corporate presentation -...

TRANSCRIPT

Corporate PresentationNovember 2017

2

Disclaimer

The material that follows comprises information about Avianca Holdings S.A. (the “Company”) and its subsidiaries, as of the date of the presentation. It has been prepared solely for informational purposes and is not

to be construed as a solicitation or an offer to buy or sell any securities and should not be treated as giving legal, tax, investment or other advice to potential investors. The information presented or contained herein

is in summary form and does not purport to be complete.

No representations or warranties, express or implied, are made as to, and no reliance should be placed on, the accuracy, fairness, or completeness of this information. Neither the Company nor any of its affiliates,

advisers or representatives accepts any responsibility whatsoever for any loss or damage arising from any information presented or contained in this presentation. The information presented or contained in this

presentation is current as of the date hereof and is subject to change without notice, and its accuracy is not guaranteed. Neither the Company nor any of its affiliates, advisers or representatives makes any

undertaking to update any such information subsequent to the date hereof.

This presentation contains forward-looking statements, which are based upon the Company and/or its management’s current expectations and projections about future events. When used in this presentation, the

words “believe,” “anticipate,” “intend,” “estimate,” “expect,” “should,” “may” and similar expressions, or the negative of such words and expressions, are intended to identify forward-looking statements, although

not all forward-looking statements contain such words or expressions. Additionally, all information, other than historical facts included in this presentation is forward-looking information. Such statements and

information are subject to a number of risks, uncertainties and assumptions. Forward-looking statements are not guarantees of future performance and actual results may differ materially from those anticipated due

to many factors. As for forward-looking statements that relate to future financial results and other projections, actual results may be different due to the inherent uncertainty of estimates, forecasts and projections.

Because of these uncertainties, potential investors should not rely on these forward-looking statements. Neither the Company nor any of its affiliates, directors, officers, agents or employees, nor any of the

shareholders or initial purchasers shall be liable, in any event, before any third party (including investors) for any investment or business decision made or action taken in reliance on the information and statements

contained in this presentation or for any consequential, special or similar damages.

Certain data in this presentation was obtained from various external sources, and neither the Company nor its affiliates, advisers or representatives has verified such data with independent sources. Accordingly,

neither the Company nor any of its affiliates, advisers or representatives makes any representations as to the accuracy or completeness of that data, and such data involves risks and uncertainties and is subject to

change based on various factors.

In addition to IFRS financials, this presentation includes certain non-IFRS financial measures, including Adjusted EBITDAR, which is commonly used in the airline industry to view operating results before depreciation,

amortization and aircraft operating lease charges, as these costs can vary significantly among airlines due to differences in the way airlines finance their aircraft and other asset acquisitions. However, Adjusted

EBITDAR should not be considered as an alternative measure to operating profit, as an indicator of operating performance, as an alternative to operating cash flows or as a measure of the Company’s liquidity.

Adjusted EBITDAR as calculated by the Company and as presented in this document may differ materially from similarly titled measures reported by other companies due to differences in the way these measures are

calculated. Adjusted EBITDAR has important limitations as an analytical tool and should not be considered in isolation from, or as a substitute for an analysis of, the Company’s operating results as reported under

IFRS.

The trademarks included herein are the property of the owners thereof and are used for reference purposes only. Such use should not be construed as an endorsement of the products or services of the Company or

this proposed offering.

3

Agenda

Company Overview and Track Record

Leading Airline in Latin America focused on

service excellence

Strong Operational and Financial Performance

1

2

3

Strategic Projects and Full Year Outlook5

Diversified Sources of Revenue with Growing

Non-Passenger Businesses4

Company Overview and Track Record

5

Successful Integration with Further Synergy Generation Potential

Source: Company.(1) Consolidated figures for the eleven months ended December 31, 2010.(2) Includes EBIT contribution of Avianca S.A. and GTH.(3) Maintenance, Repair and Overhaul providers (“MRO”) and Operational Excellence Center (“CEO”).

