corporate presentation - alicorp.com.pe · alicorp does not assume any obligation to update any...

TRANSCRIPT

0

Corporate

Presentation

August, 2018

1

This presentation may contain financial or business projections regarding recent acquisitions, their

financial or business impact, management expectations and objectives regarding such acquisitions and

current management expectations on the operating and financial performance of The Company, based

on assumptions that, as of today, are considered valid. Financial and business projections are

estimates and do not constitute any declaration of historical facts. Words such as “anticipates”,

“could”, “may”, “can”, “plans”, “believes”, “estimates”, “expects”, “projects”, “pretends”, “probable”,

“will”, “should”, and any other similar expression or word with a similar meaning pretend to identify

such expressions as projections. It is uncertain if the anticipated events will happen and in case they

happen, the impact they may have in Alicorp’s or The Consolidated Company’s operating and financial

results. Alicorp does not assume any obligation to update any financial or business projections

included in this presentation to reflect events or circumstances that may happen.

2

Topics

Bolivia´s M&A Transaction [ 1 ]

Corporate Strategy [ 2 ]

Q2 2018 Financial Results [ 3 ]

Guidance 2018 [ 4 ]

Stock Performance [ 5 ]

Appendix [ 6 ]

3

Topics

Bolivia´s M&A Transaction [ 1 ]

Corporate Strategy [ 2 ]

Q2 2018 Financial Results [ 3 ]

Guidance 2018 [ 4 ]

Stock Performance [ 5 ]

Appendix [ 6 ]

4

1 Acquisition of Fino & SAO: Key Highlights

Consumer

Business1

Revenue US$ 182mm

Crushing

Business2

EBITDA

~ US$ 360mm

US$ 22mm ~ US$ 35mm

EBITDA

Margin 6%12%

Acquisition of Fino and SAO will provide a strong platform for Alicorp to replicate it´s successful Peruvian consumer & B2B model

on the back of customized commercial strategies and market segmentation practices

Pro

du

ct

po

rtfo

lio

bra

nd

ma

na

ge

me

nt

FINANCIAL HIGHLIGHTS

OPPORTUNITY TO REPLICATE ALICORP´S STRATEGY IN CPG AND B2B IN A HIGH-GROWTH MARKET

Edible oil >40%

Margarine >60%

Lard >50%

L. Soap >25%

x% Category market share

▪ Alicorp acquired FINO for US$ 293mm on May 17th and SAO

for US$ 115mm on July 24th for a Total Equity Value of

US$ 408mm.

▪ Consolidated Enterprise Value reached US$ 368mm, where

LTM EBITDA multiples by business were 9.4x for CPG and 4.1x

for Crushing, the latter on a cycle adjusted basis2

▪ During 2017, both companies generated ~ US$ 450mm in

consolidated Revenues. CPG & Distribution EBITDA was

US$ 22mm1 while cycle - adjusted Crushing EBITDA was

US$ 35mm2

▪ Alicorp financed the acquisition via cash and debt on

balance sheet and utilization of available credit lines

TRANSACTION UPDATE

POTENTIAL PORTAFOLIO EXPANSION

1 Figures as of FY2017. 2 Cycle-adjusted basis considers taverage of historical figures for 2012 to 2017 of Fino and SAO.

Detergent >8%

5

By country

ESTIMATED PRO-FORMA SALES 2018E

By segment

By country

ILLUSTRATIVE PRO-FORMA EBITDA 2018E

By segment

Alicorp Pre – Bolivia's Transaction

Sales 18E

~ US$2,300mm

Pro-forma

Sales 18E

~ US$2,780mm

1 Proforma figures includes FY 2017 and 2018E financial figures of Fino and SAO.2 Crushing business profitability is highly associated to the cyclicity of commodities prices.

Source: Company management – Unaudited managerial figures, Alicorp’s 2018 estimates based on Brokers estimates median.

Note: Sales and EBITDA are calendarized to December.

Alicorp Pre – Bolivia's Transaction

EBITDA 18E

~ US$ 310mm

Pro-forma

EBITDA 18E

~ US$ 345mm

Peru60.3%

Brazil5.6%

Argentina6.4%

Ecuador16.4%

Bolivia0.7%

Others10.7%

Peru50.1%

Brazil4.7%

Argentina5.3%

Ecuador13.6%

Bolivia17.4%

Others8.9%

Peru71.9%

Brazil1.2%

Argentina(0.4%)

Ecuador21.8%

Bolivia0.8%

Others4.8%

Peru64.0%

Brazil1.0%

Argentina0.0%

Ecuador19.0%

Bolivia12.0%

Others4.0%

Consumer Products

50.6%

Aquaculture28.0%

B2B21.5%

Consumer Products

48.4%

Crushing10.4%

Aquaculture23.2%

B2B17.9%

Consumer Products

55.5%

Aquaculture28.0%

B2B16.5% Consumer

Products56.1%

Crushing4.5%

Aquaculture24.8%

B2B14.6%

Alicorp Pre – Bolivia's Transaction

Sales 18E

~ US$ 2,300mm

Pro-forma

Sales 18E

~ US$ 2,780mm

Alicorp Pre – Bolivia's Transaction

EBITDA 18E

~ US$ 310mm

Pro-forma

EBITDA 18E

~ US$ 345mm

1 Alicorp, Fino and SAO pro-forma1 metrics

Fino and SAO take a relevant share and complement our current international operations. Albeit Consumer Goods Peru remains the

largest business by Revenue and EBITDA

2

6

CONSUMER AND DISTRIBUTION (US$ MM)

120 113 114 119 133 133 68 76 68 50 55 48

Source: Unaudited managerial figures. Commodity Markets Outlook, WB.

Figures expressed as of December of each year1 Annualized estimated share of Fino and SAO CPG local edible Oils.2 CPG and Distribution estimated consolidated volumes.

13 16 21 20 26 223 4 2 2 0

2017A2016A2015A2014A2013ACalendar

Year2012A

CAGR 12’-17’: 10.5%

CAGR 12’-17’: -0.7%

▪ Volumes have grown at 6% solid pace, specially coming from Fino

▪ Revenues are affected by changes in commodity prices

▪ Fino surpassed 15% EBITDA margin since 2013, reaching almost 20% in 2014 and 2016. On the other hand, SAO’s

margins tend to reach 5-8%. In 2017, aggressive competition (including Fino) resulted in almost breakeven margins

for SAO

66 67 66 71 78 8328 20 30 29

CAGR 14’-17’: 6%

3 EBITDA figures for 2012, 2013 and 2017 of SAO are estimated, according to

historical business performance.4 Margins estimated considering interbusiness transferences5 Includes ony Fino’s volumes

7.0%

Revenue

EBITDA3

Volume2

(000’ TM)

10.1% 13.4% 14.7% 12.0%13.1%

11.5% 13.8% 18.3% 19.2% 16.9%16.8%

1Consolidated CPG business performance shows growing

volumes and solid profitability improvements…

13 19 25 22 28 22

189 189 182 169 188 182

91 108 11295

Consolidated business (Fino + SAO) Fino SAO

4

Fino EBITDA

Margin4

Consolidated

EBITDA Margin

Brand portfolio and market share in Bolivia

Fino

Margarine >60% Laundry Soap >25%

Edible oil >40% Lard >50%

Exports

Detergents >8% Personal Care >3%

Pastas >5%

XX% Market Share

5 5

7

CRUSHING (US$ mm)

Source: Unaudited managerial figures. Commodity Markets Outlook, WB.

