copper concentrates: smelting technologies update … ingls/presentacion fundiciones giec.pdf ·...

TRANSCRIPT

Logo Gobierno:

160x162px.

Ministerio,

Subsecretaría,

Organismo,

etc.:160x145px

COPPER CONCENTRATES:

SMELTING TECHNOLOGIES UPDATE AND CUCONS MARKET

Jorge Cantallopts

Research and Policy Director Chilean Copper Commission

April 2017

@CochilcoChile

CONTENTS

@CochilcoChile

02

04

03

05

Background and context

Introduction01

Smelting technologies

Copper concentrates market

Concluding remarks

INTRODUCTION

Chilean Copper Commission

01

INTRODUCTION

• Sulphide copper accounts for almost 80 percent of world mineproduction and more than 2/3 of Chilean production and itsexpected to grow its share over the time.

• Smelting arise as a strategic process for copper producercountries. Chile maintains around 9 percent of global smeltingproduction.

• New technology developments and higher competition forcopper concentrates motivates this study.

@CochilcoChile

BACKGROUND AND CONTEXT 02

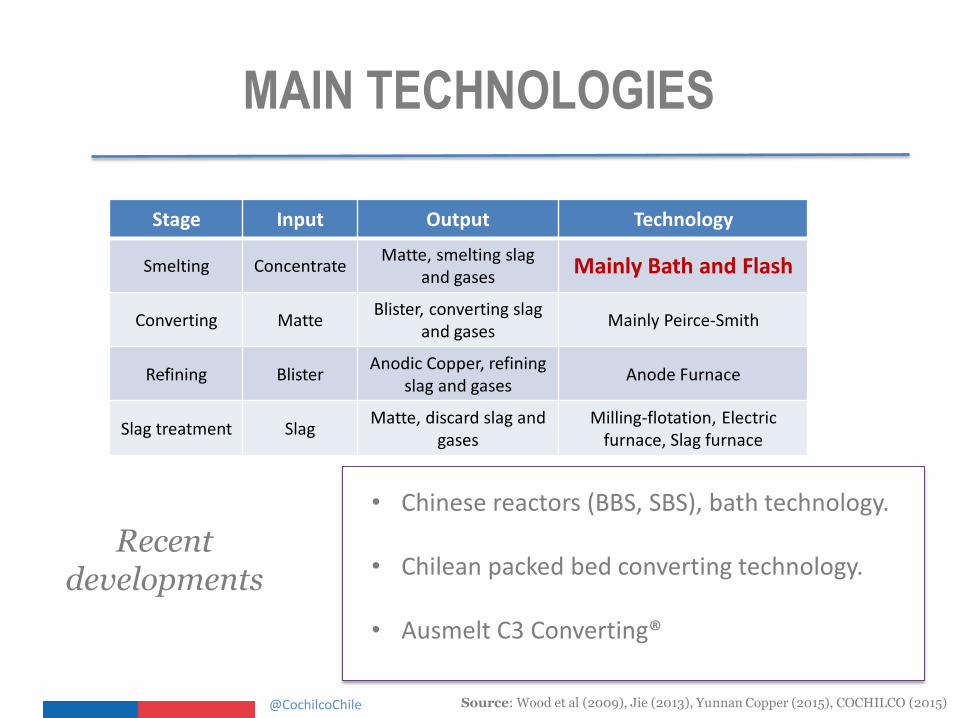

MAIN TECHNOLOGIES

@CochilcoChile Source: Wood et al (2009), Jie (2013), Yunnan Copper (2015), COCHILCO (2015)

Stage Input Output Technology

Smelting ConcentrateMatte, smelting slag

and gasesMainly Bath and Flash

Converting MatteBlister, converting slag

and gasesMainly Peirce-Smith

Refining BlisterAnodic Copper, refining

slag and gasesAnode Furnace

Slag treatment SlagMatte, discard slag and

gasesMilling-flotation, Electric

furnace, Slag furnace

Recentdevelopments

• Chinese reactors (BBS, SBS), bath technology.