Well-Defined Integration Plan

▪ Experience operating widebody aircraft offers new

opportunities for traffic from Central America and Lima

▪ Complementary networks offer a unique growth

proposition in Central and South America

▪ Only 2 routes overlapped before combination

Complementary

Routes

Complementary

Fleet

▪ Both airlines shared similar brand and customer

strategies, providing a high standard of service

▪ Talent and commitment aligned with objectives and

similar cultures

Customer

Service

Approach

Great

Talent

Shared Strengths and Values

Total Revenue’16: $4,081MM

Total Revenue‘10: $2,815MM(1)

Single Management Team

Single Loyalty Program

Network & Commercial Integration

Star Alliance

LifeMiles Maximization

Realized Revenue Synergies: $219MM

6.6% 6.2%8.4%5.3% 5.7% 7.2%~4.5%(2)EBIT Margin:

20112012

Core Systems Migration

Single Brand

Single Commercial Code

Revenue ManagementOptimization

Ancillary Revenue

ERPIntra Hub Connectivity Airport Optimization Model

Single Operations Management

Fleet Interchangeability

Cost Control Initiatives

Potential Cost-Reduction Synergies: US$80MM

2015

2016

2014

2017

Network / Fleet Optimization

MRO and CEO(3)

Single Web Page

2013

2010

7.0% - 9.0%

Colombia Domestic

#1

54.5% Market Share(3)

Intra-Home Markets(4)

#1

68.4% Market Share(3)

Home Markets to Spain

#2

24.6% Market Share(3)

6

Leading Airline with Strategic Footprint in the Americas

US$4,081 mm Total Revenues in 2016

100+ Destinations and 6,000+ Weekly Departures

US$879mm Total EBITDAR in 2016

168 Passenger and 12 Freighter Aircraft(1) as of September 2017Average Jet Fleet Age of 7.2 Years

3 Hubs:Bogota, San Salvador and Lima

Source: Company, Aeronáutica Civil de Colombia, and internal data derived from Travelport Marketing Information Data Tapes (“MIDT”). Note: market shares based on number of passengers.(1) 5 Airbus 330F, 5 Airbus 300F and 2 Boeing 767F(2) Brazilian operations reflect the code-share agreement with Oceanair (“Avianca Brasil”), including the licensing of the Avianca trademark(3) Sourced from Company, as of September 2017(4) International traffic within our Home Markets (Colombia, Ecuador, Peru, El Salvador, Costa Rica, Nicaragua, Honduras, Guatemala, Belize, excluding Central American & Caribbean (non-regional))

Complementary Business Lines –20% of Consolidated Revenues in 2016

Single commercial code✓

Single Avianca brand✓

Single website✓

Interchangeability of aircraft✓

Leading Loyalty Coalition Program with 7.5+ mm Members

Geographic Footprint

(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor(NY008B8R) 684268_1.wor

Avianca Brasil(2)

Courier

Leading Airline in Latin America focused on service excellence

Leading Airline with Strategic Footprint in the Americas(5)

Peru(4)

8

Leading Airline in Latin America…

Source: Company and local regulators.(1) Market share based on number of passengers. Colombia: Sep 17, Perú: Jul 17 and Ecuador: 17.(2) Brazilian operations reflect the code-share agreement with Oceanair (“Avianca Brasil”), including the licensing of the Avianca trademark.(3) Reflects market share in the routes it operates as of April 2017.(4) Based on domestic and international passengers. Colombia, as of September 2017 / Peru, as of July 2017(5) Market shares sourced from Company.(6) International traffic within our Home Markets (Colombia, Ecuador, Peru, El Salvador, Costa Rica, Nicaragua, Honduras, Guatemala, Belize, excluding Central American & Caribbean (non-regional)).

Significant Market Share Gains in Key Markets – Passenger Evolution (MM)

Colombia(4)

Domestic Operations

Avianca Brasil(2)

#1

Colombia Domestic54.5% Market Share

#3

Peru Domestic10.9% Market Share

#4

Brazil Domestic(2)

11.8% Market Share

24.0% Market Share in Core Network(3)

Leading Position in Latin American Markets(1)

#2

Ecuador Domestic23.6% Market Share

▪ Unparalleled route network connecting the Americas

▪ Leadership position in the markets served:

~54.5% domestic market share in Colombia

~68.4% market share in Intra-Home Markets(6)

~24.6% market share in Home Markets to Spain routes

Undisputed leadership connecting passengers across our home markets

with one another and with North America, Europe and South America

Long Term Fleet – 4 Families by 2020 2010 – 9 Families

E190 MD83 B757

ATR72

✓ ATR72s for improved

regional capacity

A330F

Boeing 787

✓More fuel efficient than

many similarly sized

airplanes

A320 Neo

✓ 15% less fuel consumption

✓ Up to 500nm of additional

range

✓ Up to 3% cost savings

✓ 40% more cargo capacity vs.

