copyright © 2003 pearson education, inc.slide 18-1 prepared by shafiq jadallah to accompany...

TRANSCRIPT

Copyright © 2003 Pearson Education, Inc.

Slide 18-1

Prepared by Shafiq Jadallah

To Accompany

Fundamentals of Multinational FinanceFundamentals of Multinational FinanceMichael H. Moffett, Arthur I. Stonehill, David K. Eiteman

Chapter 18Chapter 18Cross-Border Mergers, Acquisitions & Cross-Border Mergers, Acquisitions &

ValuationValuation

Copyright © 2003 Pearson Education, Inc.

Slide 18-2

Chapter 18Cross-Border Mergers,

Acquisitions & Valuation Learning Objectives

• Examine recent trends in cross-border M&A

• Evaluate the motivations for MNEs to pursue cross-border acquisitions

• Identify the driving forces behind the recent surge in cross-border M&A

• Detail the stages in a cross-border acquisition and show how both finance and strategy are intertwined

• Examine the difficulties in settling a cross-border acquisition

Copyright © 2003 Pearson Education, Inc.

Slide 18-3

Chapter 18Cross-Border Mergers,

Acquisitions & Valuation

Learning Objectives• Show how the complexities of post-acquisition

management are related to the creation of value

• Identify the legal and institutional issues regarding corporate governance and shareholder rights as they apply to cross-border acquisitions

• Explain the alternative methods for valuing a potential acquisition target

Copyright © 2003 Pearson Education, Inc.

Slide 18-4

Historical Cross-BorderM&A Activity

0

100

200

300

400

500

600

1995 1996 1997 1998 1999 2000

European Union United States Japan Other

Cross-Border Mergers & Acquisitions: Developed Countries (billions of US dollars)

Copyright © 2003 Pearson Education, Inc.

Slide 18-5

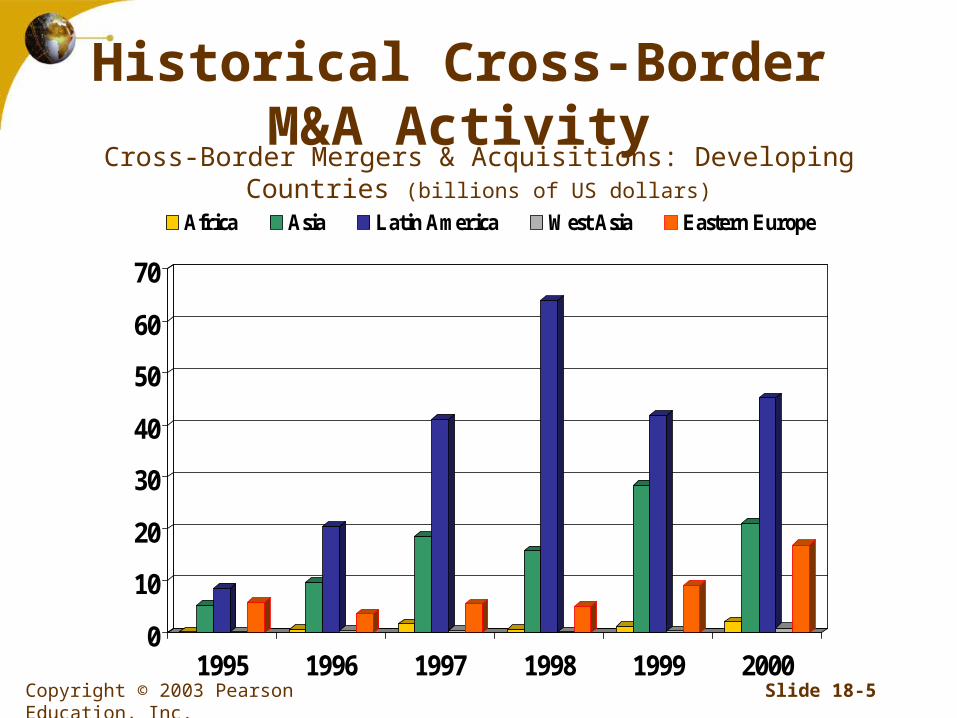

Historical Cross-BorderM&A Activity

0

10

20

30

40

50

60

70

1995 1996 1997 1998 1999 2000

Africa Asia Latin America West Asia Eastern Europe

Cross-Border Mergers & Acquisitions: Developing Countries (billions of US dollars)

Copyright © 2003 Pearson Education, Inc.

