copyright © 2013 crc credit bureau limited. all rights reserved. nigerian financial market...

TRANSCRIPT

Copyright © 2013 CRC Credit Bureau Limited. All Rights Reserved.

Nigerian Financial Market Infrastructure and Managing Credit

Risks

June

4 , 2013.

1

Ahmed ‘Tunde Popoola, FCAManaging Director / CEO, CRC Credit Bureau Limited

Presented at the 4th Nigeria Development and Finance Forum (NDFF) 2013, North America Conference at Washington Marriott, Washington DC, United States.

Introduction

Protocols, Introductions & Welcome Remarks.

2

Presentation Outline

Introduction Update on the Nigerian Financial

System & Recent Policy Drivers Nigerian Financial Market

Infrastructure Managing Credit Risks CRC’s Role as a Financial

Infrastructure Conclusion

3

4

Nigerian Financial System

Consolidation of the Banking System between 2003-2005.

The Nigerian Financial Crisis Vs Global Financial Crisis.Global Crisis influenced by subprime

mortgages.Nigeria Financial crisis influenced by

Capital Market burbleForeign Investment funds flight and repatriation.

Weak governance regime.Nigeria is emerging strong from the crisis.

5

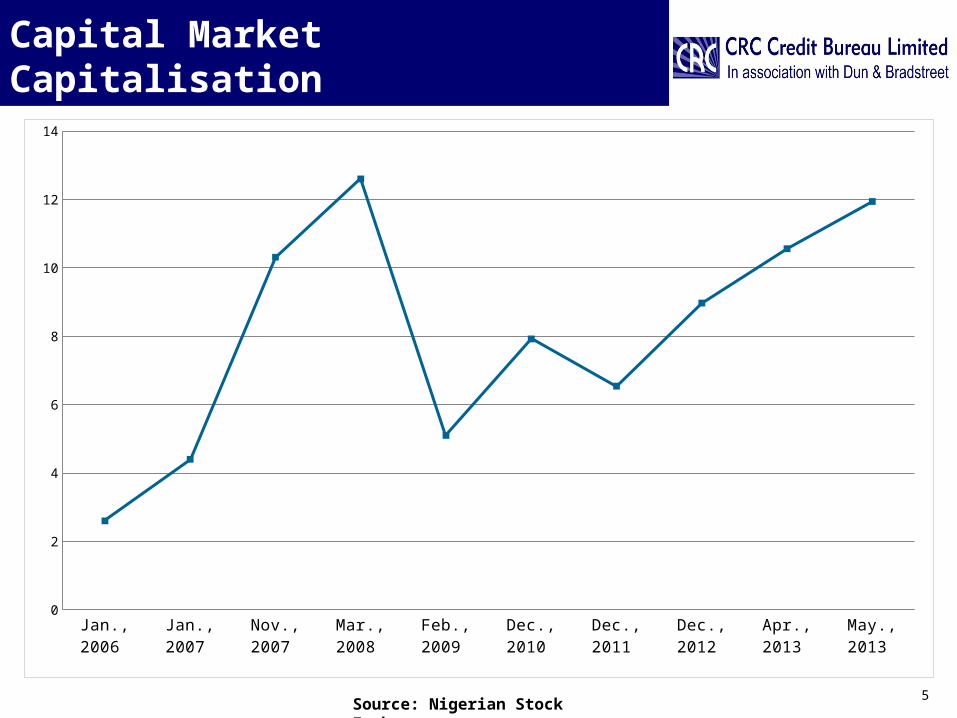

Capital Market Capitalisation

Source: Nigerian Stock Exchange

Jan., 2006 Jan., 2007 Nov., 2007 Mar., 2008 Feb., 2009 Dec., 2010 Dec., 2011 Dec., 2012 Apr., 2013 May., 2013

Market Capitalisation (=N=‘Trillion)

