corporate plan 2015-2019 - hfa plan 2015-2019 sixteenth edition | june 2015 . ... fostered by the...

TRANSCRIPT

F:\Data\Board Papers\2015\June\Paper3 Appx - Corporate Plan 2015-2019.docx

Corporate Plan

2015-2019

SIXTEENTH EDITION | JUNE 2015

Contents

CONTENTS ........................................................................................................................................................... I

TERMS OF REFERENCE ........................................................................................................................................ II

PART I: INTRODUCTION AND OVERVIEW ............................................................................................................ 1

1. FUNCTIONS AND MISSION ............................................................................................................................ 1 2. THE ECONOMIC AND FISCAL ENVIRONMENT ............................................................................................... 2 3. THE HFA’S STRENGTHS ................................................................................................................................. 2 4. SUMMARY OF THE HFA’S FINANCIAL POSITION ........................................................................................... 4

PART II: POLICY FRAMEWORK - LENDING ........................................................................................................... 5

5. SOCIAL HOUSING STRATEGY 2020 ................................................................................................................ 5 6. LOAN ADVANCES AND REDEMPTIONS .......................................................................................................... 6 7. INTEREST RATES .......................................................................................................................................... 10 8. RESEARCH ................................................................................................................................................... 11 9. MORTGAGE ARREARS RESOLUTION PROCESS (MARP) ............................................................................... 11

PART III: POLICY FRAMEWORK – FUNDING ....................................................................................................... 12

10. THE HFA’S STATUTORY BORROWING LIMIT ................................................................................................ 12 11. THE HFA’S STATE GUARANTEE .................................................................................................................... 12 12. FUNDING (GOVERNMENT GUARANTEED) .................................................................................................. 12 13. OTHER FUNDING ........................................................................................................................................ 14 14. REVIEW OF EXISTING DEBT ......................................................................................................................... 14 15. REFINANCING OF MATURING DEBT ............................................................................................................ 14 16. OPERATIONAL CONSIDERATIONS ............................................................................................................... 15

PART IV: RISK MANAGEMENT AND PROJECTED ACCOUNTS, 2015-2019 ........................................................... 16

17. OBLIGATION ON THE HFA TO MEET ITS COSTS FROM ITS OPERATIONS ..................................................... 16 18. RISK MANAGEMENT FRAMEWORK & POLICY ............................................................................................. 16 19. RISK IN THE HFA’S LOAN BOOK ................................................................................................................... 17 20. PROJECTED ACCOUNTS ............................................................................................................................... 19 21. DIVIDEND POLICY ........................................................................................................................................ 21

PART V: CUSTOMER SERVICE ............................................................................................................................ 22

22. CUSTOMER GROUPS ................................................................................................................................... 22 23. CUSTOMER SERVICE INITIATIVES ................................................................................................................ 22 24. PERFORMANCE CRITERIA ........................................................................................................................... 24 25. MONITORING ............................................................................................................................................. 25

PART VI: CORPORATE GOVERNANCE AND ADMINISTRATION ........................................................................... 26

26. CORPORATE GOVERNANCE ........................................................................................................................ 26 27. INTERNAL COMMUNICATION ..................................................................................................................... 26 28. CHANGE AND MODERNISATION ................................................................................................................. 26 29. ADMINISTRATION COSTS ............................................................................................................................ 28 30. FREEDOM OF INFORMATION ...................................................................................................................... 29

PART VII: CONCLUSION ..................................................................................................................................... 30

31. GOALS FOR THE PERIOD 2015 TO 2019 ....................................................................................................... 30 32. PERFORMANCE MEASUREMENT ................................................................................................................ 30

ANNEX 1: EVOLUTION AND DEVELOPMENT OF THE HFA SINCE ITS FOUNDATION IN 1982 ............................... 31

ANNEX 2: PROJECTED ACCOUNTS 2015-2019 ................................................................................................... 34

ANNEX 3: SENSITIVITY ANALYSIS ...................................................................................................................... 36

Terms of Reference

The Corporate Plan is drawn up in conformity with the Code of Practice for the Governance of State Bodies (Sections 2.12, 2.14 and

2.15).

The HFA’s Policies and Procedures Manual, states (paragraph 7.2.2):

A corporate plan, based upon projected accounts

covering a five year period shall be developed by the HFA within the framework of its objectives set out by

statutes and circulars from the Minister of the

Environment, Community & Local Government and the Minister for Public Expenditure & Reform. A copy of

the draft Corporate Plan should be sent to the Minister before the plan is finalised and adopted by the Board.

Views which the Minister/Department wishes to have reflected in the final plan should be made known to

the HFA within a maximum period of six weeks of submission. While final responsibility for the content of

the plan rests with the Board in each case, the views of the Minister and consideration of the public interest

should be carefully weighed by the Board.

The plan should reflect management’s assumptions

regarding: inflation;

bad debt provisions;

advances to local authorities; margins on income related/index linked loans;

the funding programme for the period, taking into account new funding, the refinancing of existing

debt and the debt maturity profile; the matching of the HFA’s assets and liabilities so

as to minimise risk; provision of adequate reserves to meet future

known risk; any other relevant matters.

The responsibility for final approval of the Corporate

Plan rests with the Board.

The Corporate Plan will be amended on an ongoing basis to reflect change as it arises.

1

PART I: INTRODUCTION AND OVERVIEW

This part of the Plan sets out the HFA’s function, its mission and its strengths,

and graphically summarises its financial history. The HFA’s evolution is set out in ANNEX 1.

1. FUNCTIONS AND MISSION

1.1 The HFA’s function is to advance loan finance to local authorities and the

Voluntary Housing Sector (“approved housing bodies” or “AHBs”) to be used by them for any purpose authorised by the Housing Acts, and to borrow or

raise funds for these purposes.

1.2 The HFA does not formulate housing policy – that is the preserve of the Minister and the Government. The HFA’s role is to provide appropriate

funding for the schemes and projects decided upon and established by the Minister and the Government. The HFA has substantial funding available at

market-leading interest rates, to enable our customers provide the social housing needed by the communities they serve.

1.3 The HFA does not lend directly to individuals or households. In relation

to local authorities the HFA is, in effect, a centralised borrower on their

behalf. It block-lends to the local authorities, and they, in turn lend at individual level, having added a margin to cover their administrative and risk

costs in so doing. The HFA sets its interest rates at a level that will enable it, taking one year with another, and taking account of risk, to achieve a

break-even result.

1.4 The HFA is required by the Housing Finance Agency Act, 1981 to meet its costs from its operations, and this it does. The HFA does not receive any

Exchequer grant or subvention.

1.5 The HFA is subject to oversight by the Ministers for the Environment, Community & Local Government, Public Expenditure & Reform, and Finance,

and review by the Joint Oireachtas Committee on the Environment, Transport, Culture and the Gaeltacht.

2

2. THE ECONOMIC AND FISCAL ENVIRONMENT

The testing economic and fiscal environment within which Ireland finds itself

will affect the State’s ability to resource housing, where needed, in the years ahead. In addition, the level of housing support required will be influenced

by asset values and their direction, affordability, the willingness and capacity

of the private sector to commit funds to housing, whether through households, local authorities or AHBs. From the HFA’s viewpoint, the

outcome is likely to be continued low levels of lending in the years ahead. The HFA’s business planning has always assumed very low levels of net new

lending per annum. In 2014 the HFA’s net redemptions were €144 million. In the current climate, therefore, the HFA has prepared projections based on

nil net loan advances for 2015 and €100 million per annum thereafter for the period 2016 to 2019.

The HFA raises the majority of its funding via the National Treasury

Management Agency (NTMA) through the HFA’s Guaranteed Notes (GN) programme. In 2014 the programme was amended to permit deal maturities

up to 10 years, to increase the size of the programme from €4.5bn to €5bn, and to facilitate floating rate issuance.

With the cooperation of the NTMA, the HFA extended the average maturity profile of its funding from 2.8 months to 3.2 years. This provides a more

stable funding base that more closely reflects the long-term weighted-average life of the asset base (c.15 years) and significantly reduces the

HFA’s short-term liquidity risk. This funding has been benchmarked against Euribor®, and the increased tenor was negotiated with the NTMA at no

increased cost to the HFA. Details are set out in Part III.

