copyright leslie lumpage 1 module 1 why are you here?

Post on 20-Dec-2015

217 views

TRANSCRIPT

Copyright Leslie Lum Page 1

Module 1Why Are You Here?

Copyright Leslie Lum Page 2

Module One Learning Objectives

• Set expectations for the course.• Explore and dispel misconceptions about investing.• Compile a personal budget.• Demonstrate the benefits of saving.• Apply compounding to savings set aside today.• Set financial goals.• Calculate present value of a sum needed in the future.• Calculate future value of annual savings.• Demonstrate the effect of varying inflation rates on future

financial goals.• Demonstrate the effect of varying rates of return on achieving

future financial goals.• Create a personal financial plan.

Copyright Leslie Lum Page 3

Learning about investing means--

• I’ll be rich.• I’ll learn about stocks only.• Once I’ve got the formula down, I’m set.• I’ll never have to change my investments.• I’ll change my investments all the time.• I’ll be able to control exactly how much I

make.• I’ll make just as much as my cousin Arnie.

Copyright Leslie Lum Page 4

I don’t need to know about investing because

• I’m going to hire someone to take care of my money.

• My employer takes care of my investing.

• I don’t have any money.

Copyright Leslie Lum Page 5

The Investment Process

• Goals• What you will and won’t invest in• Knowledge of all the different kinds

of investments• A way of selecting the ones for you• How to monitor your investments

American Financial Life Pop Quiz

Copyright Leslie Lum Page 6

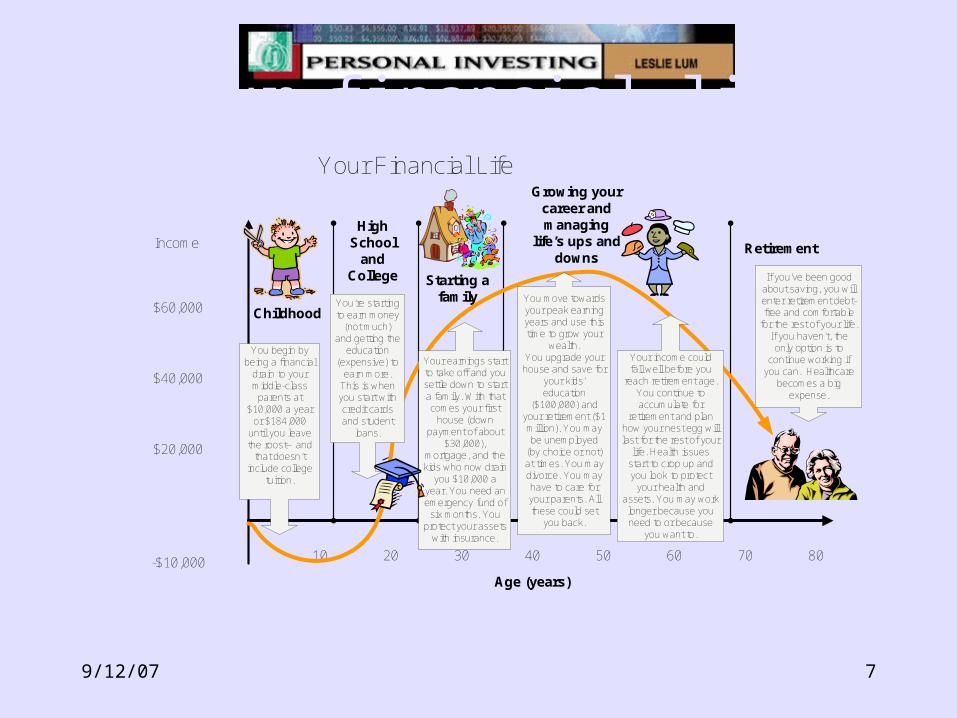

9/12/07

Age (years)

10 20 30 40 50 60 70 80

Childhood

High School

and College Starting a

family

Growing your career and managing

life’s ups and downs

Retirement

Your Financial Life

-$10,000

$20,000

$40,000

$60,000

You begin by being a financial

drain to your middle-class

parents at $10,000 a year

or $184,000 until you leave the roost—and

that doesn’t include college

tuition.

Income

You’re starting to earn money

(not much) and getting the

education (expensive) to

earn more. This is when you start with credit cards and student

loans.

Your earnings start to take off and you settle down to start a family. With that comes your first

house (down payment of about

$30,000), mortgage, and the kids who now drain

you $10,000 a year. You need an emergency fund of

six months. You protect your assets

with insurance.