Figures expressed as of December of each year

184 181 218 219 233 168

186 224 178 114 127 103

~ US$ 360m avg rev.

58 37 18 3 20

24 37

17

-8

10

-6

2017A2016A2015A2014A2013ACalendar

Year2012A

517 457 347540 363 352

xxx CBOT soybean price (US$/MT)

US$ 35m avg EBITDA

~6% avg

EBITDA mg

▪ The Bolivian market structure requires vertical integration to control quality and ensure access to grains supply. This results in a

natural hedge of raw materials for the CPG business

▪ Crushing cyclicality is clearly reflected over Revenue and EBITDA fluctuations. As international prices increase, FINO and SAO’s

maneuverability over the farmer's soybean price widens, allowing to share profit, guaranteeing supply and securing high profitability.

However, when prices are low, farmer's soybean price cannot be reduced as much, without losing volume share

▪ It’s important that as Crushing provides raw materials for CPG, any underperformance is offset by CPG profitability

Consolidated EBITDA Margin2

1 EBITDA figures for 2012, 2013 and 2017 of SAO are estimated,

according to historical business performance.

2 Margin estimated considering interbusiness transferences.

Interbusiness transference were estimated according to

managerial figures.

Revenue

EBITDA1

15.0% 12.7% 5.8% 5.4% -1.7%-0.8%

xx

1…while Crushing business’ cyclicality is aligned to Bolivia’s

commodities availability and price dynamics…

CRUSHING PROCESS DIAGRAM

Local

Farmers

Local

Demand

Exports

Crude

oil

Meals Soybean and

Sunflower beans

370 405 396 333 361 271

81 73 34 -5 29 -8

Consolidated business (Fino + SAO)

Fino

SAO

8

ENTERPRISE VALUE (EV) AND MULTIPLE ANALYSIS

SAO

FINO

CONSOL. EV

CRUSHING

CONSUMER

US$212million

EV

9.2x

LTM

EV / EBITDA

US$90million3

EV

4.1x2

CYCLE ADJ

EV / EBITDA

CRUSHING

US$66million3

EV

5.3x2

CYCLE ADJ

EV / EBITDA

US$23million

LTM

EBITDA1

US$22million2

AVERAGE

EBITDA

US$13million2

AVERAGE

EBITDA

CONSOLIDATED CONSUMER

US$212million

EV

9.2x

LTM

EV / EBITDA

US$23million

LTM

EBITDA1 EV

US$302million

US$66Million3 4

EV

CONSOLIDATED CRUSHING

US$156million3

EV

4.4x2

CYCLE ADJ

EV / EBITDA

US$35million2

AVERAGE

EBITDA

US$368million

1Valuation breakdown analysis of the Consumer and

Crushing businesses of Fino & SAO

Total Enterprise and Equity Value paid for both business amounted to US$ 368mm and US$ 408mm respectively, in line with initial

price guidance between US$ 390mm and US$ 420mm.

Source: Company management1 LTM EBITDA as of May 2018.2 Cycle adjusted EBITDA comprises results from 2012A to 2017A, on a calendarized level (January – December of each year).3 Considers inventory of grains and equivalents as cash, given the operational need of financing during the summer and winter soy campaigns for Crushing Business.4 SAO EV allocation only assigned to Crushing business, considering that profitability of Consumer and Distribution was almost breakeven over the LTM May 2018.

9

1.01x

2.37x2.18x

2.05x

Q1 18' Q2 18' Jul 18' Jul 18'

5.9%

31.6%

11.6%

4.2%

8.5%

38.2%

Internacional Bond

Local Bonds

ST Bank Debt

Fino's Working Capital

LT Bank Debt

Club Deal

Net debt:

Includes SAO’s net cash and

Club Deal financing

(S/ 354 million)

Consumer LTM EBITDA +

Cycle adj.Crushing EBITDA5:

Fino: S/ 142 million

SAO: S/ 40 million

Net Debt:

Includes (B) and (C)

adjustments, but excludes

inventory financing

(S/ 143 million)

163

564

2018 2019 2020 2021 2022 2023-2030

SAOSAO

3 Net Debt –to-EBITDA ratio with normalized LTM EBITDA.4 Debt before hedging operations, at amortized cost.5 Includes consumer LTM EBITDA and crushing cycle – adj EBITDA

Fino’s acquisition was financed through a Club Deal on Q218. In addition, in July 2018, Alicorp disbursed USD_115MM to

acquire SAOA

MATURITY PROFILE4: DURATION AS OF JULY 2018 WAS 2.71 YEARS

Duration: 2.71July 2018: Total Debt: S/ 3,418 million

982

Cash

[Jul. 18’]

928

27% 5% 16% 21% 25%6%

NET DEBT-TO-EBITDA RATIO DEBT BREAKDOWN

Club Deal SAO

Club Deal Fino

Fino’s Working Capital

707

189

141

194

A

July 2018: Total Debt: S/ 3,418 million

Fino took short-term debt of USD 43.7MM

during Q2 18’ to finance its inventory purchase.

This debt represents 4.2% of total financial debt

and 33.7% of Fino’s Debt

1 Includes SAO’s cash (USD 7MM) and Club Deal for SAO’s acquisition (USD 115MM). 2 All-in cost of debt is defined as the accumulated LTM of the Interest expense, plus hedging cost,

plus difference in exchange rate, divided between monthly average of the LTM Gross Debt.

(PEN Million)

349

465

116

Fino and SAO’s acquisition financing still leaves a

healthy Balance Sheet, reflected on our stable credit

ratings11

2,436

1,028

1,015

1,010

FINO

Net Debt LTM EBITDA All-in Cost of Debt2

2,293

1,117

B

C

B

C

3

2,436

1,117

D

3

D

862

CREDIT RATING

Glo

bal

Peru

Firm

143

All credit rating agencies have a

positive outlook on Fino and SAO’s

acquisition due to: i) increased

presence in Bolivia, strengthening

leadership in consumer goods and B2B

and ii) is aligned with Alicorp’s strategy

about adding new top brands and

product categories.

