corporate accounting - himpub.com accounting prof. (mrs.) prashanta athma ... kolkata -700 010,...

TRANSCRIPT

Corporate Accounting

Prof. (Mrs.) Prashanta AthmaProfessor,

Department of Commerce,Osmania University,

Hyderabad, Telangana State.

Mrs. N. RajyalaxmiAsst. Professor,

Department of Commerce,University College for Women,

Koti, Hyderabad, Telangana State.

MUMBAI NEW DELHI NAGPUR BENGALURU HYDERABAD CHENNAI PUNE LUCKNOW AHMEDABAD ERNAKULAM BHUBANESWAR INDORE KOLKATA GUWAHATI

© AuthorsNo part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form orby any means, electronic, mechanical, photocopying, recording and/or otherwise without the priorwritten permission of the publisher.

First Edition : 2015

Published by : Mrs. Meena Pandey for Himalaya Publishing House Pvt. Ltd.,“Ramdoot”, Dr. Bhalerao Marg, Girgaon, Mumbai - 400 004.Phone: 022-23860170/23863863, Fax: 022-23877178E-mail: [email protected]; Website: www.himpub.com

Branch Offices :New Delhi : “Pooja Apartments”, 4-B, Murari Lal Street, Ansari Road, Darya Ganj,

New Delhi - 110 002. Phone: 011-23270392, 23278631; Fax: 011-23256286

Nagpur : Kundanlal Chandak Industrial Estate, Ghat Road, Nagpur - 440 018.Phone: 0712-2738731, 3296733; Telefax: 0712-2721215

Bengaluru : No. 16/1 (Old 12/1), 1st Floor, Next to Hotel Highlands, Madhava Nagar,Race Course Road, Bengaluru - 560 001.Phone: 080-32919385; Telefax: 080-22286611

Hyderabad : No. 3-4-184, Lingampally, Besides Raghavendra Swamy Matham, Kachiguda,Hyderabad - 500 027. Phone: 040-27560041, 27550139; Mobile: 09390905282

Chennai : No. 8/2, 2nd Madley Street, Ground Floor, T. Nagar, Chennai - 600 017.Mobile: 09345345055

Pune : First Floor, "Laksha" Apartment, No. 527, Mehunpura, Shaniwarpeth(Near Prabhat Theatre), Pune - 411 030. Phone: 020-24496323/24496333;Mobile: 09370579333

Lucknow : House No 731, Shekhupura Colony, Near B.D. Convent School, Aliganj,Lucknow - 226 022. Mobile: 09307501549

Ahmedabad : 114, “SHAIL”, 1st Floor, Opp. Madhu Sudan House, C.G. Road, Navrang Pura,Ahmedabad - 380 009. Phone: 079-26560126; Mobile: 09377088847

Ernakulam : 39/176 (New No: 60/251) 1st Floor, Karikkamuri Road, Ernakulam,Kochi - 682011, Phone: 0484-2378012, 2378016; Mobile: 09344199799

Bhubaneswar : 5 Station Square, Bhubaneswar - 751 001 (Odisha).Phone: 0674-2532129, Mobile: 09338746007

Indore : Kesardeep Avenue Extension, 73, Narayan Bagh, Flat No. 302, IIIrd Floor,Near Humpty Dumpty School, Indore - 452 007 (M.P.). Mobile: 09301386468

Kolkata : 108/4, Beliaghata Main Road, Near ID Hospital, Opp. SBI Bank,Kolkata -700 010, Phone: 033-32449649, Mobile: 09883055590, 07439040301

Guwahati : House No. 15, Behind Pragjyotish College, Near Sharma Printing Press,P.O. Bharalumukh, Guwahati - 781009, (Assam).Mobile: 09883055590, 09883055536

DTP by : Nitin GodePrinted at : M/s. Charita Impressions, Hyderabad. On behalf of HPH.

The book on “Corporate Accounting” lays particular emphasis on the fundamentals ofAccounting Standards; Valuation of Goodwill and Shares; Company Final Accounts;Amalgamation and Internal Reconstruction; Bank and Insurance Accounts alongwith the Labwork wherever necessary.

A sincere and an earnest attempt is made to present the information in a non-technical,simple and lucid manner so as to enable the reader to understand the subject matter withoutdifficulty.

The book is designed focussing its attention on the Syllabus at the undergraduate level ofvarious universities. The book contains sufficiently a large number of illustrations for a bettergrasp in the subject matter. Wherever necessary, working notes and explanations have beenprovided. Lab work for the Company Accounts, Amalgamation and Bank Accounts is providedusing tally software.