You move towards your peak earning years and use this time to grow your

wealth. You upgrade your house and save for

your kids’ education

($100,000) and your retirement ($1 million). You may be unemployed

(by choice or not) at times. You may divorce. You may have to care for your parents. All these could set

you back.

Your income could fall well before you

reach retirement age. You continue to accumulate for

retirement and plan how your nest egg will last for the rest of your

life. Health issues start to crop up and you look to protect

your health and assets. You may work longer because you need to or because

you want to.

If you’ve been good about saving, you will enter retirement debt-free and comfortable

for the rest of your life. If you haven’t, the only option is to

continue working if you can. Healthcare

becomes a big expense.

Your financial life

7

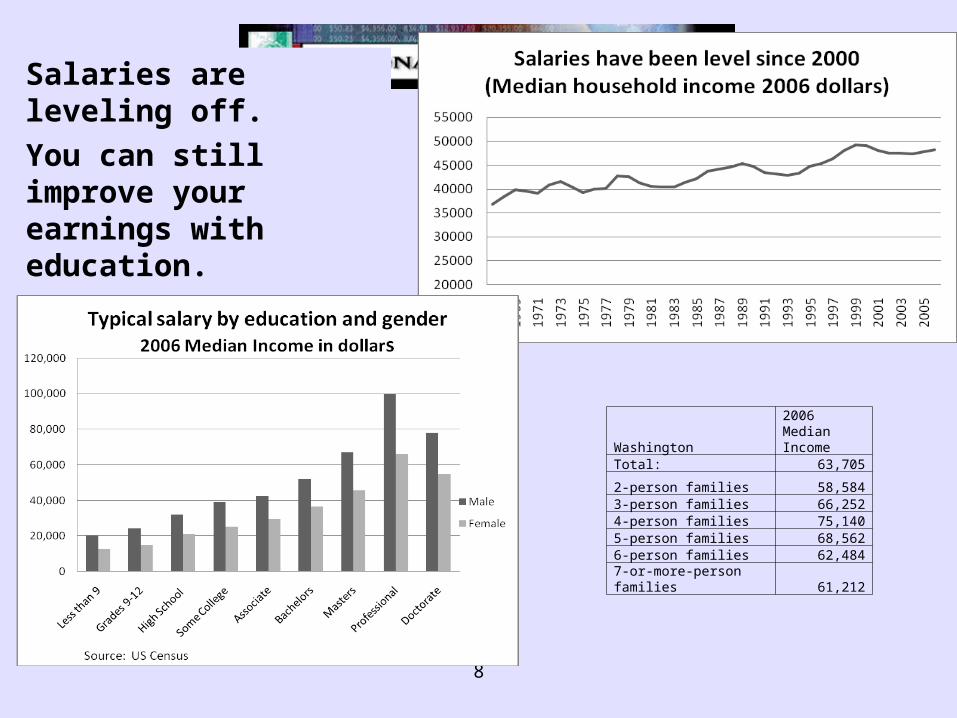

Salaries are leveling off.You can still improve your earnings with education.

Washington

2006 Median Income

Total: 63,705

2-person families 58,5843-person families 66,2524-person families 75,1405-person families 68,5626-person families 62,4847-or-more-person families 61,212