3. THE HFA’S STRENGTHS

3.1 The HFA’s position, under the aegis of the Department of the Environment, Community & Local Government (“DoECLG”) ensures

co-ordination and execution of housing policy and finance initiatives. This gives the Minister direct control over the determination, implementation and

financing of housing policy. It makes sense that all arms of housing should

be under the control of the appropriate Government Minister. This arrangement has worked very well in practice. The HFA, with Board

approval, in February 2014 entered into a Service Level Agreement (“SLA”) with the DoECLG, which includes specified’ key deliverables’ for

implementation. This SLA was renewed and updated in February 2015, with Board approval (see the HFA website for further details).

3

3.2 The HFA’s relationship with local authorities ensures that they are

kept informed and advised on all aspects of housing finance. The HFA has a well-developed 30 year working relationship with local authorities involving

key staff such as Chief Executives, Heads of Finance and Housing Officers. In particular, the HFA has a close relationship with Heads of Finance,

including a standing invitation to their representative meetings. The HFA

makes regular presentations to them on a wide range of financial, market and housing-related issues. Advice - formal and informal - is also given in

an atmosphere of trust and discretion. At Board level, this relationship is fostered by the presence of a local authority Chief Executive and an elected

representative.

3.3 The HFA’s relationship with AHBs The HFA engages actively with the Voluntary Housing Sector to provide the

necessary support and assistance to facilitate their applications for Certified Body status and to ensure individual loan applications are prepared and

submitted in a manner that will enable them to meet the necessary criteria for approval. In addition the HFA is working closely with the Sector to

support their access to alternative sources of financing.

In 2014, the HFA increased its number of Certified Bodies from six to twelve,

and approved 21 housing projects totalling €27 million. Further, the HFA also introduced finance for ‘Mortgage-to-Rent and ‘New-Build’ projects, and

it is anticipated that we will see significant growth in these areas in the life of the Plan.

3.4 The HFA’s structure as a plc. and its legislative remit to operate

on at least a break-even basis means that the financing of housing policy initiatives are assessed by reference to commercial, as well as social,

criteria. Within this context, the HFA has built up reserves adequate to manage the risks in its business, while delivering value to its customers.

4

4. SUMMARY OF THE HFA’S FINANCIAL POSITION

24 3 14 20 14

56 59

73

93 106

0

20

40

60

80

100

120

2010 2011 2012 2013 2014

€m Surplus/Deficit & Reserves 2010-2014

Surplus/Deficit Closing Reserves

4,448 4,358 4,441 4,329 4,185

0

1,000

2,000

3,000

4,000

5,000

2010 2011 2012 2013 2014

Balances due on advances 2010-2014

396

293 327

139 153

(144) (109)

70

(120) (144)

(200)

(100)

0

100

200

300

400

500

Gross and net advances 2010-2014

Gross advances Net advances

€mm

€m

5

PART II: POLICY FRAMEWORK - LENDING

2014 was a significant year in the development of a strong and sustainable

social housing sector in Ireland. With the publication of Social Housing Strategy 2020 in late November, the Government gave a clear commitment

to provide a flexible, progressive and targeted system of social housing

supports over the next six years and set out a firm foundation for a carefully calibrated, multi-annual investment programme to prioritise the provision of

social housing in the years to 2020.

The Housing Finance Agency (HFA) has a central role to play in the implementation of the Strategy through our representation in the

governance structure and our ongoing commitment to providing the most efficient and best value finance possible to our customers. We continue to

forge mutually beneficial relationships with new customers to enable them to provide housing to individuals and families who cannot secure

accommodation from the market. The HFA’s Board is drawing up a “Statement of Strategy”, in conjunction

with Government’s social housing strategy, and plans to finalise this later in 2015.

5. SOCIAL HOUSING STRATEGY 2020

5.1 There are three central Pillars in this Strategy:

Pillar 1: Provision of New Social Housing Supply

Pillar 1 of the Strategy targets the delivery of 35,000 new social housing

units over the period to 2020. The cost to the Exchequer of building, acquiring or leasing these 35,000 units is estimated over the period to 2020 to be €3.8bn.

Pillar 2: Providing Housing Supports Through the Private Rental Sector

Pillar 2 focuses on the delivery of social housing supports provided through the private rental sector. The overall tenure mix of housing is changing, with

rental increasing strongly as a share of the total, especially in Dublin and other cities. Supply pressures and consequential rising rents increase

demands on Exchequer funding for those tenants supported through the Rental Accommodation Scheme (RAS), the Housing Assistance Payment

(HAP) and Rent Supplement (RS).

6

Pillar 3: Reform Creating More Flexible and Responsive Social Housing Supports

Pillar 3 includes a range of actions to ensure that social housing supports are responsive to people’s current needs, as well as to improvements in their

circumstances.

6. LOAN ADVANCES AND REDEMPTIONS

The policy objective is to ensure that the projections of loan advances are

estimated in a conservative manner and tie in with the HFA’s projected accounts and risks models.

6.1 Estimating the annual net level, and type of, advances to be

made by the HFA. The net level of loans advanced by the HFA in any year is determined mainly by a combination of the following factors:

the number of mortgages advanced by the local authorities, which in turn is heavily influenced by Government policy, the external economic

environment and the capacity of the private sector to take on risk; the average loan size;

the amount of funding required by local authorities and AHBs for their social housing programmes, other than mortgages;

internal resources available to local authorities and AHBs from loan redemptions; and

the level of redemptions and normal-course annuity capital repayments.

6.2 The HFA’s loan book currently falls into three interest rate categories

i.e. variable rate, index linked and fixed rate loans.

6.2.1 Variable rate loans account for the vast bulk (about 95%) of HFA lending; it is expected that most new lending over the Plan period will be in

this category. The following sets out the type of lending that is expected to

fall into this category over the life of the Plan.

Leasing of social housing by the DoECLG through voluntary housing bodies:

The DoECLG leases houses from Approved Housing Bodies (voluntary bodies and co-operatives) (AHBs), which are rented to social housing tenants

nominated by local authorities. Houses are either bought or built by AHBs and financed by loan finance raised by the AHB, with a guaranteed revenue

stream via a lease taken out by the DoECLG for a period of up to 30 years.

Under Section 17 of the Housing (Miscellaneous Provisions) Act 2002, the HFA is empowered to lend directly to AHBs.

Lending to AHBs incurs a greater level of risk than lending to local authorities and requires a different level of assessment and due diligence. To

support the assessment process the services of an independent financial assessment firm has been engaged, and a Credit Committee has been

established to assess all applications and monitor borrowers on an ongoing

7

basis. The Credit Policy assists the HFA in identifying and managing the risks associated in lending to AHBs. The Credit Policy was approved by the Board

in 2013 and updated at the September 2014 Board meeting.

AHBs initially apply for Certified Body status which assesses their suitability for lending purposes by examining their financial accounts over three years,

their corporate governance structure and their financial and development plans.

Only when the AHB’s Certified Body status has been confirmed can they

apply for loan advances, which are subsequently assessed.

The HFA’s Credit Committee - consisting of board members and senior management, and advised by outside consultants - met nine times during

2014.

Other schemes expected to be variable-rate funded over the life of the Plan include house purchase annuity loans, infrastructure loans to

local authorities for water, waste and environmental purposes and lending to approved housing bodies (AHBs):

- under Section 17 of the Housing (Miscellaneous Provisions) Act 2002 - and community facilities related to housing provision under Section

11 of the Housing (Miscellaneous Provisions) Act 2009.

6.2.2 Index linked loans. There are two loan types involved:

Income Related Loans: No new loans are advanced in this category. These loans stood at €13m outstanding on 31 December 2014. Due to

redemptions, they are likely to fall to an estimated €10m by 2019.