Slide 18-6

The Driving Force forCross-Border M&A

The main reason for cross-border M&A is to create shareholder value

Public firms’ measure of enhancing shareholder is mainly reflected in their stock price• If the MNE’s share price is a combination of earnings

and the market’s opinion of those earnings, the price to earnings multiple, then management should strive to grow both

Copyright © 2003 Pearson Education, Inc.

Slide 18-7

The Driving Force forCross-Border M&A

Price = EPS PE

Management, directlycontrols through its

efforts the earnings pershare of the firm.

Management onlyindirectly influencesthe market’s opinion

of the company’s earningsas reflected in the P/E.

Increasing the shareprice means

increasing earnings.

The Goal: Increase the share price of the firm

So building “value” means growing the firm to grow earnings.The largest growth potential is global.

Copyright © 2003 Pearson Education, Inc.

Slide 18-8

Cross-Border M&A Drivers

Aside from the desire to grow, MNEs are motivated to undertake M&A activity for other factors

These drivers are usually both macro in scope, the global competitive environment, and micro in scope, the variety of industry and firm-level forces and actions driving firm value• The primary forces of change in the global competitive

environment are technological change, regulatory change, and capital market change

Copyright © 2003 Pearson Education, Inc.

Slide 18-9

Cross-Border M&A Drivers

Other cross-border M&A drivers are To gain access to strategic proprietary assets To gain market power and dominance To achieve synergies in local/global operations across

different industries To become larger and realize benefits of size in

competition and negotiation To diversify and spread risks To exploit financial opportunities

Copyright © 2003 Pearson Education, Inc.

Slide 18-10

Cross-Border M&A Drivers

Cross - BorderM & A activity

timeSource: UNCTAD, World Development Report 2000: Cross-border Mergers and Acquisitions and Development ,figure V.1., p. 154.

Firms Undertake M&As to:Firms Undertake M&As to:• Access strategic proprietary assets• Gain market power & dominance • Achieve synergies• Become larger• Diversify & spread risks• Exploit financial opportunities

Strategic responses by firmsStrategic responses by firmsto defend and enhance theirto defend and enhance theircompetitive positions in acompetitive positions in achanging environment.changing environment.

Changes in the Global EnvironmentChanges in the Global Environment

• Technology• Regulatory frameworks • Capital market changes

New businessopportunities

and risks

Copyright © 2003 Pearson Education, Inc.

Slide 18-11

Cross-Border M&A Process

Although most M&A is viewed solely as a process of valuation, there is much more such as the strategic drivers, which must also be taken into account

The process of acquiring an enterprise has three common elements• Identification and valuation of the target

• Completion of the ownership change transaction

• Management of the post-acquisition transition

Copyright © 2003 Pearson Education, Inc.

Slide 18-12

Cross-Border M&A Process

Identification& valuationof the target

Valuation&

negotiation

Management ofthe post-acquisition

transition; integrationof businessand culture

Rationalization ofoperations;

integration offinancial goals;

achieving synergies

Completion ofthe ownership

changetransaction(the tender)

Financialsettlement

&compensation

Strategy&

Management

FinancialAnalysis &

Strategy

Stage IIIStage IIIStage IIStage IIStage IStage I

Copyright © 2003 Pearson Education, Inc.

Slide 18-13

Cross-Border M&A Process

Stage 1: Identification and Valuation• This requires a well defined corporate strategy and

focus

• Identification of the target market typically precedes the identification of the target firm

• Valuation comes after identification has taken place– A variety of techniques can be used

– DCF, multiples, comparables, etc.

Copyright © 2003 Pearson Education, Inc.