• Chilean packed bed converting technology.

• Ausmelt C3 Converting®

CHILEAN CHALLENGE: COMPLEX CUCON

@CochilcoChile Source: Wood Mackenzie (2015), COCHILCO (2015)

• Mineralogical composition affects concentrates marketperformance.

• Arsenic compounds arise in northern Chile and some mines inPeru.

• Mixing concentrates from various sources and penaltiescharges could cost more than 200 $US/DMT.

SMELTING TECHNOLOGIES03

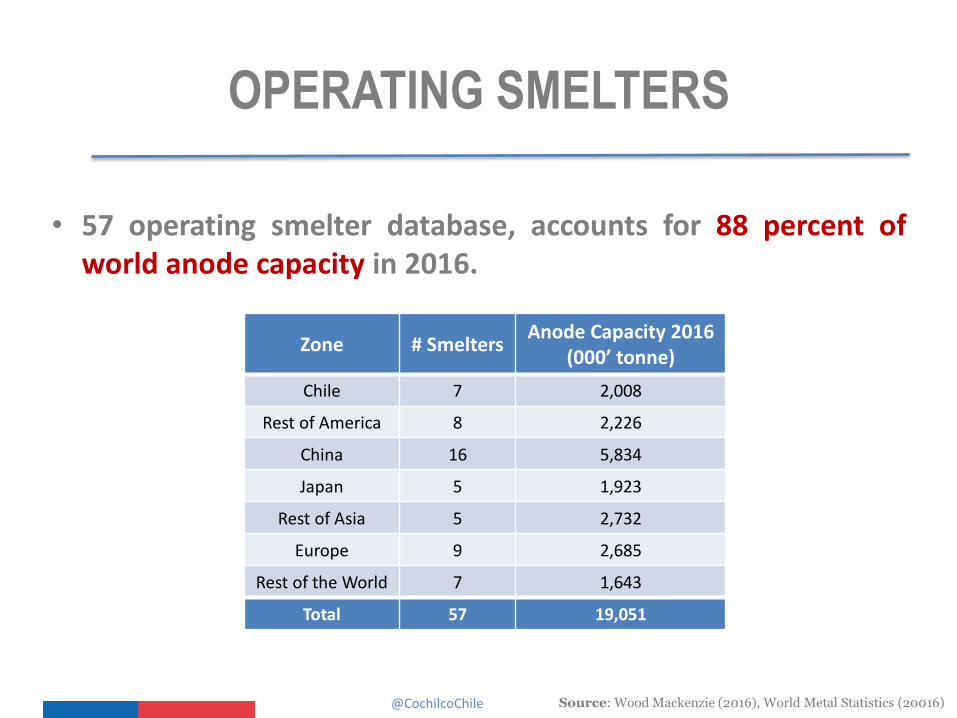

OPERATING SMELTERS

@CochilcoChile

• 57 operating smelter database, accounts for 88 percent ofworld anode capacity in 2016.

Source: Wood Mackenzie (2016), World Metal Statistics (20016)

Zone # SmeltersAnode Capacity 2016

(000’ tonne)