Outlook

Alicorp’s Bonds and Commercial Paper programs is filed

for up to S/ 1,500 million, which is a source to refinance

our debt

SAO

FINO FINO

SAOSAO

4.4%

4.8% 4.8% 4.7%

10

Consumer

products

Source: Company management

Note: Estimation by Integration Management Office

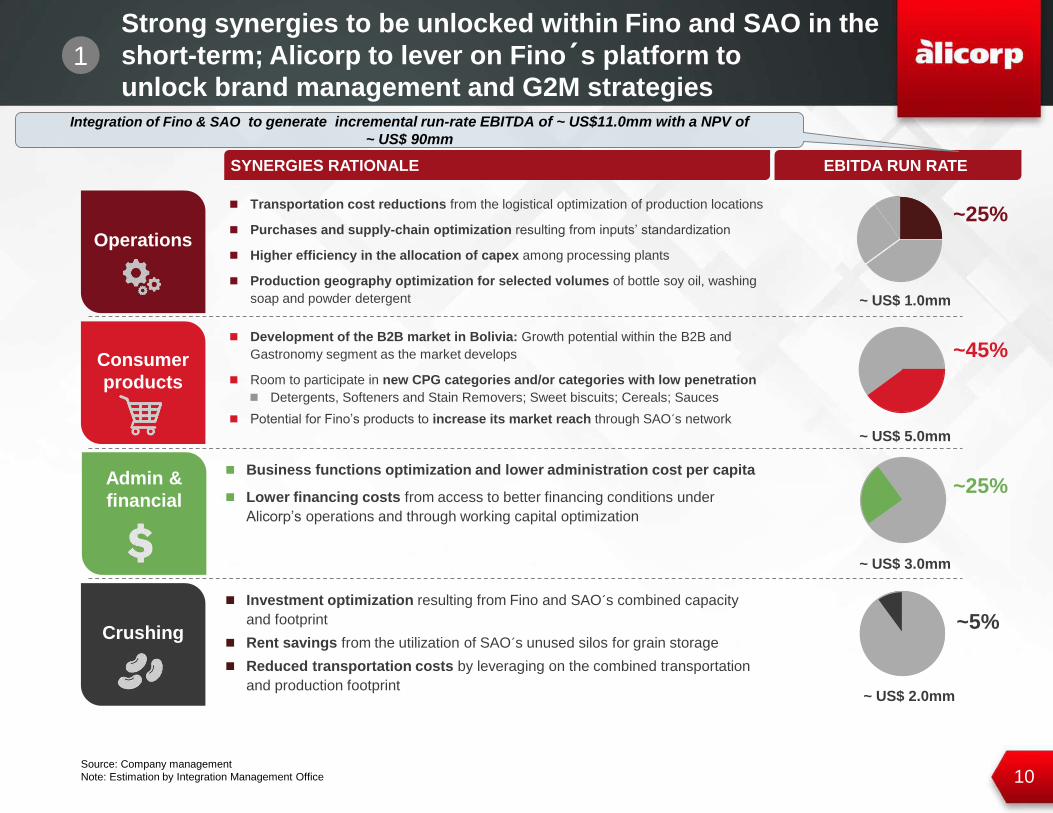

SYNERGIES RATIONALE EBITDA RUN RATE

Operations

~25%

~45%

Admin &

financial

Crushing~5%

Development of the B2B market in Bolivia: Growth potential within the B2B and

Gastronomy segment as the market develops

Room to participate in new CPG categories and/or categories with low penetration

Detergents, Softeners and Stain Removers; Sweet biscuits; Cereals; Sauces

Potential for Fino’s products to increase its market reach through SAO´s network

Transportation cost reductions from the logistical optimization of production locations

Purchases and supply-chain optimization resulting from inputs’ standardization

Higher efficiency in the allocation of capex among processing plants

Production geography optimization for selected volumes of bottle soy oil, washing

soap and powder detergent

Business functions optimization and lower administration cost per capita

Lower financing costs from access to better financing conditions under

Alicorp’s operations and through working capital optimization

Investment optimization resulting from Fino and SAO´s combined capacity

and footprint

Rent savings from the utilization of SAO´s unused silos for grain storage

Reduced transportation costs by leveraging on the combined transportation

and production footprint

1

Strong synergies to be unlocked within Fino and SAO in the

short-term; Alicorp to lever on Fino´s platform to

unlock brand management and G2M strategies

~ US$ 1.0mm

~ US$ 5.0mm

~ US$ 3.0mm

~ US$ 2.0mm

~25%

Integration of Fino & SAO to generate incremental run-rate EBITDA of ~ US$11.0mm with a NPV of

~ US$ 90mm

11

Topics

Bolivia´s M&A Transaction [ 1 ]

Corporate Strategy [ 2 ]

Q2 2018 Financial Results [ 3 ]

Guidance 2018 [ 4 ]

Stock Performance [ 5 ]

Appendix [ 6 ]

12

1 Revenue growth Q2’18 vs Q2’17.2 Categories in which we gained or maintained market share. Estimates based on volume

share.3 Savings do not include gross-to-net of 2017 and Q1 2018. In the Q1 2018, Alicorp

generated S/26M in gross-to-net savings.4 SG&A normalized saving partially offsett with incorporation of new corporate capacities5 Excludes one-off expenses related to the implementation of efficiency initiatives.

ST

RA

TE

GIC

PIL

LA

RS

“One Alicorp” Mindset• Transfer knowledge across the organization

• Leverage corporate capabilities

• Share best practices among business and geographies

“Implementing an

efficiency-driven culture

across the organization”

Savings of S/ 280M since

we started the efficiency

program3

Growth

2 Alicorp’s achievements for Q2 18’

GROSS PROFIT

3

Efficiencies

People

CONSUMER GOODS PERU B2B AQUACULTURE

Core Categories Value ChannelInnovation / R&D

Edible

Oils

Laundry

Care

Pasta

Sauces

+7.2%1MS% 15 of 19

categories2

Cereals

Pre-mixes

Baby

segment

Canned Tuna

+14.8%1

Multipurpose

Detergent

Cookies &

Crackers

Edible

Oils

Innovation / R&D Market Expansion

R&D

Special

Diets

17

51.3

31

3 0.3

Manufacturing Procurement Distribution Others Q2 18' Savings

Savings for S/ 51.3M during Q2 18’ mainly due to efficiencies in COGS

VP of Consumer

Goods International

VP of Bolivia

Pasta

5

Pizza flour

Dough Improver

Wavy potatoes CA

4

+5.7%1 +22.3%1

13

Our Efficiency Plan is showing improvements at Gross

Margin and EBITDA margins levels…2

Our efficiency plan execution has impacted our non-raw material COGS and SG&A. Both improvements were partially offset by the

increase of commodity prices and non recurrent expenses

CO

GS

▪ Raw material costs increased 3.5 p.p. YoY as

percentage of Revenue due to increasing commodity

prices, mainly wheat

▪ However, other COGS as packaging, manufacturing,

logistics, labor, energy, among others costs, decreased,

overall, 2.0 p.p. as percentage of Revenue

SG

&A

Alicorp’s organic Gross Profit margin decreased by 0.7 p.p. as a result of higher commodity inflation, but was partially

offset by savings in manufacturing and procurement costs

901 1,019 1,194

299 278 304

Q2 17' Q2 18' Q2 18'

% of Revenue (PEN Million)

1,2971,201

1,498

50.4%56.3%

16.7%

14.3%

67.2%

70.6%

53.9%

14.7%

68.6%

+

OthersRaw Materials

▪ Efficiency initiatives implemented in SG&A allowed to

reduce our expenses in 0.3 p.p.

▪ Non-recurrent expenses are i) restructuring expenses,

ii) expenses related to the transaction in Bolivia,

iii) impairments, or iv) gain or loss from sales of non-core

assets. During Q2 18’ these expenses amounted to S/

9.1 million

Total SG&A, as percentage of revenue, decreased in 0.2 p.p.. Excluding non – recurrent expenses would have decreased in

0.3 p.p.