previous cargo fleet

A320 B767 Regional

A330 B737 F100

✓ Increased fuel efficiency

✓ Improved technical dispatch

reliability

✓ Reduced training costs and

maintenance expenses

✓ Improved range and network

performance

✓ Opportunity to upgage in congested

markets

✓ Increased regional capacity

✓ New A321 Neo (2 for 2017): First

Latin American airline to operate it;

allows savings of up to 20% in jet

fuel, reduces up to 50% acoustic

footprint and reduces the emission

of CO2 by plane by 5K tons;

Jet passenger operative

Fleet average age: 6.3 years

9

Successful Fleet Optimization Leadingto Reduced Complexity

Source: Company.(1) The Airbus A320 Family is comprised of 10 – A318, 16 – A319, 49 – A320, 2 – A321, 10 – A319sharklets, 13 – A320sharklets and 9 – A321sharklets.(2) Avianca also has rights to purchase up to 10 Boeing 787 Dreamliners and 15 ATR72s. In April 30, 2015, the Company signed a Purchase Contract for a total of 100 A320 New Engine Option (NEO) family aircraft with deliveries between 2019 and 2024, which are included in the

contractual delivery schedule set above. In line with our initiatives directed towards enhancing profitability, achieving a leaner capital structure and reducing the current levels of debt, in April 2016, Avianca negotiated with Airbus a significant reduction of its scheduled aircraft deliveries for 2016, 2017, 2018 and 2019 and certain changes to the type of aircraft (both upgrades and downgrades), but did not alter the total deliveries scheduled between 2016 and 2025.

Modern

fleet

providing

platform for

higher

profitability

2017 2018 2019 2020 2021 Total

B787 2 1 3 - - 5

A319 2 - - 4 4 10

A320 - 5 6 14 17 42

A321 2 - - 2 2 6

Total(1) 6 6 9 20 23 63

Backlog Designed to Enhance Fleet Efficiency(2)

2017 – 7 Families

Boeing 787

A320 Family(1)

ATR 72 / 42

A330 Pax / 330F /300F

B767F

E190

Cessna 208

Average Jet Fleet Age of 10.1 Years

Strong Operational and Financial Performance

11

Demand outgrows capacity deployment resulting in record Load Factor

3Q17

ASK Growth

3Q17

Insights

3Q17

Load Factor

Intra Home

Markets1

HM to North

America2

Central America &

Caribbean4

HM to South

America3

Domestic*

Region

-7,4%

3Q17

RPK Growth

-3,2%

7,5%

6,4%

1,2%

11,9%

Capacity reduction in September

(last 10 days) due to pilots' strike

with slight traffic impact

Strong competitive position in

strategic markets drives demand

growth

Traffic and yield improvement

above capacity growth

Yield and demand growth driven

by economic recovery, supports

capacity increase in core markets

Broad traffic growth with yield

improvement driven by economic

recovery

TotalRPK Growth

4.9%

Load Factor

84.6%

Home Markets to

Europe

3,5%

4,9%

3,5%

1,7%

16,1%12,2%

84,8%

79,0%

86,3%

84,0%

78,5%

87,8%

ASK Growth

3.5%

Strong capacity expansion with

traffic and yield growth

*Domestic Market: Colombia, Peru, Ecuador 1 Local Intra-Markets: Colombia, Peru, Ecuador, Salvador, Costa Rica, Guatemala; 2 From Local Markets to North América including México 3 From Colombia, Perú, Ecuador and Costa Rica to Bolivia, Chile, Argentina, Brazil and Uruguay, 4 Belize, Cuba Curazao, Republica Dominicana, Panamá, Costa Rica, Guatemala, Honduras, Nicaragua

12 Source: Company InformationBp: Basics points

Demand recovery in core markets drive yield improvement

Load Factor: 3Q17 has the strongest LF in company history Yield - US¢: Continued yield recovery

RPKs – Millions: Strong demand growth outpaces Aviancas’… ASKs – Millions: capacity deployment across the network…