Chile 7 2,008

Rest of America 8 2,226

China 16 5,834

Japan 5 1,923

Rest of Asia 5 2,732

Europe 9 2,685

Rest of the World 7 1,643

Total 57 19,051

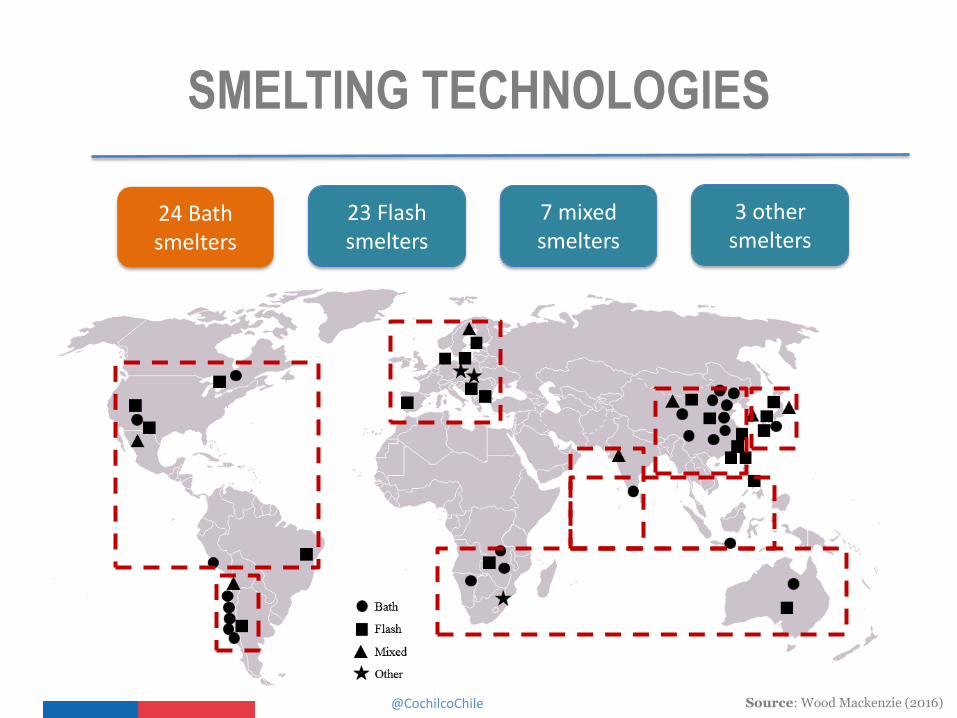

SMELTING TECHNOLOGIES

@CochilcoChile Source: Wood Mackenzie (2016)

24 Bath smelters

23 Flash smelters

7 mixedsmelters

3 othersmelters

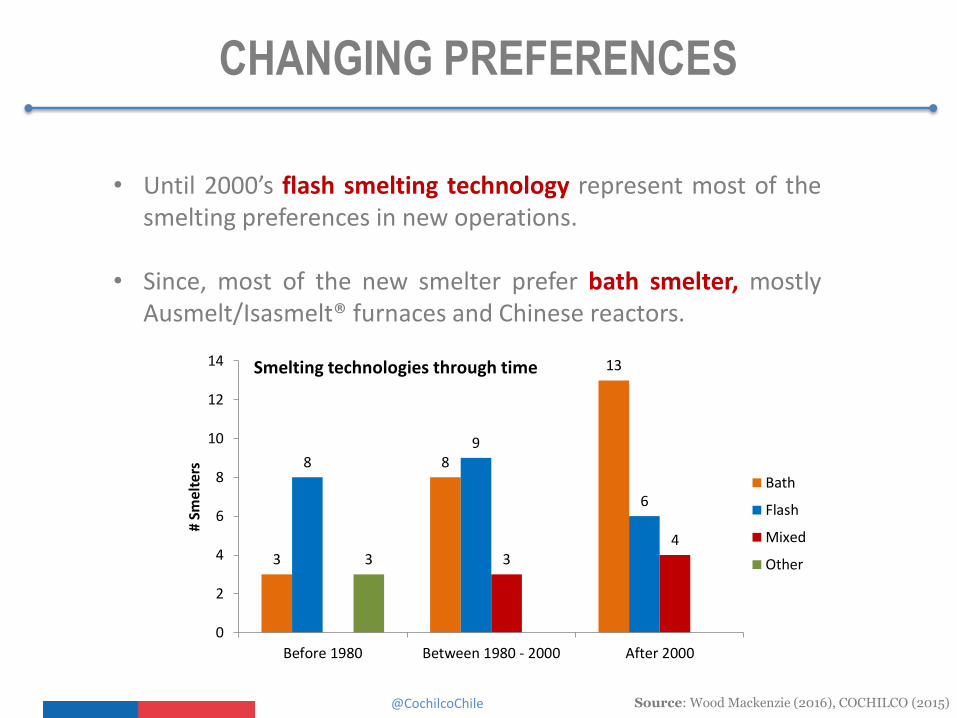

CHANGING PREFERENCES

@CochilcoChile Source: Wood Mackenzie (2016), COCHILCO (2015)

• Until 2000’s flash smelting technology represent most of thesmelting preferences in new operations.

