copyright © 2014 mcgraw-hill ryerson limited 3-1 powerpoint author: robert g. ducharme, macc, cpa,...

TRANSCRIPT

Copyright © 2014 McGraw-Hill Ryerson Limited

3-1

PowerPoint Author:

Robert G. Ducharme, MAcc, CPA, CAUniversity of Waterloo, School of Accounting and Finance

FINANCIALACCOUNTINGFifth Canadian Edition LIBBY, LIBBY, SHORT, KANAAN, GOWING

FINANCIALACCOUNTINGFifth Canadian Edition LIBBY, LIBBY, SHORT, KANAAN, GOWING

Operating Decisions and the Statement of Earnings

Chapter 3

3-2

Copyright © 2014 McGraw-Hill Ryerson Limited

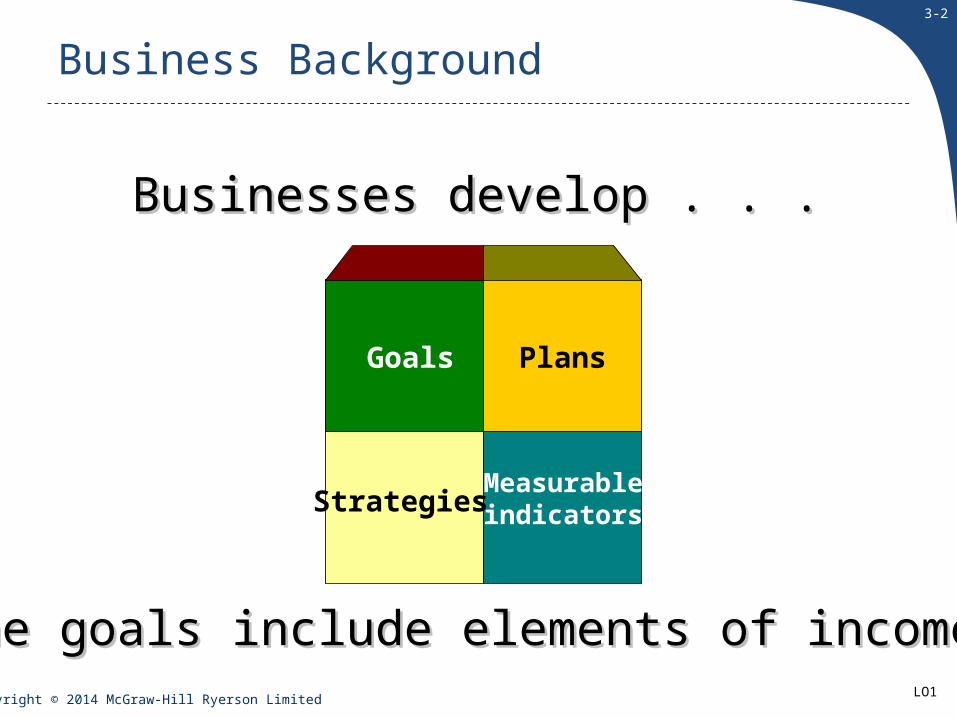

Goals Plans

StrategiesMeasurableindicators

Businesses develop . . .Businesses develop . . .

The goals include elements of income.The goals include elements of income.

Business Background

LO1

3-3

Copyright © 2014 McGraw-Hill Ryerson Limited

Understanding the Business

How do business activitiesHow do business activitiesaffect the statement of earnings?affect the statement of earnings?

How do business activitiesHow do business activitiesaffect the statement of earnings?affect the statement of earnings?

How are these activitiesHow are these activities recognized and measured?recognized and measured?

How are these activitiesHow are these activities recognized and measured?recognized and measured?

How are these activities How are these activities reported on thereported on the

statement of earnings?statement of earnings?

How are these activities How are these activities reported on thereported on the

statement of earnings?statement of earnings?