2.6 4.4 10.31 12.6 5.1 7.92 6.54 8.97 10.56 11.94

1

3

5

7

9

11

13

6

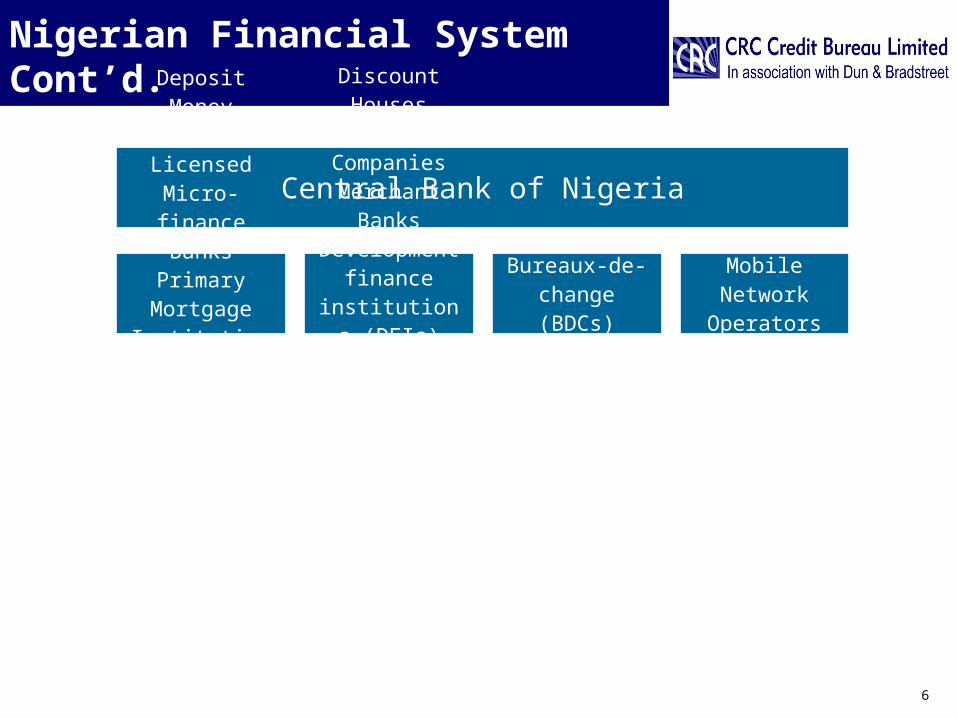

Nigerian Financial System Cont’d.

Central Bank of Nigeria

Deposit Money Banks:

Licensed Micro-finance

BanksPrimary

Mortgage Institutions

(PMIs)Commercial

BanksNon-interest

Banks

Discount HousesFinance

CompaniesMerchant

BanksDevelopment

finance institutions

(DFIs)Asset

Management companies

Leasing companies

Bureaux-de-change (BDCs)

Mobile Network

Operators

7

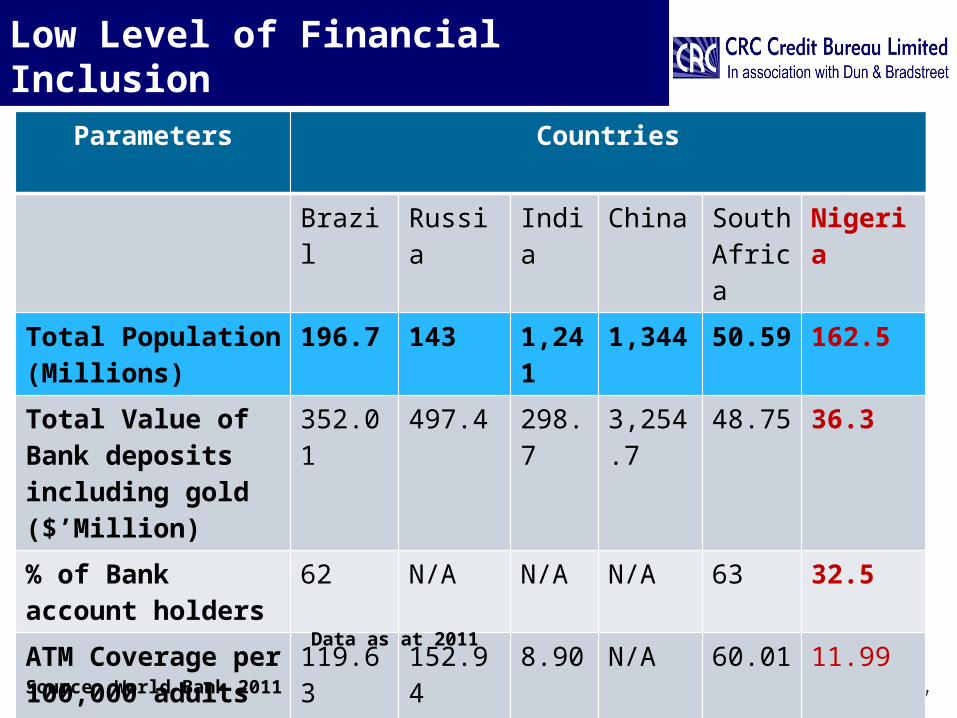

Low Level of Financial Inclusion

Parameters Countries

Brazil Russia India China South Africa

Nigeria

Total Population (Millions)