Suggestions for improvement of the work are solicited.We thank Mr. S. Chandra Babu, HR and Legal Professional; Mr. V. Sravan Kumar, Senior

Assistant, ZP, RR Dist., Mr. Vinay Aditya and Ms Simhavalli Hasini for their silent contributionin the completion of the herculean task.

We also thank the publishers for the timely publication and our special thanks are to Mr.Krishna Poojari for the keen interest taken by him in bringing out this book.

— Authors

Preface

B.Com. Degree Course (III Year)Corporate Accounting

Paper: 301 Max. Marks: 70T + 30P= 100P.P.W: 5(4+1) Time: 3 Hours

Objectives

1. To provide the knowledge relating to the Accounting Standards

2. To enable the students to prepare the final accounts using Accounting package

3. To enable the students to prepare Financial Statements of Insurance and Bank Companies

Unit-I: Accounting Standards - Valuation of Goodwill and Shares

Accounting Standards: Need and Importance - An overview of Indian Accounting Standards

Valuation of Goodwill: Need - Methods: Normal Profit Method, Super Profits Method,Capitalization Method

Valuation of Shares: Need for Valuation - Methods of Valuation: Net Assets Method, YieldBasis Method, Fair Value Method

Unit-II: Company Final Accounts - Issue of Bonus Shares and Profits Prior to Incorporation

Preparation of Final Accounts: Provisions relating to the preparation of Final Accounts –Profit and Loss Account and Balance Sheet

Computer Lab Work: Preparation of Final Accounts using Computers

Issue of Bonus Shares: Provisions of Company’s Act and SEBI Guidelines - Acquisition ofBusiness and Profits Prior to Incorporation – Accounting Treatment

Unit-III: Amalgamation and Internal Reconstruction

Amalgamation in the nature of Merger and Purchase: Calculation of PurchaseConsideration - Treatment in the Books of Transferor and Transferee (as per AccountingStandard 14, excluding Inter- Company Holdings)

Computer Lab Work: Recording of transactions relating to Mergers using Computers

Internal Reconstruction: Accounting Treatment – Preparation of Final Statements afterReconstruction

Computer Lab Work: Recording of transactions relating to Internal Reconstruction usingComputers

Syllabus

Unit-IV: Bank Accounts

Bank Accounts: Books and Registers to be maintained by the Banks - Slip System of Posting- Rebate on Bills Discounted - Schedule of Advances – Non Performing Assets - LegalProvisions relating to preparation of Final Accounts

Computer Lab Work: Preparation of Bank Final Accounts using Computers

Unit-V: Accounts of Insurance Companies

Life Insurance Companies: Preparation of Revenue Account - Profit and Loss Account -Balance Sheet and Valuation Balance Sheet

General Insurance: Preparation of Final Accounts with special reference to Fire & MarineInsurance only