LO1

3-4

Copyright © 2014 McGraw-Hill Ryerson Limited

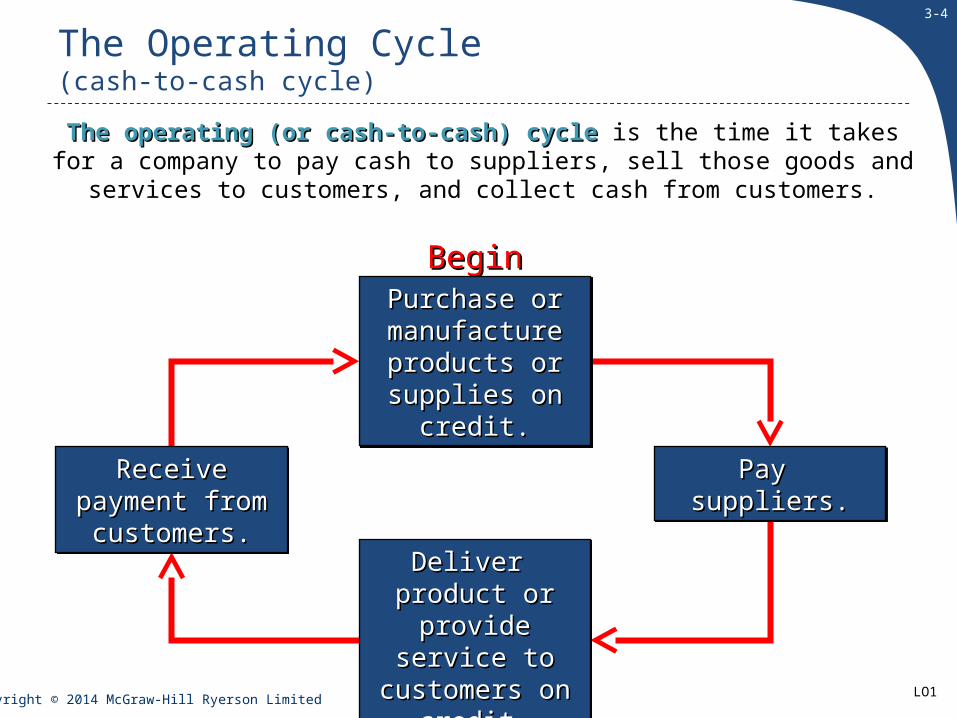

The Operating Cycle(cash-to-cash cycle)

BeginBeginPurchase or Purchase or manufacture manufacture products or products or supplies on supplies on

credit.credit.

Purchase or Purchase or manufacture manufacture products or products or supplies on supplies on

credit.credit.

Deliver product Deliver product or provide service or provide service to customers on to customers on

credit.credit.

Deliver product Deliver product or provide service or provide service to customers on to customers on

credit.credit.

Pay Pay suppliers.suppliers.

Pay Pay suppliers.suppliers.

Receive payment Receive payment from customers.from customers.

Receive payment Receive payment from customers.from customers.

The operating (or cash-to-cash) cycleThe operating (or cash-to-cash) cycle is the time it takes for a company to pay cash to suppliers, sell those goods and

services to customers, and collect cash from customers.

LO1

3-5

Copyright © 2014 McGraw-Hill Ryerson Limited

To meet the needs of decision makers, we report financial information for relatively short timerelatively short time

periodsperiods (monthly, quarterly, annually).

2011 2012 2013 2014 2015 2016 2017 2018

Life of the BusinessLife of the Business

Annual Accounting Periods

The Periodicity Assumption

LO1

3-6

Copyright © 2014 McGraw-Hill Ryerson Limited

The Operating Cycle – Underlying Accounting Assumptions

Time Period:Time Period: The long life of a company can be The long life of a company can be reported over a series of shorter time periodsreported over a series of shorter time periods..

Time Period:Time Period: The long life of a company can be The long life of a company can be reported over a series of shorter time periodsreported over a series of shorter time periods..

Recognition Issues :Recognition Issues : When should the effects of When should the effects of operating activities be recognized (recorded)?operating activities be recognized (recorded)?

Recognition Issues :Recognition Issues : When should the effects of When should the effects of operating activities be recognized (recorded)?operating activities be recognized (recorded)?

Measurement Issues:Measurement Issues: What amounts should be What amounts should be recognized?recognized?

Measurement Issues:Measurement Issues: What amounts should be What amounts should be recognized?recognized?

LO1

3-7

Copyright © 2014 McGraw-Hill Ryerson Limited

Earnings per shareEarnings per share

Results of continuing operationsResults of continuing operations

Results of discontinued operationsResults of discontinued operations

Elements on the Classified Statement of Earnings

The statement of earnings includes up to three major sections:

= net earnings

LO2

3-8

Copyright © 2014 McGraw-Hill Ryerson Limited

Results of continuing operationsResults of continuing operations can be presented in one of the two formats

Single step format list all revenues followed by all expense items and then shows the difference between revenue and expenses

Multiple step format cost of goods sold are deducted from sales to present gross margin (or gross profit) as a subtotal. Other operating expenses are then deducted to show operating earnings (income) as a second subtotal

Elements on the Classified Statement of Earnings

LO2

3-9

Copyright © 2014 McGraw-Hill Ryerson Limited

Elements on the Statement of Earnings

LossesDecreases in assets or increases in

liabilities from peripheral transactions.

LossesDecreases in assets or increases in

liabilities from peripheral transactions.

RevenuesIncreases in assets or settlement of liabilities from ongoing operations.

RevenuesIncreases in assets or settlement of liabilities from ongoing operations.

ExpensesDecreases in assets or increases in liabilities from ongoing operations.

ExpensesDecreases in assets or increases in liabilities from ongoing operations.

GainsIncreases in assets or settlement of

liabilities from peripheral transactions.

GainsIncreases in assets or settlement of

liabilities from peripheral transactions.

LO2

3-10

Copyright © 2014 McGraw-Hill Ryerson Limited

Discontinued OperationsResult from the disposal of a major segment of the business and are

reported net of the related income tax effect.

Elements on the Statement of Earnings

Discontinued operations are presented separately because of their non-recurring nature and thus are not useful in predicting the future earnings of the

company.

LO2

3-11

Copyright © 2014 McGraw-Hill Ryerson LimitedLO2

Elements on the Statement of Earnings

3-12

Copyright © 2014 McGraw-Hill Ryerson Limited

How Are Operating Activities Recognized and Measured?

Revenue is recordedRevenue is recordedwhen cash is received.when cash is received.Revenue is recordedRevenue is recorded

when cash is received.when cash is received.Expenses are recordedExpenses are recorded

when cash is paid.when cash is paid.Expenses are recordedExpenses are recorded

when cash is paid.when cash is paid.

