contents uap and old mutual, forming one of the largest financial services groups with a growing...

TRANSCRIPT

CONTENTSABOUT US03 UAP Old Mutual Tower Highlights04 UAP Old Mutual at a Glance05 Old Mutual Plc at a Glance

DIRECTORS06 UAP Holdings Board of Directors’ Profiles10 UAP Old Mutual Subsidiaries Directors

KEY STATEMENTS16 Chairman’s Statement22 Group CEO’s Statement

CORPORATE REVIEW26 Corporate Governance Report44 Sustainability and CSR Report 201652 Five-Year Financial Highlights54 Directors’ Report56 Directors’ Remuneration Report57 Statement of Directors’ Responsibilities

FINANCIAL STATEMENTS58 Report of the Independent Auditors’ to the Members of

UAP Holdings Limited63 Consolidated Statement of Profit or Loss64 Consolidated Statement of Other Comprehensive Income65 Consolidated Statement of Financial Position66 Company Statement of Financial Position67 Consolidated Statement of Changes in Equity69 Company Statement of Changes in Equity70 Consolidated Statement of Cash Flows71 Notes to the Financial Statements

AGM139 Notice of Annual General Meeting (AGM)142 Form of Proxy

OUR CONTACTS143 Contacts

THE UAP OLD MUTUAL TOWER

Located along Upper Hill Road in Upper Hill, Nairobi, the UAP Old Mutual Tower adds some 324,881 sq ft of grade A letting space in Upper Hill Commercial District.

It stands 163m tall at an altitude of 5,700ft above sea level.

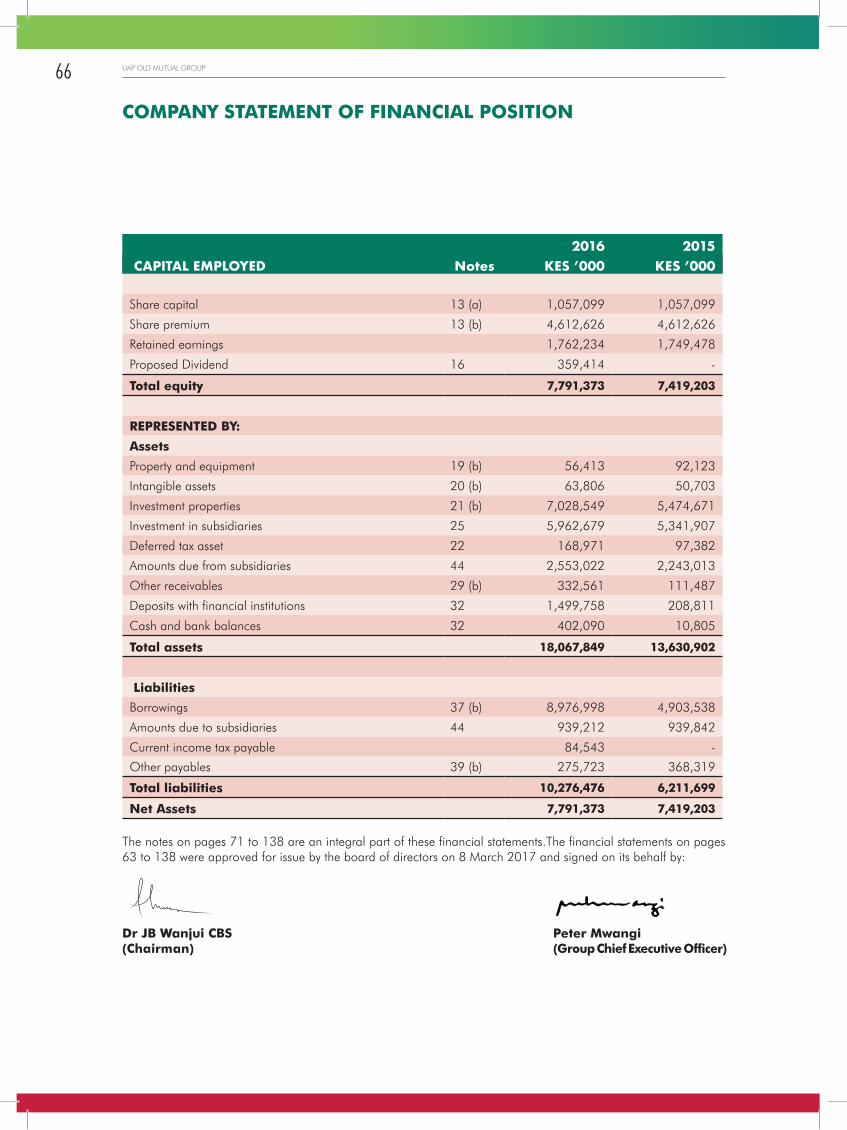

The UAP Old Mutual Kenya Group is comprised of Faulu, UAP and Old Mutual, forming one of the largest financial services groups with a growing footprint in East and Central Africa. The Group was formed in 2015 as a result of the acquisition of a controlling stake by Old Mutual in Faulu Microfinance Bank in 2014 and UAP Holdings in 2015.

The Group pursues an integrated financial services model to avail to customers a comprehensive range of financial solutions which include Investment, Insurance, Banking and Savings through a wider and more accessible distribution network.

UAP OLD MUTUAL GROUP EAST AFRICA

Our customers can now be assured of holistic solutions and unrivalled convenience to enable them realise their dreams.PETER MWANGI | GROUP CEO, UAP OLD MUTUAL GROUP

The UAP Old Mutual Group is part of the Old Mutual Emerging Markets (OMEM). As part of OMEM, UAP Old Mutual is able to leverage technology, technical expertise and the ability to offer broad career growth prospects for employees.

THE UAP OLD MUTUAL GROUP WILLOPERATE UNDER THE BANNER OF:

THE BUSINESS WILL DRIVE TWO KEY BRANDS IN THE MARKET.

NON-BANKING BUSINESS

BANKING BUSINESS

QUICK FACTS ABOUT THE GROUP

1.2M

4K

CUSTOMERSEGMENTS

160+

COUNTRIES

CUSTOMERS

SERVICE & DISTRIBUTIONOUTLETS

PROPERTIES IN 4 COUNTRIES

EMPLOYEES& AGENTS

KENYA, UGANDA, SOUTH SUDAN,RWANDA, DR CONGO & TANZANIA.

RETAIL BUSINESSCORPORATE

12

6

OLD MUTUAL PLC AT A GLANCE

OLD MUTUAL IS AN INTERNATIONAL INVESTMENT, SAVINGS, INSURANCE & BANKING GROUP

Old Mutual began in Cape Town in 1845 as South Africa’s first mutual life insurance company, offering financial security in uncertain times. Today, 172 years on, Old Mutual plc is made up of four strong businesses comprising Old Mutual Emerging Markets, Nedbank, Old Mutual Wealth and Old Mutual Asset Management serving a combined 18.9 million customers.

HEADQUARTERED IN LONDON, WE DO BUSINESS IN AFRICA, EUROPE, THE AMERICAS AND ASIA. FROM OUR ORIGINS IN SOUTH AFRICA, WE HAVE EXPANDED THROUGH ORGANIC GROWTH AND STRATEGIC ACQUISITIONS.

Our customers are at the heart of everything we do. We know that we can only be successful with their continued support and trust – we aim to be their most trusted financial partner, helping them achieve their lifetime financial goals, while investing their funds in ways that will secure a positive future for themselves and their families.

19.4M 68,527

£394.9 BN30CUSTOMERS EMPLOYEES

COUNTRIES FUNDS UNDER MANAGEMENT

THE BUSINESS MODEL:

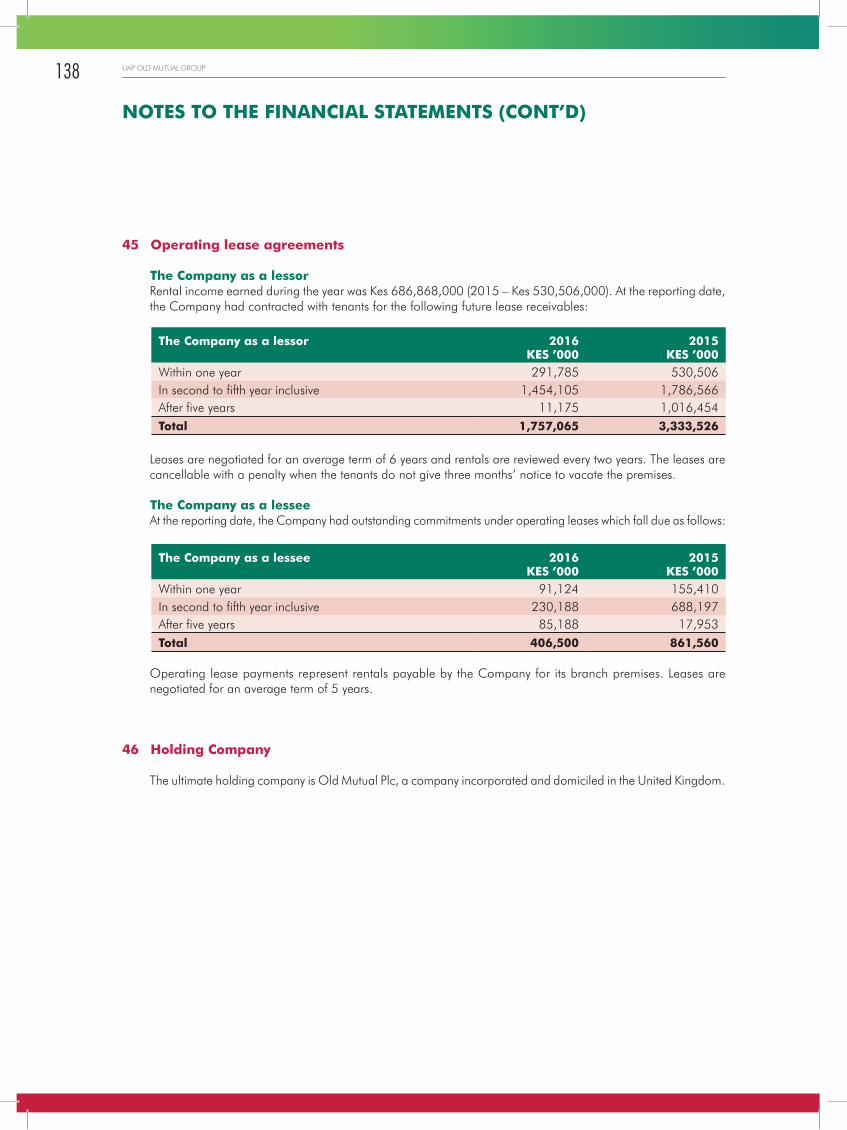

NEDBANK

7.7M CUSTOMERS IN 9 AFRICAN COUNTRIES

OLD MUTUALEMERGING MARKETS

15 COUNTRIES ACROSS AFRICA

OLD MUTUALWEALTH

3,000 UK FINANCIALADVISORS

OLD MUTUAL ASSET MANAGEMENT

£195.2BN FUNDS UNDERMANAGEMENT

5ANNUAL REPORT & FINANCIAL STATEMENTS 2016

DR JB WANJUI | CHAIRMAN

Dr. JB Wanjui cbs, the Chairman of the Board has had a long and illustrious career in the Kenyan corporate scene, the most prominent being the Chief Executive of East Africa Industries (which later became Unilever). He is a graduate of Ohio Wesleyan University, (BA Physics and Mathematics) and Columbia University, (MSC Engineering). Dr. Wanjui was the Chancellor of the University of Nairobi and was previously the Chairman of CfC Stanbic Bank Limited. He is also Chairman and Board member of a number of other Kenyan and international organizations. Dr. Wanjui has been a director of the Company since 1986 and the Chairman of the Board since 1998. In recognition of his exemplary contributions to positive change in society, he received the Chief of the Order of the Burning Spear (CBS) of the Republic of Kenya award.

PETER DE BEYER | DEPUTY CHAIRMAN

Peter De Beyer was appointed as Deputy Chairman of the Board in June 2005. He joined wider Old Mutual Group in 1978 and has served the business in various capacities including Development Actuary and Executive General Manager. In September 2000, Peter became Deputy Managing Director, South Africa, responsible for all Retail Business. Mr De Beyer retired from Old Mutual Group in November 2008 and continues to serve on its several boards. Peter holds a Bachelors in Business Science and he is a Fellow Institute of Actuaries South Africa. He also has an Advanced Management Program qualification from INSEAD. Peter has significant wealth in corporate leadership and in addition to serving on the OMLAC Board, he currently serves several Boards namely: Autumn Skies Trading 306 CC, South Africa; Oceana Group Limited, South Africa; Old Mutual (Malawi) Limited; Old Mutual (Blantyre) Nominees Limited; OMLAC; Old Mutual Investment Group (SA) Holdings (Proprietary) Limited; Old Mutual Life Assurance Company (Malawi) Limited; Old Mutual Life Assurance Company (Namibia) Limited; Old Mutual (Malawi) Unit Trust Limited; Real People Investment Holdings (Pty) Limited; Old Mutual Life Assurance Company (South Africa) Limited; Old Mutual Life Holdings (South Africa) Limited; Old Mutual Unit Trust Managers Limited; Marriott Unit Trust Management Company Limited; and Old Mutual Nigeria Life Insurance Company Limited

JONAS MUSHOSHO | DIRECTOR

Jonas Mushosho was appointed Chief Executive Officer for Old Mutual Rest of Africa in February 2017, a position covering 13 countries in Africa except South Africa. He is the current Group Chief Executive Officer of Old Mutual Zimbabwe. He brings with him a wealth of strategic experience and maturity to contribute to the development of the group. Prior to this, he headed the Old Mutual Zimbabwe Life Company as Managing Director, a position he held since June 2009. Jonas is a Chartered Accountant CA (Z), CA (SA) and holds a B. Accounting, B. Compt (Hons) and an MBA. He is a fellow of the Institute of Chartered Secretaries and Administrators (FCIS). A former Zimbabwe Deputy Commissioner of Taxes, Jonas joined Old Mutual in 1990 as a Tax Planning Accountant having worked for the Zimbabwe Tax Department for 10 years. Part of his track record in the Group includes, heading the Retail Business as General Manager (2001 - 2004) prior to his promotion to Finance Director (2004 - 2009). He was appointed to the Board of UAP Holdings on 24th August, 2016.

UAP HOLDINGS BOARD OF DIRECTORS’ PROFILES

6 UAP OLD MUTUAL GROUP

DR. PETER MUTHOKA | INDEPENDENT DIRECTOR

Dr. Peter Muthoka Ebs, Mbs, FKIb, FKIM, is an Independent Director of the Board, and he is the current Chairman of the Faulu Micro Finance Bank, which is a member of the UAP Old Mutual Group. He is also the Chairman of the UAP Old Mutual Foundation. He previously served as the Group Chairman of Kenya Commercial Bank. He is the Chairman of the Board of Fellows of the Kenya Institute of Management (KIM) and Chairman of the Board of Trustees of the Management University of Africa (MUA). He has been a corporate leader and an entrepreneur with long and varied experience in public and private sectors in the fields of management, education, finance, investment, export promotion, agriculture, real estate, corporate governance, international diplomacy and community voluntary work. In recognition of his exemplary service rendered to the Kenyan Public Service and international organizations, he was awarded the medal of Moran of the Burning Spear (MBS) in 2004 and the medal of Elder of the Burning Spear (EBS) in 2012 by H.E The President of the Republic of Kenya.

PAUL TRUYENS | INDEPENDENT DIRECTOR

Paul is a non-executive Director of the Board. He commenced his working career in 1978 as CFO and Chief Actuary, World-Wide Re (UK), a position he left in 1979. In 1980 he joined Southern Life (South Africa) as GM Product Development. In 1995 he was promoted to Executive Director, CFO & Appointed Actuary of Southern Life and subsequently rose in 1998 to become a member of the executive management team and appointed actuary of the Southern Life fund, Momentum Life which positions he served until 2001. In 2002 he took up an appointment as senior manager PwC Netherlands and served as such up to 2007. In 2008 he took up a role with Metlife in Ireland as Senior Finance Actuary. Paul currently serves on the Board of Old Mutual South Africa, where he is chairman of the Risk Committee and of the Committee for Customer Affairs; a member of the audit committee, and on the board of OMH. He holds BSc Mathematical Statistics, University of Cape Town and BA Economics, University of Cape Town. He is a fellow of the Institute of Actuaries (UK) and Fellow of the Actuarial Society of South Africa. He is also a non-executive director of Infrastructure Finance Corporation (INCA), where he has been on the board since its inception in 1996. His experience spans 38 years.He currently sits on the boards of Old Mutual Emerging Markets, Old Mutual Life Assurance Company of South Africa, Mutual and Federal Insurance Company (South Africa), Mutual and Federal Risk Finance Company and Infrastructure Finance Corporation (INCA). He has in the past served as Independent non-Executive Director of African Life (now Sanlam), Southampton Life (Zimbabwe) and Outsurance (Non-Life Insurance) SA.

JAMES MUGUIYI | DIRECTOR

James Muguiyi is a Non-Executive Director at UAPHL, having previously served as Group Managing Director. During his tenure as the Group MD he oversaw the growth of the Group’s business in Kenya and expansion into Uganda, South Sudan, Rwanda and Tanzania. He presided over the group restructuring in 2008 and the demerger of the Life Insurance Business from General Insurance Business in Kenya. Between 1988 and 2001, he was the Deputy Managing Director. During this time, he oversaw the merger of Provincial Insurance with Union Insurance to form UAP Provisional Insurance in 1994. Mr. Muguiyi is a director of several other companies and is the former Chairman of Centum Investment Company Limited, a company listed on the Nairobi Securities Exchange. He is a Fellow of the Institute of Certified Public Accountants of Kenya (FCPA (K)) where he was at one time the Chairman. He is also a Certified Company Secretary (CPS (K)) and a Chartered Management Accountant (ACMA).

UAP HOLDINGS BOARD OF DIRECTORS’ PROFILES

7ANNUAL REPORT & FINANCIAL STATEMENTS 2016

ROSE OGEGA | INDEPENDENT DIRECTOR

Rose is a qualified accountant who also serves on the Board of OMH. She is currently the Managing Director of Bloom Consultancy. Prior to assuming this role, she had served as Finance Director at Skynet Worldwide Express Ltd. She has a strong background in accounting and financial management spanning over 25 years. She started her career at PWC Kenya where she worked in Corporate Finance, Business Management and Management consulting. Rose holds a Bachelor of Commerce (Accounting Option) from University of Nairobi. She is a holder of a CPA (K) and a Fellow Member of the Institute. She is also a fellow of the African Leadership initiative; Member of the Aspen Global Leadership Network and a Coach-Academy of Executive Coach. Rose has held several non-executive directorships in the various arms of the Old Mutual Kenya businesses and also served as a non-executive Director for Barclays Bank of Kenya.