• Since, most of the new smelter prefer bath smelter, mostlyAusmelt/Isasmelt® furnaces and Chinese reactors.

3

8

13

89

6

34

3

0

2

4

6

8

10

12

14

Before 1980 Between 1980 - 2000 After 2000

# Sm

elte

rs

Smelting technologies through time

Bath

Flash

Mixed

Other

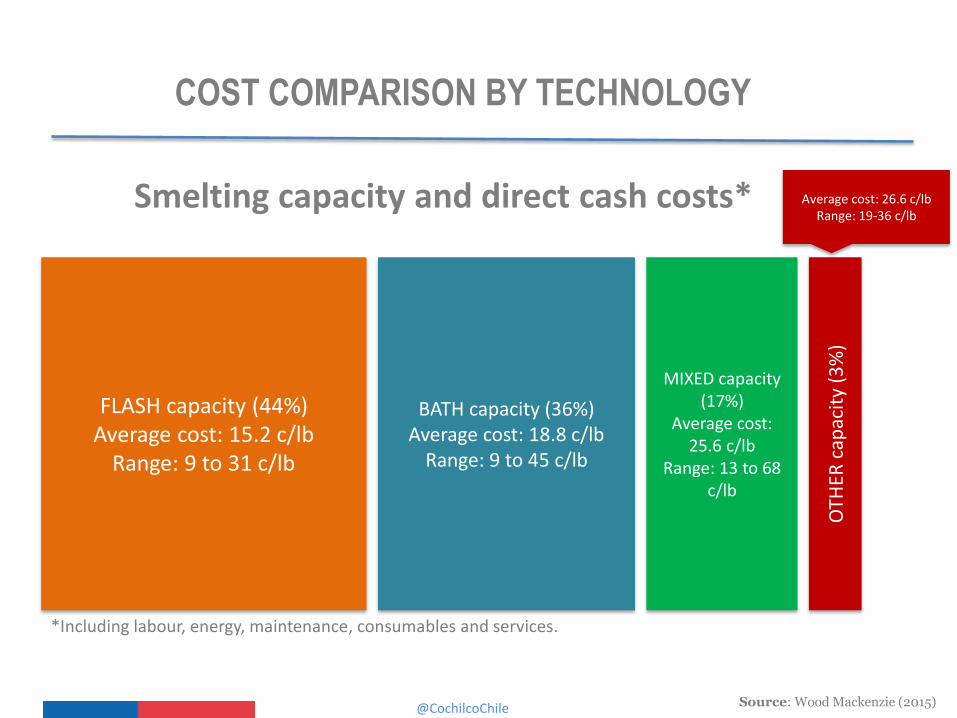

COST COMPARISON BY TECHNOLOGY

@CochilcoChile

Smelting capacity and direct cash costs*

Source: Wood Mackenzie (2015)

FLASH capacity (44%)Average cost: 15.2 c/lb

Range: 9 to 31 c/lb

BATH capacity (36%)Average cost: 18.8 c/lb

Range: 9 to 45 c/lb

MIXED capacity(17%)

Average cost: 25.6 c/lb

Range: 13 to 68 c/lb

OTH

ER c

apac

ity

(3%

)

*Including labour, energy, maintenance, consumables and services.

