contacts the lebanon weekly monitor imf foresees...

TRANSCRIPT

1Week 07 February 06 - February 12, 2012

FEBRUARY 06 - FEBRUARY 12, 2012

WEEK 07

Bank Audi sal - Audi Saradar Group - Group Research Department - Bank Audi Plaza - Bab Idriss - PO Box 11-2560 - Lebanon - Tel: 961 1 994 000 - email: [email protected]

CONTACTS

RESEARCH

Treasury & Capital Markets

Micky Chebli(961-1) [email protected]

Nadine Akkawi(961-1) [email protected]

Emile Shalala(961-1) [email protected]

Private Banking

Toufic Aouad(961-1) [email protected]

Corporate Banking

Khalil Debs(961-1) [email protected]

Marwan Barakat(961-1) [email protected]

Jamil Naayem(961-1) [email protected]

Salma Saad Baba(961-1) [email protected]

Fadi Kanso(961-1) [email protected]

Nathalie Ghorayeb(961-1) [email protected]

Lélia Tamer Badro(961-1) [email protected]

Nivine Turyaki(961-1) [email protected]

LEBANON MARKETS: WEEK OF FEBRUARY 06 - FEBRUARY 12, 2012

The LEBANON WEEKLY MONITOR

Economy___________________________________________________________________________p.2 IMF FORESEES MODERATE GROWTH IN 2012 ALONG WITH CONSIDERABLE DOWNSIDE RISKS This week saw the release of the new Article IV Consultation mission of the International Monetary Fund (IMF) on Lebanon. The IMF forecasts a 3.5% real GDP growth for 2012, mainly supported by a recovery in tourism and retail trade, on the back of an improvement in the domestic environment and a continued growth in GCC countries.

Also in this issuep.3 Balance of payments deficit at US$ 2.0 billion in 2011 p.3 Financial inflows down by 18% in 2011 p.4 Public debt to GDP ratio still on a downward trend to 133% in 2011

Surveys___________________________________________________________________________p.5 LEBANESE INDUSTRIES TO RAISE AVERAGE WAGES BY 6.5% IN 2012 The human resources consultancy firm Hay Group released a study in which it indicated that the organizations taking part in its survey forecasted a rise in overall compensation by an average of 6.5% across Lebanese industries throughout 2012.

Also in this issuep.6 EFH Hermes neutral on equity investment in Lebanon

Corporate News___________________________________________________________________________p.7 IFC INVESTS UP TO US$ 124 MILLION IN MEDGULF International Finance Corporation (IFC), the investment arm of the World Bank, announced that it is investing up to US$ 124 million in the Mediterranean and Gulf Insurance and Reinsurance Company (Medgulf ).

Also in this issuep.7 Lebanon’s Azadea signs franchise deal with UK’s Asda p.7 Kia tops car sales in Lebanon with 545 newly registered cars in January 2012 p.8 Trainstation opens its doors in Beirut p.8 World Bank finances Lebanese water project Markets In Brief___________________________________________________________________________p.9 IMF RECOMMENDS REVIEWING INTEREST RATES ON TBSActivity persisted in favor of the LP on the FX market, while interest rates on Tbs remained stable, and the equity market witnessed an ongoing demand for banking stocks. In details, FC-to-LP conversions continued, which called for the Central Bank’s intervention for one day only as a buyer of the US Dollar surpluses at LP 1,501. On the Tbs market, interest rates remained stable. It is worth mentioning that the weighted average yield on Tbs subscriptions reached 5.36% in January 2012, versus 5.45% in January 2011 and 6.82% in January 2010. This was coupled with an increase in the Central Bank’s LP securities portfolio of LP 145 billion in January 2012, which spots light on the BDL’s intervention on the Tbs primary market. Within this context, the IMF noted in its latest article IV on Lebanon that interest rates should be allowed to rise to reduce government reliance on BDL. As to the equity market, banking stocks continued to attract a decent demand, which led to a rise in the price index of 1.1%.

2Week 07 February 06 - February 12, 2012

FEBRUARY 06 - FEBRUARY 12, 2012

WEEK 07

ECONOMY______________________________________________________________________________IMF FORESEES MODERATE GROWTH IN 2012 ALONG WITH CONSIDERABLE DOWNSIDE RISKS

