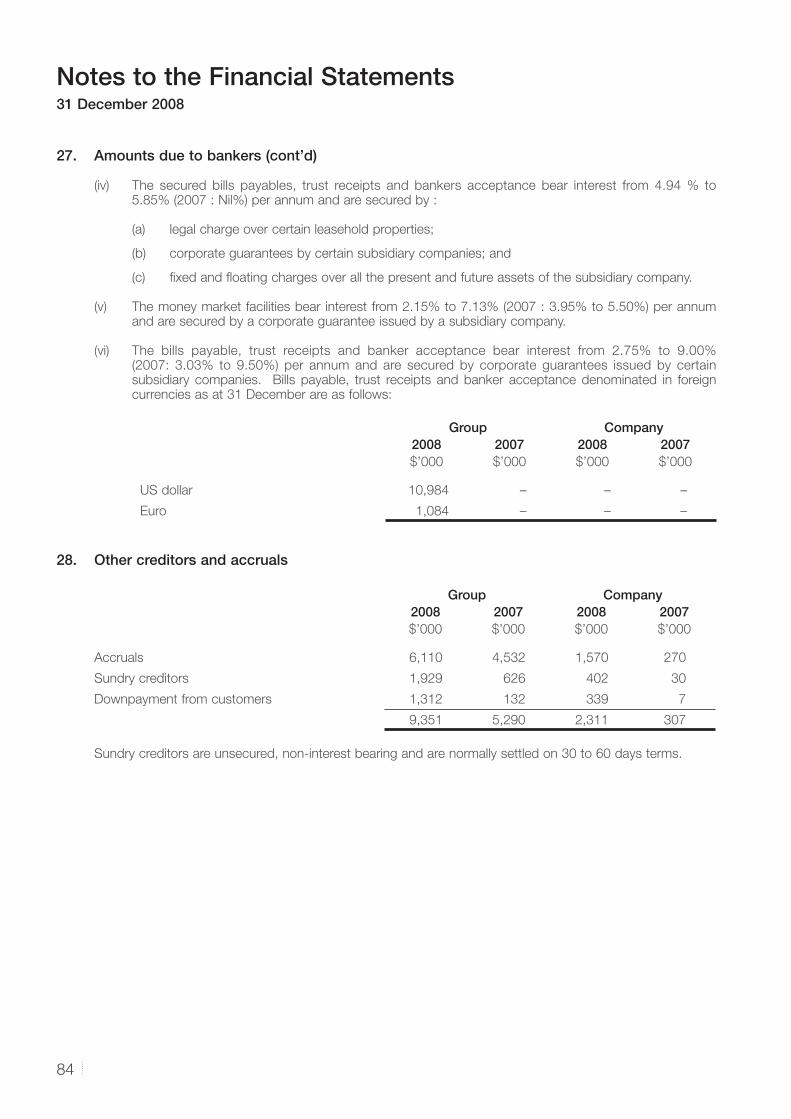

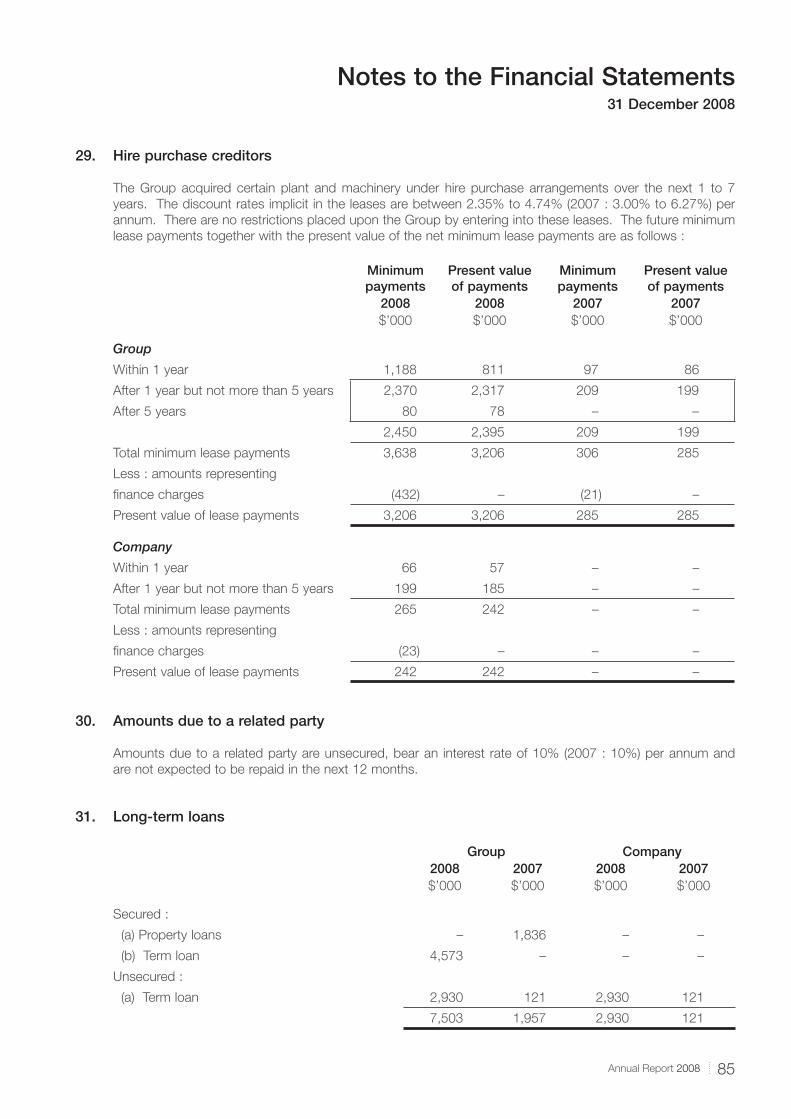

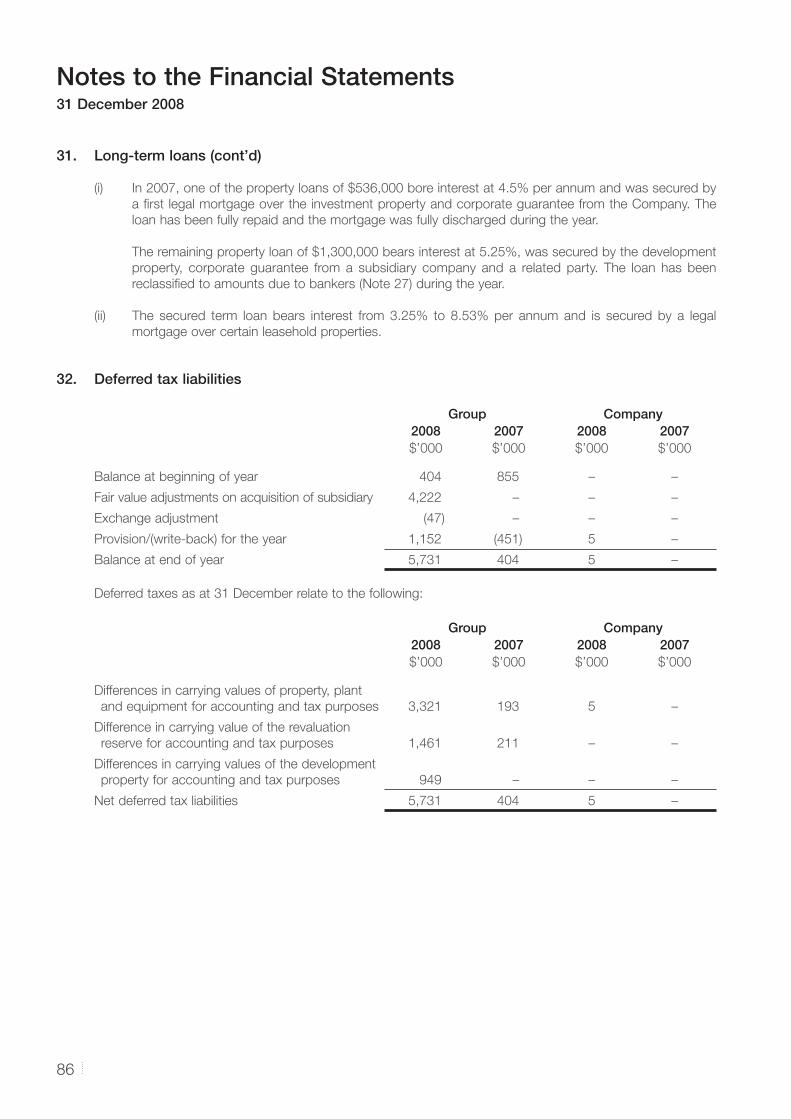

Amounts due to bankers 27 44,426 9,206 9,678 348

Gross amount due to customers for

contract work in progress 19 – 1,241 – –

Trade creditors 20,223 14,785 2,953 321

Other creditors and accruals 28 9,351 5,290 2,311 307

Hire purchase creditors 29 811 86 57 –

Amount due to related parties 21 3,232 – – –

Provision for taxation 2,230 2,683 130 –

Derivatives 25 747 – – –

81,020 33,291 15,129 976