Shared Ownership rental loans: In line with the Government decision to stand down the Shared Ownership Scheme as set out in the housing policy

statement, it is expected that no new loans in this category will be advanced over the life of the Plan. The rental element of these loans falls into two

categories, those advanced pre and post 1 January 2003. Loans advanced

prior to 2003 are charged at an annual coupon rate of 3.80%. Shared Ownership lending advanced since 1 January 2003 is funded by variable rate

debt; the interest rate charged being the local authority variable mortgage rate. The rental balance outstanding at 31 December 2014, for each

category, was €102m and €164m, respectively.

Following on from the redemption of the index linked bond which financed the index related Shared Ownership loans it is intended to reconfigure the

rate charged on these loans to be the same as the current HFA variable mortgage related interest rates. This will be discussed with both the DOECLG

and representatives from the local authorities.

8

6.2.3 Fixed rate loans

Fixed rate 10% loans: No new loans are advanced in this category. The HFA was required by Government in 1986 to make 10% fixed rate 30-year

loans available to local authorities. The HFA structured the underlying debt to fund these advances in the context of the conditions - financial and legal -

pertaining in 1987/88 and reasonably seen to be continuing. As of end-

December 2014, the HFA had €12m of 10% fixed rate advances made to local authorities, funded by a fixed rate bond. Early redemption without

penalty was introduced in June 1989, by Government, only after the bond issue and advances were made. The bond is not prepayable without penalty.

The HFA’s risk model takes account of the significant exposure on these loans, which will cease in 2018 on the maturity of the underlying bond.

Other fixed rate loans: The HFA funds 5-year fixed rate loans for

affordable housing and tenant purchase schemes. These amounted to €15 million outstanding as at 31 December 2014. It is expected that few net

new advances will be made in this category during the life of the Plan.

The HFA also offers a 10 year fixed rate product to AHBs, however given the general view that interest rates will remain low for an extended period there

has been no uptake of this product. The fixed rate offering is expected to

continue for the life of the plan with rates reviewed at regular intervals and benchmarked against Government yields and interest rate swap levels. A

significant increase in activity is not expected as long as expectations of an increase in interest rates remain subdued.

6.3 Projected net loan advances

The HFA categorises its business into two broad areas – mortgage business,

which accounts for €1.2 billion at end-December 2014 (30% of its total); and non-mortgage, which was €3.0 billion at end-December 2014 (70% of

the total).

Of the mortgage-related business 89% are variable rate annuity loans, 9% are older income-related loans and shared ownership loans and 2% are fixed

rate loans. In total, these schemes lend to over 22,000 households.

9

Non-mortgage business covers the wholesale aspects of housing by local

authorities, such as support for the voluntary housing sector through the Capital Loan and Subsidy Scheme, land acquisition, bridging finance and

projects ancillary to and supportive of housing. It also includes a small, but important, amount of finance for projects in the water services, waste and

environmental areas under the provisions of the Housing (Miscellaneous

Provisions) Act 2002. To conform to EU State Aid rules, borrowing in this area is not guaranteed by the State. The price of the debt raised has been

somewhat higher than that on guaranteed borrowings. Nevertheless, by accessing block funds from the European Investment Bank and the Council

of Europe Development Bank, individual projects deemed too small for direct borrowing have been able to benefit from the fine rates available from these

large supranational organisations. It is unlikely that, in current circumstances, unguaranteed funds will be available for further projects.

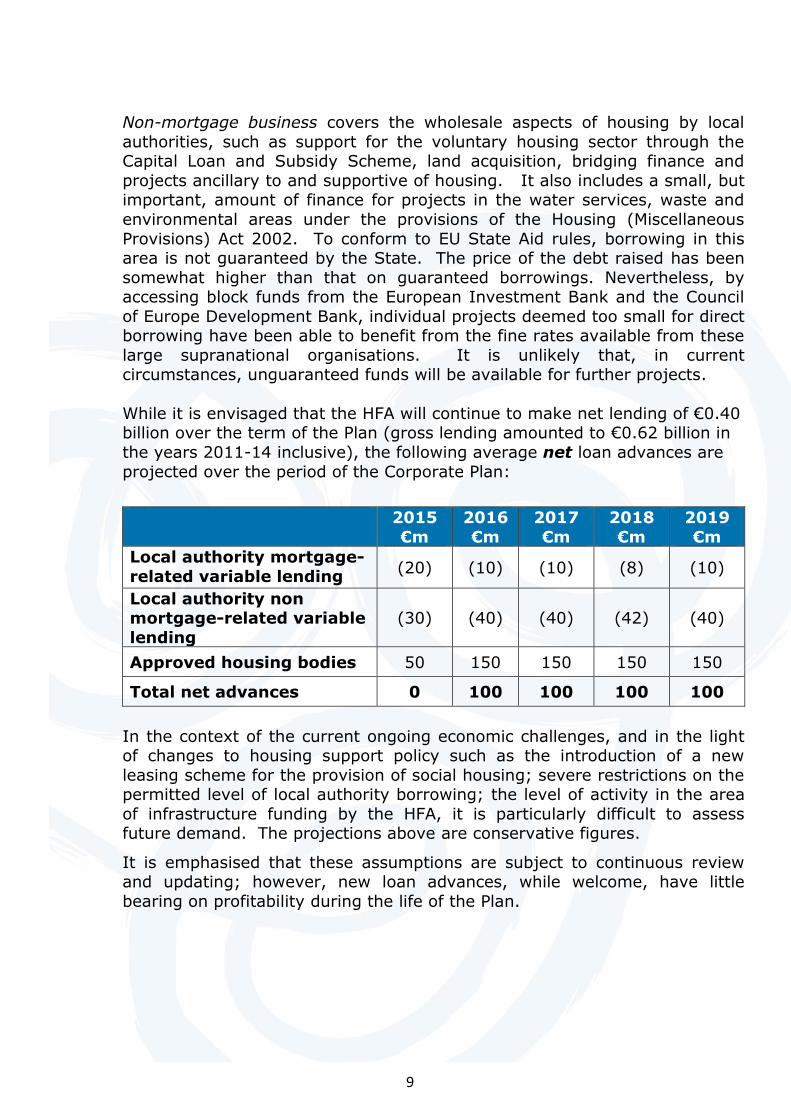

While it is envisaged that the HFA will continue to make net lending of €0.40 billion over the term of the Plan (gross lending amounted to €0.62 billion in

the years 2011-14 inclusive), the following average net loan advances are

projected over the period of the Corporate Plan:

2015

€m

2016

€m

2017

€m

2018

€m

2019

€m

Local authority mortgage-

related variable lending (20) (10) (10) (8) (10)

Local authority non mortgage-related variable

lending

(30) (40) (40) (42) (40)

Approved housing bodies 50 150 150 150 150

Total net advances 0 100 100 100 100

In the context of the current ongoing economic challenges, and in the light of changes to housing support policy such as the introduction of a new

leasing scheme for the provision of social housing; severe restrictions on the permitted level of local authority borrowing; the level of activity in the area

of infrastructure funding by the HFA, it is particularly difficult to assess future demand. The projections above are conservative figures.

It is emphasised that these assumptions are subject to continuous review and updating; however, new loan advances, while welcome, have little

bearing on profitability during the life of the Plan.

10

7. INTEREST RATES

The policy objective is to advance loans to households, local authorities and

the voluntary housing sector at the finest interest rates consistent with public policy and the financial stability of the HFA.

7.1 Mortgage related rates: The HFA, while not directly competing with

financial institutions, is mindful of pricing its loans at a rate that is cost-efficient for local authorities. The HFA has to achieve this in an environment

of meeting the social and financial objectives set by Government, supplying funds for lower-income households, and funding its costs from its

operations. The HFA continues to offer excellent value to its customers. Households benefit from an HFA-generated house purchase annuity

mortgage rate that remains about 1.75% below the average standard

variable rates in the market.

7.2 Non-mortgage related rates: Local authorities also benefit from a very cost-effective interest rate on their non-mortgage housing-related

borrowings from the HFA. This is priced off the HFA’s cost of funds. Where local authorities borrowed for non-mortgage purposes, the interest rate over

2014 averaged 2.00%. It is projected that non-mortgage variable lending rates will average 1.75% over the life of the Plan. The HFA is now offering 5

year and 10 year fixed rate lending for Section 11 at rates of 2.75% and 3.25% respectively.

