copyright 2003 prentice hall publishing1 chapter 4 chapter 4 keeping the books: the mechanics of an...

TRANSCRIPT

Copyright 2003 Prentice Hall Publishing

1

Chapter 4 Chapter 4

Keeping the Books: Keeping the Books:

The Mechanics of an The Mechanics of an Accounting SystemAccounting System

Copyright 2003 Prentice Hall Publishing

2

The Traditional Way to The Traditional Way to Keep the Books:Keep the Books:The General Ledger SystemThe General Ledger System

THE ACCOUNTING CYCLE: Transactions occur in the normal course of

business. We record them in our records with a JOURNAL ENTRY.

Journal entries are posted to the GENERAL LEDGER.

ADJUSTING ENTRIES are made and posted.

Transactions

Financial Statements

Copyright 2003 Prentice Hall Publishing

3

Accounting cycle continued...Accounting cycle continued...

A trial balance can be prepared at any time to make sure we haven’t made an error with the debit-credit part of the accounting system. More about that after we learn the nuts and bolts about DEBITS and CREDITS...

Financial statements are written. Closing journal entries are made and

posted (and a post-closing trial balance

may be prepared).

Copyright 2003 Prentice Hall Publishing

4

TerminologyTerminology

What’s a general ledger? A big book of accounting records in which

every page is an “account.” What’s an account?

A page in the general ledger that is devoted to keeping track of an individual asset or liability or type of owners’ equity.

How many are there? As many as the business find necessary for its record keeping.

Copyright 2003 Prentice Hall Publishing

5

Accounts…debits and creditsAccounts…debits and credits

Each account can be increased or decreased.

For example, CASH can be increased (when it is collected) and decreased (when it is disbursed).

Each item on the balance sheet is either an account or a composite of several accounts.

Copyright 2003 Prentice Hall Publishing

6

How this debit/credit stuff works:How this debit/credit stuff works:DEBITDEBIT means means LEFTLEFT side sideCREDITCREDIT means means RIGHTRIGHT side side

We can represent an account with a TT, where one side is the place where we put the increasesand the other side is for decreases.

The left side is always called the debit side.When we put something on the left side of an account, we are debiting the account.The right side is always called the credit side. When we put something on the right side of an account,we are crediting the account.

Copyright 2003 Prentice Hall Publishing

7

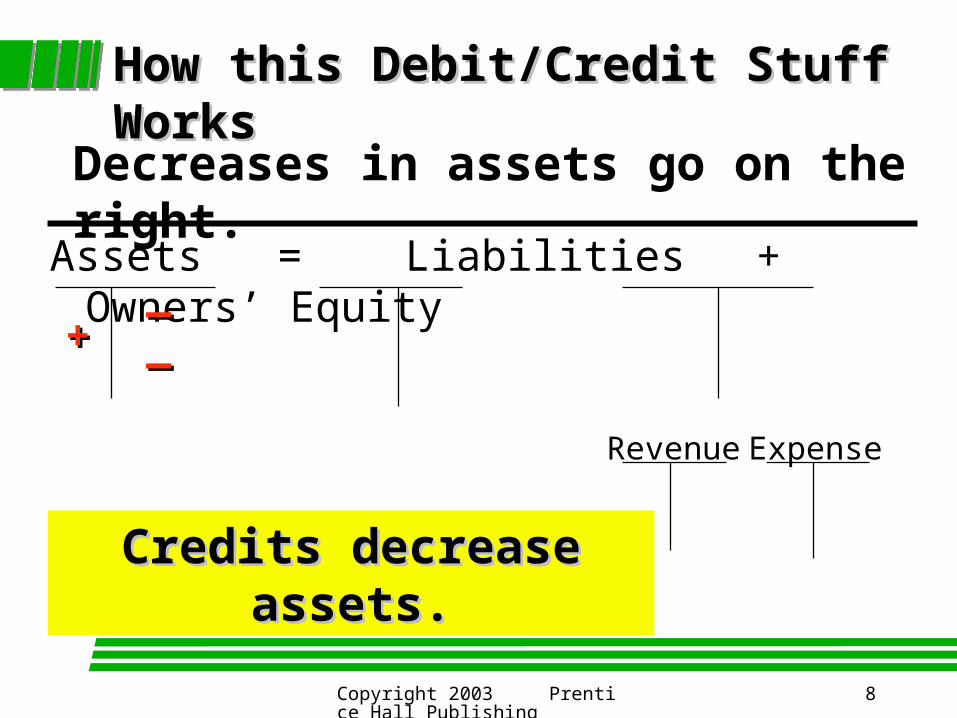

How this Debit/Credit Stuff WorksHow this Debit/Credit Stuff Works

Assets= Liabilities + Owners’ Equity

Revenue Expense

++

Increases in assets go on the left.

Debits increase assetsDebits increase assets..

Copyright 2003 Prentice Hall Publishing

8

Assets= Liabilities + Owners’ Equity

Revenue Expense

++ ____

How this Debit/Credit Stuff WorksHow this Debit/Credit Stuff Works

Decreases in assets go on the right.

Credits decrease assets.Credits decrease assets.

Copyright 2003 Prentice Hall Publishing

9

Assets= Liabilities + Owners’ Equity

Revenue Expense

++ ____

How this Debit/Credit Stuff WorksHow this Debit/Credit Stuff Works

Increases in liabilities go on the right.

Credits increase liabilities.Credits increase liabilities.

++

Copyright 2003 Prentice Hall Publishing

10

Assets= Liabilities + Owners’ Equity

Revenue Expense

++ ____

How this Debit/Credit Stuff WorksHow this Debit/Credit Stuff Works

Decreases in liabilities go on the left

Debits decrease liabilities.Debits decrease liabilities.

++____

Copyright 2003 Prentice Hall Publishing

11

Owner’s Equity AccountsOwner’s Equity Accounts

Contributed Capital and Retained Contributed Capital and Retained Earnings) are increased with credits and Earnings) are increased with credits and decreased with debits.decreased with debits.

Assets= Liabilities + Owners’ Equity

Revenue Expense++ __

++__ ++____

Copyright 2003 Prentice Hall Publishing

12

Revenue and Expense AccountsRevenue and Expense Accounts

Revenue and expense accounts are Revenue and expense accounts are not considered “owners’ equity” not considered “owners’ equity” accounts--even though they accounts--even though they effectively increase or decrease effectively increase or decrease equity!equity!

They are called They are called income statement income statement accounts,accounts, often called temporary or often called temporary or nominal accounts.nominal accounts.