8

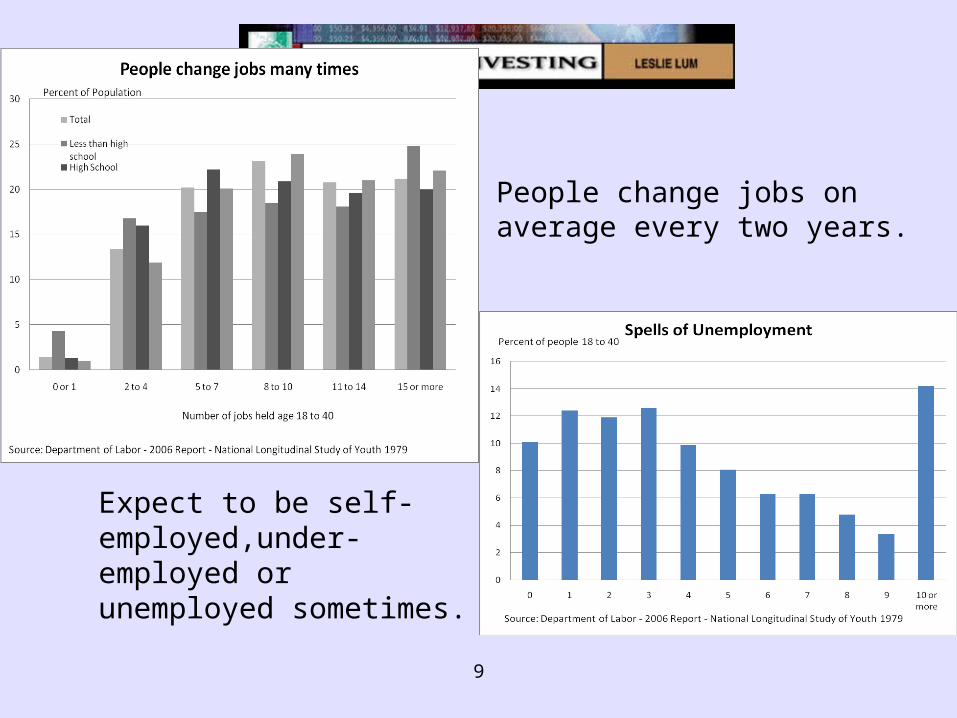

Expect to be self-employed,under-employed or unemployed sometimes.

People change jobs on average every two years.

9

9/12/07

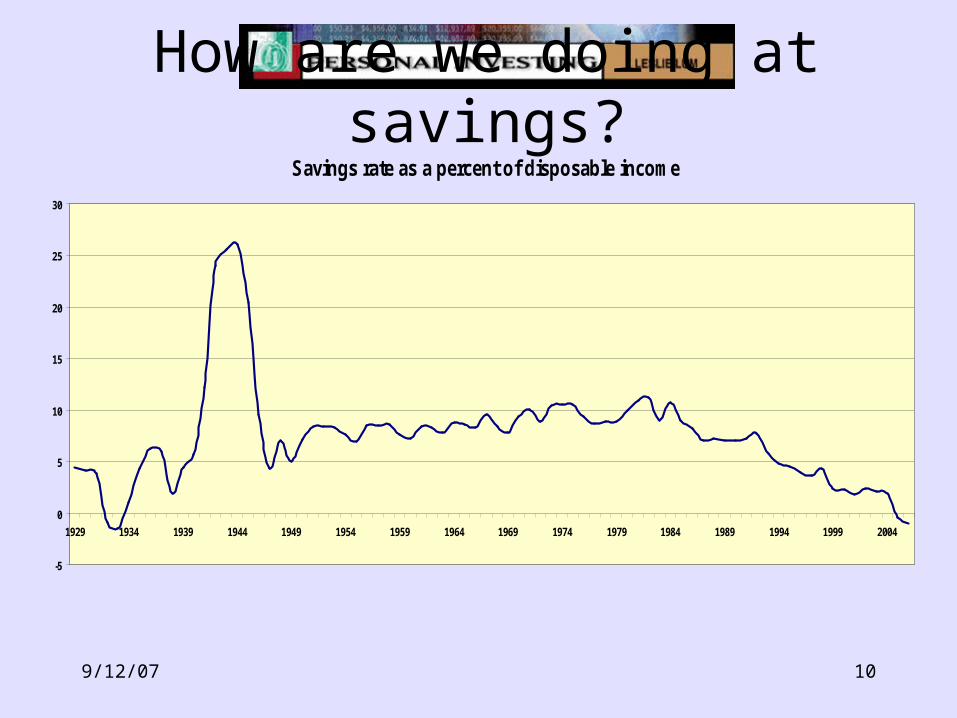

How are we doing at savings?

