copyright © 2014 pearson education chapter 10 considering internal control

TRANSCRIPT

Copyright © 2014 Pearson Education

Chapter 10

Considering Internal Control

Chapter 10

Considering Internal Control

Copyright © 2014 Pearson Education10-2

Describe the three primary objectives of effective internal control.

Contrast management’s responsibilities for maintaining internal control with the auditor’s responsibilities for evaluating and reporting on internal control.

Explain the five components of the COSO internal control framework.

Obtain and document an understanding of internal control.

Copyright © 2014 Pearson Education10-3

Assess control risk by linking key controls and control deficiencies to transaction-related audit objectives.

Describe the process of designing and performing tests of controls.

Understand Section 404 requirements for auditor reporting on internal control.

Describe the differences in evaluating, reporting, and testing internal control for nonpublic companies.

Copyright © 2014 Pearson Education

Describe the three primary objectives of effective internal control.

11

10-4

Copyright © 2014 Pearson Education10-5

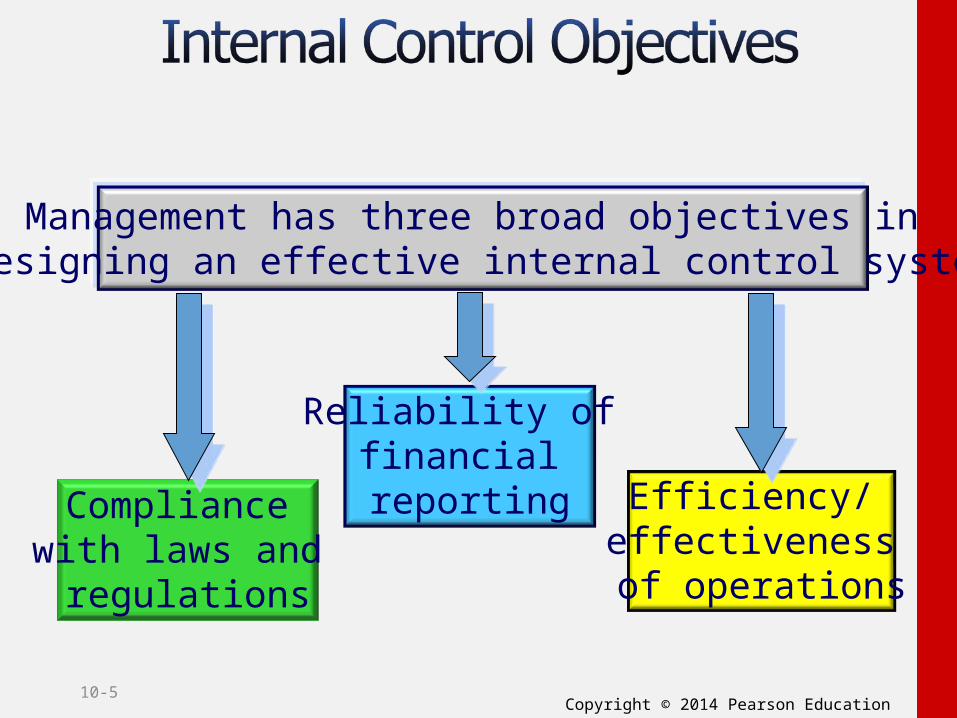

Management has three broad objectives in designing an effective internal control system

Compliance with laws and

regulations

Reliability of financial reporting Efficiency/

effectiveness of operations

Copyright © 2014 Pearson Education

Contrast management’s responsibilities for maintaining internal control with the auditor’s responsibilities for evaluating and reporting

on internal control.

22

10-6

Copyright © 2014 Pearson Education10-7

Management must establish and maintain the entity’s internal controls

Management’s design and implementation of internal controls is based on two key underlying concepts:

Reasonable assurance

Inherent limitations

Copyright © 2014 Pearson Education10-8

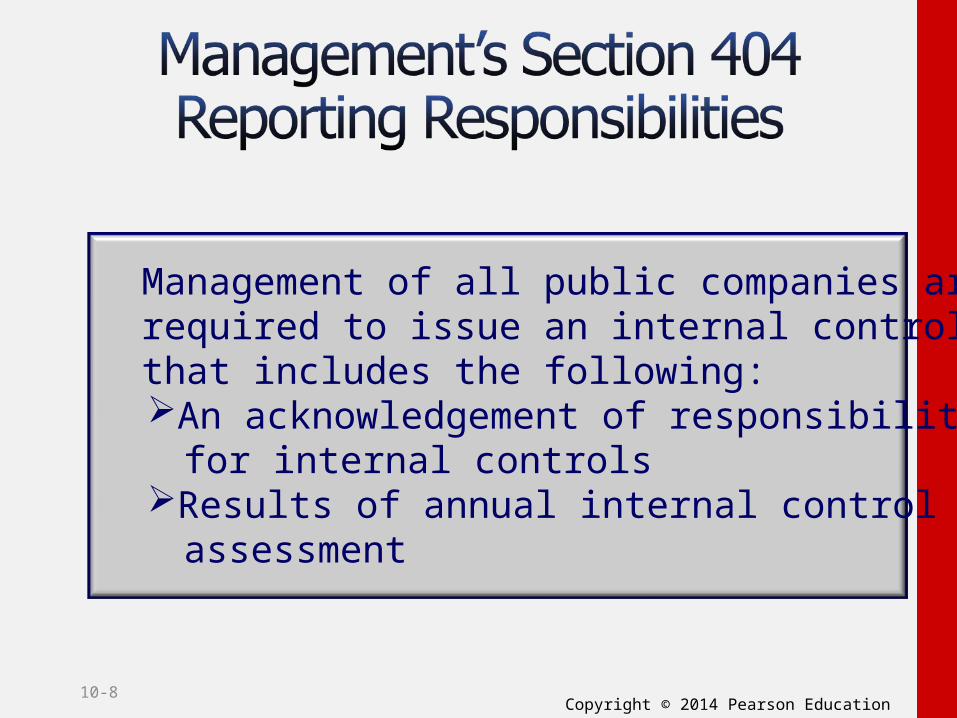

Management of all public companies are required to issue an internal control report that includes the following:An acknowledgement of responsibility

for internal controlsResults of annual internal control

assessment

Copyright © 2014 Pearson Education10-9

Management must evaluate the design of internal controls over financial reporting.

Management must also test the operating effectiveness of those controls.

Copyright © 2014 Pearson Education10-10

Copyright © 2014 Pearson Education10-11

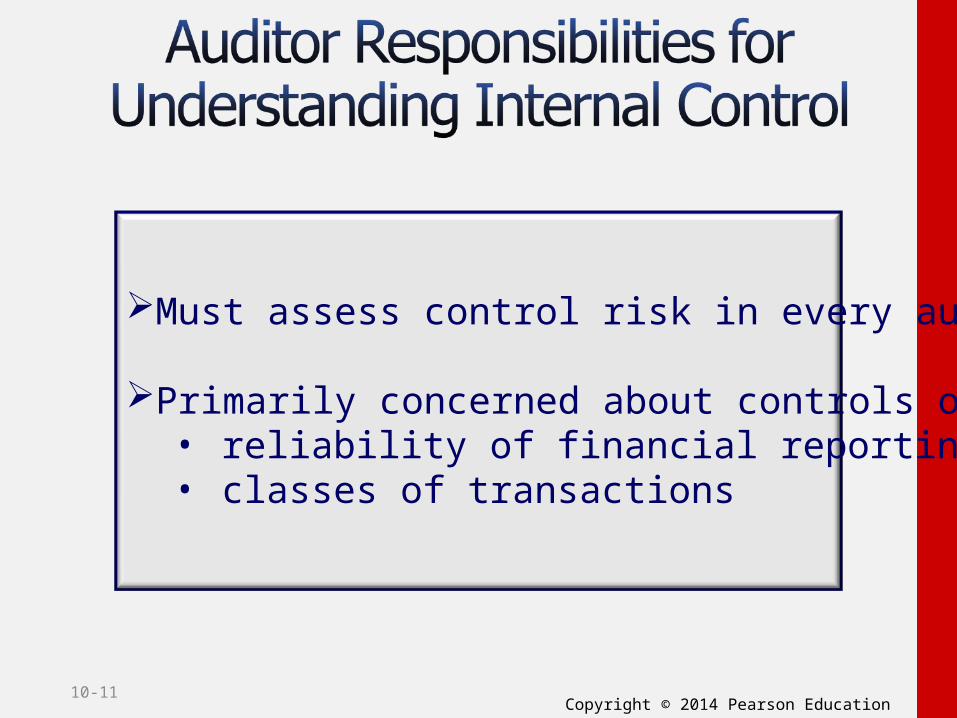

Must assess control risk in every audit

Primarily concerned about controls over: • reliability of financial reporting • classes of transactions

Copyright © 2014 Pearson Education10-12

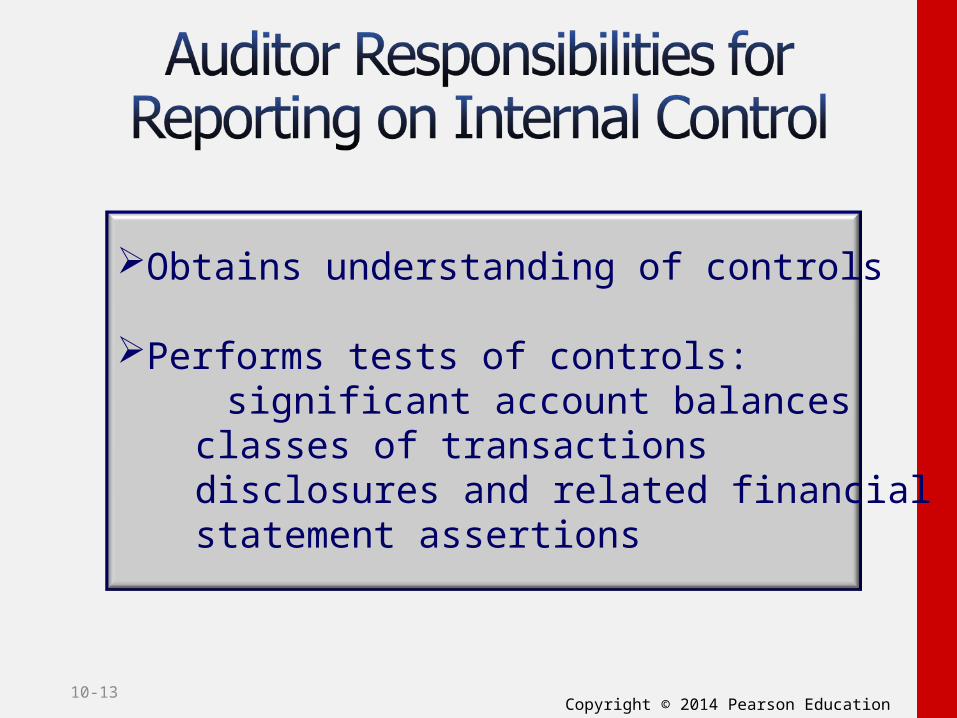

Copyright © 2014 Pearson Education10-13

Obtains understanding of controls

Performs tests of controls: significant account balances classes of transactions

disclosures and related financial statement assertions

Copyright © 2014 Pearson Education

Explain the five components of the COSO internal control framework.

