copyright 2002, pearson education canada1 monopolistic competition and oligopoly chapter 14

TRANSCRIPT

Copyright 2002, Pearson Education Canada1

Monopolistic Competition and Oligopoly

Chapter 14

Copyright 2002, Pearson Education Canada2

Monopolistic Competition

Monopolistic competition is a common form of industry structure in Canada, characterized by: a large number of firms, none of which can

influence market price by virtue of size alone some degree of market power achieved

through the production of differentiated products

no barriers to entry or exit

Copyright 2002, Pearson Education Canada3

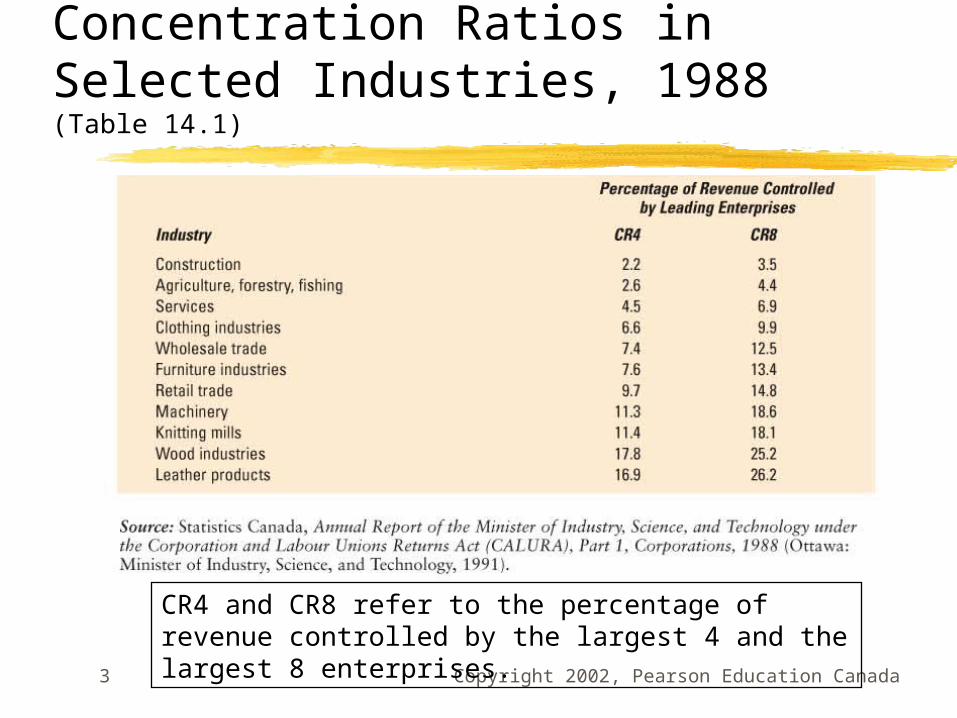

Concentration Ratios in Selected Industries, 1988 (Table 14.1)

CR4 and CR8 refer to the percentage of revenue controlled by the largest 4 and the largest 8 enterprises.

Copyright 2002, Pearson Education Canada4

Product Differentiation

Product differentiation refers to a strategy that firms use to achieve market power.

Achieved by producing products that have distinct positive identities in the minds of consumers

Copyright 2002, Pearson Education Canada5

The Case for Product Differentiation & Advertising

Provides consumers with variety in marketsEnsures that the quality of products remains

highSatisfies a wide range of consumer tastesProvides for product innovationEncourages competition among firms,

providing for efficiencyAdvertising provides information for

consumers

Copyright 2002, Pearson Education Canada6

The Case Against Product Differentiation & Advertising

Society’s scarce resources are wasted as firms attempt to make small changes in products

Information content of advertising is minimal and often misleading

High advertising costs may serve as a barrier to entry in some industries

Advertising imposes costs on society because it is bothersome

Copyright 2002, Pearson Education Canada7

Product Differentiation Reduces the Elasticity of Demand Facing a Firm (Figure 14.1)

Copyright 2002, Pearson Education Canada8

Price / Output Determination in the Short Run

To maximize profit, the monopolistically competitive firm will increase production until the marginal revenue from increasing output and selling it, no longer exceeds the marginal cost of producing it. This occurs at the point where MC = MR.

It is therefore possible for the monopolistically competitive firm to earn short-run profits or suffer short-run losses.

Copyright 2002, Pearson Education Canada9

A Monopolistically Competitive Firm Earning Short-Run Profits (Figure 14.2a)

Copyright 2002, Pearson Education Canada10

A Monopolistically Competitive Firm Suffering Short-Run Losses (Figure 14.2b)

Copyright 2002, Pearson Education Canada11

Monopolistically Competitive Firm at Long-Run Equilibrium (Figure 14.3)

As new firms enter the monopolistically competitive industry the demand curves of profit-making firms begin to shift left.

The process continues until profits are eliminated and the demand curve is just tangent to the average total cost curve.

