contents - guwahati-icai.orgguwahati-icai.org/images/eicasa_enewsletter_december_2016.pdf ·...

TRANSCRIPT

Contents

My Dear Students,

I extend my heartiest best wishes for a blessed and prosperous New

Year 2017. I wish that the New Year brings the best in you. As you move

ahead in your life you need to make firm resolutions and transform

from better to best, have alternative strategies in life to accomplish

your long term goals.

Talent wins games. But teamwork wins championships. Team building, networking and

relationship building are the keys to success. Use your voice for kindness; your ears for

compassion; your hands for charity; your mind for truth; and your heart for love. Attitude

matters, self-perception counts, harmony with oneself and energizing oneself is the key to

get ahead. Henry David Thoreau said “Success usually comes to those who are too busy

looking for it.” It is said that the road to success is always under construction and it is self-

motivation that will cruise you through the journey of life.

The month of December had been fun filled for the Students. We organised a number of

Educational Tours, Visits to Historical Places, Indoor & Outdoor Sports Meet apart from

Study Circles and One Day Seminars. The Best way to end 2016 was the Pre New Year

Cultural Extravaganza in the form of Euphoria-2016, the Annual Youth Festival. I am glad to

share that we had a participation of nearly 300 Students & 50 Members in the daylong

event. Our Students from Guwahati Branch are all set to participate in the SAFA Quiz &

Elocution Competition scheduled at Dhaka, Bangladesh in the end of January, 2017. My best

wishes to all the representatives of ICAI at SAFA. We are all set to celebrate the Saraswati

Puja at our Branch Premises on 1st February, 2017 with Mehndi Competition for the first

time.

As the nation prepares for the 68th Republic day, I extend my best wishes to all my dear

Students on the occasion. The results of CA Examination November, 2016 & CPT

Examinations December, 2016 will also be declared in the current month. My best wishes to

all the examinees. I sincerely hope that our students shall come out with flying colours. May

the forthcoming New Year be wonderful in every way and may there be happiness and love

each step, each day.

Before I wrap my communique, I quote the great comedian Charlie Chaplin, “You are happy;

but Life salutes you when you make others happy. Trust before you love; know before you

judge; commit before you promise; forgive before you forget; appreciate before you

regret.”

Wishing you most & more

CA. Kamal Mour

Editor:

CA. Ankit Agarwal

Advisors:

CA. Raginee Goyal

CA. Pankaj Jain

Members:

CA. Kamal Mour

CA. Gaurab Garodia

Ms. Aayushi Agarwal

Ms. Anamika Agarwala

Mr. Deb Krishnan Mour

Mr. Sagar Nath

Ex-Officio Members:

CA. (Dr.) Debashis Mitra

CA. Rakesh Agarwala

CA. Rohit Agarwala

Editorial Board

1 | Chairman’s Message

2 | Editor’s Desk

3 | Vice Chairperson’s

Message

4 - 7 | Students’ Articles

8 | Announcements

9 - 10 | Puzzle

11 | QUIZ Corner

12 - 15 | EICASA Guwahati

Activities

16 | EICASA Guwahati

Managing Committee

Editorial Board

Dear Student,

“Let me give you a New Year message: Believe in yourself, because no one ever achieved anything

significant without believing in himself and no one ever will! Believe in yourself powerfully, especially

when there is no reason left to believe in yourself because the ultimate bottom is the best place to start a

big rise!” – Mehmet Murat Ildan. Dear students, what the New Year brings to you will depend a great

deal on what you bring to the New Year. As the year comes to a close, it is a time for reflection – a time to

release old thoughts and beliefs and forgive old hurts. Whatever has happened in the past year, the New Year shall bring in

fresh beginnings and exciting new experiences. Let us be thankful for the blessings of the past and the promise of the

future. I wish all of you the biggest slice of happiness and good luck for the new year and may the year ahead be one where

all your dreams come true.

The month of December’2016, in fact, the Calendar Year 2016, has been an eventful year with varied activities for

enrichment of students. I would like to congratulate the EICASA Team for putting in all their effort with utmost honestly,

dedication and sincerity. The Calendar Year has witnessed several activities and events being organized for the CA students

amongst which National Convention for CA Students, Annual Youth Festival, Indoor & Outdoor Sports Competition &

Regional Level Quiz & Elocution Competition deserves special mention. It gives me immense pleasure to see all our dear

students participating in the activities organized by EICASA and contributing for the better cause of all the students. Those

who could not or did not participate, please note that these activities are aimed towards all around development of

students and you are missing out on those fronts. We should always motivate ourselves towards engaging us in all

possible opportunities that life brings to fore because it is motivation that gets you started and gradually when it becomes

a habit, it helps you keep going in life.

Dear students, always try and give your best so that you never repent for your past. In this respect, I would like to present

the following lines :

If you always try your best

Then you’ll never have to wonder

About what you could have done

If you’d summoned all your thunder.

And if your best

Was not as good

As you hope it would be,

You still could say,

“I gave today

All that I had in me.”

Wishing all of you a great year ahead.

CA. Ankit Agarwal.

“I never dreamed about success. I worked for it. ” - Charles Swindoll

Editor’s Desk...

2

Hello Friends,

“Fun is not a substitute of education but a necessity for good education.”

I welcome you all to the December edition of E-newsletter released by the EICASA Guwahati Branch. It gives me great

pleasure to take you all through the last month of the year 2016.