33

10-14

Copyright © 2014 Pearson Education10-15

Copyright © 2014 Pearson Education10-16

Integrity and ethical values

Commitment to competence

Board of directors or audit committee participation

Copyright © 2014 Pearson Education10-17

Management’s philosophy and operating style

Human resource policies and practices

Organizational structure

Copyright © 2014 Pearson Education10-18

Identify factors that may increase risk

Estimate the significance of the risk

Assess the likelihood of the risk occurring

Determine actions necessary to manage the risk

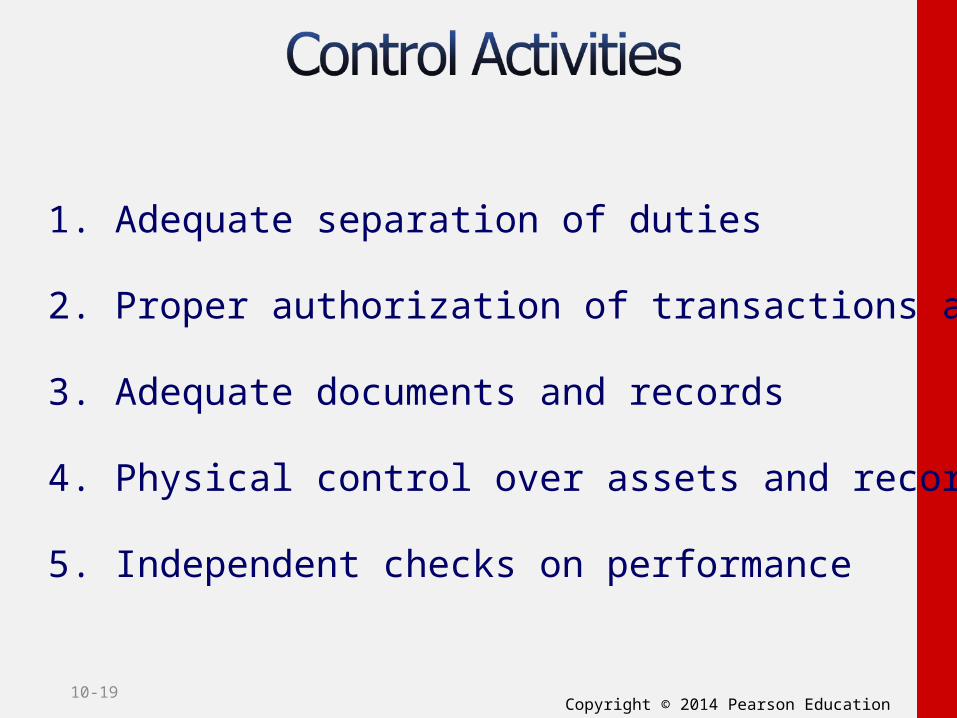

Copyright © 2014 Pearson Education10-19

1. Adequate separation of duties

2. Proper authorization of transactions and activities

3. Adequate documents and records

4. Physical control over assets and records

5. Independent checks on performance

Copyright © 2014 Pearson Education10-20

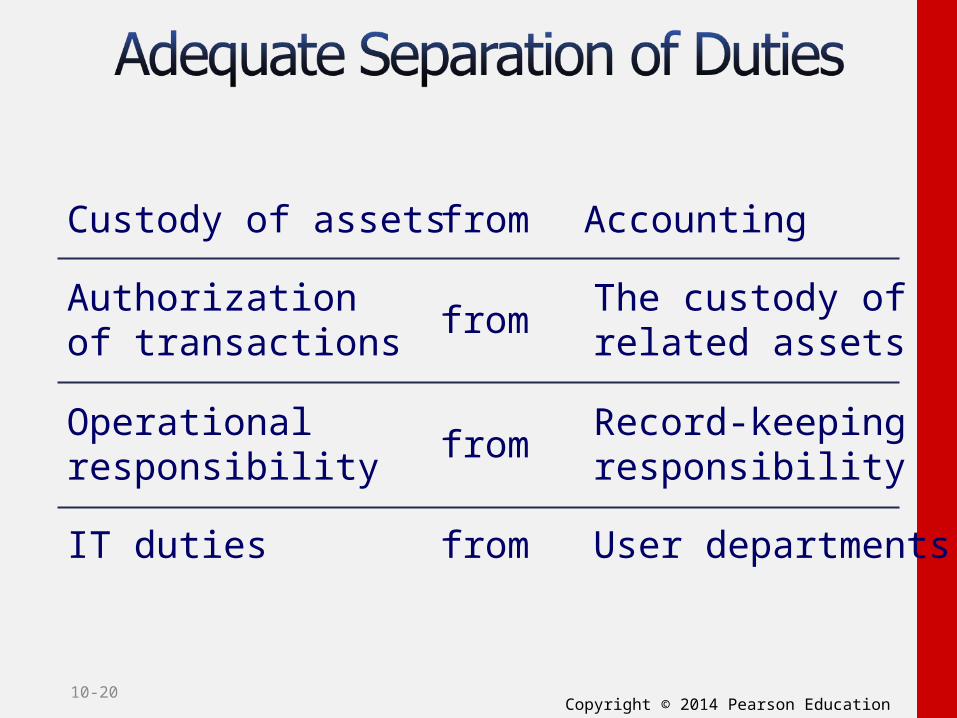

Custody of assets

Authorizationof transactions

Operationalresponsibility

IT duties

from

from

from

from

Accounting

The custody ofrelated assets

Record-keepingresponsibility

User departments

Copyright © 2014 Pearson Education10-21