Cash Basis

LO3

3-13

Copyright © 2014 McGraw-Hill Ryerson Limited

Assets, liabilities, revenues, and expenses should be Assets, liabilities, revenues, and expenses should be recognized when the transaction that causes them recognized when the transaction that causes them

occurs, occurs, not necessarily when cash is paid or received.not necessarily when cash is paid or received.

Assets, liabilities, revenues, and expenses should be Assets, liabilities, revenues, and expenses should be recognized when the transaction that causes them recognized when the transaction that causes them

occurs, occurs, not necessarily when cash is paid or received.not necessarily when cash is paid or received.

Required by -

International

Financial

Reporting

Standards

Required by -

International

Financial

Reporting

Standards

How Are Operating Activities Recognized and Measured?

Accrual Accounting

Required by -

Generally

Acceptable

Accounting

Principles

Required by -

Generally

Acceptable

Accounting

PrinciplesLO3

3-14

Copyright © 2014 McGraw-Hill Ryerson Limited

Revenue Principle

Recognize revenues when . . .Recognize revenues when . . .The entity has transferred to the buyer the The entity has transferred to the buyer the

significant risks and rewards of ownership.significant risks and rewards of ownership.The entity retains neither continuing The entity retains neither continuing

managerial involvement nor effective control managerial involvement nor effective control over the goods sold. over the goods sold.

The amount of revenue can be reliably The amount of revenue can be reliably measured.measured.

Collection is reasonably assured.Collection is reasonably assured.The costs in respect of the transaction can be The costs in respect of the transaction can be

measured reliably.measured reliably.

Recognize revenues when . . .Recognize revenues when . . .The entity has transferred to the buyer the The entity has transferred to the buyer the

significant risks and rewards of ownership.significant risks and rewards of ownership.The entity retains neither continuing The entity retains neither continuing

managerial involvement nor effective control managerial involvement nor effective control over the goods sold. over the goods sold.

The amount of revenue can be reliably The amount of revenue can be reliably measured.measured.

Collection is reasonably assured.Collection is reasonably assured.The costs in respect of the transaction can be The costs in respect of the transaction can be

measured reliably.measured reliably.

LO3

3-15

Copyright © 2014 McGraw-Hill Ryerson Limited

Revenue Principlesituation #1 – cash is received BEFORE revenue is earned

If cash is received before the company If cash is received before the company delivers goods or services, the liability delivers goods or services, the liability

account account DEFERRED REVENUEDEFERRED REVENUE is recorded. is recorded.

Cash is received before revenue is earned -

CashReceived

Cash (+A) xxx Deferred revenue (+L) xxx

LO3

3-16

Copyright © 2014 McGraw-Hill Ryerson Limited

Revenue Principlesituation #1 – cash is received BEFORE revenue is earned

When the company delivers the goods or When the company delivers the goods or services services DEFERRED REVENUEDEFERRED REVENUE is reduced is reduced

and and REVENUEREVENUE is recorded.is recorded.

Cash is received before revenue is earned -

CashReceived

Company Delivers

Cash (+A) xxx Deferred revenue (+L) xxx

Revenue will be recorded when earned.

Deferred revenue (-L) xxx Service revenue (+R) xxx

LO3

3-17

Copyright © 2014 McGraw-Hill Ryerson Limited

Revenue Principlesituation #1 – cash is received BEFORE revenue is earned

CASH COLLECTED (Goods or services due to

customers)over time will

become

REVENUE (Earned when goods or services provided)

Rent collected in advance Rent revenue

Deferred air traffic revenue Air traffic revenue

Deferred subscription revenue Subscription revenue

Typical liabilities that becomeTypical liabilities that becomerevenue when earned include . . .revenue when earned include . . .

LO3

3-18

Copyright © 2014 McGraw-Hill Ryerson Limited

Revenue Principlesituation #2 – cash is received ON the date revenue is earned

When cash is received on the date When cash is received on the date the revenue is earned, the the revenue is earned, the following entry is made:following entry is made:

CashReceived

Company Delivers

Cash (+A) xxx Revenue (+R) xxx

ANDAND

LO3

3-19

Copyright © 2014 McGraw-Hill Ryerson Limited

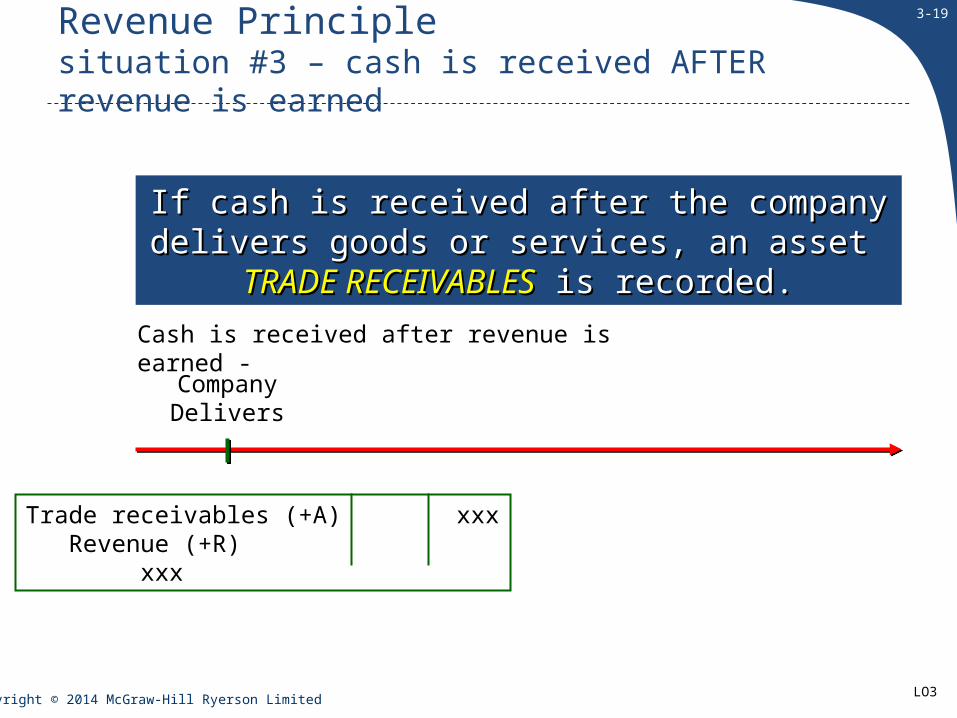

Revenue Principlesituation #3 – cash is received AFTER revenue is earned

If cash is received after the company If cash is received after the company delivers goods or services, an asset delivers goods or services, an asset TRADE TRADE

RECEIVABLESRECEIVABLES is recorded. is recorded.

Cash is received after revenue is earned -

Trade receivables (+A) xxx Revenue (+R) xxx

Company Delivers

LO3

3-20

Copyright © 2014 McGraw-Hill Ryerson Limited

Revenue Principlesituation #3 – cash is received AFTER revenue is earned

CashReceived

Trade receivables (+A) xxx Revenue (+R) xxx

Cash is received after revenue is earned -

Company Delivers

When the cash is received the When the cash is received the TRADE TRADE RECEIVABLESRECEIVABLES is reduced. is reduced.

Cash will be collected.

Cash (+A) xxx Trade receivables (-A) xxx

LO3

3-21

Copyright © 2014 McGraw-Hill Ryerson Limited

Revenue Principlesituation #3 – cash is received AFTER revenue is earned

CASH TO BE COLLECTED

(Owed by customers)

and already earned as

REVENUE (Earned when

goods or services provided)

Interest receivable Interest revenue

Rent receivable Rent revenue

Royalties receivable Royalty revenue

Assets reflecting revenues earned butAssets reflecting revenues earned butnot yet received in cash include . . .not yet received in cash include . . .

LO3

3-22

Copyright © 2014 McGraw-Hill Ryerson Limited

The Matching Process

Resources Resources consumed to earn consumed to earn

revenues in an revenues in an accounting period accounting period

should be recorded should be recorded in that period, in that period,

regardless of when regardless of when cash is paidcash is paid..

Resources Resources consumed to earn consumed to earn

revenues in an revenues in an accounting period accounting period

should be recorded should be recorded in that period, in that period,

regardless of when regardless of when cash is paidcash is paid..

LO3

3-23

Copyright © 2014 McGraw-Hill Ryerson Limited

The Matching Processsituation #1 – cash is paid BEFORE expense is incurred

If cash is paid before the company receives If cash is paid before the company receives goods or services, an asset account, goods or services, an asset account,

PREPAID EXPENSEPREPAID EXPENSE is recorded. is recorded.

Cash is paid before expense is incurred -

$Paid

Prepaid expense (+A) xxx Cash (-A) xxx

LO3

3-24

Copyright © 2014 McGraw-Hill Ryerson Limited

The Matching Processsituation #1 – cash is paid BEFORE expense is incurred

ExpenseIncurred

When the expense is incurred When the expense is incurred PREPAID PREPAID EXPENSEEXPENSE is reduced and an is reduced and an EXPENSEEXPENSE is is

recorded.recorded.

Cash is paid before expense is incurred -$

Paid

Prepaid expense (+A) xxx Cash (-A) xxx

Expense will be recorded when incurred.

Expense (+E) xxx Prepaid expense (-A) xxx

LO3

3-25

Copyright © 2014 McGraw-Hill Ryerson Limited

The Matching Processsituation #1 – cash is paid BEFORE expense is incurred

CASH PAID FORas used over

time becomes EXPENSE

Supplies inventory Supplies expense

Prepaid insurance Insurance expense

Buildings and equipment Depreciation expense

Typical assets and their relatedTypical assets and their relatedexpense accounts include. . .expense accounts include. . .

LO3

3-26

Copyright © 2014 McGraw-Hill Ryerson Limited

The Matching Processsituation #2 – cash is paid ON the date expense is incurred

When cash is paid on the date the When cash is paid on the date the expense is incurred, the following expense is incurred, the following

entry is made:entry is made:

CashPaid

ExpenseIncurred

Expense (+E) xxx Cash (-A) xxx

AND

LO3

3-27

Copyright © 2014 McGraw-Hill Ryerson Limited

The Matching Processsituation #3 – cash is paid AFTER expense is incurred

CashPaid

When cash is paid the When cash is paid the PAYABLEPAYABLE is reduced. is reduced.

Cash is paid after expense is incurred -

ExpenseIncurred

Expense (+E) xxx Payable (+L) xxx

Cash will be paid.