Savings rate as a percent of disposable income

-5

0

5

10

15

20

25

30

1929 1934 1939 1944 1949 1954 1959 1964 1969 1974 1979 1984 1989 1994 1999 2004

Source: http://www.bea.gov/bea/dn/nipaweb/TableView.asp#Mid

10

9/12/07

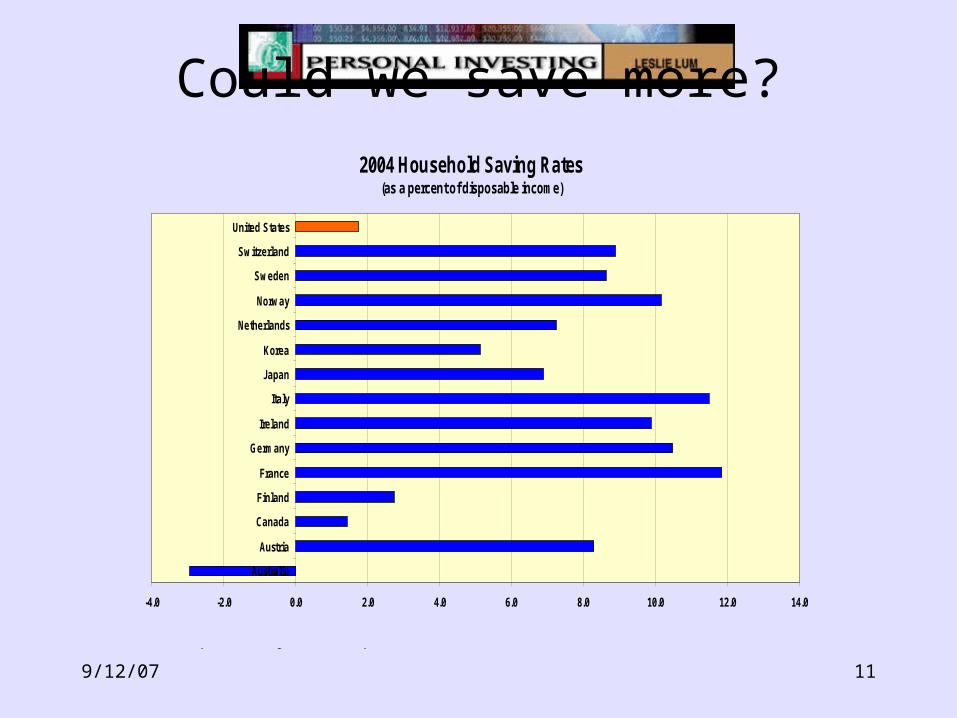

Could we save more?2004 Household Saving Rates

(as a percent of disposable income)

