contemporary issues in venture capital financing … new age banking in india : issues and...

TRANSCRIPT

1New Age Banking in India : Issues and Challenges

Contemporary Issues in Venture

Capital Financing in India

Dr. C. Viswanatha ReddyEditor

New Age Banking in India : Issues and Challenges2

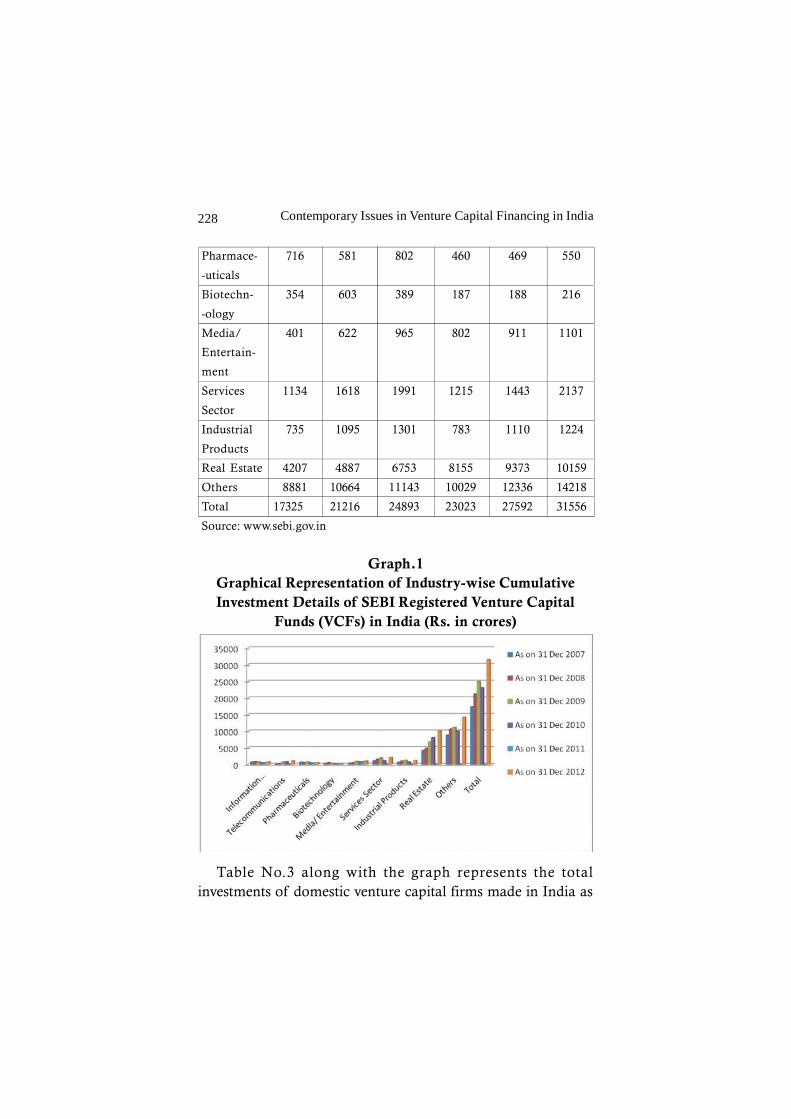

Contemporary Issues in Venture Capital Financing in India

By Dr. C. Viswanatha Reddy (Ed)

Printer and Publisher : Ramesha M.H. for Niruta Publications, # 326,

1st Floor, Opp. Syndicate Bank, Near Dr. AIT College, Kengunte,

Mallathahalli, Bangalore-560056, Ph : 080-23213710, Mob : 9980066890

Email: [email protected], [email protected]

www.socialworkfootprints.org

Copy Right : Editor

First Edition : 2015

ISBN : 978-93-84262-10-5

Pages : x + 374=384

First Impression : 500 copies

Paper : NS Maplitho 70 GSM

Price : Rs. 475-00

Size : 1/8th Demy

Typeset & Coverpage Design : Shivakumar, Niratanka

The views and opinions expressed in this book are the authors’ own and

the facts are as reported by them which have been verified to the extent

possible, and the publishers are not in any way liable for the same.

3New Age Banking in India : Issues and Challenges

Foreword

Young entrepreneurial firms with riskyproduct introduction strategies are facingtrouble in mobilizing funds from equityinvestors and banks because of two reasons.The first one is the conflicts of interest betweenentrepreneurs and investors. Debt financing

from banks may not be available either, because the entrepreneurhas incentives to handle excess risk from the bank’s perspective.He or she benefits, if the firm is successful, whereas the bankstands to lose if the firm fails. The second reason is asymmetricinformation. Equity investors fear that entrepreneurs would onlyissue equity when the firm is overvalued. Capital gains taxationalso affects the demand for venture capital. Venture capitalistsspecialize at solving these problems, thereby connecting idea-rich entrepreneurs with cash-rich investors; ensuring funding forinnovative firms has positive impact on the economy, as it makessense for governments to promote an active venture capital andprivate equity market to bring the nation on par and above thedeveloped nations.

In recent years, the government controlled financialinstitutions have initiated positive and progressive measures toprovide financial support including MSMEs at reasonable andaffordable costs and without any usual hurdles. Government-funded schemes exist at both the national and the state levels.The venture capital and private equity movement did not takedeep roots in India so far, because of lack of further support,high tax rate on capital gains, poor fiscal incentives, lack ofpublic private partnership, no proper review of existing laws,low focus on start up finance, lack of proper implementation

iii

New Age Banking in India : Issues and Challenges4

of the recommendations of the various committees, etc. Hence,there is a need to debate on the issues for the development of asound venture capital and private equity industry in India.

The Government of India in an attempt to bring the nationon the same lines with the developed nations, has beenpromoting venture capital financing to new, innovative concepts& ideas, liberalizing taxation norms, providing tax incentives toventure firms, offering incentives to the creation of local poolsof capital and holding training sessions for the emerging VCinvestors.

In this context, the edited volume entitled “ContemporaryIssues in Venture Capital Financing in India” is timely andrelevant. The issues highlighted and conclusions drawn by theauthors coincide with and reflect the problems in venture capitalfinancing in the world in general and India in particular. Theconclusions and recommendations made by the authors are, nodoubt, more practicable and hence will go a long way forstrengthening the venture capital financing activities in India.

I congratulate the editor of the book, Dr. C. ViswanathaReddy, Professor, Department of Business Administration, SreeVidyanikethan Institute of Management, A.Rangampet – 517102 and the authors of the papers for their effort, initiation,perceptive outlook and pragmatic approach in studying thecontemporary issues in venture capital financing. I hope thisedited volume will be a reference book to the researchers andthe students in the field of finance, a guide to the policy makers.

I wish the editor of the book and authors of the papers allthe best in their academic pursuits in the years to come.

Prof. B. MohanFormer Registrar, Sri Venkateswara University.

Director, Sree Vidyanikethan Inst. of Management

A.Rangampet – 517 102, A.P.

iv

5New Age Banking in India : Issues and Challenges

Acknowledgements

I have received generous help from a number of people to

carry on this work. Without their co-operation and

encouragement, I could not have completed my work. With

pleasure I acknowledge my debt to them.

I wish to express my deep sense of gratitude to our beloved

Chairman of Sree Vidyanikathan Educational Institutions

Padmashri Dr. M. Mohan Babu, for all his great motivation

and affection at every stage of editing this book. This work

would not have come to fruition had it not been for his

encouragement; his friendly advice and affection at every stage

of the work.

I wish to express my heartfelt thanks to Prof. T. Gopala

Rao, the Special officer, Sree Vidyanikethan Educational Trust

for his support and inspiration to do this work.

I will be failing in my duty if I do not express my deep sense

of gratitude and appreciation to Prof. B. Mohan, (Former

Registrar of S.V.University) Director, Sree Vidyanikethan

Institute of Management for his scholarly advice and meticulous

care in shaping my career.

I wish to place on record my profound thanks to my beloved

Teacher-cum-Mentor Prof. D. Himachalam, ICSSR Senior

Fellow, Dept., of Commerce, Sree Venkateswara University,

Tirupati, and the Visiting Professor at Essex Business School,

University of Essex, UK (2009-2015) for his everlasting and

valuable guidance.

I will be failing in my duty, if I do not express my deep sense

v

New Age Banking in India : Issues and Challenges6

of gratitude and appreciation to all the contributors, who have

graciously responded to my request and permitted me to include

their scholarly contributions in this edited volume.

I wish to thank all my colleagues in the department who

continuously encouraged and motivated me to complete this

academic endeavour successfully.

I am also thankful to my wife Smt. C. Lakhmi Tulasi, and

my son Master C. Sainatha Reddy, who have co-operated with

me during my preoccupation with this work by sacrificing their

golden moments without my presence.

Last but not the least, I would be happy to place on record

my profound gratitude and appreciation to Sri Ramesha MH

and his team of Niruta Publications, Bangalore who readily

agreed to take up the task of bringing out this volume in a short

span of time in the present shape.

