corporate debt resolution and the role of foreign …

TRANSCRIPT

The Developing Economies, XL-4 (December 2002): 564–86

CORPORATE DEBT RESOLUTION AND THE ROLE OFFOREIGN CAPITAL IN THE POST-CRISIS RESTRUC-

TURING OF THE REPUBLIC OF KOREA

CHAN-HYUN SOHN

The outbreak of the financial crisis in the Republic of Korea in 1997 exposed the struc-tural weaknesses in the country’s economy. Heated debates have failed to generate de-finitive answers on just what caused the financial crisis. Considering the importance ofrestructuring the corporate sector, this paper analyzed how the resolution of corporatedebts was accomplished and examined the role of foreign capital in Korea’s post-crisiscorporate restructuring. Special attention was given to the measures devised to recovernonperforming loans for the liquidation of corporate debts, to the foreign capital inflowsthrough cross-border M&As or privatization processes, and to the changes in controlthrough corporate governance reforms. This paper concluded that the resolution of cor-porate debts has been satisfactory and successful and that foreign capital contributedsignificantly to effective corporate restructuring and debt resolution in the post-crisisrestructuring of Korea.

I. INTRODUCTION

THE outbreak of the financial crisis in the Republic of Korea in 1997 revealedthe structural weaknesses in the country’s economy. Naturally, policymakersand experts in diverse fields from economics and finance to social policy

have sought remedies, not only to address the crisis but also to prevent another onefrom occurring and to provide a sound base on which to build a healthier economy.

Heated debates on just what caused the financial crisis have not yet led to univer-sally agreed answers. However this paper suggests, based on the Korean experi-ence, that the corporate sector played a major role.

Realizing the importance of the need for restructuring the corporate sector, thispaper aims to analyze how the resolution of corporate debts was accomplished andto determine the role of foreign capital in Korea’s post-crisis corporate restructur-ing. Emphasis is placed on the measures devised to recover nonperforming loansfor the liquidation of corporate debts, including foreign capital inflows throughcross-border M&As or privatization processes, as well as the changes in controlassociated with corporate governance reform.

The paper consists of six parts. Following this section, Section II traces the evo-

565CORPORATE DEBT RESOLUTION

lution of the financial crisis in Korea and analyzes the restructuring initiative. Sec-tion III considers various corporate debt resolution intermediaries focusing on theKorea Asset Management Corporation (KAMCO), a specialized debt resolutionagency. Section IV studies the role of foreign capital in corporate restructuring,especially through cross-border M&As and in privatization. Then, Section V exam-ines the changes in the corporate sector, in particular regarding the corporate gover-nance and control system, and discusses how they have led to better corporate per-formance. This paper is concluded in Section VI.

II. EVOLUTION OF THE FINANCIAL CRISIS ANDRESTRUCTURING INITIATIVE

A. Underlying Weaknesses of the Corporate Sector

On the surface, the financial crisis that struck many Asian regions seemed tohave stemmed from liquidity problems, that is, low foreign reserves and excessiveshort-term foreign debts. Indeed, Korea’s short-term foreign debts amounted to morethan six times the value of its foreign reserves. However, at the core of Korea’scrisis stood the inefficiency of the corporate sector, a problem which expandedduring the country’s high growth period.

The inefficiency finally surfaced in the form of a series of large-scale bankrupt-cies. The number of bankruptcies, including those of the chaebols, the large con-glomerates, increased by about 50 per cent near the onset of the crisis from 11,589in 1996 to 17,168 in 1997. This succession of bankruptcies increased the level ofuncertainty in the Korean economy and shook investors’ confidence. Banking andfinancial crises were immediate.

Three characteristics of Korean corporations are to blame. First, excessive andinefficient investment and highly leveraged and diversified businesses were financedby debts. Figure 1 shows that in the 1990s, the profitability of Korean manufactur-ing firms was substantially below the opportunity cost of capital, thereby leavingthem with a cash flow shortage and structurally vulnerable to external shocks.

As global economic conditions changed and competition got fiercer in both do-mestic and world markets in the late 1980s, debt-financed growth became everriskier.1 What was most critical, though, was the short-term liquidity problem thatplagued the corporate sector in general.

Second, the collusive relationship between the government and business groupsled to inefficient allocation of capital in the financial system. Through its strongcontrol of the financial sector, the government implicitly directed loans to selectedcompanies, in particular chaebols, without prudential regulations. This often re-

1 The warning signs of bankruptcy and high systemic risk appeared in mid-1996. They includedover-capacity in investment sector and cash flow shocks.

THE DEVELOPING ECONOMIES566

sulted in the situation where some companies could not repay debts. The inabilityof the corporate sector to pay the debt service is equivalent to the inability of thefinancial institutions to dispose of the nonperforming loans (NPLs). Thus the de-mise of the corporate and financial sectors were intertwined: the increasing numberof bankruptcies in the corporate sector burdened the financial sector with NPLs.The size of NPLs sharply increased after the financial crisis. Table I shows thistrend.

Third, the traditional and inefficient corporate governance persisted. The own-ers, who were often the controlling shareholders and usually nonprofessional man-agers, were deeply involved in corporate governance. The headquarters of chaebolscontrolled affiliates with a relatively small share of their equity through a central-ized hierarchy system known as the “control pyramid system.”2 In fact, the averagenumber of affiliates of the top thirty chaebols increased from sixteen in 1983 totwenty-seven in 1997, while the mean percentage of shareholdings decreased from15.8 per cent to 8.5 per cent during the same period. This type of corporate gover-nance contributed to poor performance and low firm value, reflecting the ineffi-ciency in the corporate sector.

The above factors are the main causes of the corporate sector inefficiency. There-fore it was imperative that the main focus for overcoming the financial crisis be

2 The control pyramid system refers to the system in which a certain shareholder controls the man-agement of the main businesses and becomes the dominant shareholder of other business lines bycontrolling the assets of other businesses with a small amount of assets (KERI 2000).

−4

−2

0

2

4

6

8

10

12

14

16

1990 1991 1992 1993 1994 1995 1996 1997

(%)

Net Profit/Net Worth Financial Expenses to Total Borrowing

Fig. 1. Profitability and Financial Expenses of Korean Manufacturing Firms

Source: Cited from Lim (2001); original sources are Bank of Korea, Financial Statement Analysis, various issues.

567CORPORATE DEBT RESOLUTION

placed on the corporate sector, especially in the case of corporate debt managementand restructuring.3 The key element for the viability and soundness of the sector iscash flow. Various measures for implementing reform, as will be shown in latersections, did succeed in lowering the debt-equity ratio and improving the interestcoverage ratio of the corporate sector. But measures to improve the cash flows ofthe cash-strapped corporate sector, in particular by attracting foreign capital in-flows, were urgently needed.

B. General Framework of Corporate Sector Reforms

The corporate sector reforms can largely be divided into two pillar measures—corporate debt restructuring and corporate governance reforms.

Corporate debt restructuring involved rectifying the first two problems specifiedin the previous section, namely, corporate financial restructuring and debt resolu-tion, while corporate governance reforms dealt with the third problem. Here thefocus will be placed on approaches to corporate restructuring based on the fivemajor principles as follows: (1) significantly improving the capital structure, (2)identifying core businesses and strengthening cooperative relationships with smalland medium-sized companies, (3) improving the transparency of corporate man-agement, (4) dismantling cross-debt guarantees, and (5) enhancing the accountabil-ity of both controlling shareholders and their management.4

At the onset of the financial crisis, there were few institutional systems and mar-ket mechanisms that could deal with large-scale insolvency. To provide a system-atic mechanism, ways to improve the existing court-based procedures as well as tointroduce an out-of-court settlement procedure were sought. Nonviable companieswere liquidated or rehabilitated through these two main mechanisms during thisperiod.