SUSAN OMANGA | INDEPENDENT DIRECTOR

Susan Omanga is the CEO and founder of Exclamation Marketing Ltd. She previously served in senior marketing positions at Colgate Palmolive, Boots Kenya, Barclays Bank, and Standard Chartered. From 2004 -2012 she served as a non-executive Director in the Group Board of KCB where she was also Chairman of KCB Foundation, Director S & L Mortgages and Director KCB Uganda. Susan sits on the Board of Longhorn Publishers and Kenya Tea Packers Limited (KETEPA). She is also an advisory board Member at the University of Nairobi’s Green Horn Mentorship programme, a member of the Marketing Society of Kenya, the Public Relations Society of Kenya (PRSK) and the International Advertising Association (IAA). Susan holds an Associate of Applied Science Degree in Business Management from North West Community College, Powel, Wyoming and a Bachelor of Science Degree in Business Management with a Minor in Advertising from Rocky Mountain College in Billings Montana.

JAMES WAMBUGU | EXECUTIVE DIRECTOR

James Wambugu is the Group Managing Director, General Insurance for UAP Old Mutual and an Executive Director of UAP Holdings. Mr. Wambugu joined UAP in July 2003 and has been involved in the development of the Group’s risk and quality management systems, business expansion and strategy development. He previously worked for PricewaterhouseCoopers in Kenya and the UK, Lonrho Africa and African Lakes Corporation in the fields of audit, transaction structuring and support and risk management. Mr. Wambugu has extensive experience across many countries in Africa. He holds an MBA and Bachelor of Commerce degrees from the University of Nairobi and a diploma in Advanced Management Programme (AMP) from IESE Business School, Barcelona and Strathmore Business School, Nairobi. He is a Qualified Risk Manager (MIRM) and a Certified Public Accountant of Kenya (CPA (K)).

DAVID MARSHALL | DIRECTOR

David Marshall is a qualified accountant with a wealth of corporate finance skills and experience in the Americas, Europe and Asia, and he is highly regarded in merchant and investment banking circles. He is a South African by birth and a graduate of Hilton College and the University of Cape Town. Before to joining Old Mutual, Mr Marshall was the Managing Director for Credit Suisse’s Southern Africa ultra-high net worth business in London, and has worked for many global companies, including UBS, Deloitte, Standard Corporate and Merchant Bank. At UBS Wealth Management he advised the board on its global strategic acquisitions. Earlier in his career he was involved in the LSE listing of Anglo American and the unbundling of De Beers from Anglo.

UAP HOLDINGS BOARD OF DIRECTORS’ PROFILES

8 UAP OLD MUTUAL GROUP

ANISHA ARCHARY | DIRECTOR

Anisha Archary is the Human Resources Director of Old Mutual Emerging Markets. The Emerging Markets portfolio spans South Africa, the rest of Africa, Colombia, Mexico, India & China and has a combined workforce of 31 000 employees. Previously Anisha held the position of Executive Vice President Global Passenger Services, Product & Marketing of SAA where she spent 12 years. She holds a Masters Degree in Psychology and has completed Leadership Programmes in Switzerland, South Africa and Harvard Business School. She has spent the last 28 years in the Corporate World learning & contributing across the Transport, Retail and Financial Services sectors. She has lived and worked in South Africa and India and her work has allowed for extensive travel across the African continent where her passion for building teams across boundaries and integrating new acquisitions into the Old Mutual business can be seen.

A.K. MAINA | INDEPENDENT DIRECTOR

A.K. Maina is the Managing Director of Kenya Railways. He previously served as General Counsel and Group Secretary & Head of Legal Services for UAP Holdings; a role that saw him provide legal advisory and company secretarial services to the twelve(12) operational businesses in East Africa. He attained a Bachelor of Laws at University of Nairobi and subsequently admitted as an advocate of the High Court. He is a Certified Public Secretary and holds various professional memberships. These include: Law society of Kenya, East Africa Law Society and is a Fellow at Institute of Certified Public Secretaries of Kenya (ICPSK).

PETER MWANGI | GROUP CEO

Peter Mwangi is a director in the company and also the Group Chief Executive Officer of the UAP Old Mutual Group in East Africa. He was appointed to this position on 1st July 2015. Before this appointment he was the Group Chief Executive Officer of the Old Mutual Group in Kenya from October 2014. Prior to joining the Old Mutual Group he had served as the CEO for the Nairobi Securities Exchange from 2008 to 2014. He had joined the NSE after serving as the Managing Director for Centum Investment Company Limited (2004 – 2008). Between 2000 and 2004 he was an Investment Manager at Centum. Between 1999 and 2000, he had worked for Economic Intelligence as an Investment Analyst. He started his working career with the Kenya Air Force where he worked for 5 years and left having attained the rank of Captain in 1999. Peter holds a Bachelor of Science Degree in Electrical Engineering from the University of Nairobi. He is a member of the CFA Institute, CFA Society of East Africa, Institute of Certified Investment and Securities Analysts, Institute of Certified Public Accountants of Kenya, Institute of Certified Public Secretaries of Kenya, Institute of Directors of Kenya and the Kenya Institute of Management. Besides serving on various Boards of UAPHL entities as well as Old Mutual entities, he also serves as a non-executive director on the boards of the Central Depository and Settlement Corporation, British American Tobacco Kenya and Funguo Investments Ltd.

MIKE HARPER | INDEPENDENT DIRECTOR

Mike Harper was appointed Chairman of Mutual & Federal in May 2012. Having worked in the Old Mutual Group since 1979, Mike has served in several executive positions including Strategy Director for Old Mutual Emerging Markets, leading strategic work across Asia, Latin America, South Africa and Africa markets. He also served as Distribution Executive on the OM Group Long Term Savings executive in London. Mike served on the Boards of Old Mutual Unit Trust, Old Mutual Investment Group and the Council of the Botanical Society of South Africa.

UAP HOLDINGS BOARD OF DIRECTORS’ PROFILES

9ANNUAL REPORT & FINANCIAL STATEMENTS 2016

UAP INSURANCE KENYA

UAP LIFE ASSURANCE KENYA

UAP PROPERTIES KENYA LIMITED BOARD

JAMES MUGUIYIKENYAN \ CHAIRMAN

JAMES MUGUIYIKENYAN \ CHAIRMAN

KAMAU KURIAKENYAN \ CHAIRMAN

GEORGE ODOKENYAN

PETER MWANGIKENYAN

PETER MWANGIKENYAN

JAMES WAMBUGUKENYAN

JACKSON THEURIKENYAN

PAUL TRUYENSDUTCH

PETER LEVETTSOUTH AFRICAN

PROF. PATRICK WEKEKENYAN

BETTY ANN MBOCHEKENYAN

WAINAINA KENYANJUIKENYAN

HANNAH G. MWANGIKENYAN

LOTFI BACCOUCHEAUSTRALIAN

PATRICIA KIWANUKAKENYAN

JOSEPH LESIEWKENYAN

PROF. J. H. KIMURAKENYAN

GARY PALSERSOUTH AFRICAN

UAP OLD MUTUAL SUBSIDIARIES DIRECTORS

10 UAP OLD MUTUAL GROUP | ANNUAL REPORT & FINANCIAL STATEMENTS 2016

UAP INSURANCE UGANDA

UAP FINANCIAL SERVICES LIMITED (UGANDA) BOARD

UAP LIFE ASSURANCE UGANDA

JAMES MUGUIYIKENYAN

JAMES MUGUIYIKENYAN

KAMAU KURIAKENYAN

PROF. G. WAVAMUNNOUGANDAN \ CHAIRMAN

DR. WILLIAM KALEMAUGANDAN \ CHAIRMAN

JAMES WAMBUGUKENYAN

MARY B. KYEYUNEUGANDAN

SOPHIE NKUUTUUGANDAN

SUZANNE BATWALAUGANDAN

PETER MWANGIKENYAN

JOHANNES !GAWAXABNAMIBIAN

DR GEORGE MUTEMAUGANDAN

ANTHONY GITHUKAKENYAN

DAVID KURIAKENYAN

DAVID KURIAKENYAN

ANDREW KASIRYEUGANDAN

PROF. SAM SEJJAAKAUGANDAN

PROF. SAM SEJJAAKAUGANDAN \ CHAIRMAN

PATRICIA KIWANUKAKENYAN

UAP OLD MUTUAL SUBSIDIARIES DIRECTORS (Cont’d)

11

UAP PROPERTIES LIMITED (UGANDA) BOARD

UAP INSURANCE SOUTH SUDAN LIMITED BOARD

UAP PROPERTIES LIMITED (SOUTH SUDAN) BOARD

JAMES MUGUIYIKENYAN \ CHAIRMAN

PETER MWANGIKENYAN

PETER MWANGIKENYAN

JOHN LAKOSOUTH SUDANESE

NICHOLAS CORBISHLEYSOUTH AFRICAN

KRIS MBAYAKENYAN

PROF. SCOPAS DIMASOUTH SUDANESE

PROF. SCOPAS DIMASOUTH SUDANESE \ CHAIRMAN

WAINAINA KENYANJUIKENYAN

WAINAINA KENYANJUIKENYAN

PHILIP COULSONKENYAN

JAMES MUGUIYIKENYAN

JAMES MUGUIYIKENYAN

PROF. G WAVAMUNNOUGANDAN \ CHAIRMAN

DR. WILLIAM KALEMAUGANDAN

ANDREW KASIRYEUGANDAN

DAVID KURIAKENYAN

BALLA NYERERESOUTH SUDANESE

UAP OLD MUTUAL SUBSIDIARIES DIRECTORS (Cont’d)

12 UAP OLD MUTUAL GROUP

UAP INSURANCE TANZANIA LIMITED BOARD

UAP INSURANCE RWANDA LIMITED BOARD

JAMES MUGUIYIKENYAN / CHAIRMAN

MOSES S KALUWATANZANIAN

YVONNE MAKOLORWANDESE

RICHARD MUGISHARWANDESE \ CHAIRMAN

KEVIN TERRYZIMBABWEAN

WILLIAM ASIKOKENYAN

PERIS KAHUKOKENYAN

NICK ITUNGAKENYAN

PERECE KIRIGITITANZANIAN

JOHN BOSCO BIRUNGIRWANDESE

CHARLES WASHOMATANZANIAN

JOSEPH WEREMATANZANIAN

TICHAONA MAKONESEZIMBABWEAN

SIMON TUMAWAKUDRC

GEORGE ODOKENYAN

JAMES WAMBUGUKENYAN

JACKSON THEURIKENYAN / CHAIRMAN

UAP DRC SARL BOARD

GRANT POTESOUTH AFRICAN

UAP OLD MUTUAL SUBSIDIARIES DIRECTORS (Cont’d)

