copyright 2014 diane scott docking1 the stock market - primary market

TRANSCRIPT

Copyright 2014 Diane Scott Docking 1

The Stock Market - Primary Market

Learning Objectives

Identify the features and characteristics common stock and preferred stock

Examine the process by which common stock is issued in the primary stock market

Understand the role that an investment bank plays in the financial markets

Copyright 2014 Diane Scott Docking 2

3Copyright 2014 Diane Scott Docking

4Copyright 2014 Diane Scott Docking

Copyright 2014 Diane Scott Docking 5

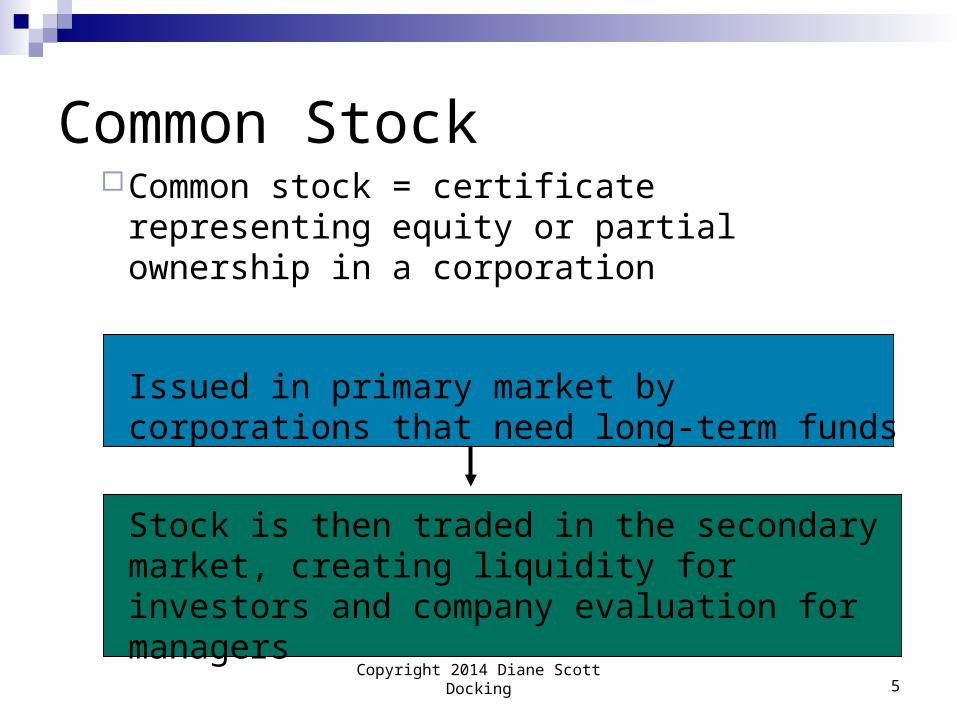

Common stock = certificate representing equity or partial ownership in a corporation

Issued in primary market by corporations that need long-term funds

Stock is then traded in the secondary market, creating liquidity for investors and company evaluation for managers

Common Stock

Copyright 2014 Diane Scott Docking 6

Common Stock Right to ___

Many investor assign their vote to management via a _____ ____________________have two classes of common

shares outstanding, with different voting rights assigned to each class

__________________ voting the number of votes assigned to each stockholder equals the number

of shares held multiplied by the number of directors to be elected The number of shares needed to elect p directors, Np, is:

goutstandin sharescommon #elected be toneeded directors # where

11n

)(

sn

snppN

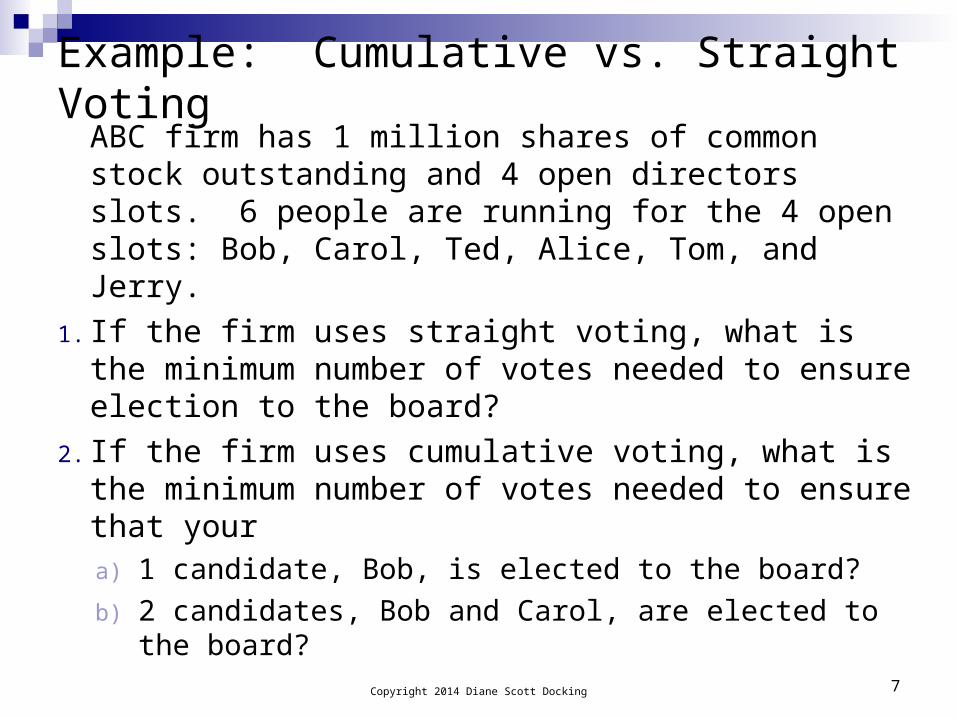

Example: Cumulative vs. Straight VotingABC firm has 1 million shares of common stock outstanding and 4 open directors slots. 6 people are running for the 4 open slots: Bob, Carol, Ted, Alice, Tom, and Jerry.

1. If the firm uses straight voting, what is the minimum number of votes needed to ensure election to the board?

2. If the firm uses cumulative voting, what is the minimum number of votes needed to ensure that youra) 1 candidate, Bob, is elected to the board?

b) 2 candidates, Bob and Carol, are elected to the board?

Copyright 2014 Diane Scott Docking 7

Example: Cumulative vs. Straight Voting1. If the firm uses straight voting, what is the minimum number of votes

needed to ensure election to the board?

(50% x # share outstanding) + 1 =

(.50 x 1,000,000) + 1 = 500,000 + 1 = 500,001 shs.

If Mary owns 500,001 shares, she can elect the entire Board:

Suppose Mary wants Ted, Alice, Tom and Jerry on the Board, then votes are cast as follows:

Copyright 2014 Diane Scott Docking 8

Candidate For Against Elected?

Bob 499,999 500,001 No

Carol 499,999 500,001 No

Ted 500,001 499,999 Yes

Alice 500,001 499,999 Yes

Tom 500,001 499,999 Yes

Jerry 500,001 499,999 Yes

Example: Cumulative vs. Straight Voting2. If the firm uses cumulative voting, what is the minimum number of

votes needed to ensure that youra) 1 candidate, Bob, is elected to the board?

Chart 1: Bob guaranteed: Chart 2: Mary’s voting Ted & Alice:

Copyright 2014 Diane Scott Docking 9

800,001

1000,80015

000,000,4

114

)000,000,14(11

1n

)(1

snpN

Candidate For Elected?

Bob 800,001 Yes

Carol 0 No

Ted 800,000 Yes

Alice 800,000 Yes

Tom 800,000 Yes

Jerry 799,999 No

Total votes 4,000,000

Candidate For Elected?