Transaction Approval Policies

General Authorization

Specific Authorization

Copyright © 2014 Pearson Education10-22

Prenumbered consecutively

Prepared at the time of transaction

Designed for multiple use

Constructed to encourage correct preparation

Copyright © 2014 Pearson Education10-23

The most important type of protectivemeasure for safeguarding assets andrecords is the use of physical precautions.

Copyright © 2014 Pearson Education10-24

The need for independent checks arisesbecause internal control tends to changeover time, unless there is frequent review.

Copyright © 2014 Pearson Education10-25

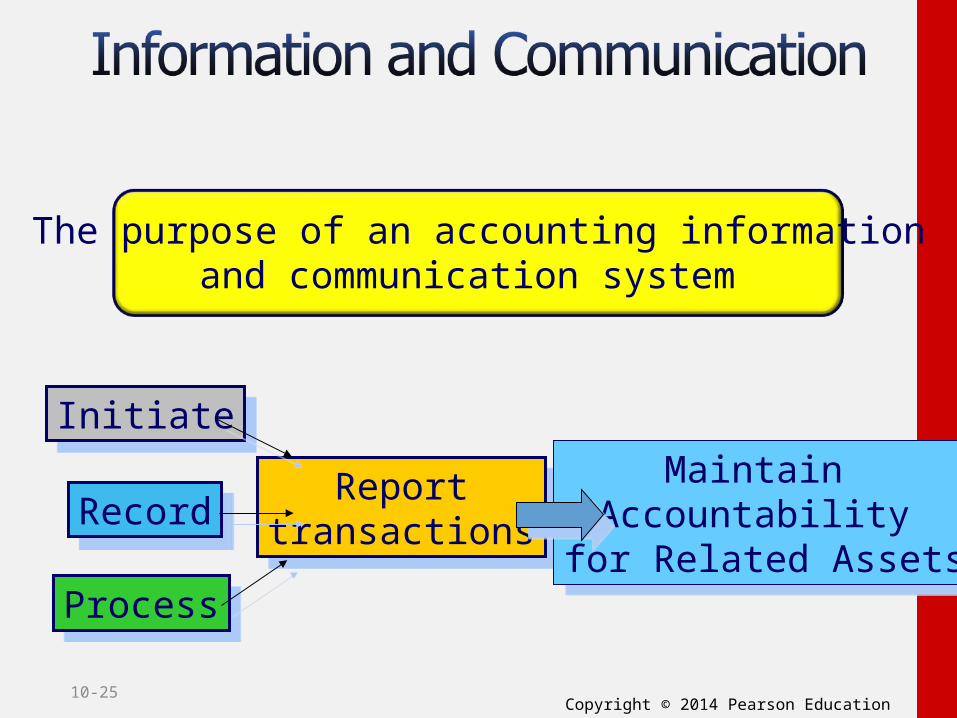

The purpose of an accounting informationand communication system

InitiateInitiate

RecordRecord

ProcessProcess

Reporttransactions

Reporttransactions

Maintain Accountability

for Related Assets

Maintain Accountability

for Related Assets

Copyright © 2014 Pearson Education10-26

Monitoring activities deal with management’songoing and periodic assessment of thequality of internal control performance…

to determine whether controls are operatingas intended and modified when needed.

