copyright by billy don walker 1977

TRANSCRIPT

Copyright by BILLY DON WALKER 1977

^^J

A COMPARISON OF SIX ALTERNATIVE MODELS FOR

EQUALIZATION OF EDUCATIONAL EXPENDITURES

IN THE TEXAS PUBLIC SCHOOLS

by

BILLY DON WALKER, B.S. IN Ed., M.A.

A DISSERTATION

IN

EDUCATION

Submitted to the Graduate Faculty of Texas Tech University in Partial Fulfillment of the Requirements for

the Degree of

DOCTOR OF EDUCATION

Approved

May, 1977

CONTENTS

LIST OF TABLES iv

I. INTRODUCTION 1

Purpose and Scope 1

The Problem 2

Theoretical Framework 11

Summary 21

II. BACKGROUND OF THE STUDY 23

History of Public School Finance in

Texas, 1876-1976 23

Review of Literature 54

Review of Related Research 82

Summary 87

III. METHODS AND PROCEDURES 89

Design of the Study 89

The Models 91

The Population 99

The Sample 100

Data Collection and Tabulation . . . . 104

Statistical Treatment and Method of

Analysis 104

Summary 105

IV. ANALYSIS OF THE MODELS 106

Dummy Model 106 11

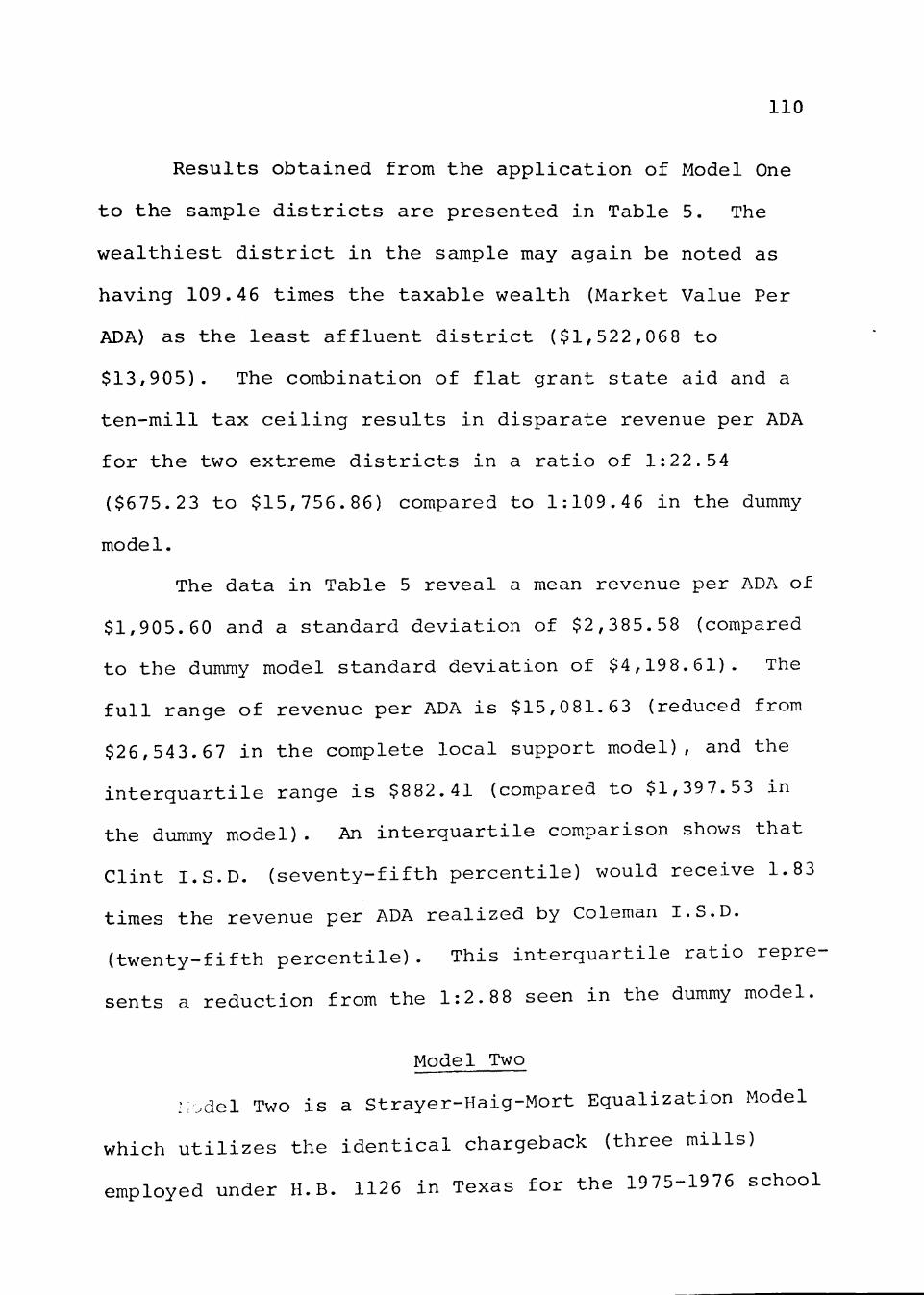

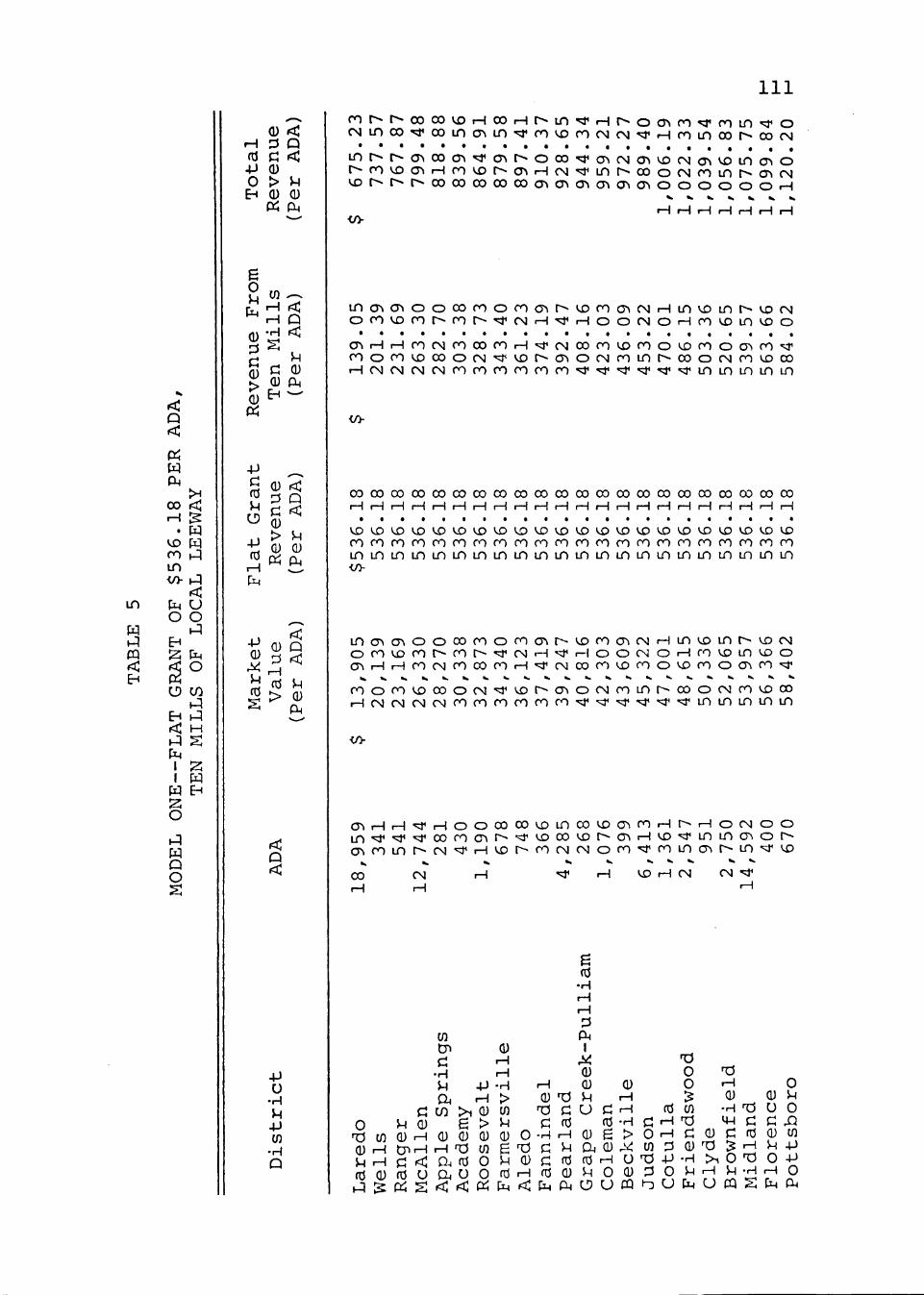

Model One 109

Model Two 110

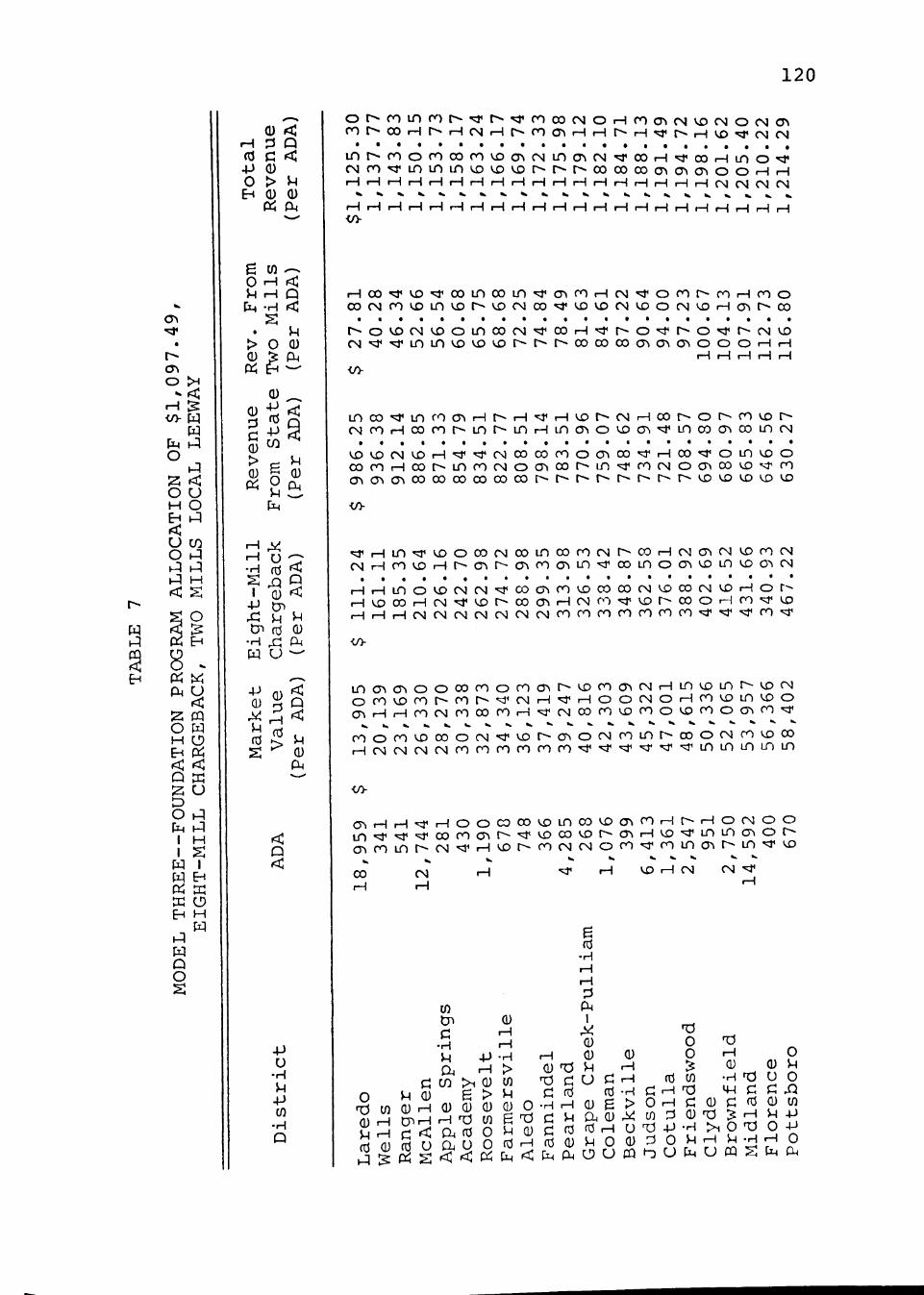

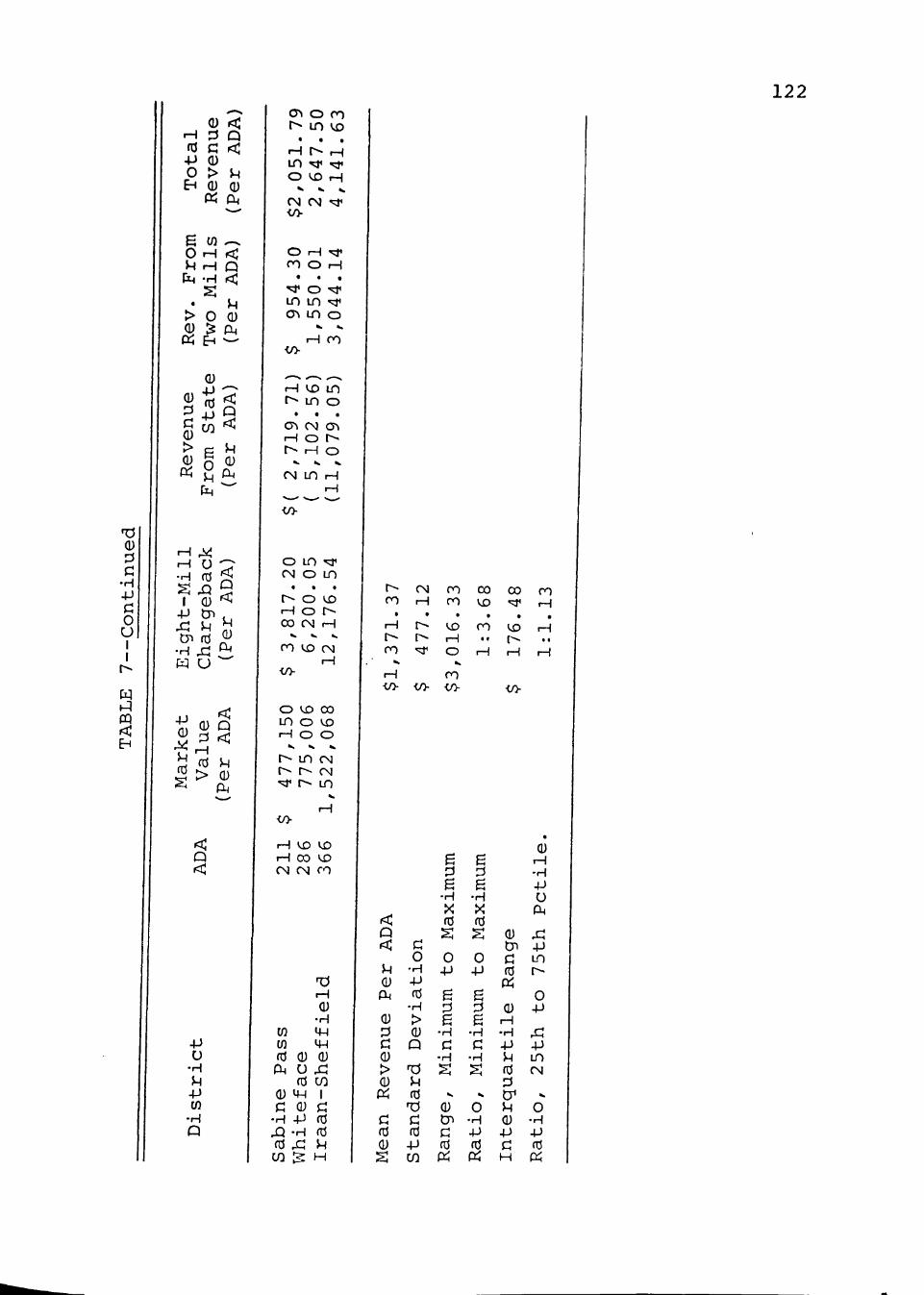

Model Three 118

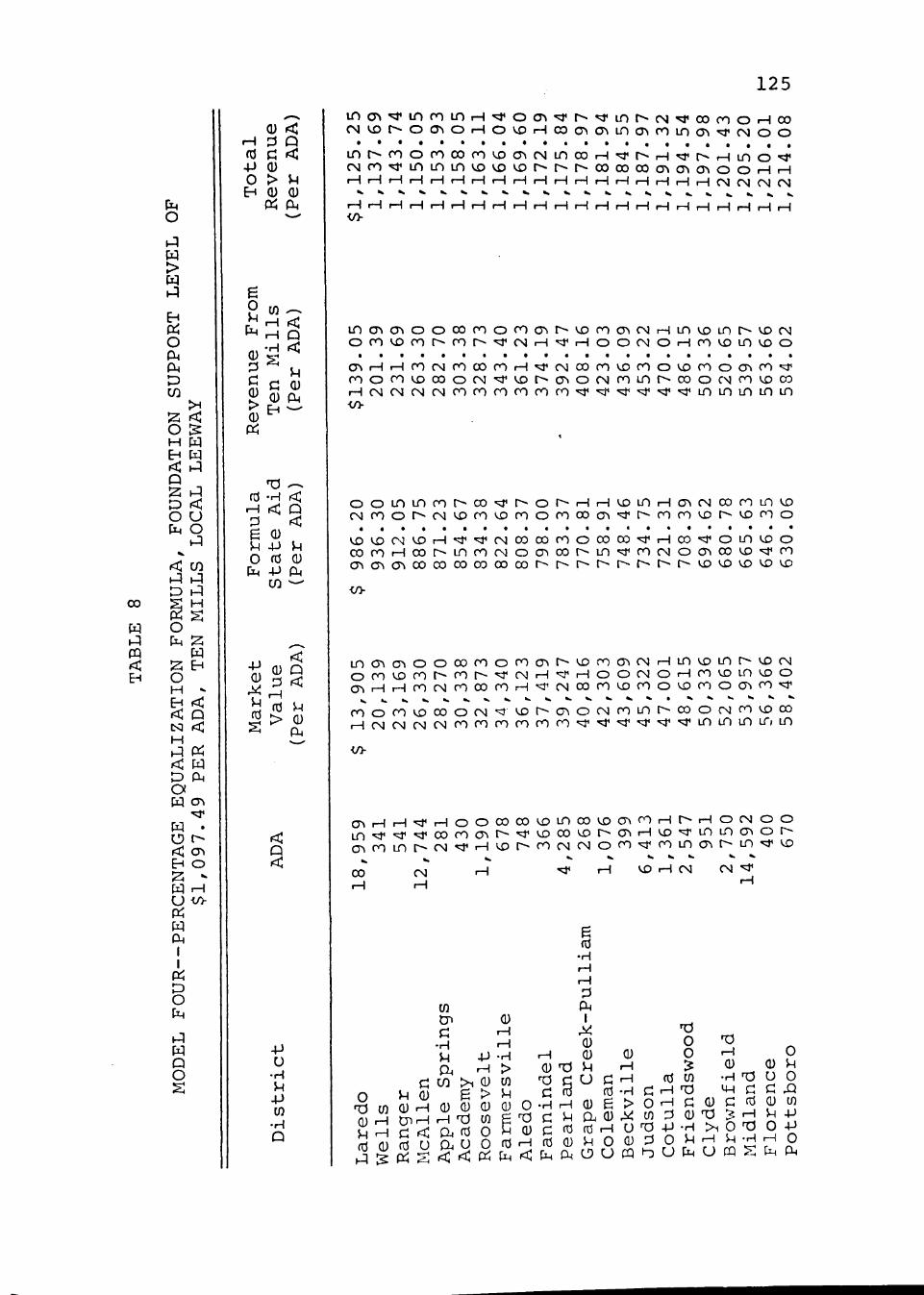

Model Four 123

Model Five 12 8

Model Six 132

Comparison of the Models 138

Summary 146

V. SUMMARY, CONCLUSIONS, AND RECOMMENDATIONS 147

Summary 147

Conclusions 152

Recommendations 160

LIST OF REFERENCES 16 8

APPENDIX 175

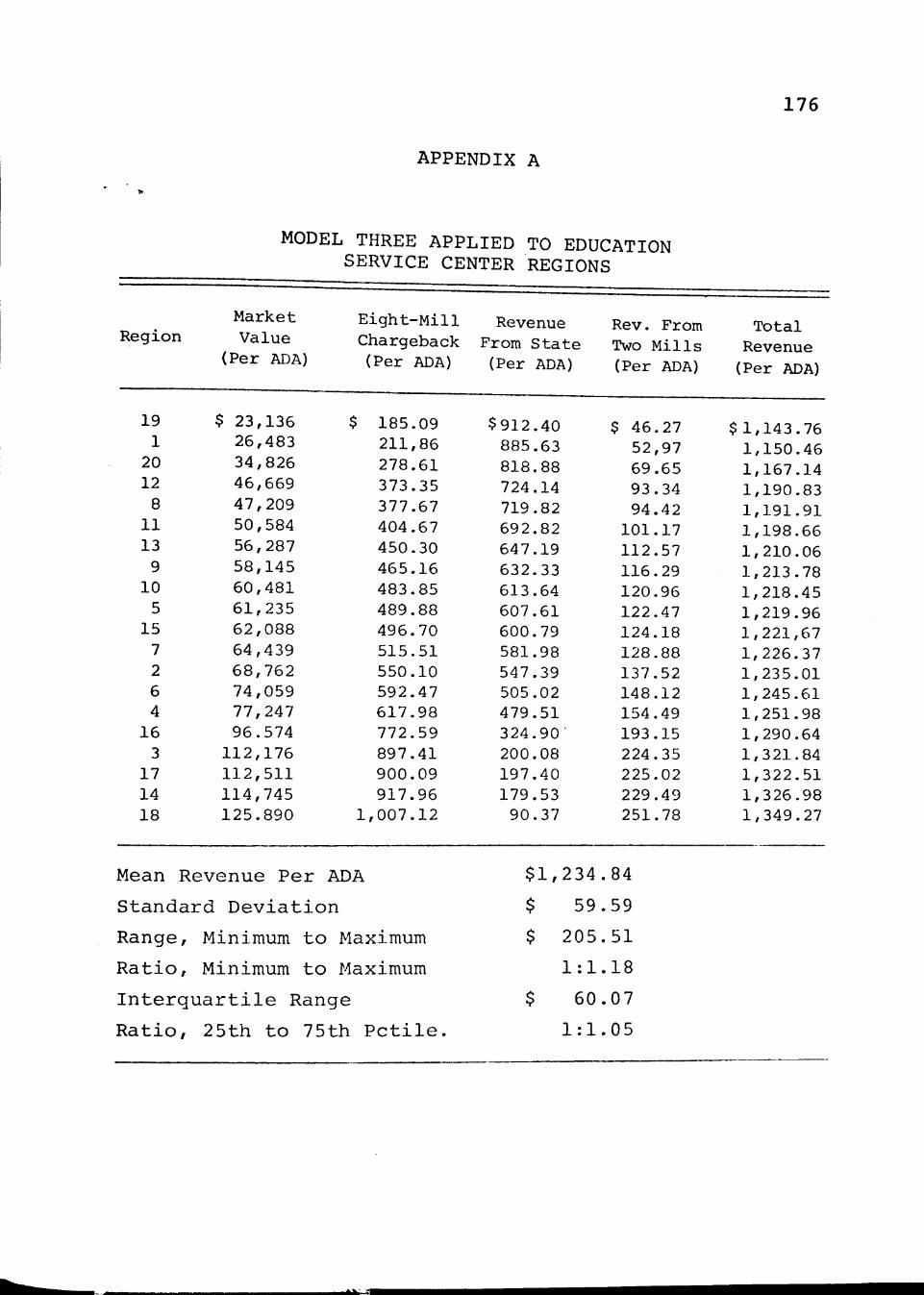

A. MODEL THREE APPLIED TO EDUCATION SERVICE CENTER REGIONS

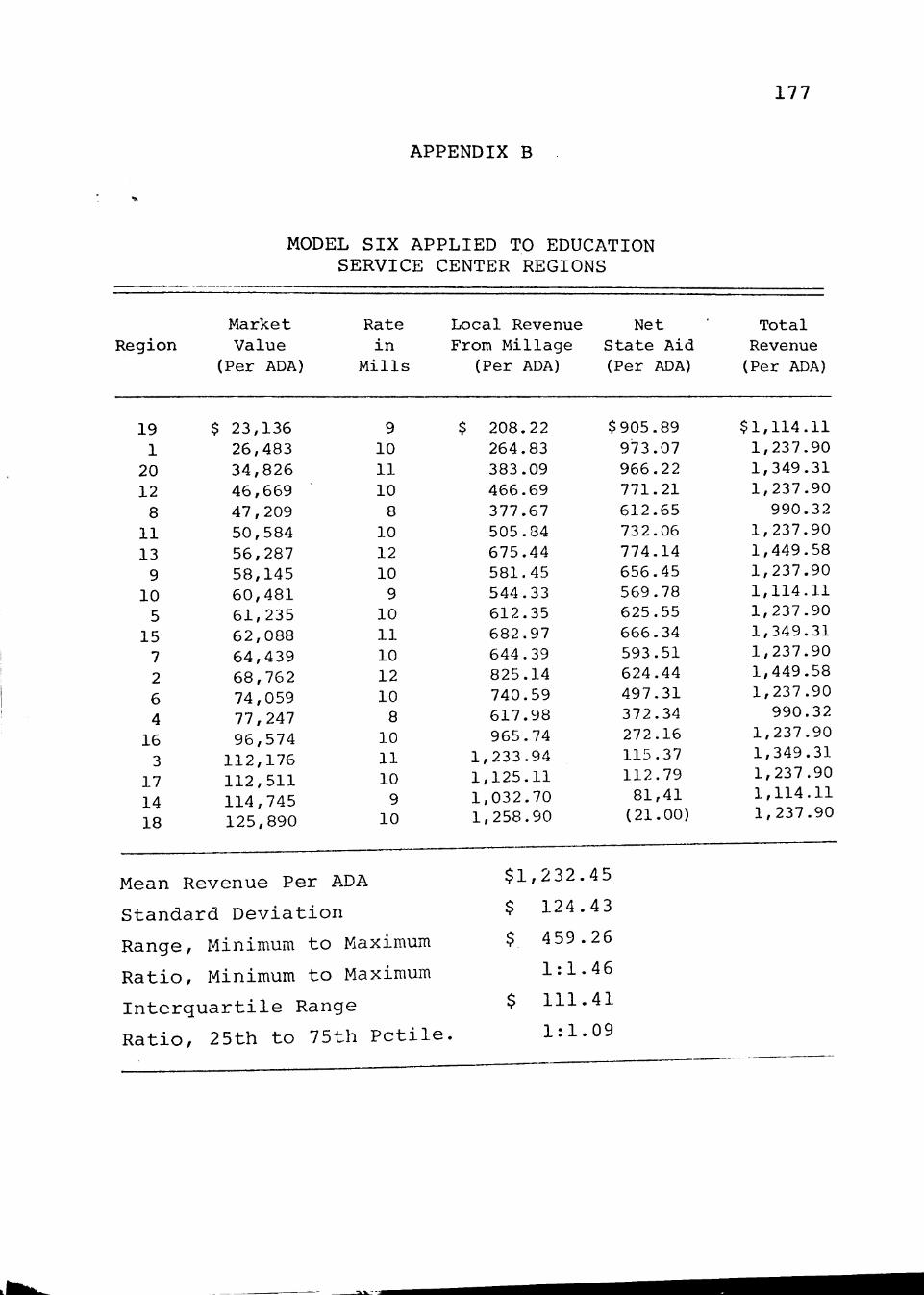

B. MODEL SIX APPLIED TO EDUCATION SERVICE CENTER REGIONS

111

LIST OF TABLES

Table Page

1. State, Local, and Total Revenues Generated from the Research Models 9 3

2. Guaranteed Revenue for Given Tax Rates, Number of Districts Selecting, and Revenue Per ADA Per Mill of Effort, Model Six . . 98