13ANNUAL REPORT & FINANCIAL STATEMENTS 2016

EXECUTIVE MANAGEMENT

UAP MAURITIUS ENTITIES

SUBSIDIARIES LEADERSHIP TEAM

PETER MWANGIGROUP CEO

ASSAD ABDULLATIFFMAURITIAN / CHAIRMAN

JAMES WAMBUGUMANAGING DIRECTOR,UAP INSURANCE KENYA

TICHAONA MAKONESEMANAGING DIRECTOR,UAP INSURANCE DRC

ISAAC NZYOKAGROUP MD - HEALTH INSURANCE

NICK ITUNGAMANAGING DIRECTOR,UAP INSURANCE TANZANIA

CHARITY WAINAINAHEAD OF MARKETING

JAMES WAMBUGUGROUP MD - GENERAL INSURANCE

FELISTUS KARANJAPRINCIPAL OFFICER,UAP INVESTMENTS KENYA

GRANT POTEGROUP CHIEF OPERATIONS OFFICER

MWANZO MOSETIPRINCIPAL OFFICER,UAP LIFE ASSURANCE KENYA

JERIM OTIENOGROUP MD - LIFE ASSURANCE

SIMON MWEBAZEMANAGING DIRECTOR,UAP FINANCIAL SERVICES UGANDA

JOE MUTUGUGROUP CHIEF FINANCIAL OFFICER

JEAN-CLAUDE PERMAL MAURITIAN

KRIS MBAYAMANAGING DIRECTOR,UAP INSURANCE SOUTH SUDAN

NKIROTE MWORIA NJIRUGROUP COMPANY SECRETARY &LEGAL COUNSEL

JAMES MUGUIYIKENYAN

DAVID KURIAMANAGING DIRECTOR,UAP INSURANCE UGANDA

APOLLO NJOROGEMD - FAULU

KEVIN TERRYZIMBABWEAN

ANTHONY GITHUKAMANAGING DIRECTOR,UAP LIFE ASSURANCE UGANDA

UAP OLD MUTUAL SUBSIDIARIES DIRECTORS (Cont’d)

14 UAP OLD MUTUAL GROUP

You make me feel so alive I can conquer all.

KEEP GOOD COMPANY

Dear Shareholder,

I am pleased to present our financial statements and reports for the year. The group has managed to grow profitability before tax despite operating in a challenging environment.

DR. JOSEPH B. WANJUI CBS

Political EnvironmentIn 2017, Kenya will have its second general election under the Constitution of Kenya promulgated in 2010. The 2013 election process was peaceful marked by steady macroeconomic conditions and decent capital markets performance. In fact, the Kenyan economy registered a GDP growth of 5.9% in 2013 in comparison to a GDP growth of 4.5% in 2012. This illustrates the strengthened capacity of the electoral agencies and dispute resolution mechanisms. Our institutions continue to grow in strength and capacity and we are heartened to note gradual improvements in governance. We are confident that the 2017 election process will be concluded with minimal disruption to business. Additionally, the devolution of governance to the 47 counties in Kenya has created tremendous opportunities for the Group to service Kenyans and we are working to make it as easy as possible for our customers to access our products countrywide.

South SudanViolence broke out in South Sudan in July 2016 plunging the nation into a crisis and disrupting normal business activities. Fortunately, we were able to maintain operations and to support our South Sudanese employees in the immediate aftermath of the fighting and throughout the remainder of 2016. A tentative calm has been restored, but the economic environment has experienced a large decline. In spite of these difficulties, we continue to invest in South Sudan. As a testament to our commitment and support, we have also relocated the head office for the UAP Insurance South Sudan business to UAP Equatoria Tower. UAP Equatoria Tower is our flagship property in Juba, South Sudan and we plan to have an official opening as soon as normality resumes. We remain committed to our customers, employees and stakeholders in South Sudan.

Macroeconomic Environment

1. East AfricaThe East African states experienced mixed fortunes with the latest 2016 GDP statistics indicating a broad slowdown. In Kenya, 2016 GDP growth was 5.8%compared to a revised growth of 5.7% for the same period in 2015 with a rise in economic activity noted in the accommodation and food services, information and communication, real estate and transport and storage sectors. In Tanzania, expansion in the transportation, mining, agriculture and construction sectors contributed to economic growth but Q3 2016 growth was lower at 6.2%compared to 7.3% for the same period in 2015. Similarly, Uganda’s growth in Q2 2016/17 was 0.8% compared to 1.5% in 2015; growth was adversely impacted by poor weather conditions and a struggling banking sector on the back of the Bank of Uganda’s takeover of Crane Bank. Rwanda’s economy grew by 5.9% in 2016, less than the 6.9% growth recorded in 2015 driven by growth in the agriculture, industry and services sectors. The worst economic performance was in South Sudan which contracted with large investors pulling out and non-oil revenues decreasing. Inflation was largely contained in the region with the exception of South Sudan and the DRC.

2. KenyaThe Kenyan economy grew by 5.8% in 2016. Key factors that contributed to the strong growth include adequate rainfall for the better part of the year, consistent agricultural production, low international oil prices and infrastructural development. The CBK and the Treasury were also able to maintain a supportive

Kenya’s GDP is estimated to have grown 5.8% according to the Economic survey 2017 published by the Kenya National Bureau of Statistics (KNBS)

CHAIRMAN’S STATEMENT

17UAP OLD MUTUAL GROUP | ANNUAL REPORT & FINANCIAL STATEMENTS 2016

monetary and fiscal regime that was of particular importance in managing inflation and foreign currency volatility. Leading indicators for the economy signalled underlying resilience throughout the year. The Government of Kenya (GOK) continued its execution of strategic infrastructure projects which will create a more conducive business environment.

However, 2016 also had its fair share of challenges some of which included:

a) The depreciation of the Kenya Shilling towards the end of the year;b) A slow-down in private sector credit growth driven by the passing of the Banking Amendment Act 2016 and a

sharp rise in Non-Performing Loan (“NPL”) ratios for the banking sector; c) The beginning of the drought towards the end of 2016; d) And, a second year of negative performance for the equity markets. The NSE 20 and NASI indices shed 21.1%

and 8.5% respectively in 2016.

Moreover, the Banking Amendment Act 2016 further dampened investor enthusiasm for equities because the Banking sector comprises a significant proportion of the market capitalization of the stock exchange.

The inflation rate in 2016 was within the CBK’s band of 2.5% - 7.5% driven by stable food prices and low oil prices. The annual inflation rate trended downwards from 7.78% in January 2016 to 6.35% in December 2016. With a steady inflation rate, the yield curve normalised in 2016 and fixed income securities provided relief for investors. The government’s appetite for borrowing to finance the budget deficit and increased risk aversion saw investors realign their portfolios and shift to low risk government paper.

Finally, the receivership of Chase Bank in 2016 substantially eroded investor and depositor confidence in Tier II and III banks, as well as microfinance institutions. This, followed soon after by the Banking Amendment Act 2016 was a stress event for the banking sector and the overall economy. Although fewer listed companies issued profit warnings in 2016 compared to 2015, earnings for bellwether corporates illustrate the magnitude of economic challenges facing Kenyan businesses in 2016.

Financial PerformanceI am glad to note that our financial performance was robust marked by continued growth in total income and a recovery in profit. Gross Written Premium grew by 15.0% to close at KES 19.4 billion in 2016. Similarly, our total income grew to KES 19.4 billion, increasing by 17.6% over the prior year due to growth in our revenues and steady investment income. Good expense management resulted in our operational expense growth generally tracking the inflation rate. Our recovery in financial performance in 2016 compared to the previous period enabled us to restore our track record of growing shareholder returns. We registered a 76.1% growth in Profit before Tax (PBT) with 2016 PBT of KES 1.2 billion compared to KES 693 million in 2015. The UAP Old Mutual Group is on a sound footing to support our customers and play a leading role in our country’s development, and in the development of the regional economies.

DividendsThe Board of Directors recommends a dividend of KES 1.70 per share (KES 359 million total payment) with respect to the financial year ended 31st December 2016. I am pleased to note that we have restored our dividend payment in line with our improved financial performance in 2016.

Changes to the Board of DirectorsOur Board of Directors is committed to elevating corporate governance standards so as to support management and staff to fulfil shareholder and stakeholder expectations. I would like to thank our departing Directors, Mr.Ralph Mupita and Mr. Tavaziva Madzinga, for their contribution to the Board. They were instrumental in the successful merger of UAP and Old Mutual and they showed us their continued support throughout the process. We wish them all the best in their future endeavours. I also take this opportunity to welcome Mr. Jonas Mushosho to the Board. Mr. Mushosho is the Chief Executive of the Old Mutual business in the Rest of Africa outside South Africa.

CHAIRMAN’S STATEMENT (CONT’D)

2. Kenya (continued)

18 UAP OLD MUTUAL GROUP

UAP Old Mutual Merger UpdateThe integration of the UAP and Old Mutual entities in East Africa continues apace and we have made substantial gains in beginning the realisation of revenue and cost synergies. To this end, we wish to conclude the shareholder and regulatory approval processes for the merger and I ask for your support. Our ultimate goal is to reorganise the UAP and Old Mutual businesses under one holding company, UAP Holdings Limited (UAPHL), so that we can augment our operating and financing capacity. This process entails the acquisition of the Old Mutual subsidiaries and the merger of some of these entities particularly the Life and Asset Management businesses. The merger will position us as a leading provider of Integrated Financial Services in East Africa.

