#connweek from angel investors to 800lb gorillas peter weigand, skipping stone tom crews, stratford...

TRANSCRIPT

#ConnWeek

From Angel Investors to 800lb Gorillas Peter Weigand, Skipping StoneTom Crews, Stratford Partners

Mike Hammons, Sail Capital PartnersJayant Kumar, ALSTOM Grid

MAY 25, 2011

Stratford PartnersEnergy Industry •Investment Banking

2#ConnWeek Santa Clara, CA May 23-26, 2011

Skipping Stone

Skipping Stone is a different kind of energy consulting company. We are energy industry veterans who have chosen to consult, rather than generalist consultants who happen to be on an energy assignment.

For clients, the distinction is significant. We understand their businesses, are involved in the energy marketplace every day and have walked many miles in their shoes. As a result, we measure every engagement based on client success metrics. Our own success comes from repeat clients and referrals, which is 80% of our business.

Market FocusOur Services

Over 230 Clients Worldwide

3#ConnWeek Santa Clara, CA May 23-26, 2011

2011 Smart Grid Financial Trends

2011 is the year for M&A!

• Early Investors will need to exit

• Acquisitions by Mega Caps has heated up

Solar & Wind

•Supply and demand: U.S. has an opportunity to pick up falling demand in Europe

•Successful companies will be ones that address:

−Bring down their costs to capture more market share (scalability)

−Work closely with their customers to implement solutions that include finance

−Are more competitive than their peers (business models will be extremely important)

Smart Grid

• More application-focused technology, less hardware

• Government stimulus will start having measurable effects

• Meter installs will shed light on related technology challenges as the U.S. “smartens” the grid

• Increased competition from the mega-caps (Google, Microsoft, Cisco) which are developing buy, build, partner strategies

Two Key Growth Areas in 2011

4#ConnWeek Santa Clara, CA May 23-26, 2011

2011 Smart Grid Financial Drivers

• Targeted and leveraged access to buy cycle market

• Technical advantage yet perceived safety and performance

• Market awareness and reputation

• Trendy is out, experience is in

• Need to fill deployment gaps and focus on end-to-end solution

• Customer behavior adoption to achieve ROI

• Revise price structures and value propositions to capture margin

• Knitting & packaging solutions

•Current valuations high for right combo

Customers Solution Providers Capital Players

5#ConnWeek Santa Clara, CA May 23-26, 2011

Smart Grid Deal Target Characteristics

Cash FlowGeneration

Revenue Capital Growth Efficient

Unique Successful Ease ofDefensible in the Field Inter-Technology operability

Committed Proven Development GeographicLong-term Experience Pipelines DiversityContracts with Utilities

6#ConnWeek Santa Clara, CA May 23-26, 2011

Smart Grid Investment Trends

0

50

100

150

200

250Q

1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Nu

mb

er

of

Inv

es

tme

nts

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.0020

0720

0820

0920

10

Inv

es

tme

nt

Va

lue

($

)

Number of Deals Investment Value

7#ConnWeek Santa Clara, CA May 23-26, 2011

Mega Cap M&A Activity is HOT

Mega-caps Active or Interested in Smart GridTechnology and Telecom Companies

Building Automation and Power Solutions

8#ConnWeek Santa Clara, CA May 23-26, 2011

Recent Smart Grid Buyers

Cleantech Industrial/Other

Utilities/IPPs Technology

9#ConnWeek Santa Clara, CA May 23-26, 2011

Food For Thought

Ernst & Young Survey findings: 300 executives at global companies with at least 1 billion in revenue:

•Approximately 80% of respondents stated they had acquired or might consider acquiring cleantech companies.

•53% of respondents stated they expect the rate of cleantech acquisitions to increase in the next three years,

Rationale for cleantech acquisitions:

• Access to innovation capabilities (42%)

• Compliment existing products and services (32%)

• Source innovation through acquisition (30%)

• Reach a new customer base (28%)

Let us help you achieve your goals!