264 274 292

8 9 9

Q2 17' Q2 18' Q2 18'

14.8%

0.4%

15.2%

13.8%

0.4%

14.2%

14.5%

0.5%

15.0%

Non – recurrent expensesSG&A

272301283

% of Revenue (PEN Million)

+

14

2…while we closely monitor all of our Efficiency initiatives to

unlock our full potential…

▪ Continuous improvement of our

payment terms allow us to partially

offset a temporary increase in the

inventory

▪ Reduction of our all-in cost of

debt to 4.8% without decreasing its

average life

Efficiencies

People

Growth

KEY INITIATIVES PHASE

NE

T I

NC

OM

ER

EV

EN

UE

CO

GS

SG

&A

▪ Pricing Strategy: Focus on maximizing marginal

Revenue

▪ Gross-to-Net: Reduction of sales discounts without

sacrificing Volume

▪ Procurement: Generate savings via efficient sourcing

program

▪ Lean Manufacturing: Optimize and standardize our

industrial processes

▪ Logistics: Effective internal distribution of raw materials

and finished product

▪ Org. Structure: Right sizing for growth

▪ Go-to-Market Strategy: Reduction of commissions and

sales expenses

▪ Marketing ROI guidelines: Increase marketing

effectiveness without additional spending

▪ ERP and Data Analytics: Real-time analytics for key

decisions

▪ Working Capital: Improvement in Cash Conversion

Cycle

▪ Liability Management: Optimize capital structure while

reducing financial expenses

▪ Hedging Strategy: Minimize FX losses

TARGET

Q4 2018

Q4 2018

Q4 2018

Q4 2018/19

Q3 2018

Q4 2019

Q2 2019

Q2 2019

Q4 2019

Q2 2018

Q2 2018

Q2 2018

Q2 18’ RESULTS

Gross-to-Net discounts improved

from 13.1% to 12.2%

▪ Procurement: Corporate Sourcing

efficiencies for PEN 31M

▪ Lean Manufacturing: 5.8% cost /

ton reduction

▪ Logistics: 7.7% cost / ton

reduction

▪ Org. Structure: Design complete

and Implementation start

▪ Go-to-market: Design phase in

Brazil

▪ ERP: Design phase through all

levels

15

Excl. corporate

expenses

EBITDA mg breakeven

2…resulting in material improvements starting to notice in

terms of profitability due to structural changes in Argentina

PILLAR

Efficiencies

29 28 23 29 28 29

Q1 17' Q2 17' Q3 17' Q4 17' Q1 18' Q2 18'

TOP LINE KEY INITIATIVES & INSIGHTS

PROFITABILITY (EBITDA)

-64-54

-79 -79

-60

-29

Q1 17' Q2 17' Q3 17' Q4 17' Q1 18' Q2 18'

-3.5%-10.5% -8.8% -14.9% -12.3% -2.4%

604 621 520 644 658 726

Q1 17' Q2 17' Q3 17' Q4 17' Q1 18' Q2 18'

Volume

Revenue

EBITDA Mg

EFFICIENCY PLAN (FY Normalized Savings)

Manufacturing

(US$ 3.2mm)

Org. Structure

(US$ 1.1mm)

Procurement

(US$ 7.5mm)

Working Capital

(US$ 1.3mm)

✓ US$ 1.1mm YTD Normalized Savings

✓ Lean Management Implementation Process in both of our

footprints: San Justo and Garín

✓ 10% Blue collar Staffing reduction

✓ US$ 5.2mm YTD Normalized Savings

✓ 78% due to better Raw Material Negotiation Prices and

22% due to Design to Value Projects

✓ Right sizing for Growth

✓ US$ 0.6mm YTD Normalized Savings

✓ 15% Administrative Staffing reduction

✓ Improve in Account Payable Cycle

✓ Reduce Financial Expenses

(TMk)

(ARSM)

(ARSM)

✓ Downsizing our industrial footprint (e.g., closing of our

pasta facility, adjust blue collar staffing)

✓ Refreshing our product portfolio (e.g., Zorro (HC) and

Plusbelle (PC)) with ad campaigns

✓ Client segmentation and pricing strategy (e.g., from 47 to 7

pricing lists, margin by client type)

✓ Focus on reverting operating cash-flow to positive (e.g., no

intercompany since February)

+24.1%

+52.4%

Pasta facility shutdown

EBITDA Mg Excluding one shots

-4.0%-10.5% -8.8% -15.3% -12.3% -9.1%

16

Topics

Bolivia´s M&A Transaction [ 1 ]

Corporate Strategy [ 2 ]

Q2 2018 Financial Results [ 3 ]

Guidance 2018 [ 4 ]

Stock Performance [ 5 ]

Appendix [ 6 ]

17

▪ EBITDA reached S/ 259.3 million, while EBITDA

Margin was 12.2% (-1.4 p.p.)

▪ Excluding Fino, EBITDA reached S/ 252.1

million, while EBITDA Margin was 13.3% (-0.3

p.p.) mainly explained by lower Gross Margin,

partially offset for lower SG&A and other expenses

1,554 1,711 1,787 1,891 2,123

6,949 7,209 7,441

26.3%27.6% 26.9% 26.2% 24.3% 27.5% 27.6% 27.0%

Q1 17' Q1 18' Q2 17' Q2 18' Q2 18' FY 17' LTMQ2 18'

LTMQ2 18'

187 210 244 252 259

903 935 942

12.0% 12.3% 13.6% 13.3% 12.2% 13.0% 13.0% 12.7%

Q1 17' Q1 18' Q2 17' Q2 18' Q2 18' FY 17' LTMQ2 18'

LTMQ2 18'

REVENUE & GROSS MARGIN

EBITDA & EBITDA MARGIN

3 Q2 2018 Key Highlights1 (1/2)

Q2 2018 was a strong quarter in terms of growth, driven by our operations in Peru and Aquaculture business performance.

Meanwhile, the international division was affected by several economic headwinds (Argentina) and political turbulence (Brazil)

(PEN Million)

(PEN Million)

▪ Total Revenue increased 18.8% YoY. Excluding

Fino, Revenue increased 5.8% explained by the

contribution of Consumer Goods Peru (+6.3% YoY),

Aquaculture (+22.3% YoY) and B2B (+5.7% YoY)

▪ Gross Margin was 24.3% (-2.6 p.p.) Excluding

Fino, Gross Margin was 26.2% (-0.7 p.p.)

HIGHLIGHTS

+

+

+

+

HIGHLIGHTS

1 Q2 2018 figures include Fino’s financials. Excluding the acquisition of Fino, Alicorp increased 5.8% YoY in Revenue, 3.4% YoY in EBITDA and decreased 1.3% YoY in Net

Income.