We anticipate that we shall table the full details of the transaction including the rationale, consideration, valuation and timelines through a Shareholders’ Circular to be distributed to all shareholders and thereafter, an extra-ordinary general meeting will be called during the second half of 2017 to approve these transactions.

We believe these transactions will enhance shareholder returns and better position the Group for future initiatives including an eventual listing on the Nairobi Securities Exchange (NSE).

An Update on Managed SeparationThe business strategy announced in 2016 aimed at conducting a managed separation of the wider Old Mutual Group’s four businesses remains on track to be substantially completed by the end of 2018. The process will result in four standalone businesses which will include Old Mutual Emerging Markets (“OMEM”), US-based Old Mutual Asset Management (“OMAM”), Old Mutual Wealth (“OMW”) and Nedbank.

Managed Separation aims to deliver value through:

1. the removal of Old Mutual Plc central operational costs;2. unlocking the conglomerate discount; 3. delivering enhanced performance of the underlying businesses.

Old Mutual Emerging Markets’ (OMEM) future focus will be on sub-Saharan Africa and, following a review of its business, OMEM will be implementing a new target operating model designed to deliver meaningful cost savings and build a foundation for cost discipline while delivering business growth. We welcome the renewed focus from Old Mutual Plc and OMEM and look forward to a beneficial collaboration to reward our shareholders.

OutlookKenya’s investment profile continues to rise with a better governance framework, a more inclusive democracy, stable fiscal and monetary management, efficient regulation and a growing middle class among others. Furthermore, our insurance penetration rate currently stands at approximately 3% meaning that with consumer education and the development of good products we will grow our revenues and profits. Other opportunities include Marine insurance in Kenya following the Government of Kenya directive that importers insure their marine cargo locally.

Rwanda’s outlook is positive with the only possible risk being the general election in 2017. Additionally, the Rwandan Government’s reliance on external funding means that its relations with donors will determine its ability to invest in the economy. For Uganda, continued investment in infrastructure, good weather and the restoration of credit growth could catalyse economic performance. With regards to Tanzania, the extraction of the enormous reserves of natural gas has the potential to radically transform the economy by providing a cheap source of power. Improvements in the political and security conditions in South Sudan will restore stability and confidence. As a whole, East Africa has significant potential and the Group plans to participate fully in the region’s economic development.

CHAIRMAN’S STATEMENT (CONT’D)

19ANNUAL REPORT & FINANCIAL STATEMENTS 2016

I wish to thank my fellow directors for their effective oversight throughout the year; management and staff for their hard work; and, our intermediaries, partners, regulators and other stakeholders. I also thank our customers for their continuous support.

AppreciationIn closing, I thank our shareholders for their patience as we work to increase our returns. We look forward to a vibrant 2017 and wish our customers, shareholders, intermediaries and other stakeholders all the best.

Dr. J. B. Wanjui CBSGroup ChairmanUAP Old Mutual Group

CHAIRMAN’S STATEMENT (CONT’D)

20 UAP OLD MUTUAL GROUP

You make me do everythingthat was once but just a dream.

KEEP GOOD COMPANY

CHAIRMAN’S STATEMENT

“I am glad to report that we have made substantial progress in the combination of our UAP and Old Mutual businesses.”

PETER MWANGI

Dear Shareholder,It is my pleasure to present this report on the progress we have made over the last year. The FY2016 was the first full financial year since the acquisition of our business by Old Mutual in June 2015. Over the course of 2016 we have made significant progress in the execution of our strategy, making operational improvements across the Group and improving financial performance. Our business proved resilient in the face of significant challenges in the Kenyan economy particularly in the banking sector and the capital markets, and political instability in South Sudan. Despite the difficult operating environment, we posted solid financial performance with strong recovery in profit before tax driven by continued revenue growth, disciplined cost control and steady investment income.

Strategic ReviewOur strategic intent is to create an East African financial services champion. We have developed a 5-year strategy spanning the period to 2020 and 2016 was the first year of implementation. The strategy will focus on:

• Maintaining current growth to improve market share across all our lines of business;

• Strengthening key areas of the value chain in our core businesses;

• Rationalization of our operations to focus on the key profit generators and exiting from marginal businesses;

• Strengthening our balance sheet to ensure we are well capitalised to support our growth ambitions;

• Acceleration of the realisation of both revenue and cost synergies from the combination of the UAP and Old Mutual businesses; and

• Innovation for growth by introducing new products and distribution models.

A key plank of our strategy is completion of the merger process for our businesses and rationalization of our marginal operations. On the merger front we have made substantial progress in the combination of the UAP and Old Mutual businesses.

As mentioned in the Chairman’s Statement and as is also explained in detail in the shareholder circular we expect to complete these transactions in the course of the second half of this year subject to your approval as shareholders at an extra-ordinary general meeting and the approval of our various regulators. It is our expectation that these transactions when complete will support the creation of increased shareholder value and therefore I urge you to support the proposals.

Gross Written Premium (“GWP”) – KES Bn

Net Earned Premium (“NEP”) – KES Bn

Net Claims Payable – KES Bn

Profit Before Tax – KES Bn

GCEO’S STATEMENT

23ANNUAL REPORT & FINANCIAL STATEMENTS 2016

On the rationalization front we have undertaken a review of the operations within the Group and identified the insurance brokerage business in the Democratic Republic of Congo as non-core given that it is not aligned to our core underwriting offering. For this reason we will be seeking your approval for us to exit from this business.

We achieved several notable milestones in our journey towards the creation of an integrated financial services group. We are now able to better provide our customers with seamless access to financial products and services that meet all their needs under one roof. The following achievements were key steps towards the realisation of a “one-stop shop” for our customers:

• The establishment of a branch in Kimathi House in Nairobi manned by staff from UAP, Old Mutual and Faulu who are able to sell our entire range of insurance and banking products;

• The expansion of Faulu product offerings to include Visa branded debit cards and countrywide ATMs;• The completion of UAP Old Mutual Tower and the phased relocation of our head office staff starting in December

2016 which is expected to be complete within the first half of 2017;• The launch of the UAP Old Mutual Brand thematic campaign dubbed “Keep Good Company” which was well

received by the market;• And, the launch of M-Tiba, a mass market health product developed in collaboration with Safaricom and Carepay.

M-Tiba has had good customer uptake and will be enhanced and ramped up in 2017.

Operating Environment2016 was a challenging year for the financial services sector especially in Kenya. Although industry Gross Premiums increased for both General and Life Insurance – 8.51% and 19.30% respectively – underwriting profits for the industry declined and investment income supplemented underwriting activities. Capital markets also performed poorly with equities experiencing negative returns for the second consecutive year but returns from interest bearing assets offset the declines from equities. Despite these challenges, we managed to grow our revenues putting us in a good position within the industry. Even so, we recognise that we must work harder to translate top-line growth to better bottom-line performance and improved shareholder returns.

South SudanNotwithstanding the deterioration in the security situation of the country, our South Sudan business contributed strongly to our revenue and profits for 2016 and remains an integral part of our East African strategy. The UAP Old Mutual Group operates a full-fledged insurance business with complementary investments in property within the capital Juba. We remain committed to our business and look forward to harnessing the investment and business potential of South Sudan and its people.

Financial PerformanceOur financial performance was resilient with continued growth in revenues, investment income, good expense control and a recovery in Profit Before Tax (PBT).

PBT recovered to Kes. 1.2 billion in 2016, a growth of 76.1% from Kes. 0.7 billion in 2015. The improvement in PBT is attributed to the following:

i. Actions to support overall business growth including diversifying the product portfolio particularly growing of the non-motor insurance book;

ii. Although our net claims increased, short term loss ratios declined as a result of claims review exercises, review of underwriting practices and better claims management;

iii. Tactical asset allocation that saw us increase our allocation to interest bearing assets and decrease our equities exposure.

These actions mitigated the impact of the tough business environment. However, our Profit After Tax (PAT) dipped slightly by 7.9% to Kes. 825.8 million compared to Kes. 896.6 million in 2015. The main reason for the decline was a significant tax credit in 2015 not enjoyed in 2016. All in all, the Group has delivered a robust set of results for 2016.

GCEO’S STATEMENT (CONT’D)

24 UAP OLD MUTUAL GROUP

OutlookWe are cautiously optimistic that the operating environment going forward will be supportive of growth. The regulatory regime is stable and we have good rapport with key regulatory bodies in the East African region. We will work with the regulators to participate in the development of the insurance sector and the overall investment climate. We are adequately capitalized and able to meet the capital requirements as stipulated by the Insurance Regulatory Authority (IRA) in Kenya particularly as it rolls out the Risk Based Capital (RBC) framework. We are similarly well prepared in the other countries as other insurance regulators adopt this framework across East Africa.

Our key areas of focus in the period ahead will include:

iv. Building out the Integrated Financial Services construct – Enrichment of our value propositions and customer experience improvements as we execute our one-stop shop strategy for financial services;

v. Completing the Merger Transactions – Finalisation of the acquisition of the Old Mutual subsidiaries followed by the mergers of our Life and Asset Management businesses in Kenya;

vi. Improving Efficiency – Making strategic investments in technology and prudent cost management to improve cost-to-income ratios across all our businesses;

vii. Continuous Innovation – Developing more relevant products and services delivered through convenient and cost effective distribution channels;People – Prioritize having the right people because talent is a key enabler of our business strategy.

It is our expectation that successful execution of these strategic initiatives will move us closer to realising our ambition to grow into the pre-eminent Integrated Financial Services provider in East Africa.