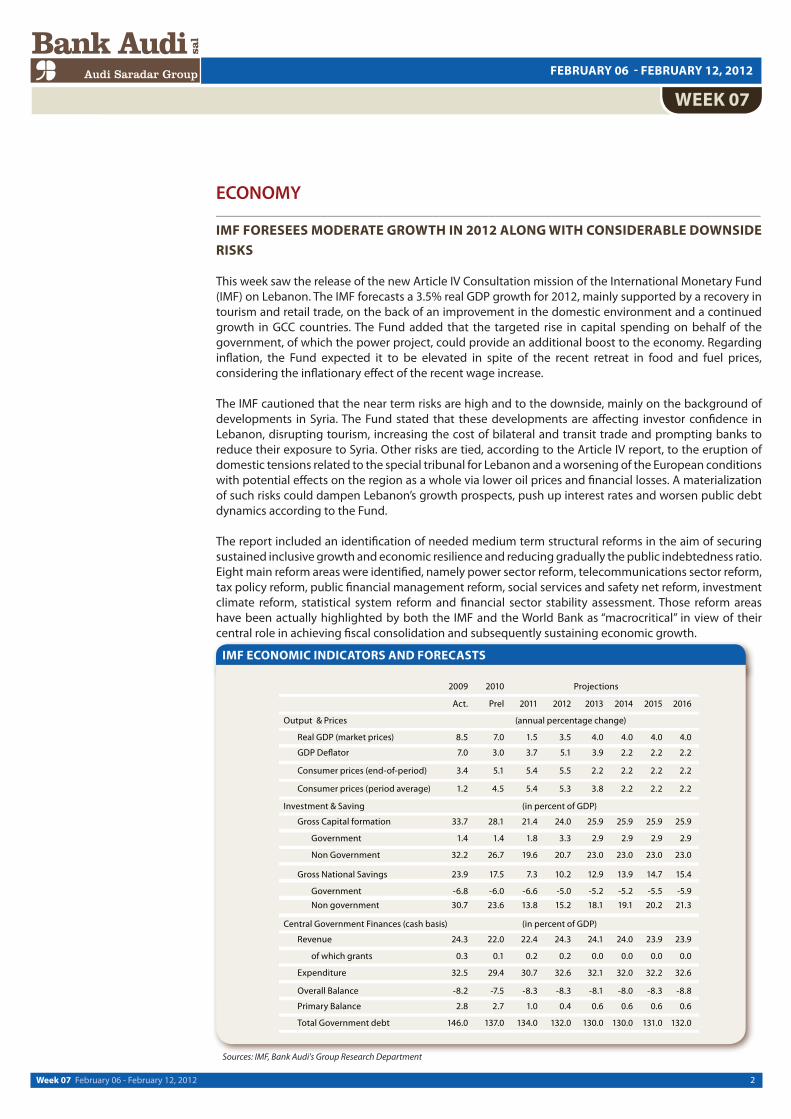

This week saw the release of the new Article IV Consultation mission of the International Monetary Fund (IMF) on Lebanon. The IMF forecasts a 3.5% real GDP growth for 2012, mainly supported by a recovery in tourism and retail trade, on the back of an improvement in the domestic environment and a continued growth in GCC countries. The Fund added that the targeted rise in capital spending on behalf of the government, of which the power project, could provide an additional boost to the economy. Regarding inflation, the Fund expected it to be elevated in spite of the recent retreat in food and fuel prices, considering the inflationary effect of the recent wage increase.

The IMF cautioned that the near term risks are high and to the downside, mainly on the background of developments in Syria. The Fund stated that these developments are affecting investor confidence in Lebanon, disrupting tourism, increasing the cost of bilateral and transit trade and prompting banks to reduce their exposure to Syria. Other risks are tied, according to the Article IV report, to the eruption of domestic tensions related to the special tribunal for Lebanon and a worsening of the European conditions with potential effects on the region as a whole via lower oil prices and financial losses. A materialization of such risks could dampen Lebanon’s growth prospects, push up interest rates and worsen public debt dynamics according to the Fund.

The report included an identification of needed medium term structural reforms in the aim of securing sustained inclusive growth and economic resilience and reducing gradually the public indebtedness ratio. Eight main reform areas were identified, namely power sector reform, telecommunications sector reform, tax policy reform, public financial management reform, social services and safety net reform, investment climate reform, statistical system reform and financial sector stability assessment. Those reform areas have been actually highlighted by both the IMF and the World Bank as “macrocritical” in view of their central role in achieving fiscal consolidation and subsequently sustaining economic growth.

IMF ECONOMIC INDICATORS AND FORECASTS

Sources: IMF, Bank Audi's Group Research Department

3Week 07 February 06 - February 12, 2012

FEBRUARY 06 - FEBRUARY 12, 2012

WEEK 07

_____________________________________________________________________________BALANCE OF PAYMENTS DEFICIT AT US$ 2.0 BILLION IN 2011

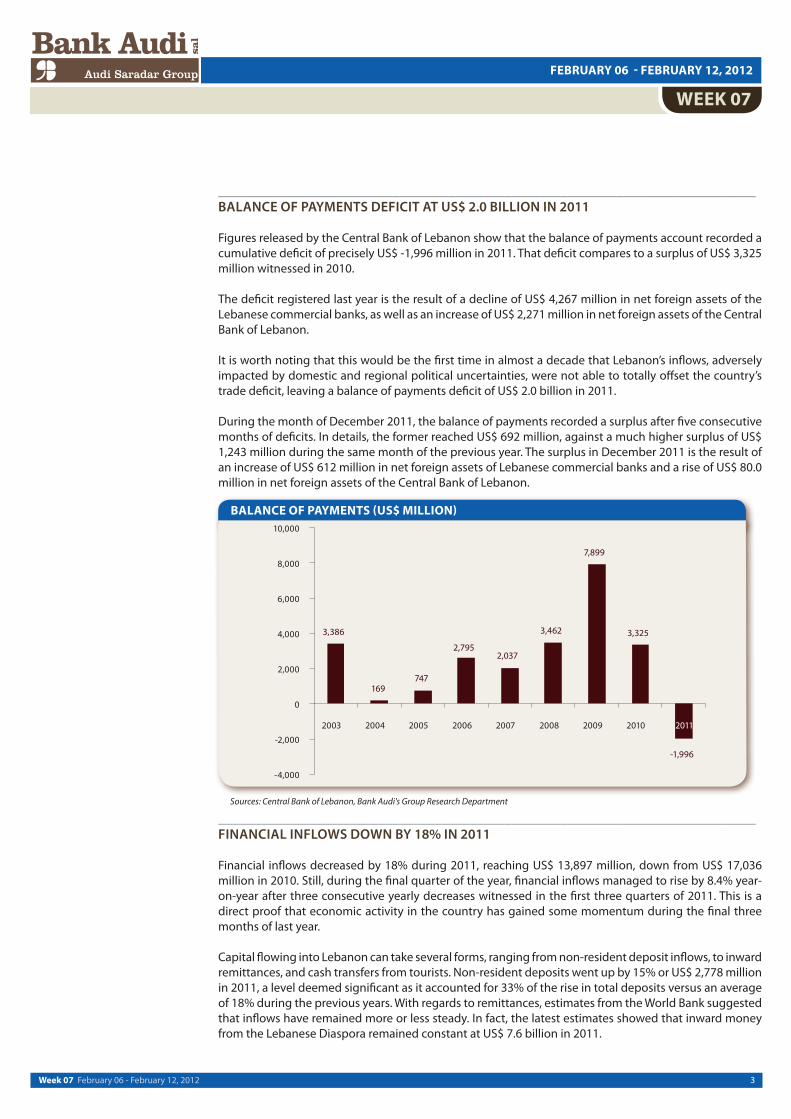

Figures released by the Central Bank of Lebanon show that the balance of payments account recorded a cumulative deficit of precisely US$ -1,996 million in 2011. That deficit compares to a surplus of US$ 3,325 million witnessed in 2010.