3 More detailed arguments and comprehensive review of financial and corporate restructuring arefound in Lieberman and Mako (1998), Zang and Wang (1998), Aiyer (1999), Ahn (2001), Mako(2001b), and Sohn (2002).

4 Considering the changes in the conditions and new problems, the following three tasks were fur-ther added on August 15, 1999: (1) improving the managerial governance of the nonbank financialinstitutions, (2) eliminating cross-financing and illegal intra-group transactions, and (3) preventingirregular inheritances and donations.

TABLE I

TREND OF NONPERFORMING LOANS

(Trillion won)

1997 1998 1999 2000 2001

Total NPLs 97.5 146.7 128.9 157.9 133.1

Source: PFOC and MOFE (2002) and Lim (2002).Note: NPLs are based on the forward-looking criteria (FLC).

THE DEVELOPING ECONOMIES568

The court-based restructuring system is composed of three elements: bankruptcy,composition, and reorganization. Bankruptcy is a procedure in which a debtor’sassets are liquidated by a court-appointed liquidator. Composition is a settlementprocedure between the debtor and creditors, in which a debtor handles its own es-tate. It is available to enterprises that owe less than 250 billion won, for it offersvery few guarantees to the creditors. In the reorganization procedure, the court di-rects the creditors to handle the debtor, and the latter’s estate is administered by anexternal administrator under the supervision of the creditor. Creditors and debtorscan start any of the procedures, if there is evidence of cash flow insolvency.

Although there actually was a court-based insolvency system before the finan-cial crisis, it barely functioned and was very inefficient.5 Reforming the court-basedrehabilitation system involved revising the bankruptcy law in February 1998: thecourt could accept and hear cases even when the file was not complete, consolida-tion of related cases under the same court was made possible, deadlines for theapproval and submission of reorganization plans were shortened to between twelveand eighteen months, and it became possible to switch from the composition orreorganization options to bankruptcy proceedings. In addition, harsher punishmentswere meted out to the former managers who were responsible for the company’sinsolvency. These penalties, intended to make the culpable managers take full re-sponsibility for their mismanagement, included compulsive retirement of sharesand deprivation of managerial rights in the reorganization procedure.

Out-of-court workout procedures involved dividing the companies into threegroups according to their restructuring capacity, and applying different restructur-ing approaches. The first group included the top five chaebols—Hyundai, Samsung,LG, Daewoo, and SK—which were considered to have the capacity to absorb theresulting losses. They were allowed to pursue “self-directed restructuring.” An ad-ditional program called Big Deals was incorporated by the December 1998 Agree-ment6 to reorganize diversified business lines,7 and reduce the overcapacity and thehigh debt-equity ratios of the chaebols. In fact it was a restructuring option avail-able only to these top chaebols.

Next was the “6 to 64” chaebols group, which consisted of the 64 largest con-

5 Out of more than 17,000 insolvency cases reported by the Bank of Korea in 1997, only 492 caseswere filed before the court. Only forty-one judges, some of which were not specialists in commer-cial law, were assigned to deal with bankruptcy cases, and the proceedings lasted several years(KERI 2001).

6 The agreement also emphasized the reduction of debt-equity ratios. Other aspects included the exitof nonviable firms, independent management of chaebol affiliates, the elimination of intra-groupdebt guarantees, and the transparency of corporate management.

7 The Korean conglomerates, chaebols, under the government’s protection, diversified their affiliatesand business areas. The average number of affiliates for the thirty largest conglomerates continuedto increase from 19.7 in 1992 to 27.3 in 1997; meanwhile, the average number of business areasalso increased from sixteen to twenty during the same period (OECD 1998).

569CORPORATE DEBT RESOLUTION

glomerates excluding the top five. They were considered to be unable to restructuresuccessfully on their own, and voluntary out-of-court workout programs were car-ried out. Daewoo, one of the top five chaebols, failed to “self-restructure” and re-ceived workout programs. A voluntary workout consists of an out-of-court settle-ment process between the creditors and debtors, based on the principle of “debtburden sharing” with financial institutions.8

The third group included the small- and medium-sized companies. Since theirfinancial structure was too weak to bear the cost of restructuring, support camefrom their creditor financial institutions and the central bank during the restructur-ing process.9

As the pace of reform and growth slowed, and the financial sector was beingthreatened by high credit risks in mid-2000, the second round of reforms waslaunched to address the problems and restore confidence in the Korean economy.Corporate restructuring from 2001 was executed on the basis of a series of systemsestablished at the former stage. Government intervention was reduced to establish amore market-based restructuring system. The Corporate Restructuring PromotionLaw (effective until 2005) and its Enforcement Ordinance were promulgated toefficiently dispose of and reduce the NPLs of financial institutions.

III. CORPORATE DEBT RESOLUTION

Corporate debts were resolved through a special resolution agency. The KoreaAsset Management Corporation (KAMCO) was the first of its kind in Korea, andother institutions including the Corporate Restructuring Fund, Corporate Restruc-turing Company, Corporate Restructuring Vehicle, and Corporate RestructuringReal Estate Investment Trust were established to assist in the resolution of corporatedebts.

8 At the end of 2000, 104 firms including Daewoo Group affiliates were nominated for the workoutprocess. Of the 104 companies nominated, 36 firms have graduated and 34 remained in the pro-gram. Among the remaining 34 firms, 8 dropped out, 11 were ejected, and 15 merged with othercompanies. Ten of the 34 remaining companies were affiliates of the Daewoo Group, while 15were affiliates of the medium chaebols and 9 were small and medium-sized firms.

9 Small and medium-sized firms were divided into three groups: priority support group, conditionalsupport group, and others. For the firms in the first two categories, accounting for almost 95 percent of all small and medium-sized firms, banks were ordered to roll over loans maturing by De-cember 1998. Second, various budgetary support programs were introduced. Loan guarantees of33 trillion won to small firms and additional budgetary support of 2.2 trillion won were granted.The sum of 1.6 trillion won was raised through the “Corporate Restructuring Fund” to assist smallcompanies. The central bank relaxed its rules on credit ceiling to encourage banks to support smallfirms. Third, tax incentives were given: income tax or corporate tax was reduced by half for newlyestablished small and medium-sized firms during their first five years of start-up and tax benefitsassociated with facility investments were increased.

THE DEVELOPING ECONOMIES570

A. Korea Asset Management Corporation

KAMCO, originally a subsidiary of the Korea Development Bank, was speciallyreorganized into a resolution agency when the financial crisis broke out.10

The main role of KAMCO, as the only bad bank,11 was to help corporate restruc-turing by clearing the nonperforming loans (NPLs) of financial institutions andnormalizing their functions. It bought nonperforming assets from banks and otherfinancial institutions with the government’s debt-guarantees and public funds.12 NPLswere resold through three channels: (1) sale in the form of loans, (2) sale in theform of real estate, and (3) sale after management of NPLs. More specifically, salein the form of loans was achieved by asset-backed securities (ABS), outright sale,and equity partnerships; sale in the form of real estate was carried out by auctionand KAMCO public sales; and sale after management of NPLs by sale of real as-sets such as factories.

To issue ABS, KAMCO established a paper company called Special PurposeVehicle (SPV) and transferred NPLs, which the paper company subsequently clearedby issuing ABS with the transferred loans as collateral. ABS worth 4.1 trillion wonwere issued by June 2002, while NPLs worth 27.7 trillion won were disposed ofduring the same period. KAMCO introduced equity partnerships with the privateand foreign sectors expecting higher recoveries by enhancing the stability and spe-cialization rather than conventional sales methods.13 Between 1999 and 2001, sixequity partnerships were established, with a total asset book value of 3.5 trillionwon. The first three partnerships aimed at the co-management of NPLs, while thesecond three aimed at more comprehensive asset management.