Dr. C. Viswanatha Reddy

vi

7New Age Banking in India : Issues and Challenges

Contents

1. An Overview of Venture Capital and - 1-31

Private Equity Financing in India

Dr. T. Narayana Reddy

Dr. C. Viswanatha Reddy

2. Venture Capital Financing: Key Elements - 32-37

Prof. P.R. Sivasankar, Mr. K. Rajaiah

3. Comparative Analysis of Sectoral - 38-66

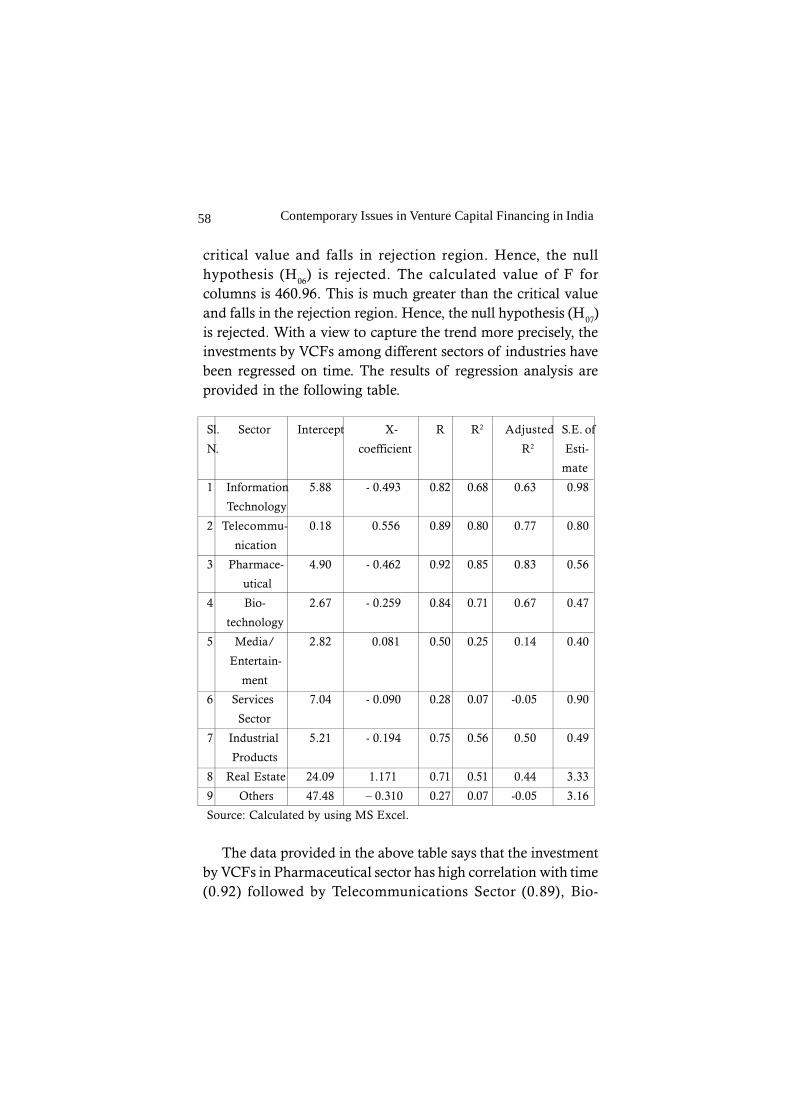

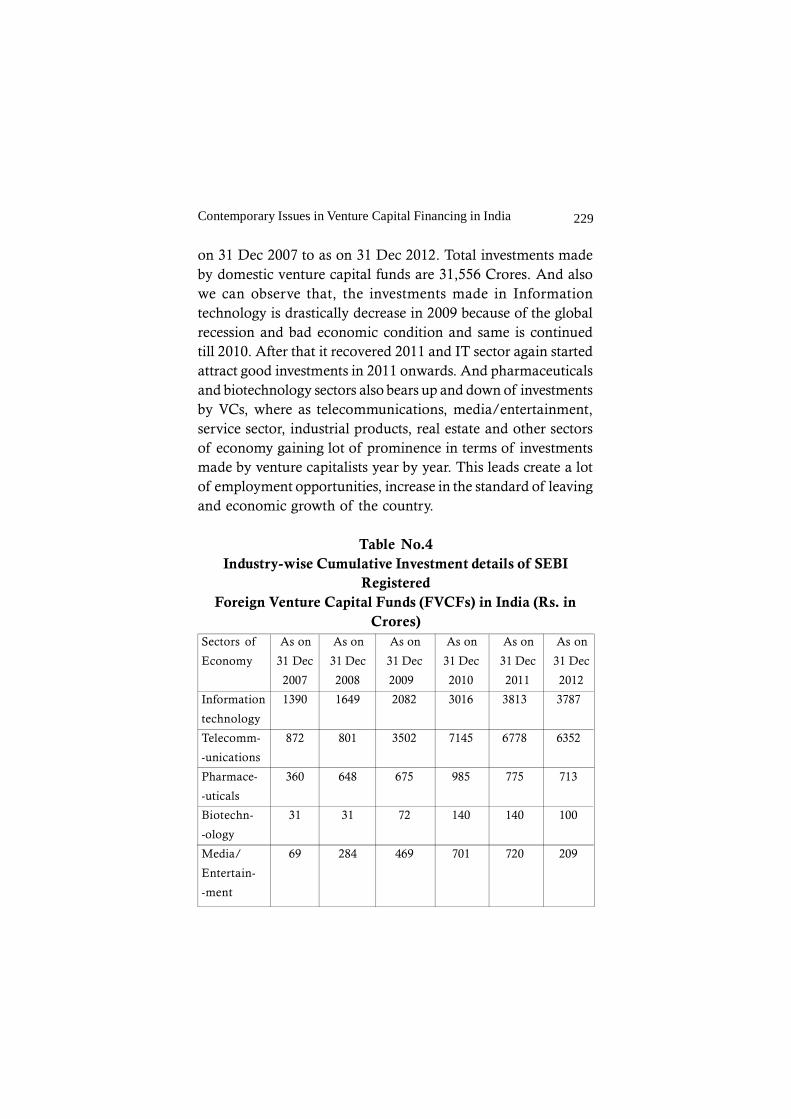

Financing by VCFs and FVCIs in India

Dr. E. Lokanadha Reddy

Dr. C. Viswanatha Reddy

4. Monitoring The Performance of Venture - 67-77

Capital Funded Companies

Dr. E. Lokanadha Reddy

Dr. A. Amruth Prasad Reddy

Dr. V.N. Jothi

5. Private Equity Investemnts in India: - 78-83

A Review

Dr. V Vijay Durga Prasad

6. Venture Capital Financing in India & - 84-93

Its Prospects

Dr. D.H. Malini Srinivasa Rao

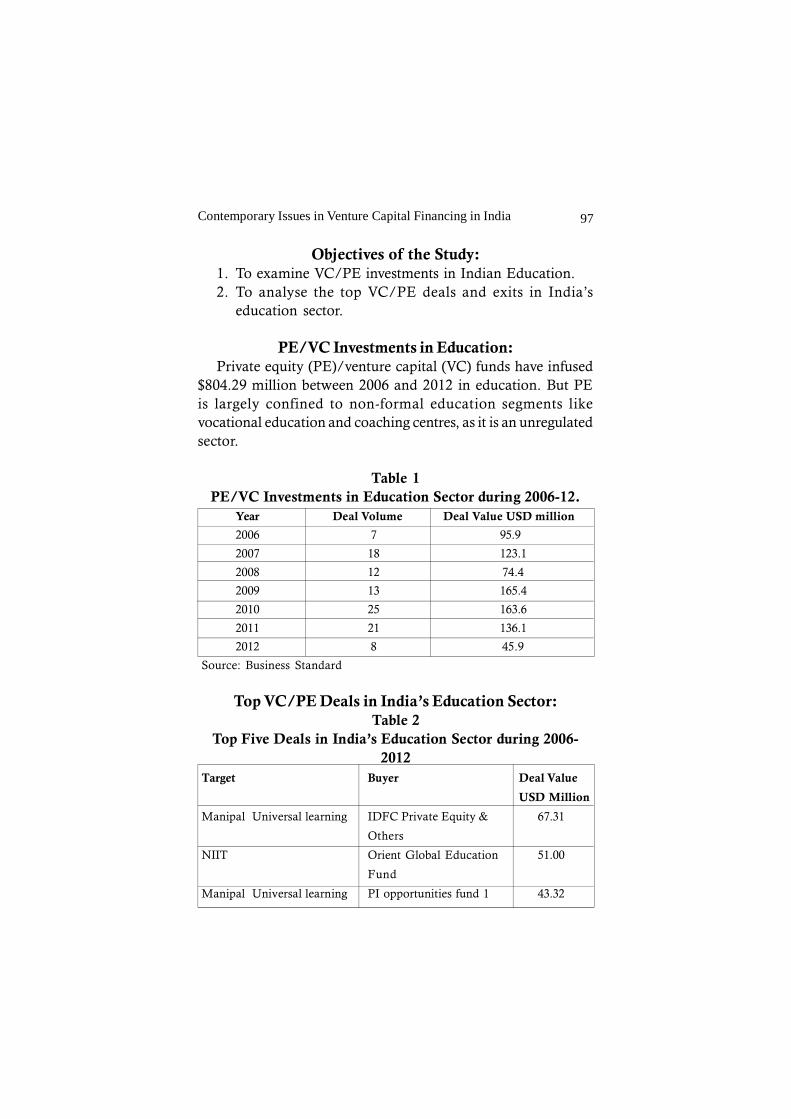

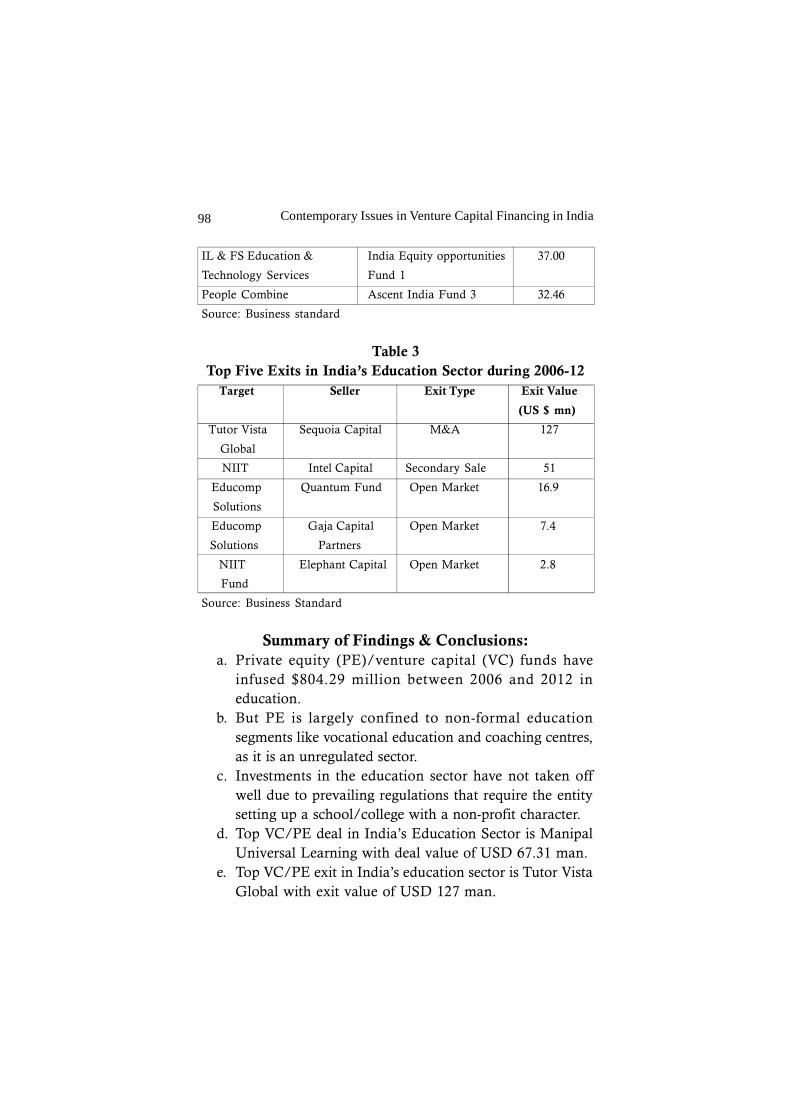

7. Venture Capital/Private Equity (Vc/Pe) - 94-99

Funding in India’s Education Sector:

A Perspective

Gangineni Dhananjhay, Archana G

vii

New Age Banking in India : Issues and Challenges8

8. Across the Sector Venture Capital - 100-110

Investments in India

Dr. P. Niranjan Reddy, Dr. J. Prakash Reddy

9. Role of Venture Capital for Growth of - 111-120

MSMEs–A Study of SIDBI Venture

Capital Limited

Dr. Sujatha Susanna Kumari D, Mr. Basavaraj

10. Development of MSMEs Through - 121-127

Public Private Partnership

Dr. G. Vijaya Bharathi, Ms. S. Masthani

Mr. P. Harinatha Reddy

11. Venture Capital Investments in India - 128-140

During 2007-12

Dr. V. N. Jothi

12. Venture Capital for MSMEs in India: - 141-151

A Review

S. Dilli, Dr. K. Jayachandra Reddy

13. Venture Capital Financing in India: - 152-160

Problems and Prospects

Dr. M. Lokanadha Reddy, Mr. Harinath. K

Mr. Lakshminarayana. S

14. A Study on Role of Venture Capital in - 161-177

Indian Economy

Gajanethi Swathi Kumari

15. Changing Scenario of Insurance Sector - 178-194

with the Entry in Private Equity–The

Way Forward

Dr. Suresh Chandra. C.H., Mr. B. Naresh

viii

9New Age Banking in India : Issues and Challenges

16. Performance Analysis on Venture - 195-222

Capital in Select Undertakings

Mr. D. Prem Kumar, Mr. B. Naresh

17. Venture Capital Investments in India - 223-232

Dr. K. Ekambaram, Sk. Rameez Raja

18. Venture Capital - A Theoretical - 233-242

Perspective, Growth and Challenges

in India

Dr. P. Subbaiah, Mr. V.Harikrishna

Mr. P.V.L.Narasimha Rao

19. Venture Capital Financing in India - - 243-260

Challenges Ahead

Dr. D. Rajashekar, D. Prem Kumar

20. Private Equity – Opportunities and - 261-269

Challenges

M. Saritha

21. A Study on Venture Capital Challenges - 270-280

in India: Conceptual Approach

Mr. A. Sreeenivasulu, Mr. M. Suresh

22. Evolution of Global Private Equity - 281-294

Market Implications and Prospects for

India

Dr. G. Venkatachalam, Mrs. K. Kalyani

Prof. P. Mohan Reddy

23. A Study on Venture Capital Financing - 295-305

Sources in India

Mrs. N. Chandrika, Prof. G. V. Chalam

ix

New Age Banking in India : Issues and Challenges10

24. A Study on Venture Capital Financing - 306-321

for MSMEs in India

W. R. Sony, S. Gautami, K. Tirumalaiah

25. Contemporary Issues in Venture Capital - 322-330

Finance for Women Entreprenuer

Mrs. Sandra Kirthy

26. Regulatory Aspects of Venture Capital - 331-335

Financing in India

V. Lava Kumar, V. Komala

27. New Venture Valuation by Venture - 336-344

Capitalists: An Integrative Approach

V. Radhika

28. Regulatory Frame Work of Venture - 345-353

Capital Financing in India

U. Chandramouli

29. Growth and Prospects of Venture - 354-362

Capital Finance in India

Dr. Ravi Kumar, Dr. Ch. Rama Krishna

30. Venture Capital Funding for Social - 363-372

Enterprises

Dr. S. Srinivasa Rao, S. Durga

x

1Contemporary Issues in Venture Capital Financing in India

An Overview of Venture Capital andPrivate Equity Financing in India

Dr. T. Narayana Reddy*

Dr. C. Viswanatha Reddy**

AbstractKnowledge based ideas, scientific technology and innovative

enterprises and converting them into commercial production are thekey motivators for the promotion of venture capital (VC) and privateequity (PE) activities in any country. Given the inherent strengths,viz., advancement in science and technology, research, competitiveentrepreneurship, the skilled and cost competitive manpower withexcellent policy support, rapid and sustainable economic growth andcompetitive global strength, India has become a strong hub for venturecapital financing activities. The budding VC and PE industry in Indiawill fill the gap between the capital requirements of start-up enterprisesin various sectors, which are of technological and knowledge basedand the funding available from traditional institutional lenders suchas banks, etc. Conversely, the venture capital activity in India did nottake deep roots so far, because of lack of proper implementation ofthe recommendations of various committees, high tax rates on capitalgains, poor economic incentives, unclear guidelines for public privatepartnership, low focus on start up finance, Therefore, the presentpaper is a modest attempt in this direction aims at explaining theprofile of venture capital and private equity industry in India, theirproblems, contemporary scenario, causes for poor performance inthe recent past, avenues for further development, etc.

Key Words: Venture Capital, Private Equity, DFIs, SIDBI.

* Assistant Professor & Head Department of Humanities, JNTUA College ofEngineering, Anantapuramu.

** Professor, Sree Vidyanikethan Institute of Management, A.Rangampet – 517102, Tirupati (A.P)

Contemporary Issues in Venture Capital Financing in India2

Introduction:Firms at young entrepreneurial stage with risky and

innovative product strategies are facing trouble in mobilizingrisk capital from equity investors and banks. There are tworeasons for such situation, i.e., (a) the conflicts of interestbetween entrepreneurs and investors; (b) asymmetricinformation. From the bankers perspective the entrepreneur hasincentives to take on excessive risk, i.e., the entrepreneur benefitsif the firm is successful, whereas the bank stands to lose if thefirm fails. Equity investors fear that entrepreneurs would onlyissue equity when the firm is overvalued. Capital gains taxationalso affects the demand for venture capital. The specializedventure capitalists plays a predominant role in solving theseproblems, therefore, linking idea-rich entrepreneurs with cash-rich investors, ensuring funding for innovative firms has positiveexternalities on the economy. So, it makes sense for governmentsto promote an active venture capital and private equity marketto bring the nation at par and above the developed nations.

In spite of the best efforts, the venture capital and privateequity movement did not take deep roots in India so far, due tolack of supplementary support, high tax rate on capital gains,poor financial incentives, lack of public private partnership,absence of review of existing laws, low focus on start up finance,ineffective implementation of the recommendations of thevarious committees, etc. Hence, there is a need to debate onthe issues for the development of a sound venture capital andprivate equity industry in India. But, in the recent years, thegovernment controlled financial institutions have initiatedpositive and progressive measures to provide financial supportincluding MSMEs at reasonable and affordable costs and withoutany usual hurdles.

Statement of the Problem:The contemporary business firms required to be resourceful

with respect to cost, productivity, labour efficiency, flexibility

3Contemporary Issues in Venture Capital Financing in India

to consumer demand, adaptability and foresightedness.Therefore, there is an imminent demand for highly cost effective,quality products and hence the need for right access to valuablehuman expertise to guide and monitor along with the necessaryfunds for financing the new projects. The Government of Indiain an attempt to fetch the nation at par and above the developednations, has been promoted venture capital financing to new,innovative concepts & ideas, liberalizing taxation norms,providing tax incentives to venture firms, giving scope for thecreation of local pools of capital and holding training sessionsfor the emerging VC investors. The present paper entitled “AnOverview of Venture Capital and Private Equity Financing inIndia” is a modest attempt in this direction which focuses onthe current scenario of Indian venture capital and private equityfinancing industry, problems in venture capital and private equityfinancing in India, risk involved in such financing, operationalperformance of venture capital and private equity financing inthe recent past in India, and offers some useful suggestions forstrengthening of such industry in India.