The deficit registered last year is the result of a decline of US$ 4,267 million in net foreign assets of the Lebanese commercial banks, as well as an increase of US$ 2,271 million in net foreign assets of the Central Bank of Lebanon.

It is worth noting that this would be the first time in almost a decade that Lebanon’s inflows, adversely impacted by domestic and regional political uncertainties, were not able to totally offset the country’s trade deficit, leaving a balance of payments deficit of US$ 2.0 billion in 2011.

During the month of December 2011, the balance of payments recorded a surplus after five consecutive months of deficits. In details, the former reached US$ 692 million, against a much higher surplus of US$ 1,243 million during the same month of the previous year. The surplus in December 2011 is the result of an increase of US$ 612 million in net foreign assets of Lebanese commercial banks and a rise of US$ 80.0 million in net foreign assets of the Central Bank of Lebanon.

Sources: Central Bank of Lebanon, Bank Audi's Group Research Department

BALANCE OF PAYMENTS (US$ MILLION)

_____________________________________________________________________________FINANCIAL INFLOWS DOWN BY 18% IN 2011

Financial inflows decreased by 18% during 2011, reaching US$ 13,897 million, down from US$ 17,036 million in 2010. Still, during the final quarter of the year, financial inflows managed to rise by 8.4% year-on-year after three consecutive yearly decreases witnessed in the first three quarters of 2011. This is a direct proof that economic activity in the country has gained some momentum during the final three months of last year.

Capital flowing into Lebanon can take several forms, ranging from non-resident deposit inflows, to inward remittances, and cash transfers from tourists. Non-resident deposits went up by 15% or US$ 2,778 million in 2011, a level deemed significant as it accounted for 33% of the rise in total deposits versus an average of 18% during the previous years. With regards to remittances, estimates from the World Bank suggested that inflows have remained more or less steady. In fact, the latest estimates showed that inward money from the Lebanese Diaspora remained constant at US$ 7.6 billion in 2011.

4Week 07 February 06 - February 12, 2012

FEBRUARY 06 - FEBRUARY 12, 2012

WEEK 07

_____________________________________________________________________________PUBLIC DEBT TO GDP RATIO STILL ON A DOWNWARD TREND TO 133% IN 2011

According to the latest figures released by the Association of Banks in Lebanon, gross public debt amounted to US$ 53.6 billion at end-2011, up by 2.0% from end-2010. Domestic debt increased by 2.2% relative to end-2010 to US$ 32.7 billion in 2011, while foreign currency debt increased by 1.7% to US$ 20.9 billion. Net public debt, which excludes the public sector's deposits at the Central Bank and at commercial banks, increased by 3.0% in 2011 to US$ 46.4 billion.

There has been an overall improvement in public indebtedness over the past few years. Indeed, Lebanon’s public debt to GDP ratio fell from a high of 180% in 2006 to reach 133% at end-2011.

Sources: Central Bank of Lebanon, Bank Audi's Group Research Department

Sources: Association of Banks in Lebanon, Bank Audi's Group Research Department

FINANCIAL INFLOWS (US$ MILLION)

GROSS PUBLIC DEBT

5Week 07 February 06 - February 12, 2012

FEBRUARY 06 - FEBRUARY 12, 2012

WEEK 07

SURVEYS_____________________________________________________________________________LEBANESE INDUSTRIES TO RAISE AVERAGE WAGES BY 6.5% IN 2012

The human resources consultancy firm Hay Group released a study in which it indicated that the organizations taking part in its survey forecasted a rise in overall compensation by an average of 6.5% across Lebanese industries throughout 2012. According to the study, which refers to data gathered from 13,000 employees across 100 Lebanese businesses, this modest rise is mainly attributed to the time needed by Lebanese organizations to implement the wage increase passed by the Cabinet.

Hay Group also signaled that the anticipated salary rise would be partly counterbalanced by a 5.8% increase in inflation. Therefore, wages would edge up by only 0.7% in real terms, giving a more accurate reflection on employee’s true increase in purchasing power. In 2011, salaries had risen by 6.9% on average and inflation by 5.0% which led to a real growth of 1.9% tick, as per Hay Group. The consultancy firm also expected that the rise in minimum wage and the potential changes in education and transportation allowances to lead to over-inflated pay increases in late 2012.

In parallel, the report indicated that the highest paying industries in Lebanon are those related to construction and construction material. In fact, employees within these sectors demand a premium and are paid 6% above the general market. Employees within the consumer goods industry also receive 4% above the market average across all sectors.

The report added that suggests companies’ recruitment remains focused on hiring in the sales, marketing and administration job functions this year. Also, functions related to engineering, finance and accounting, as well as research and development, are also high in demand. Still, not all companies are upbeat about hiring prospects, despite significant improvement recorded in comparison with past years.