The month of December has been very exciting for all of us with many activities during the whole month. We had several

educational tours which included Britannia, War Memorial, Planetarium where the opportunity to learn was ample. Study

circles on Office Etiquettes, Features of Ms Access was also organized. A 3 day workshop on English speaking was also

organised to polish the communication skills of the student. Half yearly indoor and outdoor sports meet was also organised

in Royal Global School where the students took part enthusiastically and it was amazing to organize such a sport event. This

month we also had in line the biggest festival of the year EUPHORIA 2016, the Annual Youth Festival. It turned out to be a

grand success and the students enjoyed being a part of it.

December ended in a good notion for all of us with the success of all events lined up in this month. I hope students enjoyed

all the activities of this month and look forward for their active participation in future also.

I wish all of you Best of Luck for the upcoming exam results and a very Happy New Year.

Regards,

Aayushi Agarwal

3

Vice Chairperson’s Message...

“I AM two of the most powerful words. For what you put after them shapes your reality.”

-Anonymous

EICASA

Connect

Interested students may send

“Hello EICASA” with name on

Whatsapp to : 9435559587

Write to Editor:

‘Information is Power’ and our ever evolving

profession needs more and more of that today

than ever before. Do you have any relevant

points to make, experiences to share and views

to spread among the CA students fraternity,

please email us at —

4 “In response to those who say to stop dreaming and face reality...

I say keep dreaming and make reality.” -Kristian Kan

An Introduction of Indian Accounting Standards (Ind AS)

As per the notification released by the Ministry of Corporate Affairs (MCA) on 16 February 2015, Indian Accounting Standards (Ind AS) has come into force from 1st day of April, 2015. Presently, the Institute of Chartered Accountants of India (ICAI) has issued 39 Indian Accounting Standards (Ind AS) which have been notified under the Companies (Indian Accounting Standards) Rules, 2015 (“Ind AS Rules”), of the Companies Act, 2013.

Roadmap to comply with Indian Accounting Standards (Ind AS)

The Companies and their auditors shall comply with the Indian Accounting Standards (Ind AS) specified in Annexure to Companies (Indian Accounting Standards) Rules,2015 in preparation of their financial statements and audit respectively. The roadmap for Ind AS implementation is as follows :

Voluntary Adoption :

Companies can voluntarily adopt Ind AS for accounting periods beginning on or after 1 April 2015 with comparatives for period ending 31 March 2015 or thereafter. Once the company opts to follow the Ind AS, it will be required to follow the same for all the subsequent financial statements .

Mandatory Applicability :

Phase 1 - Ind AS will be mandatorily applicable to the following companies for periods beginning on or after 1 April 2016, with comparatives for the period ending 31 March 2016 or thereafter:

Companies whose equity and/or debt securities are listed or are in the process of listing on any stock exchange in India or outside India and having net worth of 500 Crore INR or more.

Companies having net worth of 500 Crore INR or more, other than those covered above.

Phase 2 - Ind AS will be mandatorily applicable to the following companies for periods beginning on or after 1 April 2017, with comparatives for the period ending 31 March 2017 or thereafter:

Companies whose equity and/or debt securities are listed or are in the process of listing on any stock exchange in India or outside India and having net worth of less than 500 Crore INR (It means Ind AS is applicable to all listed companies from 1 April, 2017 ).

Unlisted companies other than those covered in Phase 1 and Phase 2 whose net worth are more than 250 Crore INR but less than 500 Crore INR.

Phase 3 - Ind AS will be mandatorily applicable to the following company for periods beginning on or after 1 April 2018, with comparatives for the period ending 31 March 2018 or thereafter:

NBFCs having net worth of rupees 500 Crore INR or more.

Phase 4 - Ind AS will be mandatorily applicable to the following company for periods beginning on or after 1 April 2019, with comparatives for the period ending 31 March 2019 or thereafter:

NBFCs other than those covered under phase III whose net worth are more than 250 Crore INR but less than 500 Crore INR.

Important Notes on Adoption & Applicability :

Whenever a company falls under the criteria as mentioned above, Ind AS becomes mandatory for such companies including its holding, subsidiary, associate and joint venture companies (irrespective of their net worth).

Once a company starts following the Ind AS either voluntarily or mandatorily on the basis of criteria, it shall be required to follow the Ind AS for all the subsequent financial statements even if any of the criteria specified in this rule does not subsequently apply to it.

5 “You must have long-range goals to keep you from being frustrated by short-range

failures.” -Charles C. Noble

Ind AS, once opted or becomes applicable, shall apply to both standalone financial statements and consolidated financial statements.

Net worth means the aggregate value of the paid-up share capital and all reserves created out of the profits and securities premium account, after deducting the aggregate value of the accumulated losses, deferred expenditure and miscellaneous expenditure not written off, as per the audited balance sheet, but does not include reserves created out of revaluation of assets, write-back of depreciation and amalgamation. It has been clarified that net worth will be determined based on the standalone accounts of the company as on 31 March 2014 or the first audited period ending after that date.

In case of conflict between Ind AS and the law, the provisions of law will prevail and financial statements are to be prepared in compliance with the law.

Indian Accounting Standards (Ind AS) versus International Financial Reporting Standards (IFRS) :

India has chosen a path of International Financial Reporting Standards (IFRS) convergence rather than adoption. Hence, Ind AS are primarily based on the IFRS issued by the International Accounting Standards Board (IASB). However, there are certain carve-outs from the IFRS. Few of the general differences between Ind AS and IFRS are:

The transitional provisions given in each of the standards under IFRS have not been given in Ind AS, since all transitional provisions related to Ind AS, wherever considered appropriate, have been included in Ind AS 101, First-Time Adoption of Indian Accounting Standards, corresponding to IFRS 1, First-Time Adoption of International Financial Reporting Standards.

Different terminology is used in Ind AS when compared to IFRS, e.g. the term ‘balance sheet’ is used instead of ‘statement of financial position’ and ‘statement of profit and loss’ is used instead of ‘statement of comprehensive income’.