As shown in Table II, KAMCO purchases of NPLs have been constantly increas-ing. The total purchase of NPLs at the end of 2001 accounted for 76.0 per cent oftotal NPLs worth 133.1 trillion won. The share of the remaining NPLs to the totalhas significantly decreased, suggesting the active role of KAMCO in purchasingand clearing the NPLs.

Although the total amount of NPLs increased sharply from 1999 to 2000 due tothe new addition of Daewoo’s NPLs and the introduction of a new asset classifica-

10 KAMCO was set up in 1997 as a bad bank under the Act on Efficient Management of NPLs ofFinancial Institutions and Establishment of KAMCO. The institution was renamed as KAMCO in1999.

11 A bad bank is the bank that specializes in the resolution of bad loans.12 The Non-Performing Asset Management Fund, a form of public funds, collected a total of 20.6

trillion won and had 12.1 trillion won as available capital in 1998 (KERI 2001).13 The advantage of the equity partnerships is that they can maximize the returns by introducing an

incentive system for general partners (the investors) while minimizing the holding period of theassets. Another advantage is that KAMCO does not have to bear the full burden of collectionexpenses. On the other hand, there are some weaknesses in equity partnerships. For example,KAMCO has to bear the risk of trusting foreign investors who may make poor business decisions(KAMCO 2000).

571CORPORATE DEBT RESOLUTION

tion standard, namely, forward-looking criteria,14 their share as a proportion of totalloans decreased from 11.3 per cent to 10.2 per cent during the same period. Moreremarkable is the fall of the remaining NPLs to total loans, from 17.7 per cent in1998 to 4.9 per cent in 2001. Another clear indicator of KAMCO’s significant rolein clearing NPLs is evidenced by the decreasing share of remaining NPLs, whichfell from 88.6 per cent in 1997 to 24.0 per cent of total NPLs in 2001. By 2001,NPL resolution was almost completed.

As shown in Table III, as of June 2002, total NPLs with a face value of 105.4trillion won had been purchased at the price of 39.4 trillion won. Public funds wereused to purchase the NPLs. Of these, NPLs worth 24.4 trillion won were cleared,with a recovery of 27.7 trillion won, showing a very high recovery ratio of 113 percent. In addition, NPLs worth 59.8 trillion won, which accounted for 56.7 per centof the total NPLs purchased as of June 2002, were disposed of. So far, 27.7 trillionwon, about 70.3 per cent of the 39.4 trillion won that had been invested, have beenrecovered. Such a high recovery ratio can be attributed to appropriate uses of vari-ous NPL disposal methods with different characteristics. For a large-scale disposalof NPLs through international bids and the issuance of ABS in 1999, diverse meth-ods such as sale to asset management companies and corporate restructuring com-panies were introduced and the outcome has significantly improved since 2000.

TABLE II

TREND OF NONPERFORMING LOANS AND KAMCO PURCHASES

(Trillion won)

1997 1998 1999 2000 2001

Total NPLs (A) 97.5 146.7 128.9 157.9 133.1

KAMCO purchases (B) 11.1 44.0 62.2 95.2 101.2Actual value 7.1 19.4 23.9 36.8 38.7

Remaining NPLs (A − B) 86.4 102.7 66.7 62.7 32.0Remaining NPLs/total credit (%) 13.3 17.7 11.3 10.2 4.9

Share of the remaining NPLs tototal NPLs (A − B)/(A) 88.6 70.0 51.7 39.7 24.0

Sources: PFOC and MOFE (2001, 2002), KAMCO (2002), and Lim (2002).Note: All figures were taken at the end of year.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

14 Prior to the crisis, only loans in arrears of six months or more had been classified as NPLs. Inestimating the “true” magnitude of NPLs at the end of March 1998, however, Korea followedinternationally acceptable standards and included loans in arrears of three months or more. InDecember 1999, financial institutions adopted a forward-looking approach in asset classification,taking into account the future performance of borrowers in addition to their track record in debtservice. The forward-looking criteria (FLC) forced the creditors to make a more realistic assess-ment of loan risks based on borrowers’ managerial competence, financial conditions, and futurecash flow (Lim 2002).

THE DEVELOPING ECONOMIES572

By taking over the NPLs of financial institutions, KAMCO has successfully re-solved debts and thereby improved asset mobility and asset soundness. The averageBIS capital adequacy ratio of ordinary banks increased significantly from 7.0 percent in 1997 to 10.8 per cent in March 2002, and the share of NPLs of banks de-creased from 16.9 per cent in1998 to 2.8 per cent of the total amount of loans by2001 (FSC 2002). Foreign investment and foreign reserves increased,15 and thegrowth of small and medium-sized venture enterprises was induced.

Another major role of KAMCO, apart from the resolution of debts, was to pro-vide assistance for the recovery of transferred insolvent companies. These are com-panies that may have been fundamentally competitive but became insolvent due toa temporary lack of financial resources. The assistance included withholding auc-tion of the company, withholding execution of security rights, adjustment of theredemption period and interest rates, financial assistance to debt-equity swaps andinvestment of NPLs, and provision of new loans and debt guarantees.

KAMCO also contributed to attracting foreign capital through various channels,including international bids, issuance of ABS, and sale to corporate restructuringand asset management companies.

Overall, the real contribution of KAMCO to more successful corporate restruc-turing was that by attracting capital from both domestic and foreign investors, it

TABLE III

STATUS OF NONPERFORMING LOANS RESOLUTION

(Trillion won)

Amount of NPLs 105.4 (100.0%)Purchasing value 39.4

Resolved NPLs 59.8 (56.7%)Purchasing value 24.4

Recovered value 27.7International bid 3.2Issuance of ABS 4.1Sale to AMC, CRC 1.9Sale of individual loans 0.6Court auction 3.1Repurchases and cancellation 9.7Voluntary repayment 5.1

Remaining NPLs 45.6 (43.3%)Purchasing value 15.0

Sources: KAMCO (2002) and PFOC and MOFE (2002).Note: Figures were taken at the end of June 2002.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

15 Foreign exchange reserves, which recorded $3.4 billion in December 1997, increased up to $112.4billion in June 2002.

573CORPORATE DEBT RESOLUTION

introduced a market mechanism in which nonperforming assets could be liqui-dated.

B. Other Debt-Restructuring Intermediaries

Other debt-restructuring intermediaries assisted KAMCO’s operations, includ-ing the Corporate Restructuring Fund, Corporate Restructuring Company (CRC)and vulture funds, Corporate Restructuring Vehicle, and Corporate RestructuringReal Estate Investment Trust.

CRCs and vulture funds were established under the Industrial Development Lawin February 1999 for the facilitation of market-induced corporate restructuring. CRCsare joint-stock corporations based on commercial law, whose main function was tocarry out corporate restructuring through takeovers, management restructuring, andsales of insolvent corporations.16 They also invested in and purchased the assets ofrestructuring companies, mediated M&As, and handled business for composition,reorganization, and bankruptcies. In addition, CRCs, as asset owners, issued ABSvia Special Purpose Vehicles (SPVs) and managed assets. An important contribu-tion of CRCs, apart from asset management, was that they transmitted a more ad-vanced asset management know-how. They also played a central role in corporaterestructuring, being the basis of other debt-restructuring intermediaries.

For investment funds they used vulture funds as well as their own capital. Thefunctions of vulture funds, such as management of assets or management of re-structuring of insolvent companies, were fulfilled by the CRCs.