Sources: Hay Group, Bank Audi's Group Research Department

WAGE INCREASE V/S INFLATION RATE (2007 - 2012)

6Week 07 February 06 - February 12, 2012

FEBRUARY 06 - FEBRUARY 12, 2012

WEEK 07

MENA COUNTRY WEIGHTS

Sources: EFG Hermes, Bank Audi's Group Research Department

______________________________________________________________________________EFH HERMES NEUTRAL ON EQUITY INVESTMENT IN LEBANON

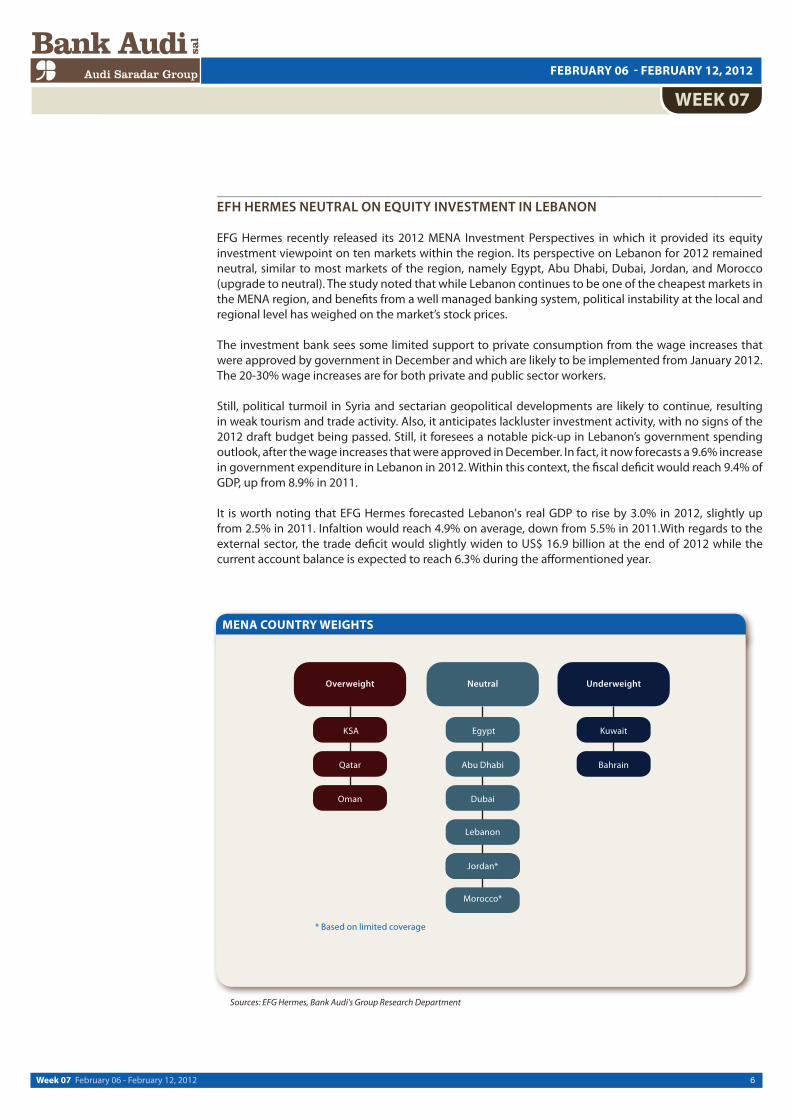

EFG Hermes recently released its 2012 MENA Investment Perspectives in which it provided its equity investment viewpoint on ten markets within the region. Its perspective on Lebanon for 2012 remained neutral, similar to most markets of the region, namely Egypt, Abu Dhabi, Dubai, Jordan, and Morocco (upgrade to neutral). The study noted that while Lebanon continues to be one of the cheapest markets in the MENA region, and benefits from a well managed banking system, political instability at the local and regional level has weighed on the market’s stock prices.

The investment bank sees some limited support to private consumption from the wage increases that were approved by government in December and which are likely to be implemented from January 2012. The 20-30% wage increases are for both private and public sector workers.

Still, political turmoil in Syria and sectarian geopolitical developments are likely to continue, resulting in weak tourism and trade activity. Also, it anticipates lackluster investment activity, with no signs of the 2012 draft budget being passed. Still, it foresees a notable pick-up in Lebanon’s government spending outlook, after the wage increases that were approved in December. In fact, it now forecasts a 9.6% increase in government expenditure in Lebanon in 2012. Within this context, the fiscal deficit would reach 9.4% of GDP, up from 8.9% in 2011.

It is worth noting that EFG Hermes forecasted Lebanon's real GDP to rise by 3.0% in 2012, slightly up from 2.5% in 2011. Infaltion would reach 4.9% on average, down from 5.5% in 2011.With regards to the external sector, the trade deficit would slightly widen to US$ 16.9 billion at the end of 2012 while the current account balance is expected to reach 6.3% during the afformentioned year.

7Week 07 February 06 - February 12, 2012

FEBRUARY 06 - FEBRUARY 12, 2012

WEEK 07

CORPORATE NEWS_____________________________________________________________________________IFC INVESTS UP TO US$ 124 MILLION IN MEDGULF

International Finance Corporation (IFC), the investment arm of the World Bank, announced that it is investing up to US$ 124 million in the and Gulf Insurance and Reinsurance Company (Medgulf ) to help the firm extend its health and commercial risk insurance services across the Middle East and North Africa, a region in which low coverage rates are hindering economic development, as per the IFC.

IFC’s acquisition of up to a 15% equity stake in Medgulf would support the company as it looks to expand into Egypt, Iraq and Turkey, where insurance penetration rates are deemed low by global standards.

According to the IFC, the Middle East has the lowest rates of insurance coverage in the world, with gross premiums around 1% of regional GDP, which breeds uncertainty within households, hindering investment and job creation. In the Middle East and North Africa, the share of the population aged 65 years and older is expected to more than triple by 2050, demanding an increase in health, life, and pension insurance services, as per the IFC. Therefore, Medgulf officials signaled that IFC’s investment would support their strategy to help extend essential services to underserved parts of the population by encouraging cross-border investments within the region IFC is the largest global development institution focused exclusively on the private sector. It helps developing countries achieve sustainable growth by financing investment, providing advisory services to businesses and governments, and mobilizing capital in the international financial markets. In fiscal year 2011, the corporation invested nearly US$ 19 billion to create jobs, strengthen environmental performance, and contribute to their local communities.