196.7 143 1,241

1,344 50.59

162.5

Total Value of Bank deposits including gold ($’Million)

352.01

497.4 298.7

3,254.7

48.75 36.3

% of Bank account holders

62 N/A N/A N/A 63 32.5

ATM Coverage per 100,000 adults as at 2011

119.63

152.94

8.90 N/A 60.01 11.99

Source: World Bank 2011

Data as at 2011

8

Low Credit Penetration

Parameters Countries

Brazil Russia

India

China

South Africa

Nigeria

Domestic credit provided by banking sector as % of GDP as at 2012

98.3 39.5 74.1 145.5 175 37.5

Private Credit Bureau Coverage to % of adults as at 2012

62.2 45.4 14.9 54.0 4.1

Source: World Bank 2012

9

Trend in Credit Penetration in Nigeria

Source: CBN, 2012.

2006 2007 2008 2009 2010 2011 2012

Credit to Private Sector (=N=' Trillion) 2.57 5.07 8.06 10.21 9.83 14.18 15.14

1

3

5

7

9

11

13

15

Presentation Outline

Introduction Update on the Nigerian Financial

System & Recent Policy Drivers Nigerian Financial Market

Infrastructure Managing Credit Risks CRC’s Role as a Financial

Infrastructure Conclusion

10

11

The Concept of Financial Infrastructure

Deposits(Surplus Zone)

Loans(Deficit Zone)

Infrastructures used are:

Automated Teller Machines (ATM)Point-of-Sale TerminalsMobile and Internet Transfers Cashless policy

Infrastructures used are:

Credit BureausCollateral RegistriesLegislation and Court System

Financial Intermediation

12

Financial Infrastructures Cont’d.

Financial Infrastructures help:Modernise financial

intermediation.Drive financial inclusion.Drive innovation.Foster transparency.Curb corruption.Enhance efficiency in service

delivery.Reduces transaction costs.

13

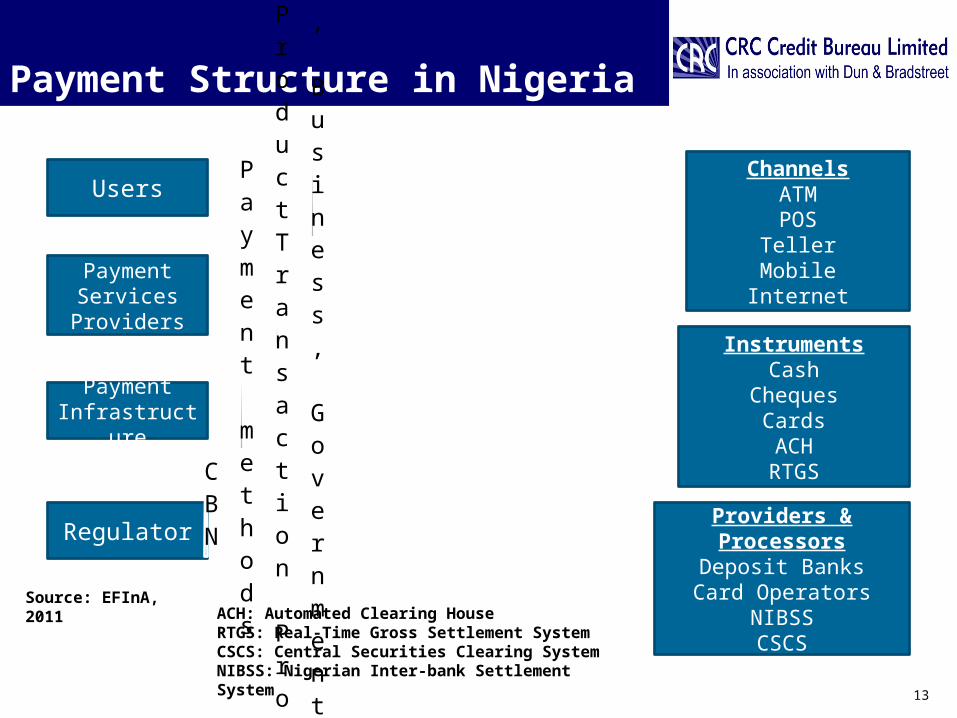

Payment Structure in Nigeria

Users

Payment Services Providers

Payment Infrastructur

e

Regulator

ChannelsATMPOSTellerMobile

Internet

InstrumentsCash

ChequesCardsACHRTGS

Providers & Processors

Deposit BanksCard Operators

NIBSSCSCS

Source: EFInA, 2011ACH: Automated Clearing HouseRTGS: Real-Time Gross Settlement System CSCS: Central Securities Clearing SystemNIBSS: Nigerian Inter-bank Settlement System