31.172

28.094 30.800

9M16 9M17

Quarterly RPK 9 Months RPK RPK ex-Strike

10.854

8.689 9.441

9.997

10.483

3Q14 3Q15 3Q16 3Q17

+4.9%

+8.6%

+9.6%

+11.0%

12.733

10.683

11.618

11.973 12.389

3Q14 3Q15 3Q16 3Q17

37.535

35.052

37.190

9M16 9M17

Quarterly ASK 9 Months ASK ASK ex-Strike

+3.5%

+6.4%

+6.1%

+7.1%

Quarterly Load Factor 9 Months Load Factor Load Factor, ex-Strike

85,2%

81,3% 81,3%

83,5% 84,6%

3Q14 3Q15 3Q16 3Q17

83,0%

80,1%82,8%

9M16 9M17

+112 bp

+175 bp

+271 bp

+294 bp

11,9

9,5 8,8 8,9

11,9

9,5 8,8

9,2

3Q14 3Q15 3Q16 3Q17

8,6 8,7

8,6

8,8

9M16 9M17

+2.1%

+4.3%

Quarterly Yield 9 Months Yield Yield, ex-Strike

+ 0.9%

+ 0.9%

13

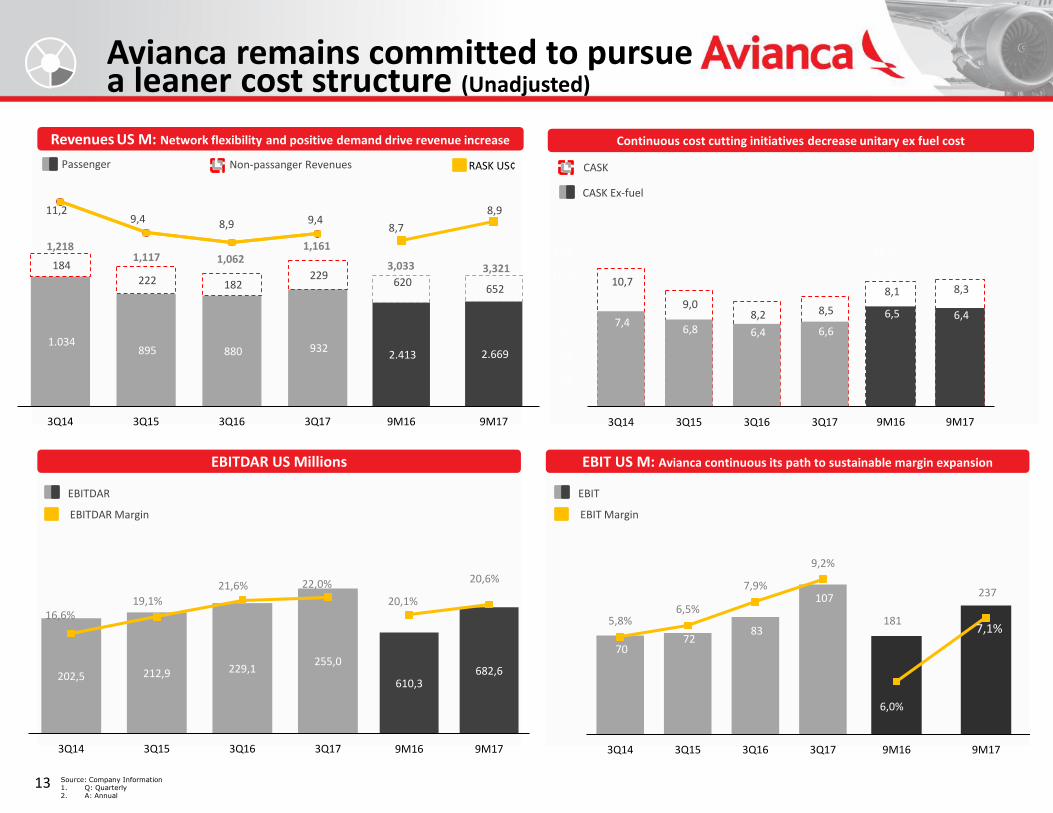

Avianca remains committed to pursuea leaner cost structure (Unadjusted)

Revenues US M: Network flexibility and positive demand drive revenue increase

EBITDAR US Millions EBIT US M: Avianca continuous its path to sustainable margin expansion

Continuous cost cutting initiatives decrease unitary ex fuel cost

Source: Company Information1. Q: Quarterly2. A: Annual

EBITDAR Margin

EBITDAR

EBIT Margin

EBIT

610,3 682,6

20,1%

20,6%

9M16 9M17

202,5 212,9 229,1255,0

16,6%19,1%

21,6% 22,0%

3Q14 3Q15 3Q16 3Q17

70 72

83

107

5,8%6,5%

7,9%

9,2%

3Q14 3Q15 3Q16 3Q17

181

237

6,0%

7,1%

9M16 9M17

CASK

CASK Ex-fuel

10,7

9,0 8,2 8,5

7,4 6,8 6,4 6,6

-

2,0

4,0

6,0

8,0

10,0

12,0

3Q14 3Q15 3Q16 3Q17

-

2,0

4,0

6,0

8,0

10,0

12,0

8,1 8,3

6,5 6,4

9M16 9M17

1.034 895 880 932

184

222 182 229

3Q14 3Q15 3Q16 3Q17

Passenger RASK US¢Non-passanger Revenues

3,033

11,29,4 8,9 9,4

2.413 2.669

620 652

9M16 9M17

1,1611,0621,117

1,218

3,321

8,7

8,9

14

Avianca remains committed to pursuea leaner cost structure (Adjusted)