Copyright 2003 Prentice Hall Publishing

13

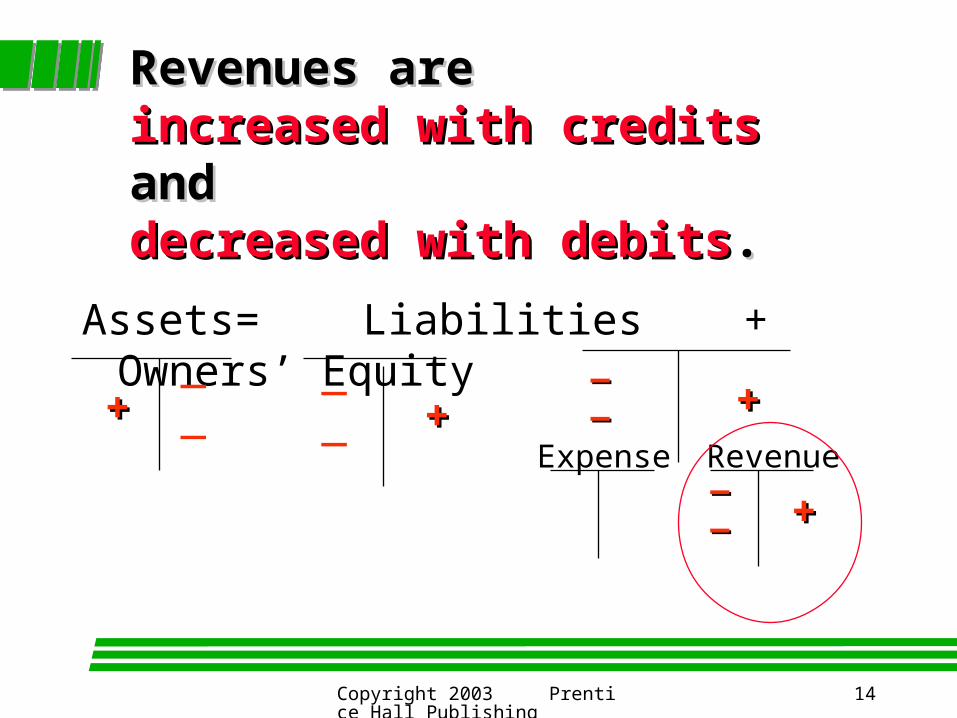

Revenue AccountsRevenue Accounts

An increase in a revenue causes an An increase in a revenue causes an increase in owners’ equity--so the increase in owners’ equity--so the debits and credits will be the same debits and credits will be the same for revenue accounts as they are for for revenue accounts as they are for owners’ equity:owners’ equity: Credits increase Credits increase revenue accounts and debits revenue accounts and debits decrease revenue accounts.decrease revenue accounts.

Revenue accounts keep track of all the Revenue accounts keep track of all the company’s earnings from sales and services.company’s earnings from sales and services.

Copyright 2003 Prentice Hall Publishing

14

Revenues are Revenues are increased with creditsincreased with credits and and decreased with debitsdecreased with debits..

Assets= Liabilities + Owners’ Equity

Revenue Expense++ __

++__ ++____

++____

Copyright 2003 Prentice Hall Publishing

15

Expenses reduce owners’ equity, so Expenses reduce owners’ equity, so the debits and credits are opposite of the debits and credits are opposite of those for the OE accounts:those for the OE accounts:debits increase expenses, debits increase expenses, credits decrease expenses.credits decrease expenses.

Assets= Liabilities + Owners’ Equity

Revenue Expense++ __

++__ ++____

++ ++________

Copyright 2003 Prentice Hall Publishing

16

SUMMARY:SUMMARY:DOUBLE-ENTRY ACCOUNTINGDOUBLE-ENTRY ACCOUNTING

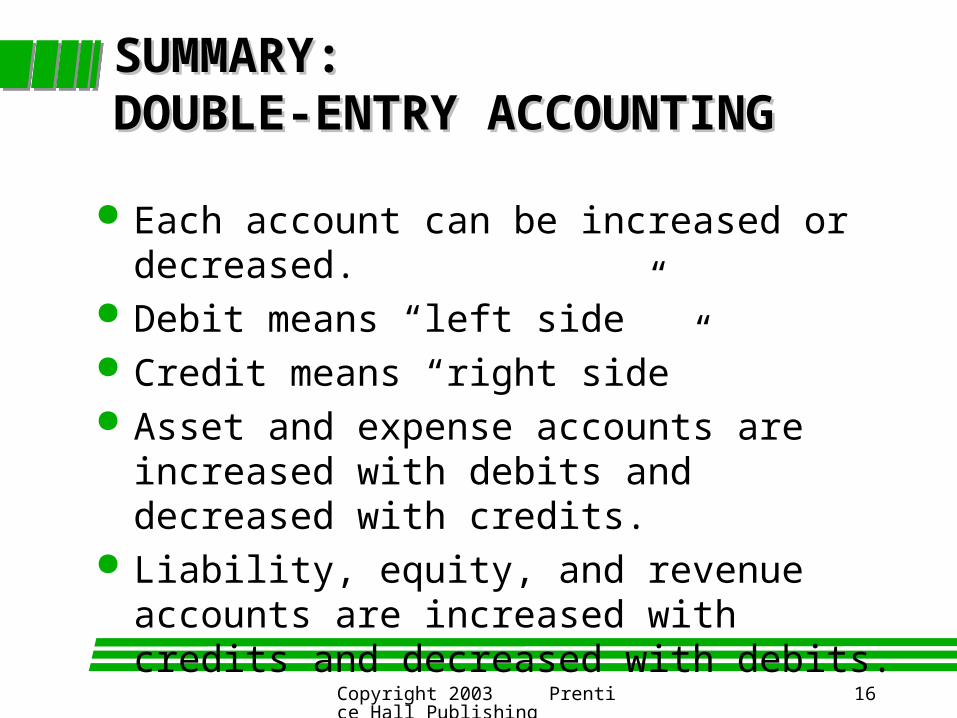

Each account can be increased or decreased. Debit means “left side” Credit means “right side” Asset and expense accounts are increased

with debits and decreased with credits. Liability, equity, and revenue accounts are

increased with credits and decreased with debits.