-4.0 -2.0 0.0 2.0 4.0 6.0 8.0 10.0 12.0 14.0

Australia

Austria

Canada

Finland

France

Germany

Ireland

Italy

Japan

Korea

Netherlands

Norway

Sweden

Switzerland

United States

http://stats.oecd.org/WBOS/default.aspx?DatasetCode=REFSERIES

11

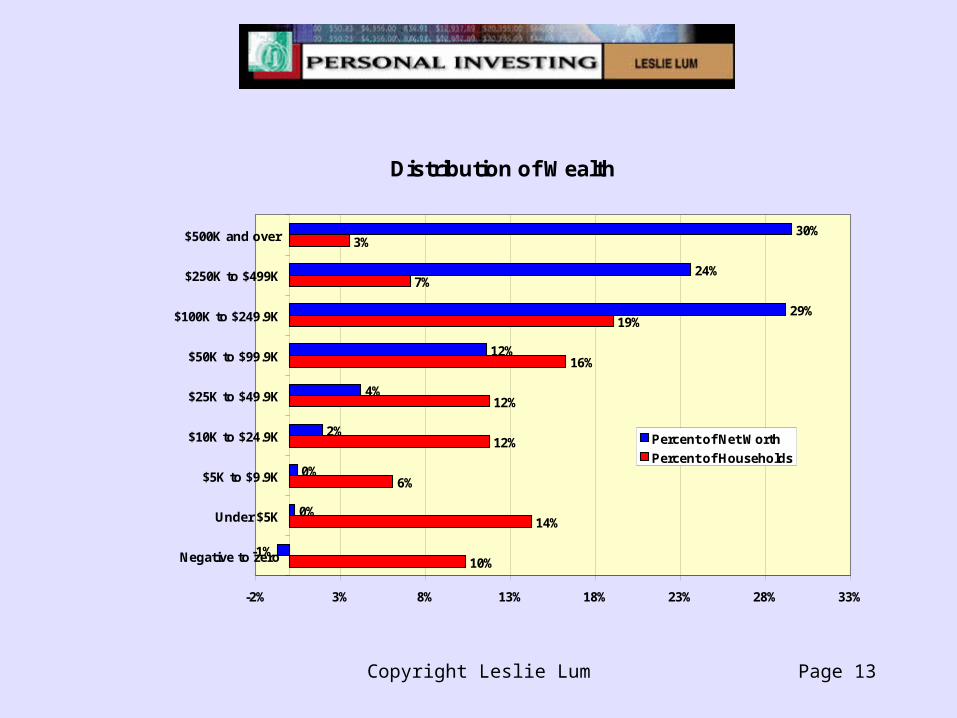

Most of our wealth is in our homes

Copyright Leslie Lum Page 13

Distribution of Wealth

10%

14%

6%

12%

12%

16%

19%

7%

3%

-1%

0%

0%

2%

4%

12%

29%

24%

30%

-2% 3% 8% 13% 18% 23% 28% 33%

Negative to zero

Under $5K

$5K to $9.9K

$10K to $24.9K

$25K to $49.9K

$50K to $99.9K

$100K to $249.9K

$250K to $499K

$500K and over

Percent of Net Worth

Percent of Households

Household Net Worth

9/12/07

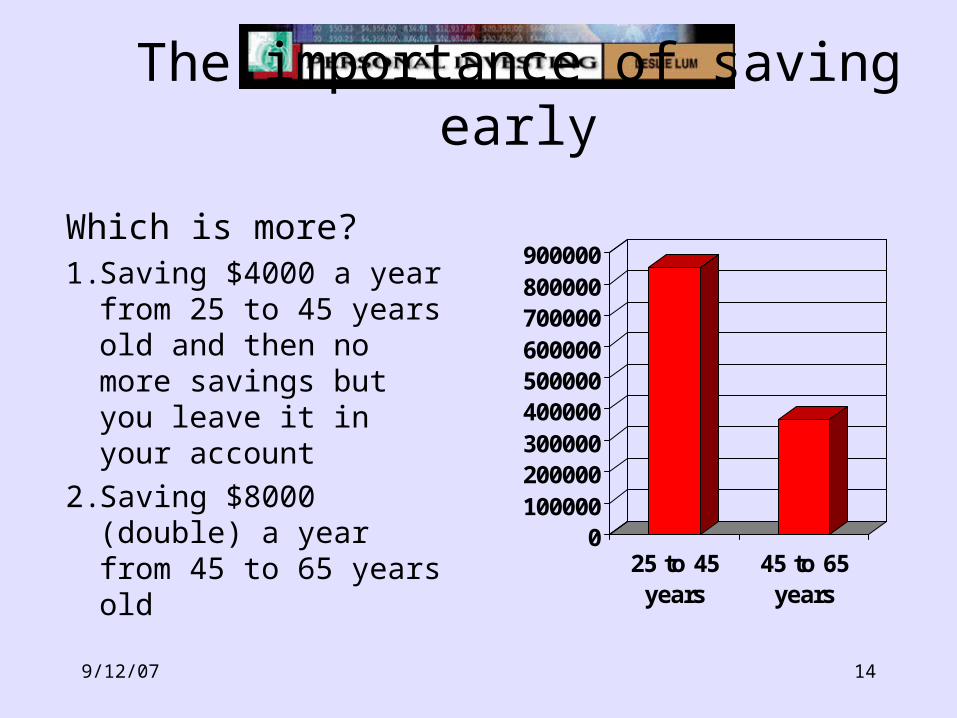

The importance of saving early

Which is more?1. Saving $4000 a year

from 25 to 45 years old and then no more savings but you leave it in your account

2. Saving $8000 (double) a year from 45 to 65 years old

0100000200000300000400000500000600000700000800000900000

25 to 45years

45 to 65years

14

Another example of starting early

Number of years

Savings per year

Total contribution

s Earnings Total

25-65 years 40 4000 160000 $798,540.45 $958,540.45

30-65 years 35 4000 140000 $552,947.51 $692,947.51

35-65 years 30 4000 120000 $377,843.15 $497,843.15

40-65 years 25 4000 100000 $252,996.15 $352,996.15

9/12/07 15

Copyright Leslie Lum Page 16

How to start

• Know yourself– What do you want out of life?– How much work are you willing to put

into it?– What trade-offs are you willing to

make?– How much turbulence can you take?– How do you stand financially?

Copyright Leslie Lum Page 17

Knowing yourself financially.What you spend every year for:

• Food at home.• Food away from home.• Transportation (Car, bus, insurance,

gas)• Housing (Rent or mortgage)• Clothing• Entertainment• Tobacco• Alcohol

Copyright Leslie Lum Page 18

One person Two person Three personFour

personFive or

more

Expenditures Total 23,507 40,359 45,508 54,395 53,805

Food at home 1,533 2,954 3,696 4,404 5,151

Food away from home 1,302 2,336 2,512 3,043 3,042

Alcoholic beverages 314 400 315 368 309

Housing 8,371 12,944 14,744 17,914 17,317

Apparel 862 1,650 2,013 2,643 2,893

Transportation 4,012 7,692 9,348 10,775 11,123

Healthcare 1,441 2,827 2,265 2,253 2,150

Entertainment 1,097 2,051 2,137 2,787 2,718

Personal 297 512 555 614 658

Reading 111 168 139 155 131

Education 423 476 830 1,059 984

Tobacco 203 312 397 349 416

Miscellaneous 518 744 843 1,156 743

Cash contributions 1,063 1,429 1,167 1,287 1,399

Personal insurance and pensions 1,960 3,864 4,547 5,589 4,770

Personal Taxes 1,829 3,599 3,066 3,900 2,652

Copyright Leslie Lum Page 19

You have the highest chance of accumulating wealth when

you:• Invest in new hot tech stocks• Have rich relatives who might

include you in their wills • Buy a lottery ticket• Marry someone with money• Save

Copyright Leslie Lum Page 20

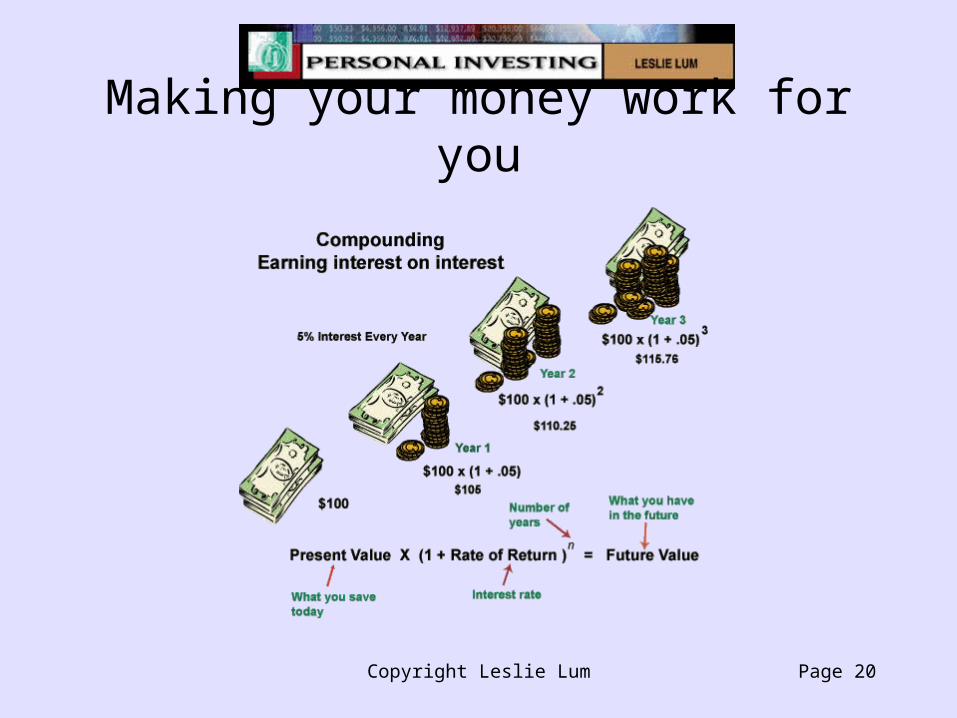

Making your money work for you

Copyright Leslie Lum Page 21

Making your money work for you.What would you have if you did the

following with $100 in 1995?

• Bought beer• Put it in the bank for 5% interest

per year• Bought Microsoft stock (10 shares)

Copyright Leslie Lum Page 22

Let’s use compounding another way—to find the (future) cost of a

purchase decision• You want to buy a second TV set for

$400. What is this (future) costing you? (Use 20 years and 8% return. We use 8% because it’s historically the rate of return on investments over a long period of time.)– $467– $892– $1,254– $1,865

Copyright Leslie Lum Page 23

Lay out your goals

• Down payment on house• Wedding• Car• Big trip• College tuition• Starting your own business• Retirement

Copyright Leslie Lum Page 24

Getting from here to your goals

Copyright Leslie Lum Page 25

What do you have to set aside today for:

(Use 8% return)• A $40,000 down payment on a house in

10 years• $50,000 college tuition for your kid in

15 years• $800,000 for retirement in 30 years• Just a minute---is it possible to save for

big goals?

