corporate governance - towards best-practice … governance — towards best-practice corporate...

TRANSCRIPT

Corporate Governance f o r M a i n M a r k e t a n d a i M C o M pa n i e s

!!!"#!$"$%&'()'*+'$%,#%,-.*/,*#%,.0+(

!"##$%&'#("'")&"

1%%23$%,#%,-.*3(%4*,+-+$*3053#-,.3%63.7*389:3%63;%<,3%,(-+05-.0%+"3=*3$-+37*>#3;%<3.%3$%&&<+0$-.*3.70535<$$*556<>>;"

!"#$%#"&'()*+,-*'./01*2//3*'1"44&5"677"'(8.-1"'*1*'9*:5";<"-.(1":/)0=*<->"?&+2@"'*A*'1"-/"&'()*+,-*'./01*2//3*'1"44&"B,"7(=(-*:"7(,C(7(-D"3,'-<*'1.(3"(<"-.*"E<(-*:"F(<8:/=G>"+.()."(1","

Page 177Corporate governance — towards best-practice corporate reporting

Reporting is a fundamental part of the UKCorporate Governance Code (the Code). It isthrough appropriate reporting of governance thatcompanies earn the right to the flexibility that aprinciples-based framework allows.

It is expected that companies will comply withmost of the provisions of the Code most of thetime — and indeed a report from the FinancialReporting Council (FRC) in December 2011,‘Developments in Corporate Governance’,showed 50 per cent of FTSE 350 companiesclaiming full compliance and 80 per cent of theremainder complying with all but one or two ofthe Code’s provisions. However, the UKframework crucially allows boards to exercisetheir judgement in respect of their governancearrangements as long as they explain theirreasons for non-compliance with the Code. Thisjudgement is not generally challenged byregulators; it is the responsibility of shareholdersto consider the judgements and the explanationsthat are provided when a company does notfollow a certain provision.

The FRC’s proposed revisions to the Code foryears beginning on or after October 1, 2012include a number of measures that are intendedto enhance engagement and stewardship bybuilding the confidence of stakeholders incompany reporting. The hope is that this willencourage the taking of a long-term view indecision-making and counteract the risk of arepeat of the short-termism that is often seenas a root cause of the financial crisis.

Governance reporting is an integral part of theFRC’s proposals, which include enhanced auditcommittee reporting. But governance reportingalso has a wider role to play in building investor

confidence and encouraging the taking of a long-term view. Governance is not just aboutconfidence in the financial statements; it is aboutconfidence in the company in general. It is aboutshowing how the company’s business model,strategy and objectives, risk, performance andreward are governed.

Governance reporting is a real opportunity to reapthe benefits of the good practice that exists withincompanies, and to build the confidence ofinvestors and other stakeholders and thereforecompany value. Few companies take thisopportunity successfully.

Current governance reporting practice — whycompanies are missing their opportunitiesWith a few exceptions, despite the huge potentialbenefits outlined above, the reporting of corporategovernance in the UK could do more to embrace

23. Corporate governance — towards best-practice corporate reporting

John Patterson, PricewaterhouseCoopers LLP

“There is some scepticism in Brussels about theeffectiveness of the ‘comply or explain’ approachto corporate governance, and the willingness andability of shareholders to hold boards to account.Some in the UK may feel that its track recordshould speak for itself, but in the currentenvironment there is a need to demonstrate that‘comply or explain’ continues to deliver strongand effective governance, and is taken seriouslyby companies and investors. Failure to do socould result in an approach which could be moreprescriptive about the way companies organisethemselves, and could give more power toregulators at the expense of shareholders.”FRC: ‘Developments in corporate governance’

The European Commission

and ‘comply or explain’

Post-IP

O c

onsid

era

tions

Page 178 Corporate governance — towards best-practice corporate reporting

the spirit of the Code. The FRC has recognisedthis and in the Preface to the Code (see the panelabove) it recommends personal reporting by thechairman of the company as a way of improvingthe situation.

Why are companies missing the opportunity foreffective communication with stakeholders thatgovernance reporting represents? Why are boardsrisking the flexibility to exercise their judgementthat the UK framework affords?