Indian Accounting Standards (Ind AS) versus existing Accounting Standards(AS) :

Ind AS is different from existing AS in many aspects. In simple terms, Ind AS are more flexible than existing AS. Morever, existing AS are rule based whereas Ind AS are principle based. Ind AS requires more detailed disclosure than existing AS. Ind AS bring crucial changes in all existing AS. Detailed differences on some of the Ind AS and existing AS are as follows:

(1) Ind AS 1 - Presentation of Financial Statements and existing AS 1 (issued 1979) - Disclosure of Accounting Policies

Ind AS 1 generally deals with presentation of financial statements, whereas existing AS 1 (issued 1979) deals only with the disclosure of accounting policies. The scope of Ind AS 1 is thus much wider and line by line comparison with the existing AS is not possible. However, the major differences as laid down in Ind AS 1 are as follows:

i. An enterprise shall make an explicit statement in the financial statements of compliance with all the Indian Accounting Standards. Further, Ind AS 1 allows deviation from a requirement of an accounting standard in case the management concludes that compliance with Ind ASs will be misleading and if the regulatory framework requires or does not prohibit such a departure.

ii. Ind AS 1 requires presentation and provides criteria for classification of Current / Non- Current assets / liabilities.

iii. Ind AS 1 prohibits presentation of any item as extraordinary Item in the statement of profit and loss or in the notes.

iv. Ind AS 1 requires presentation of balance sheet as at the beginning of the earliest period when an entity applies an accounting policy retrospectively or makes a retrospective restatement of items in the financial statements, or when it reclassifies items in its financial statements.

v. In respect of reclassification of items, Ind AS 1 requires disclosure of nature, amount and reason for reclassification in the notes to financial statements.

An Introduction of Indian Accounting Standards (Ind AS)

6 “The real failure is the one from which we learn nothing. ” -John Powell

vi. Ind AS 1 requires the financial statements to include a Statement of Changes in Equity to be shown as a part of the balance sheet which, inter alia, includes reconciliation between opening and closing balance for each component of equity

(2) Ind AS 2 - Inventories and existing AS 2 - Valuation of Inventories:

Major differences are as follows :

i. Ind AS 2 provides explanation with regard to inventories of service providers whereas the existing AS 2 does not contain such an explanation.

ii. Ind AS 2 deals with the subsequent recognition of cost/carrying amount of inventories as an expense, whereas the existing AS 2 does not provide the same.

iii. Ind AS 2 provides detailed guidance in case of subsequent assessment of net realisable value. It also deals with the reversal of the write-down of inventories to net realisable value to the extent of the amount of original write-down, and the recognition and disclosure thereof in the fianancial statements. The existing AS 2 does not deal with such reversal. Moreover Ind AS 2 defines fair value and provides an explanation in respect of distinction between ‘net realisable value’ and ‘fair value’. The existing AS 2 does not contain the definition of fair value and such explanation.

(3) Ind AS 7- Statement of Cash Flows and the existing AS 3 - Cash Flow Statements :

Major differences are as follows :

i. Ind AS 7 specifically includes bank overdrafts which are repayable on demand as a part of cash and cash equivalents, whereas the existing AS 3 is silent.

ii. Ind AS 7 provides the treatment of cash payments to manufacture or acquire assets held for rental to others and subsequently held for sale in the ordinary course of business as cash flows from operating activities. Further, treatment of cash receipts from rent and subsequent sale of such assets as cash flow from operating activity is also provided. The existing AS 3 does not contain such requirements.

iii. The existing AS 3 requires cash flows associated with extraordinary activities to be separately classified as arising from operating, investing and financing activities, whereas Ind AS 7 does not contain this requirement.

iv. As compared to the existing AS 3, Ind AS 7 requires to disclose the amount of cash and cash equivalents and other assets and liabilities in the subsidiaries or other businesses over which control is obtained or lost. Ind AS 7 also requires to report the aggregate amount of the cash paid or received as consideration for obtaining or losing control of subsidiaries or other businesses in the statement ofcash flows, net of cash and cash equivalents acquired or disposed of as a part of such transactions, events or changes in circumstances. The existing AS 3 does not contain such requirements.

(4) Ind AS 8 - Accounting Policies, Changes in Accounting Estimates and Errors and existing AS 5 (Revised 1997) Net Profit or Loss for the Period - Prior Period Items and Changes in Accounting Policies:

i. Objective of existing AS 5 is to prescribe the classification and disclosure of certain items in the statement of profit and loss for uniform preparation and presentation of financial statements. Objective of Ind AS 8 is to prescribe the criteria for selecting andchanging accounting policies, together with the accounting treatment and disclosure of changes in accounting policies, changes in accounting estimates and corrections of errors. Ind AS 8 intends to enhance the relevance and reliability of an entity’s financial statements and the comparability of those financial statements over time and with the financial statements of other entities.

ii. Keeping in view that Ind AS 1, Presentation of Financial Statements, prohibits the presentation of any items of income or expense as extraordinary items and deals with profit or loss for the period, and in accordance with the objective of Ind AS 8, this standard does not deal with the same, which at present is dealt with by existing AS 5.