18

-77 104 130 128 125

450 475 472

5.0% 6.1% 7.3% 6.8% 5.9% 6.5% 6.6% 6.3%

Q1 17' Q1 18' Q2 17' Q2 18' Q2 18' FY 17' LTMQ2 18'

LTMQ2 18'

Q2 2018 Key Highlights1 (2/2)

NET INCOME & NET MARGIN

Regarding our bottom-line results, Fino’s acquisition financing implied higher financial expenses

(PEN Million)

▪ Net Income decreased 3.4% YoY while Net

Margin was 5.9% (-1.4 p.p. YoY)

▪ Financial expenses, hedging costs and currency

exchange losses increased in 65% YoY (0.5

p.p.) mainly explained by the effect of the debt

related to Fino’s acquisition

▪ Excluding Fino, Net income decreased 1.3%

YoY while Net Margin was 6.8%

(-0.5 p.p. YoY)

HIGHLIGHTS

+

+

We launched/revamped 28 products, among these, the following can be highlighted in the Consumer Goods Peru: i) In the

Laundry Category the new “Opal Sports” specialized detergent, ii) in the Sauce category a new "Tartar" sauce was launched

under the "Alacena" brand, and iii) in the Cookies & Crackers category the new "Casino Black" limited edition was launched.

These launches were made in order to develop these platforms portfolios

CONTINUOS INNOVATION

1 Q2 2018 figures include Fino’s financials. Excluding the acquisition of Fino, Alicorp increased 5.8% YoY in Revenue, 3.4% YoY in EBITDA and decreased 1.3% YoY in Net

Income.

3

19

Net income decreased 3.4% YoY, mainly due to higher financial expenses related to Fino’s acquisition

WORKING

CAPITAL

• Cash Conversion Cycle, measured in LTM basis and excluding Fino, decreased to 8.6 days

(as of June 2018) from 10.2 days (as of December 2017)

II

NET INCOME• Net income reached S/ 125.3 million (- 3.4% YoY), while Net Margin was 5.9% (- 1.4 p.p. YoY)

• Higher financial expenses of S/ 21.8 million (+55.5% YoY) and higher FX losses of S/ 5.8 million

CREDIT

RATING

• All credit ratings agencies have reaffirmed the investment grade with a "stable" outlook

• The local agencies “Apoyo & Asociados” and “ Equilibrium” affirmed “AAA” rating of bonds, while the

international agencies S&P, Fitch and Moody’s affirmed “BBB-”, “BBB” and “Baa3” ratings,

respectively.

IV

• Net Debt-to-EBITDA ratio increased to 2.03x as of June 20182 from 1.00x as of December 2017

• Net Debt3 increased to S/ 2,082.0 million as of June 2018, from S/ 898.8 million as of December

2017 (a S/ 1,183.2 million increase)

• All-in cost of debt was 4.8% during Q2 18’2, below 5.2% as of December 2017

FINANCIAL

LEVERAGE

I

Q2 2018 Financial Highlights1

III

2 Financial information including Fino in the last 12 months.3 Net Debt is Financial Debt minus cash and cash equivalents as of Q2 18’.

1 Financial information under IFRS 9 & 15.

3

20

▪ Revenue and Volume increased by 6.3% YoY and 7.3% YoY

respectively, on the back of our core categories growth such as Laundry

Detergents, Edible Oils, Pasta, Cookies and Sauces

▪ Gross Margin increased by 1.2 p.p. YoY mainly explained by i) our

revenue management strategy and ii) savings in procurement, transport,

and production costs

▪ EBITDA reached S/ 130.5 million (-1.7% YoY) and EBITDA Margin

reached 19.3% (-1.6 p.p.) explained by higher promotional and marketing

activities

HIGHLIGHTS

REVENUE & GROSS MARGIN EBITDA & EBITDA MARGIN

Q2 2018 INSIGHTS

558 624 638 678

2,544 2,650

34.3% 36.2% 34.6% 35.8% 34.7% 35.4%

Q1 17' Q1 18' Q2 17' Q2 18' FY 17' LTMQ2 18'

Market share (Δ% YoY) > - 0.5 p.p. - 0.6 p.p. < Market share (Δ% YoY) < - 0.9 p.p. Market share (Δ% YoY) < -1.0 p.p.

INNOVATION & POSITIONING

Category Rank1

Edible Oils #1

#1

Pasta #1

#1

Cereals #1

Jelly #1

Laundry

Detergents

Mayonnaise

Consumer Goods Peru

1

(PEN Million) (PEN Million)

Sauces

Detergents

3

107 122 133 131

500 512

19.2% 19.5% 20.8% 19.3%19.7% 19.3%

Q1 17' Q1 18' Q2 17' Q2 18' FY 17' LTMQ2 18'

21

▪ Revenue and Volume increased by 5.7% YoY and 3.7% YoY

respectively, backed on the growth of Bulk Oils, Flours and Sauces across

all platforms (Food Services, Bakery and Industrial Clients)

▪ Gross Margin increased by 1.5 p.p. YoY explained by lower commodity

prices and revenue mix toward more profitable categories

▪ EBITDA reached S/ 43.2 million (+25.5% YoY) and EBITDA Margin

reached 10.9% (+1.7p.p. YoY)

HIGHLIGHTS

EBITDA & EBITDA MARGIN

PRODUCT INNOVATIONQ2 2018 INSIGHTS

REVENUE & GROSS MARGIN

Dough Improver

B2B

(PEN Million) (PEN Million)

Pizza Flour

340 351 375 397

1,503 1,536

18.3% 19.5% 17.3% 18.9% 19.8% 20.4%

Q1 17' Q1 18' Q2 17' Q2 18' FY 17' LTMQ2 18'

33 32 34 43

166 173

9.8% 9.0% 9.2% 10.9%11.1% 11.3%

Q1 17' Q1 18' Q2 17' Q2 18' FY 17' LTMQ2 18'

3

22

-5

8

15

4 5

0.1% -2.2%

2.6% 4.7%0.4% 0.5%

Q1 17' Q1 18' Q2 17' Q2 18' FY 17' LTMQ2 18'

▪ Revenue and Volume increased by 3.2% YoY and 16.2% YoY,

respectively, explained by the contribution of Fino’s consumer

business. Meanwhile, Revenue decreased in Argentina and Brazil

explained by: i) higher than expected inflation (+16% YTD) in Argentina and

ii) lower price per ton in Brazil due the ongoing “Tiering down” trend

▪ Gross Margin decreased by 2.4 p.p. YoY, explained by the effects of

Brazil and Argentina

HIGHLIGHTS

EBITDA & EBITDA MARGIN

PRODUCT INNOVATIONQ2 2018 INSIGHTS

297 250 304 313

1,145 1,108

28.8% 30.1% 31.2% 28.8%30.1% 29.8%

Q1 17' Q1 18' Q2 17' Q2 18' FY 17' LTMQ2 18'

REVENUE & GROSS MARGIN

Consumer Goods International

(PEN Million) (PEN Million)

0.3

Argentina

Brazil

3

23

604 658 621 726

2,389 2,548

20.4% 22.5% 24.3% 21.4% 21.1%

Q1 17' Q1 18' Q2 17' Q2 18' FY 17' LTMQ2 18'

20.9%

▪ Revenue in ARS increased by 16.8% YoY while Volume increased by

3.1% YoY. The Volume increase was mainly explained by the Home Care

platform (+9.8% YoY); meanwhile, Revenue in ARS grew 16.8% due to

pricing adjustments (+13.0% YoY) to pass-through inflation. Nevertheless, in

Peruvian Soles, the currency depreciation

(+51.4% YoY) affected the consolidated figures

▪ EBITDA increased in ARS 25.7 million, while EBITDA Margin improved

in 4.8 p.p.