Peter Weigand Chairman & CEO Skipping Stone [email protected]

#ConnWeek

Angel Investors

Tom CrewsManaging Director

Stratford PartnersEnergy Industry ● Investment Banking

11#ConnWeek Santa Clara, CA May 23-26, 2011

Stratford Partners – Focused on the Energy Industry

Services Offered• Strategic & Financial Consulting• Fundraising/Private Capital Advisory• Mergers, Acquisitions & Dispositions• Interim & Turnaround Management

Areas of Focus• Energy Technology• Demand Response & Distributed Generation• Renewable Energy• Energy Management• Power Markets

Stratford PartnersEnergy Industry •Investment Banking

12#ConnWeek Santa Clara, CA May 23-26, 2011

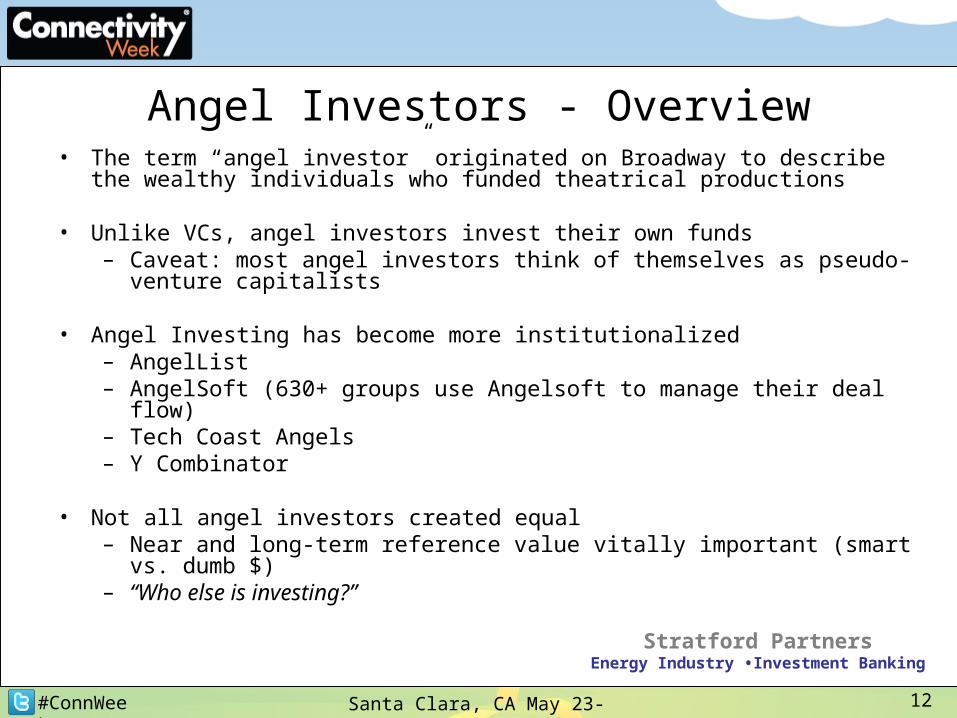

Angel Investors - Overview• The term “angel investor” originated on Broadway to describe the wealthy

individuals who funded theatrical productions

• Unlike VCs, angel investors invest their own funds– Caveat: most angel investors think of themselves as pseudo-venture

capitalists

• Angel Investing has become more institutionalized– AngelList– AngelSoft (630+ groups use Angelsoft to manage their deal flow)– Tech Coast Angels– Y Combinator

• Not all angel investors created equal– Near and long-term reference value vitally important (smart vs. dumb $)– “Who else is investing?”

Stratford PartnersEnergy Industry •Investment Banking

13#ConnWeek Santa Clara, CA May 23-26, 2011

The Role of the Angel Investor• Angel Investors typically fill the funding gap between “friends &

family” and venture capital– Angel investors play an increasingly important role as VCs

unwilling to invest in pre-revenue companies

• Angels invested $20.1 billion in 61,900 companies in 2010 (+14% over 2009)*– Software, industrial/energy and IT services received 16%, 8%

and 5%, respectively, of the total

• Most angel investors live within a 3 hour drive of the companies in which they invest