Slide 18-14

Cross-Border M&A Process Stage 2: Settlement of the Transaction

• This stage includes the approval process from management to governments to regulatory bodies

• Tender process is gaining the approval of the target company; if no approval is obtained then acquisition could become a hostile takeover

• Regulatory approval is important for anti-monopolistic threats and perceptions

– Example: GE and Honeywell being rejected by EUCompensation settlement is the last act in stage two which is the payment to the target’s shareholders

• Payment can be in forms from cash to common stock

Copyright © 2003 Pearson Education, Inc.

Slide 18-15

Cross-Border M&A Process

Stage 3: Post-acquisition Management• This stage can affect the valuation of the entire deal if

the synergies are not met or the costs of integration become higher than anticipated

• The melding of the two cultures is often the biggest challenge

– Examples: BP and Amoco, Daimler and Chrysler

Copyright © 2003 Pearson Education, Inc.

Slide 18-16

Corporate Governance &Shareholder Rights

The Tender and shareholder rights• One issue of contention is the discussion of

determining at what point in the accumulation of shares the bidder is required to make all shareholders a tender offer

• Theoretically the accumulation of shares should continue until the bidder has

– The single largest block of shares among shareholders

– Majority control

– All the shares outright

Copyright © 2003 Pearson Education, Inc.

Slide 18-17

Corporate Governance &Shareholder Rights

The Tender and shareholder rights• The issue of corporate control is regulated by varying countries

differently but typically include the following

• Creeping tenders – the secret accumulation of small blocks of shares in the private or public market in a preliminary move towards a public bid. This is prohibited in many countries for the purpose of promoting disclosure of bids for takeover

• Mandatory offers – many countries require that the bidder make a public tender to all shareholders when a certain threshold of ownership is attained. This is intended to extend the opportunity to all shareholders to sell their shares at the tender price rather than have the bidder pay the tender price only to those shareholders needed to gain control

Copyright © 2003 Pearson Education, Inc.

Slide 18-18

Corporate Governance &Shareholder Rights

The Tender and shareholder rights• Timing of takeovers – different time frames apply to takeover bids

but typically this time period is the time the bid must be left open for each individual tender offer, withdrawal or revision tender. This allows bidders and targets to consider all possibilities

• Withdrawal rights – most countries allow any security to be withdrawn as long as bid is open. This protects shareholders against tendering their shares early at lower prices than may be garnered by waiting for a better offer

• Market prices during bid – some countries allow the bidder to purchase shares in the open market during the public tender. Other countries prohibit this to protect against any potential market manipulation

Copyright © 2003 Pearson Education, Inc.

Slide 18-19

Corporate Governance &Shareholder Rights

The Tender and shareholder rights• Market sales during bid – this follows the previous regulator point

mentioned

• Limitation of defenses – some countries limit the defensive tactics of the target; in some countries this is not an explicit law but one implied through civil trials. This protects shareholders against management taking defensive measures not in their best interests

• Price integration – most countries require that the highest price paid to any shareholder be paid to all shareholders tendering their shares. This is intended to guarantee equitable price offerings yet sometimes becomes two-tiered in countries that allow front-end and back-end bids

Copyright © 2003 Pearson Education, Inc.

Slide 18-20

Corporate Governance &Shareholder Rights

The Tender and shareholder rights• Proration of acceptance – most countries require

proration when a bid is made for less than all the shares and more than the maximum is tendered. Some countries don’t allow a bid to be made for less than all the shares once the mandatory offer percentage has been reached

• Target responses – many countries require that the Board of Directors of the target make a public statement regarding their position on the public tender within a time frame following the tender. This is intended to disclose the target’s opinions and attitudes towards the tender to existing shareholders

Copyright © 2003 Pearson Education, Inc.

Slide 18-21

Cross-Border Valuation:Tsingtao Brewery Company

Anheuser-Busch targets Tsingtao Brewery in China• In January 2001, Anheuser-Busch (AB) was considering

acquiring a minority interest in China’s Tsingtao brewery

• AB’s key considerations and questions were– The valuation of Tsingtao’s share price in an illiquid Chinese

equity market

– The percentage of Tsingtao’s total equity that could be purchased

– The terms of settling the transaction

– AB’s prospects of contributing to the management of Tsingtao for a larger equity stake

– The degree of future compatibility between the two cultures

– The potential for future rationalization of operations

Copyright © 2003 Pearson Education, Inc.