7.3 Interest rate prospects: The absolute rates charged to households and local authorities over the Plan period will depend upon (a) the general

level of rates (i.e. ECB rates) in the market; (b) the costs of funding

generated via the NTMA; and, (c) the cost of borrowing raised from other sources. The projections in this plan are cost neutral in terms of funding.

7.4 New Lending: A new finance contract was agreed in December 2014,

jointly backed by the Housing Finance Agency and the European Investment Bank. It is intended that this will enable an additional 2,000 social housing

units to be developed over the next three years. The €150m funding from the European Investment Bank will be matched by the HFA to make €300m

available for lending to support investment by approved housing bodies across the country to upgrade social housing and improve energy efficiency.

7.5 AHB Lending: The HFA reduced the 10 year fixed rate offering to AHBs

to 3.85%, for non EIB supported financing up to a maximum of €100 million. The HFA commenced lending for Mortgage-to Rent and New Build projects.

The HFA now offers a 25 year fixed rate to AHBs at a rate of 3.25%.

11

8. RESEARCH

The policy objective is to assist in the carrying out of research in the field of housing or related areas in the course of the Plan, as required by the Board.

Under its Articles of Association, the HFA is empowered to engage in

research in areas related to housing. The HFA will, within expenditure

constraints, assist in the carrying out of research in the field of housing or related areas in the course of the plan as required by the Board, or

requested by the DoECLG/local authorities.

9. MORTGAGE ARREARS RESOLUTION PROCESS (MARP)

The introduction of a MARP premium by the Department of Environment, Community and Local Government to support local authorities in extending

MARP options to certain distressed local authority borrowers.

In 2012 all local authorities were required to put in place a Mortgage Arrears

Resolution Process and it was recognised that costs will arise for local authorities as a result of the options required to be made available to certain

distressed borrowers as arrears cases were resolved. The DoECLG and local authorities decided to apply the MARP premium to all existing and new

variable rate loans from 1 October 2012. At 1 January 2014 the MARP

premium was 0.80%. This charge is deducted at source by the HFA through its six-monthly billing statements in January and July each year.

As requested by the DOECLG, funds derived from this premium are held

centrally in a County and City Management Association (CCMA) MARP investment account, managed by the HFA. The HFA is not involved in the

administration of the MARP Fund, and the HFA’s only involvement in MARP is to collect the MARP premium and release payments on the instructions of

the Adjudicating Panel.

To date, €10.25 million has been released to local authorities, from the Fund. The MARP Fund had an accrued value, as at 31 March 2015, of €2.1

million and, based on current collection rates from local authorities (0.80% of the mortgage loan book), the Fund accumulates circa €10 million per

annum.

12

PART III: POLICY FRAMEWORK – FUNDING

This part of the Plan sets out the funding framework and details the amount of debt to be raised and refinanced over the Plan period.

10. THE HFA’S STATUTORY BORROWING LIMIT

The policy objective is to ensure that the limit is at a level that will enable the HFA to fund its operations efficiently.

The limit is €10 billion, as set out in the Housing (Miscellaneous Provisions)

Act 2009. It is envisaged that this will remain the limit during the currency of the Plan.

11. THE HFA’S STATE GUARANTEE

The policy objective is to ensure that the HFA has appropriate EU sanction for the use of the Ministerial guarantee on its debt.

By EU Commission decisions received in July 2001, June 2004 and December 2005, the HFA’s State guarantee on its borrowings in respect of social

housing provision, direct lending to approved housing bodies and provision of infrastructure ancillary to social housing has been cleared as compatible

with the EU treaties and law. The HFA’s lending under Section 17 of the Housing (Miscellaneous Provisions) Act 2002 is funded by unguaranteed

borrowing, for which EU state aid sanction is not required.

12. FUNDING (GOVERNMENT GUARANTEED)

The policy objective is to raise funds on the most favourable conditions and

terms, and in instruments which will be most appropriate for the HFA’s business needs.

12.1 Variable rate funding: Variable funding accounts for 93% of the

HFA’s funding requirement and following the redemption of the indexed linked bond in April 2015 will rise to around 98%. Historically the HFA’s €6

billion eurocommercial programme (ECP) and its €5.0 billion Guaranteed Notes (GN) programme has provided a stable source of funding, however

more recently, access to ECP funding has been very limited.

Following the recent restructuring of the HFA’s debt profile via the issue of

€2.8 billion of floating rate notes with the NTMA, this revised approach to funding management is consistent with the actions being taken across

financial markets as banks and regulators act on the lessons learned from the crisis, particularly with respect to liquidity and funding risk. This had the

effect of extending the average maturity profile of the HFA’s funding from 2.8 months to 3.2 years. This provides a more stable funding base that more

13

closely reflects the long-term weighted-average life of the asset base (c.15 years) and significantly reduces the HFA’s short-term liquidity risk.

A weighted-average maturity profile of three to five years for the HFA,

relative to the asset profile, represents a prudent approach to funding. This allows us to continue providing very competitive lending rates to our

customers, with corresponding benefits for their customers and tenants.

A total of €3.80 billion was drawn by the HFA under the GN programme at

31 December 2014, of which €3.15 billion was funded by NTMA GNs, the balance being investment of short-term surplus funds by local authorities

and the Environment Fund.

As the majority of the HFA’s funding needs continue to be provided through its GN programme, the €6 billion currently available through our

eurocommercial paper (ECP) programme is more than is necessary. We plan to reduce this to €1 billion in 2015.

12.2 It is the HFA’s intention to continue to monitor the possibility of raising

medium term funds from sources other than the NTMA such as supranational institutions, banks and other market participants, possibly through new

financing structures and special purpose vehicles. To this end the HFA has

begun engaging with market participants to explore opportunities and assess market interest in such structures.

In February 2015 the Minister for the Environment, Community & Local

Government, Alan Kelly, and the Minister of State with Special Responsibility for Housing, Paudie Coffey, formally announced a €300m housing

investment programme with the HFA and the EIB. The funding enables the HFA to offer customers 25-year fixed rate funding at very competitive

interest rates.

It is intended that this will enable an additional 2,000 social housing units to be developed over the next three years. The €150m funding from the

European Investment Bank will be matched by the HFA to make €300m available for lending to support investment by approved housing bodies

across the country to upgrade social housing and improved energy

efficiency.

14

13. OTHER FUNDING

The policy objective is to continue to make available fixed and index linked

funding as required and to offer a robust borrowing scheme for on-lending to local authorities for water, waste and environmental projects.

It is expected that the existing fixed and index linked funding will be

adequate to meet the HFA’s requirements over the course of the Plan. It is

not anticipated that any new funding of an unguaranteed nature will be needed for water and waste projects, under Section 17 of the Housing

(Miscellaneous Provisions) Act, 2002, during the life of the Plan.

14. REVIEW OF EXISTING DEBT

The policy objective is to ensure that existing debt is structured to meet the HFA’s business needs.

The Board reviews existing debt annually, or as required. The review

focuses on two principal elements:

the cost of existing debt in relation to current market conditions; and match funding the HFA’s debt with its advances, to ensure that risks

arising from mismatching are minimised.

It is a long-term policy aim of the HFA to lengthen its debt profile to better

match its asset/liability structure (see section 13.1).

15. REFINANCING OF MATURING DEBT

The policy objective is to ensure that appropriate arrangements are in place for repaying and/or refinancing maturing debt.

15.1 Variable rate debt: During 2015-19, one facility will mature, as

detailed in the following table:-

Facilities

description

Maturity

date

Proposed Action

Overdraft facility (€50m)

Annually This facility was renewed in February 2015.

15

15.2 Fixed rate debt: Only match-funded (i.e. linked to specific loans to local authorities) debt matures within the Plan period. This debt finances

special housing-related advances to local authorities. These advances will either be repaid to match debt repayments, or refinanced with matched

debt. The HFA has a fixed rate stock issue outstanding, which matures in 2018. The value of this stock at 31 December 2014 was €94m.

15.3 Index linked debt: The HFA has an index linked stock issue outstanding, which matured at the start of April 2015 and was refinanced by

variable rate debt on maturity.