• 67% of angel investor exits were through M&A*

* University of New Hampshire Center for Venture ResearchStratford Partners

Energy Industry •Investment Banking

14#ConnWeek Santa Clara, CA May 23-26, 2011

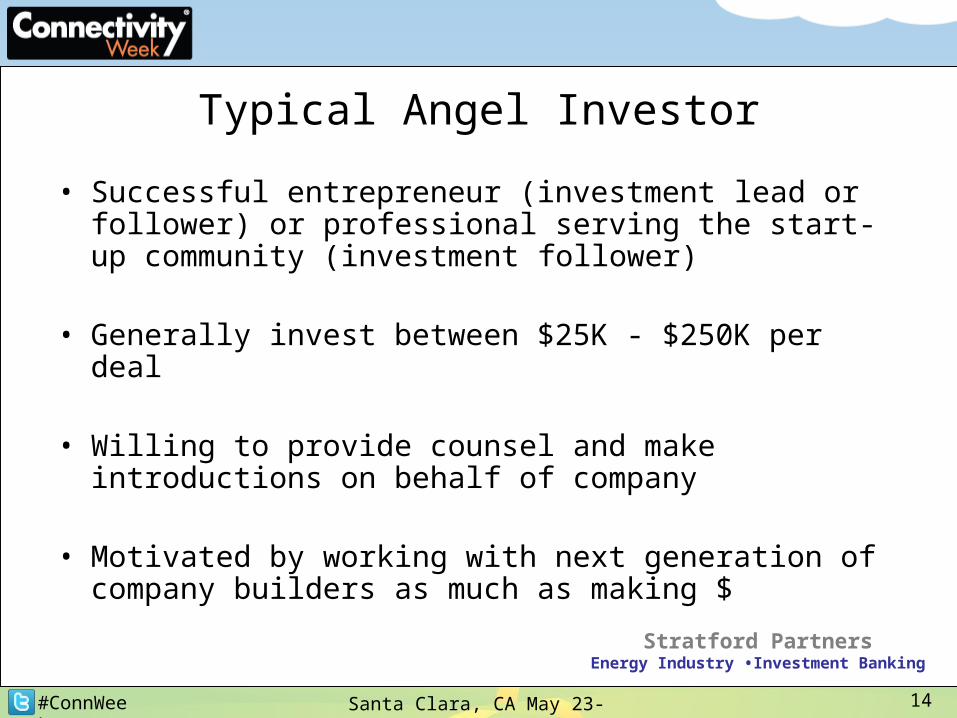

Typical Angel Investor

• Successful entrepreneur (investment lead or follower) or professional serving the start-up community (investment follower)

• Generally invest between $25K - $250K per deal

• Willing to provide counsel and make introductions on behalf of company

• Motivated by working with next generation of company builders as much as making $

Stratford PartnersEnergy Industry •Investment Banking

15#ConnWeek Santa Clara, CA May 23-26, 2011

What does it take to attract angel investment? First and foremost –

• A team that gets investors excited– Infectious passion + obvious desire to succeed– Ability to articulate the business opportunity in 15

minutes or less – Intellectual horsepower– Industry knowledge gained from industry experience– Maturity– Integrity– Balance of selling & product development skills

• Reference investors & advisors Stratford PartnersEnergy Industry •Investment Banking

16#ConnWeek Santa Clara, CA May 23-26, 2011

What does it take to attract angel investment? Secondarily –

• Clear understanding of what the $ will be used for– All funding is to milestones so make sure to have one

• Compelling business opportunity– Large market opportunity– Barriers to competition– Not too capital intensive (dilution concern)– Identifiable exit other than an IPO

• Customer references/surveys

Stratford PartnersEnergy Industry •Investment Banking

17#ConnWeek Santa Clara, CA May 23-26, 2011

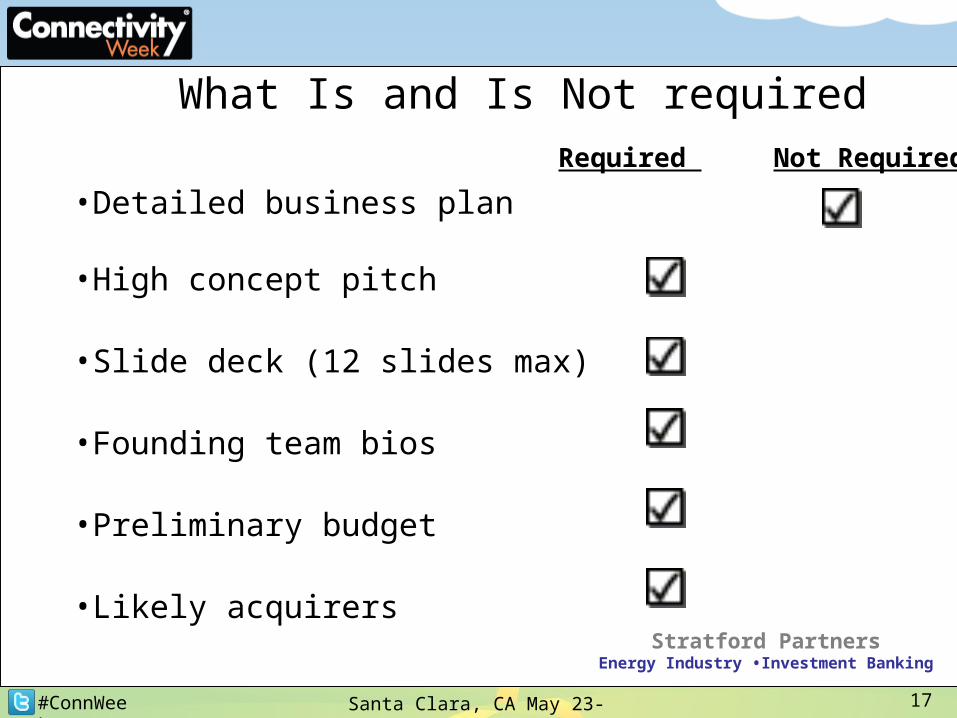

What Is and Is Not requiredRequired Not Required

•Detailed business plan

•High concept pitch

•Slide deck (12 slides max)