Payable (-L) xxx Cash (-A) xxx

LO3

3-28

Copyright © 2014 McGraw-Hill Ryerson Limited

The Matching Processsituation #3 – cash is paid AFTER expense is incurred

If cash is paid after the company receives If cash is paid after the company receives goods or services, a liability goods or services, a liability PAYABLEPAYABLE is is

recorded.recorded.

Cash is paid after expense is incurred -

Expense (+E) xxx Payable (+L) xxx

ExpenseIncurred

LO3

3-29

Copyright © 2014 McGraw-Hill Ryerson Limited

A Question of Ethics

LO3

3-30

Copyright © 2014 McGraw-Hill Ryerson Limited

A = L + SEA = L + SEASSETSASSETS

Debit for

Increase

Credit for

Decrease

LIABILITIESLIABILITIES

Debit for

Decrease

Credit for

Increase

Next, let’s see how Next, let’s see how Revenues and Revenues and

Expenses affect Expenses affect Retained Earnings.Retained Earnings.

LO4

RETAINED RETAINED EARNINGSEARNINGS

Debit for

Decrease

Credit for

Increase

CONTIBUTED CONTIBUTED CAPITALCAPITAL

Debit for

Decrease

Credit for

Increase

OTHER OTHER COMPONENTSCOMPONENTS

Debit for

Decrease

Credit for

Increase

3-31

Copyright © 2014 McGraw-Hill Ryerson Limited

EXPENSES and EXPENSES and LOSSESLOSSES

Debit for

Increase

Credit for

Decrease

REVENUES and REVENUES and GAINSGAINS

Debit for

Decrease

Credit for

Increase

RETAINED RETAINED EARNINGSEARNINGS

Debit for

Decrease

Credit for

Increase

The Expanded Transaction Analysis Model

Net losses and Net losses and dividends decrease dividends decrease Retained Earnings.Retained Earnings.

Net earnings increase Net earnings increase Retained Earnings.Retained Earnings.

LO4

3-32

Copyright © 2014 McGraw-Hill Ryerson Limited

(a) Sun-Rype sold fruit-based beverages and snacks to customers for $3,520 in cash. The cost of these sales was $1,960.

Analyzing Some of Sun-Rype’s Transactions

Debit Credit(a) Cash (+A) 3,520

Sales Revenue (+R, +SE) 3,520 Cost of Sales (+E, -SE) 1,960 Inventories (-A) 1,960

= Liabilities +Cash +3,520 Sales Revenue (+R, +SE) +3,520Inventories -1,960 Cost of Sales (+E, -SE) -1,960

Assets Shareholders' Equity

Equality checks:1.Debits $5,480 equal Credits $5,480,2.The accounting equation is in balance.

LO4

3-33

Copyright © 2014 McGraw-Hill Ryerson Limited

(b) Sun-Rype sold food and beverage products to retail outlets for $3,020; $2,020 was received in cash and the rest was due from the

outlets. The cost of products sold was $1,400.

Analyzing Some of Sun-Rype’s Transactions

Debit Credit(b) Cash (+A) 2,020

Trade Receivables (+A) 1,000 Sales Revenue (+R, +SE) 3,020 Cost of Sales (+E, -SE) 1,400 Inventories (-A) 1,400

= Liabilities +Cash +2,020 Sales Revenue (+R, +SE) +3,020Trade Receivables +1,000 Cost of Sales (+E, -SE) -1,400Inventories -1,400

Assets Shareholders' Equity

Equality checks:1.Debits $4,420 equal Credits $4,420,2.The accounting equation is in balance.

LO4

3-34

Copyright © 2014 McGraw-Hill Ryerson Limited

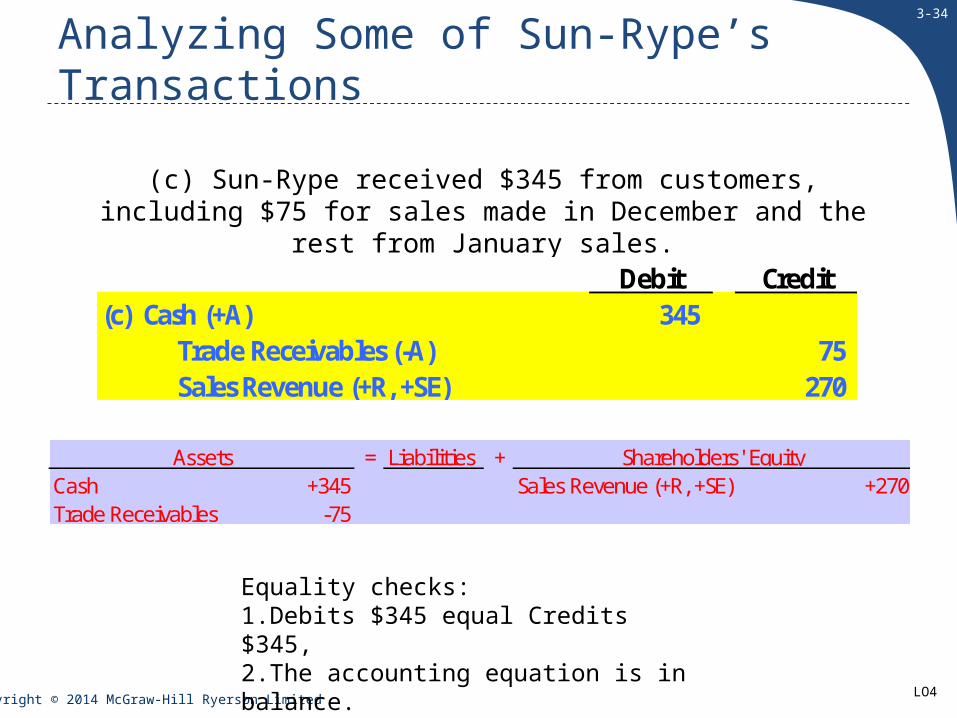

(c) Sun-Rype received $345 from customers, including $75 for sales made in December and the rest from January sales.