The Listing Rules and the ‘checklist mentality’Although relatively few of the detailed provisionsof the Code require specific disclosures (and theseare listed in Schedule B to the Code), the ListingRules require companies to provide a narrativestatement of how they have applied its MainPrinciples. Many companies find that the easiestway to demonstrate this is to explain how theyhave complied with each of the provisions thatrelate to the Main Principles. The result of this

approach is often apparently standardiseddisclosure, as companies repeat the wording of theCode provisions. This leads to a lengthy reportthat reads like ‘boiler-plate’ and can make itdifficult for the reader to identify importantinformation from mere procedure — to ‘see thewood for the trees’.

Reinforcing this, many companies have alsoexperienced a negative reaction from shareholdergroups or proxy advisers that take a mechanisticapproach to checking compliance if they attempt toomit mention of a specific provision. Our advice onthis is to resist. A number of leading governancereporters do not run through each and everyprovision of the Code in their disclosures. Similarly,external auditors have no mandate to insist on a‘box ticking’ report (see the panel above).

Corporate reporting challengesA number of the challenges that apply to corporatereporting in general play out in governance, and

The role of auditors in ‘reviewing’ the corporategovernance statement is set out in the ListingRules and under auditing standards. Theresponsibilities are restricted to reviewing ninespecific provisions of the code (C.1.1, C.2.1,and C.3.1 to C.3.7) and the going concernstatement that is required of UK incorporatedcompanies under Listing Rule 9.8.6R (3). Otherthan this responsibility, auditors read thecorporate governance statement forconsistency with the financial statements andfor any material mis-statements of fact basedon the knowledge they obtain from their otheraudit work. They will not want to be associatedwith any misleading statements in thegovernance report, but this does not mean theywill look for disclosures relating to everyprovision of the Code.

The role of auditors

“Chairmen are encouraged to report personallyin their annual statements how the principlesrelating to the role and effectiveness of theboard (in Sections A and B of the new Code)have been applied. Not only will this giveinvestors a clearer picture of the steps taken byboards to operate effectively but also, byproviding fuller context, it may make investorsmore willing to accept explanations when acompany chooses to explain rather than tocomply with one or more provisions. Above all,the personal reporting on governance bychairmen as the leaders of boards might be aturning point in attacking the fungus of ‘boiler-plate’ which is so often the preferred and easyoption in sensitive areas but which is deadcommunication.”FRC: Preface to the Corporate Governance Code

Personal reporting

Page 179Corporate governance — towards best-practice corporate reporting

there are also a number of specific challenges ingovernance reporting:

l Standardised disclosures are seen as a safeoption in corporate reporting. To givecompany-specific information — for instance,about particular events or challenges that thecompany faces — is seen as potentially riskyeven where it is not obviously commerciallysensitive

l It takes courage to ‘lead the way’ inreporting, moving away from precedent in theform of similar disclosures publishedpreviously by others. Of course largerorganisations may have more resources athand to allow them to do this, but there aremany examples of creative approachesoutside the FTSE 100

l Corporate reporting is used by a number ofdifferent audiences, each with differingneeds; companies worry that too muchcustomisation will mean their reportingfails to meet the needs of a particulargroup

l The various elements of the front half of theannual report are often drafted separately,leading to differing approaches and styles andalso to a lack of integration, perhaps beyondsome basic cross-references. This isparticularly limiting for corporate governanceas it can be related to many areas of theorganisation — in fact to almost everything inthe annual report

l Governance deals with particularly sensitiveareas: board-level governance focusesspecifically on the activities of the directors,and their individual characteristics,relationships and even the evaluation of theirperformance.

To help address these challenges it pays forthere to be oversight that ranges across thewhole annual report. Assemble a group who willbe aware of the overall plan and messaging.

Also ensure that the project plan allows enoughtime for initial mapping out of the content andfor review and integration after the content isdrafted.

Most importantly, corporate reporting needs to beowned by those able to see the big picture andwho have a vested interest in making sure it iscommunicated; the directors should be involvedearly enough to be able to influence the process.The FRC’s encouragement of personal reportingon governance by the chairman recognises this,and governance reporting particularly benefitsfrom these strategies.

The FRC’s proposed changes to the Code fromOctober 1, 2012 also include a requirement thatthe board, with the advice of the auditcommittee, should set out the basis on whichthey consider that the whole annual report is“fair, balanced and understandable” and“provides the information necessary for users toassess the company’s performance, businessmodel and strategy”. If they are introduced,these changes will emphasise the directresponsibility of the board and the auditcommittee for good reporting.

