control vs. minority interests and marketability discounts ... · pdf filecontrol vs. minority...

TRANSCRIPT

Control vs. Minority Interests and Marketability Discounts

for ESOPsOhio Employee Ownership Center

Akron/Fairlawn HiltonFairlawn, OhioApril 16, 2004

Richard A. Schlueter

COMSTOCK VALUATION ADVISORSNewport on the Levee 1 Levee Way, Suite 3109 Newport, KY 41071 859-957-2300

C AV

COMSTOCK VALUATION ADVISORS

Levels of Value

Controlling Interest ValueBuyer of a Company’s Equity or Control Equity Shareholder

Non-Marketable Minority Interest ValueNon-Controlling Shareholder of a Private Company

Marketable Minority Interest ValuePrice Quoted in the Wall Street Journal

Discount for Lack of Marketability

Discount for Lack of ControlControl Premium

COMSTOCK VALUATION ADVISORS

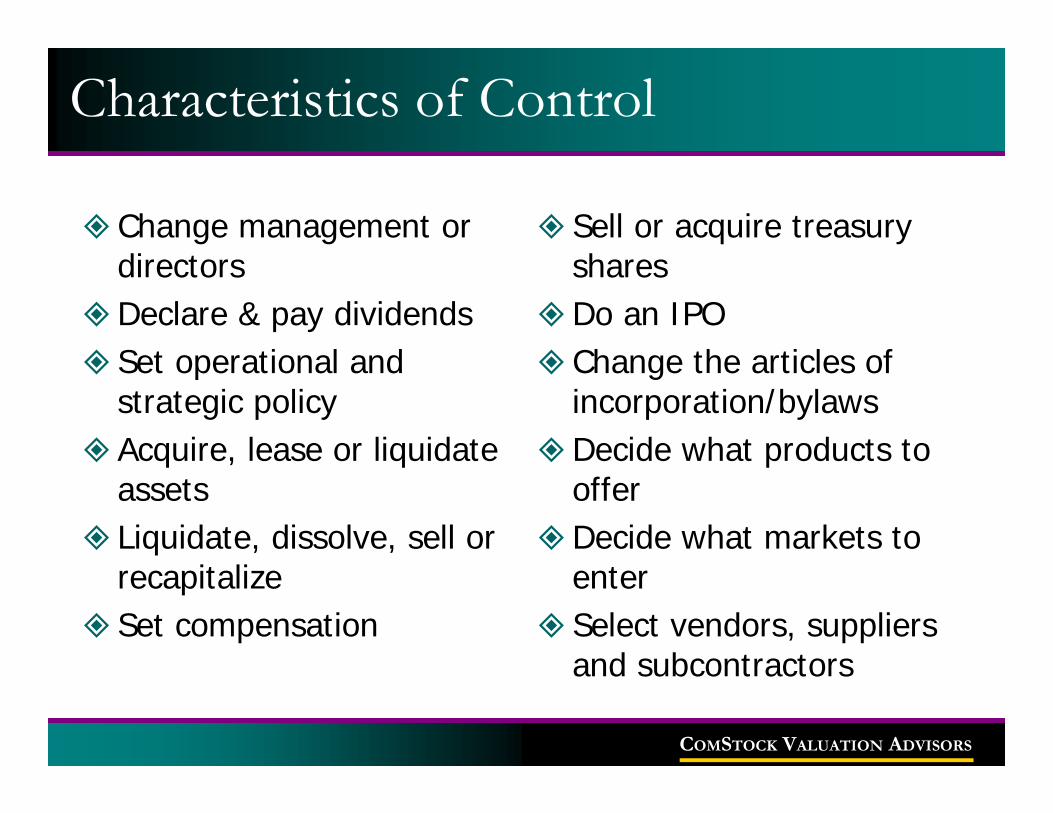

Characteristics of Control

Change management or directorsDeclare & pay dividendsSet operational and strategic policyAcquire, lease or liquidate assetsLiquidate, dissolve, sell or recapitalizeSet compensation

Sell or acquire treasury sharesDo an IPOChange the articles of incorporation/bylawsDecide what products to offerDecide what markets to enterSelect vendors, suppliers and subcontractors

COMSTOCK VALUATION ADVISORS

Size of the block of stock100% - Absolute control80% - Consolidation for tax purposes50%/50% - No Control but veto powerLarge minority - Effective controlLarge minority - No controlSwing VoteSmall minority

Factors Impacting Control/Minority Interest Discounts

COMSTOCK VALUATION ADVISORS

Company’s industryNature/magnitude of discretionary expensesQuality of existing managementBusiness opportunities not currently being exploitedPotential synergiesCost savings