An Introduction of Indian Accounting Standards (Ind AS)

7 “Success is like your own shadow, if you try to catch it you will never succeed, ignore it

and walk in your own way, and it will follow you...” -Anonymous

iii. Ind AS 8 requires that changes in accounting policies should be accounted for with retrospective effect subject to limited exceptions viz., where it is impracticable to determine the period specific effects or the cumulative effect of applying a new accounting policy. On the other hand, existing AS 5 does not specify how change in accounting policy should be accounted for.

iv. Existing AS 5 defines prior period items as incomes or expenses which arise in the current period as a result of errors or omissions in the preparation of financial statements of one or more prior periods. Ind AS 8 uses the term errors and relates it to errors or omissions arising from a failure to use or misuse of reliable information (in addition to mathematical mistakes, mistakes in application of accounting policies etc.) that was available when the financial statements of the prior periods were approved for issuance and could reasonably be expected to have been obtained and taken into account in the preparation and presentation of those financial statements. Ind AS 8 specifically states that errors include frauds, which is not covered in existing AS 5.

Ind AS 10 - Events after the Reporting Period and existing AS 4 - Contingencies and Events occurring after the Balance Sheet Date

In Ind AS 10, material non-adjusting events are required to be disclosed in the financial statements, whereas the existing AS 4 requires the same to be disclosed in the report of approving authority.

As per Ind AS 10 dividend proposed or declared after the reporting period, can not be recognised as a liability in the financial statements because it dose not meet the criteria of a present obligation as per Ind AS 37. Such dividend is required to be disclosed in the notes in the financial statements as per Ind AS 1, whereas as per the existing AS 4 the same is required to be adjusted in financial statements because of the requirements prescribed in the Schedule VI to the Companies Act, 1956.

If after the reporting date, it is determined that the fundamental accounting assumption of going concern is no longer appropriate, Ind AS 10 requires a fundamental change in the basis of accounting. Whereas existing AS 4 requires assets and liabilities to be adjusted for events occurring after the balance sheet date that indicate that the fundamental accounting assumption of going concern is not appropriate. In this regard, Ind AS 10 refers to Ind AS 1, which requires an entity to disclose the fact that the financial statements are not prepared on a going concern basis together with the basis on which the financial statements are prepared and state the reason why entity is not regarded as a going concern.

Here, I have made an attempt to discuss on few of the Ind AS and its differences with existing AS. Likewise, other Ind AS also contain some crucial changes which have not been mentioned in my article. I hope my efforts on the subject help the readers to understand the applicability, need, and importance of Ind AS. I have tried best to make it error free however few mistakes might have crept in for which i am apologetic. Thanking You !

By Rajesh Jain

Reg No. ERO 0210582

An Introduction of Indian Accounting Standards (Ind AS)

Announcement

8 “People are training for success when they should be training for failure. Failure is far

more common than success; poverty is more prevalent than wealth; and disappoint-

ment more normal than arrival.“ -J. Wallace Hamilton

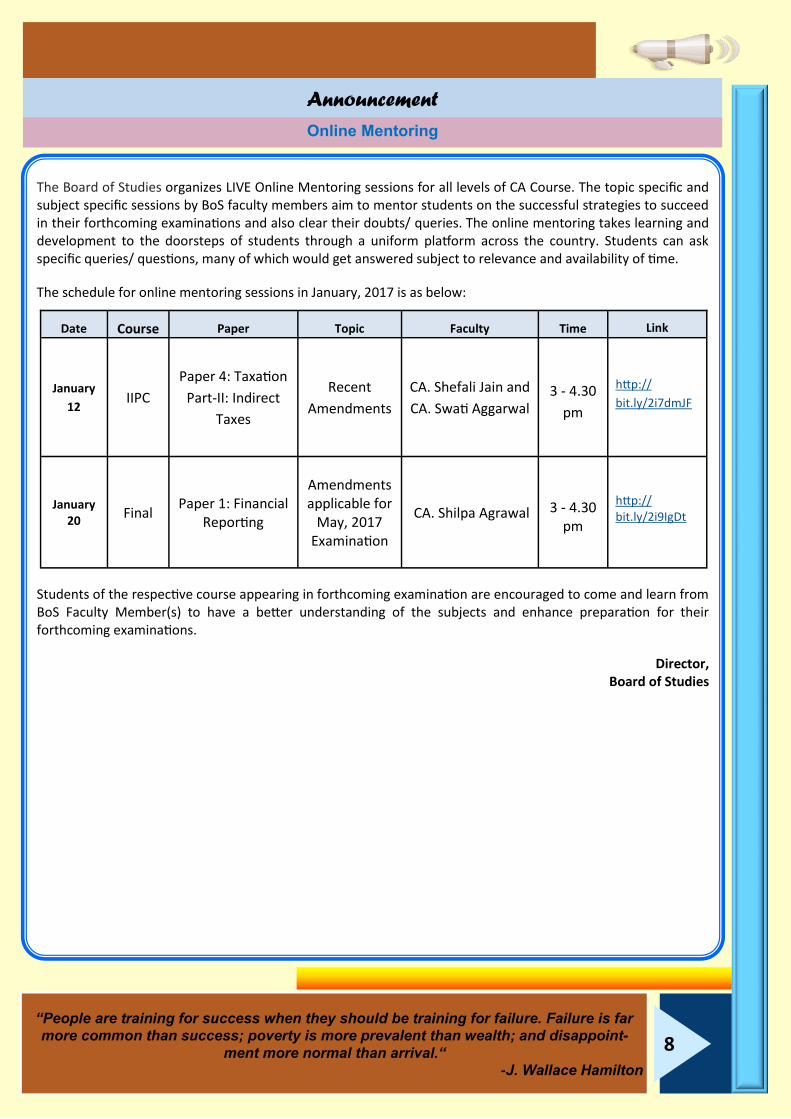

Online Mentoring

The Board of Studies organizes LIVE Online Mentoring sessions for all levels of CA Course. The topic specific and subject specific sessions by BoS faculty members aim to mentor students on the successful strategies to succeed in their forthcoming examinations and also clear their doubts/ queries. The online mentoring takes learning and development to the doorsteps of students through a uniform platform across the country. Students can ask specific queries/ questions, many of which would get answered subject to relevance and availability of time.