Copyright © 2014 Pearson Education

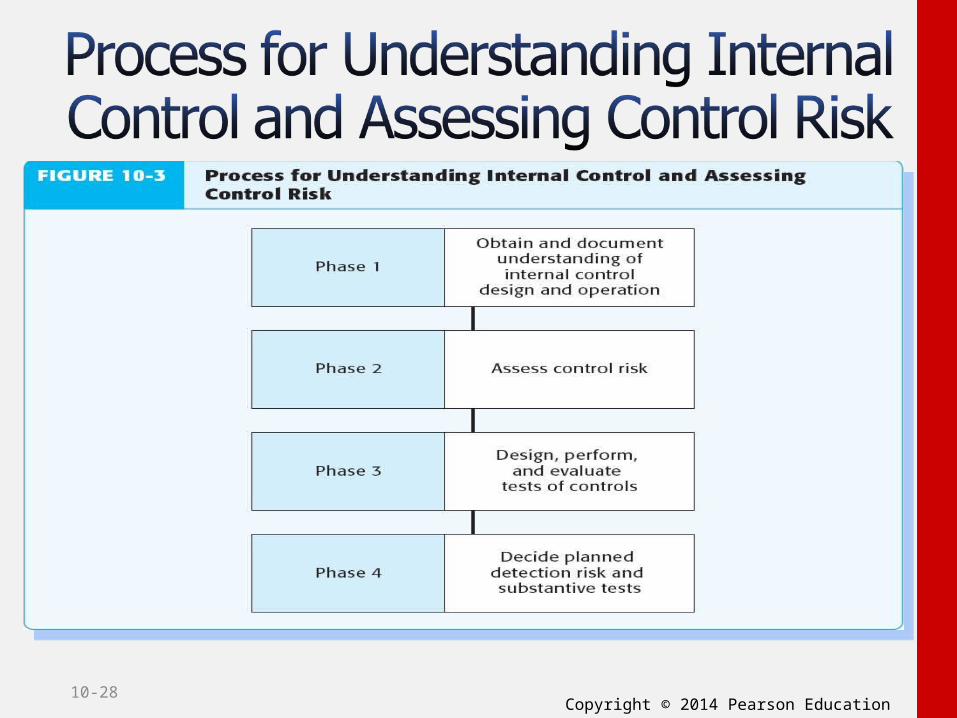

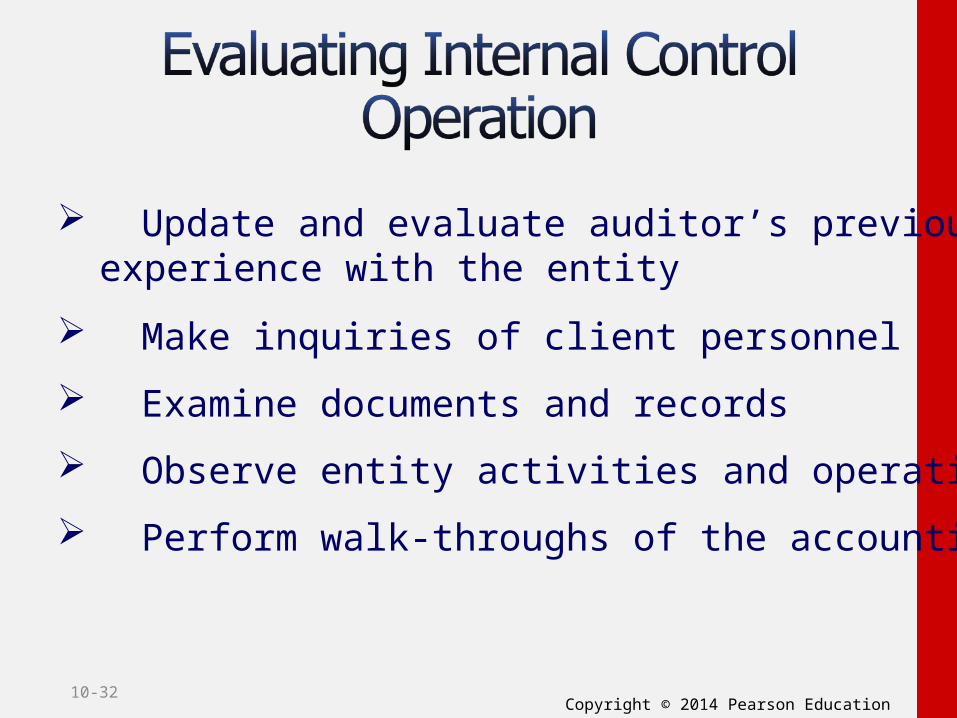

Obtain and document an understanding of internal control.

44

10-27

Copyright © 2014 Pearson Education10-28

Copyright © 2014 Pearson Education10-29

Auditing standards require auditors to obtain an understanding of internal control for every audit.

Procedure to obtain an understanding: Inspection Inquiry of entity personnel Observation of employees