Factors Impacting Control/MinorityInterest Discounts

COMSTOCK VALUATION ADVISORS

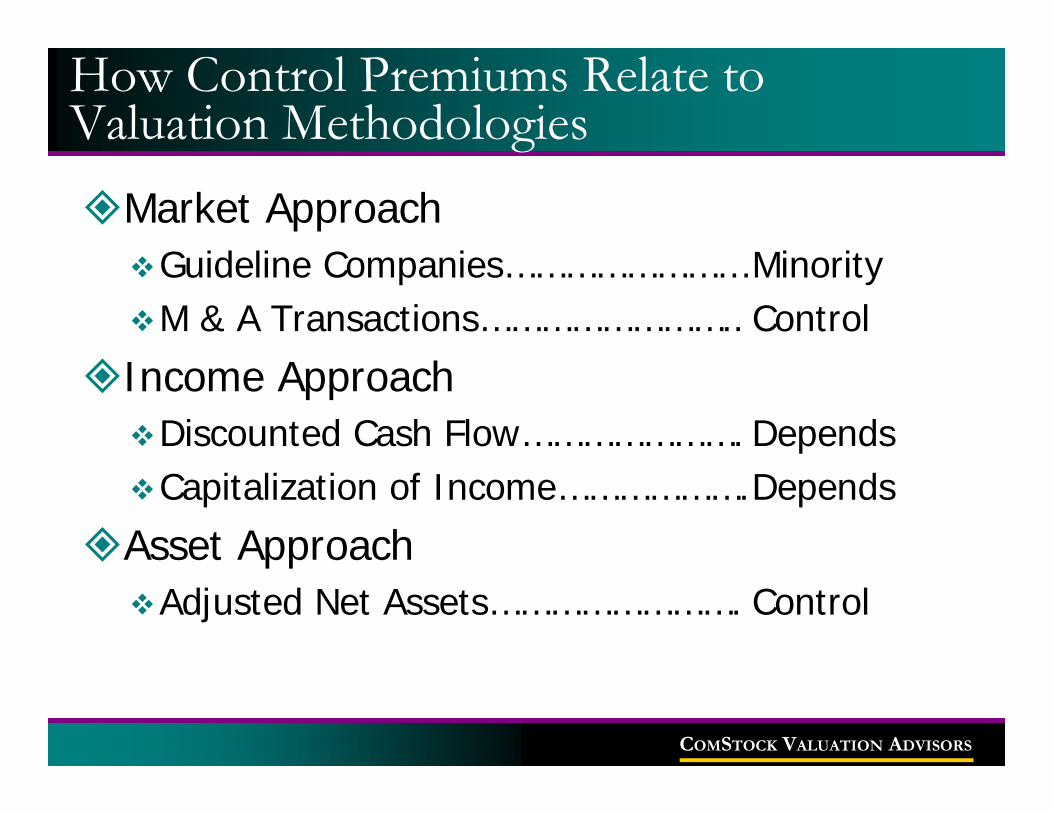

How Control Premiums Relate toValuation Methodologies

Market ApproachGuideline Companies……………………MinorityM & A Transactions…………………….. Control

Income ApproachDiscounted Cash Flow…………………. DependsCapitalization of Income……………….Depends

Asset ApproachAdjusted Net Assets……………………. Control

COMSTOCK VALUATION ADVISORS

Equity Control Premiums (Mergerstat Review)

Percent Premium Offered Over Market and Implied Minority Discount

02000400060008000

100001200014000

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 20020.0%

10.0%

20.0%

30.0%

40.0%

50.0%

DJIA High DJIA Low

Median Premium Offered Implied Minority Discount

COMSTOCK VALUATION ADVISORS

When Can ESOP Pay a Control Price?DOL Proposed Regulations

ESOP can only pay control price if it has control “in form and in substance.”

ESOP purchases greater than 50 percent of the voting stock.A control premium can be paid to the extent that a willing buyerwould pay a premium, although it may not be reasonable for an ESOP to pay a “strategic” control premium.

ESOP initially buys a minority stake but also obtains an option for control.

Proposed Regulations state that if there is a written, binding agreement that allows the ESOP to gain control in a reasonable period of time, a control price can be paid.

Multi-step transactionsESOP already owns a large minority interest in the company that it acquired in one or a series of minority interest transactions. It then has the opportunity to purchase enough stock for the ESOP to gain control. Can the ESOP pay a control price in the second transaction?

COMSTOCK VALUATION ADVISORS

Impact of Leveraged ESOP on Control PremiumsTraditional Market Equity Approach

Pre Post Change

Minority Firm Value $10.0 $10.0 $0.0Debt $0.0 $7.8 ($7.8)

Equity Value $10.0 $2.2 $7.8Control Premium @ 30% $3.0 $0.7 $2.3

Control Equity Value $13.0 $2.9 $10.1

ESOP buys 60% $7.8

COMSTOCK VALUATION ADVISORS

Impact of Leveraged ESOP on Control PremiumsMarket Capital Approach

Pre Post Change

Minority Firm Value $10.0 $10.0 $0.0Control Premium @ 30% $3.0 $3.0 $0.0

Control Value of Firm $13.0 $13.0 $0.0Debt $0.0 $7.8 ($7.8)

Control Equity Value $13.0 $5.2 $7.8

ESOP buys 60% $7.8

COMSTOCK VALUATION ADVISORS

Impact of Leveraged ESOP on Control Premiums

Control premiums may be better measured on the basis of the firm’s capital value (including both debt and equity) in leveraged ESOP transactions.Alternatively, control premiums computed based upon the firm’s equity value may need to be adjusted to reflect the impact of adding debt to the firm’s capital structure.