16. OPERATIONAL CONSIDERATIONS

The policy objective is to ensure that the NTMA delivers cost effective funding to the HFA, within the parameters laid down by the HFA.

Section 17 of the Housing (Miscellaneous Provisions) Act, 2002 and Section

19 of the Planning and Development (Amendment) Act, 2002, give the HFA the power to request the NTMA to undertake borrowing and debt

management on the HFA’s behalf.

The arrangement referred to in Paragraph 13.1 above gives the HFA access

to a stable EURIBOR-related source of variable funding which will allow the HFA meet the needs of its customers over the life time of the Plan.

With the cooperation of the NTMA, the HFA extended the average maturity

profile of its funding from 2.8 months. This funding has been benchmarked against Euribor®, and the increased tenor was negotiated with the NTMA at

no increased cost to the HFA.to 3.2 years. The restructuring of the debt in this manner will significantly reduce the HFA’s liquidity risk profile and will

have no new terms or negative impact on the cost of funding to our borrowers.

16

PART IV: RISK MANAGEMENT AND PROJECTED ACCOUNTS,

2015-2019

Using the lending and funding framework set out in Parts II and III, and taking account of the risks inherent in the portfolio, this part of the Plan

details the management of risk by the HFA, and projected accounts

between 2015 and 2019.

17. OBLIGATION ON THE HFA TO MEET ITS COSTS FROM ITS OPERATIONS

17.1 Section 4 of the Housing Finance Agency (Amendment) Act, 1988,

states that “the Agency, in performing its functions, shall ensure that, having regard to any contribution which may be made by the Minister and

taking one year with another, all of its costs are met from its operations.”

17.2 The HFA has adopted a policy of setting interest rates that will enable it, taking risk into account, to achieve a break-even result in accordance

with the provision of the Act. This policy was adopted by the Board on 22 March 2000 and approved by the Minister for the Environment, Community

and Local Government with the consent of the Minister for Finance on 18

May 2000. The HFA therefore sets its variable interest rates at margins over the cost of funds to meet the cost of administration and risk.

18. RISK MANAGEMENT FRAMEWORK & POLICY

The policy objective is to ensure that the HFA has in place a Risk

Management Framework & Policy that captures, measures and assesses the risks in its business.

In accordance with the revised Code of Corporate Governance for State Bodies, the HFA’s Board has adopted a Risk Management Framework &

Policy which covers all known risks in the HFA, financial and non-financial. This was reviewed and redeveloped by independent consultants, at the

request of the Board, and approved by the Board at its October 2011 meeting. Risk is overseen collegially by a committee of the Chief Executive

Officer, Head of Treasury and Company Secretary in accordance with the Code. This is a standing item on the agenda of the Board. Also, the task of

reviewing risks, in detail, continues to be reserved as a standing agenda item for future meetings of the Audit Committee, with the Board tasked with

overseeing risk and considering recommendations from the Committee.

17

19. RISK IN THE HFA’S LOAN BOOK

The principal risks in the HFA’s book are those relating to the redemption of land acquisition loans; fixed rate funding mismatches; provisions in respect

of capital balances of borrowers over 75 years with income-related loans; pension scheme contributions; interest rate risk; liquidity risk; and credit

risk. Each risk is examined in more detail below.

19.1 Redemption of land acquisition loans: Land acquisition loans,

totalling €800m, for the purpose of developing into affordable housing and other schemes, were advanced to local authorities in the period 2000-2010.

Following the recent economic downturn, many local authorities found themselves with land banks which could not easily be developed and sold

on, and for which the underlying land price had declined substantially. Outstanding balances on these loans at 31 December 2014 were €480m

(2013: €507m).

The DoECLG Land Aggregation Scheme (‘LAGS’) first became operational in 2010 with the objective of gradually, over a period of about 10 years,

reducing the outstanding loan balance for land on local authority books. New arrangements were advised by the DoECLG to local authorities in June

2012 in which the terms of the scheme were altered such that interest only

land loans that have matured or are due to mature in 2012 and after, must either be repaid or converted into a standard annuity with a term of up to 25

years with the DoECLG recouping the full cost of the capital and interest annuity payments. At 31 December 2014 the outstanding balance of loans

transferred to LAGS was €51m.

In the context of the continuing pressure on Exchequer resources, a further review of the operation of LAGS by the DoECLG, in consultation with the

Department of Public Expenditure (“DPER”) and Reform was completed in 2013. The review concluded that the land aggregation scheme be

discontinued. Funding will continue to be made available, by the DoECLG, for the recoupment of annuity loan payments to local authorities in respect of

land already approved into the Scheme. Local authorities with loans not already accepted into the scheme were encouraged to contact the HFA to

make arrangements as necessary.

The DoECLG will continue to engage with the HFA and the local government

sector in relation to the management of the local authority loan book generally. The HFA have offered renegotiated loans terms for such loans,

with Local Authorities, up to five years interest-only, with loans to revert thereafter to normal course annuities. This will enable the affected Local

Authorities find alternative uses for the lands.

18

19.2 Fixed rate funding mismatches: The HFA has substantial risk in part of its portfolio – principally in its fixed rate books - as a result of

structural changes in the level of interest rates since Economic and Monetary Union in 1998. The HFA has long term and fixed interest rate debt, financed

by bond which will expire in 2018. This debt was raised to finance specific housing schemes in the 1980s. It represented exceptional value at the time

and into the early 1990s. However, the structural fall in interest rates since

the mid-1990s precipitated a substantial increase in loan redemptions. Together with the Government granting a right to prepay fixed rate loans

without penalty in 1989 (after the bond was issued) the result for the HFA has been the development of a considerable mismatch in the loan book. As

at 31 December 2014, the mismatches stood at €82 million.

The present value cost of this mismatch to 2019 is currently estimated at about €30m. (This figure will fluctuate as interest rates and market

conditions change.) The HFA has recognised this debt/loans mismatch for many years. The challenge is to maintain the HFA’s cost-effective rates for

borrowers while providing for reserves (€106m as at 31 December 2014) to meet the cost. This will be achieved by a continuous review of margins,

adjusting them as required to generate the required reserves.

19.3 Provisions in respect of capital balances of borrowers over 75

years with income-related loans: The HFA has made provisions in respect of a potential liability arising from a mortgage protection insurance

issue affecting borrowers with income-related loans. In 2014, after a detailed assessment of outstanding loans with local authorities as part of our

annual audit process, this provision was increased by €0.25m to €1.96m. No claims against this provision have yet been received. An estimated provision

increase of €0.25m per annum has been included in the 2015 – 2019 projections. As at 31 December 2014, €13m of pre-May 1986 loans

remained outstanding with the HFA from local authorities, of which €11m was owed by individual borrowers.

19.4 Pension scheme contributions: As at 31 December 2014, the HFA’s

pension scheme (as certified by the Actuary for the scheme) was fully funded and in accordance with The Pension Board’s Funding Standard. As

published in its FRS17 Actuarial Report for the year to 31 December 2014,

the HFA reported total plan assets of €3.19m and liability obligations of €3.78m, leaving a fair value deficit of €(0.60)m (2013: deficit €(0.08)m.

It has always been the policy of the HFA, being a plc, to ensure that its

pension scheme meets the Funding Standard, by making capital payments as deemed necessary by the actuaries.

19

19.5 Interest rate risk exposure is managed by minimising mismatches between its borrowings and its advances within its individual programmes –

index linked, fixed rate and variable rate. The following uncertainties are taken into account in determining the policy: (a) where borrowers can

redeem without penalty; (b) where specialised markets (e.g. index linked) may not always be receptive to issues and redemptions; and (c) where the

HFA is subject to changes in Government policy. The HFA’s general

approach in relation to managing its interest rate risk exposure is to set aside reserves to protect the HFA against perceived residual risks after

matching, by reference to various scenarios and assumptions. The Board assesses the situation regularly and determines the level of reserves

required annually.

19.6 Liquidity risk: The HFA’s policy in relation to liquidity risk is to

ensure, by periodic reviews of cash flow requirements, that it can meet its funding obligations for an appropriate period ahead, usually up to six

months. The Board has in place a policy of regular assessment of maturing debt and its refinancing and/or repayment. For further details, see

paragraph 13.1.