Copyright © 2014 Pearson Education10-30

Narrative

FlowchartInternalcontrol

questionnaire

Copyright © 2014 Pearson Education10-31

1. The origin of every document and record in the system

2. All processing that takes place

3. The disposition of every document and record in the system

4. An indication of the controls relevant to the assessment of control risk

Copyright © 2014 Pearson Education10-32

Update and evaluate auditor’s previousexperience with the entity

Make inquiries of client personnel

Examine documents and records

Observe entity activities and operations

Perform walk-throughs of the accounting system

Copyright © 2014 Pearson Education

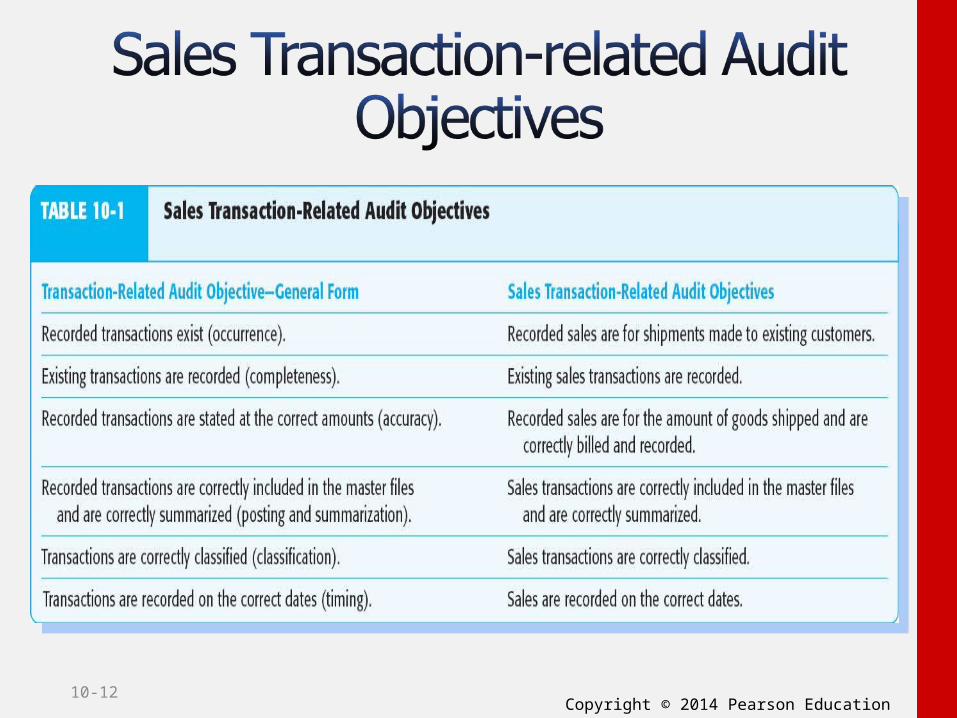

Assess control risk by linking key controls and control deficiencies to transaction-related audit

objectives.

55

10-33

Copyright © 2014 Pearson Education10-34

Assess whether the financial statementsare auditable.

Determine assessed control risk supportedby the understanding obtained.

Use a control risk matrix to assesscontrol risk.

Copyright © 2014 Pearson Education10-35

Many auditors use the control risk matrixto assist in the control risk assessmentprocess at the transaction level.

Copyright © 2014 Pearson Education10-36

Identify audit objectives

Identify existing controls

Associate controls with related audit objectives

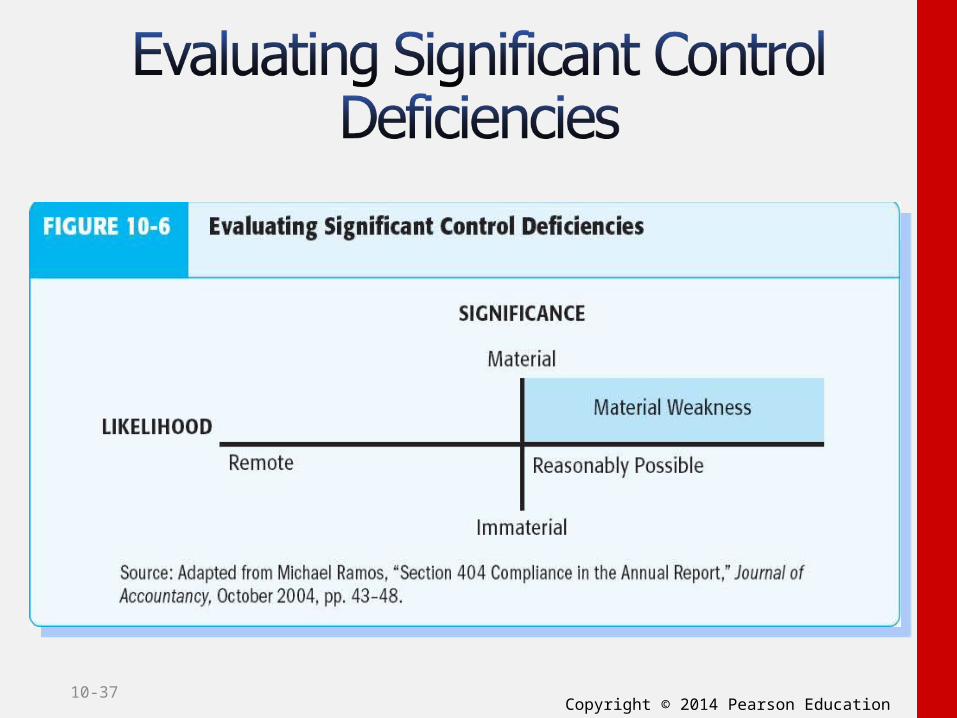

Identify and evaluate control deficiencies, significant deficiencies, and material weaknesses