HIGHLIGHTS

EBITDA & EBITDA MARGIN

Q2 2018 INSIGHTS

REVENUE & GROSS MARGIN

Consumer Goods International - Argentina

(ARS Million) (ARS Million)

-64 -60 -54 -29

-277 -248 -10.5%-9.1%

-8.8%-4.0%

-11.6% -9.7%

Q1 17' Q1 18' Q2 17' Q2 18' FY 17' LTMQ2 18'

PRODUCT INNOVATION

“Plusbelle” brand

Hair Care Bath Soap

Deodorant

3

24

▪ Revenue in BRL and Volume decreased by 9.0% YoY and 1.0% YoY,

respectively. The Volume decline was driven by a trucker’s strike.

Revenue decreased due to the ongoing market dynamic, a “Tiering

down” trend, that reduces the market price per ton and a regional

Revenue mix that increases sales in regions with lower prices

▪ EBITDA was BRL 1.7 million compared to BRL 10.7 million in Q2 17’,

while EBITDA Margin decreased 7.2 p.p YoY to 1.5%

HIGHLIGHTS

EBITDA & EBITDA MARGIN

Q2 2018 INSIGHTS

119 103 122 111

475 448

34.3% 33.0% 35.0% 34.4% 33.5%

Q1 17' Q1 18' Q2 17' Q2 18' FY 17' LTMQ2 18'

32.3%

REVENUE & GROSS MARGIN

Consumer Goods International - Brazil

(BRL Million) (BRL Million)

8

-1

11

2

32

14

7.0% -1.0% 8.7%

1.5%6.7% 3.0%

Q1 17' Q1 18' Q2 17' Q2 18' FY 17' LTMQ2 18'

Hair Care

Jelly

PRODUCT INNOVATION

3

25

HIGHLIGHTS

BUSINESS INSIGHTS

EBITDA & EBITDA MARGINREVENUE & GROSS MARGIN

Consumer Goods International - Bolivia

(US$ Million) (US$ Million)

ALICORP BOLIVIA´S PORTFOLIO

Edible oil Lard>40% >50%

Fino Exports

Margarine Laundry Soap>60% >25%

Detergents > 8%

Pastas > 5%

Personal Care > 3%

33

5

2

21 15

12

30

39.7% 42.3% 38.7%40.2% 29.8% 41.1% 42.7% 34.0%

Q1 17'Q1 18' Q2 17'Q2 18' Q2 18' FY 17' LTMQ2 18'

LTMQ2 18'

+

1

0

1

0

3 3

2

4

22.5%15.3%23.6%

14.1%14.1% 20.3% 15.8% 14.8%

Q1 17'Q1 18' Q2 17'Q2 18' Q2 18' FY 17' LTMQ2 18'

LTMQ2 18'

▪ Revenue amounted US$ 21.0 millions. Excluding

Fino’s figures revenue reached to US$ 2.4 millions

▪ EBITDA was US$ 3.0 millions, while EBITDA

Margin reached to 14.1%

Market share

+

+

+

xxx

3

26

1,009 806 911 938 1,008

1,120 1,198 1,156 1,253 1,313 1,262

1.8 1.7 1.82.0

2.32.1

2.3 2.2 2.3 2.32.0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

HIGHLIGHTS

BUSINESS INSIGHTS

CRUSHING PROCESS DIAGRAMREVENUE & GROSS MARGIN

Crushing

(US$ Million)

SOYBEAN MARKET

EBITDA & EBITDA MARGIN

48.3

1.2%

Q2 18'

21% 23% 23% 19% 18% 20% 17% 16% 19% 19% 20%

17% 13% 14% 13% 13%

CAGR 12’-17’: 2.4%

Soybean Area

(ha)

Soybean Yield

(MT/ha)

Local Production

Purchased by Fino

Local Production

Purchased by SAO

Avg: 1,089

(US$ Million)

▪ Soybean is the main crop of Bolivia with ~1.3M productive

hectares located mainly in the Santa Cruz region

▪ Price trend along with the low yield in Bolivia have

affected the current performance of the business

▪ The business added 93.7 thousand tons and

S/ 157.6 million in the Q2 18’ consolidated figures

▪ For Q2 18’ Gross Margin was 1.2% while EBITDA

Margin was -1.8%

-0.9

-1.8%

Q2 18'

May & June May & June Local

Growers

Local

Demand

Exports

Crude oil MealsSoybean and

Sunflower beans

3

27

▪ Revenue and Volume increased by 22.3% and 23.2% YoY, respectively.

The main Revenue increase contributor was the shrimp feed platform

(+31.9% YoY), while the fish feed platform grew 6.6% YoY

▪ Gross Margin decreased by 3.0 p.p. YoY to 18.5%, mainly due to higher

raw material prices and a “Tiering down” trend in the shrimp feed platform

▪ EBITDA reached S/ 74.0 million (-3.3% YoY) and EBITDA Margin

reached 12.8% (-3.4 p.p.)

HIGHLIGHTS

Q2 2018 INSIGHTS

359 485 471

576

1,756

1,987

19.6% 21.0% 21.5% 18.5%22.0% 21.3%

Q1 17' Q1 18' Q2 17' Q2 18' FY 17' LTMQ2 18'

45 63

77 74

258 274

12.5% 13.0% 16.2% 12.8%14.7% 13.8%

Q1 17' Q1 18' Q2 17' Q2 18' FY 17' LTMQ2 18'

EBITDA & EBITDA MARGINREVENUE & GROSS MARGIN

Aquaculture

(PEN Million) (PEN Million)

Shrimp Feed

3

28

Topics

Bolivia´s M&A Transaction [ 1 ]

Corporate Strategy [ 2 ]

Q2 2018 Financial Results [ 3 ]

Guidance 2018 [ 4 ]

Stock Performance [ 5 ]

Appendix [ 6 ]

29

4 Updated Guidance for FY 2018

1 Previous estimate as of May 2018.2 Excludes excess cash3 New guidance includes financial figures of Fino and SAO since acquisition date and

expected year-to-go “figures 2018

4 2018E do not include EBITDA from synergies5 Proforma guidance includes FY financial figures of Fino and SAO

Q2’ strong results are aligned with our organic guidance for Alicorp (ex Fino and SAO). Updated guidance includes the

previous guidance for Alicorp coupled with Fino and SAO expectations

Key Considerations

▪ Healthy Nutrition Act

▪ FX and commodities volatility

▪ Raw material prices volatility

▪ Current political uncertainty

FY 2017

7.3%

13.0%

6.5%NET MARGIN (%)

13.7%ROIC (%)2

REVENUE

GROWTH (PEN) (%)

EBITDA MARGIN (%)