Individuals, Business, Government

Channels & ProductTransaction Processing

Payment methods

CBN

14

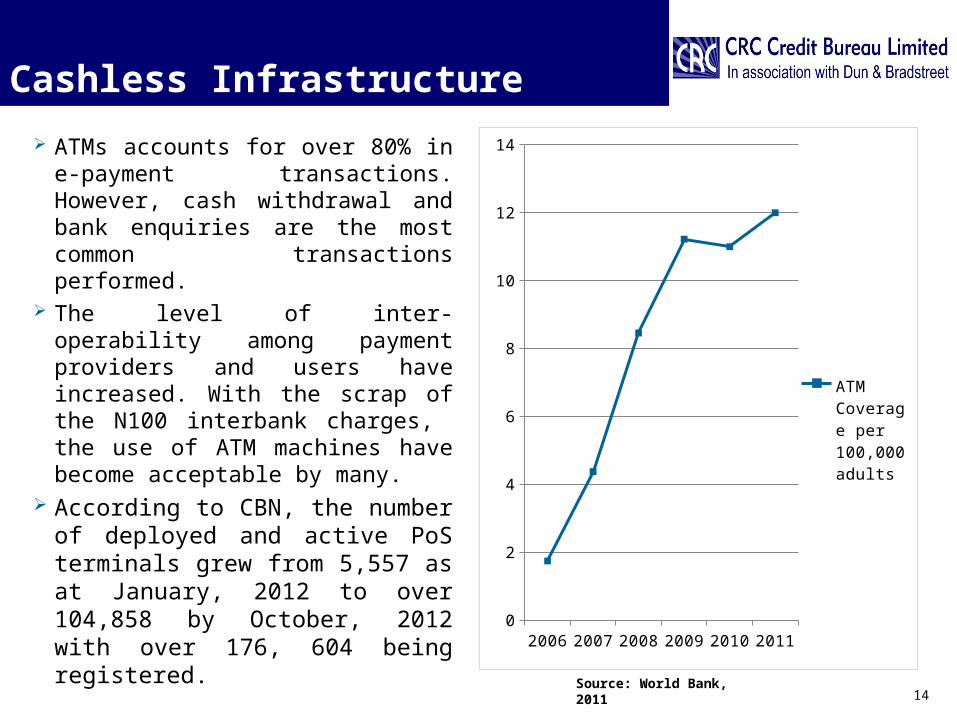

Cashless Infrastructure

2006 2007 2008 2009 2010 20110

2

4

6

8

10

12

14

ATM Coverage per 100,000 adults

Source: World Bank, 2011

ATMs accounts for over 80% in e-payment transactions. However, cash withdrawal and bank enquiries are the most common transactions performed.

The level of inter-operability among payment providers and users have increased. With the scrap of the N100 interbank charges, the use of ATM machines have become acceptable by many.

According to CBN, the number of deployed and active PoS terminals grew from 5,557 as at January, 2012 to over 104,858 by October, 2012 with over 176, 604 being registered.

15

Other Policy Drivers

Mobile Banking and Money TransferCashless PolicyRevised Microfinance PolicyRevised Prudential Guidelines