Average cost: 26.6 c/lbRange: 19-36 c/lb

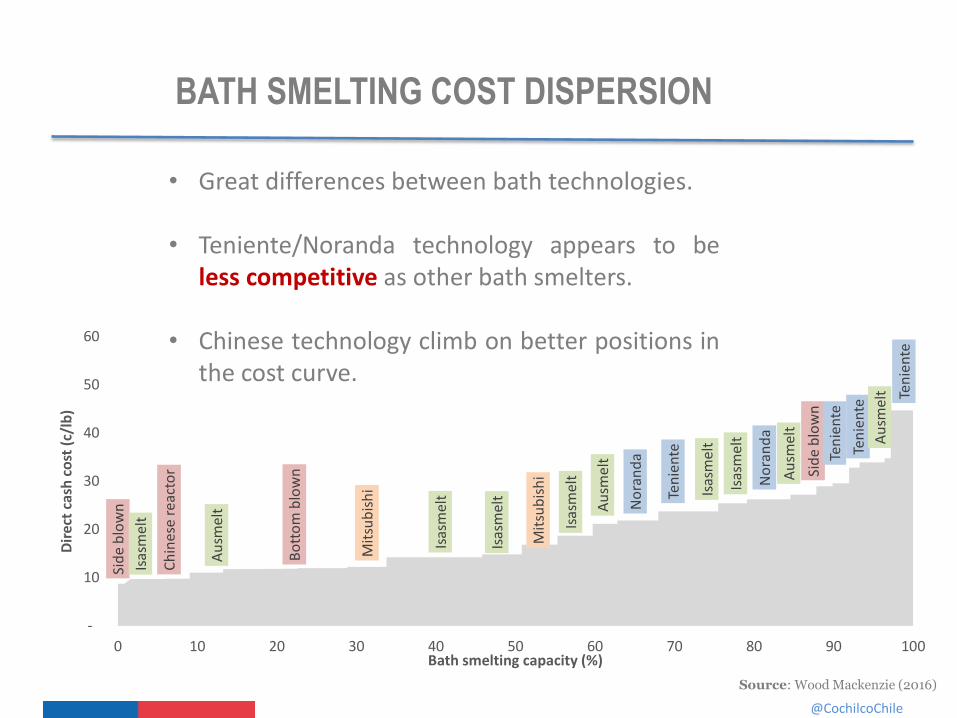

BATH SMELTING COST DISPERSION

@CochilcoChile

• Great differences between bath technologies.

• Teniente/Noranda technology appears to beless competitive as other bath smelters.

• Chinese technology climb on better positions inthe cost curve.

Source: Wood Mackenzie (2016)

Sid

e b

low

n

Isas

mel

t

Ch

ines

e re

acto

r

Au

smel

t

Bo

tto

m b

low

n

Mit

sub

ish

i

Isas

mel

t

Isas

mel

t

Mit

sub

ish

i

Isas

mel

t

Au

smel

t

No

ran

da

Ten

ien

te

Isas

mel

t

Isas

mel

t

No

ran

da

Au

smel

t

Sid

e b

low

n

Ten

ien

te

Ten

ien

te

Au

smel

t Ten

ien

te

-

10

20

30

40

50

60

0 10 20 30 40 50 60 70 80 90 100

Dir

ect

cash

co

st (

c/lb

)

Bath smelting capacity (%)

0

10

20

30

40

50

60

70

0 3 6 9 12 15 18

Dir

ect

cost

(c/

lb)

Anode capacity [Mton]