Established in 1980, Medgulf Group covers retail and institutional markets with all risk coverage requirements through its operations in Lebanon, KSA, Bahrain, UK, UAE, Turkey and Jordan. Its services include insurance and reinsurance, risk management, and third party administration._____________________________________________________________________________LEBANON’S AZADEA SIGNS FRANCHISE DEAL WITH UK’S ASDA

UK’s Asda, the British arm of US retailer Wal-Mart stores, concluded a franchise deal with Lebanon-based Azadea Group to introduce its Georges budget clothing brand to the Middle East.

Last year, Asda had announced plans to establish a small number of pilot Georges stores in the Middle East, in the aim to increase their non-food segment revenue.

The Georges label includes everything from budget bridal dresses to school uniforms, and currently accounts for around half of Asda’s general merchandise sales.

Founded in 1949, Asda Stores Ltd. is a British supermarket chain which retails food, clothing, general merchandise, toys and financial services. It also has a mobile telephone network (via the Vodafone Network), termed Asda Mobile.

Established in 1978, Azadea Group Holding owns and operates retail outlets including clothing, accessories, footwear, home furnishings, eyewear, sporting goods, music and entertainment, restaurants and coffee shops. The group also specializes in real estate development._____________________________________________________________________________KIA TOPS CAR SALES IN LEBANON WITH 545 NEWLY REGISTERED CARS IN JANUARY 2012

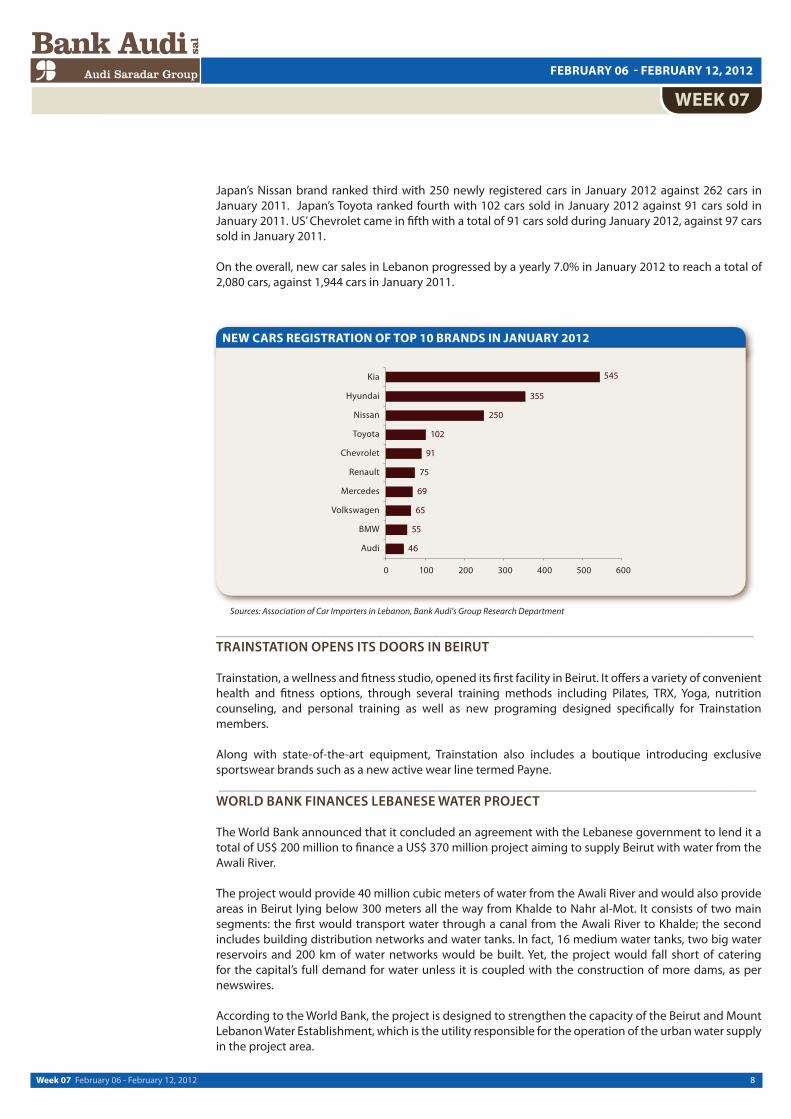

The new cars registration statistics in Lebanon, as compiled by the Association of Car Importers in Lebanon, show that Korea’s Kia cars topped the rankings with sales of 545 new cars in January 2012, against 454 cars in the same month of last year. Korea’s Hyundai cars ranked second with 355 vehicles sold in January 2012 versus 214 cars sold in the same month of 2011.

8Week 07 February 06 - February 12, 2012

FEBRUARY 06 - FEBRUARY 12, 2012

WEEK 07

_____________________________________________________________________________TRAINSTATION OPENS ITS DOORS IN BEIRUT

Trainstation, a wellness and fitness studio, opened its first facility in Beirut. It offers a variety of convenient health and fitness options, through several training methods including Pilates, TRX, Yoga, nutrition counseling, and personal training as well as new programing designed specifically for Trainstation members.

Along with state-of-the-art equipment, Trainstation also includes a boutique introducing exclusive sportswear brands such as a new active wear line termed Payne. _____________________________________________________________________________WORLD BANK FINANCES LEBANESE WATER PROJECT

The World Bank announced that it concluded an agreement with the Lebanese government to lend it a total of US$ 200 million to finance a US$ 370 million project aiming to supply Beirut with water from the Awali River.