The schedule for online mentoring sessions in January, 2017 is as below:

Students of the respective course appearing in forthcoming examination are encouraged to come and learn from BoS Faculty Member(s) to have a better understanding of the subjects and enhance preparation for their forthcoming examinations.

Director, Board of Studies

Date Course Paper Topic Faculty Time Link

January

12 IIPC

Paper 4: Taxation

Part-II: Indirect

Taxes

Recent

Amendments

CA. Shefali Jain and

CA. Swati Aggarwal 3 - 4.30

pm

http://

bit.ly/2i7dmJF

January 20

Final Paper 1: Financial

Reporting

Amendments applicable for

May, 2017 Examination

CA. Shilpa Agrawal 3 - 4.30 pm

http://bit.ly/2i9IgDt

9

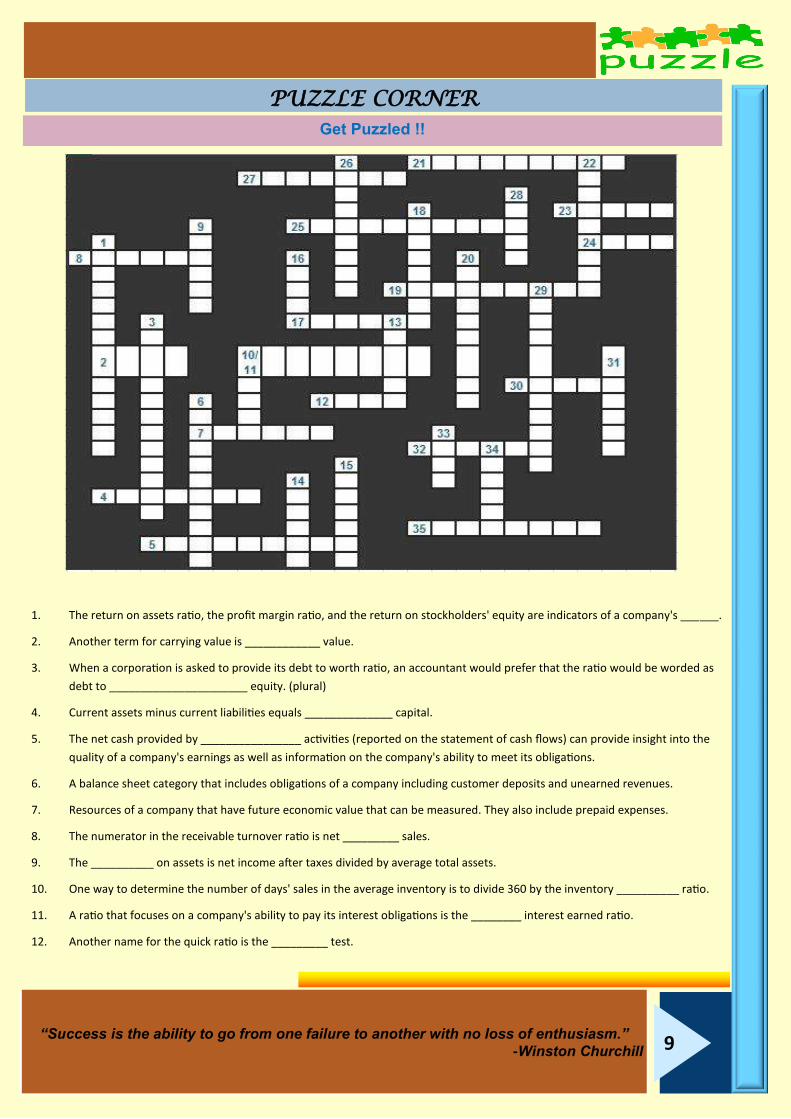

PUZZLE CORNER

“Success is the ability to go from one failure to another with no loss of enthusiasm.” -Winston Churchill

Get Puzzled !!

1. The return on assets ratio, the profit margin ratio, and the return on stockholders' equity are indicators of a company's ______.

2. Another term for carrying value is ____________ value.

3. When a corporation is asked to provide its debt to worth ratio, an accountant would prefer that the ratio would be worded as

debt to ______________________ equity. (plural)

4. Current assets minus current liabilities equals ______________ capital.

5. The net cash provided by ________________ activities (reported on the statement of cash flows) can provide insight into the

quality of a company's earnings as well as information on the company's ability to meet its obligations.

6. A balance sheet category that includes obligations of a company including customer deposits and unearned revenues.

7. Resources of a company that have future economic value that can be measured. They also include prepaid expenses.

8. The numerator in the receivable turnover ratio is net _________ sales.

9. The __________ on assets is net income after taxes divided by average total assets.

10. One way to determine the number of days' sales in the average inventory is to divide 360 by the inventory __________ ratio.