Objectives of the study:The objectives of the study are as follows:1. To emphasize the chronological progress of venture

capital and private equity financing in India.2. To illuminate the contemporary scenario of venture

capital and private equity financing system in India.3. To scrutinize problems involved and risks connected with

venture capital and private equity financing in India.4. To bid some valid suggestions for further reinforcement

of venture capital and private equity financing in India.

Research Methodology:Research design:

In view of the objectives of the study listed above, thedescriptive research design has been adopted. Descriptive

Contemporary Issues in Venture Capital Financing in India4

research is one which largely interprets the historical data/information and it lays particular emphasis on analysis andinterpretation of the existing and available information and itmakes use of secondary data.

Sources of data:The study is based on secondary data. The secondary data

required for the study has been collected from the variouswebsites, websites of different venture capital and private equityfinanciers, etc. The respective source from which the data hascompiled is mentioned at each table under source.

Hypothesis of the Study:Based on the data available and association between them,

the following hypothesis is developed.H0: There is a statistical relationship between volume of

private equity deals (number of deals) and deal value (amountin million dollars).

Tools of Analysis:The data collected for the study has analysed logically and

meaningfully to arrive at logical and meaningful conclusions.The statistical tools applied for data analysis are percentage,average, pie-diagrams, line graphs, correlation coefficient, leastsquares analysis, etc.

Scope of the study:The scope of the present paper is defined in terms of concepts

under focus. Firstly, the Indian scenario of venture capital andprivate equity financing, policy support for the growth anddevelopment of such activities in India, and SEBI’s role hasbeen covered. Secondly, the risks involved in venture capitaland private equity financing in India, innovative instrumentsfor venture capital financing, recent avenues for investment, arehighlighted. Thirdly, the binary concepts of venture capital and

5Contemporary Issues in Venture Capital Financing in India

private equity financing in terms of number of deals, deal valueand the relationship between them has been discussed. Fourthly,the problems of venture capital and private equity financing inIndia were examined. Lastly, few of the suggestions were offeredfor further strengthening of these activities in India.

Limitations of the Study:Since the concept of venture capital and private equity

financing is a strange subject in India, much research has nottaken place. So, it is difficult to find enough amount of literatureon the topic.

Historical Development of VC and PE Financing inIndia:

Before the emergence During this period, the DFIs have beenof Venture Capital partially playing the same role –Financing System in through direct equity participation toIndia. ventures at pre-public issue stage.

During early 70’s when Govt of Indiaappointed a committee lead by LateShri R.S.Bhatt to find out the ways tomeet a void in conventional financingfor funding start-up companies basedon absolutely new innovativetechnologies. Such companies either didnot get any financial support or thefunding was inadequate which resultedinto their early mortality. Thecommittee recommended starting ofVenture Capital industry in India.

Mid 80’s In mid 80’s three All IndiaDevelopment Financial Institutions(DFIs), viz., IDBI, ICICI, IFCI startedinvesting into the equity of smalltechnological companies.

Contemporary Issues in Venture Capital Financing in India6

Institutionalization of In Nov 1988, Govt of India decidedVC Industry to institutionalize Venture Capital

Industry and announced the guidelinesin parliament. Controller of CapitalIssues implemented these guidelinesknown as CCI for VC and suchguidelines were very restrictive andfollowed a very narrow definition ofVC. They required venture capital tobe invested in companies based oninnovative technologies started by firstgeneration entrepreneur. This made VCinvestment highly risky andunattractive.

World Bank’s During the same era, the World BankIntervention in selected 6 institutions to start VCIndian VC Industry investment in India, viz., TDICICI

(ICICI), GVFL, Can bank VentureCapital Fund, APIDC, RCTC (nowknown as IFCI Venture Capital FundsLtd.) and ILF (now known asPathfinder).

Exemption from IT Up to 1995, the VCFs were paying aon Dividend and 20% tax on capital gains fromCapital gains investments. During the budget speech

for the year 1995-96, the financeminister made an announcement thatthe exemption from tax on income byway of dividend and long- term capitalgains from equity investments made byapproved VCFs in unlisted companies.CBDT took the responsibility andnotified a scheme. Section 10(23FA)of Income Tax Act was re-enacted to

7Contemporary Issues in Venture Capital Financing in India

provide for automatic income taxexemption to VCFs registered withSEBI (like in the case of mutual funds)which will eliminate the taxation at thepool level while maintaining the sameat investor level.

Issue of Guidelines In September 1995, Govt of Indiafor Foreign Finance issued guidelines and permitted foreignCompanies finance companies to make

investments in India and many foreignventure capital and private equity firmsentered India.

Govt. guidelines to In 1996, government announced theregulate VC Industry guidelines to regulate the VC industry.

Though there were manyshortcomings these guidelines were thestarting point.

IT Boom & VC In 1997, IT boom in India made VCIndustry industry more significant. Due to

symbiotic relationship between VC andIT industry, VC got more prominenceas a major source of funding for therapidly growing IT industry. Indian VC’swhich were so far investing in all thesectors changed their focus to IT andtelecom industry.

VC Industry during The recession during 1999 - 2001 tookRecession the wind out of VC industry. Most of

the Venture Capitalists either closeddown or wound-up their operations.Almost all of them changed their focusto existing successful firms for theirgrowth and expansion. Currently, justa few firms are taking the risk of

Contemporary Issues in Venture Capital Financing in India8

investing into the start-up technologybased companies. VC firms also gotengaged into funding buyouts,privatisation and restructuring.

SEBI’s Role in Indian Venture Capital Industry:The Government of India constituted a SEBI committee

headed by K. B. Chandrasekhar to make recommendations tofacilitate the growth of VC industry in India. This committeesubmitted its report in July 2000 with the following salientrecommendations, all of which were accepted and implemented:

1. SEBI should be the nodal regulator for VC funds in Indiaproviding a smooth, single window, problem-freeregulatory framework for quick and efficient flow ofmoney into VC funds in India.

2. Tax pass-through status should be granted to all regulatorycompliant VC funds, similar to that which is provided tomutual funds, ensuring that at the “pool-level” (VC Fund)profits are tax exempt.

Foreign venture capital investors (FVCI) should also beregistered with SEBI. This registration should enable them tohave the same facilities as the foreign institutional level of easyinvestments and disinvestments without any FIBP/RBIapprovals

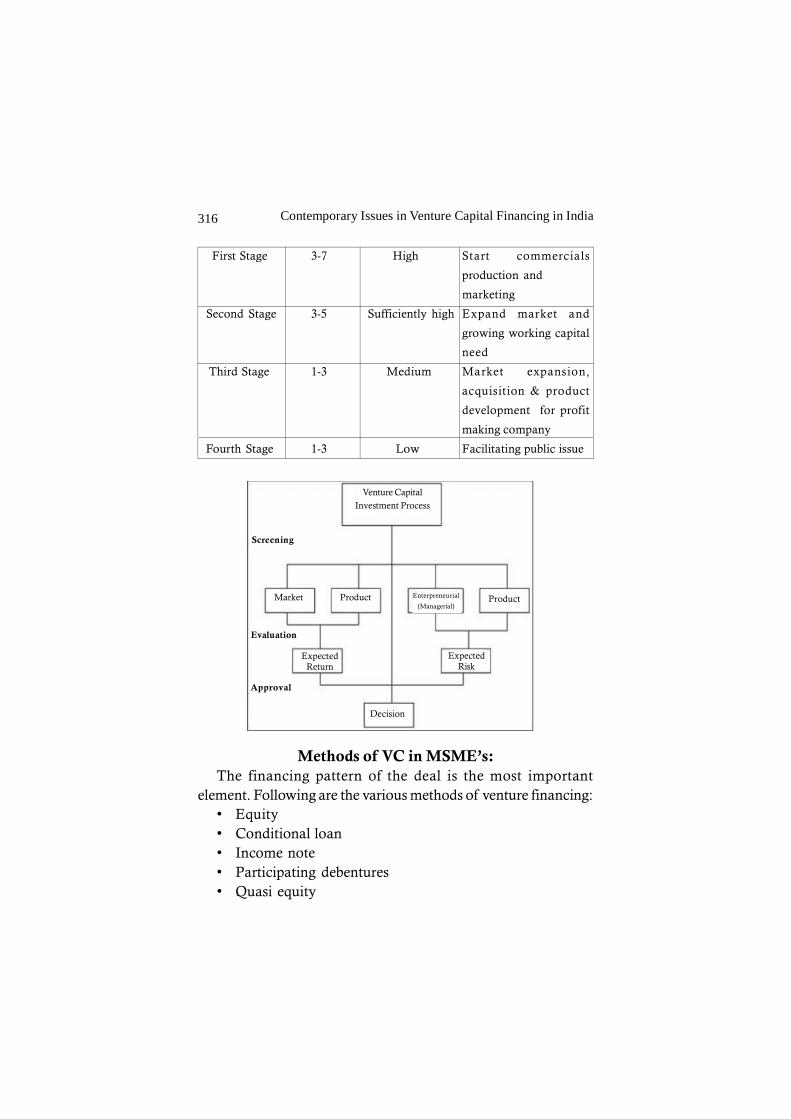

Table No.1Financing Stage of Venture Capital and Risk Perception

Stages of Funds Lock- Risk Perception Activities to be Financed

Financing in Period

(Years)

Seed Money 7-10 Extreme High * To Support the Concept

or Idea.

* R & D for Product

Development.

9Contemporary Issues in Venture Capital Financing in India

Start Up 5-9 Very High * To Initialize Operations.

* To develop Prototypes.

First Stage 3-7 High * To start commercials

production and

marketing.

Second 3-5 Sufficiently High * To expand market.

Stage * To meet the growing

capital needs.

Third Stage 1-3 Medium * To expand market.

* Acquisition of profit

making company.

Fourth Stage 1-3 Low * For facilitating public

issue.

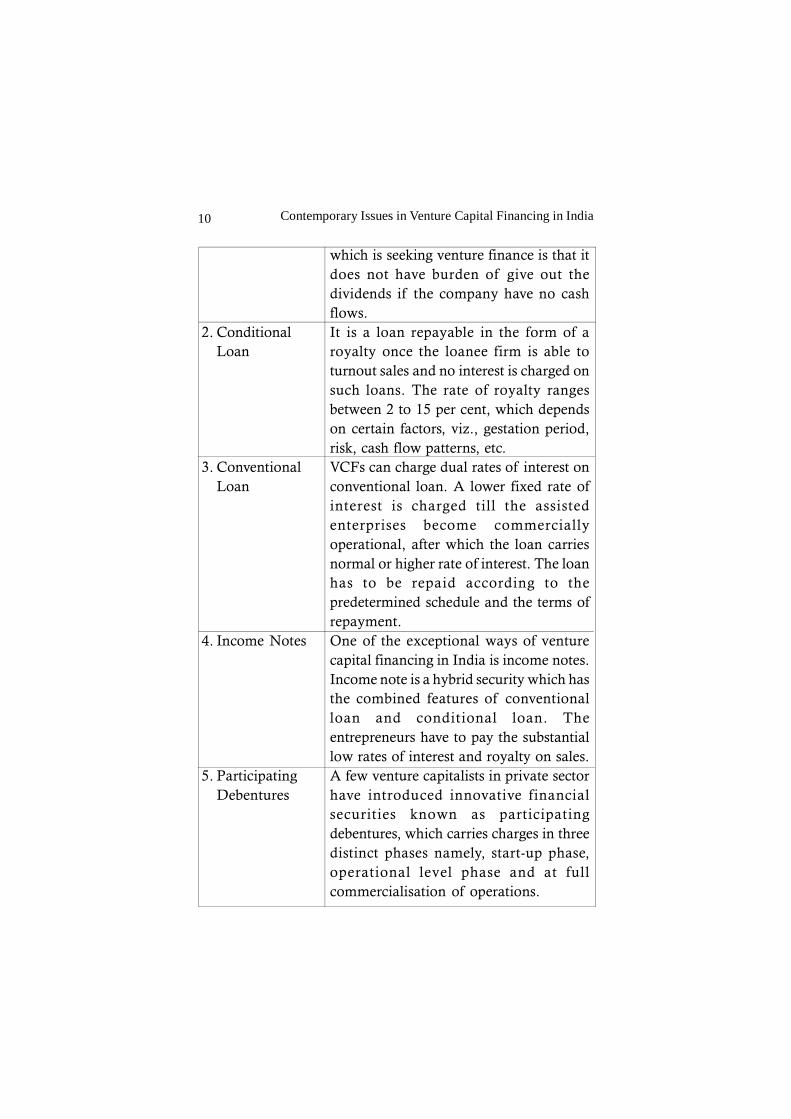

Innovative Instruments for Venture Capital Financing:One of the preconditions for the development of an active

and healthy venture capital industry is the availability of anarray of financial instruments, which will trade-off between risk-return needs of investors. Innovation in financial instruments isan added feature of developed and developing nations for thegrowth of venture capital industry. There is a line of variationbetween such instruments among developed and developingcountries. Following table No.2 provides the information oninnovative financial instruments designed for venture capitalfinancing.

Table No.2Instruments Intended for Venture Capital Financing

Case-1: In Developed and Developing countries:1. Equity All VCFs in India are providing financing

through participation. The majority ofownership and control over the firm in thehands of the entrepreneur. The gain ofequity financing intended for the company

Contemporary Issues in Venture Capital Financing in India10

which is seeking venture finance is that itdoes not have burden of give out thedividends if the company have no cashflows.

2. Conditional It is a loan repayable in the form of aLoan royalty once the loanee firm is able to

turnout sales and no interest is charged onsuch loans. The rate of royalty rangesbetween 2 to 15 per cent, which dependson certain factors, viz., gestation period,risk, cash flow patterns, etc.

3. Conventional VCFs can charge dual rates of interest onLoan conventional loan. A lower fixed rate of

interest is charged till the assistedenterprises become commerciallyoperational, after which the loan carriesnormal or higher rate of interest. The loanhas to be repaid according to thepredetermined schedule and the terms ofrepayment.

4. Income Notes One of the exceptional ways of venturecapital financing in India is income notes.Income note is a hybrid security which hasthe combined features of conventionalloan and conditional loan. Theentrepreneurs have to pay the substantiallow rates of interest and royalty on sales.

5. Participating A few venture capitalists in private sectorDebentures have introduced innovative financial

securities known as participatingdebentures, which carries charges in threedistinct phases namely, start-up phase,operational level phase and at fullcommercialisation of operations.

11Contemporary Issues in Venture Capital Financing in India

6. Cumulative Particularly, in Indian context, theConvertible Cumulative Convertible Preference SharesPreference are very attractive because the holders ofShares these shares do not have voting right.