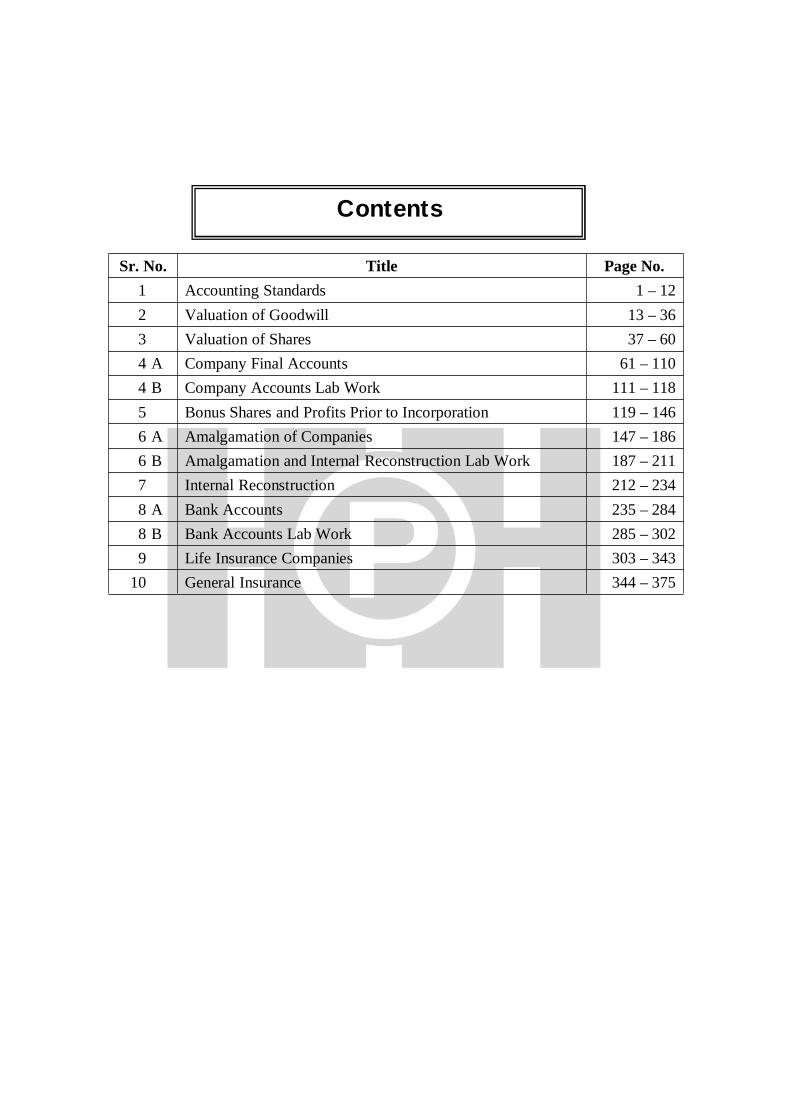

Sr. No. Title Page No.1 Accounting Standards 1 – 122 Valuation of Goodwill 13 – 363 Valuation of Shares 37 – 604 A Company Final Accounts 61 – 1104 B Company Accounts Lab Work 111 – 1185 Bonus Shares and Profits Prior to Incorporation 119 – 1466 A Amalgamation of Companies 147 – 1866 B Amalgamation and Internal Reconstruction Lab Work 187 – 2117 Internal Reconstruction 212 – 2348 A Bank Accounts 235 – 2848 B Bank Accounts Lab Work 285 – 3029 Life Insurance Companies 303 – 343

10 General Insurance 344 – 375

Contents

CONTENTS Introduction Definition Need for Accounting Standards Importance of Accounting Standards Accounting Standards Board of India Compliance with the Accounting Standards Objectives of the Accounting Standards Scope of Accounting Standards Procedure for Issue of Accounting Standards Accounting Standards Issued in India Implementation of IFRS in India Summary Glossary Questions

OBJECTIVESThe objectives of this chapter are to: Appreciate the need for Accounting Standards Know the scope of Accounting Standards Learn the Accounting Standards issued by the Accounting Standards Board of India

INTRODUCTIONThe main objective of Accounting Theory is to give a coherent set of logical principles for the

evaluation and development of Accounting Practices. To achieve this purpose, some sound accountingprinciples are to be followed.

The main purpose of Accounting Standards is to serve as the working basis for the Institutions. Itis not proper to compare the Financial Statements of the different Companies as the Accounting

Accounting Standards1

Chapter

– 2 – Corporate Accounting

Concepts and Conventions permit a variety of alternative practices. Therefore, the AccountingStandards are required, which conform to the applicable laws, customs, and usage and businessenvironment.

DEFINITIONAccording to Kohler, Accounting Standards mean “A mode of conduct imposed on accountants

by custom, law or professional body”.Michael Bromwich defines “Accounting Standards are uniform rules for financial reporting

applicable to either all or to a certain class of entity promulgated by what is perceived of aspredominantly an element of the accounting community specially created for this purpose. Standardsetters can be seen as seeking to perceive a preferred accounting treatment from the available set ofmethods for treating one or more accounting problems, other policy statements by the profession willbe referred to as recommendations”.

NEED FOR ACCOUNTING STANDARDSFinancial Statements are prepared in monetary terms by an enterprise to summarize the end-result

of all the business activities during an accounting period. These business activities vary from oneenterprise to another. The divergence in the methods and principles adopted by the enterprises inpreparing their financial statements will pose some difficulties if the financial statements of variousreporting enterprises are to be compared. Therefore, standards are evolved, to make these methods andprinciples uniform and comparable, to the extent possible.

The Institute of Chartered Accountants of India (ICAI) recognizing the need to harmonize thediverse accounting policies and practices in use in India constituted Accounting Standards Board(ASB) on April 21, 1977. The main role of ASB is to formulate Accounting Standards from time totime.

Section 211(3A) of Companies Act, 1956 provides that every Profit and Loss Account andBalance Sheet of the company shall comply with the Accounting Standards. The Statutory Auditorsare required to make qualification in their report in case any item is treated differently from theprescribed Accounting Standard. However, while qualifying, they should consider the materiality ofthe relevant item. In addition to this, Section 227(3) (d) of Companies Act, 1956 requires an Auditor toreport whether in his opinion; the Profit and Loss Account and Balance Sheet are complied with theAccounting Standards referred to in Section 211(3C) of Companies Act, 1956.

The basic objective of Accounting Standards is to remove the variations in the treatment ofseveral accounting aspects and to bring about standardization in presentation. They intend toharmonize the diverse accounting policies followed in the preparation and presentation of the financialstatements by different reporting enterprises so as to facilitate intra-firm and inter-firm comparison.