Other debt-restructuring intermediaries operates through CRCs. The CorporateRestructuring Fund is a paper company, a form of mutual fund created under theSecurities and Investment Trust Law. It was established to extend support to troubledsmall and medium-sized businesses and some leading companies. The CorporateRestructuring Vehicle was set up as a device for market-induced restructuring. Itis also a paper company, a type of mutual fund for a limited period of time. Itgenerated profits through asset operations and distributed them to shareholders.Its functions included facilitating the disposal of assets by creditor banks, facilitat-ing effective management and governance, and stimulating capital market develop-ment.

Finally, Corporate Restructuring Real Estate Investment Trusts were introducedthrough the enactment of the Real Estate Investment Trust Law in April 2001. Dur-ing the financial crisis, real estate was a collateral for many distressed corporations.Real Estate Investment Trusts, by speedily converting real estate into capital, helpedto improve the liquidity and cash flow of the companies and thus promoted corpo-

16 Insolvent corporations were taken over through the acquisition of stocks or through merger anddivestiture. Then their management was restructured through a group of managers or a board ofdirectors from the CRC. Investment funds were paid back within five years through sales of stockand assets.

THE DEVELOPING ECONOMIES574

rate restructuring activities. They were also expected to provide minority investorswith more investment opportunities and develop the real estate market.

Most of all, for the better operation of these debt-restructuring intermediaries,foreign capital inflows and the foreign know-how of debt restructuring were important.

IV. ROLE OF FOREIGN CAPITAL IN CORPORATE RESTRUCTURING

Foreign capital was important as the only source of liquidity to improve the cashflow of the cash-strapped, highly leveraged, and indebted corporate sector of Ko-rea. Ultimately it promoted and funded market-oriented corporate restructuring,and also brought other nonfinancial and nontangible benefits such as foreign par-ticipation in management or financial market discipline.

Bold reforms were carried out to attract foreign direct investment (FDI) whichwas first allowed to be introduced into Korean enterprises, although to a limiteddegree,17 in April 1998. Because of continuous efforts, foreign investments in Ko-rea have increased sharply since 1998.18 This was largely due to the government’sinitiatives to deregulate the financial market and open it more to foreigners, but thedevaluation of assets at the onset of the crisis was also a contributory factor. For-eign corporations, on the other hand, pursued globalization and increased the mar-ket share through investments in Korea.

This section focuses on the two major forms of foreign investment—cross-bor-der M&As and investment in privatization of state-owned enterprises—and exam-ines their role in the process of corporate restructuring.

A. Cross-Border M&As

Cross-border mergers and acquisitions increased significantly after prominentefforts to encourage them were initiated in 1997. M&As by foreign firms increasedespecially after the financial crisis, in response to deregulation of laws restrictinghostile M&As, but also to lower asset prices and depreciation of the won. In addi-tion, there were abundant acquisition opportunities, as many of the distressed firmswere selling off parts of their business lines in the process of restructuring. In manycases, rescue funds flowed in from existing foreign partners to ease liquidity con-straints. Common forms of M&As have included: existing foreign partners buyingout Korean joint venture partners; existing foreign investors expanding throughacquisition; and creating new establishments in collaboration with Korean partnersto acquire existing business units (Yun forthcoming).

Several key industries had been opened up, including construction, leasing, se-curities, and futures brokerage, with a liberalization rate of 98.9 per cent by May

17 At that time, FDI was still prohibited in thirty-one business lines.18 The foreign investments until 1999 were focused on the financial and corporate sectors, but ex-

tended to the real estate market in 2000.

575CORPORATE DEBT RESOLUTION

1998.19 In May 1998, the rule limiting foreign ownership to not more than 10 percent without the approval of the board of directors was eased to allow 33 per centforeign ownership. The ceiling on total foreign shareholdings in individual compa-nies was completely abolished in May 1999. In addition, all forms of M&As, in-cluding hostile takeovers, were fully liberalized by the same time—before the fi-nancial crisis, even friendly M&As were limited to cases where the total assets ofthe companies involved did not exceed 2 trillion won. Furthermore, two stock mar-ket rules—the rule requiring statutory tender offers in the case of purchase of 25per cent or more, and the rule requiring disclosure of incremental acquisitions ofstakes larger than 5 per cent—were abolished.

Because of these deregulation efforts in cross-border M&As, foreign purchaseof shares and assets of Korean companies increased. In 1998, sales of newly issuedand outstanding corporate stocks and corporate assets bought by the foreign inves-tors reached $1.84 billion and $2.93 billion. Together they accounted for 60.9 percent of the total foreign investment in that year. In case of acquisition of outstand-ing stocks, the foreign companies acquired the shares of troubled domestic jointventure partner companies and subsequently became the sole owners. In case ofacquisition of newly issued stocks, the investments took the form of joint venturesthrough additional infusion of capital into existing businesses, and establishment ofnew companies through asset acquisition. These forms of investment are close toM&As (Rhee 1999).

As Table IV shows, a large bulk of foreign direct investment took place throughM&As rather than greenfield investments. More specifically, a large part of corpo-rate restructuring was carried out through foreigners’ acquisition of assets and out-standing stocks. In 1998, for example, M&As accounted for 47.8 per cent of allFDI inflows and, in particular, acquisition of assets accounted for 37.4 per cent.

19 This effort raised M&As by foreign companies sevenfold, which accounted for a fifth of all suchdeals in Korea in 1998 (OECD 1999).

TABLE IV

PATTERN OF INWARD FDI IN 1998

(U.S.$ million)

Invested amount 1,020 2,049 3,069 820 2,930 3,750 1,019 7,838Percentage (13.0) (26.1) (39.2) (10.5) (37.4) (47.8) (13.0) (100.0)

Investment size per case 46.4 42.7 43.8 27.3 154.2 76.5 113.2 61.2

Source: Rhee (1999) based on the data of the Ministry of Commerce, Industry and Energy.Note: Only investments exceeding U.S.$10 million were considered. AOS = acquisition ofoutstanding stocks; AA = acquisition of assets.

Classification

Acquisition of NewlyIssued Stocks

SubtotalNew Added AOS SubtotalAATotal

Long-TermLoans

M&A

THE DEVELOPING ECONOMIES576

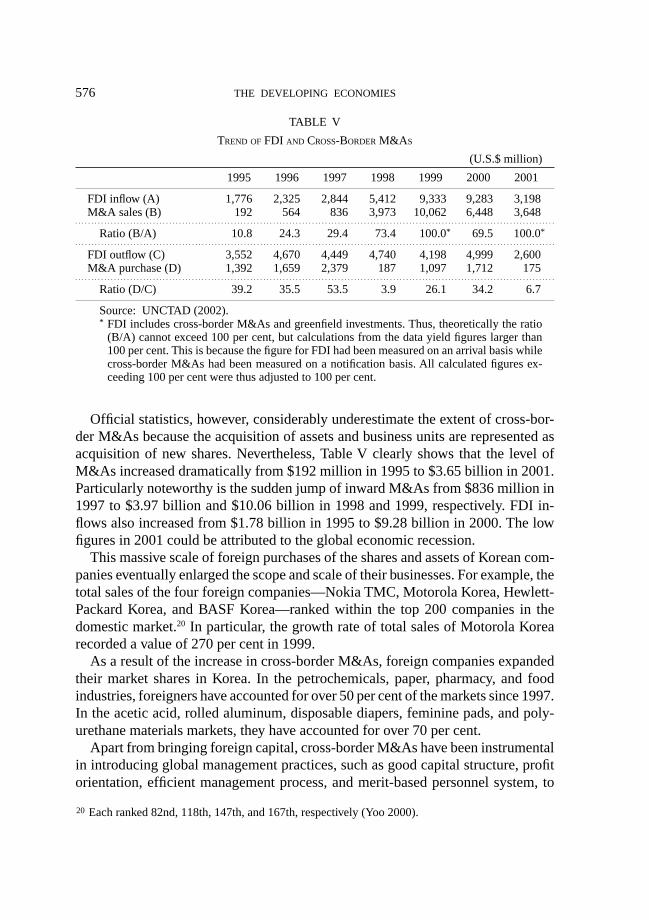

Official statistics, however, considerably underestimate the extent of cross-bor-der M&As because the acquisition of assets and business units are represented asacquisition of new shares. Nevertheless, Table V clearly shows that the level ofM&As increased dramatically from $192 million in 1995 to $3.65 billion in 2001.Particularly noteworthy is the sudden jump of inward M&As from $836 million in1997 to $3.97 billion and $10.06 billion in 1998 and 1999, respectively. FDI in-flows also increased from $1.78 billion in 1995 to $9.28 billion in 2000. The lowfigures in 2001 could be attributed to the global economic recession.