However, they are entitled to vote if theydo not receive dividend consecutively fortwo years.

Case-2: In Developed Countries:7. Deferred Shares Deferred shares are those shares do not

have any rights to the assets of a companyundergoing bankruptcy until all commonand preferred shareholders are paid. Thevalue of these shares fluctuates with themarket and cannot be accessed by thebeneficiary for the purpose of liquidationuntil they are no longer employees of thecompany. In other words, deferred sharesare the shares where ordinary share rightsare deferred for a certain number of years.

8. Convertible Convertible loan stock is an unsecuredLoan Stock long-term loan to a company in the form

of bonds that can later be converted intoordinary shares under certain conditions.

9. Special Ordinary The holders of these shares will haveShares voting right but no commitment towards

dividends.10.Preferred Preferred ordinary share holders will have

Ordinary Shares voting right with a right get a modest fixeddividend and share in profits.

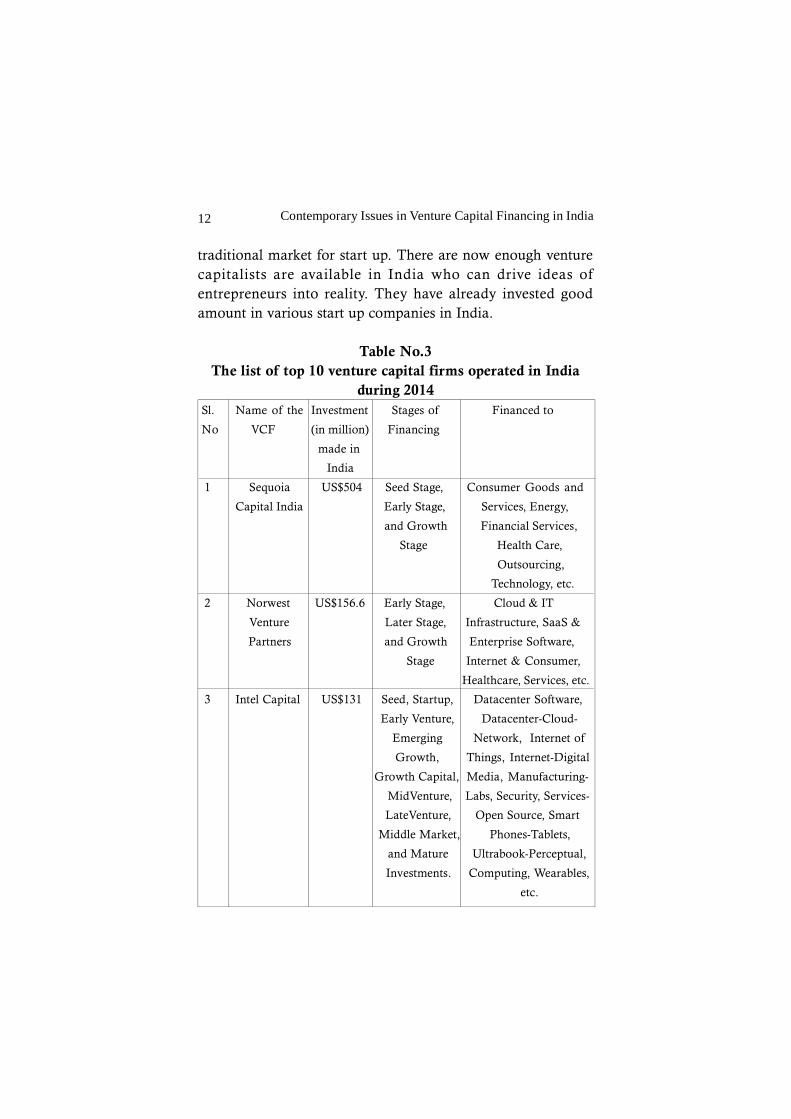

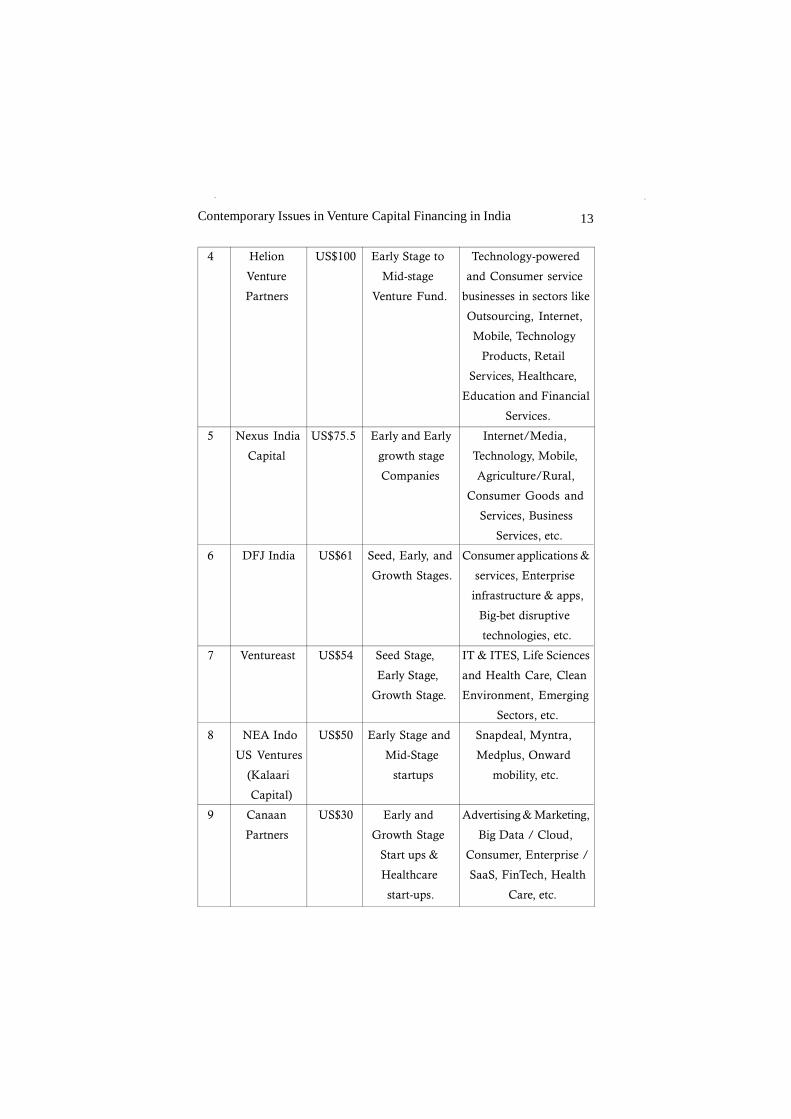

Top 10 Venture Capital Companies in India by theirinvestments:

Ventura capital is the lifeline of any start up in their growthstory. In the past, it was difficult to raise funds from the

Contemporary Issues in Venture Capital Financing in India12

traditional market for start up. There are now enough venturecapitalists are available in India who can drive ideas ofentrepreneurs into reality. They have already invested goodamount in various start up companies in India.

Table No.3The list of top 10 venture capital firms operated in India

during 2014Sl. Name of the Investment Stages of Financed to

No VCF (in million) Financing

made in

India

1 Sequoia US$504 Seed Stage, Consumer Goods and

Capital India Early Stage, Services, Energy,

and Growth Financial Services,

Stage Health Care,

Outsourcing,

Technology, etc.

2 Norwest US$156.6 Early Stage, Cloud & IT

Venture Later Stage, Infrastructure, SaaS &

Partners and Growth Enterprise Software,

Stage Internet & Consumer,

Healthcare, Services, etc.

3 Intel Capital US$131 Seed, Startup, Datacenter Software,

Early Venture, Datacenter-Cloud-

Emerging Network, Internet of

Growth, Things, Internet-Digital

Growth Capital, Media, Manufacturing-

MidVenture, Labs, Security, Services-

LateVenture, Open Source, Smart

Middle Market, Phones-Tablets,

and Mature Ultrabook-Perceptual,

Investments. Computing, Wearables,

etc.

13Contemporary Issues in Venture Capital Financing in India

4 Helion US$100 Early Stage to Technology-powered

Venture Mid-stage and Consumer service

Partners Venture Fund. businesses in sectors like

Outsourcing, Internet,

Mobile, Technology

Products, Retail

Services, Healthcare,

Education and Financial

Services.

5 Nexus India US$75.5 Early and Early Internet/Media,

Capital growth stage Technology, Mobile,

Companies Agriculture/Rural,

Consumer Goods and

Services, Business

Services, etc.

6 DFJ India US$61 Seed, Early, and Consumer applications &

Growth Stages. services, Enterprise

infrastructure & apps,

Big-bet disruptive

technologies, etc.

7 Ventureast US$54 Seed Stage, IT & ITES, Life Sciences

Early Stage, and Health Care, Clean

Growth Stage. Environment, Emerging

Sectors, etc.

8 NEA Indo US$50 Early Stage and Snapdeal, Myntra,

US Ventures Mid-Stage Medplus, Onward

(Kalaari startups mobility, etc.

Capital)

9 Canaan US$30 Early and Advertising & Marketing,

Partners Growth Stage Big Data / Cloud,

Start ups & Consumer, Enterprise /

Healthcare SaaS, FinTech, Health

start-ups. Care, etc.

Contemporary Issues in Venture Capital Financing in India14

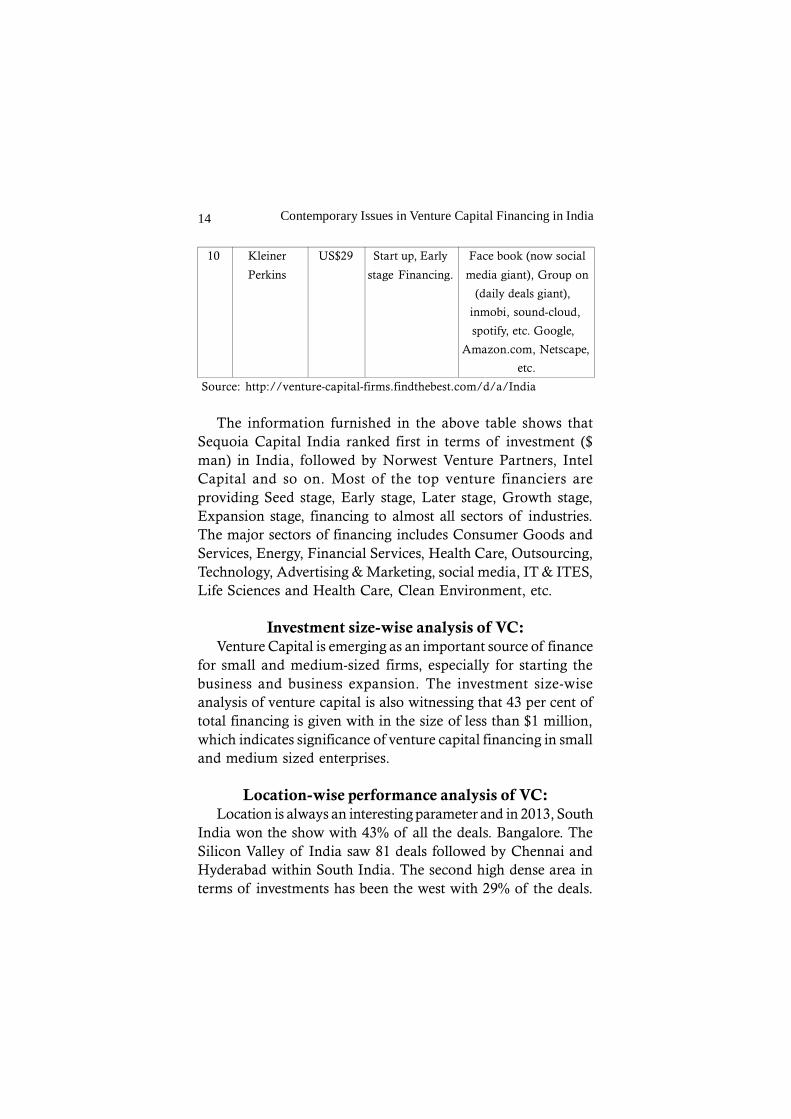

10 Kleiner US$29 Start up, Early Face book (now social

Perkins stage Financing. media giant), Group on

(daily deals giant),

inmobi, sound-cloud,

spotify, etc. Google,

Amazon.com, Netscape,

etc.

Source: http://venture-capital-firms.findthebest.com/d/a/India

The information furnished in the above table shows thatSequoia Capital India ranked first in terms of investment ($man) in India, followed by Norwest Venture Partners, IntelCapital and so on. Most of the top venture financiers areproviding Seed stage, Early stage, Later stage, Growth stage,Expansion stage, financing to almost all sectors of industries.The major sectors of financing includes Consumer Goods andServices, Energy, Financial Services, Health Care, Outsourcing,Technology, Advertising & Marketing, social media, IT & ITES,Life Sciences and Health Care, Clean Environment, etc.

Investment size-wise analysis of VC:Venture Capital is emerging as an important source of finance

for small and medium-sized firms, especially for starting thebusiness and business expansion. The investment size-wiseanalysis of venture capital is also witnessing that 43 per cent oftotal financing is given with in the size of less than $1 million,which indicates significance of venture capital financing in smalland medium sized enterprises.

Location-wise performance analysis of VC:Location is always an interesting parameter and in 2013, South

India won the show with 43% of all the deals. Bangalore. TheSilicon Valley of India saw 81 deals followed by Chennai andHyderabad within South India. The second high dense area interms of investments has been the west with 29% of the deals.

15Contemporary Issues in Venture Capital Financing in India

Mumbai is the clear winner here with 55 of all the deals. NorthIndia came in third with 57 deals.

Companies headquartered in Bangalore and Mumbai werethe favourite among VC investors. During 2013 attracting 49investments each, followed by Delhi based companies thataccounted for 24 investments and Chennai based companieswith 21 investments.