Copyright 2003 Prentice Hall Publishing

17

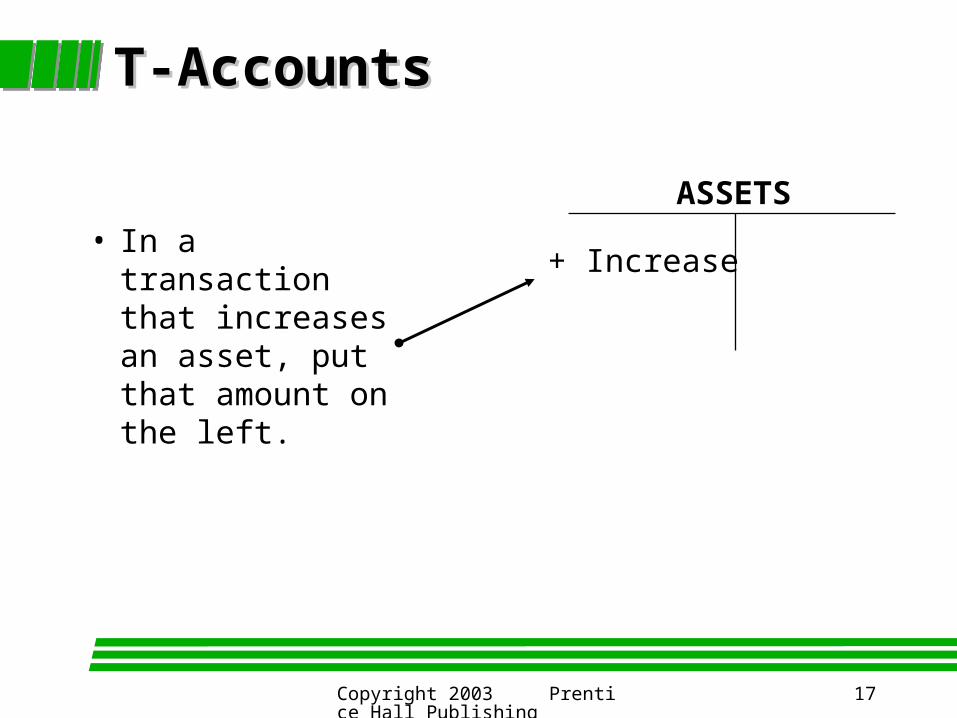

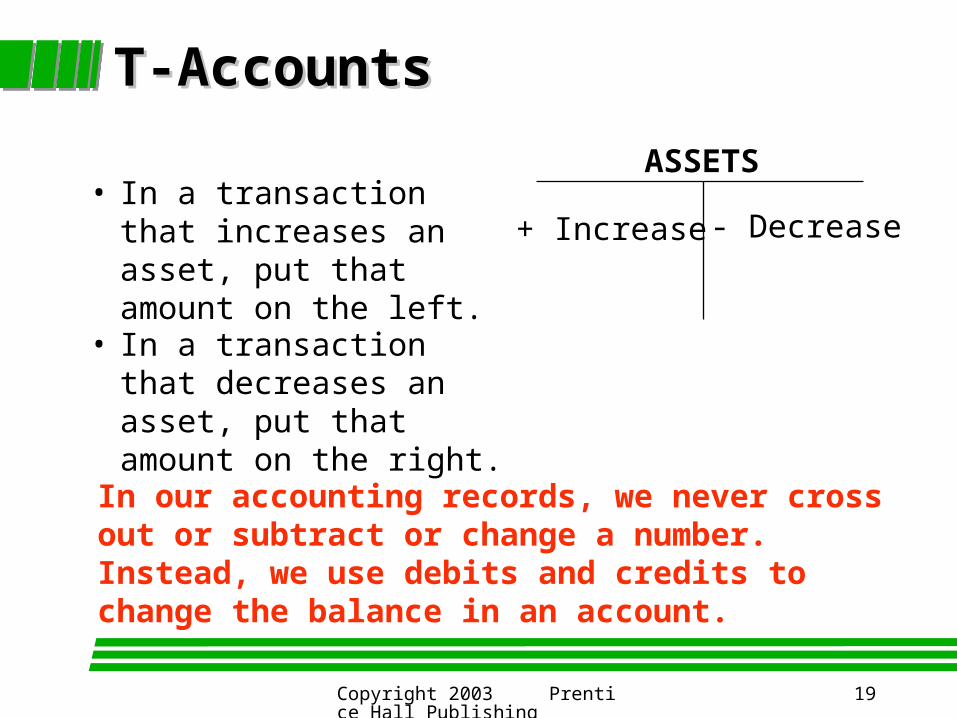

T-AccountsT-Accounts

+ Increase

ASSETS • In a transaction that

increases an asset, put that amount on the left.

Copyright 2003 Prentice Hall Publishing

18

T-AccountsT-Accounts

+ Increase

ASSETS

- Decrease

• In a transaction that increases an asset, put that amount on the left.

• In a transaction that decreases an asset, put that amount on the right.

Copyright 2003 Prentice Hall Publishing

19

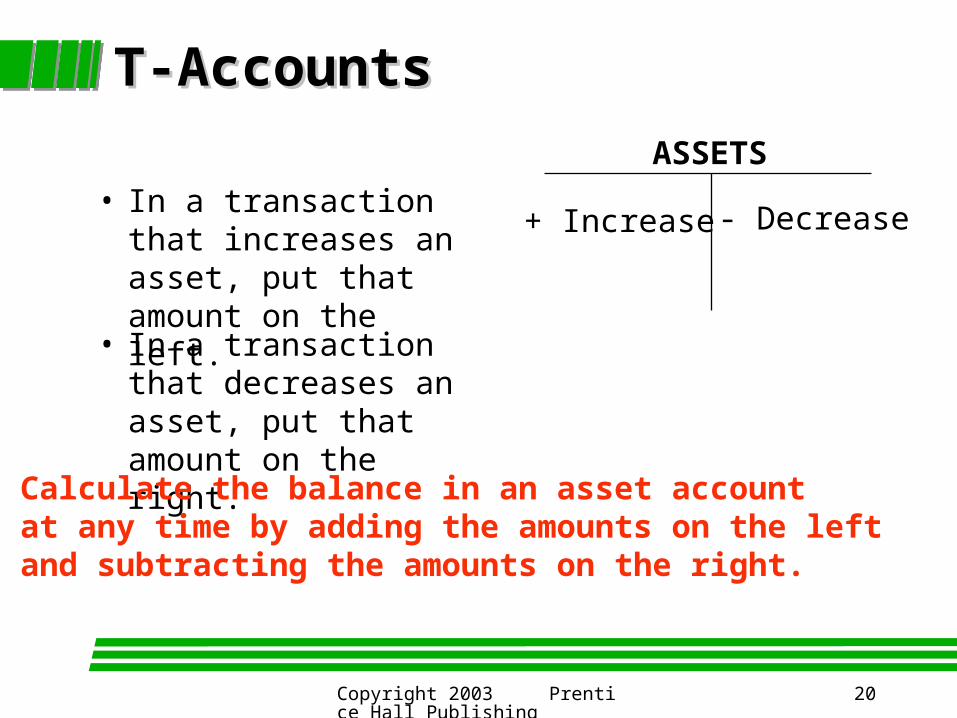

T-AccountsT-Accounts

+ Increase

ASSETS

- Decrease • In a transaction that

increases an asset, put that amount on the left.

• In a transaction that decreases an asset, put that amount on the right.

In our accounting records, we never cross out or subtract or change a number. Instead, we use debits and credits to change the balance in an account.

Copyright 2003 Prentice Hall Publishing

20

T-AccountsT-Accounts

+ Increase

ASSETS

- Decrease • In a transaction that

increases an asset, put that amount on the left.

• In a transaction that decreases an asset, put that amount on the right.

Calculate the balance in an asset accountat any time by adding the amounts on the left and subtracting the amounts on the right.

Copyright 2003 Prentice Hall Publishing

21

T-Accounts: AssetsT-Accounts: Assets

CASHCASH

debitsincreaseassets

e.g., when we receive cash, we debit the CASH account

DEBITS

on the

left!!

Copyright 2003 Prentice Hall Publishing

22

T-Accounts: AssetsT-Accounts: Assets

CASHCASH

debitsIncrease assets

creditsdecreaseassets

e.g., when wereceive cash,we debit the CASH account

Credits

on the

right!!

e.g., when we disburse cash, we credit theCASH account

Copyright 2003 Prentice Hall Publishing

23

T-Accounts: Liabilities and EquityT-Accounts: Liabilities and Equity

Accounts PayableAccounts Payable

debits liabilities

credits liabilities

e.g., when we pay off some of our accounts payable

Credits

on the

right!!

Debits

on the

left!!

e.g., when we record an amount we owe someone

24Copyright 2003 Prentice Hall Publishing

T-AccountsT-Accounts

LIABILITIES

+ Increase-Decrease EQUITY

-Decrease + Increase

Additions to theseaccounts are put on the right.

Deductions from theseaccounts are put on the left.

Equity accounts work like liability accounts:

Copyright 2003 Prentice Hall Publishing

25

What about What about Revenue and Expense Accounts?Revenue and Expense Accounts?

Since revenuesrevenues increase owners’ equity, they are increased with credits---just like owners’ equity accounts.