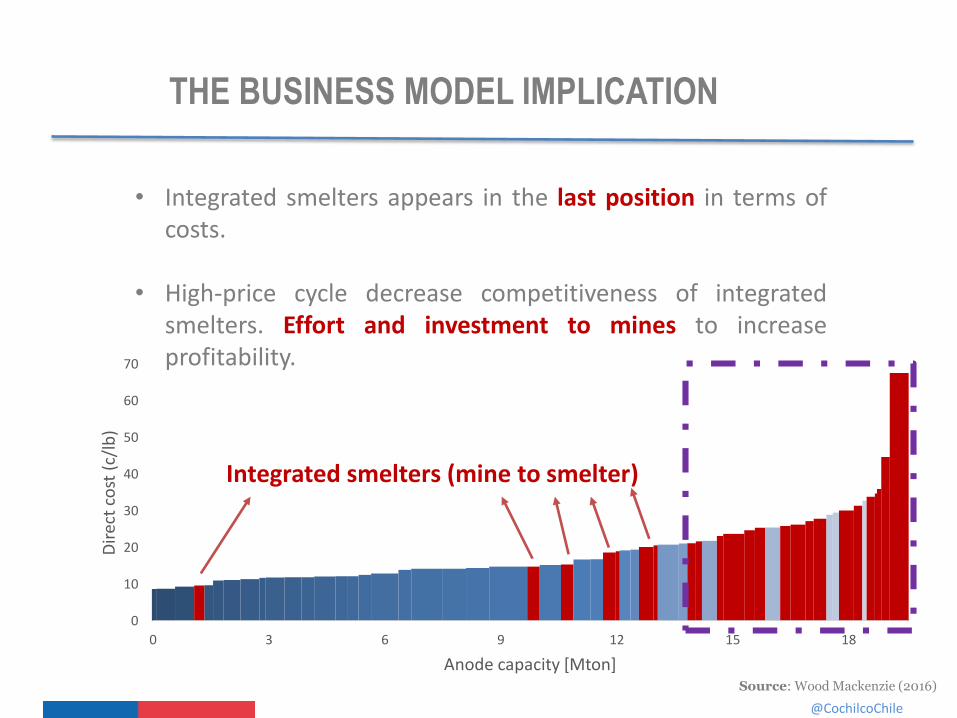

THE BUSINESS MODEL IMPLICATION

@CochilcoChile

• Integrated smelters appears in the last position in terms ofcosts.

• High-price cycle decrease competitiveness of integratedsmelters. Effort and investment to mines to increaseprofitability.

Integrated smelters (mine to smelter)

Source: Wood Mackenzie (2016)

0

2

4

6

8

10

12

14

16

18

20

2015

c/lb

Direct Cash Costs

On-site Services (c/lb)

Consumables (c/lb)

Maintenance (c/lb)

Total Gross Energy (c/lb)

Labour (c/lb)

22%

35%14%

12%

17%

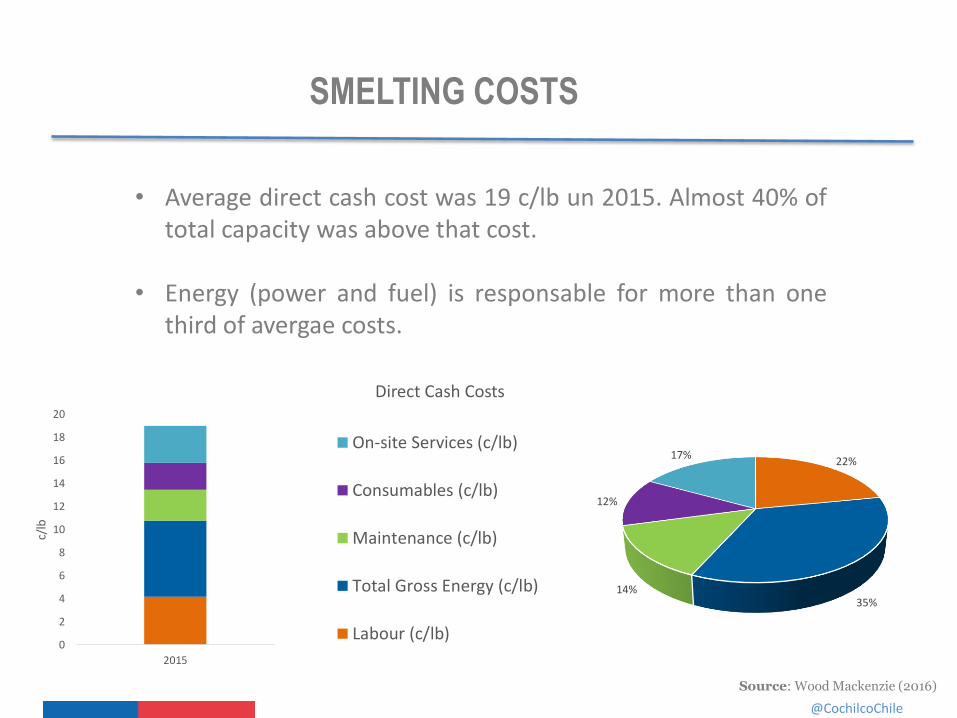

SMELTING COSTS

@CochilcoChile

• Average direct cash cost was 19 c/lb un 2015. Almost 40% oftotal capacity was above that cost.