3. Characteristics of the Sample . 102

4. Dummy Model—Complete Local Support Based on a Tax Rate of 17.6 Mills 107

5. Model One—Flat Grant of $536.18 per ADA, Ten Mills of Local Leeway Ill

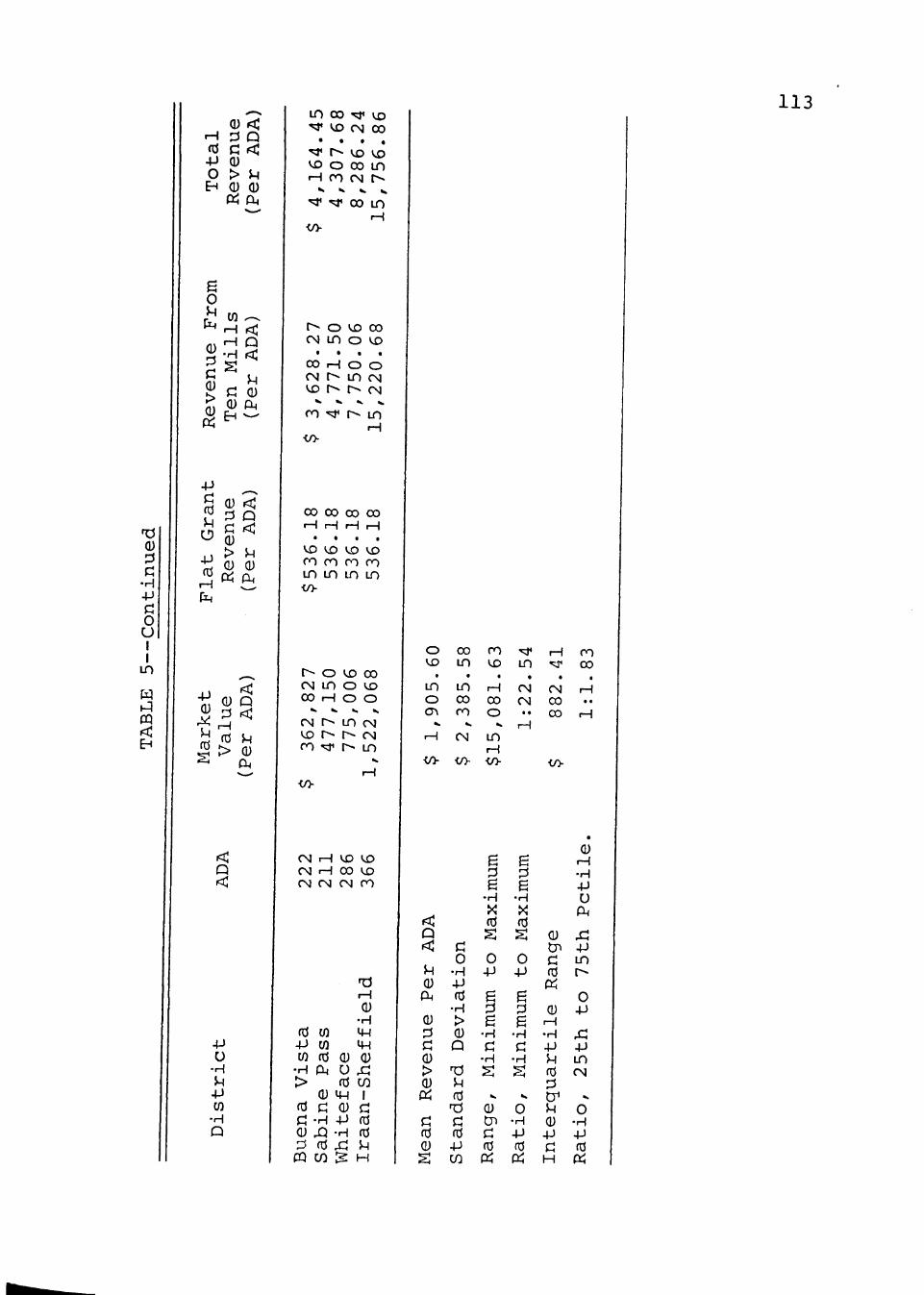

6. Model Two—Foundation Program Allocation of $746.70, Three-Mill Chargeback, Seven Mills Local Leeway 115

7. Model Three--Foundation Program Allocation of $1,097.49, Eight Mill Chargeback, Two Mills Local Leeway 120

8. Model Four—Percentage Equalization Formula, Foundation Support Level of $1,097.49 per ADA, Ten Mills Local Leeway 125

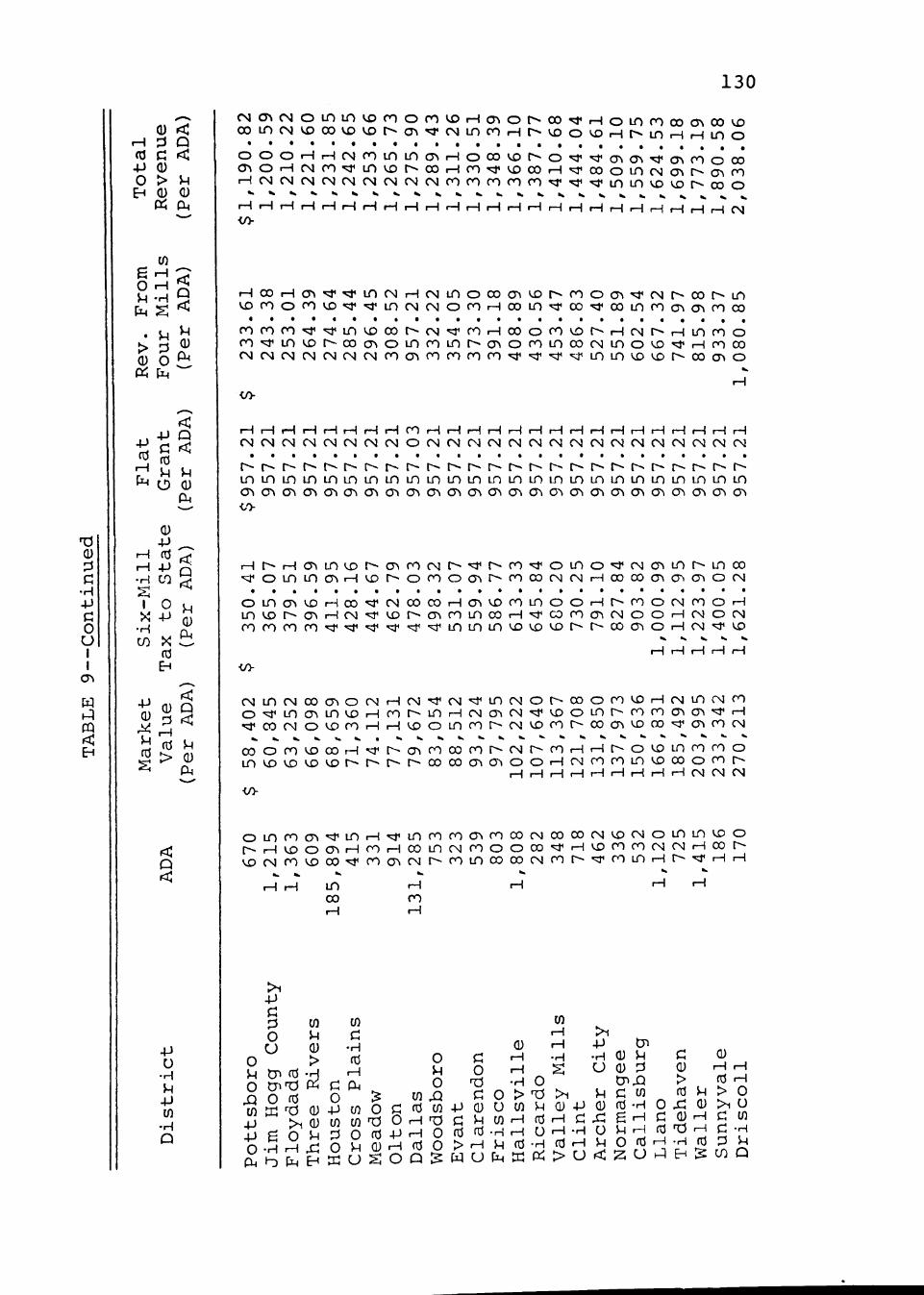

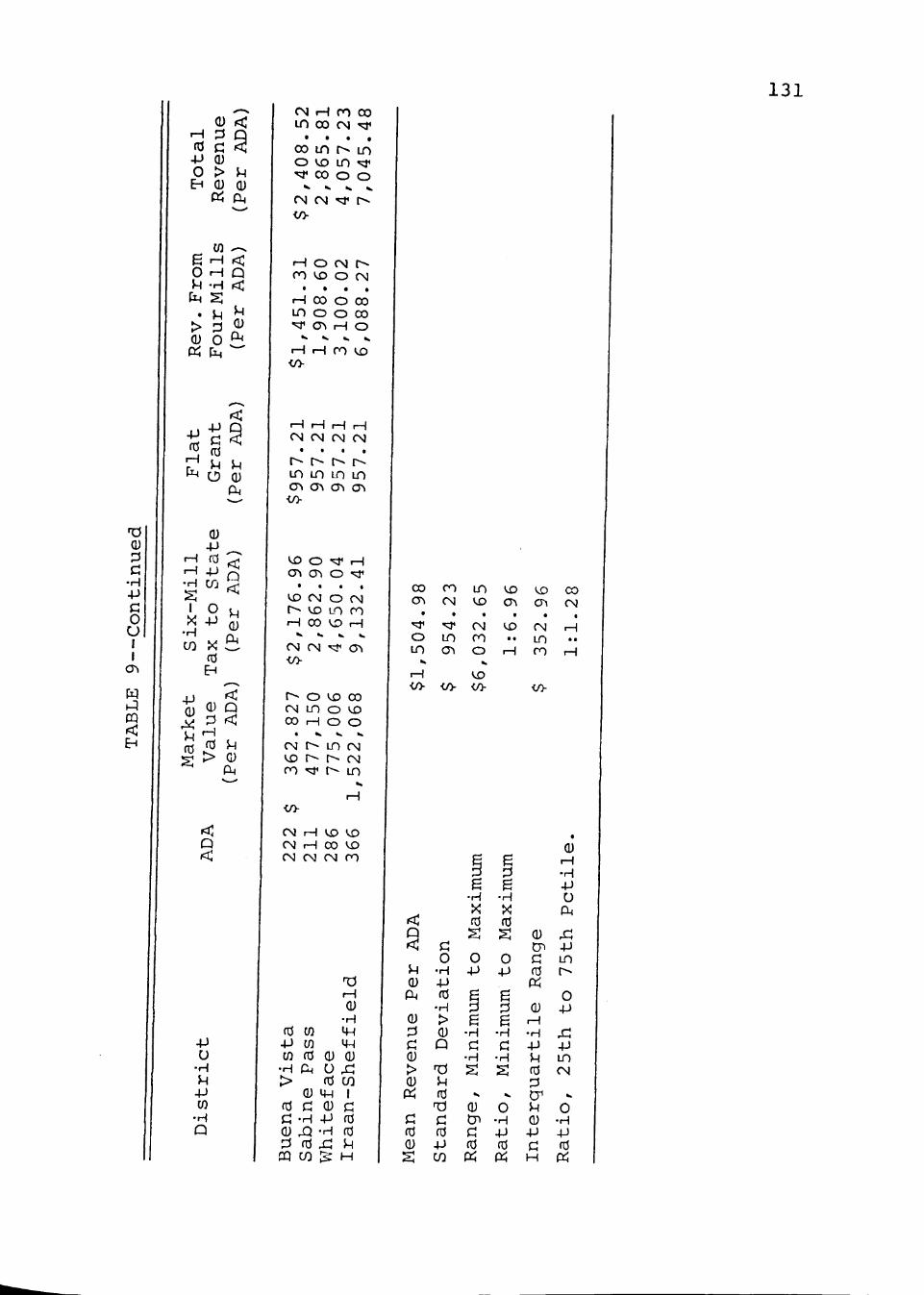

9. Model Five—Flat Grant of $957.21 per ADA, Six-Mill Levy to the State, Four Mills Local Leeway 129

10. Model Six--Power Equalization with Variable State-Guaranteed Revenue per ADA, Kinks Above Ten-Mill Effort 133

11. Descriptive Statistics Accruing from the Six Research Models 138

12. Total Revenue per ADA, By District and Model 142

IV

CHAPTER I

INTRODUCTION

Public school finance in the decade of the 1970s is

in the throes of an egalitarian revolution. The prospects

for change are imminent, if not established fact, in most

states. In a number of instances the courts have ruled

that existing state systems of educational finance are dis

criminatory, irrational, or both. State legislatures are

confronted with a fundamental dilemma; that is, they are

coerced by judicial intervention or political mandate to

work fundamental changes in public school finance systems

when available solutions are meager, untested, or politi

cally unfeasible.

Purpose and Scope

The purpose of this dissertation is to investigate

viable alternative approaches to the development of a

financing plan which would tend to equalize available reve

nue per pupil in the school districts of the state of

Texas as they were organized during the 1975-1976 school

year. Six alternative models are studied as they apply

specifically to the scholastic populations and tax

resources of Texas school districts. Ultimately, recom

mendations are made relative to the most tenable model or

models from statistical comparison and related literature

and research. Although confined to the theoretical realm

in its scope, the explorations could have practical impli

cations, given the current state of flux in Texas public

school finance.

The Problem

Education in the United States in the current decade

is in a substantial measure of economic and fiscal dis

tress. Three basic crises exist, one of which provides

the basis for and major emphasis of this dissertation.

^First, costs in education have been increasing more

rapidly than revenue and, in many cases, too swiftly for

the ability of taxpayers to keep apace. Burrup (19 74) has

observed that "a nationwide taxpayer revolt . . . is no

longer more imaginary than real."

Second, while educational costs have risen precipi

tately and the scope of educational services has dilated at

an unprecedented rate, the public has not ceased to demand

higher quality in both educational processes and products.

Such a state of affairs has serious implications for the

future of education in at least two ways: (1) the very

existence of some educational institutions is threatened,

and (2) the schools are prompted to seek out and to utilize

more efficient methods of operation (Benson, 1975a).

Third, a crisis exists, both in the nation as a

whole and in Texas in particular, which involves the con

cept of equal educational opportunity as measured by

equity in terms of both the allocation and revenue dimen

sions of public school finance. Inequities are apparent

in both expenditures for education and in the tax efforts

required to underwrite the expenditures. While it is evi

dent that inequities in ability to pay, effort exerted,

and actual spending exist among the various states, the

primary focus of efforts at remediation has been on intra

state equity in school finance since education is essen

tially a governmental function of the various states. / Burrup (1974) has summarized the basic reasons for

inequality in educational opportunity; i.e., inequity in

public school finance, as: (1) inadequate school district

organization, creating wide disparities in taxable wealth

among districts; (2) small districts, which are inefficient

in terms of per-pupil costs; (3) differences in ability and

effort among districts, somewhat as a result of inadequate

district structure; and (4) unsound legal and financial

provisions, including methods of allocating state funds for

education in the districts of a state.

It is primarily upon the last cause, with concomitant

reference to differences in local abilities, that interest

has coalesced in recent years although all the reasons have

drawn some measure of attention. All the causes listed by

Burrup are applicable in Texas, where more than a thousand

school districts exist with wealth disparities which would

stun even the most ardent imagination. However, Texas is

not unique, and Jordan and Hanes (1976) have noted that

since 1971 no less than sixteen states, Texas not included,