Service Revenue

+

Revenue accountsare rarely debited..

Copyright 2003 Prentice Hall Publishing

26

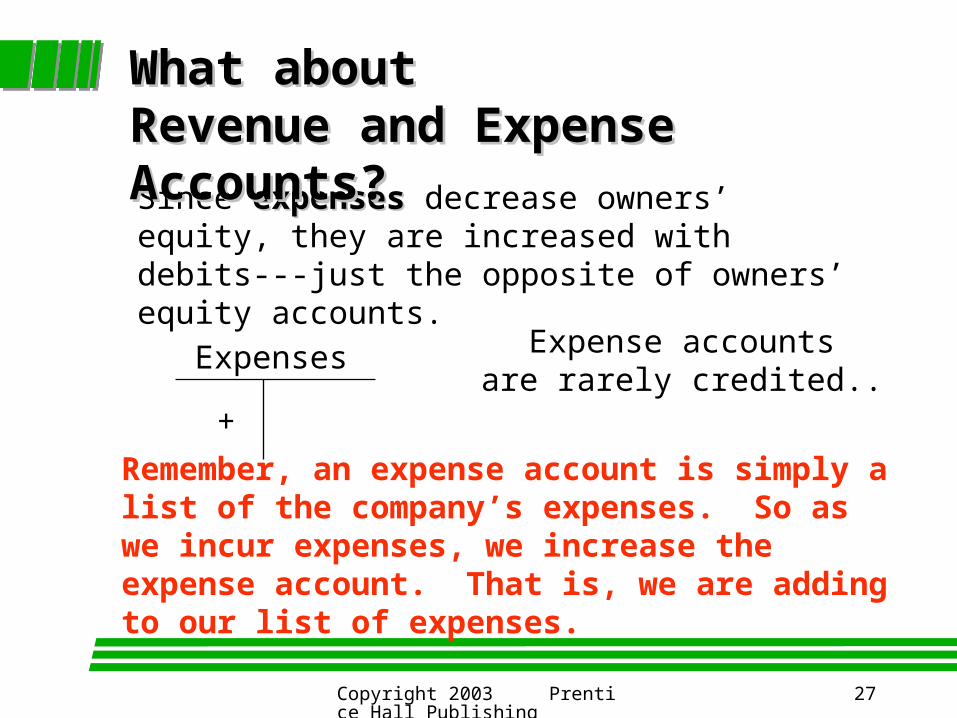

Since expensesexpenses decrease owners’ equity, they are increased with debits---just the opposite of owners’ equity accounts.

Expenses

+

Expense accountsare rarely credited.

What about What about Revenue and Expense Accounts?Revenue and Expense Accounts?

Copyright 2003 Prentice Hall Publishing

27

Since expensesexpenses decrease owners’ equity, they are increased with debits---just the opposite of owners’ equity accounts.

Expenses

+

Expense accountsare rarely credited..

Remember, an expense account is simply a list of the company’s expenses. So as we incur expenses, we increase the expense account. That is, we are adding to our list of expenses.

What about What about Revenue and Expense Accounts?Revenue and Expense Accounts?

Copyright 2003 Prentice Hall Publishing

28

What is a journal and a journal entry?What is a journal and a journal entry?

A journal is a book where a chronological record of transactions is recorded.

Only basic information is contained in the journal.

A “journal entry” is just a recorded transaction. Because of the design of the debit/credit

system to go with the accounting equation, in every journal entry there are equal dollar amounts of debits and credits.

Copyright 2003 Prentice Hall Publishing

29

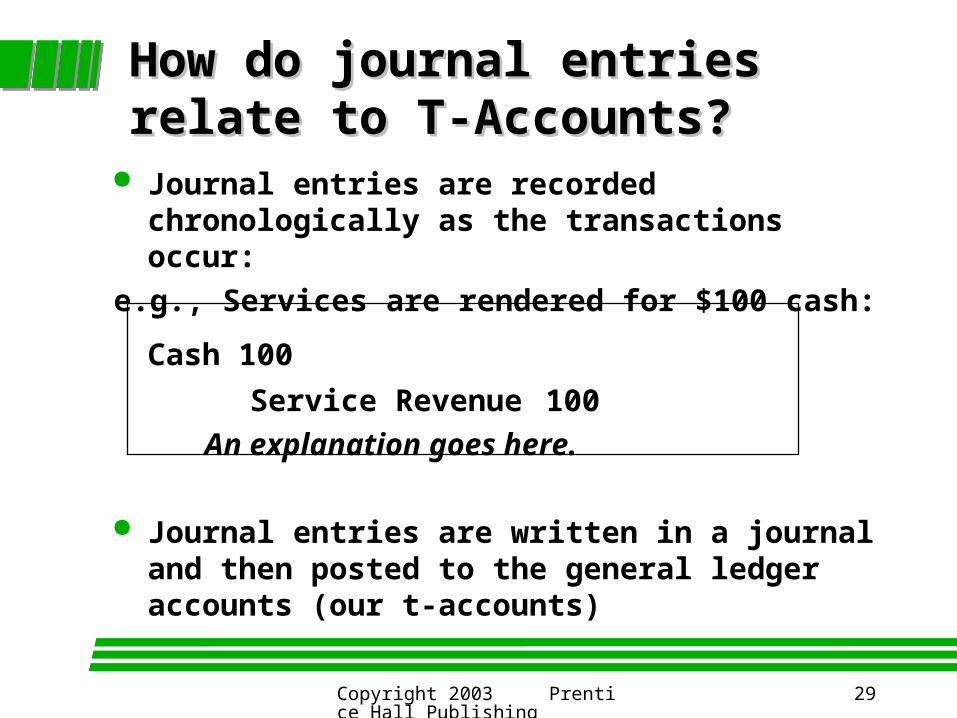

Journal entries are recorded chronologically as the transactions occur:

e.g., Services are rendered for $100 cash:

Cash 100

Service Revenue 100

An explanation goes here.

Journal entries are written in a journal and then posted to the general ledger accounts (our t-accounts)

How do journal entries How do journal entries relate to T-Accounts?relate to T-Accounts?