Bob 800,001 Yes

Carol ? 1,199,995 Yes

Ted 800,000 Yes

Alice 800,000 Yes

Tom ? 0 No

Jerry ? 400,004 No

Total votes 4,000,000

Example: Cumulative vs. Straight Votinga) 2 candidates, Bob and Carol, are elected to the board?

Chart 1: Bob & Carol guaranteed: Chart 2: Mary’s voting Ted & Alice:

Copyright 2014 Diane Scott Docking 10

Candidate For Elected?

Bob 800,001 Yes

Carol 800,000 Yes

Ted 800,000 Yes

Alice 800,000 Yes

Tom 0 No

Jerry 799,999 No

Total votes 4,000,000

Candidate For Elected?

Bob 800,001 Yes

Carol 800,000 Yes

Ted 800,000 Yes

Alice 800,000 Yes

Tom 400,004 No

Jerry 399,995 No

Total votes 4,000,000

2 candidate to 800,000 and

1 candidate to 800,001 with

1,600,001

1000,600,115

000,000,8

114

000,000,14(21

1n

)(2

snpN

Copyright 2014 Diane Scott Docking 11

Common Stock Characteristics (cont.) Right to ________ , but they are discretionary and are thus

not guaranteed

Common stockholders have the lowest priority claim in the event of bankruptcy (i.e., a claim)

___________ implies that common stockholders can lose no more than their original investment

Par Value

No maturity

Copyright 2014 Diane Scott Docking 12

Preferred Stock Characteristics

Hybrid security Represents equity or ownership

interest, but usually _________ rightsTrade voting rights for stated fixed

annual dividend Maturity

Perpetual vs. Limited life Call provisions

Copyright 2014 Diane Scott Docking 13

Preferred Stock Characteristics (cont.)

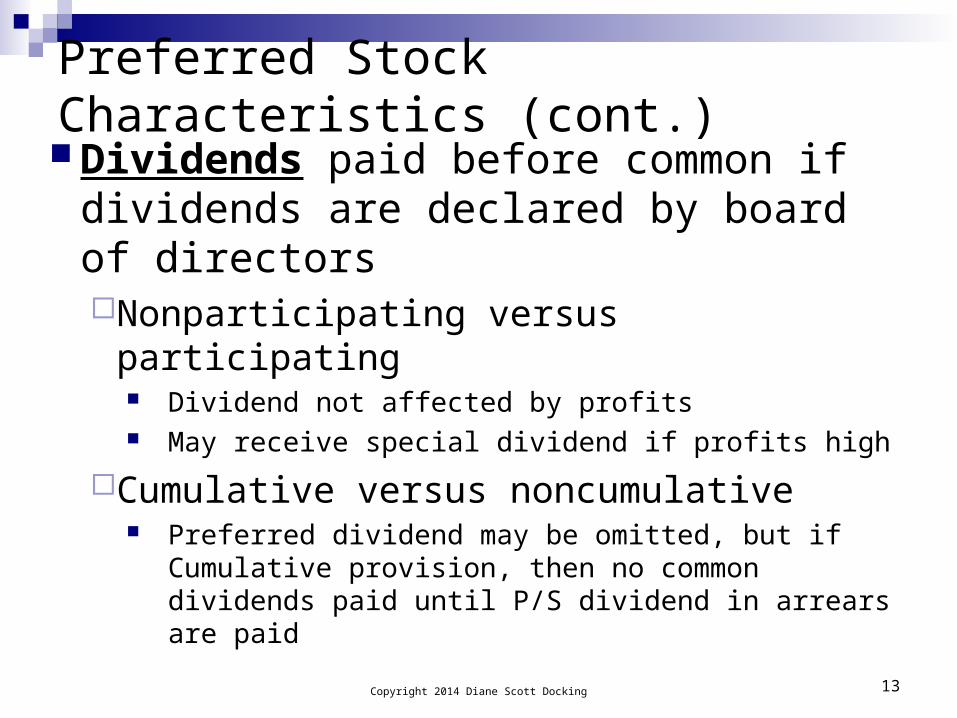

Dividends paid before common if dividends are declared by board of directorsNonparticipating versus participating