have enacted new school financing measures in the pursuit

of greater equalization of educational opportunities.

Emphasis upon the legal and financial provisions of

the states has no doubt been enhanced in recent years by

judicial intervention into the financing of education.

Wise (196 8) has explained equal educational opportunity as

a natural extension of litigation favoring school integra

tion, legislative reapportionment, and protection of the

civil rights of the poor. Various state and federal courts

have amplified that theme in a number of landmark decisions

related to public school finance. Some representative

examples serve to elucidate the dilemma created in educa

tional finance.

\ In August, 19 71, in the case of Serrano v. Priest,

the California Supreme Court ruled the California school

finance system unconstitutional on the grounds that it

violated the "equal protection of the law" guaranteed by

both the federal and state constitutions. The decision

was based primarily upon the fact that the school districts

of the state were vastly unequal in local property wealth,

the basic source of educational revenue. Thus was created

in "poor" districts a financial support limitation which

substantially disequalized educational opportunity. The

court held that a child's education should not be depen

dent upon the wealth of the school district in which he

resided, but rather upon the wealth of the state as a

whole. Although the decision had immediate ramifications

for only the state of California, the potential effects

were great, for the facts in the case were duplicated in

almost every state in the nation (Burrup, 1974). Within

five months three similar cases captured the attention of

educators and students of public school finance.

In October, 1971, in Van Dusartz v. Hatfield, a

federal district court in Minnesota declared that state's

school finance system unconstitutional, once again relying

upon the Fourteenth Amendment as a rationale. In January,

1972, in Robinson v. Cahill, a New Jersey Superior Court

struck down that state's school finance system because it

violated the state constitution's "thorough and efficient"

clause relating to education. In an important modification,

that court stated that educational expenditures need not be

absolutely equal but should vary according to differing

pupil needs.

In the interim, in December, 1971, in the case of

Rodriguez v. San Antonio Independent School District, a

federal district court in Texas declared the Texas school

finance system in violation of the "equal protection"

clause of the Fourteenth Amendment in view of the wide

disparities in local property tax wealth; that is, in view

of the existence of "tax high, spend low" districts in the

same state-created system as "tax low, spend high" dis

tricts. The case is discussed at greater length in

Chapter II, but the court's thinking might appropriately

be summarized at this juncture.

As in the Serrano case, the distribution of wealth

in a district structure created by the state was found to

discriminate against students living in "poor" districts.

Upon appeal, the United States Supreme Court in 19 73 over

turned the Rodriguez decision on the principal ground that

education was not a fundamental interest protected by the

Fourteenth Amendment. The Court's decision was foreshad

owed by two earlier cases, Mclnnis v. Shapiro (1968) and

Burruss v. Wilkerson (1970), in which the Court had

affirmed without discussion the lower courts' decisions

that the finance structures of Illinois and Virginia were

not unconstitutional. Nevertheless, even the majority

opinion in the 5-4 decision indicated dismay with the

inequitable Texas system and suggested that state

legislators in Texas and throughout the nation give full

attention to the problem.

By the time of the Supreme Court's Rodriguez deci

sion, there were about thirty Serrano-Rodriguez-type

cases pending in state and federal courts throughout the

country (Education Commission of the States, 19 74). The

Rodriguez reversal stemmed the tide in regard to judicial

review in the federal courts, but recourse was still pos

sible through the state court systems. However, the

Rodriguez decision established a temper which resulted in

several setbacks for the idea of equality through

expenditures. '

In 1973, the Michigan Supreme Court vacated an

earlier (1972) decision in Milliken v. Green, a case which

had voided that state's financing provisions as discrimi

natory. Swift on the heels of this decision came three

other state-level cases in which the constitutionality of

finance structures was upheld: Shofstall v. Hollins

(Arizona, 1973), Northshore School District No. 417 v.

Kinnear (Washington, 1974), and Thompson v. Engleking

(Idaho, 1975). On the other hand, the Robinson v. Cahill

decision was upheld in the New Jersey Supreme Court in

1973, and the Connecticut school finance system was struck

down in 19 74 in Horton v. Meskill. The upshot of the post-

1973 state court decisions is that decisions in the states

8

in reference to constitutionality are of little value as

precedents in other states since the circumstances may

vary.