Table No.4Size-wise and Region-wise analysis of Venture capital

Financing in 2014Size of Investment Percentage to Total Region of the Percentage to

Country Total

Less than $1 million 43 per cent South Region 43 per cent

Less than $5 million 30 per cent West Region 29 per cent

Between $5 and 15 per cent North Region 21 per cent

$10 million

Greater than 12 per cent Others 7 per cent

$10 million

Source: www.vccedge.com

Investment Banks and Private Equity in India:An investment bank is a financial institution that assists

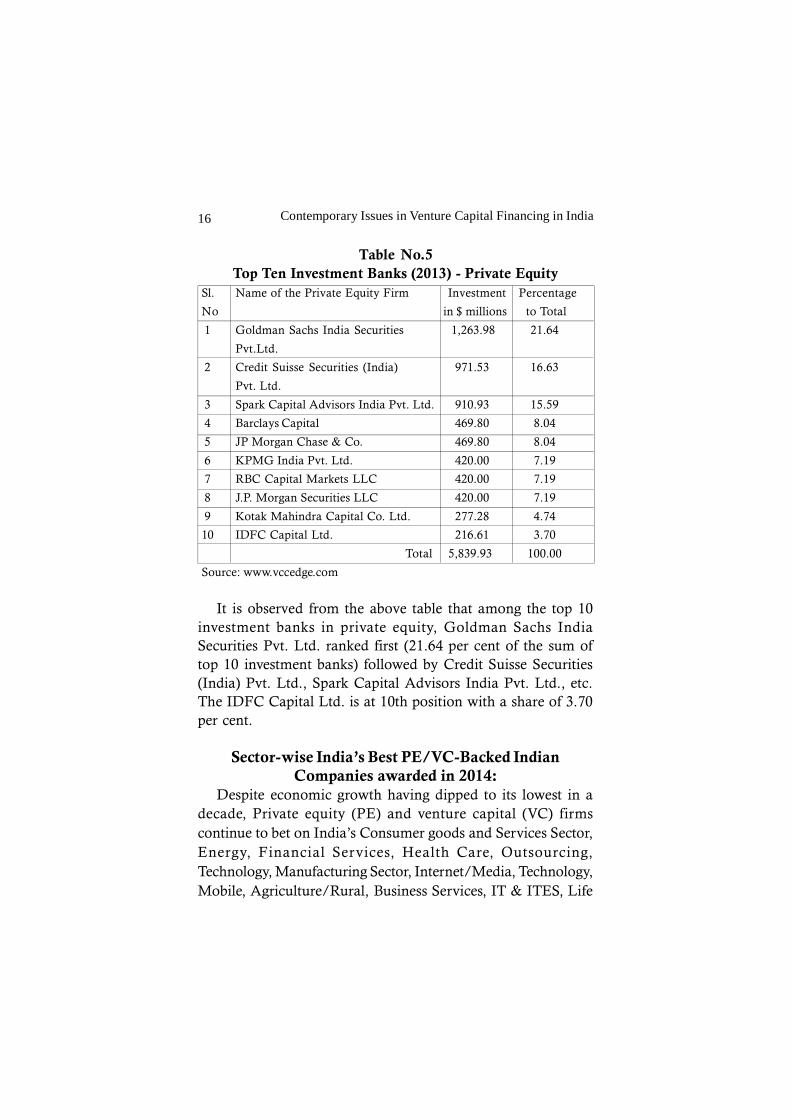

individuals, corporations, and governments in raising capital byunderwriting or acting as the client’s agent in the issuance ofsecurities (or both). An investment bank may also assistcompanies involved in mergers and acquisitions and provideancillary services such as market making, trading of derivativesand equity securities, and FICC services (fixed incomeinstruments, currencies, and commodities). Private equityinvestors function similar to Investment Bankers, but whereInvestment Bankers advise on transactions, Private Equityinvestors make investments directly into private companies orconduct buyouts of public and private companies. The list oftop 10 investment bankers along with their investment is givenin the following table No.5.

Contemporary Issues in Venture Capital Financing in India16

Table No.5Top Ten Investment Banks (2013) - Private Equity

Sl. Name of the Private Equity Firm Investment Percentage

No in $ millions to Total

1 Goldman Sachs India Securities 1,263.98 21.64

Pvt.Ltd.

2 Credit Suisse Securities (India) 971.53 16.63

Pvt. Ltd.

3 Spark Capital Advisors India Pvt. Ltd. 910.93 15.59

4 Barclays Capital 469.80 8.04

5 JP Morgan Chase & Co. 469.80 8.04

6 KPMG India Pvt. Ltd. 420.00 7.19

7 RBC Capital Markets LLC 420.00 7.19

8 J.P. Morgan Securities LLC 420.00 7.19

9 Kotak Mahindra Capital Co. Ltd. 277.28 4.74

10 IDFC Capital Ltd. 216.61 3.70

Total 5,839.93 100.00

Source: www.vccedge.com

It is observed from the above table that among the top 10investment banks in private equity, Goldman Sachs IndiaSecurities Pvt. Ltd. ranked first (21.64 per cent of the sum oftop 10 investment banks) followed by Credit Suisse Securities(India) Pvt. Ltd., Spark Capital Advisors India Pvt. Ltd., etc.The IDFC Capital Ltd. is at 10th position with a share of 3.70per cent.

Sector-wise India’s Best PE/VC-Backed IndianCompanies awarded in 2014:

Despite economic growth having dipped to its lowest in adecade, Private equity (PE) and venture capital (VC) firmscontinue to bet on India’s Consumer goods and Services Sector,Energy, Financial Services, Health Care, Outsourcing,Technology, Manufacturing Sector, Internet/Media, Technology,Mobile, Agriculture/Rural, Business Services, IT & ITES, Life

17Contemporary Issues in Venture Capital Financing in India

Sciences and Health Care, Clean Environment, EducationSector, Emerging Sectors, etc. Table No.6 gives us the datapertaining to the India’s best PE/VC backed companies awardedin 2014 in different sectors.

Table No.6 Sector-wise India’s Best PE/VC-Backed Indian Companies

awarded in 2014Sector Company

IT Company iGate Corporation

Consumer Internet Company Myntra Designs Private Ltd.

Education Company Manipal Global Education Services Private

Ltd

Financial Services Company Repco Home Finance Ltd.

Healthcare Company Cloudnine Hospitals (Kids Clinic)

Manufacturing Company International Tractors Ltd.

Infrastructure Company GMR Airports Ltd.

Source: www.vccedge.com

It is observed from the above table that the iGate Corporationawarded as the best PE/VC backed company awarded from ITSector, Myntra Designs Private Ltd., from Consumer InternetSector, Manipal Global Education Services Private Ltd., fromEducation Sector, Repco Home Finance Ltd., from FinancialServices Sector, Cloudnine Hospitals (Kids Clinic) from HealthCare Sector, International Tractors Ltd., from ManufacturingSector and GMR Airports Ltd., from Infrastructure Industry.

Snapshot of Volume and Value of Private equity deals in2013 &14:

Private Equity and Venture Capital is an increasingly sourceof finance for high growth potential companies. The goal ofprivate equity and venture capital is to help more businesses toachieve their ambitions for growth by providing them with

Contemporary Issues in Venture Capital Financing in India18

finance, strategic advice and information at critical stages oftheir development. The month-wise analysis of private equityinvestments is provided in the following table No.7.

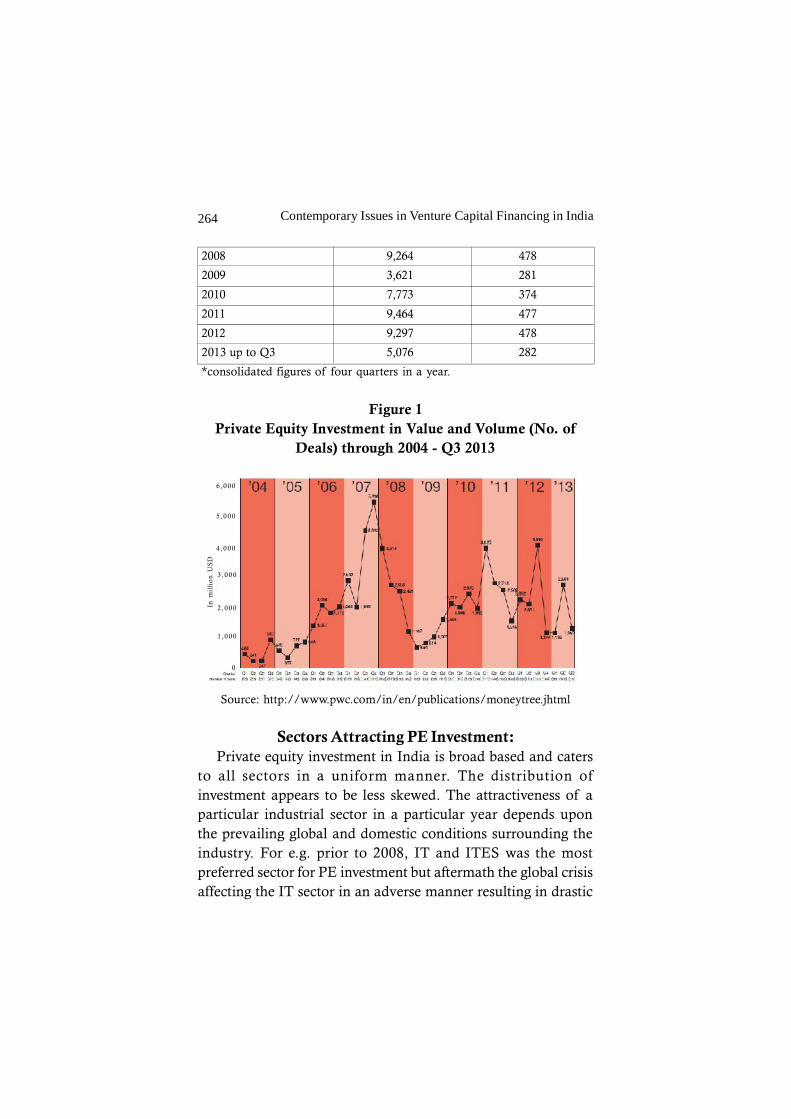

Table No.7Month-wise analysis of Private Equity Investments

Month Volume of Deal Month Volume of Deal

Private Value Private Value

Equity ($mn) Equity ($mn)

Deals Deals

June, 2013 51 987 April, 2014 77 1,051

July, 2013 50 951 May, 2014 62 1,430

August, 2013 58 738 June, 2014 71 926

September, 50 830 July, 2014 59 1,496

2013

October, 51 940 August, 2014 60 747

2013

November, 61 495 September, 65 813

2013 2014

December, 65 347 October, 2014 61 1,576

2013

January, 39 574 November, 75 1,467

2014 2014

February, 48 1,164 December, 64 865

2014 2014

Source: www.vccedge.com

It is observed from the data provided in the above table thatthe volume of private equity deals has increased from 51 inJune, 2013 to 77 in April, 2014. Further the same has declinedto 64 in December, 2014. During the same period, the deal valuehas increased from $987mn in June, 2013 to $1,164mn inDecember, 2014 and again increased to $1,576mn in October,2014. The correlation analysis between the volume of privateequity deals and deal value ($man) is as follows:

19Contemporary Issues in Venture Capital Financing in India

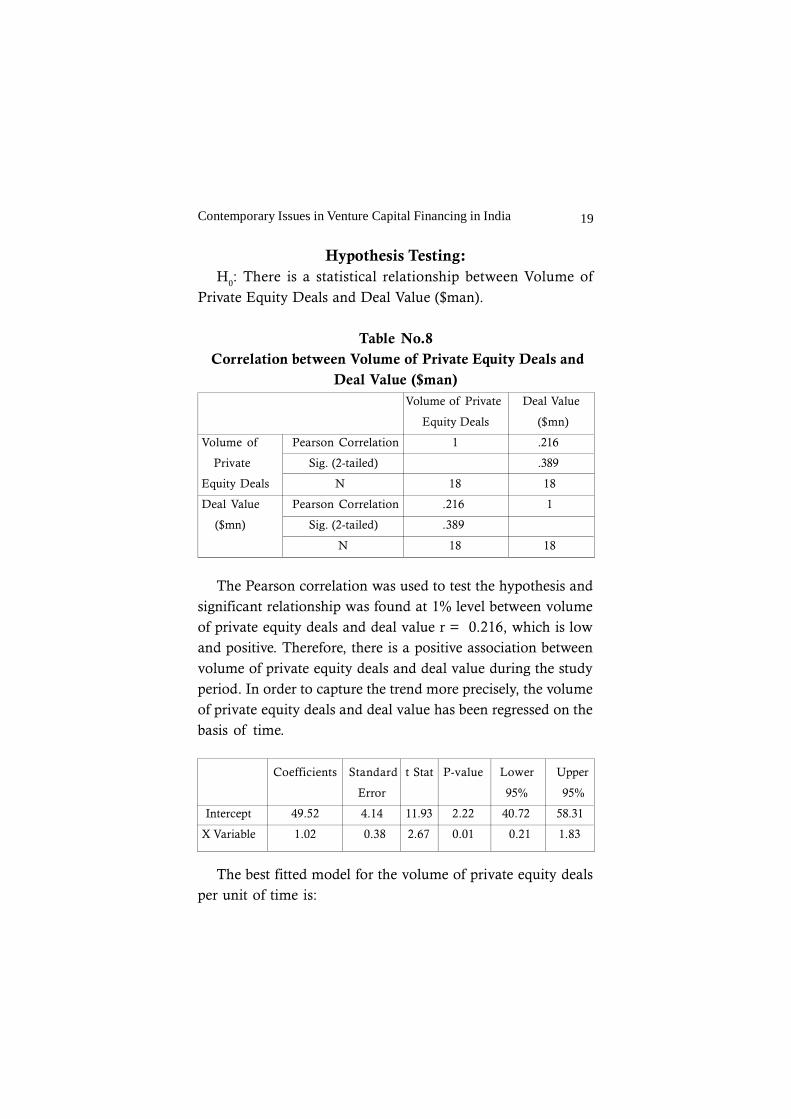

Hypothesis Testing:H0: There is a statistical relationship between Volume of

Private Equity Deals and Deal Value ($man).

Table No.8 Correlation between Volume of Private Equity Deals and

Deal Value ($man)Volume of Private Deal Value

Equity Deals ($mn)

Volume of Pearson Correlation 1 .216

Private Sig. (2-tailed) .389

Equity Deals N 18 18

Deal Value Pearson Correlation .216 1

($mn) Sig. (2-tailed) .389

N 18 18

The Pearson correlation was used to test the hypothesis andsignificant relationship was found at 1% level between volumeof private equity deals and deal value r = 0.216, which is lowand positive. Therefore, there is a positive association betweenvolume of private equity deals and deal value during the studyperiod. In order to capture the trend more precisely, the volumeof private equity deals and deal value has been regressed on thebasis of time.