AppreciationI wish to thank management and staff for their dedication and hard work. I thank the Board of Directors, the regulators, our partners, intermediaries and other stakeholders. I thank our customers for trusting us as their financial partner, to assist them plan to for their future and to meet their needs for financial services. Finally, I thank you the shareholder and reiterate our commitment to meet your expectations in 2017 and beyond.

Peter K. MwangiGroup Chief Executive OfficerUAP Old Mutual Group

GCEO’S STATEMENT (CONT’D)

25ANNUAL REPORT & FINANCIAL STATEMENTS 2016

2016

CORPORATE GOVERNANCE REPORTFOR THE YEAR ENDED 31 DECEMBER 2016

INTRODUCTION

2016 marked the first full year of operation post Old Mutual’s acquisition of a 60.67% stake in UAP Holdings Limited (“The Group”).

During the year, the Group’s strategic focus was “Becoming the Financial Services Champion in Eastern Africa”. In approving this strategic direction, the Board determined that the execution of the strategy would only be enabled by adherence to the robust corporate governance framework and practices that were rolled out and adopted in 2015. The Group Strategy was impacted by the macro-economic developments in the East African region and in particular, one of the commercial banks in Kenya being put under receivership - Chase Bank (K) Limited (In Receivership) and the increased focus and scrutiny from the Regulators emanating from the introduction of the risk based supervision regime and the increasing impetus to ensure financial stability in the region. The Board and senior management remained intently focused on these emerging issues.

The Group’s corporate governance practices provide the foundations for effective decision making and accountability. We are pleased to present our 2016 Corporate Governance Statement which details our key governance practices at UAP Holdings Limited. This statement has been approved by the Board and is current as at 8th March 2017. In 2016, the Group complied with the Companies Act 2015 and the Capital Markets Authority Corporate Governance Principles and Regulations.

References in this Statement to 2016 mean the year ended 31st December, 2016. Unless otherwise indicated, references to the UAP Holdings Group, mean UAP Holdings Limited and all its subsidiaries. In connection with our Financial Statements for 2016, the Board has received an audit opinion from the auditors of the company, KPMG East Africa.

CORPORATE GOVERNANCE REPORTFOR THE FINANCIAL YEAR ENDED 31 DECEMBER 2016

Directors following the proceedings during the UAP Old Mutual Group Board Engagement and Strategy session on 21st June 2016.

28 UAP OLD MUTUAL GROUP

CORPORATE GOVERNANCE REPORT (CONT’D)

2.1. Board Functions and Responsibilities

The Board is responsible for the formulation, implementation and monitoring of the Group’s Strategic Plan thus providing appropriate strategic direction for the Group. In the same vein, the Board defines the Vision, Mission and Core Values to enable realisation of the set strategic plan. The Board has delegated the day to day operations of the Group to Management which is headed by the Group Chief Executive Officer. The Group’s business is therefore conducted in accordance with a carefully formulated strategy, annual business plans and budgets which set out clear objectives. Roles and responsibilities have been clearly defined with approved authority delegated. Performance against the objectives is reviewed and discussed monthly and quarterly by the management teams in the Group.

The Managing Directors/Chief Executive Officers and General Managers as well as their respective Management teams prepare an annual business review report which is presented to the Group Board during its annual retreat for consideration and approval. Each subsidiary board is expected to monitor the performance of each subsidiary. Consolidation of the financial position is undertaken on a quarterly basis and presented to the Board. Through this processes performance trends, forecasts as well as actual performance against budgets and prior periods are closely monitored by Management.

The Board ensures that the Group espouses proper corporate governance practices by confirming that the requisite codes of conduct, procedures and practices are existent, relevant and adhered to. The Board also achieves this by ensuring that the Group complies with all the statutory requirements.

The Board is responsible for managing the Group’s risks and the Board and Management have been trained on risk management.The Board recognises and honours its responsibility to its stakeholder and in this case Board Members are fully aware of their responsibility to discharge their function in good faith, with prudence, diligence and due care. The overall functions of the Board are as follows:

FUNCTION DETAILSStakeholder Management Enhancing long-term shareholder returns and safeguarding the

interests of stakeholders including customers, suppliers, employees and the communities in which we operate.

Strategy Ensuring that the Group has the appropriate resources to deliver the strategy and business plans.

Performance Reviewing Business Results.Monitoring Budgets.

Integrity of External Reporting Reviewing and monitoring - with the guidance of the Audit Committee, the processes - controls and procedures in place to maintain the integrity of accounting and financial records and statements.

Risk Management and Compliance Reviewing and monitoring with the guidance of the Risk Committee, the risk management profile and processes for compliance in line with regulatory requirements.

Executive Review and Succession Planning Approving key executive appointments and remuneration, monitoring and reviewing executive succession planning and diversity.Reviewing and monitoring the performance of the Group CEO and senior management.

29ANNUAL REPORT & FINANCIAL STATEMENTS 2016

Our Board provides overall strategic direction for the UAP Old Mutual Group, and represents and serves the interests of our shareholders through the creation of sustainable value.

UAP HOLDINGS BOARD OF DIRECTORS

30 UAP OLD MUTUAL GROUP

STANDING FROM LEFT TO RIGHTPeter De Beyer | Dr Peter W Muthoka | Paul Truyens | Susan Omanga | Peter MwangiDr. Joseph Barrage Wanjui | James Muguiyi | James Wambugu | Anisha ArcharyMike Harper | Rose Ogega | David Marshall

SEATED FROM LEFT TO RIGHTJonas Mushosho | AK Maina

31ANNUAL REPORT & FINANCIAL STATEMENTS 2016

The Board’s composition is driven by the following Principles which are set out in the Board Charter:

• The Board will be of an appropriate size to allow efficient decision making;• The Board must be comprised of at least one third independent non-executive directors;• The Board should consist of directors with a broad range of expertise, skills and experience from a diverse range

of backgrounds, including sufficient skill and experience appropriate to the Group’s business.

Newly appointed directors are required to stand for re-election by the Shareholders at the next Annual General Meeting. Re-election of a director is undertaken in accordance with UAP Holdings’ Memorandum and Articles of Association.

The following changes to the composition of the Board have occurred within 2016:

2.2. Board Composition & Board Skills Matrix

NAME OF BOARD MEMBER

MEMBERSHIP PROFESSION NATIONALITY

Dr. Joseph Barrage Wanjui Chairman Engineer/ Entrepreneur KenyanMr. Peter De Beyer Deputy Chairman Actuary South AfricanMr. James Muguiyi Non-Executive Member Finance/Insurer KenyanDr. Peter Wanyaga Muthoka Independent, Non-Executive Member Management Consultant KenyanMr. Ralph Mupita Non-Executive Member Engineer ZimbabweanMr. Tavaziva Madzinga Non-Executive Member Actuary ZimbabweanMr. David Marshall Non-Executive Member Accountant South African/BritishMs. Rose Ogega Independent, Non-Executive Member Accountant/ Financial Consultant KenyanMs. Susan Omanga Independent, Non-Executive Member Marketer Kenyan Mr. Paul Truyens Independent, Non-Executive Member Actuary DutchMr. Mike John Harper Independent, Non-Executive Member Actuarial Science South AfricanMr. James Wambugu Executive Member Audit and Risk Management KenyanMr. Atanas Kariuki Maina Non-Executive Member Advocate KenyanMr. Peter King’ori Mwangi Group Chief Executive Officer/Executive

MemberEngineer Kenyan

Ms. Anisha Archary Non-Executive Member Human Resource Specialist South African

APPOINTMENTSMr. Jonas Mushosho Non-Executive Member Accountant Zimbabwean

RESIGNATIONSMr. Tavaziva Madzinga Effective 30th September 2016Mr. Ralph Mupita Effective 31st January 2017

CORPORATE GOVERNANCE REPORT (CONT’D)

32 UAP OLD MUTUAL GROUP

Board Skills MatrixThe Board’s Corporate Governance and Nominations (CGN) Committee undertakes a continuous review of Board composition using a matrix to assess the skills and experience of each director and the combined capabilities of the Board. Where a Board vacancy is anticipated, the CGN Committee assesses the skills and experience required and then identifies suitable candidates using external consultants as appropriate. The most suitable candidate is appointed by the Board after appropriate checks are undertaken. The Group has formal letters of appointment for its directors, setting out the key terms and conditions of their appointment.

During the year under review, the Committee with the assistance of an external consultant, undertook a Non-Executive Director search process to provide a pipeline of potential candidates the Group could tap into for appointment across the East Africa business.

The skills matrix below demonstrates alignment of the Board’s responsibilities with the current skills mix. The Board is confident that this mix results in an appropriate mix of experience and expertise, and a diverse range of views and perspectives for effective governance, oversight and strategic leadership of the Group.Candidates were solicited based on the following and other relevant considerations:

SKILL CATEGORY EXPLANATIONStrategy Development and oversight of execution of strategic objectives.

Financial Acumen Analysis of key financial statements, assessment of financial viability and performance, contribution to strategic financial planning, ability to oversee funding arrangements and accountability.

Actuarial Management Provide oversight and steer development of risk management strategies in respect of the long and short-term businesses.

Risk Management Oversight of risk frameworks and practices which identify and manage key risks.

Marketing Brand promotion and preservation, strategic planning and providing oversight on organisationsal crisis management plans.

People and Remuneration Oversight over the Group’s talent management framework including reward and succession planning.

Legal and Compliance Oversight of operations and obligations in a highly complex and regulated environment.

Corporate Governance Commitment to the highest standards of governance.

CORPORATE GOVERNANCE REPORT (CONT’D)

33ANNUAL REPORT & FINANCIAL STATEMENTS 2016

2.3. Board CommitteesIn order to discharge its mandate, the Board has established the following committees:

• Audit Committee;• Risk and Compliance Committee;• Remuneration Committee;• Corporate Governance and Nominations Committee;• Customer Affairs Committee;• Integration Committee;• UAP Tower Committee (ad hoc);• Project Saffron Independent Oversight Committee (ad hoc).