IMPORTANCE OF ACCOUNTING STANDARDSThe importance of accounting standards is due to the following reasons. Accounting Standards help to develop uniformity in the preparation of the Financial

Statements. Accounting Standards facilitate the comparison of the Financial Statements of the various

Companies and manipulation can be reduced. Accounting Standards increases the credibility and the reliability of the Financial Statements.

Accounting Standards – 3 –

Uniformity in Accounting Practices and Policies may bring transparency in the Accountingdata.

Accounting Standards provide meaningful information to the various users of the FinancialStatements so that they can make better investment decisions.

ACCOUNTING STANDARDS BOARD OF INDIAThe Institute of Chartered Accountants of India constituted the Accounting Standards Board

(ASB) on 21st April, 1977. It provides support to its members and it recognized the need for harmonyof the diverse Accounting Policies and Practices followed in India.

Accounting Standards Board’s primary function is to formulate the Accounting Standards aftertaking into consideration the applicable laws, customs, usages and business environment. It also givesimportance to the International Accounting Standards issued by the International AccountingStandards Committee (IASC). It gives suggestions and publicizes the Accounting Standards andpersuades the concerned parties to adopt them in the preparation and presentation of the FinancialStatements. ASB has the responsibility of issuing clarifications on issues arising from the standardsand also review the Accounting Standards at periodical intervals.

COMPLIANCE WITH THE ACCOUNTING STANDARDSThe Companies Amendment Act, 1999 has made the compliance of Accounting Standards

mandatory. Accounting Standards guide as to how a particular type of transaction and other eventsshould be reflected in the Financial Statements and accordingly, compliance with AccountingStandards will normally be necessary for the Financial Statements to give a true and fair view.

Accounting Standards are mandatory and the mandatory status of an Accounting Standardimplies that while discharging their functions, it will be the duty of the Members of theInstitute to examine whether the Accounting Standards are complied with in the presentationof the Financial Statements which are covered by their audit. In the event of any deviationfrom the Accounting Standard, it will be their duty to make adequate disclosures in theirAudit Reports so that the users of the Financial Statements may be aware of such deviation.

Ensuring compliance with the Accounting Standards while preparing the FinancialStatements is the responsibility of the Management of the enterprise. Statutes governingcertain enterprises require the enterprises to prepare the Financial Statements in compliancewith the Accounting Standards, e.g., The Companies Act, 1956 (Section 211), The InsuranceRegulatory and Development Authority (Preparation of the Financial Statements andAuditor’s Report of the Insurance Companies Regulation, 2000).

Financial Statements cannot be stated as complying with the Accounting Standards unlessthey comply with all the requirements of each applicable standard.

Business Community is required to adopt the Accounting Standards in order to achieveuniformity in the preparation and presentation of the Financial Statements.

In the formulation of the Accounting Standards, the emphasis would be on laying down theAccounting Principles and not on detailed rules for the application and implementationthereof.

– 4 – Corporate Accounting

OBJECTIVES OF THE ACCOUNTING STANDARDSThe following are the objectives of the Accounting Standards To conceive of and suggest the areas in which Accounting Standards need to be developed. To formulate the Accounting Standards with a view to assisting the council of the ICAI in

evolving and establishing the Accounting Standards in India. To examine as to how far the relevant International Accounting Standards/International

Financial Reporting Standards can be adopted while formulating the Accounting Standardsand to adapt the same.

To review, at regular intervals, the Accounting Standards from the point of view of theacceptance or changed conditions and if necessary, revise the same.

To provide from time to time, interpretations and guidance on Accounting Standards. To carry out such other functions relating to the Accounting Standards.

SCOPE OF ACCOUNTING STANDARDSThe scope of the Accounting Standards is detailed below. Efforts will be made to issue Accounting Standards which are in conformity with the

applicable laws, customs, usages and business environment in India. However, if a particularAccounting Standard is found to be not in conformity with the law, the provisions of thesaid law will prevail and the Financial Statements should be prepared in conformity withsuch law.

Accounting Standards by their nature cannot and do not override the local regulations whichgovern the preparation and presentation of the Financial Statements in the country.However, the ICAI will determine the extent of disclosures to be made in the FinancialStatements and the Auditor’s Report thereon. Such disclosure may be by way of appropriatenotes to explain the treatment of particular items. Such explanatory notes will be only in thenature of clarification and therefore, need not be treated as adverse comments on the relatedFinancial Statements.

Accounting Standards are intended to apply only to the items which are material. Anylimitations with regard to the applicability of a specific Accounting Standard will be madeclear by the ICAI from time to time. The date from which it will apply, will also be specifiedby the ICAI. However, no standard will have retrospective application, unless otherwisestated.