Dividend not affected by profits May receive special dividend if profits high

Cumulative versus noncumulative Preferred dividend may be omitted, but if

Cumulative provision, then no common dividends paid until P/S dividend in arrears are paid

Copyright 2014 Diane Scott Docking 14

How Securities Are Issued Investment banker role Public placement

IPO Secondary/Seasoned Offerings Shelf Registration Preemptive Rights Offering Bought Deal Auction

Private placement

Copyright 2014 Diane Scott Docking 15

Role of Investment Banker in Bringing New Securities to Market

Three steps of bringing a new security issue to market include:

1. Origination

2. Underwriting

3. Sales and distribution

Copyright 2014 Diane Scott Docking 16

Role of Investment Banker in Bringing New Securities to Market

Three steps of bringing a new security issue to market include:

1. Origination

2. Underwriting

3. Sales and distribution

Copyright 2014 Diane Scott Docking 17

Role of Investment Banker in Bringing New Securities to Market

Three steps of bringing a new security issue to market include:

1. Origination

2. Underwriting

3. Sales and distribution

Copyright 2014 Diane Scott Docking 18

Tombstone Ad

Syndicate members

Copyright 2014 Diane Scott Docking 19

Tombstone Ad

Syndicate members

Copyright 2014 Diane Scott Docking 20

Front Page of a Final Prospectus

IPO

IPO

Syndicate members

Firm commitment

Copyright 2014 Diane Scott Docking 21

Initial Public Offerings (IPOs) First-time offering of shares to the public Firm must provide information to public

Firm is assisted by an investment banker Registration statement to SEC Red-Herring Prospectus Road shows www.retailroadshow.com Final Prospectus Difficulty in buying IPO

Copyright 2014 Diane Scott Docking

22

Google’s IPO: S-1 filing

http://www.sec.gov/Archives/edgar/data/1288776/000119312504073639/0001193125-04-073639-index.htm

As filed with the Securities and Exchange Commission on April 29, 2004 Registration No. 333-

SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549

FORM S-1 REGISTRATION STATEMENT

Under

The Securities Act of 1933

GOOGLE INC. (Exact name of Registrant as specified in its charter)

Delaware 7375 77-0493581

(State or other jurisdiction of incorporation or organization)

(Primary Standard Industrial Classification Code Number)

(I.R.S. Employer Identification Number)

1600 Amphitheatre Parkway Mountain View, CA 94043

(650) 623-4000 (Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Eric Schmidt

Chief Executive Officer Google Inc.

1600 Amphitheatre Parkway Mountain View, CA 94043

(650) 623-4000 (Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Larry W. Sonsini, Esq. David J. Segre, Esq.

Wilson Sonsini Goodrich & Rosati, P.C.

650 Page Mill Road Palo Alto, California 94304-1050

(650) 493-9300

David C. Drummond, Esq. Jeffery L. Donovan, Esq.

Anna Itoi, Esq. Google Inc.

1600 Amphitheatre Parkway Mountain View, CA 94043

(650) 623-4000

William H. Hinman, Jr., Esq. Simpson Thacher & Bartlett LLP

3330 Hillview Avenue Palo Alto, California 94304

(650) 251-5000

Copyright 2014 Diane Scott Docking 23

Google’s IPO: S-1 filing

http://www.sec.gov/Archives/edgar/data/1288776/000119312504073639/0001193125-04-073639-index.htm

Copyright 2014 Diane Scott Docking 24

Initial Public Offerings (IPOs) First-time offering of shares to the public Firm must provide information to public

Firm is assisted by an investment banker Registration statement to SEC Red-Herring Prospectus Road shows www.retailroadshow.com Final Prospectus Difficulty in buying IPO