Analyzing Some of Sun-Rype’s Transactions

Debit Credit(c) Cash (+A) 345

Trade Receivables (-A) 75 Sales Revenue (+R, +SE) 270

= Liabilities +Cash +345 Sales Revenue (+R, +SE) +270Trade Receivables -75

Assets Shareholders' Equity

Equality checks:1.Debits $345 equal Credits $345,2.The accounting equation is in balance.

LO4

3-35

Copyright © 2014 McGraw-Hill Ryerson Limited

(d) Sun-Rype signed contracts with new clients and received $50 cash. The company earned $40 immediately by performing services

for these clients; the rest will be earned over the next several months.

Analyzing Some of Sun-Rype’s Transactions

Debit Credit(d) Cash (+A) 50

Service Revenue (+R, +SE) 40 Deferred Service Revenue (+L) 10

= Liabilities +Cash +50 Deferred Service Revenue +10 Sales Revenue (+R,+SE) +40

Assets Shareholders' Equity

Equality checks:1.Debits $50 equal Credits $50,2.The accounting equation is in balance.

LO4

3-36

Copyright © 2014 McGraw-Hill Ryerson Limited

(e) Sun-Rype paid $740 in advance for the following: $160 for insurance covering the next four months beginning January 1, $450 for rent of warehousing facilities for the next three months beginning

January 1, and $130 for advertising to be run in February.

Analyzing Some of Sun-Rype’s Transactions

Debit Credit(e) Prepayments (+A) 740

Cash (-A) 740

= Liabilities +Cash -740Prepayments +740

Assets Shareholders' Equity

Equality checks:1.Debits $740 equal Credits $740,2.The accounting equation is in balance.

LO4

3-37

Copyright © 2014 McGraw-Hill Ryerson Limited

(f) Sun-Rype paid $731 for utilities, repairs, and fuel for delivery vehicles, all considered distribution expenses.

Analyzing Some of Sun-Rype’s Transactions

Debit Credit(f) Distribution Expenses (+E, -SE) 731

Cash (-A) 731

= Liabilities +Cash -731 Distribution Expenses (+E, -SE) -731

Assets Shareholders' Equity

Equality checks:1.Debits $731 equal Credits $731,2.The accounting equation is in balance.

LO4

3-38

Copyright © 2014 McGraw-Hill Ryerson LimitedLO4

The balances in the statement of financial position accounts and statement of earnings accounts after posting the transactions to the T-accounts (all revenue and expense accounts begin with a zero balance).

3-39

Copyright © 2014 McGraw-Hill Ryerson Limited

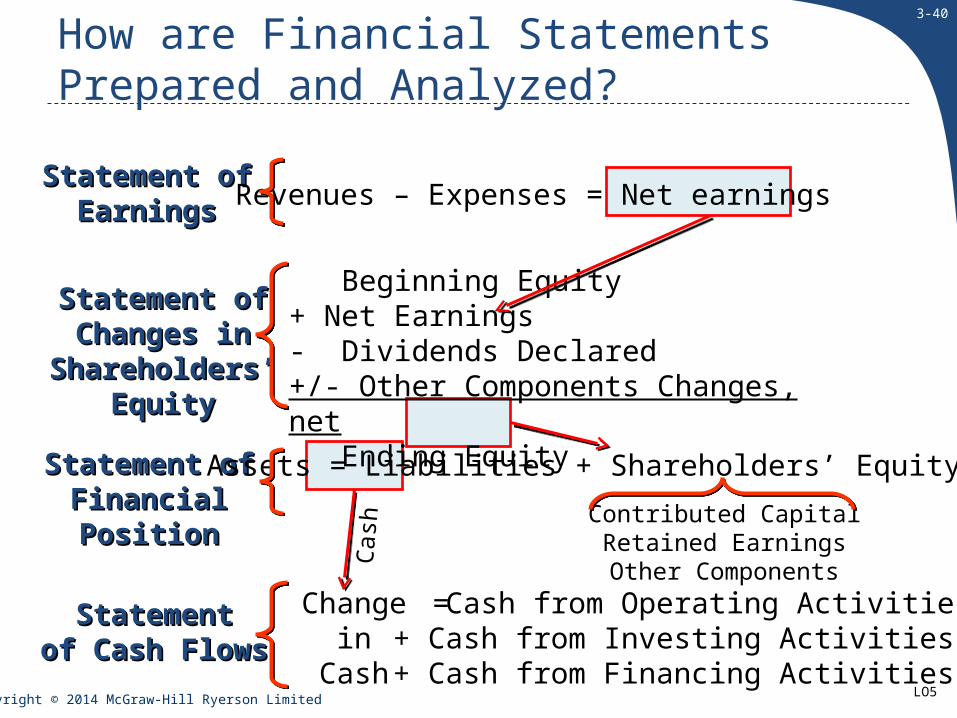

How are Financial Statements Prepared and Analyzed?