Two principal outcomes emerged from the educational

equity cases of the early 19 70s. Firsjt, in regard to

Texas, public attention was focused upon the problems of

equity to such a degree that the body politic continued ^

to demand school finance reform even after the Rodriguez

reversal (Yudof and Morgan, 1974). Second, in those

cases which emphasized the discriminatory nature of cer

tain school finance systems, some basic principles of

equity in educational opportunity were established for

future reference. These principles are discussed in

Chapter II.

The dilemma faced by the various state legislatures,

including the Texas Legislature, is framed by deliberation

over two basic tasks, the first of which is the subject of

this dissertation. First, legislators must address the

problem of interdistrict disparities in wealth, school

revenue, and expenditures per pupil. Second, legislators

must address the problem of property tax equity since it

is foreseen that the property tax, at either the state or

local level, will remain a major source of income for

education (Benson, 1975a). State legislatures have little

to guide them save a few significant studies done in recent

years by selected groups; e.g., the President's Commission

on School Finance (1972), the Fleischmann Commission on

School Finance (1973), and the National Education Finance

Project (1969-1973).

Statement of the Problem

In a study conducted by the National Education

Finance Project in 1972, the fifty states were ranked

according to equalization scores based on the N.E.F.P.

typology and scoring method. Texas ranked twenty-eighth

among the states in terms of equalization of public school

expenditures (Johns and Morphet, 1972). In the inter

vening years at least seven of the states ranked below

Texas have taken measures to approach equalization. It is

true that Texas, through the enactment of H.B. 1126 in

1975 (see Chapter II for details), has taken halting move

ments toward equalization, but Texas remains in an unen

viable position in respect to the other states as far as

school finance equity is concerned.

The specific problem addressed by the dissertation is

the comparison of available revenue per student in Texas

school districts from six alternative models of state edu

cational finance. The six models, which are discussed in

more detail below and in Chapter III, are as follows:

Model One: Flat Grant Model, entailing a flat grant of n dollars per ADA (pupils in average

10

daily attendance) and a local tax rate allowable to a maximum of ten mills on the equalized property valuation of each district.

Model Two: Strayer-Haig-Mort Equalization Model, entailing a minimum foundation program allocation of n dollars per ADA, less a three-mill required levy (chargeback), plus seven mills of local leeway as applied to the equalized property valuation of each district.

Model Three; Strayer-Haig-Mort Equalization Model, entailing a minimum foundation program allocation of n dollars per ADA, less an eight-mill required levy (chargeback), plus two mills of local leeway as applied to the equalized property valuation of each district.

Model Four: Percentage Equalization Model, entailing a formula for state aid grants commensurate with each district's equalized property valuation per ADA as a percentage of the statewide average equalized property valuation per ADA.

Model Five: Flat Grant Model, entailing a flat grant of n_ dollars per ADA; a six-mill required local levy, with revenue going to the state for redistribution; and four mills of local leeway as applied to the equalized property valuation in each district.

Model Six: Power Equalization Model, with identical local tax efforts generating identical revenue of n dollars per ADA (tax efforts randomly distributed).

Significance of the Problem

Benson (1975a) has identified three principal issues

in educational finance which will likely have a significant

impact upon the future of public school financing policies :

(1) the improvement of family choice in the selection of

educational services, (2) whether and how the technological

efficiency of schools can be enhanced, and (3) how we

11

distribute educational services to different client groups

and how we raise money to pay for these services. The

dissertation addresses, in part, the last issue. Moreover,

to reiterate the opening statement of this chapter, public

school finance is in a difficult period of transition;

therefore, a study of some of the modes proposed to ease

the transition is both timely and important.

Theoretical Framework

Definitions

Flat Grant Model

Models One and Five in the dissertation are illus

trations of flat grant models. Under a school finance

model of this type, allocations of funds are "flat

amounts" transferred to local districts without considera

tion of local taxpaying ability. In Texas a portion of the

revenue of all public schools is distributed in this

manner; e.g., per capita apportionments from the Available

School Fund. Each district receives a flat amount per

pupil in average daily attendance.

Stayer-Haig-Mort Equalization Model

Models Two and Three in the dissertation are illus

trations of Stayer-Haig-Mort equalization models. Under

this type of model allocations are made to local school

12

districts in inverse proportion to local taxpaying ability.

Stated simply, in theory, more state funds flow to "poor"

districts than to "wealthy" districts. The most commonly

used model for apportioning state funds is the Strayer-

Haig model (Strayer and Haig, 1923), especially as ampli

fied by Mort (1924). In the Strayer-Haig-Mort equalization

scheme the cost of the foundation program which the state

legislature chooses to support is computed; from that cost

is deducted the amount of funds the local district can

raise through a required minimum tax effort. The differ

ence becomes the state allocation to the district. Although

the model appears simple at first inspection, there are

myriad variations which have a profound impact on the

finances of local districts (Johns and Morphet, 1972).

Texas has operated a variation of the Strayer-Haig-Mort

equalization model since 1949.

Percentage Equalization Formula

Model Four in the dissertation is an example of a

percentage equalization model. Under this formula scheme

the state's share of a foundation program is computed by

multiplying the cost of the foundation program of any

single district by 100 percent minus a predetermined per

centage figure, which, in turn, is multiplied by the quo

tient of the equalized property value per ADA (see below

13

for definition) in the district divided by the state

average equalized property valuation per ADA. This pro

cess may be stated in formula motif as:

State Revenue = A x 1 - (D/S x E)

where:

A = Cost of the foundation program

D = Equalized value of property per ADA in the district

S = State average equalized property value per ADA

E = Predetermined constant factor (percentage of state support desired)

Power Equalization Model

Model Six of the dissertation is a power equaliza

tion model. Also known as DPE (District Power Equaliza

tion) , this model guarantees a specific number of dollars

in revenue per ADA for a specific tax rate selected

locally within the parameters of applicable laws. Each

district selecting tax rate N would be guaranteed n dollars

regardless of district wealth; each district selecting tax

rate R would receive r_ dollars per ADA; and so on. In

practice, the model usually has "kinks" built in; that is,

points at which the amount of revenue derived from a cer

tain tax rate declines in utility in comparison to the tax

effort required.

14

Chargeback

A "chargeback" is any given amount of funds which

are "charged back" against a school district's allocation

of state funds; that is, a chargeback constitutes funds

not received from the state. It is the local portion, to

be provided from local funds, of a foundation program (see

Models Two and Three). In Texas, the chargeback feature

of the Foundation School Program is termed the "local fund

assignment." Chargebacks are generally calculated from

minimum legal tax rates; e.g., if the state guarantees a

district $1,000 per pupil and the application of the

minimum legal tax rate in the district yields $400 per

pupil, the $400 figure becomes a chargeback and the dis

trict receives $600 per pupil from the state. The greater

the wealth of the distict, the higher the chargeback, and

the less the amount of state aid.

Local Leeway

Local leeway may be defined as optional tax leeway

allowed a school district between minumum and maximum legal

tax rates.

Mill

A mill is defined as one-tenth of one cent. Tax

rates are generally expressed in terms of "mills per

dollar" or in terms of "dollars, cents, or dollars and

15

cents per $100." A tax rate of ten mills is equal to one

cent per dollar, or $1.00 per $100.

Recapture

Recapture is a term used to define the process of

state collection of certain local tax monies. When a

district's "chargeback" exceeds the amount of funds guar

anteed by the state, the state "recaptures" the excess

funds. In effect, the local district, in such case,

would receive no state aid.

Save-Harmless Provision

A "save-harmless provision" may be defined as a

legal provision which allays the impact of certain school

finance program features upon a district. As a general

rule, such provisions protect affluent districts from

precipitate decreases in state aid during periods of

equalization reform.

Property Tax Circuit-Breaker

The term "circuit-breaker," as applied to property

taxation, represents a specified level at which the impact

of the property tax is "broken" in order to reduce tax

burdens on low-income property holders. Since theories of

taxation hold that property taxes obtain a higher percen

tage of discretionary income of low-income property holders

16

than of high-income property holders, circuit-breakers are

utilized to rectify this point and make the property tax

more progressive. Low-income property holders may be

exempted from property taxes or may be rebated a given

portion of property taxes paid.

Weighted Pupil

The "weighted pupil" method of allocating funds to

school districts grows from a recognition that certain

types of education (i.e., certain types of pupils) are

more costly than others. Therefore, pupils are "weighted"

in some fashion to reflect cost differentials; e.g., for

compensatory education, vocational education, special edu

cation, etc.

ADA

ADA is defined as the abbreviation for "average

daily attendance," usually as applied to "pupils in aver

age daily attendance."

Assumptions

The preeminent assumption of the study is that local

property taxation will be retained as a method of financing

public school operations in Texas. Although it is certain

that a possibility exists for abolition of local property

taxation as a revenue source, and although the petroleum,

sales, and income tax sources in Texas are viable

17

alternatives in respect to revenue possibilities, the

assumption is relatively safe. First, the local property

tax has been too productive of revenue to be abandoned in

the near future (Benson, 1975a). Second, Governor Dolph

Briscoe has on numerous occasions voiced his opposition to

new state taxes; e.g., a state income tax, increased sales

taxes, increased gasoline taxes, etc. However, it is not

realistic to assume that local property taxation as it

presently exists in Texas will continue unabated. Reforms

are already afoot to improve administration of the tax and

to make it more equitable. Such reforms can only serve to

further the effects of equity in regard to educational

expenditures.

A second major assumption of the study is the pre

sumption of 100 percent collection of taxes by local edu

cation agencies. In reality such an assumption would be

unfeasible, not to say Utopian. However, for purposes of

simplicity in the study, 100 percent collection of local

taxes is assumed. In the case of actual implementation of

one of the models investigated, the state might assume a

certain percentage of collections (perhaps 95 percent) and

make allocations accordingly, allowing local education

agencies to add those collections over the given percentage

to their local budgets. Thus would incentives be given for

avid local collection; such incentives would be especially

18

crucial in cases where the state "recaptures" local taxes.

Under current Texas law no allowance is made for uncol

lected or uncollectable taxes in computing the district's

share of the Foundation School Program.

A third major assumption is that future state

efforts at school finance equity will center upon "oper

ating costs"; that is, upon costs inherent in maintaining

and operating the schools. No effort has been made in the

past, nor have any plans been forthcoming, to equalize

expenditures for capital outlay and debt service in Texas.

This is not to say that equalization of capital outlay and

debt service expenditures would not be desirable, but is

merely a reflection upon the urgency of the equalization

of operating expenditures, which comprised 81.7 percent of

public school spending in Texas during the 1975-76 school

year (Texas Research League, 19 76). Therefore, the models

presented in the study are directed at equalizing mainten

ance and operation costs.

A fourth assumption, somewhat more marginal than the

previous three, is that utilization of unweighted pupil

data will not have an adverse effect upon the conclusions

reached by the study. It is likely that the state will at

some future time utilize a weighted pupil or adjusted

instructional unit approach in determining allocations to

local districts. The state already employs an adjusted

19

instructional unit approach in the calculation of local

district personnel entitlements under the Foundation

School Program.

Unweighted pupil data are used in the study for

several reasons. First, weighted pupil data for the school

districts of Texas are unavailable. Second, the assumption

is followed that the most equitable model utilizing

unweighted data will only be enhanced by the use of

weighted pupil data (Johns and others, 19 72), but only sub

sequent research can validate such an assumption insofar as

cost differentials in Texas are concerned. Third, refer

ence to unweighted pupil data serves as an appropriate base

point for comparison of the relative efficacy of the models

tested.

A fifth assumption is that categorical state grants

to districts will be added to, rather than be a part of,

the districts' basic allocations. In addition to its

basic state aid for maintenance and operation, local dis

tricts would receive aid in accordance with demonstrated

needs in areas such as transportation, food service,

technical-vocational education (if not part of a weighted

pupil methodology), community education, compensatory edu

cation (if not part of a weighted pupil methodology), and

others.

20

Delimitations

Two delimitations are established at the outset.

First, the scope of the study is confined to Texas and to

Texas school districts. This delimitation precludes trans

position of the findings of the study to other states, for

each state has separate sets of circumstances such as

number of districts, local tax resources available, range

of affluence, and others. However, it may be pointed out

that the progenitor of this study, the research conducted

by the National Education Finance Project, did not utilize

a real state at all but a prototype state created for

research purposes.