Slide 18-22

• Having identified the target (Stage I), AB needed to undertake a valuation of the target (Stage II). Since AB would at best only have a minority interest, it also needed to assess its prospects for post-acquisition influence in Tsingtao’s operations (Stage III)

The challenge and the opportunity• Tsingtao was China’s largest brewer; it operated 43

breweries, 2 malt plants and 49 distributors covering 15 Chinese provinces

• The Chinese beer market was undergoing consolidation due to high competitiveness

Cross-Border Valuation:Tsingtao Brewery Company

Copyright © 2003 Pearson Education, Inc.

Slide 18-23

Cross-Border Valuation:Tsingtao Brewery Company

Copyright © 2003 Pearson Education, Inc.

Slide 18-24

Tsingtao had grown through acquisitions over the past years and was now struggling with post-acquisition integration and digestion from the heavy load used to finance the growth

Cross-Border Valuation:Tsingtao Brewery Company

Copyright © 2003 Pearson Education, Inc.

Slide 18-25

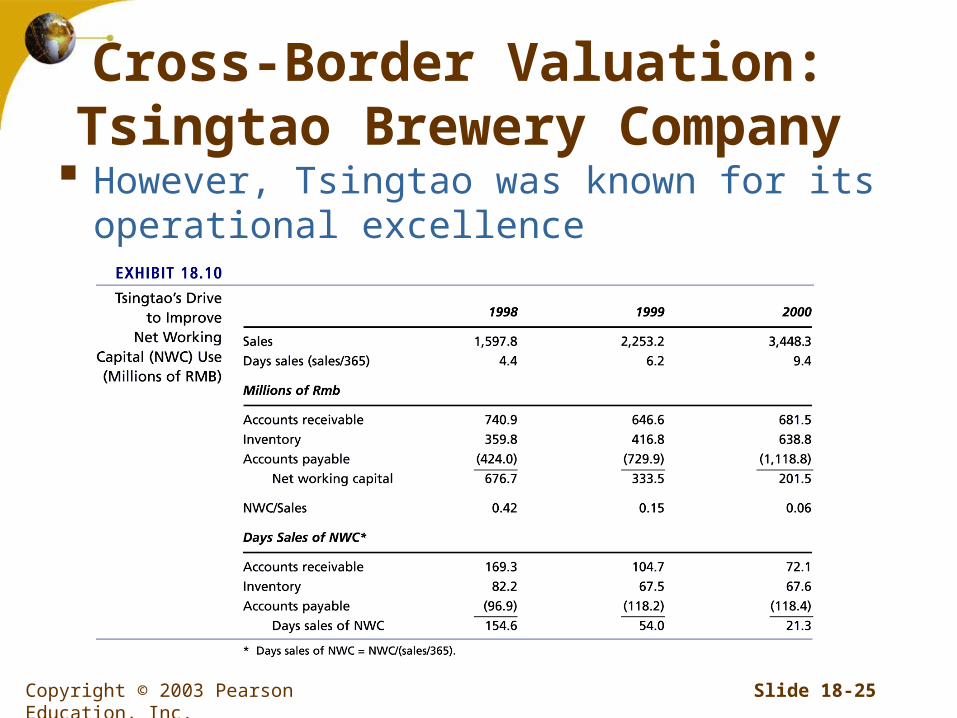

However, Tsingtao was known for its operational excellence

Cross-Border Valuation:Tsingtao Brewery Company

Copyright © 2003 Pearson Education, Inc.

Slide 18-26

Cross-Border Valuation:

Tsingtao Brewery Company

Copyright © 2003 Pearson Education, Inc.

Slide 18-27

Cross-Border Valuation:Tsingtao Brewery Company

Copyright © 2003 Pearson Education, Inc.

Slide 18-28

Cross-Border Valuation:Tsingtao Brewery

Company

Copyright © 2003 Pearson Education, Inc.