Copyright 2014 Diane Scott Docking

25

Image of a “Red Herring” Prospectus

Copyright 2014 Diane Scott Docking 26

Initial Public Offerings (IPOs) First-time offering of shares to the public Firm must provide information to public

Firm is assisted by an investment banker Registration statement to SEC Red-Herring Prospectus Road shows www.retailroadshow.com Final Prospectus Difficulty in buying IPO

Copyright 2014 Diane Scott Docking

27

Google’s IPO: Final Prospectus

http://www.sec.gov/Archives/edgar/data/1288776/000119312504143377/d424b4.htm

Prospectus August 18, 2004

19,605,052 Shares

Class A Common Stock

Google Inc. is offering 14,142,135 shares of Class A common stock and the selling stockholders are offering 5,462,917 shares of Class A common stock. We will not receive any proceeds from the sale of shares by the selling stockholders. This is our initial public offering and no public market currently exists for our shares. The initial public offering price is $85.00 per share.

Following this offering, we will have two classes of authorized common stock, Class A common stock and Class B common stock. The rights of the holders of Class A common stock and Class B common stock are identical, except with respect to voting and conversion. Each share of Class A common stock is entitled to one vote per share. Each share of Class B common stock is entitled to ten votes per share and is convertible at any time into one share of Class A common stock.

Our Class A common stock will be quoted on The Nasdaq National Market under the symbol “GOOG.”

Investing in our Class A common stock involves risks. See “ Risk Factors” beginning on page 4.

Price $85.00 A Share

Price to Public

Underwriting Discounts and Commissions

Proceeds to Google

Proceeds to Selling

Stockholders

Per Share $ 85.00 $ 2.3839 $ 82.6161 $ 82.6161 Total $ 1,666,429,420 $ 46,736,483 $ 1,168,368,039 $ 451,324,897

The selling stockholders have granted the underwriters the right to purchase up to an additional 2,940,757 shares to cover over-allotments.

Copyright 2014 Diane Scott Docking 28

Initial Public Offerings (IPOs) First-time offering of shares to the public Firm must provide information to public

Firm is assisted by an investment banker Registration statement to SEC Red-Herring Prospectus Road shows www.retailroadshow.com Final Prospectus Difficulty in buying IPO

Copyright 2014 Diane Scott Docking 29

Initial Public Offerings (IPOs) Performance of IPOs

Price generally rises on first day Average a 19% gain on first day of trading.

On average, the longer-term performance of IPOs is poor

Average 3-year return of IPO stocks lagged the average 3-year returns of similar non-IPO stocks by 7.2%.

Copyright 2014 Diane Scott Docking 30

Long-term Relative Performance of Initial Public Offerings

Copyright 2014 Diane Scott Docking 31

Example: Best Efforts vs. Firm Commitment

Stevens Bank intends to issue 2 million shares of common stock.

The bank’s investment banker has offered two alternatives:

Plan A:

A best efforts offering at $16 per share subject to an underwriting commission of 2% of expected gross proceeds plus $300,000. The investment banking firm expects 93% of the issue will be sold.

Plan B:

A firm commitment offer at $15.50 per share plus an underwriting fee of 7% of the gross proceeds.

1) Which plan offers the highest net proceeds to Stevens Bank?

2) What other factors must Stevens consider when making their choice?

Copyright 2014 Diane Scott Docking 32

Example: Best Efforts vs. Firm CommitmentProceeds to Firm Proceeds to IB

Plan A:

Gross Proceeds (2 mill. shs. x $16/sh x .93)

$29,760,000

Less: Commission ($29,760,000 x .02) - 595,200 $ 595,200

Less: Fee - 300,000 300,000

Net proceeds $28,864,800* $ 895,200

Plan B:

Gross Proceeds (2 mill. shs. x $15.50/sh) $31,000,000 - $31,000,000

Less: Fee ($31,000,000 x .07) - 2,170,000 2,170,000

Proceeds from sale of shares _________0 ?