This massive scale of foreign purchases of the shares and assets of Korean com-panies eventually enlarged the scope and scale of their businesses. For example, thetotal sales of the four foreign companies—Nokia TMC, Motorola Korea, Hewlett-Packard Korea, and BASF Korea—ranked within the top 200 companies in thedomestic market.20 In particular, the growth rate of total sales of Motorola Korearecorded a value of 270 per cent in 1999.

As a result of the increase in cross-border M&As, foreign companies expandedtheir market shares in Korea. In the petrochemicals, paper, pharmacy, and foodindustries, foreigners have accounted for over 50 per cent of the markets since 1997.In the acetic acid, rolled aluminum, disposable diapers, feminine pads, and poly-urethane materials markets, they have accounted for over 70 per cent.

Apart from bringing foreign capital, cross-border M&As have been instrumentalin introducing global management practices, such as good capital structure, profitorientation, efficient management process, and merit-based personnel system, to

TABLE V

TREND OF FDI AND CROSS-BORDER M&AS

(U.S.$ million)

1995 1996 1997 1998 1999 2000 2001

FDI inflow (A) 1,776 2,325 2,844 5,412 9,333 9,283 3,198M&A sales (B) 192 564 836 3,973 10,062 6,448 3,648

Ratio (B/A) 10.8 24.3 29.4 73.4 100.0* 69.5 100.0*

FDI outflow (C) 3,552 4,670 4,449 4,740 4,198 4,999 2,600M&A purchase (D) 1,392 1,659 2,379 187 1,097 1,712 175

Ratio (D/C) 39.2 35.5 53.5 3.9 26.1 34.2 6.7

Source: UNCTAD (2002).* FDI includes cross-border M&As and greenfield investments. Thus, theoretically the ratio

(B/A) cannot exceed 100 per cent, but calculations from the data yield figures larger than100 per cent. This is because the figure for FDI had been measured on an arrival basis whilecross-border M&As had been measured on a notification basis. All calculated figures ex-ceeding 100 per cent were thus adjusted to 100 per cent.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

20 Each ranked 82nd, 118th, 147th, and 167th, respectively (Yoo 2000).

577CORPORATE DEBT RESOLUTION

Korea (Rhee 1999). The market competition was also affected—domestic compa-nies now face fiercer competition in both domestic and global markets.

B. Privatization

A second new channel for FDI consists of privatization. On July 3, 1998, the firstprivatization plans for public enterprises were announced. The plans included 32public enterprises—11 public investment and financing institutions and their 21subsidiaries—out of 108.21 Privatization was characterized by two stages—imme-diate and phased privatization. As a general rule, more market-oriented public en-terprises were privatized, and when early privatization was not immediately fea-sible, privatization followed structural reforms of the enterprises with yearly checkupprograms. The former case included five public enterprises and the latter case in-cluded six others. The number of public enterprises subject to privatization ac-counted for only 30 per cent of 108 public enterprises, but in terms of the number ofemployees and sales revenues, they accounted for 70 per cent (Cho 2001).

Foreign investors could acquire shares of Korean companies without being re-stricted by foreign investment ceilings except in five designated companies—POSCO(Pohang Iron and Steel Corporation), Korea Electric Power Corporation, KoreaTelecom, Korea Gas Corporation, and Korea Tobacco and Ginseng Corporation—although the specified ceilings varied for different state-owned enterprises (Yunand Park 1999). However, in the process of privatization, the government graduallyreduced the level of regulation: POSCO’s 30 per cent ceiling on the acquisition ofshares by foreigners and 3 per cent ceiling for a single foreign investor were liftedin 2001, while the restrictions on the acquisition of Korean Tobacco and GinsengCorporation by a single person were eliminated in 2000.

International offers in the process of privatization have mainly taken the form ofdepository receipts (DRs) issuance. The issuance of DRs was an attractive way ofprivatizing Korean public enterprises because it allowed relatively easier access tothe international capital markets and ownership of shares could be dispersed withlittle threat of an M&A, since purchases were made mainly by institutional inves-tors.

Looking at the outcomes so far, foreign investors and capital, indeed, have beendeeply involved in the process of privatization. A remarkable example is POSCO,which successfully offered its shares in the form of DRs: it sold the government’sshareholdings (3.14 per cent) and the shareholdings of the Korea Development Bank(2.73 per cent) through the issuance of DRs at the NYSE in New York and LSE inLondon; further shareholdings of Korea Development Bank in the amounts of 8 percent and 4.6 per cent were sold in 1999 and 2000, respectively.

21 Public enterprises include 13 public investment institutions and their 30 subsidiaries and 13 publicfinancing institutions and their 52 subsidiaries.

THE DEVELOPING ECONOMIES578

Korea Electric Power Corporation issued foreign DRs twice—14.5 per cent oftotal shares in 1999 and 17.8 per cent in 2001—and issued foreign exchangeablebonds and bonds with warrants—11.8 per cent of total shares—in December 2001.Korea Tobacco and Ginseng Corporation issued 10 per cent of its shares owned bythe Industrial Bank of Korea as foreign exchangeable bonds in 2000, and in 2001,19.8 per cent owned by the government and Industrial Bank of Korea was trans-formed into foreign DRs and exchangeable bonds. The government currently plansto sell its shareholdings of government-run banks which account for 33 per cent oftotal shares in the domestic (19 per cent) and foreign (14 per cent) markets. KoreaElectric Power Corporation sold the government’s share of 5 per cent on the NYSEthrough DRs and, in 2000, the facilities of the Korea District Heating Corporationwere sold to LG-Caltex.

Korea Electric Power Corporation was privatized in the form of DRs issuanceand trade sale of generation plants. Its foreign share as of June 1999 amounted to25.8 per cent. POSCO was privatized in the form of DRs and sale of Korea Devel-opment Bank shares. Foreign share of the company was 51.0 per cent in 1999.Finally Korea Telecom was privatized in the form of DRs and strategic tie-ins withforeign telecommunication firms. Foreign share of the company amounted to 19.4per cent in 1999. However, without strategic cooperation with foreign telecommu-nication companies, it is still difficult to promote privatization.

As discussed so far, in addition to KAMCO’s sale of NPLs to foreigners throughindirect methods such as international auctions, issuance of ABS, and sale to CRCs,cross-border M&As and privatization contributed significantly to increasing for-eign capital inflows. As such, the role of foreign capital has been significant andimportant in helping corporate restructuring.

V. CORPORATE GOVERNANCE AND CHANGES IN CONTROL

Many authors have suggested that the problem of huge debt burden on Koreanenterprises was due to the inherent problem of chaebol-type governance and own-ership structure. Approaches to deal with this problem can thus fundamentally changeand improve the corporate sector of Korea. In this section, the various reformsundertaken to attempt to bring changes to corporate governance and control areexamined and the outcomes are assessed.