2018

YTD Results

7.1%

12.7%

6.0%

11.1%

Updated Guidance4

7.0% - 9.0%

12.0% - 13.0%

5.0% - 6.0%

Under

Review

Previous

Guidance1

5.0% - 7.0%

13.0% - 13.5%

6.5% - 7.0%

13.5% - 14.0%

New Guidance

2018 with Bolivia3

Proforma

Full Year 20185

6.0% - 8.0%

12.0% - 13.0%

5.0% - 6.0%

Under

Review

CAPEX (PEN million) 83.9 200 - 25085.5 220 - 270 220 - 270

EPS (PEN) 0.53 0.55 - 0.600.27 0.50 - 0.60 0.50 - 0.60

NET DEBT/ EBITDA 1.00x 0.60x - 0.80x2.03x 2.20x- 2.50x 2.30x- 2.60x

NET DEBT/ Norm. EBITDA 1.00x 0.60x - 0.80x2.03x 2.10x- 2.40x 2.20x - 2.50x

ADJ. NET DEBT/ Norm. EBITDA 1.00x 0.60x - 0.80x2.03x 2.05x – 2.35x 2.15x – 2.45x

30

4

We maintain a cautious guidance in Peru, Argentina, Brazil and Bolivia, while Aquaculture is expected to continue its

growing trend. We will constantly review our guidance based in the performance of our business units

Revenue Guidance FY 2018 by Business

1 Previous estimate as of May 2018. Excludes Fino and SAO operations.2 Growth calculation includes FY financial figures of Fino and SAO.

CONSUMER

GOODS PERU

B2B

CGI ARGENTINA

FY 2017

CGI BRAZIL

CGI BOLIVIA

AQUACULTURE

CRUSHING

2018

YTD Results

Previous

Guidance

New Guidance

2018 with Bolivia

Proforma

Full Year 2018

6.4%

3.4%

(3.7%)

11.1%

(0.7%)

(5.4%)

13.3%

17.2%

21.8%

25.9%

n.a

n.a

8.9%

4.5%

(18.1%)

12.9%

(18.2%)

(11.3%)

n.a

n.a

27.8%

28.8%

n.a

n.a

4.0% - 6.0%

3.5% - 5.5%

(6.0%) - (4.0%)

n.a

(5.0%) - (3.0%)

n.a

n.a

n.a

12.0% - 14.0%

n.a

n.a

n.a

7.0% - 9.0%

5.0% - 7.0%

(8.0%) - (6.0%)

(7.5%) - (5.5%)

18.0% - 20.0%

19.0% - 21.0%

14.0% - 18.0%

(8.0%) - (6.0%)

(7.0%) - (5.0%)

19.0% - 21.0%

1.0% - 3.0%

(8.0%) - (6.0%)

30.0% - 36.0%

(14.0%) - (12.0%)

(5.0%) - 0.0%

30.0% - 36.0%

(5.0%) - 0.0%

1.5% - 3.5%14.5% - 16.5%

Guidance in PEN

Guidance in local currency

31

Topics

Bolivia´s M&A Transaction [ 1 ]

Corporate Strategy [ 2 ]

Q2 2018 Financial Results [ 3 ]

Guidance 2018 [ 4 ]

Stock Performance [ 5 ]

Appendix [ 6 ]

32

0 2 4 6 8 10 12 14

40

60

80

100

120

140

160

Jul-1

7

Aug-1

7

Sep-1

7

Oct-

17

No

v-1

7

De

c-1

7

Jan-1

8

Feb

-18

Ma

r-1

8

Apr-

18

Ma

y-1

8

Jun-1

8

ALICORC1 EPU IGBVL

Buy 90%

Hold 10%

Research Recommendation Important Awards

Current Stock Price Consensus vs. Previous ALICORC1, EPU and BVL Benchmark – July 27th LTM

Sell-Side Research Estimates on ALICORC1

“Top 10 – Most

Admired Companies

in Peru”

“Latin America

Executive Team

Rankings”4

Stock price Jul. 27, 2018: 11.80

Previous Current Upside 1

Previous median: 10.672 Current median: 12.453

Potential upside: 5.5%

Stock performance LTM: Stock performance YTD:

(Jan. – Jul. 27, 2018)ALICORC1:

EPU

IGBVL

+42.2%

+15.9%

+20.9%

+11.3%

-0.7%

+2.0%

ALICORC1:

EPU

IGBVL

Buy 70%

Hold 30%

CurrentPreviousDec. 29 2017 Jul. 27 2018

Sept. 17’

Jul. 18’

Apr. 18’

Jul. 18’

Jul. 18’

May. 18’

Dec. 17’

Jun. 18’

Jul. 18’

0.0%

2.5%

5.9%

16.9%

9.3%

22.9%

9.0%

-5.9%

5.1%

-21.5%

Apr. 18’

1Potential stock price appreciation against price market as of July 27 (PEN 11.80).

2 As of December 31, 2017.

3 As of July 27, 2018.

4 Ranked within the top-three companies within the categories of i) “Best CEO”, ii) “Best

CFO”, iii) “Best IRO” and iv) “Best IR Team”, for Mid Cap Food & Beverages Sector.

InstitutionalInvestor

“Good Corporate

Index – Lima Stock

Exchange”

5

33

Topics

Bolivia´s M&A Transaction [ 1 ]

Corporate Strategy [ 2 ]

Q2 2018 Financial Results [ 3 ]

Guidance 2018 [ 4 ]

Stock Performance [ 5 ]

Appendix [ 6 ]

About Alicorp

35

6,157 6,437 6,475 6,949 7,209 7,441

481 722 802 903 935 942

7.8% 11.2% 12.4% 13.0% 13.0% 12.7%

2014 2015 2016 2017 Q2 18' Q2 18'

Revenue EBITDA EBITDA Margin

Ownership structure

Business overview

Strong growth track record

(PEN million)

1 EBITDA and EBITDA Margin for 2014 accounted S/ 688.4 million and 11.0% respectively, ex extraordinary losses of S/ 207.5 million.

2 LTM.

3 Includes Fino´s figures (May-Jun 18’).

Source: Cavali as of June 2018

Revenue CAGR 2014-2018: 4.8%3

6Alicorp is a leading consumer branded products

company in Peru and South America…

1

Consumer Goods

Food, home & personal care products

Peru Brazil Argentina Ecuador

Edible Oils

Sauces

Laundry Care

Cookies & Crackers

Pasta

Personal Care

68

Fish Feed

Aquaculture

Shrimp and fish feed

Shrimp Feed

Ecuador PeruChile

2

B2B

Bakeries, industrial products and food

service

Peru

Industrial Sauces

Ind. Baking Flour

Ind. Margarines

Shortenings

45

Business

Platforms

Key

Categories

# of Brands

Direct

Presence

22

+

Bolivia

Romero Group; 45.8%

Pension funds; 26.9%

Inv. & mutual funds; 17.1%

Other; 10.2%

36

…By jointly leveraging through its competitive advantages and strategic initiatives

Diversified revenue base – Q2 18' LTM Diversified EBITDA base 1 – Q2 18’ LTM

Alicorp carries a diversified portfolio and maintains leadership in all of its business units…

1 EBITDA calculation per business ex unassigned corporate expenses.2 Information provided by the Consumer Goods Peru division.