Net proceeds $28,830,000 $2,170,000 + net profit from share sales**

* This amount could change since IB could sell < 93% or > 93% of the issue.

________________bears the risk.

**IB may not be able to sell the shares at a profit.

_______________ bears the risk.

Copyright 2014 Diane Scott Docking 33

Secondary Stock Offerings

New stock issued by firm that already has shares outstandingQuanta Services-secondary stock offering

Filed an S-3

http://www.sec.gov/Archives/edgar/data/1050915/000095012904002449/h14786sv3.htm

Copyright 2014 Diane Scott Docking 34

Regulation of the Primary Market

Securities and Exchange Commission (SEC) regulates underwriting activities

Securities Act of 1933 governs issuance of securities

Rule 415: Shelf Registration Rule file single registration document for selling securities on

a continuous basis (within 2 years)

CryoLife’s Shelf Registration: S-3 and check Rule 415

http://www.sec.gov/Archives/edgar/data/784199/000091406204000552/0000914062-04-000552-index.htm

Copyright 2014 Diane Scott Docking 35

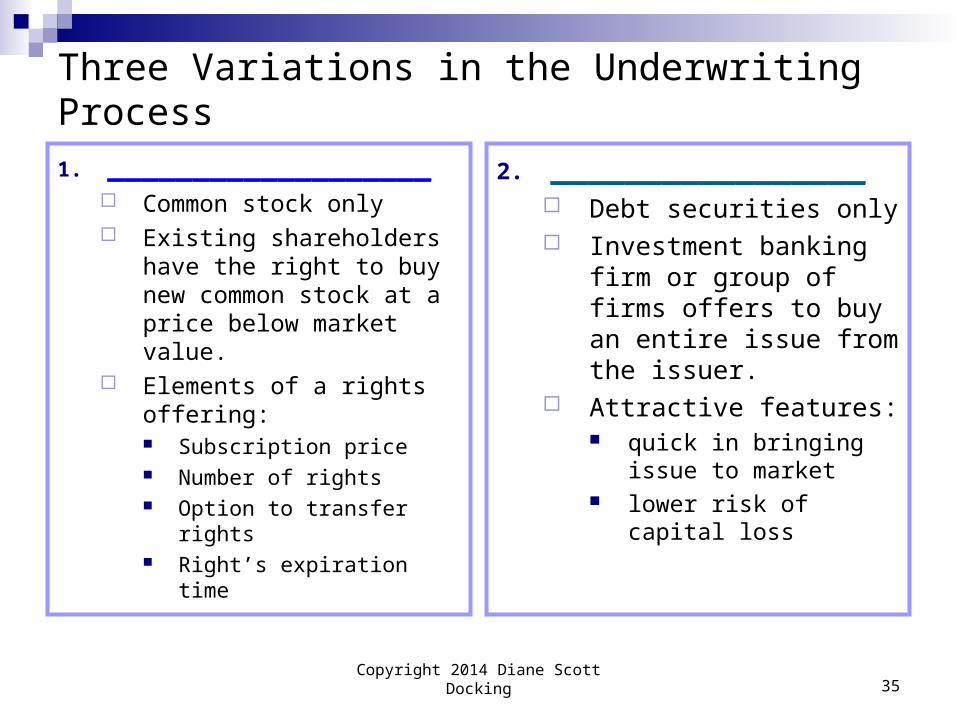

Three Variations in the Underwriting Process

1. ___________________ Common stock only Existing shareholders

have the right to buy new common stock at a price below market value.

Elements of a rights offering: Subscription price Number of rights Option to transfer rights Right’s expiration time

2. _________________ Debt securities only Investment banking firm

or group of firms offers to buy an entire issue from the issuer.