Going beyond compliance – starting to take thecommunication opportunityBecause current governance reporting is oftenuninspired, it’s not difficult to make an impression.Here are some quick wins to consider:

Those preparing annual reports should refer tothe FRC’s ‘Cutting Clutter’ publication. Thisincludes a specific disclosure aid ongovernance reporting, but its real importancelies in its emphasis on only reportinginformation that is material, and in a way thatis open and honest, clear and understandable,and interesting and engaging.

Cutting clutter

Post-IP

O c

onsid

era

tions

Page 180 Corporate governance — towards best-practice corporate reporting

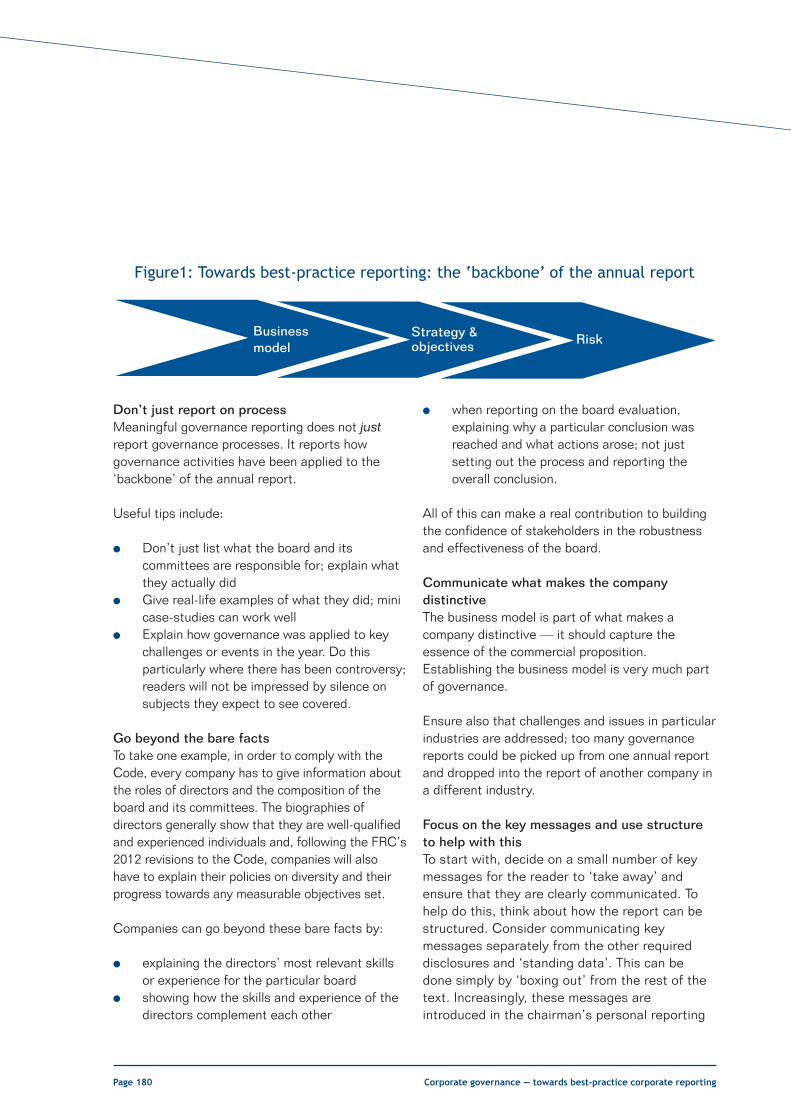

Don’t just report on processMeaningful governance reporting does not justreport governance processes. It reports howgovernance activities have been applied to the‘backbone’ of the annual report.

Useful tips include:

l Don’t just list what the board and itscommittees are responsible for; explain whatthey actually did

l Give real-life examples of what they did; minicase-studies can work well

l Explain how governance was applied to keychallenges or events in the year. Do thisparticularly where there has been controversy;readers will not be impressed by silence onsubjects they expect to see covered.

Go beyond the bare factsTo take one example, in order to comply with theCode, every company has to give information aboutthe roles of directors and the composition of theboard and its committees. The biographies ofdirectors generally show that they are well-qualifiedand experienced individuals and, following the FRC’s2012 revisions to the Code, companies will alsohave to explain their policies on diversity and theirprogress towards any measurable objectives set.