Copyright Leslie Lum Page 26

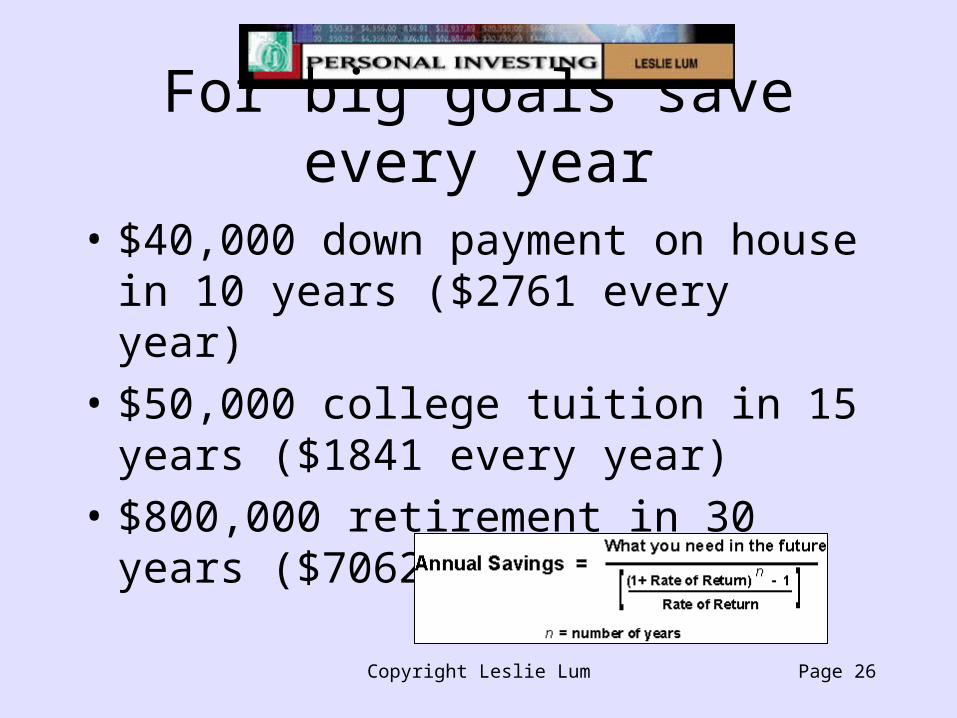

For big goals save every year

• $40,000 down payment on house in 10 years ($2761 every year)

• $50,000 college tuition in 15 years ($1841 every year)

• $800,000 retirement in 30 years ($7062 every year)

Copyright Leslie Lum Page 27

Which is more (and how much more)?

• Saving $1000 a year for 5 years at a 10% return

• Saving $300 a year for 45 years at a 5% return

Copyright Leslie Lum Page 28

You’re 25 and plan to retire in 40 years. How much do you save every year to have a $1 M nest

egg.

• If you start at age 45.• If you start at age 35.• If you start now.