Copyright 2002, Pearson Education Canada12

Economic Efficiency and Resource Allocation for Monopolistic Competition

Price is greater than marginal cost, greater than the perfectly competitive solution.

The long-run equilibrium quantity of output is to the left of the minimum of ATC.

Copyright 2002, Pearson Education Canada13

Oligopoly

Oligopoly is a form of industry structure characterized by: a few firms, each large enough to influence

market price differentiated or homogeneous products firms behaving in a way that depends to a

great extent on the behaviour of other firms

Copyright 2002, Pearson Education Canada14

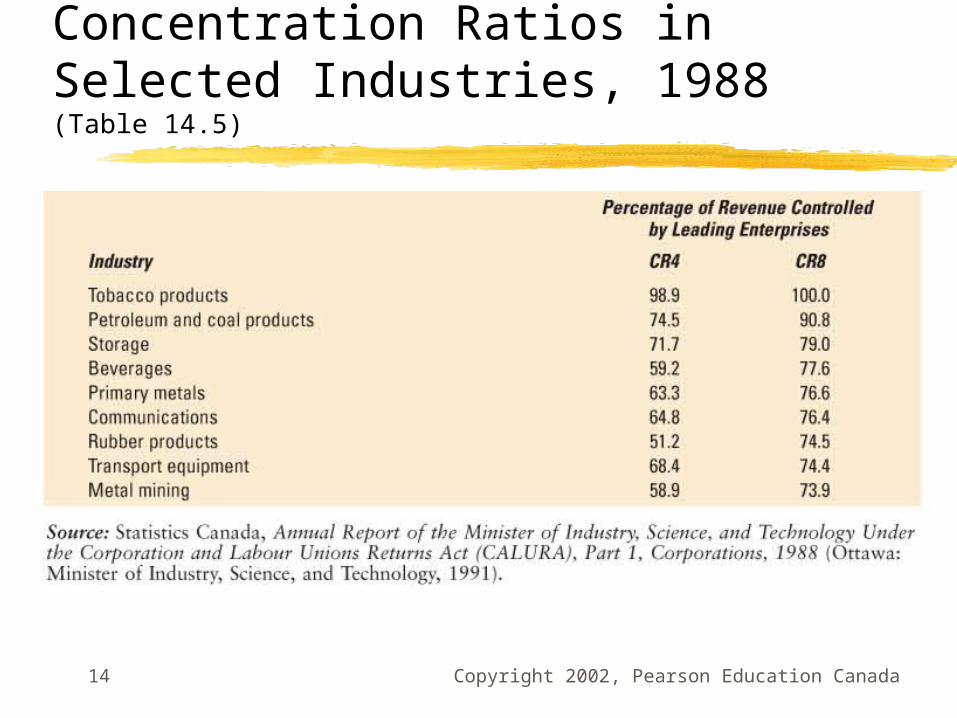

Concentration Ratios in Selected Industries, 1988 (Table 14.5)

Copyright 2002, Pearson Education Canada15

Oligopoly Models

The Collusion ModelThe Cournot ModelThe Kinked Demand ModelThe Price Leadership ModelGame Theoretic Models

Copyright 2002, Pearson Education Canada16

Collusion Model

Cartel refers to a group of firms that gets together and makes joint price and output decisions in order to maximize joint profits.

A modern example is OPEC.Collusion occurs when price and quantity

fixing agreements among producers are explicit.

Tacit collusion occurs when such agreements are implicit.

Copyright 2002, Pearson Education Canada17

Assumptions of the Cournot Model

There are two firms in the industry - a duopoly.

Each firm takes the output of the other firm as given.

Both firms maximize profits.

Copyright 2002, Pearson Education Canada18

Cournot Model

The Cournot Model is model of a two-firm industry (duopoly) in which a series of output adjustment decisions leads to a final level of output that is between that which would prevail if the market were organized competitively and that which would be set by a monopoly.

Copyright 2002, Pearson Education Canada19

The Kinked Demand Curve Model

The kinked demand curve model is a model of oligopoly in which the demand curve facing each individual firm has a kink in it.

The kink follows from the assumption that competitive firms will follow suit if a single firm cuts price, but will not follow suit it a single firm raises price.

Copyright 2002, Pearson Education Canada20

The Kinked Demand Curve Oligopoly Model (Figure 14.4)

If the firm increases its price the demand will fall off quite quickly.

If the firm drops its price the other firms follow and quantity demanded does not change as much.

Demand is elastic above P* and inelastic below P*.

Copyright 2002, Pearson Education Canada21

The Price Leadership Model

The price leadership model is a form of oligopoly in which one dominant firm sets prices and all the smaller firms in the industry follow its pricing policy.

Copyright 2002, Pearson Education Canada22

The Price Leadership Model (Figure 14.5)

The leading firm maximizes profits by assuming that the demand it will face is the total market demand minus the amount supplied by the firms that are expected to follow its leadership.