Slide 18-29

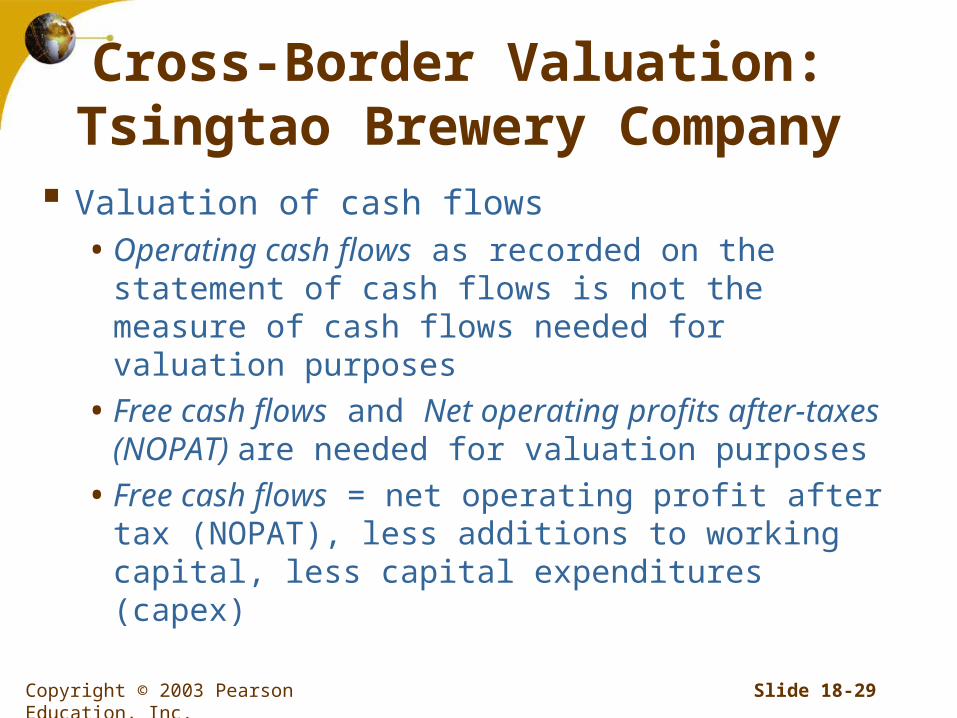

Valuation of cash flows• Operating cash flows as recorded on the statement of

cash flows is not the measure of cash flows needed for valuation purposes

• Free cash flows and Net operating profits after-taxes (NOPAT) are needed for valuation purposes

• Free cash flows = net operating profit after tax (NOPAT), less additions to working capital, less capital expenditures (capex)

Cross-Border Valuation:Tsingtao Brewery Company

Copyright © 2003 Pearson Education, Inc.

Slide 18-30

In 2000, Tsingtao’s NOPAT was a positive Rmb430.9 million

Tsintao’s FCF was equal to:• A NOPAT of 430.9

• Less a reduction in working capital of 133.7

• Less a capital expenditure of 1,330.0,

• For a total of negative Rmb765.4 million

Cross-Border Valuation:Tsingtao Brewery Company

Copyright © 2003 Pearson Education, Inc.

Slide 18-31

Tsingtao’s DCF valuation requires three critical components for proper calculation

The three critical components for the valuation are• Expected future free cash flows

• Terminal value

• Risk-adjusted discount rate

Cross-Border Valuation:Tsingtao Brewery Company

Copyright © 2003 Pearson Education, Inc.

Slide 18-32

Terminal value is critical for DCF analysis because it must capture all the FCF’s for an indefinite future

Typically terminal value is calculated using a dividend growth model formula• Here we assume a discount rate (k) of 10%

• and a FCF growth rate (g) of 2%

Rmb7,539.602.010.0

)02.1(3.591Rmb

gk

g)1(FCF valueTerminal

WACC

2000

Cross-Border Valuation:Tsingtao Brewery Company

Copyright © 2003 Pearson Education, Inc.