Statement ofStatement ofEarningsEarnings Revenues – Expenses = Net Earnings

Statement ofStatement ofChanges inChanges in

Shareholders’Shareholders’EquityEquity

Beginning Equity+ Net Earnings- Dividends Declared+/- Other Components Changes, net Ending Equity

Statement ofStatement ofFinancialFinancialPositionPosition

Assets = Liabilities + Shareholders’ Equity

Contributed CapitalRetained EarningsOther Components

StatementStatementof Cash Flowsof Cash Flows

Changein

Cash

= Cash from Operating Activities+ Cash from Investing Activities+ Cash from Financing Activities

LO5

3-40

Copyright © 2014 McGraw-Hill Ryerson Limited

How are Financial Statements Prepared and Analyzed?

Statement ofStatement ofEarningsEarnings Revenues – Expenses = Net earnings

Statement ofStatement ofChanges inChanges in

Shareholders’Shareholders’EquityEquity

Beginning Equity+ Net Earnings- Dividends Declared+/- Other Components Changes, net Ending Equity

Statement ofStatement ofFinancialFinancialPositionPosition

Assets = Liabilities + Shareholders’ Equity

Contributed CapitalRetained EarningsOther Components

StatementStatementof Cash Flowsof Cash Flows

Changein

Cash

= Cash from Operating Activities+ Cash from Investing Activities+ Cash from Financing Activities

Cas

h

LO5

3-41

Copyright © 2014 McGraw-Hill Ryerson Limited

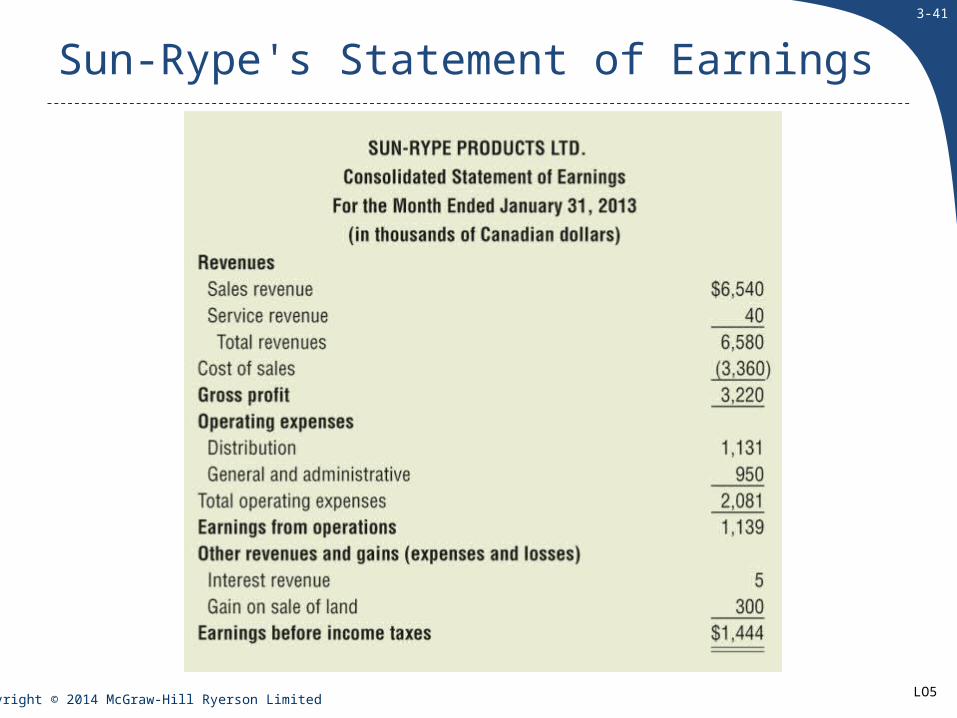

Sun-Rype's Statement of Earnings

LO5

3-42

Copyright © 2014 McGraw-Hill Ryerson Limited

Focus on Cash Flows

Effect onOperating activities Cash Flows Cash received: Customers +

Interest and div idends on investments + Cash paid: Suppliers -

Employees -Interest on debt obligations -Income taxes -

Cash Flows from Operating Activities TotalInvesting Activities Purchase of property, plant or equipment - Purchase of other long-term assets - Sale of property, plant or equipment + Sale of other long-term assets + Cash Flows from Investing Activities TotalFinancing Activities Issuance of long-term debt + Issuance of contributed capital + Dividends paid - Repurchase of long-term debt - Repurchase of contributed capital - Cash Flows from Financing Activities Total Net increase or (decrease) in cash Beginning balance in cash account Ending balance in cash account

Direct approach to preparing operating cash flows.

Direct approach to preparing operating cash flows.