•Founding team bios

•Preliminary budget

•Likely acquirers

Stratford PartnersEnergy Industry •Investment Banking

18#ConnWeek Santa Clara, CA May 23-26, 2011

Remember

• Most angel investors are followers

• Angel investors tend to invest in packs

• Make sure you are not the angel investor’s only investment

• Who invests matters as much as how much they invest

Stratford PartnersEnergy Industry •Investment Banking

19#ConnWeek Santa Clara, CA May 23-26, 2011

SAIL Venture PartnersSAIL Venture Partners

California | New York | Washington DC | California | New York | Washington DC | BostonBoston

Mike HammonsMike Hammons

20#ConnWeek Santa Clara, CA May 23-26, 2011

What is CleanTech?

• Technology innovation in the more efficient use of energy, water, food and other scarce and valuable global resources:

• Optimize use of natural resources• Reduce ecological impact, and• Add economic value by lowering costs and improving

profits

• Cleantech is the world’s fastest growing investment category

• The 3rd largest venture capital investment category: over 14% market share in North America; 18% in Europe

• Cleantech markets are large multibillion dollar global markets

• “May be the largest wealth creation opportunity of the 21st century” -- John Doerr

• Multiple waves of technological innovation

Clean Technology

Clean Technology

Large, Growing, Profitable Markets

Large, Growing, Profitable Markets

Enormous Growth

Potential

Enormous Growth

Potential

21#ConnWeek Santa Clara, CA May 23-26, 2011

Company life cycle

Idea/Science Discovery

Idea/Science Discovery IncubateIncubate InfantInfant Adolescent Adolescent Mature Mature

Business•R&D team•Zero rev.

Tech/Prod•Alpha & Beta•“Prototype” or “Proof of Concept”

CHARACTERISTICS

Business•Build team•Rev. Gen Begins

Tech/Prod•Production Transition

Business•Business Process/ Std.•Predictable Sales cycle

Tech/Prod•Product Refinement•Version Control

Business•Balance Cap.

Tech/Prod•Brand mgt.•Refinement

22#ConnWeek Santa Clara, CA May 23-26, 2011

Capital Sources by StageIdea• Founder• Universities• Government • Commercial labs

Incubate• Founder, Friends and Family• Angel Investors• Seed Venture • Commercial incubators• Other (grants, universities, etc.)

Infant• Angel & Seed Investors• Venture Capital• Other

23#ConnWeek Santa Clara, CA May 23-26, 2011

Capital Sources by Stage

Adolescent • Venture Capital• Joint Ventures• Growth Capital firms• Debt lines • Commercial and Investment Banks• Others

Mature• Joint Ventures• Growth Capital Firms• Public Markets• Debt Lines (Balance Capital Structure)• Commercial and Investment Banks• Others