Copyright © 2014 Pearson Education10-37

Copyright © 2014 Pearson Education10-38

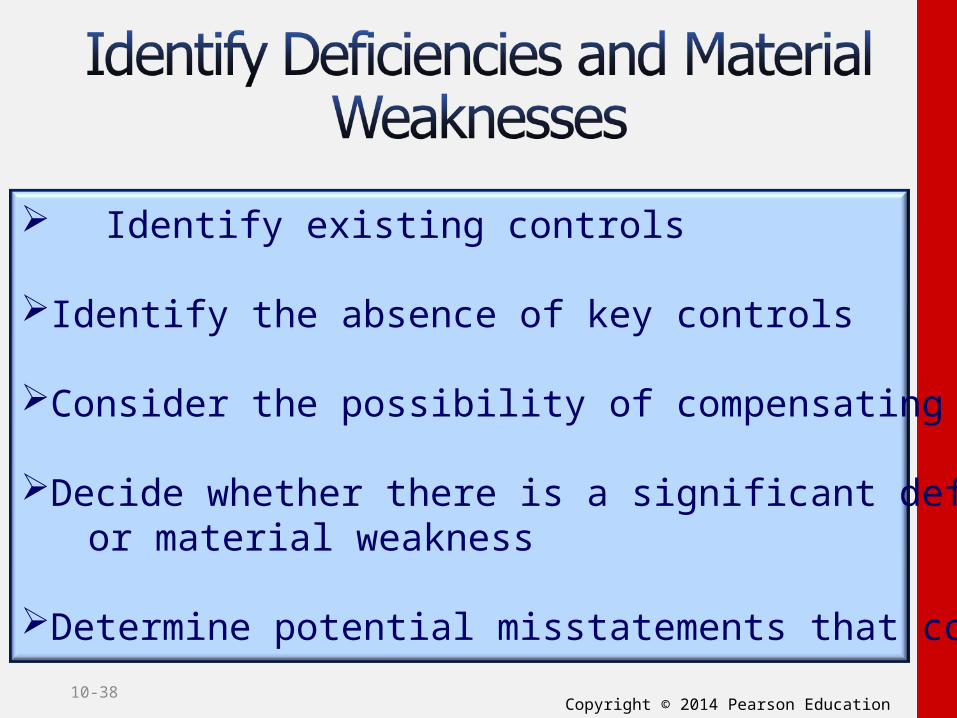

Identify existing controls

Identify the absence of key controls

Consider the possibility of compensating controls

Decide whether there is a significant deficiency or material weakness

Determine potential misstatements that could result

Copyright © 2014 Pearson Education10-39

Auditor must communicate in writing significant deficiencies and material weaknesses to the audit committee

Management letters from the auditor Less significant control weaknesses Ideas for operational improvements

Copyright © 2014 Pearson Education

Describe the process of designing and performing tests of controls.

66

10-40

Copyright © 2014 Pearson Education10-41

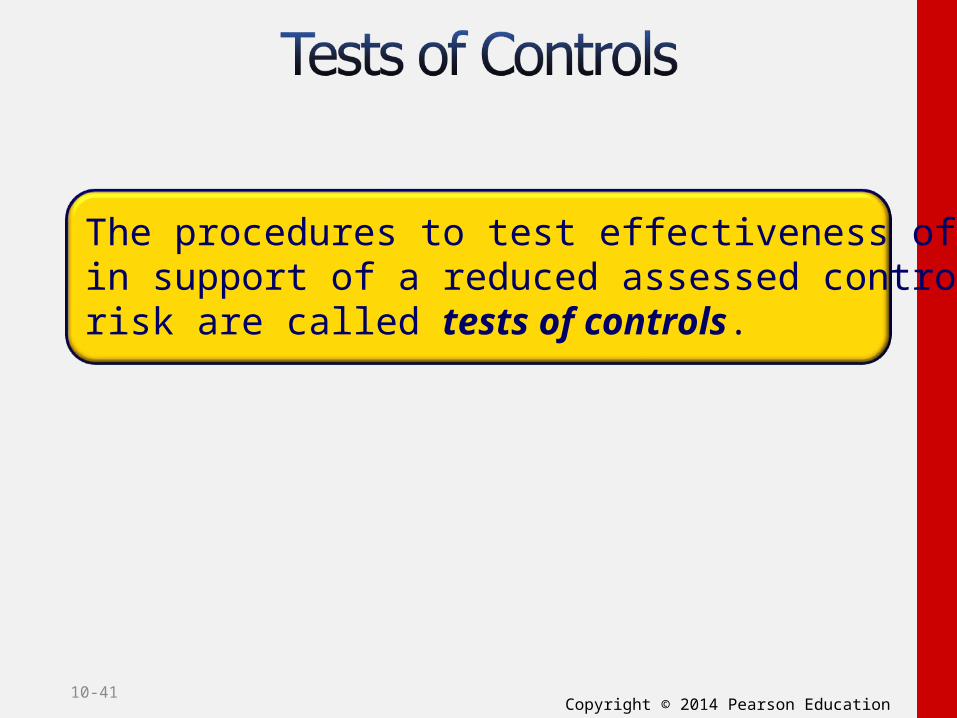

The procedures to test effectiveness of controlsin support of a reduced assessed controlrisk are called tests of controls.