11. A ratio that focuses on a company's ability to pay its interest obligations is the ________ interest earned ratio.

12. Another name for the quick ratio is the _________ test.

10

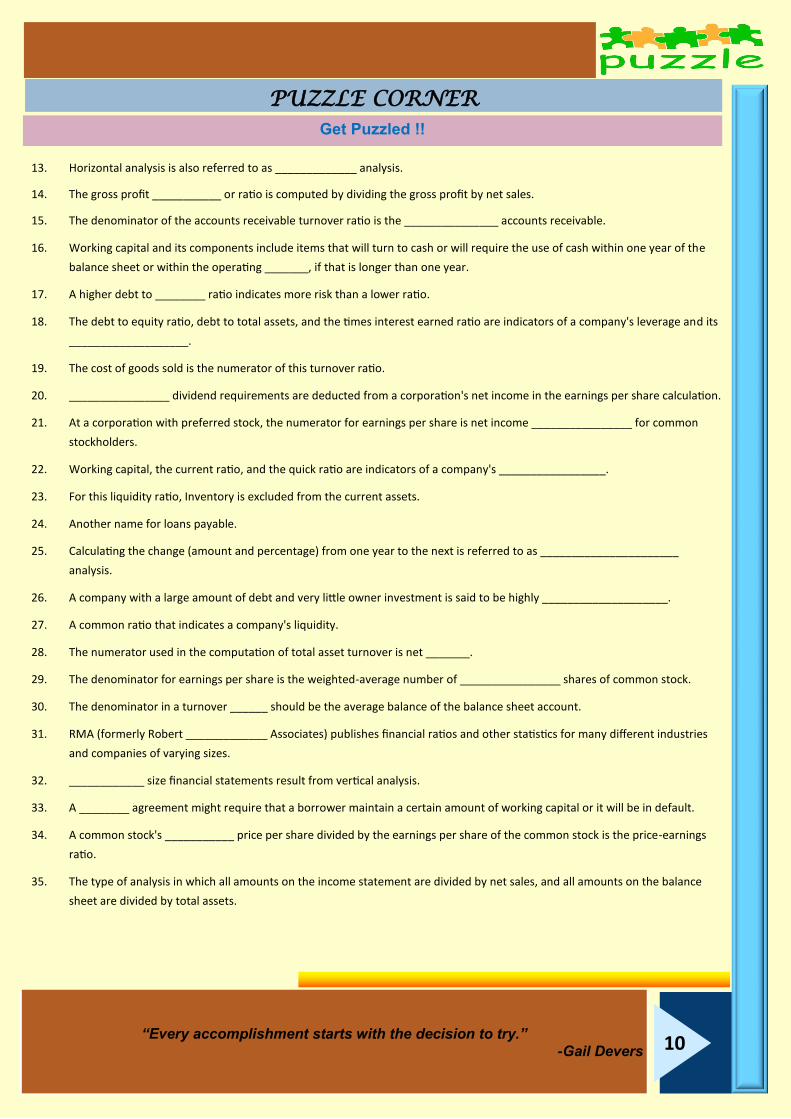

PUZZLE CORNER

“Every accomplishment starts with the decision to try.” -Gail Devers

Get Puzzled !! 13. Horizontal analysis is also referred to as _____________ analysis.

14. The gross profit ___________ or ratio is computed by dividing the gross profit by net sales.

15. The denominator of the accounts receivable turnover ratio is the _______________ accounts receivable.

16. Working capital and its components include items that will turn to cash or will require the use of cash within one year of the

balance sheet or within the operating _______, if that is longer than one year.

17. A higher debt to ________ ratio indicates more risk than a lower ratio.

18. The debt to equity ratio, debt to total assets, and the times interest earned ratio are indicators of a company's leverage and its

___________________.

19. The cost of goods sold is the numerator of this turnover ratio.

20. ________________ dividend requirements are deducted from a corporation's net income in the earnings per share calculation.

21. At a corporation with preferred stock, the numerator for earnings per share is net income ________________ for common

stockholders.

22. Working capital, the current ratio, and the quick ratio are indicators of a company's _________________.

23. For this liquidity ratio, Inventory is excluded from the current assets.

24. Another name for loans payable.

25. Calculating the change (amount and percentage) from one year to the next is referred to as ______________________

analysis.

26. A company with a large amount of debt and very little owner investment is said to be highly ____________________.

27. A common ratio that indicates a company's liquidity.

28. The numerator used in the computation of total asset turnover is net _______.

29. The denominator for earnings per share is the weighted-average number of ________________ shares of common stock.

30. The denominator in a turnover ______ should be the average balance of the balance sheet account.

31. RMA (formerly Robert _____________ Associates) publishes financial ratios and other statistics for many different industries

and companies of varying sizes.

32. ____________ size financial statements result from vertical analysis.

33. A ________ agreement might require that a borrower maintain a certain amount of working capital or it will be in default.

34. A common stock's ___________ price per share divided by the earnings per share of the common stock is the price-earnings

ratio.

35. The type of analysis in which all amounts on the income statement are divided by net sales, and all amounts on the balance

sheet are divided by total assets.