Second, only six models are studied from among the

myriads extant. For various reasons no attempts are made

to investigate the potential effects of proposed school

finance reforms such as full state funding, family power

equalization, contracts, vouchers, decentralization, cen

tralization, district consolidation, and many others. In

most cases, sufficient data are not available for Texas or

the proposed model is not subject to empirical study. Full

state funding is considered a viable model (Benson, 1975b).

However, since the net result of application of such a

model would be absolute equity in the amount of basic state

aid to local education agencies, the model can be ignored

for three reasons: (1) the results are apparent, (2) such

21

a model does not appear to be politically feasible in

Texas in the near future, and (3) it is perhaps good prac

tice to allow for some local tax leeway (Johns and

Morphet, 19 72).

Summary

Public school finance in the current decade is in

the midst of an egalitarian revolution in which judicial,

social, and political pressures have been brought to bear

on state legislatures (including the Texas Legislature) to

fashion more equitable school finance systems in terms of

educational expenditures per pupil. The purpose of the

dissertation is to investigate the effects of six alterna

tive models of public school financial support on educa

tional finance in Texas. The desirability of a more

equitable system in Texas has been emphasized by generic

inequity in public school finance throughout the nation,

the Rodriguez case, aroused public sensibilities, and the

fact that (by some measures) Texas has one of the least

equitable school finance systems among the fifty states.

The models to be investigated include two types of

flat grant models, two types of foundation program equali

zation models (in the Strayer-Haig image), one percentage

equalization model, and one power equalization model. Five

of the models were chosen for their effectiveness or

22

representativeness from among eighteen models studied by

the National Education Finance Project in 19 72. One

model, power equalization, was chosen for its currency

among proposals for school finance reform (Coons, Clune,

and Sugarman, 19 70; Guthrie, 19 75). Five assumptions and

two delimitations are enumerated at the outset.

CHAPTER II

BACKGROUND OF THE STUDY

The background of the research incorporated in the

dissertation lends itself to division into three phases:

(1) the history of public school finance in Texas, 1876-

1976; (2) a review of related literature on equalization

of public school finance and educational opportunities;

and (3) a review of research related to the models utilized

in the study.

History of Public School Finance in Texas, 1876-1976

The concept of public support for education came

early to Texas. By 1876 Texas had a heritage of educa

tional support which included at least three significant

actions. First, the Education Act of 1839, passed during

the presidency of Mirabeau B. Lamar, had initially laid

the foundation for governmental educational support in

Texas and had served as a model for the Morrill Act of

1862 (Connor, 1971). The act had set aside land grants for

each county in the young nation for the support of public

academies. In addition, fifty leagues of land were set

aside for two future universities. However, land was so

abundant that little income was realized. By 1855 only

23

24

forty-one of the ninety-nine counties had even had their

land surveyed. State intent had been good, but it was

apparent that land grants alone could not give proper

emphasis to education (Eby, 1925).

Second, the Texas Constitution of 1845, adopted when

Texas was admitted as a state to the United States, con

tained a strong charge relative to education. The legis

lature was "to establish free schools throughout the State,

and . . . furnished means for their support, by taxation on

property" (Article X, Section 2, 1845). A minimum of one-

tenth of the general revenue was to go to the schools.

These funds were appropriated but were never disbursed.

The number of Texas citizens who actually supported public

schools financed by the state were few, for "free" schools

(those for orphans, paupers, etc.) were viewed as differ

ent from "public" schools by most people (Lane, 1903).

Third, the School Law of 1854 had been passed during

the administration of Governor Elisha M. Pease. This act

set aside $2,000,000 of the state funds realized from the

Compromise of 1850 to establish a permanent endowment fund

for education. To this endowment was later added one-half

the pioblic domain (in 1876) and, still later, all remaining

public lands (in 1899).

In September, 1875, a Constitutional Convention met

in Austin which mirrored statewide sentiment for retrench

ment, economy, and disestablishment of the centralized

25

state government established in 1869 during Radical Recon

struction in Texas (Connor, 1971). There was heated

debate over the education article to be included in the

new state constitution. Despite the fact that educational

measures had been among the strong points of Governor E. J.

Davis' Republican regime, many advances were negated by

the sentiment against centralized authority (Eby, 1925).

Among other things, the new article abolished the office

of the state superintendent, disposed of the centralized

state education agency, revoked the compulsory attendance

law, eliminated the districting of counties, returned the

county school lands to the counties, and limited financial

support for the schools (Article VII, 1876).

The Constitution of 1876 provided for state support

of schools by setting aside a maximum of one-fourth of the

state's general revenue from ad valorem and occupational

taxes. In addition, it stipulated that one-half the

public lands contained in railroad and internal improvement

surveys would be set aside for education, with revenue

going into the permanent school fund. All previous funds

allocated to education but never expended were also placed

in the permanent school fund. At the same time the Consti

tution rendered impractical local taxation for the purpose

of building and maintaining schools by establishing the

26

"community" system of school organization (Article VII,

Section 5, 1876).

In the "community" system of organization parents

and guardians reorganized school districts each year and

applied to the county judge, who appointed the trustees.

This "floating district" system proved untenable for

several reasons. First, local taxation was impossible

since district boundaries were not fixed. For the same

reason no permanent buildings could be constructed. Third,

many small inefficient districts operated in areas not

large enough for one district. Since nothing permanent

resulted, state revenue was dissipated. Fifth, provision

of a new board of trustees each year disallowed transition

and long-range planning. Sixth, parents often crippled

local schools by subscribing to some distant district

without actually participating (Eby, 1925) .

School expenditures from state funds, allocated on

a per capita basis as provided by the Constitution (Article

VII, Section 5, 1876), amounted to $479,400 for 133,568

scholastics ($3.59 per pupil) in 1876-1877. In 1877-1878

spending figures increased to $757,323 for 146,946 schol

astics, or $5.15 per pupil. There was still another

increase during the 1878-1879 school year, to $869,474 for

192,654 scholastics ($4.51 per pupil). The upward trend

under the new Constitution was gradual yet promising.

27

However, a precipitate decline occurred during the 18 79-

1880 school year. Expenditures decreased to $679,317 for

186,786 pupils, or $3.64 per scholastic (Biennial Report,

1880) .

By 1879 many citizens were demanding reform in state

financing of the schools. The dilation of pupil attendance

in public schools had focused attention on the needs for

better teachers, for state and local supervision, for for

mation of permanent districts, and for increased finances.

However, Governor O. M. Roberts was determined to balance

the state budget and eliminate state debts, and he twice

vetoed appropriations bills which included the usual maxi

mum of one-fourth of the general revenue for education.

Roberts insisted on fiscal retrenchment in all areas,

including education, and succeeded in reducing the appro

priation for education to one-sixth of the general revenue

for the biennium encompassing the 1879-1880 and 1880-1881

school years.

Roberts' fiscal policy helped to focus attention on

the need for other sources of revenue for education (Eby,

1925). The other existing source, besides legislative

appropriations, was land. Revenue from the permanent

school fund was not increasing to any marked degree, yet

school population trends were constantly on the rise. Two

remedies were apparent: (1) increasing the amount of the

/^

28

permanent school fund through a rapid increase in land

sales, and (2) resorting to local taxation (Eby, 1925).

Many incorporated towns had already adopted local taxation

for school purposes since taxation by municipal school

districts was permissible. The common schools were forced

to consider the identical prospect. In turn, both remedies

were attempted.

The Four Section Settler Act of 1879 provided for the

sale of school lands to actual settlers at $1.00 per acre.

The Fifty Cent Law of 1879 provided for the sale of unap

propriated public domain at 50<: per acre, with half the

revenue going to the school fund. Over 360,000 acres were

sold during the first nine months after the laws took

effect, but little cash was added to the school fund

because of the long-term notes on the land. In 1883, under

Governor John Ireland, the Fifty Cent Law was repealed, and

the Four Section Settler Act was modified. The bid to

increase school revenues through land sales was acknowl

edged as unsuccessful, and attention turned to local taxa

tion (McKay, 1943) .

In 1883 a constitutional amendment .was passed which

favored the establishment of permanent school districts and

the right of local taxation for school support whenever

local citizens voted to do so. The amendment specified the

sources of revenue for school support: (1) one-fourth of

29

the revenue from state occupational taxes, (2) a poll tax

of $1.00 on all males between the ages of 21 and 60, and

(3) a state ad valorem tax not to exceed 20<: per $100.

In order to qualify for state funds a district had to

operate the schools for a minimum of six months during the

school year (Eby, 1918).

The state school law was rewritten in 1884. It pro

vided for the popular election of a state superintendent,

the organization of all but fifty-three counties into

school districts (those fifty-three retained the "community"

plan), and local taxation in organized districts to a maxi

mum of 20<: per $100 (if approved by a two-thirds vote of

property owners) . The state ad valorem tax of 20<: per $100

was implemented, and provisions were made for the invest

ment of the permanent school fund in order to increase

revenues. Theretofore, the school fund could be invested

only in United States and Texas bonds; county bonds were

added to the list (Cooper, 1934).

In the late 1870s and early 1880s the work of the

Peabody Fund and Dr. Barnas Sears resulted in the estab

lishment of model schools in Houston, Brenham, San Antonio,

and a few other Texas cities. As these "town" schools

developed, so did the idea of local control for town

schools and local taxation for the support of town schools.

30

A series of laws in the period 1875-1881 had the

result of allowing urban centers to exercise more self-

determination relative to schools. An 1875 law gave

"incorporated cities" the right to assume control of the

schools in the city limits, to build schoolhouses, and to

levy local taxes by a vote of the citizens. The Consti

tution of 18 76 vested legal authority for urban school con

trol in the city councils, reaffirmed the authority granted

in 1875, and set a two-thirds vote as a necessary antece

dent to local taxation for school support. A law enacted

in 1879 limited school taxes in the town schools to 50<: per

$100, and still another act in 1881 allowed unincorporated

towns and villages over 200 in population to incorporate

for school purposes. The net effect of these laws was to

grant urban "town" districts an advantage over the rural

"common" school districts (Eby, 1925).

Despite the apparent progress made through the con

stitutional amendment of 18 83 and the concomitant school

law of 1884, little forward movement was realized (Eby,

1925). The responsibility for educational progress was,

in effect, shifted to the counties and local districts. At

the time this movement was thought beneficial because of

tlie success of some town schools, but rural districts dis

played little zeal for the task. The people were generally

ignorant of good standards for schools, the two-thirds vote

31

necessary for local taxation was difficult to muster, and

stagnation remained the hallmark of the rural common

schools for many years (Eby, 1925). Local' control also

provided for a wide spectrum of educational quality and

school support (Connor, 1971). Such was the general rule

during the remainder of the nineteenth century and well

into the twentieth century (Bralley, 1907). In retrospect,

it can be seen that inequities in educational opportuni

ties came to Texas as early as state support did, but it

was reliance upon local property wealth which brought the

inequalities into sharper perspective (Eby, 1925).

The chief cause of the lack of progress was no doubt

absence of input (Eby, 1925). In 1880 the total taxable

wealth of Texas was $825,000,000, and 12.5<: per $100 was

paid to education. By 1900 the taxable wealth was over

$2.3 billion, and still only 19.2<: per $100 went to educa

tion (Henderson, 1907). Many people erroneously believed

that the colossal permanent school fund could handle the

problem, and this delusion undoubtedly created citizen

apathy. Others were merely ignorant. To be sure, some

were even convinced that Texas schools were the best in the

nation, all evidence to the contrary notwithstanding

(Eby, 1925).

By 1900 the discrimination in terms of dollars

expended for education was apparent throughout the state,

32

especially in terms of urban-rural comparisons. In 1900

there were 729,217 scholastics in the state, of which

571,536 (78 percent) were rural students. Rural districts

in 1900 expended an average of $4.97 per pupil compared to

urban spending of $8.35 per pupil. Average school terms

were 9 8 days in rural schools and 162 days in urban

schools. Despite the fact that urban districts had only

22 percent of the state's scholastics, they had about two-

thirds of the school-owned property in Texas ($5,000,000

to $2,600,000). Average salaries in town schools were

$458.50 compared to $226.82 in rural schools. Of the

11,460 rural districts existent in 1900, only 930 were

graded; the remaining 92 percent were one-teacher schools

(Biennial Report, 1900).