Coefficients Standard t Stat P-value Lower Upper

Error 95% 95%

Intercept 49.52 4.14 11.93 2.22 40.72 58.31

X Variable 1.02 0.38 2.67 0.01 0.21 1.83

The best fitted model for the volume of private equity dealsper unit of time is:

Contemporary Issues in Venture Capital Financing in India20

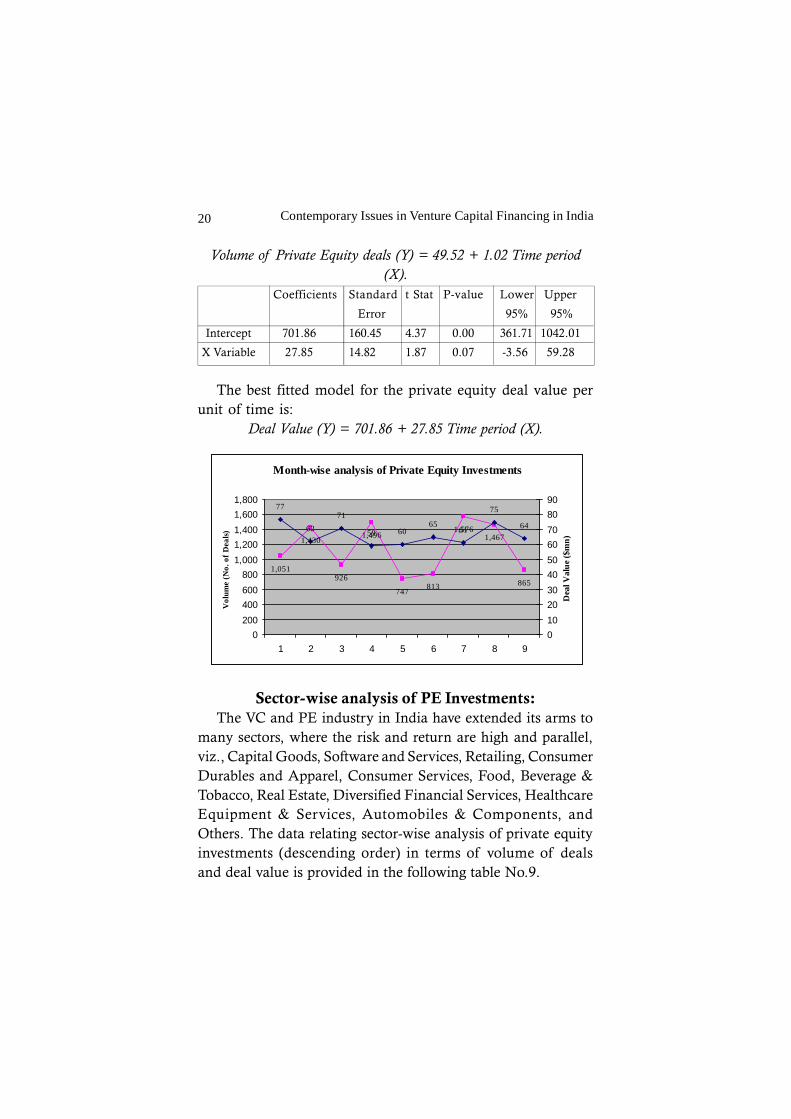

Volume of Private Equity deals (Y) = 49.52 + 1.02 Time period(X).

Coefficients Standard t Stat P-value Lower Upper

Error 95% 95%

Intercept 701.86 160.45 4.37 0.00 361.71 1042.01

X Variable 27.85 14.82 1.87 0.07 -3.56 59.28

The best fitted model for the private equity deal value perunit of time is:

Deal Value (Y) = 701.86 + 27.85 Time period (X).

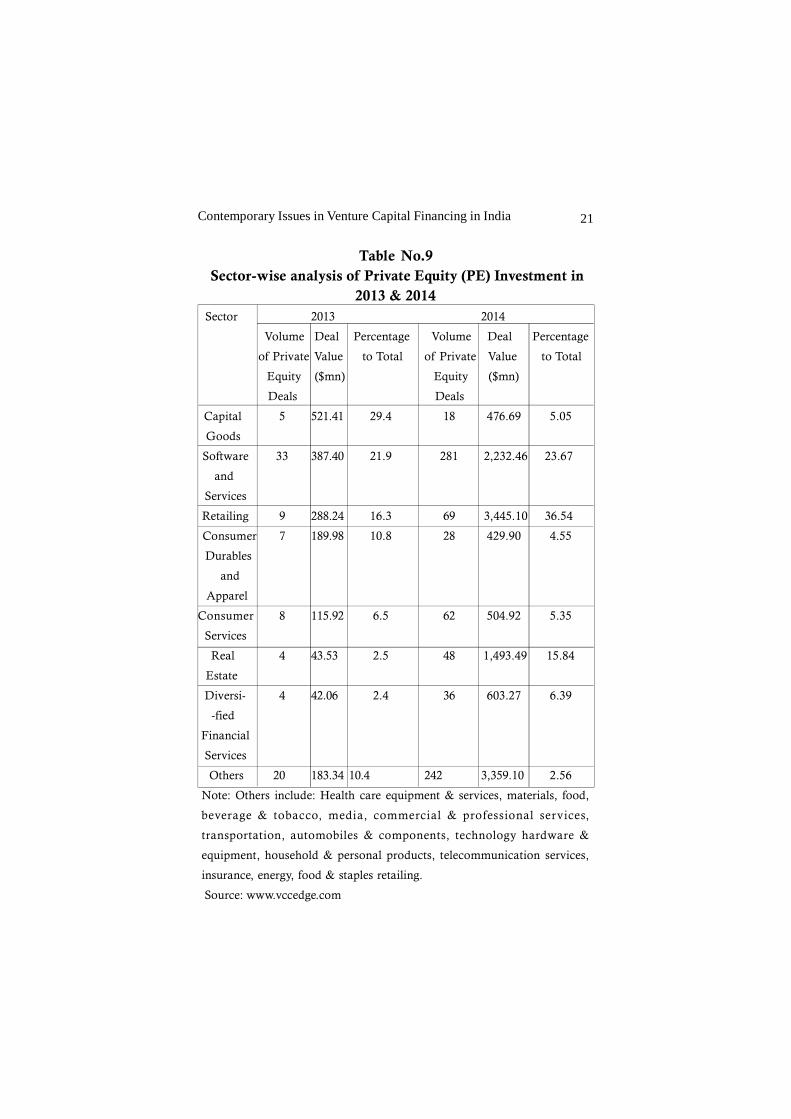

Sector-wise analysis of PE Investments:The VC and PE industry in India have extended its arms to

many sectors, where the risk and return are high and parallel,viz., Capital Goods, Software and Services, Retailing, ConsumerDurables and Apparel, Consumer Services, Food, Beverage &Tobacco, Real Estate, Diversified Financial Services, HealthcareEquipment & Services, Automobiles & Components, andOthers. The data relating sector-wise analysis of private equityinvestments (descending order) in terms of volume of dealsand deal value is provided in the following table No.9.

Month-wise analysis of Private Equity Investments

1,051

1,430

926

1,496

747813

1,5761,467

865

77

62

71

59 6065

61

75

64

0200400600800

1,0001,2001,4001,6001,800

1 2 3 4 5 6 7 8 9

Vol

ume

(No.

of

Dea

ls)

0102030405060708090

Dea

l Val

ue

($m

n)

21Contemporary Issues in Venture Capital Financing in India

Table No.9 Sector-wise analysis of Private Equity (PE) Investment in

2013 & 2014 Sector 2013 2014

Volume Deal Percentage Volume Deal Percentage

of Private Value to Total of Private Value to Total

Equity ($mn) Equity ($mn)

Deals Deals

Capital 5 521.41 29.4 18 476.69 5.05

Goods

Software 33 387.40 21.9 281 2,232.46 23.67

and

Services

Retailing 9 288.24 16.3 69 3,445.10 36.54

Consumer 7 189.98 10.8 28 429.90 4.55

Durables

and

Apparel

Consumer 8 115.92 6.5 62 504.92 5.35

Services

Real 4 43.53 2.5 48 1,493.49 15.84

Estate

Diversi- 4 42.06 2.4 36 603.27 6.39

-fied

Financial

Services

Others 20 183.34 10.4 242 3,359.10 2.56

Note: Others include: Health care equipment & services, materials, food,

beverage & tobacco, media, commercial & professional services,

transportation, automobiles & components, technology hardware &

equipment, household & personal products, telecommunication services,

insurance, energy, food & staples retailing.

Source: www.vccedge.com

Contemporary Issues in Venture Capital Financing in India22

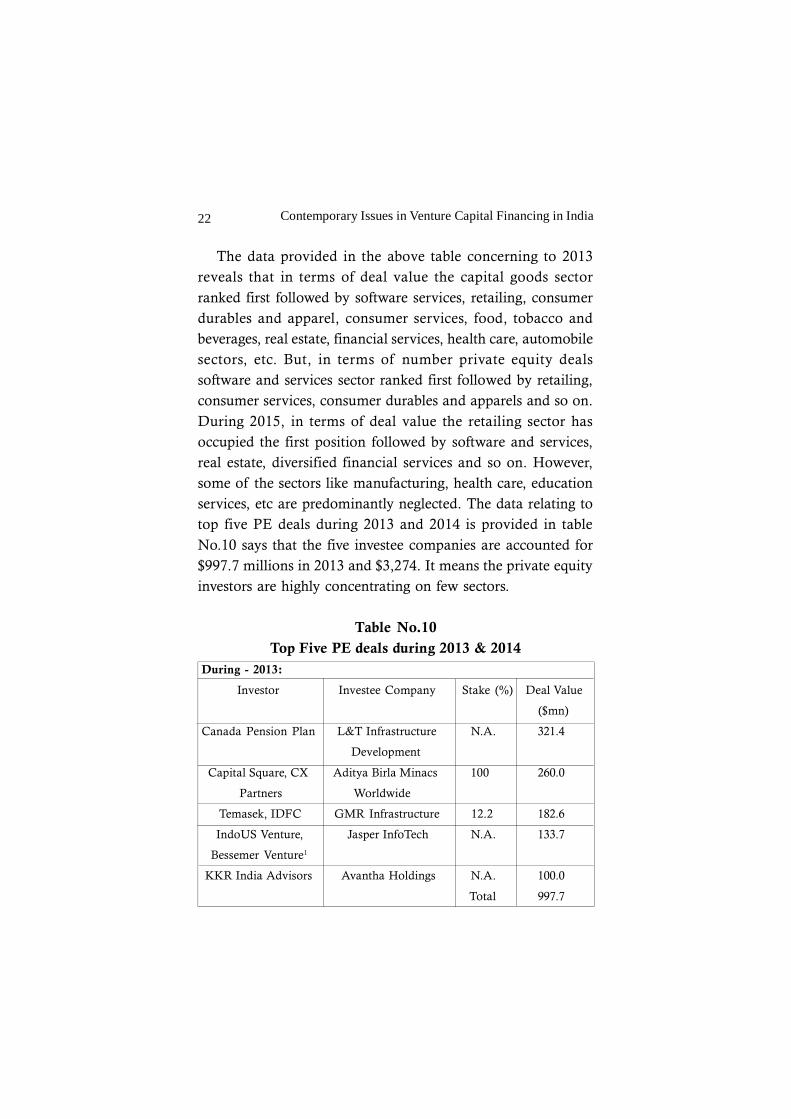

The data provided in the above table concerning to 2013reveals that in terms of deal value the capital goods sectorranked first followed by software services, retailing, consumerdurables and apparel, consumer services, food, tobacco andbeverages, real estate, financial services, health care, automobilesectors, etc. But, in terms of number private equity dealssoftware and services sector ranked first followed by retailing,consumer services, consumer durables and apparels and so on.During 2015, in terms of deal value the retailing sector hasoccupied the first position followed by software and services,real estate, diversified financial services and so on. However,some of the sectors like manufacturing, health care, educationservices, etc are predominantly neglected. The data relating totop five PE deals during 2013 and 2014 is provided in tableNo.10 says that the five investee companies are accounted for$997.7 millions in 2013 and $3,274. It means the private equityinvestors are highly concentrating on few sectors.

Table No.10Top Five PE deals during 2013 & 2014

During - 2013:

Investor Investee Company Stake (%) Deal Value

($mn)

Canada Pension Plan L&T Infrastructure N.A. 321.4

Development

Capital Square, CX Aditya Birla Minacs 100 260.0

Partners Worldwide

Temasek, IDFC GMR Infrastructure 12.2 182.6

IndoUS Venture, Jasper InfoTech N.A. 133.7

Bessemer Venture1

KKR India Advisors Avantha Holdings N.A. 100.0

Total 997.7

23Contemporary Issues in Venture Capital Financing in India

During - 2014:

Tiger Global, Accel Flipkart 7.0 1,000

India Venture Fund2

Steadview Capital Flipkart 6.4 700

Master Fund, Tiger

Global3

Black Rock, Inc, Jasper Info-tech 32.5 636.7

Tybourne Capital4

Brookfield Asset Unitech IT Park SEZ N.A 563.2

Management Inc Business

Canada Pension Plan Kotak Mahindra Bank 3.2 373.7

Investment Board Ltd

Total 3,2741Includes Nexus India Capital II, eBay Inc., Intel Capital, Saama Capital II.2Includes: Iconiq Capital LLC, MIH Holdings Ltd, Morgan Stanley

Investment Management Inc, DST Global, GIC Special Investments Pte

Ltd, Sofina Societe.3Includes: MIH Holdings Ltd, DST Global, The Qatar Investment

Authority, GIC Special Investments Pte Ltd, Iconiq Capital LLC.4Includes: Temasek Holdings Advisors India Pvt. Ltd, Soft Bank Corp, PI

Opportunities Fund-I, Myriad Asset Management

N.A.: Not Available.