The Institute will use its best endeavors to persuade the Government, appropriateAuthorities, Industries and Business Community to adopt the standards in order to achieveuniformity in the preparation and presentation of the Financial Statements.

In the formulation of the Accounting Standards, the emphasis would be on laying downAccounting Principles and not on detailed rules for application and implementation thereof.

The ASB may consider any issue requiring interpretation on any Accounting Standard.

PROCEDURE FOR ISSUE OF ACCOUNTING STANDARDSThe following procedure is adopted for issuing Accounting Standards by the Accounting

Standards Board:

Accounting Standards – 5 –

The Accounting Standards Board (ASB) identifies the broad areas in which AccountingStandards need to be formulated and the priority thereof.

In the preparation of the Accounting Standards, ASBs holds a dialogue with the StudyGroups, Representatives of the Government, Public Sector Undertakings and OtherOrganizations.

ASB prepares the draft of the proposed standards which includes, Objective of the Standard,Scope of the Standard, Definition of the terms used in the Standards, Recognition andMeasurement Principles, Presentation and Disclosure Requirements.

The ASB will circulate the draft of the Accounting Standards to the Council Members of theICAI and the following specified Bodies for their comments: Department of Company Affairs (DCA) Comptroller and Auditor General of India (C &AGI) Central Board of Direct Taxes (CBDT) The Institute of Cost and Works Accountants of India (ICWAI) The Institute of Company Secretaries of India (ICSI) Securities and Exchange Board of India (SEBI) Standing Conference of Public Enterprises (SCOPE) Indian Bank’s Association (IBA) Any other Body considered relevant by the ASB keeping in view the nature of the

Accounting Standard After considering the views of the representatives of the specified Bodies on the draft of the

proposed Accounting Standard, the ASB will finalize the Exposure Draft of the proposedAccounting Standard.

The final draft of the proposed standard will be issued to the Council of the ICAI and ifnecessary, ICAI modifies the same in consultation with the ASB.

The Accounting Standards will be mandatory from the respective dates mentioned in theAccounting Standards. It is the duty of the Members of the Institute to examine whether theAccounting Standards are complied within the presentation of the Financial Statements covered bytheir audit.

ACCOUNTING STANDARDS ISSUED IN INDIAList of Accounting Standards (mandatory) as on July 1, 2012

No. of AccountingStandards (ASs)

Title of the Accounting Standard RevisedDatesw.e.f.

AS – 1 Disclosure of Accounting Policies 1/4/1993

AS – 2 Valuation of Inventories 1/4/1999

AS – 3 Cash Flow Statement 1/4/2001

AS – 4 Contingencies and Events Occurring after the Balance Sheet Date 1/4/1998

AS – 5 Net Profit or Loss for the Period, Prior Period Items and Changes inAccounting Policies

1/4/1997

– 6 – Corporate Accounting

AS – 6 Depreciation Accounting 1/4/1995

AS – 7 Accounting for Construction Contracts 1/4/2003

AS – 9 Revenue Recognition 1/4/1993

AS – 10 Accounting for Fixed Assets 1/4/1993

AS – 11 The Effects of Changes in Foreign Exchange Rates 1/4/2003

AS – 12 Accounting for Govt. Grants 1/4/1994

AS – 13 Accounting for Investments 1/4/1995

AS – 14 Accounting for Amalgamations 1/4/1995

AS – 15 Employee Benefits 1/4/1995

AS – 16 Borrowing Costs 1/4/2000

AS – 17 Segment Reporting 1/4/2001

AS – 18 Related Party Disclosures 1/4/2001

AS – 19 Leases 1/4/2001

AS – 20 Earnings per Share 1/4/2001

AS – 21 Consolidated Financial Statement 1/4/2001

AS – 22 Accounting for Taxes on Income 1/4/2003

AS - 23 Accounting for Investment in Associates in Consolidated FinancialStatements

1/4/2002

AS – 24 Discontinuing Operations 1/4/2005

AS – 25 Interim Financial Reporting 1/4/2005

AS – 26 Intangible Assets 1/4/2003

AS – 27 Financial Reporting of Interests in Joint Venture 1/4/2002

AS – 28 Impairment of Assets 1/4/2008

AS – 29 Provisions, Contingent Liabilities and Contingent Assets 1/4/2004

Note: AS - 8 is no longer in force as it is merged with AS - 26List of Accounting Standards (not mandatory) as on 1st July, 2012

No. of AccountingStandards (ASs)

Title of the Accounting Standard

AS – 30 Financial Instruments: Recognition and Measurement

AS – 31 Financial Instruments: Presentation

AS – 32 Financial Instruments: Disclosures

Source: The Institute of Chartered Accountants of India and other websites

AS–1 Disclosure of Accounting PoliciesThis Standard deals with the Accounting Policies and specific Accounting Principles and the

Methods of applying those principles to be adopted by the Enterprises in the preparation andpresentation of the Financial Statements.