Perhaps the most apparent feature of the discrimina

tion against the rural schools was the fact that it was

constitutional and legal. Where the constitutional tax

limit was 50<: per $100 in town districts, the ceiling was

20<: in common districts. Moreover, country schools were

guaranteed only a six-month school term. Towns were

allowed to vote bonded indebtedness; rural schools were not.

Moreover, there were no high schools in the rural areas

(Evans, 1955).

Despite the overriding difficulties, some educational

progress was made during the period 1900-1920 (Connor,

33

1971). The value of school-owned property increased

eight times during the two decades; the number of scholas

tics rose to 1,233,860; and professional personnel

increased from about 15,000 to over 31,000. State per

capita funds increased from $4.50 per pupil to $14.50.

However, Texans' comfortable existence was shaken by a

study in 1920 which revealed that Texas ranked thirty-

ninth among the forty-eight states in both efforts and

results relative to education (Connor, 1971).

Fiscal progress in the early 1900s included a fuller

tax rendition law in 1905 and the addition of personal

property to the tax rolls in 1907. In November, 1908, a

constitutional amendment was passed v;hich allowed common

school districts to utilize local tax monies for equipment

of buildings; abolished the two-thirds vote needed for

local taxation, substituting a simple majority vote; and

increased the tax limitations of common school districts to

50< per $100. However, moves for consolidation of the vast

numbers of districts in the early 1900s failed. In 1901-

1902 there were 7,446 common districts and 288 independent

districts; twenty years later the totals were 7,369 and

858 (Eby, 1925).

Public support of secondary education was slow to

develop and did not begin on a large scale until after

1910 (Connor, 1971). In the rural areas the problem was

34

especially acute. In 1911, during the governorship of

0. B. Colquitt, a rural high school law was passed which

created county boards of education and authorized them

(at local option) to consolidate common districts and

establish rural high schools at local expense. James E.

Ferguson campaigned on a platform which included state

aid for rural high schools and was elected as governor in

1914. The rural high school law was strengthened with

state aid in 1915 (Connor, 19 71). More importantly, the

34th Legislature in 1915 appropriated $1,000,000 for the

biennium for special rural school aid. In order to

receive the aid, a rural district had to tax at its maxi

mum rate of 50C per $100. In effect, the funds offered a

bonus for local effort; they were the first "equalization"

funds distributed by the state. This rural school "equali

zation aid" was legitimatized after the fact by constitu

tional amendment in 1918 (Steen, 1942).

In 1918 another constitutional amendment provided for

free textbooks and a state tax to finance them. Ground

work for this move had been laid with the establishment of

a state textbook selection board in 190 3, the enactment of

a law in 1911 allowing local boards to expend state-derived

funds for textbooks, and enactment of a textbook law in 1915

allowing the use of local funds to buy books. The amendment

of 1918 provided for an increase in the state ad valorem

35

tax from 20C per $100 to 35<: per $100, with the extra 15<:

per $100 earmarked for a textbook fund (Eby, 1925) .

By the early 1920s the modern dilemma of public

school finance in Texas was taking form. Eby (1925)

observed that: "The problem of the equalization of taxa

tion for schools and the problem of equalizing the oppor

tunities of education for all children of the state are

now being more generally discussed." It was already being

noted that disparities in local wealth and local effort

were creating inequities in educational opportunity

(Works, I, 19 25).

In the 1920s most state funds were distributed to

local districts on a per capita basis. These funds com

promised the "available school fund," which consisted of

interest from the permanent school fund, interest from the

different county permanent funds, revenue from the state

ad valorem tax (with 15< per $100 going for textbooks) ,

one-fourth of the occupational taxes, and revenues from

special state taxes on automobiles, oil, etc. To these

per capita funds were added the rural school aid, which was

distributed in a different manner as described above. How

ever, Texans were still slow to reconcile themselves to

local taxation for school purposes (Eby, 1925) . In 1918

Texas ranked forty-fourth among the forty-eight states in

the amount of local support for schools. The average

36

amount per pupil raised by local taxes in 1921-1922 was

only $13.02. In fact, in 1922-1923, fully 11 percent of

the common school districts in Texas levied no taxes at

all (Eby, 1925).

The structure of public school finance in Texas

changed little during the next two decades although state

appropriations continued to increase due to increased reve

nues (Steen, 1942). In 1937 the entire rural school aid

act of 1915 was rewritten, refinanced, and renamed the

"Equalization Fund." In addition, the 1937 law provided

salary aid and transportation aid to rural districts. It

also provided funds for high school tuition for those stu

dents residing in districts without high schools (Evans,

1955).

By 1940-1941 the available school fund provided

almost $40 per child, approximately half of which was

derived from interest earned by the permanent school fund;

by 1948-1949 the per capita apportionment was up to $101

(Texas Research League, 19 56). The remaining portion of

school expenditures, save rural school aid and a small

amount of federal aid, was raised by local school districts

through ad valorem property taxes, the only legal local

school tax (Article VII, Section 3, 1876).

Certain communities and districts in Texas had tax

able wealth sufficient to produce extravagant enrichment

37

at very low tax rates, while others were too poor to

enrich programs at all. Still other districts were tax

havens which levied no taxes whatsoever (Texas Research

League, 1972)." The results were, quite naturally, wide

variations in per pupil expenditures. Equality, other than

the small portion of rural aid, was never much of an issue

until after World War II (Texas Research League, 1972).

By 1947 the pressures for change in Texas public

school finance were irresistible. The post-war world

brought rises in both school enrollments and the cost of

living along with a concomitant fear that educational

revenue could not keep apace under the existing structure.

Moreover, legal attacks on segregation and gross inequities

in spending between white and black students were increas

ing. There were over 5,000 school districts in the state,

the majority of which operated as tax havens (Yudof and

Morgan, 19 74). In addition, the troubling concept of equal

educational opportunity was beginning to filter into the

school finance logic in Texas. The result was the forma

tion of the Gilmer-Aikin Committee in 1947 during the

administration of Governor Beauford Jester. Its charge was

to design a new system for financing the public schools of

the state (Still, 1950). \

The Gilmer-Aikin Committee (1948), in a report

entitled To Have What We Must, publicized the plight of the

38

Texas public schools and the needs for equality, preser

vation of the local control of schools, a minimum salary

schedule for teachers, fairer distribution of tax burdens,

and the concept of a state-supported minimum education.

It proposed the Minimum Foundation Program, a set of for

mulas for allocating state funds for personnel and opera

tions. The aim was "equal minimum educational opportunity,"

not complete equity.

In its essential theory the Minimum Foundation Pro

gram recommended by the Gilmer-Aikin Committee (1948) was

based on the Strayer-Haig-Mort model of "equalization."

In fact, Paul Mort served as a consultant to the legisla

ture during the creation of the law in 1949 (Still, 1950).

By use of a complicated economic index, local education

agencies were assigned their proportionate share of the

20 percent of the Minimum Foundation Program to be financed

locally in the form of a chargeback called the "local fund

assignment." The state, in theory at least, assumed 80

percent of the cost of the total Minimum Foundation Pro

gram. Local districts were free to "enrich" their programs

beyond the state minimum program in keeping with their

local ability and willingness. The proposals were accepted

without radical change and were enacted into law by the

Fifty-first Legislature in 1949.

39

The immediate impact of the Gilmer-Aikin Law was a

significant rise in state support levels. However,

equality was not achieved; in fact, it had not been the

intent of the law except insofar as the Strayer-Haig-Mort

theory was concerned (Yudof and Morgan, 19 74). The pur

pose was to provide a minimum program for every district

with some attention given to the financial abilities of

the local agencies. The law did save many districts from

fiscal chaos. By 1955-1956 the average state contribu

tion was $159 compared to $101 in 1948-1949, the last year

under the "old plan." The Minimum Foundation Program cov

ered about 60 percent of all educational expenditures in

the state in 1955-1956. By 1956-1957 the figure for state

Minimum Foundation Program aid had increased to an average

of $174 per student (Texas Research League, 1957).

Many weaknesses in the Minimum Foundation Program

became apparent soon after enactment of the Gilmer-Aikin

Law. First, a number of small, low-tax-rate districts

were perpetuated by the act. Otherwise, these districts

might have been forced to consolidate with larger dis

tricts. Second, the economic index proved to be a com

plex and inaccurate measure of local district wealth due

to: (1) flaws in the formula itself, not the least of

which was insufficient statistical data; (2) credits

given to certain types of land and to certain districts;

40

and (3) the fact that the index primarily measured income

while district wealth was premised upon taxable property

(Hooker, 1972). Third, the amount of state funds

injected became more a function of the legislative

process than a function of actual costs of an adequate

minimum education. The result was that the Minimum Foun

dation Program covered an ever-decreasing percentage of

the total school expenditures in the state (Yudof and

Morgan, 1974).

By 1965 there were so many deletions, additions,

substitutions, and footnotes to the original Gilmer-

Aikin Law that Texas school finance was aptly described

as "a majority of exceptions" (Texas Research League,

1972). Realizing the need for drastic changes in the

state's public school financing scheme. Governor John

Connally created in 1965 the Governor's Committee on

Public School Education, charging it to develop a long-

range plan which would vault Texas to foremost leadership

in public education. The Governor's Committee was the

first official body in the history of the state to address

itself to the issue of inequities in public school finance

(Yudof and Morgan, 1974).

Against a backdrop of general national concern for

equality in access to school services and about educa

tional outcomes, the Governor's Committee conducted

41

extensive research into nearly every facet of public edu

cation in Texas. The Committee's final report made

numerous proposals and recommendations for reform (Gov

ernor's Committee, 1968), but only a few are listed here

for illustrative purposes:

1. All districts with less than 2,600 students should be consolidated; every district with less than 2,600 students should be at least county-wide. The number of districts in the state would have been reduced to 353, 219 of which would have been county-wide.

2. The state should finance a kindergarten program to be made available first to low-income and non-English-speaking students; opportunities for others would be phased in gradually.

3. The Minimum Foundation Program should be strengthened through additional funds for personnel, operations, textbooks, and materials.

4. The State Board of Education should be redirected to become a policy-setting body, with commensurate authority, for education in the state.

5. All major current expenditure items should be brought under the umbrella of the Minimum Foundation Program so that more equality between "poor" and "wealthy" districts could be achieved.

6. The economic index should be abandoned gradually as a means of calculating local ability and be replaced by measures of equalized property value.

7. The state should adopt a system of guaranteed salary increases for teachers covering a ten-year period.

For its time the report of the Governor's Committee

was radical in scope. Neither did it lack ambition. In

42

regard to public school finance policy, the Committee pro

posed to achieve equalization through the institutional

ized Minimum Foundation Program. Such an ambition was,

in itself, contradictory; however, the immediate effects

likely would have been a large measure of equalization

through massive injections of state aid aimed at a

widened Minimum Foundation Program. The need for many

districts to rely heavily upon local wealth (or the lack

of it) would have been alleviated, thus equalizing expen

ditures to a great extent (Governor's Committee, 1968).

By 196 8, when the Governor's Committee report was

published, John Connally was no longer governor. His

successor, Preston Smith, showed little inclination to

press the issue of school finance reform (Yudof and

Morgan, 19 74). Only three of the Governor's Committee

proposals were enacted into law in 1969: (1) the state-

financed kindergarten program, with a ten-year phase-in

period (Texas Education Code, Section 21.131, amended

1971, 1975); (2) a $400 bonus for vocational teacher

units (Texas Education Code, Section 16.304); and (3) a

teacher's salary scale (Texas Education Code, Chapter 16,

Subchapter D, amended 1973, 1975). The principal^effect

of the teacher salary increase was to suppress movement

toward equalization, for the combined costs of both became

politically unfeasible (Yudof and Morgan, 1974).

43

On December 23, 1971, the United States District

Court for the Western District of Texas handed down a

judicial decision which stunned Texans into a realization

of the ramifications of years of neglect of the problems

of equity in school finance. The case of Rodriguez v.