• Energy (power and fuel) is responsable for more than onethird of avergae costs.

Source: Wood Mackenzie (2016)

COPPER CONCENTRATES MARKET04

COPPER CONCENTRATES MARKET

@CochilcoChile Source: Wood Mackenzie (2015), COCHILCO (2015)

• XXXXXXXXXXXXXX

• XXXXXXXXXXX

COPPER CONCENTRATES MARKET

@CochilcoChile Source: Wood Mackenzie (2015), COCHILCO (2015)

• XXXXXXXXXXXXXX

• XXXXXXXXXXX

COPPER CONCENTRATES MARKET

@CochilcoChile Source: Wood Mackenzie (2015), COCHILCO (2015)

• XXXXXXXXXXXXXX

• XXXXXXXXXXX

COPPER CONCENTRATES MARKET

@CochilcoChile Source: Wood Mackenzie (2015), COCHILCO (2015)

• XXXXXXXXXXXXXX

• XXXXXXXXXXX

CONCLUDING REMARKS05

CONCLUDING REMARKS

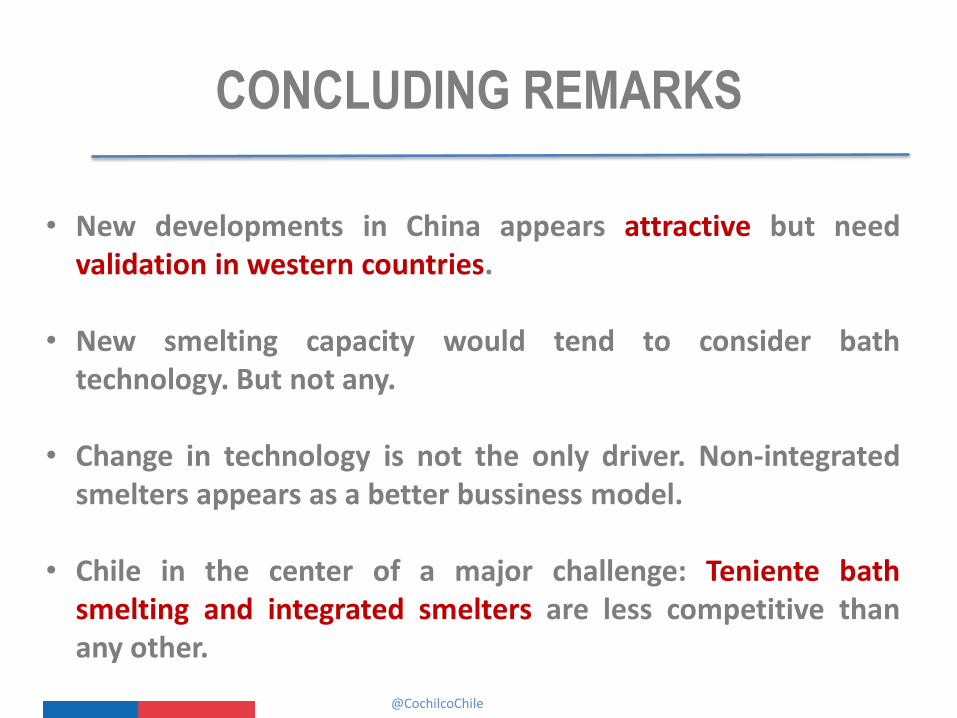

• New developments in China appears attractive but needvalidation in western countries.

• New smelting capacity would tend to consider bathtechnology. But not any.

• Change in technology is not the only driver. Non-integratedsmelters appears as a better bussiness model.

• Chile in the center of a major challenge: Teniente bathsmelting and integrated smelters are less competitive thanany other.

@CochilcoChile

THANK YOU!

www.cochilco.cl

Follow us

@CochilcoChile