The project would provide 40 million cubic meters of water from the Awali River and would also provide areas in Beirut lying below 300 meters all the way from Khalde to Nahr al-Mot. It consists of two main segments: the first would transport water through a canal from the Awali River to Khalde; the second includes building distribution networks and water tanks. In fact, 16 medium water tanks, two big water reservoirs and 200 km of water networks would be built. Yet, the project would fall short of catering for the capital’s full demand for water unless it is coupled with the construction of more dams, as per newswires.

According to the World Bank, the project is designed to strengthen the capacity of the Beirut and Mount Lebanon Water Establishment, which is the utility responsible for the operation of the urban water supply in the project area.

NEW CARS REGISTRATION OF TOP 10 BRANDS IN JANUARY 2012

Sources: Association of Car Importers in Lebanon, Bank Audi's Group Research Department

Japan’s Nissan brand ranked third with 250 newly registered cars in January 2012 against 262 cars in January 2011. Japan’s Toyota ranked fourth with 102 cars sold in January 2012 against 91 cars sold in January 2011. US’ Chevrolet came in fifth with a total of 91 cars sold during January 2012, against 97 cars sold in January 2011.

On the overall, new car sales in Lebanon progressed by a yearly 7.0% in January 2012 to reach a total of 2,080 cars, against 1,944 cars in January 2011.

9Week 07 February 06 - February 12, 2012

FEBRUARY 06 - FEBRUARY 12, 2012

WEEK 07

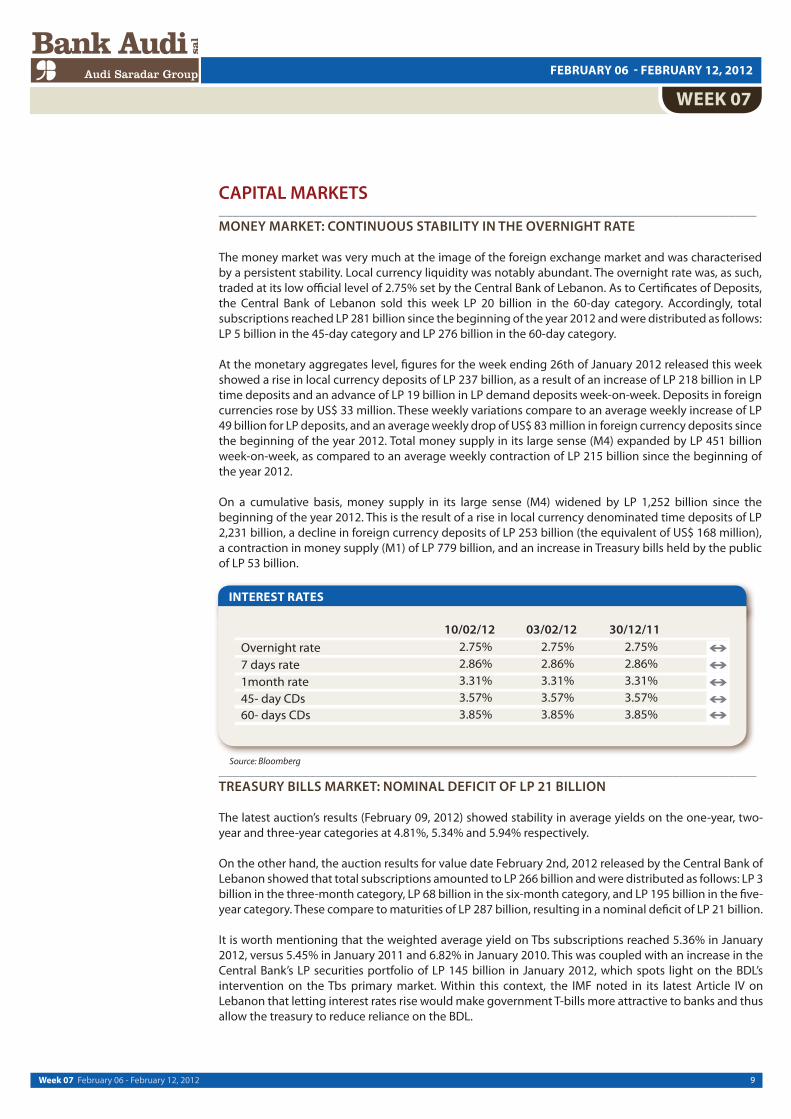

CAPITAL MARKETS_____________________________________________________________________________MONEY MARKET: CONTINUOUS STABILITY IN THE OVERNIGHT RATE

The money market was very much at the image of the foreign exchange market and was characterised by a persistent stability. Local currency liquidity was notably abundant. The overnight rate was, as such, traded at its low official level of 2.75% set by the Central Bank of Lebanon. As to Certificates of Deposits, the Central Bank of Lebanon sold this week LP 20 billion in the 60-day category. Accordingly, total subscriptions reached LP 281 billion since the beginning of the year 2012 and were distributed as follows: LP 5 billion in the 45-day category and LP 276 billion in the 60-day category.

At the monetary aggregates level, figures for the week ending 26th of January 2012 released this week showed a rise in local currency deposits of LP 237 billion, as a result of an increase of LP 218 billion in LP time deposits and an advance of LP 19 billion in LP demand deposits week-on-week. Deposits in foreign currencies rose by US$ 33 million. These weekly variations compare to an average weekly increase of LP 49 billion for LP deposits, and an average weekly drop of US$ 83 million in foreign currency deposits since the beginning of the year 2012. Total money supply in its large sense (M4) expanded by LP 451 billion week-on-week, as compared to an average weekly contraction of LP 215 billion since the beginning of the year 2012.

On a cumulative basis, money supply in its large sense (M4) widened by LP 1,252 billion since the beginning of the year 2012. This is the result of a rise in local currency denominated time deposits of LP 2,231 billion, a decline in foreign currency deposits of LP 253 billion (the equivalent of US$ 168 million), a contraction in money supply (M1) of LP 779 billion, and an increase in Treasury bills held by the public of LP 53 billion.