A. Toward a New Governance

Corporate governance structure is the system that commands and controls a cor-poration.22 Recognizing that the numerous problems in the corporate governance

22 Cadbury Committee Report (1992) gives this definition. Normally, corporate governance structurerefers to a systematic relationship between an owner and the management. In a broad sense, it

579CORPORATE DEBT RESOLUTION

structure played a major role in the financial crisis of the Korean economy, variousreforms have been sought.

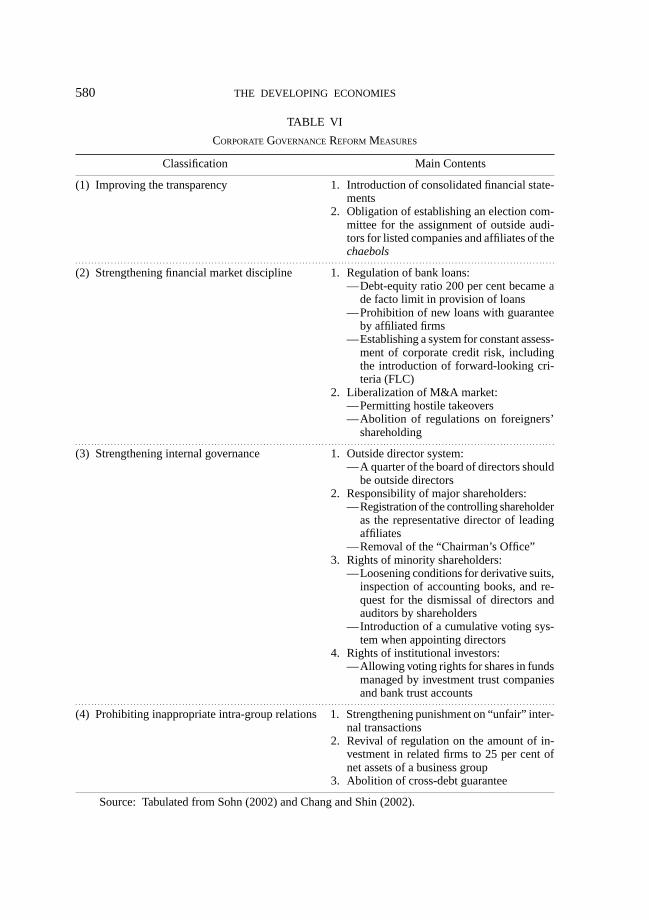

The reforms focused on four major areas: (1) improving the transparency of cor-porate management, (2) strengthening financial market discipline, (3) strengthen-ing internal governance, and (4) prohibiting inappropriate intra-group relationships.Improving the transparency included the introduction of consolidated financial state-ments, and appointment of outside auditors. Strengthening financial market disci-pline included the strengthening of deregulation of bank loans, and liberalization ofM&As. Strengthening internal governance included the introduction of the outsidedirector system, protection of the rights of minority shareholders and institutionalinvestors, and strengthening of the responsibility of major shareholders. Finally,prohibition of inappropriate intra-group transactions included the following: harsherpunishments for unfair internal transactions, revival of some regulations, and aboli-tion of debt guarantees. The main contents of the corporate governance reforms aresummarized in Table VI.

Several cases of changes in corporate governance could be observed after thereforms. In particular, the changes in corporate laws and regulations have beenquite dramatic (Park 2000). Improvements in the transparency were apparent in1996 as the shareholders of Oriental Brewery Company requested to inspect thecompany’s books—the first such case in Korean corporate history. These actionsposed a serious threat to the management of the company. The case of SamsungElectronics shows how the voice of minority shareholders could be heard after thereforms. Shareholders of the company had been questioning a large suspicious lossand inefficiencies in some investment projects. In 1998, they eventually filed a share-holder derivative action suit against the directors of the company on various ac-counts including illegal insider transactions among affiliates. The management wasalso fined by the district court for not disclosing the contents of the minutes of theboard of directors’ meeting, which was requested by the shareholders. In turn, in1998, SK Telecom was forced to elect two outside directors and an independentauditor chosen by the shareholders. The outside directors actually cancelled twodeals between firms in the group. In 1997, the Fair Trade Commission ordered thecompany to recover the subsidy provided to its affiliate, SK Logistics.

B. Changes in Control

The major characteristic of the chaebols is the concentration of ownership. Thefounding families of a chaebol group normally own a large share of the firms. Thecommon practice in the management of chaebols is that the owners, who are often

––––––––––––––––––––––––––indicates that there is a systematic process to maintain and manage a clear or implied contractamong the persons concerned of the corporation, such as shareholders, creditors, employees, andso on.

THE DEVELOPING ECONOMIES580

TABLE VI

CORPORATE GOVERNANCE REFORM MEASURES

Classification Main Contents

(1) Improving the transparency 1. Introduction of consolidated financial state-ments

2. Obligation of establishing an election com-mittee for the assignment of outside audi-tors for listed companies and affiliates of thechaebols

(2) Strengthening financial market discipline 1. Regulation of bank loans:—Debt-equity ratio 200 per cent became a

de facto limit in provision of loans—Prohibition of new loans with guarantee

by affiliated firms—Establishing a system for constant assess-

ment of corporate credit risk, includingthe introduction of forward-looking cri-teria (FLC)

2. Liberalization of M&A market:—Permitting hostile takeovers—Abolition of regulations on foreigners’

shareholding

(3) Strengthening internal governance 1. Outside director system:—A quarter of the board of directors should

be outside directors2. Responsibility of major shareholders:

—Registration of the controlling shareholderas the representative director of leadingaffiliates

—Removal of the “Chairman’s Office”3. Rights of minority shareholders:

—Loosening conditions for derivative suits,inspection of accounting books, and re-quest for the dismissal of directors andauditors by shareholders

— Introduction of a cumulative voting sys-tem when appointing directors

4. Rights of institutional investors:—Allowing voting rights for shares in funds

managed by investment trust companiesand bank trust accounts

(4) Prohibiting inappropriate intra-group relations 1. Strengthening punishment on “unfair” inter-nal transactions

2. Revival of regulation on the amount of in-vestment in related firms to 25 per cent ofnet assets of a business group

3. Abolition of cross-debt guarantee

Source: Tabulated from Sohn (2002) and Chang and Shin (2002).

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

581CORPORATE DEBT RESOLUTION

nonprofessional managers, have greater voting power than other shareholders andthus can exercise exclusive control of the firm. Moreover, it has been suggested thatin these chaebols, controlling shareholders exercise control in excess of their hold-ings through a hierarchical chain of ownership (Chang 2002). This is an example ofthe nonseparation of ownership and management in chaebols.

Agency theories suggest two different strategies. According to one strategy, basedon the convergence-of-interest hypothesis, nonseparation of ownership and man-agement is beneficial to the performance of the firms because there is less conflictof interest between the two groups. In the other strategy, based on the entrenchmenthypothesis, it is suggested that the firm value decreases as managerial ownershipincreases, because managers—be they professional or the owners—hold a substan-tial share of the firm which would provide them with voting power that guaranteestheir employment with a handsome salary.23 The two very different strategies, how-ever, converge to an agreed conventional wisdom that the ownership structure af-fects the firm performance or value.

Many previous studies had focused on issues of concentrated ownership ornonseparation of ownership and management. This paper, however, pays attentionto another characteristic of the chaebols—the single-nationality of ownership. Here,the managerial aspects that could be improved by making ownership multinationalare being illustrated.

The massive inflow of foreign capital after the financial crisis through cross-border M&As, privatization, and the sale of KAMCO’s assets brought major changesin corporate control and ownership. Foreign investment can exert significant effectson corporate management, especially in terms of sharing control and power.24 Theexperience of three companies, Hansol PCS, the Korea First Bank, and SamsungHeavy Industry illustrates the point very well.