19.7 Credit risk: Consists principally of the risk that loans to local

authorities will not be repaid. No material credit risk arises on loans advanced to local authorities on or after 27 May 1986 and no loan loss provisions are

recorded in respect of these loans. Local authorities are bodies under statute and all loans advanced to local authorities are approved by the Minister.

It is the Board’s belief as published in the HFA’s 2014 Annual Report that, in

this context, credit risk does not arise. In the case of loans advanced prior to 27 May 1986 (€13m outstanding at 31 December 2014) the HFA is liable for

any impairment losses that may arise, only in the event of the underlying mortgage property and mortgage protection insurance not being sufficient to

discharge the debt.

20. PROJECTED ACCOUNTS

20.1 Assumptions used: In the context of its risk management, the HFA

has a projected accounts model out to 2018, when the index linked/fixed rate portfolio mismatch ends. The model, together with the assumptions,

was assessed independently by an outside firm of consultants. The model was found to be of robust construction and the assumptions were deemed to

be conservative. The assumptions have been updated in the light of current trends, and are as follows:

Nil net advances for 2015 and €100 million per annum thereafter

(See Section 7.6). Inflation at -0.60% for 2015, 2.00% for 2016 to 2019.

Net variable margins are: Mortgage: 0.35% in 2015; 0.25% in 2016 and 0.20% thereafter

(2014: 0.55%).

20

Non-mortgage:0.85% in 2015, 0.75% in 2016, 0.50% in 2017 and 0.25% thereafter (2014: 0.75%).

AHB margins: 2.10% in 2015, 1.80% in 2016, 1.0% in 2017 and thereafter (2014:1.95%).

Cost of funds ranges from 1.0%, in 2015 and 2016; to 1.50% for 2018 to 2019.

20.2 Summary of results: On this basis, a summary of projected results for the period of the Plan is as follows:

Year Operating

surplus

€m

Closing

Reserves

€m 2015 21.7 127.6

2016 21.6 149.3

2017 15.7 164.9

2018 16.9 181.9

2019 20.3 202.2

The closing reserves do not take account of the following, which together have the potential to raise or lower the figure: -

ECP fair value accounting changes (2014: nil) Pension fund FRS 17 adjustments (2014: -€1.14m)

20.3 Detailed projected accounts, 2015-2019: Details are set out at ANNEX 2.

20.4 Sensitivity analysis The HFA regularly reviews its exposure to changes in its lending terms and

external factors such as increase in interest rates and inflation and how such changes would impact on the projected gains/ (losses).

As part of this review the HFA has considered the sensitivity analysis on the

projected results allowing for a further 5.0% of the current loan book to avail of the following flexible loan repayment options as follows:

Interest only for a 5 year period Extend loan terms for a period of 10 year

Increase in local authority arrears Increase in the inflation rates

Increase and decrease in interest rates

Refer to ANNEX 3 for details of the analysis.

In conclusion the overall effect of offering Local Authorities the above mentioned flexible repayment options and the changes in inflation rates has

an insignificant effect on the operating income and cash flow of the HFA.

21

21. DIVIDEND POLICY

The dividend policy of the HFA is as follows:

The HFA’s Dividend Policy is to award up to 30% of its “Total recognised

gains for the previous financial year”, provided that the payment of a dividend is appropriate and prudent in the context of the HFA’s financial

position, strategic objectives and prospects.

It is possible that the HFA could award dividends, based on projected returns

detailed in Section 20.2, of circa €6 million per annum.

Alternatively, the HFA may at the request of its beneficial shareholder award a more significant dividend.

22

PART V: CUSTOMER SERVICE

This Part of the Plan details how the HFA delivers and measures its

services to customers.

22. CUSTOMER GROUPS

Currently, the HFA’s customers are the local authorities and approved housing bodies. The HFA is fully committed to the principles of Quality

Customer Service (QCS). Details are given in the Annual Report of the performance measurement criteria set down for monitoring and reporting.

23. CUSTOMER SERVICE INITIATIVES

The policy objective is to deepen and broaden the existing liaison measures with our customer groups as appropriate.

Recent and ongoing initiatives include:

Participation in Heads of Finance meetings: The HFA’s

relationship with local authorities involves it attending all Heads of Finance meetings where regular presentations are made on a wide

range of related issues involving both the HFA and the local authorities. Participation at these meetings also provides the HFA

with a forum to obtain the views of local authorities on the various issues that arise from time to time. This work will continue and

expand during the Plan period.

HFA/Local Authority Liaison Committee: In 2014, The Board of

the HFA and the County and City Managers’ Association reactivated a Liaison Committee consisting of Directors and Managers to review

ongoing operations and plan the development of the service. The Committee meets on a semi-annual basis. It gives the Managers a

direct channel to the Board.

Code of Conduct for staff: The HFA’s Personnel Code of Conduct provides guidance for staff in dealing with our customers covering

written correspondence, personal calls to our offices and phone calls. The Personnel Code of Conduct provides that correspondence

must be acknowledged unless a reply (if required) can be sent within a week. Where delay in unavoidable staff are advised of the

desirability of sending an interim reply.

23

Code of Conduct for Directors: Previously, the code of conduct

contained within the Institute of Public Administration’s Guide for Board Members of State Bodies in Ireland has been adopted by the

HFA’s Board. The HFA has adopted a new code of conduct for its Directors in 2013.

Representation on the Board: Our principal customers, the local authorities, are represented on the Board by a Chief Executive and

an elected representative.

Local authority information roadshows: Within its resources, the HFA intends to continue its policy of hosting local authority

informational road shows, to liaise with and inform its principal customers, the local authorities, of the services the HFA provides.

Electronic information: All information is now issued by e-mail to

finance and housing officials. Board and Committee meeting papers are also issued electronically.

Programmes of regional workshops are held from time to time

in conjunction with local authorities, to train local authority staff in

the HFA’s online loan system. It is planned that a series of regional workshops will be held in late 2015/ early 2016 on the introduction

of the HFA’s redeveloped Local Authority Billing System (LABS)

The HFA has published a Customer Charter, which is available on the HFA’s website.

Central Government reporting: The HFA has developed a module

on its website, which allows local authorities obtain current period actual and 3-year loan projections of principal and interest

repayments for Central Government reporting purposes.

Seminars: The HFA held a seminar in February 2014 titled “Financing Social Housing in Ireland” which was attended by many

key stakeholders in the sector. Guest speakers from the UK, Austria,

Holland and Ireland presented different models and structures for financing social housing. The seminar received very positive

feedback from those who attended and the outputs will be used in the ongoing development of new financing structures for social

housing in Ireland.

Redevelopment of LABS system: The HFA’s LABS system is an essential tool in how the HFA does business with local authorities

and AHBs, and it is imperative that this remains fully functional and secure. The HFA is currently redeveloping its system. The

redevelopment process has been subdivided into a number of phases, with ‘go-live’ implementation planned for June 2015. The

24

proposed new system will also interface seamlessly with the HFA’s current financial management information system, which uses IRIS

Exchequer Enterprise. The new system will be delivered as a Java™-based application and will be optimised to take account of current

technologies. Users will enjoy a modern web-based universal interface. The new system when introduced should see a very

significant improvement in processing time.

24. PERFORMANCE CRITERIA

The policy objective is to develop, in conjunction with the DoECLG,

appropriate performance measures for the HFA.

Public service reform measures speak of measuring the performance of non-commercial state bodies by using performance frameworks and output

statements: Given the HFA’s structure, the appropriateness of these systems of measurement for the HFA will be discussed with the DoECLG during the

currency of the Plan. It should be noted that, currently, targets in relation to loan advances are set by Government. Outputs are determined by factors

largely outside the HFA’s control - the general economic climate, the take-up of the various social housing schemes, the cost of housing, availability of

sites, and the operational efficiency of local authorities and so on. The HFA

has therefore set down Quality Customer Service Performance criteria that are within the HFA’s control, for monitoring and reporting in the Annual

Report, as follows:-

24.1 Comply with Best Practice: The HFA regulates its day to day operations by following a strict code of practice as laid down in the Policy

and Procedures Manual. Compliance is reported upon twice a year and reviewed by the Audit Committee.