Source: www.vccedge.com

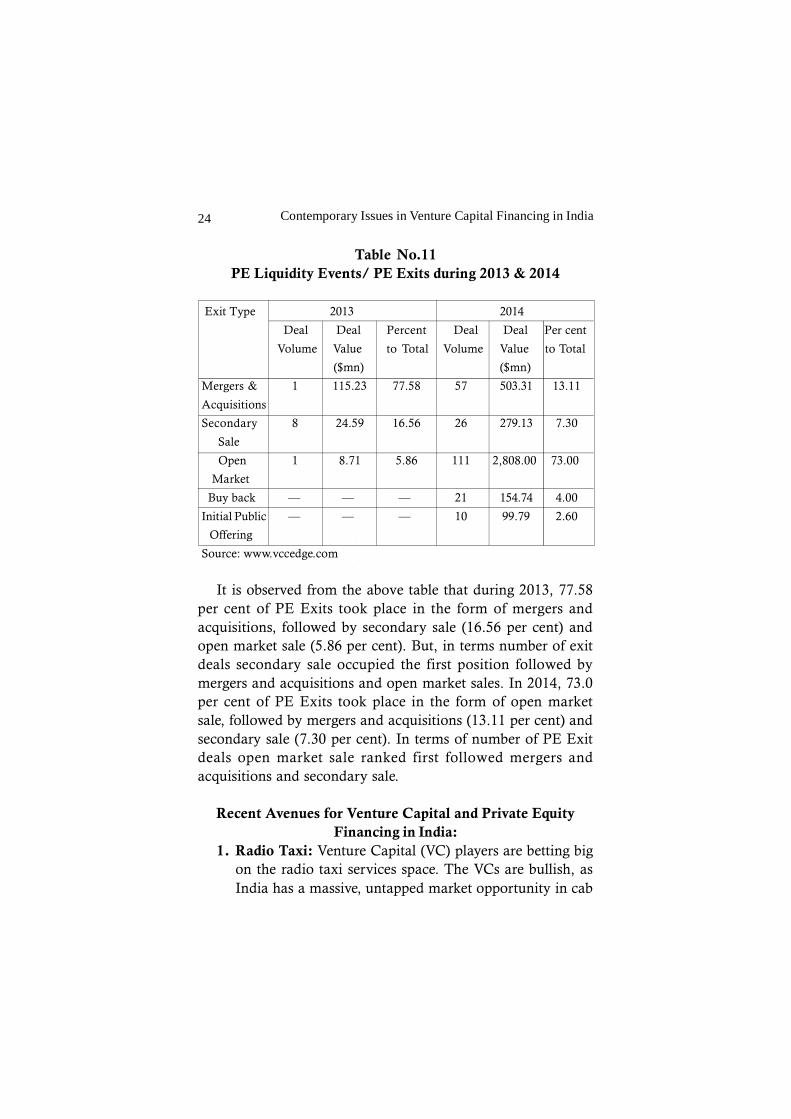

PE Exits during 2013:One of the serious limitations of private equity financing is

the investors may withdraw their funds as and when they foundunhappy with the investee company. Normally, PE exists takesplace in the form of mergers and acquisitions, secondary saleand open market sale. The information pertaining to PE exitsduring 2013 is provided in table No.11.

Contemporary Issues in Venture Capital Financing in India24

Table No.11PE Liquidity Events/ PE Exits during 2013 & 2014

Exit Type 2013 2014

Deal Deal Percent Deal Deal Per cent

Volume Value to Total Volume Value to Total

($mn) ($mn)

Mergers & 1 115.23 77.58 57 503.31 13.11

Acquisitions

Secondary 8 24.59 16.56 26 279.13 7.30

Sale

Open 1 8.71 5.86 111 2,808.00 73.00

Market

Buy back — — — 21 154.74 4.00

Initial Public — — — 10 99.79 2.60

Offering

Source: www.vccedge.com

It is observed from the above table that during 2013, 77.58per cent of PE Exits took place in the form of mergers andacquisitions, followed by secondary sale (16.56 per cent) andopen market sale (5.86 per cent). But, in terms number of exitdeals secondary sale occupied the first position followed bymergers and acquisitions and open market sales. In 2014, 73.0per cent of PE Exits took place in the form of open marketsale, followed by mergers and acquisitions (13.11 per cent) andsecondary sale (7.30 per cent). In terms of number of PE Exitdeals open market sale ranked first followed mergers andacquisitions and secondary sale.

Recent Avenues for Venture Capital and Private EquityFinancing in India:

1. Radio Taxi: Venture Capital (VC) players are betting bigon the radio taxi services space. The VCs are bullish, asIndia has a massive, untapped market opportunity in cab

25Contemporary Issues in Venture Capital Financing in India

aggregation. There are about 6,00,000 taxis in theunorganised sector that can be aggregated, which is a $2.5-billion opportunity. Five deals worth $30 million had takenplace in 2013 against $7 million in 2012. The radio taxiservices segment has witnessed 21 deals worth about $103million in the past seven years.

2. Apparel Space: Venture capital and PE firms haveconsistently shown interest in the apparel space, as a proxyof domestic consumption demand. Investors pumped in$115.4 million in 15 apparel firms in 2013.

3. Eco System: 2013 has been a year full of activity for theIndian start-up ecosystem. A wave of optimism surgingthrough a pool of pessimism, there has always beensomething to cheer about. 2012 saw more than $760million being invested via more than 200 deals and thenumber has risen in 2013 to over a $1.6 billion via 293deals.

4. Logistics: Logistics is another area in which VCs areexpected to invest (data is not available).

5. Film Production: The other prospective area in whichVCs and PEs would make huge investments includesIndian film production. The Indian film industry currentlyis worth 1.8 billion and is expected to grow @of over25% and would reach a level of USD over 5 billion by2011. With the newly accorded status of industry andprofessionalism on film industry, it will emerge as newvenue for VCs.

6. Education: This is another prospective area in which VCsand PEs would make huge investments. With a boomingeconomy and concurrent talent shortage, denying forservices from the domestic education sector is slated tocreate a lucrative opportunities for VCs. A global privateequity firm with $36 billion in assets is planningapproximately $200 million investments in the Indian

Contemporary Issues in Venture Capital Financing in India26

education sector by taking up strategic positions incompanies offering e-learning, distant learning, vocationaltraining and the like.

7. Beauty Saloon: In Mumbai, Affinity Beauty Salon Pvt.Ltd is in talks with private equity (PE) firms to raise asmuch as Rs.100 crores by selling a significant minoritystake to fund its expansion plans, according to a companyofficial.

8. Real Estate: Looking at Venture Capital in the last fewyears, the biggest investment in India would have been inInfo-tech, or in services (like Flip kart) or even in telecom.But strangely, the biggest investment as a percentage hasbeen Real Estate. Since 2007, Venture Capital Investmentsin Real Estate have beaten others by a large margin, andas of December 2012 were nearly at Rs. 10,000 crores(about 30% higher than the next sector - Telecom).

Problems of Indian Venture Capital and Private EquityIndustry:

The issues relating to venture capital funding are:1. Product risk: The products concerned may have little or

no track record in the markets as they are largely untestedand usually have high rates of obsolescence.

2. Entrepreneur risk: Another of the disadvantages ofventure capital funding is that it is difficult to evaluatethe new management and new business applicationwithout any prior track record.

3. Concentration risk: Focusing on small market, which canrelate to either the product or in geographical terms, raisesexposure to sectoral downturn.

4. Technology risk: It is very hard to assess new technologyon small set of products.

5. Duration risk: Generally a longer long-gestation period forfunding is needed (longer pay-back period).

27Contemporary Issues in Venture Capital Financing in India

6. Asset risk: Due to a high percentage of fixed assets withhigh obsolescence, along with a high fraction of humancapital, there is a lack of collateralizable assets, which isone of the drawbacks in venture capital funding.

7. Small deal size: This is not found economical by mostinvestors.

Obtaining private equity financing is not without risks.Some of the risks or challenges include:

1. The private equity investor may replicate the business ideathat he was presented with and pass it on to anotherestablished company where he holds ownership stakes.

2. Private equity investors may use the company to furtherthe cause of other companies where they have largerinvestments. For example, he may force or influence thecompany into supplying materials to another company atbelow-market prices.

3. Performance-oriented private equity investors maywithdraw their funds if the company does not perform inaccordance with the required returns.

4. Since there is no market valuation for the stake in thecompany’s shares, the company may be ‘under-valued’by private investors with strong bargaining power. This isespecially so if the management of the company hascomparatively less information.

Suggestions:In the light of the foregoing analysis in various dimensions

of the performance of venture capital and private equityfinancing in India, the researcher has offered the followingsuggestions for better performance and to become a major sourceof finance/capital for the Indian industry.

1. There is a serious mismatch between the kind of venturecapital available in India and what the market demands.

Contemporary Issues in Venture Capital Financing in India28

Most of the venture capital financiers are offering secondstage and expansion financing (which is less risky) andcompletely neglecting the start-up finance. So, it issuggested that the government should make a policy thatcertain percentage of financing (based on demand) mustbe meant for start-ups (ex: 40:60).

2. In India there are many idea rich, cash less entrepreneursand cash rich and idea less investors. In order to encouragesuch idea rich entrepreneurs, the policy making body atthe national level should set up separate cell for thecollection of ideas. Periodically, those ideas must bescreened by the experts and recommend the best andcommercially viable ones for financing. No doubt, thiswould promote the concept of financing innovation andwould provide an opportunity to the many youngtechnocrats to become entrepreneurs.

3. Most operators of VC Financing in India are an extendedarm or a division of global investment institutions. Theirrepresentation is more than 95 per cent of the VC investedin India. The investment mandates of these VCFs are oftendriven by the parent institutions’ global view, which oftenignores local market needs. To overcome this limitation,it is necessary to promote India VCFs by establishingdomestic VCF Association.

4. Indian rupee deprecation is another serious bottleneckmaking international VCFs in India unattractive. Everyinternational VC investor in India has been a victim ofthe depreciation of the rupee against the dollar. The returnsproduced by Indian VCFs, measured in US dollars or otherWestern currencies, turn out to be considerably lessattractive than that measured in Indian currency. Manynations such as the Netherlands, Portugal, Finland,Norway and Israel recognized the limitations of dependingon foreign funds at the time of evolving a policy for

29Contemporary Issues in Venture Capital Financing in India

developing a local VC industry. Their first step was to kickstart VCFs in the private sector with funds from domesticinstitutions. Over a decade, or even less, they succeededin creating a local VC industry that depended less and lesson government support and international investors. Hence,there is an urgent need that the government of India shouldencourage domestic venture capital financiers byliberalizing the policy guidelines, viz, licensing system,taxation, etc.

5. In place of multiple regulatory mechanisms, a singlewindow regulatory mechanism must be developed. SEBI’sregulations, DFI’s regulations, regulations for private equityfinanciers, regulations for domestic financiers, regulationsfor venture financiers in India backed by internationalfinanciers should be brought into single platform.

6. There should be no place for restricted entry and exit forthe venture capitalists and private equity financiers, i.e.,free and entry and exit must be allowed.

7. Like US and Swedan, the double taxation (at corpus andinvestor level) was abolished in India. The same shouldbe implemented effectively.

8. In addition to DFIs, SIDBI and other State level financialinstitutions (Ex: SFCs), the identified nationalizedcommercial banks must also be permitted to performventure capital financing.

9. In PE financing, there is a scope for under valuation(because of the absence of market valuation) by privateinvestors with strong bargaining power. This is especiallyso if the management of the company has comparativelyless information. Therefore, there is a need for thedevelopment of an accounting system for fair valuation.

10. Most of VCFs and PEFs in India are focusing on fewsectors only, viz., IT & ITES, Bio-techno ology,Pharmaceutical and Service sectors. It is suggested that

Contemporary Issues in Venture Capital Financing in India30

they should expand their wings in to modern areas likeClean Technology, Green Technology, Power Generation(Solar Power and Wind Power), Education Sector,Infrastructure, Film Production, Radio Taxi, BeautySaloon, Apparel, Eco System, Cloud Computing, etc.

11. Another issue for slow performance of VCF and PEFs inIndia is the poor quality of corporate governance and lackof sensitivity among entrepreneurs and investors, to eachother’s legitimate business aspirations. So, there is needto develop a model code of conduct for entrepreneursand investors for their win-win association.

References:1. “Annual Report of Indian Venture Capital Association (IVCA)”, 2012-

13.2. Andrew C. Quale Jr., Sidley Austin Brown & Wood. The Risks in

Private Equity Investing. Private Equity3. Andrew Ross Sorkin (2007) The Ranks of the Comfortable Are Still

Thinning. New York Times, September 9, 2007.4. Ernst & Young. (2007) Acceleration: Global Venture Capital Insights

Report 2007. Retrieved April 12, 2008, from http://www.ey.com5. Financial Review, Supplement, Yearbook 2001. Retrieved April 12,

2008, from http://www.iflr.com/6. http://venture-capital-firms.findthebest.com/d/a/India7. http://www.nvca.org/8. I M Pandey, “Venture Capital”, The Indian experience prentice Hall

of India Pvt., New Delhi.1996.9. Investment in Emerging Market Countries. Retrieved April 13, 2008,

from www.baft.org/content_folders/asfsaf/presentationQuale,%20Andrew.PPT

10. Patient Capital : How venture capital investment drives revolutionarymedical innovation. (2008) Retrieved April 15, 2008, from http://www.nvca.org/pdf/NVCAPatientCapital.pdf

11. Rejeshwari Adappa Thakur. (2008) Infrastructure Financing: BettingBig on India. Retrieved April 16, 2008, from http://www.ibef.org/download/funding.pdf

12. Sandhya Prakesh, “Venture Capital comes of Age, IndianManagement”, pp. 5-21, April 2000.

31Contemporary Issues in Venture Capital Financing in India

13. Siddharth Shah. (2001) Private equity investments in India: a Legaland Structural Overview. International

14. T. Satyanarayana Chary, “Venture Capital in India-An overview”,Management Researcher, 2000, Tiruvanathapuram.

15. T. Satyanarayana Chary, “Venture Capital Industry”, JIMS 8M, Nov-Dec 2001.

16. T. Satyanarayana Chary, “Venture Capital Industry-Issues andMeasures for Development”, Pratibimba, 2001.

17. T. Satynarayana Chary, “A Mission of Venture Capital in promotionof New Enterprises a study”, Udyog Pragathi, January-March 2005,the Journal of Practising Management, NITIE, Mumbai.

18. T. Satyanarayana Chary, “Venture Capital Concepts & amp;Applications”, Macmillan India Limited, 2005.

19. www.vccedge.com20. Zider, Bob, “How venture capital works?” Harvard Business Review

(Nov-Dec., 1998) pp. 131-139.