Accounting Standards – 7 –

AS–2 Valuation of InventoriesThis Standard deals with the determination of the value of the Closing Stock/Inventory at which

the inventory is to be shown in the Balance Sheet till it is not sold and recognized as revenue.

AS–3 Cash Flow StatementsThis Accounting Standard is not mandatory for Small and Medium Sized Companies. It is

additional information to the users of the Financial Statements. This Standard deals with the provisionof the information about the historical changes in cash and cash equivalents of an Enterprise by meansof a Cash Flow Statement which classifies the cash flows during the period into Operating, Investingand Financing Activities.

AS–4 Contingencies and Events Occurring after the Balance Sheet DateThe main purpose of this Standard is to prescribe the method of Accounting Contingencies and

the Events, which take place after the Balance Sheet date but before the approval of the Balance Sheetby the Board of Directors.

AS–5 Net Profit or Loss for the Period, Prior Period Items and Changes inAccounting Policies

The Objective of this Accounting Standard is to prescribe the disclosure of certain items in theProfit and Loss Account so that all the firms prepare and present such a statement on a uniform basis.This Accounting Standard also deals with the changes in the Accounting Policy, Accounting Estimatesand Extraordinary Items.

AS–6 Depreciation AccountingIt is a measure of depreciation of an asset arising from the use and passage of time. Different

Enterprises adopt different Accounting Policies for Depreciation. Disclosure of Accounting Policiesfollowed for Depreciation is necessary for appreciating the view presented in the Financial Statementsof the Enterprise.

AS–7 Accounting for Construction ContractsThis Accounting Standard deals with the Accounting for Construction Contracts in the Financial

Statements of the Contractors. This Standard does not apply to the Contractees and would not beapplicable for the construction projects undertaken by the Enterprise as a commercial venture which isin the nature of production activities.

AS–8 Revenue RecognitionThe objective of this standard is to explain as to when the revenue should be recognized in the

Profit and Loss Account and also state the circumstances in which revenue recognition is postponed.This Standard deals with the revenue arising in the course of an ordinary activities of an enterprisesuch as the sale of goods, rendering of services and use of the Enterprises resources for earninginterest, dividend and royalties etc.

– 8 – Corporate Accounting

AS–9 Accounting for Fixed AssetsThis Standard deals with Accounting for Fixed Assets such as Land, Buildings, Plant and

Machinery, Vehicles, Furniture and Fittings, Goodwill, etc. The Assets held with the intention ofbeing used for the purpose of producing or providing services and not held for sale in the normalcourse of business will be considered as the Fixed Assets and are expected to be used for more thanone Accounting Period.

AS–10 Effects of Changes in the Foreign Exchange RatesThis Standard deals with the accounting for the transactions in Foreign Currencies, in translating

in the Financial Statements of Foreign Operations, Integral as well as non-integral and also accountingfor Forward Exchange. Amount of Exchange Difference included in the Net Profit or Loss; AmountAccumulated in Foreign Exchange Translation Reserve, Reconciliation of Opening and ClosingBalance of Foreign Exchange Translation Reserve should be disclosed to know the effect of changesin the Foreign Exchange Rate.

AS–11 Accounting for Government GrantsThis Accounting Standard deals with the Government Grants such as subsidies, cash incentives,

duty drawbacks, etc. It also deals with the Government assistance (such as Tax Holliday in backwardareas) other than in the form of Government Grants. Government participation in the ownership of theEnterprise is not covered in this Standard.

AS–12 Accounting for InvestmentsIt deals with the assets held for earning income by way of dividend, interest and rentals, for

capital appreciation or for other benefits.

AS–13 Accounting for AmalgamationsThis Accounting Standard considers only those amalgamations which may be either an

amalgamation in the nature of merger or an amalgamation in the nature of purchase. This Standard isnot applicable to the cases of acquisition of shares when one company acquires/purchases the shares ofanother company and the acquired company is not dissolved and its separate entity continues to exist.

AS–14 Employee BenefitsIt mainly focuses on the accounting for retirement benefits and is mandatory in nature. The scope

of this Accounting Standard has been enlarged by Revised Committee of ICAI, in the year 2006 andincludes accounting for short-term employee benefits and termination benefits.

AS–15 Borrowing CostsTo build and install the Fixed Assets and other Assets, Enterprises borrow funds and incur the

interest expenses to acquire and build these Assets. This Accounting Standard mainly deals with theaccounting treatment of borrowing cost (interest + other cost) and whether the cost of borrowingshould be included in the cost of the assets or not.