Companies can go beyond these bare facts by:

l explaining the directors’ most relevant skillsor experience for the particular board

l showing how the skills and experience of thedirectors complement each other

l when reporting on the board evaluation,explaining why a particular conclusion wasreached and what actions arose; not justsetting out the process and reporting theoverall conclusion.

All of this can make a real contribution to buildingthe confidence of stakeholders in the robustnessand effectiveness of the board.

Communicate what makes the companydistinctiveThe business model is part of what makes acompany distinctive — it should capture theessence of the commercial proposition.Establishing the business model is very much partof governance.

Ensure also that challenges and issues in particularindustries are addressed; too many governancereports could be picked up from one annual reportand dropped into the report of another company ina different industry.

Focus on the key messages and use structureto help with thisTo start with, decide on a small number of keymessages for the reader to ‘take away’ andensure that they are clearly communicated. Tohelp do this, think about how the report can bestructured. Consider communicating keymessages separately from the other requireddisclosures and ‘standing data’. This can bedone simply by ‘boxing out’ from the rest of thetext. Increasingly, these messages areintroduced in the chairman’s personal reporting

Business model

RiskStrategy &objectives

Figure1: Towards best-practice reporting: the ‘backbone’ of the annual report

Page 181Corporate governance — towards best-practice corporate reporting

rather than in the main body of the governancereport.

A number of the disclosure requirements in theCode may be met by placing information (such asthe terms of reference of committees) on thecompany’s website. The provisions that allow forthis are listed in Schedule B to the Code.

Towards best-practice reporting of corporategovernanceAchieving good practice in governance reporting isthe first step. Really to build stakeholder confidencemeans tackling matters of importance that arerarely addressed properly in governance reportingor that continue to be particularly sensitive, such assome aspects of remuneration reporting.

The challenge for companies is to move the gameon. The Code and the guidance around it need tobe applied in a wide range of circumstances, sothey do not deal with the ‘content’ of disclosures indetail. This allows companies to add real value;best-practice corporate reporting gets to the heartof what stakeholders want to know andgovernance reporting should be a part of this.

Building confidence in the annual report as awholeFollowing the financial crisis, the FRC has beenbehind two initiatives related to buildingconfidence in not only financial reporting but theannual report as a whole:

Revisions to the CodeAs discussed above, under the FRC’s proposed

revisions to the Code after October 1, 2012,boards will have to set out the basis on which theyconsider that the whole annual report is “fair,balanced and understandable” and “provides theinformation necessary for users to assess thecompany’s performance, business model andstrategy”. If this is to go beyond a description ofprocess, boards will need to disclose the keypoints considered in arriving at their conclusion.

To help them with this, the audit committee is toreport on “the significant issues that it consideredin relation to the financial statements and howthese issues were addressed”. Currently, only afew best-practice reporters discuss the keyjudgements and estimates made by the board inthe preparation of the financial statements; thiswill in future be part of the Code itself.

The Sharman Inquiry into going concern andliquidity risk assessmentsGoing concern disclosures have often beenviewed as a technicality, particularly where thereis no perceived problem within the usual timehorizon of 12 months (in the UK) from the dateof signing the financial statements. Currently,although the FRC issued guidance in 2009designed to improve the quality of going concerndisclosures, relatively few companies have takenthis fully on board.

The Sharman Inquiry, which reported in 2012,signalled a move away from the current model —where a company only highlights going concernrisks when there are significant doubts about theentity’s survival — to one that integrates the

Control RewardPerformance

Post-IP

O c

onsid

era

tions

Page 182 Corporate governance — towards best-practice corporate reporting

directors’ going concern reporting with the otherelements of their discussion of strategy andprincipal risks. It also signalled a move away fromthe current ‘three category model’ for auditorreporting to an explicit statement in the auditor’sreport that the auditor is satisfied that, havingconsidered the assessment process, there isnothing to add to the disclosures made by thedirectors.

These are both real opportunities to buildconfidence in the annual report, and we encouragecompanies to embrace them when they becomeapplicable.

Getting to the heart of what stakeholders wantto know — ‘applied governance’Stakeholders are interested in each element of thecontent ‘backbone’ of the annual report, and theyare also interested in how governance has beenapplied to each of them. But they are notinterested in mere descriptions of process. To buildtheir confidence in the board and in the companyas a whole, stakeholders should be provided withinformation on how governance has been applied.This is not to confuse governance with‘management’ or ‘control’; the focus is on how theboard and its committees have been involved inthe right things, and at the right time.