Target for 2015: limit the number of policy and procedures breaches (other than those arising from staff absences) to less than 10. Outturn for 2014:

We achieved our target, with no such exception reports in 2014.

24.2 Lending at a competitive interest rate that will achieve the required trading surpluses: The HFA supplies funds for mortgage-related

(ultimately to households) and non-mortgage-related (to local authorities for

their housing-related programmes) purposes. In the case of mortgage-related loans, the HFA aims to use the State Guarantee and its own

expertise to lend at a rate competitive with an average standard market rate. For non-mortgage-related loans, the HFA aims to lend to local

authorities at rates competitive with the commercial sector.

The Board of the HFA sets the operating surplus to be achieved each year in the period to 2019 to meet its reserves requirements.

Target for 2015:€23.6m Outturn for 2014: €13.9m

25

24.3 Quality Customer Service for local authorities: The HFA has set

the following goals:-

Target for 2015: 95% of loan applications to be paid within 7 days of receipt provided they meet all loan criteria. Outturn for

2014: 99%

Target for 2015: All incoming correspondence to be replied to within one week. Outturn for 2014: Met

Target for 2014: Expenditure on staff training to be a minimum of 4.0% of salary costs, Outturn for 2014: 4.0%

24.4 Quality Customer Service for Approved Housing Bodies: It is

envisaged that the HFA will set quality customer service criteria for dealing with Approved Housing Bodies, based on feedback following a customer

survey in 2014.

24.5 Productivity: The HFA aims to use technology to ensure that it can deliver the required services to our customers in Local Authorities and the

Voluntary Housing sector at its existing staff establishment (11 Whole Time Equivalents) (see also paragraph 27 below).

Service Level Agreement with DoECLG: As required by Section 11.1 of the Code of Practice for the Governance of State Bodies, the Board of the

HFA has approved a Service Level Agreement at the February 2015 meeting (See HFA website for further details).

25. MONITORING

A monitoring process has been in place since 1 July 2002 to ensure the HFA

achieves its target in each area, the results of which are reported to the Minister and published in our Annual Report.

26

PART VI: CORPORATE GOVERNANCE AND ADMINISTRATION

This Part of the Plan deals with Board governance, operations and staff

matters.

26. CORPORATE GOVERNANCE

The HFA aims to achieve the highest standards of corporate governance. The HFA, in its business, has chosen to comply with, so far as is possible

given the HFA’s particular circumstances, the UK Corporate Governance Code 2012 (issued by the Financial Reporting Council), the Irish Corporate

Governance Annex (issued by the Irish Stock Exchange) and the Code of Practice for the Governance of State Bodies (as issued by the Department of

Finance).

The Board has established a Performance Review Committee, which

evaluates its own performance and those of individual Directors, and reports to the Board on its findings each year (see page 21 of the Annual Report).

The Chairman, in line with the Code of Practice for the Governance of State Bodies, instigated ‘one-to-one’ appraisals with Board members in 2010

which will be continued throughout the plan.

27. INTERNAL COMMUNICATION

One of the HFA’s most valuable assets is the ability and knowledge of its staff, which number eleven whole-time equivalents. The HFA has been able

to increase its business with low numbers of staff by an efficient use of information technology. Procedures are the subject of continuous review to

ensure that efficiency is maintained at the highest level.

28. CHANGE AND MODERNISATION

The public service is undergoing a major process of change with the

implementation of the Haddington Road Agreement. The HFA is prepared to play its part in that process. The Department of Finance indicated that the

appropriate approach to preparation of an action plan for ‘Agencies with a small number of staff who are self-financing’, such as the HFA, was to

prepare such plans on the basis of improvements to current practice where feasible and improving productivity. This the HFA has done, while also

projecting to minimise administrative expenditure increases over the life of the plan to 1% per annum.

27

Currently, the following principal elements make up the HFA’s commitment to change and modernisation: -

28.1 Human resources

There has been a strong emphasis on training and development of staff in

the last three years.

Staff rotation and atypical work arrangements introduced since 2004

continue to produce positive benefits for both the HFA and the employees availing of these schemes. The HFA will endeavour to maintain these

schemes and arrangements insofar as it is possible within the constraints of ensuring that the HFA’s business can be carried out effectively and cost-

efficiently. Staff number have remained static at eleven whole-time equivalents (WTEs) since 2010, although this may increase slightly during

the Plan.

28.2 Information Technology

There will be ongoing encouragement of staff to train in and broaden their knowledge of information technology.

The HFA has implemented electronic payments for all regular suppliers and also for employees’ and Directors’ expenses payments. In line with

Department of Finance’s Circular 1/2013, operational from September 2014, as far as is practically possible the HFA no longer write cheques to business

users, or accepts cheques from business users (except in exceptional circumstances).Virtually no cheques are now used in HFA business.

28

29. ADMINISTRATION COSTS

29.1 Background: In line with Section 7.2.4 of the HFA’s Policies and Procedures manual, an administration budget is prepared for the HFA

annually, approved by the CEO, and submitted to the Board for approval. Within the overall approved budget the CEO has responsibility of managing

the sub-categories of such expenditure as necessary.

While the HFA is a self-financing body not in receipt of an Exchequer

allocation, nonetheless the Board and the HFA are keen to support the Government position in relation to expenditure control insofar as is possible

within the HFA’s business model.

The HFA pays its own way by taking a small margin from its lending – an

estimated 0.03% of its loan book (€4.2 billion) in 2014. As part of its normal business management, the HFA aims to keep its operating costs as

low as possible, while delivering the service required to its customers, the local authorities and voluntary housing bodies. Most of its business is

carried out through a dedicated custom-built members’ website

(www.hfa.ie), which allows for loan advances and treasury dealing to be done on-line, involving the HFA, local authorities and the DoECLG. The

HFA’s staff complement has been 11 since 2010. The HFA projects minimising increases in its administration costs to 1% per annum. The

HFA’s pension fund was fully funded as at September 2014.

29.2 Administration budget for 2015: The following is the Board-approved budget for administration expenditure.

Projected for 2015 (Corp. Plan, 15th

ed.)

Outturn for 2014*

Projected for 2015

% change in projections

2015 over 2014

€1.58m €1.39m €1.58m 5%

* Out of an overall budget of €1.50m for 2014, the HFA spent €1.39m,

costs were lower than budget due to lower consultancy and rating agency fees than forecast.

Despite additional expected costs arising in 2015, relating to direct lending

assessments of AHBs, and the redevelopment of the loan billing system, the HFA aims to keep administrative expenditure to the same level as that

budgeted for in 2014.

29.3 Administration fees to local authorities: These are fees amounting

to 0.50% of the balance outstanding on the pre 1986 income related loans, paid to local authorities for administering them. This cost is reducing over

time due to the decline in the loan portfolio. As loans are being redeemed by individuals, the local authorities collect less money and less commission

is paid by the HFA.

29

29.4 Trend analysis in administration expenditure: The following table

gives details of the above costs in the three years to December 2014:

Description 2012

€m

2013

€m

2014

€m

Administration expenditure 1.35 1.37 1.39

Administration fees to local authorities

0.10 0.10 0.10

Totals 1.45 1.47 1.49

30. FREEDOM OF INFORMATION

The HFA has been subject to the Freedom of Information Act from 22 November 2002. The HFA had one request in 2013 which was dealt with

promptly. The Freedom of Information Officer is Mr. Seán Cremen and the internal reviewer is Mr. Barry O’Leary. A manual, under section 15 of the

Act has been published and is available on the HFA’s website (www.hfa.ie). The Board annually reviews the HFA’s operation of the Act.

0.00%

0.01%

0.02%

0.03%

0.04%

0.05%

2010 2011 2012 2013 2014

Administration costs as a % of total &

variable loan books 2010-2014

Admin as % of var loan book Admin as % of total loan book

30

PART VII: CONCLUSION

31. GOALS FOR THE PERIOD 2015 TO 2019

The key objectives of the HFA in the period are:

introducing new funding models and sources to meet Government

requirements and to better match the asset profile of the HFA;

engaging with the Department of the Environment, Community & Local Government and local authorities, to work towards the implementation

of Social Housing Strategy 2020; and

facilitating and encouraging further participation by approved housing

bodies in the provision of social housing. .