San Antonio Independent School District had been filed as

a class action suit by residents of the Edgewood Indepen

dent School District in San Antonio in behalf of "all

children throughout Texas who live in school districts

with low property valuations" (Rodriguez v. San Antonio

I.S.D., 1971). The plaintiffs claimed that the method of

financing elementary and secondary education in Texas

deprived their class (school children in poor districts)

of the equal protection of the laws guaranteed by the

Fourteenth Amendment to the U.S. Constitution.

The court, after reviewing evidence of the great

disparities in wealth among Texas school districts, found

merit in the claim and held that "the current system of

financing public education in Texas discriminates on the

basis of wealth by permitting citizens of affluent dis

tricts to provide a higher quality education for their

children, while paying lower taxes" (Rodriguez v. San

Antonio I.S.D., 1971). The court ruled that the Texas

school finance system was unconstitutional and granted

the state legislature two years to develop an equitable

system.

44

On appeal, arguments in the Rodriguez case were

made in the United States Supreme Court in October, 19 72.

In March, 1973, the Court rendered a decision reversing

the lower court's findings by a vote of five to four.

The Texas system was not found to be unconstitutional.

The Court's rationale has been summarized by Hoffman

(1973) as: (1) poor people live in all districts and not

necessarily in districts with low taxable wealth, (2) the

Texas aim to provide an adequate program for each child

in the state was accomplished through the Minimum Founda

tion Program, (3) educational expenditures are not easily

equated to educational quality, and (4) education is not

viewed as a fundamental interest protected by the federal

constitution.

The Supreme Court's reversal of the Rodriguez case

was astounding to many observers of the law and public

school finance. Indeed, the majority opinion, despite the

reversal vote, carried strong encouragement to Texas

legislators to create a better method of state public

school financial support. One dissenting justice, Thurgood

Marshall, expressed concern that the decision went counter

to the trend in many state and federal court decisions in

the early 1970s (San Antonio I.S.D. v. Rodriguez, 1973).

Among these cases were Serrano v. Priest (California, 1971), Van Dusartz v. Hatfield (Minnesota, 1971),

45

In the fifteen-month period from December, 19 71, to

March, 19 73, most Texas educators assumed, not without a

note of terror, that the Supreme Court would uphold the

district court's decision, true to the emerging trend.

Elsewhere in the nation, no less than eleven states drew

up new financing plans for public education in the 2

interim. In each case the intent of the state legisla

ture was to attempt to equalize educational expenditures

across districts (Grubb, 1974).

In the aftermath of the district court decision in

the Rodriguez case, several studies were launched in Texas

Only three actually presented school finance reform plans:

(1) the State Board of Education (Texas Education Agency,

1972, 1973); X2) the Texas State Teachers Association

(1972); and (3) the Joint Interim Senate Committee to

Study School Finance (1973).

The first State Board of Education resource alloca

tion plan ignored the no-wealth discrimination principle

of the Rodriguez decision (Texas Education Agency, 1972).

Caldwell v. Kansas (1972), Milliken v. Green (Michigan, 1972), and Robinson v. Cahill (New Jersey, 1972).

2 The eleven states were California, Colorado,

Florida, Illinois, Kansas, Maine, Michigan, Montana, North Dakota, Utah, and Wisconsin. The flurry of activity was also prompted by the earlier 19 71 suit Serrano v. Priest in which the California Supreme Court struck down that state's school finance system.

46

Three months later the State Board recanted and adopted

a variant form of district power equalization as a proposal

(Texas Education Agency, 1973). The T.S.T.A. proposal

centered around an "improved" Minimum Foundation Program

and did little to address the cogent problem at hand

(T.S.T.A., 1972). The Joint Interim Senate Committee pre

sented twelve alternative schemes resulting from four

allocation plans and three revenue plans (J.I.S.C., 1973).

Its preferred approach was a district power equalization

approach to a new Foundation Program with increased levels

of support, legal minimum tax rates, and legal maximum tax

rates. However, the revenue plan called for increased

local property taxes (J.I.S.C, 1973), a proposal doomed

from its inception.

In Austin the Sixty-third Legislature met in January,

19 73, amid an air of uncertainty. When the Supreme Court's

verdict was learned in March, most of the legislators

breathed a collective sigh of relief and resolved them

selves to enjoy the "stay of execution." One measure

(H.B. 946) was passed in the House of Representatives

which included an equalization feature, but it suffered a

swift demise in the Senate. In all probability it would

have been vetoed by Governor Dolph Briscoe, who was bent

on pursuing a more deliberate course toward equalization

(Yudof and Morgan, 1974).

47

Subsequent to the adjournment of the Sixty-third

Legislature, a number of study groups began preparation

for the Sixth-fourth Legislature in 1975: (1) the Gover

nor's Office of Educational Research and Planning,

headed by Richard Hooker; (2) a Senate study group;

(3) several House study groups; (4) the State Board of

Education; (5) the Texas Research League; (6) the Legis

lative Property Tax Committee; and (7) the Texas Advisory

Commission on Intergovernmental Relations.

When the Sixty-fourth Legislature convened in Janu

ary, 1975, school finance headed the list of major issues

contronting the legislators. Within the school finance

issue, arguments revolved around the key word "equaliza

tion." Moreover, there was renewed cognizance of the fact

that the Minimum Foundation Program encompassed only 55

percent of school expenditures in Texas (Texas Advisory

Commission on Intergovernmental Relations, 1976). However,

the net effect of the intervening studies was that the

legislature was inundated with school finance reform pro

posals of a multiplicity of types.

In finality, the tangible outcome of efforts to

reform Texas public school finance was a compromise bill

(H.B. 1126), hastily constructed in the twilight hours of

the session. In total, H.B. 1126 added about $400,000,000

to the renamed Foundation School Program through increases

48

in salaries for foundation program personnel, transporta

tion funding, operational cost allowances, and categorical

grants for compensatory and driver education (Texas Edu

cation Code, Section 16.004).

The full ramifications of H.B. 1126 are as yet

unknown, but some positive factors are apparent. First,

a state policy was codified which established that:

. . . it is the policy of this state that each student enrolled in the public school system shall have access to programs and services that are appropriate to his educational needs and that are substantially equal to those available to any similar student, notwithstanding varying local economic factors (Texas Education Code, Section 16.001).

Second, the law required that a district had to be

accredited by the Texas Education Agency by 1977-1978 in

order to be eligible to receive Foundation School Program

assistance (Texas Education Code, Section 16.053). Third,

minimum staffing ratios for school districts were codified

(Texas Education Code, Section 16.054). Fourth, and per

haps most important, the chargebacks (local fund assign

ments) of districts were to be calculated on the basis of

actual market value of taxable property as established by

the governor (Texas Education Code, Section 16.252).

Some factors in the new law were revealed as lacking

in foresight, but not all will be enumerated here. As an

example, equalization aid was offered to districts with

local fund assignments per ADA which were less than 125

49

percent of the total statewide local fund assignment per

ADA, to a limit of $70 per ADA or $50,000,000, whichever

was greater (Texas Education Code, Sections 16.301,

16.302):

ax?7y - 1 DLFA/ADA ^^^ ^^-^^^ - ^ - (SLFA/ADA) X 1.25 ^ ^^^ ^ ^^^

In effect, 62.5 percent of the districts in the state

became eligible for equalization aid, and such aid even

tually amounted to only $56 per ADA because of the

$50,000,000 ceiling (T.A.C.I.R., 1976). Nevertheless, a

precedent was established for equalization aid based upon

local tax resources available.

Still another example of the weaknesses in the law

was a provision for $40 per disadvantaged pupil to a limit

of $25,400,000 per year (Texas Education Code, Section

16.176). In effect, districts realized about $39 per dis

advantaged pupil; the Governor's Committee (19 68) had

recommended $100 per disadvantaged pupil as a reasonable

figure before the inflation of school costs during the

1970s. Therefore, state aid for compensatory education

was ineffectual in regard to amount of input.

A third and perhaps most important weakness of the

law was that the chargeback calculation was ineffective in

creating equalization. Although based upon the equalized

50

market value of property, chargeback to districts by 19 76-

1977 was required at a rate equal to 35<: per $100 of valu

ation (Texas Education Code, Section 16.252). Whereas in

1974-1975 the Minimum Foundation Program accounted for

only 55 percent of school expenditures, by 1976-1977 the

percentage was still only about 60 percent (Texas Research

League, 1976). Heavy reliance upon local property tax

wealth without some countermeasure, such as "recapture"

from wealthy districts, was still being perpetuated and was

counterproductive relative to equalization. Increases in

Foundation School Program costs were expended primarily for

salary increases, and salaries accounted for 85.6 percent

of operating costs in 1975-1976 (Texas Research League,

19 76). Allocations for operating costs were not enough to

allay effectively the specter of inflation. In short, the

law only perpetuated, at an inflated scale, the same

inequities apparent since the pre-Gilmer-Aikin era.

In enacting H.B. 1126 the legislature directed the

governor to:

. . . conduct a study to determine methods of allocating state funds to school districts which will insure that each student of this state has access to programs and services that are appropriate to his educational needs regardless of geographic differences and varying local economic factors. . . . The study shall include a determination of each school district's ability to support public education based on the value of taxable property in the district (Texas Education Code, Section 16.001, note).

51

The report of this study, contained in the Preliminary

Report of the Governor's Office, Education Resources

(1976) , was presented to the public simultaneously with

Governor Briscoe's school finance proposals for the

Sixth-fifth Legislature on November 1, 1976. '

The Governor's Plan, as it was known, called for an

increase of $850,000,000 in state aid to schools through

funds providing for: (1) expanded Foundation School Pro

gram allocations, (2) a substantial raise in equalization

aid (to $250,000,000), (3) increased transportation allot

ments, (4) renewal and accountability, and (5) aid for the

improvement of school tax office operations (G.O.E.R.,

1976). In addition, the plan called for a chargeback rate

of 9<J: per $100 in valuation, with the state assuming

90 percent of the cost of the Foundation School Program.

Also presented were the new equalized valuations of prop

erty as determined by the Governor's Office, Education

Resources, headed by John Poerner. Especially hard hit

were districts with large amounts of rural land (Manage

ment Services Associates, 1976a).

Even as the Governor's Plan was being revealed,

other proposals for reform were afoot. Chief among the

new plans was that voted out of the Special House Com

mittee on Alternatives to Public School Finance. It con

tained recommendations that: (1) the state assume

52

100 percent of the cost of the Foundation School Program,

(2) that local districts be required to lower property

taxes to reflect increased state aid, and (3) that local

tax increases beyond legally established local enrichment

limits (15 percent) be submitted to the voters of a dis

trict for approval (Management Services Associates, 1976b)

Governor Briscoe then added to his plan the notion of a

ceiling on local taxes, a move calculated to appease

beleaguered property-taxpayers as well as to point toward

equalization (M.S.A., 1976b).

Chief among the objections to both the Governor's

Plan and the Special House Committee plan was a concern

that both proposals would result in the majority of new

state funds flowing to districts which were larger,

wealthier, or could well afford to support a program

locally without intensive state supplement (M.S.A., 1976b).

Other sources of consternation were the Governor's

obliviousness to the issue of a teacher pay raise and the

Special House Committee's insistence upon a local plebi

scite. To these questions was added the prospect of

increased state taxes to finance the anticipated expendi

tures. The possibility of no-wealth discrimination reform

by the Sixty-fifth Legislature is, then, still

problematical.

53

The long-term prospects for school reform in Texas

are as uncertain as the immediate circumstances. Yudof

and Morgan (1974) have identified several critical factors

which are not current in Texas but which must be present

if reform is to be effected. Two factors are of note.

First, there must be a public consensus that school

finance reform to achieve equity is in the best interest

of all citizens, not just minorities or residents of

"poor" districts.

At present, two philosophies are competing for public

favor: (1) the idea of a free market approach to educa

tional goods and services similar to that taken toward

other private and public goods and services; that is,

since all consumer goods are not equally accessible to all

citizens, education should be no exception; and (2) the

idea of a controlled market in which access to educational

goods and services is equal for all rather than a result

of wealth or poverty in a school district. Especially

crucial to the consensus are legislators, educators, tax

reformers, the governor, and teacher organizations (Yudof

and Morgan, 19 74) .

Second, it is an acknowledged principle that equali

zation of educational expenditures requires large input

from state-derived revenues (Phi Delta Kappa Commission,