Accounting Standards – 9 –

AS–16 Segment ReportingThe main objective of this Standard is to establish principles for reporting financial information

about the different types of products and services an enterprise produces or renders and the differentgeographical areas in which it operates.

AS–17 Related Party DisclosersThis Accounting Standard deals with the requirements for the disclosure of the related party

relationships and transactions between a reporting enterprise and its related parties. Related Partyrelationship affects the volume and decisions of the business of one enterprise for the benefit of theother enterprise.

AS–18 LeaseAs per this Standard, if a sale and leaseback transaction results in a Financial Lease, any excess

or deficiency of sales proceeds over the carrying amount should not be immediately recognized asincome or loss in the Financial Statements of a seller-lessee. Instead, it should be deferred andamortized over the lease term in proportion to the depreciation of the lease assets. If a sale andleaseback transaction results in an Operating Lease, any profit or loss should be recognizedimmediately.

AS–19 Earning per ShareThis Accounting Standard is applicable to the Enterprises whose equity shares or potential equity

shares are listed in a recognized Stock Exchange in India. It is a Financial Ratio that gives theinformation regarding earnings available to each equity share. Accounting Standard givescomputational methodology for the determination and presentation of Earning per Share.

AS–20 Consolidated Financial StatementsThe main objective of this statement is to present the Financial Statements of a parent and its

Subsidiary/ies as a single economic entity. In other words, the Holding Company and itsSubsidiary/ies are treated as one entity for the preparation of the Consolidated Financial Statements.

AS–21 Accounting for Taxes on IncomeThis Accounting Standard prescribes the accounting treatment for taxes on income. Traditionally,

amount of tax payable is determined on the profit/loss computed as per the Income Tax Laws. Tax onincome is determined on the principle of accrual concept.

AS–22 Accounting for Investments in Associates in Consolidated FinancialStatements

The objective of this Standard is to formulate the principles and procedures for recognizing theinvestment in Associates in the Consolidated Financial Statements of the Investing Company, so thatthe effect of investment in Associates on the Financial Position of the group is indicated.

– 10 – Corporate Accounting

AS–23 Discontinuing OperationsThis Standard establishes the principles for reporting information about the discontinuing

operations. The main aim of the disclosure of the information is about the operations which theenterprise plans to discontinue rather than disclosing the operations which are already discontinued.

AS–24 Interim Financial ReportingThe main purpose of this Standard is to prescribe the minimum content of an Interim Financial

Report and lay down the principles for recognition and measurement of the Assets, Liabilities,Revenue and Expenses for an interim period.

AS–25 Intangible AssetsThis Standard is mandatory in nature and comes into effect in respect of the expenditure incurred

on Intangible Assets during the accounting periods commencing on or after 1/4/2003. It definesIntangible Asset as an identifiable Non-monetary Asset without physical substance, held for use in theproduction or supply of goods and services for rentals to others, for administrative purpose.

AS–26 Financial Reporting of interest in Joint VenturesThe objective of this Standard is to set out the principles and procedures for accounting for

interest in Joint Ventures and reporting of Joint Ventures Assets, Liabilities, Income and Expenses inthe Financial Statements of Venturers and Investors.

AS–27 Impairment of AssetsAccording to this Standard, an Asset is said to be impaired when carrying amount of the Assets is

more than its recoverable amount. As per this Standard, the carrying amount at which an Asset isrecognized in the Balance Sheet should be after deducting any accumulated depreciation andaccumulated impairment losses thereon.

AS–28 Provisions, Contingent Liabilities and Contingent AssetsThe objective of this Standard is to prescribe the method of Accounting for Provisions,

Contingent Liabilities, Contingent Assets, and Provision for Restructuring Cost.

Implementation of IFRS in IndiaIFRS is a globalization theme and many countries in the world like Hong Kong, Australia,

Pakistan, Russia, South Africa, Singapore, Turkey, and European Union are following. Approximately,150 Countries across the world are following IFRS. Adoption of IFRS means the use of theInternational Financial Reporting Standards as the primary Generally Accepted Accounting Principles(GAAP) by the domestic listed and unlisted companies in their consolidated Financial Statements forthe external Financial Reporting. This means that, the basis of the presentation, Note and Auditor’sReport indicate that the Financial Statements are prepared on the basis of IFRSs. It will provide achance for India to integrate with the common Accounting International Standards which will save thecost which has to be incurred by MNCs and internationally listed companies for maintaining dualaccounting and reporting system.