Copyright 2002, Pearson Education Canada23

Results of the Price Leadership Model

The quantity demanded in the industry is split between the dominant firm and the group of smaller firms.

This division of output is determined by the amount of market power that the dominant firm has.

The dominant firm has an incentive to push smaller firms out of the industry in order to establish a monopoly.

Copyright 2002, Pearson Education Canada24

Game Theory

Game theory analyzes oligopolistic behaviour as a complex series of strategic moves and reactive countermoves among rival firms.

In game theory, firms are assumed to anticipate rival reactions.

Copyright 2002, Pearson Education Canada25

Dominant Strategy and Nash Equilibrium

A dominant strategy in game theory is a strategy that is best no matter what the opposition does.

Nash equilibrium is the result in game theory, when all players play their best strategy given what their competitors are doing.

Copyright 2002, Pearson Education Canada26

Payoff Matrix for an Advertising Game (Figure 14.6)

The dominant strategy for A and B is to advertise.

Copyright 2002, Pearson Education Canada27

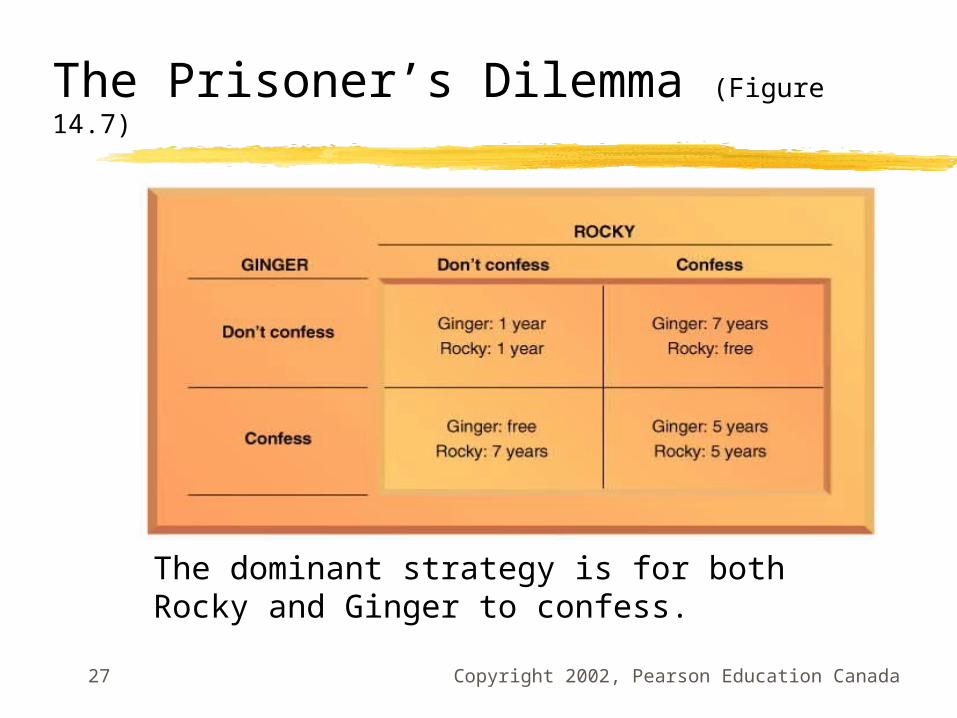

The Prisoner’s Dilemma (Figure 14.7)

The dominant strategy is for both Rocky and Ginger to confess.

Copyright 2002, Pearson Education Canada28

Payoff Matrixes for Left / Right - Top / Bottom Strategies (Figure 14.8a)

In this game C does not have a dominant strategy but D does, right.

Since D’s behaviour is predictable C will play accordingly, in this case bottom.

Copyright 2002, Pearson Education Canada29

Payoff Matrixes for Left / Right - Top / Bottom Strategies (Figure 14.8b)

In this game C does not have a dominant strategy but D does, right.

Since C stands to lose such a large amount, uncertainty and risk will probably cause C to choose top rather than risk bottom, despite knowledge of D’s dominant strategy.

Copyright 2002, Pearson Education Canada30

Maximin Strategy

A maximin strategy in game theory is a strategy chosen to maximize the minimum gain that can be earned.

Copyright 2002, Pearson Education Canada31

Contestable Markets

A market in which entry and exit are costless.

Because entry is cheap, firms are continually faced with competition or the threat of competition.

In contestable markets, firms behave like perfectly competitive firms.

Copyright 2002, Pearson Education Canada32

Oligopoly and Economic Performance

Market concentration leads to pricing above marginal cost and output below the efficient level.

Entry barriers prevent the efficient flow of resources between firms and industries.

Product differentiation may lead to efficiency losses.

Copyright 2002, Pearson Education Canada33

Review Terms & Concepts

cartel cournot model dominant strategy game theory kinked demand curve

model maximin strategy monopolistic

competition

Nash equilibrium oligopoly perfectly contestable

market price leadership product differentiation tacit collusion