Presentation Outline

Introduction Update on the Nigerian Financial

System & Recent Policy Drivers Nigerian Financial Market

Infrastructure Managing Credit Risks CRC’s Role as a Financial

Infrastructure Conclusion

16

17

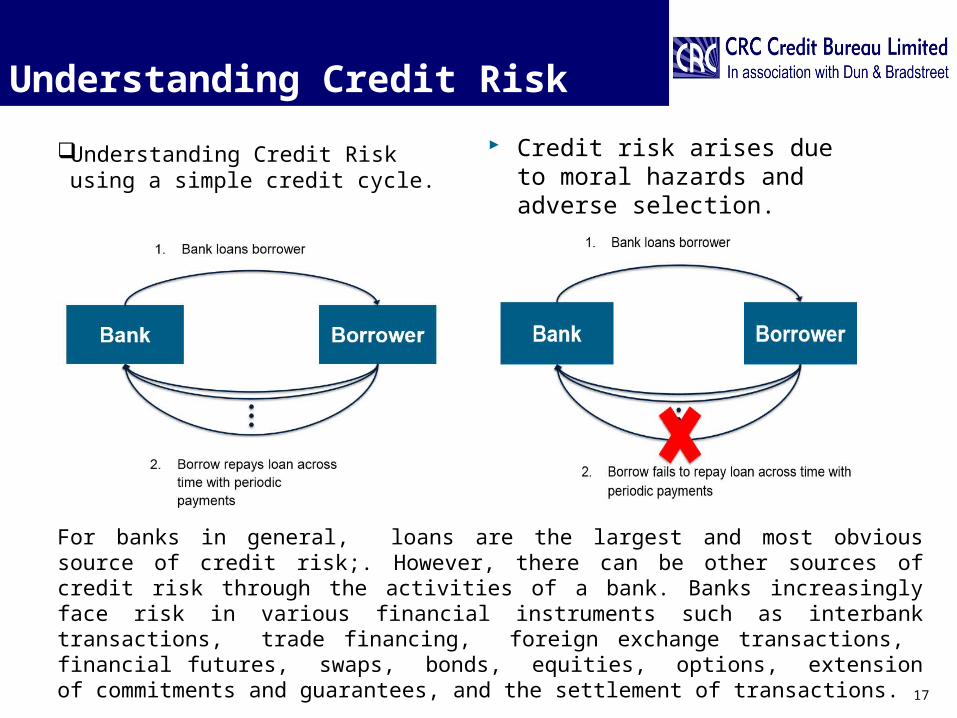

Understanding Credit Risk

Understanding Credit Risk using a simple credit cycle.

Credit risk arises due to moral hazards and adverse selection.

For banks in general, loans are the largest and most obvious source of credit risk;. However, there can be other sources of credit risk through the activities of a bank. Banks increasingly face risk in various financial instruments such as interbank transactions, trade financing, foreign exchange transactions, financial futures, swaps, bonds, equities, options, extension of commitments and guarantees, and the settlement of transactions.

18

Laying the Foundation for Risk Management

Collaboration among key risk management players.

Establishment of an appropriate credit risk environment and culture.

Operating under a sound credit-granting process.

Maintenance of an appropriate credit administration, measurement and monitoring process.

Ensuring adequate controls over credit risk and adopting a sound internal lending policy.

Use of credit bureaus.Use of collateral registries.Compliance to Basel’s Accord.

19

Financial Infrastructure: Presence of Credit Bureaus in Africa

The countries in are those that uses private credit bureaus in Africa.

Ghana is the only country in West Africa with a Collateral Registry.

20

Credit Bureaus in Nigeria

Credit bureaus, also known as credit information services, credit registries, credit reporting agencies or consumer credit reference agencies are organizations that are well established in advanced economies. The bureau compiles information on individuals and corporate organization. These include information on credit repayment records, court judgment and bankruptcies and then creates a comprehensive reports that is sold to business users in form of credit reports, credit scores and other products.

Presently, Nigeria has three private credit bureaus and one owned by the Central Bank of Nigeria. Having credit bureaus places Nigeria in a enviable position as they have enabled the country reach a respectable level in database coverage, improved loan processing speed and costs, reduced selection records and information asymmetry, reduced credit risk and overall enhanced access to credit.