LO6

3-43

Copyright © 2014 McGraw-Hill Ryerson Limited

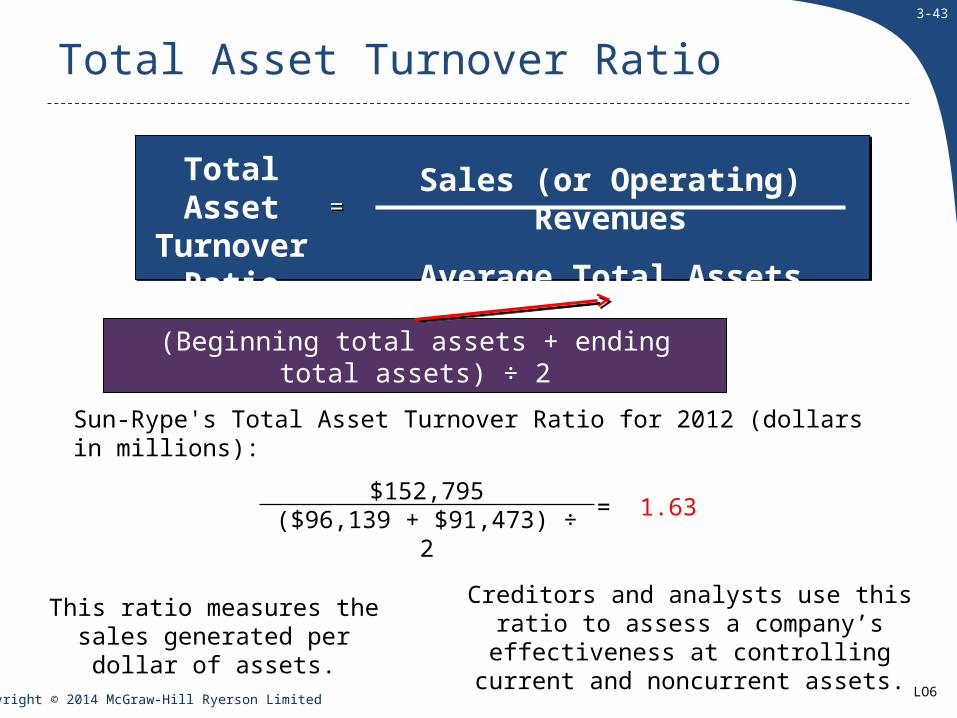

Total Asset Turnover Ratio

Total AssetTurnover

Ratio

Sales (or Operating) Revenues

Average Total Assets==

(Beginning total assets + ending total assets) ÷ 2

Sun-Rype's Total Asset Turnover Ratio for 2012 (dollars in millions):

$152,795($96,139 + $91,473) ÷ 2 = 1.63

This ratio measures the sales generated per dollar of assets.

Creditors and analysts use this ratio to assess a company’s effectiveness at

controlling current and noncurrent assets.

LO6

3-44

Copyright © 2014 McGraw-Hill Ryerson Limited

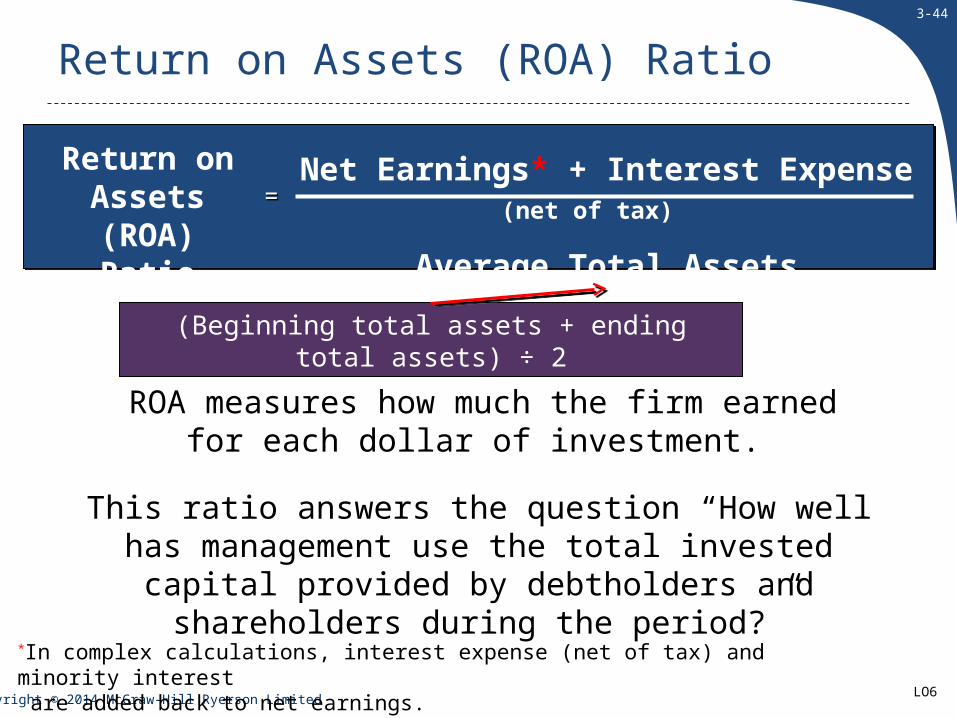

Return on Assets (ROA) Ratio

ROA measures how much the firm earned for each dollar of investment.

*In complex calculations, interest expense (net of tax) and minority interest are added back to net earnings.

Return on Assets (ROA)

Ratio

Net Earnings* + Interest Expense (net of tax)

Average Total Assets

==

(Beginning total assets + ending total assets) ÷ 2

This ratio answers the question “How well has management use the total invested capital provided by

debtholders and shareholders during the period?”

LO6

3-45

Copyright © 2014 McGraw-Hill Ryerson Limited

End of Chapter 3