Hansol PCS, a mobile phone operator and a subsidiary of Hansol, a major chaebol,received investment from Bell Canada International and AIG, an American invest-ment fund. Thirty-eight per cent of the total outstanding shares of Hansol PCS wasdivided between the two investors. They consequently adopted “super majority votingrights,” which gave minority shareholders enhanced power and gained about 33–49per cent of voting rights by electing four representatives to the board.

The Korea First Bank also came under foreign ownership. Although it was thelargest bank in Korea in terms of assets and profits, when it became insolvent in1998, its nonperforming loans reached $3.2 billion. Soon Newbridge Capital ac-quired 50.99 per cent of shares and a foreign manager was elected as president andchief executive officer of the bank. The most important change in the Korea FirstBank from the entry of foreign capital and management was the general reorgani-

23 Theories are well summarized in the report of Cho and Chae (2002).24 Case studied by Yun (forthcoming).

THE DEVELOPING ECONOMIES582

zation of the bank involving the organizational structure redesigned after the west-ern style division system, an employee reward mechanism, and new business strat-egy.

Volvo’s acquisition of Samsung Heavy Industry significantly contributed to themanagement of the Korean firm. The so-called “flat management” introduced byVolvo reduced direct and indirect transaction costs by eliminating steps in the deci-sion-making process.

VI. ASSESSMENT AND CONCLUSION

The Korean economy has almost recovered and reached its pre-crisis level, basedon its macroeconomic performances. The GDP growth rate recovered and reachedthe pre-crisis level of 5.5 per cent in 2001 from −6.7 per cent in 1998. Foreignexchange reserves, owing to a trade surplus that has continued for the last fouryears, recorded over $112.4 billion in June 2002 from $3.4 billion in December1997. The foreign exchange rate appreciated to about 1,200 won to U.S.$1.00 inJune 2002 from 1,840 won in January 1998. In addition, the interest rate decreasedto 5.4 per cent from over 19.0 per cent. Moreover, the unemployment rate droppedto 2.7 per cent from 6.8 per cent. Owing to its rapid economic recovery, Korea wasable to repay its IMF loans in August 2001, two years and eight months earlier thanoriginally scheduled.

The sharp recovery of the post-crisis Korean economy can be best assessed andreflected in the various sovereign ratings of the global credit rating agencies. InMarch 2002, Moody’s raised Korea’s sovereign rating to A3, as seen in Table VII.This is a rise from Korea’s rating of Ba1 during the crisis period, the lowest level ithad ever received, and only two levels below the country’s pre-crisis rating. BothS&P and Fitch IBCA also raised the sovereign rating to A− and A, respectively.

Structural reforms, especially corporate restructuring, contributed significantlyto Korea’s rapid economic recovery. In the Article IV consultation with Korea inFebruary 2002, the IMF expressed its appreciation for the “sustained implementa-

TABLE VII

TREND IN KOREA’S SOVEREIGN RATING

Rating Agency Pre-crisis During the Crisis Post-crisis

Fitch IBCA AA− B− (−12) A (+10)S&P AA− B+ (−10) A− (+7)Moody’s A1 Ba1 (−6) A3 (+4)

Source: Ministry of Finance and Economy, “S&P Raises Korea’s Sovereign Rating,” PressRelease, July 24, 2002.Note: The numbers in the parentheses denote the changes in the stages from the pre-crisisperiod for the second column and during the crisis period for the third column.

583CORPORATE DEBT RESOLUTION

tion of structural reform,” stating that the Korean government policy enhanced marketdiscipline, along with macroeconomic fundamentals, and therefore the resilienceof its economy.25 During the five years since the financial crisis, the financial situa-tion of Korean corporations markedly improved.26

Table VIII lists various financial indicators that clearly show improvements. Boththe debt-equity ratio and interest coverage ratio have shown improvements sincethe financial crisis. But these figures can be misleading guides of the viability andsoundness of firms. The fall in debt-equity ratio might have been induced by therevaluation of equity, rather than by an actual reduction in debts. Also, the improve-ment in the interest coverage ratio may be due to the cut in interest rates after 1999rather than to improved profitability.27

However, as discussed earlier, it is clear that the sharp increase in foreign capitalin the form of FDI inflows, particularly in cross-border M&As, significantly con-tributed to successful corporate restructuring. Cash flows also increased throughother channels: KAMCO’s operations including international bidding, issuance ofABS, and sales to CRCs and AMCs,28 cross-border M&As, and foreign inwardprivatization.

Also, it appears that various restructuring intermediaries, in particular KAMCO,have successfully contributed to the resolution of corporate debts. NPLs have con-tinuously been purchased and cleared, and the share of remaining NPLs to the totalhas significantly decreased from 88.6 per cent in 1997 to 24.0 per cent in 2001. In

TABLE VIII

FINANCIAL INDICATORS

1995 1996 1997 1998 1999 2000 2001

Debt-equity ratio 286.8 317.1 396.3 303.0 214.7 210.6 182.2Ordinary income to sales 3.6 1.0 −0.3 −1.9 1.7 1.3 0.4Operating income to sales 8.3 6.5 8.3 6.1 6.6 7.4 5.5Return on equity 11.02 11.03 2.02 −4.21 0.04 −5.8 0.02Return on assets 2.83 0.5 −0.93 −3.59 0.01 −1.9 0.01Interest coverage ratio 149.6 112.1 129.1 68.3 96.1 157.2 132.6

Source: Bank of Korea, Financial Statement Analysis, various issues.

25 Ministry of Finance and Economy (2002, p. 24).26 On the other hand, it cannot be ignored that favorable external conditions—an information technol-

ogy boom in the United States and a low interest rate in the world market between 1999 and2000—also exerted positive impacts on the recovery of the Korean economy. Especially, the lowinterest rate in the world market gave the Korean government the leeway to steadily achieve eco-nomic recovery in spite of its low interest rate policy, evading the problem of capital outflow.

27 A review and comparison of the pre- and post-crisis corporate performance can be found in Chopraet al. (2001) and Richards et al. (2002).

28 International bidding, issuance of ABS and sales to AMCs and CRCs account for about one-thirdof KAMCO’s total operations.

THE DEVELOPING ECONOMIES584

particular, the remaining NPLs to total credit decreased to less than 5 per cent in2001. As of June 2002, KAMCO had recovered 27.7 trillion won, or 113 per cent ofthe purchasing value of NPLs, making profits of 3.3 trillion won. Also as of June2002, the remaining NPLs accounted for 43.3 per cent of the total NPLs. However,if Daewoo’s NPLs are excluded, KAMCO’s operations have been very successful,clearing almost three-quarters of the total NPLs.29 Korea’s performance in resolv-ing corporate debts can be compared with that of other crisis-struck countries. WhileKorea cleared three-quarters of its total NPLs, Indonesia cleared 9 per cent andMalaysia 85 per cent.30

The financial crisis and the resulting reform measures suggest some lessons. First,the importance of short-term cash flows and liquidity of the firms must be recog-nized. The objective of the firms and restructuring of the corporate sector shouldnot focus only on conventional targets such as growth, productivity, and profitability,but also on the efficient management of cash flows. Second, although the resolutionof corporate debts has been successful, there should be continuous legal and insti-tutional efforts to resolve the remaining NPLs. Third, the benefits and importanceof foreign capital are now recognized. Thus both financial and corporate sectorsmust continue to attract more foreign capital, not only to reinforce the on-goingcorporate restructuring, but also to improve the viability and soundness of the cor-porate sector. Fourth, the changes in corporate governance and ownership structuremust successfully be linked to better corporate performance.