Contemporary Issues in Venture Capital Financing in India32

Venture Capital Financing: Key Elements

Prof. P. R. Sivasankar*

Mr. K. Rajaiah**

What is Venture Capital?The term ‘Venture Capital’ is understood in many ways. In a

narrow sense it refers to, investment in new and tried enterprisesthat are lacking a stable record of growth. In a broader sense,venture capital refers to the commitment of capital asshareholding for the formulation and setting up of small firmsspecializing in new ideas or new technologies. The emergingscenario of global competitiveness has put an immense pressureon the industrial sector to improve the quality level withminimization of cost of products by making use of latesttechnological skills. The implication is to obtain adequatefinancing along with the necessary hi-tech equipments to producean innovative product which can succeed and grow in the presentmarket condition. Venture Capital is money provided byprofessionals who invest and manage young rapidly growingcompanies that have the potential to develop into significanteconomic contributors. According to SEBI regulations, venturecapital fund means a fund established in the form of a companyor trust, which raises money through loans, donations, issue ofsecurities or units and makes or proposes, to make investmentsin accordance with these regulations. The funds so collectedare available for investment in potentially highly profitableenterprises at a high risk of loss. A Venture Capitalist is an

* Registrar (1/c), Vikrama Simhapuri University, SPSR Nellore (Dt), A.P.* * Research Scholar,Dept of Commerce,Vikrama Simhapuri University P.G.

Centre, Kavali – 524 202, (A.P.)

33Contemporary Issues in Venture Capital Financing in India

individual or a company who provides, Investment Capital,Management Expertise, Networking & marketing support whilefunding and running highly innovative & prospective areas ofproducts as well as services. Thus, the investments made byVenture Capitalists generally involves Financing new and rapidlygrowing companies , purchasing equity securities, taking higherrisk in expectation of higher reward, Having a long frame oftime period, generally of more than 5-6 years, actively workingwith management to devise strategies pertaining for overallfunctioning of project.

Defining Venture Capital internationally:As has been mentioned, countries with market-based

systems have higher levels of venture capital activity. It shouldbe noted, however, that any comparison of venture capitalactivity internationally is bound to run into problems, sincedefinitions and demarcation lines vary. See Box 2 forinternational organisations of relevance for such analysis, andBox 3 for issues that complicate interpretations. In the US,venture capital is defined as capital provided by professionalswho invest alongside management in young rapidly growingcompanies. It is considered an important source for start-upcompanies in particular. The European Venture CapitalAssociation (EVCA) accords a somewhat broader definition toventure capital. Here, venture capital is viewed as a subset ofprivate equity and refers to equity investment s made for thelaunch, early development or expansion of a business.

Thus the terminology varies somewhat internationally andemploying a universal venture capital definition is troublesomefor various reasons. In countries that have little or no early-stagefinancing, expansion or later stage finance is more often referredto as venture capital. For instance, whereas the definition in theUS, generally, is restricted to start-up companies, Europeanventure capital is less developed and includes both early-stageand expansion companies.

Contemporary Issues in Venture Capital Financing in India34

Venture Capital financing:It generally involves start up financing to help technically

sound, globally competitive and potential projects to competein the international markets with the high quality and reasonablecost aspects. The growth of South East Asian economiesespecially Hong Kong, Singapore, South Korea, Malaysia alongwith India has been due to the large pool of Venture Capitalfunds from domestic / offshore arenas.

Venture Capitalists draw their investment funds from a poolof money raised from public and private investors. These fundsare deployed generally as equity capital (ordinary and preferenceshares) and sometimes as subordinated debt which is a semisecured investment in the company (through debenture) rankingbelow the secured lenders that often requires periodicrepayment. Today, a VC deal can involve common equity,convertible preferred equity and subordinated debt in differentproportions.

The Venture Capital funding varies across the different stagesof growth of a firm. The various stages are:

1. Pre seed Stage: Here, a relatively small amount of capitalis provided to an entrepreneur to conceive and market apotential idea having good future prospects. The fundedwork also involves product development to some extent.

2. Seed Stage: Financing is provided to complete productdevelopment and commence initial marketing formalities.

3. Early Stage / First Stage: Finance is provided to companiesto initiate commercial manufacturing and sales.

4. Second Stage: In the Second Stage of Financing workingcapital is provided for the expansion of the company interms of growing accounts receivable and inventory.

5. Third Stage: Funds provided for major expansion of acompany having increasing sales volume. This stage is metwhen the firm crosses the breakeven point.

6. Bridge/Mezzanine finance or Later Stage Financing:

35Contemporary Issues in Venture Capital Financing in India

Bridge/Mezzanine Financing or Later Stage Financing isfinancing a company just before its IPO (Initial PublicOffer). Often, bridge finance is structured so that it canbe repaid, from the proceeds of a public offering.

There are basically four key elements in financing of ventureswhich are studied in depth by the venture capitalists. These are:

1. Management: The strength, expertise & unity of the keypeople on the board bring significant credibility to thecompany. The members are to be mature, experiencedpossessing working knowledge of business and capableof taking potentially high risks.

2. Potential for Capital Gain: An above average rate of returnof about 30-40% is required by venture capitalists. Therate of return also depends upon the stage of the businesscycle where funds are being deployed. Earlier the stage,higher is the risk and hence the return.

3. Realistic Financial Requirement and Projections: Theventure capitalist requires a realistic view about the presenthealth of the organization as well as future rejectionsregarding scope, nature and performance of the companyin terms of scale of operations, operating profit and furthercosts related to product development through Research& Development.

4. Owner’s Financial Stake: The financial resources owned& committed by the entrepreneur/ owner in the businessincluding the funds invested by family, friends and relativesplay a very important role in increasing the viability ofthe business. It is an important avenue where the venturecapitalist keeps an open eye.

Summary:Recognising the importance of finance in the early stages of

company development, countries over time have developed arange of measures to support the allocation of seed and venture

Contemporary Issues in Venture Capital Financing in India36

capital to new and entrepreneurial companies, especially to thosedeemed to have growth potential. Some countries, such as Japanand Germany, are traditionally characterised by a bank-basedfinancial system which relies on concentrated ownership, strongmonitoring of managers, emphasis on traditional collateral, andso forth. Others, such as the US and the UK, have developedmarket-based systems characterized by widely dispersedownership, stronger protection for minority shareholders,versatile markets for control and ownership and greatertransparency and openness to measuring intangible assets. Inboth systems, solid relationships between entrepreneurs lookingfor funds to establish new companies and outside investors arefundamental to the development of economic growth.

However, risk aversion and demands for high collateral aremaking the regular bank-based system inappropriate for financinginnovation in new, high-risk enterprises. Hence, alternativesources of finance are required. The market-based systemdeveloped partly in response to the need for supporting intangibleassets with high growth potential. In this system, most corporatefinancing is undertaken through capital markets. Venturecapitalists provide, per definition, financial and non-financialsources to high-risk start-ups and expansion companies, andthrough active involvement, they manage to overcome marketfailures such as asymmetric information. Various types of privateand institutional venture capital investors play a key role inentrepreneurial companies depending on the stage of companydevelopment. But private forces and market competition alonecannot provide socially desirable quantities of risk capital.Deficiencies remain visible in the mechanisms for channellingfunding to start-up or early stage expansion of companies. Today,bank-based systems have moved in the direction of the market-based in some respects; transparency has increased as has theprotection for minority shareholders and competition forownership and control. In both kinds of system, however,

37Contemporary Issues in Venture Capital Financing in India

governments are looking for ways to strengthen the supply offinancial and associated resources to new, potential high-growth,companies.

When moving to correct market failure in the provision ofventure capital, governments may stimulate private investorsto invest in fragile but important market segments that theywould otherwise ignore due to expectations of poor economicreturns. Public intervention may be particularly important instages when entrepreneurial companies are subjected to the firstor second equity gaps, as discussed in this chapter. Above allpolicy makers must strive for a state of play that is conduciveto healthy interactions and learning processes. The extent towhich government policies actually contribute to solving themarket problems is dubious in many cases, however. As noted,venture capital allocated to early stage investment remains muchsmaller in the EU than in the US. As will be further highlightedin the ensuing chapters, venture capital activity varies greatlybetween countries, although national markets are, in part,confronted with similar challenges.

References:• Andrew C. Quale Jr., Sidley Austin Brown & Wood. The Risks in

Private Equity Investing. Private Equity• Ernst & Young. (2007) Acceleration: Global Venture Capital Insights

Report 2007. Retrieved April 12, 2008, from http://www.ey.com• http://www.nvca.org/• I M Pandey, “Venture Capital”, The Indian experience prentice Hall

of India Pvt., New Delhi.1996.• Sandhya Prakesh, “Venture Capital comes of Age, Indian

Management”, pp. 5-21, April 2000.

Contemporary Issues in Venture Capital Financing in India38

Comparative Analysis of Sectoral Financing

by VCFs and FVCIs in India

Dr. E. Lokanadha Reddy*

Dr. C. Viswanatha Reddy**

AbstractVenture capital is a way of financing swift growing private

companies who are in their pubescent phase and are in require of

support in the form of money and corporate guidance. Venture capital

financiers are ready to take risks and invest money in companies

which are still making efforts to establish themselves in the market

but because of the novelty of their ideas and innovations in their filed

of business they are capable of earning high returns in near future.

Therefore VCFs and FVCIs are not only a source of funds for newly

established private companies but also a means of encouraging

business innovations. The government of India has made the SEBI as

nodal regulator for domestic and overseas venture capital financiers

in India for hassle free flow of venture capital. The present paper is

divided into four parts. Firstly, the Indian scenario, policy support

and the SEBI’s role for the growth and development of venture capital

financing activities has been covered. Secondly, the number of VCFs

and FVCIs registered with SEBI and the details of cumulative

investments made by them during the period of analysis has been

discussed. Thirdly, the industry-wise cumulative investments made

in India by VCFs and FVCIs together and alone were examined. In

order to capture the trend precisely the cumulative investments made

by VCFs and FVCIs in various industries have been regressed on

* Professor & Controller of ExaminationsSri Venkateswara College ofEngineering & Technology, Chittoor, (A.P.).

** Professor, Sree Vidyanikethan Institute of Management, A.Rangampet – 517102, Tirupati (A.P).

39Contemporary Issues in Venture Capital Financing in India

time. With a view to analyse whether there is a significant difference

between various industries respect to investments made by VCFs and

FVCIs over the years of the study period, ANOVA: Two-Factor

without replications has been performed. Fourthly, the problems of

venture capital financing in India were examined. Lastly, few

suggestions were offered for further strengthening of these activities

in India.

Key Words: Venture Capital, VCFs, FVCIs, SEBI, VCUs.

JEL Classification: G24

Introduction:The concept of venture capital has emerged with a view to

provide finance innovative ideas backed by entrepreneurialtalent and business skills, which have potential for high growthbut with intrinsic uncertainties. Apart from finance, venturecapitalists provide networking, management and marketingsupport as well. In the broadest sense, venture capital connotesrisk finance as well as managerial support. India has a vast poolof scientific and technical research carried out in researchlaboratories, defence laboratories as well as in universities andtechnical institutes. Conducive environment together withincubation facilities can help a great deal in identifying andactualizing some of these researches into commercialproduction. Further, with the given the inherent strengths, viz.,advancement in science and technology, research, competitiveentrepreneurship, the skilled and cost competitive manpowerwith excellent policy support, rapid and sustainable economicgrowth and competitive global strength, India has become adestination for venture capital financing activities.

The specialized venture capital financing system is requiredto endow with linkage between idea-rich entrepreneurs and cash-rich investors, ensuring funding for innovative firms havepositive externalities on the economy. So, it makes sense forgovernments to promote an active venture capital market to

Contemporary Issues in Venture Capital Financing in India40

bring the nation equal to the developed nations. TheGovernment of India has rightly attempted to fetch the nationat par and above the developed nations, has been promotedventure capital financing to new, innovative concepts and ideas,by way of liberalizing taxation norms, providing tax incentivesto venture firms, giving scope for the creation of local pools ofcapital and holding training sessions for the emerging VCinvestors.

Venture capital activities in India began in 1986 with thestart of the economic liberalisation. In 1988, the Indiangovernment formalised venture capital by issuing a set ofguidelines. Initially, venture capital was limited to subsidiariesset up IDBI, ICICI and the IFCI, and focused on large industrialconcerns. But the turning point came when the well-establishedstart-ups by Indians in the Silicon Valley convinced foreigninvestors that India had the talent and the scope for economicdevelopment and growth. Over the years, more and more privateinvestors from India and abroad have entered the Indian venturecapital market.

The Government of India constituted a SEBI committeeheaded by K. B. Chandrasekhar to make recommendations tofacilitate the growth of VC industry in India. This committeesubmitted its report in July 2000 with the prominentrecommendations, all of which were accepted and implemented:(a) SEBI should be the nodal regulator for VC funds in Indiaproviding a smooth, single window, problem-free regulatoryframework for quick and efficient flow of money into VC fundsin India; (b) Tax pass-through status should be granted to allregulatory compliant VC funds, similar to that which is providedto mutual funds, ensuring that at the “pool-level” (VC Fund)profits are tax exempt; and (c) A foreign investor who wants tomake investment in venture capital company in India has toensure that it has been registered as a Foreign Venture CapitalInvestor (FVCI) in India with SEBI under SEBI (Foreign Venture

41Contemporary Issues in Venture Capital Financing in India

Capital Investor) Regulations 2000. This registration shouldenable them to have the same facilities as the foreign institutionallevel of easy investments and disinvestments without any FIBP/RBI approvals. The investments by foreign investors in IndianVenture Capital Undertakings (VCU) and Venture Capital Funds(VCF) are governed by Foreign Exchange Management (Transferor Issue of Security by a person Resident outside India)Regulations, 2000 and SEBI (Foreign Venture Capital Investor)Regulations 2000. A registered FVCI is allowed to invest 100%of its funds in a VCF registered under SEBI (Venture CapitalFund) Regulations in the following modes:

1. It has to invest at least 66.67% of its investible funds inunlisted equity shares or equity linked instruments of VentureCapital Undertakings.

2. It can invest only 33.33% of its funds (and not more),by –a. Subscribing to initial public offer of adventure capital

undertaking whose shares are proposed to be listed;b. Investing in debt or debt instrument of the VCU

provided it has already invested by way of equity insuch a VCU;

c. Preferential allotment of equity shares of a listedcompany subject to lock in period of one year;

d. Investment by subscription or purchase in the equityshares or equity-linked securities of a financially weaklisted company or industrial listed company;

e. Investment by way of subscription or purchase inSpecial Purpose Vehicles created for the purpose offacilitating or promoting investment in accordance withthese regulations.

Review of Literature:Dr Reddy C.V. (2014)1 in his study entitled “Performance

Analysis of Venture Capital and Private Equity Financing in

Contemporary Issues in Venture Capital Financing in India42