Copyright © 2014 Pearson Education10-42

Inquire of client personnel

Reperform client

procedures

Examine documents,

records, reports

Observe control-related

activities

Copyright © 2014 Pearson Education10-43

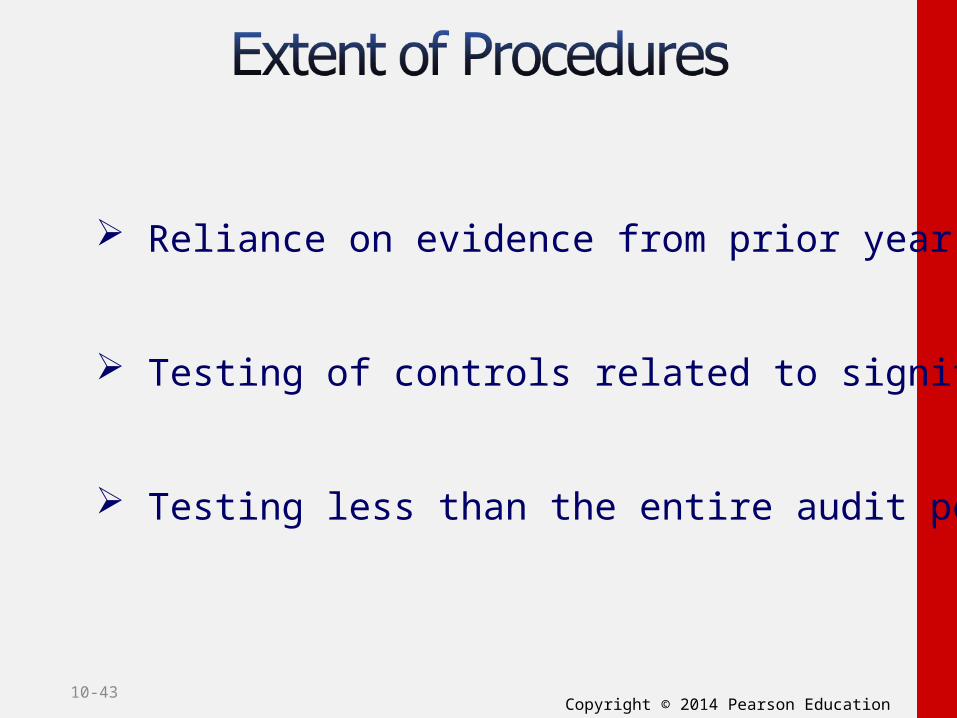

Reliance on evidence from prior year’s audit

Testing of controls related to significant risks

Testing less than the entire audit period

Copyright © 2014 Pearson Education10-44

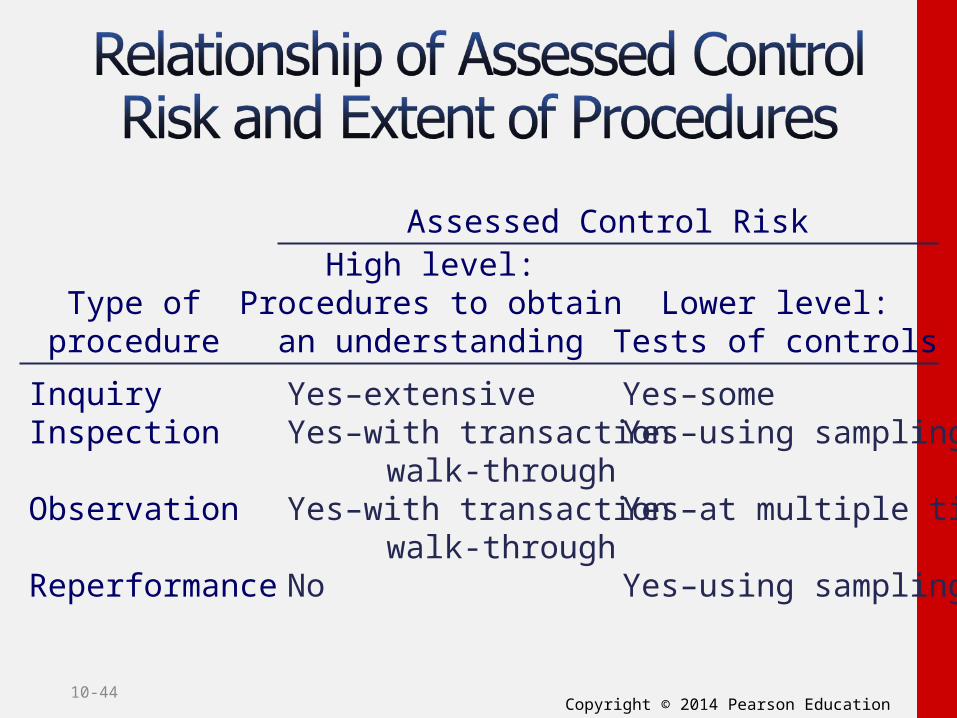

Assessed Control Risk

Type ofprocedure

High level:Procedures to obtain

an understandingLower level:

Tests of controls

InquiryInspection

Observation

Reperformance

Yes–extensiveYes–with transaction

walk-throughYes–with transaction

walk-throughNo

Yes–someYes–using sampling

Yes–at multiple times

Yes–using sampling

Copyright © 2014 Pearson Education10-45

Control risk assessment

process results

Tests of controls

Control risk assessments

Planned detection

risk

Related substantive

tests

Balance related audit

objectives

Copyright © 2014 Pearson Education

Understand Section 404 requirements for auditor reporting on internal control.

77

10-46

Copyright © 2014 Pearson Education10-47

The scope of the auditor’s report on internal controlis limited to obtaining reasonable assurance that material weaknesses in internal control are identified.

Copyright © 2014 Pearson Education10-48

No material weaknessesNo scope restrictions

One or more material weaknesses

Scope limitation

Unqualified

Adverse

Qualified or disclaimer

Copyright © 2014 Pearson Education

Describe the differences in evaluating, reporting, and testing internal control for

nonpublic companies.

88

10-49

Copyright © 2014 Pearson Education10-50

1. Reporting requirements

2. Extent of required internal controls

3. Extent of understanding needed

4. Assessing control risk

5. Extent of tests of controls needed

Copyright © 2014 Pearson Education10-51

Internal controls over financial reportingInternal controls over financial reporting

Internal controls used to assesscontrol risk below maximum

Controls that must be tested inan audit of internal controls

Controls that must be tested inan audit of financial statements

Copyright © 2014 Pearson Education10-52

Copyright © 2014 Pearson Education10-53

Copyright

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the publisher. Printed in the United States of America.