The particular content of ‘applied governance’disclosures will of course vary from company tocompany and it is beyond the scope of thischapter to go into detail, but we have providedillustrative examples below for each element ofthe backbone.

Business model –people andrelationshipsMany organisations

rely on the expertise of their people, built up overmany years in some cases, leading to closeworking relationships that create value in the

business. In our experience, the importance ofpeople and relationships is seldom recognised inannual reports in any depth, though in suchbusinesses we would expect it to be a highpriority year in, year out for the board andperhaps the nomination committee.

Strategy andobjectives — mergersand acquisitionsactivity

A lot of time is devoted to the financial reportingissues around M&A activity, such as acquisitionaccounting and impairment reviews, and there isgenerally extensive disclosure of underlying andadjusted profitability numbers, exceptionalitems, and even tracking the financial benefit of

Business model

Strategy &objectives

People and relationships: reporting tobuild confidence in the company and the board:l recognition that this is a key feature of the

business modell discussion of employee satisfaction,

including retention and professionaldevelopment

l evidence that there is succession planningand a pipeline of talent

l appropriate recognition of the relationshipbetween diversity in the company andunderstanding the customer base.

M&A activity: reporting to buildconfidence in the company and the board:l the key issues that went to board level l significant risks that the board considered

in relation to the deal (price and terms, forexample)

l how the board is monitoring/drivingsynergies (restructuring decisions, forexample)

l the outcome of post-investment reviews.

Page 183Corporate governance — towards best-practice corporate reporting

synergies. The financial statement disclosuresare often accompanied by commentary in thefront half of the annual report, typically includingsome indication of future developments.However, there is rarely much discussion of howthe underlying decisions and judgements werereached by the board, or of how they continue tomonitor outcomes.

Risk — appetite andmanagementAlthough there hasbeen an improvement

in recent times in the quality of the disclosuresof principal risks and uncertainties in annualreports, there is rarely any meaningfulconnection between these disclosures and thegovernance of risk. This is despite the re-emphasis of the board’s responsibility for risk inthe Code (see the panel above).

This reworded principle focuses on ‘risk appetite’without using the specific term. In the narrativedisclosures of how the main principles of the Codehave been applied, it is therefore particularlyimportant to focus on this aspect of risk, which isthe key link between risk and strategy and verymuch a board responsibility.

The Turnbull Guidance, published by the FRC inOctober 2005, provides more information on howthe board’s responsibilities around risk

management and internal control should beaddressed. However, it has not tended to generatedisclosures that cover everything stakeholderswould be interested in.

Example — supply chain governance. Anexample of how reporting could be improved isgovernance of the supply chain, which isfundamental to the operation of companies andis frequently partially outsourced or dependenton joint ventures or associates. This brings withit a number of governance challenges that arerarely addressed in the annual report. TheTurnbull Guidance requires disclosure wherejoint ventures or associates are excluded fromthe risk and internal control systems of thegroup but nothing more specific than this. Thereis also a tendency for such issues to be seen as‘below board level’ and not part of thegovernance to which the annual reportdisclosures relate.

To build confidence in the company and theboard, reporting might detail how a decision tooutsource or place reliance on a third party wasseen by the board as consistent with thecompany’s risk appetite. It could also addressthe question of what the board has done tomake sure it’s clear where the responsibilities ofthe company stop and start — avoiding the riskof ‘falling between stools’.

Risk

“The board is responsible for determining thenature and extent of the significant risks it iswilling to take in achieving its strategicobjectives. The board should maintain soundrisk management and internal controlsystems.”FRC: UK Corporate Governance Code, MainPrinciple C.2

Risk appetite and management: reportingto build confidence in the company and theboard:l how the board engineers ‘risk resilience’

into the company, including resilienceagainst ‘black swans’, or unforeseen riskevents

l how risk is measured and reported to theboard and how governance is applied to it.

Board responsibility for risk

Post-IP

O c

onsid

era

tions

Page 184 Corporate governance — towards best-practice corporate reporting

Control — group andsubsidiarygovernanceAnnual report

governance disclosures tend to focus on the group,but there can be a disconnect between the groupgovernance structures and those that operate in(often very significant) individual territories. This canlead to a lack of clarity around responsibility formatters that do not map easily to the groupstructure, such as local legal or regulatoryrequirements (including tax and pensions), andalso to uncertainty as to the responsibilities ofdirectors in local statutory entities.