11

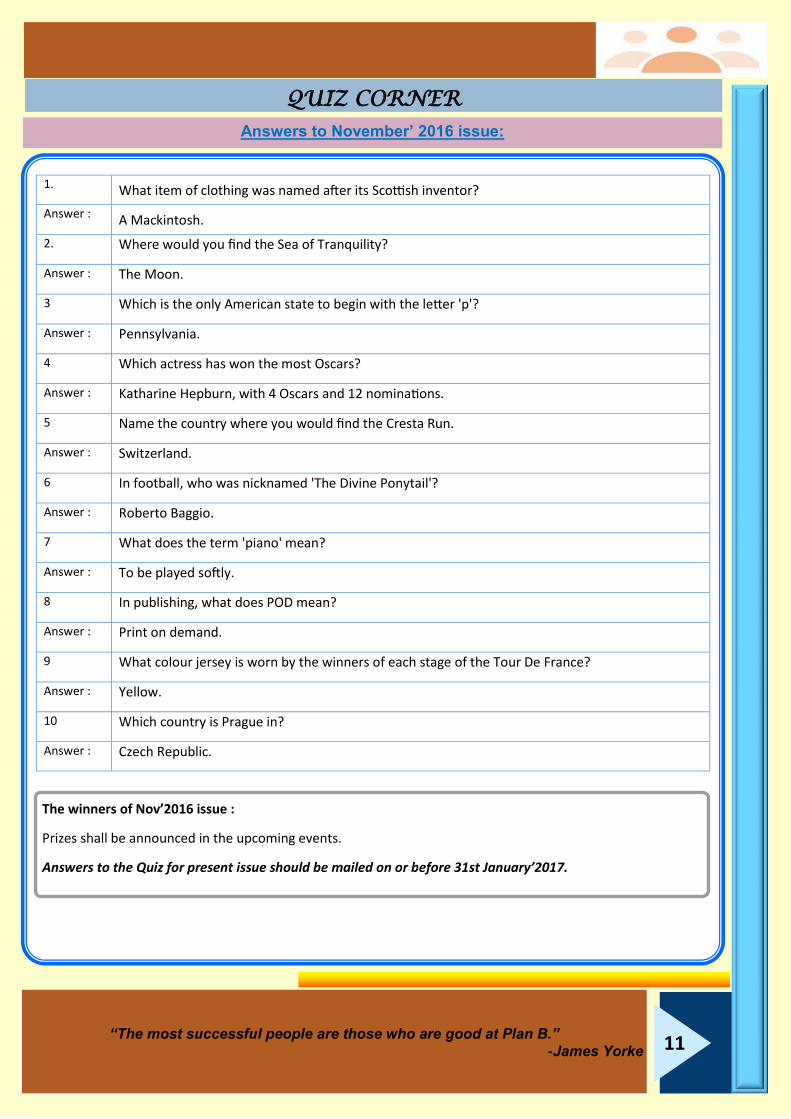

QUIZ CORNER

“The most successful people are those who are good at Plan B.” -James Yorke

Answers to November’ 2016 issue:

The winners of Nov’2016 issue :

Prizes shall be announced in the upcoming events.

Answers to the Quiz for present issue should be mailed on or before 31st January’2017.

1. What item of clothing was named after its Scottish inventor?

Answer : A Mackintosh.

2. Where would you find the Sea of Tranquility?

Answer : The Moon.

3 Which is the only American state to begin with the letter 'p'?

Answer : Pennsylvania.

4 Which actress has won the most Oscars?

Answer : Katharine Hepburn, with 4 Oscars and 12 nominations.

5 Name the country where you would find the Cresta Run.

Answer : Switzerland.

6 In football, who was nicknamed 'The Divine Ponytail'?

Answer : Roberto Baggio.

7 What does the term 'piano' mean?

Answer : To be played softly.

8 In publishing, what does POD mean?

Answer : Print on demand.

9 What colour jersey is worn by the winners of each stage of the Tour De France?

Answer : Yellow.

10 Which country is Prague in?

Answer : Czech Republic.

12

Career Counselling at Kendriya Vidyalaya, Dimapur

A Career Counselling

Programme was

organised at Kendriya

Vidyalaya Dimapur on

06.12.2016. CA. Lalit

Kumar Khandelwal

was the resource

person for the

programme.

The Programme was attended by 65 Students.

Educational Tour at Sunrise Biscuit Company Limited

An Educational Tour

was organised at

Sunrise Buiscuit

Company Limited,

Britannia on

07.12.2016 by EICASA.

Around 28 Students

participated in the

tour. The program was

coordinated by CA. Adarsh Agarwal.

Batch No-2 of Orientation Programme

The Second batch of Orientation Program (15 Days) was

organised at ICAI Bhawan from 08.12.2016 to 25.12.2016.

Around 48 Students participated in the Batch.

Career Counselling at Dronacharya Academy, Barpeta

Road

A Career Counselling

Programme was

organised at

Dronacharya

Academy, Barpeta

Road on 09.12.2016.

CA. Lalit Kumar

Khandelwal was the

resource person for the programme.

The Programme was attended by 60 Students.

Career Counselling at Kendriya Vidyalaya, Khatkhati, Assam

A Career Counselling

Programme was

organised at Kendriya

Vidyalaya, Khatkhati on

14.12.2016. CA. Bijay

Kumar Agarwal was the

resource person for the

programme.

The Programme was attended by 31 Students.

Half Yearly Indoor & Outdoor Sports Meet

The Second Half Yearly

Indoor & Outdoor

Sports Meet for CA

Students was organised

at Royal Global School

on 17th & 18th

December, 2016. The

Meet was inaugurated

by Mrs. Anubha Goyal,

Principal Royal Global School, in presence of Mr. Mrinmoy

Kanti Das, Vice Principal Royal Global School. Around 150

Students participated in the event. Various types of sports

viz. Cricket (Boys & Girls), Race, Relay Race, Tug of War,

Pool, Chess, Carrom, Badminton, Table Tennis etc. were

organised for the overall benefit of students.

The Meet ended with

Prize Distribution

Ceremony on 18th

December, 2016. CA. K.

P. Sarda, Past Chairman

of Guwahati Branch of

ICAI and Ms. Kusum

Sarda, were the Chief

Guest. Mr. Biswajit

Bharadwaj, Secretary of Assam Chess Association, was

present as Guest of Honor. CA. (Dr.) Debashis Mitra,

member Board of Studies was also present during the event.

EICASA Guwahati Activities

“No man will make a great leader who wants to do it all himself or get all the credit for

doing it.” -Andrew Carnegie

13

The Winners of major games were as under:

Table Tennis (M) : Akash Agarwal

Table Tennis (F) : Rekha Singh

Carrom (Doubles- Boys) : Amit Srivastav &

Abhishek Das

Carrom (Doubles- Girls) : Amrita Sinha &

Saloni Mandal

Chess : Rajesh Jain

Pool : Ravi Sharma

Badminton (Girls) : Aayushi Agarwal

Badminton (Boys) : Ashish Bansal

The Programme ended with a formal vote of thanks from

Mr. Deb Krishnan Mour, EICASA Treasurer.