Revenues1 US M: Network flexibility and positive demand drive revenue increase

EBITDAR1 US Millions EBIT1 US M: Avianca continuous its path to sustainable margin expansion

Continuous cost cutting initiatives decrease unitary ex fuel cost

Source: Company Information1. When indicated the figures are adjusted by the following one-time items:$-31,580m: ACDAC’s Foregone Revenues; $-14,530M: ACDAC’s operatives expenses; $ 6,522M: Aerogal's Reservs Adjust, Opex; $ 1,356MM: Engines Incidents B787, Opex.2. Q: Quarterly3. A: Annual

EBITDAR Margin

EBITDAR

EBIT Margin

EBIT

CASK

CASK Ex-fuel

Passenger RASK US¢Non-passanger Revenues

10,5

8,7 8,2 8,6

7,2 6,5 6,4 6,6

-

2,0

4,0

6,0

8,0

10,0

12,0

3Q14 3Q15 3Q16 3Q17

-

2,0

4,0

6,0

8,0

10,0

12,0

7,9 8,3

6,3 6,4

9M16 9M17

2.413 2.701

563 652

9M16 9M17

1.034 895 880 963

158 198 182

229

3Q14 3Q15 3Q16 3Q17

2,977

1,193

1,0621,0931,192

3,352

11,2

9,4 8,9 9,6

8,5

9,0

70

82 83

132

5,9%

7,5% 7,9%

11,0%

3Q14 3Q15 3Q16 3Q17

193

265 6,5%

7,9%

9M16 9M17

202,5 222,6 229,1278,6

17,0%

20,4%21,6%

23,4%

3Q14 3Q15 3Q16 3Q17

2,0%

7,0%

12,0%

17,0%

22,0%

27,0%

622,4 708,7

20,9%

21,1%

9M16 9M17

15,0%

16,0%

17,0%

18,0%

19,0%

20,0%

21,0%

22,0%

129302 278 268

1.142

130

100 92 92

325

0

29 30

550

0

2017 2018 2019 2020 2021+

AIRCRAFT CORPORATE DEBT BONDS

94,33%

1,91% 3,76%

59,66%

22,03%

1,83% 16,49%

By Currency

EurosColombianPesos

U.S.Dollars

Type(1) Currency Avg. Rate

Aircraft Debt U.S. Dollars 3.53%

BondsColombian

Pesos11.19%

Bonds U.S. Dollars 7.95%

CorporateDebt

U.S. Dollars 4.56%

Total 4.65%

15

Debt Overview and Deleveraging Plan

____________________Source: Company.(1) Excludes US$6.3 Millions of corporate debt in COP and US$128.2 Millions of aircraft debt in EUR.(2) Current installments of long term debt + long term debt – cash. Cash includes cash and cash equivalents + restricted cash + available for sale securities + short term certificates of bank deposits + long term restricted cash.(3) Current installments of long term debt + long term debt + (aircraft rentals 12M x 7) – cash. Cash includes cash and cash equivalents + restricted cash + available for sale securities + short term certificates of bank deposits + long term restricted cash.(4) Consolidated net profit for the period plus the sum of income tax expense, depreciation, amortization and impairment and aircraft rentals, minus interest expense, minus interest income, minus derivative instruments, minus foreign exchange.(5) EBITDAR coverage ratio calculated as EBITDAR divided by the sum of aircraft leases and interest expense.

3Q17 Debt Amortization Schedule (US$MM)

3Q17 Debt Profile

By Type(1)

USD Aircraft Debt

COPBonds

USD Bonds

USD CorporateDebt

258

432400

910

1.467

Diversified Sources of Revenue with Growing Non-Passenger Businesses

17

Avianca Holdings: More Thanan Airline

Source: Company.(1) Considers 5 Airbus 330F, 5 Airbus 300F and 2 Boeing 767F.(2) Includes bellies and excludes Colombia domestic operations. Includes commercial agreements with OceanAir Linhas Aereas, not included in official statistics.(3) Last twelve month figures ending June 30, 2017.