IFRS would enhance the comparability between the Financial Statements of various companiesacross the globe. The industry would be able to raise capital from the foreign markets at lower cost if it

Accounting Standards – 11 –

can create confidence in the minds of the foreign investors that its Financial Statements comply withthe Globally Accepted Accounting Standards. It would reduce different accounting requirementsprevailing in the various countries thereby enabling the enterprises to reduce the cost of compliances.It serves the international clients by providing professional opportunities. It would increase theirmobility to work in different parts of the world either in industry or practice.

The Government has created general awareness about IFRS and the ground is prepared to bringnecessary changes in the accounting practices. The Ministry of Corporate Affairs is constraineddelaying the adoption of IFRS. It is made optional to the companies to either report their FinancialStatements based on the existing Indian AS or adopt IFRS. A decision may be taken to make theapplication of IFRS mandatory from the year 2016. Though the time line of convergence of IndianGAAP with IFRS was from April 2011, many large listed companies have already adopted newstandards and those who are in transition will be actively incorporating the change in the coming years.

SUMMARYAccounting Standards serve as the working basis for the Institutions. It is not proper to compare

the Financial Statements of the different Companies as the Accounting Concepts and Conventionspermit a variety of alternative practices. Therefore, the Accounting Standards are required, whichconform to the applicable laws, customs, and usage and business environment.

Accounting Standards help to develop uniformity in the preparation of the Financial Statements.The Accounting Standards facilitate the comparison of the Financial Statements of the variousCompanies and manipulation can be reduced. It increases the credibility and the reliability of theFinancial Statements. Uniformity in Accounting Practices and Policies may bring transparency in theAccounting data. It provides meaningful information to the various users of the Financial Statementsso that they can make better investment decisions.

The Institute of Chartered Accountants of India constituted the Accounting Standards Board(ASB) on 21st April, 1977. It provides support to its Members and it recognized the need for harmonyof the diverse Accounting Policies and Practices followed in India.

Accounting Standards Board’s primary function is to formulate the Accounting Standards aftertaking into consideration the applicable laws, customs, usages and business environment. It also givesimportance to the International Accounting Standards issued by International Accounting StandardsCommittee (IASC). It gives suggestions and publicizes the Accounting Standards and persuades theconcerned parties to adopt them in the preparation and presentation of the Financial Statements. ASBhas the responsibility of issuing clarifications on issues arising from the standards and also review theAccounting Standards at periodical intervals.

The Companies Amendment Act, 1999 has made the compliance of Accounting Standardsmandatory. Accounting Standards guide as to how a particular type of transaction and other eventsshould be reflected in the Financial Statements and accordingly, compliance with the AccountingStandards will normally be necessary for the Financial Statements to give a true and fair view. ICAIhas so far issued 29 Accounting Standards which are mandatory in India and the adoption of threeother Accounting Standards is voluntary.

IFRS is a globalization theme and many countries in the world like Hong Kong, Australia,Pakistan, Russia, South Africa, Singapore, Turkey, and European Union are following. Approximately,150 Countries across the world are following IFRS. Adoption of IFRS means the use of theInternational Financial Reporting Standards as the primary Generally Accepted Accounting Principles

– 12 – Corporate Accounting

(GAAP) by the domestic listed and unlisted Companies in their consolidated Financial Statements forthe external Financial Reporting.

The Government has created general awareness about IFRS and the ground is prepared to bringnecessary changes in the Accounting Practices. The Ministry of Corporate Affairs is constraineddelaying the adoption of IFRS. It is made optional to the Companies to either report their FinancialStatements based on the existing Indian AS or adopt IFRS. A decision may be taken to make theapplication of IFRS mandatory from the year 2016. Though the time line of convergence of IndianGAAP with IFRS was from April 2011, many large listed companies have already adopted newstandards and those who are in transition will be actively incorporating the change in the coming years.

GLOSSARY Accounting Standards: Mean a mode of conduct imposed on Accountants by custom, law

or Professional Body. Accounting Standard Board: Is constituted by the Institute of Chartered Accountants of

India to frame the Accounting Standards to be followed by all the Companies uniformly inIndia.

IFRS: Adoption of IFRS means the use of the International Financial Reporting Standardsas the primary Generally Accepted Accounting Principles (GAAP) by the domestic listedand unlisted companies in their consolidated Financial Statements for the external FinancialReporting.

QUESTIONS1. Define Accounting Standards.2. What is the need for Accounting Standards?3. Explain the importance of Accounting Standards.4. What is the role of Accounting Standards Board in India?5. Write a note on compliance with the Accounting Standards6. What are the objectives of Accounting Standards?7. Explain the Scope of Accounting Standards.8. Briefly describe the procedure for issuing Accounting Standards.9. Give an account of Accounting Standards.

10. Write about IFRS.

.........

Accounting Standards – 13 –