_____________________________________________________________________________TREASURY BILLS MARKET: NOMINAL DEFICIT OF LP 21 BILLION

The latest auction’s results (February 09, 2012) showed stability in average yields on the one-year, two-year and three-year categories at 4.81%, 5.34% and 5.94% respectively.

On the other hand, the auction results for value date February 2nd, 2012 released by the Central Bank of Lebanon showed that total subscriptions amounted to LP 266 billion and were distributed as follows: LP 3 billion in the three-month category, LP 68 billion in the six-month category, and LP 195 billion in the five-year category. These compare to maturities of LP 287 billion, resulting in a nominal deficit of LP 21 billion.

It is worth mentioning that the weighted average yield on Tbs subscriptions reached 5.36% in January 2012, versus 5.45% in January 2011 and 6.82% in January 2010. This was coupled with an increase in the Central Bank’s LP securities portfolio of LP 145 billion in January 2012, which spots light on the BDL’s intervention on the Tbs primary market. Within this context, the IMF noted in its latest Article IV on Lebanon that letting interest rates rise would make government T-bills more attractive to banks and thus allow the treasury to reduce reliance on the BDL.

INTEREST RATES

Source: Bloomberg

10Week 07 February 06 - February 12, 2012

FEBRUARY 06 - FEBRUARY 12, 2012

WEEK 07

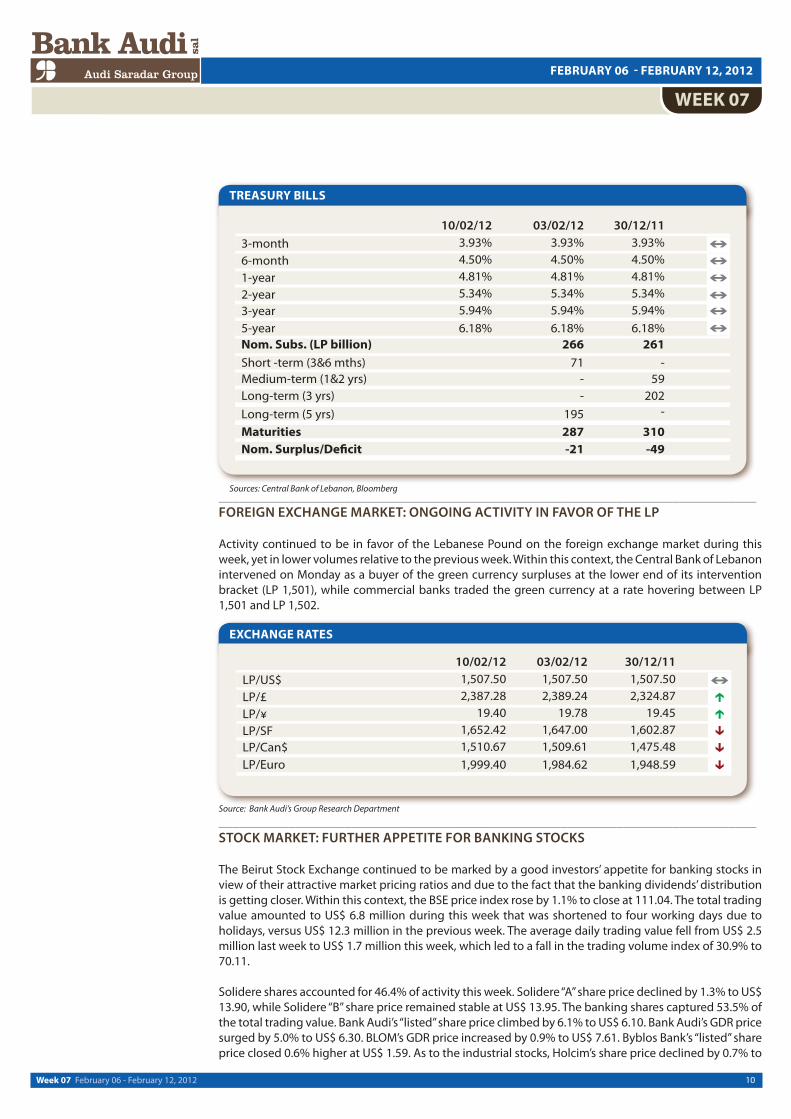

TREASURY BILLS

Sources: Central Bank of Lebanon, Bloomberg

_____________________________________________________________________________STOCK MARKET: FURTHER APPETITE FOR BANKING STOCKS

The Beirut Stock Exchange continued to be marked by a good investors’ appetite for banking stocks in view of their attractive market pricing ratios and due to the fact that the banking dividends’ distribution is getting closer. Within this context, the BSE price index rose by 1.1% to close at 111.04. The total trading value amounted to US$ 6.8 million during this week that was shortened to four working days due to holidays, versus US$ 12.3 million in the previous week. The average daily trading value fell from US$ 2.5 million last week to US$ 1.7 million this week, which led to a fall in the trading volume index of 30.9% to 70.11.

Solidere shares accounted for 46.4% of activity this week. Solidere “A” share price declined by 1.3% to US$ 13.90, while Solidere “B” share price remained stable at US$ 13.95. The banking shares captured 53.5% of the total trading value. Bank Audi’s “listed” share price climbed by 6.1% to US$ 6.10. Bank Audi’s GDR price surged by 5.0% to US$ 6.30. BLOM’s GDR price increased by 0.9% to US$ 7.61. Byblos Bank’s “listed” share price closed 0.6% higher at US$ 1.59. As to the industrial stocks, Holcim’s share price declined by 0.7% to

_____________________________________________________________________________FOREIGN EXCHANGE MARKET: ONGOING ACTIVITY IN FAVOR OF THE LP

Activity continued to be in favor of the Lebanese Pound on the foreign exchange market during this week, yet in lower volumes relative to the previous week. Within this context, the Central Bank of Lebanon intervened on Monday as a buyer of the green currency surpluses at the lower end of its intervention bracket (LP 1,501), while commercial banks traded the green currency at a rate hovering between LP 1,501 and LP 1,502.