Control — anti-bribery measuresThe UK Bribery Act 2010 came into force inthe middle of 2011 after much initialuncertainty and delays in guidance on theexpectations for ‘adequate procedures’. With itswidening of liability to those acting on acompany’s behalf worldwide, the Bribery Act

represents a major source of ongoingreputational risk that boards should bemeasuring and managing.

Many companies currently note that processeshave been put in place (as the Bribery Actrequires) but few provide disclosures beyond thebare facts.

Performance —governance over non-financialmeasures

Non-financial measures are intrinsically bound upwith governance, and this will become moresignificant as corporate reporting moves towardsintegrated reporting, driven by initiativeslaunched by groups like the InternationalIntegrated Reporting Council to link financial

performance with non-financial areas such as theenvironment and corporate social responsibility.A number of companies are already providingperformance statements on environmentalissues such as the consumption of finiteresources.

As these developments continue, stakeholders willbecome more and more interested in how theboard has engaged with them.

Group and subsidiary governance:reporting to build confidence in the companyand the board:l how the structure of the group/business

maps to territories or legal entitiesl how the governance structures inter-relatel an outline of where responsibilities lie.

Anti-bribery measures: reporting to buildconfidence in the company and the board:l how the board tracks the group’s response

to the new anti-bribery regime — is it partof ongoing monitoring?

l continuous reassessment of the risksbased on experience.

Governance over non-financial measures:reporting to build confidence in the companyand the board:l Does the board consider these issues

throughout the elements of the ‘backbone’of the annual report, from business modelto reward?

l Are the issues dealt with by the board orare they wholly delegated to asubcommittee?

Control

Performance

Page 185Corporate governance — towards best-practice corporate reporting

Reward — reportingremunerationThe reporting ofdirectors’ reward is part

of the ‘backbone’ of the annual report, and there is aparticular focus on its alignment with the rest of thatbackbone. This alignment is a key concern for manyinvestor groups, including proxy advisers, whoregularly recommend that shareholders vote againstor consider withholding their votes on theremuneration report at the annual general meeting. Inrespect of the remuneration policy part of the report,this is to change to a binding vote from 2013, when itis planned that the Enterprise and Regulatory ReformAct will come into force.

Companies’ remuneration policies will come undereven more scrutiny and careful disclosure will beone way to avert a crisis. It is certainly not inanyone’s interest to create uncertainty, which maygive rise to unnecessary questions.

Reporting for newly listed, Standard Listed andsmaller listed companiesA number of specific challenges can arise fornewly listed or smaller listed companies, thoughsome of these may also apply to any company.

Newly listed companiesAlthough adequate financial reporting proceduresshould be in place prior to listing, it may take timefor companies to work towards full compliancewith the Code (or compliance to the extentthought appropriate for the particularorganisation).

As all Premium Listed companies must now applythe Code, those that are incorporated overseasand are therefore accustomed to other governanceframeworks may take time to adjust theirarrangements. This may result in a need to explainmore departures from the Code than is the casewith other companies and — for those provisionsof an ongoing nature where arrangements wereput in place during the year — the periods of non-compliance and compliance.

We recommend that this is done clearly in thegovernance report, with areas of non-complianceat the end of the period being identifiedseparately. Strictly speaking, all instances of non-compliance for provisions of an ongoing natureshould be included in the compliance statementrequired under Listing Rule 9.8.6 (6), but webelieve that it is adequate for them to bementioned in the narrative statement under LR9.8.6 (5), provided that the non-compliance isclearly described and the compliance statementidentifies those provisions that have still not beencomplied with at the end of the period.

Remuneration: reporting to buildconfidence in the company and the board:l showing that the remuneration committee

and its chairman have been active duringthe course of the year, including takingadvice from appropriate parties andengaging with stakeholders on a timelybasis

l being clear about the performance-rewardlink in all variable elements of remuneration,and particularly the alignment of thatperformance with business objectives

l providing clear disclosure of amountsearned in the year and the entitlements forfuture years

l dealing head-on with specific known issues— especially where these have been raisedby shareholders

l recognising any industry-specificchallenges, and discussing how they havebeen addressed, but being careful not toimply over-reliance on market benchmarks

l dealing with the remuneration of senioremployees below board level

l clear disclosure of potential or actualexposure to compensation for loss of office.