Copyright 2003 Prentice Hall Publishing

30

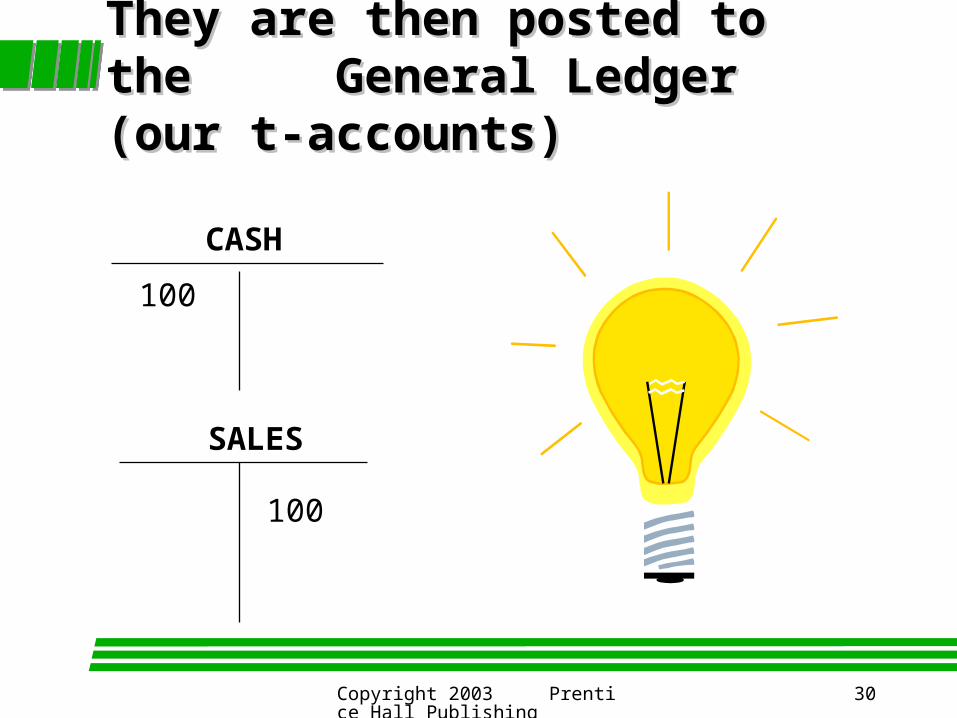

They are then posted to the They are then posted to the General Ledger (our t-accounts)General Ledger (our t-accounts)

CASH

SALES

100

100

Copyright 2003 Prentice Hall Publishing

31

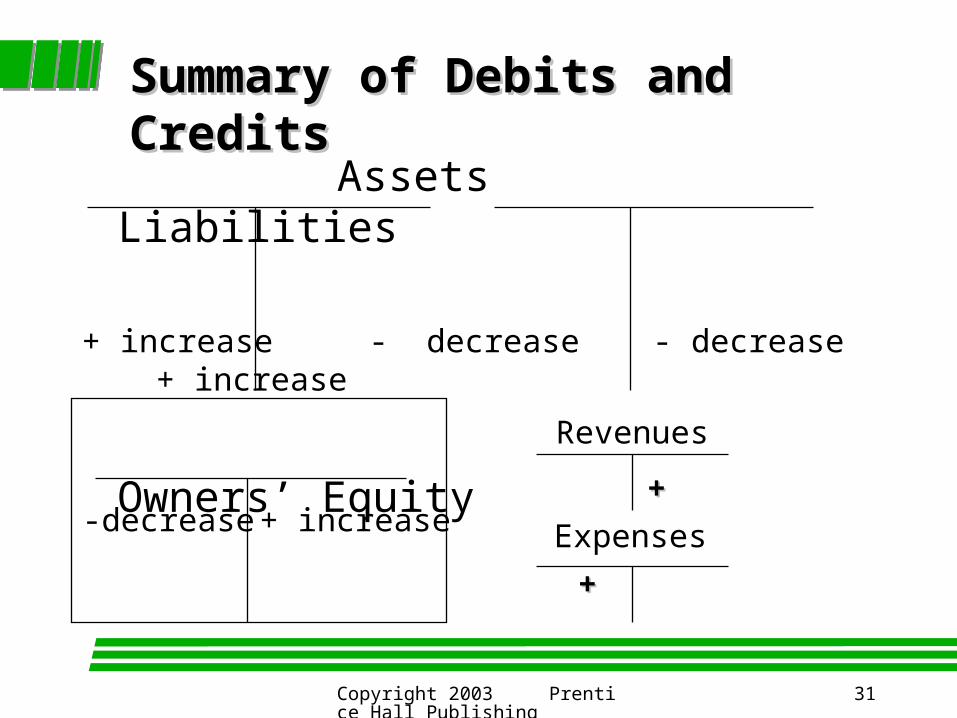

Assets Liabilities

+ increase - decrease - decrease + increase

Owners’ Equity

-decrease + increase

Summary of Debits and CreditsSummary of Debits and Credits

Revenues

Expenses

++

++

Copyright 2003 Prentice Hall Publishing

32

Summary of Journal EntriesSummary of Journal Entries

Assets and Expenses are increased with debits.

Assets include Cash A/R Inventory Supplies Prepaid Rent Equipment

Liabilities and Owners’ Equity and Revenue accounts are increased with credits.

Liabilities include all PAYABLES.

Equity accounts include: Contributed Capital Retained Earnings

Copyright 2003 Prentice Hall Publishing

33

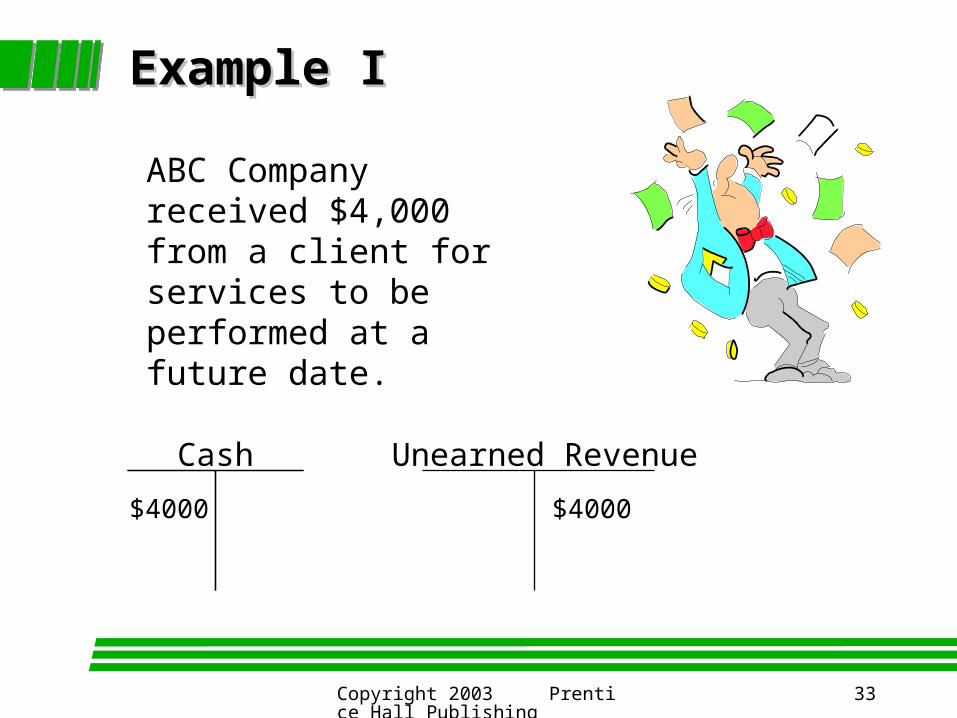

ABC Company received $4,000 from a client for services to be performed at a future date.