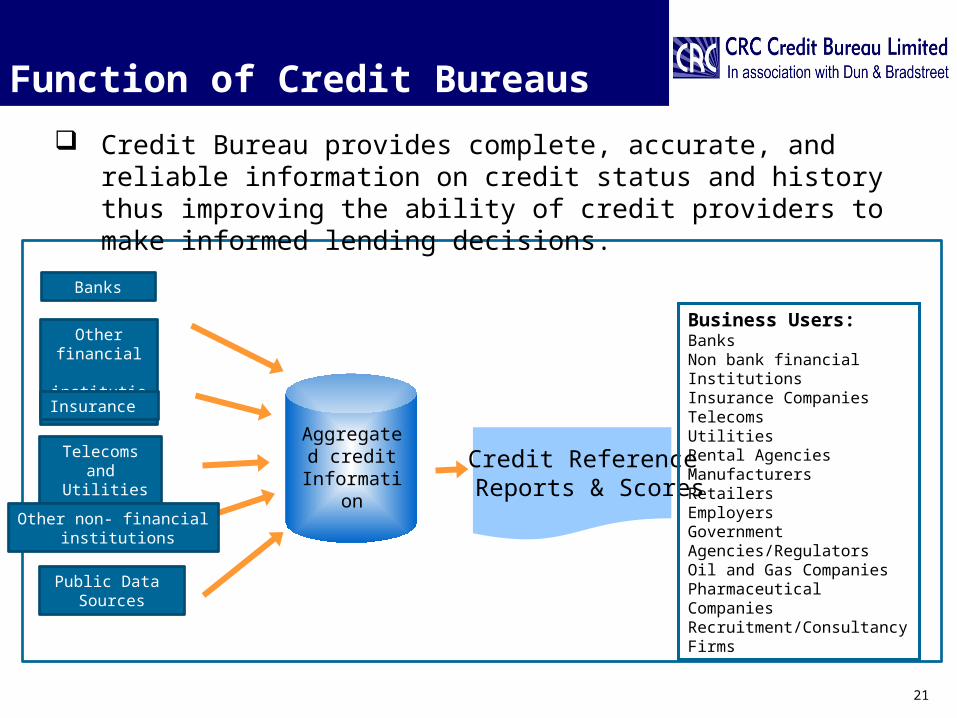

Function of Credit Bureaus

Credit Bureau provides complete, accurate, and reliable information on credit status and history thus improving the ability of credit providers to make informed lending decisions.

21

Aggregated credit

Information

Other financial

institutions

Insurance

Banks

Telecoms and

Utilities

Other non- financial institutions

Credit Reference Reports & Scores

Business Users:BanksNon bank financial InstitutionsInsurance CompaniesTelecomsUtilitiesRental AgenciesManufacturersRetailersEmployersGovernment Agencies/RegulatorsOil and Gas CompaniesPharmaceutical CompaniesRecruitment/Consultancy Firms

Public Data Sources

22

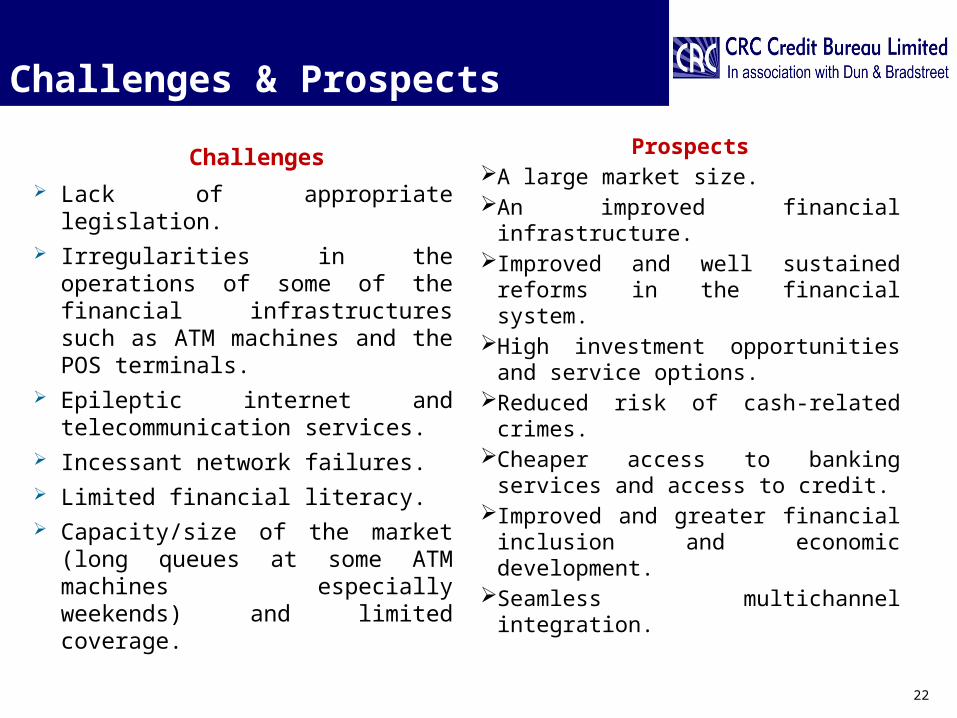

Challenges & Prospects

ProspectsA large market size.An improved financial

infrastructure.Improved and well sustained

reforms in the financial system.High investment opportunities

and service options.Reduced risk of cash-related

crimes.Cheaper access to banking

services and access to credit.Improved and greater financial

inclusion and economic development.