32. PERFORMANCE MEASUREMENT

The HFA strives to raise funds at competitive rates while prudently managing funding and liquidity risk. The benefits are passed on to customers and are

also used to build reserves where required. The cost of borrowings related to

appropriate bench-marks give an indication of success in borrowing at the most competitive rates.

The HFA will strive to achieve the highest ratings in all areas, subject to

performance measurement as detailed in the Plan.

31

ANNEX 1: EVOLUTION AND DEVELOPMENT OF THE HFA SINCE ITS FOUNDATION IN 1982

1982: The HFA was originally set up to operate a specific scheme of

income-related mortgage loans, based on index-linked funding

from pension and life funds primarily. This scheme allowed some 16,000 households to acquire houses between 1982 and 1986

who would not otherwise have been able to do so. Loans advanced amounted to €403m, while loans outstanding as at 31

December 2012 were €20m, approximately.

1986: The HFA was given responsibility for funding all house purchase loans to local authorities

Borrowing limit increased to €635m

1991: Plan for Social Housing The HFA to fund:

- rented element of shared ownership scheme - capital finance for rental subsidy scheme

1992: Housing Act The HFA to fund any of the housing functions of a local

authority The HFA can lend to the National Building Agency

Borrowing limit increased to €1,904m

1995: Social Housing - The Way Ahead Short term funds for housing co-operatives

Loans for land purchase for housing

2002: Housing (Miscellaneous Provisions) Act Loans can be given to local authorities for sanitary

services and waste management Loans can be given directly to approved voluntary bodies

for the acquisition of land and provision of housing

The HFA’s borrowing limit increased to €6,000m

2002: Planning and Development Act The National Treasury Management Agency was given

powers to perform certain functions of the HFA in regard to debt raising and management.

2003-2005: EU Commission decisions on State Aid. The EU

Commission approves the use of the Government Guarantee on borrowing for the provision of

Lending for social housing Direct lending to voluntary housing bodies

32

Lending for social housing-related projects, including local authority offices

2007-2008: Lending for water, waste and environmental projects.

Lending totalling some €49 million was advanced to local authorities, funded by unguaranteed loans from the EIB and CEB.

2009: Housing (Miscellaneous Provisions) Act an increase in the HFA’s borrowing limit from €6 to €10

billion; phasing out of the shared ownership scheme (This

accounted for €4.0 million of gross advances by the HFA in 2012 – 1% of total gross advances); and

repeal of Section 56 of the 1966 Housing Act, and its replacement in this Act with a similar, though slightly

wider, provision that enables local authorities to borrow for housing- and community-related developments.

Other powers enacted but not implemented by Government were:

- recycling of funds received from affordable house purchasers through an Affordable Dwellings Fund, to

be managed and accounted for separately by the HFA;

and - Potential involvement of the HFA (providing an

investment outlet, via its Guaranteed Notes programme) in the apartment complex support fund

for tenant purchases of apartments.

2010: The HFA ‘opens for business’ for accepting applications for direct lending to AHBs (voluntary housing bodies and co-operative

housing societies).

2014: To date, twenty eight applications for Certified Body status have been received from AHBs. Twelve AHBs were successful and

fourteen were unsuccessful in their initial applications, with two still pursuing the path to a successful application.

As at 31 December 2014, the HFA has approved 44 loan applications totalling €63 million, €36 million of which has been

advanced. In the last year the number of AHBs with Certified Body status has doubled. The HFA now deals with a variety of

AHBs which specialise in helping homeless persons, elderly persons and a small sized AHB. It is anticipated that 2015 will

herald continued growth in the level of lending in this area. The HFA continues to have frequent interaction with the AHBs to

develop and fine tune the suite of products which it offers.

33

Schemes currently funded by the HFA:

(a) House purchase loans: These include annuity loans, the

affordable loan scheme and the shared ownership scheme. They include bridging finance and land acquisition loans.

(b) Rented voluntary accommodation: Capital loan and subsidy

scheme. (c) House improvement loans: House improvement loans for both

private and local authority houses. (d) Miscellaneous loans: Loans under section 11 of the Housing

(Miscellaneous Provisions) Act 2009. These include facilities associated with social housing provision, local authority offices

with housing functions, etc. (e) Loans for water, waste and environmental projects under

the Housing (Miscellaneous Provisions) Act, 2002. (f) Loans to Approved Housing Bodies (AHBs) under the

Government are Social Housing Leasing Initiative including Mortgage to Rent and New Build projects and, recently, long term

fixed rate finance.

34

ANNEX 2: PROJECTED ACCOUNTS 2015-2019

Projected Income and Expenditure Account

31 December 2015 31 December 2016 31 December 2017 31 December 2018 31 December 2019 €'000 €'000 €'000 €'000 €'000 Income - continuing activities 75,308 73,363 78,506 85,538 89,426

Interest expense and fees

1 (51,624) (49,720) (60,765) (66,465) (66,997)

Net interest income 23,683 23,643 17,740 19,073 22,429

Expenses 2 (1,979) (2,019) (2,059) (2,100) (2,142)

Gain on ordinary activities for the financial year 21,704 21,624 15,681 16,973 20,286

Closing Reserves 127,635 149,259 164,940 181,913 202,199

Balance due on loan advances 4,189,185 4,290,047 4,390,888 4,491,708 4,592,506

35

Projected Notes forming part of the Financial Statements

1. Direct expenditure 31 December 2015 31 December 2016 31 December 2017 31 December 2018 31 December 2019

€'000 €'000 €'000 €'000 €'000

Index Linked Bonds

Bond interest (1,928)

- - -

Premium on redemption of bonds (465) - - -

Stock and Loan Costs Interest payable on bank borrowings, commercial paper, (48,485) (49,974) (61,019) (66,719) (67,251) guaranteed notes and stock Eurocommercial paper (ECP) fees 254 254 254 254 254

Total interest expense (51,624) (49,720) (60,765) (66,465) (66,997)

2. Indirect expenditure 31 December 2015 31 December 2016 31 December 2017 31 December 2018 31 December 2019

€'000 €'000 €'000 €'000 €'000

Administrative expenditure (1,979) (2,019) (2,059) (2,100) (2,142)

Total Expenditure (1,979) (2,019) (2,059) (2,100) (2,142)

36

ANNEX 3: SENSITIVITY ANALYSIS

Renegotiated Loans currently in place

In 2014 the HFA put in place the following renegotiated loans terms with

Local Authorities Type of Loan Amounts Outstanding

at time of renegotiation

€’000

As a % of

Total Loan

Book

New Terms

Non Mortgage 117,532 2.80%

Land Acquisition loans

transferred to annuity

Non Mortgage 97,960 2.30%

Interest only for 5 years

Non Mortgage 20,956 0.5% Interest only for one year

Non Mortgage 1,900 0.05%

Interest only for 2 years

Non Mortgage 602 0.01% Variable Loan Land

Acquisition to LAGS

Total 238,950

Less:

Loans no longer

renegotiated

Mortgage (1,568) (0.04)% Interest only for 3 years

Non Mortgage (31,617) (0.75)% Interest only for 2 years

Non Mortgage (3,368) (0.08)% Interest only for one year

Total Overall

Renegotiated Loans

202,397

4.79%

The following is a sensitivity analysis on the projected 2015 results for the following options:

Interest Only Period currently restricted for 5 years. Analysis shows

effect of 5% of loan book being designated as interest only:

o Decrease in the cash flow, due to non-receipt of annuity

repayments

o Increase in operating profit due margin differential on the interest

charge on greater outstanding principal amounts offset against

cost of additional interest charge of financing outstanding loan.

37

Interest Only Period for 5

years

2015 €’000

2016 €’000

2017 €’000

2018 €’000

2019 €’000

Projected

operating surplus

21,704 21,624 15,681 16,973 20,286

Net effect 101 99 120 141 138

Adjusted operating surplus

21,805 21,723 15,801 17,114 20,424

% change in operating surplus