24#ConnWeek Santa Clara, CA May 23-26, 2011

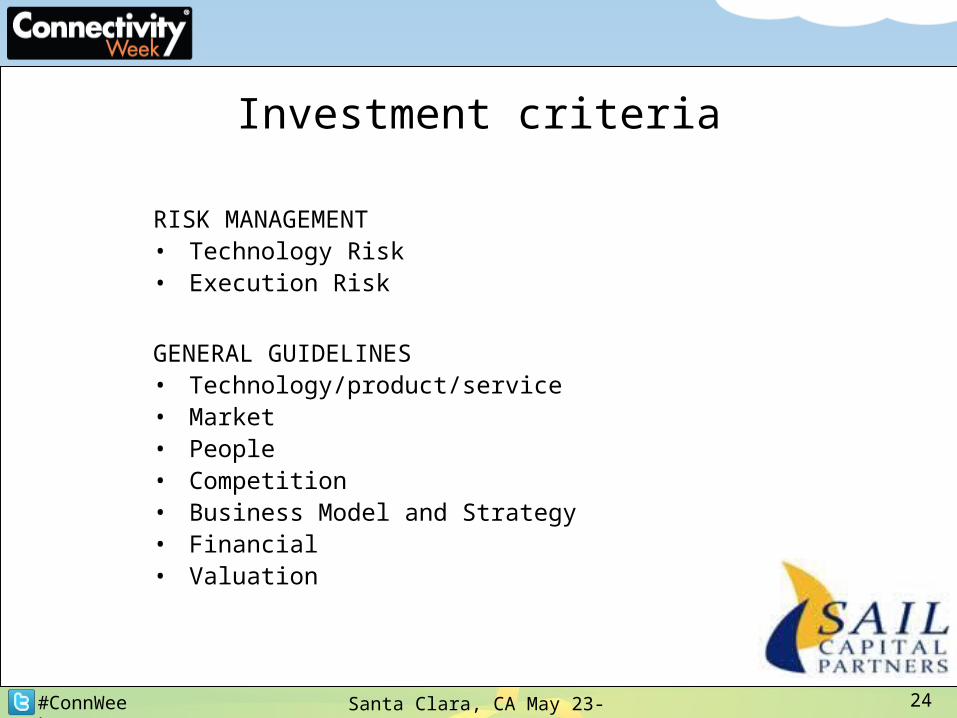

Investment criteria

RISK MANAGEMENT• Technology Risk• Execution Risk

GENERAL GUIDELINES• Technology/product/service• Market• People• Competition• Business Model and Strategy• Financial• Valuation

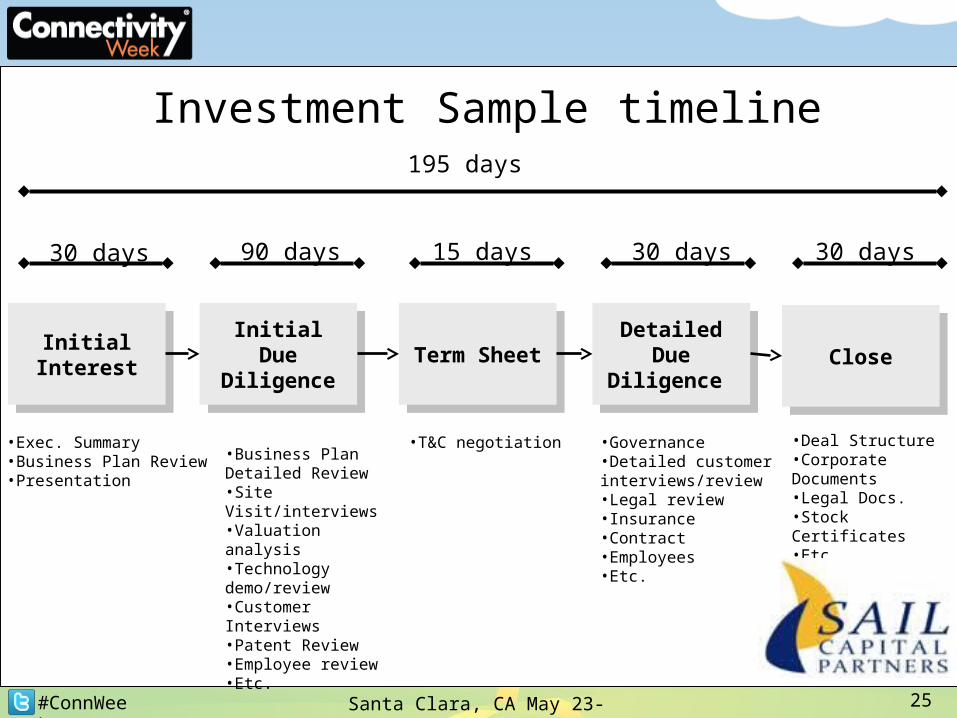

25#ConnWeek Santa Clara, CA May 23-26, 2011

Investment Sample timeline

Initial InterestInitial Interest Initial Due Diligence

Initial Due Diligence Term SheetTerm Sheet Detailed Due

Diligence

Detailed Due Diligence CloseClose

•Exec. Summary•Business Plan Review•Presentation

30 days 90 days 15 days 30 days 30 days

195 days

•Business Plan Detailed Review•Site Visit/interviews•Valuation analysis•Technology demo/review•Customer Interviews•Patent Review•Employee review•Etc.

•T&C negotiation •Governance•Detailed customer interviews/review•Legal review•Insurance•Contract•Employees•Etc.

•Deal Structure•Corporate Documents•Legal Docs.•Stock Certificates•Etc.