COMSTOCK VALUATION ADVISORS

Should an ESOP-Owned Company Pay a Premium to Acquire Another Company?Control ESOP Example

Control ControlESOP Acquired

Company Company Combined

Minority Firm Value $10.0 $8.0 $18.0Control Premium @ 30% $3.0 $2.4 $5.4

Control Value of Firm $13.0 $10.4 $23.4Debt $0.0 $10.4 $10.4

Control Equity Value $13.0 $0.0 $13.0

Assume 60% ESOP $7.8 $7.8

COMSTOCK VALUATION ADVISORS

Should an ESOP-Owned Company Pay a Premium to Acquire Another Company?Minority ESOP Example

Minority ControlESOP Acquired

Company Company Combined

Minority Firm Value $10.0 $8.0 $18.0Debt $0.0 $10.4 $10.4

Minority Equity Value $10.0 ($2.4) $7.6

Assume 30% ESOP $3.0 $2.3

COMSTOCK VALUATION ADVISORS

Should an ESOP-Owned Company Pay a Premium to Acquire Another Company?

If the ESOP owns control and acquisition is made at fair market value on a controlling interest basis and the ESOP is being valued on a controlling interest basis, then share value should not be dilutive to the ESOP.If the ESOP owns a minority interest or owns a controlling interest but is being valued on a minority interest basis, the value after the transaction could be dilutive to the ESOP unless the control premium can be rationalized on the basis of cash flow enhancements.

COMSTOCK VALUATION ADVISORS

MarketabilityThe ability to convert an asset to cash at minimal cost.

Discount for Lack of MarketabilityAn amount or percentage deducted from the value of an ownership interest to reflect the relative absence of marketability.

Empirical DataRestricted stock studiesPre-IPO studies

Discount for Lack of Marketability

COMSTOCK VALUATION ADVISORS

Factors Affecting the Discount for Lack of Marketability

Dividends/DistributionsPotential BuyersSize of InterestProspect of Sale/IPOAccess to InformationRestrictive Transfer ProvisionsPut Rights

Built-in Capital GainsSize of the CompanyRedemption PolicyCompany ManagementNature of the BusinessFinancial Condition of the Company

COMSTOCK VALUATION ADVISORS

Summary of Restricted Stock Studies

Study

Years Covered

Discount

SEC, Overall Averagea 1966-1969 25.8 SEC, Non-reporting OTC Companiesa 1966-1969 32.6 Gelmanb 1968-1970 33.0 Troutc 1968-1972 33.5

k

Moroneyd Unknownh 35.6 Mahere 1969-1973 35.4 Standard Research Consultantsf 1978-1982 45.0

k

Silberg 1981-1988 33.7k Houlihan, Lokey, Howard & Zukin 1991-1993 22.0 Management Planning, Inc. Unknown 30.0-35.0 Johnsoni 1991-1995 20.0 Columbia Financial Advisorsj 1996-1997 21.0 Columbia Financial Advisorsj 1997-1998 13.0

COMSTOCK VALUATION ADVISORS

Robert W. Baird Pre-IPO Studies

Years Covered # of Qualifying Average Price Median Pricein Study Transactions Discount (%) Discount (%)

1980-1981 13 60% 66%1985-1986 21 43% 43%1987-1989 27 45% 45%1989-1990 23 45% 40%1990-1992 35 42% 40%1991-1993 54 45% 44%1994-1995 46 45% 45%1995-1997 91 43% 42%1997-2000 36 48% 50%

COMSTOCK VALUATION ADVISORS

Marketability Discount

Public companies do not suffer discounts for lack of marketability as they may be readily converted into cash.Some public companies that have limited trading activity may be subject to a blockage discount if the block of stock owned by the ESOP is large enough to have an adverse impact on the stock price if sold in the open market within a short period of time.

COMSTOCK VALUATION ADVISORS

ESOP Specific Marketability IssuesLevel of control by ESOP (Controlling vs. Minority Interest)ESOPs can gain liquidity in one of two ways:

A sale of all of its stock as is often observed in M & A transactions. Participant can put shares back to company upon termination.

Studies on marketability discounts have limited use in the context of ESOP valuations because the participants’ put right under ERISA creates a market for the stock.DOL Proposed Regulations requires consideration of:

Extent to which put rights are enforceableAbility of company to meet repurchase obligation

Other factors to consider:Past practices in repurchases by the companyForm and timing of payments

COMSTOCK VALUATION ADVISORS

ESOP Marketability Discounts

Discounts for controlling interest ESOPs are typically zero to 10 percent.Discounts for minority interest ESOPs are more often found to be greater than zero but are typically in the range of zero to 15 percent. Occasionally we have observed discounts greater than 15 percent for minority interest ESOPs.