Seamless multichannel integration.

Challenges Lack of appropriate legislation. Irregularities in the operations

of some of the financial infrastructures such as ATM machines and the POS terminals.

Epileptic internet and telecommunication services.

Incessant network failures. Limited financial literacy. Capacity/size of the market

(long queues at some ATM machines especially weekends) and limited coverage.

23

The Future

Quick implementation of the national identity project.Establishment a collateral registry.Support existing Credit Bureaus to enable them deliver on their mandate e.g. regulations. The efficiency and transparency of the judicial system.

24

Investment Finance Opportunities

Top 10 African Destination countries for infrastructure projects, up to February, 2013

Countries Number of Projects Sum of capital invested (US$ million)

South Africa 134 129, 934.0

Nigeria 106 95,480.5

Egypt 82 60,164.7

Uganda 63 17,730.3

Kenya 60 32,851.5

Algeria 34 87,154.1

Mozambique 31 32,085.0

Libya 29 20,668.4

Tanzania 29 16,185.1

Cameroon 25 8,470.8

Source: African Project Access, Business Monitor International; Ernst and Young analysis

25

Investment Finance Opportunities in Nigeria

Project Opportunities in Nigeria are:Transport and Logistics

infrastructure.Housing Infrastructure.Oil and Gas.Power and Utilities.Agriculture.

Presentation Outline

Introduction Update on the Nigerian Financial

System & Recent Policy Drivers Nigerian Financial Market

Infrastructure Managing Credit Risks CRC’s Role as a Financial

Infrastructure Conclusion

26

Who We Are CRC Credit Bureau is a private limited company

incorporated in June 2006. The Bureau was licensed by the Central Bank of Nigeria in June 2009 and commenced live operations in the same month.

CRC Credit Bureau provides an industry-wide information repository on credit profiles of both consumers and corporate entities. We are the leading credit bureau company in Nigeria with credit information covering commercial banks, non-banking institutions, retailers and utility providers and other credit granting institutions.

Our main objective is to generate and supply reliable and accurate credit information reports on borrowers in the consumer and corporate sectors for permissible purposes.

We serve as a neutral third party service provider to our customers and subscribers.