Business Lines

PassengerTransport

Loyalty Business

Other Services

Courier and Cargo Services

Business Overview Brands Key Highlights (2017)

■ Result of the combination of Avianca and Taca with

complementary operations in Andean Region and

Central America

■ Extensive route network from hubs in Bogota, San

Salvador and Lima

■ Member of Star Alliance since 2012

■ Aircraft maintenance, crew training and other airport

services to other carriers

■ Travel-related services to customers including all-

inclusive vacation deals

■ In-flight duty-free sales

■ 13 freighter aircraft complemented by passenger fleet

bellies

■ Deprisa is a leading express courier operation in

Colombia with broad domestic and international

product portfolio; UPS allied in Colombia

■ Strong brand recognition and reputation in Colombia

■ One of the largest coalition loyalty programs in Latin

America

■ 20-year agreement, guaranteed exclusivity and seat

availability from Avianca

■ Solid burn-to-earn ratio

■ $3,3 Billions passenger revenue

■ 168 passenger aircraft(1)

■ 28 countries reached

■ 6,000+ weekly departures

■ 12% YoY growth in 2015 in revenue from

external clients

■ 2,700+ hours of flight simulators

commercialized

■ 12 cargo aircraft(1)

■ $671mm revenue

■ 1,917 mm ATKs(2)

■ 1,054 mm RTKs(2)

■ 41.1% | 11.0% market Share Colombia |

Miami

■ 7.5+ mm members(3)

■ 626k+ active co-branded credit cards

■ +322 commercial Partners

■ Freddie award winner 2013 – 2017

Courier

LifeMiles

19

LifeMiles at-a-Glance

Source: Company.(1) LifeMiles home markets include Colombia, Peru, Ecuador and Central America.

LifeMiles won 2 categories in the 2017 Freddie Awards

Best Redemption Ability, Best Promotion, Up-and-Coming Program

Selected Air Companies

Selected Financial Institutions

~70 banks with active contracts

Selected Regional Hotels

Other Selected Commercial Partners

Strong Brand RecognitionStrong and Growing Network Commercial Partners

Co-Branded Credit Cards

Robust Financial and Performance and Leading Market Positions

HomeMarkets(1)

Members (MM) Quarterly Highlights Geographic Presence

2015

Best Promotion

Up and Coming Program

2016

Redemption Ability

Up and Coming Program

Best Promotion

2017

1

1

1

1

1

Best Promotion

Up and Coming Program

1

1

• 3Q’17 revenues increased 8.8% vs 3Q´16

• 626K active cobranded credit cards, an increase of 21.7% vs. 3Q’16

• More than 7.5 million members, a 9.0% increase vs. 3Q’16

• 322 commercial partners, +6.3% vs 3Q’16

4,44,9

5,46

6,57

7,52

2011 2012 2013 2014 2015 2016 3Q17

RTK (MM)(3) Load Factor

21

Increasing Footprint in Latin AmericanMarkets

Source: Company.(1) On a per trip basis.(2) Includes consolidated revenues from the cargo operation in Mexico.(3) Includes bellies and excludes Colombia domestic operations. Includes commercial agreements with OceanAir Linhas Aereas, not included in official statistics.(4) International Cargo – Aeronáutica Civil de Colombia (as of June 2017) – (5) Miami-Dade Aviation Statistics, by airline group (as of June 2017)

▪ First A330F operating under Peruvian certification (COA)

allowing for more efficient asset utilization and network

optimization

▪ Strong performance for 3 Quarter 2017, with an increase of

+8.8% in transported tons when compared to same period in

2016

▪ New A330Fs provide reduced unit costs, higher capacity (up to

40% more than the previous fleet)(1) and improved reliability

Market Share Colombia (2017)(4)

Segment Overview

Market Share Miami (2017)(5)

Key Metrics (Cargo and Courier)

ATK (MM) (3)Revenue (US$MM)(2)

(% Market share by freight carried) (% Market share by freight carried)