Cash Unearned Revenue

Example IExample I

$4000 $4000

Copyright 2003 Prentice Hall Publishing

34

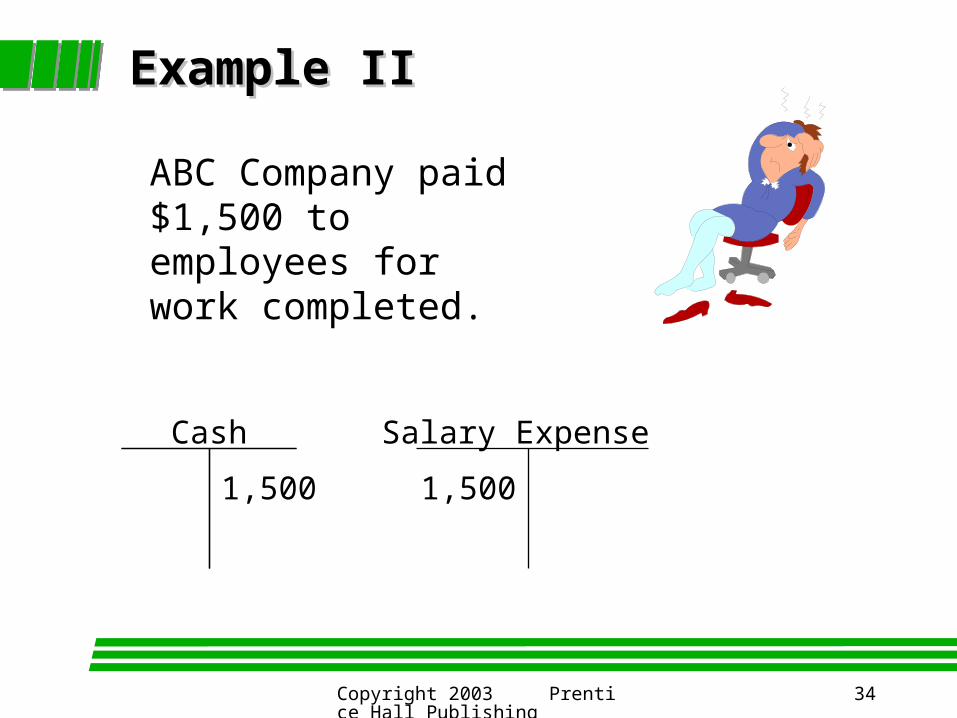

ABC Company paid $1,500 to employees for work completed.

1,500 1,500

Example IIExample II

Cash Salary Expense

Copyright 2003 Prentice Hall Publishing

35

ABC Company paid $3,000 for a new piece of office equipment.

$3,000

Cash Equipment

$3000

Example IIIExample III

Copyright 2003 Prentice Hall Publishing

36

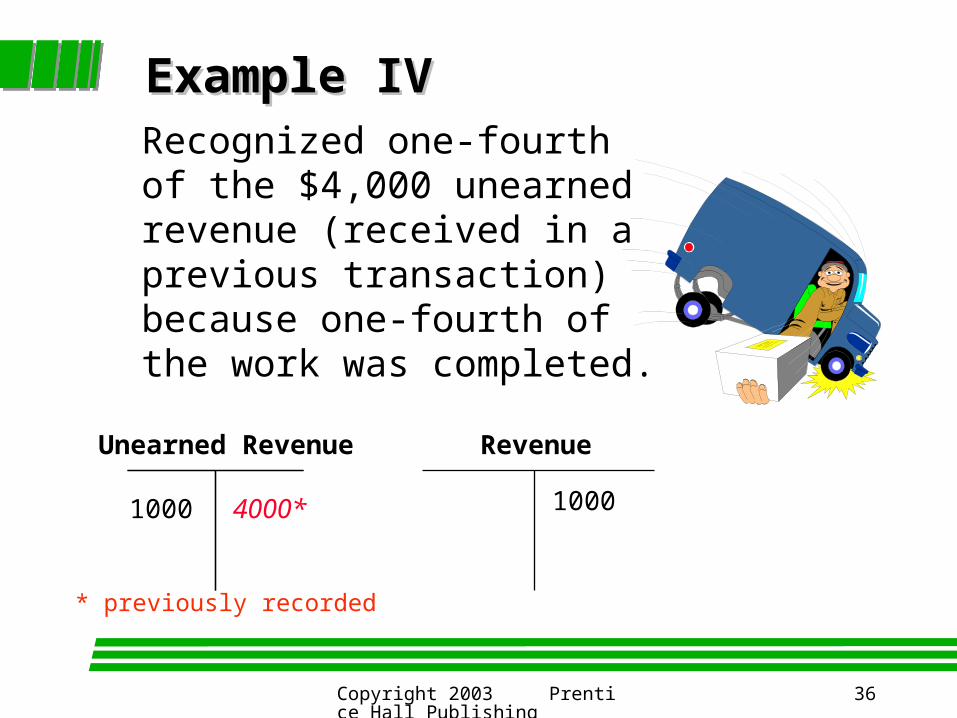

Recognized one-fourth of the $4,000 unearned revenue (received in a previous transaction) because one-fourth of the work was completed.

* previously recorded

Example IVExample IV

Unearned Revenue Revenue

1000 4000* 1000

Copyright 2003 Prentice Hall Publishing

37

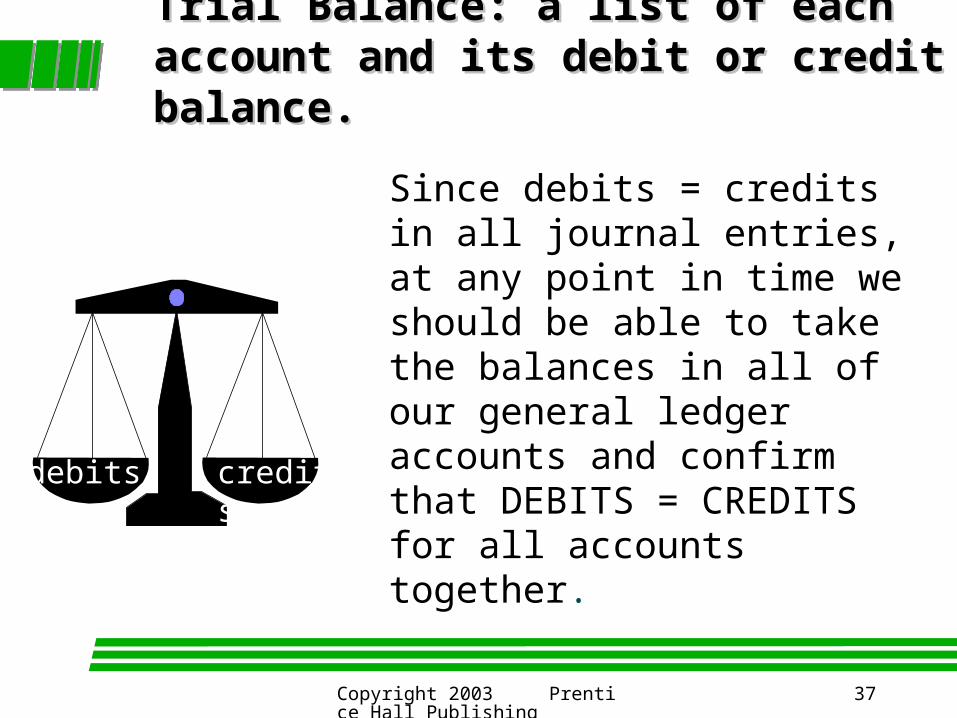

Trial Balance: a list of each account Trial Balance: a list of each account and its debit or credit balance.and its debit or credit balance.

Since debits = credits in all journal entries, at any point in time we should be able to take the balances in all of our general ledger accounts and confirm that DEBITS = CREDITS for all accounts together.

debits credits

Copyright 2003 Prentice Hall Publishing

38

Adjusting EntriesAdjusting Entries

Before financial statements are prepared, adjusting entries must be recorded to make sure that all accounts are properly stated and that nothing has been omitted.