The Board has adopted Terms of Reference for each Committee setting out its responsibilities and composition. The Board receives a copy of the Committee’s report and minutes of each Committee meeting.

AUDIT COMMITTEE

RISK COMMITTEE

REMUNERATION COMMITTEE

CORPORATE GOVERNANCE & NOMINATIONS COMMITTEE

CUSTOMER AFFAIRS COMMITTEE

INTEGRATION COMMITTEE

Membership as at 31st December 2016

Rose Ogega (Chair)Peter De BeyerPaul TruyensSusan Omanga

Paul Truyens (Chair)Peter De BeyerRose OgegaJames MuguiyiPeter Mwangi

Dr. Peter Muthoka (Chair)Jonas MushoshoJames MuguiyiAnisha Archary

Peter De Beyer (Chair) Dr. JB WanjuiDr. Peter MuthokaA K MainaAnisha Archary

Mike Harper (Chair)Anne MutahiJames Wambugu

Jonas Mushosho (Chair)Dr. JB WanjuiJames MuguiyiDavid Marshall

CORPORATE GOVERNANCE REPORT (CONT’D)

Standing from Left to Right: Dr. P. Muthoka, P. De Beyer, Hon. Ngenye Kariuki, C.S. Joe Mucheru, CBK D.G. Sheila M’Mbijjewe and Group Chairman Dr. JB. Wanjui at the farewell cocktail for outgoing UAP Old Mutual Directors Hon. Ngenye Kariuki, Joe Mucheru and Sheila M’Mbijjewe at the Crowne Plaza Hotel on 22nd June, 2016.

34 UAP OLD MUTUAL GROUP

The Board has two ad hoc Committees: The UAP Tower Committee and the Project Saffron Independent Oversight Committee. The UAP Tower Committee was set up to provide oversight to the construction of the largest capital investment in the Group: The UAP Old Mutual Tower. Upon full handover of the project, the Committee shall be considered to have duly discharged its mandate. As such in November 2016 the Board decided to stand down its UAP Tower Committee as the construction of the UAP Tower, which it was established to monitor was largely complete.

The Project Saffron Independent Oversight Committee was set up as part of requirements under the Capital Markets Act which requires that an independent committee should be set up where a company intends to undertake transactions between related parties. During the year in review, the UAP Holdings Board, through the Project Saffron Committee, considered reorganisation of the legal structures of the UAP and Old Mutual Kenya entities. The exercise is expected to come to an end within 2017 at which point the Committee shall be considered to have duly discharged its mandate.

2.3.1. Audit Committee The Chair of the Audit Committee, Ms. Rose Ogega, is a Certified Public Accountant [CPA (k)]. The Chair is not an auditor nor accountant for the Company. The Committee meets at least four (4) times a year or at such other times as the Chairman of the Committee shall require.

In addition to the foregoing, the Audit Committee is responsible for the selection, evaluation, compensation and where appropriate, replacement of the external auditor. The external auditor, KPMG (East Africa) attends the Annual General Meeting (AGM) and is available to answer shareholder questions regarding aspects of the external audit and their report. Details of the fees paid to the External Auditors are set out within the 2016 Annual Financial Report.

The Audit Committee is also responsible for assessing whether the Internal Audit function is independent of management and is adequately resourced and funded. Internal and External Audit operate, perform and report as separate, independent functions.

Roles and ResponsibilitiesThe Audit Committee Charter sets out the responsibilities of the Committee members. The key responsibilities are to provide oversight on the following:

a) The integrity of the financial statements;b) The auditor’s qualifications and independence;c) The performance of the Group’s Internal Audit Function and the external auditors;d) The compliance by the Group with legal and regulatory requirements;e) The effective management by the Group of financial risks;f) Review the adequacy and effectiveness of UAP’s Internal Control and financial controls systems.

Key Activities Undertaken During 2016The Audit Committee met six (6) times in the year 2016 with senior representatives from KPMG and Internal Audit attending every scheduled meeting, and the key activities undertaken included:

• Review and approval of the 2016 plans of the external and internal auditor and providing oversight on the work performed throughout the year;

• Review of Audit reports from all subsidiary Audit and Risk Committees within the Group;• Review of significant accounting, financial reporting and other issues raised by management, Internal Audit and

the External Auditor;• Review and recommendations to the Board for the adoption of the Group’s half-year and annual financial

statements;• Consideration and recommendations to the board on significant accounting policies and areas of accounting

and judgment including those related to accounting for provisions for bad and doubtful debt.

CORPORATE GOVERNANCE REPORT (CONT’D)

35ANNUAL REPORT & FINANCIAL STATEMENTS 2016

2.3.2. Risk and Compliance Committee The Group’s Risk Committee supports the Board by providing oversight to the Group’s risk profile in the context of the Board approved risk appetite and making recommendations regarding future risk appetite and in particular risks or risk management practices. This includes reviewing (at least annually) management’s plans for risk mitigation, monitoring the implementation and operation of the risk management framework and internal compliance and control systems, and stress testing the risk portfolio through scenario and sensitivity analysis. The Board through the risk Committee promotes awareness of a risk based culture within the Group. Mr. Paul Truyens is the current Chair of the Committee.

The Chief Risk Officer attends every scheduled Risk Committee Meeting to provide a report which includes updates on identified material risk categories, the Group’s capital and liquidity position. In addition, the Committee also receives and reviews the Risk Committees reports from all subsidiary companies within the Group.

CORPORATE GOVERNANCE REPORT (CONT’D)

36 UAP OLD MUTUAL GROUP

Roles and ResponsibilitiesAs set out in the Risk Committee Charter, the key obligations of the Committee include:• To review, approve and recommend to the Board for approval the system of governance, including the risk

management system, processes, methodologies and tools, and the Combined Group’s internal model, including the internal capital model;

• To monitor and express an opinion to the Board on the adequacy and effectiveness of the systems of governance and risk management, and the internal model;

• To review and express an opinion to the Board on annual operating plans for the Group’s overall risk management, forensics, compliance and second line of defence actuarial function, ensuring these functions are adequately resourced and have appropriate standing within the organization;

• To review, approve and recommend to the Board for approval the methodologies used to identify, assess, measure, monitor and report on risks, including methods used for the calculation of risk exposures, capital requirements, scenario analysis and stress testing, and the identification and recording of actual losses;

• To Review, monitor and challenge the actual assessment and reporting of risks, trends and concentrations, including risk profiles, exposures, capital requirements, risk events, assessments and indicators and any associated attestations and letters of representation.

Key Activities Undertaken During 2016The Risk Committee met four (4) times during the year. The key activities included:

• Review of the key risks and risk management framework;• Review of the Group’s Capital Adequacy framework;• Review of declarations and assurances from Internal Audit in relation to effectiveness of internal controls and

risk management framework;• Review of Risk Reports from subsidiary Board Committee meetings.

2.3.3. Remuneration Committee The Remuneration Committee supports the Board by reviewing and assessing the Group’s remuneration policies and practices in the context of the regulatory environment and the enhancement of corporate and individual performance. Dr. Peter Muthoka is the current Chair of the Committee. The Committee meets at least four (4) times a year or at such other times as the Chairman of the Committee shall require.

Roles and ResponsibilitiesAs set out in the Remuneration Committee Charter, the key roles and responsibilities of the Committee are as follows:a) Set review and make recommendations to the Board on the remuneration and benefits arrangements of non-

executive directors; b) Set, review and make recommendations to the Board for approval, the Combined Group remuneration and

benefits philosophy, policies and practices;c) In conjunction with the Board, approve the Directors’ Remuneration Policy and/or Annual Remuneration Statement

to be included in the Annual Financial Statements report having regard to the fulfilment of the provisions of the Capital Markets Authority or securities disclosure requirements;

CORPORATE GOVERNANCE REPORT (CONT’D)

37ANNUAL REPORT & FINANCIAL STATEMENTS 2016

a) Determine the remuneration, incentive structure and benefits of the Group Chief Executive Officer and members of the Executive Leadership Team as recommended by the Group Chief Executive Officer based on an evaluation of their performance;

b) Establishing annual and long-term performance goals and objectives for the Group Chief Executive Officer and reviewing the goals approved by the Group Chief Executive Officer for the members of the Executive Leadership Team.

Key Activities Undertaken in 2016• Review and recommendation to the Board on the incentives, including long term incentive plan payable to

senior executives;• Review and recommendation to the Board of non-executive directors’ fees, including for subsidiary companies;• Approval of harmonized Human Resource Policies for implementation across the Group;

• Oversight of the Group’s performance management framework.

2.3.4. Corporate Governance and Nominations CommitteeThe Corporate Governance and Nominations Committee supports the Board by monitoring the size and composition including succession planning for directors and senior management, evaluation Board Committee and individual director performance and providing oversight to the Board’s professional development. Mr Peter De Beyer is the current Chairman of Corporate Governance and Nominations’ Committee.

Roles and ResponsibilitiesAs set out in the Corporate Governance and Nominations Committee Charter, the key roles and responsibilities of the Committee are as follows:a) Assist the Board in its determination and evaluation of the adequacy, efficiency and appropriateness of the

corporate governance structure and practices of the Combined Group;b) Provide guidance to the Board on strategy in regard to sound Corporate Governance in the Group’s investments

as deemend appropriate and relevant;c) Make recommendations to the Board on sound Corporate Governance practices in the Combined Group, and

to the extent relevant or appropriate;d) Promote the overall effectiveness of Corporate Governance within the Group, and to the extent appropriate

or relevant, its investments, in accordance with the recommendations of the relevant local and international reports on best practice corporate governance and other requirements of good corporate practice other than in respect of risk management, compliance and internal control which remain the remit of the Audit and Risk and Compliance Committee.