27

Our Shareholders

28

-Investor & Technical Partners

-Investors

29

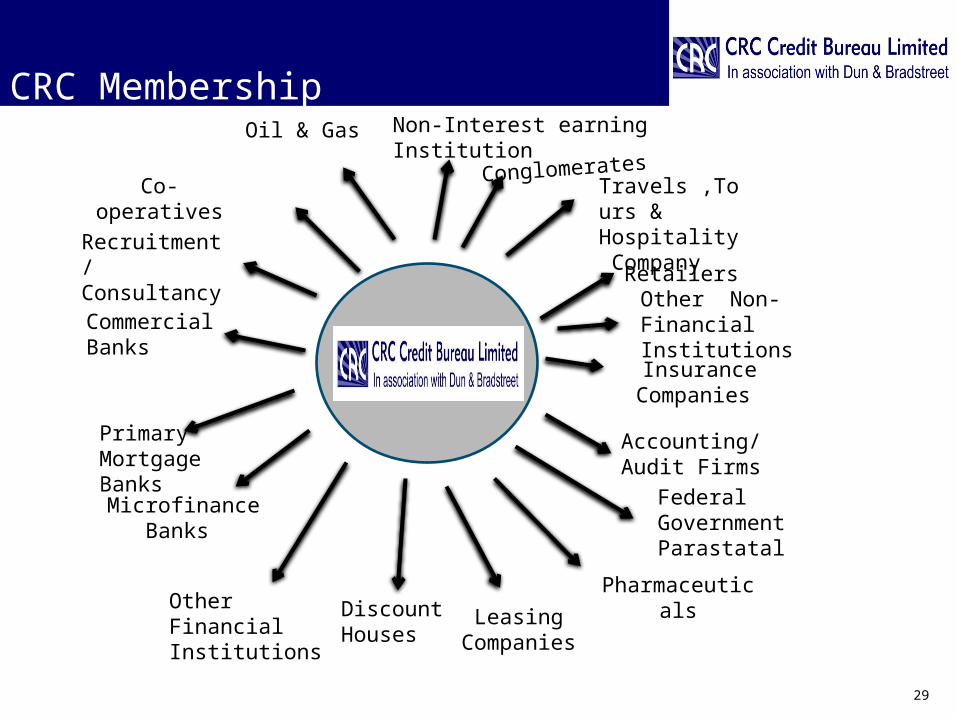

Retailers

Oil & Gas

Commercial Banks

Primary Mortgage Banks

Non-Interest earning Institution

Travels ,Tours & Hospitality Company

Federal Government Parastatal

Accounting/Audit Firms

Insurance Companies

Other Financial Institutions

Microfinance Banks

Discount Houses

Leasing Companies

CRC Membership Chart

Recruitment/Consultancy

Other Non-Financial Institutions

Pharmaceuticals

Co-operatives Conglomerates

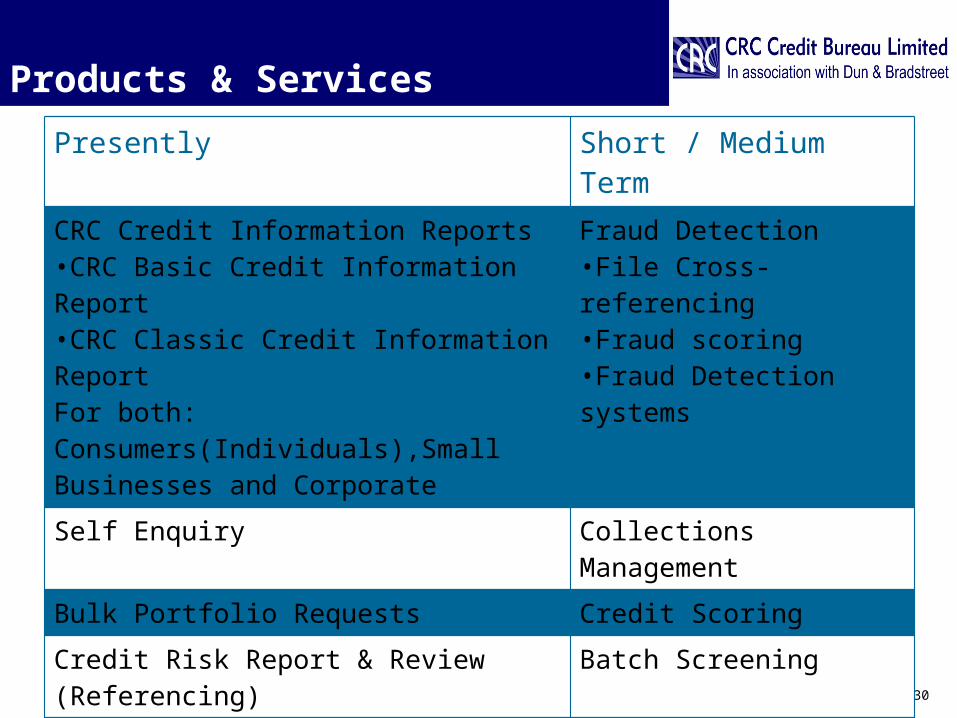

Products & Services

30

Presently Short / Medium TermCRC Credit Information Reports•CRC Basic Credit Information Report•CRC Classic Credit Information ReportFor both: Consumers(Individuals),Small Businesses and Corporate

Fraud Detection•File Cross-referencing•Fraud scoring•Fraud Detection systems

Self Enquiry Collections Management

Bulk Portfolio Requests Credit Scoring

Credit Risk Report & Review (Referencing)

Batch Screening

Data Management

Monitors & Alerts

CRC Financial Education

Presentation Outline

Introduction Update on the Nigerian Financial

System & Recent Policy Drivers Nigerian Financial Market

Infrastructure Managing Credit Risks CRC’s Role as a Financial

Infrastructure Conclusion

31

32

CONCLUSION Nigeria financial system is set for the next decade with the

aggressive adoption of financial infrastructure for financial intermediation – payments system and access to credit

All efforts are also geared towards improving on the financial inclusion including the introduction of mobile money

Credit bureau is set to change the face of access to lending in Nigeria especially for consumers and SMEs who face the challenges of access to credit

Nigerian banks are taking leadership in Africa with presence in most attractive economies in Africa and with improvements in size and governance

Nigeria is also a hot destination for FDIs due to environmental friendliness, market size and stable polity

We need to address the challenge of power, internet access, unique identification, legislation, etc.

THANK YOU.

33