Adjustments need to be made for Accruals Deferrals

Copyright 2003 Prentice Hall Publishing

39

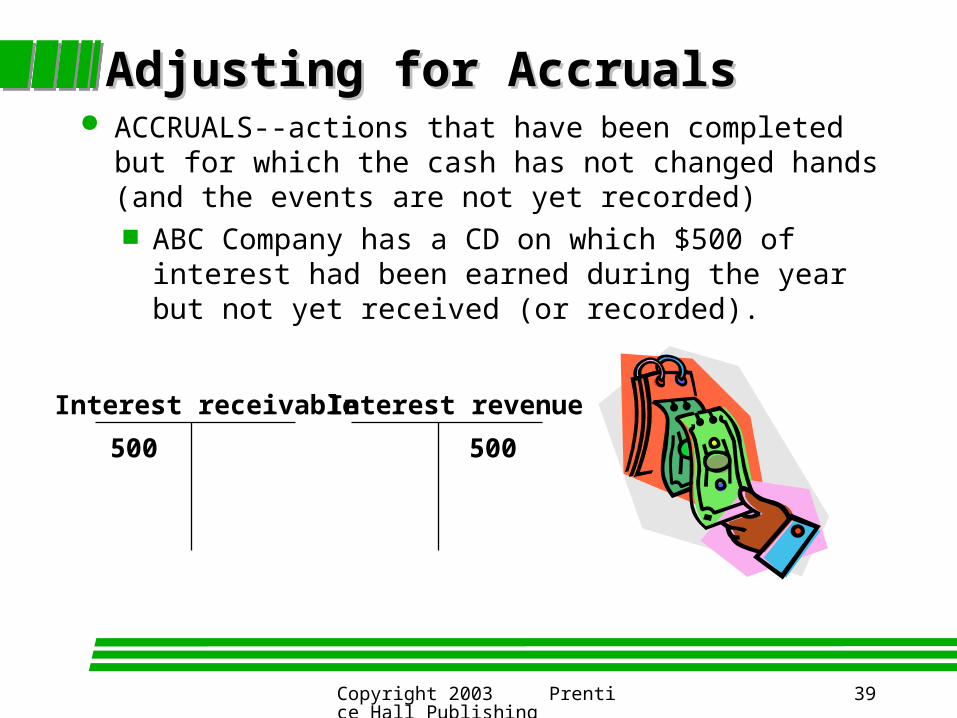

Adjusting for AccrualsAdjusting for Accruals ACCRUALS--actions that have been completed but for

which the cash has not changed hands (and the events are not yet recorded) ABC Company has a CD on which $500 of interest

had been earned during the year but not yet received (or recorded).

Interest receivable Interest revenue

500 500

Copyright 2003 Prentice Hall Publishing

40

Adjusting for DeferralsAdjusting for Deferrals Deferrals--dollars have been exchanged and recorded

before the action is completed ABC Company paid $600 for rent on December 1.

The rent was for three months, beginning in December. When they paid it, ABC recorded it as Prepaid Rent. Now, on 12/31, one month’s worth of rent has been used.

* previously recorded

Prepaid Rent Rent Expense

600* 200 200

Copyright 2003 Prentice Hall Publishing

41

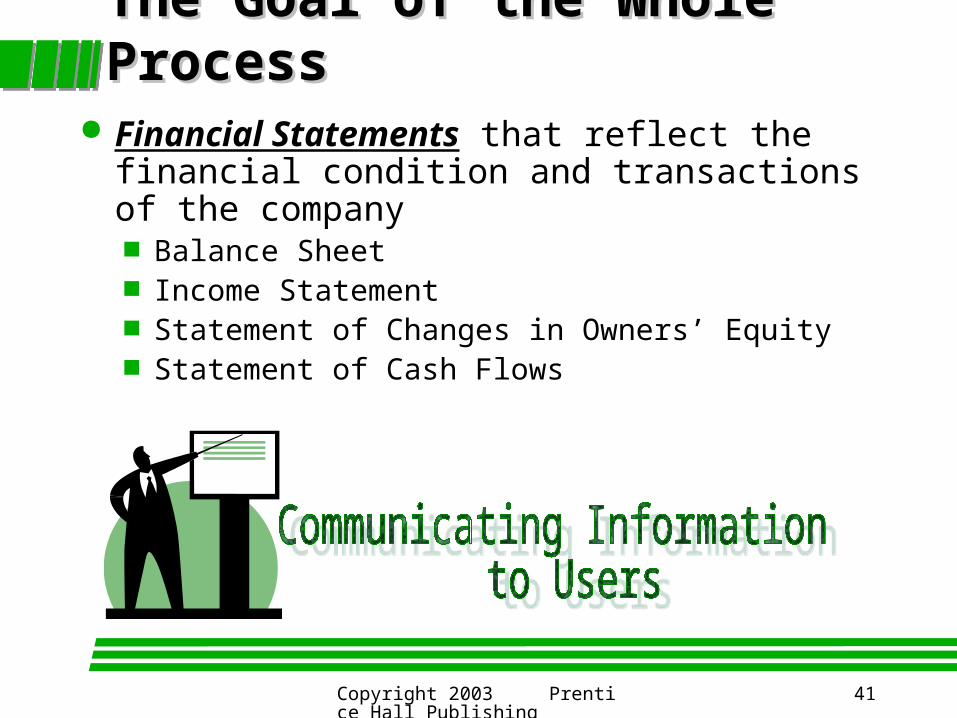

The Goal of the Whole ProcessThe Goal of the Whole Process Financial Statements that reflect the financial

condition and transactions of the company Balance Sheet Income Statement Statement of Changes in Owners’ Equity Statement of Cash Flows

Copyright 2003 Prentice Hall Publishing

42

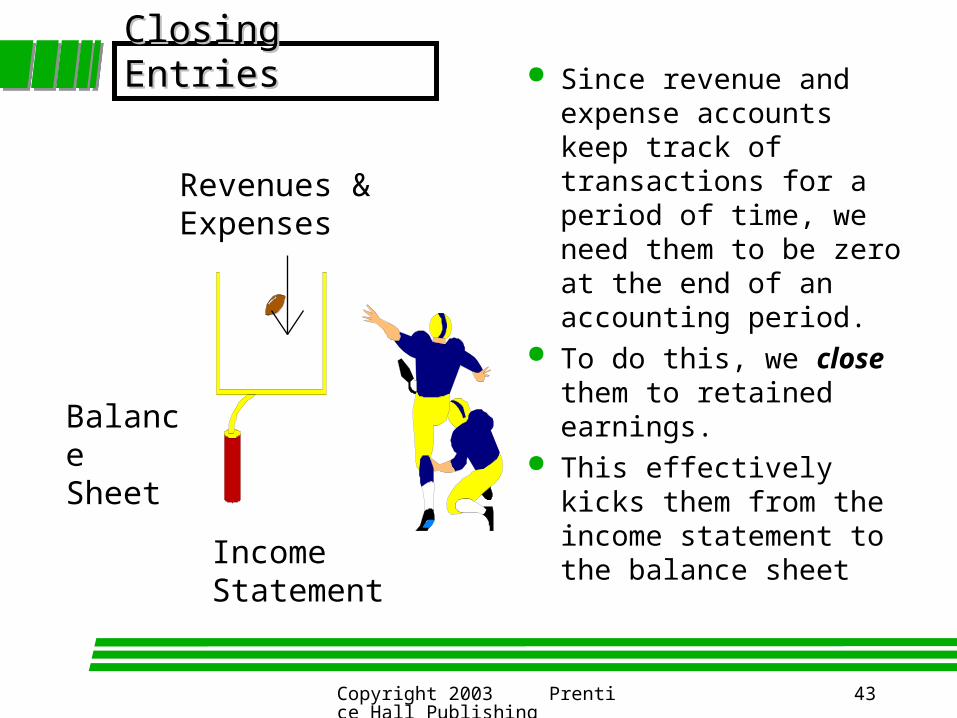

Closing EntriesClosing Entries

All temporary accounts (income statement accounts and distributions) are closed at the end of the accounting period, after the statements are prepared.