Principal Activities Undertaken in 2016i) Assessment of the appropriate size and composition of the Board and its Committees;ii) Succession planning for non-executive directors, together with making recommendations to the Board on the

appointment of new directors;iii) Approval of methodology for the annual Board performance review.

CORPORATE GOVERNANCE REPORT (CONT’D)

38 UAP OLD MUTUAL GROUP

2.3.5. Customer Affairs CommitteeThe Customer Affairs Committee supports the Board by assisting in the identification, evaluation and monitoring of customer trends, issues and concerns in a bid to position the Group to anticipate and adjust to customer needs and preferences. The Committee Chair is Mr. Mike Harper.

Roles and ResponsibilitiesThe Customer Affairs Charter sets out the Key Roles and Responsibilities as follows:

a. Provide input into the development and the monitoring of the Group Customer Strategy, and review and report to the Board on the impact of such on customer value and fair treatment of customers;

b. Play an important role at the time of strategy and plan creation by reviewing and providing input into the consideration of the customer environment, as part of the strategy creation and plan formulation processes for the Group Customer Strategy;

c. Provide oversight regarding the extent to which the UAP Old Mutual Group is implementing fair treatment of its customers through the implementation of applicable Treating Customers Fairly Frameworks;

d. Review the practical results of the implementation of TCF outcomes to ascertain whether they are aligned with the TCF goals;

e. Consider the market conduct Principles and explicit rules underpinning TCF and ensure that measures implemented by UAP Old Mutual Group pursuant to TCF requirements, generate the benefits envisaged.

Key Activities Undertaken Within the Year1. The Committee adopted the Terms of Reference and defined its key objectives.2. Members reviewed the Treating Customers Fairly Principals as they apply to the Group and set out action items,

monitoring framework and key reporting items.

CORPORATE GOVERNANCE REPORT (CONT’D)

39ANNUAL REPORT & FINANCIAL STATEMENTS 2016

2.4. Board Meetings and Information to DirectorsThe Board meets at least once every quarter but the business may warrant the convening of special meetings from time to time. All Board meetings are scheduled in advance of the respective year through an Annual Calendar of Board Meetings including a rolling calendar, which facilitates planning and availability of the members. Board Committee meetings are scheduled in advance of the Board Meeting so that all technical matters are appropriately addressed and reported to the Board for ratification or approval.

The directors are given appropriate and timely information on key activities of the business regularly and on request in order to carry out their roles. Specifically the directors are provided with all available information in respect of items to be discussed at a meeting of the Board or Committee prior to the meeting. They may also seek independent professional advice, at the Company’s expense, concerning the affairs of the Group in consultation with the Group Chief Executive Officer and the Group Company Secretary.

2.5. Director IndependenceThe Board’s composition adheres to the requirements of independence as set out in the Capital Markets Act, Code of Corporate Governance Practices. The Board is satisfied that each non-executive director who has served on the Board during 2016 has retained independence of character and judgement.

2.6. Conflicts of Interests The Group Board Charter places an obligation on Directors to make declarations on their personal or commercial interests with a view of avoiding any action, position or interest that conflicts or appears to conflict with a Group interest. This is a matter for active and ongoing consideration by all directors, and thus a standard declaration form has been developed for recording and updating directors’ interests as they occur and on an annual basis.

2.7. Director Induction Each new director is provided with an orientation program which includes discussions with executives and management, briefings and workshops on the Group’s strategic plans, risk management strategy and framework, significant financial accounting and risk management matters, compliance programs, internal and external audit programs and director’s duties and responsibilities.

2.8. Board Performance Directors are expected to prepare adequately for, attend and participate in Board and Committee Meetings. The Board has put in place a performance evaluation system to enable it set its objectives and review its performance annually against these objectives. Due to the number of changes effected in the governance structures during the period under review, the Board held a strategy session on 21st and 22nd June 2016 to set out the strategic objectives against which it would be evaluated in 2017. The performance and evaluation tools were developed and approved in the period under review and the exercise would be conducted and the results communicated to the Board through the approved process.

2.9. Board AttendanceDuring the Financial Year under review eight (8) Board Meetings [4 being ordinary board meetings and 4 being special board meetings] and forty (40) Committee Meetings were held. A review of attendance to meetings by individual members during the period under review indicates that all members gave sufficient time and attention to the affairs of the Board. The highest level of individual attendance was 100% of eligible board meetings and the lowest level of attendance was 55% of eligible meetings, with an average of 78.97% attendance across the current membership of the Board. This marks an 8.23% improvement in the average attendance for the Board compared to prior year.The Board members gave prior notice of inability to attend and gave meaningful input on the agenda items as appropriate.

CORPORATE GOVERNANCE REPORT (CONT’D)

40 UAP OLD MUTUAL GROUP

2.10. Board Development Board development needs were identified and/or analysed for each Member and for the Board as a whole during the period under review. Thereafter, the Board would be developed in accordance with the Board induction and development plan to address areas of improvement for individual members and to provide up to date information on new areas of business and risk for the group including: - corporate governance training, risk management training, training on anti-money laundering legislation as well as training on the Group Operating Model.

The Company values the input of the shareholders and engages directly with them when making any revisions to the Board remuneration package which is approved by the shareholders at the Annual General Meeting of Members.

2.11. Statement of Compliance The Board is satisfied that the Group has, to the best of their knowledge, complied with all applicable laws and conducted its business affairs in accordance within the law. In accordance with the Group Operating Model, the Board has reviewed the attestation of Management in this regard and to the knowledge of the Board no director, employee or agent of the Group acted or committed any indictable offence under the Anti-Corruption laws in conducting the business of the Group in the period under review nor was involved or been used as a conduit for money laundering or any other activity incompatible with the relevant laws.

The Board continues to abide by its Charter, the internal codes of conduct, the Memorandum and Amended Articles of Association of the Company and the Terms of Reference of Board Committees. The Group continues to comply with all the statutory requirements relevant to its operation as a body corporate and complies with relevant regulatory guidelines as issued from time to time.

2.12. Group Company SecretaryThe Group Company Secretary co-ordinates the Board activities and ensures, in conjunction with the Chairman and Group Chief Executive Officer, that the Board meetings are held procedurally. The Group Company Secretary links flow of information between the Management and the Board as well as ensures the Board receives adequate and timely information and that Management receives feedback in a similar manner.

All Board Members have direct access to the Group Company Secretary who is also responsible for implementing and monitoring good corporate governance practices at the Board. The Secretary ensures that the business of the Board meets all statutory requirements, keeps all legal and regulatory requirements under review and briefs the Board accordingly about these developments. In the year under review, the Group Company Secretary assisted by the Deputy Group Company Secretary performed this function.

CORPORATE GOVERNANCE REPORT (CONT’D)

41ANNUAL REPORT & FINANCIAL STATEMENTS 2016

2.13. ShareholdingAt 31 December 2016, the top ten shareholders in the Company were:

NO. OF SHARES HOLDINGS %1 OLD MUTUAL HOLDINGS LIMITED 78,919,889 37.33%

2 OLD MUTUAL LIFE ASURANCE COMPANY (SOUTH AFRICA) 49,332,445 23.33%

3 BAWAN LTD 43,258,299 20.46%

4 JAMES NGATIA MUGUIYI 12,611,247 5.97%

5 ESTATE OF THE LATE WILLIAM KIMUTAI MARTIN 2,341,480 1.11%

6 ANDREW STEPHEN GRAY SMITH 1,789,189 0.85%

7 GENGHIS NOMINEES A/C 017 1,544,900 0.73%

8 STANDARD CHARTERED NOMINEES A/C 9230 1,403,000 0.66%

9 TIMOTHY MICHAEL JOHN OWEN-BURKE 1,371,562 0.65%

10 SAYANI INVESTMENTS LIMITED 1,194,957 0.57%

CORPORATE GOVERNANCE REPORT (CONT’D)

42 UAP OLD MUTUAL GROUP

Distribution of Shareholders as at 31-Dec-2016

CORPORATE GOVERNANCE REPORT (CONT’D)

SHARES RANGE SHAREHOLDERS SHARES SHARES %

01 - 100000 1,035 7,359,380 3.48

100001 - 1000000 26 9,175,081 4.34

>1000000 11 194,885,428 92.18

TOTALS 1,072 211,419,889 100

Shareholder Analysis by Domicile

Individual Investors

KENYA 877 29,746,059 14.07

EAST AFRICAN 27 99,000 0.05

FOREIGN 19 941,865 0.45

TOTALS 923 30,786,924 14.56

Shareholder Analysis by Domicile

Corporate Investors

KENYA 145 131,236,245 62.07

EAST AFRICAN 02 49,200 0.02

FOREIGN 02 49,347,520 23.34

TOTALS 149 180,632,965 85.44

The directors’ direct and indirect interest in the ordinary share capital of the Company on 31 December 2016was as follows:

NO. OF SHARES HOLDINGS %

1 OLD MUTUAL HOLDINGS LIMITED 78,919,889 37.33%2 OLD MUTUAL LIFE ASSURANCE (SOUTH AFRICA) 49,332,445 23.33%

By order of the Board

Nkirote Mworia NjiruSecretary

8 March 2017

43ANNUAL REPORT & FINANCIAL STATEMENTS 2016

SUSTAINABILITY & CSR REPORT 2016

From a nondescript village track 13 years ago, our partnership with the Ndakaini Dam Environmental Conservation Association (NDEKA) has impacted millions of lives through environmental conservation, job creation and nurturing athletic talent.

The annual event has converted the UAP Old Mutual Ndakaini Half Marathon into one of the best breeding grounds for Kenya’s record breaking athletes.