This paper analyzed various corporate sector reforms encompassing corporatedebt restructuring and corporate governance reforms and identified two major fac-tors behind this rapid rehabilitation of the Korean economy as follows: the success-ful resolution of corporate debts and large inflows of foreign capital through suchchannels as cross-border M&As and privatization, which have improved, amongother things, the cash flows of the corporate sector. Thus the conclusion of thispaper is straightforward. First, the resolution of corporate debts has been satisfac-tory and successful. Second, foreign capital has contributed significantly to effec-tive corporate restructuring and debt resolution. However, to draw more concreteand firmer conclusions, we need more detailed and in-depth research to identify theprecise channels through which corporate debts were resolved. As yet, comprehen-sive statistics and research on the role of foreign capital in corporate restructuringare still lacking. We consider that this current study may pave the way for furtherinvestigations.

29 Daewoo’s NPLs have remained uncleared following political difficulties.30 The official figure for Korea is 40 per cent, but as mentioned previously, the exclusion of Daewoo’s

NPLs leads to three-quarters. Malaysia recorded the highest rate among the crisis-ridden countries(Mako 2001a).

585CORPORATE DEBT RESOLUTION

REFERENCES

Ahn, Choong-Yong. 2001. “Financial and Corporate Sector Restructuring in South Korea:Accomplishments and Unfinished Agenda.” Japanese Economic Review 52, no. 4: 452–70.

Aiyer, Sri-Ram. 1999. “Corporate Reform: Key to Consolidating Korea’s Recovery.” Paperpresented at the International Conference on Economic Crisis and Restructuring in Ko-rea, hosted by the Korea Development Institute, December 3, Seoul.

Chang, Ha-Joon, and Jang-Sup Shin. 2002. “Restructuring ‘Korea Inc.’— Evaluating thePost Crisis Corporate Restructuring in Korea.” Paper presented at the 10th Seoul Jour-nal of Economics International Symposium on the Socio-Economic Roles of Firms andChaebols, August 29, Seoul.

Chang, Sea-Jin. 2002. “Ownership Structure, Expropriation, and Performance of Group-Affiliated Companies in Korea.” Paper presented at the 2nd Asian Corporate Gover-nance Conference, hosted by the Asian Institute of Corporate Governance, May 16,Seoul.

Cho, Myeong-Hyeon, and Hee-Bong Chae. 2002. “Ownership Structure and the Value ofthe Firm in Korean Chaebols: An Empirical Analysis.” In The Post-Financial CrisisChallenges for Asian Industrialization, ed. Richard Hooley and Jang-Hee Yoo. Oxford:Elsevier Science.

Cho, Sung-Hoon. 2001. “Jabon sijangeul tonghan gonggieop minnyeonghwa jeongchaekbanghyang” [Privatization policy of state-owned enterprises through capital market].Korea Securities Research Institute Issue Paper 01-03.

Chopra, Ajai; Kenneth Kang; Meral Karasulu; Hong Liang; Henry Ma; and Anthony Richards.2001. From Crisis to Recovery in Korea: Strategy, Achievements, and Lessons. IMFWorking Paper WP/01/154.

Committee on the Financial Aspects of Corporate Governance (Cadbury Committee). 1992.Financial Aspects of Corporate Governance.

Financial Supervisory Commission (FSC). 2002. “Gieop sinnyong pyeongga monitoringgyeolgwa” [Results of monitoring of corporate credit risks]. Press Release, February14.

Korea Asset Management Corporation (KAMCO). 2000. “Busil chaegwon jeongniuipiryoseonggwa hyanghu gwaje” [Methods of nonperforming loan resolution and policyimplications]. KAMCO Research Paper.

———. 2002. “Gukhoe jeongmu wiwonhoe bogo jaryo” [Report to the National Assem-bly]. Internal Report, July 29.

Korea Economic Research Institute (KERI). 2000. Jaebeol gujowa jaebeol jeongchaek [Struc-ture and policy of chaebols]. Policy Paper 2000-05.

———. 2001. Hyeonhaeng gieop gujo jojeong system-ui munjejeomgwa baljeon banghyang[Problems of current corporate restructuring system and future direction]. Policy Paper2001-06.

Lieberman, Ira W., and William P. Mako. 1998. “Korea’s Corporate Crisis: Its Origins and aStrategy for Financial Restructuring.” Paper presented at the International Seminar onKorean Economic Restructuring: Evaluation and Prospects, hosted by the Korea Insti-tute for International Economic Policy, October, Seoul.

Lim, Won-Hyuk. 2001. “Market-Led Corporate Restructuring in a State-Led Economy: A

THE DEVELOPING ECONOMIES586

Problem of Transition.” In Korea’s Economy 2001, ed. James M. Lister. Washington,D.C.: Korea Economic Institute of America.

———. 2002. “Korea: Corporate Vulnerabilities and Restructuring.” Mimeographed. Ko-rea Development Institute.

Mako, William P. 2001a. “Corporate Restructuring and Reform: Lessons from East Asia.”Paper presented at the 26th Senior Policy Forum on Economic Crisis and StructuralAdjustment in Korea, November 5–9.

———. 2001b. “Corporate Restructuring and Reform: Lessons from Korea.” Paper pre-sented at the Conference on the Korean Crisis and Recovery, hosted by the InternationalMonetary Fund and the Korea Institute for International Economic Policy, May 18,Seoul.

Ministry of Finance and Economy (MOFE). 2002. Economic Bulletin 24, no. 3.Organisation for Economic Co-operation and Development (OECD). Various years. OECD

Economic Surveys: Korea.Park, Kyung-Suh. 2000. “Corporate Governance in Korea: Its Institutional Structures and

Operations.” Paper presented at the UNDP Conference on Corporate Governance andthe Financial Crisis, November 20–21, Kuala Lumpur.

Public Fund Oversight Committee (PFOC), and Ministry of Finance and Economy (MOFE).2001 and 2002. Gongjeok jageum gwalli baekseo [White paper on the oversight of pub-lic funds].

Rhee, Dong-Kee. 1999. “The Entry of Foreign Multinationals and Its Impact on the KoreanMarket.” Paper presented at the International Seminar on the Entry of Foreign M&Aand the Globalization of the Korean Economy, hosted by the Korea Institute for Interna-tional Economic Policy, November 30, Seoul.

Richards, Anthony; Kenneth Kang; Henry Ma; Hong Liang; Aung Win; Paul Cashin; MeralKarasulu; Thomas Laryea; and Sungbin Cho. 2002. Republic of Korea: Selected Issues.IMF Country Report 02/20.

Sohn, Chan-Hyun. 2002. “Korea’s Corporate Restructuring since the Financial Crisis: Mea-sures and Assessment.” Paper presented at Asia–Latin America Cooperation (ALAC)Seminar on Promoting Growth and Welfare, Santiago, April 29–30, and Rio de Janeiro,May 2–3.

UN Conference on Trade and Development (UNCTAD). 2002. World Investment Report:Transnational Corporations and Export Competitiveness.

Yoo, Yong-Joo. 2000. “Oejawa hanguk gyeongje” [Foreign capital and the Korean economy].CEO Information, no. 264. Samsung Economic Research Institute.

Yun, Mi-Kyung. Forthcoming. “FDI and Corporate Restructuring in Post-Crisis Korea.” InEconomic Crisis and Corporate Restructuring in Korea, ed. Stephan Haggard, WonhyukLim, and Euysung Kim. Cambridge: Cambridge University Press.

Yun, Mi-Kyung, and Young-Ho Park. 1999. “The Role of Foreign Investment in KoreanPrivatization.” Daeoe gyeongje yeongu [Journal of International Economic Policy Stud-ies] 3, no. 2: pp. 29–70.

Zang, Hyoung-Soo, and Yun-Jong Wang. 1998. IMF chejehaui hanguk gyeongje [Adjust-ment reforms in Korea since the financial crisis: A comprehensive report I]. Korea Insti-tute for International Economic Policy.