Copyright Leslie Lum Page 29

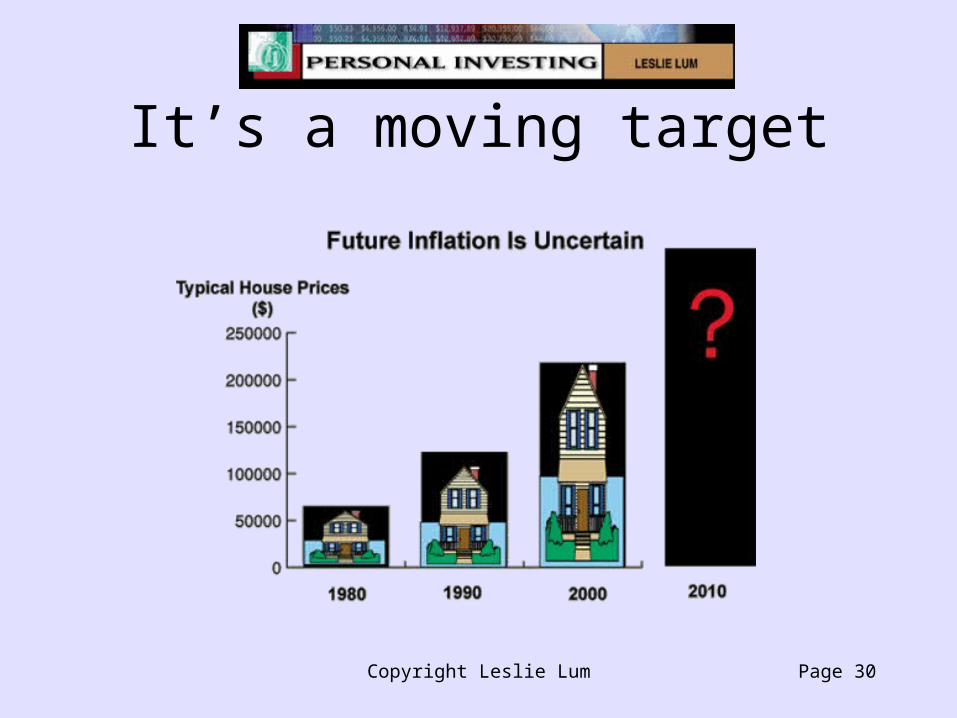

Copyright Leslie Lum Page 30

It’s a moving target

Copyright Leslie Lum Page 31

Calculate the effects of inflation on financial goals. Use 2% and

4% inflation.

• House in 10 years. Today’s price $200,000

• Kid’s college education in 18 years. Today’s price $50,000

Copyright Leslie Lum Page 32

That’s not the only uncertaintyFuture Investment Returns Are Uncertain

6%

9%

5%6%

14%

8%

-2%

18%19%

-5%

0%

5%

10%

15%

20%

25%

1970's 1980's 1990's 2000's

Av

era

ge

Ye

arl

y R

etu

rn f

or

De

ca

de

Cash

Bond

Stock

Copyright Leslie Lum Page 33

Calculate and comment on the annual savings needed

• Wedding in 5 years. Return 8%. Is 8% a good return to use?

• College education in 20 years. Return 13%. Is 13% a good return to use?

• Conclusion: Use sensitivity analysis in your financial planning. The future is uncertain.

Copyright Leslie Lum Page 34

Copyright Leslie Lum Page 35

Copyright Leslie Lum Page 36

Applying the annual savings formula

• Wedding - $1329 for 5 years• First House - $5185 for 7 years• Trade-up House - $5,449 for 8 years• Kid 1 College - $4592 for 18 years• Kid 2 College - $4871 for 18 years• Retirement - $7166 for 40 years

Copyright Leslie Lum Page 37

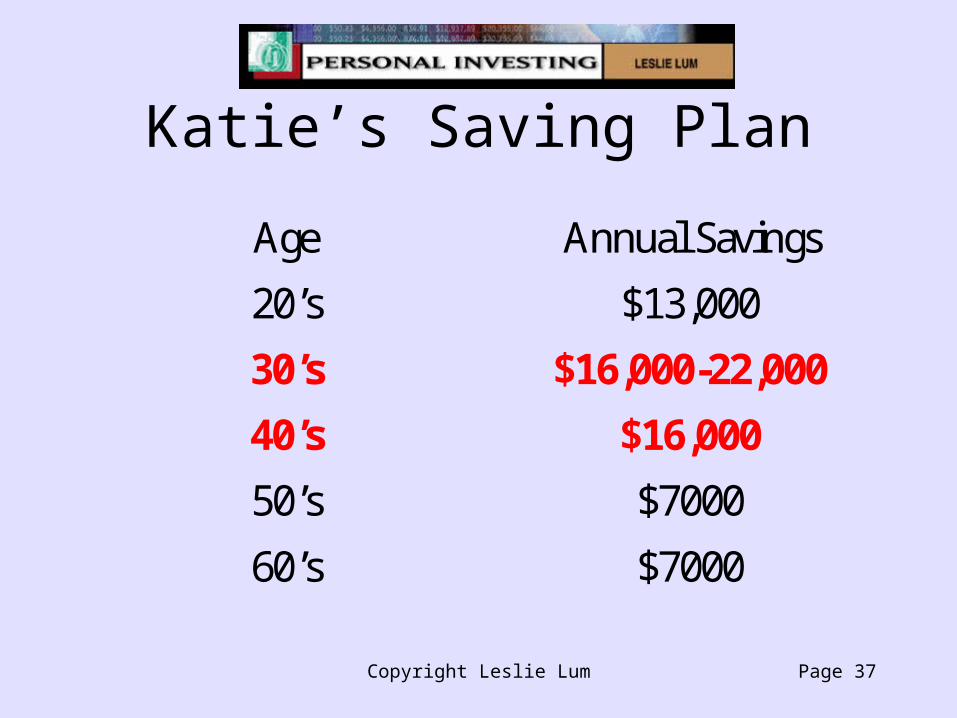

Katie’s Saving Plan

Age Annual Savings

20’s $13,000

30’s $16,000-22,000

40’s $16,000

50’s $7000

60’s $7000