Their balances are brought to ZERO, and the balancing entry is made to the retained earnings account.

Copyright 2003 Prentice Hall Publishing

43

Closing EntriesClosing Entries Since revenue and expense accounts keep track of transactions for a period of time, we need them to be zero at the end of an accounting period.

To do this, we close them to retained earnings.

This effectively kicks them from the income statement to the balance sheet

Revenues & Expenses

IncomeStatement

BalanceSheet

Copyright 2003 Prentice Hall Publishing

44

Journal Entries to Close Journal Entries to Close Revenue and Expense Accounts: Revenue and Expense Accounts: Closing EntriesClosing Entries

Revenue accounts have credit balances, so we must DEBIT them to close them (to get a zero balance)

What should we credit?

RETAINED EARNINGS

Copyright 2003 Prentice Hall Publishing

45

Closing continued...Closing continued... To close expense accounts, we should

credit the expense account and debit the Retained Earnings account.

We are emptying the revenue and expense accounts…

All revenue and expense accounts will have a balance of ZERO after we close them.

Copyright 2003 Prentice Hall Publishing

46

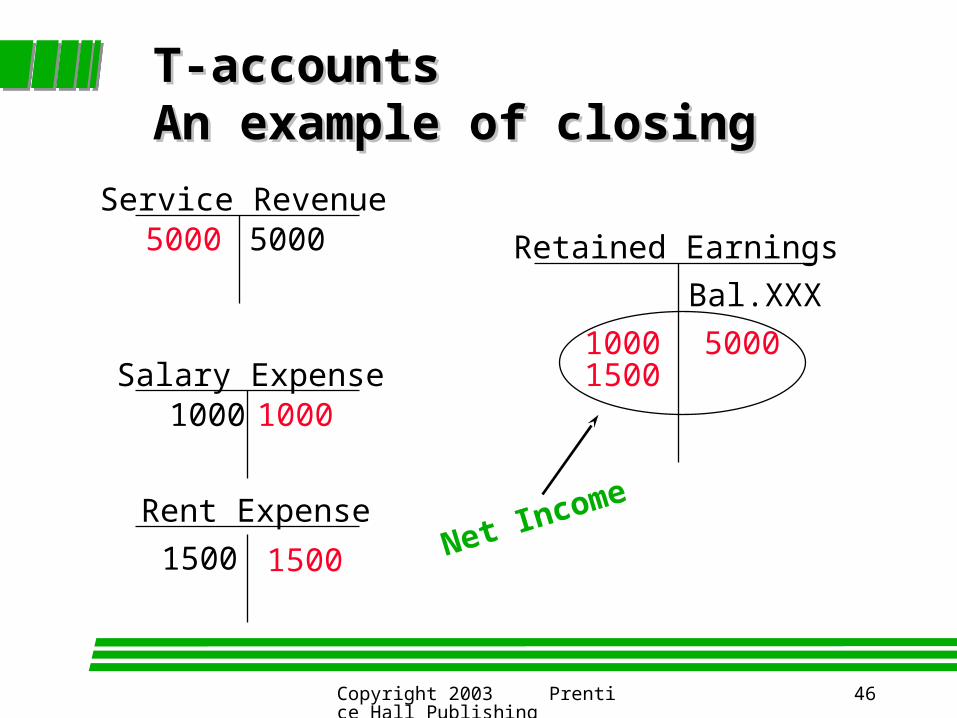

T-accountsT-accountsAn example of closingAn example of closing

Service Revenue

Salary Expense

Rent Expense

Retained Earnings

Bal.XXX

5000

1000

1500

5000

5000

1000

1000

1500

1500

Net Income

Copyright 2003 Prentice Hall Publishing

47

Retained Earnings

Beginning balance

+ Net Income

Ending balance

The DISTRIBUTIONS (to owners) account is closed with a credit, since it has a debit balance, and a debit to RETAINED EARNINGS.

Distributions

$xxx $xxx

$xxx

One More Account to CloseOne More Account to Close

Copyright 2003 Prentice Hall Publishing

48

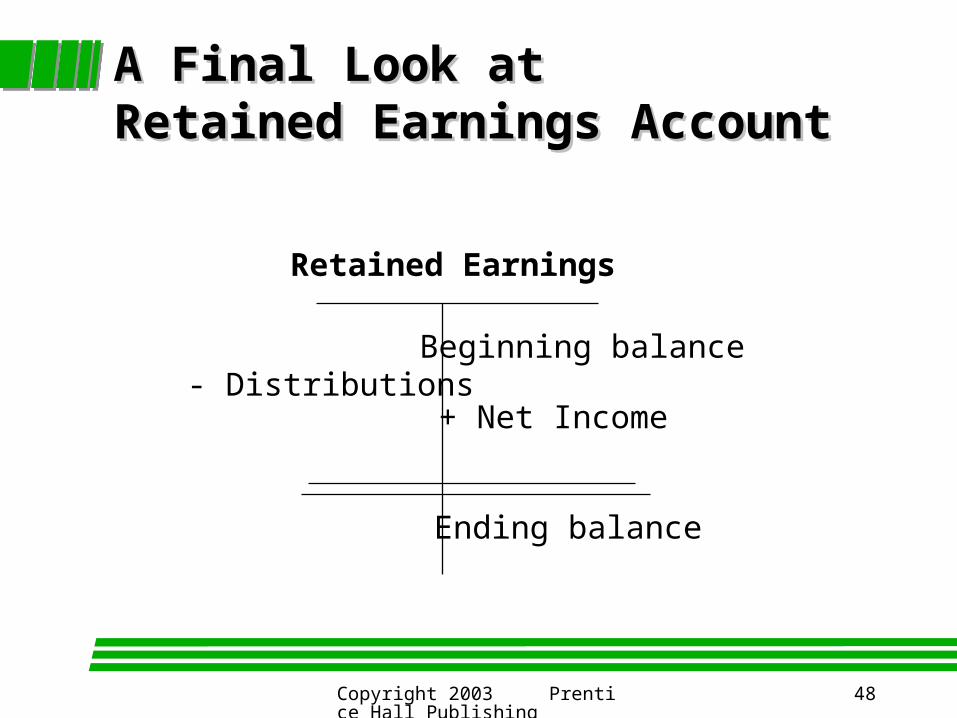

Beginning balance

+ Net Income

Ending balance

- Distributions

Retained Earnings

A Final Look atA Final Look atRetained Earnings AccountRetained Earnings Account

Copyright 2003 Prentice Hall Publishing

49

The Post-closing Trial Balance:The Post-closing Trial Balance:A trial balance written after closing the books is called a post-closing trial balance sheet.

ONLY the BALANCE SHEET ACCOUNTS -- the revenue and expense accounts have zero balances.

What accounts will be on this trial balance?