EXCHANGE RATES

Source: Bank Audi’s Group Research Department

11Week 07 February 06 - February 12, 2012

FEBRUARY 06 - FEBRUARY 12, 2012

WEEK 07

EUROBONDS INDICATORS

Source: Bank Audi’s Group Research Department

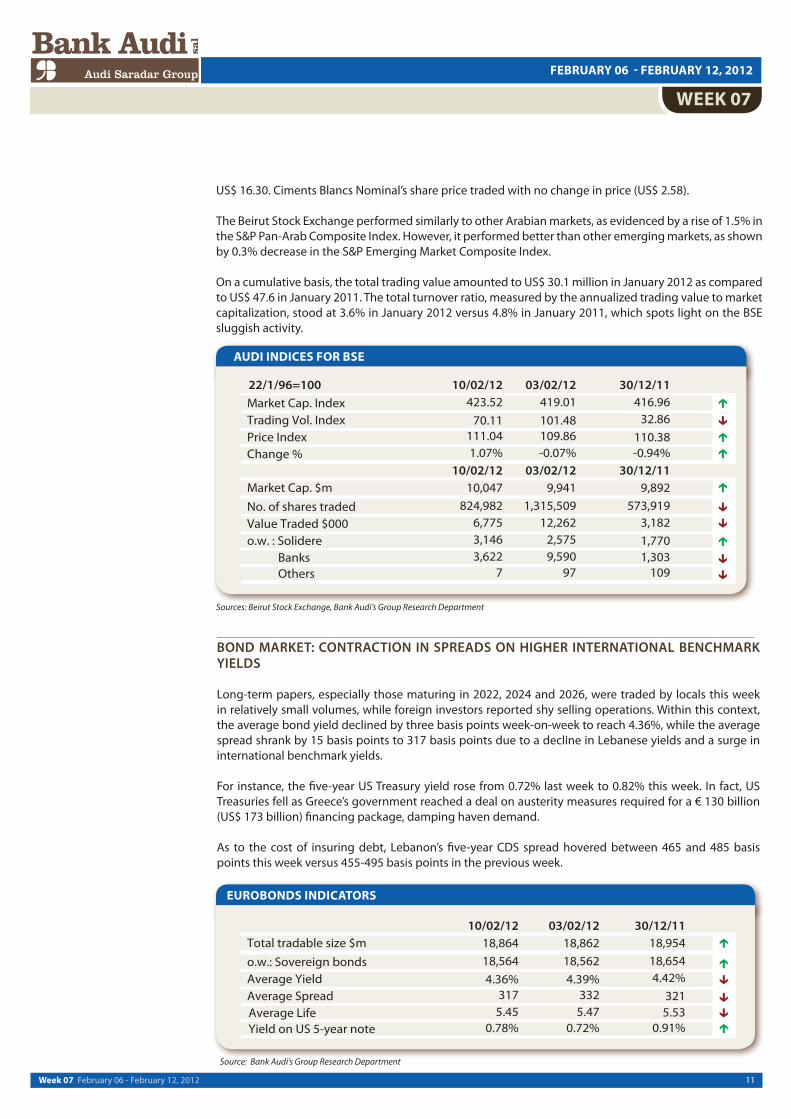

US$ 16.30. Ciments Blancs Nominal’s share price traded with no change in price (US$ 2.58).

The Beirut Stock Exchange performed similarly to other Arabian markets, as evidenced by a rise of 1.5% in the S&P Pan-Arab Composite Index. However, it performed better than other emerging markets, as shown by 0.3% decrease in the S&P Emerging Market Composite Index.

On a cumulative basis, the total trading value amounted to US$ 30.1 million in January 2012 as compared to US$ 47.6 in January 2011. The total turnover ratio, measured by the annualized trading value to market capitalization, stood at 3.6% in January 2012 versus 4.8% in January 2011, which spots light on the BSE sluggish activity.

_____________________________________________________________________________BOND MARKET: CONTRACTION IN SPREADS ON HIGHER INTERNATIONAL BENCHMARK YIELDS

Long-term papers, especially those maturing in 2022, 2024 and 2026, were traded by locals this week in relatively small volumes, while foreign investors reported shy selling operations. Within this context, the average bond yield declined by three basis points week-on-week to reach 4.36%, while the average spread shrank by 15 basis points to 317 basis points due to a decline in Lebanese yields and a surge in international benchmark yields.

For instance, the five-year US Treasury yield rose from 0.72% last week to 0.82% this week. In fact, US Treasuries fell as Greece’s government reached a deal on austerity measures required for a € 130 billion (US$ 173 billion) financing package, damping haven demand.

As to the cost of insuring debt, Lebanon’s five-year CDS spread hovered between 465 and 485 basis points this week versus 455-495 basis points in the previous week.

AUDI INDICES FOR BSE

Sources: Beirut Stock Exchange, Bank Audi’s Group Research Department

12Week 07 February 06 - February 12, 2012

FEBRUARY 06 - FEBRUARY 12, 2012

WEEK 07

INTERNATIONAL MARKET INDICATORS

Sources: Bloomberg, Bank Audi's Group Research Department

___________________________________________________________________________DISCLAIMER

The content of this publication is provided as general information only and should not be taken as an advice to invest or engage in any form of financial or commercial activity. Any action that you may take as a result of information in this publication remains your sole responsibility. None of the materials herein constitute offers or solicitations to purchase or sell securities, your investment decisions should not be made based upon the information herein.

Although Bank Audi Sal Audi Saradar Group considers the content of this publication reliable, it shall have no liability for its content and makes no warranty, representation or guarantee as to its accuracy or completeness.