Study Circle Meet- Features of MS Access

A Study Circle meet on

features of MS Access

was organised at ICAI

Bhawan on 19.12.2016.

Around 40 students

participated in the

Meet. Mr. Sagar Nath

was the speaker of the

meet.

The program ended with a formal vote of thanks from Ms.

Anamika Agarwal, Secretary of EICASA, Guwahati Branch.

One Day Seminar on “Overview of ICDS”

A One Day Seminar on “Overview of ICDS” was organised

on 20.12.2016. CA.

Ankit Agarwal

spoke on the

different features

of ICDS vis a vis

Accounting

Standards. He also

explained the

practical aspects in

implementation of

ICDS.

Mr. Gaurav Agarwal, motivational speaker enlightened the

Students on Art of Living- The Science of Breath.

The Seminar was attended by more than 70 Students. The

program ended with a formal vote of thanks from Ms.

Anamika Agarwal, Secretary of EICASA.

Study Circle Meet on Business & Office Etiquettes

A Study Circle Meet

was organised on

the Topic “Business

& Office

Ettiquettes” on

22.12.2016. CA.

Kamal Mour was

the speaker on the

subject.

The meet was attended by around 48 Students. The meet

ended with a formal vote of thanks from Ms. Aayushi

Agarwal.

Educational Tour to War Memorial

An Educational Tour

was organised on

21.12.2016. The

Students team led

by CA. Kamal Mour

visited the War

Memorial at

Dighalipukuri,

Guwahati.

The Visit was attended by 46 Students.

Educational Tour to Assam State Museum

An Educational Tour

was organised at

Historic Assam State

Museum for CA

Students on

22.12.2016. CA.

Kamal Mour

coordinated the

Tour.

The Tour was attended by 45 Students.

EICASA Guwahati Activities

“In the middle of difficulty lies opportunity.” -Anonymous

14

Workshop on English Speaking, Writing Skills & Business

Correspondence

A Three Day Workshop

on “English Speaking,

Business

Correspondence &

Writing Skills” was

organised between

21.12.2016 to

23.12.2016. More than

48 Students participated in the Workshop. The First Day of

the Workshop was addressed by CA. Pankaj Jain on the

topic of Business correspondence and Group Discussion &

tips on improving Word Power. The Second day of the

event was addressed by CA. Anjana Mour on writing Skills

and English Grammar. The Third day of the workshop was

addressed by CA. Vasundhara Jalan who discussed on

Public Speaking & Vocabulary.

Career Counselling at Lachit Barphookan Commerce

Academy

A Career Counselling

Programme was

organised at Lachit

Barphookan Commerce

Academy, Doboka Road,

Nagaon on 26.12.2016.

The Counselling was

conducted by CA. Bijay

Agarwal. Around 63 Students participated in the Career

Counselling.

Batch of ITT Classes

A Batch of ITT Classes was conducted at ICAI Bhawan from

01.12.2016 to 31.12.2016. Around 40 Students participated

in the Batch.

Youth Festival for CA. Students

The Annual Youth Festival-2016 titled

Euphoria-2016 was organised on

30.12.2016 at Royal Global School.

The event was attended by around

300 Students and 50 Members.

Shri Partha Sarathi Mahanta, IPS, Superintendent of Police ,

Kamrup was the Chief Guest in Inaugural Session. Prof. (Dr.)

S.P. Singh, Vice Chancellor of The Assam Royal Global

University was the guest of Honor. The Inaugural Session

was also attended by members of the Royal Global School.

A number of activities like Paint your face competition, One

Minute Dance Competition, Musical Housie, Rangoli

Competition, Stage Show on Bhagat Singh, Inter CA Firm

Quiz etc, were organised during the day.

EICASA Guwahati Activities

“Obsessed is a word the lazy use to describe the dedicated.” -Anonymous

15

CA. Vidya Garg, CA. Deepika Agarwal, Ms. Suman Patwa,

Ms. Poonam Agarwal, Ms. Ritu Agarwal, Ms. Aruna Bansal

were judges for the different activities.

CA. Vivek Jalan performed the Stage show on Bhagat Singh.

CA. Ravi Patwa and CA. Vasundhara Jalan conducted the

Quiz.

The program ended with a valedictory session. Central

Council Member and Member Board of Studies, CA. (Dr.)

Debashis Mitra was present as the Chief Guest. CA. (Dr.)

Debashis Mitra congratulated the Students and also

emphasized on the importance of such events amongst the

hectic study calendar. He also appraised the students of the

recent initiatives being taken by Board of Studies.

EICASA Guwahati Activities

“Success doesn't come to you, You go to it.” -Marva Collins

Managing Committee of Guwahati Branch of EICASA

CA. KAMAL MOUR

CHAIRMAN

CA. GAURAB GARODIA

MEMBER

16

DISCLAIMER

The news and views expressed here are the personal views of the authors / editorial board and do not necessarily reflect the views of

The Institute of Chartered Accountants of India. This newsletter has been sent to you as a member / well-wisher of ICAI.

“Excellence is a continuous process & not an accident.” -Dr. A.P.J. Abdul Kalam

MS. AAYUSHI AGARWAL

VICE-CHAIRPERSON

MS. ANAMIKA AGARWALA

SECRETARY

MR. DEB KRISHNAN MOUR

TREASURER

MS. SWATI SHARMA

PROGRAM COORDINATOR

MR. AKSHAT AGARWAL

SPORTS COORDINATOR

MR. HIMPAL SEN

CULTURAL COORDINATOR