Attractive features: quick in bringing issue to

market lower risk of capital loss

Copyright 2014 Diane Scott Docking 36

Three Variations in the Underwriting Process

3. ______________________ Applies to stocks and bonds Mandatory for certain securities of regulated

utilities and municipals Competitive Bidding Underwriting

______________________________ All at same bid price

______________________________ All at individual bid price

Copyright 2014 Diane Scott Docking 37

Private Placement of Securities

Sale of securities to a limited number of institutional investors.

SEC specified conditions to be met for private placement.

Issuers usually work with investment bankers.

Rule 144A offering or non-Rule 144A offering

Copyright 2014 Diane Scott Docking 38

Rule 144 A SEC rule permitting large institutions to trade

securities acquired in a private placement among themselves without having to register these securities with the SEC.

SEC Rule 144A improves liquidity of privately placed securities.

Encourages non-U.S. firms to issue securities in the U.S. private placement market.

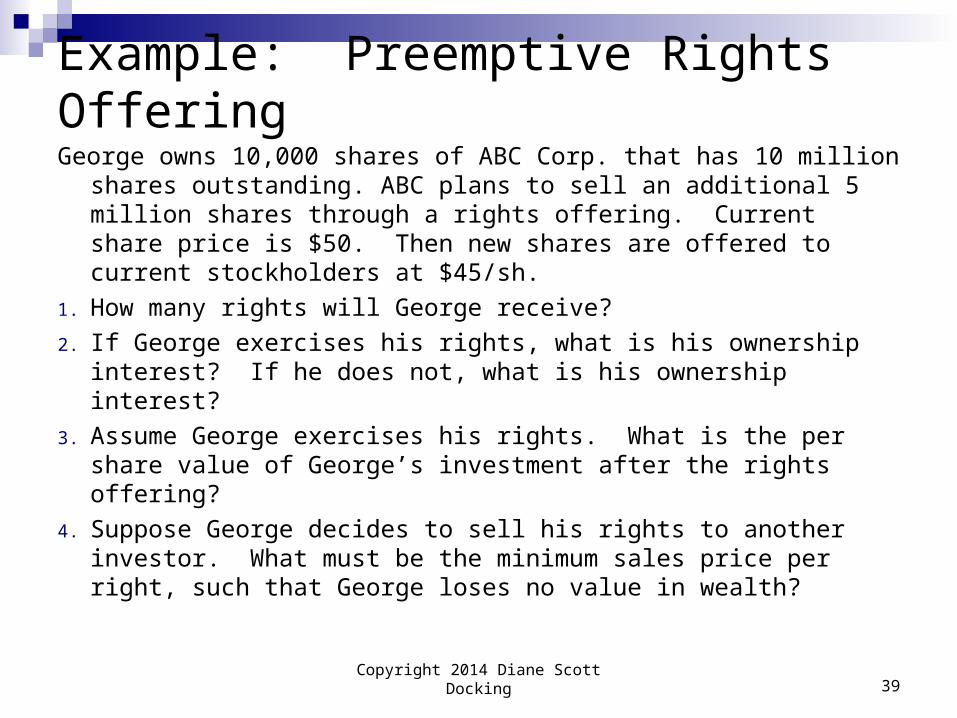

Example: Preemptive Rights Offering

George owns 10,000 shares of ABC Corp. that has 10 million shares outstanding. ABC plans to sell an additional 5 million shares through a rights offering. Current share price is $50. Then new shares are offered to current stockholders at $45/sh.

1. How many rights will George receive?

2. If George exercises his rights, what is his ownership interest? If he does not, what is his ownership interest?

3. Assume George exercises his rights. What is the per share value of George’s investment after the rights offering?

4. Suppose George decides to sell his rights to another investor. What must be the minimum sales price per right, such that George loses no value in wealth?