Reward

Post-IP

O c

onsid

era

tions

Standard Listed companiesAlthough Standard Listed companies (regardlessof their place of incorporation) do not have toreport against the Code under the Listing Rules, ifthey apply any code (one applicable in theircountry of incorporation, for instance) on either avoluntary or mandatory basis, they must reportagainst it to comply with the Disclosure andTransparency Rules.

Smaller quoted companiesThe Quoted Companies Alliance (QCA) issuesguidelines for smaller quoted companies on howthey may implement the Code appropriately. TheCode still applies to all Premium Listed companies,and the only relaxations from it are for thoseprovisions that the FRC has applied exclusively toFTSE 350 companies, mainly around thecomposition of audit and remunerationcommittees, the re-election of directors andexternal facilitation of board performance.

Our recommendation is that smaller companiesaim to implement the Code to the extent that itapplies to them, and refer to the QCA guidelineswhere they believe that a specific provision doesnot suit their circumstances.

Page 186 Corporate governance — towards best-practice corporate reporting

Where appropriate, companies should take intoaccount the FRC’s February 2012 guidance onthe three elements of a meaningful explanation:

“It should set out the background, provide aclear rationale for the action it is taking, anddescribe any mitigating actions taken to addressany additional risk and maintain conformity withthe relevant principle. The explanation shouldindicate whether the deviation from the Code’sprovisions is limited in time and, if so, when thecompany intends to return to conformity with theCode’s provisions.”

‘Comply or explain’: explanations

PricewaterhouseCoopers LLP 1 Embankment Place, London WC2N 6RHTel +44 20 7583 5000Fax +44 20 7822 4652 Web www.pwc.co.uk

John PattersonConsultant, Assurance Risk & Quality, LondonEmail [email protected] Patterson works in a consultant role oncorporate governance matters within theAssurance Practice of PwC, providing adviceand updates on corporate governancedevelopments to client management andboards as well as to PwC teams. He has 15years’ experience with UK public companies,including AIM, small cap and mid tierorganisations.

Much of Mr Patterson’s work focuses onthe reporting of corporate governance, andhe has contributed to a number of PwC’spublications on corporate reporting. He hasalso developed the firm’s responses toconsultations from the Financial ReportingCouncil, the UK government and theEuropean Commission, including revisions tothe FRC’s UK Corporate Governance Code.

���������������������� � � � � � � � � � � � � � � � � � � �� � � � �

Published by White Page Ltd, in association with the London Stock Exchange, ‘CorporateGovernance for Main Market and AIM Companies’ aims to encourage companies and executivesto consider corporate governance in the widest sense, including board efficiency, transparency,reporting requirements, investor communications and sustainability.The wealth of expert insightsfrom professionals in this publication’s 27 chapters is therefore an invaluable resource.

The information in this publication is not offered as advice on any particular matter and must not be treated as asubstitute for specific advice. In particular, information in this publication does not constitute legal, professional,financial or investment advice. Advice from a suitably qualified professional should always be sought in relation to anyparticular matter or circumstances. The chapters provided by the contributors are not the opinions of the London StockExchange plc or any of its group undertakings (‘group undertakings’ shall be construed in accordance with Section 1161of the United Kingdom Companies Act 2006). This publication is provided for information and educational purposesonly. While all information contained herein is obtained from sources believed to be accurate and reliable, neither theLondon Stock Exchange plc nor any of its group undertakings accepts responsibility for any errors, omissions, orinaccurate information. All information in this document is provided ‘as is’ without warranty of any kind. Neither theLondon Stock Exchange nor any of its group undertakings make any representations and disclaims all express, impliedand statutory warranties of any kind in relation to this publication, including warranties as to accuracy, timeliness,completeness, performance or fitness for a particular purpose.

The London Stock Exchange crest and logo, AIM, RNS and SETS are registered trade marks of London Stock Exchangeplc. No part of these trade marks or any other trade mark owned by the London Stock Exchange or any of its groupundertakings can be used, reproduced or transmitted in any form without express written consent by the owner of thetrade mark.

Published by White Page Ltd (www.whitepage.co.uk) © London Stock Exchange plc, 2012

Copyright in individual chapters rests with the authors. No photocopying: copyright licences do not apply.

To view the book in which this chapter was published, or to download iPad andKindle-compatible editions, please go to

www.londonstockexchange.com