Slide 18-33

The discount rate was calculated using CAPM and the following assumptions• 34% Tax rate

• Pre-tax cost of debt of 8% (after-tax cost of 5.28%)

• Risk free rate of 7%

• Equity risk premium of 6.7%

• Tsingtao’s H-shares beta of 0.80

• Hong Kong stock exchange return of 13.7%

%36.12)0.77.13(80.00.7)kk(kk fmrfe

10.0%%)(.333x5.28 x12.36%)667(.k x t)-(1 x V

Dk x

V

Ek deWACC

Cross-Border Valuation:Tsingtao Brewery Company

Copyright © 2003 Pearson Education, Inc.

Slide 18-34

Cross-Border Valuation:Tsingtao Brewery

Company

Copyright © 2003 Pearson Education, Inc.

Slide 18-35

Valuation using multiples• Multiples such as P/E or Market-to-book can be used

as well to compare the valuation of the target

• P/E ratios are the most widely used for valuation

• Tsingtao’s valuation using P/E ratios would be

4.34HK$0.064

HK$2.20

HK$in 2000for EPS

HK$in priceCurrent P/E

Cross-Border Valuation:Tsingtao Brewery Company

• Tsingtao’s 34.4 earnings is considerably higher than the Hong Kong exchange’s average of 12

Copyright © 2003 Pearson Education, Inc.

Slide 18-36

• The second most widely used multiple is the Market-to-book (MTB) ratio

• This is the measure of the firm’s book value per share relative to its market price; or the market’s assessment of the employed capital versus what the capital cost

• Tsingtao's MBT ratio would be

94.0HK$2.35

HK$2.20

HK$in shareper Book value

HK$in priceCurrent MTB

Cross-Border Valuation:Tsingtao Brewery Company

• According to this, Tsingtao is selling for less than its historical cost of capital invested

Copyright © 2003 Pearson Education, Inc.

Slide 18-37

Cross-Border Valuation:Tsingtao Brewery Company

Copyright © 2003 Pearson Education, Inc.

Slide 18-38

Summary of Learning Objectives The number and dollar value of cross-border mergers and

acquisitions has grown rapidly in recent years, but the growth and magnitude of activity is taking place in developed countries, not developing countries

As opposed to fighting for market share, the global marketplace offers greater growth potential. There are a variety of ways for an MNE to enter foreign markets including Greenfield investments and acquisitions

The drivers of M&A activity are both macro in scope, the global competitive market, and micro in scope, the variety of industry and firm-level forces and actions driving individual firm value

Copyright © 2003 Pearson Education, Inc.

Slide 18-39

Summary of Learning Objectives The primary forces of change in the global competitive market

are technological change, regulatory change, and capital market change – these create new opportunities for MNEs

The process of acquiring an enterprise has three common elements, (1) identification and valuation of the target, (2) completion of the ownership change transaction and (3) the management of post-acquisition transition

The settlement stage of a cross-border acquisition requires gaining the approval of management, shareholders and regulators

Cross-border acquisitions, mergers and alliances all face similar challenges: they must value the target on the basis of its projected performance. This process of target valuation combines elements of strategy, finance, and management

Copyright © 2003 Pearson Education, Inc.

Slide 18-40

Summary of Learning Objectives One of the most controversial issues in shareholder rights is at

what point in the accumulation of share is the bidder required to make all shareholders a tender offer. Theoretically this share accumulation could continue until the bidder had (1) the single largest block of shares, (2) majority control, or (3) all shares outright

Every country possesses a different set of regulations for the transfer of control of publicly traded companies. This market, the market for corporate control, has been the subject of debate in recent years

Copyright © 2003 Pearson Education, Inc.

Slide 18-41

Summary of Learning Objectives There are a variety of valuation techniques widely used in global

business each with its relative merits. In addition to the fundamental methodologies of DCF and multiples, there are also a variety of industry specific measures

The DCF approach calculates the value of the enterprise as the PV of all future free cash flows less the cash flows due to creditors and minority interest holders

The P/E ratio is an indication of what the market is willing to pay for a currency unit of earnings and how secure the market’s perception is about the future earnings of the firm

The MBT ratio is a method of valuing the firm on the basis of what the market believes the firm is worth over and above its capital and original investment and subsequent retained earnings