149

116

140

3Q16 3Q17

+28.6%

+20.7%

+11.9%

564 631

3Q16 3Q17

+18.5%

311

369

3Q16 3Q17

55,20% 58,45%

3Q16 3Q17

325 bp

41,1%

8,6% 8,6% 8,6%4,9%

3,1%

25,2%

AVH Atlas Latam UPS Skylease Cargolux Others

13,3%11,5% 11,0%

8,0%6,3% 6,0%

44,0%

Atlas UPS AVH Amerijet American Airlines Latam Others

Revenueex-Strike

Full Year Outlook and Additional Information

Avianca is committed to achieve its full year outlook

24

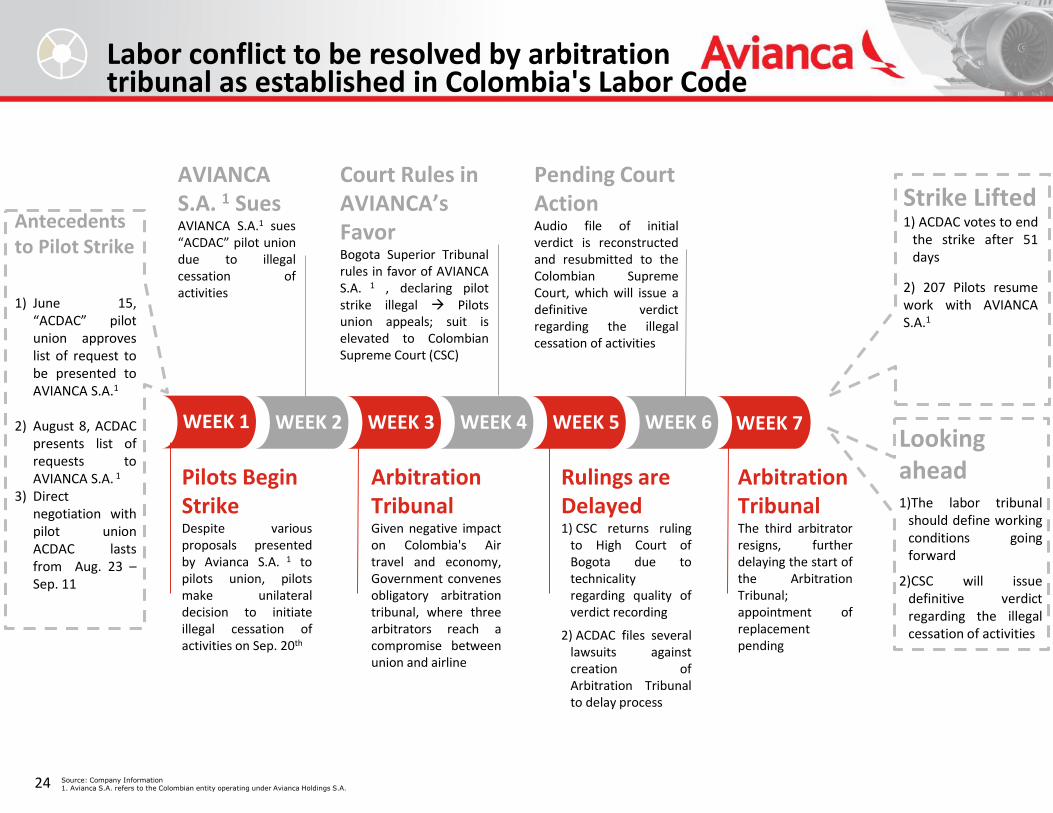

Labor conflict to be resolved by arbitrationtribunal as established in Colombia's Labor Code

WEEK 6WEEK 2 WEEK 4WEEK 3 WEEK 5 WEEK 7

Pilots Begin StrikeDespite variousproposals presentedby Avianca S.A. 1 topilots union, pilotsmake unilateraldecision to initiateillegal cessation ofactivities on Sep. 20th

ArbitrationTribunal Given negative impacton Colombia's Airtravel and economy,Government convenesobligatory arbitrationtribunal, where threearbitrators reach acompromise betweenunion and airline

Rulings are Delayed1) CSC returns ruling

to High Court ofBogota due totechnicalityregarding quality ofverdict recording

2) ACDAC files severallawsuits againstcreation ofArbitration Tribunalto delay process

ArbitrationTribunalThe third arbitratorresigns, furtherdelaying the start ofthe ArbitrationTribunal;appointment ofreplacementpending

AVIANCA S.A. 1 SuesAVIANCA S.A.1 sues“ACDAC” pilot uniondue to illegalcessation ofactivities

Court Rules in AVIANCA’s Favor Bogota Superior Tribunalrules in favor of AVIANCAS.A. 1 , declaring pilotstrike illegal Pilotsunion appeals; suit iselevated to ColombianSupreme Court (CSC)

Pending Court Action Audio file of initialverdict is reconstructedand resubmitted to theColombian SupremeCourt, which will issue adefinitive verdictregarding the illegalcessation of activities

Looking ahead 1)The labor tribunal

should define workingconditions goingforward

2)CSC will issuedefinitive verdictregarding the illegalcessation of activities

Antecedentsto Pilot Strike

1) June 15,“ACDAC” pilotunion approveslist of request tobe presented toAVIANCA S.A.1

2) August 8, ACDACpresents list ofrequests toAVIANCA S.A. 1

3) Directnegotiation withpilot unionACDAC lastsfrom Aug. 23 –Sep. 11

Source: Company Information1. Avianca S.A. refers to the Colombian entity operating under Avianca Holdings S.A.