3 Includes Supermarkets and Cash & Carrier.

4 YTD Jun. 18´.

6…with a well-defined strategy that provides sustainable

growth rates…

Commodity purchasing

Go-to-market strategy

Brand management

Strategic M&A

Product development

105 brands in 13 countries & exports to 9 countries

42 new products launched & revamped in 2017

37 new products launched & revamped in 20184

Economies of scale and centralized platform

250K POS for traditional channel2

366 POS for modern channel3

8 acquisitions since 2012

Health & wellness products

Plant consolidation &

automation

Continuous costs saving

program

Co

mp

eti

tive

Ad

va

nta

ge

s

Str

ate

gic

In

itia

tive

s

CMP36%

CMI 15%

Aquaculture27%

B2B21%

Crushing 2%

CMP37%

CMI 14%

Aquaculture28%

B2B21%

CMP53%

CMI 0.6%

Aquaculture28%

B2B18%

Crushing -0.3%

CMP54%

CMI-0.4%

Aquaculture29%

B2B18%

+

Revenues: S/ 7,209 million Revenues: S/ 7,441 million

+

Revenues: S/ 935 million Revenues: S/ 942 million

37

12

25 28

43 43

33

4237

2011 2012 2013 2014 2015 2016 2017 YTD Jun.2018

Selected products launched in Q2 18'

Successful new product launch strategy, with 263 launches since 2011

Growth focused on core and next-to-core platforms

(# of products)

Growth through Mergers & Acquisitions

20122004 2005 2006 2007 2008 2010 2011 2013 2014

Consumer Goods Peru Consumer Goods

International

Aquaculture

6 …both organic and inorganic

B2B

2018

International Acquisitions Domestic Acquisitions

38

Category Brands Position % of sales2 % of EBITDA3 Competitors

Laundry Detergents #1 7.6% 18.3%

Edible Oils #1 7.3% 9.0%

Pasta #1 5.0% 5.9%

Cookies & Crackers #1 3.5% 1.2%

Mayonnaise & other

Sauces#1 2.8% 7.9%

Laundry Soap #1 1.8% 4.3%

Cereals #1 1.3% 1.5%

Margarines #1 1.1% 2.4%

Household Flour #1 0.9% 2.2%

Dessert #1 0.9% 2.1%

Alicorp is the leading consumer goods company, competing with global and local players, such as

Procter & Gamble, Unilever, Mondelez, Nestle, Carozzi, among others

Ranked #1 in over 10 product categories1

1 Alicorp has +50% of the market share.2 Based on consolidated Revenue Q2 18' LTM. 3 Q2 18' LTM . Calculation per business.4 Total CGP/ Consolidated Revenue.5 Total CGP/ Consolidated EBITDA.

35.6% 4 54.4% 5

6In Consumer Goods Peru (CGP), we are market leaders in

almost every category in which we participate

Source: Kantar World Panel

391Includes Detergents and Laundry Soap.

Pre

miu

mM

ain

str

ea

mV

alu

e

Market and customer segmentation allows a more efficient pricing process and pass-through of

commodities price increases

Product classification

Edible Oils Pasta Laundry Care1 Cookies & CrackersFlour

6…thanks to a strategy that focuses on effective market

and customer segmentation…

40

Consumer Goods Peru: Go-to-Market model1

1 Data as of February 2018.2 Data: All from Jun’ 18, except for Margarines (Nov´17), Juice powders (Nov´17), Mayonnaise (Abr´18), Laundry Soap (Aug´17) and Jelly (Oct´17).3 As measured by market penetration in each category against Alicorp’s closest competitor.

TR

AD

ITIO

NA

L C

HA

NN

EL

A

L

I

C

O

R

P

Average

Sales ticket

S/ 7,250

Average

Sales ticket

S/ 10,000

Non-Exclusive

distributors

Wholesalers

Direct distribution

Indirect distribution

S

H

O

P

P

E

R

25%

10%

17%

MO

DE

RN

Supermarkets

366 Stores

Average

Sales ticket

S/ 150

Exclusive

distributors

48%

Superior availability of Alicorp’s products in the

marketplace2/3

6…and to our unique model of distribution that reaches all

channels

Alicorp Competitor

59.7

48.8

58.4

39.0

0.0

87.3

89.6

63.7

85.9

84.8

Pasta

Edible Oils

JuicePowders

Margarines

Mayonnaise

39.0

88.6

81.9

0.6

52.0

94.6

93.4

99.5

Jelly

Cookies &Crackers

LaundryDetergents

LaundrySoap

41

Category Brands Position % of sales2 % of EBITDA3 Competitors

Industrial Baking Flour #1 7.5% 2.2%

Industrial Oil #1 6.0% 8.2%

Shortenings #1 2.1% 3.3%

Sauces #1 1.3% 2.7%

Industrial Margarines #1 0.8% 2.2%

Frozen Products #1 0.7% 0.2%

Ranked #1 in main categories1

20.6%4 18.4% 5Source: Kantar World Panel

6 Likewise, in B2B we are also market leaders…

ACTUALIZADO

1 Alicorp has +50% of the market share.2 Based on consolidated Revenue Q2 18' LTM. 3 Q2 18' LTM . Calculation per business.4 Total B2B/ Consolidated Revenue.5 Total B2B/ Consolidated EBITDA.

42

Category Brands Position1 % of sales2 Competitors

Brazil

Pasta #1 3.9%

Argentina

Hair Care #2 2.0%

Laundry Detergents #3 1.5%

Skin Care #2 1.2%

Ecuador

Pasta #3 0.4%

Sauces #2 0.1%

Bolivia

Laundry Detergents #3 0.2%

Laundry Soap #3 0.2%

Edible Oils4 #1 0.2%

Lard4 #1 0.1%

Margarine4 #1 0.1%

Pastas #4 0.1%

6Meanwhile, in Consumer Goods International (CGI), we

continue to grow in relevance and brand recognition

Alicorp’s business model has proven to be successfully replicable in other countries

1 Alicorp has ~35% of market share in pastas (Area II in Brazil) and [15% -25%] of Market Share in Personal Care (Argentina). 2 Based on consolidated Revenue Q2 18' LTM.3 Total CGI/ Consolidated Revenue.4 Q2 18’ / consolidated Revenue Q2 18' LTM

ACTUALIZADO

One of the largest consumer goods companies in Latin America

14.9%3

Source: Nielsen NRI

43

6Finally, in Aquaculture, we differentiate among our

competitors thanks to constant innovation and quality

Category Brands Position % of sales2 Competitors

Shrimp

Ecuador #1 15.1%

Peru #2 0.9%

Nicaragua #2 0.6%

Honduras #3 0.5%

Panamá #3 0.2%

Costa Rica #1 0.05%

Fish

Chile #4 8.0%

Peru #1 0.9%

One of the largest aquaculture companies in Latin America1

1 In shrimp feed more than 50% of market share in Peru and Costa Rica, while more than 30% in Ecuador. In fish feed we have +10% of market share in Chile.2 Based on consolidate Q2 18' LTM. 3 Total Aquaculture/ Consolidated Revenue.

Source: Internal Estimates

We are leaders in the Shrimp Feed market in Ecuador and Peru and the 4th largest competitor in

the Fish Feed Market in Chile (Salmon)

26.7 %3