Copyright 2014 Diane Scott Docking 39

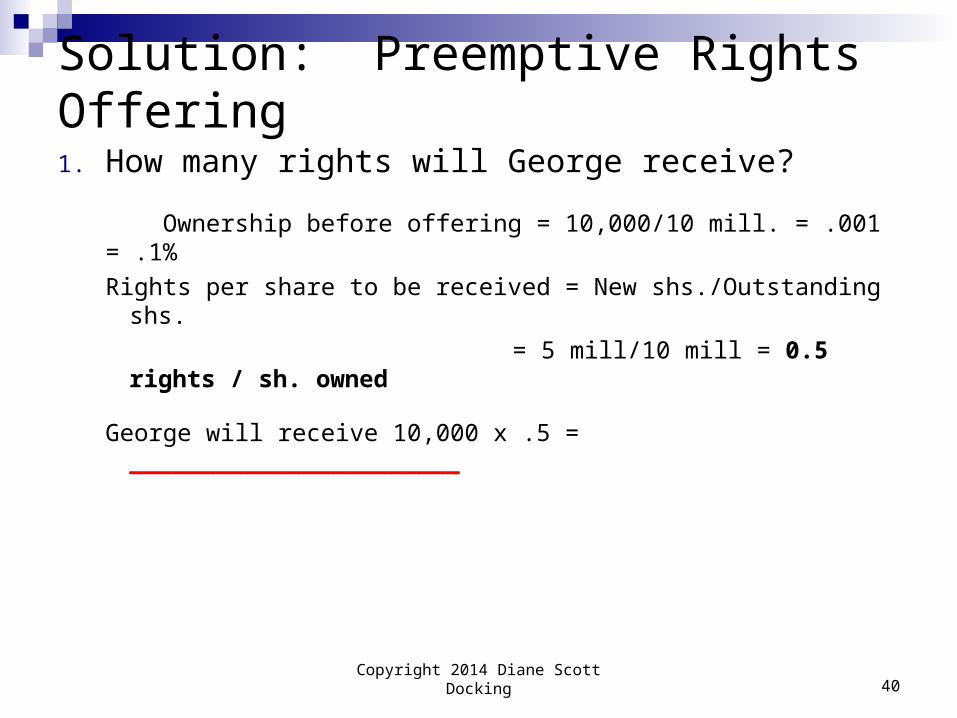

Solution: Preemptive Rights Offering

1. How many rights will George receive?

Ownership before offering = 10,000/10 mill. = .001 = .1%

Rights per share to be received = New shs./Outstanding shs.

= 5 mill/10 mill = 0.5 rights / sh. owned

George will receive 10,000 x .5 = _______________________

Copyright 2014 Diane Scott Docking 40

Solution: Preemptive Rights Offering

2. If George exercises his rights, what is his ownership interest? If he does not, what is his ownership interest?

Ownership after exercising rights =

= (10,000 +5,000)/(10 mil. + 5 mil.)

= 15,000/15 mill. = _______________________

Ownership interest if he does not exercise rights =

= 10,000/15 mill. = .000667 = ______________________

Copyright 2014 Diane Scott Docking 41

Solution: Preemptive Rights Offering

3. Assume George exercises his rights. What is the per share value of George’s investment after the rights offering?

Share value before offering = 10,000 x $50/sh = $500,000

Cost of rights = 5,000 x $45/sh = $225,000

15,000 $725,000

Share value after = $725,000/15,000 = _________________

It is same for Total Firm:

15 mill. shs x $48.33 = $725 mill.

Copyright 2014 Diane Scott Docking 42

Solution: Preemptive Rights Offering

4. Suppose George decides to sell his rights to another investor. What must be the minimum sales price per right, such that George loses no value in wealth?

$48.33 - $45 = _____________________

Total wealth:

Stock value 10,000 shs x $48.33 = $483,333.33

Rights sold 5,000 x $3.33 = 16,666.67

Wealth remains the same as before offering = $500,000

Copyright 2014 Diane Scott Docking 43