[email protected] partner microfinance foundation weathering the storm case study from bosnia and...

TRANSCRIPT

[email protected] www.e-mfp.eu

Partner Microfinance FoundationPartner Microfinance Foundation

Weathering the stormWeathering the storm

Case Study from Bosnia and HerzegovinaCase Study from Bosnia and Herzegovina

[email protected] www.e-mfp.eu

Partner Microcredit FoundationPartner Microcredit Foundation

Basic indicators as of Sept 30th 2011Basic indicators as of Sept 30th 2011

No of loan disbursed from the beginning of

the operations

Total amount of disbursed loans

from the beginning of

the operations

Active clients/rural

clients

No of employees

/loan officers

No of brench offices

280 946 451 million EUR 35,633 .................

80,43%

255 ...............

13153

[email protected] www.e-mfp.eu

The main reasons The main reasons that caused the that caused the crises in MF sector:crises in MF sector:

• Global financial crisis• Increasing unemployement rate• Bad political situation and social tensions• Market limitations• Strong competition• Poor response to the crisis from the Government• Strong banking lobby

[email protected] www.e-mfp.eu

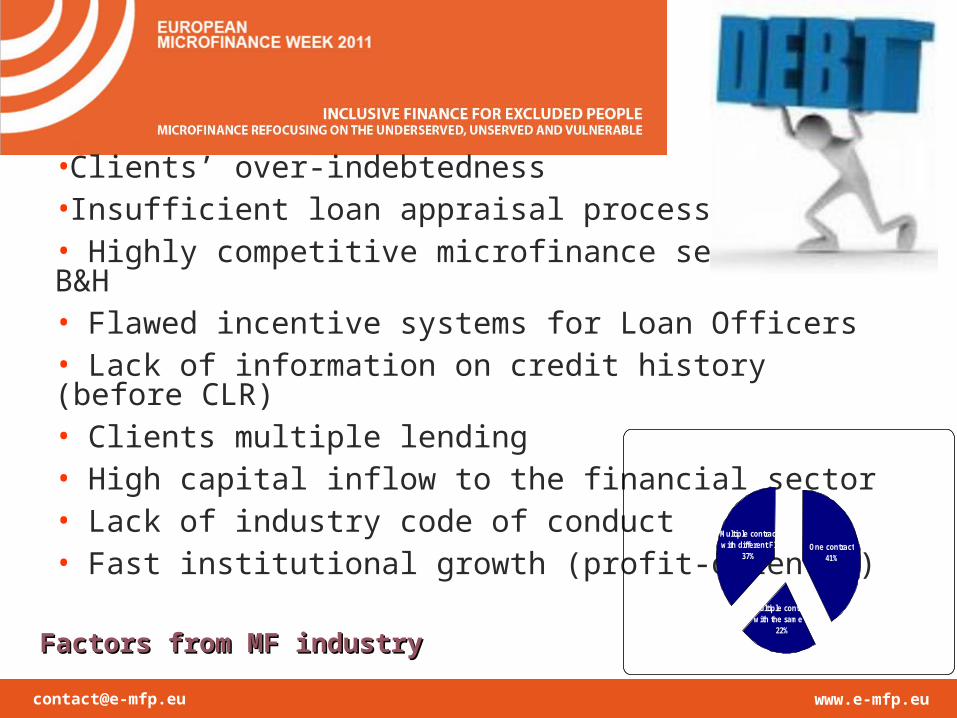

Factors from MF industry Factors from MF industry

•Clients’ over-indebtedness •Insufficient loan appraisal process• Highly competitive microfinance sector in B&H• Flawed incentive systems for Loan Officers • Lack of information on credit history (before CLR)• Clients multiple lending • High capital inflow to the financial sector• Lack of industry code of conduct• Fast institutional growth (profit-oriented)

Distribution of clients by borrowing patern

One contract41%

Multiple contractswith the same FI

22%

Multiple contractswith different FI

37%

[email protected] www.e-mfp.eu

Deterioration in portfolio quality as result of the financial crisis

PUR > 30 Partner Average of the sector

2006 0,79% 0,76%2007 0,62% 1%2008 1,57% 2,40%2009 4,72% 8,30%

I-Q 2010 5,94% 10%II-Q 2010 5,88% 10,42%

[email protected] www.e-mfp.eu

Compromised quality of portfolio The increase in the level of total debt write-offs The lack og demand General sense of insecurity among employees

The effect of the crisis on Partner MCF:The effect of the crisis on Partner MCF:

[email protected] www.e-mfp.eu

Actions taken by Partner:Actions taken by Partner:

Social responsibility Financial education of clients Inovative approach for lending (Mercy Corps projects) Innovative loan products (youth, farmers, etc). ISO standards (ISO 9001, 27001, 31000, 10000, etc)

[email protected] www.e-mfp.eu

The six principlesThe six principles

Avoidance of over-indebtedness

Transparent and Responsible pricing

Appropriate collections practices

Ethical staff behavior

Mechanisms for redress of grievances

Partner’s response in client’s protection:Partner’s response in client’s protection:

Privacy of client data

[email protected] www.e-mfp.eu

• New products and services (Youth loan, Fruity loan, Insurance loan)• Market leader in clients’ protection• Rigorous analysis and approval • Good image, clients’ trust• Constant market survey• Sophisticated internal systems• Client oriented management

• Organizational:• Centralization • Separation of sales, approval and loan collection units Monitoring• Separating sales, approval and collection of loans• Employees’ satisfaction

Partner’s response to the crisis:Partner’s response to the crisis:

[email protected] www.e-mfp.eu

Improvement in portfolio quality as result of taken actions

PUR > 30 Partner Average of the sector

III-Q 2010 3,79% 6,83%IV-Q 2010 3,05% 5%I-Q 2011 3,05% 7,09%II-Q 2011 2,58% 5,91%III-Q 2011 1,88% 5%

[email protected] www.e-mfp.eu

Financial or social performance objectives?Financial or social performance objectives?

Achieving social performance objectives leads to financial gain, which is necessary in order to

continue providing social benefits to our clients.

[email protected] www.e-mfp.eu

Recommendations:Recommendations:

Limit credit exposure per client Reduce internaly cross-borrowing from multiple

institutions Strengthen loan appraisal and monitoring Develop industry-wide standards of conduct Investors should include the assessment of the

compliance with the standards of the code of conduct into due diligence

Harmonize risk classification (A-E) methodology in the county

Clearly mark restructured loans Conduct trend analysis of comprehensive CRK data

[email protected] www.e-mfp.eu

Selma Jahic, Assistant Director for Marketingemail: [email protected]