WEEK 1

Strike Lifted1) ACDAC votes to end

the strike after 51days

2) 207 Pilots resumework with AVIANCAS.A.1

25

AVIANCA’s contingency plan mitigateseffects of pilot strike

Source: Company Information

Cost Impact

Revenue Impact

10 strike days took place in the 3Q17. The resulting impact translates intoUSD $ 2.0 - $ 2.5 Million per day in forgone revenues, while variable costsdecreased between USD $ 1.0 - $ 1.5 Million per day.

Avianca has no restrictions on ticket sales; therefore, all tickets for flightsoperated by Avianca are currently available for sale, which significantlyreduced passenger compensation

Avianca confirms EBIT margin guidance of 7%-9% despite impact of pilotsstrike

On September 20th approx. 700 Avianca Colombia Pilot members of theACDAC union, of a total of 1350 Pilots, went on strike effectively reducing thecompany's deployable capacity, measured in ASK, by 45%

Avianca quickly enacted a contingency plan to mitigate the impact, largercapacity aircraft were deployed, more efficient use of staff, change in mix ofoperating carriers, focus on operation of key domestic city pairs, wet leaseaircraft deployed. Avianca also shifted administrative staff to work atairports; Administrative savings program.

For the Fourth Quarter peak season, Avianca Colombia will continue toincorporate new pilots and returning pilots into its domestic operations, tooperate as closely as possible to its pre-strike capacity (measured in ASK)

9,2%

EBIT Adjustedex-ACDAC

Strike Impact on EBIT

Thank YouContact Information:Investor Relations [email protected]: (57) 1 – 5877700 www.aviancaholdings.com

27

Reconciliation of Adjusted EBITDAR

This presentation includes certain references to non-IFRS measures such as our Adjusted EBITDAR and Adjusted EBITDAR margin. Adjusted EBITDAR represents our consolidated net profit for the year plus the sum of

income tax expense, depreciation, amortization and impairment, aircraft rentals and interest expense, minus interest income, minus derivative instruments, minus foreign exchange. Adjusted EBITDAR is presented as

supplemental information, because we believe it is a useful indicator of our operating performance and is useful in comparing our operating performance with other companies in the airline industry. However,

Adjusted EBITDAR should not be considered in isolation, as a substitute for net profit determined in accordance with IFRS or as a measure of a company’s profitability. These supplemental financial measures are not

prepared in accordance with IFRS or Colombian GAAP. Accordingly, you are cautioned not to place undue reliance on this information and should note that Adjusted EBITDAR and Adjusted EBITDAR margin, as

calculated by us, may differ materially from similarly titled measures reported by other companies, including our competitors.

Adjusted EBITDAR is commonly used in the airline industry to view operating results before depreciation, amortization and aircraft operating lease charges, as these costs can vary significantly among airlines due to

differences in the way airlines finance their aircraft and other asset acquisitions. However, Adjusted EBITDAR should not be considered as an alternative measure to operating profit, as an indicator of operating

performance, as an alternative to operating cash flows or as a measure of our liquidity. Adjusted EBITDAR as calculated by us and as presented in this presentation may differ materially from similarly titled measures

reported by other companies due to differences in the way these measures are calculated. Adjusted EBITDAR has important limitations as an analytical tool and should not be considered in isolation from, or as a

substitute for an analysis of, our operating results as reported under IFRS or Colombian GAAP. Some of the limitations are:

Adjusted EBITDAR does not reflect cash expenditures or future requirements for capital expenditures or contractual commitments;

Adjusted EBITDAR does not reflect changes in, or cash requirements for, working capital needs;

Adjusted EBITDAR does not reflect the interest expense or the cash requirements necessary to service interest or principal payments on debt;

Although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will often have to be replaced in the future, and Adjusted EBITDAR does not reflect any cash requirements

for such replacements;

Adjusted EBITDAR does not reflect expenses related to leases of flight equipment and other related expenses; and

other companies may calculate Adjusted EBITDAR or similarly titled measures differently, limiting its usefulness as a comparative measure.